FEDERAL COURT OF AUSTRALIA

Murphy v Westpac Banking Corporation [2014] FCA 1104

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

Applicant | |

|

AND: |

Respondent |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 384 of 2010 |

|

BETWEEN: |

Stuart Moore Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 31 of 2010 |

|

BETWEEN: |

Danielle Lavars Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 90 of 2010 |

|

BETWEEN: |

Corey Wittenberg Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 690 of 2010 |

|

BETWEEN: |

William Lawson Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 1980 of 2011 |

|

BETWEEN: |

Lucky Poulos Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 1839 of 2011 |

|

BETWEEN: |

Paul Smith Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

DATE OF ORDER: |

|

|

WHERE MADE: |

THE COURT ORDERS THAT:

1. The parties are to seek to agree proposed short minutes of order which give effect to these reasons for judgment and also deal with costs by 11 November 2014.

2. If agreement cannot be reached, the parties should file and serve by 11 November 2014 their respective proposed short minutes of order together with an outline of written submissions in support, which are to be in normal font and format and must not exceed 20 pages.

3. The parties should indicate in their outline of written submissions whether or not they request a further oral hearing before final orders are made.

4. Liberty to apply on the giving of 48 hours' notice.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 1157 of 2009 |

|

BETWEEN: |

LOUISE MURPHY Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 31 of 2010 |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 384 of 2010 |

|

BETWEEN: |

Stuart Moore Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

BETWEEN: |

Danielle Lavars Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 90 of 2010 |

|

BETWEEN: |

Corey Wittenberg Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 690 of 2010 |

|

BETWEEN: |

William Lawson Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 1980 of 2011 |

|

BETWEEN: |

Lucky Poulos Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 1839 of 2011 |

|

BETWEEN: |

Paul Smith Applicant |

|

AND: |

WESTPAC BANKING CORPORATION Respondent |

|

JUDGE: |

GRIFFITHS J |

|

DATE: |

14 OCTOBER 2014 |

|

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

1 These proceedings involve claims by seven former employees of St George Bank (SGB) against Westpac Banking Corporation (Westpac), which formally merged with SGB on 1 March 2010. The proposed merger was announced in May 2008. As will emerge below, it set in train a series of events over the ensuing two years which give rise to the applicants' complaints relating to their employment with SGB.

2 Although there are important factual differences between the individual circumstances of each of the applicants, there is a considerable overlap in some of their claims, which are all employment-related. The claims arise under various causes of action, including in contract, the torts of deceit and negligence, as well as misleading or deceptive conduct under the Trade Practices Act 1974 (Cth) (the TPA). The proceedings were all heard together. It is convenient to publish reasons for judgment which cover all seven applications.

3 In broad terms, and putting to one side for the moment the fact that not every applicant makes the same claims, the following primary allegations are made:

(a) Westpac is liable to pay damages, including exemplary damages, because by letters dated 18 June 2008 which were sent to all the applicants (together with other SGB employees who were identified as SGB's most valuable employees), misrepresentations were made concerning the true target for the payment of a retention incentive. It is claimed that the misrepresentations created an inducement for each of the relevant applicants to remain in SGB's employ throughout the merger process, with the result that, when each of their employment relationship with SGB ultimately ceased (for one reason or another), they had missed the opportunity for alternative employment which had earlier been available to them. The relevant applicants rely on causes of action in contract, deceit, negligence and misleading or deceptive conduct in respect of the retention incentive. For convenience, these claims will be referred to as "the retention incentive scheme claims";

(b) SGB breached the individual contracts of employment of some of the applicants by:

(i) failing to pay those applicants bonuses under various SGB bonus schemes which were known as the Treasury Incentive Plan (the TIP), the Medium Term Treasury Incentive Plan (the MTIP), the Divisional Incentive Plan (the DIP) (which applied to Mr Poulos alone) and the Short Term Incentive Annual Opportunity (the STIA) (which applied to Ms Murphy alone);

(ii) not giving some of the applicants reasonable notice of the termination of their contracts of employment with SGB (the wrongful dismissal claim(s)); and

(iii) failing to calculate and pay some of the applicants the correct severance payment to which they were entitled when they were made redundant.

4 With one exception, Westpac defends all these causes of action. The exception relates to the claims in contract concerning non-payment of the retention incentive. Although these claims were initially denied by Westpac in its filed defence, the claims were conceded by it before the hearing started. The Court was informed that Ms Lavars and Messrs Moore and Poulos already have verdicts on their contract claims in the amounts of the sums individually promised to them under the retention incentive scheme, but costs are reserved. Ms Murphy and Messrs Lawson, Smith and Wittenberg seek a verdict to the same amount in respect of their contract claims. All the applicants say that the Bank's belated concession should attract costs consequences and they seek to be heard on that matter. They have foreshadowed that they will seek indemnity costs.

5 The trial was conducted over a period of approximately seven weeks. The parties tendered approximately 1500 pages of documents. Twenty-six lay witnesses gave evidence (and most were cross-examined). Three expert witnesses gave evidence and participated in a concurrent evidence session. The applicants' closing written submissions (including their written reply) totalled 374 pages. Westpac's closing written submissions totalled 489 pages. The parties handed up supplementary notes and/or submissions which totalled almost 200 pages. There were 2,057 pages of transcript.

6 It is convenient to now outline in more detail the lay evidence and claims made by the seven individual applicants, then outline Westpac's lay evidence before summarising the expert evidence. I will then describe the key issues and summarise the parties' respective submissions before setting out my consideration and determination of all relevant matters.

7 Accordingly, these reasons for judgment are structured as follows.

8 Mr Lawson is aged 46, is married and has two young children. He swore four affidavits and also gave lengthy oral evidence in chief after large parts of his affidavits were ruled inadmissible.

9 Mr Lawson began work as a fixed income trader in Melbourne in December 1990, when he was employed by Potter Warburg. In August 1992, he started work with SBC Dominguez Barry trading semi-government bonds. He subsequently worked for the National Australia Bank (NAB) in Melbourne from 1995-1998, after which he took up an appointment in Sydney with Credit Suisse First Boston (Credit Suisse) trading and market making in government bonds. His position was made redundant at Credit Suisse in January 2005 when its trading business was relocated to Hong Kong.

10 Mr Lawson commenced employment with SGB in July 2005 as Executive Manager, Non-Credit Trading. He received a total salary of $175,000 per annum. He joined SGB after being approached in April 2005 by Mr Ian Hamilton (Chief Manager, Financial Markets), whom he had known for approximately 15 years. He was interviewed by two senior SGB executives, Mr Peter Fitzgerald (General Manager, Institutional and Financial Markets) and Mr Hamilton.

11 Mr Lawson's original written contract of employment was set out in a letter dated 22 July 2005. It contained provisions dealing with annual performance reviews and the SGB Employee Reward Share Plan. The letter also dealt with the termination of his employment. That could occur by either Mr Lawson or SGB giving written notice. In particular, the letter stated that:

(a) his employment could be terminated by SGB giving him four weeks' written notice;

(b) at its discretion, SGB could make a payment of the equivalent amount in lieu of notice; and

(c) if Mr Lawson was over 45 years of age and had accumulated two years' continuous service when his employment was terminated, he would be entitled to an additional one weeks' notice.

12 The letter also stated that, by signing it, Mr Lawson agreed "to abide by the policies and procedures of St George as may be amended from time to time". This has important implications for the question whether various policies regarding redundancy and secondment developed by SGB either at or after his work commencement applied to him.

13 Mr Lawson's employment position with SGB subsequently changed. In September/October 2006 he was promoted to the more senior position of Head of Non-Credit Trading and his salary increased. As will be further developed below, his duties and responsibilities expanded with this promotion. Mr Lawson also received an increased base salary and other entitlements in the following Bank financial year, such that his total remuneration had doubled in two years. The nature and extent of these changes is relevant to a significant issue in the proceeding, namely whether his duties and status changed to such an extent that his original contract of employment was varied with the consequence that the original provisions dealing with such matters as notice of termination changed to reflect his new role.

14 Mr Lawson also contends that it was a term of his employment that he would be paid not only an annual or base salary, but also an annual bonus. Mr Lawson gave evidence that he was never provided with any written rules or terms relating to the annual bonus. He claims that this alleged term of his employment was conveyed to him prior to his recruitment by Messrs Fitzgerald and Hamilton. Mr Lawson contends that he was told and understood that the express purpose of the annual bonus was to provide him with a remuneration which, together with his base salary, was commensurate with market rates.

15 Mr Lawson gave evidence that in his performance review in September-October 2006, he was told by Mr Hamilton that he had been promoted to Head of Non-Credit Trading at SGB, for which his base salary increased from $175,000 to $240,000. In October 2007, his salary was further increased to $250,000 and his bonus for the Bank's financial year ending 30 September 2007 was $180,500 under the bonus scheme known as the IP.

16 By a letter dated 17 December 2007, Mr Lawson was invited to participate in another SGB bonus scheme, the MTIP. The MTIP was offered to the more senior executives of SGB and provided them with an opportunity to be allocated SGB shares. In Mr Lawson's case he was offered the opportunity to take up two equal tranches of shares up to a maximum value of $50,000, with the first tranche to be exercisable on or after 30 September 2009 and the second tranche to be exercisable on or after 30 September 2010. The MTIP operated to increase Mr Lawson's annual remuneration in a way which avoided any conflict with SGB's base salary increase restrictions. It was also intended to encourage participants to remain with the Bank. It might be interpolated here that in his written reply submissions, Mr Lawson accepted that he only received 90 per cent of his MTIP opportunity in 2007/2008, which reflected the fact that SGB did not achieve the 10 per cent EPS growth and as such the Group component of 20 per cent was reduced by half.

17 Mr Lawson worked in the Treasury Division of SGB's Institutional and Banking Division. He received annual bonuses under the TIP. The terms of the TIP were apparently not reduced to writing (save in respect of one year which affected Mr Wittenberg). Annual bonuses distributed under the TIP were derived from a bonus pool calculated by reference to Treasury's financial performance. If employment was terminated before a full year had been worked, a pro rata annual bonus would be paid. According to Mr Lawson, the annual bonus and awards under the TIP were both "regular and consistent" and were paid annually irrespective of performance, propositions which Westpac strongly denies. By a letter dated 31 October 2008, which was signed by Mr Bartlett, Mr Lawson was informed that his TIP bonus for the year ending 30 September 2008 was $250,000. He was informed that he would receive a payment of $250,000 under the TIP (payable in two equal tranches on May 2009 and November 2009 as long as he remained at SGB on those dates). He was also given information as to his MTIP entitlements as part of the 2007/2008 annual review and also for 2008/2009. His "MTIP opportunity" was stated to be $50,000. The letter also contained the following information on Mr Lawson's "Total Reward Opportunity":

Your Total Reward Opportunity for 2008/2009 will be as follows pending the outcome of the proposed merger with Westpac:

|

Total Employment Cost (TEC) (includes fixed salary and compulsory superannuation) |

$257,500 |

|

Medium Term Incentive Opportunity |

$50,000 |

|

Total Reward Opportunity (excluding Treasury Incentive plan) |

$307,500 |

You will continue to be eligible to participate in the Treasury Incentive Plan for 2008/2009.

Please be aware that your Total Reward Opportunity is an estimate only and the final amount depends on a number of factors including your individual performance and continued employment with the St. George Group. Your leave and all other entitlements are calculated on the basis of your Total Employment Cost.

18 Finally, Mr Lawson was informed that, because the Bank's EPS outcome was below 90 per cent of the target, the Board had determined that no additional incentive would be paid to anyone at SGB. The letter also dealt with the possibility of pro rata payments being made in the event of certain contingencies. These included the possibility that if, for example, the merger was implemented but Mr Lawson was not appointed to a permanent role with Westpac and left the organisation within six months, Westpac would make an ex-gratia payment calculated as a pro rata percentage of his MTIP target.

The merger announcement and its effect on Mr Lawson

19 As noted above, in May 2008, SGB announced its intention to merge with Westpac. Mr Lawson became very concerned about his job security and he gave evidence that he raised the matter with both Mr Hamilton and with Mr Fitzgerald. He gave evidence that Mr Fitzgerald assured him that a retention incentive scheme would be devised to reward key SGB executives. He said that Mr Fitzgerald told him that key staff were essential to the Bank whether or not the merger was finalised and that he and two other members of his team had been identified as key members for SGB's operations.

20 At around this time, Mr Lawson says that he was approached by senior employees at JPMorgan, who expressed interest in recruiting Mr Lawson and his team (including Mr Paul Smith and Mr Stuart Moore, who are also applicants in the proceedings). Mr Lawson says that he discussed this possibility with representatives of JPMorgan on behalf of himself, as well as his team at SGB. This evidence is relevant to the issue of alternative employment for these three applicants. Mr Lawson said that the JPMorgan representatives with whom he met were Messrs Mark Stephens (Director, Fixed Income Sales), Adrian Janschek (Vice-President of Fixed Income Sales) and David Ioannidis. The discussions took place after Mr Stephens had contacted Mr Lawson to inquire whether he and Messrs Smith and Moore would be interested in opportunities outside SGB given the proposed merger between Westpac and SGB.

21 Mr Lawson said that he attended a lunchtime meeting in early June 2008 with Messrs Stephens and Ioannidis, which was also attended by Mr Moore. At the end of the lunch, Mr Lawson was invited to pursue further discussions with JPMorgan and it was left to him to follow that up. Mr Lawson said that within a week of the luncheon meeting he had a further conversation with Mr Janschek. Mr Lawson said that Mr Janschek told him that he had been approached by Mr Ioannidis and another JPMorgan employee (Mr Jeff Herbert-Smith) to provide a reference check for Mr Lawson. Mr Janschek told Mr Lawson that he had recommended that JPMorgan employ Mr Lawson in its fixed income business. Mr Lawson also gave evidence that around this time he had a separate conversation with Mr Stephens, who informed him that he had given "a glowing reference" for Mr Lawson to Messrs Ioannidis and Herbert-Smith.

Mr Janschek's evidence concerning alternative employment opportunities for Mr Lawson

22 It is convenient at this point to summarise Mr Janschek's evidence, who was called as a witness by Mr Lawson. Mr Janschek said that he and Mr Lawson had worked together at Credit Suisse for four years up to January 2005. He confirmed that JPMorgan had approached Mr Lawson in circumstances where JPMorgan was hiring fixed income traders. He said that he had been approached in mid-June 2008 by Mr Ioannidis and Mr Herbert-Smith (with whom Mr Janschek had also worked), who inquired about Mr Lawson's abilities and suitability. Mr Janschek deposed that, while he did not recall the exact words he used, he had conveyed to them that Mr Lawson had made money at Credit Suisse and that he considered that he would bring significant advantages to JPMorgan's trading team. Mr Janschek also recalled Mr Lawson telling him in late June 2008 that he had decided to stay at SGB and not pursue the opportunity at JPMorgan. I accept this evidence.

23 Mr Janschek gave evidence, which I also accept, that JPMorgan was building up a new business division in the first half of 2008 and that he had been engaged by JPMorgan in May 2008 for that purpose in the position of Vice President, Fixed Income Sales and that other people were recruited by JPMorgan at that time as part of its expansion plans.

24 In cross-examination, Mr Janschek gave evidence that redundancies commenced at JPMorgan in December 2008, which were related to the global financial crisis (GFC). He said that the redundancies were "meaningful" and resulted in 20 per cent of his particular section within JPMorgan being made redundant. The redundancies continued in 2009. Mr Janschek also gave evidence that he played no role in the hiring or firing of employees at JPMorgan in 2008. I accept that evidence.

Mr Lawson is invited to participate in SGB's retention incentive scheme

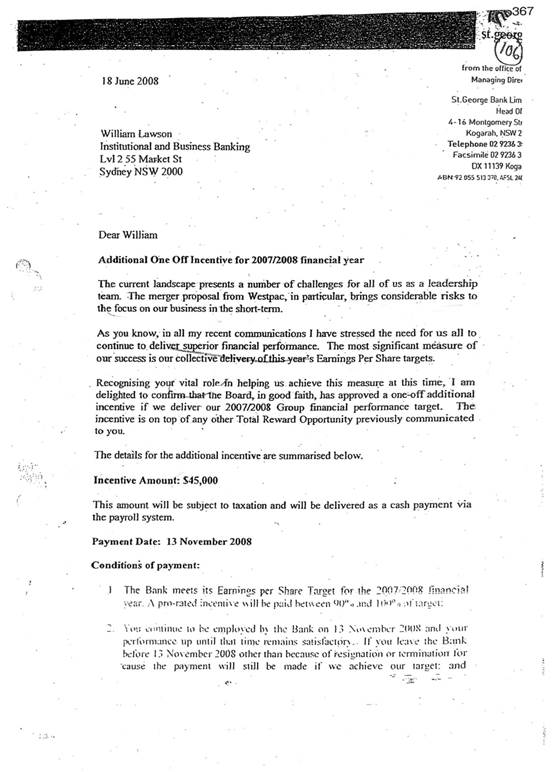

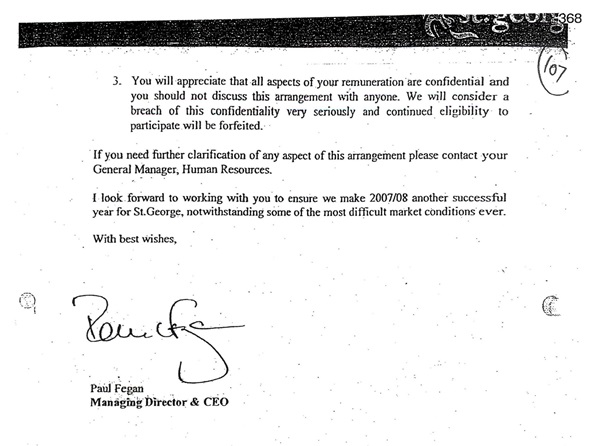

25 Mr Lawson gave evidence that his interest in possibly taking another job changed in mid-June 2008 when he was advised by SGB in a letter dated 18 June 2008 that he had been selected as a key executive within SGB to whom a retention incentive would apply in order to encourage him to stay with SGB during the implementation of the merger with Westpac. The letter was signed by the Managing Director and Chief Executive Officer of SGB, Mr Paul Fegan. In view of the importance of the letter, not only to Mr Lawson's case, but also to other applicants who received similar letters, it is convenient to set out the full text of the letter:

26 Mr Lawson and some of the other applicants contend that the letter was deliberately misleading and untrue in its references to achievement of SGB's "earnings per share target" insofar as the 2007-2008 financial year is concerned. The EPS growth target which was published to the market and to staff generally was originally said to be 10 per cent, but that was then later revised to a range of 8-10 per cent. Mr Lawson, and the other relevant applicants complain that, unbeknownst to them, the SGB Board had set a different EPS growth rate for the purposes of the retention incentive scheme at a level of 10.1 per cent. They complain that this was never disclosed to them at the relevant time and was known only to the SGB Board (which included Mr Fegan) and to four of the most senior SGB executives.

27 In his affidavit dated 29 October 2010, Mr Lawson deposed that he relied upon the retention incentive letter and the discussion he had with Mr Fitzgerald when the letter was handed to him in deciding to terminate his discussions with JPMorgan on behalf of both himself and his team. He said that if he had known the true position, he would not have remained with SGB during the merger process and rather would have pursued the opportunity with JPMorgan. Mr Lawson said that he accepted the truth of Mr Fitzgerald's statement that he had been identified as a key person for a role in the merged organisation and he added that this fact, together with the financial incentive, persuaded him to cease looking outside SGB for an alternative role. He also said that if he had known that the EPS target was 10.1 per cent and not 8-10 per cent, he would have discounted the incentive as being "effectively worthless". Mr Lawson gave evidence that he only became aware of the 10.1 per cent figure after the proceedings were commenced and he added that, if he had known that the true target was 10.1 per cent, he would have regarded the retention incentive "to be practically unachievable and therefore of no real value". As will shortly emerge, Mr Lawson was closely cross-examined on this and other parts of his evidence.

28 Mr Lawson also deposed that he was approached by senior executives of ING Investment Management around August 2008, who expressed an interest in recruiting him. He said that he did not pursue that opportunity for the same reasons as he gave for terminating his discussions with JPMorgan.

Mr Lawson's secondment to Westpac

29 Around 28 November 2008, Mr Lawson was informed by a letter written on SGB letterhead but signed by Ms Cathy Graycon (Managing Director - People, Westpac Institutional Bank) that he would be seconded to Westpac to occupy the position of Portfolio Manager - Strategic Risk. The letter included the following paragraphs:

In your role of Portfolio Manager - Strategic Risk you will be required to assist with work for the broader Westpac Group. As such, while you remain employed by your current employer, you will be seconded for the portion of the work that you do for the Westpac Group. The secondment arrangement is a requirement of our corporate structure following the merger.

During the secondment the employment policies of your employer would continue to apply to you. Some additional policies may also apply, for example, compliance policies related to the portion of work that you do on secondment. All other terms and conditions of your employment continue to apply, as varied by this letter.

The application of SGB's redundancy policies to Mr Lawson

30 An important issue in Mr Lawson's case is the SGB policies which applied to him. He claims that he was subject to the following policies:

(a) a redundancy policy entitled "St George Bank Limited Redundancy Policy" ("the 2001 Redundancy Policy") which provided that, upon termination through retrenchment, an employee would be paid a special lump sum severance payment in full settlement of all claims calculated as six weeks' salary in lieu of notice, seven weeks' for the first full year of service and three weeks' salary for each subsequent year or part year of continuous service. It further stated that the maximum payment would be 65 weeks' salary;

(b) a further redundancy policy which was published on SGB's intranet website (the HR Express Redundancy Policy) (note that Mr Lawson claims that he had been told by Mr Hamilton that this latter policy did not affect his entitlement to notice under the 2001 Redundancy Policy). Under that document, redundancy payments in respect of staff employed under the SGB Enterprise Agreement were described as comprising six weeks' pay in lieu of notice, seven weeks' pay for the first completed year of service, four weeks' pay for each subsequent year from two to ten completed years of service, three weeks' pay for each subsequent year from 11 to 16 completed years of service and two weeks' pay for each subsequent year to a maximum of 25 completed years of service, including the first year. In addition, such staff would receive one weeks' pay for each year over 45 years of age and pro rata pay for each completed month of work to a maximum of 85 weeks' pay (90 weeks for staff over 45 years old), including the six weeks' notice period; and

(c) a secondment policy (the Secondment Policy), which contained the following statements:

A secondment is a temporary transfer or promotion to another role for a minimum period of 6 weeks and a maximum period of 12 months. No extensions beyond 12 months are possible. Only permanent staff can be seconded to another role.

31 The Secondment Policy further stated that as a term and condition of any secondment, the seconded employee "must return to your original position, salary and conditions when the period of the secondment ends, unless you are appointed to the role to which you were seconded, or you are moved to another role".

32 Mr Lawson contends that it was an express term of the 2001 Redundancy Policy that, if his employment was terminated for redundancy, he would be paid a lump sum severance payment of up to a maximum of 18 months' salary, including a notice period. He says further that SGB's Managing Director and Chief Executive Officer, Mr Fegan, had a discretion to increase that notice period to reflect the applicable period of "reasonable notice", having regard to such matters as age, seniority, length of service and specialisation.

33 Mr Lawson also contends that it was an express term of the HR Express Redundancy Policy that he would receive a severance payment up to a maximum of 90 weeks' "pay", but without affecting his entitlement to reasonable notice under the 2001 Redundancy Policy and/or his common law entitlements to reasonable notice. Mr Lawson places particular emphasis on the use of the term "pay" instead of "salary" in the HR Express Redundancy Policy. He contends that the term "pay" described his total remuneration, which included not only his base salary but also his bonus entitlements.

34 On 1 March 2010 (which was after Mr Lawson's employment with SGB had been terminated by way of redundancy and retrenchment), the terms of the policy relating to retrenchment entitlements for those employees who were employed by SGB prior to the Bank ceasing to exist on 1 March 2010 were varied. The policy was varied so as to define "severance pay" as: "your fixed pay only and does not include any bonuses, incentives, commissions, overtime, superannuation or any other separately identified entitlement". Mr Lawson draws attention to these changes, which he contends did not reflect the earlier position when his employment with SGB was terminated.

35 Mr Lawson's secondment with Westpac commenced on 1 December 2008. He contends that his seconded position was different from his SGB position in that:

(a) his budget at Westpac represented a substantial additional burden to that which he had at SGB (his budget at Westpac was $3.3 million compared with a budget of $1.5 million which had been set for him at SGB around October 2008);

(b) his trading limits and reporting requirements differed;

(c) he no longer had any managerial responsibilities; and

(d) the bonuses were not comparable with those available to him at SGB.

36 Mr Lawson gave evidence of a telephone conversation which he had in early 2009 with Mr Harvey from SGB Human Resources in which he says he told Mr Harvey that he was concerned about his employment arrangements. He explained that that was because although he had been told that he was on secondment, he felt that he was being treated like a Westpac employee, having been allocated a Westpac budget, Westpac trading limits and Westpac reporting requirements. He said that he also told Mr Harvey that he had been advised that he would be remunerated under the Westpac bonus scheme and not the SGB bonus scheme. He said that Mr Harvey told him that he was working on the matter with Westpac. Mr Lawson gave further evidence that Mr Harvey subsequently told him in around April or May 2009 that he was involved in the process of selecting employees who would be employed by Westpac but that he was unable to tell him anything more about the topic.

37 Mr Lawson also gave evidence that from at least February 2009 onwards, he regularly made inquiries with a view to clarifying the employment status at Westpac of both himself and Messrs Moore and Smith. He said that he did not get any response to those inquiries.

38 Mr Lawson gave evidence of bonus payments he received while he was working at Westpac. By a letter dated 3 December 2009, which was written on SGB letterhead and signed by Mr James Land from Westpac, Mr Lawson was told that given the results of his 2009 remuneration review, he would receive a $60,000 bonus for the three months that he had worked at SGB and zero bonus for the period he was seconded to Westpac. Mr Lawson also gave evidence of a discussion he had with Mr Land in late October or early November 2009 regarding his performance review. He said that Mr Land told him that he had been rated as an employee who needed development because he did not meet his Westpac budget. Mr Lawson added that Mr Land was unable to tell him whether that would have any impact to his entitlement under SGB's MTIP.

39 Mr Lawson gave evidence of another conversation he had with Mr Land in early December 2009 in which he was told by Mr Land that he would not be receiving any payment or entitlement under the MTIP because he had been rated as an employee who needed development under the Westpac Performance Review Scheme. Mr Lawson complained to Mr Land that he considered that he was entitled to receive the MTIP because his SGB budget for the year was $1.5 million and that he had achieved that budget for the period that he was working at SGB. He said that Mr Land responded by saying that he would not receive any MTIP, that he had been taken off the MTIP scheme and that he would not be given an equivalent plan at Westpac.

40 Mr Lawson gave further evidence which responded to an affidavit sworn by Mr Doyle on behalf of Westpac. Mr Doyle worked at Westpac. Mr Lawson denied that Mr Doyle ever told him that the percentage based bonus system for the Strategic Risk Group (SRG) at Westpac was "discretionary". He also denied ever being told by Mr Doyle that there was no incentive scheme for the SRG for 2008/2009, or that bonuses for that year would be paid at Westpac's discretion.

41 Mr Lawson contends that the duties relating to his secondment position at Westpac amounted to a substantial and radical change to his terms and conditions of employment. As noted above, this issue bears upon the question whether the terms of his original contract of employment, including the notice period to which he was entitled, were replaced or varied to reflect his changed employment role.

42 On 14 December 2009, Mr Lawson was advised both by letter and orally by Mr Doyle that Westpac would close its SRG and, consequently, that his seconded position was redundant. He was also told that he would start a period of redeployment in which other employment opportunities within Westpac would be explored, taking into account his skills, experience and interests. He was advised that the redeployment period was expected to be six weeks starting on 15 December 2009 and concluding no later than 29 January 2010. By a further letter dated 28 January 2010, Mr Doyle informed Mr Lawson that his redeployment period would be extended by a further week until 5 February 2010, during which time other employment opportunities would be sought for him.

43 Mr Lawson's employment was ultimately terminated by way of retrenchment on 5 February 2010. Mr Lawson received a redundancy payment of $93,903, representing 19 weeks at the rate of his base salary only. He also received a further payment on account of notice of $107,083 (representing five months' notice and, again, calculated only by reference to his base salary and not his annual bonuses).

Cross-examination of Mr Lawson

44 Mr Lawson was subjected to a lengthy cross-examination. One of the prominent issues in that cross-examination was his claim that he had been told that his annual bonuses would be "regular and consistent". I found his evidence on this topic at times to be inconsistent and uncertain. Mr Lawson initially said that he had been told that he would receive 100 per cent of his base salary as an annual bonus. He later modified that to say that he had been told that he would receive "around" 100 per cent. Initially, he created the impression that he had received repeated assurances about his receiving an annual bonus both before and after he took up his employment with SGB. Ultimately, however, when pressed during cross-examination, he accepted that he had only ever been told that in his pre-employment discussions with Mr Hamilton. I accept that evidence.

45 Another topic on which he was closely cross-examined concerned the proposition that the payment of the annual bonus depended upon a range of factors, which included an individual employee's own performance as well as SGB's overall performance. Initially, Mr Lawson seemed reluctant to accept that proposition. He was then taken to [3] of his statement of claim and to the reference there to the "engagement conversations" he had with Mr Hamilton and to the claim there that his remuneration would be made up of a base salary and variable annual bonuses. It was put to him that the use of the word "variable" must mean that his annual bonus could fluctuate according to various performance criteria. Initially, Mr Lawson resisted that obvious proposition. His response was that all he had to do to get his annual bonus was to receive a competency rating, which he explained simply meant achieving a level of base competency. Mr Lawson had some difficulty recollecting the different ratings which were apparently attributed to SGB employees, including himself, as part of the annual performance reviews. He was taken to the review which he had completed in respect of Mr Stuart Moore, who was a member of his team at SGB. Mr Lawson accepted that he had had responsibility for filling out the manager's comments in that review, although Mr Hamilton also had some involvement. Mr Lawson acknowledged that he had rated Mr Moore as exceptional, which was the highest grade. When it was pointed out that Mr Moore had received a 120 per cent bonus that year (against his base salary), Mr Lawson acknowledged that it was because Mr Moore had had a "stupendous" year. This confirmed that which Mr Lawson seemed reluctant to acknowledge, namely that an employee's personal performance had an important bearing on the quantum of any bonus he or she received.

46 Mr Lawson was also asked a series of questions in cross-examination relating to the fact that in his first year at SGB, he had received an annual bonus which represented only 60 per cent of his base salary. He was asked why he did not complain that he had not received around 100 per cent given his earlier evidence to the effect that that is what he had been told. Mr Lawson responded by saying that he did not complain and that he was happy with the bonus he received.

47 Mr Lawson was then asked to comment on the fact that, in the following year, he received an annual bonus which represented only 75 per cent of his base salary. He was asked to comment on the proposition that this indicated the variability of his annual bonus and that he had obviously performed better personally in the second year, thereby receiving an increase of approximately 15 per cent in his annual bonus. Mr Lawson was reluctant to respond directly to that proposition. He simply repeated that he was grateful to receive any bonus and that he was happy with it. I found this part of his evidence to be unconvincing and difficult to reconcile with his central claim concerning the assurances he said he was given about the level of the annual bonus which he could expect to receive. I also consider that the evidence demonstrated that annual bonuses were not guaranteed as claimed by Mr Lawson. In my view, his resistance to the proposition that annual bonuses were tied to individual performance and were variable did not reflect well on his credibility.

48 Other aspects of Mr Lawson's evidence cast further doubts about his credibility. One such area concerns the cross-examination in respect of a letter dated 22 November 2007 which he received from Mr Bartlett at SGB. That letter informed him that he had received an annual bonus of $180,500. It also confirmed that he was invited to participate in the MTIP. A condition of such participation was that he would need to enter into a service agreement, a copy of which would be sent to him shortly. He had no recollection of ever receiving or executing any such service agreement. The letter foreshadowed that Mr Lawson would be entitled to three months' notice under that service agreement, which is a period significantly less than his claim to be entitled to receive a period of notice of at least 15 months. When confronted with that letter, Mr Lawson rather unconvincingly said that he did not pay close attention to the details of the letter and simply focused on the numbers. This arose in the context of Mr Lawson saying that he did not appreciate the qualifications expressed in that letter which explicitly stated that payment of the bonus was subject to achievement of certain conditions, including performance and that there was no guarantee involved. In my view, it is difficult to accept that Mr Lawson would not have shown close interest in the detail of these matters, impacting as they did directly on his personal remuneration, which must have been a matter of particular concern to him.

49 Another topic on which Mr Lawson was closely cross-examined related to the nature of the discussions he had had with representatives of JPMorgan. Mr Lawson confirmed that during the two-hour luncheon in early June 2008, there was no discussion at all of conditions of employment or salary if Mr Lawson left SGB and joined JPMorgan.

50 During further cross-examination, Mr Lawson was asked various questions about how his conduct would have changed if he had been aware at the relevant time that the EPS target for the incentive program was 10.1 per cent. He said had he known that he would have looked for jobs elsewhere. He was asked repeatedly to explain why that was so in circumstances where he never raised any written or oral complaint about the fact that he was told by letter on 31 October 2008 that no additional incentive would be paid to anyone at the Bank. When he was pressed he said that the reason why he would have looked elsewhere was because he would not have had confidence in his future at SGB. I found his answers on this topic to be unconvincing and insufficient by themselves to demonstrate that he would not have remained with SGB save for the retention incentive scheme described in the letter dated 18 June 2008 which he had received.

51 Mr Lawson was also asked a series of questions regarding the Westpac bonus system and whether or not he was told that the previous bonus system at SGB would not apply to his time at Westpac. Mr Lawson's evidence was to the effect that he had been told by various Westpac executives, including Messrs Land, Doyle and Wilson, that his bonus when at Westpac would be 12.5 per cent of revenue up to a figure of $5 million and then 15 per cent above that. He said that he was told by Mr Land that the Group hurdle was $2 million and that those figures would apply. Mr Lawson was then cross-examined on an email he had received from Mr Wilson where he told that there was no contractual arrangement in place concerning bonuses. When shown that document, Mr Lawson agreed that he never challenged that proposition but said that whatever might have been recorded in writing was overtaken by what he had been told orally. It might also be noted that Mr Lawson received another letter, which was to similar effect and indicated that there was no contractual commitment to receive a bonus and that all that was offered was on the basis of "best endeavours".

52 As indicated above, I have some reservations concerning Mr Lawson's credibility. They highlight the need to view his evidence carefully. In the absence of objective corroborating evidence, I am reluctant to accept Mr Lawson's evidence at face value.

53 Ms Lavars swore two affidavits dated 4 November 2010 and 20 February 2012 respectively. She also gave oral evidence in chief after large parts of her affidavits were ruled to be inadmissible. Ms Lavars was cross-examined.

54 Ms Lavars commenced employment with SGB around September 1998, after she was approached by an executive search firm. She was employed in the position as an Account Manager in the margin lending area of SGB and was employed pursuant to a letter of offer dated 10 August 1998. The letter made express reference to her being covered by the policies and procedures of SGB as set out in the Bank's Corporate Manual. Her "total employment cost" (TEC) was stated to be $45,000. She was informed that TECs were generally reviewed annually, with adjustments effective from 1 October each year and with an annual performance review. The letter also stated that Ms Lavars' employment could be terminated on the giving of four weeks' notice (or payment in lieu of notice).

55 Although Ms Lavars was initially appointed to the position of Account Manager, her position changed several times thereafter as follows (noting also that she was never provided with a replacement written contract of employment):

(a) in early 2000, she was promoted to the position of Manager, Institutional Sales in SGB's Treasury Division, and she received a bonus each year in which she was employed within Treasury;

(b) in 2002, she took on the additional position of Cash Dealer;

(c) in 2004 she took on a new position assisting in developing the Financial Institutions Group of SGB, which consisted of establishing relationships with contacts and other banks;

(d) in 2005-2006 she returned to the position as a Senior Manager in the Institutional Sales Section of the Treasury Division, at which time she reported to Mr Hamilton. She also became more active in the marketing of SGB funding programs and was responsible for the day-to-day distribution of relationships for particular programs in which the Bank was a panel member; and

(e) from 2006, she reported to Mr Wittenberg and, while she continued to perform her institutional sales functions, she also assisted Mr Wittenberg in expanding the origination capabilities of the Bank. Her client list was expanded to include financial borrowers.

56 Ms Lavars deposed in her first affidavit that, during the course of her pre-employment interview with Ms Michelle Davies, she was told that at SGB she would receive a base salary and a bonus which would be payable at the end of each year. She recalled receiving a bonus of $2000 to $3000 at the end of her first year with SGB.

57 Ms Lavars also gave evidence of the circumstances surrounding her transfer to the dealing room. She said that she had a meeting with Messrs Fitzgerald and Hamilton about the possibility of her transferring to that area and that, during the course of the meeting, Mr Hamilton told her that she would be remunerated by way of a base salary together with an annual bonus. She said that he explained to her that because Treasury could not match the big base salaries paid by other investment banks and that because there was also a cap on base salary increases, the bonus was used "to ensure that you are kept up to the market for the role that you perform within Treasury".

58 Ms Lavars gave evidence as to what she was told regarding her base salary and annual bonus under the TIP. She said that she attended annual reviews and annual meetings with either Mr Fitzgerald or Mr Hamilton and she was told on these occasions that she would be paid a bonus to keep her position at market remuneration levels and that the amount of the bonus she would receive took into account not only her individual performance but also the performance of the dealing room. She gave evidence that she was told that annual bonuses were allocated from a bonus pool, calculated by reference to the financial performance of the Treasury Division and that the levels of bonuses were determined by Messrs Hamilton and Fitzgerald.

59 Ms Lavars says that her annual bonuses were regular and substantial and that she received an annual bonus each year of her employment.

60 Ms Lavars also gave evidence of a meeting which she had with Mr Fitzgerald on 18 June 2008, during which he handed her a copy of the 18 June 2008 letter offering her the incentive retention scheme. She said that he told her that the Bank was offering incentives to key people to have them stay with the Bank during the merger and due diligence period.

61 Ms Lavars also gave evidence that she was aware from market announcements that the earnings per share growth target for SGB for 2007/2008 was 8-10 per cent. She said that she had to know that figure in order to provide investor updates on SGB's performance. She said that she understood from the terms of the 18 June 2008 letter that the retention incentive would be paid to her if SGB met its earnings per share growth target of 8-10 per cent.

62 Ms Lavars said that she was told by Mr Jim Fingleton on or around 13 November 2008 that she would not receive a retention incentive. It was only after the proceedings were commenced that she learned that the target for the retention incentive scheme was in fact 10.1 per cent.

63 On 31 October 2008, i.e. several months after the proposed merger was announced, Ms Lavars received a letter which informed her that she would continue to be eligible to participate in the TIP for 2008-2009.

64 Ms Lavars also gave evidence of various meetings she had with Mr Fitzgerald from around October 2008 regarding the prospects for SGB employees arising from the proposed merger. She said that he told her that the merged organisation would provide a greater opportunity for her than was currently available at SGB. She said that Mr Fitzgerald also told her that there would be "contestable positions" if an employee's role at SGB was repeated at Westpac and that she would be notified if she was to contest one of those positions. She gave further evidence that Mr Fitzgerald told her in mid-November 2008 that there was a contestable position in the merged organisation in rate sales. She said that she told Mr Fitzgerald that she did not like her chances because she was working in credit sales but that he said that it was the only contestable position available to her.

65 Ms Lavars said that she was unsuccessful in obtaining a position in rate sales.

66 Ms Lavars also gave evidence of a job interview which she had with Mr Simon Ling for a role in the originations area of the Debt Capital Markets section (DCM) of Westpac. Mr Ling held the position of Executive Director, DCM - Debt and Hybrid Securities. Ms Lavars said that she was advised by Mr Ling on 28 November 2008 that her application for the position was successful. Ms Lavars received a letter dated 1 December 2008, written on SGB's letterhead by Ms Graycon (Managing Director, WIB-People) appointing her to the position of Manager, DCM-Debt & Hybrid Securities at Westpac, but stating that she would continue to be employed by SGB. Her secondment letter, which was in similar terms to secondment letters received by other relevant applicants, contained the following paragraphs:

In your role of Manager, DCM-Debt & Hybrid Securities you will be required to assist with work for the broader Westpac Group. As such, while you remain employed by your current employer, you will be seconded for the portion of the work that you do for the Westpac Group. The secondment arrangement is a requirement of our corporate structure following the merger.

During the secondment the employment policies of your employer would continue to apply to you. Some additional policies may also apply, for example, compliance policies related to the portion of work that you do on secondment.

All other terms and conditions of your employment continue to apply, as varied by this letter.

(Emphasis added).

67 Ms Lavars gave evidence, which I accept, that shortly after she received this secondment letter, she reviewed the Secondment Policy which was on the HR Express intranet site. She observed that the maximum period for any secondment was 12 months. The policy also stated that no extensions beyond 12 months were possible.

68 The relevant terms of the Secondment Policy as at this time were as follows.

Secondment

A secondment is a temporary transfer or promotion to another role for a minimum period of 6 weeks and a maximum period of 12 months. No extensions beyond 12 months are possible. Only permanent staff can be seconded to another role.

Secondments can be advertised or negotiated directly with individual staff members.

If you are seconded to another position you must be informed of and agree to the terms and conditions of the secondment in a secondment letter of offer.

Secondment terms and conditions

• You are expected to work the hours and work pattern that apply to the secondment role.

• You are paid the minimum salary (non-package staff) or TEC/TR (package staff) for the grade of the position you are seconded to and are automatically paid the appropriate rate from the start date of the secondment.

• Any additional allowances that apply to the secondment role are paid from the start date of the secondment and any allowances from your original role from the start date of the secondment.

• You must return to your original position, salary and conditions when the period of the secondment ends, unless you are appointed to the role to which you were seconded or you are moved to another role.

• St George can vary secondment end dates within the agreed timeframe for any reason by giving you one week's notice, or by setting a new end date by mutual agreement.

69 It is to be noted that the Secondment Policy refers in its terms only to a secondment for a temporary period - it does not contemplate a secondment for a permanent period. As will emerge below, this issue assumes some importance in Ms Lavars' case because in October 2009 the Secondment Policy was amended by SGB by the addition of the following paragraph immediately before the heading "Secondment terms and conditions":

Clarification of Scopy (sic) of Policy - St George / Westpac merger

This policy does not apply to employees who are employed in a permanent position following the St George/Westpac merger and who, as part of that permanent position, undertake some or all of their duties for another Westpac Group company. This is the case even if the duties which the employee provides for another Westpac Group company have been described as a "secondment". This is because this policy is limited to "secondments" under which an employee is not undertaking duties as part of their permanent work, but rather is seconded to another role on a temporary basis.

70 In her oral evidence in chief, Ms Lavars said that she discussed the secondment letter with Mr Fitzgerald and he told her that, because of the speed of the merger between Westpac and SGB, they were not able to offer her a contract and a secondment was the only way forward, but that she might expect to negotiate a contract later. Ms Lavars recollected Mr Fitzgerald saying that she had a "foot in the door". I accept that evidence.

71 Ms Lavars commenced her secondment with Westpac on 2 December 2008 in her new role. She said that from that point onwards she only performed duties for Westpac and marketed products under the Westpac banner and brand. She said that she was provided with a business card bearing the name and logo of Westpac and that her email signature also indicated Westpac and not SGB. She said that, although her remuneration continued to be paid by SGB, she did not do any work for SGB. As far as she was aware, all wholesale funding operations of the Treasury Division of SGB had ceased to operate from 1 December 2008. From and after 2 December 2008 all her work functions were performed at Westpac's premises in Kent Street, Sydney. She said that her duties at Westpac were exclusively concerned with originations and that she performed none of the sales functions that had been a major part of her work at SGB. Instead of liaising directly with investors, as she had done at SGB, her work in originations involved liaising with issuers, i.e. the other banking institutions who sought to raise money. The bonuses she was to earn were less attractive than at SGB and she says that she would not have accepted the secondment if she had been told about the substantial changes to her bonus entitlements. I accept that evidence.

72 In her oral evidence in chief, Ms Lavars said that while she worked at Westpac she reported to Mr Ling. She gave evidence of a discussion about her remuneration which she had with Mr Ling in November 2009 after he asked her what her pay and bonus had been the previous year at SGB. She told him $250,000 and $150,000 respectively. She said that Mr Ling told her that he did not think that she would be paid those amounts at Westpac. She said that she responded by saying that she was still employed by SGB and not Westpac. I accept that evidence.

73 Ms Lavars also gave oral evidence in chief concerning another conversation she had with Mr Ling a few weeks later relating to her bonus. Her evidence was to the effect that Mr Ling told her that she had got a reasonably high bonus relatively speaking and that he had tried to get her $100,000, but his management capped her bonus at $80,000. Ms Lavars said that she was very disappointed about that because she had performed well at Westpac and she believed that she would have done better under the SGB bonus scheme. Ms Lavars said that she was accepted into the Westpac incentive plan around November 2009. I accept that evidence.

74 Ms Lavars also gave evidence of a conversation she had with Ms Renee Bissett around February 2009. Ms Bissett worked in Human Resources at Westpac. Ms Bissett told Ms Lavars that she had to remain an SGB employee on secondment to Westpac until Westpac was able to give her a new contract, but that could not happen at that stage and had to await the surrender of the SGB banking licence. She also gave evidence that she was given similar information by other Westpac employees at a focus group meeting held on 28 April 2009. She said that at that meeting, Ms Kellie Penridge from Westpac said that Westpac would not be offering full time contracts to SGB staff members before the full merger had gone through and the SGB banking licence had been surrendered. She said that Ms Penridge explained that this situation arose because if Westpac offered contracts of employment to SGB staff at that time, Westpac would have to pay stamp duty on the transfer of the staff as they were classified as assets, and that would cost the Bank a substantial amount of money. I accept that Ms Lavars was told these things.

75 Ms Lavars gave evidence, which I also accept, of several conversations she had with Mr Ling about her dissatisfaction arising from the fact that she remained on secondment and was uncertain about her future because she did not know when she would receive a written contract of employment with Westpac. In an email dated 12 August 2009, Mr Ling told Ms Lavars that, despite her secondment to Westpac "it would seem that you are seconded to Westpac with no time limit although I am sure we will sort that out over time" (emphasis added). He attached another email from Ms Bissett which stated that Ms Lavars was not working with Westpac on a temporary secondment basis. Ms Bissett added in her email that the SGB Secondment Policy had no application to Ms Lavars because Ms Lavars had not been "temporarily moved or promoted to another role, she had been directly appointed to the role of Manager, DCM - Debt & Hybrid Securities" at Westpac.

76 Ms Lavars also gave evidence concerning a letter which she received from Mr Bartlett on or around 31 October 2008 which informed her of her bonus for 2007/2008. The letter was written on SGB's letterhead. She was advised that she would receive a TIP payment of $150,000, payable in two tranches on May 2009 and November 2009, and conditional on her remaining employed by SGB. She was advised that her total employment cost (including fixed salary and superannuation) was $205,000 and that she would continue to be eligible to participate in the TIP for 2008/2009.

77 By a later letter dated 3 December 2009, which was also written on SGB letterhead, Ms Lavars was informed of the results of her 2009 remuneration review. She was told that her total employment cost remained at $205,000. She was further advised that she had been awarded a total amount of $80,000 under the TIP, which amount would be payable in two equal tranches in May and November 2010 respectively. She was told that those payments were subject to her "continuous employment" with the Westpac Group. Finally, it was confirmed that, for the performance year beginning 1 October 2010, "you will move from your current St George variable reward scheme to the WIB Reward framework" and that further information on that framework could be found on the WIB intranet page.

78 Ms Lavars gave evidence that she never agreed to the change in her employment contract which had the effect of removing her from the SGB bonus scheme and that she would not have accepted the position set out in the letter dated 1 December 2008 if it amounted to employment with Westpac but without a written contract setting out the terms and conditions of her employment with Westpac. I accept that evidence.

Ms Lavars' desire to return to SGB after 12 months at Westpac

79 Ms Lavars gave evidence that, in accordance with her understanding of the terms and conditions of the Secondment Policy, she was to return to SGB and to her original position after 12 months on secondment. She said that as she did not wish to continue to work in the DCM Originations position at Westpac, she gave notice to Mr Ling by letter dated 26 November 2009 that she would report to SGB on 2 December 2009, which was the day after the 12 months secondment period ended. In her letter, she also stated that because the Treasury Division within SGB was no longer active, it would be necessary for SGB to provide her with comparable and appropriate alternative employment.

80 By letter dated 27 November 2009, which was written on SGB letterhead, Ms Lavars was advised by Mr Ganesh Chandrasekkar (Acting Managing Director WIB - People), that her employment with SGB was ongoing and that there would be no change as at 1 December 2009 to the role to which she had been appointed by the letter dated 28 November 2008 (sic). (There was no such letter adduced in evidence: the only relevant letter is that dated 1 December 2008). She was further advised that her employment "will continue to be subject to your existing St George terms and conditions of employment" and that she should continue to report to the same office where she had been working for the previous 12 months.

81 Ms Lavars gave evidence that she had a meeting on 27 November 2009 with Ms Amanda Matehaere (who worked in Westpac's Human Resources area), during the course of which she was told by Ms Matehaere that her position was on going, that she was not on secondment and that she was required to continue in the role to which she had been appointed. Ms Lavars said that she pointed out that her letter of appointment had said that she was on secondment and that the terms of her employment at SGB would not change. She also drew attention to the fact that she had been taken off the SGB TIP and moved over to the Westpac incentive bonus scheme, something to which she never agreed and which had resulted in a reduction of $70,000 in her remuneration. She said that Ms Matehaere directed her to attend work in her existing role at Westpac and that, if she declined to do so, Westpac would terminate her employment. I accept that this is what Ms Lavars was told.

82 Ms Lavars also gave evidence, which I accept, of another meeting which she attended with Ms Karen Silk (another Westpac human resources employee) and Ms Bissett on 1 December 2009, during which Ms Silk told her that the Secondment Policy was inapplicable to the position she was performing at Westpac. Ms Silk said that this was a permanent position and that if Ms Lavars did not report to work after 1 December 2009 her employment would be terminated. Ms Lavars said that she responded by saying that that was inconsistent with what was set out in the letter dated 28 November 2008 (sic).

83 Ms Lavars said that on 2 December 2009 she reported for work at the SGB office at 55 Market Street, Sydney, where she had previously worked. She had a conversation with an employee in the SGB Human Resources area and was told that SGB did not want to be involved in a dispute about the nature of her employment and that it was being handled by Westpac. I accept that evidence.

84 Ms Lavars received a letter dated 3 December 2009, which was written on SGB letterhead and signed by Mr Chandrasekkar. The letter rehearsed the history of the matter, including the secondment letter dated 1 December 2008. It noted that Ms Lavars had not attended work the previous day and had provided no valid reason for her absence. She was again directed to report to the Westpac offices at 275 Kent Street and to continue working in the position as Associate Director, DCM-Debt & Hybrid Securities and that if she failed to do so, SGB would regard her non-attendance as providing a basis for summary termination. She was told that if her employment was terminated in this way, she would receive no payment in respect of notice and that she would be ineligible to receive any 2009 variable reward because she would no longer remain employed by SGB. All she would receive was her unpaid salary and accrued leave entitlements.

Termination of Ms Lavars' employment

85 By a letter dated 8 December 2009, also written on SGB letterhead, Mr Chandrasekkar advised Ms Lavars that her employment with SGB had been summarily terminated, effective 10 am on 4 December 2009 and that, in view of "the seriousness" of her conduct, she would not be paid salary in lieu of notice for the termination of her employment, but that all other entitlements would be processed through the usual payroll systems. Ms Lavars gave evidence that she was not paid any redundancy or termination payments by SGB, however, she did receive her annual and long service leave entitlements. I accept that evidence.

Ms Lavars' understanding about SGB bonuses

86 In her further oral evidence in chief, Ms Lavars described her understanding of the pool from which SGB bonuses were paid. She gave evidence of conversations she had had with Mr Fitzgerald and Mr Hamilton on that topic. Ms Lavars could not recall the timing of those conversations but she thought they were in the context of her annual reviews. She said that Mr Fitzgerald told her that the pool was there from year to year and flowed over so as to pay "consistent bonuses".

87 When she was asked to explain her understanding of what she had to do in order to qualify for a bonus, Ms Lavars said she understood that she needed to perform her job to a competency level. She said the source of that information was Messrs Fitzgerald and Hamilton. Ms Lavars said that she had been told by Mr Fitzgerald that the annual bonus was paid to ensure that SGB met market value in terms of overall remuneration. She says that she was told that she had to be competent and also remain employed at SGB in order to get the bonus. Ms Lavars also explained that she understood that the bonus was drawn from the pool but she did not know the ins and outs of its operation. I accept her evidence.

Cross-examination of Ms Lavars

88 In cross-examination, Ms Lavars was asked a series of questions on the topic of whether she was angling to get a redundancy from around mid-2008. She was taken to an email dated 25 June 2008 which she sent to a friend in which she made reference to redundancy. Ms Lavars said that at the time she was ebbing and flowing on whether she wanted redundancy and that it was a volatile time for everyone because of the uncertainty. Ms Lavars also said that she had been at SGB for ten years and ended up getting no redundancy payment.

89 Ms Lavars was taken to a letter dated 10 July 2008 in which she was given a guaranteed bonus for 2007/2008 of $150,000. That was a considerable improvement on her earlier bonuses for previous financial years, which were $85,000 for 2006 and $95,000 for 2007. She received the $150,000 in two tranches, the second payment being in November 2009. Ms Lavars said that she understood that she was an important employee because she was in the funding wing of SGB at a difficult time and was successful in attracting funds to the bank. I understood this to be a reference to a risk that she may have been "poached" by a rival business. She also said that at this time she moved into a "slightly different role" and her salary had increased by $25,000. I accept that evidence.

90 In further cross-examination, Ms Lavars was asked some questions about her understanding of the nature of her employment and whether she was on temporary or permanent secondment. When it was put to Ms Lavars that she understood that Westpac's position was that she had been seconded to Westpac for an indefinite time, she responded by saying that the SGB Secondment Policy had a 12 month cap and she had been informed in the secondment letter that that Policy continued to apply to her. When it was put to Ms Lavars that she continued to work at Westpac on the basis of her understanding that the Bank believed that she had been seconded for an indefinite period, she said she continually asked whether she would be offered a contract of employment. She was told by Mr Ling that that ultimately would happen. It was put to her that the time taken to move to a single ADI prevented that from occurring within her timeframe.

91 Ms Lavars was then taken to an email dated 9 November 2009 which she had sent to her sister and in which she makes a reference to her "trying to angle today for a redundancy". It appears that she sought and obtained legal advice at about this time. It was put to her that Westpac wanted her to stay pending the finalisation of the merger but that she was angling for redundancy. She said that she wanted a contract. She was taken to her statement in the email to being "trapped" and it was put to her that she could have left. She explained that it was not as easy as that because she would have forfeited her bonus because she had to stay in employment in order to obtain it. She said that she wanted to get terms and conditions of employment at Westpac which were similar to those which she enjoyed at SGB. I accept all that evidence.

92 Ms Lavars was then asked in cross-examination about her knowledge of the SGB Secondment Policy as it appeared on the HR Express website towards the end of 2009. She said she was unsure whether she had access to the website at that time.

Broad outline of Ms Lavars' claims

93 In his opening, Mr Neil SC (who appeared for the applicants together with Mr O'Dowd and Mr Shariff) submitted that the issues which arise in respect of Ms Lavars are:

(a) was her position with SGB redundant and, if so, was she entitled to payment in accordance with the applicable redundancy policies;

(b) what are the correct bases for calculating her entitlements, i.e. should the bonus entitlements be included and should her entitlements be calculated against her total remuneration of both base salary and bonuses or only base salary;

(c) is she entitled to a pro rata annual bonus for the part of her final year of service, including her time with Westpac on secondment and, if so, in what amount;

(d) is she entitled to damages for failure to provide a reasonable period of notice;

(e) what are her rights arising from her secondment and what effect did the secondment have on her ongoing employment with SGB;

(f) is she entitled to be compensated for SGB's misleading or deceptive conduct in relation to the 18 June 2008 letter;

(g) alternatively, did SGB repudiate her contract of employment and, if so, what damages is she entitled to; and

(h) is she entitled to exemplary damages?

94 Although it was said in opening that the retention incentive scheme was a "feature" of Ms Lavars' case, it later emerged that in fact Ms Lavars' only claim in respect of that scheme was in contract (which the Bank ultimately conceded) and that she did not press any claim in relation to the scheme under the TPA or in tort.

95 Mr Moore swore three affidavits (dated 9 November 2010, 20 February 2012 and 10 August 2012 respectively) and, with leave, also gave lengthy oral evidence in chief after large parts of his affidavits were ruled inadmissible. He was cross-examined.

96 Mr Moore commenced employment with SGB in August 1994. Mr Moore gave evidence of a meeting he had in August 1994 with Mr Craig Busch (then Head of Foreign Exchange at SGB) regarding him switching to SGB from the ANZ Bank, where he worked in the financial markets area and then, subsequently, in the dealing room as a trader. He was employed by SGB pursuant to a letter of offer dated 1 September 1994. The letter offered Mr Moore a position with SGB as senior foreign exchange dealer and he was told that his employment could be terminated by the giving of four weeks' notice or the payment of salary in lieu thereof. His annual salary was $70,000.

97 Mr Moore also gave evidence that, up until 2002, he participated in performance reviews with Mr Busch at SGB, during which his performance was discussed and his budget and plans for the next financial year were settled. Mr Moore gave evidence that his remuneration over the previous five years was as follows:

|

Base |

Bonus |

MTIP | |

|

2003/2004 |

$220,500 |

$150,000 |

$68,000 |

|

2004/2005 |

$237,737 |

$160,000 |

$68,000 |

|

2005/2006 |

$247,000 |

$180,000 |

$68,000 |

|

2006/2007 |

$256,880 |

$190,000 |

$68,000 |

|

2007/2008 |

$264,586 |

$220,000 |

$68,000 (sic) |

|

2008/2009 (Westpac) |

$264,568 |

$ 53,280 |

Nil |

98 Mr Moore deposed to a conversation he had with Mr Busch during the course of his annual review in October 2001. He was told that, because his base salary was falling behind the market, he would be brought into the MTIP in order to help bring his total remuneration up to market. He was told that he could only receive the MTIP in shares and that there were performance hurdles which were linked to the earnings per share growth targets of SGB. Mr Moore said that he had always received an MTIP of $68,000 and that the last such payment he received was in October 2008. It should be interpolated at this point that Mr Moore subsequently accepted that his MTIP figure in the table above is incorrect for 2007/2008, when he received $61,200 in circumstances where SGB did not achieve the 10 per cent EPS growth and the Group component of 20 per cent was reduced by half.

99 Mr Moore deposed that he began reporting to Mr Fitzgerald rather than to Mr Busch in 2003 and that his annual reviews continued with Mr Fitzgerald. He also said that he sat down each year with Messrs Fitzgerald, Busch or Hamilton to review base salaries and bonuses for Treasury staff from the previous year and what was available for the next year. They discussed what amounts should be paid to individual employees in Mr Lawson's team by way of a bonus to provide a total remuneration which was at market.

100 In 1996, Mr Moore was appointed to the position of Manager of Foreign Exchange Trading and, the following year, he was appointed the head of that area and had four traders reporting to him. In late 2006 or early 2007 he was promoted to the position of Head of the Currency and Option Trading Group, at which time he had only one person reporting directly to him but immediately before that, he said that nine staff were reporting to him.

101 Mr Moore gave evidence that he became concerned about his job security when the merger was announced in May 2008 and he had numerous discussions on that topic with Messrs Fitzgerald and Hamilton. He said that they assured him that there would be opportunities for him in the merged organisation.

102 Mr Moore also gave evidence of a meeting he had with Mr Fitzgerald around 18 June 2008, when he was handed a copy of the 18 June 2008 letter. He said that he was aware at that time that the EPS growth target for 2007/2008 was 8-10 per cent. He also said that it was only after the proceedings were commenced that he became aware that the Board had set a target of 10.1 per cent. He said that he considered that target to be "unachievable" and that there was never a prospect of the one-off payment being paid to him.

Mr Moore's secondment to Westpac

103 Mr Moore also gave evidence relating to the circumstances of him being seconded to Westpac. He said that he was told by Mr Edie of Westpac that there was a position available there as a proprietary trader in the foreign exchange area. In response to a question from Mr Moore, Mr Edie said that there were two options under Westpac's bonus arrangements. An employee could elect to be on a percentage of what they earn or, alternatively, they could be part of a general pool. He said that Mr Edie recommended the latter option because, even if the individual employee did not have a good year, he or she could still participate in the bonus scheme if the trading room did well.

104 By letter dated 28 November 2008, which was written on SGB's letterhead, Ms Graycon wrote to Mr Moore and confirmed his "direct appointment to your new role of Proprietary Trader", but said that he would continue to be employed by SGB. The letter contained substantially similar paragraphs to those set out above in respect of Mr Lawson and Ms Lavars concerning the continuation of their employment with SGB while on secondment to Westpac, as well as the continuing application of SGB's employment policies during the secondment.

105 Mr Moore gave evidence that he accessed a copy of the Secondment Policy on the SGB HR Express intranet site and that he understood that his secondment would be for a maximum period of 12 months in accordance with that Secondment Policy. I accept that evidence.

106 In his further oral evidence in chief, Mr Moore was asked some questions about the 28 November 2008 secondment letter. He said that Mr Fitzgerald handed him the letter, he read it and then said to Mr Fitzgerald that he was only being seconded and it was not a permanent appointment. Mr Moore also said that Mr Fitzgerald told him that Westpac was not able to give permanent positions to SGB employees and could only use secondees, and that the terms and conditions of his employment at SGB continued to apply to him. I accept that evidence.