FEDERAL COURT OF AUSTRALIA

Australian Competition and Consumer Commission v Stott [2013] FCA 88

VICTORIA DISTRICT REGISTRY | |

GENERAL DIVISION | VID 504 of 2012 |

BETWEEN: | AUSTRALIAN COMPETITION AND CONSUMER COMMISSION Applicant

|

AND: | LESLIE FORSYTH STOTT Respondent

|

JUDGE: | MIDDLETON J |

DATE: | 7 FEBRUARY 2013 |

PLACE: | MELBOURNE |

REASONS FOR JUDGMENT

INTRODUCTION

1 On 7 February 2013, I made orders in this proceeding in the form proposed by the parties, granting the relief sought by the Applicant, the Australian Competition and Consumer Commission (ACCC), against the Respondent, Mr Leslie Stott. At that time, I reserved my reasons for judgment. My reasons are as follows.

2 On 18 July 2012, the ACCC commenced this Fast Track proceeding against Mr Stott, seeking:

(a) declarations under s 21 of the Federal Court of Australia Act 1976 (Cth);

(b) injunctions and other orders under ss 80 and 86E of the Trade Practices Act 1974 (Cth) (TPA); and

(c) injunctions and other orders under ss 232 and 248 of Sch 2 of the Competition and Consumer Act 2010 (Cth) (CCA) containing the Australian Consumer Law (ACL).

3 Specifically, the ACCC alleged that:

1. Crimeguard International Security Systems Pty Ltd (CISS) had participated in pyramid selling schemes in contravention of s 65AAC(1) of the TPA and s 44(1) of the ACL;

2. CISS had induced others to participate in a pyramid selling scheme in contravention of s 65AAC(2) of the TPA and s 44(2) of the ACL;

3. CISS had engaged in misleading or deceptive conduct in contravention of s 52 of the TPA and s 18 of the ACL;

4. CISS had made misleading representations about its business activities in contravention of s 59(2) of the TPA and s 37(2) of the ACL; and

5. Mr Stott was liable for CISS’s conduct as a person knowingly concerned in and party to that conduct.

4 The ACCC now does not press its allegations that CISS induced others to participate in a pyramid selling scheme as previously alleged.

5 After attending mediation, the parties were able to agree upon a resolution to this dispute. Pursuant to this agreement, they filed Joint Submissions, a Statement of Agreed Facts (in which was set out the agreed facts considered to be material to the Court’s determination of this proceeding) along with accompanying agreed documents, and minutes of proposed consent orders, by which it was proposed that the Court grant final relief in the way of declarations and injunctions. A copy of the Statement of Agreed Facts is annexed to these reasons (Annexure A).

6 Much of the conduct alleged by the ACCC in its Fast Track Statement has been admitted by Mr Stott. For example, Mr Stott admits that he was knowingly concerned in and party to CISS’s participation in pyramid selling schemes in contravention of s 65AAC(1) of the TPA and s 44(1) of the ACL.

7 Mr Stott further admits that he was knowingly concerned in and party to CISS’s misleading and deceptive conduct in contravention of s 52 of the TPA and s 18 of the ACL.

8 He also admits that he was knowingly concerned in and party to CISS’s misleading representations about its business activities in contravention of s 59(2) of the TPA and s 37(2) of the ACL.

9 The parties submitted that the agreed facts support the necessary findings that CISS engaged in the primary contraventions with which Mr Stott admits he was knowingly concerned. The ACCC did not name CISS as a respondent to this proceeding and does not seek relief against it because since about 22 August 2011, CISS has beens without a director and is now part way through the process of being removed from the register of companies.

10 The parties further submitted that the Court should determine the proceeding on the basis of the agreed facts and joint submissions. I made the orders sought on 7 February 2013.

BACKGROUND

11 At all material times CISS carried on business in trade or commerce in Australia as the owner of the exclusive distribution licence for certain vehicle and home contents etching products (CISS Products).

12 Mr Stott was a director of CISS with involvement in its day-to-day operations. John Medcalf and George Patroungas were also directors of CISS with involvement in its day-to-day operations.

13 The admitted contraventions of the prohibition against participation in pyramid selling schemes relate to:

(a) CISS’s dealings with Christopher Pattas in Victoria from about 10 October 2009 to about 31 October 2009 (CISS Victoria Scheme);

(b) CISS’s dealings with DK Insure Invest Pty Ltd (DK Insure) from about 15 June 2010 to about 4 August 2010 (CISS NSW Scheme); and

(c) the investment opportunities that CISS advertised in the period from 9 February 2008 to 25 June 2011 (CISS Scheme).

14 Mr Stott has also admitted that he is liable for CISS’s contraventions of the prohibition against misleading or deceptive conduct found in s 52 of the TPA and s 18 of the ACL. He has further admitted that he is liable for CISS’s contraventions of the prohibition against false or misleading representations about the profitability of a business found in s 59(2) of the TPA and s 37(2) of the ACL. Those admitted contraventions concern CISS’s representations in advertisements it published promoting the CISS Scheme.

RELEVANT LEGISLATIVE PROVISIONS

Transitional matters

15 The TPA was substantially amended by the Trade Practices Amendment (Australian Consumer Law) Act (No. 2) 2010 (Cth) (TPA Amendment Act No 2).

16 The short title of the TPA is now the Competition and Consumer Act 2010 (Cth): see s 1, which was amended by item 2 of Sch 5 of the TPA Amendment Act No 2.

17 By item 6(1) of Sch 7 of the TPA Amendment Act No 2, the TPA as in force immediately before the commencement of that item (1 January 2011) continues to apply to acts and omissions before that date.

Prohibition against participation in pyramid selling schemes

18 Section 65AAC(1) of the TPA states:

A corporation must not participate in a pyramid selling scheme.

19 The expression “pyramid selling scheme” is defined in s 65AAD(1) of the TPA as “a scheme with both the following characteristics”:

(a) to take part in the scheme, some or all new participants must make a payment (a participation payment) to another participant or participants in the scheme;

(b) the participation payments are entirely or substantially induced by the prospect held out to new participants that they will be entitled to a payment (a recruitment payment) in relation to the introduction to the scheme of further new participants.

20 Section 65AAD(2) of the TPA provides that “a scheme may be a pyramid selling scheme”:

(a) no matter who holds out to new participants the prospect of entitlement to recruitment payments; and

(b) no matter who is to make recruitment payments to new participants; and

(c) no matter who is to make introductions to the scheme of further new participants.

21 Section 65AAD(3) relevantly expands the definition of “pyramid selling scheme”, such that “a scheme may be a pyramid selling scheme even if it has any or all of the following characteristics”:

(a) the participation payments may (or must) be made after the new participants begin to take part in the scheme;

(b) making a participation payment is not the only requirement for taking part in the scheme;

....

(e) the scheme involves the marketing of goods or services (or both).

22 The equivalent provisions of the ACL are stated in substantially the same terms. Section 44 of the ACL relevantly states:

(1) A person must not participate in a pyramid scheme.

...

(3) To participate in a pyramid scheme is:

(a) to establish or promote the scheme (whether alone or together with another person); or

(b) to take part in the scheme in any capacity (whether or not as an employee or agent of a person who establishes or promotes the scheme, or who otherwise takes part in the scheme).

