FEDERAL COURT OF AUSTRALIA

Ebooks Corporation Limited, in the matter of EBooks Corporation Limited [2013] FCA 305

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

IN THE MATTER OF EBOOKS CORPORATION LIMITED

|

EBOOKS CORPORATION LIMITED (ACN 079 690 679) Plaintiff | |

|

DATE OF ORDER: |

|

|

WHERE MADE: |

THE COURT ORDERS THAT:

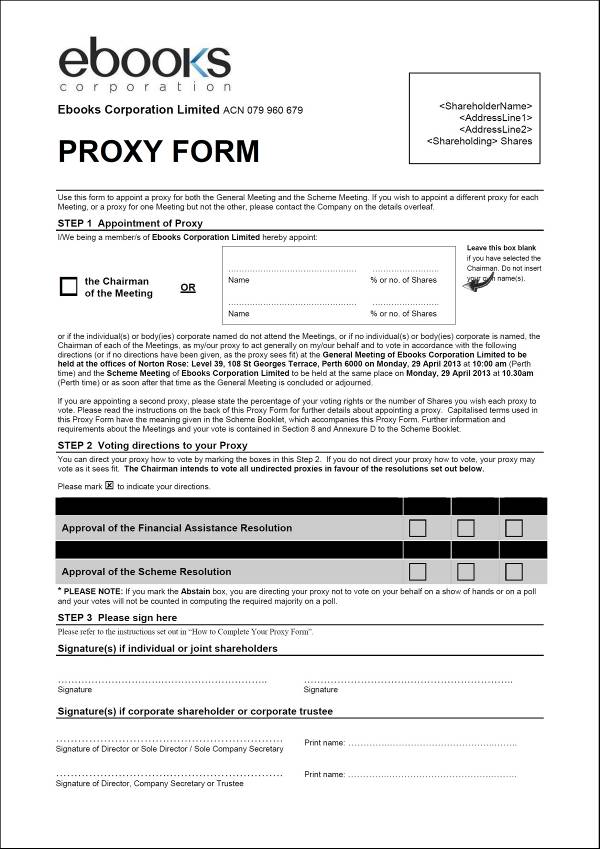

1. Pursuant to subsection 411(1) of the Corporations Act 2001 (Act) the Plaintiff, Ebooks Corporation Limited (Ebooks), convene a meeting (Scheme Meeting) of its shareholders (Ebooks Shareholders) for the purpose of considering, and if thought fit, agreeing (with or without modification) to a scheme of arrangement between Ebooks and the Ebooks Shareholders (Scheme) substantially in the form contained in the explanatory statement in relation to the Scheme at Exhibit 1 (Scheme Booklet), which is approved as the explanatory statement required by section 412(1)(a) of the Act.

2. The Scheme Meeting be held on 29 April 2013 at 10:00am at the offices of Norton Rose, Level 39, 108 St Georges Terrace, Perth.

3. Kevin Shaun Gibson or failing him, Stephen James Cole act as Chairperson of the Scheme Meeting.

4. The Scheme Meeting be convened by sending to each Ebooks Shareholder by 5:00pm on 5 April 2013 by ordinary pre-paid post and, in respect of any shareholder who has as their registered address in the Plantiff’s register of members, an address outside of Australia, by pre-paid airmail post or air courier:

(a) a document substantially in the form of the Scheme Booklet, which contains among other things the notices of the general meeting (General Meeting) at the Scheme Meeting (which is to take place immediately after the General Meeting) at Annexures C and D of the Scheme Booklet;

(b) a proxy form in respect of the General Meeting and the Scheme Meeting substantially in the form of Annexure A to this Order;

(c) a request form in respect of the Ebooks Shareholders’ (other than Ebooks Shareholders resident outside of Australia or the United Kingdom) election to receive their scheme consideration as a mixture of cash and shares in Ebooks.com Limited (currently a wholly owned subsidiary of Ebooks); and

(d) two return addressed envelopes, reply paid to facilitate the return of the proxy forms and the request form referred to in paragraphs (a) and (b) of this Order.

5. The Chairperson appointed to the Scheme Meeting have power to adjourn the Scheme Meeting in his absolute discretion.

6. For the purposes of voting at the Scheme Meeting and the General Meeting, shares in the Plaintiff will be taken to be held by the persons who appear as the registered holders of the shares in the Plaintiff’s register of members as at 10:00am on 27 April 2013.

7. All voting at the Scheme Meeting be by poll as declared by the Chairperson, except for procedural motions.

8. Pursuant to section 411(1) of the Act, the Scheme Booklet be approved for distribution to Ebooks Shareholders.

9. Other than regulation 5.6.13 of the Corporations Regulations 2001 (Cth), regulations 5.6.11 to 5.6.36A of the Corporations Regulations shall not apply to the Scheme Meeting.

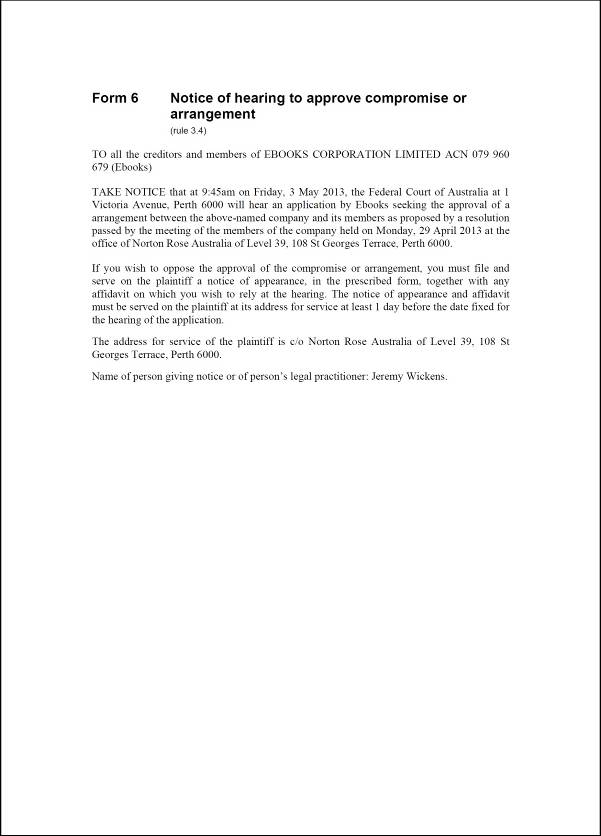

10. Notice of the hearing of an application pursuant to section 411(4)(b) of the Act for orders approving the Scheme be published by an advertisement substantially in the form of Annexure “B” to this order, such advertisement to be published on or before 27 April 2013 on the Australian Securities and Investments Commission website, and that Ebooks otherwise be exempted from compliance with rule 3.4 of the Rules.

11. The Originating Process filed 6 March 2013 be adjourned to 3 May 2013 at 9:45am.

12. There be liberty to apply.

Date that entry is stamped:

Deputy District Registrar

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

Annexure A

Annexure B

|

WESTERN AUSTRALIA DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

WAD 63 of 2013 |

IN THE MATTER OF EBOOKS CORPORATION LIMITED

|

EBOOKS CORPORATION LIMITED (ACN 079 690 679) Plaintiff | |

|

JUDGE: |

BARKER J |

|

DATE: |

2 APRIL 2013 |

|

PLACE: |

PERTH |

REASONS FOR JUDGMENT

OVERVIEW

1 On 2 April 2013, the Court made an order under s 411 of the Corporations Act 2001 (Cth) (Act) convening a first meeting of shareholders of the plaintiff, Ebooks Corporation Limited (Ebooks), for the purpose of considering a proposed scheme of arrangement between Ebooks and the holders of ordinary shares issued in Ebooks in relation to the transfer of all of the shares of the Ebooks shareholders to ProQuest Australia Pty Ltd (ACN 161 699 743) (PQA).

2 These are short reasons for the making of the order.

proposed scheme

3 Stephen James Cole, managing director of Ebooks, by affidavit provided background to the business of Ebooks and the circumstances in which the scheme of arrangement is proposed.

4 Ebooks was incorporated in the State of Western Australia on 4 September 1997.

5 Ebooks is an unlisted public company involved in the sale and distribution of ebooks throughout the world. It has established businesses at three points in the digital book supply chain: library, technical services and retail. Ebooks owns technologies for receiving, processing, managing and securely delivering digital books in multiple formats from hundreds of publishers.

6 The board of directors of Ebooks comprises three directors: Kevin Gibson, Trudy Cole and Mr Cole.

7 The issued capital of Ebooks comprises 14,727 ordinary shares and 1,772 options. Ebooks has 96 shareholders, 19 of whom are located outside Australia. Ebooks has nine option holders, four of whom are located outside Australia.

8 Ebooks shareholders initially contributed approximately a nominal amount of share capital at incorporation and have since contributed a total of $6,419, 237 in share capital.

9 Mr Cole says there is no secondary market for Ebooks shares and, apart from the proposed scheme, no generally applicable opportunity for Ebooks shareholders to exit their shareholding in Ebooks.

10 Since incorporation the only dividends Ebooks has paid to its shareholders are a $29 per share dividend in February 2011, comprising a total of $488,621.

11 Since its incorporation Ebooks has not returned capital to shareholders apart from a selective buy back in July 2012 for $730.59 per share in respect of 2,122 shares, and a return of capital to shareholders in February 2010 totalling $600,000.

12 While Ebooks returned a dividend of $29 per share to shareholders in February 2011, its profits in recent years were as follows:

Year ended 30 June 2011, $202,810 (audited).

Year ended 30 June 2012, $1,179,083 (audited).

Year ended 31 December 2012, $206,258 (unaudited but reviewed).

13 Three directors of Ebooks hold 50.97% of its shares and the remaining shares are held by 93 other members, including employees of Ebooks.

14 PQA was incorporated on 18 December 2012. It is wholly owned by ProQuest LLC (ProQuest), an unlisted company incorporated in Delaware, USA, with its head office in Michigan. ProQuest carries on business as a provider of digital books to schools, higher education institutions, companies, public libraries and government agencies worldwide.

15 The scheme now proposed results from Ebooks entering into a binding scheme implementation agreement with PQA and ProQuest on 18 January 2013.

16 If the scheme is implemented each Ebooks shareholder will receive approximately US$1,648.78 to US$1,857.24 cash per Ebooks share, or a combination of cash and shares in a subsidiary of Ebooks, called Ebooks.com Limited.

17 The scheme consideration is subject to a working capital adjustment and a portion of the purchase price being placed into an escrow account for a period of 15 months to satisfy certain claims that PQA may have against Ebooks shareholders. As a result Ebooks shareholders may not receive all of the possible cash payments forming part of their consideration on the implementation date, with some of the consideration held back to satisfy working capital shortfall and claims.

18 As the independent expert advises in a report attached to the draft scheme booklet, in anticipation of the scheme Ebooks has been recently split into two divisions:

The Ebook library business and Ebook collections business, which will remain part of Ebooks and be acquired by PQA under the scheme; and

the retail business which has been transferred to Ebooks.com Limited and will be demerged under the scheme.

19 Thus, under the scheme the shareholders have the choice of consideration mentioned above, which is either cash or cash and shares in Ebooks.com Limited.

20 Ebooks.com Limited, at the risk of simplification, would become a entity likely controlled by the present directors of Ebooks but which will not compete with PQA following the completion of the scheme.

21 Ebooks has granted 1,772 options to acquire Ebooks shares, which have variously been granted as employee options and director options. PQA has entered into an option purchase deed with each holder of Ebooks options to purchase their options for cash consideration as set out in the terms of the option purchase deeds to be entered into between PQA and each option holder.

22 PQA’s offers to purchase the options are conditional upon the scheme become effective by 18 July 2013 and the scheme implementation agreement not being terminated prior to the implementation date.

Aspects of the scheme

23 Mr Cole also discloses that on 16 October 2012, ProQuest paid US$500,000 to Ebooks in exchange for the grant of exclusivity until the earlier of the implementation date, termination of the scheme implementation agreement and 18 July 2013.

24 Clause 14.2 of the scheme implementation agreement provides that Ebooks has agreed to pay ProQuest a reimbursement fee of US$300,000 in specified circumstances.

25 Mr Cole says these provisions were inserted as a result of commercial negotiations between the parties. PQA required provisions of that nature to be included and Ebooks was satisfied that the final form was acceptable to it. Mr Cole considers that none of the exclusivity provisions or reimbursement provisions operate against the interests of Ebooks shareholders.

26 Mr Cole provides reasons why he considers the reimbursement fee is reasonable and appropriate:

The reimbursement fee is only paid by Ebooks in particular circumstances;

The reimbursement fee will not be payable by Ebooks simply by reason of a director changing his or her recommendation that the scheme be approved;

The amount is US$300,000 which is a genuine and reasonable pre-estimate of advisory costs, costs of management and directors’ time, out of pocket expenses and reasonable opportunity costs of PQA;

PQA requested provision be made for a reimbursement fee, without which it would not have entered into the scheme implementation agreement;

The amount of the reimbursement fee represents approximately 1% of the aggregate scheme consideration agreed to be paid by PQA to Ebooks shareholders of approximately US$28,750,000;

It seeks to protect the interests of Ebooks shareholders and ensure that should PQA not proceed Ebooks is not out of pocket for the costs expended, a view shared by all other directors.

27 Mr Cole also considers the exclusivity provisions are reasonable and appropriate:

The exclusivity provisions take into account the significant transaction costs of PQA which would be incurred in the event the scheme was not to proceed;

There are fiduciary calve-outs from the “no talk”, “no due diligence”, “notification of approaches” and matching right requirements;

The matching right is only afforded to PQA at the time the board or any director proposes to change or withdraw their recommendation or intention to vote in favour of the scheme and not before;

The matching right, if utilised by PQA, will result in higher scheme consideration for Ebooks shareholders.

28 Mr Cole further explains that at the first meeting the approval of Ebooks shareholders and Ebooks as sole shareholder of Ebooks.com Limited will be sought for the purpose of s 260A of the Act for Ebooks and Ebooks.com Limited to financially assist PQA’s acquisition of shares under the scheme by:

Ebooks transferring all shares it holds in Ebooks.com Limited to PQA;

Ebooks procuring the issue to PQA by Ebooks.com Limited of the balance of the number of shares in Ebooks.com Limited required to be transferred to those Ebooks shareholders who validly elect to receive the cash and share alternative and Ebooks.com Limited issuing those shares.

consideration

29 The Court is satisfied that the scheme is one that may be approved under s 411 of the Act.

30 The level of disclosure to be provided by the draft scheme booklet is satisfactory.

31 An independent expert has provided a report, to be included with the scheme booklet to be given to shareholders, that states the scheme on its face is one that is sufficiently fair and reasonable to be put to members for their approval or rejection.

32 It is not for the Court at this point to exercise commercial judgment in respect of the proposed scheme, but to leave the members to exercise that judgment.

33 All necessary procedural matters required under the Act concerning the calling and conduct of the meeting have been met.

34 The first meeting will be chaired either by the director, Mr Gibson, or, if he is not available, Mr Cole. Each has disclosed the extent of their commitments and obligations to Ebooks, none of which disqualifies them as an appropriate chairperson at the meeting.

35 There is nothing in the exclusivity provisions that, in my opinion, should cause the Court to think that members at the meeting may not fairly consider supporting or rejecting the proposed scheme. I accept the statements made by Mr Cole as to the reasonableness of the exclusivity provisions in the circumstances.

36 I also accept that the reimbursement fee, if it were required to be paid, is not an unreasonable, commercial provision in the circumstances of the scheme.

37 It is also clear that interested shareholders will be able, if they so elect, to take as part consideration shares in the retail business formerly conducted by Ebooks which will now be demerged from Ebooks and operated by Ebooks.com Limited.

38 As noted, an independent expert has concluded that the scheme is both fair and reasonable and in the best interests of the shareholders in the absence of a superior proposal.

39 Ebooks has also engaged a chartered accountant as an investigating accountant to prepare a report on certain pro forma historical financial information on Ebooks.com Limited, for inclusion in the scheme booklet. The chartered accountant has concluded that nothing has come to his attention that causes him to believe that this information does not present fairly the pro forma statement of comprehensive income of Ebooks.com Limited for the six months ended 31 December 2012 and the pro forma statement of financial position as at 31 December 2012 in accordance with applicable requirements.

40 So far as the consideration to be paid to shareholders is concerned, the adjustment provision and the escrow provision do not on their face cause any concern to the Court that should prevent the proposed scheme being considered by shareholders.

41 There is no demonstrated performance risk in relation to the proposed scheme that should prevent the scheme from going forward to the first meeting of shareholders.

42 The Australian Securities and Investments Commission (ASIC) has been given notice of the hearing of the application and has provided a letter indicating that it does not, at this point, propose making any submission in relation to the proposed scheme.

orders

43 In all of these circumstances, appropriate disclosure of any relevant matters having been made on behalf of Ebooks, the Court is satisfied that the orders proposed enabling the convening of the first meeting of shareholders should be made.

|

I certify that the preceding forty-three (43) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Barker. |

Associate: