FEDERAL COURT OF AUSTRALIA

Kismet International Pty Ltd v Guano Fertilizer Sales Pty Ltd [2013] FCA 375

| IN THE FEDERAL COURT OF AUSTRALIA | |

| JUDGE: | MURPHY J |

| DATE: | 29 APRIL 2013 |

| PLACE: | MELBOURNE |

REASONS FOR JUDGMENT

introduction

1 This proceeding relates to guano, which is the excrement, faeces and urine of seabirds, bats and seals, which in this case has been mined for use as a fertiliser.

2 From about May 1996 the applicants imported guano into Australia from Indonesia, and marketed and sold it as an organic fertiliser under and by reference to the name “Guano Gold Kwik Start” or “Guano Gold” (“the Guano Gold trademarks”). In early 2010 the respondents also commenced to import guano from Indonesia. They too marketed and sold the guano under and by reference to the Guano Gold trademarks between January 2010 and August 2011, doing so because they mistakenly believed that the trademarks belonged to the Indonesian guano supplier.

3 The applicants’ primary claim is that by using the trademarks in this way the respondents made false and misleading representations and engaged in misleading or deceptive conduct in breach of ss 52 and 53 of the Trade Practices Act 1974 (Cth) (“TPA”) before 1 January 2011, and the relevant successor provisions ss 18, 29 and 33 of the Australian Consumer Law in Schedule 2 of the Competition and Consumer Act 2010 (Cth) (“ACL”) after that date. The applicants also claims that the respondents engaged in passing off their guano as Guano Gold.

4 The respondents admit the statutory contraventions and the claim of passing off. The Court is required to assess the damages to be awarded to the applicants for:

(a) lost sales of Guano Gold (“the Lost Sales claim”); and

(b) diminution in the value of the applicants’ goodwill and reputation (“the Reputational Damage claim”).

5 Another claim in the proceeding arises out of the provision of warehouse services to the applicants by the second respondent, Grain Haul Pty Ltd. Pursuant to an agreement with the applicants, Grain Haul collected Guano Gold from the Melbourne wharf and stored it at its warehouse until it was required by the applicants’ customers. The applicants claim that in breach of its duty as a bailee for reward, or alternatively in negligence, detention or conversion, Grain Haul was unable to account for 4.55 tonnes of Guano Gold it warehoused in the period to February 2011, and 19.74 tonnes of Guano Gold in the period to July 2011. The applicants claim lost profits, or alternatively the replacement cost, of the guano that could not be accounted for (“the Lost Guano claim”).

6 The applicants, Kismet International Pty Ltd and Guano Australia Pty Ltd, are both companies controlled by their sole director, John Kismet Jashar. The fourth respondent, James Alfred McMahon, effectively controls the other three respondents. He is the sole director and shareholder of the first and second respondents, Guano Fertilizer Sales Pty Ltd and Grain Haul Pty Ltd, and he carries on the guano sales business of the third respondent. It is unnecessary for present purposes to differentiate between the two applicants on the one hand, or between the four respondents on the other. As such, unless the context otherwise requires, I will identify the applicants as Mr Jashar and the respondents as Mr McMahon.

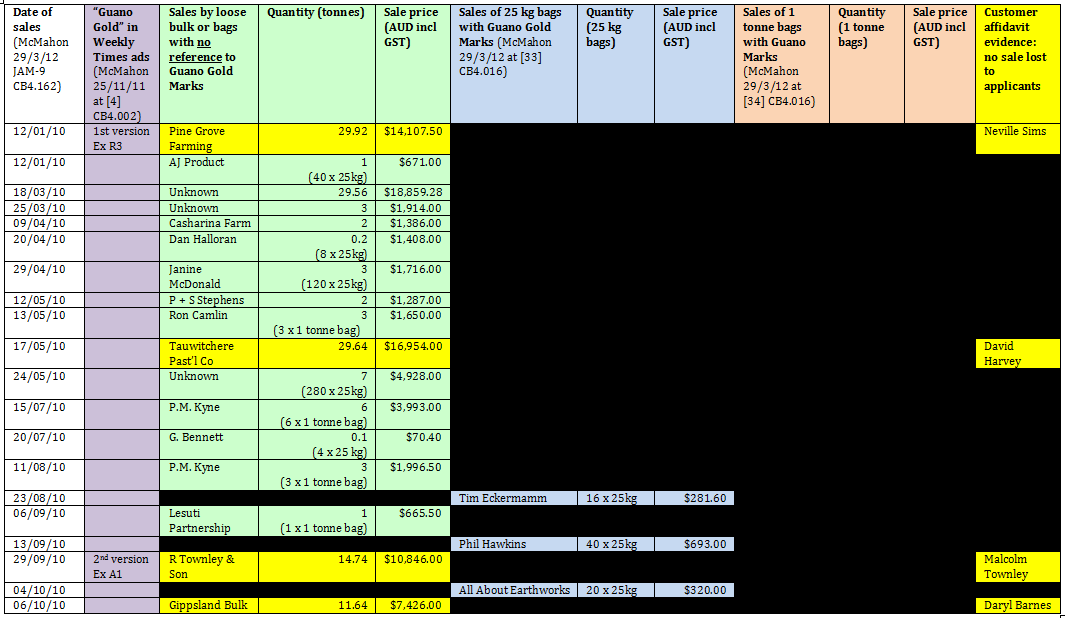

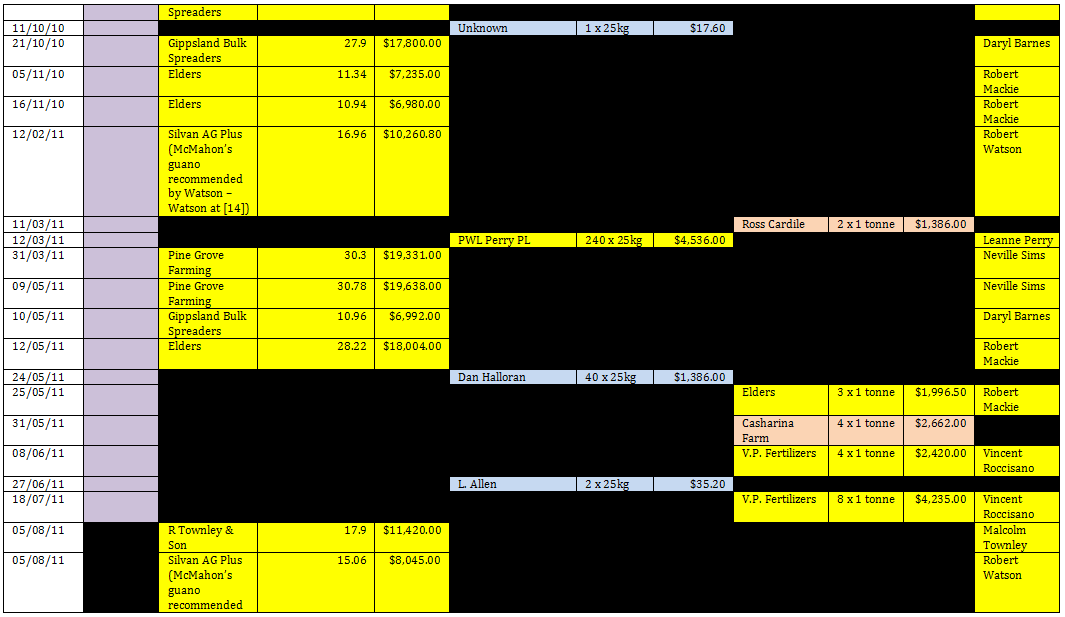

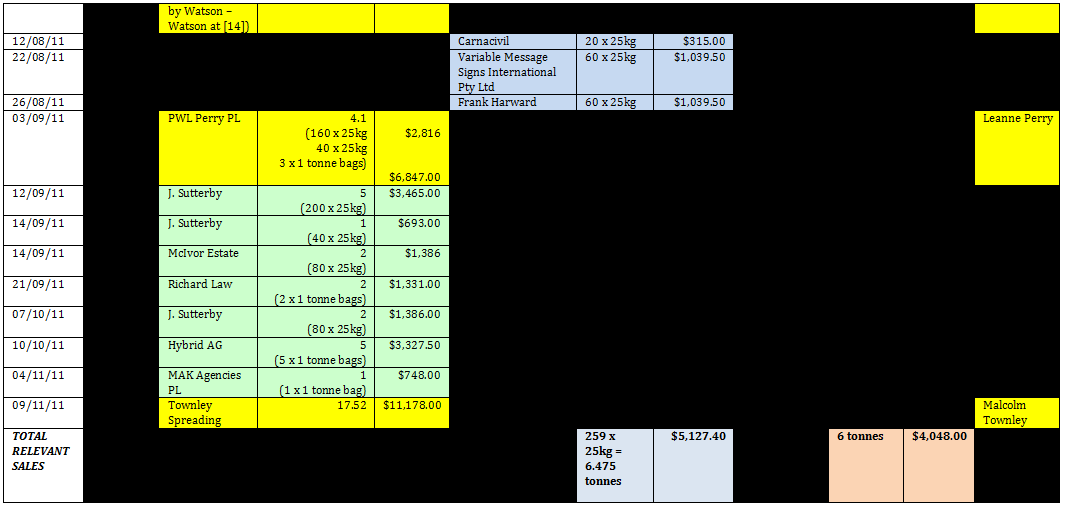

7 For the reasons I set out below, I consider that the applicants failed to establish an entitlement to damages under the Lost Sales claim, and are entitled to only modest damages under the Reputational Damages claim. I also consider that the applicants are entitled to only modest damages under the Lost Guano claim, reflecting the replacement cost of ten tonnes of Guano Gold.

The facts

The use of the Guano Gold trademarks in advertising

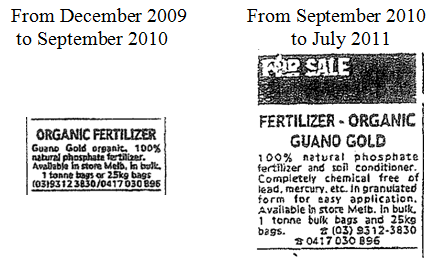

8 Mr McMahon admits that from at least 16 December 2009 until the end of July 2011 (except for a few weeks in early 2011) he ran small classified advertisements in The Weekly Times newspaper offering to sell guano fertiliser, describing it as Guano Gold. The first advertisement, running from December 2009 to September 2010, was headed “Organic Fertilizer” followed by smaller text reading “Guano Gold organic 100% natural phosphate fertiliser. Available in store Melb, in bulk, 1 tonne bags or 25 kg bags [telephone numbers]”. The second advertisement, running from September 2010 to July 2011, was headed “Fertilizer Organic” with the words “Guano Gold” in the second line. The advertisements ceased to refer to Guano Gold from 3 August 2011. The words “Kwik Start” did not appear in the advertisements.

9 It must be noted that the advertisements were neither large nor prominently positioned. They only ran weekly in the classified section of one rural newspaper. The two advertisements are set out below in the size that they appeared in the newspaper.

10 After July 2011 the advertisements no longer included the words Guano Gold, and instead just referred to guano. There can be, and is, no complaint in regard to Mr McMahon marketing his product by reference to the word “guano” as this is purely descriptive of the seabird and bat excrement that both he and Mr Jashar were importing from Indonesia. The complaint only relates to the use of the words Guano Gold and/or Kwik Start.

The use of the trademarks on bags of guano fertiliser and on dockets and invoices

11 Mr McMahon admits to making sales of guano packaged in bags bearing the words “Guano Gold Natural Kwik Start Fertiliser and Soil Conditioner” in the relevant period, selling some of it in 25 kg and 1 tonne bags carrying the Guano Gold trademarks.

12 He also sold a significant quantity of guano in loose bulk form, loaded directly from his warehouse onto customers’ trucks with no packaging that contained the trademarks. There was no evidence of usage of the trademarks by Mr McMahon on the invoices or dockets issued by him to his customers when they purchased loose bulk guano.

The similarity between guano from the two sources

13 Although there was evidence of some small differences between Mr McMahon’s and Mr Jashar’s guano, the weight of the evidence is that they were similar in appearance and in effect as fertiliser. Both were mined from the same region of Indonesia. Both parties accept that - for the purposes of assessing lost sales - one tonne of Guano Gold is interchangeable with one tonne of Mr McMahon’s guano.

The history of use of the trademarks

14 It is uncontroversial that Mr Jashar had used the Guano Gold trademarks extensively in the marketplace for many years. It is admitted that they have each come to signify to the trade and a substantial or, alternatively, a not insignificant proportion of the Australian public, Mr Jashar's goods so that persons seeking to acquire fertiliser under or by reference to the trademarks expect or intend to acquire Mr Jashar’s products and not the goods of any other person or from any other source.

The exclusive and valuable reputation in the trademarks

15 It is also admitted that Mr Jashar has, and for many years has had, substantial and valuable goodwill and reputation in the Guano Gold trademarks.

The total sales made by Mr McMahon

16 Mr McMahon put into evidence Annexure JAM-9 entitled “Second Amended Summary Document of Purchases and Sales by Guano Fertiliser Sales Pty Ltd”. It sets out the purchases and sales of guano made by him in the relevant period, the customers he sold to, the sale prices, the quantity sold, and whether the guano was sold in 25 kg bags, one tonne bags, or in loose bulk.

17 Mr Jashar accepts JAM-9 as accurate and it is common ground that Mr McMahon sold a total of about 424 tonnes of guano in the relevant period. The sales were made up of:

(a) 39.575 tonnes in 25 kg bags;

(b) 51 tonnes in 1 tonne bags; and

(c) 333.38 tonnes in loose bulk.

There are some slight differences between the totals proffered by the respective parties, but they are not material. My decision is based on the sales figures accepted by Mr Jashar in closing submissions. It is not in dispute that some of these sales were made to former customers of Mr Jashar.

the lost Sales claim

18 Mr Jashar has elected to claim damages, claiming lost profits from lost sales, rather than an account of profits. As such, he must show that he has lost sales to Mr McMahon as a result of the infringing conduct and he must quantify the lost profit that arises. His claim requires me to consider the counterfactual hypothesis of the sales that Mr Jashar would have made absent the infringing conduct, and the revenue and costs associated with those sales: TS & B Retail Systems Pty Ltd v 3Fold Resources Pty Ltd and Others (No 3) (2007) 158 FCR 444 at [207] per Finkelstein J.

19 As Mr McMahon’s admitted infringing conduct relates to sales of 424 tonnes of guano interchangeable with Guano Gold, the outer boundary of Mr Jashar’s claim is lost sales of 424 tonnes of Guano Gold.

The evidence necessary to establish loss and damage

20 The applicants bear the onus of proving the loss and damage claimed, with as much certainty as is reasonable having regard to all the circumstances. As Hayne J, with whom Gleeson CJ, McHugh and Kirby JJ agreed, explained in Placer (Granny Smith) Pty Ltd v Thiess Contractors Pty Ltd (2003) 196 ALR 257; [2003] HCA 10 at [37]-[38] (“Placer”):

[37] Placer undoubtedly bore the burden of proving not only that it had suffered damage as a result of Thiess Contractors' breach of contract, but also the amount of the loss it had sustained. It goes without saying that it had to prove these matters on the balance of probabilities and with as much precision as the subject matter reasonably permitted. (The Commonwealth v Amann Aviation Pty Ltd (1991) 174 CLR 64 at 80, 83-84 per Mason CJ and Dawson J, 138 per Toohey J, 153 per Gaudron J, 161 per McHugh J; Ratcliffe v Evans [1892] 2 QB 524)

[38] It may be that, in at least some cases, it is necessary or desirable to distinguish between a case where a plaintiff cannot adduce precise evidence of what has been lost and a case where, although apparently able to do so, the plaintiff has not adduced such evidence. In the former kind of case it may be that estimation, if not guesswork, may be necessary in assessing the damages to be allowed. (Fink v Fink (1946) 74 CLR 127; McRae v Commonwealth Disposals Commission (1951) 84 CLR 377; Jones v Schiffmann (1971) 124 CLR 303; Pennant Hills Restaurants Pty Ltd v Barrell Insurances Pty Ltd (1981) 145 CLR 625; Commonwealth v Amann Aviation Pty Ltd (1991) 174 CLR 64 at 83 per Mason CJ and Dawson J, 138 per Toohey J.) References to mere difficulty in estimating damages not relieving a court from the responsibility of estimating them as best it can (Fink v Fink (1946) 74 CLR 127 at 143 per Dixon and McTiernan JJ; McRae v Commonwealth Disposals Commission (1951) 84 CLR 377 at 411-412 per Dixon and Fullagar JJ; Commonwealth v Amann Aviation Pty Ltd (1991) 174 CLR 64 at 83 per Mason CJ and Dawson J) may find their most apt application in cases of the former rather than the latter kind.

21 It is established that in assessing damages the Court must do its best to quantify the loss suffered by the applicants by reason of the respondents’ breaches even if some degree of speculation and guesswork is involved: Aristocrat Technologies Australia Pty Ltd v DAP Services (Kempsey) Pty Ltd (in liq) (2007) 157 FCR 564; [2007] FCAFC 40 at [35] (“Aristocrat”) per Black CJ and Jacobson J; Placer at [38]; Enzed Holdings Ltd v Wynthea Pty Ltd (1984) 4 FCR 450; 57 ALR 167 at 183 (“Enzed Holdings”) per Sheppard, Morling and Wilcox JJ.

22 In Enzed Holdings the Full Court explained:

The principle is clear. If the court finds damage has occurred it must do its best to quantify the loss even if a degree of speculation and guess work is involved. Furthermore, if actual damage is suffered, the award must be for more than nominal damages. We should add that we can see no reason why this principle should not apply in cases under the Trade Practices Act as well as in cases at common law. We emphasise, however, that the principle applies only when the court finds that loss or damage has occurred. It is not enough for a plaintiff merely to show wrongful conduct by the defendant.

(Emphasis added.)

23 As Brooking J observed in JLW (Vic) Pty Ltd v Tsiloglou and Others [1994] 1 VR 237 at 241 to 246, it may be doubted that the Full Court in Enzed Holdings intended to lay down a general proposition that if damage is proved the court must, regardless of the circumstances, make some assessment of the damages. Consistently with the High Court’s later explanation in Placer, his Honour read down the remarks in Enzed Holdings to cases where “precise evidence” was not obtainable. His Honour noted at 241:

It is often said that the amount of the damage must be proved with certainty, but this only means as much “certainty” as is reasonable in the circumstances: Ratcliffe v Evans [1892] 2 QB 524 at 532-3. Where precise evidence is obtainable, the court naturally expects to have it; where it is not, the court must do the best it can: Biggin and Co Ltd v Permanite [1951] 1 KB 422, at 438; Commonwealth v Amann Aviation Pty Ltd (1991) 174 CLR 64 at 83 per Mason CJ and Dawson J. The nature of the damage may be such that the assessment of damages will really be a matter of guesswork, as in the well-known case of Chaplin v Hicks [1911] 2 KB 786, where the plaintiff had lost a chance of winning an engagement as an actress as a prize. So damages will be assessed for the wrongful detention of a racehorse even though it may be necessary to guess at the amount: Wilson v Matthews [1913] VLR 224… But while in some cases guesswork may be permissible in assessing damages, in others it is not.

24 At 243 his Honour continued:

There is no rigid dividing line between cases in which guesswork is permissible in assessing damages and cases in which it is not. The borderline between guesswork and rational assessment is itself indistinct, as is the line between evidence that is “precise” (the Permanite Case dictum) and evidence that is not. In Enzed Holdings v Wynthea (1985) 57 ALR 167, at 182-3…the Full Federal Court thought the case to be one in which precise evidence of the loss was not obtainable, so that if the trial judge found that the plaintiffs had suffered some loss he must do his best to quantify the loss even if “a degree of speculation and guesswork” was involved.

25 Mr Jashar argues that in assessing loss and damage resulting from the infringing conduct I should use the methodology applied in GM Holden Ltd and Others v Paine and Others (2011) 281 ALR 406 at [77] and [84] per Gordon J (“GM Holden”). Her Honour adopted the six step methodology employed in Elwood Clothing Pty Ltd v Cotton On Clothing Pty Ltd (2009) 81 IPR 378; [2009] FCA 633 at [11] (“Elwood”) and Norm Engineering v Digga Australia (2007) 162 FCR 1; [2007] FCA 761 at [266]-[271] (“Norm Engineering”), as follows:

(a) examine the number of sales made by the respondents;

(b) assume the respondents were trying to capture sales from the applicants;

(c) assume that the number of sales made by the respondents is equal to the number of sales lost by the applicants;

(d) discount the number in (c) to reflect the fact that not all sales made by the respondents can be considered sales lost by the applicants;

(e) apply any further discount necessary in the circumstances of the case; and

(f) multiply the resulting quantity by the applicants’ net profit.

26 The principles set out above are of importance in this case. As I explain below, I consider that Mr Jashar has failed to prove his claim of lost sales resulting from the infringing conduct, and also what his lost profit would be if he did prove some lost sales. In relation to the proposed six step methodology, I do not consider that is the best method for assessing damages in the present case, although if it is used the result is the same.

27 I turn now to deal with the evidence of the various witnesses going to whether Mr McMahon's sales should be seen as having resulted from the infringing conduct.

The applicants’ evidence that the sales resulted from the use of the trademarks

Mr Jashar

28 Mr Jashar’s evidence is that he was the first commercial supplier of guano fertiliser in Australia, that he established the market for guano fertiliser in Australia, that he coined the Guano Gold trademarks, and that his companies are the leading commercial suppliers of guano fertiliser in Australia. This evidence is unchallenged.

29 He gave detailed evidence as to his long usage of the trademarks such that they are strongly associated with him and his goods. This is admitted by Mr McMahon. He states that customers sometimes specifically asked for his goods by name. I accept this.

30 He says that Mr McMahon used the trademarks on the same type of goods, in the same market, selling to many of the same customers who had previously purchased guano from Mr Jashar. While I accept that Mr McMahon was selling fertiliser to Mr Jashar’s customers in my view Mr Jashar only established that some of Mr McMahon’s customers had previously purchased guano from him rather than many.

31 Although it is no great significance in my decision, I found Mr Jashar’s evidence of limited assistance when determining the number of Mr McMahon’s customers who were previously customers of his. Mr Jashar often sold his goods through distributors and he concedes that in giving evidence of sales to previous customers he is relying upon what he says he had been told by the distributors. Mr McMahon objects to this evidence on the basis that it is hearsay. Although called on to produce invoices of guano sales to previous customers the only invoices Mr Jashar produces relate to the Elders Koo Wee Rup branch and to Gippsland Bulk Spreaders. This did not assist him in his claim of sales resulting from the infringing conduct because both of these former customers gave evidence that their respective decisions to purchase guano from Mr McMahon were unrelated to the use of the trademarks.

32 On this issue Mr Jashar tended to overstatement and I have given his evidence little weight. His evidence is of limited assistance to his case because, while arguing that there were former customers of his whose decisions to transfer their custom to Mr McMahon were made because of the use of the trademarks, he adduces no direct evidence in this regard and did not even identify any such customer.

33 His evidence is also of limited assistance in regard to the extent to which those customers who transferred their custom to Mr McMahon had previously been exposed to the trademarks. Mr Jashar did not adduce evidence contradicting the evidence that the loose bulk guano was sold without any packaging carrying the trademarks nor did he contradict the evidence that many customers had no idea whether the source of the guano they earlier purchased was Mr Jashar. He also did not meet the evidence that when distributors on-sold loose bulk guano to farmers they simply described it as guano rather than referring to it by a brand name. Of course, against this is Mr McMahon’s admission that the trademarks signify Mr Jashar's goods to the trade and a substantial proportion of the Australian public, such that they have come to signify Mr Jashar's goods and not the goods of others.

Richard Jackson – agronomist

34 Richard Jackson, an expert agronomist, gave evidence for Mr Jashar. His evidence is that he has worked as an agronomist for approximately 26 years including 19 years as a consulting independent agronomist.

35 He says that soon after meeting Mr Jashar in the mid-1990s he was engaged on a fee-for-service consulting basis to provide agronomy services to Mr Jashar. In his opinion Guano Gold is a high quality product with unique features and benefits compared to other fertilisers on the market due to the combination of its silica and phosphorous content. In his view Guano Gold gives plants a quick start in terms of growth because it provides phosphorous in a form that is immediately available for their use. From the mid-1990s, together with Mr Jashar, he promoted Guano Gold to farmers and fertiliser dealers through printed materials, visits, field days and industry events around Australia.

36 Based on his experience and interactions with farmers, dealers and other agronomists he believes they strongly associate the trademarks with Mr Jashar and his companies.

Douglas Haas

37 Douglas Haas, the chairman of Biological Farmers of Australia Ltd, also gave evidence for Mr Jashar, stating that the trademarks are strongly associated with Mr Jashar and his companies.

The respondents’ evidence that the sales do not result from the use of the trademarks

Robert Watson - agronomist

38 Robert Watson, another expert agronomist, gave evidence for Mr McMahon. He has worked in the Gippsland region of Victoria for over 27 years advising and consulting to a large number of farmers in the region.

39 He says that guano is most effective when used as part of a fertiliser blend and that there is little difference between one type of guano and another. Rather than being different to each other he refers to Mr Jashar’s and Mr McMahon’s goods as “just guano”. In his view guano is a commodity, and it is not the type of product that attracts loyalty by customers to a particular brand. He says that sales of guano are made primarily on price.

40 Importantly, he states that he enthusiastically recommended to about 50 of his farmer clients that they purchase guano from Mr McMahon, many of whom went on to do so. In making this recommendation he did not recommend that they use Guano Gold, or any other brand of guano.

41 The thrust of his evidence, which I accept, is that his recommendation to farmers to purchase guano from Mr McMahon had nothing to do with the use of the trademarks. He says, and I accept, that he made the recommendation for other reasons including that there is no significant difference between Mr McMahon’s and Mr Jashar's guano, and that many of his clients that were already purchasing guano told him that they had a bad relationship with Mr Jashar and no longer wanted to deal with him. Two of Mr Watson's clients - Daryl Barnes of Gippsland Bulk Spreaders and Mr Mackie of Elders Koo Wee Rup branch - confirmed such difficulties in their evidence.

The evidence given by the seven named customers

42 Of even greater significance, and in an unusual step in a case of this nature, Mr McMahon called evidence from the following seven of his customers:

(a) Mr Daryl Barnes of Gippsland Bulk Spreaders Pty Ltd;

(b) Mr Robert Mackie of the Koo Wee Rup branch of Elders;

(c) Mr Neville Sims of Pine Grove Farming;

(d) Mr Vincent Roccisano of V & P Fertilizers Pty Ltd;

(e) Mr Malcolm Townley of Townley Spreading.

(f) Ms Leanne Perry of PWL Perry Pty Ltd; and

(g) Mr David Harvey of Tauwitchere Pastoral Company;

collectively, “the seven named customers”.

Daryl Barnes of Gippsland Bulk Spreaders

43 Mr Barnes’ is a director of Gippsland Bulk Spreaders Pty Ltd, a Gippsland -based supplier and spreader of fertiliser to farmers. His evidence is that he made three relevant purchases of guano from Mr McMahon totalling 50.5 tonnes. This is about 12% of the 424 tonnes in respect of which the applicants claim damages. Contrary to the applicants claim, on Mr Barnes’ evidence these sales had nothing to do with Mr McMahon's unauthorised use of the Guano Gold trademarks.

44 While Mr Barnes recalls seeing Mr McMahon's advertisement in The Weekly Times he says it was not a reason why he contacted Mr McMahon to purchase guano. He says he contacted Mr McMahon because of the recommendation made to him by Mr Watson, who had not recommended the purchase of any particular brand name of guano.

45 He further says that all of his purchases of guano were in loose bulk and none carried any packaging bearing the trademarks. He testifies that he was not aware that the guano he purchased from Mr McMahon had a brand name, and was not under the impression that the guano was in any way related to Mr Jashar or his companies.

46 His evidence is that one of the reasons behind his decision to transfer his custom to Mr McMahon was the fact that he found it difficult to deal with Mr Jashar as a supplier, describing him as a “serial pest”. He says that he told Mr Watson of his difficulties in dealing with Mr Jashar and Mr Watson recommended Mr McMahon as an alternative supplier.

47 Mr Barnes saw no significance in the brand name Guano Gold, and did not perceive any difference in the performance of Mr McMahon’s guano compared to Mr Jashar’s guano. So far as he was concerned both were just guano.

48 In the finish, counsel for Mr Jashar accepted that Mr Barnes’ evidence does not provide a basis for a finding that the sales to Gippsland Bulk Spreaders resulted from the admitted contraventions or passing off. I accept Mr Barnes’ evidence.

Robert Mackie, the branch manager of Elders, Koo Wee Rup

49 From about June 2010 Mr Mackie has been the branch manager of Elders in Koo Wee Rup which supplies various products and services to farmers in that part of Gippsland. He had also worked in the business from 1999 to 2004. On his evidence, Elders made four relevant purchases of guano from Mr McMahon totalling 53.5 tonnes, which is about 13% of the 424 tonnes of sales made. On his evidence, which I accept, these sales also had nothing to do with Mr McMahon's admitted contraventions and passing off.

50 Mr Mackie’s evidence is that while he read The Weekly Times and remembered seeing an advertisement for guano he did not recall whether the advertisement he saw was Mr McMahon's advertisement. He states that he paid the advertisement no attention and it was not relevant to his decision to purchase guano from Mr McMahon. The thrust of his evidence in this regard is that Elders is a substantial company and would not buy fertiliser based on a classified advertisement. He says that he contacted Mr McMahon as a result of a referral from one of his dairy farmer clients, Mr Brett Loughbridge, who was in turn a client of Mr Watson.

51 Mr Mackie purchased guano primarily in bulk, but on one occasion he purchased three one tonne bags. He states that he was simply seeking to purchase guano from Mr McMahon rather than a particular brand of guano, and was not aware that the guano he purchased was branded as Guano Gold or in any way connected to Mr Jashar or his companies. In his view, Mr McMahon's guano looked to be the same as Mr Jashar’s guano. He says that in invoicing the product to his own clients he referred to the product only as guano and not by reference to the trademarks, thereby illustrating the insignificance of the trademarks to him.

52 He states that an important factor in his decision to buy guano from Mr McMahon was that it was significantly cheaper. Finally, and similarly to Mr Barnes, another factor in his decision to transfer his custom to Mr McMahon was that he found Mr Jashar “very pushy” and did not like dealing with him.

53 Again, in the finish counsel for Mr Jashar accepted that it was not appropriate for the Court to infer that these sales resulted from use of the trademarks.

Neville Sims of Pine Grove Farming

54 Mr Sims owns and operates a grain, dairy and sheep farm named Pine Grove Farming near Echuca in Victoria. Mr Sims gave evidence that he had previously purchased guano from Nichol Trading, a fertiliser reseller in Rochester, but he did not recall it having any particular brand name. His evidence is that in early 2010 he saw one of Mr McMahon’ advertisements in The Weekly Times and he then telephoned and spoke to Mr McMahon.

55 On his evidence he made three relevant purchases of guano from Mr McMahon totalling 88 tonnes which is about 21% of Mr McMahon's sales. His evidence is that he had never heard of Mr Jashar or his companies, that he noticed only that the advertisement related to guano and did not notice the words Guano Gold, and that he was not looking to purchase guano of any particular brand. He states that, in their telephone conversation, Mr McMahon did not mention any brand name for the guano he was selling.

56 Mr Sims states that his purchases of guano were made in loose bulk, and therefore without any packaging indicating the trademarks. No invoices to him or dockets were produced which described the guano by reference to the trademarks.

57 Importantly, the thrust of Mr Sims’ evidence is that the most significant factor in his decision to purchase guano from Mr McMahon was that it was much cheaper than from other suppliers. He says that the price of $475 per tonne for guano from Mr McMahon was about $100 per tonne cheaper than the guano prices elsewhere.

58 Again, counsel for Mr Jashar accepted in closing submissions that there is no proper basis to infer that these sales resulted from the use of the trademarks.

Vincent Roccisano of V & P Fertilizers Pty Ltd

59 Mr Roccisano swore an affidavit in the proceeding and was not required for cross examination. He deposes that since 1991 he has been a director of V & P Fertilizers Pty Ltd, a fertiliser distribution business and a farm at Nichols Point in Victoria. His evidence is that during the relevant period he purchased some guano from Mr McMahon in one tonne bags. JAM-9 illustrates that he made two purchases totalling 12 tonnes which is about 3% of the relevant sales.

60 Mr Roccisano’s evidence is that he had known Mr McMahon for some years and in about May 2011 was told by somebody else that he was selling guano. He telephoned Mr McMahon to enquire about purchasing some guano and in the ensuing telephone conversation Mr McMahon simply referred to “guano” rather than referring to it by a brand name. He says that he had not seen the relevant advertisement in The Weekly Times at that time.

61 He says that he ordered some guano and when it was delivered he noticed that some of it was in plain bags with no trademarks, and some in bags carrying the trademarks. However, his evidence is that the trademarks did not mean anything to him and he was not under the impression that the guano was sourced from Mr Jashar or his companies. Again, the evidence does not support an inference that these sales resulted from the use of the trademarks and counsel for Mr Jashar accepted this.

Malcolm Townley of Townley Spreading

62 Mr Townley is a director of R Townley and Sons Pty Ltd trading as Townley Spreading, which operates a wholesale farm supplies and fertiliser spreading and distribution business in Bayles, Victoria. The evidence is that he made three purchases of bulk guano from Mr McMahon in the relevant period totalling 50.16 tonnes which is a further 12% of Mr McMahon's sales. The thrust of his evidence, which I accept, is that his decision to purchase guano from Mr McMahon had nothing to do with the use of the trademarks.

63 Mr Townley’s evidence is that prior to purchasing guano from Mr McMahon he had purchased bulk guano from distributors named Peter Abel and Southern Cross Rural. He also states that he purchased bulk guano in the late 2000’s from a distributor named EPC. He says that the bulk guano he then purchased did not carry any brand name and he did not recall any brand name being used on the invoices and dockets he received. He produces an invoice from Southern Cross Rural which referred to the product only as guano. Although I note that prior to early 2010 Mr Jashar was the only importer of guano, I accept Mr Townley's evidence that he did not know from whom his distributors sourced the guano.

64 Mr Townley says that in about September 2010 he saw one of Mr McMahon's advertisements in The Weekly Times and he telephoned him. He says that he does not recall the use of the words Guano Gold in the advertisement. He also says that Mr McMahon did not mention any brand name for the guano he was selling, referring to it just as guano. He states that he was not interested in whether the guano he purchased had a particular brand name, being more interested in the product itself and its chemical analysis.

65 Importantly, his evidence is that he was not acting under the impression that the guano he purchased was sourced from, or in any way connected to, Mr Jashar’s business. He had heard of Mr Jashar’s business at the time he saw the advertisement but he had never purchased anything from him or had any direct dealings with him.

66 In cross examination Mr Townley was taken to two weighbridge tickets relating to the relevant guano sales. On his evidence weighbridge tickets are created by the weighbridge operator, but based on information provided by the truck driver. From the tickets he identified the truck driver as his brother Lyall Townley, who is also employed by Townley Spreading. The two weighbridge tickets identified the goods being carried as Guano Gold. I infer from this that Lyall Townley knew that the product that he was carrying was called Guano Gold, and also infer that Townley Spreading knew this.

67 Mr Jashar contends that I should further infer that the sales of guano to Townley Spreading resulted from the use of the trademarks. I do not agree. It was Malcom Townley (and not his brother Lyall) who made the decision to buy the guano and his evidence is that he did not recall the words Guano Gold in the advertisement, that Mr McMahon did not attempt to sell guano to him by reference to any brand name, and that he did not purchase the guano because of the use of the trademarks.

68 His evidence is also that prior to these purchases he had never purchased any guano from Mr Jashar’s business, or to his knowledge guano under or by reference to the trademarks. This also points away from an inference that the sale resulted from the use of the trademarks. This conclusion is confirmed by later interactions between Townley Spreading and Mr Jashar. The evidence is that on two separate occasions in early 2012, well after Mr McMahon had stopped using the trademarks, Mr Townley declined an offer from Mr Jashar to sell him guano at a cheap price. He says that he found Mr Jashar “pushy” and that if he had wanted to purchase some more guano he would have simply called Mr McMahon.

69 I conclude from Mr Townley's evidence that these sales did not result from the use of the trademarks.

Leanne Perry of PWL Perry Pty Ltd

70 Ms Perry is a director of PWL Perry Pty Ltd which owns and operates a farm growing certified strawberry runners in Toolangi, Victoria. Her evidence is that she made two relevant purchases of guano totalling 14 tonnes, representing 3% of Mr McMahon's sales.

71 She says that in early 2011, being dissatisfied with her existing supplier of organic fertiliser, she saw Mr McMahon's advertisement for organic guano fertiliser in The Weekly Times. She states that she had not used guano as a fertiliser before, and was not aware of anyone else who had done so, but she was looking for organic fertiliser. She states that she did not recognise the name Guano Gold when she first saw the advertisement, and does not recall having seen that name previously or ever having heard of Mr Jashar or his companies.

72 She says that she telephoned Mr McMahon and placed an order for 240 25 kg bags of guano. When she later received delivery in March 2011 she noted that the bags carried the trademarks and she “googled” Guano Gold and looked at Mr Jashar’s website.

73 In relation to the significance of her looking at this website the following exchange occurred between Ms Perry and counsel for Mr Jashar,:

So it gave you confidence to keep buying the product? --- Well, I think went more on our own assessment of, you know, how it went, rather than what was said on the website, yes.

But having had – looked at the material on the website, you found it had all these wonderful properties you weren’t previously aware of? --- Yes.

And that you gave you reason to keep continually buying? --- Yes. Well, yes, to an extent, yes.

74 In September 2011 Ms Perry placed a further order for 200 25 kg bags and three one tonne bags of guano. She says that in making her later purchase of guano she was not concerned about any particular trademark and it is not controversial that when the second order arrived the bags did not carry the trademarks, as by then Mr McMahon had stopped using the trademarks.

75 Mr Jashar contends that this evidence shows that Ms Perry was concerned to buy Guano Gold, and that I should find that her second purchase was made because of Mr McMahon’s use of the trademarks. I do not agree. Although I accept that it is sufficient if the unauthorised use of a trademark is a contributing factor to the purchase (Hanave Pty Ltd v LFOT Pty Ltd (formerly Jagar Projects Pty Ltd) and Others (1999) 43 IPR 545 at [45]) I do not draw the inference contended by Mr Jashar.

76 The evidence is that Ms Perry was happy with her first purchase of guano because it proved to be an effective organic fertiliser. She says that her decision to continue to purchase the guano was mostly based on her assessment of its effectiveness. I had the benefit of seeing her in the witness box and I saw her concession that the applicants’ website was relevant “to an extent” in her continuing to purchase Mr McMahon’s guano, as quite limited. In my view it does not support an inference that the second sale resulted from the use of the trademarks.

77 Put another way, there is no evidence that Mr Jashar would have had the benefit of this sale if Mr McMahon had not used the trademarks. Given Ms Perry's ignorance about Guano Gold before she received her first order it is more likely that Mr Jashar’s guano would have remained unknown to her.

Mr David Harvey of Tauwitchere Pastoral Company

78 Mr Harvey has owned and operated a farm named Tauwitchere Pastoral Company at Narrung, South Australia since 1991, farming a range of organic produce. His evidence is that he made one relevant purchase of bulk guano from Mr McMahon of 29.64 tonnes, which represents a further 7% of the 424 tonnes in respect of which Mr Jashar claims damages.

79 Mr Harvey says he had previously bought guano from other suppliers in South Australia for about four years prior to purchasing from Mr McMahon, but did not recollect it having any particular brand name. However, in preparing to swear his affidavit in the proceeding he had checked an old guano bag (from guano supplied to him by a distributor, Grant Lyons in Strathalbum) and he noticed that it was marked Guano Gold. Importantly though, he says that he was unaware of this brand name when he made his first purchase of guano from Mr McMahon.

80 His evidence is that he considered guano to be an effective fertiliser and in May 2010 he saw and advertisement for guano in The Weekly Times and telephoned Mr McMahon. He does not recall noticing the words Guano Gold in the advertisement, and does not recall having seen those words at any time prior to the advertisement. He says that Mr McMahon did not mention Guano Gold to him in the telephone conversation, saying only that he was selling bulk guano which came from Indonesia. He made his first purchase of guano from Mr McMahon at that time.

81 He says that the guano he purchased arrived in loose bulk form - which meant that it did not have any packaging carrying the trademarks. His evidence is also that he did not understand that the guano that he purchased had any brand name and says that he had not heard of Mr Jashar or his companies at the time.

82 Mr Jashar contends that I should infer that this sale resulted from the use of the trademarks. I do not agree. Mr Harvey's evidence is that he did not notice the trademarks in the advertisement and that they meant nothing to him, that Mr McMahon did not mention the trademarks in making the sale, and that he did not understand that the guano he was purchasing was by reference to any brand name. When it arrived it did not carry any packaging with the trademarks.

83 In my view the proper inference from the evidence is that Mr Harvey’s purchase was unrelated to the use of the trademarks.

Consideration regarding Lost Sales claim

The failure to adduce any direct evidence from customers

84 Apart from sales to four of the seven named customers, Mr Jashar invites the Court to infer from the admissions and the evidence that the balance of Mr McMahon’s sales should be treated as lost sales and that the resulting total sales should be multiplied by the relevant profit margin per tonne so as to arrive at an appropriate damages award. I do not agree.

85 Although I have indicated other limitations in the applicants’ case, its most significant deficiency is the failure to adduce evidence from any customer that a relevant purchase from Mr McMahon resulted from the use of the trademarks, or that Mr Jashar would have likely achieved the relevant sale if not for Mr McMahon’s use of the trademarks.

86 In order to establish its loss and damage the applicants must provide sufficient evidence to establish it with sufficient certainty in all the circumstances of the case. Although evidence of actual deception is likely to be given great weight, it is not essential: Australian Woollen Mills Ltd v FS Walton and Co Ltd (1937) 58 CLR 641 at 658 per Dixon and McTiernan JJ; Facton Ltd v Toast Sales Group Pty Ltd [2012] FCA 612 (“Toast Sales”) at [175] per Middleton J. There are, of course, many cases of misleading conduct, and passing off where loss may be proved through inference , but the presence or absence of evidence showing actual sales resulting from the infringing conduct is a relevant consideration in evaluating whether loss and damage has been proven.

87 In the circumstances of the present case, I consider the absence of any evidence of actual sales resulting from the infringing conduct to be of real significance. JAM-9 illustrates that Mr McMahon only made sales of guano to between 30 and 35 customers, and 78% of the sales were made to only 8 customers. Well in advance of trial Mr Jashar was told the date, quantity and nature of the sales and the identity of each customer. He was provided, well in advance of trial, with affidavits by Mr Watson and seven of Mr McMahon’s customers (representing 71% of the sales made) deposing that the use of the trademarks played no role in the sales.

88 Mr Jashar’s evidence is that he and his distributors previously sold Guano Gold to many of these customers, which meant that he had a previous commercial relationship with them. Although he was confronted by powerful evidence directly contrary to his claim of lost sales resulting from the use of the trademarks, Mr Jashar did not adduce any evidence of actual sales to contradict it. He also concedes that he made attempts to have two customers give evidence in support of his claim but he had been unsuccessful.

89 Having regard to the principles set out by Hayne J in Placer and the other authorities I have referred to, there can be no question that Mr Jashar should be treated as having been “apparently able” to adduce precise evidence as to the reasons why some of these sales were made, and in particular why some of his former customers transferred their custom to Mr McMahon.

90 Mr Jashar knew and had previously enjoyed a commercial relationship with some of the customers who purchased guano from Mr McMahon. One indicator of the availability of direct evidence is that Mr Jashar admits that he spoke to two of these customers in an unsuccessful attempt to obtain direct evidence that their purchases resulted from the use of the trademarks. Another indicator is that Mr McMahon was able to adduce direct evidence from the seven named customers, and from Mr Watson as to his recommendation.

91 While the guesswork and speculation as to Mr Jashar’s lost sales which his contentions invite might be permissible when precise evidence is unavailable, as Enzed Holdings makes clear, it is not appropriate in the circumstances of this case. The evidence of Mr Watson and the seven named customers, and the fact that Mr Jashar was unable to find even one former customer to give evidence in support of his claims, strongly points away from the inference that the sales by Mr McMahon resulted from the infringing conduct.

Conclusion regarding the sales to the seven named customers

92 The evidence is that about 71% of the Mr McMahon’s sales during the relevant period were made to the seven named customers, and all gave evidence which weighs strongly against the conclusion that the sales resulted from the use of the trademarks. Mr Roccisano’s evidence was unchallenged, and I found the evidence of the others credible and persuasive.

93 In fact, following cross examination counsel for Mr Jashar conceded that the evidence of four of these customers allowed no basis for a finding in his favour in relation to those sales. His concession did not go far enough in my view and I am satisfied that there is no basis for a finding in favour of Mr Jashar in relation to the sales made to any of the seven named customers.

Conclusion regarding the sales to Silvan AG

94 JAM-9 also illustrates that a business named Silvan AG made two relevant purchases of guano totalling 32.02 tonnes, representing about 7% of Mr McMahon's sales. No evidence was adduced from Silvan AG but evidence in relation to these purchases was given through Mr Watson. Mr Watson’s evidence is that Silvan AG was one of his clients and that he recommended to Fred Rodowsky of Silvan AG that he buy guano from Mr McMahon.

95 Mr Watson gave evidence of an enthusiastic recommendation to his clients to purchase guano from Mr McMahon without reference to it being of any particular brand name, and it is plain that many of them followed his recommendation. Those of his clients that gave evidence say that their decision to purchase guano from Mr McMahon was unrelated to the use of the trademarks. As against this, Mr Jashar points to a weighbridge ticket dated 12 February 2011 which describes a truckload of guano being transported from Mr McMahon's warehouse to Silvan AG as Guano Gold. I accept that the driver of the truck, and probably also Silvan AG, knew the guano it was purchasing as Guano Gold, but this does not mean that the sale resulted from the use of the trademarks.

96 In my view the evidence indicates that these sales likely resulted from Mr Watson’s recommendation rather than from the use of the trademarks.

Conclusion regarding other categories of sales

97 Other than sales to the seven named customers and Silvan AG (which totalled 78% of the relevant sales) there are three further categories of sales which require consideration. The remaining sales are conveniently categorised into a colour-coded schedule based on JAM-9 prepared by the respondents (“the colour coded schedule”), which is marked “A” and attached to these reasons. The three different categories are identified in the colour-coded schedule by the use of the colours green, blue and salmon. No customer gave evidence in relation to any of these sales.

Conclusion regarding sales identified in green in the colour coded schedule

98 The sales identified in green in the colour coded schedule for the period 12 January 2010 to 6 September 2010 (made by between 8 and 11 purchasers) total 60.86 tonnes. Further sales identified in green occurred in the period 12 September 2011 to 4 November 2011 (made by a further 5 purchasers) total 18 tonnes. The sales totalled 78.86 tonnes overall, representing about 19% of Mr McMahon's sales.

99 Given the evidence and the admissions that the trademarks have been used extensively in the marketplace for many years, and:

(a) that they have come to signify Guano Gold to the trade and a substantial proportion of the public;

(b) that Mr Jashar has a substantial and valuable reputation in the trademarks; and

(c) that Mr McMahon's guano was sold using the same trademarks, from the same premises, in the same market, to some of the same customers who had purchased it from him;

Mr Jashar argues that I should start with the presumption that these sales resulted from the use of the trademarks.

100 I doubt that such a starting presumption is appropriate given the evidence of Mr Watson and the seven named customers as to the insignificance of the trademarks in about 78% of Mr McMahon’s sales. However, even if one starts with this presumption, the sales identified in green must be considered in light of the fact that each are either:

(a) sales of loose bulk guano (which did not carry any packaging with the trademarks and there is no evidence of invoicing by reference to the trademarks); or

(b) sales of guano in bags which did not carry the trademarks.

I note too that the sales made in the period 12 September 2011 to 4 November 2011 were made after the use of the trademarks in the advertisements ceased on 3 August 2011.

101 It is not controversial that in this category of sales there was no usage of the trademarks upon bags. As such, Mr Jashar’s claim largely turns on the use of the trademarks in the advertisements during the first set of sales from January to September 2010 because the advertisements had ceased by the second set of sales. While I accept that the misleading effect of false trademark usage in an advertisement can have a continuing effect for some time after publication ceases, in this case the advertisements were small classified advertisements, unlikely to have a significant impact. The evidence is that the trademarks played no role in the sales made to those of the seven named customers who saw the advertisements. In my view it is unlikely that the use of the trademarks in earlier advertisements resulted in the set of sales made after the advertisements had ceased.

102 The evidence of Mr Watson and the seven named customers that the use of trademarks played no part in 78% of the sales, that the trademarks did not appear on the goods themselves, and that the advertisements ceased to run in early August 2011, leads to the conclusion that I am not satisfied that these sales resulted from the use of the trademarks.

103 However, as I explain below, even if some modest percentage of these sales are properly to be seen as resulting from the use of the trademarks, Mr Jashar failed to prove the margin of profit on such sales and, as such, failed to prove his claim to damages.

Conclusion regarding sales identified in blue and salmon in the colour coded schedule

104 I will consider together the sales identified in blue and salmon in the colour-coded schedule. Taken together these two categories constitute sales of guano made to only nine customers, all of which were made in one tonne and 25 kg bags carrying the trademarks and totalling about 12.47 tonnes. They represent about 3% of Mr McMahon's sales.

105 Mr Jashar says again that I should start with the presumption that these sales resulted from the use of the trademarks. Again, I doubt that this presumption is appropriate given the evidence of Mr Watson and the seven named customers. It seems to me that, having determined that the use of the trademarks did not result in the significant majority of sales, I would need a good reason to reach a different view in relation to these further sales.

106 There are though some differences in the factual circumstances surrounding these sales and those that I have already dealt with. Unlike sales in the other categories, there is no direct evidence as to the reasons why customers made these purchases, they were made in either one or 25 kg bags which carried the trademarks, they predominantly occurred while the advertisements still referred to the trademarks, and there is no evidence of a recommendation by Mr Watson to any of these customers.

107 Despite these differences I have again concluded that Mr Jashar has failed to produce evidence sufficient to establish his loss and damage. The direct evidence of Mr Watson and the seven named customers, and Mr Jashar’s failure to adduce any direct evidence in response means that I am not prepared to draw the inference that he invites. He failed to prove that the relevant sales resulted from the infringing conduct and also failed to prove the profit margin lost on any sales that might be seen to have resulted.

108 I note in passing that even if some modest percentage of these sales are treated as sales resulting from the infringing conduct it would only result in a very small award of damages. If, say, 40% of these sales are accepted as sales resulting from the infringing conduct then Mr Jashar has a claim for lost profits on about five tonnes of Guano Gold. On the average profit margin of $358.47 per tonne that he claimed (but did not prove) his lost profit would only amount to about $1800.

The unreliable evidence as to Mr Jashar's profit margin

109 Having concluded that Mr Jashar has not proven any lost sales resulting from the infringing conduct it is strictly unnecessary to consider the evidence in relation to the profit margin on any lost sale. However, I do so because it illustrates further the evidentiary weaknesses in the Lost Sales claim. It confirms my view that no damages should be awarded under this head because, even if Mr Jashar could establish that some modest amount of sales resulted from the use of the trademarks, he failed to prove the profit lost on the sales.

110 In his affidavit sworn 27 February 2012 Mr Jashar produces Annexure JKJ-47 setting out the revenue derived from sales of Guano Gold in the years 1998 to 2011. It provides that in the 2011 financial year he sold approximately 1453 tonnes of Guano Gold, earning revenue of approximately $791,000. This calculates to claimed revenue from sales of an average of about $544.39 per tonne of Guano Gold.

111 Mr Jashar also produces Annexure JKJ-48 and deposes that it sets out the profit that his business earns per tonne of product sold in loose bulk, in 1 tonne bags and in 25 kg bags based on the average costs for a shipment of 15 full container loads containing 375 tonnes of Guano Gold product. He deposes that “[f]or each tonne of Guano Gold product that my business did not sell as a result of the respondents’ sales of their product under or by reference to Guano Gold or Guano Gold Kwik Start, my business lost the profit set out in Confidential exhibit JKJ-48.” I note in passing that Mr Jashar later accepted that JKJ-48 is not confidential.

112 In JKJ-48 Mr Jashar states that the profit he derives from sales of Guano Gold is:

(a) $326.147 per tonne when sold in loose bulk;

(b) $343.147 per tonne when sold in 1 tonne bags; and

(c) $406.147 per tonne when sold in 25 kg bags.

113 Also in JKJ-48 he sets out the sale prices per tonne of Guano Gold as:

(a) $599.75 per tonne when sold in loose bulk;

(b) $659.75 per tonne when sold in 1 tonne bags; and

(c) $699.75 per tonne when sold in 25 kg bags.

114 However, it became apparent in cross examination of Mr Jashar that there were various inconsistencies between the profit margin he claims in JKJ-48, the sale prices per tonne he sets out in JKJ-47, and financial statements of Kismet International Pty Ltd for the year ended 30 June 2011 (“the financial statements”).

115 Of particular significance is the inconsistency between the sale prices per tonne of Guano Gold claim in JKJ-48 and the sale prices per tonne revealed in JKJ-47. In fact, the profit margin he claims in JKJ-48 is based on a sale price per tonne ranging between $55 and $155 per tonne more than the average sale price he specifies in JKJ-47.

116 Other inconsistencies between JKJ-48 and the financial statements include differences in the total cost of purchases, the total trucking costs and the total storage costs, for Guano Gold. In each example the costs set out in the financial statements are significantly higher than in JKJ-48.

117 Counsel for Mr McMahon argues that the inconsistencies indicate that Mr Jashar deliberately overstated his revenue and understated his expenses so as to overstate the profit margin per tonne. I do not accept that Mr Jashar was deliberately untruthful in his evidence in this regard and some of the inconsistencies are capable of explanation because the income and cost figures in the financial statements are not limited to Guano Gold. That is, the cost of purchases, the trucking costs, and the storage costs relate to other goods as well as Guano Gold and it is therefore unsurprising that the figures in JKJ-48 are lower.

118 Even so, the cross examination of Mr Jashar reveals that behind some of the inconsistencies lay questions as to the adjudication of various costs and expenses. In seeking to explain some of the inconsistencies he states:

All my accounts are done by a bookkeeper by MYOB. I don't have very much to do with it. When all the invoices come to the office for our Customs, our AQIS, our trucking, our storage, all of our purchasing, all the costings that you can see on here, they are very complex. In a lot of times the costs and fees are bundled into one as is - as trucking or AQIS or Customs, so it is a very difficult task for the bookkeeper to adjudicate precisely what is an actual storage costs, what's a trucking cost, what’s an AQIS cost, what’s a Customs cost and that’s the only light that I can shed on that component…

119 I have no difficulty in accepting that the adjudication of some of the costs is a complex task and that there is some complexity to the calculation of his profit margin. However, he disclaims any expertise in relation to the books of his business and his explanation above effectively concedes the shortcomings in the evidence he adduces in this regard. In particular he offers no explanation for the significantly greater sale prices per tonne of Guano Gold claimed in JKJ-48 compared to the sale prices per tonne set out in JKJ-47. He has the burden of proof and he did not call any evidence to properly explain the inconsistencies or explain how the necessary adjudication of the large trucking and storage costs was performed.

120 I note also that the basis for Mr Jashar’s calculation of the profit margin is not as he swore in evidence in chief. He said that the profit margin calculation in JKJ-48 was made by him based on the average costs for a shipment of 15 full container loads containing 375 tonnes of Guano Gold product. However, in cross examination he conceded that the calculations were based on only three or four shipments in the 2011 financial year. He does not explain the rationale under which he selected - as the basis for his profit margin calculation - these three or four shipments from all of the shipments that had occurred.

121 Notwithstanding these obvious problems Mr Jashar submits that the Court should rely on JKJ-48 in doing its best to quantify Mr Jashar’s loss. In the alternative, he argues that the figures in the 2011 financial statement may be used to quantify his lost profits per tonne. In an attempt to reflect the fact that the figures in the financial statements relate to other goods sold by Mr Jashar as well as Guano Gold, he proposes that I rely on the various revenue and expense figures in the financial statements, but apply various percentage reductions to the income from sales, and the costs referable to the sales.

122 I do not accept these submissions. First, there is no proper foundation in the evidence for a reliable determination of the proper percentage reductions to be applied to the revenue and expense figures to reflect the sales by Mr Jashar of other goods. Secondly, in the circumstances of this case the authorities do not countenance the type of speculation and guesswork Mr Jashar’s submissions invite.

The application of the six step methodology in this case

123 In reaching my assessment of damages I have not utilised the six step methodology often used in cases of this type. In not doing so I mean no criticism of the methodology as it is plainly appropriate in many cases. However, it must be seen as a tool for performing the task of assessing loss and it should not be applied in such a way that it subverts the purpose of a damages award, that is, to compensate Mr Jashar for any loss resulting from the infringing conduct.

124 The six step methodology is particularly suited to circumstances where precise evidence of the infringing sales is unavailable - a not uncommon occurrence in cases of this type. For example, in GM Holden Gordon J applied this methodology in circumstances where, amongst other things, the respondents had failed to comply with a court order to provide relevant evidence: GM Holden at [73]. In Adidas-Salomon AG v Turner (2003) 58 IPR 66 at 67 Goldberg J took a similar approach in a counterfeiting case where the respondent did not produce any documents evidencing the purchases or sales of the infringing items. In Elwood Gordon J took the same approach in circumstances where the applicant chose not to provide proper sales data and relied solely on the proposition that sales made by the respondent should be taken as sales lost by the applicant: Elwood at [13] and [24].

125 These are not the circumstances of the present case. Mr McMahon has adduced evidence setting out the dates of all sales he made, the quantities sold, the identities of the customers and, most significantly, detailed evidence that indicates that at least 70% of the sales had nothing to do with the use of the trademarks.

126 I note too that even if I use the methodology Mr Jashar prefers, the result would be the same. Applying the first three steps of the six step methodology would identify the number of relevant sales as sales totalling 424 tonnes. Step four provides for a discount to reflect the fact that not all the Mr McMahon’s sales can be considered Mr Jashar’s lost sales, and step five requires the application of a further discount in all the circumstances of the case.

127 Using this methodology, Mr Jashar concedes that a discount should be applied so that the sales made to Mr Barnes, Mr Mackie, Mr Sims and Mr Roccisano are excluded. However, he argues that there should be no further discount applied because, amongst other things, he was the first commercial supplier of guano fertiliser in Australia, he established the market for guano fertiliser in Australia, he coined the trademarks which have been used extensively for many years, and his companies are the leading commercial suppliers of guano fertiliser in Australia. He notes that Mr Haas and Mr Jackson both gave unchallenged evidence that the trademarks are strongly associated with him, and that it is admitted that he has developed an exclusive and valuable reputation in the trademarks. He reiterates that Mr McMahon's guano was sold using the same trademarks, from the same premises, in the same market, to many of the same customers who had purchased it from him.

128 Mr Jashar relies on Colbeam Palmer Ltd v Stock Affiliates Pty Ltd (1968) 122 CLR 25 at 44 per Windeyer J and argues that in these circumstances I should start with the presumption that the use of the trademarks by Mr McMahon was a material factor in his sales of guano. I do not agree that such a presumption is appropriate on the evidence. However, even if it were, the weight of the evidence is that the use of the trademarks played little or no role in the sales and any presumption would be rebutted.

129 It must be said that Mr Jashar's contention that no discount should be applied, except in relation to the sales made to four identified customers does not withstand examination. Without reiterating it in detail, the evidence in support of a substantial discount includes the following:

(a) Mr Watson's enthusiastic and effective recommendation to his farmer clients that they purchase guano from Mr McMahon;

(b) Mr Watson's evidence and recommendation that there is little difference between the two sources of guano, it being “just guano”;

(c) Mr Watson's evidence that guano is not the type of product that attracts loyalty by customers to a particular brand;

(d) that many of the customers who gave evidence were unaware of Guano Gold or of Mr Jashar or his companies;

(e) that some customers considered the much cheaper price an important factor in their purchasing decision;

(f) Mr Watson's evidence that some of his clients wanted a different supplier to Mr Jashar, and the confirming evidence of Mr Barnes, Mr Mackie and Mr Townley of difficulties in their relationship with Mr Jashar; and

(g) most importantly, that seven named customers making up 71% of the sales state that their purchases did not result from the use of the trademarks.

There is no direct evidence contradicting the credible and persuasive evidence given by Mr Watson and the seven named customers.

130 Various decisions of this Court also indicate a much higher discount than that proposed by Mr Jashar. In Elwood at [25] Gordon J applied a two thirds discount to the total number of sales in recognition of the fact that the respective T-shirts of the competing parties were sold at different prices and through differing retail and wholesale channels. In GM Holden at [84] Gordon J applied a discount of 40% in circumstances where the customers of the infringing replica 20 inch alloy car wheels were owners of GM Holden VE Commodore cars seeking to purchase Holden branded wheels specifically designed by GM Holden for those cars.

131 In Norm Engineering at [292] to [296] Greenwood J applied a 50% discount even though there was evidence that both parties operated in a similar market and the respondent was actively seeking to divert sales from the applicant as the market leader. In Review Australia Pty Ltd v Innovative Lifestyle Investments Pty Ltd and Another (2008) 166 FCR 358 at [23], [25] to [26] (“Review v Innovative”) Jessup J effectively applied a 100% discount to the total number of sales on the basis that the applicant had failed to put forward sufficient evidence to allow an inference that any sales made by the respondent could be properly characterised as sales lost by the applicant, even though the parties were selling to similar markets at similar prices.

132 In each these cases the trademark was central to the infringing product and likely to be important in a customer's decision to purchase it. By way of comparison, in the present case the weight of the evidence included that the trademarks played little or no role in the customer's decision, that the product is “just guano”, and that there were many other significant reasons for the sales. In my view the applicants in the cases discussed above had much stronger claims for lost profits than Mr Jashar, yet substantial discounts were made.

133 In my opinion the evidence in the present case is so strongly indicative that the relevant sales did not result from the infringing conduct that the appropriate discount under the six step methodology is at, or close to, 100%. As such, whichever approach is taken, I consider that Mr Jashar failed to establish that he suffered loss or damage under his Lost Sales claim.

The Reputational Damage claim

Relevant legal principles

134 In GM Holden at [90] Gordon J summarised the approach taken in a number of recent cases to assessing damages to reputation. Her Honour explained:

Where reputational damages are sought, evidence is usually led to establish: (a) the importance of singularity, distinctiveness, quality or some other commercially valuable aspect of reputation to the victim; and (b) how, and to what extent, the infringing product or conduct damage that aspect of the victim' s reputation…

135 In Facton Ltd and Others v Rifai Fashions Pty Ltd and Another (2012) 199 FCR 569 (“Rifai”) the Full Court per Lander, Gilmour and Gordon JJ considered reputational damages in the context of sales of counterfeit copies of exclusive G-Star clothing. The primary judge had refused to award reputational damages on the basis that the applicants had not adduced evidence to demonstrate the value of their goodwill or reputation. The Full Court overturned this decision, Lander and Gordon JJ holding at [25] that reputational damages were justified on the basis of findings:

(a) that the applicants had established a substantial, exclusive and valuable reputation in Australia in relation to the trademarks, brand and goods;

(b) that the brand would be diminished by the sale of counterfeit items; and

(c) that customers would be lost because the goods are no longer considered exclusive.

Gilmour J reached the same conclusion referring to similar considerations at [118] to [120] and [123] to [125]. These principles will guide me in assessing whether Mr Jashar suffered reputational damage.

Consideration

136 The facts relevant to this claim have already been set out. Being admitted, the first limb of the test in Rifai is satisfied.

137 In dealing with the last limb of the test, I reiterate my view that Mr Jashar has not proven that he lost any customers by the use of the trademarks. It is unnecessary that I again detail the evidence supporting this conclusion.

Has Mr Jashar's substantial and valuable goodwill and reputation in the trademarks been diminished

138 The remaining issue is whether Mr Jashar’s admitted substantial and valuable goodwill and reputation in the trademarks is likely to have been diminished by the infringing conduct.

139 Mr McMahon contends that there is no basis for the Court to conclude that Mr Jashar’s goodwill and reputation has been diminished as a result of the use of the trademarks. I will not detail his arguments in this regard as he relies upon the same evidence - already traversed in detail - given by Mr Watson and the seven named customers. The respondents argue that it was available to Mr Jashar to call evidence from some identified customers who purchased Mr McMahon’s guano as to whether that customer’s view of Guano Gold was detrimentally affected as a result of the use of the trademarks. He says that if there is any merit to the inference that the market’s view of Mr Jashar’s product was diminished by the use of the trademarks, then one would expect that at least one customer would have given evidence to support his claim. There is some force to these contentions.

140 Mr McMahon also points to the decision of Jessup J in Facton Ltd v Mish Mash Clothing Pty Ltd (2012) 94 IPR 523 at [49] to [52] (“Facton v Mish Mash”). In this case Jessup J reviewed several earlier decisions where the Court had awarded reputational damages, namely Review Australia Pty Ltd v New Cover Group Pty Ltd (2008) 79 IPR 236 per Kenny J (“Review v New Cover”), Elwood per Gordon J, and his own decision in Review v Innovative.

141 His Honour noted that in Review v Innovative evidence was given that the applicant had “a reputation for originality of design in relation to dresses and frocks” and unchallenged evidence led by the applicant showed that when its designs were adopted by other traders the originality was lost. His Honour considered that Review v New Cover was also a “designs case” in which Kenny J accepted on the evidence in that case at [46] “that ‘exclusivity’ (and design ‘freshness’) was of commercial value”. Jessup J considered that Elwood was also a case in which the intellectual property sought to be protected was associated with something striking about the appearance of products in relation to which exclusivity was both asserted and established. His Honour refused to award reputational damages, noting the obscure rather than conspicuous nature of the relevant labels in the case before him, in contrast to the striking elements upon which the claims to exclusivity were established in the other cases. He noted too the lack of evidence that the mark was associated with a reputation for exclusivity or originality: Facton v Mish Mash at [53].

142 Mr McMahon submits that the present case is also very different to these three cases. He argues that the question of reputational damage falls to be considered in the circumstances that the relevant goods are guano fertiliser - that is bird, bat and seal excrement -and that there is no significant difference in appearance or effect between the competing guanos. In effect he says it is “just guano”.

143 As against these submissions, it must be remembered that Mr McMahon admits that:

(a) the trademarks have been used extensively in the marketplace for many years;

(b) they have each come to signify Mr Jashar's goods to the trade and a substantial or, alternatively a not insignificant, proportion of the Australian public, so that persons seeking to acquire fertiliser under or by reference to the trademarks expect or intend to acquire Guano Gold; and

(c) Mr Jashar has, and for many years has had, a substantial and valuable goodwill and reputation in the trademarks.

144 While it may be accepted that Mr Jashar’s guano is not “exclusive” in the same sense as the fashion clothing in the “design cases” discussed above, I consider that the admitted substantial and valuable goodwill and reputation in the trademarks must mean that the trademarks signify the singularity and distinctiveness of his product. This singularity and distinctiveness is likely to have suffered some damage as a result of Mr McMahon's sales of competing guano over an extended period under or by reference to the trademarks, in the same market, and to many of the same customers.

145 Notwithstanding the evidence of Mr Watson and the seven named customers, I am drawn to the conclusion that the distinctiveness of the trademarks has likely been diminished because of the admitted infringing conduct, and because reputation is inherently fragile and susceptible to diminution. This is particularly the case where, as here, the trademarks were not registered at the relevant time and the distinctiveness arising from their use is the foundation of Mr Jashar’s rights in the trademarks. If the trademarks cease to be singular or distinctive of Mr Jashar’s goods their reputation is undermined

146 I note also that no evidence as to reputational damage was adduced from any customer in Rifai and this was not fatal to the claim of reputational damage. Although strictly referring to the primary judge's conclusion that there was no evidence to demonstrate the value of the goodwill or reputation, Lander and Gordon JJ observed at [27] that “we cannot think of any further evidence that the appellant's could have adduced in relation to the damage to their reputation.” Nor, in Rifai was it fatal to the claim of reputational damage that there was no evidence that the applicant’s reputation had suffered because the counterfeit products were inferior in quality to the genuine articles. Gilmour J allowed reputational damages although noting the absence of such evidence at [126].

The quantum of reputational damages

147 The quantum of damages to be awarded for loss of reputation is notoriously difficult to assess. In these circumstances the courts have long recognised that imprecise assessment is allowed and the Court must do the best that it can. As Lander and Gordon JJ observed in Rifai at [28]:

It is not easy in any given case to establish a reputation and to identify in monetary terms the value of the loss of that reputation. However, in our opinion the appellants established the former, and the Court was obliged to consider the latter: Enzed Holdings Ltd v Wynthea Pty Ltd (1984) 4 FCR 450. In Commonwealth v Amman Aviation Pty Ltd (1991) 174 CLR 64 at 83, Mason CJ and Dawson J said:

The settled rule, both here and in England, is that mere difficulty in estimating damages does not relieve a court from the responsibility of estimating them as best it can. Indeed, in Jones v Schiffmann Menzies J. went so far as to say that the “assessment of damages…does sometimes, of necessity involve what is guess work rather than estimation”. Where precise evidence is not available the court must do the best it can…

Similarly, Gilmour J noted at [117] that:

…mere difficulty in assessing damages does not relieve the Court of its responsibility of estimating them as best it can, and although damage to reputation may be difficult to quantify, it is compensable nonetheless.

148 Both parties focussed in their submissions on assessments of reputational damages made in other cases. They pointed to the assessment in Rifai at [29] and [128] where the Full Court allowed reputational damages at $5000, in GM Holden at [93] where Gordon J assessed the damage to reputation at $20,000, and in Elwood at [12] and [34] where her Honour awarded damages of $10,000 in respect of 28,139 infringing garments sold. They referred to the assessments of Jessup J in Review v Innovative at [31] of $7500 and in Facton v Mish Mash where his Honour found damage was not proven.

149 Mr Jashar argues that the decision in Rifai is not a reliable guide in this case, and that a significantly higher award is appropriate in the present case having regard to the larger quantity of the infringing sales in the present case and the longer time period of time over which the infringements took place. Given my finding that none of the sales occurred as a result of the infringing conduct I do not accept that Rifai should be distinguished on the basis contended by Mr Jashar.

150 Even so, the question of whether the applicants have suffered reputational damage must be decided on the facts of this case, and the various decisions referred to are of limited assistance. The assessment of reputational damages is a matter of judgement, and in my view the damages in the present case must be modest. Although I accept that some reputational damage is likely to have occurred through the use of the trademarks, the evidence indicates that any damage to the applicants’ goodwill and reputation is slight. In particular this is indicated by the evidence of Mr Watson as to the nature of the goods and that they are seen as “just guano”, the fact that the claim relates to bird and bat excrement rather than exclusive products like fashion clothing, and the evidence of Mr Watson and the seven named customers (representing most of the market) that the sales made to them had nothing to do with the use of the trademarks. Doing the best I can, I award $5000 for reputational damage.

the Lost Guano claim