23 The expression “pyramid scheme” is defined in s 45(1) of the ACL as “a scheme with both of the following characteristics”:

(a) to take part in the scheme, some or all new participants must provide, to another participant or participants in the scheme, either of the following (a participation payment):

(i) a financial or non-financial benefit to, or for the benefit of, the other participant or participants;

(ii) a financial or non-financial benefit partly to, or for the benefit of, the other participant or participants and partly to, or for the benefit of, other persons;

(b) the participation payments are entirely or substantially induced by the prospect held out to new participants that they will be entitled, in relation to the introduction to the scheme of further new participants, to be provided with either of the following (a recruitment payment):

(i) a financial or non-financial benefit to, or for the benefit of, new participants;

(ii) a financial or non-financial benefit partly to, or for the benefit of, new participants and partly to, or for the benefit of, other persons.

24 Equivalent provisions to the provisions in s 65AAD(2) and s 65AAD(3) of the TPA which broaden the definition of “pyramid scheme” are found in s 45(3) and s 45(4) of the ACL respectively.

Misleading or deceptive conduct

25 Section 52(1) of the TPA states that:

A corporation shall not, in trade or commerce, engage in conduct that is misleading or deceptive or is likely to mislead or deceive.

26 For the purposes of this proceeding, there is no material difference between s 52 of the TPA and the equivalent provision in the ACL, s 18, which is in substantially the same terms:

A person must not, in trade or commerce, engage in conduct that is misleading or deceptive or is likely to mislead or deceive.

Misleading representations about certain business activities

27 Section 59(2) of the TPA states:

Where a corporation, in trade or commerce, invites, whether by advertisement or otherwise, persons to engage or participate, or to offer or apply to engage or participate, in a business activity requiring the performance by the persons concerned of work, or the investment of moneys by the persons concerned and the performance by them of work associated with the investment, the corporation shall not make, with respect to the profitability or risk or any other material aspect of the business activity, a representation that is false or misleading in a material particular.

28 Again, there is no material difference for the purposes of this proceeding between this and the equivalent provision in the ACL, s 37(2). Section 37(2) provides:

A person must not, in trade or commerce, make a representation that:

(a) is false or misleading in a material particular; and

(b) concerns the profitability, risk or any other material aspect of any business activity:

(i) that the person invites (whether by advertisement or otherwise) other persons to engage or participate in, or to offer or apply to engage or participate in; and

(ii) that requires the performance of work by other persons, or the investment of money by other persons and the performance by them of work associated with the investment.

CONTRAVENTIONS - MR STOTT’S CONDUCT

Contraventions in respect of the CISS Victoria Scheme

29 In summary, the parties agree that the CISS Victoria Scheme had the following characteristics:

(a) an investor (in return for making a substantial payment to CISS) would obtain the title of “State Director” and would incorporate a company with Victorian distribution rights for the CISS Products;

(b) CISS would then advertise for the recruitment of persons to various positions within the Victorian company;

(c) persons recruited to the various positions would be required to make recruitment payments to the “State Director” which were shared with CISS; and

(d) the investor would receive recruitment payments even if no CISS Products were sold, and was substantially induced by the prospect of receiving those payments.

30 The agreed investment costs, position descriptions and payment amounts which relate to the CISS Victoria Scheme were set out in the Statement of Agreed Facts.

31 It is agreed that on 15 October 2009, Mr Pattas purchased the position of Victorian State Director in return for a payment to CISS of $360,000.

32 It is also agreed that CISS subsequently published advertisements in The Age newspaper for the recruitment of a “CEO” position relating to the CISS Victoria Scheme.

33 Mr Stott admits that the CISS Victoria Scheme was a pyramid selling scheme within the meaning of s 64AAD of the TPA. Mr Stott admits that CISS participated in the CISS Victoria Scheme by:

(a) promoting the scheme through advertisements CISS caused to be published in The Age newspaper on 10, 21, 24 and 31 October 2009;

(b) meeting with Mr Pattas at CISS’s offices on 12 October 2009;

(c) preparing and providing Mr Pattas with overview documents relating to the CISS Victoria Scheme; and

(d) entering into and being a party to an agreement regarding the CISS Victoria Scheme, and accepting a payment from Mr Pattas.

34 Mr Stott admits that he was a director of CISS and was involved in its day-to-day operations. He further admits that he was knowingly concerned in and party to CISS’s contravention of s 65AAC(1) of the TPA within the meaning of s 80(1)(e) of the TPA by his involvement in:

(a) writing and authorising the advertisements, overview document, and agreement referred to above;

(b) attending the meeting referred to above;

(c) providing Mr Pattas with the overview documents;

(d) orally describing the CISS Victoria Scheme and offering Mr Pattas the opportunity to participate in the CISS Victoria Scheme;

(e) acting as a signatory for CISS in the CISS Victoria Scheme; and

(f) issuing a receipt to CISS Victoria on behalf of CISS.

Contraventions in respect of the CISS NSW Scheme

35 In summary, the parties agree that the CISS NSW Scheme had the following characteristics:

(a) David Burman, director of DK Insure, would (in return for making a substantial payment to CISS) obtain the title of “State Director” for NSW, and DK Insure would obtain NSW distribution rights for the CISS Products;

(b) CISS and DK Insure would then recruit “Regional Directors” who would in turn recruit “Service Agents”;

(c) persons recruited to the various positions in the CISS NSW Scheme would be required to make recruitment payments to DK Insure which were shared with CISS; and

(d) DK Insure would receive recruitment payments even if no CISS Products were sold, and was substantially induced by the prospect of receiving those payments.

36 The agreed investment costs, position descriptions and payment amounts which relate to the CISS NSW Scheme are set out in the Statement of Agreed Facts.

37 It is agreed that on or about 15 June 2010, DK Insure paid $200,000 to CISS pursuant to the CISS NSW Scheme.

38 Mr Stott admits that the CISS NSW Scheme was a pyramid selling scheme within the meaning of s 64AAD of the TPA. Mr Stott admits that CISS participated in the CISS NSW Scheme by:

(a) preparing overview documents relating to the CISS NSW Scheme; and

(b) entering into and being a party to an agreement regarding the CISS NSW Scheme and accepting a payment from DK Insure.

39 Mr Stott admits that he was a director of CISS with involvement in its day-to-day operations. He further admits that he was knowingly concerned in and party to CISS’s contravention of 65AAC(1) of the TPA within the meaning of s 80(1)(e) of the TPA by his involvement in:

(a) writing and authorising the overview document, and agreement referred to above; and

(b) acting as a signatory for CISS in relation to the CISS NSW Scheme.

Contraventions in respect of the CISS Scheme

40 The parties agree that CISS promoted the CISS Scheme from about 9 February 2008 to at least 11 December 2010. In summary, it is agreed that the CISS Scheme had the following characteristics:

(a) an investor (in return for making a substantial payment to CISS) would obtain the title of “State Director” for a particular state and the investor and/or a company of which they were a director would obtain distribution rights for the CISS Products in that state;

(b) CISS and/or the State Director would then advertise for the recruitment of persons to various positions within the company;

(c) persons recruited to the various positions would be required to make recruitment payments to the “State Director” which were shared with CISS; and

(d) the investor would receive recruitment payments even if no CISS Products were sold, and was substantially induced by the prospect of receiving those payments.

41 The investment costs, payment amounts (which varied over time and between States) and position descriptions which relate to the CISS Scheme are set out in the Statement of Agreed Facts.

42 It is agreed that CISS received the following payments in respect of the CISS Scheme:

(a) on 18 March 2009, S Zambuni paid CISS $400,000;

(b) on 12 February 2009, Laurie Fisher / UBET Investments Pty Ltd paid CISS $325,000; and

(c) on 19 January 2009 Mark Atkinson / KMS ANS Pty Ltd paid CISS $148,000 on 19 January 2009.

43 Mr Stott admits that the CISS Scheme was a pyramid selling scheme within the meaning of s 65AAD of the TPA (in respect of the scheme prior to 1 January 2011) and a pyramid scheme within the meaning of s 45 of the ACL (in respect of the scheme from 1 January 2011). Mr Stott admits that CISS participated in the CISS Scheme by:

(a) promoting the scheme through advertisements CISS caused to be published in newspapers around Australia; and

(b) receiving money from individuals and/or corporations as previously set out .

44 Mr Stott admits that he was a director of CISS with involvement with its day-to-day operations. He further admits that he was knowingly concerned in and party to CISS’s contravention of 65AAC(1) of the TPA within the meaning of s 80(1)(e) of the TPA and CISS’s contravention of s 44(1) of the ACL within the meaning of s 232(1)(e) of the ACL by his involvement in writing and authorising the advertisements referred to above.

Contraventions in respect of the CISS advertising

Misleading or deceptive conduct

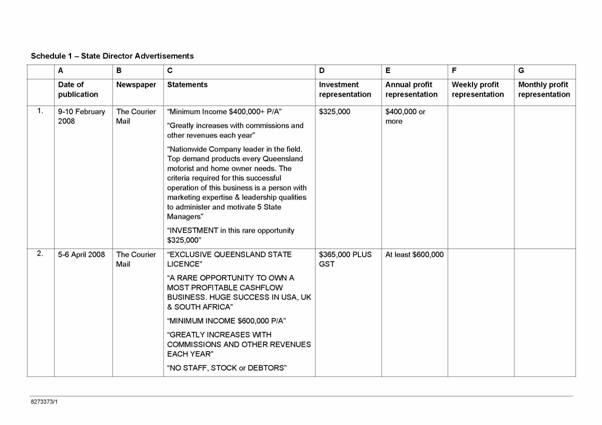

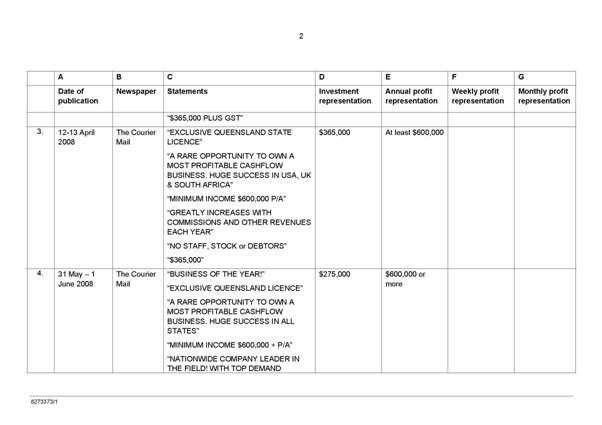

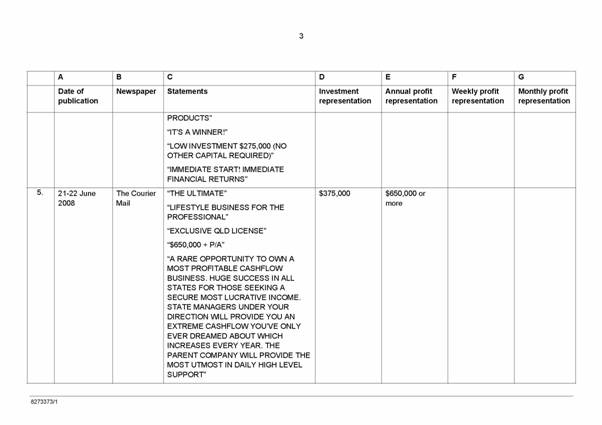

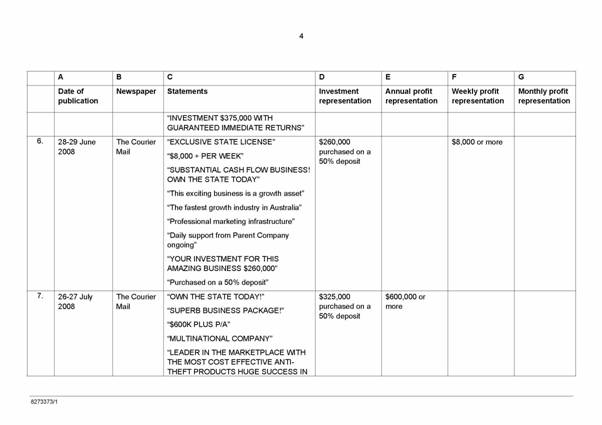

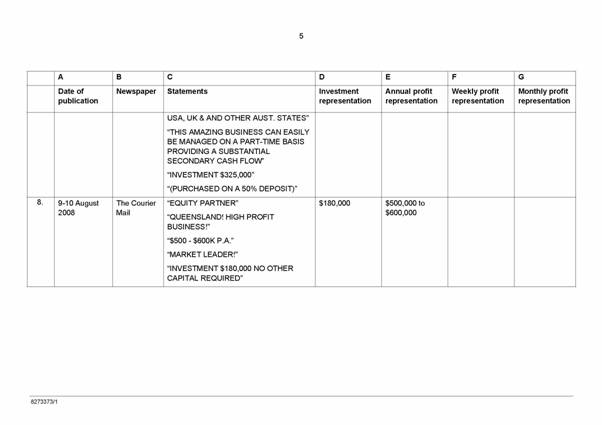

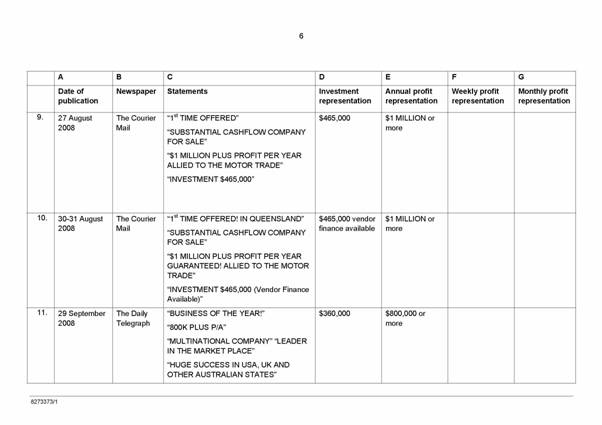

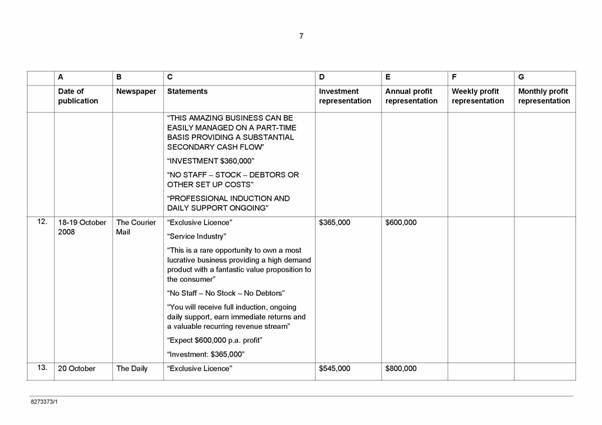

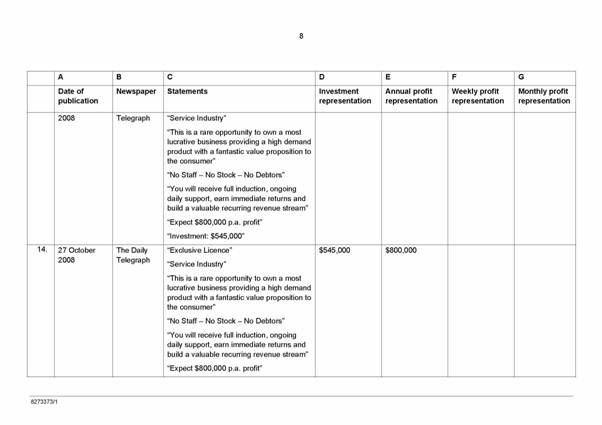

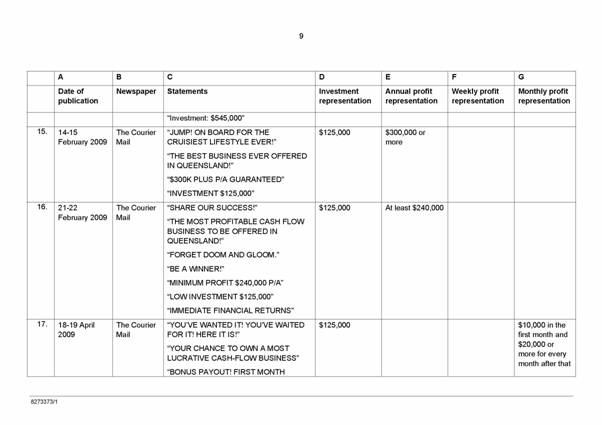

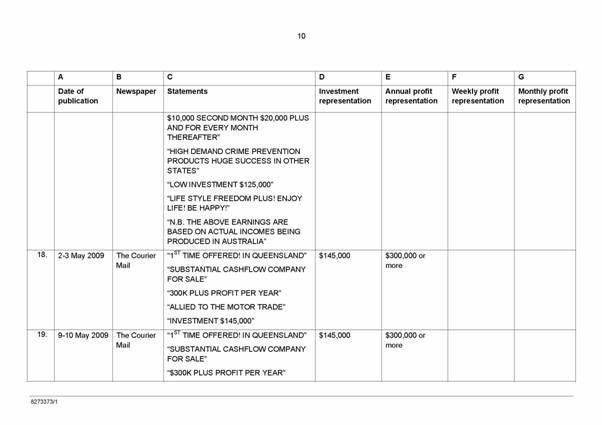

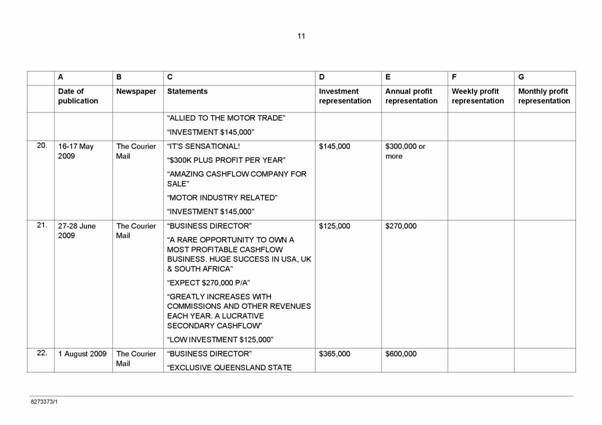

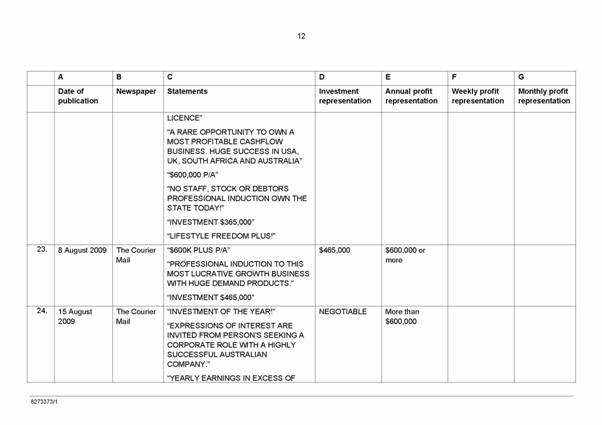

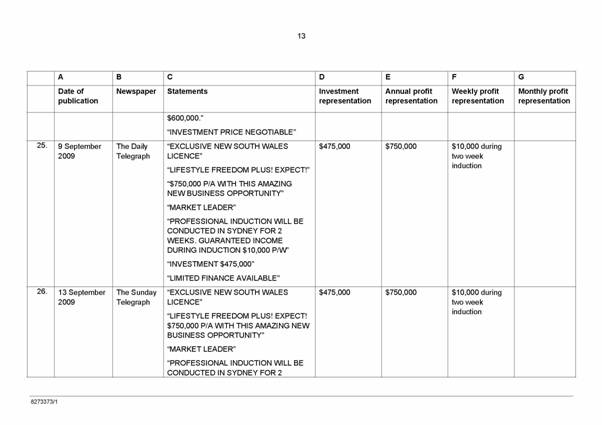

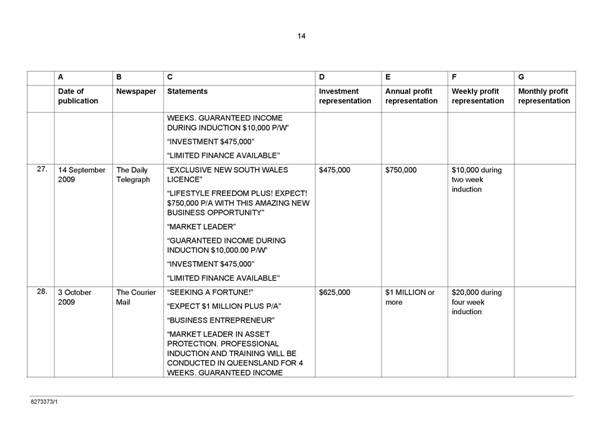

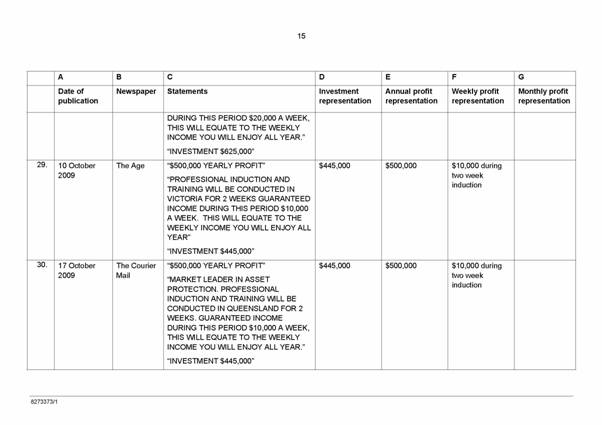

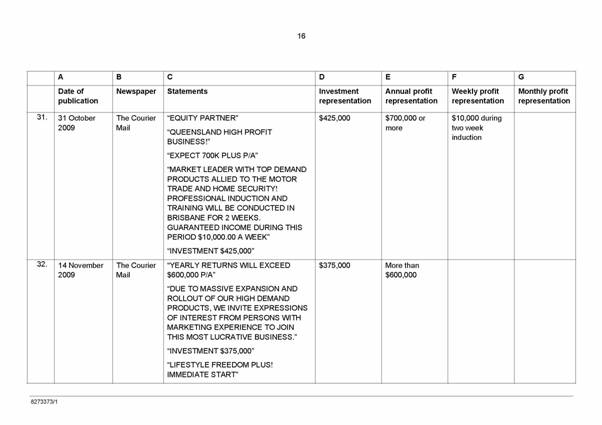

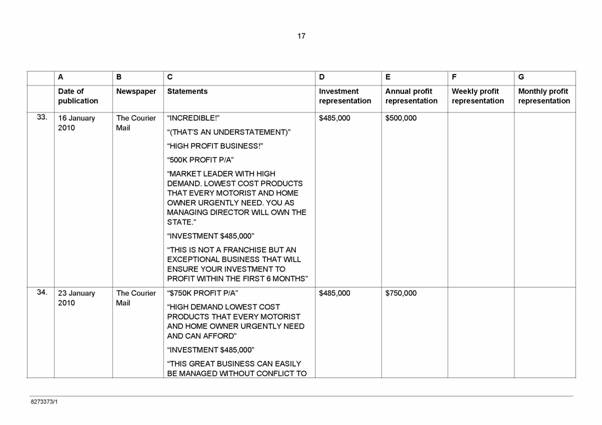

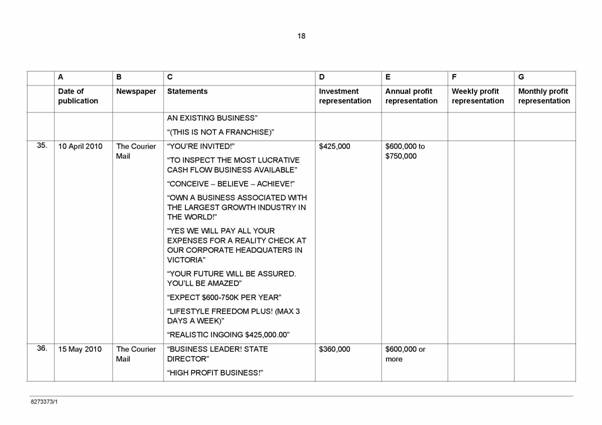

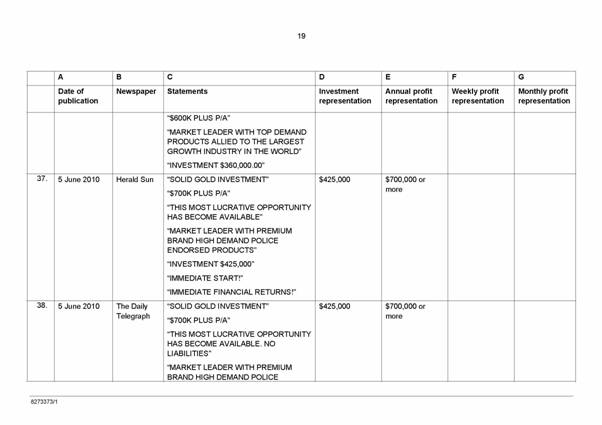

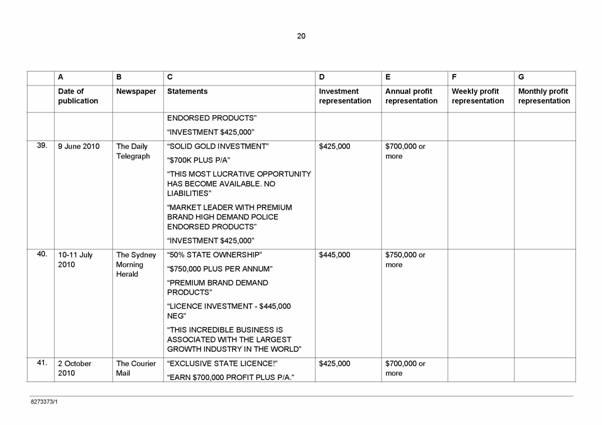

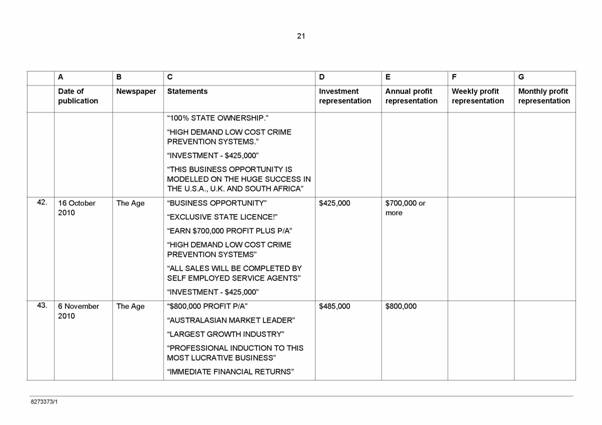

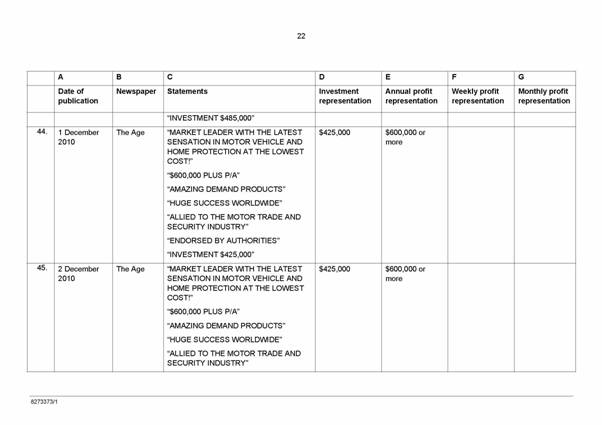

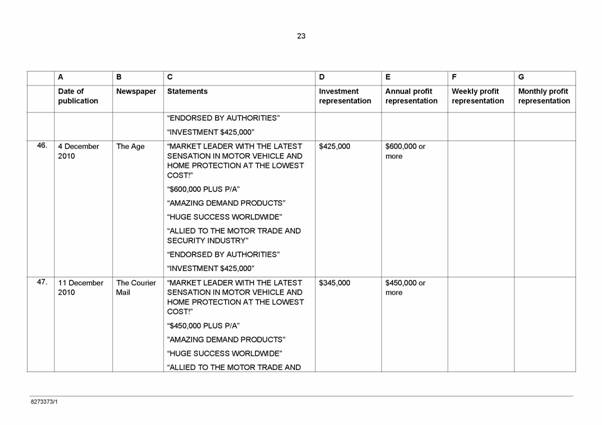

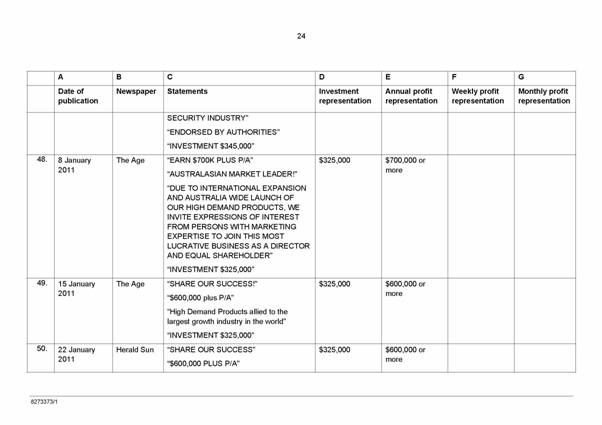

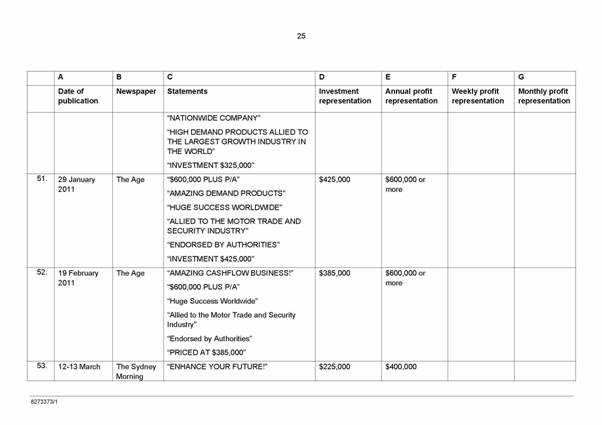

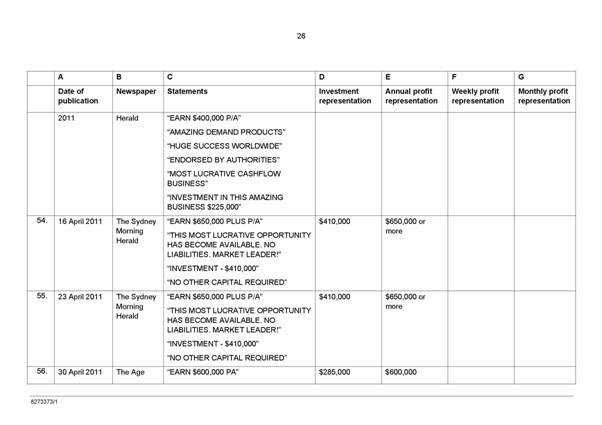

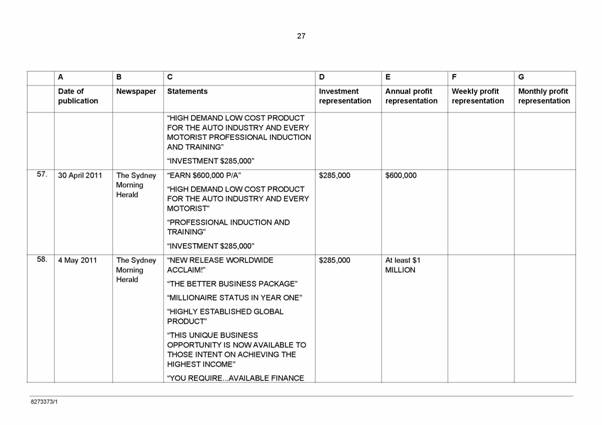

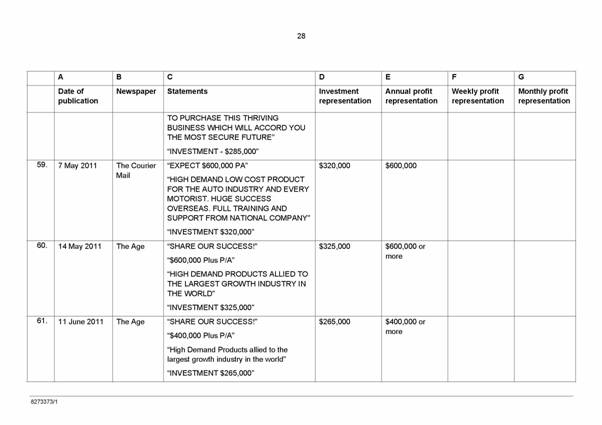

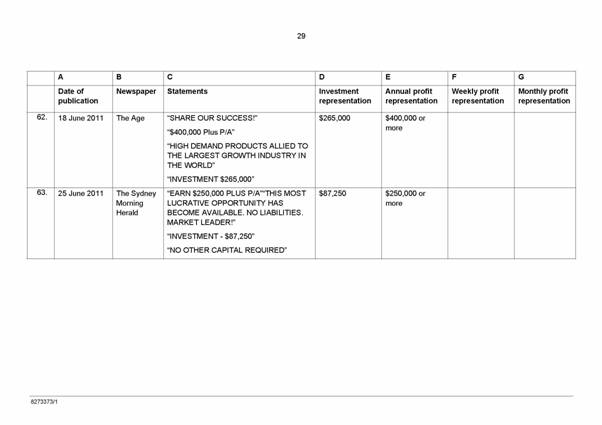

45 It is agreed that CISS published, or caused to be published, each of the State Director Advertisements that are set out in Schedule 1 to the Statement of Agreed Facts. These State Director Advertisements appeared in various newspapers in Queensland, New South Wales and Victoria in the period from about 28 June 2008 to 25 June 2011. The State Director Advertisements contained a number of statements such as the following (which appeared in a State Director Advertisement published in The Age newspaper on 14 May 2011):

“SHARE OUR SUCCESS!”

“$600,000 Plus P/A”

“HIGH DEMAND PRODUCTS ALLIED TO THE LARGEST GROWTH INDUSTRY IN THE WORLD”

“INVESTMENT $325,000”

46 It is agreed that by publishing statements such as these, CISS made representations to the effect that there was a reasonable basis for potential investors to expect that they would receive a return on their investment comprising a weekly, monthly, and/or annual income amount (Profit Representations). The investment amounts and expected investment return amounts are set out in the Statement of Agreed Facts. In the example set out above, it is agreed that CISS represented to potential investors that they would receive an annual income of $600,000 or more in return for their investment of $325,000.

47 It is agreed that at the time CISS published, or caused to be published, each of the State Director Advertisements:

(a) CISS did not have a reasonable basis for making the State Director Representations; and

(b) there was no realistic prospect that the advertised investment would generate the amounts specified as set out in the Statement of Agreed Facts.

48 This is because it is agreed that, at the time CISS published each of the State Director Advertisements:

(c) no investor who had participated in a CISS Scheme had ever received an investment return equivalent to any amount referred to in the Profit Representations as a result of their participation in the CISS Scheme;

(d) CISS had no record of the profits any investor had received as a result of their participation in the CISS Scheme;

(e) there was not an established market in Australia for the CISS Products; and

(f) CISS premised the projected profits on all proposed positions within the CISS Scheme being purchased and paid for when in fact, there had never been a time at which CISS had recruited and received payment for all positions within a CISS Scheme.

49 Mr Stott admits that by publishing or causing to be published the State Director Advertisements, CISS engaged in misleading or deceptive conduct, or conduct that was likely to mislead or deceive, in contravention of s 52 of the TPA (which applies to the State Director Advertisements published prior to 1 January 2011) and s 18 of the ACL (which applies to the State Director Advertisements published after 1 January 2011).

50 Mr Stott admits that he was a director with day-to-day involvement in CISS’s operations and that he was involved in writing and authorising the State Director Advertisements. He admits that he was knowingly concerned in and party to CISS’s contravention of s 52 of the TPA within the meaning of s 80(1)(e) of the TPA (in respect of the State Director Advertisements published prior to 1 January 2011), and that he was knowingly concerned in and party to CISS’s contravention of s 18 of the ACL within the meaning of s 232(1)(e) of the ACL (in respect of the State Director Advertisements published after 1 January 2011).

Misleading representations about business activities

51 It is further agreed that by publishing or causing to be published the State Director Advertisements containing the statements referred to above, CISS invited potential investors to make an investment in the amount set out in the Statement of Agreed Facts, and to perform work associated with that investment. In the example provided above, it is agreed that CISS, by that advertisement, invited potential investors to make an investment of $325,000 and to perform work associated with that investment.

52 It is agreed that each of the Profit Representations was a representation as to:

(a) the profitability or risk of a material aspect of the advertised investment opportunity; and

(b) a future matter for the purposes of s 51A of the TPA and s 4 of the ACL.

53 Mr Stott admits that there was no basis for the Profit Representations and that there was no realistic prospect that the advertised investment would generate the profit CISS advertised. Mr Stott admits that CISS accordingly contravened s 59(2) of the TPA and s 37(2) of the ACL by making the State Director Representations, which he admits were false and misleading representations as to the profitability of CISS’s business.

54 Further, Mr Stott admits that by his involvement in the day-to-day operations of CISS (and more particularly, his involvement in writing and authorising the State Director Advertisements), he was knowingly concerned in and party to CISS’s contravention of s 59(2) of the TPA within the meaning of s 80(1)(e) of the TPA. He further admits that he was knowingly concerned in and party to CISS’s contravention of s 37(2) of the ACL within the meaning of s 232(1)(e) of the ACL.

RELIEF BY CONSENT

55 It is appropriate to make some comments about the Court’s task in cases of this nature, and the granting of relief by consent.

56 The Court is entitled to treat the Mr Stott’s consent as involving an admission of all facts necessary or appropriate to the granting of the relief sought: Thomson Australian Holdings Pty Ltd v TPC (1981) 148 CLR 150 at 164 per Gibbs CJ, Stephen, Mason and Wilson JJ. For the avoidance of doubt, I note that the Statement of Agreed Facts and Joint Submissions filed by the parties provided comprehensive bases for the relief sought.

57 There is a well-recognised public interest in the settlement of cases under the TPA (and by extension, the relevant legislation in its present form, the ACL): NW Frozen Foods Pty Ltd v ACCC (1996) 71 FCR 285 at 291.

58 The Court will not refuse to give effect to settlements under the TPA or the ACL which are within the Court’s jurisdiction and are otherwise not inappropriate. As Lee J explained in ACCC v Target Australia Pty Ltd (2001) ATPR 41-840; [2001] FCA 1326 at [24]:

In conclusion, I mention the role of the Court in making consent orders in matters under the Act. It is the Court's duty in receiving consent orders in any matter to scrutinise such orders as to their appropriateness. However, after being satisfied as to the appropriateness of the orders, the Court should be slow to impede final settlement of such matters, particularly those involving public interest considerations. Moreover, the public has an interest in the mutual resolution of litigation, and subject to the foregoing the Court should be careful not to refuse to make orders simply because the orders may have been different had it been the Court's task to formulate them.

Declarations

59 The declarations made on 7 February 2013 are based on s 21 of the Federal Court of Australia Act 1976 (Cth). In Forster v Jododex Australia Pty Ltd (1972) 127 CLR 421 at 437-438, Gibbs J held that three threshold requirements should be satisfied before a declaration will ordinarily be made (adopting the comments of Lord Dunedin in Russian Commercial and Industrial Bank v British Bank for Foreign Trade Ltd [1921] 2 AC 438):

(a) the question must be a real and not a hypothetical or theoretical one;

(b) the Applicant must have a real interest in raising it; and

(c) there must be a proper contradictor.

60 Each of these requirements is satisfied in this case:

(a) the proposed declarations relate to conduct that contravenes the TPA or ACL and the matters in issue have been identified and particularised by the parties;

(b) it is in the public interest for the ACCC to seek to have the declarations made and for the declarations to be made; and

(c) although Mr Stott does not oppose the making of declarations, he has an interest to oppose declaratory relief and is therefore a proper contradictor.

61 The parties provided ample support for the declarations sought in the form of the Statement of Agreed Facts and agreed documents. Accordingly, it is appropriate for me to make those declarations.

Injunctions

62 Prior to the TPA Amendment Act No 2, s 80 of the TPA provided for the Court to grant an injunction when it was satisfied that a person had engaged in conduct that contravened (among other things) Pt V of the TPA. The equivalent power is conferred on the Court in respect of contraventions of the ACL by s 232 of the ACL. Under these provisions, the Court has power to grant an injunction against a person who is ‘in any way, directly or indirectly, knowingly concerned in, or party to’ a relevant contravention of the TPA or ACL.

63 Pursuant to item 7(2) of Sched 7 of the TPA Amendment Act No 2, any proceedings for an injunction under s 80 of the TPA that were in force at 31 December 2010 are taken, after that date, to be proceedings for an injunction under s 232 of the ACL.

64 In ICI Australia Operations Pty Limited v Trade Practices Commission (1992) 38 FCR 248 at 255, Lockhart J, with whom French J agreed, stated:

Section 80 is essentially a public interest provision. Conduct of the kind proscribed by both Pts lV and V may be detrimental to the public interest because many persons can be affected and considerable loss or damage may be sustained by them.

65 The granting of injunctions is appropriate to deter a repetition of the contraventions by attaching the sanctions available for contempt of court to any repetition of the contraventions (see eg ICI Australia (1992) 38 FCR 248 per French J at 268). However, the Court has power to grant an injunction against a person whether or not there is a likelihood of the conduct being repeated.

66 As French J (as he then was) has observed, the discretion under s 80 “is as wide as the phrase ‘as the court determines to be appropriate’”: OD Transport Pty Ltd v WA Government Railways Commission (1987) 13 FCR 500 at 508.

67 But broad as the Court’s power is in this respect, it is subject to at least three limitations, identified in ACCC v Z-Tek Computer Pty Ltd (1997) 78 FCR 197 at 203-4:

(a) The power is confined by reference to the scope and purpose of the legislation. Consequently, the relief should be designed to prevent a repetition of the conduct for which the relief is sought.

(b) Because the jurisdiction to grant an injunction is enlivened by an alleged or actual contravention there needs to be a sufficient nexus or relationship between the contravention and the injunction granted.

(c) The Federal Court exercises judicial power under Ch III of the Constitution in a ‘matter’. Consequently, the injunction must be related to the case or controversy.

68 The parties submitted that the injunction they seek in this proceeding is within the Court’s power because it:

(a) is designed to prevent Mr Stott from having any further involvement in a pyramid selling scheme or the making of misleading representations similar to those that are the subject of this proceeding;

(b) is expressed in terms that are tightly tied to the terms in which Mr Stott has admitted his contraventions of the TPA and ACL; and

(c) arises in the circumstances of this Fast Track proceeding appropriately issued in the Federal Court.

69 The parties also submitted that the proposed injunction, which is intended to have a permanent application, is appropriate in view of the admitted contraventions which were wilful, took place over four years, across numerous Australian States and which involved flagrant misrepresentations designed to lure participants to CISS’s various pyramid selling schemes. Mr Stott’s agreement to be bound by the proposed injunction also weighs in favour of the Court granting it. I accept these submissions.

Disqualification order

70 Section 86E(1B) – which permits the Court to make an order disqualifying a person from managing corporations for contraventions of Pt V of the TPA for a period the Court considers appropriate – was inserted into the TPA by Trade Practices Amendment (Australian Consumer Law) Act (No 1) 2010 (Cth) (TPA Amendment Act No 1). These provisions of the TPA Amendment Act No 1 commenced on 15 April 2010. They were subsequently repealed by the TPA Amendment Act No 2. The equivalent power is now conferred on the Court in respect of contraventions of the ACL by s 248 of the ACL.

71 However, s 86E(1B) (as it existed prior to being repealed) continues to authorise the disqualification of a person in respect of conduct occurring on or after 15 April 2010 up to and including 31 December 2010: see items 6 and 7 of Sched 7 of the TPA Amendment Act No 2. Accordingly, the parties submit that in this proceeding (which concerns conduct which pre-dates the application of the TPA Amendment Act No 2 and continued after its commencement), s 86E(1B) of the TPA and s 248 of the ACL both confer power on the Court to grant the disqualification order sought by the parties.

72 The parties submitted that the Court should make an order disqualifying Mr Stott from managing corporations for a period of five years. The Court has the power to make such a disqualification order if it is satisfied that Mr Stott contravened or was involved in a contravention of a provision of Pt V of the TPA (which contains ss 52, 59(2) and 65AAC), or Pt 3-1 of the ACL (which contains ss 37(2) and 44), and that the order is justified. Section 86E(2) of the TPA and s 248(2) of the ACL provide that a Court may have regard to the following matters in determining whether the disqualification is justified:

(a) the person’s conduct in relation to the management, business or property of any corporation; and

(b) any other matters that the Court considers appropriate.

73 The parties agree that the Court should impose an order disqualifying Mr Stott from being involved in the management of corporations until 20 February 2018. The parties submitted the duration of the proposed order – being less than medium range – is justified because the contravening conduct:

(a) involved continued and deliberate conduct in contravention of the TPA and ACL which demonstrated a disregard for the legal obligations of both CISS and Mr Stott over a period of about four years.

(b) reflected a lack of understanding of the proper role of a company director and the duties that are owed to the company, particularly as the conduct involved unsupported representations about CISS’s profitability and the promotion of various pyramid selling schemes.

(c) had the potential to cause significant harm as it involved a prolonged advertising campaign targeted at an audience in numerous Australian States which sought (and on occasion, obtained), through the use of misleading statements, the payment of substantial investment amounts. In addition to false and misleading statements, the contravening conduct involved the promotion of pyramid selling schemes which carry an inherent risk to the economy.

(a) involved the registration of numerous companies for the purpose of implementing pyramid selling schemes, and in this regard, represented a serious misuse of the corporate structure.

74 There is limited authority on the making of an order under s 86E of the TPA. The Court has previously exercised this power in ACCC v Halkalia Pty Ltd (No 2) [2012] FCA 535. However, there is a useful body of case law which has developed in relation to disqualifying officers under ss 206C and 206E of the Corporations Act 2001 (Cth). Section 206C is in identical terms to s 86E of the TPA.

75 Justice Santow in ASIC v Adler (2002) 42 ACSR 80 surveyed the case law on the granting of disqualification orders under the Corporations Act 2001 (Cth), and distilled from it a number of key propositions. While his Honour’s observations regarding the nature of disqualification orders being purely protective and not punitive were rejected by the High Court in Rich v ASIC (2004) 220 CLR 129, the remaining principles provide useful assistance to Courts in considering applications for orders under s 86E(1B) of the TPA and s 248(2) of the ACL (see ACCC v Halkalia Pty Ltd (No 2) [2012] FCA 535 at [111]). As the parties in this proceeding have agreed on the terms of the orders to be made under s 86E(1B) of the TPA and s 248(2) of the ACL, it is sufficient that I record that, having had regard to the principles identified by Santow J in ASIC v Adler (2002) 42 ACSR 80, I am satisfied that a five-year disqualification order is appropriate in the circumstances of this case. My reasons are as follows.

76 Mr Stott has cooperated with the ACCC by reaching an agreed settlement to this proceeding. His cooperation has spared the ACCC and the Court from committing resources to the preparation and running of a trial. The parties also submitted that Mr Stott has no discernable intention to hold a future position as a manager of a company. Mr Stott submitted that CISS made partial and substantial refunds of the payments it received from a number of “State Directors”. The ACCC has not been able to confirm these repayments. However, both parties acknowledged that on 21 December 2009, CISS refunded $20,000 of the payment it received from Mr Pattas.

77 The Court may (under s 86E(2) of the TPA and s 248(2) of the ACL) also have regard to Mr Stott’s involvement in companies other than CISS in determining whether to grant the proposed disqualification order against him. In this regard it is submitted that Mr Stott has held directorships in seven different companies since 3 December 1998. All of these companies are now either deregistered or in the process of being struck off the register of companies. Many of those companies shared a similar name to CISS, for example, “Crimeguard (Australia) Pty Ltd”, which was registered in 2004. The parties submitted that this corporate history further supports the granting of the proposed disqualification order against Mr Stott.

78 Mr Stott is currently an undischarged bankrupt and therefore unable to manage a corporation. However, this does not militate against there being utility in the proposed disqualification order. Mr Stott will immediately be able to manage companies after his bankruptcy is discharged. While it is accepted that Mr Stott has no discernable intention or ability to discharge his bankruptcy in the near future, he will be automatically discharged from bankruptcy on 20 September 2014 (three years from the date on which he filed his statement of affairs). In the only case in which a disqualification order has previously been made under s 86E(1B) of the TPA, ACCC v Halkalia Pty Ltd (No 2) [2012] FCA 535, this Court made a 15-year disqualification order against a bankrupt respondent. The proposed disqualification order in this case will have effect for more than three years after Mr Stott is automatically discharged from his bankruptcy. This period of time is appropriate in the circumstances of Mr Stott, particularly in light of his cooperation.

COSTS

79 I note that in a case such as this, the ACCC is entitled to (and would usually seek) a contribution to its costs from the respondent. However, the ACCC acknowledges that Mr Stott has, through his agreement to the proposed relief, ensured that he will not be in any way involved in similar contraventions in the future. This cooperation has spared the ACCC legal expenses that (as a matter of commercial practicality) it was unlikely to ever recover. In those circumstances, the ACCC does not seek an order requiring Mr Stott to contribute to its costs of the proceeding.

I certify that the preceding seventy-nine (79) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Middleton. |

Associate:

ANNEXURE ‘A’