FEDERAL COURT OF AUSTRALIA

Tax Practitioners Board v Shanahan [2013] FCA 764

IN THE FEDERAL COURT OF AUSTRALIA | |

| Applicant | |

AND: | Respondent |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT DECLARES THAT:

1. On each of the 47 separate occasions detailed in Schedule A to these orders between about May 2010 and about June 2012, the respondent supplied a tax agent service in contravention of subsection 50-5(1) of the Tax Agent Services Act 2009 (Cth) by providing a service to the taxpayers referred to in Schedule A by reason of the following:

(a) the respondent requesting and receiving from the taxpayer information that was potentially relevant to the preparation of the taxpayer’s income tax return and completing details of the taxpayer’s income tax return in preparation for lodgement with the Australian Taxation Office;

(b) for which the respondent either received or charged a monetary payment for providing the said service;

(c) with knowledge of the matters referred to in sub-paragraphs 1(a) and 1(b) above;

(d) while the respondent was not a registered tax agent pursuant to the Tax Agent Services Act 2009 (Cth) or working under the supervision and control of a registered tax agent;

(e) which was not a service relating to a business activity statement; and

(f) which was not provided as a legal service;

in each case:

(g) by reason of the matters referred to in sub-paragraphs 1(a) and 1(b) above, provided a service that the taxpayer could reasonably be expected to rely upon to satisfy liabilities or obligations, or claim entitlements, that arise, or could arise, under a taxation law.

2. On each of the 2 separate occasions detailed in Schedule B to these orders between about December 2010 and September 2011, the respondent supplied a BAS service in contravention of subsection 50-5(2) of the Tax Agent Services Act 2009 (Cth) by providing a service to the taxpayers referred to in Schedule B by reason of the following:

(a) the respondent requesting and receiving from the taxpayer information that was potentially relevant to ascertaining liabilities, obligations, or entitlements under A New Tax System (Goods and Services) Act 1999 (Cth) and preparing a Business Activity Statement for the taxpayer;

(b) for which the respondent either received or charged a monetary payment for providing the said service;

(c) with knowledge of the matters referred to in sub-paragraphs 2(a) and 2(b) above;

(d) while the respondent was not a registered tax agent or BAS agent pursuant to the Tax Agent Services Act 2009 (Cth) or working under the supervision and control of a registered tax agent or BAS agent; and

(e) which was not provided as a legal service;

in each case:

(f) by reason of the matters referred to in sub-paragraphs 2(a) and 2(b) above, provided a service that the taxpayer could reasonably be expected to rely upon to satisfy liabilities or obligations, or claim entitlements, that arise, or could arise, under A New Tax System (Goods and Services) Act 1999 (Cth).

3. On the 20 occasions detailed in Schedule C to these orders between about April and October 2010, the respondent falsely represented to the taxpayers referred to in Schedule C that the respondent was a registered tax agent in contravention of subsection 50-15 of the Tax Agent Services Act 2009 (Cth).

THE COURT ORDERS THAT:

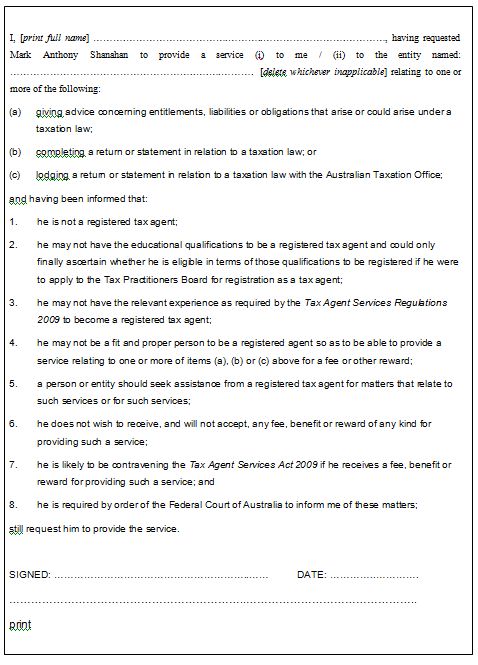

4. An order that the respondent, for a period of 3 years from the date of this order, if he is requested to provide to another person or entity a service relating to one or more of:

(a) advising another person or entity in relation to their entitlements, liabilities or obligations in relation to an Australian taxation law or A New Tax System (Goods and Services) Act 1999 (Cth);

(b) completing for another person or entity a return or statement in relation to an Australian taxation law or A New Tax System (Goods and Services) Act 1999 (Cth); or

(c) lodging for another person or entity a return or statement in relation to a taxation law or A New Tax System (Goods and Services) Act 1999 (Cth) with the Australian Taxation Office;

then, before providing or agreeing to provide the said service, he must, unless then registered as a tax agent or, in respect of a BAS service, a registered BAS agent, pursuant to the Tax Agent Services Act 2009 (Cth) or working under the supervision and control of a registered tax agent or, in respect of a BAS service, a registered BAS agent, inform the person or entity of the matters referred to in paragraphs 1 to 8 in Form A annexed hereto and, if the person or entity still requests the service be performed by the respondent:

(d) have the person or entity complete and sign Form A annexed hereto;

(e) retain a copy of the form for a period of 3 years; and

(f) provide any such signed forms to the Tax Practitioners Board (TPB) within 14 days of its request.

5. In respect of each of the 47 separate contraventions of s50-5(1) of the Tax Agent Services Act 2009 (Cth), the respondent pay to the Commissioner of Taxation for the Commonwealth a pecuniary penalty of $617.02 for each contravention.

6. In respect of each of the 2 separate contraventions of s50-5(2) of the Tax Agent Services Act 2009 (Cth), the respondent pay to the Commissioner of Taxation for the Commonwealth a pecuniary penalty of $500, for each contravention.

7. The respondent pay the applicant’s costs in the sum of $1,000 by 31 December 2013.

8. The respondent pay the pecuniary penalties totalling $30,000 referred to in orders 5 and 6 by instalments as follows:

(a) $5,000 by 30 June 2014;

(b) $5,000 by 30 June 2015;

(c) $5,000 by 30 June 2016;

(d) $5,000 by 30 June 2017;

(e) $5,000 by 30 June 2018;

(f) $5,000 by 30 June 2019.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

SCHEDULE A

| Column 1 | Column 2 | Column 3 | Column 4 |

Taxpayer | Relevant tax years | Amount of fee paid or charged for | Approximate date of the preparation of the income tax return | |

1 | Alan Boyd | 2009 | $155 | 21 June 2010 |

2 | Alan Boyd | 2010 | $165 | 3 November 2010 |

3 | Debra Boyd | 2009 | $155 | 21 June 2010 |

4 | Debra Boyd | 2010 | $165 | 3 November 2010 |

5 | Janet Carrigan | 2009 | Portion of $1,782 | 3 May 2010 |

6 | Janet Carrigan | 2010 | $160 | 27 April 2011 |

7 | Michael Carrigan | 2009 | Portion of $1,782 | 3 May 2010 |

8 | Michael Carrigan | 2010 | $160 | 27 April 2011 |

9 | Partnership of J Carrigan and M Carrigan | 2009 | Portion of $1,782 | 3 May 2010 |

10 | Partnership of J Carrigan and M Carrigan | 2010 | Portion of $1,340 | 27 April 2011 |

11 | Carrigan Constructions Pty Ltd | 2009 | Portion of $1,782 | 3 May 2010 |

12 | Carrigan Constructions Pty Ltd | 2010 | Portion of $1,340 | 27 April 2011 |

13 | Gregory Chittick | 2010 | $671 | 3 February 2011 |

14 | Jessica Chittick | 2010 | $100 | October 2010 |

15 | Julie Chittick | 2010 | $95 | 28 October 2010 |

16 | Glenda Cook | 2009 | Portion of $515 | 27 May 2010 |

17 | Glenda Cook | 2010 | Portion of $575 | 29 October 2010 |

18 | Kenneth Cook | 2009 | Portion of $515 | 27 May 2010 |

19 | Kenneth Cook | 2010 | Portion of $575 | 29 October 2010 |

20 | Robert Croll | 2010 | $105 | 26 October 2010 |

21 | Robert Croll | 2011 | $110 | 10 July 2011 |

22 | Jarrod Gehrmann | 2010 | $112.50 | 5 August 2010 |

23 | Mark Harris | 2009 | Portion of $2,387 | 14 July 2011 |

24 | Andrew Hart | 2010 | $120 | 9 September 2010 |

25 | Andrew Hart | 2011 | $120 | 12 April 2012 |

26 | Natasha Hart | 2010 | $115 | 6 August 2010 |

27 | Natasha Hart | 2011 | $120 | 12 April 2012 |

28 | Brien Hosking | 2010 | $120 | 17 January 2011 |

29 | Natasha Hosking | 2010 | $120 | 17 January 2011 |

30 | Jayne Lewis | 2010 | $600 | 19 November 2010 |

31 | Jayne Lewis | 2011 | $535 | 19 October 2011 |

32 | William Moore | 2010 | $125 | 1 September 2010 |

33 | William Moore | 2011 | $125 (approx) | 15 November 2011 |

34 | Catherine Murray | 2010 | $110 | 30 July 2010 |

35 | Catherine Murray | 2011 | $145 | 23 August 2011 |

36 | Brett Murray | 2010 | $125 | 30 July 2010 |

37 | Brett Murray | 2011 | $145 | 23 August 2011 |

38 | Arianna Nash | 2010 | $140 | 17 August 2010 |

39 | Deborah Sedgwick | 2010 | $195 | 9 February 2011 |

40 | Deborah Sedgwick | 2011 | $360 | 21 June 2012 |

41 | Jan-Marie Tai | 2010 | $110 | 17 August 2010 |

42 | Jan-Marie Tai | 2011 | $120 | 10 August 2011 |

43 | Michael Tai | 2010 | $110 | 19 August 2010 |

44 | Michael Tai | 2011 | $110 | 17 August 2011 |

45 | Andrew Tom | 2010 | $110 | 5 August 2010 |

46 | Andrew Tom | 2011 | $110 | 26 October 2011 |

47 | William Toulmin | 2010 | $125 | 23 August 2010 |

Schedule B

Column 1 | Column 2 | Column 3 | |

Taxpayer | BAS period | Amount of fee paid | |

1 | Gwinn Pty Ltd (Brien Hosking) | 2010 | $3,600 |

2 | Gwinn Pty Ltd (Brien Hosking) | 2011 | $3,600 |

SCHEDULE C

Column 1 | Column 2 | |

Taxpayer | Approximate date of representation | |

1 | Alan and Debra Boyd | 16 June 2010 |

2 | Janet Carrigan | 20 April 2010 |

3 | Michael Carrigan | 14 April 2010 |

4 | Glenda and Kenneth Cook | 27 May 2010 |

5 | Glenda and Kenneth Cook | 29 October 2010 |

6 | Robert Croll | 28 October 2010 |

7 | Andrew Hart | 9 September 2010 |

8 | Natasha Hart | 6 August 2010 |

9 | Natasha Hart | 24 September 2010 |

10 | William Moore | 1 September 2010 |

11 | William Moore | 1 October 2010 |

12 | Catherine Murray | 2 September 2010 |

13 | Catherine and Brett Murray | 30 July 2010 |

14 | Brett Murray | 16 September 2010 |

15 | Stuart and Adrianna Nash | 17 August 2010 |

16 | Adrianna Nash | 16 September 2010 |

17 | Jan-Marie Tai | 17 August 2010 |

18 | Jan-Marie Tai | 17 September 2010 |

19 | Michael Tai | 17 September 2010 |

20 | William Toulmin | 21 September 2010 |

Form A

NEW SOUTH WALES DISTRICT REGISTRY | |

GENERAL DIVISION | NSD 28 of 2013 |

BETWEEN: | TAX PRACTITIONERS BOARD Applicant

|

AND: | MARK ANTHONY SHANAHAN Respondent

|

JUDGE: | RARES J |

DATE: | 19 JULY 2013 |

PLACE: | SYDNEY |

REASONS FOR JUDGMENT

(REVISED FROM THE TRANSCRIPT)

1 This is an application by the Tax Practitioners Board for the imposition of civil penalties under the Tax Agent Services Act 2009 (Cth), together with declaratory and injunctive relief in respect of numerous contraventions of the Act alleged against Mark Shanahan. The parties have largely agreed the facts and the orders and relief appropriate to give effect to findings of the contraventions.

The Legislative scheme

2 Critically, s 50-5(1) of the Act provides that a person contravenes the Act if he or she provides a service knowing, or where he or she ought reasonably to know, that it is a tax agent service and charges a fee or other reward for providing that service, when not a registered tax agent. Correspondingly, s 50-5(2) establishes an analogous contravention where the service provided is a BAS service. It is not necessary to go into the definitions of those services. Additionally, a person contravenes s 50-15 if he or she represents that he or she is a registered tax agent or BAS agent, and the representation is untrue.

3 The maximum penalties for contravention of s 50-5(1) and (2), for an individual, were 250 penalty units. At the time of Mr Shanahan’s contraventions, one penalty unit equated to $110. The maximum penalty for a contravention of s 50-15, for an individual, was 50 penalty units. Importantly, s 50-35(3) provided that if conduct contravened two or more civil penalty provisions of the Act, proceedings could be instituted against the person in relation to the contravention of any one or more of those provisions, but he or she was not liable to more than one pecuniary penalty in respect of the same conduct. The Court is given jurisdiction by s 70-5 to grant an injunction against a person whom it is satisfied had engaged, or was proposing to engage, in conduct that would constitute a contravention of a civil penalty provision. In addition, the Court has a general power under s 21 of the Federal Court of Australia Act 1976 (Cth) to grant declaratory relief.

The contraventions of the Act

4 Mr Shanahan gave oral evidence this morning which supplemented the agreed facts. Over the period May 2010 to June 2012, Mr Shanahan provided tax agent services to 28 taxpayers who were clients of his accounting business. That gave rise to 47 separate contraventions of s 50-5(1) of the Act in respect of his having provided tax agent services for fees when he was not a registered tax agent. He also provided BAS services to a company owned by one of his clients, in respect of whom the contraventions of s 50-5(1) occurred, in respect of two financial years for reward, in contravention of s 50-5(2). In addition, Mr Shanahan used letterhead when rendering his fees to some of those clients that represented that he was a registered tax agent when that was not the true position, in contravention of s 50-15.

Mr Shanahan’s circumstances

5 Mr Shanahan is 50 years of age. He is married and has an 18-year-old daughter. Mr Shanahan finished school in 1979 and attended Wollongong University while training with a large accounting firm. After he obtained his degree in accountancy, he joined a small firm and worked there until made a partner in 1988. About a year later, he left the partnership and worked principally as the finance manager of the Kiama Leagues Club for the next 11 and a half years. When he ceased that employment, he opened an accountancy practice in Kiama using a corporate vehicle, M & P Consultancy (Australia) Pty Limited, which was a registered tax agent under previous legislation. The business was a general purpose accounting business providing accountancy and tax advice, bookkeeping and tax agent services. Mr Shanahan had formed a business relationship with William Butler who had been the auditor of the Kiama Leagues Club while he worked there, and who had indicated that he wished to downsize his operations as he moved towards retirement. Mr Butler shared Mr Shanahan’s business premises with him. Mr Butler was a registered tax agent at all times.

6 By late 2007, the business was struggling and just making ends meet. At that point, Mr Shanahan, sought and obtained psychological counselling to deal with issues of depression, stress and anxiety that he was then feeling as a result of both serious illnesses of his mother and parents-in-law who lived in Orange in New South Wales. He failed to respond timeously to requests of the Board’s predecessor, the Tax Agents’ Board of New South Wales, to provide information in answer to a letter asking his firm to show cause why it should not be re-registered. On 27 November 2008, the Board’s predecessor, refused to re-register Mr Shanahan’s company as a tax agent. The letter informing him of that decision identified that he had the right to seek merits review in the Administrative Appeals Tribunal within 28 days. However, he appears to have filed his application out of time and, after a period, realised that it needed to be withdrawn.

7 After Mr Shanahan ceased to have any registration as a tax agent personally or through his company, he continued to do work for clients. That work involved, at the times of the contraventions, the provision of tax agent services or, in the case of the BAS matters, BAS services. He used an old letterhead of his own which to send fees which had his name, qualifications and the statement “registered tax agent and public accountant” underneath as part of the letterhead.

8 The Board has not suggested, that in the performance of his work, Mr Shanahan acted in any way that caused any of his clients to fail to comply with any obligations under the taxation laws. The substantial complaint is that he knowingly and deliberately represented himself as a tax agent and received payment for performing services as a tax (or BAS) agent when he had no right to do so. By the time of the contraventions, Mr Shanahan’s evidence, which I accept, was that his practice was not producing a great deal of income. Indeed, he thought it was breaking even or making very small profits, and that the two staff whom he employed were earning more than he was. He found his financial circumstances to be difficult and, as regrettably often happens in such cases, was willing to engage in conduct that contravened the law in order to keep his clients coming to him for the performance of the range of services that he offered.

9 The contraventions of s 50-5(1) involved Mr Shanahan preparing and submitting tax returns for his clients for the income years ending 30 June 2009 to 2011, the last contravention occurring on 21 June 2012. Mr Shanahan agreed to requests by each of his clients to provide services connected with the preparation and lodgement of those tax returns. For that purpose, received from the clients, or their authorised representatives, information and documents that were potentially relevant for the preparation of the return, considered that information and documents, where necessary requesting further information and documents, determined the taxpayer’s assessable income and allowable deductions and offsets and prepared an income tax return for the taxpayer with the information provided. He subsequently lodged the income tax return with the Australian Taxation Office on behalf of the taxpayer through a tax agent portal using the tax agent number of Mr Butler, who still remained a registered tax agent. But he did that without Mr Butler’s knowledge.

10 Mr Shanahan performed his work believing that his clients or their authorised representatives, such as their family members, or the directors or officers of companies for whom he was working, were relying on his specialist knowledge in relation to their income tax returns for the purpose of their satisfying their liabilities or obligations or claiming entitlements that had arisen under a taxation law.

11 None of the contraventions of s 50-5(1) occurred in relation to a business activity statement and were not provided by Mr Shanahan acting as a legal practitioner for the purposes of the exceptions in s 50-5(1)(b) and (e). And correspondingly when he provided the two BAS services, Mr Shanahan was aware that those services were of that character, that he was not a registered BAS agent within the meaning of the Act and that, accordingly, he had contravened s 50-5(2). The essential ingredients for each of the admitted contraventions are set out in the agreed statement of facts. The fees which Mr Shanahan earned for the provision of these services performed in contravention of the law were relatively modest, ranging from about $105 to about $700, albeit that some of the fees were a portion of a greater lump sum charge that he made for the provision of other services to some of his clients. Mr Shanahan charged a total of $6,269 for 36 of the admitted contraventions. It is likely that the other contravening conduct earned him a proportionately similar sum, although the parties have not been able to identify precisely how much.

12 The maximum penalty that could be imposed for the contraventions was over $1.35 million. Mr Shanahan’s current financial position is in evidence. He has a house which he shares with his wife, but is in his name alone. It is worth in the order of $460,000 on his estimate, which has not been challenged. It is subject to mortgages to his bank securing about $260,000 in respect of a home loan and about $36,700 in respect of a business loan. He is in default of the business loan and the bank is seeking repayment. He has made arrangements with his mother to obtain a loan from her with which to repay the business loan to the bank and has promised his mother that he will pay her about 5% interest on the money borrowed.

13 Mr Shanahan is also in default in respect of credit card debts worth about $24,000 which are in the hands of a collection agency. In addition, he has business debts of about $65,000 and household debts of about $6,000. His current salary is in the order of about $60,000. Mr Shanahan, in his oral evidence, said that he earned about $1,100 after expenses net per week, with almost nothing left over. He now works, and has since August last year, for a company that provides financial planning advice. He is employed as an accountant and small business strategist under the supervision of a registered tax agent in his employer. His employer’s principal has given Mr Shanahan a reference that demonstrates that he is receiving appropriate support to deal with the issues arising from this litigation and in developing the skills necessary to seek to put himself in the position of being registered as a tax agent once again. The employer regards him as a very competent team member and a person who is highly valued by its clients.

Consideration

14 When the parties made their written submissions for the hearing today, they had agreed on a penalty of $45,000 and a contribution towards the Board’s costs of $1,000. Their agreement had been predicated on Mr Shanahan having a pecuniary penalty imposed on him for contraventions of each of ss 50-5(1) and (2), and as well as s 50-15. He said that he thought deeply for about three or four days about the amount that he could responsibility agree to pay by way of a penalty and the period over which he could do so. The agreement between the parties recorded that he would pay $6,000 by 31 December this year, and $10,000 by 31 December of each subsequent year until the total amount of $46,000 had been paid.

15 Having heard his evidence, I was not satisfied that, first, Mr Shanahan realistically has the capacity to make those payments or, secondly, that $46,000 marked an appropriate penalty in all of the circumstances. I raised with the parties the question of whether they had overlooked in their discussions the application of s 50-35(3) in respect of the overlap between the contraventions of ss 50-5(1) and (2) and s 50-15, albeit that the overlap in penalties was, in one sense, a minor matter in the scheme of things. The parties then, over a short adjournment, discussed whether the agreed penalty should be re-considered. They have now agreed on a total penalty of $30,000 payable by instalments of $5,000 commencing on 30 June next year, with the $1,000 in costs being payable on 31 December 2013.

16 The task of the Court in considering an agreed civil penalty was authoratively explained by Burchett and Kiefel JJ in NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission (1996) 71 FCR 285 at 290-298. Ultimately, it is for the Court, and the Court alone, to impose a penalty under the Act. But where parties agree as to an appropriate penalty, that agreement can assist the Court in arriving at a conclusion that that agreement is a proper figure. In NW Frozen Foods 71 FCR at 291A-B, Burchett and Kiefel JJ said in a passage that has equal application to similar agreements by individuals and regulators generally in respect of civil penalties:

“There is an important public policy involved. When corporations acknowledge contraventions, very lengthy and complex litigation is frequently avoided, freeing the courts to deal with other matters, and investigating officers of the Australian Competition and Consumer Commission to turn to other areas of the economy that await their attention. At the same time, a negotiated resolution in the instant case may be expected to include measures designed to promote, for the future, vigorous competition in the particular market concerned. These beneficial consequences would be jeopardised if corporations were to conclude that proper settlements were clouded by unpredictable risks. A proper figure is one within the permissible range in all the circumstances. The Court will not depart from an agreed figure merely because it might otherwise have been disposed to select some other figure, or except in a clear case.”

17 That approach has recently been called into question by the Court of Appeal of the Supreme Court of Victoria in Australian Securities and Investments Commission v Ingleby [2013] VSCA 49. Nonetheless, I am bound by the decisions of the Full Court in NW Frozen Foods 71 FCR 285 and Minister for Industry Tourism and Resources v Mobil Oil Australia Pty Limited [2004] FCAFC 72 at [70].

18 The original penalty figure agreed by the parties was arrived at without the benefit that I have had of seeing and hearing Mr Shanahan’s oral evidence. I am satisfied that he fully appreciates his wrongdoing, its gravity and its inappropriateness. I am also mindful that this occurred during a period of great personal stress in his life, where misguidedly and, as he said, wrongly, he was not only supporting his own family, but two employees who were working for him. Those matters do not excuse, but they explain, a series of contraventions that have had profoundly upsetting and distressing impact on Mr Shanahan. I am quite satisfied that he has learnt his lesson.

19 In his evidence, Mr Shanahan acknowledged that what he had done was wrong and that he was conscious that, at the time he did it, it was wrong. I am quite satisfied from having seen him in the witness box that he is genuinely remorseful and contrite. He clearly is suffering significantly from the burden of his recognition of the transgressions of responsibility and trust which the conduct he engaged in amounted to. There is no suggestion that that conduct was anything other than exceptional for him, albeit that it was conduct that occurred over a lengthy period of nearly two years and was deliberate.

20 Nonetheless, the contraventions in which he engaged were deliberate and involved him consciously misusing Mr Butler’s tax portal without Mr Butler’s knowledge in order to get around his own personal situation of not being a registered tax, or BSA, agent.

21 The community must be satisfied that the courts will recognise the need to deter such conduct, both for the individual concerned and to deter others. In the present case, I am mindful that while Mr Shanahan has lost his integrity through that conduct, it is not suggested that his clients or the tax office suffered adverse consequences, except for their reliance on Mr Shanahan’s contravening behaviour of holding himself out as qualified to do something that the law said he was not.

22 I am also satisfied that although Mr Shanahan’s very strained and modest financial circumstances will be severely impacted on by the presently agreed penalty of $30,000 in a way that while reflecting an appropriate condemnation of his conduct, will not impose such a burden as to overwhelm or crush him in the future. The agreed penalty is close to about one half of one year’s pre-tax wage or earnings for Mr Shanahan, in circumstances where he currently is not making ends meet. He has expressed genuine contrition and remorse, and is not likely, in my view, to fall into the error of his contravening conduct again.

23 I am satisfied that the now agreed penalty of a total of $30,000 with $1,000 in respect of the Board’s costs, payable in the structure that the parties have agreed, is within a range that I would regard as appropriate in all of the circumstances. For these reasons I will make the orders and declarations that the parties have agreed.

I certify that the preceding twenty-three (23) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Rares. |

Associate: