FEDERAL COURT OF AUSTRALIA

Richards v Macquarie Bank Limited (No 2) [2012] FCA 1403

| QUEENSLAND DISTRICT REGISTRY | |

| GENERAL DIVISION | QUD 590 of 2010 |

| BETWEEN: | TRACEY RICHARDS Applicant |

| AND: | MACQUARIE BANK LIMITED Respondent |

| JUDGE: | REEVES J |

| DATE: | 12 DECEMBER 2012 |

| PLACE: | BRISBANE |

REASONS FOR RULING

Introduction

1 Mrs Richards, the applicant, has sought to tender certain evidence in this trial as tendency evidence. Tendency evidence is covered by s 97 of the Evidence Act 1995 (Cth) (Evidence Act). In broad terms, it is not admissible unless two conditions are met. Section 97(1) provides:

Evidence of the character, reputation or conduct of a person, or a tendency that a person has or had, is not admissible to prove that a person has or had a tendency (whether because of the person’s character or otherwise) to act in a particular way, or to have a particular state of mind unless:

(a) the party seeking to adduce the evidence gave reasonable notice in writing to each other party of the party’s intention to adduce the evidence; and

(b) the court thinks that the evidence will, either by itself or having regard to other evidence adduced or to be adduced by the party seeking to adduce the evidence, have significant probative value.

2 There is no issue that this provision determines the admissibility of the evidence concerned in this instance and nor is there an issue that the notice condition set out in s 97(1)(a) has been compiled with. The only question, therefore, is whether, in the terms of the condition set out in s 97(1)(b), I “think” the evidence will have “significant probative value”.

3 For the reasons that follow, I do not consider that, in the circumstances of this case, the evidence concerned meets this condition. Before setting out my reasons for this conclusion, it is first necessary to describe how this question arose in these proceedings.

