FEDERAL COURT OF AUSTRALIA

Bowcher (Liquidator); In the Matter of Meares Nominees Pty Ltd (In Liq) [2013] FCA 631

IN THE FEDERAL COURT OF AUSTRALIA | |

IN THE MATTER OF MEARES NOMINEES PTY LTD (IN LIQUIDATION) (ACN 005 573 035)

ANDREW JOHN BOWCHER AND TIMOTHY ROBERT GUMBLETON (AS LIQUIDATORS OF MEARES NOMINEES PTY LTD (IN LIQUIDATION) (ACN 005 573 035)) Plaintiffs |

DATE OF ORDER: | |

WHERE MADE: | SYDNEY (via video link to MELBOURNE AND TELEPHONE LINK TO BOWRAL) |

THE COURT ORDERS THAT:

1. Pursuant to s 588FF(3)(b) of the Corporations Act 2001 (Cth) (the Corporations Act), the period during which the plaintiffs may make any application which they are minded to make against any person or entity pursuant to s 588FE and s 588FF(1) of the Corporations Act in relation to Meares Nominees Pty Ltd (ACN 005 573 035) (the company) be extended up to and including 31 March 2014.

2. The plaintiffs’ costs of and incidental to their Originating Process be costs in the winding up of the company.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

AUSTRALIAN CAPITAL TERRITORY DISTRICT REGISTRY | |

GENERAL DIVISION | ACD 3 of 2013 |

IN THE MATTER OF MEARES NOMINEES PTY LTD (IN LIQUIDATION) (ACN 005 573 035)

BETWEEN: | ANDREW JOHN BOWCHER AND TIMOTHY ROBERT GUMBLETON (AS LIQUIDATORS OF MEARES NOMINEES PTY LTD (IN LIQUIDATION) (ACN 005 573 035)) Plaintiffs

|

JUDGE: | FOSTER J |

DATE: | 25 JUNE 2013 |

PLACE: | SYDNEY (VIA VIDEO LINK TO MELBOURNE and telephone link to bowral) (HEARD IN CANBERRA) |

REASONS FOR JUDGMENT

1 The plaintiffs are the joint Official Liquidators of Meares Nominees Pty Ltd (ACN 005 573 035) (In Liquidation) (the company), having been appointed as such when the company was wound up in insolvency by the Supreme Court of the Australian Capital Territory on 22 March 2010 (the liquidation date).

2 The application to wind up the company was filed on 3 February 2010 by Manion Home Loans–Wagga Pty Ltd (Manion Home Loans), a creditor of the company. That date is, therefore, the relation-back day in respect of the company’s liquidation (as to which see subpar (a) of the definition of relation-back day in s 9 of the Corporations Act 2001 (Cth) (the Corporations Act) and see also s 513A(e) of that Act).

3 By Originating Process filed on 1 February 2013, the plaintiffs sought relief pursuant to s 588FF(3)(b) of the Corporations Act. By Amended Originating Process filed on 8 March 2013, the plaintiffs now seek the following relief:

1. An order that the period during which the plaintiffs may make any application pursuant to section 588FF(1) of the Act in relation to Meares Nominees Pty Limited (ACN 005 573 035) (“the Company”) against any party be extended until such time as the Court directs.

2. In the alternative, an order that the period during which the plaintiffs may make any application pursuant to s588FF(1) of the Act in relation to the Company against those individuals and entities listed at Annexure “A” be extended until such time as the Court directs.

3. An order that the costs of and incidental to this originating process be costs in the winding up.

4. Such further or other orders as the Court considers appropriate.

4 Annexure “A” to the Amended Originating Process is in the following terms:

“Annexure A”

1. Robarch Pty Ltd ACN 102 768 043

2. Robert Archer Meares

3. Robert Chancellor Meares

4. Murray Irrigation Limited ACN 067 197 933

5. Sheila Mary Meares

6. Slater & Gordon Ltd ACN 097 927 400

7. Robert Strang

5 At the hearing before me, Counsel for the liquidators abandoned any ongoing interest in Murray Irrigation Limited and Robert Strang as potential defendants to any s 588FF claims which the liquidators might bring in the future in the event that they obtain the extension of time which they seek. The liquidators continued to contend that they should be given more time to investigate potential claims against the remaining three individuals and two corporations. They seek an extension of six to eight months.

6 There are no defendants in the proceedings although the liquidators’ claims for relief are opposed by the sole director of the company and by several other interested persons. All of the persons and entities listed in Annexure “A” to the Amended Originating Process were served with that process and with the affidavits relied upon in support of the relief claimed in that process. With the exception of Mr Strang and Murray Irrigation Limited, all of those persons and entities were represented at the hearing before me. Mr Strang swore an affidavit on 13 May 2013. That affidavit was not read at the hearing before me although it was tendered in evidence by Counsel for the liquidators (without objection).

7 These Reasons for Judgment determine the liquidators’ application.

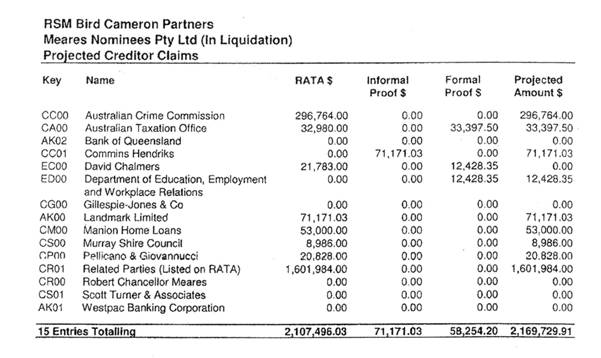

The Potential Claims

8 The liquidators have identified six claims the possibility of bringing which they contend ought to be preserved by the Court by making the orders sought in the present application. Those claims are:

(a) A claim for the recovery of certain plant and equipment (or the value thereof) apparently sold to Robarch Pty Limited (ACN 102 768 043) (Robarch) by the company on 28 October 2008 for the total purchase price of $132,000 or a claim in debt for the same amount of money (Claim 1).

(b) A claim for the recovery of certain motor vehicles and a tractor (or the value thereof) apparently sold to Robarch by the company on 11 December 2008 for the total purchase price of $38,000 or a claim in debt for the same amount of money (Claim 2).

(c) A claim for the recovery of a 2003 Jeep Wrangler (SFQ 810) (or the value thereof) apparently sold to Anna Kate Pizzini (née Meares) on 30 June 2009 for $11,371.80 or a claim in debt for the same amount of money (Claim 3).

(d) A claim for the repayment of $110,111.04 paid to Slater & Gordon Ltd (S & G) on 19 August 2009 (Claim 4).

(e) A claim for the repayment of two amounts (viz $244,339.88 and $241,865.12) paid to Sheila Mary Meares (Sheila Meares) on 25 August 2009 (Claims 5 and 6).

9 I shall refer to the transactions the subject of Claims 1 to 6 as “the impugned transactions”.

10 As to the transactions the subject of Claims 1, 2 and 3, the liquidators contend that each of those transactions is a voidable transaction within the meaning of s 588FE of the Corporations Act in that each of them is an insolvent transaction within the meaning of s 588FC of the Corporations Act being in each case an uncommercial transaction within the meaning of s 588FB or an unreasonable director-related transaction within the meaning of s 588FDA.

11 As to the payment which is sought to be attacked by Claim 4, the liquidators contend that it is a voidable transaction in that it is a preference or an uncommercial transaction which is an insolvent transaction.

12 As to the payments which are the subject of Claims 5 and 6, the liquidators contend that those payments are voidable transactions because they are unfair preferences or uncommercial transactions which are insolvent transactions or unreasonable director-related transactions.

13 The liquidators seek an extension of time so that:

(a) They can conduct public examinations of various members of the Meares family and the company’s accountants;

(b) They can investigate the potential claims outlined above and obtain information and documentation in relation to them; and

(c) They can seek advice and ultimately determine whether to institute proceedings against one or more of the persons and entities of interest.

The Relevant Legislative Provisions

14 Part 5.7B of the Corporations Act deals with voidable transactions which may be attacked by the liquidator of an insolvent company for the benefit of its creditors.

15 Part 5.7B, Div 1 (ss 588C to 588F) contains definitions of certain terms and expressions used in Pt 5.7B and also specifies certain presumptions which are to be operative for the purposes of that Part. Part 5.7B, Div 2 (ss 588FA to 588FDA) contains provisions which specify the elements of certain concepts which underpin liquidators’ actions for recovery of monies in respect of voidable transactions—unfair preferences (s 588FA), uncommercial transactions (s 588FB), insolvent transactions (s 588FC), unfair loans to a company (s 588FD) and unreasonable director-related transactions (s 588FDA). Section 588FG sets out the elements of certain statutory grounds for refusing relief under s 588FF. None of the parties to the impugned transactions relied upon s 588FG.

16 Subsections (1), (2), (3), (4), (5), (6) and (6A) of s 588FE provide:

588FE Voidable transactions

(1) If a company is being wound up:

(a) a transaction of the company may be voidable because of any one or more of subsections (2) to (6) if the transaction was entered into on or after 23 June 1993; and

(b) a transaction of the company may be voidable because of subsection (6A) if the transaction was entered into on or after the commencement of the Corporations Amendment (Repayment of Directors’ Bonuses) Act 2003.

(2) The transaction is voidable if:

(a) it is an insolvent transaction of the company; and

(b) it was entered into, or an act was done for the purpose of giving effect to it:

(i) during the 6 months ending on the relation-back day; or

(ii) after that day but on or before the day when the winding up began.

…

(3) The transaction is voidable if:

(a) it is an insolvent transaction, and also an uncommercial transaction, of the company; and

(b) it was entered into, or an act was done for the purpose of giving effect to it, during the 2 years ending on the relation-back day.

(4) The transaction is voidable if:

(a) it is an insolvent transaction of the company; and

(b) a related entity of the company is a party to it; and

(c) it was entered into, or an act was done for the purpose of giving effect to it, during the 4 years ending on the relation-back day.

(5) The transaction is voidable if:

(a) it is an insolvent transaction of the company; and

(b) the company became a party to the transaction for the purpose, or for purposes including the purpose, of defeating, delaying, or interfering with, the rights of any or all of its creditors on a winding up of the company; and

(c) the transaction was entered into, or an act done was for the purpose of giving effect to the transaction, during the 10 years ending on the relation-back day.

(6) The transaction is voidable if it is an unfair loan to the company made at any time on or before the day when the winding up began.

(6A) The transaction is voidable if:

(a) it is an unreasonable director-related transaction of the company; and

(b) it was entered into, or an act was done for the purposes of giving effect to it:

(i) during the 4 years ending on the relation-back day; or

(ii) after that day but on or before the day when the winding up began.

17 Section 588FF is in the following terms:

588FF Courts may make orders about voidable transactions

(1) Where, on the application of a company’s liquidator, a court is satisfied that a transaction of the company is voidable because of section 588FE, the court may make one or more of the following orders:

(a) an order directing a person to pay to the company an amount equal to some or all of the money that the company has paid under the transaction;

(b) an order directing a person to transfer to the company property that the company has transferred under the transaction;

(c) an order requiring a person to pay to the company an amount that, in the court’s opinion, fairly represents some or all of the benefits that the person has received because of the transaction;

(d) an order requiring a person to transfer to the company property that, in the court’s opinion, fairly represents the application of either or both of the following:

(i) money that the company has paid under the transaction;

(ii) proceeds of property that the company has transferred under the transaction;

(e) an order releasing or discharging, wholly or partly, a debt incurred, or a security or guarantee given, by the company under or in connection with the transaction;

(f) if the transaction is an unfair loan and such a debt, security or guarantee has been assigned—an order directing a person to indemnify the company in respect of some or all of its liability to the assignee;

(g) an order providing for the extent to which, and the terms on which, a debt that arose under, or was released or discharged to any extent by or under, the transaction may be proved in a winding up of the company;

(h) an order declaring an agreement constituting, forming part of, or relating to, the transaction, or specified provisions of such an agreement, to have been void at and after the time when the agreement was made, or at and after a specified later time;

(i) an order varying such an agreement as specified in the order and, if the Court thinks fit, declaring the agreement to have had effect, as so varied, at and after the time when the agreement was made, or at and after a specified later time;

(j) an order declaring such an agreement, or specified provisions of such an agreement, to be unenforceable.

(2) Nothing in subsection (1) limits the generality of anything else in it.

(3) An application under subsection (1) may only be made:

(a) during the period beginning on the relation-back day and ending:

(i) 3 years after the relation-back day; or

(ii) 12 months after the first appointment of a liquidator in relation to the winding up of the company;

whichever is the later; or

(b) within such longer period as the Court orders on an application under this paragraph made by the liquidator during the paragraph (a) period.

(4) If the transaction is a voidable transaction solely because it is an unreasonable director-related transaction, the court may make orders under subsection (1) only for the purpose of recovering for the benefit of the creditors of the company the difference between:

(a) the total value of the benefits provided by the company under the transaction; and

(b) the value (if any) that it may be expected that a reasonable person in the company’s circumstances would have provided having regard to the matters referred to in paragraph 588FDA(1)(c).

18 In the present case, the liquidators were required to bring their claims under s 588FE by 3 February 2013 unless they obtained an extension of the period within which they were required to bring those claims pursuant to s 588F(3)(b).

Some Uncontentious Relevant Facts

19 The company was incorporated in Victoria on 6 July 1979. At all relevant times after its incorporation, the company was the trustee of the Meares Family Trust (MFT). In its capacity as trustee of the MFT, the company conducted a farming business on a property known as “Bultarra” located at 423 Yarraman Lane, Womboota, NSW. Bultarra was and is a rural property of approximately 6,500 acres in area. Womboota is a locality in the central part of the southern Riverina district. It is situated north of the Murray River. The MFT’s farming business comprised the raising of sheep and the growing of crops.

20 Although it is not entirely clear, between 1979 and the liquidation date, the company’s sole activity appears to have been to act as the trustee of the MFT. All of the transactions which it undertook from time to time in that period were most likely effected by it in that capacity. The company ceased to trade some time before 1 July 2009, probably in January 2009.

21 Robert Chancellor Meares (RC Meares) was a director of the company throughout the period from 21 July 1979 to 24 February 1998 and the sole director of the company from 21 August 2006 to the liquidation date. Sheila Meares was a director of the company in the period from 24 February 1998 to 2 April 2002. Robyn Catherine Meares (Robyn Meares), the former wife of RC Meares, was a director of the company in the period from 21 July 1979 to 21 August 2006. Robyn Meares died in 2006. RC Meares was the secretary of the company throughout the period from 21 August 2006 to the liquidation date. Robyn Meares was the secretary before RC Meares.

22 As at the liquidation date, Mellisa Luella Swindley (a daughter of RC Meares and Robyn Meares) owned one ordinary share in the company. The other issued share was jointly owned as at that date by Robert Archer Meares (RA Meares), Anna Kate Meares and Mellisa Swindley. RA Meares is the son of RC Meares and Robyn Meares. RC Meares is the son of Sheila Meares.

23 RA Meares is the sole director and secretary of Robarch which was incorporated on 8 November 2002. He is married to Michelle Dawn Meares (née Herrick) (MD Meares).

24 From 1998 to early 2007, Pellicano & Giovannucci acted as the accountants of the company. Thereafter, until the liquidation date, Scott Turner & Associates were the company’s accountants.

25 All of the company’s MYOB files were forwarded to the liquidators by Scott Turner by email sent on 14 April 2010. Prior to 14 April 2010, those files were brought up-to-date by MD Meares and sent to Scott Turner on 24 March 2010 under cover of an email sent on that day.

26 The company’s records were transferred to the MYOB system in early 2009. The starting point for that transfer was the company’s hard copy records (including its Financial Statements) as at 30 June 2008.

27 According to its Balance Sheet as at 30 June 2008, the company had funds totalling $650,638 in its bank accounts as at that date. Most of those funds were paid out to S & G in the eleven days following balance date.

28 The liquidators and their staff have had infrequent and spasmodic contact with some members of the Meares family and with Scott Turner since the liquidation date. I shall discuss that contact in more detail below.

Other Evidence

The Liquidators’ Evidence

29 On 9 April 2010, RC Meares signed a Report as to Affairs in respect of the company. The following matters are specified in that Report:

(a) As at the liquidation date, the value of the company’s assets was $4,318, comprising shares in AWB Limited (valued at $4,245) and cash at bank ($73).

(b) As at the liquidation date, the company owed $21,783 to its only employee. As at the same date, there was a disputed debt to Landmark of $6,200,000 and a debt owed to the National Crime Commission (NCC) of $296,764. The total amount due to unsecured creditors was said to be $1,717,778 comprising:

(i) $15,412 due to the ATO for unremitted GST and $17,568 due to the ATO for unremitted PAYG tax instalments.

(ii) $20,828 due to Pellicano & Giovannucci.

(iii) $8,986 due to the Council of the Shire of Murray.

(iv) $53,000 due to Manion Home Loans.

(v) $1,601,984 owed to “related parties”. No further details of these debts were provided.

30 On the same day, RC Meares completed and signed a 58-question questionnaire required by the liquidators. That questionnaire contained the following information:

(a) RC Meares was responsible for the day-to-day management of the company.

(b) The company, in its capacity as trustee of the MFT, commenced a farming business on 6 July 1979. Thereafter, it traded under the name “Meares Nominees”.

(c) It had ceased to trade by 22 March 2010.

(d) RC Meares was also an officer of ICW Pty Ltd (ICW). ICW owned property that was rented to the company. No details of this lease arrangement were provided.

(e) The company maintained its accounting records in an MYOB system. RC Meares had some books and records of the company in his possession as at 9 April 2010. Those records related to the Landmark mortgage and the dispute with Landmark. Some books and records had been destroyed by 9 April 2010.

(f) Balance Sheets and Profit and Loss Statements were prepared by the company’s accountants and reviewed by RC Meares. RC Meares carried out monthly stocktakes and performed regular bank reconciliations.

(g) RC Meares and his late wife, Robyn, were the signatories on the company’s bank accounts. These accounts were held at the Deniliquin branch of Westpac Banking Corporation (Westpac).

(h) Landmark took possession of the company’s farming property in January 2009 and sold that property in March 2010.

(i) RC Meares leased property to the company at a monthly rent of $5,000. That property was located at Bultarra, Womboota, NSW.

(j) With the exception of the unpaid GST and PAYG amounts disclosed in the Report as to Affairs, the company regularly complied with its taxation obligations.

(k) RC Meares first realised that the company might have to go into external administration in February 2010 when, as a result of Manion Home Loans obtaining a “court order”, he spoke to a liquidator in order to assess options.

(l) Creditors had begun pressing the company for payment of their debts in mid-2008.

(m) The company had unsuccessfully tried to compromise and resolve Landmark’s claims.

(n) Landmark and Manion Home Loans had both taken action against the company to recover their debts. Manion Home Loans was the plaintiff in the proceedings in which the order winding up the company was made.

31 Question 51 was in the following terms:

Are you aware of any payment, transfer of assets, conveyance or the granting of a charge or incurring of an obligation in favour of a creditor, not detailed in the previous questions, which may have had the effect of giving a creditor a preference, priority or advantage over other creditors? If so, please provide the details as outlined above.

32 RC Meares answered question 51: “No”.

33 In answer to question 58 in the questionnaire, RC Meares said that the causes of the failure of the company were:

Drought and no irrigation water over extended period.

34 For the Financial Year ended 30 June 2007, the MFT made a primary production loss of $1,428,168 following on from a loss in the previous year of $145,379. It had a deficiency in its Balance Sheet as at 30 June 2007 of $1,939,289 (up from $511,121 as at 30 June 2006). Included as an asset in the company’s Balance Sheet for both the 2006 and 2007 Financial Years was an item:

Intangible – NCC | $547,111 |

Also included as non-current assets were:

Loan – ICW Pty Ltd (Wesfarmers) | $600,000 |

Land – Bultarra Womboota | $1,480,457 |

Plant & Equip. – At W.D.V. | $757,357 |

35 The company’s accountants, Scott Turner & Associates, prepared Financial Statements for the Year ended 30 June 2010. Those Financial Statements showed the position of the company as at 22 March 2010—the date when it was put into liquidation. The Trading, Profit and Loss Statements included within the 2010 Financial Statements showed a trading loss of $989,913 for the year ended 30 June 2009 and $615,427 for the year ended 30 June 2010.

36 The Balance Sheets included within those Financial Statements recorded the following matters:

(a) As assets as at both 30 June 2009 and 30 June 2010:

A loan to ICW | $84,346 |

Intangibles – legal | $116,352 |

Intangibles – NCC | $547,111 |

(b) As liabilities as at both 30 June 2009 and 30 June 2010:

Loan from ICW | $276,776 |

Loan from JB and S Meares | $826,305 |

Loan from Lochshiel Pty Limited | $107,716 |

Liability to the NCC | $296,764 |

(c) The reduction to zero by 30 June 2010 of cash held in the trust account of S & G on behalf of the company. The amount of cash held by S & G as at 30 June 2009 was shown as $547,000.

(d) A reduction in the loan from Robarch from $538,564 as at 30 June 2009 to $28,788 as at 30 June 2010 suggesting a repayment by the company to Robarch of $509,776 in the period between 1 July 2009 and 30 June 2010.

(e) A minor change in the quantum of the debt due from the company to Sheila Meares from $319,363 as at 30 June 2009 to $322,210 as at 30 June 2010.

37 I pause to observe that the Balance Sheet included within the Financial Statements of the MFT for the year ended 30 June 2009 forwarded by Mr JK Guy of Boulton Cleary and Kern, the lawyers representing Robarch and RA Meares, to the liquidators under cover of his letter dated 7 February 2013, which were also prepared by Scott Turner & Associates, showed the following:

(a) The amount of $857,927 as a current liability of the company to Robarch. This amount differs from the amount recorded in the 30 June 2010 Balance Sheet in respect of that liability as at 30 June 2009 (viz $538,564).

(b) Apart from the company’s liability to JB and S Meares, there was no liability item in respect of Sheila Meares on her own account for the year ended 30 June 2009. In the 30 June 2010 Balance Sheet, an amount of $319,363 is shown as a liability to Sheila Meares as at 30 June 2009.

38 These discrepancies between the two versions of the 2009 Balance Sheet tendered in evidence before me were not explained.

39 The liquidators prepared a schedule containing their projection of claims against the company. That schedule is in the following terms:

40 In the period from 22 March 2010 to 29 January 2013, the liquidators received various amounts which totalled $25,112.15. In the same period, they paid out a total of $17,897.77. Of the surplus ($7,214.38), $5,822.18 is held in trust for Robarch being half the proceeds of the sale of certain plant and equipment (an air seeder). Therefore, the liquidators currently hold $1,392.20 as funds of the company. As to this, one of the liquidators, Mr Gumbleton said:

… I hold funds totalling $1,392.20 in the winding up of the Company. I am therefore without sufficient funds, and have always been without sufficient funds during the winding up, to carry out a comprehensive investigation into the Company’s affairs and transactions, as well as to retain solicitors to advise me on the potential claims I identify below as well as to conduct a public examination of the various parties that I propose to examine, as discussed further below.

41 On 24 January 2013, Mr Gumbleton met with a representative of a litigation funder (Pretium Litigation Funding Pty Ltd) (Pretium). At pars 34 to 38 of his affidavit sworn on 31 January 2013, Mr Gumbleton said:

34. On 24 January 2013 I met with Mr Kovi Paneth of Pretium Litigation Funding Pty Ltd. Also present at the meeting was my solicitor Mr Clayton Davis of Herman Davis Lawyers. The purpose of this meeting was to discuss an unrelated matter in respect of which I was seeking litigation funding. During the course of our discussions I mentioned the winding up of the Company, and noted that there were only a few days left in which to bring any proceedings covered by section 588FF(I) of the Act.

35. Mr Paneth indicated that subject to being satisfied that there was merit in pursuing such proceedings he would be prepared to fund an application under section 588FF(3)(b) of the Act.

36. That being the case my solicitor undertook an urgent review of the books and records presently in my possession, and I was advised by him that there were a considerable number of potential claims, but that on the basis of the existing available material such claims may be speculative and hopeful rather than based on sound foundation.

37. During further discussions involving both my solicitor and Mr Paneth a view was formed that the appropriate way forward would be to conduct public examinations pursuant to sections 596A and 596B of the Act. Once these examinations were completed a decision could then be made as to which claims should be pursued by way of litigation (in the absence of any negotiated settlements).

38. Now produced and shown to me and marked “TRG-17” is a copy of a letter from Mr Paneth in which he confirms that subject to compliance with section 477(2B) of the Act and a successful application pursuant to section 588FF(3)(b) of the Act, he would provide litigation funding to cover the cost of the proposed public examinations and any legal proceedings found to have merit as a result.

42 Mr Gumbleton did not suggest that he had had any earlier contact with any litigation funder in respect of claims which might be brought by the liquidators under s 588FE and s 588FF of the Corporations Act or by the company in connection with its demise nor did he provide any evidence of attempts by him to obtain funding for such claims from other sources. In light of the absence of such evidence, I conclude that the liquidators took no steps whatsoever prior to late January 2013 to procure funding for claims which they or the company might bring as a result of the liquidation of the company.

43 In his first affidavit (the affidavit sworn on 31 January 2013), Mr Gumbleton identified the following potential claims, namely, claims against Robarch and others totalling $170,000 in respect of the apparent sale to Robarch by the company of the following plant, equipment and motor vehicles:

(a) On 28 October 2008, the sale of:

1 x John Deer tractor | $33,636.36 | |

1 x Sheep crutching machine EL6-10 | $18,181.82 | |

1 x John Deer front end loader | $22,727.27 | |

Plus GST | $7,454.55 | |

TOTAL | $82,000.00 |

(See Tax Invoice dated 28 October 2008).

(b) On 28 October 2008, the sale of:

1 x Irrigator and spans | $45,454.55 | |

Plus GST | 4,545.45 | |

TOTAL | $50,000.00 |

(See Tax Invoice dated 28 October 2008).

(c) On 11 December 2008, the sale of:

1 x Nissan Patrol (XUJ 508) | $7,272.72 | |

1 x Nissan Patrol (AA 48 NX) | $25,454.55 | |

1 x Tractor (1980 John Deer) | $1,818.18 | |

Plus GST | $3,454.55 | |

TOTAL | $38,000.00 |

(See Tax Invoice dated 11 December 2008).

44 In the same affidavit, Mr Gumbleton described the potential claims described at [43] above as follows:

27. I consider that each of the transactions identified in paragraphs 23 to 26 give rise to potential claims, that vest in either me as liquidator and/or the Company, as follows:

(a) a claim against Robarch for a voidable transaction under Part 5.7B of the Act on the basis that it is an unreasonable director-related transaction and/or an unfair preference and/or an uncommercial transaction;

(b) a claim against Robert Chancellor Meares for breach of his fiduciary and director’s duties to the Company under the Act; and

(c) a claim against Robert Archer Meares for being knowingly involved in Robert Chancellor-Meares’ breach of his duties under the Act.

45 On 16 January 2013, the liquidators sent letters of demand dated that day to each of Robarch, RC Meares and RA Meares seeking to recover the total of the amounts invoiced to Robarch by the company in respect of the sale of the plant, equipment and motor vehicles, details of which are set out at [43] above. As against Robarch, the liquidators relied upon s 588FE of the Corporations Act and, in the alternative, claimed the total of the invoiced amounts as a debt due to the company upon the basis that those amounts had never been paid to the company. In their letter of demand sent to RC Meares, they claimed an additional amount of $11,371.80 in respect of the sale to Anna Kate Pizzini (née Meares) of a 2003 Jeep Wrangler Sport 2D soft top (SFQ 810) on 30 June 2009. As against RC Meares and RA Meares, the liquidators relied upon s 588FE and breach of the duties owed by them to the company (both statutory and fiduciary). In their letter of demand to RC Meares, the liquidators also suggested that other plant and equipment belonging to the company had been sold without the company receiving value for those items. That additional claim was not explained further in the letter or anywhere else.

46 In addition, in his first affidavit, Mr Gumbleton identified several cheques and two payments which he considered are unexplained. At the hearing before me, Counsel for the liquidators abandoned any claims against Murray Irrigation Limited, the payee of those cheques. The liquidators maintained interest in a payment of $110,111.04 made on 19 August 2009 to S & G and a payment of $244,339.88 to Sheila Meares on 25 August 2009. The liquidators also claimed some interest in the unsecured debt of $296,764 said to be due to the NCC according to the Balance Sheet of the company as at 30 June 2007, 2008, 2009 and 2010. Finally, in submissions, Counsel for the liquidators also suggested that another payment made by the company on 25 August 2009 (viz the cheque drawn in favour of Leveraged Equities in the amount of $241,865.12) was also suspicious and should be investigated.

47 Mr Gumbleton gave no evidence of any attempts by the liquidators to investigate the payments and debt described at [46] above. He merely identified them as matters requiring further investigation.

48 The MYOB entries in respect of the payment to S & G showed a payment to that corporation of $110,111.04 on 19 August 2009. That amount was the total of the amounts rendered in five separate invoices dated in the period between 1 July 2009 and 5 August 2009. Those invoices related to purchase orders numbered 379 to 383.

49 The MYOB entries in respect of Sheila Meares showed a payment by cheque no 165 of $244,339.88 on 25 August 2009 to Sheila Meares. The record describes the payment as:

2-1059 | Leveraged Equit-Loan S Meares | $244,339.88 |

50 The MYOB records also referred to a payment of $241,865.12 to Leveraged Equities by cheque no 164.

51 There was no evidence before me as to the circumstances in which either of the payments made to Sheila Meares had been made. There was no evidence as to the involvement of Leveraged Equities with the company, the MFT, RC Meares or Sheila Meares.

52 At the hearing before me, Counsel for the liquidators abandoned the potential claims against Mr Strang which they had earlier identified.

53 Mr Gumbleton filed two further affidavits sworn on 9 April 2013 and 29 May 2013 respectively. In the first of these additional affidavits, Mr Gumbleton commented upon the contents of a letter dated 7 February 2013 from Mr Guy in which Mr Guy proffered on behalf of his clients explanations of the transactions the subject of the letters of demand sent to those clients on 16 January 2013. I will deal with Mr Gumbleton’s observations when addressing the explanations proffered by Mr Guy on behalf of Robarch and RA Meares. In addition, Mr Gumbleton gave evidence of a teleconference which took place on 1 July 2011. The substance of the discussion which took place during that teleconference is recorded in a file note prepared by Mr Thorsness, an employee of the liquidators. That file note is in the following terms:

Meares Nominees Pty Ltd (In Liquidation)

File Note: Conducting Investigation I1

Date: 1/7/2011

Time: 11.05am

Teleconference meeting held in office of Tim Gumbleton (TG), with John Thorsness (JT) attending, and on the phone the Mears’ family members, being Robert Mears (snr), Robert Mears (jnr), and Michelle Meares (nee Herrick).

Primary purpose of meeting: to confirm status of missing or sold assets, outstanding finance liability, and to confirm assets sold to related parties.

TG greeted other parties and introduced JT. All exchanged pleasantries and TG commenced meeting.

TG raised questions related to sale of Air Seeder (which was, supposedly, sold previously by Mears Nominees to Robarch for $110K), and the relevant amount owed on this piece of equipment. TG confirmed approximate payout figure is $54K. TG pointed out that technically there was no sale because, arguably, liability for Bank of QLD (BOQ) finance was not transferred to the purchaser, Robarch. Because liability was not transferred to Robarch, liability still sits with Meares Nominees. This particular technically needs to be addressed and resolved.

TG raised questions surrounding sale of plant & equipment. Some plant & equipment appears to be missing when comparing the list (from accounting records) as compared to those, supposedly, sold by Landmark. MH made point Landmark removed equipment from the property, when they took possession, without any reference to them.

TG read out (some of) the items listed on accounting report and MH claimed it is likely some of them had not existed (in a physical sense) for a long time, & certainly not at time of repossession. TG asked if any equipment not sold was left on the property and later removed by Landmark. MH seemed to think this was the case. TG asked if his equipment list can be reviewed by MH with a view to noting which items were sole by Landmark and which were not physically exist at time of vacating property. MH agreed to this suggestion and will be happy to review list once received.

TG asked if there was a possibility Landmark sold equipment of which they did not hold security against. MH seemed to think this was quite possible. Once the equipment list is reviewed by MH and returned to RSM, TG will raise any queries and questions with Landmark.

MH claimed their many attempts to make communicate with the Landmark legal team were met with difficulty. She reiterated their overall impression, of being ‘mistreated’ by the legal representatives of Landmark. MH questions the basis upon which interest was charged (on money owned to Landmark) after the sale of property by Landmark. MH claims they should not be penalized because of a delayed settlement arrangement, which was negotiated by Landmark.

TG raised query regarding the transfer of assets, and their value, to Robarch, in light of prima-facie impression approximately $121K of equipment is missing. He asked for clarity on this point by way of obtaining confirmation of the amount and value of any transfer (by way of purchase or otherwise) from the Meares Nominees accountant, Scott Turner. This confirmation should be supported by a statutory declaration. The purpose of the request is to establish whether or not any preference or uncommercial transactions have occurred. TG reiterated need to assure creditors that approximately $121K of assets has not been transferred to family members of Meares Nominees.

Conversation moved on to the presentation of balance sheet / P&L and the creditors list as per RATA. TG focused specifically on the Crime Commission liability. Rob (jnr) confirmed this relates to a personal case, with him, regarding possible proceeds from illegal activity. TG raised various questions regarding specific asset lines on the balance sheet, including loans ICW and Intangibles. MH & Rob (jrn) seemed to think Loans ICW did not operate any more and the value of Intangibles is a mystery. They referred these entries to their accountant, and suggestions there might be a need to refer back to their previous accountant.

Conversation moved on to possible value obtainable from the sale of the Air Seeder. TG said estimated value for this piece of equipment is approximately $70K, with a payout figure of approximately $54K. These amounts would leave a shortfall of only $16K. MH raised doubts of ability to sell this piece of specialized equipment, at this time.

MH asked about the status of superannuation owned to ex-employee, David Charmers. TG confirmed his status as a creditor, being listed after BOQ and RSM.

As meeting concluded, MH reiterated claim Landmark have not been transparent regarding interest charges (to them), deposits, etc. Rob (jnr) raised concerns about receipts and hinted Landmark have not been fair, having gained benefit from receipt of $1M which they should have not received. He conveyed a rough calculation of money paid and claims it does not add up. MH claimed Landmark is avoiding the issue. In light of these claims, TG asked to see all loan documents related to Landmark, in order to work thru the funds.

TG summarized immediate issues to be addressed as follows:

1. BOQ,

2. Review of depreciation schedule (ie equipment listing),

3. Scott Turner to confirm sale of equipment to related parties.

Meeting closed at 12noon.

54 The substance of the discussion held on 1 July 2011 was not really in dispute. MD Meares suggested that Mr Thorsness’ file note was not accurate in a couple of minor respects. RC Meares did not give evidence before me. RA Meares did not dispute the accuracy of the file note.

55 Mr Gumbleton testified that he did not subsequently receive any correspondence from Scott Turner concerning the impugned transactions.

56 On 5 July 2011, Mr Gumbleton sent an email to MD Meares with six or seven queries arising out of the teleconference held on 1 July 2011. MD Meares did not respond immediately to Mr Thorsness’ email. He followed up his requests on 26 August 2011. On 7 September 2011, MD Meares answered Mr Gumbleton’s queries as best as she could at that time. She said that she was unable to provide any real assistance in relation to some of them. In her response, she indicated that RC Meares was soon to visit her and RA Meares in Queensland and that she would discuss the impugned transactions with him then and “fax/scan back to” the liquidators her comments in respect of the depreciation schedule which had been forwarded to her on 5 July 2011. She also promised to send relevant bank statements.

57 The liquidators had no contact with any member of the Meares family in the period between 7 September 2011 and 14 November 2012.

58 On 14 November 2012, an employee of the liquidators telephoned MD Meares and requested her to provide the bank statements which she had promised in September 2011. Later that same day, MD Meares forwarded to the liquidators bank statements for an account held by RA Meares at Westpac for the period from September 2008 to July 2009. She highlighted on those statements the relevant MFT transactions. She also sent reconciliations for that bank account. She also returned the MFT depreciation schedule sent to her in July 2011 annotated with her comments. She emphasised that a lot of the items on the schedule “… did not exist any more”. She offered to provide Robarch’s bank account details for the air seeder payment.

59 The liquidators tendered evidence that, as at 28 May 2013, RA Meares and MD Meares owned real property in Queensland which they had purchased in September 2011 for $595,000. The property appears to be unencumbered and is their family home.

60 Exhibited to the third affidavit of Mr Gumbleton was a bundle of documents relating to the impugned transactions. Those documents proved the following relevant matters:

(a) The company in its capacity as trustee of the MFT retained S & G in May 2008 to represent them in respect of the claims for possession of Bultarra then being pressed by Landmark and a related corporation of Landmark.

(b) Pursuant to the MFT retainer of S & G, S & G rendered invoices to the company for fees and disbursements due to it. As at late August 2009, the MFT owed S & G $110,111.04. Almost all of that amount had been rendered in July and August 2009. On 19 August 2009, the company authorised S & G to transfer $110,111.04 from moneys held in its Trust Account to its general account in payment of the total amount of fees and disbursements then due to it.

(c) On 19 August 2009, S & G paid to the company the amount of $542,000. That sum may have been held by S & G in trust for RA Meares or for the company. On the same day, the company paid $40,000 to Robarch. As at 17 August 2009, S & G held $760,030 in trust for the company or for various members of the Meares family or for both. Five amounts totalling $755,030 had been received by S & G and deposited into its Trust Account on 8 July 2009. One of those five deposits was for an amount of $542,000. S &G recorded that the payer of that deposit was RA Meares. It also recorded that the repayment of $542,000 made by it on 19 August 2009 was a “return of trust monies to depositor (RA Meares)”. A separate MYOB record showed that the payer of the amount of $542,000 to S & G was the company and that the payment had been made on 22 June 2009.

Approximately one week earlier, the same record showed a deposit of $491,175 made by Sheila Meares with the company.

(d) On 25 August 2009, the company drew two cheques as follows:

Cheque no 164 for $241,865.12 in favour of Leveraged Equities.

Cheque no 165 for $244,339.88 in favour of Sheila Meares. This cheque is described in one MYOB record as “Sheila Meares loan”.

61 The liquidators did not attempt to analyse the records available to them in order to assess whether breaches of the Corporations Act had or might have occurred.

62 The liquidators rested with the following statements of position made by Mr Gumbleton:

… I was advised by [my solicitor] that there were a considerable number of potential claims, but that on the basis of the existing available material such claims may be speculative and hopeful rather than based on sound foundation.

…

For the reasons set out below [in paragraphs 6 to 32 of Mr Gumbleton’s second affidavit], I do not consider that the explanation of the Relevant Transactions provided by Mr Guy’s letter [referring to Mr Guy’s letter dated 7 February 2013] is sufficient or persuasive and I remain of the view that the Relevant Transactions require further investigation and are potentially void under Part 5.7B of the [Corporations Act].

63 The solicitor for the liquidators, who is experienced in conducting public examinations in this Court under s 596A and s 596B of the Corporations Act, estimated the time that would be required for the liquidators to organise and conduct examinations of all relevant persons in relation to the impugned transactions and to be in a position to decide whether to commence proceedings and, if so, against whom. He expressed the following opinion:

I therefore believe that if the Court is prepared to adjourn the present application for a period of six months, then the plaintiffs can reasonably expect to be in a position to provide the Court at the expiration of that period with sufficient evidence, if any exists, to enable the Court to determine the application.

64 Obviously the solicitor’s opinion which I have extracted at [63] above is directed to the question of whether the present application should be adjourned in order to enable public examinations to take place so that the present application can be determined in light of the outcome of those examinations. This was the approach taken by Emmett J in Kugel, In the Matter of Charben Haulage Pty Ltd (in Liquidation) [2009] FCA 1039. Nonetheless, the evidence of the liquidators’ solicitor is of assistance to the Court in determining the application which is presently before the Court.

The Evidence Tendered on Behalf of the Opponents

65 RC Meares did not give evidence before me.

66 Sheila Meares swore an affidavit on 13 May 2013 which was read at the hearing before me. She was not cross-examined.

67 She said that:

(a) She is now 94 years of age.

(b) She lives in Melbourne and her health is failing. She has recently had knee surgery.

(c) She has never been contacted by the liquidators or anyone on their behalf in relation to the affairs of the company or the alleged payment of $244,339.88 made to her on 25 August 2009. She has no recollection of such a payment nor does she know why it was made.

(d) She had never had any involvement in the day-to-day running of the company.

(e) She claimed that she would suffer prejudice if the liquidators were to obtain the extension of time which they seek. That prejudice rises no higher than the obvious prejudice of being sued. There was nothing to suggest that, in reality, Sheila Meares’ forensic situation had been altered to her prejudice by the liquidators’ delay.

68 Mr Guy swore an affidavit on 30 May 2013. He annexed to his affidavit copies of various documents lodged by the liquidators with ASIC from time to time in respect of the company. These were Presentation of Accounts and Statement documents. Those documents showed:

(a) As at 19 April 2011, Mr Gumbleton claimed that he was pursuing alleged voidable transactions and finalising the liquidation.

(b) As at 4 October 2011, Mr Gumbleton claimed that he was pursuing alleged voidable transactions, finalising investigations and realising discovered assets. He said that he expected to complete the liquidation by December 2011.

(c) As at 10 April 2012, Mr Gumbleton claimed that he was pursuing alleged voidable transactions and finalising investigations. He said that he expected to complete the liquidation by December 2012.

(d) As at 17 October 2012, Mr Gumbleton made the same claims that he had made on 10 April 2012. He revised his estimate of the end date of the liquidation to June 2013.

(e) As at 17 April 2013, Mr Gumbleton made the same claims that he had made on 10 April 2012. He again revised his estimate for the completion of the liquidation—this time to March 2014.

69 Mr Guy swore a second affidavit on 5 June 2013. I do not need to refer to the contents of that affidavit for present purposes.

70 RA Meares sworn an affidavit on 13 May 2013. He was cross-examined by Counsel for the liquidators.

71 In his evidence-in-chief, Mr Meares said:

(a) In about May 2003, Robarch acquired a rural property known as Yarraman which was located next to Bultarra. Yarraman comprised approximately 1,005 acres. Yarraman was sold in November 2011.

(b) In the period from 2003 to about 2008, the company leased Yarraman from Robarch and conducted farming and grazing operations on Yarraman. This arrangement ceased in early 2008. Thereafter, Robarch conducted its own farming and grazing operations on Yarraman.

(c) Prior to sending their letters of demand in mid-January 2013, the liquidators never asked him for information about the payment of $100,030 made by him to Mr Strang on 28 October 2008.

(d) The liquidators have never asked him for information in respect of an alleged transaction between the company, Robarch and Westpac whereby Robarch acquired from the company an irrigator and spans for $50,000, $43,672.96 of which was “paid” by Robarch assuming responsibility in lieu of the company vis-à-vis Westpac and the balance of which ($6,327.04) was paid or to be paid to the company by Robarch in cash. A similar position obtained in respect of a payment of $200,000 allegedly made by Robarch to Landmark on 3 April 2009 and the alleged sale of plant and equipment to Robarch.

(e) He has always been ready and willing to assist the liquidators. He did so whenever he was asked.

(f) He and his wife, MD Meares, have moved to Queensland in order to put behind them the stress brought about by the collapse of the company and the farming businesses conducted by the MFT. MD Meares is pregnant with twins and should not now be vexed with the stress of public examinations.

(g) Robarch is a creditor of the company and was not notified of the creditors’ meeting held on 25 March 2013. It was denied the opportunity to vote on whether the liquidators should enter into a litigation funding arrangement with Pretium.

72 With the exception of some brief evidence concerning the purchase of plant and equipment by Robarch from the company and the payment to Mr Strang, RA Meares did not give any first-hand explanation of any of the impugned transactions or any of the other matters raised by the liquidators. He appeared implicitly to rely upon the explanations given by Mr Guy in his letter dated 7 February 2013. RA Meares knew nothing about the transactions with the NCC which were recorded in the company’s financial records.

73 MD Meares swore two affidavits which were read at the hearing. She said that:

(a) She commenced as the bookkeeper for the company, the MFT and Robarch in early 2009.

(b) She always made herself available to the liquidators in order to answer any questions which they had. She always replied promptly and fully to requests for information.

(c) She has never been asked about the impugned transactions or the other matters of interest to the liquidators.

(d) She faxed the bank statements and annotated depreciation schedule to the liquidators in September or October 2011, soon after she had been first requested to do so. She sent a further copy of those documents to the liquidators on 14 November 2012 after being requested to do so by an employee of the liquidators.

(e) The grant of an extension of time as sought by the liquidators will cause considerable inconvenience to her, given the advanced state of her pregnancy.

74 Mr Guy’s letter to Mr Gumbleton dated 7 February 2013 and the documents forwarded with that letter were tendered in evidence before me by the liquidators. In his letter, Mr Guy endeavoured to explain the sale of plant, equipment and motor vehicles by the company to Robarch in October and December 2008. These were the transactions which were the subject of the letters of demand sent to Robarch and to RA Meares dated 16 January 2013. In his letter, Mr Guy conveyed his instructions in respect of those transactions. The substance of his response was:

(a) The sale of the plant, equipment and motor vehicles referred to in Annexure “A” to the letters of demand was a genuine sale for fair value. Payment for those items was made on 28 October 2008 by RA Meares, on behalf of Robarch. It was made on that day by means of a Westpac staff-assisted withdrawal in the amount of $100,030. $100,000 of that amount was paid to Mr Strang by way of discharge of a debt due to him from the company. I pause to note that no explanation was offered in respect of the remaining $18,000 (the difference between $100,000 and $82,000).

(b) The repayment by the company of the loan from Mr Strang is evidenced in the Balance Sheet for the MFT for the year ended 30 June 2009. That Balance Sheet suggests that $100,000 was repaid to Mr Strang by or on behalf of the company at some time in the 2008–2009 Financial Year.

(c) The sale of the irrigator and spans by the company to Robarch on 28 October 2008 for $50,000 was also a genuine sale for fair value. Robarch assumed the company’s liability to Westpac in respect of those items in the amount of $43,672.96 and paid the balance in cash. The sum of $43,672.96 plus interest was paid to Westpac as follows:

(i) As to $23,826.71, by RA Meares, on behalf of Robarch, on 31 March 2009; and

(ii) As to $26,869.38, by Robarch, on 8 September 2010.

The balance of $6,327.04 should be accepted as having been satisfied by the surplus $18,000 paid to Mr Strang as part of $100,000 paid to him on 28 October 2008.

(d) The discharge of the liability of the MFT to Westpac in respect of the irrigator and spans is reflected in the 2008–2009 Balance Sheet for the MFT.

(e) The price for the other items referred to in the liquidators’ letters of demand (viz $38,000) was paid and discharged by a payment of $200,000 made to Landmark by RA Meares, on behalf of Robarch, on 3 April 2009.

75 Mr Guy went on to address a transaction involving an air seeder owned by the company. As I understand the liquidators’ contentions in support of the present application, they do not suggest that they have any potential claim arising out of the sale of that item of equipment. It was sold by agreement among Bank of Queensland, the liquidators and Robarch. The proceeds have been distributed in accordance with that agreement.

76 Mr Gumbleton commented upon Mr Guy’s assertions as follows:

(a) The circumstances of the payment to Mr Strang are not clear. No explanation for making a payment of $100,030 in discharge of a debt from Robarch to the company of $82,000 was provided. No evidence that this payment was made on behalf of Robarch was provided.

(b) The payments allegedly made to Westpac in respect of the irrigator and spans are not supported or explained by any documents. A similar state of affairs obtains in respect of the alleged payment to Landmark.

(c) The explanations offered on behalf of Robarch and RA Meares do not prove that the transactions took place as alleged by RA Meares and Robarch or that they were genuine transactions for fair value.

77 In his affidavit, Mr Strang said that, in about October 2007, a company with which he is associated, ARC Strang Australia Pty Ltd (ARC) lent $100,000 to RC Meares. The terms of that loan are documented in a formal Loan Agreement dated 1 October 2007. Neither the company nor Robarch was the borrower from ARC. The amount of the loan (viz $100,000) was repaid by RA Meares on behalf of RC Meares on 28 October 2008. The loan was a personal loan made to RC Meares and was not in any way related to any sale of plant, machinery and motor vehicles by the company to Robarch.

The Parties’ Submissions

The Liquidators’ Submissions

78 Counsel for the liquidators submitted that, when determining an application of the kind with which I am presently dealing, three matters must usually be considered. These are:

(a) Any explanation given by the liquidator for the delay in commencing the foreshadowed proceedings within the three year period contemplated by s 588FF(3) of the Corporations Act;

(b) Whether the proposed extension of time can be seen to be likely to serve some useful purpose. In particular, where an extension is sought for the purpose of investigating or conducting particular proceedings, whether, on a preliminary review, such proceedings appear to have any reasonable prospects; and

(c) Whether any party who would be affected by the extension (including, in particular, any potential defendants to identified proceedings) is likely to suffer prejudice in the event that an extension is granted.

79 These considerations were identified as relevant matters by Ward J in Re Clarecastle Pty Ltd (In Liq) (2011) 85 ACSR 260 at 267 [22]; and by Nicholas J in Walker v CBA Corporate Services (NSW) Pty Ltd (2012) 88 ACSR 153 at 161 [43]. See also 161–162 [44]–[46] in Walker v CBA Corporate Services (NSW) Pty Ltd per Nicholas J.

80 As to the liquidators’ explanation for their delay, Counsel for the liquidators submitted that the principal reason for the liquidators’ inactivity was a lack of funds. He submitted that a liquidator is not obliged to incur expense, including that which would be involved in the conduct of examinations or other investigations or the commencement of proceedings, where there are insufficient funds available in the winding up to meet those costs and expenses. He submitted that a liquidator should not be criticised for declining to take positive steps to investigate or prosecute claims where he or she could only do so by exposing his or her personal assets. Counsel accepted that a lack of funds, on its own, did not justify an extension. It was merely a factor to be taken into account with all other relevant considerations. It was submitted on behalf of the liquidators that prima facie the company’s lack of funds was caused by the very transactions which they now wished to investigate.

81 Counsel for the liquidators addressed two other matters when dealing with the question of delay. First, as is obviously the case, he emphasised that, with the exception of the payment to S & G, all of the impugned transactions were with related parties. Second, he stressed that all of those transactions were outside the ordinary course of business. His point was that the transactions were very suspicious indeed.

82 As to the liquidators’ prospects of success, Counsel submitted that all of the transactions which the liquidator wishes to investigate are susceptible to attack by engaging the provisions of Pt 5.7B of the Corporations Act. He submitted that no first hand, comprehensive or satisfactory explanation of any of the transactions had been offered by any of the related parties.

The Submissions of RC Meares and Sheila Meares

83 Counsel who appeared for RC Meares and Sheila Meares adopted the submissions made on behalf of RA Meares and Robarch.

84 He also submitted that the liquidators bore the onus of satisfying me that I should exercise my discretion in their favour. He submitted that, in the present case, the delay was extremely serious and was unexplained. He said that the liquidators had not bothered to seek further information from RC Meares after 1 July 2011 and had never contacted Sheila Meares. He also submitted that the documents filed with ASIC by the liquidators indicated that the liquidators had had in mind pursuing further investigations and possibly commencing proceedings against persons with whom the company had had dealings in the relevant periods for a long time but had not done so. He submitted that the delay was “… delay with knowledge …”. Counsel went on to submit that there was no suggestion of any lack of co-operation on the part of RC Meares or Sheila Meares. He also submitted that the additional allegations of breach of statutory and fiduciary duties made against RC Meares were not causes of action which could be brought pursuant to s 588FF of the Corporations Act and that those causes of action had a limitation period of six years. He said that the liquidators had failed to identify with any precision at all any s 588FE claim that could conceivably be brought against either RC Meares or Sheila Meares. Counsel relied upon the following statements made by Ward J in Re Clarecastle Pty Ltd (In Liq) at 303 [206]–[209]:

206 Mr Pritchard submits that the prejudice to Mr and Ms Shea is that, by reason of the liquidators undertaking their duties in piecemeal fashion they are becoming involved in successive proceedings (three to date), rather than the liquidator putting forward one claim containing all actions. It is said to be unfair to require a defendant to be “peppered” with claims many years after the event and that the multiplicity of actions should be discouraged.

207 On the question of prejudice to the interested parties for whom Mr Castle appeared, that was largely put in relation to the then forthcoming examinations summonses (and the prejudice arising from the fact that evidence would be compelled to be given in advance of the pending criminal trials against Messrs McCarthy and Seller). That prejudice has been considered and, to the extent I considered appropriate, dealt with by the orders I made in the examination proceedings. There seems to be no further specific prejudice to which those parties point (other than the presumptive prejudice arising from delay).

208 As to the issue of presumptive prejudice, in Agricultural & Rural Finance (at [192]) Tobias JA said:

[192] Although I accept the principle of presumptive prejudice is applicable to a case such as the present, I do not think that it should carry much weight when balancing the various factors which the court is required to take into account in the re-exercise of the relevant discretion.

209 I have already noted above the dicta of White J in New Cap (at [55]) in this regard in which his Honour observed that the absence of prejudice is not itself decisive but is, rather, a relevant factor to be taken into account in the exercise of the general discretion.

The Submissions of RA Meares and Robarch

85 Counsel who appeared for RA Meares and Robarch made two broad submissions. These were:

(a) The application must fail because it omits to identify a determinate time to decide whether to pursue voidable transactions; and

(b) In the alternative, the liquidators’ delay and the public policy against interring corporate corpses militate against the granting of the orders sought.

86 Counsel developed both of these arguments both in writing and orally.

87 The first argument is based upon a number of observations made by Spigelman CJ in BP Australia Ltd v Brown (2003) 58 NSWLR 322 at 345–346 [112]–[119]. In those passages, the Chief Justice said:

112 There is, in my opinion, a broader public interest to be served by allowing persons who have had dealings with companies which become insolvent to conduct their commercial affairs with a degree of certainty about their exposure to having past transactions unravelled.

113 I note the traditional hostility of the common law to the exhumation of bodies which was once described as an “inhuman and barbarous felony”. (Haynes’ case (1614) 12 Co Rep 113, 77 ER 1389. See also R v Lynn (1788) TR 733, 100 ER 394; R v Sharpe (1857) 7 Cox CC 214, 169 ER 959.) In this respect, equity followed the common law. (P W Young “The Exclusive Right to Burial” (1965) 39 Australian Law Journal 50; Beard v Baulkham Hills Shire Council (1986) 7 NSWLR 273 esp at 280.) This policy is informed by considerations of decency and human respect. Nevertheless, in my opinion, there is also a public policy against the disinterring of corporate corpses. Commercial life must at some stage rule off the past and focus energy on the future.

114 The commercial and economic life of the community is sometimes better served by allowing the loss to lie where it falls, so that all concerned may proceed with a high degree of certainty as to their financial position. The passage of time, even the passage of three years, can be seen to legitimately alter the balance of conflicting interests in this regard.

115 A creditor or other person who has received the benefit of a voidable transaction is at risk of having to surrender it. The time limit in s 588FF(3) has the effect that at the end of the period of three years, such a person will know whether s/he remains at risk. In a legislative scheme which seeks to balance conflicting commercial interests of this character, that appears to me to be a perfectly reasonable requirement. Those who have an interest, or who represent those who have an interest, to disturb transactions must indicate, within three years, whether they wish to keep open the option of doing so. In this, as in other areas, legal policy favours certainty.

116 As the House of Lords said in another context in R (Burkett) v Hammersmith and Fulham London Borough Council [2002] 1 WLR 1593 at [46]:

“… [L]egal policy favours simplicity and certainty rather than complexity and uncertainty. In the interpretation of legislation this factor is a commonplace consideration. In choosing between competing constructions a court may presume, in the absence of contrary indications, that the legislature intended to legislate for a certain, predictable regime.”

117 While s 70 and s 1322 of the Act may constitute contrary indications for many purposes, the legal policy in favour of certainty is nevertheless manifest in the text of s 588FF(3).

118 Section 588FF(3) does not have the effect of requiring all applications to be brought within a short period of time. It does, however, have the effect of requiring those who wish to keep open the option to do so, to determine that they do wish to do so within the three year period and to seek a determinate extension of the period. One thing that must be decided within the three year period is how long the process of deciding whether to pursue voidable transactions will take. Eventually, investigations to overcome deficiencies of information or the pursuit of funding must cease. Parliament has identified a reasonable time for such matters to occur, subject to a single determinate extension of time.

119 In a context where conflicting interests have to be balanced, the eventual loss of the ability to make a relevant claim can reasonably be regarded as something to be surrendered, in favour of providing certainty to others who have had dealings with the company, including other creditors, so that they can proceed with their business affairs with an assurance that they are no longer at risk.

88 Counsel submitted that extensions of time granted to liquidators pursuant to s 588FF(3)(b) may have significant impacts upon proprietary rights. He also submitted that the High Court had made clear in Gordon v Tolcher in his capacity as liquidator of Senafield Pty Ltd (In Liq) (2006) 231 CLR 334 that s 588FF(3)(b) was not merely a time stipulation of a procedural nature but that the time for making an application pursuant to that provision is of the essence of the provision itself (see 347 [37] per the Court).

89 In Gordon v Tolcher, at 347 [39], the High Court cited Spigelman CJ at 344 [107] with apparent approval.

90 Counsel for RA Meares and Robarch then submitted that any s 588FF(3)(b) application must identify within the three year period stipulated in s 588FF how long the process of deciding whether to pursue voidable transactions will take. He submitted that this requirement follows logically from the language of the section as well as the “normative justification” articulated by Spigelman CJ. It was then submitted that the period of extension sought by the liquidators in the present application is indeterminate with the consequence that the application does not satisfy a fundamental requirement of s 588FF(3). It seemed that this requirement was being elevated to the level of being a jurisdictional prerequisite to the engagement of the Court’s discretion.

91 Counsel for RA Meares and Robarch then moved on to deal with the question of delay. He submitted (correctly, in my view) that, when dealing with applications of the present kind, the Court must do what is “fair and just in all the circumstances” (Re Clarecastle Pty Ltd (In Liq) at 290 [130] per Ward J).

92 Counsel submitted that, when proper regard is had to the chronology of the dealings between the liquidators and his clients in relation to the company, it is apparent that the liquidators were well aware of the suspicious transactions as early as April 2010 but did nothing to investigate them until Pretium came onto the scene. He submitted that there has been no proper explanation offered for the liquidators’ delay. He submitted that the transactions in question are not particularly complex. He also submitted that RA Meares and MD Meares had made themselves available whenever requested. Counsel went on to submit that the Court should not reward the liquidators’ indolence in the present case.

Submissions of S & G

93 Counsel for S & G adopted the submissions made on behalf of RA Meares and Robarch. In addition, Counsel submitted that there was no evidence that the payment made to S & G of $110,111.04 on 19 August 2009 had been made from funds of the company. Counsel submitted that the liquidators had no prospects of succeeding in the claim against S & G on the evidence presently before the Court.

Consideration

The Threshold Point

94 Section 588FF(3) provides that an application made under s 588FF(1) can only be made within the periods specified in subpars (a) and (b). The periods specified in subpar (a) are certain. They are delineated by reference to known specific events. The period specified in subpar (b) is not marked out by the text of the provision itself in the same way. Rather, the period is to be determined by the Court in the exercise of the discretion bestowed upon it by the statute. The only requirement is that the application for the extension must be filed within the relevant period specified in subpar (a).

95 There is nothing in the language of s 588FF(3) which requires an application filed pursuant to s 588FF(3) to specify the claimed extension period in the application itself.

96 Furthermore, although I accept that Spigelman CJ in BP Australia Ltd v Brown did hold that a liquidator can make only one extension application pursuant to s 588FF(3)(b) (a conclusion with which I agree), in my judgment, his Honour did not hold that it was a jurisdictional or fundamental statutory prerequisite that an application made under that subsection must, in the text of the application itself, specify the length of the extension sought. The observations relied upon by Counsel for RA Meares and Robarch (at 341 [89]) and at 345–346 [112]–[119]) do not support the submission made by him. The remarks made by the Chief Justice at 352–355 [160]–[174] support the opposite conclusion. All that the Chief Justice intended to convey by the remarks relied upon by Counsel was that the Court was not authorised to grant an indeterminate extension but rather was obliged to fix a definite period for the making of the substantive applications contemplated by s 588FF(1) and to do so once only.

97 I reject the threshold submission made on behalf of RA Meares and Robarch.

Discretion

98 I accept the statement of the principles given by Counsel for the liquidators in his submissions as accurately capturing the relevant considerations which must guide the exercise of the Court’s discretion in a case such as the present. There was no real dispute as to those principles.

99 As to the question of delay, the only real explanation proffered by the liquidators for their inaction between the liquidation date and January 2013 is their lack of funds. It is true that, in 2010 and in 2011, they took some preliminary steps to investigate the company’s financial position and to seek to obtain information about some of the obviously suspicious transactions which they had by then discovered. However, they did not pursue RC Meares, Sheila Meares, RA Meares or MD Meares with any vigour. For example, although the response which MD Meares gave to Mr Gumbleton’s email of 5 July 2011 did not provide any information of substance, he did not follow up his queries until November 2012 (15 months later). MD Meares suggested that she had answered those queries promptly. She said that she forwarded bank statements and the annotated depreciation schedule by fax to the liquidators’ office in September or October 2011. I very much doubt that she did so. When she was contacted by an employee of the liquidators in November 2012, she did not mention that she had already sent the material. Rather, she simply complied with his request to send the information which he had outlined orally and by email. It would have been natural for MD Meares to have recorded in her email of 14 November 2012 that she had already sent the same material to the liquidators 15 months before, had she in fact done so.

100 Nonetheless, I do not think that MD Meares’ failure to respond to the liquidators’ requests can be fairly characterised as a lack of co-operation. She did make some response relatively quickly and was not pursued for further information.

101 Furthermore, there is no doubt that the liquidators made no further enquiries of either RC Meares or RA Meares after July 2011 and never spoke to or contacted Sheila Meares.

102 The liquidators’ explanation for their delay really comes to this: “We had no funds and it was not reasonable to take further or other action until Pretium came on the scene”. Somewhat faintly, the liquidators point to a lack of co-operation from Meares family members. The significance of the delay in the present case and of the liquidators’ explanations for their inaction must be assessed and weighed in the balance with the other relevant factors—namely, the prospects of the liquidators’ claims and prejudice to the affected parties (if any).

103 The liquidators have in mind investigating and possibly pursuing the six claims which I have described at [8] above.

104 None of those transactions took place during the six months ending on the relation-back day (ie between 3 September 2009 and 3 February 2010). In particular, none of the suspicious payments (Claims 4, 5 and 6) were made in that period. For this reason, those transactions could not be attacked as unfair preferences.

105 However, all of the impugned transactions may potentially be attacked as insolvent transactions which are uncommercial transactions (as to which see ss 588FB, 588FC, 588FE(3) and 588FF(1)).

106 The sale of plant, equipment and motor vehicles to Robarch in October 2008 and December 2008 did not produce funds for the company. The explanations proffered on behalf of RA Meares and Robarch as to the means by which payment was made by Robarch for these items are convoluted and unconvincing. On the evidence before me, the payment to Mr Strang of $100,030 on 28 October 2008 cannot sensibly be regarded as a discharge of the obligations of Robarch under the alleged sale arrangements. One transaction (the December 2008 transaction) took place some time after that payment; the payment to Mr Strang does not correspond to the purchase price; and Mr Strang says that the payment he received was to discharge a personal liability owed to him by RC Meares. These transactions were not fully explained by those who participated in them (RC Meares and RA Meares) although, of course, they could have been.

107 In addition, there is evidence to suggest that the company may have been insolvent by mid-2008 and remained in that state at all times thereafter. If that evidence is accepted, it would follow that the company was insolvent when it “sold” the relevant plant, equipment and motor vehicles to Robarch.

108 The two payments made to or on behalf of Sheila Meares on 25 August 2008 are suspicious. Apparently she knows nothing about these two payments or the affairs of the company. There is a discrepancy between the two versions of the 2009 Balance Sheet of the company tendered in evidence before me as to whether the company was indebted to Sheila Meares at all as at 30 June 2009 and, if so, to what extent. There is no explanation from RC Meares as to the circumstances in which these payments were made. When regard is had to the fact that the company had $650,000 cash at bank as at 30 June 2008 and no funds to speak of by the liquidation date and when account is taken of the several payments to and from S & G’s Trust Account in the period from June 2008 to August 2009, the liquidators are well justified in treating these payments as matters to be investigated. They may well be able to be recovered as insolvent uncommercial transactions.

109 The payment of $110,111.04 made to S & G on 19 August 2009 is in the same category as the payments made to Sheila Meares. The records of both S & G and the company are confusing as to the identity of the party upon whose behalf the pool of funds held by S & G out of which this payment was made were held. If those funds were held in trust for the company, as the MYOB records of the company and some of the records of S & G suggest, the payment may well be susceptible to attack as an insolvent uncommercial transaction.