FEDERAL COURT OF AUSTRALIA

Merost Pty Ltd v CPT Custodian Pty Ltd [2014] FCA 97

| IN THE FEDERAL COURT OF AUSTRALIA | |

| MEROST PTY LTD (ACN 005 272 346) (AS TRUSTEE FOR CD BURGESS FAMILY TRUST) Applicant | |

| AND: | CPT CUSTODIAN PTY LTD (ACN 077 870 243) (AS CUSTODIAN FOR CENTRO MCS 5) Respondent |

| DATE OF ORDER: | |

| WHERE MADE: |

THE COURT ORDERS THAT:

1. The respondent pay the applicant the sum of $260,000.

2. The question of any orders consequential on these reasons for judgment, including orders for costs, is reserved.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

| VICTORIA DISTRICT REGISTRY | |

| GENERAL DIVISION | VID 14 of 2012 |

| BETWEEN: | MEROST PTY LTD (ACN 005 272 346) (AS TRUSTEE FOR CD BURGESS FAMILY TRUST) Applicant |

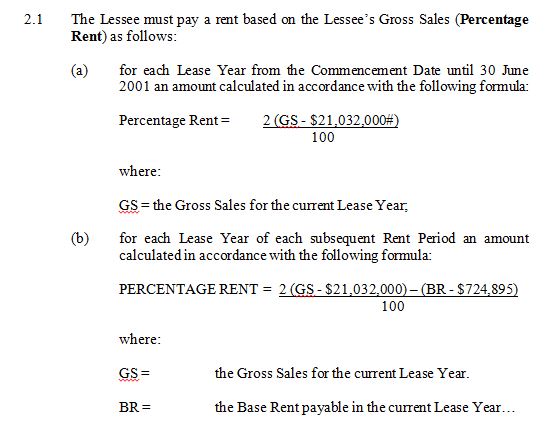

| AND: | CPT CUSTODIAN PTY LTD (ACN 077 870 243) (AS CUSTODIAN FOR CENTRO MCS 5) Respondent |

| JUDGE: | NORTH J |

| DATE: | 19 FEBRUARY 2014 |

| PLACE: | MELBOURNE |

REASONS FOR JUDGMENT

introduction

1 The applicant, Merost Pty Ltd (Merost), purchased a shopping centre from the respondent, CPT Custodian Pty Ltd (Centro). In this proceeding Merost relies on s 18(1) of the Australian Consumer Law (the Australian Consumer Law) to claim that Centro misled it about the amount of rent payable by the major tenant of the shopping centre. As a result of that conduct Merost claims that it has suffered loss and damage amounting to $700,000.

2 Centro denies that the pleaded conduct was misleading or deceptive, denies that Merost relied on it in the decision to purchase the shopping centre, and denies that the conduct was the cause of any loss or damage. Then, in reliance on s 137B of the Competition and Consumer Act (Cth) 2010 (the Act), Centro argued that if Merost suffered loss and damage, such loss and damage was caused or contributed to by Merost itself. The amount of damages should be reduced by the extent of the contributory negligence of Merost. Then, in reliance on s 87CD of the Act, Centro argued that, if it is liable to Merost, then Abrahams Meese Lawyers (AML), the solicitors for Merost, independently caused the loss or damage, and that Centro’s liability to Merost should be reduced proportionately.

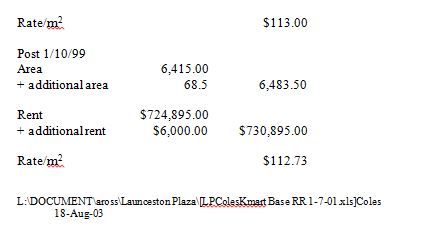

the evidence

3 Oral evidence was given for Merost about the circumstances of the transaction by Christopher David Burgess, the director of Merost, and the person who negotiated the purchase of the shopping centre.

4 Mr Burgess engaged Ingrid Alexandra Filmer to assist him in making calculations concerning the financial performance of the shopping centre. Ms Filmer is the Director of Asset Management at Burgess Rawson, a commercial real estate agency. The agency was founded by Mr Burgess in 1975, but he retired from active involvement in that business about two years ago.

5 An expert report relating to the value of the shopping centre at the date of acquisition was provided to Merost by Timothy John Perrin, who also gave oral evidence on the issue. Mr Perrin is a director of Burgess Rawson.

6 Thomas Lance Forrest gave evidence for Centro. He is the Manager, Property Transactions, and administered the sale of the shopping centre for Centro.

7 An expert report relating to the value of the shopping centre was prepared for Centro by Stephen Ross Thomas, a valuer with CBRE Valuations Pty Ltd. Mr Thomas also gave oral evidence on the subject.

8 An expert report relating to the obligations of the solicitor acting for a purchaser such as Merost in a transaction like the present was prepared for Centro by Peter Van Manser, a barrister practising in Hobart with past experience as a solicitor in transactions of that nature. He also gave oral evidence on the subject.

9 An agreed court book was filed containing all the documents relevant to the proceeding.

the facts

10 The facts were in many respects uncontroversial. The following description of the circumstances constitutes findings of fact made on the evidence before the Court.

11 The shopping centre is about two kilometres from the CBD in Launceston, Tasmania. It sits on a site of approximately 3.5 hectares. It has two major tenants, namely, Kmart which operates a discount department store, and Coles which operates a supermarket. There are eight speciality tenancies, two kiosks and two ATMs. Together the two major tenants, Kmart and Coles, account for about 80 per cent of the rental revenue.

12 The case concerns the terms of the Kmart lease (the lease). The lease commenced on 29 November 1999. It was for a term of 11 years, 7 months and 2 days, expiring on 30 June 2011. The lease provided for three five year options thereafter.

13 The rent had two components, a base rent and a percentage rent. The base rent commenced at $730,895 per annum until 30 June 2006. It was reviewed then every five years. At the review the base rent was fixed at one third of the total of the base rent and percentage rent in the three years immediately preceding the review date. By early 2011 the base rent had increased to $876,041. The next scheduled rent review was on 1 July 2011.

14 The percentage rent was calculated in accordance with a formula set out in cl 2.1(b) of schedule B of the lease as follows:

15 Central to the issues in this case is a variation of cl 2.1(b) of schedule B of the lease (the variation) which was in the following form:

[D]eleting the letters and figures ‘2(GS – $21,032,000) – (BR – $724,895)’ in clause 2.1(b) and substituting ‘2(GS – $24,311,569) – (BR – $730,895).

16 The variation was executed on 8 December 2009 and registered in the Tasmanian Land Titles Office on 21 May 2010.

17 The significant effect of the variation was to increase the figure to be deducted from gross sales in the percentage rent equation from $21,032,000 to $24,311,569 (the breakeven figure). The breakeven figure was a component of the calculations of the figure from which the two per cent percentage rent would commence to be paid. The effect of the variation was that, by increasing the breakeven figure, the amount of rent which would have been payable under the original form of the lease was reduced, because the two per cent percentage rent was payable on a gross sales figure reduced by a larger deductible. The variation also increased the amount of the rent deductible from the base rent from $724,895 to $730,895.

18 The conduct of Centro which Merost alleges was misleading and deceptive was to publish, in an information memorandum distributed to potential purchasers of the shopping centre, a breakeven figure of $21,032,000 for the lease when the correct figure was $24,311,569. It is now necessary to outline the relevant circumstances relating to the transaction.

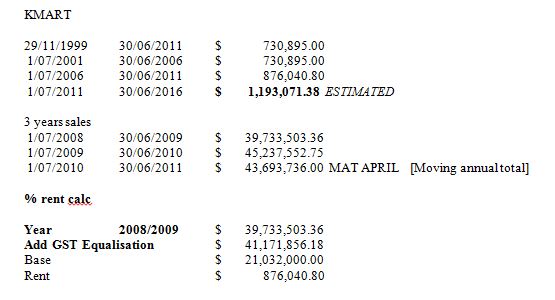

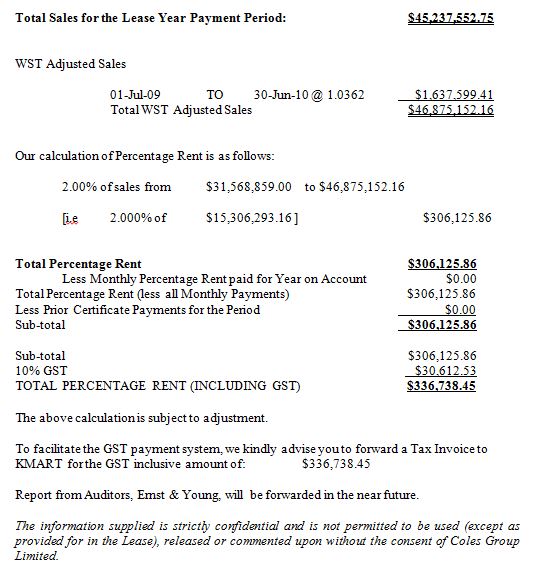

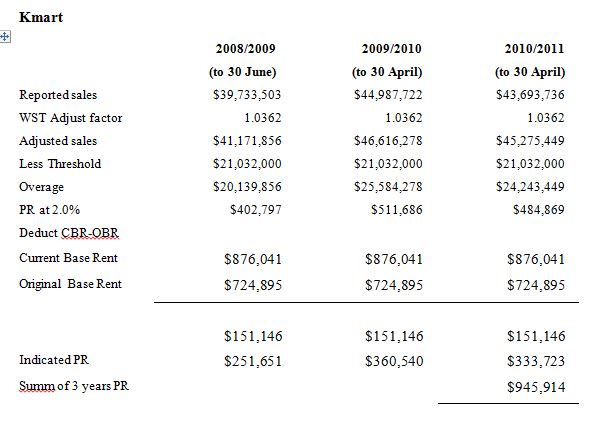

19 Mr Burgess grew up in Launceston and his parents live there now. He became aware that Centro was selling the shopping centre. He knew Mr Forrest and rang him late in 2010 to enquire about the proposed sale of the shopping centre. Mr Forrest said that the sale was not yet ready to proceed but that it would be going ahead shortly. Then, in April 2011, Mr Burgess was put in touch with Knight Frank, Tasmania which had been appointed selling agents. It was shortly after that he obtained the information memorandum prepared by Knight Frank. The information memorandum had been prepared by Knight Frank on instructions from and with documents provided by Centro.

20 The information memorandum set out details of the shopping centre zoning, site, and improvements together with a commentary on the Tasmanian retail market. The information memorandum also set out in detail the lease profiles of the major tenancies. It advised that Kmart had exercised its right of renewal for a further term of five years effective from 1 July 2011. After setting out details of the base rent, the lease profile for Kmart dealt with the percentage rent as follows:

Percentage Rent is calculated as follows:

- 29 November to 30 June 2001: 2.0% of gross sales in excess of $21,032,000;

- From 1 July 2001 to 30 June 2011: 2.0% of gross sales in excess of $21,032,000;

less:

the current Base Rent minus $724,895.

21 The reference to the breakeven figure of $21,032,000 is wrong. The actual figure which resulted from the variation should have been $24,311,569. This erroneous statement is one of the foundations of the claim made by Merost.

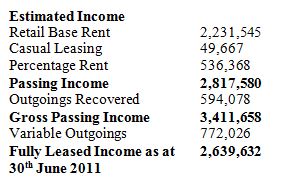

22 The information memorandum also provided the following financial summary:

23 The information memorandum stipulated that the sale process would be by expressions of interest which were to be submitted by 26 May 2011.

24 The information memorandum contained a disclaimer relevantly in the following terms:

The information contained in this report is published by Knight Frank as agents for the Vendor, solely for potential purchasers to assist them in deciding whether or not they wish to make further enquiries with respect to the property.

None of the information contained in this report can constitute any representation or offer by the Vendor or the agent. Prospective purchasers and their advisers should make their own enquiries to satisfy themselves as to the correctness of the information.

25 The information memorandum also stated that:

An electronic data room containing comprehensive due diligence information is available for access by interested parties following the completion Deed of Confidentiality available from the agents.

26 Mr Burgess signed a confidentiality deed in order to obtain access to the electronic data room (the confidentiality deed). He accessed the electronic data room for the first time on about 5 May 2011.

27 The confidentiality deed also contained a disclaimer as follows:

10 Disclaimer

(a) Neither the Disclosers, nor any of its related bodies corporate nor any of their respective officers, employees or advisers:

(1) makes any representation or warranty as to the accuracy or completeness of the Confidential Information;

(2) makes any representation or warranty that the Confidential Information has been audited, verified or prepared with reasonable care;

(3) makes any representation or warranty that the Confidential Information is the totality of the information that a prospective purchaser of the Centres may require or expect to find in order to evaluate the Centres;

(4) accepts any responsibility for any interpretation, opinion or conclusion that the Recipient or a Specified Person may form as a result of examining the Confidential Information;

(5) accepts any responsibility to inform the Recipient of any matter arising or coming to the Discloser’s notice which may affect or qualify any Confidential Information which the Discloser provides to the Recipient; and

(6) is liable, and the Recipient covenants not to make any claim or commence or pursue any proceedings against any of them, for any loss of any kind (including, without limitation, damages, costs, interest, loss of profits, or special loss or damage) arising from an error, inaccuracy, incompleteness or similar defect in the Confidential Information or arising from any default, negligence or lack of care in relation to the preparation or provision of the Confidential Information.

(b) The Recipient acknowledges that it is making an independent assessment of the Confidential Information and that it will:

(1) carry out, and rely solely on, its own investigation and analyses in relation to the Confidential Information; and

(2) verify all information on which it intends to rely to its own satisfaction.

(c) Any reliance by the Recipient, or any Specified Person, on any Confidential Information, or any use of any Confidential Information, is solely at its own risk.

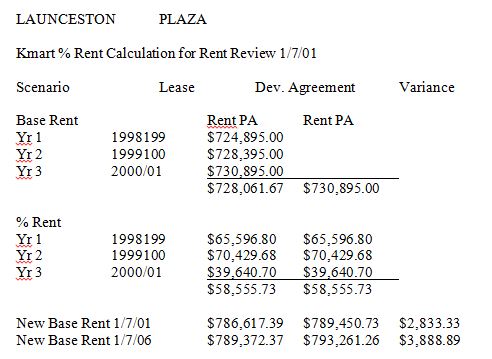

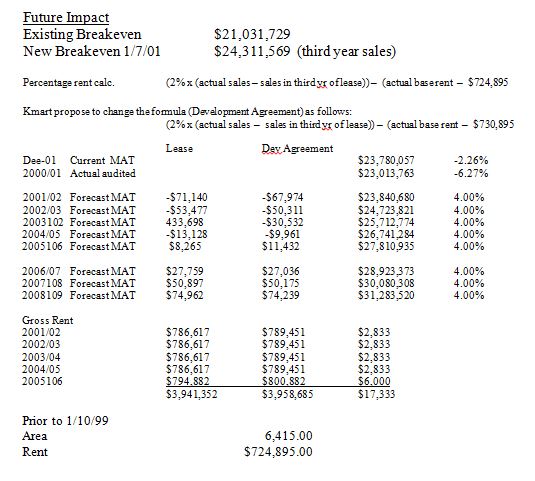

28 The electronic data room was operated by Freehills, solicitors. Mr Burgess estimated that there were around 100 documents in the electronic data room. At times, additional documents were added to the electronic data room as they became known or available. Particularly relevant to this case is the presence in the electronic data room in early May of the lease, and also of a document entitled “Launceston Plaza Kmart % Rent Calculation for Rent Review 1/7/01” (2001 Rent Review Calculation) in the following form:

29 Mr Burgess said that he saw the 2001 Rent Review Calculation in May or early June 2011. The data room access record discloses that he accessed the document on 6 May 2011. He said that this document did not change his view of the breakeven figure shown in the information memorandum. When asked in examination in chief what he made of the document he responded:

Well, it appeared to me – and I got another opinion from Ingrid Filmer, who was consulting to me - that this was a proposal. And nothing in the document led me to believe that there was any change – there was no ratification by lessor/lessee, it was just a – it looked like a proposal. It was dated 2001. And so with the lease, the main Kmart lease being dated 2008, I took it as a proposal and something that had not been included in the lease.

30 On 26 May 2011, Mr Burgess made an offer via email to Scott Newton of Knight Frank to purchase the shopping centre for $29,150,000. In that email he stated “[o]ur due diligence has been extensive” and, “[t]he offer below is not subject to further due diligence apart from contract approval.”

31 In response, Mr Forrest phoned Mr Burgess and said that he would need to increase the offer to $29.6 million to secure the property. Mr Burgess then increased the offer to that figure.

32 As a result of making that offer, Merost was asked, and agreed on 31 May 2011, to enter into heads of agreement with Centro which gave Merost an exclusive negotiation period (the heads of agreement). The heads of agreement included a warranty which in part provided:

Purchaser has satisfied itself as to the:

1. value of the Property, from its own independent valuations and reports;

2. present and future economic feasibility and economic return of the Property;

33 On 3 June 2011, Mr Burgess sent an email to Mr Abrahams, the principal of AML, indicating that he wanted the contract of sale approved and signed quickly. Mr Abrahams was overseas. But, on 4 June 2011, Mr Burgess saw Mr Norman, a solicitor at AML, and Mr Norman’s file note recorded:

I asked Chris if he needs me to review leases; he said that it wasn’t necessary – he would look at them and would get Ingrid to do so.

34 Mr Burgess gave evidence that Mr Abrahams had been his solicitor for about ten years and the instructions which he gave AML for this transaction were explained in evidence in chief as follows:

I wanted them not to look at the – not necessarily look at the leases or the IM, because we had the expertise to do that ourselves.

All right? --- I did want them to do the conveyancing and also to negotiate the contract.

Right. So just in respect of leasing, what instructions did you give to Abrahams Meese in respect of investigating leases? --- I said to them, “Don’t bother reading the leases, we will do that ourselves.”

Right. And in respect of the information memorandum, what instructions did you give? --- The same, “Don’t worry about looking at that, we’re doing that.”

So your instructions to Abraham Meese to Andrew Norman were to negotiate contract terms; is that right? --- Correct.

And handle the conveyance? --- Correct.

35 On 5 June 2011, AML ordered a title search and the result was returned the following day. The search disclosed the lease and also the variation which the search indicated was registered on 21 May 2010. This was not provided to Merost.

36 The contract of sale for the shopping centre dated 27 June 2011 was executed by Merost and Centro and provided for settlement on 31 August 2011.

37 On 24 August 2011, which was after the exchange of contracts, Mr Forrest, and then Mr Burgess, learned of the variation for the first time. Mr Forrest advised Mr Burgess of the variation on that day and arranged for it to be placed in the electronic data room.

38 In summary, there is no dispute that the information memorandum wrongly stated the breakeven figure as $21,032,000. It is also not in dispute that Mr Burgess did not learn of the variation until notified by Mr Forrest on 24 August 2011, after Merost had agreed to buy the shopping centre on 27 June 2011. It is also not in dispute that on 6 June 2011 AML had a title search which disclosed that there was a variation. It is now necessary to examine what material was available to Merost to establish the correct breakeven figure, and what steps were taken by Mr Burgess to do so.

material available to, and steps taken by merost to ascertain the correct breakeven figure

39 Mr Burgess said that he made the offer of $29.6 million on 26 May 2011 on the basis of a 9.2 per cent return, and in the belief that the breakeven figure was $21,032,000 as stated in the information memorandum.

40 He asked Ms Filmer to assist him in undertaking the due diligence by reviewing all the documents in the electronic data room, particularly the leases, and specifically to calculate the percentage rent payable from 1 July 2011 pursuant to the lease.

41 As the basis for her calculations Ms Filmer used a spread sheet which was lodged in the electronic data room (the Centro spreadsheet). The Centro spreadsheet showed the percentage rent for the financial year 2008/9 as $192,059.95, and the percentage rent for the financial year 2009/10 as $306,125.86. Those calculations were also based on an understanding that the breakeven figure was $21,032,000 as stated in the information memorandum and the lease. She set out her workings in a document sent to Mr Burgess as follows:

42 Ms Filmer’s calculations of the percentage rent payable by Kmart in the financial years 2008/9 and 2009/10 did not tally with the Centro spreadsheet. In each of those years the percentage rent paid by Kmart was about $60,000 less than the amount Ms Filmer had calculated was due under the lease.

43 When Mr Burgess received Ms Filmer’s calculations he took several steps.

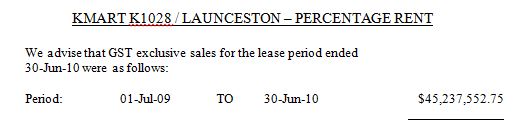

44 He asked Mr Forrest to obtain some verification of the figures from Kmart and informed him that, “We’re having difficulty – Ingrid is having difficulty with the Kmart percentage rent”. Mr Forrest responded by email on 10 June 2011 by attaching a letter dated 23 July 2010 from Kmart to Centro (the 2010 Kmart letter) which read as follows:

45 Mr Burgess also asked Ms Filmer to recheck the calculation. After he received the 2010 Kmart letter from Mr Forrest, Mr Burgess met with Ms Filmer. Mr Burgess gave evidence in chief about the meeting as follows:

We had a meeting, and I said, “Have you changed your mind on the – on the calculations you’ve come up with”. And she said, “No. I think my figures are right. I’ve been back to the lease”. And we looked at the – the Kmart letter, and we concluded that our figures were right and their figure was wrong.

Did that document at court book 220 [the 2010 Kmart letter] make any reference, as you understood it, to a new breakeven figure for Kmart? --- No. It didn’t. And furthermore, you couldn’t work out what the breakeven was from the calculation they provided. It had no – it had no reference to the formula.

46 Mr Burgess said that he also rang the senior retail leasing manager at Kmart to confirm the details of the Kmart letter. He told the Court that he was not certain of the identity of the woman with whom he spoke, but stated that he did speak with someone from Kmart. He asked about the 2010 Kmart letter. Mr Burgess was told that Kmart would not talk to him until he had bought the property. Kmart would only deal with the proprietor which, at that time, was Centro.

47 Further, Mr Burgess approached Mr Bernard Sweeney to check his figures against Mr Sweeney’s calculations. Mr Sweeney was a valuer from Jones Lang LaSalle who was instructed by the National Australia Bank to provide a valuation of the shopping centre as Mr Burgess had asked the bank to finance the purchase.

48 On 15 June 2011 Mr Sweeney sent an email to Mr Burgess, and to Narelle Cormack, the National Australia Bank lending officer, stating:

Please find attached my revised calculations to estimate the base rent to apply from next ratcheting due on 1 July, following our discussion in Narelle’s office.

My figures are pretty close to those estimated by Ingrid Filmer. I have taken the 2008/9 sales from Ingrid’s sheet and the next two years sales from the Centro April 2011 sales report. The actual ratcheting will be based on audited sales figures, but these figures have 10 of the 12 months applicable so hopefully will not be greatly different.

49 The calculation relating to Kmart attached to the email was as follows:

|

| |||

|

| |||

50 Mr Sweeney’s calculation used the $21,032,000 breakeven figure and arrived at a figure for the percentage rent very close to Ms Filmer’s figure.

51 In chief, Mr Burgess explained the position at this point as follows:

MR MESSER: So having received Mr Sweeney’s email, did you make any other inquiry about the percentage rent question; this is prior to exchanging contracts of sale? --- What we did have as a plan was to sit down with Kmart at the time of the rent review and sort it out. We thought that their figure was wrong and that we would sort it out at the appropriate time.

…

HIS HONOUR: What did you think was the reconciliation of the Kmart figures with yours? You thought the Kmart figures were wrong. Did you have some theory about where the mistake was? --- Well, we knew it wasn’t the – we knew it wasn’t the 21 million turnover cut in point because that was clearly in the lease. So we assumed they may have made a miscalculation in their formula, which we couldn’t understand. Somewhere we weren’t quite sure where the error was, but we kept going back to the lease and we kept going back to the IM and saying, “Well, this can’t be wrong. The turnover is correct.” So but from the calculation that they put up there, we couldn’t really make head nor tail of that.

52 Then on 23 August 2011, after the contract of sale had been entered into, Mr Forrest sent Mr Burgess an email advising that the Kmart rent review had been agreed and the new rental figure was $1,131,445.16. This figure was about $62,000 less than Ms Filmer’s calculation. Mr Burgess spoke to Ms Filmer and they agreed that they should talk to Kmart because of the disagreement over the figure. Mr Burgess described the conversation with Kmart in examination in chief as follows:

[S]he said you – you still haven’t settled the property so you don’t own it, so I can’t really talk to you, but you need to be aware of a variation to the lease, after I explained to her that our figures were different to hers.

Had you ever heard mention made of a variation of lease before then? --- Never.

It seems that this conversation must have occurred with someone from Kmart and that, in attributing the remarks to Ms Rebecca Koochew, a senior property accountant employed by Centro, Mr Burgess was probably mistaken.

53 Also, on 23 August 2011, Mr Burgess sent an email to Mr Forrest requesting the audited turnover figures to check the calculations as, “we differ on K-Mart”. On 24 August 2011, Mr Burgess sent Mr Forrest a further email requesting Kmart’s correct moving annual totals and sales for July. Relevantly, he stated that “[t]here appears to be no signed dogs [sic] in the data room that would suggest that K Marts breakdown has moved up beyond the origional [sic] $21m.” It is likely that this caused Mr Forrest to make further enquiries which led to the discovery of the variation. Mr Forrest gave the following evidence:

MR O’FARRELL: How did you come to find out about the variation? --- I spoke to our head of lease administration, and after asking him numerous times if there was a variation – which in the first two occasions, he said there wasn’t – on the third occasion of approaching him, he said he would have a look, and by the time I walked back to my desk there was a variation document attached to an email from Mr Gynn.

Right. And what did you do as soon as you found out about it? --- I immediately forwarded it to Mr Burgess, and I added it to the data room.

…

HIS HONOUR: Well, sorry. What caused you to ask him for it? --- Discussions with Mr Burgess.

54 It is common ground that the variation was placed in the electronic data room on 24 August 2011 and that Mr Forrest sent the variation to Mr Burgess via email on this date.

submissions of merosT on liability

55 Mr Messer, who appeared as counsel for Merost, contended that Centro’s conduct in circulating the wrong breakeven figure in the information memorandum, and confirming it by lodging the lease in the electronic data room, was misleading and deceptive within the terms of s 18 of the Australian Consumer Law.

56 It was common ground that the conduct had to be viewed in the context of the whole of the circumstances of the transaction. In that regard Merost contended that the information memorandum was intended to be an important document produced on a serious occasion.

57 Merost submitted that Mr Burgess read the information memorandum and relied on the breakeven figure contained in it. It was confirmed by the terms of the lease lodged in the electronic data room. Mr Burgess relied on the breakeven figure in the information memorandum when he made the offer to purchase, but more importantly, when Merost entered into the contract of sale.

58 Merost claimed that if it had known the correct breakeven figure it would not have bought the shopping centre for the price offered. It said that its loss was the difference between the price paid and the real value of the shopping centre.

59 Merost argued that Centro’s conduct was the cause of the loss and damage suffered by it.

60 It was common ground that causation had to be approached in a practical and common sense way.

61 Merost emphasised that Centro was liable even if its conduct was not the only cause of the loss and damage. It is sufficient for liability under s 18 that the conduct is a cause of the loss and damage.

62 Merost denied that it was fixed with the knowledge acquired by AML. First, the knowledge acquired by AML from the title search was only information that there was a variation, but not as to the content of that variation.

63 Next, Merost argued that the question is whether the information memorandum had an effect on Mr Burgess’ action and not whether Mr Burgess would have been affected if AML had discovered the terms of the variation. Merost relied on the following passage in the judgment of Lockhart J in Henjo Investments Pty Ltd v Collins Marrickville Pty Ltd (No 1) (1988) 39 FCR 546; [1988] FCA 40 (Henjo) at 559-560 (with which Burchett J and Foster J agreed on the issue):

Doubtless Collins Marrickville could have ascertained the true position about the restaurant's licences if it had inquired about them; but it did not do so. Even if Mr Tadd or Mr Jones, as advisers to the plaintiff, were on inquiry as to the matter in issue, this should not itself be taken to exclude recovery under s 52. It is true that at common law, the principal has imputed knowledge of that which is or ought to be known by his agent. There is authority that a client who employs a solicitor in a conveyancing transaction has imputed to him knowledge of anything which is known to his solicitor or would have been known to his solicitor on the proper inquiries: Kadner v. Brune Holdings Pty. Limited [1973] 1 NSWLR 498 per Mahoney JA at 501; Sargent v. ASL Development Ltd (1974) 131 CLR 634 per Stephen J at 649, per Mason J at 658-659. In an action under s 52, however, the issue is whether the misleading and deceptive conduct alleged continues to be operative in fact, whatever the knowledge which might have been obtained had the applicant's advisers conducted their investigations in a proper manner, and whatever the matters of which those advisers might have constructive notice: Obaleco Pty Ltd v Taveraft Pty Ltd (1986) 10 FCR 518 per Wilcox J at 532. This reasoning is the stronger where a party who would otherwise be liable on account of conduct found to be misleading or deceptive seeks to rely upon knowledge notionally attributed to the innocent party so as to avoid liability.

(Emphasis added.)

64 Constructive notice has no role to play in the operation of s 18. Consequently, s 5 of the Conveyancing and Law of Property Act 1884 (Tas) or s 199 of the Property Law Act 1958 (Vic) which fix purchasers with notice of matters concerning a transaction known to their solicitor, or of matters which should have been known if reasonable enquiries had been made, do not apply to the analysis of the circumstances of this case.

65 Merost disputed Centro’s contention that Mr Burgess was not misled by the erroneous breakeven figure but rather simply confused by it, and that mere confusion is not protected by s 18. Merost contended that Mr Burgess was not confused about the breakeven figure. He always thought that it was $21,032,000 because that was what the information memorandum stated and the lease in the electronic data room confirmed that figure. Mr Burgess and Ms Filmer believed that the explanation for the discrepancy in the rental figures probably arose from a mistake made by Kmart in the calculation. But Mr Burgess did not think that there was any issue about the breakeven figure.

66 Merost also rejected Centro’s contention that Mr Burgess should have raised with Mr Forrest directly the accuracy of the breakeven figure rather than merely asking him to obtain verification of Kmart’s figures. Merost argued that the nature of the enquiry was a result of Mr Burgess’ belief, derived from the information memorandum, that the breakeven figure was $21,032,000.

67 Merost then submitted that the disclaimers in the information memorandum, the confidentiality deed and the heads of agreement could not operate to defeat the claims under s 18. There is abundant authority that it would be against public policy to allow a private agreement to prevent a statutory remedy designed to protect consumers from misleading and deceptive conduct.

submissions of centro on liability

68 Mr O’Farrell SC, who appeared as senior counsel for Centro, also submitted that all relevant circumstances must be taken into account to determine whether conduct is misleading and deceptive.

69 Centro contended that the pleaded case was restricted to the effect of the statement of the breakeven figure in the information memorandum and the lodgement of the lease in the electronic data room. Mr Burgess was a sophisticated purchaser familiar with property transactions from long experience. The information memorandum cautioned potential purchasers to make their own enquiries to satisfy themselves as to the correctness of the information provided by the document. The confidentiality deed explicitly stated that Centro did not make any representations as to the completeness of the information in the electronic data room. These circumstances demonstrated to Merost that the electronic data room was not a complete repository of all the documents relevant to the transaction.

70 Centro accepted that the disclaimers could not be used to contract out of the statutory prohibitions in s 18. But it argued that the disclaimers formed part of the circumstances in which the transaction occurred such that Merost was required to check the information in the information memorandum including the breakeven figure. That was the very purpose of the due diligence exercise. Section 18, so Centro argued, does not protect people from their own carelessness.

71 Centro then contended that there was material in the electronic data room which enabled Mr Burgess and Ms Filmer to determine the correct breakeven figure. In particular, the calculation of the percentage rent in the 2010 Kmart letter allowed the breakeven figure to be “instantly discoverable”.

72 As the calculation of the correct breakeven figure was easily done on all the material available in the electronic data room, the effect of the incorrect statement of the breakeven figure in the information memorandum was merely to create confusion as to the correct breakeven figure. But producing confusion does not amount to misleading or deceptive conduct. The question whether particular conduct causes confusion or wonderment cannot be substituted for the question whether the conduct answers the statutory description contained in s 18: Campomar Sociedad, Limitada v Nike International Ltd (2000) 202 CLR 45; [2000] HCA 12 at [105].

73 Then, Centro argued that Mr Burgess and Ms Filmer were confused about the calculation of the percentage rent figure, but instead of asking Mr Forrest about the way the calculation was undertaken, they simply asked for confirmation of what Kmart was paying.

74 Next, Centro submitted that it defied common sense for Mr Burgess to ask his solicitor to do a title search but not to instruct AML to report the results back to him. He was coordinating the due diligence exercise and any loss was a result of Mr Burgess failing to arm himself with the results of that search as a cross check against the documents in the electronic data room.

75 Further, Centro contended that an applicant in a claim under s 18 does not establish reliance on the misleading and deceptive conduct if the evidence demonstrates that the applicant entered into a transaction indifferent to the representation said to constitute the misleading and deceptive conduct: De Bortoli Wines Pty Ltd v HIH Insurance Ltd (In liq) (2011) 200 FCR 253; [2011] FCA 645 at [64].

76 The present case, so it was argued, was a case of indifference. Once Mr Burgess discovered the problem in the calculation of the percentage rent, the cure was so simple that to ignore it was indifferent. All that was necessary was to tell Mr Forrest that he had received the 2010 Kmart letter but that he could not get the figures to work. Mr Forrest had been willing throughout to supply any information requested by Mr Burgess.

77 Centro also argued that the effect of the erroneous breakeven figure had no impact until a calculation was made of the percentage rent. Centro contended that the evidence showed that Mr Burgess did not make any calculation of the percentage rent figure before he made the offers to purchase. By that time he was, in practical terms, even though not legally, committed to the transaction. He was very anxious to buy the property.

consideration – liability - was the information memorandum misleading and DECEPTIVE?

78 The first question is whether the representation made by Centro was misleading or deceptive or likely to mislead or deceive. Centro does not contest the fact that the breakeven figure stated in the information memorandum was wrong and that the lease in the electronic data room contained the same breakeven figure.

79 Both Merost and Centro agreed that it was necessary to judge the nature of the alleged contravening conduct by reference to all the circumstances surrounding the transaction.

80 Some of the surrounding circumstances support the conclusion that the information memorandum and the lease were misleading.

81 The information memorandum and the information in the data room were designed to equip potential purchasers with material necessary to submit an expression of interest for the purchase of the shopping centre. The income which the shopping centre produced was a critical factor for a purchaser. Hence, the information memorandum gave detailed attention to the issue. As Kmart was one of the two major tenants, and it contributed around 60 per cent of the rent revenue of the property, the information memorandum set out in detail and at length the main features of the lease and the way in which the rent was calculated. The lease profile for the lease occupied two full pages of the information memorandum. The information memorandum indicated that an electronic data room was available “containing comprehensive due diligence information”.

82 Further, the standing of the professionals involved in the transaction gave Mr Burgess an assurance of the reliability of the information provided. The information memorandum was prepared by Knight Frank one of the leading agents in Tasmania. It was prepared for Centro, which was the largest operator of community and neighbourhood shopping centres. Mr Forrest was managing the sale and he is a qualified valuer. The electronic data room was administered by Freehills, one of the largest law firms in Tasmania. From these circumstances, Mr Burgess said “[t]here’s no real requirement to go outside of” the information memorandum and the electronic data room.

83 Other circumstances of the transaction suggest that the error in the information memorandum would not mislead a purchaser. Thus, Mr Burgess was an experienced operator in the property industry, and particularly in commercial transactions of this nature. The sale was a commercial transaction in which both parties were expected to take precautions and undertake due diligence. Mr Burgess was aware of the importance of title searches in property transactions. Normally the person negotiating the terms of purchase would arrange to have access to the result of the title search and hence be aware of the requested dealings. Further, the disclaimers made it clear that the information provided was incomplete. That gave Centro a reason to assume that potential purchasers would make their own enquiries by conducting a title search, which would reveal the variation.

84 Then, Centro relied on the circumstances that, so it said, the correct breakeven figure could be calculated easily from other material in the information memorandum and the electronic data room.

85 This argument relied on the provision by Centro to Mr Burgess of the 2010 Kmart letter which included a calculation of the percentage rent. It stated that the two per cent was calculated on the sales figure from $31,568,859.

86 Mr Forrest explained how one could derive the correct breakeven figure of $24,311,569 from this figure. The current rent was $876,041. That information was available from the electronic data room and was not in contention. From this figure one deducts $730,895, the original rent, to arrive at $145,146. Then one grosses up this figure by multiplying it by .02 to arrive at $7,257,300. This represents the rent adjustment side of the percentage rent calculation. As the $31,568,859 represents the result of the deduction of the rent adjustment from the sales element of the percentage rent calculation formula one deducts $7,257,300 from $31,568.859 to arrive at the breakeven figure of $24,311,559. This is the breakeven figure (less $10) in the variation.

87 However, as Ms Filmer explained, the percentage rent calculation has two sets of variables, namely, the sales element and the rent adjustment element. Mr Forrest’s calculation fixes the rent adjustment element at $730,895. This is the figure in the variation. But the variation changed this figure from $724,895 in the original lease. If one did the calculation with the knowledge of Mr Burgess only of the terms of the lease, then one would use the $724,895 not the $730,895. The resulting breakeven figure is $24,011,559 not $24,311,569 – a difference of $300,010.

88 When Mr Forrest was asked what one would have thought if one had done the reverse calculation using the 2010 Kmart letter but without the figures in the variation he answered that one would have concluded “that there was confusion around what the threshold is actually”. Mr Forrest, who was a frank witness, was correct. His answer and the facts to which he responded contradict the case of Centro that the correct breakeven figure could be calculated from the information in the 2010 Kmart letter without the variation.

89 What would be produced by the reverse calculation would not have been the correct figure, and the process would not reveal which of the two variables was wrong. But Centro said that the calculation would, at least, disclose that the breakeven figure was more than $24 million.

90 However, this does not take sufficient account of the degree of difficulty in identifying the 2010 Kmart letter as containing information which could be used to calculate the breakeven figure. Neither does it take account of the significance of the fact identified by Ms Filmer that the lease was dated as recently as 2008. She said:

in the scheme of Coles and Kmart [this is] brand new. It’s a beautiful brand new lease. There was no reason to think that that was incorrectly drafted, or it was varied, or that there was anything wrong with it.

91 And she also said:

…if you’re dealing with Kmart or Coles and there is any side agreement there is 10,000 pages of paper that comes with it… you don’t change the most valuable lease in the centre with two pages of paper. There would be legal letters, there would be variations, there could be commentary somewhere. There would be something.

92 In all the circumstances the 2010 Kmart letter did not provide a sufficiently accessible means to correct the error in the information memorandum confirmed by the presence of the lease in the electronic data room.

93 Neither did the financial summary of the shopping centre as set out in the information memorandum disclose the correct percentage rent calculation. The financial summary contains a figure of the past percentage rental income for the entire shopping centre, and does not show individual percentage rents or how they were calculated. Centro suggested that the total percentage rent figure in the financial summary would have been higher if the breakeven figure in the lease had been used. However, the error could have been in any, and there was more than one, of the percentage rent calculations for the shopping centre. Consequently, the correct breakeven figure could not be determined from the financial summary nor would it have alerted Merost to the particular error.

94 Then, Centro argued that a further relevant circumstance was that the 2001 Rent Review Calculation disclosed the correct breakeven figure of $24,311,569. When asked what he made of this document, Mr Burgess said in chief in a passage previously quoted but which bears repeating:

Well, it appeared to me – and I got another opinion from Ingrid Filmer, who was consulting to me - that this was a proposal. And nothing in the document led me to believe that there was any change – there was no ratification by lessor/lessee, it was just a – it looked like a proposal. It was dated 2001. And so with the lease, the main Kmart lease being dated 2008, I took it as a proposal and something that had not been included in the lease.

For the reasons given by Mr Burgess, this document did not counteract or nullify the erroneous statement of the breakeven figure in the information memorandum.

95 Centro relied on the expert opinion of Mr Thomas. He prepared a report for the purpose of the litigation. In that report he explained that he acted for another potential purchaser of the shopping centre. He said that he identified an inconsistency between the percentage rent calculated by him and the percentage rent recorded in the Centro spreadsheet. He said he noticed a reference to a proposed change in the percentage rent formula in the 2001 Rent Review Calculation. These two factors caused him, on 24 May 2011, to send an email to Scott Newton, the Chief Executive Officer of Knight Frank. The email stated:

We have been provided with two different spreadsheets relating to the calculation of Kmart’s % Rent which indicate different amounts were payable for 08/09 and 09/10. Please refer to the attached documents and confirm which set of calculations we should be relying on. At this point the sales provided do not support the percentage rent amounts contained in document 02.02.0067 [the Centro spreadsheet].

96 On 25 May 2011, Mr Thomas received a response from Mr Cramer, Assistant Manager, Property Transactions and Valuations for Centro, which included a spreadsheet setting out how the Kmart percentage rent was calculated.

97 In oral evidence Mr Thomas explained that the initial inconsistency which he identified arose because “I had not factored in the variations of the lease into my analysis”. He read the breakeven figure in the information memorandum. It is probable that his initial steps were induced by that source. In an exchange with the Court, he then explained the effect of the 2001 Rent Review Calculation thus:

But then you come across this document, and what did it say to you in relation to the problem that you were confronting? --- That it made reference to a development agreement, and when you have development agreements, it could have given rise to a change in the lease for the Kmart tenancy.

What’s a development agreement? What did you take it to be? --- It can mean a lot of things. It usually relates to – if there’s an agreement between the tenant and the owner, if they’re entering into an agreement. It could – it can mean a lot of things, but that was the reason I delved further, because on face value, that does not solve the – does not provide all the answers. That was just another document that led me to ask more questions.

And was it just good luck that you happen to be taken by this document to ask particular questions, or do you say it was obvious that something – that this disclosed something that was significant about resolving the conflict? --- I don’t believe it was good luck. I think it was just part of not – as part of a transaction, there’s a natural inclination to ask more questions, and as part of that process, I was not comfortable with what I had. So it was just – my natural path is to explore further, because I couldn’t reconcile the numbers, and percentage rank for this particular centre was part of the income. So it was valid to explore further.

98 Then, he said:

Upon receiving a response to the email that I sent to Mr Scott Newton, I received information from Centro confirming the formula for the calculation of percentage rent, which disclosed the new threshold.

99 It can be seen that the 2001 Rent Review Calculation provoked Mr Thomas to ask more questions. It did not give him the answer. Mr Burgess and Mr Filmer were also provoked into asking for further information although their concern was not raised by the 2001 Rent Review Calculation. Their response to that document was rational. I am not persuaded that Mr Thomas’ reliance on it was not a matter of luck, despite his denial. Whatever the source, both Mr Thomas and Mr Burgess became aware of the inconsistency between the percentage rent figures supplied and the percentage rent figures they calculated.

100 Mr Thomas went to Mr Newton to clarify the situation. Mr Burgess went to Mr Forrest to clarify the situation. Mr Thomas received comprehensive information which “disclosed the new threshold”. Mr Burgess received the 2010 Kmart letter which, for reasons explained, did not disclose the new threshold. Consequently, Mr Thomas’ experience and opinion does not assist Centro’s case.

101 Mr Thomas proffered the opinion that, although he did not have the 2010 Kmart letter, it should have alerted Merost to the possible existence of the variation. For the reasons given at [87] – [94] this opinion should not be accepted.

102 Thus, the submission that the correct breakeven figure was easily discoverable from the material available is not made out.

103 Further, it cannot be said that Mr Burgess was merely confused about the breakeven figure. From the information he was given, Mr Burgess was always clear that the figure stated in the information memorandum was the correct breakeven figure.

104 It follows from this discussion that the erroneous statement of the breakeven figure in the information memorandum confirmed by the terms of the lease lodged in the electronic data room was misleading and deceptive within the terms of s 18.

Reliance

105 The next question is whether Merost relied on the erroneous breakeven figure as a basis for entering into the purchase. Mr Burgess gave evidence that he relied on this information to make the offers to purchase.

106 Centro contended that this evidence was unsatisfactory. Centro relied on the evidence of Mr Burgess that he calculated the percentage rent with Ms Filmer before he made the offer to purchase on 26 May 2011. This, so it was submitted, was inconsistent with the evidence of Ms Filmer that she became involved on 30 May 2011 being a date after the offer was made.

107 This submission should not be accepted for several reasons. First, it is not clear that the evidence given by Mr Burgess and Ms Filmer is inconsistent. When asked in chief when she became involved, Ms Filmer said “about 30 May”. This answer was translated in cross examination into questions which asserted that she became involved on 30 May. Although Ms Filmer did not demur in the form of the question, she probably responded on the basis of her unprompted evidence in chief. Ms Filmer’s evidence should be understood to accept that she might have been involved a few days before 26 May and hence contributed to the calculation of the percentage rent for the purpose of the offer. Second, Mr Burgess did hesitate on the timing of Ms Filmer’s involvement and gave an alternative position, namely, that he calculated the percentage rent himself before Ms Filmer became involved but before the offer was made. But he said, “I called her very early on… we were really doing it together”. Third, the point only goes to whether the calculation was made before the offers were made. It does not challenge the relevant issue, namely, whether the calculation reliant on the information memorandum was made before contracts were exchanged. On this issue there is no doubt and no challenge. Finally, on the probabilities it is altogether unlikely that Mr Burgess did not work out the percentage rent before he made the offer. He presented in the witness box as an astute and professional person with an approach which was careful and thorough. He had nearly 40 years’ experience in property dealings including recent involvement in the purchase and sale of shopping centres. It is beyond doubt that his concern was fastened on the major tenant which accounted for about 60 per cent of the rental income of the property.

108 Then, it was said that Merost was indifferent to ascertaining the true breakeven figure and did not rely on the erroneous information because the disclaimer in the information memorandum stated that none of the information could constitute a representation by Centro, and the disclaimer in the confidentiality deed stated that Centro did not warrant the accuracy or completeness of the information in the electronic data room.

109 The fact that Merost entered into agreements containing the disclaimers must be taken into account as one among the number of circumstances of the transaction to determine whether, as a matter of fact, Merost relied on the erroneous breakeven figure. It is not however determinative of the question.

110 Both of these agreements containing disclaimers emanated from Centro and were not subject to negotiation by Mr Burgess. The terms were fixed by Centro. They were not negotiated. Mr Burgess had to sign the confidentiality deed in order to gain access to the data room.

111 Another circumstance said to demonstrate Mr Burgess’ indifference was that after receiving the 2010 Kmart letter Mr Burgess made no specific enquiry from Mr Forrest why he could not get his calculation to match the amount of the percentage rent recovered from Kmart.

112 Mr Burgess’ response after receiving the 2010 Kmart letter does not demonstrate that he was indifferent to ascertaining the true breakeven figure. As outlined earlier in these reasons for judgment, he took a number of further steps following the receipt of that letter. He asked Ms Filmer to recheck the figures and then met with her to discuss the matter. He tried to speak directly to Kmart but they referred him back to Centro. And he approached Mr Sweeney for a further opinion. These are not actions of a person indifferent to ascertaining the true basis of the calculation.

113 The fact that Mr Burgess did not ask Mr Forrest directly “what is the correct breakeven figure?” does not demonstrate indifference. Rather it shows that Mr Burgess continued to labour under the misleading breakeven figure. He had no reason to question that element of the calculation because the information memorandum nominated the breakeven figure and it correlated with the figure in the lease lodged in the electronic data room.

114 In order to make the finding that Merost did not rely on, or was indifferent to, the erroneous breakeven figure it is necessary to reject Mr Burgess’ direct evidence that he did rely on it. There is no sufficient basis to reject his evidence. On the contrary, he was an impressive witness. As indicated earlier, he has been involved in the property market as an estate agent for nearly 40 years. He has also dealt in property on his own account in recent times. He presented in the witness box as a knowledgeable property professional who is astute, careful and thorough. He gave his evidence directly, generally without hesitation, and with a clear and detailed recall of the events and of his thinking at the time. Mr Burgess’ direct evidence that he relied on the breakeven figure in the information memorandum should be accepted. It is not displaced by the circumstances surrounding the transaction including his agreement to the disclaimers proposed by Centro.

115 Finally, for the reasons explained in Henjo in the passage extracted at [63] of these reasons, Merost was not fixed with constructive notice of the variation as a result of the title search conducted by AML.

116 It follows that Merost relied on the erroneous breakeven figure as an inducement to purchase the shopping centre.

causation

117 Save for one issue now to be considered, the above reasoning also establishes that the loss and damage was caused by the misleading and deceptive conduct of Centro. The remaining argument on causation by Centro was that Merost’s case was pleaded, opened, and run on the basis that but for the representation in the information memorandum and the lease lodged in the electronic data room Merost would have purchased the shopping centre for a lower price. However, on the evidence, so it was argued, it is improbable that Centro would have sold the shopping centre for less than the $29.6 million which Merost agreed to pay. Centro argued that the situation was analogous to that which arose in Marks v GIO Australia Holdings Ltd (1998) 196 CLR 494; [1998] HCA 69 (Marks). In that case borrowers had been promised a specified interest rate on their loans. Contrary to that representation the lender had power to alter the interest rate and did so. Gummow J explained at [104]:

There was obvious difficulty in classifying entry into the contracts themselves as "loss or damage" sustained at that stage by the borrowers and in providing monetary compensation for that injury as if there had been the loss of a bargain. At the times when the contracts were made, there was no cheaper financing on the market. None of the borrowers suggested that he or she would not have borrowed at all if the AAA facility had been other than as represented. None said that, had the truth of the matter been told, he or she would have entered into alternative financial arrangements. At this factual level, the present case thus is to be distinguished from the situation in authorities such as Demagogue Pty Ltd v Ramensky and Akron Securities Ltd v Iliffe. In those cases (where relief was obtained under s 87, not s 82), there had been a finding that, if prior to their entry into the transactions in question the applicants had been aware of the true situation, they would not have entered into the transaction.

(Footnotes omitted.)

118 This argument should not be accepted. Merost’s case was pleaded, opened, and run on the basis that Merost would not have entered into the purchase for $29.6 million if it had known the correct breakeven figure. Mr Burgess gave evidence to that effect. That evidence should be accepted. Consequently, this is a no transaction case rather than an alternative transaction case. Even if this were an alternative transaction case, then, for reasons explained later in [133-134] of this judgment, Centro has not established that it would not have sold the shopping centre to Merost for a price less than $29.6 million.

loss and damage

119 In Kizbeau Pty Ltd v WG & B Pty Ltd (1995) 184 CLR 281; [1995] HCA 4 (Kizbeau); the High Court (Brennan, Deane, Dawson, Gaudron and McHugh JJ) said at 290-291 in relation to statutory provisions which were materially the same as the present:

Actions based on s 52 are analogous to actions for torts. It follows that, in assessing damages under s 82 of the Act, the rules for assessing damages in tort, and not the rules for assessing damages in contract, are the appropriate guide in most, if not all, cases.

In an action for damages for deceit for inducing a person to enter a contract of purchase, which is an action that is closely analogous to an action for damages for breach of s 52, the courts have consistently held that the proper measure of damages is the difference between the real value of the thing acquired as at the date of acquisition and the price paid for it.

(Footnotes omitted.)

120 Merost submitted that the loss and damage suffered by it was the price paid, namely $29.6 million, less the real value of the shopping centre at the date of acquisition, namely $28.9 million, leaving a deficiency of $700,000. Centro contended that the real value of the shopping centre at the date of acquisition was somewhere between $29.25 million and $30.4 million and thus the loss and damage was between nil and $350,000.

121 The valuation of $30.4 million is derived from the offer of $31.1 million made by a potential purchaser after the close of expressions of interest. If it is assumed in favour of Merost that this offer was made without knowledge of the variation, then it should be reduced by $700,000 to take account of the reduction in the rental income as a result of the variation. If the true value of the shopping centre at the date of acquisition was $30.4 million then Merost suffered no loss or damage by paying $29.6 million which was less than the real value.

122 A valuation of $29.3 million is derived from a valuation report prepared by Mr Sweeney of Jones Lang LaSalle. The date of the valuation was 9 June 2011. It was made for the National Australia Bank for mortgage security purposes in anticipation of the bank financing the transaction. The report valued the shopping centre at $30 million. It noted the existence of the variation, but made the rent calculation based on the unvaried Kmart percentage rent breakeven figure of $21,311,569. Allowing again for a reduction of $700,000 to take account of the impact of the wrong breakeven figure yields a valuation of $29.3 million.

123 Then, a valuation of $29.25 million is derived from a valuation report prepared by Stephen Andrew of Colliers International. The date of the valuation is 31 December 2010. It was obtained by Centro itself to establish the market value of the shopping centre for statutory reporting purposes. The report annexed a title search which discloses the variation. However, in the body of the report the unvaried breakeven figure is referred to and used for the purpose of the valuation. The valuation is $29.95 million. Again, allowing for a reduction in value of $700,000 as a result of the use of the wrong breakeven figure yields a valuation of $29.25 million.

124 Both the reports of Mr Sweeney and Mr Andrew were in evidence as documents contained in the Court Book. Neither Mr Sweeney nor Mr Andrew was called to give evidence.

125 Mr Thomas provided an expert report for Centro which included some observations on Mr Perrin’s report but in the end neither the report nor Mr Thomas’ oral evidence contested Mr Perrin’s valuation figure of $29.6 million.

126 It is not appropriate to assess the real value of the shopping centre by a reference to the offer of $31.1 million. The potential purchaser was not named or called to give evidence. Having regard to Mr Forrest’s evidence about the unsatisfactory nature of previous dealings between Centro and that potential purchaser, there is doubt that the offer represents a price that would actually be paid.

127 The range between $29.25 million and $29.6 million represents a variation inherent in the valuation process which is not an exact science. The methodology used in each valuation is the same. There is some scope for differences about the numerous variables which go into the calculations.

128 Centro criticised Mr Perrin’s valuation on the basis that Mr Perrin lacked independence from Merost. Mr Perrin is a director of Burgess Rawson. The solicitor for Merost, Mr Abrahams, is the chairman of the board of Burgess Rawson. Burgess Rawson manages properties for Mr Burgess. He founded the company nearly 40 years ago and remained actively involved until about three years ago. On the other hand, Mr Perrin is a valuer of 30 years standing and no issue of substance was put to him in cross examination which reflected on the correctness of his approach to the valuation. What is perhaps more significant is that he was briefed with the statement of claim in this proceeding which articulated the loss and damage calculation in the amount of $700,000. Given that valuation is not an exact science, his valuation would have been more persuasive if he had not been briefed with the result advocated by Merost. The appeal of the Collier and Jones Lang LaSalle valuations is that they were obtained outside the context of the proceedings.

129 The best reflection of the loss and damage caused by Centro’s conduct is achieved by taking the mid-point of these two valuations, namely, $29.275 million, as the real value of the shopping centre at the date of acquisition. As Merost paid $29.6 million the loss and damage incurred by Merost in the transaction was $325,000.

130 Centro argued that the measure of damages is not constrained by analogies to tort, contract or equitable remedies. In Marks McHugh, Hayne and Callinan JJ said at [38]:

It can be seen, therefore, that both ss 82 and 87 require examination of whether a person has suffered (or, in the case of s 87, is likely to suffer) loss or damage “by conduct of another person” that was engaged in the contravention of one of the identified provisions of the Act. That inquiry is one that seeks to identify a causal connection between the loss or damage that it is alleged has been or is likely to be suffered and the contravening conduct. But once that causal connection is established, there is nothing in s 82 or s 87 (or elsewhere in the Act) which suggests either that the amount that may be recovered under s 82(1), or that the orders that may be made under s 87, should be limited by drawing some analogy with the law of contract, tort or equitable remedies. Indeed, the very fact that ss 82 and 87 may be applied to widely differing contraventions of the Act, some of which can be seen as inviting analogies with torts such as deceit (eg, s 52) or with equity (eg, s 51AA) but others of which find no ready analogies in the common law or equity, shows that it is wrong to limit the apparently clear words of the Act by reference to one or other of these analogies.

131 Their Honours explained at [41] how Kizbeau should be understood as follows:

This is not to say that no help can be had from the common law in deciding what damages may be allowed under s 82 in cases of conduct contravening s 52. Very often, the amount of the loss or damage caused by a contravention of s 52 will coincide with what would have been allowed in an action for deceit. But that is because the inquiry in both cases is to find out what damage flowed from (in the sense of being caused by) the deceit or contravention. Leaving aside questions of remoteness of damages in assessing damages for deceit (a question that was left unresolved in Gould v Vaggelas), the damages for deceit will be the sum representing the loss suffered by the plaintiff because the plaintiff altered its position in reliance on the defendant’s misrepresentation. But the analogy cannot be pressed too far. It should not be pressed to the point of concluding that the only damages that may be allowed under s 82 are those that would be allowed in an action for deceit. The question presented by s 82 is not what would be allowed in deceit, it is what loss or damage has been caused by the conduct contravening the Act.

(Footnotes omitted.)

132 Centro submitted that no loss or damage was occasioned by the representation because Centro would not have sold the shopping centre for less than $29.6 million which was the price paid by Merost.

133 However this argument is not supported by the facts. The closest Mr Forrest came to addressing the question was when asked his reasons for approaching Mr Burgess to increase his original offer. He explained:

The book value that we were holding the asset at was in excess of where the offers came in. There was a chance, a possibility that we would not sell the asset if we didn’t achieve a pricing level.

134 On the other hand, Mr Forrest said that the sale was in part a response to Centro’s financial difficulties. Although Mr Forrest could not recall a specific reason for the sale, he thought one reason may have been that Centro had trouble refinancing the property. It is also noteworthy that even though Centro had a valuation of $29.95 million from Colliers, it was prepared to sell to Merost for $29.6 million. That does not indicate a vendor unprepared to reduce the price to achieve a sale.

135 It follows that the loss and damage suffered as a result of the contravention of s 18 was $325,000.

contributory negligence

136 Section 137B of the Act provides:

If:

(a) a person (the claimant) makes a claim under subsection 236(1) of the Australian Consumer Law in relation to economic loss, or damage to property, suffered by the claimant because of the conduct of another person; and

(b) the conduct contravened section 18 of the Australian Consumer Law; and

(c) the claimant suffered the loss or damage as result:

(i) partly of the claimant's failure to take reasonable care; and

(ii) partly of the conduct of the other person; and

(d) the other person did not intend to cause the loss or damage and did not fraudulently cause the loss or damage;

the amount of the loss or damage that the claimant may recover under subsection 236(1) of the Australian Consumer Law is to be reduced to the extent to which a court thinks just and equitable having regard to the claimant's share in the responsibility for the loss or damage.

137 In the alternative to a complete denial of responsibility for the loss and damage, Centro submitted that the loss and damage incurred by Merost in part resulted from failure by Merost to take reasonable care of its own interests. Centro argued that it was routine in a property purchase transaction to do a title search. Mr Burgess had his solicitor undertake such a search. The search disclosed the variation. Mr Burgess expressly instructed his solicitors that they not look at the lease documents because he would do so. His expertise was in the commercial assessment of the transaction and he expressly relieved his solicitors from involvement in that side of the transaction. Consequently, the solicitors did not pass on to Mr Burgess the information that there was a variation. Had they done so he would have obtained the variation and seen that the breakeven figure had been changed. The failure of Mr Burgess to coordinate the various inputs into the due diligence process meant that he was not directed to the variation and did not pick up the mistake in the information memorandum concerning the breakeven figure.

138 Some useful guidance on the approach to the question of contributory negligence is found in Pennington v Norris (1956) 96 CLR 10; [1956] HCA 26. This was a claim by a pedestrian injured by the driving of the plaintiff. The High Court said at 16:

What has to be done is to arrive at a “just and equitable” apportionment as between the plaintiff and the defendant of the “responsibility” for the damage. It seems clear that this must of necessity involve a comparison of culpability. By “culpability”, we do not mean moral blameworthiness but the degree of departure from the standard of care of the reasonable man.

139 And in Podrebersek v Australian Iron and Steel Pty Ltd (1985) 59 ALR 529; [1985] HCA 34 the High Court said at 532-533:

The making of an apportionment as between a plaintiff and a defendant of their respective shares in the responsibility for the damage involves a comparison both of culpability, ie of the degree of departure from the standard of care of the reasonable man (Pennington v Norris (1956) 96 CLR 10 at 16) and of the relative importance of the acts of the parties in causing the damage: Stapley v Gypsum Mines Ltd [1953] AC 663 at 682; Smith v McIntyre [1958] Tas SR 36 at 42-49 and Broadhurst v Millman [1976] VR 208 at 219, and cases there cited. It is the whole conduct of each negligent party in relation to the circumstances of the accident which must be subjected to comparative examination. The significance of the various elements involved in such an examination will vary from case to case; for example, the circumstances of some cases may be such that a comparison of the relative importance of the acts of the parties in causing the damage will be of little, if any, importance.

140 The degree of departure from the standard of care of the reasonable vendor of Centro was considerable. It was the primary source of the information concerning leases over the shopping centre because the leases were transactions in which Centro was a party. It had a particular responsibility with respect to the lease because Kmart was the largest tenant and contributed around 60 per cent of the rental revenue of the property. The reason Centro misstated the breakeven figure was a result of poor and inadequate administration within the organisation. The variation was held by the lease administration department. Despite Mr Forrest more than once requesting all relevant documents relating to the shopping centre so he could provide these to Knight Frank to prepare the information memorandum, he was not provided with the variation notwithstanding that it was held in the lease administration department. Consequently, he relied on the lease, which was given to him, to state the breakeven figure in the information memorandum.

141 Further, Mr Forrest was aware of the fact that the breakeven figure had been varied. Before the information memorandum was published, he wrote to Mr Gynn in the Centro lease administration department and requested clarification of the percentage rent calculation as he could not see “any documentation that matches the way we calculate it internally”. Mr Gynn replied:

Kmart 2% of Gross Sales over $21,311,569 less the amount by which the base rent exceeds $730,895 (as per the lease varied by a variation).

(Emphasis added.)

142 Mr Forrest replied, correcting Mr Gynn:

Accounting has adjustment factors on both majors at Launceston and the threshold for Kmart is $24,311,569!!

143 He did not correct the incorrect breakeven figure published in the information memorandum, despite having reviewed it prior to its publication. Mr Forrest also did not inform Mr Burgess of the correct percentage rent calculation when Mr Burgess informed him that Merost was having difficulty with the calculation, even though Mr Forrest was aware that there was no document recording the variation in the electronic data room.

144 The degree of departure from the standard of a reasonable purchaser by Merost was relatively markedly less. It was, certainly in retrospect, unwise of Mr Burgess to limit the role of his solicitors and not ask them to provide him with the result of the title search. However, the information memorandum stated that there was an electronic data room containing “comprehensive” due diligence information. On inspection of the electronic data room that description appeared accurate. Ms Filmer said she looked at every document lodged there. The electronic data room contained more than 100 documents. Mr Burgess felt confident about the information provided because Centro was the biggest player in the neighbourhood or community shopping centre sector. He gave evidence that “you would assume … they would be on top of their stuff”. He also said:

[Y]ou’re dealing with – you’re dealing with one of the top agencies in Knight Frank and – they’re a global company. Dealing with Centro, who specialises in this product, you’re dealing with Tom Forrest who’s a qualified valuer, and you’re dealing with probably the biggest law firm in Hobart, so – and you know, you’re matching things up. There’s no real requirement to go outside of that. You would spend your whole life searching. You’ve got the information you need, as far as I was concerned.

145 Mr Burgess was aware of the disclaimers in the information memorandum, the confidentiality deed, and the heads of agreement. However, against the assurances gained from the circumstances described, it was reasonable for him to place more faith in those factors.

146 Then, it is necessary to consider the relative importance of the acts of the parties causing loss and damage. Again, the incorrect statement of the breakeven figure by Centro was considerably more important than the act of Merost in failing to have its solicitors report the outcome of the title search to it. The failure of Merost was part of the cause of the loss and damage because, if it had learned of the variation, it would have discovered the true breakeven figure. But Centro’s statement in the information memorandum in the circumstances in which it was made pointed away from the need to check that figure.

147 In the end, having regard to Merost’s share in the responsibility for the loss and damage, it is just and equitable to reduce the amount it may recover from Centro by 20 per cent, or $65,000. Centro’s responsibility therefore is for loss and damage in the sum of $260,000.

proportionate liability

148 Centro argued that if it is held liable to Merost for loss and damage, then AML’s omission to report the result of the title search to Mr Burgess independently caused the loss and damage. Hence, AML was a concurrent wrongdoer (s 87CB(3) of the Act). The liability of Centro is limited to an amount reflecting that proportion of the loss and damage claimed that the Court considers just having regarding to the extent of Centro’s responsibility for the loss and damage (s 87CD(1) of the Act).

149 Centro argued that AML is a concurrent wrongdoer because it failed to advise Merost on the result of the title search. That was negligence because it is the function of the solicitor retained to obtain title searches to advise about the title including leases or variations. The failure of AML to do so contributed to Merost entering into the contract of sale. Centro relied on the evidence of Mr Manser who practised as a solicitor in Tasmania from 1969 until 2008 and who is now a barrister. Mr Manser has had a long experience as a solicitor in property transactions. In his view a solicitor acting in this transaction who was asked to do a title search was bound to advise the client of the result of the search. Mr Manser understood that the instructions received by AML did not require it to comment on the lease documents, but he said that this did not mean that AML was not obliged to report the result of the title search. Mr Manser described the obligation of a solicitor thus:

[F]rom the perspective of a solicitor acting for an intending purchaser, I believe that the solicitor has to regard themselves as the prime instrument of inquiry here, unless they receive an unequivocal instruction from their client that they are not required to pursue a particular line of inquiry.

150 Mr Manser’s opinion was constrained by the information on which it was based. He had regard to Mr Norman’s file note which read:

I asked Chris if he needs me to review leases; he said that isn’t necessary – he would look at them and also get Ingrid to do so.

Mr Manser thought this instruction was ambiguous. It did not instruct AML to withhold the result of the search from Mr Burgess.

151 However, when forming his opinion Mr Manser did not have the oral evidence given by Mr Burgess about the instructions he gave to his solicitors. Those instructions were clear. They provided for a limited role for AML. AML was to negotiate the terms of the contract and arrange for the conveyance. It was implied in these instructions that it was not necessary for AML to provide the title search to Mr Burgess.

152 I find that the arrangement between Mr Burgess and AML did not require AML as part of its retainer to advise him of the result of the title search. So far as the solicitors were concerned, the search was undertaken only for the purpose of fulfilling the functions of negotiating the terms of the contract of sale and completing the conveyance. Thus, AML was not a concurrent wrongdoer and Centro’s liability should not be reduced as a result of the acts of AML.

conclusion

153 For these reasons there will be judgment for Merost against Centro in the sum of $260,000.

154 The question of consequential orders, including orders for costs, is reserved as requested by the parties.

| I certify that the preceding one hundred and fifty-four (154) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice North. |

Associate: