FEDERAL COURT OF AUSTRALIA

Waters v Commonwealth of Australia (Australian Taxation Office) [2014] FCA 1107

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

Applicant | |

|

AND: |

COMMONWEALTH OF AUSTRALIA (AUSTRALIAN TAXATION OFFICE) Respondent |

|

GRIFFITHS J | |

|

DATE OF ORDER: |

|

|

WHERE MADE: |

THE COURT ORDERS THAT:

1. The applicant is to provide security for the costs of and incidental to the proceedings in the amount of $30,000 (exclusive of GST) in the form of a bank guarantee (or in such other form as is acceptable to the District Registrar) to be lodged with the District Registrar and a copy of which is to be served on the solicitor for the respondent.

2. The bank guarantee required by order 1 be lodged with the District Registrar within 21 days hereof.

3. The proceedings be stayed until security for costs has been provided as required by the above orders.

4. The applicant is to pay the respondent’s costs of the interlocutory application.

5. Liberty to apply on the giving of 48 hours’ notice.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

|

NEW SOUTH WALES DISTRICT REGISTRY |

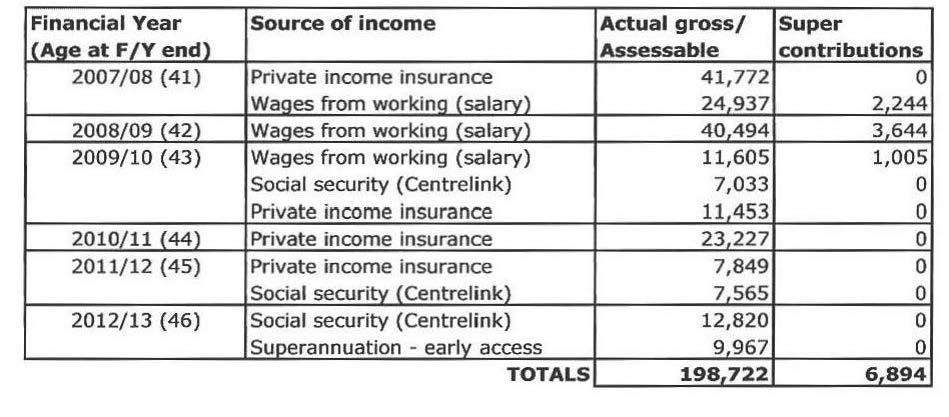

|

|

GENERAL DIVISION |

NSD 108 of 2014 |

|

BETWEEN: |

NATALIE ELIZABETH WATERS Applicant |

|

AND: |

COMMONWEALTH OF AUSTRALIA (AUSTRALIAN TAXATION OFFICE) Respondent |

|

JUDGE: |

GRIFFITHS J |

|

DATE: |

16 OCTOBER 2014 |

|

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

1 By an interlocutory application filed on 21 March 2014, the respondent (the ATO) seeks an order that the applicant (Ms Waters) provide security for costs in the amount of $30,000 (exclusive of GST) or such other amount as the Court thinks fit. It also seeks an order that security be given by bank guarantee to the ATO’s solicitors within 14 days and that the proceedings be stayed until security is given. The ATO seeks a further order that the proceedings be dismissed, or alternatively stayed, if security is not provided on or before the date so ordered. It also seeks costs of the interlocutory application.

2 The substantive proceedings involve a claim brought by Ms Waters as a former employee of the ATO. Ms Waters alleges that she was discriminated against by the ATO on the basis of her disability, contrary to various provisions in the Disability Discrimination Act 1992 (Cth) (Disability Discrimination Act). She also claims that the conduct was in breach of her contract of employment. Ms Waters was employed by the ATO from early 2000 until she was constructively dismissed on 19 November 2004. In March 2004 she was diagnosed with obsessive compulsive disorder (OCD).

3 In broad outline, Ms Waters complains that, when she returned to work at the ATO in late March 2004, a “special supervisor” (Manager) was appointed to “micromanage” her employment and access to flextime. She alleges that the Manager:

(a) induced workplace stress by isolating and degrading her;

(b) refused to accept that her sick leave was related to her psychiatric illness;

(c) restricted her schedule to exacerbate her illness;

(d) accessed her medical history (and advised her of this) without consent prior to becoming her Manager; and

(e) threatened her with notices of breach of the APS Code of Conduct for trivial matters.

4 The ATO has filed a defence to Ms Waters’ statement of claim, in which it denies her primary allegations.

5 As will shortly emerge, Ms Waters has also unsuccessfully brought proceedings in relation to the same broad subject matter in the Supreme Court of New South Wales.

6 In support of the interlocutory application, the ATO relied on an affidavit by its instructing solicitor, Ms Donna Trembath. She was briefly cross-examined by Mr King, who appeared for Ms Waters.

7 Ms Trembath described previous litigation involving the parties relating to Ms Waters’ employment with the ATO. On 5 November 2010, Ms Waters commenced proceedings in the Supreme Court of New South Wales. Ms Waters was solely responsible for drafting her pleadings. On 13 July 2012, Barr AJ struck out Ms Waters’ second further amended statement of claim and ordered her to pay the ATO’s costs (see Waters v Commonwealth of Australia (Australian Taxation Office) [2012] NSWSC 790) (the Supreme Court Proceedings). It is evident from Barr AJ’s judgment that Ms Waters changed solicitors four times prior to the hearing before his Honour, at which Ms Waters apparently represented herself.

8 On 12 October 2012, Ms Waters sought leave to appeal from the judgment and orders of Barr AJ. On 6 February 2013, leave to appeal was refused by McColl JA and Basten JA. Ms Waters was ordered to pay the ATO’s costs (see Waters v Commonwealth of Australia (Australian Taxation Office) [2013] NSWCA 5; (2013) 274 FLR 338) (the Court of Appeal Proceedings).

9 On 6 March 2013, Ms Waters applied for special leave to appeal to the High Court. On 9 October 2013, Hayne and Crennan JJ dismissed that application with costs after hearing the application on the papers (see Waters v Commonwealth of Australia (Australian Taxation Office) [2013] HCASL 172 (the Special Leave Application).

10 Ms Trembath estimated the ATO’s costs of the Supreme Court Proceedings, the Court of Appeal Proceedings and the Special Leave Application as $219,963 on a party/party basis and using a multiple of 50 – 66.66 per cent to be in the range of $109,981 to $146,642.

11 Ms Trembath attached copies of a long series of correspondence between the parties regarding the payment of these costs, which remain unpaid. Mr King objected to the correspondence being admitted into evidence on the ground of relevance. I do not accept his objection. The subject matter of the correspondence is plainly relevant to the exercise of the Court’s discretion whether or not to order security for costs and, in particular, in relation to discretionary matters which are peculiar to the circumstances of this case (see further below).

12 The first relevant letter which was sent to Ms Waters is dated 1 August 2012. After referring to Barr AJ’s decision, the ATO’s lawyers stated that, instead of incurring further costs by having the ATO’s costs assessed, the parties could seek to reach agreement as to costs. Ms Waters responded by asking for more time to consider that proposal, which was granted. By letter dated 28 August 2012, Ms Waters informed the ATO’s solicitors that she had taken advice, and that because she had decided to seek leave to appeal any negotiation regarding payment of costs to the ATO was premature.

13 It is evident that Ms Waters’ current solicitors acted for her in her proceedings in both the Court of Appeal and the High Court. By letter dated 12 March 2013, the ATO’s solicitors wrote to Ms Waters’ solicitors concerning the orders for costs made in the ATO’s favour by both Barr AJ and the Court of Appeal. Reference was made again to the option of having the costs assessed, however, Ms Waters was invited again to consider whether she wished to seek to reach an agreement with the ATO on costs so as to avoid both parties additional expense. It appears that no response was received to that letter. The ATO’s solicitors wrote again to Ms Waters’ solicitors on 7 March 2014. They estimated the ATO’s costs of the Supreme Court Proceedings, the Court of Appeal Proceedings and the Special Leave Application to be approximately $220,000. A similar invitation was made as in the previous correspondence as to whether Ms Waters was willing to negotiate an agreement with the ATO as to costs. Copies of the earlier correspondence on costs were enclosed with the letter dated 7 March 2014.

14 By a letter dated 20 March 2014, Ms Waters’ solicitors replied and stated that they were not retained on the subject of costs in the prior proceedings. The ATO’s solicitors were told to deal directly with Ms Waters on the topic.

15 The interlocutory application was filed the following day.

16 Ms Trembath deposed that, while she was not aware whether or not Ms Waters is in fact impecunious or currently employed, she relied on the following reasons for believing that Ms Waters is not impecunious:

Ms Waters is aged 46 and holds a Bachelor of Arts from the University of Sydney, as well as a joint Master’s Degree in Economics/Econometrics from the same university;

after ceasing employment with the ATO on 22 November 2004, Ms Waters returned to work in the private sector on 5 November 2007;

she was represented at various stages in the Supreme Court Proceedings by solicitors;

Ms Waters was represented by a solicitor and Counsel throughout the Court of Appeal Proceedings and the Special Leave Application; and

a titles search indicated that Ms Waters holds title to a property in Maroubra and has a mortgage in relation to it with the Commonwealth Bank of Australia.

17 Ms Trembath acknowledged that Ms Waters had experienced difficulty in the past in obtaining legal representation and this might be due in part to her inability to meet the high costs of legal representation.

18 Finally, Ms Trembath deposed that, on her instructions, the ATO was not seeking to prevent Ms Waters from bringing the proceedings or to stifle them, but rather, was seeking to have protection for any costs incurred in defending the proceedings in circumstances where Ms Waters had still not paid the three extant costs orders.

19 The application for security for costs was opposed. Ms Waters did not give evidence herself. She relied on an affidavit sworn by her solicitor, Mr Michael Coffey. Mr Coffey was not required for cross-examination. The primary points made by Mr Coffey in his affidavit may be summarised as follows.

20 Ms Waters was a self-represented applicant in the Supreme Court Proceedings. As noted above, she drafted the pleadings there without the benefit of any legal advice.

21 Mr Coffey said that he was “informed” (presumably by Ms Waters) that Barr AJ made certain errors of fact in his findings, including that:

(a) Ms Waters had received compensation benefits for her injury from Comcare/the ATO;

(b) she had elected not to pursue common law remedy by accepting statutory compensation; and

(c) Ms Waters “gave no reason to believe that she could or would engage” a legal representative.

22 Mr Coffey also deposed that, after the Court of Appeal Proceedings, a Commonwealth Parliamentary Report prepared by Mr Peter Hanks QC was published (the SRC Act Review). Mr Coffey said that the Review “provides some submissions consistent with the Applicant’s arguments: namely … that the exclusionary provisions in the SRC Act operate unfairly, are ‘an exception to the standard approach in workers (sic) compensation legislation’ (not a true “no-fault” scheme); submissions to the SRC Act Review identify consequential ‘undue hardship on employees’ and that it is ‘legally inconsistent’”.

23 Mr Coffey said that the High Court had made the same mistakes of fact as had Barr AJ.

24 Mr Coffey also gave evidence regarding the exchange of correspondence on the issue of costs, as outlined above.

25 Mr Coffey deposed that, although the ATO had estimated in early December 2011 that its likely costs of its motion seeking to have the pleadings struck out were in the range of $15,000-$25,000, in fact it now claimed those costs to be $154,000, which he described as “disproportionate” when compared with the ATO’s earlier estimate. Mr Coffey drew attention to the fact that the ATO’s estimated costs of the current proceedings were based on the ATO retaining two barristers, including Senior Counsel, as well as the ATO’s internal lawyers. He believed that this was “excessive” relative to the ATO’s case and “the imbalance of resources between the parties”.

26 Mr Coffey gave some evidence relating to Ms Waters’ financial and employment position. He set out in his affidavit a table which he said Ms Waters had provided to the ATO on 13 July 2011, which described her assessable income (and its source) between the financial years 2008/2013. The table is as follows:

27 As to Ms Waters’ current financial position, Mr Coffey said that she was eligible for a Pensioner Concession Card from Centrelink. He further explained that Ms Waters had accessed some of her superannuation early, based on grounds of financial hardship. He annexed a copy of Ms Waters’ income tax return for the financial year ended 30 June 2013. He also said that he was instructed that Ms Waters has maintained restructured repayments on the mortgage over her residential address, despite her financial difficulties from time to time in doing so.

28 Mr Coffey described Ms Waters’ tertiary qualifications, as well as her recent employment history. He deposed that Ms Waters’ psychiatric illness did not prevent her from being employed, even though that illness persists; however, he said that, since late 2009, Ms Waters had experienced difficulty in maintaining regular, paid employment. Mr Coffey added that he was instructed that “the destruction of the Applicant’s paid employment prospects and resultant loss of income were caused by the disability discrimination, workplace bullying, resulting stress and Obsessive Compulsive Disorder… arising from her employment with [the ATO], which has been increased by extensive time off from her professional career (and concurrent postgraduate studies)”. It is to be noted that Ms Waters filed no medical evidence in support of those “instructions”.

29 Mr Coffey also described the “intensive assistance” which Ms Waters had obtained over the last two years from Centrelink in an endeavour to overcome the barriers to her return to employment. He said that Ms Waters had been offered unpaid employment placements of a general nature, but that Ms Waters had not taken up those offers because “it would not necessarily assist resumption of her professional career and is not otherwise a viable option at this time”. He added that Ms Waters remained open to that option at an appropriate time.

30 Mr Coffey explained that his firm was acting for Ms Waters “on the basis of a flexible payment arrangement”, and that outstanding fees were owed to his firm. He also gave evidence regarding legal fees in respect of Ms Waters’ earlier litigation.

31 Mr Coffey gave evidence relating to an investigation carried out October 2006 and December 2007 by the Australian Public Service Commission. He annexed medical reports dated February and April 2006. He described certain instructions he had received relating to the circumstances surrounding an unsigned Deed of Settlement.

32 Finally, Mr Coffey deposed that he had formed the view that any security for costs would not only stifle the current proceedings, but would actually prevent them from being brought at all which he said would result in an outcome which was favourable to the ATO without Ms Waters ever having had her complaints heard on their merits by any Court.

Outline of relevant legal principles

33 There was no significant disagreement between the parties as to the relevant legal principles guiding the exercise of the discretion whether or not to order security for costs. The relevant principles are well established. I discussed many of them in Ninan v St George Bank Ltd [2012] FCA 905; (2012) 294 ALR 190 (Ninan), to which both parties made reference. The difference between the parties essentially related to the different weight and emphasis to be given to particular relevant considerations.

34 Under s 56 of the Federal Court of Australia Act 1976 (Cth) (the Act), the Court has a discretion to order an applicant in a proceeding to give security for the payment of costs that may be awarded against him or her. The amount of such security and its manner and form is at the Court’s discretion. It is further provided in s 56(4) that if security is not given in accordance with an order made by that Court, the Court may order that the proceeding be dismissed.

35 Rule 19.01 of the Federal Court Rules 2011 (Cth) is also relevant. It provides:

Part 19 Security for costs

19.01 Application for an order for security for costs

(1) A respondent may apply to the Court for an order:

(a) that an applicant give security for costs and for the manner, time and terms for the giving of the security; and

(b) that the applicant’s proceeding be stayed until security is given; and

(c) that if the applicant fails to comply with the order to provide

security within the time specified in the order, the proceeding be stayed or dismissed.

(2) An application under subrule (1) must be accompanied by an affidavit stating the facts on which the order for security for costs is sought.

(3) The respondent’s affidavit should state the following:

(a) whether there is reason to believe that the applicant will be unable to pay the respondent’s costs if so ordered;

(b) whether the applicant is ordinarily resident outside Australia;

(c) whether the applicant is suing for someone else’s benefit;

(d) whether the applicant is impecunious;

(e) any other relevant matter.

Note: Section 56 of the Act deals with security for costs.

(4) In this rule:

applicant includes a cross-claimant.

respondent includes a cross-respondent.

36 It is incontrovertible that the discretion is broad and unfettered and that the only limitation is that the discretion must be exercised judicially (see, for example, Bell Wholesale Co Pty Ltd v Gates Export Corporation (1984) 2 FCR 1 (Bell Wholesale) at 3 per Sheppard, Morling and Neaves JJ). It is a discretion to be exercised according to the merits of each case and without any particular predisposition (see Bryan E Fencott Pty Ltd v Eretta Pty Ltd (1987) 16 FCR 497 at 511 per French J (as his Honour then was)). The discretion is to be exercised by reference to the particular circumstances in each case (see Woodhouse v McPhee (1997) 80 FCR 529 at 533 per Merkel J).

37 In Chapman v Luminis Pty Ltd [2002] FCA 496 at [13], Tamberlin J referred approvingly to the following six matters which had been identified in Equity Access Ltd v Westpac Banking Corporation (1989) ATPR 40-972 (Equity Access) as relevant for consideration in deciding whether security for costs ought to be awarded (without limiting the broad discretion):

the prospects of success;

the quantum of risk that a costs order will not be satisfied;

whether the making of an order would be oppressive in that it would stifle a reasonably arguable claim;

whether any impecuniosity arises out of the conduct complained of;

whether there are aspects of public interest which weigh in the balance against such an order; and

whether there are particular discretionary matters which are peculiar to the circumstances of the case.

38 These matters have been regarded as providing general guidance in many subsequent cases (including, for example, Croker v Sydney Institute of TAFE (NSW) [2003] FCA 942 per Bennett J; Elshanawany v Greater Murray Area Health Service [2004] FCA 1272 (Elshanawany) per Jacobson J and Ninan).

39 Some other relevant additional principles may also be mentioned. First, as Jacobson J observed in Elshanawany at [11]:

The applicant is a natural person and there is long standing authority for the proposition that, in general, a natural person who commenced litigation will not be required to provide security for the costs merely because that person is impecunious.

40 Justice Mortimer recently observed in Kiefel v State of Victoria [2014] FCA 604 that the consideration referred to above (namely, impecuniosity) is somewhat contradictory. At [51], her Honour observed:

There is something of a contradiction in examining impecuniosity in the context of an application for security for costs. Asserted impecuniosity may be the catalyst for an application, because that status provides a rational foundation for the proposition that a respondent cannot reasonably expect to recover its costs if a proceeding (or appeal) is successfully defended. Yet, asserted impecuniosity also tells against capacity to provide security for costs. This seems to be what underlies the consistent line of authority to the effect that impecuniosity by itself is not a justification for an order for security for costs.

I respectfully agree with those observations.

41 Secondly, although the party moving for an order for security of costs carries the normal onus, it is now recognised that the onus of establishing that the making of an order would stultify the proceeding rests on the party who resists security (see Bell Wholesale at [4] and Madgwick v Kelly [2013] FCAFC 61; (2013) 212 FCR 1). As Allsop CJ and Middleton J observed in Madgwick at [81]:

The respondents submitted that the characteristics of the group were relevant to the question of stultification. The onus of establishing that the making of an order would stultify the suit rests on the party resisting security: Bell Wholesale Company Ltd v Gates Export Corporation (1984) 2 FCR 1 at 4; Pioneer Park Pty Ltd (in liq) v Australia and New Zealand Banking Group Ltd (2007) 2 BPRA 753; Green v CGU Insurance Ltd at [45] and [82]. That proposition is, to a degree, uncontroversial. A failure to prove stultification does not mean, however, that security must be provided. Indeed, as Hodgson JA (sitting alone as referrals judge) said in Dae Boong International Company Pty Ltd v Gray [2009] NSWCA 11 at [26], if the evidence does not permit a conclusion of stultification that does not make the impecunosity of the party and the difficulties in providing security (such as they are proved) irrelevant. As Hodgson JA said, if those who stand to benefit from the proceedings are reasonably unwilling, even though possibly able, to provide security, that may be a factor to be taken into account.

42 Thirdly, in Kiefel, Mortimer J made the following observations at [34]:

The potential chilling effect of requirements to provide security for costs on individual litigants are well recognised, and the impediment which such orders could otherwise impose on access to justice means, at first-instance level, an individual impecunious litigant will rarely be ordered to provide security.

43 While I respectfully agree with the general thrust of her Honour’s observations, I do not believe that the word “rarely” should be taken as circumscribing the breadth of the relevant discretion (the notion that security will be ordered against an impecunious natural person only in rare instances was also referred to by Stein JA in Melville v Craig Nowlan & Associates Pty Ltd [2002] NSWCA 32; (2002) 54 NSWLR 82 at [22]). Each case necessarily turns on its own particular facts and circumstances. I prefer to approach the matter on the basis that there is no predisposition one way or the other to ordering security for costs in the case of an individual impecunious litigant. In expressing that view, I do not intend to enter the debate as to whether s 56 of the Act has the effect of altering earlier approaches to this matter as discussed by Heydon JA (as his Honour then was) in Melville at [81]-[98]. Neither party suggested that this issue had to be determined in considering the interlocutory application and I prefer to express no opinion on it.

44 Fourthly, it is also well established that delay in bringing an application for security for costs is another relevant consideration (see, for example, Fairlight.au Pty Ltd v Peter Vogel Instruments Pty Ltd (No 2) [2014] FCA 1037 at [35] per Edmonds J).

45 Fifthly, and again without seeking to circumscribe the broad discretion, it has been recognised in many cases that another relevant consideration in determining whether or not to order security for costs is the fact that an applicant or appellant has failed to pay the costs of the other party in previous litigation (see, for example, Croker at [41] and [44] per Bennett J; Chang v Comcare Australia [1999] FCA 1677 at [31] per Moore J and Bride v Stewart, unreported decision of French J, 19 January 1990).

46 It may well be that the fourth and fifth matters described above are simply examples of the relevance to the discretion of the sixth matter identified in Equity Access (i.e. particular discretionary matters which are peculiar to the circumstances of the case).

Disposal of the interlocutory application

47 As is common with applications of this type, there are factors which weigh both for and against ordering the applicant to pay security for costs. The key factors in favour of granting the relief sought are as follows.

48 First, and most significantly, there are three costs orders against the applicant in the ATO’s favour which have not been paid and in respect of which Ms Waters has refused meaningfully to engage. I accept Ms Trembath’s estimate that the ATO is likely to recover approximately $100,000 on an assessment of those costs.

49 I do not accept Ms Waters’ submission that the issue of the outstanding costs has only arisen relatively recently. The correspondence reveals that the ATO wrote to her on 1 August 2012, shortly after Barr AJ’s judgment was handed down. Ms Waters was put on notice that the ATO would seek its costs if her foreshadowed application for leave to appeal to the Court of Appeal failed. After granting Ms Waters more time to consider her position, the ATO received a letter dated 28 August 2012 from Ms Waters in which she said that as “appeal proceedings will commence… any negotiation regarding payment of costs… is premature”.

50 I am also satisfied that the ATO acted promptly in raising the issue of its outstanding costs after both the Court of Appeal Proceedings and the Special Leave Application.

51 As is evident from the exchange of correspondence which is summarised above, Ms Waters has chosen not to engage with the ATO on the issue of its outstanding costs despite having been given several opportunities to do so.

52 Mr King submitted that no significance should attach to Ms Waters’ conduct in declining to accept the invitation to seek to reach an agreement on costs because there is no debt owing to the ATO. In support of that submission, Mr King referred to ss 368(4) and (5) of the Legal Profession Act 2004 (NSW). It is desirable to set out s 368 in its entirety.

Certificate as to determination

368 Certificate as to determination

(1) On making a determination of costs referred to in Subdivision 2 or 3 of this Division, a costs assessor is to issue a certificate that sets out the determination.

(2) A costs assessor may issue more than one certificate in relation to an application for costs assessment. Such certificates may be issued at the same time or at different stages of the assessment process.

(3) However, any such certificate may not set out the costs of the costs assessment within the meaning of section 369.

Note : Section 369 makes provision for the recovery of the costs of costs assessments relating to costs to which either section 317 (Effect of failure to disclose) or 364 (Assessment of costs-costs ordered by court or tribunal) applies. The section requires a costs assessor to issue a separate certificate setting out the costs of such costs assessments. That section also makes provision for the effect of such a certificate.

(4) In the case of an amount of costs that has been paid, the amount (if any) by which the amount paid exceeds the amount specified in any such certificate may be recovered as a debt in a court of competent jurisdiction.

(5) In the case of an amount of costs that has not been paid, the certificate is, on the filing of the certificate in the office or registry of a court having jurisdiction to order the payment of that amount of money, and with no further action, taken to be a judgment of that court for the amount of unpaid costs, and the rate of any interest payable in respect of that amount of costs is the rate of interest in the court in which the certificate is filed.

(5A) The costs assessor must forward the certificate or a copy of the certificate to:

(a) the Manager, Costs Assessment, and

(b) each party to the assessment, unless subsection (6) applies.

(6) If the costs of the costs assessor are payable by a party to the assessment as referred to in section 369, the costs assessor must:

(a) forward a copy of the certificate to the Manager, Costs Assessment only, and

(b) advise the parties that the certificate has been so forwarded and will be available to the parties on payment of the costs of the costs assessor.

(7) Subsection (6) does not apply:

(a) in respect of a certificate issued before the completion of the assessment process under subsection (2), or

(b) in such circumstances as may be prescribed by the regulations.

53 As is evident from their terms, ss 368(4) and (5) provide no support for Mr King’s submission. In particular, those provisions do not have the effect for which he contended, namely that there is no debt in relation to an order for costs unless and until a certificate as to the determination of those costs had been obtained under s 368. Nor do the observations of Master Macready in Advanced Management Consultancy Pty Ltd v Beech [2003] NSWSC 638 at [9] support Mr King’s submission, as contended by him. In that paragraph, Master Macready said:

It can be seen from the provisions of s 208J(3) [of the Legal Profession Act 1987 (NSW)] to which I have referred earlier that a certificate of the Costs Assessor may achieve the status of a judgment. That happens when the certificate is filed in the appropriate registry of the court. Until then it merely has in effect as a determination, in other words a decision, on the amount of costs payable.

54 Mr King also relied on [18.32] of GE Dal Pont, Law of Costs, (3rd ed) and what is said there regarding s 368 of the Legal Profession Act 2004 (NSW). As noted above, I do not consider that that provision supports his submission.

55 In any event, I consider that the relevant issue here is not whether a debt immediately arises upon a Court making a costs order, as opposed to after costs have been assessed, but rather, the reasonableness of Ms Waters’ refusal to enter into discussions with the ATO with a view to agreeing an amount and thereby obviating the need for those costs to be assessed. Having regard to Ms Waters’ refusal to engage in any such discussions and that the costs remain unpaid, I do not consider that it is unreasonable of the ATO to seek security for costs in respect of the current proceedings with a view to protecting its position on costs in these proceedings. Ms Waters’ past conduct is a relevant consideration in the particular circumstances of the current case.

56 Secondly, I accept the ATO’s submission that the amount of security it seeks is not oppressive and is significantly less than the amount which the ATO is likely to receive on an assessment. I am satisfied that Ms Trembath provided sufficient details in her affidavit of how her estimate of the ATO’s costs of these proceedings was determined.

57 Thirdly, I accept the submission by Mr Glover (who appeared for the ATO) that the evidence indicates that Ms Waters is relatively impecunious. Indeed, Mr Coffey acknowledged as much in his affidavit and, in particular, in the limited information which he gave concerning Ms Waters’ financial and employment position, as outlined above. That information included the fact that Ms Waters is currently eligible for a Pensioner Concession Card and that for the income tax years 2012 and 2013, the tax withheld from Ms Waters’ income amounted to only $1,613 and $777 respectively. It might also be noted that Ms Waters failed to adduce any evidence relating to the following matters which would have given a clearer picture as to her current financial circumstances:

(a) the quantum of the restructured mortgage payments she is making in respect of her residence or the equity she has in that property;

(b) the quantum of outstanding fees owed to her current solicitors;

(c) the amount of the discounted legal fees the subject of her arrangement with her lawyers; and

(d) the fee arrangements regarding her Counsel.

58 In the circumstances of this case, I consider that Ms Waters had at least an evidentiary onus in respect of these matters, which are peculiarly within her own knowledge.

59 Fourthly, as I observed in Ninan at [37], an applicant who wishes to resist security for costs on the basis that there is causal connection between his or her impecuniosity and the respondent’s conduct needs to substantiate that claim by appropriate evidentiary material and not mere assertion or submission. In my view, Ms Waters has not discharged her onus of establishing that her relative impecuniosity was caused by the ATO’s conduct in circumstances where:

(a) it is now over nine years since the relevant alleged events occurred;

(b) Ms Waters resigned from the ATO on 19 November 2004, but then returned to work in the private sector on 5 November 2007;

(c) she is well qualified and she does not assert that her psychiatric illness prevents her from being employed; and

(d) in her statement of claim in the proceedings, Ms Waters pleads that her illness prevented her from working for only three of the ten years which have now elapsed since the conduct of which she complains occurred.

60 Fifthly, there is the important consideration of whether the making of a security for costs order would stultify the proceedings. As noted above, Ms Waters has the onus of making good her position on this issue. I am not satisfied that she has discharged that onus, particularly in circumstances where her own pleading claims that her illness has prevented her from working for only three of the ten years since she worked at the ATO. Nor does she contend that her psychiatric illness prevents her from currently being employed.

61 The only material put forward by Ms Waters in support of her submission that the making of the security for costs order would stifle the current proceedings is to be found in [76] of Mr Coffey’s affidavit, which is in the following terms:

Based on my own analysis, evidentiary material and information within my knowledge and the statements made in the foregoing paragraphs, I have formed the view that any security for costs would not only “stifle” the current proceeding in this court, but would actually “prevent” them being brought at all. Thus, the proceeding would be decided in the Respondent’s favour without the Applicant ever having had her complaints heard by any court.

62 Mr Coffey was not cross-examined on any of his evidence but, self-evidently, this particular paragraph warrants little, if any, weight. The nature of Mr Coffey’s “analysis” is unclear, as is the “evidentiary material and information” within his personal knowledge upon which he relies in expressing his opinion. It is also unclear precisely which “statements made in the foregoing paragraphs” Mr Coffey was referring to.

63 In circumstances where Ms Waters elected not to provide more detailed evidence as to her financial affairs (noting in particular the matters referred to in [57] above), and the objectively reasonable amount which is sought way of security, I am not satisfied that the making of the order will stifle the proceedings.

64 Sixthly, I do not consider that there are any relevant public interest considerations which point against the making of an order for security for costs. Merely because the ATO is a public authority does not mean that there is a public interest component in litigation which is brought by a disgruntled former employee. Nor do I consider that a sufficient public interest component is provided by the fact that Ms Waters raises complaints of contraventions of the Disability Discrimination Act. I consider that the subject matter of the litigation is very much in the nature of an inter partes dispute which has no appreciable public interest aspect.

65 The factors which point against the making of any security for costs order include the stability and consistency of Ms Waters’ place of residence. However, in the particular circumstances, I do not consider that this matter deserves much weight in the overall balancing exercise.

66 As noted above, her prospects of success are also relevant. The authorities indicate that, as a general rule, this is not the occasion for a major hearing on prospects (see Ninan at [39], citing Appleglen Pty Ltd v Mainzeal Corporation Pty Limited (1988) 79 ALR 634 and High Tower Pty Limited v Island Motel Pty Limited (unreported decision of von Doussa J, 12 April 1989)). The ATO submitted that her prospects are low, primarily because it contends that Ms Waters’ statement of claim remains defective. For example, the ATO contends that Ms Waters’ cause of action in respect of unlawful disability discrimination is deficient because her pleading fails to identify how the alleged unlawful discrimination disadvantaged her, or indicates which “requirement or condition” she is required by the ATO to comply with, which is the basis for her allegation of indirect discrimination. Nor does her pleading identify “a comparator” for all relevant purposes. The ATO also criticises that part of Ms Waters’ pleading which relates to her allegations concerning breach of contract and, in particular, its failure to address the Limitation Act 1969 (NSW) as well as the applicable statutory framework within the Australian Public Service for implying terms of the type that are raised by Ms Waters.

67 There may be some force in these submissions but, for the purposes of the interlocutory application, I am prepared to accept that Ms Waters has an arguable case (see Elshanawany at [17] per Jacobson J). This weighs in her favour, but it is not determinative of the interlocutory application. It needs to be weighed in the balance with all other relevant considerations.

68 Mr King also contended that the application for security for costs was brought for “a collateral purpose” because it was designed to stifle the current litigation and was oppressive in denying Ms Waters a right to litigate her substantive claims. I reject that submission. As found above, I do not consider that Ms Waters has established that the litigation will be stifled. I also consider that it is not unreasonable for the ATO to seek some protection in respect of its existing and future costs, having regard to the earlier litigation and Ms Waters’ conduct in relation to its outstanding costs.

Conclusion

69 Considering and weighing the totality of the circumstances here, I am satisfied that an order for security for costs should be made. A matter of particular relevance is Ms Waters’ past conduct in relation to the ATO’s outstanding legal costs and her failure fully to disclose her financial position. It is not unreasonable for the ATO to seek to have some limited protection insofar as its legal costs of the proceedings are concerned having regard to Ms Waters’ conduct in the previous litigation. Moreover, I consider that $30,000 as security for costs is not oppressive in the circumstances of this litigation, nor am I satisfied that the proceedings will be stultified if an order is made in that amount.

70 In my view, however, it is appropriate that the security be lodged with the District Registrar of the Court and a copy provided to the ATO’s solicitors, as opposed to the security being given directly to those solicitors. Ms Waters should have 21 days to arrange the security. I also consider that it is inappropriate at this stage to make an order that the proceedings be dismissed, or alternatively stayed, if security is not provided on or before the date so ordered. The proceedings should be stayed until security is given and, if Ms Waters defaults, it will then be open to the ATO to apply to have the proceedings dismissed or alternatively stayed. I do not think it is appropriate at this point to have a guillotine order.

71 No reason was given why costs should not follow the event.

I will make orders accordingly.

|

I certify that the preceding seventy-one (71) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Griffiths. |

Associate: