FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v GDK Financial Solutions Pty Ltd (No 16) [2014] FCA 274

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

|

AND: |

GDK FINANCIAL SOLUTIONS PTY LTD (IN LIQUIDATION) (ACN 085 488 311) (AND OTHERS IN ACCORDANCE WITH THE ATTACHED SCHEDULE) Defendant |

|

DATE OF ORDER: |

|

|

WHERE MADE: |

THE COURT ORDERS THAT:

1. The Mews Receivers are authorised to draw from the Receivership Account (as defined in paragraph 9(b) of the Orders of the Court dated 13 March 2008) the amount of $61,283.25 on account of income tax owing to the Australian Taxation Office by the Mews Scheme for the financial years ending 30 June 2012 and 30 June 2013.

2. The Mews Receivers’ costs of the application for the approval sought by paragraph 1 of these orders are costs properly incurred in the exercise of their duties and powers as receivers of the Mews Scheme.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

|

VICTORIA DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

VID 590 of 2006 |

|

BETWEEN: |

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff |

|

AND: |

GDK FINANCIAL SOLUTIONS PTY LTD (IN LIQUIDATION) (ACN 085 488 311) (AND OTHERS IN ACCORDANCE WITH THE ATTACHED SCHEDULE) Defendant |

|

JUDGE: |

DODDS-STREETON J |

|

DATE: |

25 MARCH 2014 |

|

PLACE: |

MELBOURNE |

REASONS FOR JUDGMENT

1 On 25 February 2014, I made the orders set out above “on the papers”.

2 On 28 November 2006, Mark Francis Xavier Mentha and Brian Keith McMaster were appointed joint and several receivers of the Mews Land improvements thereon and related development rights and approvals for the purposes of winding up the Mews Scheme (as defined in the orders of Finkelstein J dated 28 November 2006 in these proceedings) (“the Mews Receivers”).

3 The Mews Scheme and the history of relevant litigation is described more fully in, inter alia, Re GDK Financial Solutions Pty Ltd and Others; Australian Securities and Investments Commission v GDK Financial Solutions Pty Ltd (2006) 236 ALR 699; [2006] FCA 1415 at [4]-[15] and Australian Securities and Investments Commission v GDK Financial Solutions Pty Ltd (No 10) [2011] FCA 1496 at [2].

4 On 20 December 2013, the Mews Receivers sought orders that:

1. The Mews Receivers are authorised to draw from the Receivership Account (as defined in paragraph 9(b) of the Orders of the Court dated 13 March 2008) the amount of $61,283.25 on account of income tax owing to the Australian Taxation Office by the Mews Scheme for the financial years ending 30 June 2012 and 30 June 2013.

2. The Mews Receivers’ costs of the application for the approval sought by paragraph 1 of these orders are costs properly incurred in the exercise of their duties and powers as receivers of the Mews Scheme.

5 Simon Harris, a director employed by KordaMentha, is responsible for the day to day conduct of the file associated with the receivership of the Mews Scheme and reports to and receives instructions from the Mews Receivers.

6 By an affidavit sworn on 19 December 2013, Mr Harris deposed that on or around 16 August 2011, the Australian Taxation Office (“ATO”) issued a private ruling with authorisation number 1011809364137 (“the ATO Ruling”) which, inter alia, provided that the Mews Scheme is required to lodge tax returns.

7 Mr Harris deposed that the Mews Receivers engaged Ernst & Young to prepare the income tax returns for the Mews Scheme for the years ending 30 June 2012 and 30 June 2013 in accordance with the ATO Ruling.

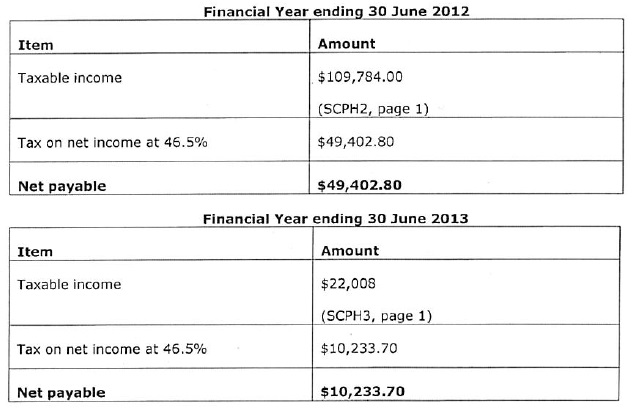

8 Mr Harris exhibited to his affidavit the notice of assessment from the ATO for the financial year commencing 1 July 2011 and ending 30 June 2012 stating an amount payable of $51,049.55.

9 Mr Harris exhibited to his affidavit the tax return lodged with the ATO on behalf of the Mews Scheme for the financial year commencing 1 July 2012 and ending 30 June 2013. The tax return included a taxation estimate from Ernst & Young, estimating that a tax payable of $10,233.70.

10 The net tax payable or refundable for each of the financial years ending 30 June 2012 and 30 June 2013 is calculated as follows:

11 Mr Harris deposed that the Mews Scheme’s total tax liability is $61,283.25, calculated by adding together the net tax payable for the financial years ending 30 June 2012 and 30 June 2013.

12 In 2012, the Mews Receivers applied for, and were granted, order authorising them to pay a tax liability of $272,095.67 owed by the Mews Scheme to the ATO for the financial years ending 30 June 2008, 30 June 2009, 30 June 2010, and 30 June 2011: Australian Securities and Investments Commission v GDK Financial Solutions Pty Ltd (No 12) [2012] FCA 1035.

13 In the light of the material filed in support, I was satisfied that it was appropriate to make the orders sought.

|

I certify that the preceding thirteen (13) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Dodds-Streeton. |

Associate:

SCHEDULE TO PARTIES

Receivers of the Mews Scheme: (Ashurst, Perth) - Brian McMaster and Mark Mentha

Plaintiff: AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION

First Defendant: GDK FINANCIAL SOLUTIONS AND INVESTMENTS COMMISSION

Second Defendant: WINDSOR VILLAGE MANAGEMENT PTY LTD (IN LIQUIDATION) (ACN 088 339 913)

Third Defendant: WESTERN RETIREMENT VILLAGE MANAGEMENT PTY LTD (ACN 091 443 239)

Fourth Defendant: THE MEWS VILLAGE NOMINEES PTY LTD (IN LIQUIDATION) (ACN 091 526 224)

Fifth Defendant: PERIDON MANAGEMENT PTY LTD (IN LIQUIDATION) (ACN 088 322 276)

Sixth Defendant: ROSEDALE VILLAGE NOMINEES PTY LTD (IN LIQUIDATION) (ACN 089 667 096)

Seventh Defendant: PETER HASTINGS WARNE

Eighth Defendant: RENTAL FLEETS AUSTRALIA PTY LTD (ACN 082 558 978)

Ninth Defendant: JOHN MONTGOMERIE

Tenth Defendant: ANDREW REGINALD YEO (TRUSTEE OF BANKRUPT ESTATE OF ROHAN ELLIOT VON STANKE)

Eleventh Defendant: GIUSEPPE DE SIMONE

Twelfth Defendant: SEACHANGE MANAGEMENT PTY LTD (ACN 091 443 211)

Thirteenth Defendant: ZMB AUSTRALIA PTY LTD (ACN 105 746 067)

Fourteenth Defendant: YOUNG TURKS PTY LTD (ACN 005 872 122)

Fifteenth Defendant: TOUMA PTY LTD (ACN 124 195 366)

Sixteenth Defendant: PHILLIP CLEMENTS