FEDERAL COURT OF AUSTRALIA

McPharlin, in the matter of United Investments Trust (in liq) [2013] FCA 635

IN THE FEDERAL COURT OF AUSTRALIA | |

IN THE MATTER OF UNITED INVESTMENTS TRUST (IN LIQUIDATION)

ACN 102 195 568

HUGH LACHLAN MCPHARLIN AS LIQUIDATOR OF UNITED INVESTMENTS TRUST (IN LIQUIDATION) ACN 102 195 568 Plaintiff | |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

1. Pursuant to s 485(2) of the Corporations Act 2001 (Cth) the Court adjusts the rights of the contributories on the basis that the remaining assets in the managed investment scheme known as United Investments Trust (“the scheme”) are to be distributed on a pro-rata basis calculated by reference to the difference (if positive) between the sum paid to the scheme by a contributory for unit subscription and any sum repaid to the contributory by the scheme.

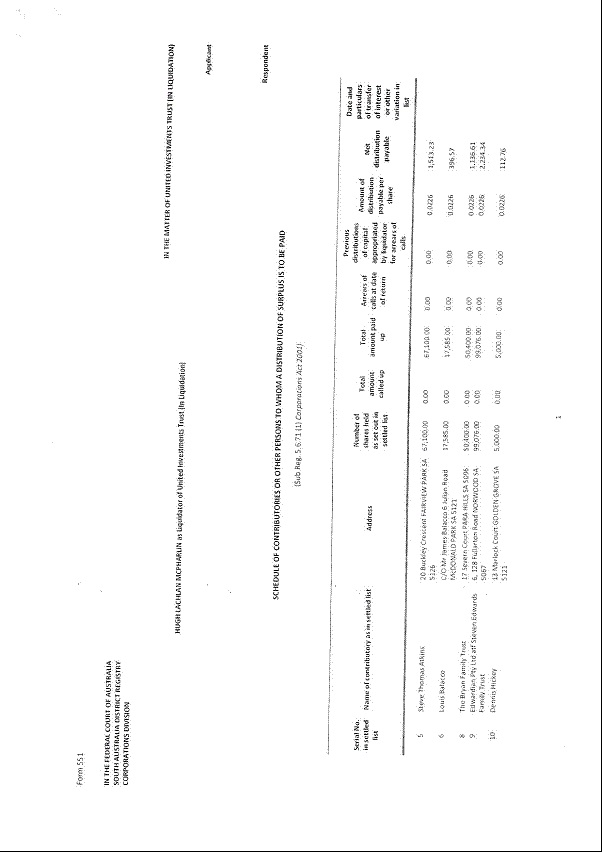

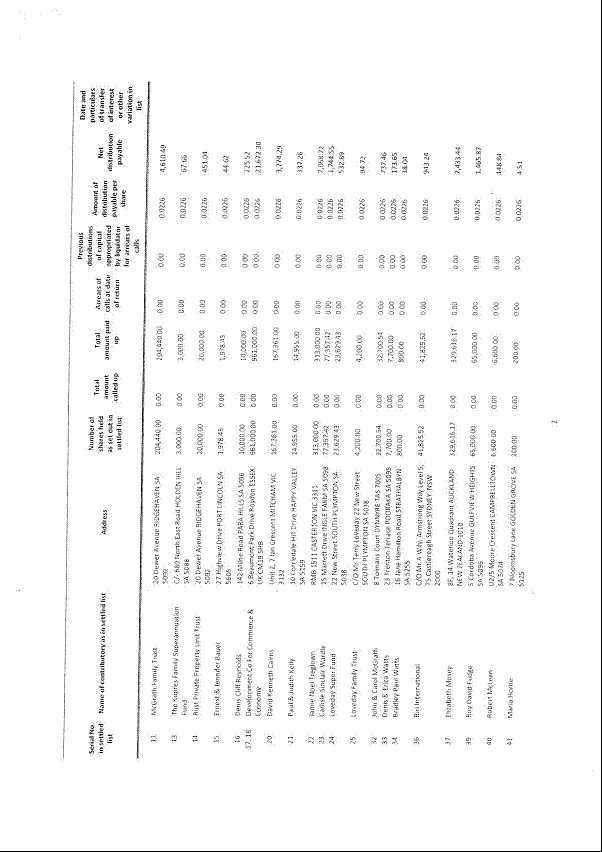

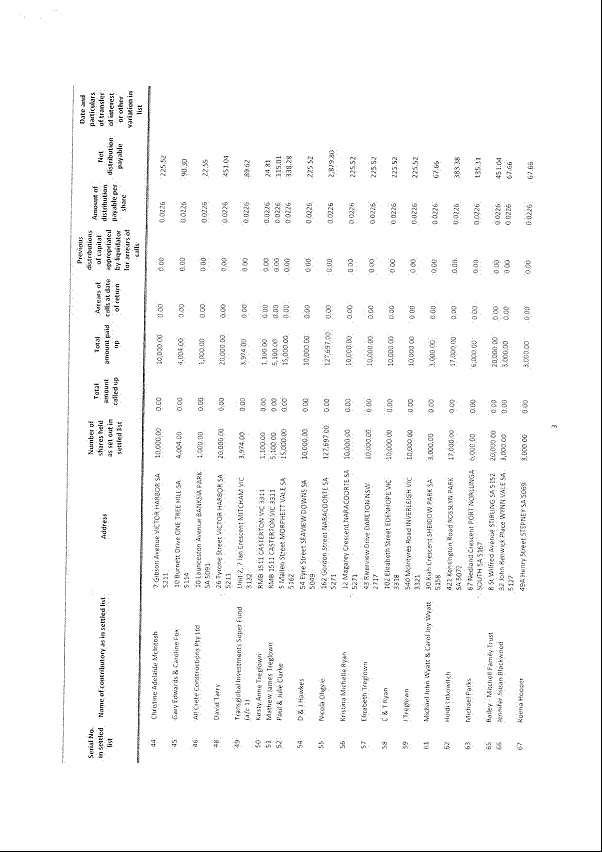

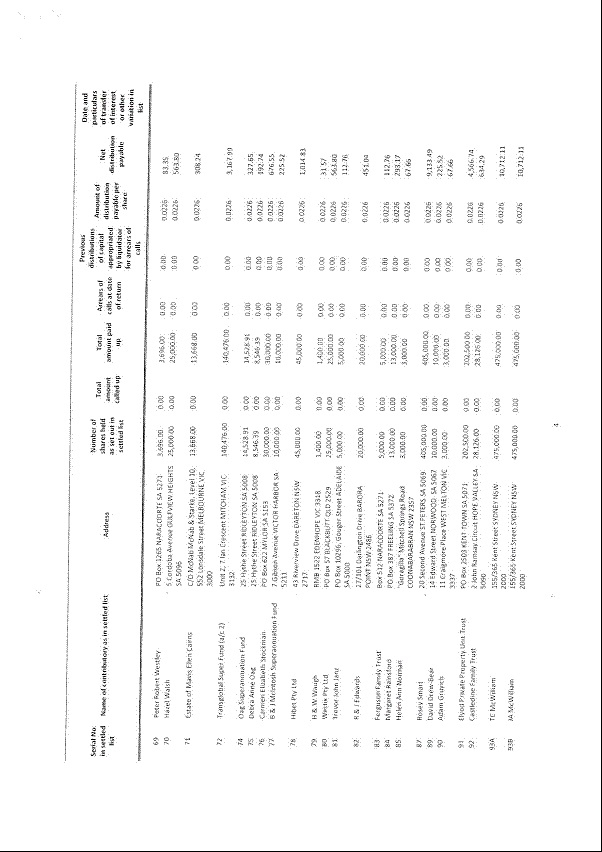

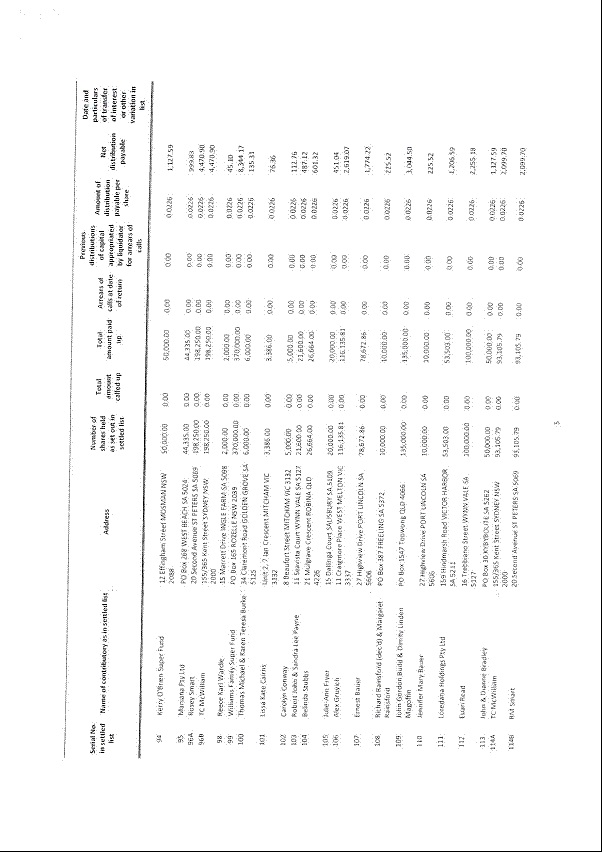

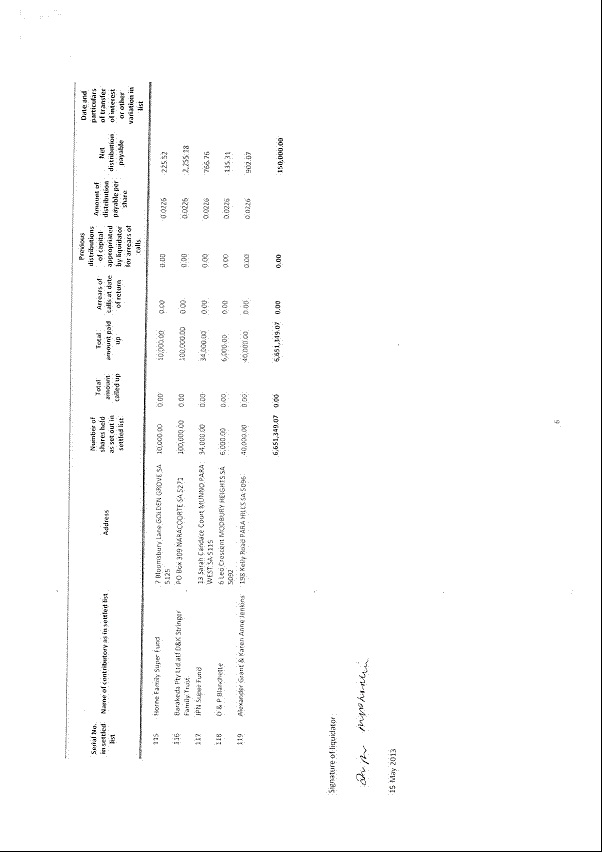

2. Special leave is granted to the plaintiff pursuant to s 488(2) of the Corporations Act 2001 (Cth) to distribute a surplus of $150,000 to the contributories of the scheme in accordance with the foregoing item 1 and in accordance with the Form 551 Schedule annexed to this order.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

SOUTH AUSTRALIA DISTRICT REGISTRY | |

GENERAL DIVISION | SAD 94 of 2013 |

IN THE MATTER OF UNITED INVESTMENTS TRUST (IN LIQUIDATION)

ACN 102 195 568

BETWEEN: | HUGH LACHLAN MCPHARLIN AS LIQUIDATOR OF UNITED INVESTMENTS TRUST (IN LIQUIDATION) ACN 102 195 568 Plaintiff

|

JUDGE: | BESANKO J |

DATE: | 27 June 2013 |

PLACE: | ADELAIDE |

REASONS FOR JUDGMENT

1 This is an application by the plaintiff who is the liquidator of a managed investment scheme. He seeks the following orders:

1. Pursuant to s 485(2) of the Corporations Act 2001 (Cth) the Court adjusts the rights of the Contributories on the basis that the remaining assets in the managed investment scheme known as United Investments Trust (the Scheme) are to be distributed on a pro-rata basis calculated by reference to the difference (if positive) between the sum paid to the Scheme by a Contributory for unit subscription and any sum repaid to the Contributory by the Scheme.

2. Special leave is granted to the Plaintiff pursuant to s 488(2) of the Corporations Act 2001 (Cth) to distribute a surplus of $150,000 to the Contributories of the Scheme in accordance with the foregoing item 1 and in accordance with the Form 551 Schedule annexed to this Order.

2 The amount of the surplus is said to be $150,000. Before making the orders sought by the plaintiff I should be satisfied that the provisions of the Corporations Act 2001 (Cth) and the Corporations Regulations 2001 (Cth) (“the regulations”) have been complied with. I should be satisfied that there is a surplus of $150,000. Finally, I should be satisfied that the proposed adjustment of the rights of the contributories among themselves is the appropriate adjustment in the circumstances. For the reasons which follow, I am satisfied of these matters and I will make the orders sought.

3 The evidence before me on the application consisted of the following:

(1) an affidavit of the plaintiff sworn on 20 May 2013;

(2) an affidavit of the plaintiff’s solicitor sworn on 24 May 2013;

(3) a second affidavit of the plaintiff sworn on 19 June 2013; and

(4) brief oral evidence of the plaintiff on 21 June 2013.

4 The United Investments Trust (“UIT”) is an unregistered managed investment scheme. On the application of the Australian Securities and Investments Commission (“ASIC”) a judge of this Court made an order on 13 September 2002 that UIT be wound up and that the plaintiff be appointed liquidator of UIT. The judge further ordered that the liquidator has or may exercise such functions and powers as set out in Chapter 5 of the Corporations Act as he would be entitled to exercise if the scheme were a company, with such modifications as are reasonably necessary in the circumstances.

5 UIT was established on 12 July 1999 as a discretionary trust. At the hearing on 21 June 2013 the trust deed was put before me. From July 2002 UIT operated as a fixed unit trust contrary to the terms of the trust deed. UIT was an unregistered managed investment scheme contrary to s 601ED of the Corporations Act.

6 The corporate trustee of UIT was Jetsby Pty Ltd (“Jetsby”) and at all relevant times Jetsby’s directors were Mr Terry Loveday and Mr James Balacco. The plaintiff states that at the time of his appointment parties investing in UIT were known as unitholders. The plaintiff refers to them throughout his evidence as contributories.

7 The funds of contributories were initially invested in shares, derivatives and other equities of other companies. From mid 2001, UIT’s activities escalated and its funds were applied in a manner which involved much greater risks than its initial more modest investments.

8 As a result of his investigations, the plaintiff has determined that nearly all of the monies invested by contributories in UIT were lost in connection with speculative overseas investments in New Zealand and the United States of America. In his first affidavit the plaintiff describes the speculative investments. It is not necessary for me to set out the details.

9 In early September 2002, the directors of Jetsby approached ASIC with concerns about one of the schemes and the overseas investments they had made. ASIC commenced an investigation into UIT and then applied for the plaintiff’s appointment as liquidator. As a result of investigations by ASIC, criminal charges were laid against Messrs Loveday and Balacco in the District Court of South Australia by the office of the Director of Public Prosecutions. Those criminal charges related to their roles in carrying on an unregistered managed investment scheme. Messrs Loveday and Balacco pleaded guilty to certain charges and were sentenced by a judge of the District Court. Mr Loveday was sentenced to 20 months imprisonment with a non-parole period of 6 months. Mr Balacco was sentenced to 14 months imprisonment and was released upon entering into a good behaviour bond.

10 In his first affidavit the plaintiff provides a summary of his investigations since his appointment in September 2002. He describes the process as extensive and he states that it has been delayed at various stages due to its general complexity, legal complications, and an absence of documentation. The plaintiff expresses the opinion that all legal avenues for the recovery of all available assets have been explored and resolved, and that consequently, the winding up should be completed.

11 UIT’s only assets are cash deposits of approximately $176,000. The plaintiff is of the view that UIT has no other creditors other than his own unpaid costs and the costs of his solicitors in relation to the present application. He anticipates that after the payment of legal fees and his unpaid costs there will be a surplus of $150,000 available to be distributed to contributories.

12 On 10 October 2002 UIT’s Committee of Inspection was established by a meeting of contributories. The Committee has been consulted on all major decisions in the winding up. The Committee met on 19 June 2012 and it agreed that the plaintiff should bring the present application and that after this application has been determined, the plaintiff should apply to the Court for the completion of the winding up of UIT.

13 On 31 August 2012 the final list of contributories was settled. The plaintiff is of the view that the list was settled in accordance with regulation 5.6.58 – 5.6.62 of the regulations.

14 One of the issues the plaintiff has had to consider in connection with the distribution of UIT’s remaining funds has been the appropriate basis for ranking the claims of contributories. The plaintiff considers that the possible bases for doing that include an apportionment based on the purported number of issued units and the purported value of issued units by reference to a register of the attributed value of individual investments. The plaintiff has determined that units were issued to contributories for various notional values. He has been unable to verify the true value of the units by reference to the register of investments. At the time of the plaintiff’s appointment some of the contributories had received from UIT a repayment of funds they had advanced to UIT. The plaintiff considers that the most equitable basis for the distribution of UIT’s remaining funds is on a net cash basis rather than by reference to the notional value of the units. In other words, he considers that the surplus should be distributed on a pro rata basis calculated by reference to the difference (if positive) between the sum paid to UIT by a contributory for the unit subscription and any sum repaid to the contributory by UIT. He considers that that is the most equitable basis for the distribution of UIT’s remaining funds because he cannot verify the true value of the units. At its meeting on 19 June 2012, the Committee of Inspection approved the distribution of funds on the basis proposed by the plaintiff.

15 In his first affidavit, the plaintiff not only outlines the investigations he has undertaken in the liquidation, but he also states his views as to possible recovery actions. He states that ultimately for commercial reasons and taking into account the limited funds within the administration and the unlikelihood of gaining litigation funding, no substantive foreign proceedings were commenced.

16 The plaintiff outlines the assets which have been recovered and the liabilities which have been paid since the commencement of the liquidation.

17 As far as creditors are concerned, the plaintiff states that on 20 June 2007 he placed a notice in The Australian newspaper requiring any creditors whose debts or claims had not yet been admitted to submit particulars of their debts or claims by 20 July 2007. The plaintiff did not receive any new claims as a result of this publication.

18 In October 2009 the plaintiff rejected claims by three participants in the managed investment scheme and those parties have not subsequently pursued their claims against UIT. He also rejected claims by various trade creditors on the basis that any such claims should be made against Jetsby not UIT and that, because of its breach of duty, Jetsby had no right of indemnity against UIT. The claims of the various trade creditors totalled approximately $22,500. By letter dated 24 May 2012, the plaintiff reiterated his view to the trade creditors that they had no claims against UIT, and as at 20 May 2013 he had received no response. The plaintiff holds the view that UIT has no creditors other than those already mentioned.

19 The plaintiff outlines the steps he has undertaken to comply with the regulations dealing with the settlement of the list of contributories.

20 By reason of the affidavit of the plaintiff’s solicitor sworn on 24 May 2013, I am satisfied that proper notice of this application has been given.

21 In his second affidavit, the plaintiff states that with the exception of AGL which claimed $813.09, none of the trade creditors completed any proofs of debt in the liquidation of UIT. By letter dated 22 January 2003, the plaintiff advised AGL that its claim was properly addressed to UIT’s trustee, Jetsby, and that, as liquidator of UIT, the plaintiff denied any claim for indemnity by Jetsby by reason of Jetsby’s various failures to deal properly with UIT’s assets. The plaintiff outlines in further detail the content of the letter sent to trade creditors on 24 May 2012 and the letter sent to alleged participants in the managed investment scheme on 7 October 2009 (see [18]).

22 The plaintiff excluded various contributories from his settled list on the basis that they had received all, or more cash, than they had contributed with respect to their units in UIT. The plaintiff is of the view that the number of units held by contributories or the value attributed by UIT to the units should not be used as a basis to distribute the surplus to contributories. He notes the following. First, units in UIT were initially issued at $1, and thereafter, a value was attributed to all issued units at the end of the month. Secondly, by the end of June 2002, which was three months before his appointment, the unit values had purportedly increased to $2.4021 per unit. Thirdly, the unit values attributed during the life of the scheme and as at June 2002 could not be substantiated by reference to UIT’s underlying assets or financial records. Fourthly, the financial performance of UIT on a monthly basis was described in the register as “intrest (sic) + bonus”. In some instances, the interest and bonuses were negative. Fifthly, the interest and bonuses, in the plaintiff’s view, could not be substantiated by reference to UIT’s underlying assets or financial records. Sixthly, the allocation of interest and bonuses, whether positive or negative, was recorded by UIT in the register as equating to a number of units. The number of units recorded appeared to relate to the prior month end unit value adopted by UIT. Finally, cash transactions with contributories in the form of deposits (cash in) and withdrawals (cash out) were also recorded by UIT in the register as equating to a number of units. The number of units recorded appeared to relate to the prior month end unit value adopted by UIT. The plaintiff said that he could not substantiate the month end value attributed by UIT to each cash transaction or the interest and bonuses.

23 I am satisfied that the requirements of the Corporations Act and the Corporations Regulations have been met. I am satisfied that there is a surplus of $150,000.

24 As to the proposed adjustment of the rights of the contributories among themselves, in Birch v Cropper (1889) 14 App Cas 525 the House of Lords, in the case of a voluntary winding up, said that in the absence of provision to the contrary surplus assets are to be distributed rateably, that is to say, in proportion to the nominal amounts of the shares held by members at the commencement of winding up (see McPherson, The Law of Company Liquidation 4th Edition, Andrew Keay, LBC Information Services 1999 at 611 et seq).

25 In Re Sullivans Cove IXL Nominees Pty Ltd (ACN 104 321 682) (in liq); Crawford and Another v de Kantzow and Others (2011) 82 ACSR 224 Crawford CJ considered the adjustment of the rights of contributories amongst themselves in the context of a compulsory winding up. His Honour said at 231, paragraphs [48] and [49]:

[48] The general principle is that a surplus upon winding up belongs to the members according to their proportionate interests in the share capital, measured according to the nominal amount — subject, however, to recognition of any preferred or superior claims created by the company’s constitution: Birch v Cropper (1889) 14 App Cas 525 at 543; Re Driffield Gas Light Company [1898] 1 Ch 451 at 455. That general principle applies equally to the holders of all classes of shares, although its application is subject to the provisions of the company’s constitution and the terms on which the respective shares have been issued by the company. The right of a member in accordance with the principle is a legal right that attaches to the shareholding itself: Archibald Howie Pty Ltd v Commissioner of Stamp Duties (NSW) (1948) 77 CLR 143 at 153 ; [1948] 2 ALR 489 at 491; Re BM2008 Pty Ltd (in liq) [2010] VSC 337 at [11]. Since the abolition of the concept of par value and nominal amount of shares by the Company Law Review Act 1998 (Cth), the reference to nominal amount in the general principle is now taken to mean the sum of all amounts paid to the company at any time for the share, not including any premium: Re Yanollee Pty Ltd (in liq) (2006) 24 ACLC 1087 ; [2006] NSWSC 705 at [13].

[49] The application of the general principle to this case, absent the shareholder agreement, would mean that the respective entitlements of the company’s shareholders to the surplus is in proportion to the number of shares held, regardless of the class of share.

26 In Re D S Millard & Son Pty Ltd [1997] NSWSC 201 Young J referred to the requirement of “special leave” in s 488(2). His Honour considered that the words merely meant that “a special application must be made to the court rather than the matter being dealt with as part and parcel of some administrative procedure”.

27 In Lombe as liquidator of Ulicorp Pty Ltd [2009] NSWSC 536 Barrett J considered the distribution of a surplus in the case of the compulsory winding up of a company. His Honour referred to s 485(2) and the decision in Re Yanollee Pty Ltd (in liq) [2006] NSWSC 705; (2006) 24 ACLC 1087. His Honour said that the relevant entitlements to the surplus within subsection 485(2) were to be fixed by the number of shares held, subject to any contrary or adjusting provision of the constitution.

28 In this case, I am satisfied that the adjustment of the rights of contributories proposed by the plaintiff should be approved. I am satisfied that the plaintiff has adopted a methodology which is, in the circumstances, the only reasonably reliable way of determining the respective entitlements of contributories (Maertin v Klaus Maertin Pty Ltd (2009) 232 FLR 239 at 247 [38] per Austin J; FAI General Insurance Co Ltd v FAI Car Owners Mutual Insurance Co Pty Ltd (2009) 262 ALR 552 at 557 – 558 [15] – [23] per Barrett J).

29 In the circumstances, I will make the orders sought by the plaintiff.

I certify that the preceding twenty-nine (29) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Besanko. |

Associate: