FEDERAL COURT OF AUSTRALIA

Garrett v Deputy Commissioner of Taxation [2014] FCA 576

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

First Applicant ACN 133 861 579 PTY LTD (IN LIQUIDATION) (CONTROLLER APPOINTED) Second Applicant | |

|

AND: |

DEPUTY COMMISSIONER OF TAXATION Respondent |

|

DATE OF ORDER: |

|

|

WHERE MADE: |

THE COURT ORDERS THAT:

1. The originating process filed 7 May 2014 be dismissed.

2. The applicant is to pay the respondent’s costs of the proceeding, including reserved costs, such costs to be taxed in default of agreement.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

|

VICTORIA DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

VID 198 of 2014 |

|

BETWEEN: |

ANDREW MORTON GARRETT First Applicant ACN 133 861 579 PTY LTD (IN LIQUIDATION) (CONTROLLER APPOINTED) Second Applicant |

|

AND: |

DEPUTY COMMISSIONER OF TAXATION Respondent |

|

JUDGE: |

DAVIES J |

|

DATE: |

5 JUNE 2014 |

|

PLACE: |

MELBOURNE |

REASONS FOR JUDGMENT

Introduction

1 ACN 133 861 579 Pty Ltd (in liquidation) (controller appointed) (previously known as OenoViva (Australia & New Zealand) Pty Ltd) (“the company”) was wound up in insolvency on 22 January 2014 on the application of the Deputy Commissioner of Taxation (“DCT”). The applicant (“Mr Garrett”) has applied under s 482 of Corporations Act 2001 (Cth) (“the Act”) to have the liquidation of the company terminated. A preliminary issue has arisen as to whether Mr Garrett has standing to make that application.

Does Mr Garrett have standing to bring the application?

2 By s 482(1A) of the Act, the application to terminate the winding up of the company can only be made by the liquidator, or a creditor or contributory of the company. Mr Garrett initially claimed standing to make the application as the “managing controller” of the company but conceded, correctly, that his claimed status as “managing controller” of the company did not give him standing under s 482(1A). Mr Garrett also claimed to have standing to make the application as a creditor and as a contributory of the company.

3 For the reasons that follow, Mr Garrett has not demonstrated that he has standing either as a creditor or as a contributory of the company.

Whether Mr Garrett is a creditor of the company

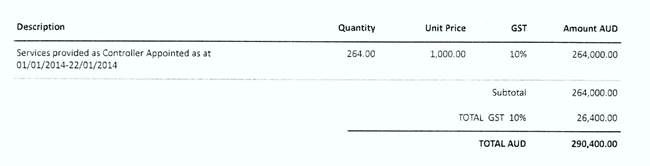

4 Mr Garrett claimed that the company owes him for work that he performed for the company before it went into liquidation. He supported his claim by presenting tax invoices issued to OenoViva (Australia & New Zealand) Pty Ltd as Trustee for the Andrew Garrett Family Trust No 3. The invoices are in similar form and each stated that the invoices were for “Services provided as Controller”. An example (extracted) is annexed to these reasons for decision as annexure A, being the tax invoice issued to OenoViva (Australia & New Zealand) Pty Ltd as Trustee for the Andrew Garrett Family Trust No 3 bearing the date 22 January 2014. When asked about the services provided, Mr Garrett said that the company had appointed him managing controller of 57 companies in the exercise of its rights under charges provided by those companies and that he was entitled under the terms of his appointment to bill the company for his services as managing controller. Mr Garrett also said that the amounts invoiced were brought to account in the company’s accounts. When asked to identify what those accounts were and where the charges were brought to account, Mr Garrett referred to the item “Bad Debt Expense” in the 1 July 2013 to 14 April 2014 Profit and Loss statement for “the trustee for The Andrew Garrett Family Trust No 4”. When asked who prepared those accounts, Mr Garrett advised that he had himself prepared those accounts with the assistance of his bookkeeper.

5 I am not satisfied on the state of the evidence that Mr Garrett is a creditor of the company as claimed. The evidence that he relies on is far from satisfactory and his claim that he is a creditor of the company is unsupported by probative evidence. The tax invoices containing the general description of “Services provided as Controller” are at best a bare assertion of indebtedness and are insufficient proof of the existence of debts owed by the company to Mr Garrett and there is no corroborating evidence to show that the invoices are genuine and that there are debts owed by the company to Mr Garrett. The profit and loss statement to which Mr Garrett referred does not constitute independent corroborative evidence of the existence of any debt actually owed by the company to Mr Garrett first, because Mr Garrett prepared them himself and, secondly, because that profit and loss statement does not of itself show that any amount is owed by the company to Mr Garrett. Moreover, unexplained was why such charges, if they were brought to account, appear in the profit and loss statement of the trustee of the Andrew Garrett Family Trust No 4 when the work was claimed to have been performed for, and the invoices were rendered to, the company as trustee for the Andrew Garrett Family Trust No 3.

6 Mr Garrett’s claim to be a creditor is also inconsistent with other evidence that is before the Court, namely that:

(a) it is apparent from an email dated 6 May 2014 from the liquidator to Mr Garrett that the liquidator has received only two proofs of debt, neither of which is from Mr Garrett and that Mr Garrett has not lodged a proof of debt in respect of the amounts claimed to be owed to him in the liquidation of the company; and

(b) in the Report as to Affairs of the Company that Mr Garrett himself prepared, signed on 19 March 2014, and filed with the Australian Securities Investments Commission (“ASIC”) in his stated capacity as the managing controller of the company, he has recorded “nil” unsecured creditors of the company.

7 In the circumstances, I do not accept the tax invoices as proof of the existence of debts owed by the company to Mr Garrett and reject his claim that he is a creditor of the company.

Whether Mr Garrett is a contributory of the company

8 Mr Garrett also claimed to be a contributory of the company. He supported his claim by producing a Declaration of Trust that Mr Christopher Paul McCarthy holds 100 ordinary shares in the company (under its former name) upon trust for Mr Garrett in his capacity as trustee of the Andrew Garrett Family Trust No 4. The Declaration of Trust was said to have been made on 9 January 2009. The copy produced to the Court is unexecuted but Mr Garrett provided a reason as to why it is that he was not able to produce an executed copy of the declaration.

9 I do not accept the document furnished to the Court as proof that Mr Garrett is the beneficial owner of shares in the company as he claims. First, the claim that Mr Garrett holds any shares is inconsistent with an extract of the records maintained by ASIC with respect to the company obtained on 7 February 2014. That record shows that the company has only ever had two issued shares, not the 100 shares that Mr McCarthy purports to hold on trust for him. The record also shows that of the two shares, one is held by Mr McCarthy and the other by a Mr Ibrahim Saeed and that both persons are recorded as beneficially owning their shares. Secondly, Mr Garrett did not tender any independent corroborative evidence showing that any share is held by him beneficially. In view of the inconsistent corporate records and the absence of any independent corroborative evidence, I am not satisfied that Mr Garrett is a contributory of the company.

Is the proceeding an abuse of process?

10 The DCT, with the consent of ASIC, provided to the Court a letter that ASIC sent to Mr Garrett on 23 October 2012 reminding Mr Garrett that he is disqualified from taking part in the management of a corporation for a period of five years from 22 October 2010, being the date of his conviction for contravening s 140 of the Criminal Law Consolidation Act 1935 (SA). The disqualification is automatic under s 206B(1)(b)(ii) of the Act. By s 206A of the Act it is an offence if a person who is disqualified from managing corporations:

(a) makes or participates in making decisions that affect the whole or a substantial part of the corporation; or

(b) exercises the capacity to affect significantly the corporation’s financial standing; or

(c) communicates instructions or wishes (other than advice given by the person in the proper performance of functions attaching to the person’s professional capacity or their business relationship with the directors or the corporation) to the directors of the corporation;

(i) knowing that the directors are accustomed to act in accordance with the person’s instructions or wishes; or

(ii) intending that the directors will act in accordance with those instructions or wishes.

11 The DCT submitted that this application by Mr Garrett is an abuse of process because he is contravening s 206A by acting as the managing controller of those companies to which he purports to have been appointed. On the face of the evidence before me there appears to be some substance to the submission that by acting as managing controller of those companies Mr Garrett is in contravention of s 206A. However, given my conclusion that Mr Garrett does not have standing to bring this application it is unnecessary to form any concluded view on whether Mr Garrett is in contravention of s 206A for the purpose of determining whether the proceeding is an abuse of process. The application is to be dismissed because Mr Garrett does not have standing to bring the application. Further, given that s 206A is a strict liability provision (pursuant to s 206A(1A)), I also consider that it is inappropriate in the present case to make any such finding. Whether there has been a contravention of s 206A is a matter that ASIC will be able to investigate.

Conclusion

12 As Mr Garrett has no standing to bring the application to terminate the winding up of the company the application will be dismissed.

|

I certify that the preceding twelve (12) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Davies. |

Associate:

Annexure A