Brief factual context

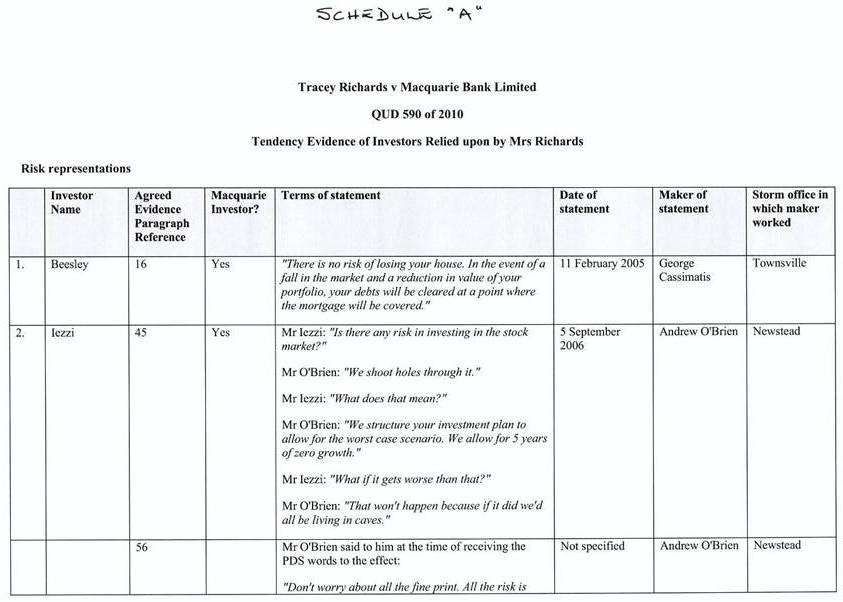

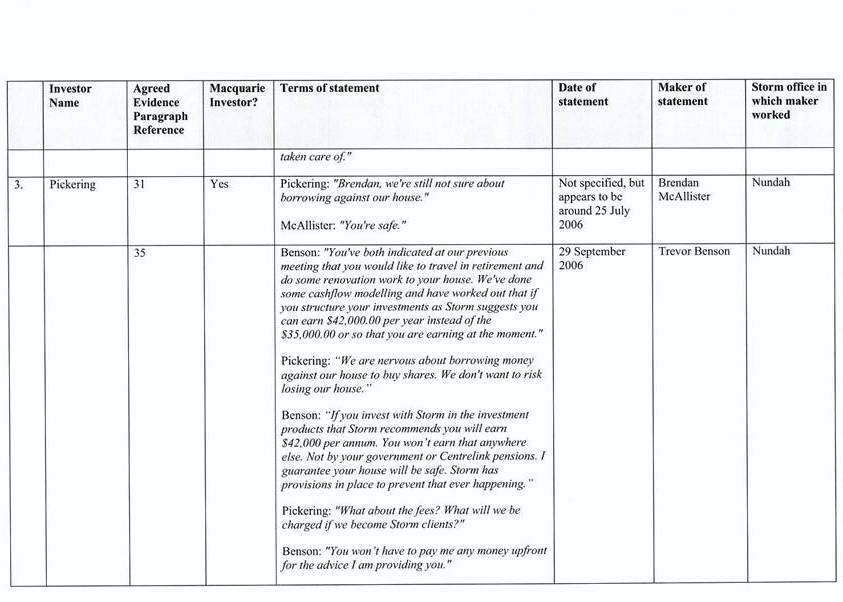

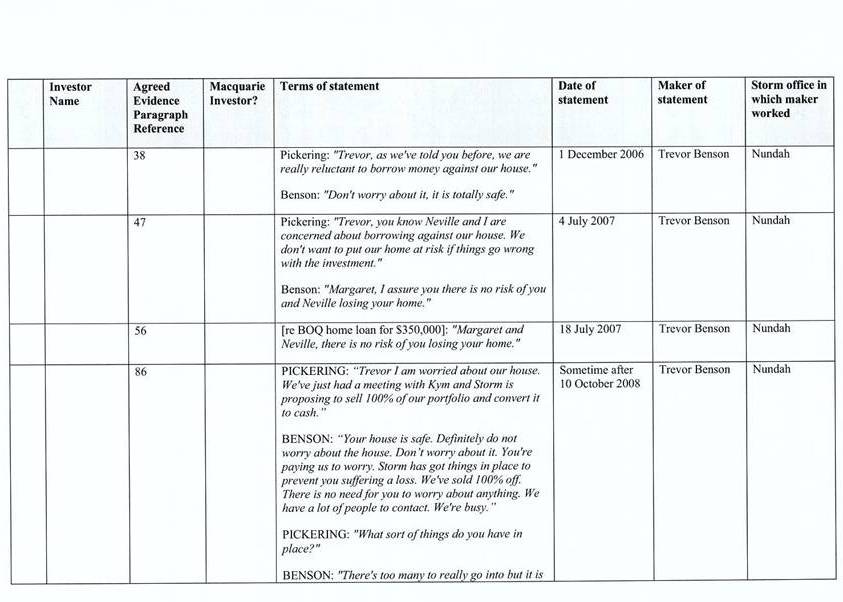

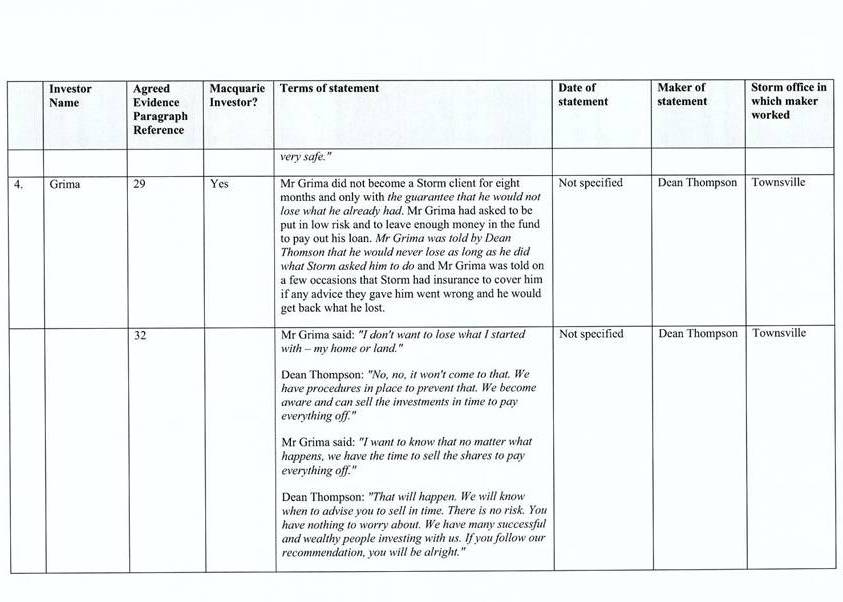

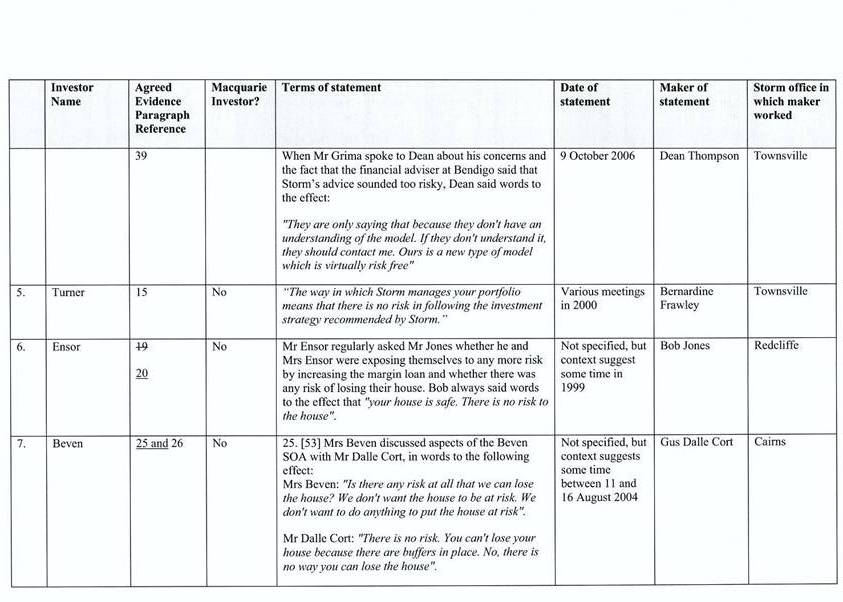

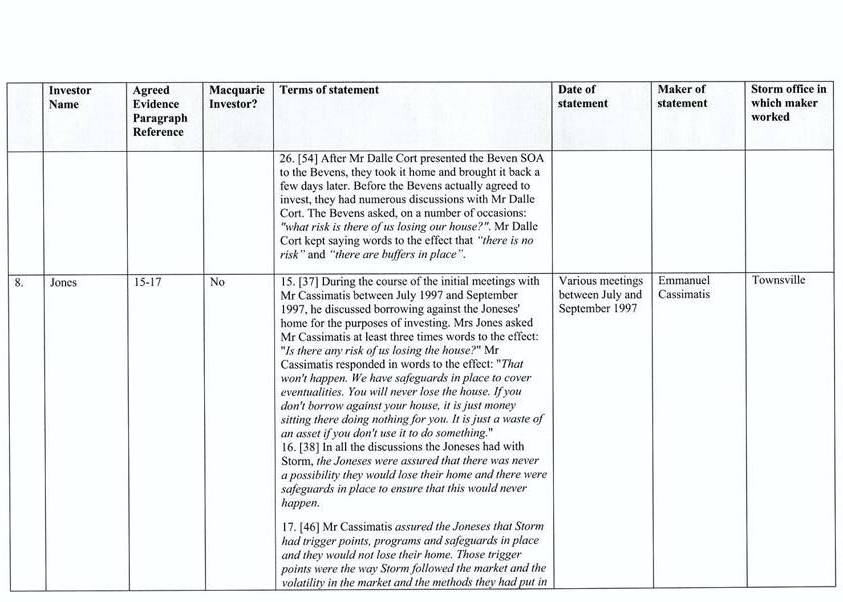

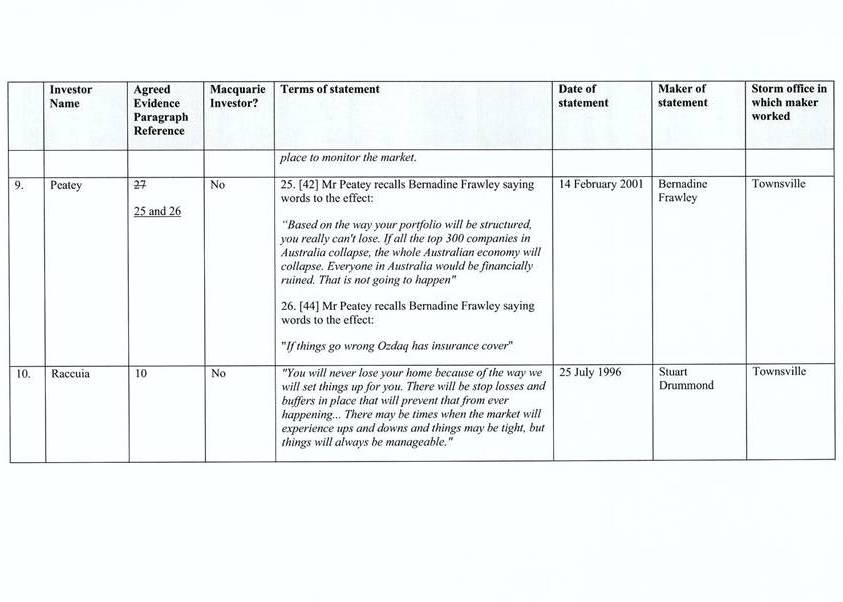

4 Storm Financial Services Limited (Storm) was a company which provided financial advice to customers in North Queensland and various other parts of Australia. It operated as such from the late 1990s until early 2009, when it was placed in liquidation. During this period, Storm developed an approach to investment which involved it advising its customers to access the capital base they had accumulated (usually, but not always, in the equity in their homes) and to leverage, or gear it, by way of a margin loan so that they could then invest the combined sum in the Australian share market using index funds as the investment vehicle.

5 Between 2001 and 2008, Mrs Richards, the applicant in these proceedings, was a customer of Storm. From 2001, when she first became a customer, until some time in early 2005, her financial adviser at Storm was a Ms Nancy Seymour. Thereafter, until late 2008, it was a Mr Stuart Drummond.

6 In their dealings with its customers, Storm required its financial advisers to follow a particular process. During the initial stages of their dealings, that process included completing a detailed document entitled “Confidential Financial Profile” for each customer and, based on that, providing them with a lengthy written statement of advice.

Mrs Richards’ evidence

7 This tendency issue was argued on the basis that Mrs Richards would give evidence that, during her initial dealings with Storm, Ms Seymour took her through her Confidential Financial Profile document and discussed its contents with her. Relative to the risk of her following the Storm investment strategy, Mrs Richards is to give evidence as follows:

I recall reading the sections under the heading “risk/volatility statement” and under the heading “Personal Profile”. Having re-read that section of the document I recall Nancy [Seymour] explaining the difference between “real risk” and “manageable risk”. She told me that ‘manageable risk’ was concerned with volatility in the share market but did not involve any risk to capital over the long term and that “real” risk meant that I could lose some or all of my capital. She told me that provided I had an investment time frame of 5-7 years there was no “real risk” involved in investing in shares, because the share market always goes up over that period.

8 And further:

Don’t worry there really is no risk. If anything goes wrong, it is covered by insurance.

9 In relation to her first meeting with Mr Drummond (after he became her financial adviser), Mrs Richards is to give evidence that she discussed the question of risk with him in the following terms:

I had a number of discussions with Stuart [Drummond] about risk during this meeting. By this time I had misgivings about the quality of Nancy [Seymour]’s advice and I wanted reassurance. I recall at one point asking Stuart whether it was “risky to put all my eggs in one basket” (referring to the share market). I recall Stuart responding in words to the following effect: “Not at all. We invest across the All Ordinaries index so that your investments are diversified across many industries. Over time the index always makes money. When events adversely affect particular industries others will benefit. Diversification is the key. There is no risk.”

The issues of fact as pleaded

10 These statements were taken up in Mrs Richards’ further amended statement of claim where she claimed, among other things, that Storm had made certain representations to her that were misleading or deceptive in contravention of s 52 of the Trade Practices Act 1974 (Cth).

11 The allegations in relation to Ms Seymour were contained in para 72 of that document as follows:

In or about June or July 2001 Storm made the following representations to the Applicant:

(a) Storm would devise an investment strategy for the Applicant which involved no risk of the Applicant losing her Equity Contribution (“First Risk Representation”);

(b) if the investment strategy devised by Storm for the Applicant did involve any risk of capital loss, such losses would be covered by insurance (‘Second Risk Representation”).

Particulars

The representations were made expressly by Nancy Seymour (Storm) during meetings with the Applicant in or around June or July 2001.

(c) Storm would prepare an investment plan for the Applicant which, over the medium to long term, would involve minimal or no risk of capital loss (“Third Risk Representation”).

Particulars

(i) The representation is partly express and partly implied.

(ii) In so far as it was express, it was set out on page 8 of the Confidential Financial Profile completed by Ms Seymour on behalf of the Applicant on 19 June 2001 and signed by the Applicant on that date.

(iii) In so far as it was implied, the representation arises from the text on page 8 of the Confidential Financial Profile and in circumstances in which the Applicant selected the pro forma “Personal Profile’ statement on the that document which provided that she was prepared to ‘accept volatility over the medium to long term if the investment growth is higher and the risks over that term are minimal or eliminated” and Ms Seymour signed and accepted that Confidential Financial Profile.

12 The allegations in relation to Mr Drummond were contained in para 74 as follows:

On or about 6 May 2005, Storm represented to the Applicant that:

(a) there was no risk of capital loss associated with investing all of her assets in the share market in accordance with Storm’s recommendations (“Fourth Risk Representation’);

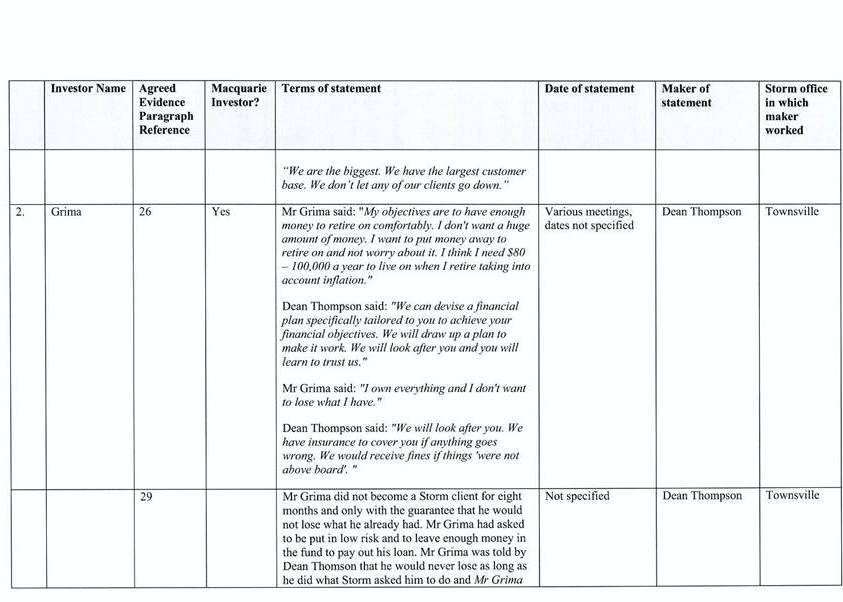

(The representations described in paragraphs 72(a), 72(b) 72(c) and 74(a) above will be referred to collectively as the “Risk Representations”).

(b) there was little or no risk that the investment strategy devised by Storm for the Applicant would result in the applicant’s margin loan going into margin call (First Margin Call Representation); and

(c) in the unlikely event that the applicant’s margin loan went into margin call, Storm would lend money to the Applicant to cover any amount required to be paid to the bank to cover it (Second Margin Call Representation).

(The representations referred to in paragraphs (b) and (c) above will be referred to collectively as the “Margin Call Representations”).

Particulars

Express statements made by Mr Drummond to the Applicant during a meeting on or about 6 May 2005.

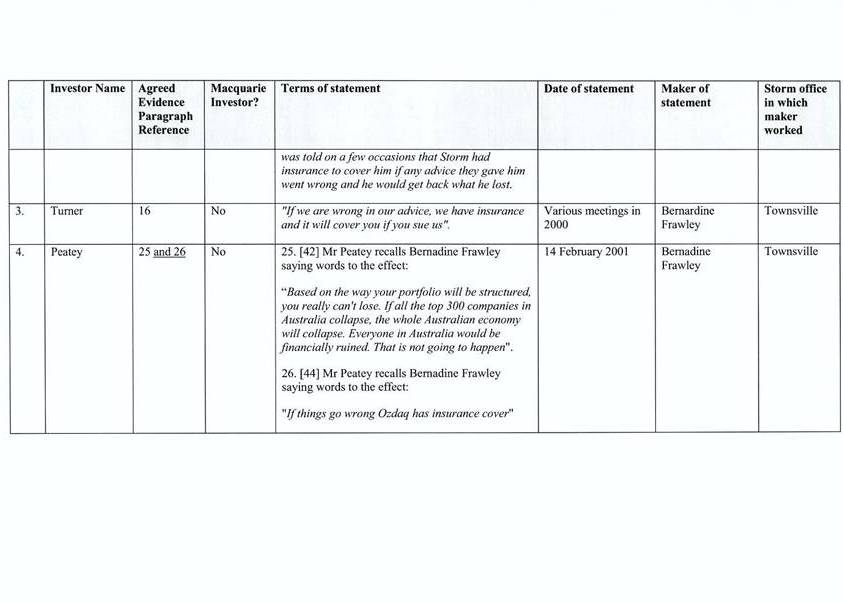

13 In its defence, Macquarie Bank Limited (Macquarie) did not admit the allegations in paras 72 or 74.

The Storm investors’ evidence

14 This tendency issue first arose with the tender of a statement by Mr Beesley, a person who was also a customer of Storm at about the same time as Mrs Richards. While both Mr Beesley and Mrs Richards broadly followed the same Storm investment strategy, their circumstances differed in at least one respect. To obtain the equity necessary to establish his margin loan, Mr Beesley accepted Storm’s advice to mortgage his home, whereas Mrs Richards had cash available for that purpose. She obtained that cash from the sale of her home following a matrimonial property settlement with her former husband shortly before she became a customer of Storm.

15 The particular paragraph of Mr Beesley’s statement to which objection was taken was as follows:

George [Cassimatis] said words to the following effect: “There is no risk of losing your house. In the event of a fall in the market and a reduction in value of your portfolio, your debts will be cleared at a point where the mortgage will be covered.”

(Emphasis in original)

16 Mr George Cassimatis was a financial adviser employed by Storm. He was also a brother of Mr Emmanuel Cassimatis who, along with his wife Mrs Julie Cassimatis, were the sole directors and shareholders of Storm.

17 In addition to Mr Beesley’s statement, Mrs Richards’ counsel also sought to tender as tendency evidence the statements of 11 other persons who were customers of Storm in the period from the late 1990s to late 2008. During the trial of these proceedings, this group of witnesses became known as the Storm investors. The statements of all 12 Storm investors (including Mr Beesley) were tendered on the basis that those parts of them connected with this tendency issue would be either admitted, or rejected, following this ruling.

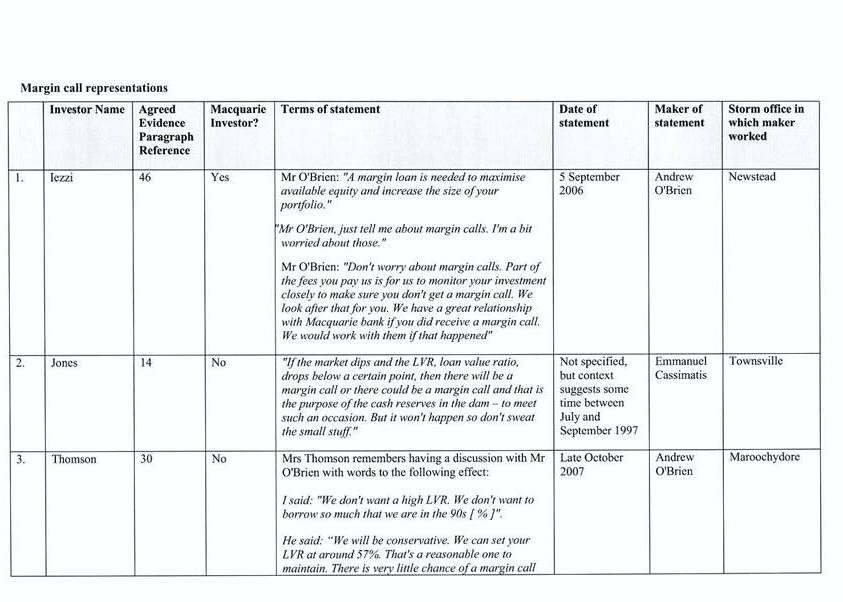

18 Mrs Richards’ counsel prepared a schedule identifying the apposite parts of the 12 Storm investors’ statements. Macquarie’s counsel responded with a more detailed schedule. That schedule included details of each representation in contention, the date upon which it was made, the Storm adviser who made it and the location of the maker of the statement when he or she made it. The parties have agreed that this Macquarie schedule is accurate and should be relied upon for the purposes of this ruling. For convenience, it is attached to these reasons marked “A”. A couple of aspects of it require some explanation. First, it is separated into three sections: risk representations; insurance representations; and margin loan representations corresponding to paras 72(a), 72(c) and 74(a); 72(b); and 74(b) and 74(c) of Mrs Richards’ further amended statement of claim, respectively. Secondly, like Mr George Cassimatis (see at [16] above), the persons identified in the column headed “Maker of statement” were all financial advisers employed by Storm.

Contentions

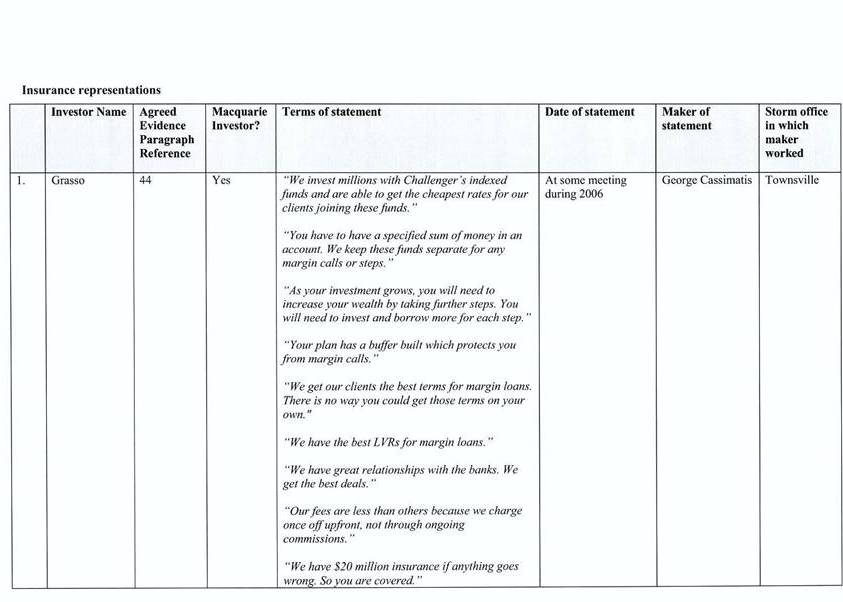

19 Mr Campbell SC, counsel for Mrs Richards, submitted that the evidence of Mr Beesley and the other 11 Storm investors was both relevant to, and highly probative of, a tendency of Storm to make representations to its clients, through its employed financial advisers, that there was “no risk” of them losing their capital, ie their equity contribution, if they followed Storm’s investment strategy. He submitted that this tendency made it more likely that a similar statement about risk was made to Mrs Richards by her Storm financial advisers, Ms Seymour and Mr Drummond. He submitted the evidence was not directed to whether the representations made to Mrs Richards were misleading, but to whether they were made at all. This evidence was necessary, so he submitted, because Macquarie had not admitted that those representations were made.

20 Mr Campbell emphasised that in this instance the relevant person who had the tendency to act in a particular way was Storm, not Ms Seymour, Mr Drummond, or any of the other individual Storm financial advisers. He submitted that the fact that the representations were repeated by a range of Storm financial advisers over a long period of time was itself highly probative of the existence of the tendency of Storm, via its financial advisers, to make such statements. He submitted that while some of the representations made to some of the Storm investors about risk were directed to the investors not losing their homes, those representations were substantively the same as the representations made to Mrs Richards about not losing her equity contribution. He also submitted that it was the effect of each of the representations that was critical, not the precise form of the words used.

21 Mr Campbell submitted that, on a common sense assessment, the effect of the representations made to the 12 Storm investors and to Mrs Richards revealed “‘striking similarities’, ‘unusual features’, ‘underlying unity’, ‘system’ or ‘pattern’”, relying upon Hoch v The Queen (1988) 165 CLR 292 (Hoch) at 294–5. Finally, Mr Campbell submitted that s 97 of the Evidence Act applied to Storm as a corporate entity, relying upon Combined Insurance Company of America v Trifunovski [2011] FCA 271 (Trifunovski) at [9]. It is convenient to note at this point that in his oral submissions Mr Sheahan SC, counsel for Macquarie, did not seek to challenge this conclusion in Trifunovski. I will therefore make this ruling on the basis of that construction of s 97.

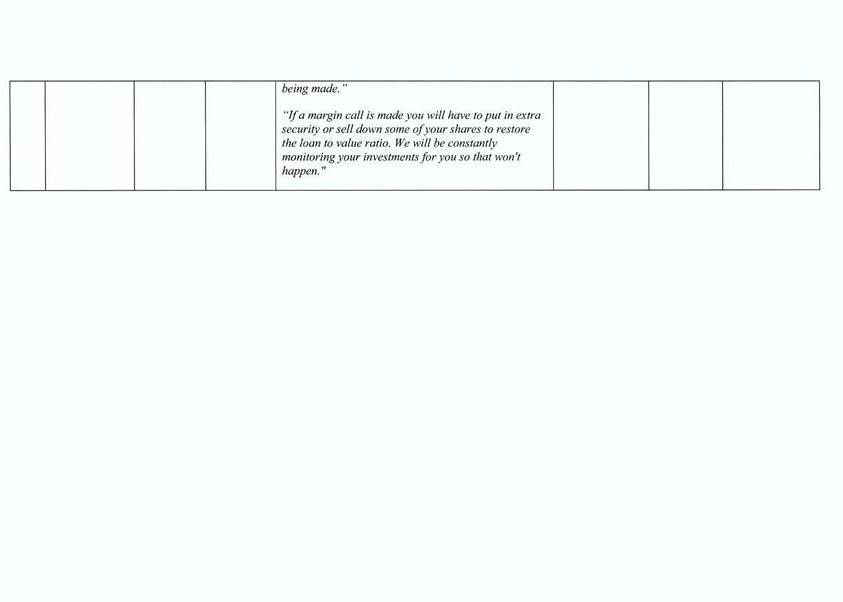

22 Mr Sheahan submitted that the appropriate starting point was to identify the relevant fact in issue. He claimed it was whether, at a meeting in June or July 2001, Ms Seymour of Storm made an oral representation to Mrs Richards to the effect set out in para 72(a) of Mrs Richards’ further amended statement of claim. Similarly in relation to the representation allegedly made to her by Mr Drummond in May 2005, Mr Sheahan submitted the relevant fact in issue was to the effect set out in para 74 thereof. He submitted that the requirement in s 97(1)(b) of the Evidence Act that the evidence had to have “significant probative value” required more than mere relevance within the meaning of s 55 of the Evidence Act. Instead, he submitted, it had to be “clearly and strongly probative” of the fact in issue, relying upon Zaknic Pty Ltd v Svelt Corporation Pty Ltd (1995) 61 FCR 171 at 176.

23 Mr Sheahan referred to the schedule of the tendency evidence (“A” to these reasons) and pointed to what he claimed were significant differences between the representations allegedly made to Mrs Richards by Ms Seymour in June/July 2001 and Mr Drummond in mid-2005; and the representations made to Mr Beesley and the 11 other Storm investors. First, he submitted that none of the other Storm investors involved representations made by Ms Seymour and only one (Ms Raccuia) involved a representation made by Mr Drummond. However, in relation to Ms Raccuia, he pointed to the fact that there was a nine year gap between the representation by Mr Drummond allegedly made to her; and the representation Mr Drummond allegedly made to Mrs Richards. As to the representations made to the other Storm investors, he pointed to the fact that only one occurred in 2001 – Ms Frawley’s representation to Mr Peatey in February 2001 – and only one occurred in 2005 – Mr George Cassimatis’ representation to Mr Beesley on 11 February 2005. Further, he pointed to the differences in the accounts given by the 12 Storm investors. By way of example, he pointed to the fact that Mr Beesley claimed that Mr George Cassimatis said “[t]here is no risk of losing your house” and he (Mr Beesley) did not say Mr Cassimatis related this statement to any explanation about the “risk/volatility statement” that was the particular focus of their discussions at the time and which statement Mr Beesley later initialled. By comparison, he pointed out that Mrs Richards claimed that Ms Seymour told her there was no real risk of losing her equity contribution in the context of a discussion that was expressly directed to the “risk/volatility statement”.

24 Further, Mr Sheahan submitted that Mrs Richards’ statement that Ms Seymour told her there was no real risk differed significantly from the allegation in para 72(a) of the further amended statement of claim that she (Ms Seymour) said there was “no risk” involved. It is convenient to deal with this submission immediately. This ruling requires an assessment as to whether I think the evidence of Mr Beesley and the other 11 Storm investors will be of significant probative value in relation to the apposite facts in issue. In this instance, the facts in issue are those pleaded in paras 72 and 74 of the further amended statement of claim (see at [11] and [12] above). It is those allegations that provide the standard for this assessment. Mrs Richards’ evidence (at [7]–[9] above) is germane to those issues, but the question whether it goes to prove those pleaded facts is a matter that will fall to be determined as part of the substantive issues following the conclusion of the trial of this matter. Thus, the alleged inconsistency between Mrs Richards’ evidence and the allegations in para 72 of the further amended statement of claim (if it exists and I express no view either way) is therefore immaterial to the assessment I have to make in this ruling.

25 Finally, Mr Sheahan pointed to the fact that Mrs Richards was relying upon representations made to 10 other Storm investors (re the risk representations: see schedule “A”) over a period of more than 12 years (July 1996 to post-October 2008) when there were more than 1,000 Storm investors comprising her class in these representative proceedings and there were about 3,000 Storm investors that pursued geared investments in the period concerned. Mr Sheahan submitted that the representation made to some of the other Storm investors about the insurance representations and the margin call representations (see [18] above) did not have significant probative value for the same reasons.

26 As an alternative to the above submissions, Mr Sheahan submitted that if this evidence is held to meet the condition set by s 97(1)(b), it should be rejected under s 135 of the Evidence Act on the basis that it will be unfairly prejudicial to Macquarie, misleading or confusing and likely to result in an undue waste of time at the trial of these proceedings. Among other things, he pointed to the hearing time that would most likely need to be devoted to the cross-examination of the 12 Storm investor witnesses to test their recollections of conversations that occurred up to 15 years ago, eg the conversation between Mr Emmanuel Cassimatis and Mr Jones that occurred in 1997.

Principles on the operation of section 97

27 Both counsel relied upon a number of authorities in support of their contentions about the operation of s 97 of the Evidence Act. It is appropriate to begin with the most authoritative decision, that of the Full Court of this Court in Jacara v Perpetual Trustees WA Ltd (2000) 106 FCR 51; [2000] FCA 1886 (Jacara), which considered the operation of s 97 in some depth. While both counsel referred to this decision, Mr Sheahan placed particular reliance upon it. In Jacara, the applicant (Jacara) claimed it had been induced to enter into a lease of a kiosk in a shopping centre by a series of representations allegedly made to it by a Ms Kelly, who was an agent of Perpetual Trustees WA Ltd, the proprietor of the shopping centre concerned. The critical representations were allegedly made to a Mr Williams, who was associated with Jacara. They were to the effect that there would be a substantial increase in the number of customers attending the shopping centre, and therefore Jacara’s turnover, following its redevelopment. For present purposes, the pertinent question raised on the appeal was whether the trial judge had erred in excluding evidence of representations to similar effect allegedly made by Ms Kelly to five other persons who were also contemplating entering into leases of shops in the redeveloped shopping centre. The Full Court concluded that the trial judge did not so err and dismissed the appeal.

28 Sackville J delivered the primary decision and Whitlam J (at [1]) and Mansfield J (at [108]) agreed. In the course of his reasons, Sackville J set out: the apposite provisions of the Evidence Act (at [17]–[24]); the legislative scheme in the Evidence Act governing tendency evidence (at [47]–[53]); the common law position on similar fact or propensity evidence (at [68]–[71]) and the test for “significant probative value” under s 97 (at [72]–[76]). It may also be noted that there was an issue in Jacara as to whether s 97 of the Evidence Act governed the evidence concerned at all (see at [54]–[67]). As is noted above (at [2]), no such issue arises in this case.

29 It is convenient to set out a summary of the relevant principles that can be extracted from his Honour’s comprehensive and detailed examination in Jacara of the operation of s 97 and the other related provisions of the Evidence Act. They are as follows:

(a) the effect of s 56 of the Evidence Act is that irrelevant evidence is inadmissible in a proceeding while relevant evidence is admissible, except as otherwise provided by the Evidence Act: see at [47];

(b) under s 55(1), relevant evidence is that evidence which, if it were accepted, could rationally affect the assessment of the probability of the existence of a fact in issue in a proceeding: see at [47];

(c) the definition of “relevant evidence” requires a minimal logical connection between the evidence and the fact in issue. However, the relevant evidence does not need to render a fact in issue probable, or even sufficiently probable. Instead, it is enough if it only makes the fact in issue more probable, or less probable, than it would be without the evidence, ie if it affects its probability: see at [47];

(d) relevant evidence is only excluded if one of the exclusionary rules applies, or if the Court exercises a discretionary power to exclude the evidence: see at [48];

(e) the tendency rule in s 97 of the Evidence Act is a contingent exclusionary rule in the sense that the tendency evidence is excluded only if the Court forms a view that the evidence would (now “will”: see at [30] below) not have significant probative value: see at [48];

(f) the Evidence Act was not intended to be a mere codification of the common law rules of evidence. Instead, it was intended to make, and did make, substantial changes to the law of evidence: see at [50];

(g) the tendency rule in s 97(1) of the Evidence Act departs from the more relaxed common law approach to the admission of similar fact evidence in civil proceedings set out in authorities such as Sheldon v Sun Alliance Australia Ltd (1989) 53 SASR 97: see at [68]–[71]. Thus, under s 97(1) of the Evidence Act, even if the evidence is relevant, it will not be admissible if the Court thinks that the evidence would (now “will”: see at [30] below) not have “significant probative value”: see at [72];

(h) for the evidence to have “significant probative value”, more is required than mere statutory relevance (under s 55 (see above)) but something less than a “substantial” degree of relevance is required: see at [73];

(i) this means that the evidence has to be “important” or “of consequence” in establishing the fact in issue, or that it has to be “clearly and strongly probative of the relevant fact in issue”: see at [73] and the cases cited; and

(j) however, the statutory language provides the standard that has to be applied and statements in authorities (such as cited above) are not to supplant that statutory language: see at [74].

30 Before identifying how Sackville J proceeded to apply these principles in Jacara, it is convenient to note that s 97(1) of the Evidence Act has been amended since the decision in Jacara. While that amendment was achieved by repealing s 97(1) in its entirety and replacing it with a new section, the changes to it were not as radical as this legislative approach might otherwise suggest. In fact, only three words were changed: the word “if” at the end of the introductory words to the provision was changed to the word “unless”; the word “or” between sub-sections (a) and (b) was changed to the word “and”; and the word “would” in the first line of sub-section (b) was changed to the word “will”: see Evidence Amendment Act 2008 (Cth).

31 The background to these amendments is recorded by Buchanan J in Astram Financial Services Pty Ltd v Bank of Queensland Ltd [2010] FCA 1010 at [235]–[238]. In this process, his Honour quoted from the Explanatory Memorandum where the purpose of the amendments is described (see at [238]): “[t]he amendment does not change the substantive law, but makes the provision easier to understand”. Taking into account the changes made by these amendments (at [30] above), I consider that the Legislature has achieved this purpose. I therefore agree with the observation in Odgers S, Uniform Evidence at Law (10th ed, Thomson Reuters) (at 1.1.60) that: “The provision has been amended to make it clear that the onus is on the party seeking to have the evidence ruled admissible to persuade the court that … the evidence ‘will’ have ‘significant probative value’.” Otherwise, I do not consider the principles on the operation of s 97(1) of the Evidence Act as set out in Jacara (above) have been affected by these amendments.

32 In Jacara, Sackville J concluded (at [77]–[82]) that the trial judge did not err in rejecting the evidence of the five other persons as to what Ms Kelly had allegedly said to them. In his submissions, Mr Sheahan relied upon the two factors specifically identified by his Honour: the differences in the accounts and the period of time that had elapsed. Those factors were summarised by his Honour (at [81]) as follows:

In my view, it was well open to the primary Judge to conclude that the various accounts differed among themselves and from Mr Williams’ version to such an extent that the evidence could not be said to have significant probative value on the facts and issues. This conclusion is reinforced by the fact that the conversations with the five tenants are said to have occurred some four to twelve months after the dealings with Mr Williams and Ms Kelly.

33 Mr Sheahan submitted that, in this case, the corresponding factors were even more remote than those in Jacara. He submitted that the representations were made by a range of different Storm financial advisers, rather than one; they were made over a period of many years (from 1996 to 2008), rather than four to twelve months; and they were different in content and effect and made in different market circumstances. As a consequence, he submitted there was all the more reason why the tendency evidence in this case was not significantly probative of the facts in issue.

34 Mr Campbell responded that this case was different from Jacara. This was so because, in Jacara, the factual accounts were diverse and they did not go to the central issue, whereas in this case, all of the representations made were to the same effect: there was “no risk” of investing with Storm. Furthermore, he submitted they go to the central issue as to whether representations of this kind were made by Ms Seymour and Mr Drummond to Mrs Richards.

35 Both counsel relied upon a number of other authorities, in particular: Mr Campbell on Trifunovski and Twynam Pastoral Co Pty Ltd v AWB (Australia) Limited [2008] FCA 1922 (Twynam); and Mr Sheahan on Australian Competition and Consumer Commission v CC (NSW) Pty Ltd (1999) 92 FCR 375; [1999] FCA 954 and DF Lyons Pty Ltd v Commonwealth Bank of Australia (1991) 28 FCR 597 (DF Lyons). Since the principles in relation to the operation of s 97 of the Evidence Act have been authoritatively outlined in Jacara, it is unnecessary to consider any of these decisions for the purpose of identifying those principles. Furthermore, as Gummow J said in DF Lyons (at 607), “each case has to be considered with close regard to its particular circumstances”. This can be aptly demonstrated from a brief consideration of the decisions in DF Lyons and Twynam, both of which, unlike the other two decisions above, involved claims for misleading or deceptive conduct under s 52 of the Trade Practices Act 1974 (Cth). In DF Lyons, Gummow J rejected as similar fact evidence on common law principles the evidence of three persons to whom similar statements had been made about foreign currency loans, at about the same time, by Mr Green, the CBA bank official concerned. It was Mr Green who had allegedly made the misleading or deceptive representations to Mr Lyons, one of the applicants, about the same subject matter. His Honour’s conclusions about the admissibility of that similar fact evidence was as follows (at 607):

In the present case, Mr Green had dealings with various customers of the Bank at Taree concerning foreign exchange loans and they took place in the period in which he was dealing with Mr Lyons. In that sense, there was an underlying unity in Mr Green’s activities, but as one might expect, the dealings with customers varied with the particular circumstances as they arose. The nature of the causes of action propounded by the applicants means that specific representations must be established. That is why in the oral evidence of Mr Lyons, both in chief and in cross-examination, great attention was paid in eliciting what was or was not said in precise terms on particular occasions. As a matter of ordinary experience of human behaviour, the evidence which the applicants seek to lead would not tend to prove the making of the representations upon which the applicants rely.

(Emphasis added)

36 On the other hand, in Twynam, Jagot J admitted as tendency evidence under s 97 of the Evidence Act the affidavit evidence of four persons who deposed to having conversations with a Mr Adams about the sale of wheat at about the same time as he (Mr Adams) allegedly made the misleading or deceptive representations to Mr Setter about the same subject matter. While her Honour noted a number of differences in the various conversations, she was nonetheless persuaded by the “striking similarities” between the critical parts of them. Her Honour’s conclusion that this tendency evidence should be admitted was as follows (at [13]):

Despite these differences there are striking similarities in respect of the essential allegation in paragraph 12(d) of the statement of claim and Mr Setter’s evidence that if the applicant did not buy wheat “now” there would be none left until the next harvest in October 2003. First, it is apparent that the disputed conversations are all said to have occurred in late October or early November 2002 and thus are proximate in time. Secondly, the disputed conversations all involve the respondent’s customers or potential customers for the purchase of grain. Thirdly and most importantly, each conversation refers not only to the availability of wheat or grain but to the need to buy now as either no grain would be available until October 2003 (Mr Vickery and Mr Rowland) or grain could become unavailable (Mr Gillogly and Mr Roberts). Hence, the time, context and essential or critical content of the conversations are all remarkably similar. For these reasons I consider that the disputed evidence, taken together with Mr Setter’s evidence, has significant probative value within the meaning of s 97 of the Evidence Act (at least in its current form) and is provisionally relevant. The disputed evidence will involve additional time but its probative value is not substantially outweighed by any undue waste of time. As such, I do not accept that it should be excluded under s 135(c).

(Emphasis added)

37 Not surprisingly, Mr Sheahan placed particular reliance on the conclusion in DF Lyons and Mr Campbell placed particular reliance on the conclusion in Twynam. However, in relation to Twynam, Mr Sheahan also pointed to at least two factual distinctions which he submitted were significant in this case. They were: that in Twynam, the same officer of the respondent (Mr Adams) was involved in all of the conversations; and all of the conversations occurred in a short period of time, in late October and early November 2002.

38 Given the more relaxed approach taken to the admission of similar fact evidence in civil proceedings according to common law principles as identified in Jacara (see at [29(g)] above), one might have expected the opposite results in these two cases. This underscores the importance of the statement above (at [35]) that one must look closely to the particular factual circumstances of each case. Accordingly, with all these principles in mind, I will now turn to consider the particular factual circumstances of this case.

Consideration

Striking similarities, unusual features or underlying unity, system or pattern

39 It is important to begin by noting that the evidence to which s 97 of the Evidence Act is directed is evidence (of the kind described) by which a party seeks to prove a person has, or had, a tendency to “act in a particular way, or to have a particular state of mind”. In this case it is the former: to prove a tendency of Storm, through the conduct of its financial advisers, to act in a particular way. The particular way in which Storm is alleged to have had that tendency to act was to make representations to its customers that there was “no risk” associated with them investing in accordance with the Storm investment strategy. The question, therefore, is whether I think the evidence of the 12 Storm investors will have significant probative value in establishing that tendency and, in turn, the apposite facts in issue, viz that Ms Seymour and/or Mr Drummond made the alleged representations to Mrs Richards.

40 To establish this, Mr Campbell relied upon the approach in Hoch: “that the evidence reveals ‘striking similarities’, ‘unusual features’, ‘underlying unity’, ‘system’ or ‘pattern’”. Whilst eschewing this as the only basis for assessing tendency evidence, Sackville J appeared to accept it as at least one of the valid approaches in Jacara, where his Honour said (at [82]):

None of this is to suggest that the only basis for the admissibility of tendency evidence under s 97(1) of the Evidence Act is if the evidence, to use the language in Hoch v The Queen, reveals “striking similarities” or “unusual features”.

41 It will also be apparent from the conclusion of Jagot J in Twynam (see above at [36]) that her Honour appears to have relied upon the same approach. I therefore propose to adopt that approach in assessing the tendency evidence in this case. That requires me to consider factors such as the nature and content of the representations concerned to ascertain whether there are any striking similarities, or unusual features apparent in them, and to consider the timing and circumstances in which they were made and any other features that may reflect an underlying unity, system or pattern such that this evidence has the requisite significant probative value relative to the facts in issue. I will therefore turn to consider these factors in turn.

Nature and content

42 Turning first to the risk representations, it should be noted, at the outset, that they involve representations that were allegedly made to 10 of the 12 Storm investors (see [18] above and schedule “A”). Mr Campbell submitted that those representations were substantially the same as the representations constituting the facts in issue because the risk of losing one’s home, viz in Mr Beesley’s case, is to the same substantive effect as the risk of losing one’s equity contribution, viz in Mrs Richards’ case. While I accept that both sets of representations address the fact of a loss of capital, in my view, Mr Campbell’s submission is misdirected. That is so because it focuses on the nature of the loss involved rather than the extent of the risk of that loss occurring. It is the latter that comprises the critical component of the facts in issue. So much is clear from the thrust of the allegations in Mrs Richards’ further amended statement of claim that Ms Seymour and/or Mr Drummond made unqualified representations to her that there was “no risk” of loss by following the Storm investment strategy.

43 However, I do consider that these pleaded representations are of an unusual nature. It is a matter of common experience that risk is a central factor requiring consideration by anyone embarking upon any investment strategy. It is also well-known that when one invests, the level of risk generally corresponds with the level of return. Thus, the axiom that the lower the risk, the lower the return or, conversely, the higher the risk, the higher the return. There is therefore nothing unusual, in my view, in a financial adviser like Ms Seymour, or Mr Drummond, discussing risk with a potential investor like Mrs Richards. However, because risk is an ever present factor affecting any investment strategy, I consider it is unusual for a financial adviser to make an unqualified statement that there is “no risk” associated with following a particular investment strategy. So, accepting for the purposes of this ruling that Ms Seymour and/or Mr Drummond made the risk representations as pleaded in Mrs Richards’ further amended statement of claim (see my observations at [24] above), I consider those representations are of an unusual nature. Then the question is whether the risk representations contained in the evidence of the 10 Storm investors concerned is of significant probative value in establishing whether these unusual representations (as pleaded) were made.

44 To answer this question, it is necessary to analyse the nature and content of the representations allegedly made to the 10 Storm investors concerned to ascertain whether they are of a similar nature or, put in other words, are strikingly similar. When that analysis is done, I consider the following conclusions can be drawn. To begin with, the representations made to six of the 10 Storm investors concerned (Beesley, Iezzi, Pickering, Grima, Ensor and Beven) suffer from the same misdirection that is present in Mr Campbell’s submissions (see at [42] above) in that they focus on the nature of the loss that is likely to be involved with following the Storm investment strategy, rather than the extent of the risk of that loss occurring. Further, and in any event, they were all qualified by an explanation, or by the language used, or by the circumstances in which they occurred.

45 All of the risk representations are set out in schedule “A” to these reasons, so three examples will suffice. First, Mr Beesley claims he was told “[t]here is no risk of losing your house. In the event of a fall in the market and a reduction in value of your portfolio, your debts will be cleared at a point where the mortgage will be covered.” Thus, the statement focused on the loss of his home and was immediately followed by a statement that identified how that risk of losing his home would be avoided by clearing the debts so that the mortgage on his home would be repaid.

46 Secondly, Mr and Mrs Ensor were told by Mr Jones some time in 1999 that “[y]our house is safe. There is no risk to the house.” Again, the focus of this statement was the possibility of the Ensors losing their home. Further, it was specifically expressed in terms of their home being “safe” if they were to expose themselves to “more risk” by increasing their margin loan. In this context, the word “safe” clearly implies a level of risk. It necessarily follows that it is incompatible with the complete absence of risk reflected in the pleaded risk representations.

47 Thirdly, at least one of the statements made to Mr and Mrs Pickering (that in [86] and possibly two more, those in [47] and [56]: see schedule “A”) was made in October 2008 after the significant falls in the Australian share market that occurred from late 2007. Against this background, that statement could, in my view, more accurately be characterised as having been given by way of reassurance after the risk of the loss that had eventuated, rather than a statement at the outset of the Storm investment strategy directed to the complete absence of any loss associated with following it.

48 It follows that none of this group of six representations has a striking similarity with the unusual feature of the representations comprising the pleaded facts in issue, viz that there was “no risk” of investing according to the Storm investment strategy.

49 Next, it is to be noted that the risk representations made to three of the 10 Storm investors concerned (Jones, Peatey and Raccuia) did not mention the word “risk” at all. Instead, they were allegedly told things such as “[y]ou will never lose the house”; “you really can’t lose”; or “[y]ou will never lose your home because of the way we will set things up for you”. It follows that these statements were not specifically directed to the issue of risk and instead focused more generally on the question of loss. While in this context loss and risk are obviously related concepts, in the particular circumstances of this case, I do not consider broad statements such as “you cannot lose” provide significantly probative evidence that the quite specific representations as pleaded about there being “no risk” were made.

50 Finally and significantly, as a consequence of the exclusion of the two groups of representations above, only one of the 10 Storm investors concerned remains. Mr Turner was told by Ms Frawley at various meetings in 2000 that: “[t]he way in which Storm manages your portfolio means there is no risk in following the investment strategy recommended by Storm”. This representation does, in my view, bear a striking similarity to the representations constituting the pleaded facts in issue. That is so because it comprises an unqualified statement to the effect that there was “no risk” of investing in accordance with the Storm strategy. However, I do not consider this striking similarity is sufficient by itself to make it of significant probative value relative to the facts in issue. Before that conclusion can be drawn, it is necessary to consider the timing of this representation and the circumstances in which it was made, matters to which I will now turn.

Timing and circumstances

51 As to its timing, Mr Turner’s representation was allegedly made to him approximately one year before the representations were allegedly made by Ms Seymour to Mrs Richards. Further, it was allegedly made approximately five years before the representations were allegedly made by Mr Drummond to Mrs Richards. As to the relevant circumstances, Mr Turner’s representation was allegedly made to him by Ms Frawley in the Townsville offices of Storm, whereas Mrs Richards’ statements were allegedly made to her by Ms Seymour and by Mr Drummond in the Fortitude Valley, Brisbane, offices of Storm. This means that there was a long lapse of time between these various sets of representations (between one and five years) and they were made by entirely different persons in completely different locations. It follows, in my view, that any striking similarity in the nature of these representations is outweighed by the stark differences in their timing and circumstances. For these reasons, I do not consider, on balance, that Mr Turner’s evidence has the significant probative value necessary to justify its admission as tendency evidence under s 97(1) of the Evidence Act.

52 While I am dealing with matters of timing and circumstances, it is convenient to analyse the evidence from the other 9 Storm investors concerned to ascertain whether they display some underlying unity, system or pattern. That analysis (insofar as dates are disclosed) reveals that representations were made by different Storm financial advisers to a particular Storm investor (or couples) in each of the years 1996, 1997, 1999, 2000, 2001, 2004, 2005 and 2008. Further, in the years 2006 and 2007: five representations were made by different Storm financial advisers to three different Storm investors (or couples); and two representations were made by one Storm financial adviser to a particular Storm investor (couple), respectively. The latter involved Mr Benson making representations on two separate occasions in 2007 to Mr and Mrs Pickering. The former involved four different Storm financial advisers and three individual Storm investors (or couples): Mr O’Brien to Mr Iezzi; Mr McAllister to Mr and Mrs Pickering; Mr Benson on two occasions to Mr and Mrs Pickering; and finally, Mr Thompson on one occasion to Mr Grima. Of all these, the occasions that are most proximate in time to the two occasions involving Mrs Richards are Mr Peatey, on 14 February 2001, and Mr Beesley, on 11 February 2005.

53 In the case of Mr Peatey, the representation was allegedly made by Ms Frawley in the Townsville office of Storm to the following effect:

Based on the way your portfolio will be structured, you really can’t lose. If all the top 300 companies in Australia collapse, the whole Australian economy will collapse. Everyone in Australia would be financially ruined. That is not going to happen.

54 Taking into account my observations above (at [42]–[43]) about the critical unusual feature of the facts in issue and the nature and content of this representation, together with its timing –approximately three months before the representation Ms Seymour allegedly made to Mrs Richards – and the circumstances in which it was made – a different Storm financial adviser in a different location – I do not consider it is sufficiently similar in nature or content, nor sufficiently proximate in time or circumstances, to be of significant probative value relative to the facts in issue.

55 In the case of Mr Beesley, the representation was allegedly made by Mr George Cassimatis on 11 February 2005 – approximately three months before the representation Mr Drummond allegedly made to Mrs Richards – in the Townsville offices of Storm. For the same reasons as I have outlined above (at [54]), I do not consider the evidence about the representation made to Mr Beesley is sufficiently similar in nature or content, nor sufficiently proximate in time or circumstances, to be of significant probative value relative to the facts in issue.

56 Finally on this factor, I do not consider the eight incidents when representations were allegedly made to a particular investor (or couple) in the 12 years between 1996 and 2008 (see at [55] above) displays any underlying unity, system or pattern. Insofar as the series of representations made in 2006 may reveal an underlying pattern during that year, I do not consider that pattern displays any commonality in personnel or location, nor a sufficient proximity in time to the representation Mr Drummond allegedly made to Mrs Richards (May 2005), much less to the representations Ms Seymour allegedly made to Mrs Richards (June/July 2001), that this tendency evidence has significant probative value relative to the facts in issue.

Other factors – Storm as a corporate entity

57 To attempt to avoid the outcome of the analysis undertaken above, Mr Campbell placed particular reliance upon the difference between the conduct of the individual financial advisers and their conduct viewed as the human agents of Storm as a corporate entity. Thus, as I understood his submissions, it does not matter if there is no evidence that Ms Seymour made any representations to any of the other 12 Storm investors, or that Mr Drummond’s two representations are so far apart in time (to Ms Raccuia in 1996 and to Mrs Richards in 2005) that they are of little, if any, probative value to the facts in issue. Instead, he submitted, the whole course of conduct of all of the individual financial advisers must be viewed together as the conduct of Storm as a corporate entity. Further, he submitted, if one analyses that conduct, there emerges an underlying unity, system or pattern that provides significant probative evidence of the facts in issue. On the basis of this approach, Mr Campbell drew strength from the facts that the risk representations were allegedly made to the 10 Storm investors concerned over a long period of time (12 years from 1996 to 2008), by a range of different financial advisers (10 different financial advisers are identified in schedule “A”) and at a variety of different Storm offices (five different offices are identified in schedule “A”). He submitted that the repetition of the same representations by different Storm financial advisers in a diversity of circumstances and locations over a long period of time demonstrated that Storm’s financial advisers were following “a company line”, or that there was a “culture” in Storm which provided evidence of significant probative value going to whether Ms Seymour and/or Mr Drummond made the representations in issue to Mrs Richards.

58 In my view, there are two fundamental defects in this approach. The first is that combining all of the occasions and representations reflected in the evidence of the 10 Storm investors concerned as one course of conduct by Storm does not overcome the conclusion above (at [50]) that only one of the representations (that made to Mr Turner) was so strikingly similar in nature and content that it might be regarded as evidence of significant probative value to the facts in issue. This conclusion therefore destroys both the repetition and the diversity of personnel and circumstances that are fundamental elements in Mr Campbell’s approach.

59 The second is that, even if that conclusion was to be put aside and instead it was to be assumed that all of the 19 representations (approximately) identified in schedule “A” were strikingly similar in nature to the pleaded representations, I consider Mr Sheahan is correct in his submissions that any assessment of Storm’s corporate conduct over this 12 year period must also take account of the nature and extent of Storm’s overall corporate operations in that same period. It follows that the assessment of this tendency evidence must take account of the fact that, in this 12 year period, Storm had approximately 3,000 customers who were pursuing a similar investment strategy to that of Mrs Richards. Thus, there were likely to have been many thousands of occasions and circumstances where risk was discussed between financial advisers employed by Storm and this large body of customers. So, even if it was assumed the statements of the 10 Storm investors concerned provided evidence that 19 representations (approximately) had been made to the effect that there was “no risk” of investing according to the Storm strategy, when that number of incidents is considered against the full nature and extent of Storm’s corporate operations in this period, it is likely to represent such a miniscule fraction of all those occasions that I do not consider it can be regarded as being of any significance. It follows that this evidence does not, even on this basis, establish an underlying unity, system or pattern demonstrating the existence of “a company line” or “culture” in Storm as a corporate entity, such that Storm may have had a tendency to make the pleaded representations.

The insurance and margin call representations

60 Finally, it is necessary to address the other two groups of representations pleaded in Mrs Richards’ further amended statement of claim: the insurance representations and the margin call representations (see at [18] above). To begin with, it is worth noting that these two groups of representations only involve four (the insurance representations) and three (the margin call representations) of the 12 Storm investors, respectively. Furthermore, in the case of two of the 12 Storm investors, their evidence is solely directed to either the insurance representations (Grasso), or the margin loan representations (Thomson).

61 As to the nature and content of these two groups of representations, unlike the “no risk” representations allegedly made by Ms Seymour and/or Mr Drummond to Mrs Richards, I do not consider there is anything unusual about the nature of either of them when they are considered in context. In this regard, two matters should be noted. It was (and still is) a requirement of the financial services licensing regime that licensees such as Storm had to have professional indemnity insurance. I do not therefore consider it would be unusual for financial advisers employed by Storm to remark on this fact from time to time during their discussions with their customers. Furthermore, all of the 12 Storm investors involved with this tendency evidence issue borrowed money through margin loans. Given this background, it could not be considered unusual for the subject of margin calls to be discussed with them by Storm’s financial advisers.

62 Nor do I consider there is anything remarkable about the timing and circumstances of either of these sets of representations such that it displays any underlying unity, system or pattern. With the insurance representations, only three representations are alleged over a period of six years (Turner 2000, Peatey 2001 and Grasso 2006 – no dates are specified for the two representations involving Grima). Those representations are alleged to have been made by three different financial advisers (G Cassimatis, Thompson and Frawley), none of whom was either Ms Seymour or Mr Drummond. While all the representations were alleged to have been made at the Townsville offices of Storm, I do not consider that aspect, or any other aspect of this evidence, displays any underlying unity, system or pattern such that the evidence is of significant probative value relative to the facts in issue insofar as they constitute the insurance representations.

63 With the margin call representations, only three representations are alleged over a period of 10 years (Jones 1997, Iezzi 2006 and Thomson 2007). Those representations are alleged to have involved two different financial advisers (O’Brien and E Cassimatis), neither of whom was either Ms Seymour or Mr Drummond. Further, it is alleged that each of these three representations was made at a different location. Again, I do not consider this evidence displays any underlying unity, system or pattern such that it provides evidence of a significant probative value relative to the facts in issue insofar as they constitute the margin call representations.

64 Finally, even if the evidence in relation to the five separate insurance representations, or the three separate margin call representations, were to be taken together as the corporate conduct of Storm, when one considers the unexceptional nature of the subject matters involved (see at [61] above) in the context of Storm’s overall corporate operations in the period concerned (see at [59] above), I do not consider this evidence is of any significance in establishing any underlying unity, system or pattern going to the existence of a “company line” or “culture” in Storm as a corporate entity such that it may have had a tendency to make representations of either kind.

Conclusion

65 For these reasons, I do not think that the tendency evidence contained in the statements of the 12 Storm investors is such that it meets the “significant probative value” condition set out in s 97(1)(b) of the Evidence Act. It necessarily follows that this tendency evidence may not be admitted as evidence in this trial. Because of this conclusion, it is unnecessary to consider whether this tendency evidence should be excluded under s 135 of the Evidence Act.

| I certify that the preceding sixty-five (65) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Reeves. |

Associate: