Hundy (Liquidator); In the Matter of Enviro Friendly Products Pty Ltd (In Liq) [2013] FCA 852

FEDERAL COURT OF AUSTRALIA

Hundy (Liquidator); In the Matter of Enviro Friendly Products Pty Ltd (In Liq) [2013] FCA 852

CORRIGENDUM

1. Delete [77] and replace it with the following [77]:

77. The liquidators affirmed that their costs up to the date of the hearing (23 October 2012) comprising both their fees and expenses were $228,678.36. They also estimated that their costs to finalise the matter were in the range $15,928.28 to $43,053.91.

2. In [78], delete the figure $81,577 and replace it with the figure $228,678.36.

I certify that the preceding two (2) numbered paragraphs are a true copy of the Corrigendum to the Reasons for Judgment herein of the Honourable Justice Foster. |

Associate:

Dated: 3 October 2013

IN THE FEDERAL COURT OF AUSTRALIA | |

IN THE MATTER OF ENVIRO FRIENDLY PRODUCTS PTY LTD (IN LIQUIDATION) (ACN 114 944 713)

STEPHEN JOHN HUNDY AND IVOR WORRELL IN THEIR CAPACITIES AS LIQUIDATORS OF ENVIRO FRIENDLY PRODUCTS PTY LTD (IN LIQUIDATION) (ACN 114 944 713) Plaintiffs |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT:

1. DIRECTS that the plaintiffs/liquidators would be justified in deciding that in relation to the Small-scale Technology Certificates standing in the name of Enviro Friendly Products Pty Ltd (In Liq) (ACN 114 944 713) (the company) on the Register of those certificates maintained by the Clean Energy Regulator:

(a) The company holds the certificates referred to in paragraph 34 of the affidavit affirmed by Stephen John Hundy on 29 June 2012 in its own right, and those certificates are part of the general assets of the company available to satisfy creditors in the winding up; and

(b) The company holds the remaining certificates (the trust STCs) on trust for the persons named in the schedule to these orders (the beneficiaries).

2. ORDERS that in respect of the trust STCs, the liquidators be appointed as receivers and managers of that trust pursuant to s 57 of the Federal Court of Australia Act 1976 (Cth).

3. DIRECTS that the receivers and managers would be justified in pooling the trust STCs and selling them as soon as practicable.

4. ORDERS that, in the event of such a sale, the reasonable costs and expenses of the receivers and managers (including the costs of the liquidators relating to the investigation of the STCs) be paid from the proceeds of such sale.

5. DIRECTS that the receivers and managers would be justified in distributing to the beneficiaries the remainder of the proceeds of that sale in the proportion that the STC entitlement of each beneficiary bears to the overall STC entitlement of all beneficiaries.

SCHEDULE

1. Rob Allan

2. Denis Anderson

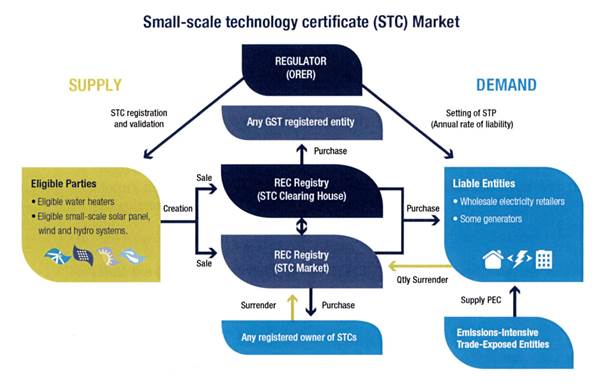

3. Dr Lyn Austen

4. Carol Bates

5. Virginia Batham

6. Kambelle Beck

7. Bill Bowron

8. Hans Van Brakel

9. Michael Bremers

10. Ray Brewer

11. Susan Bruce

12. Valentina Carnazola

13. Jane and Michael Chalker

14. Annie Chiew

15. Jenny Chiu

16. Howard and Rosemary Dalton

17. Barbara de-Bryon-Faes

18. Penny and Ji Delander

19. John Deuis

20. Shayne Di Camillo

21. Tim Dunnett

22. Gred Dunstone

23. Edwin Harris

24. Michael Ernst-Russell

25. Nigel Erpic

26. Graham Flynn

27. Rob Gee

28. Daniel Gibson

29. Graffix Construction

30. Felicity and Matthew Grant

31. Mark and Alisa Harriott

32. Bob Harrison

33. Angie Henley

34. Ian Hill

35. Klaus Matthaei and Caryl Hill

36. Lyle Hingley

37. David and Jenny Hobson

38. Jan Hopkins

39. Gary Hosking

40. Neil James

41. Simon and Bridget Johnson

42. Vitaly Kashkarov

43. Konrad Knerr

44. George Kriz

45. Frank Lehman

46. John Loughhead

47. Narelle Lovell

48. Colin and Robyn Lowe

49. Dorothy Magnusson

50. Laurie Mclauchlan

51. Rachel Mander

52. Paul McCarroll

53. David McCook

54. MA and DM McKenzie

55. Andrew McNaughton

56. Carol Mellor

57. Glenn Mitchell

58. John and Susan Moore

59. Helen Morrissey

60. Moyer Sheena

61. Cornelius Joseph Mulvehill

62. Susan Murray

63. Jenny and Karl Newport

64. Catherine Nilsson

65. Andrew Nowland

66. Michael Nowland

67. Scott Nowland

68. Pam Okeeffe

69. Anton Osti

70. Des Page

71. Jing Ping

72. Bruce Pink

73. Roy Rae

74. Faith and Tony Anderson and Raynor

75. Dr Peter Boncevich

76. Don De Rota

77. Peter Ryan

78. Jan Sismey

79. Ian Smith

80. Steve Graham

81. Laurence Stonard

82. Urip Sutiyono

83. Lana Tham

84. Gerry Thomas

85. Francis Tisseverasinghe

86. Tony and Cathy Tummillo

87. Greg Turner

88. Jill Turner

89. Uniting Church of St James

90. Uniting Church – St Margarets Congregation

91. John Vidakovic

92. Ian Warfield

93. Richard Willimott

94. Ross Wilson

95. Greg Wolfe

96. Ian Woodward

97. Victor Zaharov

98. Eden Zanatta

99. Benjamin Nicolson

100. Christopher Lowe

101. Erwin Diaz

102. Ian Baird

103. Ian Martin

104. Jackie Wraight

105. Jane Hathaway

106. Pauline Vial

107. Penny Howarth

108. Rhonda Riches

109. Robyn Schussig

110. Tony Fischer

111. Gareth Dawes

112. Fiona Fraser

113. Murray

114. Mathew Meischke

115. Andrew Gilbert

116. Georgina Gordon

117. Trundle RSL

118. Jenny Harrison

119. Carleen Dennington

120. Robin Stanton

121. Russell Reid

122. Kate Pearson

123. Simon Johnson

124. Arthur Davies

125. John Mitchell

126. Jennifer Atkinson

127. Ray Greenaway

128. David Holmes

129. John Green

130. Keith Barlin

131. Gary Krecher

132. Richard Martin

133. Felix Tan

134. Simon Coulson

135. Marcus Waugh

136. Lester Watson

137. Davy Cattle

138. Rita Pethroholos

139. Lawrence Fransen

140. Astley Tually

141. Steve and Jill Crisp

142. Winston Newman

143. Fay Fox

144. Kimberley Rowlands

145. Margaret Funnell

146. Kirsty Young

147. John Condon

148. Crawford Proporties Unit Trust

149. InfoMining

150. Canturf Properties Pty Ltd

151. Neal Bates – Bates Motor Sports Pty Ltd

152. Peter Lewis

153. Bernadette Maynard

154. Willem Rethmeier

155. Helen Strong

156. Keats Wilmot

157. Colin Bateson

158. Dorte Conroy

159. Andrew Emery

160. Matthew Garrett

161. Joe Gianquitto

162. Angleo Demilo

163. David Arnold

164. Murray Charlton

165. Carolyn Cronan

166. Neil Fahey

167. Lisa Miosge

168. Geraldine Murphy

169. Michael Rogers

170. Adrian Rumsey

171. Dennis Wicklander

172. Jenny Williams

173. Vanessa Jud

174. Lachlan Schubert

175. Lorraine Soloman

176. Phil Trinder

177. Rod Banyard

178. Jeff Brown

179. Norm Burmester

180. Andrew Carter

181. Wendy Duncan

182. Bryan Furnass

183. Laurel Giles

184. Margaret Lee

185. Luis Teran

186. Steven March

187. Liz Morris

188. Chris Riddell

189. John Trotter

190. Linda Houseman

191. David Happold

192. Victor and Heather Douglas

193. Alan Reynolds

194. Lloyd Ashton

195. Doug and Karen Fox

196. Robyn Quach

197. Richard Bowman

198. Carl Brinkley

199. Tim Burns

200. Murray and Lisa Curtis

201. Ray O Donohue

202. Matthew Dwyer

203. Tom Lowrie

204. Vivian Martin

205. Daniel and Weronica Webster

206. Ann Wornes

207. Pam Wright

208. Peter Bryan

209. Hal Butterfield

210. Margaret Redzic

211. Keshini Richards

212. Anita Scherrer

213. Lilla Hendry

214. Ken Lanfear

215. Bertie Hennicke

216. Ian Campbell

217. Greg and Fiona Hammond

218. Andrew Davis

219. Ross Griffiths

220. Victoria Matthews

221. David Mcewan

222. David Newman

223. Keith Fifield

224. Kevin Jones

225. Andrew Moloney

226. Robin Osborne

227. Jeremy Cook

228. David Beattie

229. Meridith Ashton

230. Greg Convine

231. Mark Love

232. Bruce and Susan Young

233. Neil McKenzie

234. Juan Varela

235. Chris Mortlock

236. Mary Hoffman

237. John Mangos

238. Canturf Holdings Pty Ltd

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

AUSTRALIAN CAPITAL TERRITORY DISTRICT REGISTRY | |

GENERAL DIVISION | ACD 48 of 2012 |

IN THE MATTER OF ENVIRO FRIENDLY PRODUCTS PTY LTD (IN LIQUIDATION) (ACN 114 944 713)

BETWEEN: | STEPHEN JOHN HUNDY AND IVOR WORRELL IN THEIR CAPACITIES AS LIQUIDATORS OF ENVIRO FRIENDLY PRODUCTS PTY LTD (IN LIQUIDATION) (ACN 114 944 713) Plaintiffs

|

JUDGE: | FOSTER J |

DATE: | 20 AUGUST 2013 |

PLACE: | SYDNEY VIA VIDEO LINK TO CANBERRA (HEARD IN CANBERRA) |

REASONS FOR JUDGMENT

1 The plaintiffs are the joint and several liquidators of Enviro Friendly Products Pty Ltd (in Liquidation) (ACN 114 944 713) (the company). The company was wound up on 13 February 2012 by resolution of its creditors passed on that day. The liquidators had previously been the joint and several administrators of the company.

2 By Originating Process filed on 2 July 2012, the liquidators sought directions and determinations of questions pursuant to s 479(3) and, to the extent necessary or appropriate, s 511 of the Corporations Act 2001 (Cth) (the Act) in relation to four particular matters. The liquidators articulated those matters in the following terms:

(a) The classification of Renewable Energy Certificates (RECs) known as Small Scale Technology Certificates (STCs) believed to be held by the company as trust assets and thus separate from the general assets of the company;

(b) The identification of persons and entities that are beneficially entitled to the STCs held by the company;

(c) The determination of entitlements of those persons and entities that are determined to be beneficially entitled to the STCs held by the company; and

(d) The sale of the STCs held by the company and the distribution of the proceeds of such sale to persons and entities that are determined to be beneficially entitled.

3 As part of the work-out of the Court’s consideration of the subject matter of subpar (d) of [2] above, the liquidators seek an order that they be appointed as receivers and managers of the STCs held by the company in order to facilitate the independent sale of those STCs and that their reasonable costs in respect of administering the STCs be paid out of those proceeds of sale.

4 In their Originating Process, the liquidators propounded certain particular declarations and orders. At the hearing, the precise relief sought by the liquidators was set out in alternative versions of Proposed Orders. Those alternatives are styled “Option 2” and “Option 4”. The references to Option 2 and Option 4 are references to two of the options described by Mr Hundy, who is one of the liquidators, at pars 56 to 69 of an affidavit affirmed by him on 29 June 2012 and filed in this proceeding (Mr Hundy’s first affidavit). I note at this point that Options 1, 3 and 5 as described in those paragraphs of Mr Hundy’s first affidavit are not favoured by the liquidators.

5 The books and records of the company have not been well maintained. This has presented considerable difficulties for the liquidators in identifying and communicating with persons who might be interested in the subject matter of the present application. In the lead-up to the hearing, I made various orders designed to bring to the attention of all such persons the fact that the liquidators were making the present application and to inform those persons briefly but as accurately as possible of the nature of the liquidators’ application. These efforts may not have led to all interested persons being notified. However, I am satisfied that all reasonable steps were taken to bring this proceeding to the attention of the company’s former customers. Included within the orders which I made were orders requiring persons who intended to appear at the hearing to file a Notice of Appearance and also to file and serve any evidence and submissions upon which they intended to rely. Four persons filed a Notice of Appearance: They are Klaus and Caryl Matthaei, Margaret Reiby Lee and Bruce Stanley Pink. Mr and Mrs Matthaei also filed a submission. Mr Matthaei also appeared at the hearing and made oral submissions. Neither Ms Lee nor Mr Pink filed any documentary material. Both of those persons attended at the hearing and supported Mr Matthaei’s submissions. Mr Pink supplemented Mr Matthaei’s submissions with certain submissions of his own.

The Nature of the Current Proceeding

6 Senior Counsel who appeared for the liquidators addressed the nature of the current proceeding by reference to certain well-known authorities.

7 The first of these was Re GB Nathan and Co Pty Ltd (In Liq) (1991) 24 NSWLR 674. In that case, McLelland J, at 677–681, explained the history of the Court’s power to give directions and to make determinations of the kind sought in the present case. At 679–681, his Honour said:

There are significant similarities between the winding up of a company under the control of the court, and the administration of a deceased estate under the control of the court, and there are also similarities between the status of a court-appointed liquidator and that of a court-appointed receiver. It is reasonable to conclude that the statutory procedures for directions enacted in relation to trustees in bankruptcy by the 1869 Act and in relation to liquidators of companies by the 1890 Act were intended, so far as was consistent with the statutory framework, to be of the same nature and attended by the same incidents as the equivalent procedures under the general law, and under s 30 of the 1859 Act. It is also reasonable to conclude that the same considerations apply to s 479 of the Corporations Law which (like s 379 of the Companies (New South Wales) Code) is in practically identical terms to s 23 of the 1890 Act.

The historical antecedents of s 479(3), the terms of that subsection and the provisions of s 479 as a whole combine to lead to the conclusion that the only proper subject of a liquidator's application for directions is the manner in which the liquidator should act in carrying out his functions as such, and that the only binding effect of, or arising from, a direction given in pursuance of such an application (other than rendering the liquidator liable to appropriate sanctions if a direction in mandatory or prohibitory form is disobeyed) is that the liquidator, if he has made full and fair disclosure to the court of the material facts, will be protected from liability for any alleged breach of duty as liquidator to a creditor or contributory or to the company in respect of anything done by him in accordance with the direction.

Modern Australian authority confirms the view that s 479(3) “does not enable the court to make binding orders in the nature of judgments” and that the function of a liquidator's application for directions “is to give him advice as to his proper course of action in the liquidation; it is not to determine the rights and liabilities arising from the company’s transactions before the liquidation”: see Re Security Provident Fund Ltd (In Liq) (1984) 73 FLR 264 at 265; 9 ACLR 56 at 57; 2 ACLC 594 at 595; Murdoch v Crawford [1986] VR 97 at 99; Re Sportsman’s Leisure & Hobby Warehouse Pty Ltd (In Liq) [1990] 2 Qd R 93 at 96 and Re Byron Moore Journeaux Ltd (In Liq) [1990] VR 683 at 684; see also Re TTC (SA) Pty Ltd (In Liq) (1983) 32 SASR 532 at 535 and, in relation to a receiver’s application for directions, Re Odessa Promotions Pty Ltd (1979) ACLC ¶40-523 at 32,105-32,106. Canadian authority is to similar effect. In Re Ward (1987) 66 CBR (NS) 165 at 171, Dickson J of the Supreme Court of New Brunswick said in relation to the equivalent provision under the (Canadian) Bankruptcy Act:

“It seems well settled in law that in an application under s 16 of the Act a court must confine itself, in giving directions, to matters concerning administration of the estate and has no authority to resolve substantive matters in dispute between a trustee and a third party.”

It should be observed that there are instances where a court has, in proceedings commenced as a liquidator’s application for directions, gone on to make orders declaratory of substantive rights, clearly intended to be of binding effect on the parties to the proceedings, and where necessary has made representative orders for this purpose: see, eg, Re Staff Benefits Pty Ltd and the Companies Act [1979] 1 NSWLR 207 and cf Re Securitibank Ltd (In Liq) [1978] 1 NZLR 97; Re Securitibank Ltd [1978] 2 NZLR 133 and Re Securitibank Ltd (No 2) [1978] 2 NZLR 136. The procedures of the court are sufficiently flexible to enable proceedings commenced as an application for directions to be changed into proceedings for the determination of substantive rights, and this is sometimes a convenient course in order to avoid the need to commence further proceedings involving additional cost and delay: see, eg, Anmi Pty Ltd v Williams [1981] 2 NSWLR 138 at 156-157. However it is important that the distinction between the two kinds of proceedings be not lost sight of or blurred, and such a fundamental change should not be permitted unless the court is satisfied that those affected either consent to that course (see, eg, Re Standard Insurance Co Pty Ltd (1963) 5 FLR 292; 80 WN (NSW) 1355 and Murdoch (at 100-101)), or will not suffer injustice in consequence of the alteration to the status of the proceedings.

I should add that it does not necessarily follow that there is no appeal from an order of the court made on a liquidator's application for directions, although there are statements to this effect in some of the Australian cases commencing with the decision of Hanger J in Re Blackbird Pies (Management) Pty Ltd (No 2) [1970] QWN 14. The availability of an appeal in any particular case must depend upon the legislative provisions and rules regarding appeals in the particular court: cf Re Securitibank Ltd [1978] 2 NZLR 133. The availability of an appeal is primarily a matter for decision by the relevant appellate court, but in New South Wales it seems to me to be at least strongly arguable that an order made upon a liquidator's application for directions would constitute an interlocutory order from which an appeal would lie to the Court of Appeal with leave, pursuant to s 101(2)(e) of the Supreme Court Act 1970, and cases may arise where the practical consequences of the giving of directions could justify an appeal.

The primary matters of significance in the present application arising from the above considerations are that any directions which may be given to the liquidator (a) will not give rise to any conclusive determination as between GBN and its clients as to (i) whether particular assets held by GBN are held in trust for those clients or (ii) whether any such trust assets may properly be applied by the liquidator in payment of his remuneration and expenses; and (b) will not protect the liquidator against the claims of clients asserting that assets held by GBN are held in trust for those clients. However if the liquidator acts in accordance with any such directions (assuming full and fair disclosure of the material facts) he will be protected from claims by unsecured creditors or by contributories (or by the company itself), of any alleged breach of his duties as liquidator by so acting.

8 In Bastion v Gideon Investments Pty Ltd (2000) 35 ACSR 466 at 476 [49], Austin J said:

The directions are sought by the applicant as liquidator under s 479(3). No direction is sought by the company in liquidation under s 63 of the Trustee Act 1925 (NSW). I should note the very limited scope of the protection that directions under s 479(3) will give in the present circumstances. The directions will not determine as between the company and the investors whether there is a trust or any particular person is a beneficiary or any particular assets are held by the company in trust for the investors, and will not protect the company or liquidator from any claims by persons who do not receive a distribution but are able to establish that they should have been recognised as beneficiaries. As McLelland J pointed out in the G B Nathan case (at NSWLR 681), the significance of the directions is only that if the liquidator acts in accordance with them and has made full and fair disclosure of the material facts, he will be protected from claims by unsecured creditors or contributories in respect of any alleged breach of his duties as liquidator.

9 In the present case, the liquidators submitted that, as between those persons and entities for whom the Court concludes the company holds STCs in trust, on the one hand, and the general body of creditors, on the other hand, the Court’s determination on the question of whether those STCs are, in fact, held in trust, will have the practical effect of determining whether the relevant STCs are held in trust because the liquidators will be protected from liability in the event that they act in accordance with the directions of the Court in dealing with the relevant STCs. I agree.

Factual Background

10 Mr Hundy has had the primary carriage of the liquidation of the company. In support of the present application, he affirmed his first affidavit and affirmed two further affidavits, being those affirmed on 13 September 2012 (Mr Hundy’s second affidavit) and on 23 October 2012 (Mr Hundy’s third affidavit). The relevant facts are not controversial.

11 The business of the company was the sale and installation of various hot water and solar products. These products included domestic water tanks, water pumps, solar hot water systems, commercial hot water systems, solar power generators, grey water systems and smart-flow guttering. Within these classes of product, the company deployed various types and brands of product. Most of the sales were retail sales.

12 The company would retain subcontractors to perform the installation work for a set fee. The company would then charge the retail customer an agreed price from which the subcontractor would be paid. The company would then retain the difference as income.

13 The products sold and installed by the company which are relevant to the present application were Small Generation Units (SGUs) and Solar Hot Water Heaters (SWHs). The SGUs were solar power generation systems (including solar panels) and the SWHs were solar hot water systems within the meaning of the relevant legislation. As a consequence of the sale and installation of solar power generation systems and solar hot water systems, the retail customer became entitled to a certain number of STCs.

The Relevant Legislative Scheme

14 On 18 January 2001, the Renewable Energy (Electricity) Act 2000 (Cth) (the REE Act) came into force. As part of a program to increase the generation of electricity from renewable energy sources, the Australian Government established two schemes through this legislation. These are:

(a) The Large-Scale Renewable Energy Target; and

(b) The Small-Scale Renewable Energy Scheme.

15 Part 2 of the REE Act creates a scheme whereby persons who generate renewable electricity may create RECs. Under the REE Act, where a liable entity does not have enough RECs to surrender, the liable entity will have to pay a renewable energy shortfall charge. RECs are used to avoid or reduce the amount of renewable energy shortfall charges that liable entities who acquire electricity have to pay. The liable entities will generally acquire certificates by purchasing them.

16 A person who, during a year, makes a relevant acquisition of electricity is called a liable entity (s 5 and s 35 of the REE Act). A relevant acquisition of electricity is a wholesale acquisition of electricity or a notional wholesale acquisition of electricity (ss 5, 31, 32 and 33 of the REE Act).

17 RECs are created by persons or entities who generate power from accredited power stations using eligible energy sources where the amount generated exceeds the relevant 1997 eligible renewable power base line. RECs are also created for approved installations of SWHs and SGUs. RECs are created based upon the amount of electricity generated from renewable energy sources. The higher the output from such sources, the more RECS are created. A SGU, as defined in s 5 of the REE Act, is a device that generates electricity that is specified by the Regulations to be a small generation unit. The solar power generation systems sold and installed by the company were SGUs within the meaning of s 5 of the REE Act.

18 A person needs to be registered under Pt 2, Div 2 of the REE Act, before that person can create a REC. A REC must be registered when it is created. Every transfer of a REC must also be registered. The initial registration of RECs is done on line in an Internet-based registry managed by the Clean Energy Regulator (the Regulator).

19 When a REC has been surrendered by a liable entity, it ceases to be valid.

20 Part 2, Divs 1–4 of the REE Act govern the creation, trading and extinguishment of RECs.

21 RECs may be transferred after they have been registered by the Regulator.

22 Part 3 and Pt 4 of the REE Act impose a proportional liability on wholesale purchasers of electricity to hold a prescribed number of RECs in each year (s 35 and s 39 of the REE Act). Liable entities can satisfy the statutory liability by surrendering RECs to the Regulator.

23 The intention of the legislature in creating the scheme which I have described at [14]–[22] above is to put in place a market incentive to create renewable energy through the creation, registration, transfer and surrender of RECs in accordance with the statutory scheme.

24 From 2001 to 2010, there was a single certificate commodity, the REC. Since 1 January 2011, RECs have been reclassified into two types of certificate: Large-scale generation certificates and STCs.

25 Although the company created some large-scale generation certificates prior to 31 December 2010, these are no longer in the company’s possession or control. The present application concerns only STCs.

26 As submitted by the liquidators, the booklet published by the Regulator entitled “Increasing Australia’s Renewable Electricity Generation” provides a summary of the creation, assignment and sale of STCs as follows:

a. The number of STCs an ‘eligible installation’ is entitled to is dependent upon the amount of electricity generated by the solar panel or solar hot water system over a given period of time.

b. The STCs must be created within 12 months of the installation of the solar panel or solar hot water system.

c. All STCs must be created through the online Renewable Energy Certificate Registry (the REC Registry) before they can be traded, transferred or sold. The REC Registry is maintained by the Regulator.

d. The ownership of STCs vests in the customer but the STCs can be assigned to a registered agent (such as an installer or supplier), with the customer then receiving a financial benefit such as a discount on their invoice in exchange for the agent having the right to create and sell the STCs.

e. A customer wishing to assign his or her STCs to the agent must complete an ‘STC Assignment Form’ for the assignment to be effective. These forms are available from the Regulator's website.

f. Once the ‘STC Assignment Form’ is complete, the agent can then create the STCs through the online REC Registry and list them for sale through the STC market or the Regulator-managed ‘STC Clearing House’ (the Clearing House).

g. STCs sold on the STC market can be made available for sale to an interested buyer once they have been created and validated in the REC Registry.

h. STCs managed through the Clearing House are added to the end of the Clearing House transfer list. The STCs remain there until sold or withdrawn. The Clearing House operates on a 'first in first out' basis. Existing STCs in the transfer list must be sold before subsequently added STCs are eligible for sale through the Clearing House.

i. The price achieved on the sale of an STC depends on the way it is sold. If sold through the open market, the price will depend on demand and supply. If sold through the Clearing House, a statutory guarantee of $40 applies per STC. The market price has not reached the guaranteed price.

j. The demand for STCs is created by liable entities (commonly electricity retailers and wholesalers) that are mandated by law to buy and surrender a certain number of STCs per year. Surrendered STCs are invalidated by the Regulator and cannot be bought or sold again. The scheme is intended to operate such that when there are no STCs available on the open market, the liable entities must purchase their STCs from the Clearing House at $40 each.

27 At par 19 of his first affidavit, Mr Hundy said:

To assist the Court, I have extracted this diagram from the booklet reproduced at [123] which explains how the STC Market works:

The Company’s Transactions

28 The liquidators’ investigations indicate that, when a customer approached the company with a request for installation of a solar power generation system or a solar hot water system, the company provided the customers with a quotation in which it detailed the cost of installation and the number of STCs for which the company considered the customer would become eligible. The company also provided customers with a document entitled “Small Scale Technology Certificate (STC) Your option explained” in which the company set out the customer’s options in respect of the creation, assignment and trade of STCs.

29 After the solar power generation systems and solar hot water systems were installed at the customers’ premises, the customers would complete the relevant assignment form for the creation of the STCs that related to their installation. The liquidators’ investigations have led them to believe that the company, through its representatives and by means of information published on its website, represented to customers that the ownership of the STCs would remain with the customers. The liquidators based their conclusions to this effect upon a consideration of the company’s brochure to which I have referred at [28] above, upon information furnished to them by former employees and upon the circumstance that most of the STC Assignment Forms were completed and returned by the customers with the mandatory declaration sections concerning the assignment of the STCs to the company having been left blank.

30 It is for these reasons that the liquidators concluded that the company never suggested to its customers that it would be, or intended to be, the beneficial owner of the STCs created by the installation to which I have referred.

31 It appears that the company created and registered with the Regulator, or had been in the process of creating and registering with the Regulator, a total of 51,216 STCs.

STCs Now Held by the Company

32 The liquidators have carefully and continuously investigated the current holdings of STCs by the company. Mr Hundy dealt with that subject in his first affidavit and has updated the position in his subsequent affidavits.

33 As submitted on behalf of the liquidators, the company:

(a) Holds 21,987 STCs registered in the company’s name. Those STCs had a value in late 2012 of approximately $675,000;

(b) Should hold 37,145 STCs (but does not);

(c) Brought about a shortfall between the number of STCs which the company should hold and the number of STCs which, according to the REC register maintained by the Regulator, the company in fact holds. That shortfall is 15,158 (viz 37,145 minus 21,987).

34 The liquidators have endeavoured to ascertain what happened to the 15,158 STCs that are no longer held by the company.

35 There is no doubt that some STCs were sold by the company. It appears that the proceeds of those sales (at least in some cases) were applied by the company to its general operating costs. The proceeds were not distributed to its customers.

36 In addition, Mr Hundy testified that the liquidators have received numerous enquiries from persons who believe that they are owners of STCs held by the company claiming an entitlement to have those STCs returned by the company.

37 As submitted by Senior Counsel on behalf of the liquidators, these requests have raised considerable difficulty for the liquidators because:

a. there are discrepancies between the Company’s records of how many STCs it should hold and the number of STCs actually held by the Company. This is problematic because the Company's records indicate that there are only a few dozen STCs still with the Company (other than the 21,987 registered with the Regulator). There is a significant shortfall in the number of STCs compared with the number of entitled customers;

b. there is an order of priority for the sale of STCs in the Clearing House that is directly related to the original listing of the STCs on the Clearing House transfer list. The Company must withdraw from the Clearing House the earliest STCs without reference to the original owner of them, because the Company is listed as the holder of the STCs. The consequence of this is that some STCs that are linked to particular owners have been sold on behalf of other owners because the Company has sold them as ‘next available’ STCs; and

c. the Company’s records do not properly record the sale proceeds of particular owners’ STCs.

The Trust STCs

38 During the course of the liquidators’ investigations, they have made enquiries of those persons who they believe are entitled to STCs requesting them to provide certain information set out on a questionnaire.

39 Based on the responses received from customers and the investigations carried out by the liquidators of the company’s records, the liquidators have determined that:

(a) The persons listed in the Schedule to the Originating Process, which list has been updated by Mr Hundy’s second affidavit (eligible beneficiaries):

(i) Are STC holders; or

(ii) Should be STC holders;

(b) The persons listed in document 16 exhibited to Mr Hundy’s first affidavit have had their STCs sold by the company;

(c) The company holds 21,987 STCs as follows:

(i) 21,858 in the STC Clearing House; and

(ii) 129 available in the REC Registry (ie not in the Clearing House); and

(d) The company should hold 37,145 STCs on behalf of the eligible beneficiaries. The liquidators have categorised the eligible beneficiaries into three classes:

(i) Class A, being those customers who no longer have all or any STCs registered in connection with their installation;

(ii) Class B, being those customers who have received their full entitlements and are not therefore entitled to share in the distribution that may be forthcoming notwithstanding that they may still have STCs registered in their name in connection with their installation; and

(iii) Class C, being those customers that still have the full number of STCs registered in connection with their installation.

The Liquidators’ Analysis and Submissions

40 Senior Counsel for the liquidators referred me to the decision of Austin J in Bastion v Gideon Investments Pty Ltd, a case in which his Honour addressed most helpfully a number of issues which call for consideration in the present case. At 473–474 [33]–[38], his Honour said:

The present applications have been made on the basis that the liquidator must decide whether there is a trust governing the investors’ rights. The issue being uncertain, he properly seeks the protection of directions.

If there is no trust, the investors became unsecured creditors of the company when they deposited money with it. The liquidator must wind up the company and distribute its assets rateably to the unsecured creditors. The legal position is comparatively straightforward.

If there is a trust, the investors have equitable proprietary rights as beneficiaries and the company has the duties of a trustee, to be discharged by its liquidator. Those equitable proprietary rights are to be asserted against the trust fund and any assets into which the fund can be traced. It appears that there is no trust fund, but the company has acquired assets (the two insurance policies, the unit in Melbourne, and the shares) which might arguably be trust assets. The question becomes whether the beneficiaries can trace into those assets.

The evidence about the financial affairs of the company and the trust is very slim, and the position is unlikely to become much clearer through further investigations (given the thorough work that has already been done). However, we do have the statements by Ms Byrnes, which are consistent with information supplied by Mr Charlton, that the company did not maintain separate bank accounts for the trust or for moneys received from investors, and that Mr Bastion moved money in and out of accounts without any regard to the nature of the accounts or the sources of the money. Therefore (assuming there is a trust) the company has mixed all of the trust money received from investors with its own money, and has made some investments from the mixed fund and then dissipated the remainder. In such a case equity allows the beneficiaries to trace into the investments: Re Oatway; Hertstet v Oatway [1903] 2 Ch 356; see Jacobs’ Law of Trusts in Australia, 6th ed, 1997, Butterworths, p 746. It follows, on this analysis, that all of the company's remaining assets are trust assets which it holds for the benefit of the investors as beneficiaries.

The evidence does not point to any identified voidable transactions which might be attacked by the liquidator. However, any recovery of this nature would probably augment the trust assets rather than the company's own property, since on the tracing analysis presented above, money or assets used by the company in any such transaction would be presumed to be trust money or trust assets. It is likely that the company as trustee has a claim against Mr Bastion's estate for misappropriation of trust assets by him, but it appears that the estate is insolvent. I am unable to say, on the evidence, whether there is any basis for recovery from Mrs Bastion as the remaining director and if so, whether the proceeds of recovery would be for the benefit of the investors.

If there is no trust, the five “non-trust” creditors rank as unsecured creditors with the investors, unless they have statutory liens or other similar protection. If there is a trust, the debts to the “non-trust” creditors are best regarded as debts incurred by the trustee in the course of management of the affairs of the trust. That would be so as regards debts connected with ownership of the Melbourne unit, and while the Telstra account is less clear, the trustee would be justified in treating it in the same way. Although the debts might have been incurred in the course of unauthorised activity, the trustee probably has a right of recoupment or exoneration out of trust assets for these debts, having regard to the nature of the debts and the terms of the trust deed. Consequently the debts are to be paid in full out of company's assets (all of which are trust assets, on the present analysis).

41 At 476–477 [51]–[56], his Honour said:

In my opinion the evidence, though in some respects flimsy (like the evidence that was before me in the Graf Holdings case), persuades me that the funds of investors were collected by Mr Bastion on behalf of the company as trustee of an investment trust, and it is more likely than not that the terms of the investment trust were contained in the trust deed. I have indicated that the trust deed is very much a draft document, noting particularly that internal cross-references were frequently incorrect. However, one can work out the correct references, with patience, and so in the end the terms of the trust are reasonably precise. The most serious problem is that the number of units held by each initial unitholder is not set out in the schedule, as it should be according to cl 3(2), but the liquidator appears to have worked out the value of their investments from other evidence.

I am particularly influenced by the fact that the draft management agreement recites that the GHF Trading Trust was constituted by a deed dated 1 August 1993 (evidently the trust deed), and the evidence that investors believed that they were investing in accordance with it.

On the evidence before me I cannot reach the conclusion that the trust was amended by the management agreement. I note that the information memorandum appears to proceed on the basis that the management agreement was at that time operative, and some investors appear to have believed that they invested on the basis of the management agreement. However, the draft management agreement seems to contemplate the issue of new redeemable units, and I can see no evidence that any such units were issued.

Even if I had formed the view, on the evidence, that the management agreement became operative, its terms would not apply to investors who had become beneficiaries prior to its commencement.

The significance of this conclusion may be that it affects the question whether the company has acted in breach of trust by investing in property other than equities, bonds, currency markets and futures. It will be recalled that the powers of investment in the trust deed are very wide, but they would have been restricted if the management agreement had become operative.

In summary, I am prepared to give the direction sought in para (1) of the interlocutory process, since that paragraph identifies the trust deed but not the management agreement.

42 The liquidators submitted that, upon the basis of their investigations, the following matters were established:

(a) The company had, at one time or another, created or was in the process of obtaining 51,216 STCs;

(b) In respect of most of the STCs, the mandatory declaration sections of the assignment forms were left blank;

(c) Most of the STCs were registered in the STC Clearing House in the company’s name, despite there being no formal assignment of entitlements to the company by the corresponding customers;

(d) The company has already sold approximately 15,158 STCs with an estimated current value of approximately $465,350; and

(e) There is a shortfall of 15,158 STCs between the actual number of STCs in the STC Clearing House and the number of STCs that ought to be in the STC Clearing House.

43 Senior Counsel for the liquidators also emphasised that:

(a) The STC registration system required strict compliance with the legislative requirements, including the proper execution of any assignment of STCs to a registered agent;

(b) In the absence of an assignment by a customer to the company of the right to create the STCs, the company was not entitled to create or deal with the STCs in its own right.

44 For the reasons captured in the submissions made by the liquidators which I have summarised at [42]–[43] above, the liquidators submitted that there was strong support in the material which they have uncovered for the proposition that, with the exception of a small number of STCs, the company held the STCs on trust for the named customers as beneficiaries. If that conclusion be correct, the STCs are trust property and are, for that reason, not assets which are available to the general pool of creditors of the company. In addition, because the company appears to have sold STCs without authorisation from the beneficial owners and applied the proceeds to its own account, there is a substantial shortfall in trust assets arising from the company’s breach of trust as trustee. As a result, the beneficiaries would be entitled to pursue the company as trustee for any shortfall. This would make them creditors of the company to the extent of the shortfall.

45 The liquidators went on to submit that, if the STCs are held by the company on trust for the eligible beneficiaries, directions under s 479(3) of the Act would not be sufficient to protect the liquidators nor would they be sufficient to allow the trust to be managed and brought to an end. The liquidators submitted that, for these reasons, it was desirable that the Court appoint a person as receiver and manager of the STCs still held by the company pursuant to s 57(1) of the Federal Court of Australia Act 1976 (Cth).

46 At 478–480 [64]–[68] in Bastion v Gideon Investments Pty Ltd, Austin J said:

In the present case, in contrast with the Indopal case, there are no substantial trust creditors (assuming that the investors are beneficiaries), there is no suggestion of lack of cooperation by Mrs Bastion, and the assets are safely under the control of the liquidator. Nevertheless my opinion there is a justification for appointing a receiver and manager to the assets of the trust. Section 67 of the Supreme Court Act 1970 (NSW) gives the court a wide discretion to appoint a receiver and manager of assets upon an interlocutory application, and the jurisdiction is clearly available to protect trust assets. The appointment will not be made unless the case in favour of it is a strong one (Yunghanns v Candoora No 19 Pty Ltd (No 2) [2000] VSC 300 (unreported, SC(Vic), Warren J, 2093/99, 4 August 2000, BC200004629)), since receivership is an expensive process which could adversely affect rights of third parties. But the court will not hesitate to act where there is a real risk to the assets of a company or trust, as the Indopal case shows.

Here the problem is not only that the affairs of the trust are in disorder. To a substantial degree that is a problem to be addressed by the liquidator as such, and he has ample powers to do so. The difficulty is that he is the liquidator of a company which may have duties as trustee to the investors, requiring the company to ascertain, protect and ultimately distribute trust assets to them. But he does not know whether there is a trust in favour of the investors, and consequently whether those duties apply. The court is able to give him directions which will protect him in the steps he takes as liquidator, to the effect that he would be justified in recognising the existence of the trust. But those directions would not give any protection to third parties, including those who may wish to acquire the assets from the liquidator should he decide to sell them in the course of administration.

It seemed to me, therefore, that if I leave the liquidator to discharge the company's duty as trustee by realising the assets for the purpose of making distributions, he is likely to have difficulty in persuading buyers, especially in the case of the real estate, that he has good title to the assets. The problem will be overcome if I appoint him receiver and manager with an express power of sale as well as the powers contained in s 420 of the Corporations Law. That is what I intend to do.

The functions of the receiver and manager will relate to protection and realisation of the assets of the company, which are trust assets on the analysis that I have presented. I shall make orders requiring him to prepare a report on the performance of his functions, and to distribute it to the investors for their consideration, and then to account as receiver and manager to the company as trustee for the amount realised, after taking into account the investors’ views. I shall make an order treating the receiver and manager as a liquidator and the investors as creditors the purposes of Pt 5.6 Div 5 of the Corporations Law and Pt 5.6 of the Corporations Regulations, so as to provide machinery for the convening and conduct of the meeting of investors that I envisage. I have in mind that the realisation of assets, the report and the meeting should take place within three months of the date of this judgment, though I shall hear any submissions the liquidator has to make on that subject.

As long as he is required to report as receiver and manager to a meeting of investors in the manner that I envisage, I am prepared to appoint the liquidator as receiver and manager. The issue for the court to consider is whether there is any real possibility of conflict between the duties of the two offices, or between duty and interest, as McLelland J pointed out in the Grime Carter and Indopal cases. Given that the principal investigations have already been carried out, and in light of the limited functions of the receiver and manager, my opinion is that there is no such risk of conflict as would justify the cost involved in engaging another person as receiver and manager.

47 I have found the approach taken by Austin J in the paragraphs which I have extracted at [40]–[41] and [46] above to be most helpful in providing appropriate guidance in the present case. I intend to follow his Honour’s approach in determining the present application.

48 At pars 56–69 of his first affidavit, Mr Hundy said:

56. The Originating Process sets out several alternative options for the administration of the STCs. I am uncertain of the nature of the equitable entitlement of the former customers of the Company because of the shortfall in STCs.

57. The first option set out in the Originating Process provides that the STCs are held on trust by the Company for the benefit of the Eligible Beneficiaries; the STCs are to be treated as a single pool of trust assets to be sold and distributed rateably between the Eligible Beneficiaries only without regard to any existing registration or official reference to any particular Eligible Beneficiary (Option 1).

58. Option 1 is the most efficient and cost effective solution to sell and distribute the STCs. However, this option will result in the Correct Holding Customers and Shortfall Customers that still have some STCs registered in their name receiving less than they are entitled to. This option will also disregard the Company's entitlements and any entitlements the general creditors of the Company may have to the proceeds of the sale of the STCs.

59. The second option set out in the Originating Process provides that the STCs with the exception of the Company STCs are treated as a single pool of trust assets to be sold and distributed rateably between the Eligible Beneficiaries and the Company STCs forming part of the general pool of assets of the Company to be divided between the general creditors of the Company (Option 2).

60. Option 2 is also efficient and cost effective, as the STCs can still be sold and distributed as in Option 1 with an additional effort in dealing with the Company STCs. The main feature of this option is that the general creditors will be given access to the proceeds of the sale of the Company STCs.

61. The third option set out in the Originating Process provides that the Shortfall Customers and the Correct Holding Customers receive the full benefit of any STCs registered in their names, with the remaining STCs (Surplus Customers' STCs) to be distributed rateably to the Shortfall Customers (Option 3).

62. Option 3 is inefficient and less cost effective, as it involves more administrative costs in dealing with the distribution of the STCs either by sale or direct transfer to the entitled Eligible Beneficiaries. The problem with this option is that high administrative costs will result in a lower return to Eligible Beneficiaries. Further, there will be an unequal distribution between the Eligible Beneficiaries, as the Shortfall Customers will be disadvantaged in that they will receive a lesser distribution as compared to Options 1 or 2. This option will also disregard any entitlements the general creditors of the Company may have to the proceeds of the sale of the STCs.

63. The fourth option set out in the Originating Process provides that the Shortfall Customers and the Correct Holding Customers receive the full benefit of any STCs registered in their names with the remaining STCs (Surplus Customers' STCs), with the exception of the Company STCs, to be distributed rateably to the Shortfall Customers and the Company STCs forming part of the general pool of assets of the Company to be divided between the general creditors of the Company (Option 4).

64. The administrative costs associated with Option 4 are similar to Option 3 but this option has the additional requirement to deal with the Company STCs. This option further limits the return to Shortfall Customers.

65. The fifth option set out in the Originating Process provides that all STCs be treated as part of the general pool of assets of the Company to be sold and divided between the general creditors of the Company including the Eligible Beneficiaries (Option 5).

66. Option 5 is also efficient and cost effective but my main concern with this option is that the entitlements of the Eligible Beneficiaries to the Trust Assets will not be met. As mentioned in paragraphs 54 and 55 above, the total amount owed by the Company to its general creditors is large, which would likely result in the Eligible Beneficiaries receiving a small distribution or nothing at all.

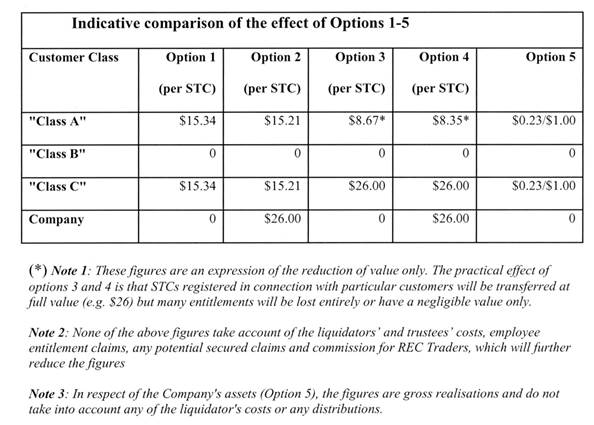

67. Using the nominal figure of $26 per STC, a conceptual example of the financial effects of the above options is as follows:

68. It is for the above reasons that I am seeking a direction from the Court that I am justified in taking one of the alternative courses set out in the Originating Process. From my perspective the most efficient course is for Option 1 being as follows:

a. finding that all of the STCs still held by the Company are held on trust for the benefit of the Eligible Beneficiaries;

b. proceeding with a sale of the STCs and distributing the proceeds of sale as follows:

i. Paying the costs and expenses of the joint & several Administrators and joint & several Liquidators in determining, reconciling and preserving the trust assets and determining the entitlements of the Eligible Beneficiaries.

ii. Paying the costs and expenses of the Receiver & Manager in realising and distributing the trust assets to the Eligible Beneficiaries.

iii. Distributing the balance to the Eligible Beneficiaries who are to rank rateably according to the number of their STCs.

69. I consider that the proposal set out at paragraph 67 is the most practical, cost effective and timely means of finalising the distribution of the STCs, because the 'first in first out' rule of the Clearing House means that any STCs sold by this avenue could be waiting for an unspecified and indeterminable period of time as the value of the STCs on the open market is currently less than the statutory guarantee of $40 for STCs sold through the Clearing House.

49 When Mr Hundy refers to “paragraph 67” in par 69 of his affidavit, I have taken him to be referring to par 68 of that affidavit.

50 The liquidators also mentioned a theoretical Option 6. This option would involve seeking to recover the amounts already paid to Class B beneficiaries and adding those amounts to the overall pool, which would then be shared among all beneficiaries including members of Class B. Quite apart from legal difficulties thrown up by such a course, the liquidators submitted that the course was impractical because it would require the liquidators or receiver and manager to bring a string of small claims against beneficiaries for relatively small amounts of money in each case. It was submitted that it was likely that the recovery costs would far outweigh any benefit obtained by the process, even if recovery was achieved. In addition, the liquidators submitted that it was likely the purchases were bona fide purchases for value, in any event, with the result that the purchasers would be able successfully to resist any claims brought by the liquidators or any receiver and manager.

Mr Matthaei’s Submissions

51 Mr Matthaei made the following submissions:

(a) Representatives of the company had informed his wife and him that STCs created in respect of his installation would be registered in their names;

(b) In fact, those STCs were registered in the name of the company;

(c) Neither he nor his wife were ever told that the STCs in respect of the installation at their premises would become assets of the company or be part of any trust fund;

(d) The STCs created in respect of the installation at his premises were “illegally” sold to Flinders Operating Services on 16 August 2011 without the consent of either his wife or him;

(e) The STCs in respect of the installation at their premises were resold to Alinta Sales on 6 February 2012;

(f) The Court should not be satisfied that all interested persons had been notified of the present proceeding; and

(g) Mr Matthaei and his wife, and others in a similar position, want the STCs which should have been held for them returned to them without any diminution in value by reason of the liquidators’ costs.

52 Specifically, at par 20 of his written submission, Mr Matthaei said:

Briefly we unanimously agreed that

(i) we all believed that the STCs were listed in our names and were not the assets of EFP

(ii) we require that the STCs be returned to us and distributed to us without any deductions to cover the costs the liquidators. The liquidators input was not requested or authorised by us, hence their costs should be confined to the liquidation of EFP.

(iii) we do not want Worrells to administer the STCs.

(iv) On the question "how should the STCs be administered?" it was unanimously agreed that

(a) the STCs be treated as a single pool of trust assets;

(b) the Eligible Beneficiaries be treated as a single class of beneficiaries without regard to any existing registration or official reference to any particular Eligible Beneficiaries;

(c) the STCs be sold;

(d) the proceeds of sale of the STCs be divided between the Eligible Beneficiaries:

(i) on a pro rata basis in accordance with the number of STCs held by each of the Eligible Beneficiaries; and

(ii) without regard to any exist

53 Mr Matthaei also submitted that the 418 STCs which were registered in the name of the company should be put into the general pool of trust STCs to be made available to the eligible beneficiaries and not be set aside for the general body of creditors.

The Submissions of Mr Pink

54 As I mentioned at [5] above, Mr Pink made oral submissions at the hearing. Mr Pink explained that, once STCs were in the Clearing House, they would be dealt with on a first in, first out, basis. He then said that, if they are taken out of the Clearing House, his understanding was that it was last in, first out. He agreed that the end result was much the same, either way.

The Liquidators’ Response to Messrs Matthaei and Pink

55 The liquidators filed a written response to the submission made by Mr Matthaei in writing. The liquidators’ responsive document was filed on 19 October 2012. It is not necessary to go to that document in any detail. However, the following submissions contained in that document are presently significant, namely:

(a) The liquidators had nothing to do with the resale of the STCs created in respect of the installation at the premises of Mr and Mrs Matthaei;

(b) The liquidators have done their very best to inform all interested parties of the present proceedings. In particular, the liquidators have sought and complied with Orders of the Court to notify such persons of the existence and subject matter of the present proceeding;

(c) The STCs cannot now be returned to the beneficiaries in specie without deduction. That is the underlying difficulty facing the liquidators which has caused them to make the present application; and

(d) Any question as to the liability of the directors of the company in respect of the way in which STCs were handled is not a matter that falls for consideration in the present application.

Decision

56 I have found the liquidators’ submissions to be most helpful. I accept and adopt them. I propose to adopt Option 2 propounded by the liquidators. My reasons may be briefly stated as follows.

57 The affairs of the company were in considerable disorder prior to its going into liquidation. The trust assets are incomplete. There are substantial costs involved in the management of the trust assets and a trustee or receiver and manager will need to seek indemnity from the remaining assets of the trust in respect of the management of the trust.

58 As the liquidators submitted, the assets of the trust will need to be sold in order to:

(a) Deal with the claims of beneficiaries whose trust assets have been wrongly dealt with; and

(b) Indemnify the trustee or receiver and manager.

59 The beneficial owners of the STCs can be classified into three groups.

60 Class A (shortfall customers) are those who should still have STCs, but who do not. These are customers who did not ask for their STCs to be sold but who suffered the sale of their STCs in lieu of the sale of other customers’ STCs who had made a request for sale. An example of a customer in Class A is given in par 43 of Mr Hundy’s first affidavit.

61 Class B (surplus customers) are those who instructed that their STCs be sold but, as a result of that instruction, other customers’ STCs were sold instead. These customers have already been paid for the sale of their STCs. This means that the instructing party’s STCs remain notionally on the books of the company. There is also an example of a Class B customer in par 43 of Mr Hundy’s first affidavit.

62 Class C (correct holding customers) are those customers who are unaffected by the problems of Class A and Class B. These are customers who gave no instructions to sell their STCs and in respect of whom no STCs were actually sold.

63 In addition to the customers in Classes A, B and C, there is a small number of STCs that were never held on behalf of any customer of the company. These STCs are identified in par 34 of Mr Hundy’s first affidavit. These STCs are assets of the company in the winding up and are to be held by the liquidators for distribution to the general body of creditors. They are not assets held on trust.

64 The liquidators seek a direction that the STCs referred to in par 34 of Mr Hundy’s first affidavit (418 STCs) should be declared to be assets available for distribution to the general body of creditors.

65 As I have already noted at [51]–[54] above, Mr Matthaei, Mr Pink and Ms Lee all submit that the Court should direct that the 418 STCs in this category be sold and that the proceeds of sale be added to the general pool of funds available for the eligible beneficiaries. Unfortunately, as much as I would like to make the direction sought by Mr Matthaei, Mr Pink and Ms Lee, I cannot do so. The 418 STCs to which I have referred must be dealt with in accordance with general corporations law principles. In the circumstances of this case, as matters presently stand, that means that they must be regarded as part of the assets of the company to be made available for the general body of creditors.

66 For reasons advanced by the liquidators and effectively supported by the eligible beneficiaries from whom I have heard, I have reached the conclusion that the remaining STCs held by the company are held on trust for the eligible beneficiaries. Given that I have already concluded that the 418 STCs identified in par 34 of Mr Hundy’s first affidavit must be held for the benefit of the general body of creditors, the options available to the Court for determining the present application are Option 2 and Option 4 as outlined by Mr Hundy in his first affidavit at pars 60, 63 and 64.

67 Because the Class B customers have already been paid for the sale of STCs which were supposed to be theirs but which were not, to include these customers in the distribution would be to give them a windfall to which they are not entitled. The Court’s direction in relation to these customers should therefore be that the Class B STCs be included in the distribution of STCs to other customers (that is to say, other eligible beneficiaries) and that the Class B beneficiaries not be entitled to any further distribution from the trust assets.

68 As far as the Class C customers are concerned, I think that the fairest approach is to pool the STCs of all of the Class A and Class C customers together and to allow them to share in the pooled STCs held on trust. This result seems to me to be a fairer way of addressing the consequences of the shortfall with which the liquidators are confronted because it recognises that the difference in outcome presently existing between the Class A and the Class C customers is a pure happenstance in the sense that the outcome for those customers has depended entirely upon the luck of the draw.

69 To adopt Option 4 is to favour Class C customers over Class A customers in circumstances where, in truth, the consequences of the company’s actions should be borne by all customers in both Class A and Class C, rather than idiosyncratically by Class A customers only.

70 It seems that Option 2 is favoured by both the liquidators and such of the eligible beneficiaries from whom I have heard.

71 For these reasons, I propose to adopt Option 2.

72 I also propose to appoint the liquidators as receivers and managers of those STCs held on trust by the company. Although there may be some theoretical possibility that there will be a conflict of interest, I think that that possibility is more theoretical than real. The advantages to be gained by all concerned in having the same persons who have conducted all of the investigations and inquiries in respect of the company’s affairs to date as receivers and managers of the trust assets are obvious. In addition, the obligations of the plaintiffs as liquidators of the company and the obligations of the plaintiffs as receivers and managers of the trust assets are quite distinct. Apart from the 418 STCs to which I have referred at [63]–[65] above, the remaining STCs held by the company are trust assets and should be dealt with on that basis.

Costs

73 Senior Counsel for the liquidators cited the judgment of Campbell J in Re French Caledonia Travel Service Pty Ltd (In Liq) (2003) 204 ALR 353 (French Caledonia) in support of his submissions in respect of costs. In that case, Campbell J cited and relied upon the following passage from the judgment of Finkelstein J in 13 Coromandel Place Pty Ltd v CL Custodians Pty Ltd (In Liq) (1999) 30 ACSR 377 at 385:

These cases establish, clearly enough in my opinion, that provided a liquidator is acting reasonably he is entitled to be indemnified out of trust assets for his costs and expenses in carrying out the following activities: identifying or attempting to identify trust assets; recovering or attempting to recover trust assets; realising or attempting to realise trust assets; protecting or attempting to protect trust assets; distributing trust assets to the persons beneficially entitled to them.

The position is a little more involved as regards work done and expenses incurred in what may be described as general liquidation matters. If that work is unrelated to the beneficiaries and their claims it is difficult to see whether costs could be charged against their assets. In the case of a company which has carried on the business of trustee it might be that much of the work involved in the liquidation is chargeable against trust assets if it can be shown that the liquidation is necessary for the proper administration of the trust. But it is unlikely that this will be so where the company did not act solely as trustee or at least did not act in that capacity to a significant extent. In that event, the liquidator will be required to estimate those of his costs that are attributable to the administration of trust property and only those costs will be charged against the trust assets.

74 At 413–414 [211]–[213] in French Caledonia, Campbell J said:

The overlap there is, in the duties of a liquidator of a corporate trustee, between some of the activities which he carries out qua liquidator, and some of the activities which he carries out as the person with administrative control of the trustee, is of particular importance in this case. Even though a liquidator needs to go to court to have it established that he has a right of remuneration from trust assets for work done in administering them, that right is one which is not accorded the liquidator in the exercise of some kind-hearted discretion of the court, but is accorded to him in accordance with equitable principle. The liquidator's right to receive such a payment, when the factual circumstances are made out, is every bit as much a matter of legal right as is a solicitor's “fruits of the action” lien (Firth v Centrelink (2002) 55 NSWLR 451), or a provisional liquidator’s lien over property he or she has preserved (Shirlaw v Taylor (1991) 31 FCR 222; 102 ALR 551). As Lord Browne-Wilkinson said in Foskett v McKeown [2001] 1 AC 102 at 109; [2000] 3 All ER 97 at 102:

The rules establishing equitable proprietary interests and their enforceability against certain parties have been developed over the centuries and are an integral part of the property law of England. It is a fundamental error to think that, because certain property rights are equitable rather than legal, such rights are in some way discretionary. This case does not depend on whether it is fair, just and reasonable to give the purchasers an interest as a result of which the Court in its discretion provides a remedy. It is a case of hard-nosed property rights.

To the extent that the liquidator does work which would entitle him both to remuneration as liquidator, and also to payment in accordance with the principle recognised in Berkeley Applegate, there is a situation where two funds — the distributable property of the company, and the trust assets — are each liable to bear that expense. If two funds are both liable to meet an expense, principle ordinarily requires that there be contribution between the two funds in meeting that expense. As this is a case where there are no assets of the company available to meet the liquidator's general expenses it is not necessary to decide whether, if there were both trust assets, and other assets of the company, available to meet expenses of the liquidator which fell into this “overlap” area, there is any reason to deny the application of contribution in the case of the liquidator of a corporate trustee. (Arguments for denying it and requiring the liquidator to resort primarily to the non-trust assets, so far as liquidator's remuneration were concerned, though possibly not concerning out-of-pocket expenses, might possibly be put by analogy with a trustee's inability to make a profit from his trust. An argument against denying it might be put that the trust beneficiaries ought not freeload on the general creditors concerning an expense for their mutual benefit.) The usual principle concerning contribution is that if one of two parties each liable to pay some particular amount is insolvent, the other party must bear the whole of that amount. The other party will have a right of contribution against the insolvent party, which would be provable in the bankruptcy or liquidation of the insolvent party. Whether or not contribution is available in cases where there are both trust assets and non-trust assets available to meet a liquidator's expense in the “overlap” area, the equitable lien recognised in Berkeley Applegate means that all costs of the liquidator properly attributable to the administration of the trust assets can be paid from the trust assets. Thus, a liquidator has done work which is attributable equally to the winding up of the company, and the administration of trust assets, and there are no assets of the company at all to meet his expenses in doing so, the expenses are payable solely from the trust assets.

However in no circumstances will the liquidator be able to recover from the trust assets the expense of doing any work which could not be fairly categorised as administering the trusts. Further, as Finkelstein J noted in 13 Coromandel Place (at 586) if a liquidator is administering, through the company of which he is liquidator, more than one trust:

… the liquidator is not entitled to charge the beneficiaries of one trust with the costs and expenses incurred in relation to the other trust. Accordingly, it will be necessary for the liquidator to estimate the costs and expenses incurred insofar as they relate to each trust and only charge those costs to the trust on whose behalf the work was performed. If that estimate is not possible then a pari passu distribution of the costs and expenses will be in order as was envisaged by King CJ in Suco Gold, supra. The second difficulty is the possibility that the liquidator has performed work on behalf of investors for whom no property is held on trust. If that is the case the liquidator could not look to the existing trust assets for the costs and expenses of that work unless, in accordance with the foregoing principles, the liquidator is entitled to charge those assets with a proportionate share of the costs. That would be so if the costs and expenses are not so divisible.

75 Relying upon the principles to which I have referred at [73]–[74] above, the liquidators submitted that their investigations into the affairs of the company included the analysis and identification of the trust assets now being dealt with as trust assets for the benefit of the eligible beneficiaries. These investigations fell into the “overlap” mentioned by Campbell J at 413–414 [211]–[213] of French Caledonia. Senior Counsel for the liquidators submitted that his clients’ investigations concerned both investigations into the affairs of the company in their capacity as liquidators for the purposes of winding up and also investigations into the whole issue of whether the STCs were trust assets. It was said that the liquidators’ investigations had revealed the existence of the trust which, in turn, had led to the present application. These submissions are correct and I accept them.

76 In evidence before me, Mr Hundy explained that the costs to which he referred at par 72 of his first affidavit all related to the administration of the trust. Consequently, it was submitted on behalf of the liquidators that the work described in that part of Mr Hundy’s first affidavit and the costs of carrying out that work should all be allowed to the liquidators as trustees of the relevant trust. I agree.

77 The liquidators have estimated their fees to date to be $81,577. Their estimate as to future likely fees is in the range of $71,272.85 to $90,982.10.

78 Upon the basis of the evidence tendered before me, I think that the amount of $81,577 as being the liquidators’ estimate of their costs to date is reasonable. In my judgment, that amount is also attributable to work done as trustees of the STCs held by the company and thus attributable to the administration of that trust.

Conclusion

79 For all of the above reasons, I propose to make orders in accordance with Option 2 propounded by the liquidators.

80 There will be orders accordingly.

I certify that the preceding eighty (80) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Foster. |

Associate: