FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Letten (No 20)

[2012] FCA 1283

IN THE FEDERAL COURT OF AUSTRALIA | |

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | First Defendant (and others according to the attached schedule) |

DATE OF ORDER: | |

WHERE MADE: |

For the purpose of this Order, Property, Receivers, Scheme and Secured Lender have the meanings ascribed to them respectively in the Orders made in this proceeding on 25 February 2010, 4 March 2010 and 30 July 2010.

Additional Scheme has the meaning given to it in the 30 July 2010 Orders.

Corporate Defendants means each of the corporate defendants to this proceeding.

Schemes means each Scheme and each Additional Scheme.

Pooling Orders means the Orders made in this proceeding on 11 November 2010.

THE COURT DIRECTS THAT:

1. In adjudicating the Claims of members of the Schemes to the Common Fund for the purposes of paragraph 1(b) of the Pooling Orders and determining members’ entitlements to receive a distribution from the Common Fund, the Receivers are justified in:

(a) determining a member’s total contributions to the Schemes by reference to the amounts actually paid by the member to one of the Corporate Defendants in respect of that member’s investment in the Schemes and excluding any “capital gains” or other “entitlements” reported but unpaid by any of the Corporate Defendants to the member;

(b) including in a member’s contributions to the Schemes any amounts paid by a member to a Corporate Defendant in respect of:

(i) the “Project Reserve Bonds”;

(ii) the “War Chest”; and

(iii) the “LGH Development JVs” or “LGH Joint Ventures”,

and any other investments which did not relate to a specific project, Property or any of the Schemes;

(c) requiring members of the Schemes who have made a Claim against the Common Fund to account, in accordance with paragraph 1(d) below, for all payments which the member has previously received from any of the Corporate Defendants in respect of the member’s contribution to any of the Schemes, including:

(i) all periodic payments whether described by the Corporate Defendants at the time as “distributions”, “interest”, “income” or otherwise; and

(ii) all other payments whether described by the Corporate Defendants at the time as “capital returns”, “capital gains” or otherwise,

(collectively, the Payments Received); and

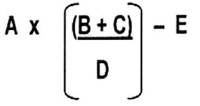

(d) determining a member’s entitlement to receive a distribution from the Common Fund in respect of a Claim in accordance with the following formula:

where:

(i) “A” means that member’s total contributions in respect of the Schemes determined in accordance with paragraphs (a) and (b) above;

(ii) “B” means the total of all funds in the Common Fund which are available for distribution;

(iii) “C” means the total Payments Received by all members who have made Claims on the Common Fund (which have not been withdrawn or rejected in part or in full);

(iv) “D” means the total of all Claims (which in respect of members of each of the Schemes, represents members’ total contributions to the Schemes as determined in accordance with paragraphs (a) and (b) above) which have not been withdrawn or rejected in part or in full; and

(v) “E” means the Payments Received by that member.

2. To the extent that there is any inconsistency between the directions in paragraphs 1(c) and (d) above and the Pooling Orders, paragraphs 1(c) and (d) above are to prevail.

3. Nothing in paragraphs 1 or 2 above is to affect the rights of any person to claim that they have, or any other person has, an entitlement to distribution from an asset of a Scheme or a Corporate Defendant (or the proceeds of sale of such asset) which differs from the distribution which they would receive pursuant to the directions in paragraphs 1 and 2 above or under the Pooling Orders.

AND THE COURT ORDERS THAT:

4. The further hearing be adjourned to a date to be fixed.

5. Costs be reserved except for the costs referred to in paragraph 5 of the Orders made on 10 October 2012.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011 (Cth).

VICTORIA DISTRICT REGISTRY | |

GENERAL DIVISION | VID 95 of 2010 |

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff

|

AND: | MARK RONALD LETTEN First Defendant (and others according to the attached schedule) |

JUDGE: | GORDON J |

DATE: | 19 NOVEMBER 2012 |

PLACE: | MELBOURNE |

REASONS FOR JUDGMENT

INTRODUCTION

1 This is the twentieth judgment in a series about unregistered managed investment schemes in which Mr Mark Ronald Letten (Mr Letten), the first defendant, was involved. The history of the proceedings was most recently summarised in Australian Securities and Investments Commission v Letten (No 7) (2010) 80 ACSR 401 at [7]-[12] (the Pooling Judgment). I adopt the same terms and abbreviations in these reasons for judgment.

2 On 11 November 2010, orders were made that (the Pooling Orders):

… Notwithstanding the terms and conditions of any joint venture agreement or other instrument governing the administration, management or winding up of the Schemes, the Receivers are justified in proceeding and making distributions out of the funds comprising the Common Fund:

(i) as if and on the basis that the Common Fund includes the “scheme property” of each of the Schemes;

(ii) as if and on the basis that the Common Fund constitutes a single fund; and

(iii) in the following order of priority:

(A) [after certain priority payments]

(B) second, to Claimants, a rateable share of the balance of the Common Fund, calculated by reference to the amount adjudged by the Receivers to be the amount of their respective Claims, …

(Pooling Order 1(b).)

3 “Claim” was defined to mean:

• In respect of members of each Scheme, the members’ total net contributions to a Scheme or Schemes as established by that member pursuant to the proof of claim process conducted under Direction 1(c) below;

and

• In respect of all other Claimants, any net proprietary claim on the Common Fund which can be established by the Claimant pursuant to the proof of claim process conducted under Direction 1(c) below.

(Emphasis added.)

This definition is important.

4 Paragraph 1(c) of the Pooling Orders provided that:

For the purposes of effecting distributions in accordance with Direction 1(b) above, the Receivers shall conduct a proof of claim process, which to the extent practicable conforms with (and is governed by the rules and regulations applicable to) the proof of debt or claim process applicable in a liquidation, pursuant to which the existence and value of Claims will be finally determined by the Receivers, subject to all rights of appeal to the Court (including pursuant to s 1321 of the [Corporations Act 2001 (Cth) (the Corporations Act)]).

(Pooling Order 1(c).)

5 Finally, reference should be made to paragraph 2 of the Pooling Orders. It provided that:

Nothing in paragraph 1 above is to affect the rights of any person to claim that they have, or any other person has, an entitlement to distribution from an asset of a Scheme or a Corporation Defendant (or the proceeds of sale of such asset) which differs from the distribution which they would receive pursuant to the process outlined in paragraph 1 above.

(Pooling Order 2.)

6 The basis on which those Pooling Orders were made was summarised in the Pooling Judgment in the following terms:

332 The facts of the present case disclose circumstances which may be classified as exceptional. Circumstances in which the general principle (that there should be no distribution of surplus assets other than to those entitled to the assets in proportion to their relevant entitlements) must yield to pragmatism. Why? Because in the present case, in addition to the matters raised in paragraph [250] and [259] above, it is to no-one’s advantage that a very long time and very large costs be spent in working out the entitlements and liabilities on a Scheme by Scheme basis (see [249] to [260] above and Re TVSN Limited [2005] NSWSC 692 at [17] ff) where:

1. as a result of the way in which Mr Letten and companies associated with him (including the Corporate Defendants) conducted the Schemes, it is not possible to say now what are the net assets of any Scheme and there appear to have been so many inter-Scheme transactions that it is not possible to say what assets were acquired by what Scheme using whose money;

2. the Receivers have been unable to trace investor contributions because receipts and payments in relation to each Scheme were made through four primary LGHA bank accounts and funds frequently were moved between these accounts, the LGHA bank accounts were often in overdraft and payments were commingled;

3. a number of the Schemes were oversubscribed in that the amount of investor contributions in relation to a particular Scheme exceeded the funding requirements for that Scheme. These oversubscriptions were not refunded or returned to investors: see, by way of example, Schemes numbered 14 (Twinview, see [135] above), 8 (Low Head - see [148] above) and 5 (Cimitiere House, see [205] above);

4. a significant proportion (up to $38 million) of investor contributions to Schemes appears to have been used to pay distributions to investors in other Schemes in circumstances where there were not sufficient profits or funds in the other Schemes to fund payment of distributions: see, by way of example, Scheme numbered 18 (Aurora Park, see [72] above);

5. the tracing of funds is further complicated and, I consider, rendered impossible by the lack of reliable financial and accounting data and the estimated cost ($18 million). Such a cost and burden would reduce what is already a limited expected return with no guarantee of any certainty of outcome.

333. Such a conclusion is consistent with authority: see [275] to [286] above. In each of Nelson, Enterprise Solutions 2000 and Tasman, the fund available for distribution to beneficiaries of the trust or members of the scheme (as applicable) was not substantial and the liquidators in each were concerned about the impact that the costs of making further investigations would have on the prospects of making a distribution. On that basis, the liquidators sought, and were granted, orders or directions for rateable distribution of the fund rather than to incur further costs in carrying out further investigations. Here, there is a mixed fund that has been conducted for a period of at least 12 years during which time there was in excess of 110,000 transactions through the relevant bank accounts. The relationship between the Schemes and Corporate Defendants is far from clear and the accounts cannot be traced.

334. As noted earlier, in Re French Caledonia Travel Services, the Supreme Court of New South Wales addressed the possibility that where there was evidence that various claimants ought be divided into separate classes with differential dividends, such an order should be made. In my view, given the complicated facts which the Receivers and the Court now face in the present case, proposed paragraph 2 of the directions preserves the possibility that a claimant may seek to prove that it should be entitled to a different dividend.

335. Subject to the proof of claim process, there is no basis for distinguishing the claims of investors whose contributions to the relevant Scheme are governed by a joint venture agreement as the terms of each of the joint venture agreements are similar (but not identical). In relation to investors whose contributions to Schemes are not governed by joint venture agreements, the claims are substantially equal to the claims of those who contributed by joint venture agreements. Their funds were treated on the same basis by LGHA (and the other Letten Entities) and by the other Corporate Defendants. To adopt the same language as the Court of Appeal in Lehman Brothers, the investors suffered a “common misfortune”, and any method of distribution should reflect that fact. Put simply, the alternative – distribution of Scheme property in a particular Scheme to those entitled to the property in proportion to their entitlements – is practically impossible at a number of levels. Given the manner in which these Schemes were operated and the difficulties identified in unscrambling the affairs of the Schemes, no rational person would undertake or engage in that task.

336. That leaves the question of method or basis of distribution. In my view, not only should the surplus be pooled but the surplus should be distributed rateably – the distributions made proportionally to the claims assessed by the Receivers: see [282] – [286] above. For the sake of completeness, the effect of the directions sought, and granted, does not affect the rights of any person to claim that they have, or any other person has, an entitlement to distribution from an asset of a Scheme or a Corporate Defendant (or the proceeds of sale of such an asset) which differs from the distribution which they would receive if the pooling process identified by the Receivers is adopted.

(Emphasis in original.)

7 Before turning to the substance of the directions now sought by the Receivers, it is necessary to recall that at the time of the Pooling Orders the Court decided (at [296] and [297]) that the issue of distributions and any residual uncertainties concerning other entitlements should await the proof of debt process provided for in Pooling Order 1(c): see [4] above. The relevant passage of the Pooling Judgment stated:

296. What of those investors that received distributions? The Receivers acknowledged the observations of Campbell J in Re French Caledonia Travel Services at [179] to [185] where his Honour referred to the personal equity which arises as a consequence of the principle that a person seeking to participate in the distribution of a fund must “bring to hotchpot” the benefits already received by that claimant from the fund. As the screeds reveal, investors were told that they would receive periodic payments in addition to a capital return. On that basis, the Receivers submitted that the investors may have an entitlement to receive distributions that is collateral to their claim for the return of the amounts invested. In those circumstances, the Receivers submitted that the investors would not be required to bring any distributions received into “hotchpot” in order to make a claim on the common fund in respect of their contributions.

297. Indeed, the Receivers submitted that the resolution of the investors’ entitlements with respect to distributions may depend, to some extent, on the representations that were made to each individual investor. Therefore, the Receivers submitted that the issue of distributions, and any residual uncertainties in respect of other entitlements, would best be resolved as part of the proof of debt process the Receivers propose to conduct in relation to the investors’ claims. I agree.

8 As a result, the Court directed that:

1. the Receivers were justified in paying the specified amounts out of the proceeds of sale of each asset of the Schemes and the Corporate Defendants, in a designated order of priority, the fourth priority being the creation of and payment into a Common Fund: paragraph 1(a)(iv) of the Pooling Orders;

2. notwithstanding the terms and conditions of any joint venture agreement or other instrument governing the administration, management or winding up of the Schemes, the Receivers were justified in proceeding and making distributions out of the funds comprising the Common Fund: Pooling Order 1(b);

3. for the purposes of enabling the Receivers to make distributions out of the Common Fund, the Receivers were to conduct a proof of claim process, which to the extent practicable conformed with (and was governed by the rules and regulations applicable to) the proof of debt or claim process applicable in a liquidation and pursuant to which the existence and value of Claims would be finally determined by the Receivers, subject to all rights of appeal to the Court (including pursuant to s 1321 of the Corporations Act): Pooling Order 1(c).

9 In April 2012, the Receivers commenced the proof of claim process by sending a circular and a proof of claim form to all known investors in any of the Schemes. On the face of the matter, that process has taken far too long to be commenced and to be completed. That is unfortunate. How and why there has been such a delay is not explained but may later bear on how the remuneration and expenses of the Receivers should be dealt with. It is neither necessary nor appropriate to consider the matter further in these reasons beyond saying that the process must be brought to an end without delay.

10 The circular sent to investors called for investors to submit formal proofs setting out full details of their Claims and all documents evidencing their Claims by 18 May 2012. Investors were asked to provide the following:

To assist with the efficient review of Claim Forms, Investors should provide full details of their claim and all documents evidencing their claim. In particular, the details that Investors are required to provide in respect of their claims include all amounts contributed by Investors and the dates of those investments and all payments received by Investors from the Letten Schemes in respect of their investments. If Investors rely on any verbal conversations to establish their claims, Investors should provide full details of those conversations. The types of documents that the Receivers expect may substantiate Investors’ claims includes, but not limited to:

1. Receipts, statements and other relevant communications from LGHA.

2. A copy of the signed Joint Venture Agreement between the Investor and the relevant scheme manager / trustee (or equity deposit bond or other terms governing the investment).

3. Copies of any “screed”, brochure, email, or any other correspondence with the Letten Entities which may be relevant to Investors’ entitlements in respect of their investments.

4. Investor Tax Returns for each investment year.

5. A copy of any bank statement(s) evidencing payment of investments and receipt of return of capital.

11 701 investors lodged proofs. In the course of that process, the Receivers identified uncertainties about which they now seek directions from the Court. The uncertainties may be described as follows:

1. whether investors are entitled to include in their Claims against the Common Fund any “capital gains” declared by the Corporate Defendants in addition to moneys actually paid by the investors to one of the Corporate Defendants (the Capital Gains Issue);

2. whether investors are entitled to claim against the Common Fund in respect of investments which do not relate to any particular Scheme (such as the “War Chest”, the “Project Reserve Bonds”, the “LGH Joint Ventures” or the “LGH Development JVs”) (the War Chest Claim);

3. whether investors are required to account for any payments received by the investors from the Corporate Defendants in respect of their investments in the Schemes (including payments described as periodic “distributions”, “capital returns” or “capital gains”) in making their Claims against the Common Fund (the Prior Distribution Claims); and

4. if investors are required to account for any payments received, how that accounting ought to take place (the Accounting Issue).

It would appear that some of the uncertainties foreshadowed by the Receivers at the time of the Pooling Orders have eventuated and are now defined.

12 By an interlocutory process dated 4 October 2012, the Receivers sought directions under ss 1323 and 601EE(2) of the Corporations Act, alternatively under ss 23 and 57 of the Federal Court of Australia Act 1976 (Cth) and paragraph 29 of the Orders made by the Court on 25 February 2010. The other bases for relief were abandoned. The directions sought were and remained:

1. A direction that, in adjudicating the Claims of members of the Schemes to the Common Fund for the purposes of paragraph 1(b) of the Pooling Orders and determining members’ entitlements to receive a distribution from the Common Fund, the Receivers are justified in:

(a) determining a member’s total contributions to the Schemes by reference to the amounts actually paid by the member to one of the Corporate Defendants in respect of that member’s investment in the Schemes and excluding any “capital gains” or other “entitlements” reported by any of the Corporate Defendants to the member;

(b) including in a member’s contributions to the Schemes any amounts paid by a member to a Corporate Defendant in respect of:

(i) the “Project Reserve Bonds”;

(ii) the “War Chest”; and

(iii) the “LGH Development JVs” or “LGH Joint Ventures”,

and any other investments which did not relate to a specific project, property or Scheme;

(c) requiring members of the Schemes who have made a Claim against the Common Fund to account, in accordance with paragraph 1(d), for all payments which the member has previously received from any of the Corporate Defendants in respect of the member’s contribution to any of the Schemes, including:

(i) all periodic payments whether described by the Corporate Defendants at the time as “distributions”, “interest”, “income” or otherwise; and

(ii) all other payments whether described by the Corporate Defendants at the time as “capital returns”, “capital gains” or otherwise,

(collectively, the Payments Received); and

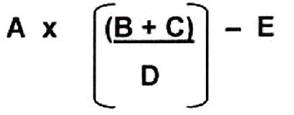

(d) determining a member’s entitlement to receive a distribution from the Common Fund in respect of a Claim in accordance with the following formula:

where:

(i) “A” means that member’s total contributions in respect of the Schemes determined in accordance with paragraphs (a) and (b) above;

(ii) “B” means the total of all funds in the Common Fund which are available for distribution;

(iii) “C” means the total Payments Received by all members who have made Claims on the Common Fund (which have not been withdrawn or rejected in part or in full);

(iv) “D” means the total of all Claims (which in respect of members of each of the Schemes, represents members’ total contributions to the Schemes as determined in accordance with paragraphs (a) and (b) above) which have not been withdrawn or rejected in part or in full; and

(v) “E” means the Payments Received by that member.

2 Orders that, to the extent that there is any inconsistency between the directions sought in paragraphs 1(c) and (d) above and the Pooling Orders, paragraphs 1(c) and (d) of these orders are to prevail.

3 Orders that nothing in paragraphs 1 or 2 above is to affect the rights of any person to claim that they have, or any other person has, an entitlement to distribution from an asset of a Scheme or a Corporate Defendant (or the proceeds of sale of such asset) which differs from the distribution which they would receive pursuant to the directions sought in paragraphs 1 and 2 or under the Pooling Orders.

Those directions were opposed by Light Investments Pty Ltd (Light Investments), appointed by the Court to act as a contradictor. Mr Kelly SC and Mr Costello appeared on behalf of Light Investments. Their written and oral submissions were of considerable assistance in the determination of the Receivers’ application for directions.

13 These reasons for judgment will address each issue in turn – the Capital Gains Issue, the War Chest Issue, the Prior Distributions Claims and then the Accounting Issue.

CAPITAL GAINS ISSUE

Introduction

14 Throughout the life of the various Schemes, a number of investors were advised by the Corporate Defendants that they had made a “capital gain” on their investment in the Schemes. In each case, the so called “capital gain” was declared but not returned or paid to the investors at the time that it was declared. Under the Pooling Orders, investors are entitled to claim for their “net contributions” to the Schemes: see definition of “Claim” at [3] above. The issue about which the Receivers seek a direction is whether a declared but unpaid “capital gain” should be construed as a “contribution” by an investor to a Scheme.

Receivers’ contention

15 The Receivers contended that, from the manner in which the Schemes operated, it was likely that, in many cases, those reported “capital gains” did not reflect any underlying financial state of the relevant Scheme. Further, due to the inextricable mixing of funds, and based on the conclusions reached by the Court in the Pooling Judgment (see [6] above), the Receivers submitted that any “capital gain” on an individual project should, in effect, be “pooled”. Indeed, the Receivers submitted that there was no reason why a purported “capital gain” on an earlier project ought to be treated any differently than, say, the gain on the Nicholson Street project which was realised upon the sale of the relevant property: see the Pooling Judgment at [336]. Accordingly, the Receivers submitted that any “capital gains” declared but unpaid by the Corporate Defendants in respect of investors’ investments in the Schemes do not form part of investors’ “net contributions” to the Schemes and that investors ought not be entitled to claim on the Common Fund in respect of any such “capital gains”.

Contradictor’s contention

16 The Contradictor opposed the direction sought by the Receivers on three bases. First, the Contradictor submitted that the Receivers have not adduced evidence to establish how or why “capital gains” declared but unpaid should not be recognised as a “contribution” in the proof of debt process. Secondly, the Contradictor submitted that any declared “capital gains” do not comprise “scheme property” but rights in the hands of the investors against the fund comprised by the scheme property which are analogous with units in a registered managed investment scheme or shares issued by a company pursuant to a dividend reinvestment scheme and, thirdly, that the directions now sought by the Receivers would have the effect of expropriating those declared entitlements and would thereby disentitle long term investors from vindicating those rights.

Analysis and conclusion

17 I reject the Contradictor’s submissions.

18 First, the Contradictor’s assertion that the Receivers have not adduced evidence to establish how or why such “capital gains” as were declared but unpaid should not be recognised in the proof of debt process is not correct. Evidence was tendered by the Receivers of investors who claimed amounts for allegedly reported but unpaid “capital gains” at the end of the term of each investment and which they contended they had reinvested. So, for example, the proofs lodged by Investor A and Investor B were in evidence. The proofs identified the “capital gain” as part of their Claim and provided documentary material (in the form of correspondence and other documents) in support of the Claim. Investor A and Investor B claimed the following amounts for allegedly reported but unpaid “capital gains”:

1. $4,800 in respect of an initial investment of $30,000 in the Tomasetti House Joint Venture;

2. $4,500 in respect of an initial investment of $300,000 in Low Head Beach Front Village Part 1;

3. $5,140 in respect of an investment in Low Head Beach Front Village Part 2; and

4. $3,000 in respect of an initial investment of $20,000 in Moorhouse Shopping Centre Project Part 1.

19 The fact that the evidence did not disclose how or why the “capital gains” were declared is not surprising. As was explained in the Pooling Judgment at [29]:

The form and timing of the investment in each Scheme was not consistent within Schemes or between Schemes. Some investors executed joint venture agreements. Other investors bought or invested in what were described as “equity deposit bonds” or “equity mortgage investments”. Others appear to have contributed money to the Scheme without executing any documentation. Other investments occurred by way of “rollovers” from other Schemes. Some investors invested after the asset was bought. Others invested before the asset was acquired. Some investors fall into more than one of these categories. The varying forms of investment are complicated further by the fact that many Schemes received contributions through a combination of these methods.

20 By way of further example, in relation to the Tomasetti House Joint Venture, the Pooling Judgment addressed the “terms” of the so called “capital gains” and the issues that were created in the following terms:

182. One of the undated screeds offered investors the opportunity to participate in a joint venture with LGHH. The proposal was to lease the building for 18 months and redevelop the site. The proposal offered investors a 12 month investment with a predetermined income and capital gain return. The “income” return was net income of 9% paid monthly. The capital return was 10% payable on or around 31 January 2005. The amount to be subscribed was $1.5 million. However, one of the “2005” joint venture agreements produced by the Receivers only provided for the latter (a capital return).

183 In the joint venture agreements, the recitals provided that:

The Investors and the Manager have agreed to associate themselves as Joint Venturers for the purpose of acquiring an Interest in the Tomasetti House 277-279 Flinders Lane, Melbourne Project (hereinafter defined) and to hold the same as an investment and to earn income therefrom (“the Project”).

As with other Schemes, the phrase “Tomasetti House 277-279 Flinders lane, Melbourne Project” was not defined. “Interest” was defined as a “share or interest in the investment known ‘the Project’”. The manager for the joint venture was Melville Corporation Pty Ltd, the 46th defendant (Melville).

184 No documentation in relation to the subsequent investments by investors was produced.

185 Notwithstanding the terms of the screed and the joint venture agreement, over the life of the Scheme:

1. investors contributed $8.68 million;

2. the over-funding at the time of acquisition of the property was $2.3 million and was retained by LGHA;

3. the extent of the refurbishment was reduced (approximately $1.084 million was spent on capital expenditure). LGHA continued to retain the surplus;

4. investors received distributions of $2.4 million; and

5. investors received returns of capital of $3.03 million.

186. LGHA may be understood to have performed a central treasury function. LGHA collected all receipts from any debt or investment raising. It also funded distributions to investors, received rental income receipts from tenants and settled amounts owing to third party suppliers / financiers of Melville. The Receivers suggest that it was possible that moneys advanced to LGHA by investors in other Schemes were used to acquire and develop the property or to make payments to investors in this Scheme or both and that the funds of this Scheme which were held by LGHA were used to meet demands in other schemes.

(Emphasis in original.)

As is self evident, the documentation was inconsistent between investors in the same Scheme and the funds invested and distributed did not reflect reality.

21 That conclusion also addresses the Contradictor’s next contention concerning the nature of any “capital gain”. The Contradictor was right to contend that there was no evidence which identified the “nature” of any alleged but unpaid “capital gain”. That is unsurprising. There was no evidence to suggest that any of the Schemes identified in the relevant proofs did in fact generate a “capital gain” capable of being declared and distributed. And, in light of the findings in the Pooling Judgment, it is neither necessary nor appropriate for the Receivers to ascertain whether any “capital gain” was capable of being declared and distributed: see [19] above. Next, even if any particular declared but unpaid “capital gain” reflected an actual capital gain realised in respect of a particular project, due to the historical operation of the various projects as one mixed fund (see Pooling Judgment at [250]-[260]):

1. each of the investors in all of the Schemes would be entitled to a share of any “capital gain” realised in respect of any project as the investors’ equitable charge over the mixed fund would attach to that “capital gain”;

2. to the extent that any “capital gain” has been declared in favour of any particular investor, the effect of that declaration (if recognised) would be to deprive other investors of the benefit of that “capital gain”; and

3. the only equitable approach is for all “capital gains” on individual projects to be, in effect, “pooled”.

22 In those circumstances, it is neither possible nor appropriate to treat a declared but unpaid “capital gain” in a Scheme as a “contribution” by an investor for the purposes of determining that investor’s Claim on the Common Fund.

23 The exclusion of any declared but unpaid “capital gain” from an investor’s “net contributions” would extend to include any “capital gains” “rolled over” and “reinvested” in a Scheme. As with a declared and unpaid “capital gain”, it cannot be said that an investor who was informed of a declared and unpaid “capital gain” and then rolled it over “contributed” that amount to a Scheme. If a “capital gain” allegedly rolled over was recognised as a “contribution” by an investor, it would recognise a fiction. The fiction would be to treat a “capital gain” (cf Re York Street Mezzanine Pty Ltd (in liq) (2007) 162 FCR 358 at [26]) as declared, paid and reinvested when the declaration of the “capital gain” did not reflect factual or legal reality. In relation to a declared but unpaid “capital gain”, the legal basis for a “capital gain” by any particular investor in a particular Scheme to be declared was and remains in doubt: see [20] above.

24 Moreover, there is another matter which must be borne steadily in mind. The investors’ claims to the mixed fund (now defined as the Common Fund) did not spring into existence when the Court appointed the Receivers or on the making of the Pooling Orders. The investors’ claims arose immediately when moneys paid by the investors to one or more of the Corporate Defendants on trust were mixed together with other moneys held on other trusts. The mixing was complex: see the Pooling Judgment at [252]-[257]. No less significantly, on the declaration of a “capital gain” which was unpaid, no money left the mixed fund and no money entered the mixed fund. No amount was in fact paid and reinvested.

25 For those reasons, the Receivers are entitled to a direction that in adjudicating the Claims of members of the Schemes to the Common Fund for the purposes of Pooling Order 1(b) and determining members’ entitlements to receive a distribution from the Common Fund, the Receivers are justified in:

(a) determining a member’s total contributions to the Schemes by reference to the amounts actually paid by the member to one of the Corporate Defendants in respect of that member’s investment in the Schemes and excluding any “capital gains” or other “entitlements” reported by any of the Corporate Defendants to the member; …

WAR CHEST ISSUE

Introduction

26 There were investors who invested moneys in the “War Chest”, in the “Project Reserve Bonds”, in the “LGH Development JVs” or the “LGH Joint Ventures” rather than investing in a specific property development or project.

27 The evidence before the Court discloses that:

1. the LGH Companies solicited “equity” investments in the War Chest and the Project Reserve Bonds in the 2009 financial year from existing investors expressly to help protect the Schemes during the global financial crisis and to avoid immediate liquidation of Scheme assets by way of “fire sales”;

2. the majority of the investors who contributed moneys to the War Chest and the Project Reserve Bonds were already investors in one or more of the Schemes. The funds which were raised in respect of these investments were:

2.1 $767,000 in respect of the War Chest;

2.2 $565,150 in respect of the Project Reserve Bonds;

3. funds appear also to have been contributed by investors in respect of the “LGH Development JVs” and the “LGH Joint Ventures”;

4. it is likely that the funds contributed by investors to the War Chest, Project Reserve Bonds, LGH Development JVs and LGH Joint Ventures:

4.1 were intermingled with investors’ contributions to the Schemes and the assets of the Schemes generally; and

4.2 were applied by LGHA and the other Corporate Defendants in the same way as the funds which were contributed by investors specifically in relation to one of the Schemes.

28 There are other complicating factors. The terms of the War Chest investment were less than settled. The “screed” for the War Chest indicated that the intended purpose of the War Chest was to build cash reserves to create a “fire wall of protection around the LGH Projects to get us through”. The screed stated that:

The vast majority of LGH Joint Venture Participants are in numerous Projects across the Group.

Therefore the plan is designed that takes into account the Projects totally, not Project by Project.

29 Other marketing material provided to investors in relation to the War Chest described the purpose of the War Chest as follows:

1. to “stabilise the value of the Projects”;

2. to “build a pool of cash funds to buffer the Projects against the ‘market storms’”;

3. to “make sure our Banks are comfortable and supportive”;

4. to “ultimately sell each Project for value”;

5. to “at worst achieve our capital returned”;

6. “the ultimate aim is to get our capital through this period of melt down unscathed”; and

7. to “build security around the Projects in the short term”.

30 It is also not entirely clear what were the terms of the Project Reserve Bonds investment. The screed for the Project Reserve Bonds described the nature of the Project Reserve Bonds investment as follows:

1. $2.5 million to be raised;

2. $2.5 million raised will be directed to a special purpose company;

3. the special purpose company would then purchase bank term deposits or bills of exchange to the value of $2.5 million (issued by one of the four major banks in Australia);

4. the Project Reserve Bond would be used or pledged against the equity held by the LGH Projects;

5. the LGH Projects would repay in the first instance any advances secured by the Project Reserve Bond;

6. each Investor would be paid a monthly income plus an accrued gain at the end of the 12 month period;

7. the gain would be funded by LGH and unrealised gains held by the joint venture participants; and

8. the anticipated net income was 6% per annum and an estimated 14% gain on the capital invested.

31 The position in relation to the terms of the LGH Development JVs or the LGH Joint Ventures is less clear. The evidence discloses that at least one investor believed that the LGH Development JVs was simply a rollover of an earlier investment in a Scheme. Most recently, Mr Letten’s solicitors wrote to the Receivers and told them that their instructions were:

… that neither LGH Development Bonds nor LGH Development Joint Ventures were investments. … [T]hese were classification devices used to describe money in LGH’s accounts that had not yet been allocated to particular joint venture projects.

So, for example, a proof of debt lodged by one investor claims $178,875 in respect of four separate investments in “LGH Development JVs”. None of the LGH Development JVs was a Scheme.

32 What then is the position? Investors in the War Chest, the Project Reserve Bonds, the LGH Development JVs or the LGH Joint Ventures were, save in one case (see [31] above), already investors in one or more of the Schemes. For example, Investors D, E, and F were investors who had investments in a number of the Schemes and also an investment in the War Chest, the Project Reserve Bonds, the LGH Development JVs or the LGH Joint Ventures. Further, the one investor in the LGH Development JVs who was not also an investor in a Scheme was connected with other entities which had many and various investments in the Schemes.

33 An analogous position was considered in the Pooling Judgment (at [242]-[248]) in respect of investments by way of equity deposit bonds, equity mortgage investments and contributions in the absence of a joint venture agreement in respect of each of the Schemes. The conclusion reached was that those investments were received by LGHA (or the relevant Corporate Defendant) subject to a trust in favour of the investors even though the terms of the relevant instruments did not expressly create a trust because:

1. the responsible entity of a registered managed investment scheme is required, pursuant to s 601FC(2) of the Corporations Act, to hold scheme property on trust for scheme members; and

2. if an arrangement is required to be registered as a managed investment scheme (but is not), then “by force of the legislation, scheme property is to be held on trust by the responsible entity”: Brookfield Multiplex Ltd v International Litigation Funding Partners Pty Ltd (2009) 180 FCR 11 at [64].

As a result, investors by way of equity deposit bonds, equity mortgage investments and contributions in the absence of a joint venture agreement were entitled to claim against the Common Fund.

34 The status of the investments in the War Chest, the Project Reserve Bonds, the LGH Development JVs or the LGH Joint Ventures which did not relate to any particular Scheme was not addressed in the Pooling Judgment because the facts set out at [27]-[32] above have only emerged as a result of the Receivers’ further enquiries.

35 The question now raised is whether these investments constitute contributions to the Scheme or Schemes, proprietary claims against the Common Fund, or whether these investors are merely unsecured creditors of LGHA.

Receivers’ submissions

36 The Receivers submitted that investors ought to be able to include their contributions to the War Chest, the Project Reserve Bonds, the LGH Development JVs or the LGH Joint Ventures in their Claims against the Common Fund for the purposes of the Pooling Orders on the basis that:

1. these contributions were likely made by investors to preserve other investments in specific Schemes; and

2. these investments may have come about as the result of the rollover of an investment in one of the Schemes; and

3. these contributions were intermingled with investors’ other contributions to specific Schemes and were applied by LGHA and the other Corporate Defendants in the same way as the funds which were contributed by investors specifically in relation to one of the Schemes.

Accordingly, the Receivers submitted that the contributions to the War Chest and Project Reserve Bonds, LGH Development JVs or LGH Joint Ventures formed part of the investors’ “total net contributions to the Scheme or Schemes” for the purposes of the definition of “Claim” in the Pooling Orders.

Contradictor’s submissions

37 The Contradictor submitted that the investors’ contributions to the War Chest and the Project Reserve Bonds were in the nature of a loan and not moneys contributed on trust. To understand the force of that submission, it is necessary to set out the facts relied upon by the Contradictor.

38 First, the Contradictor referred to the fact that the terms of these various direct forms of investment are not clear. That is apparent from the summary at [27]-[31] above. Indeed, the LGH Companies’ Report included a graph which confirmed the paucity of reliable information for the 2002-2008 financial years for the accounts designated “NAB – LGH”, which related to the War Chest.

39 By way of emphasis, the Contradictor referred to what it described as “another problematic feature” of the War Chest “investments”. Although the investment was described in the screed as “The Property Projects 3% Plan”, the War Chest did not involve any promise that the investment would accrue interest at 3%. Instead the “plan” was, as noted earlier, expressly directed to raising a fund “[t]o help get us all through unscathed”. The Contradictor submitted that the reference to 3% was clearly directed to investors effectively advancing 3% of their capital to the War Chest on terms that it was repayable (without interest) after 12 months. The Contradictor submitted that those investors could never have reasonably expected any return, apart from repayment of their capital.

40 Accordingly, the Contradictor submitted that an advance of these kinds was far more easily characterised as moneys paid on loan than on trust.

Analysis and conclusion

41 These “contributions” may be divided into two general classes. The first class comprises those payments made by investors to preserve investments in other specific Schemes: the War Chest and the Project Reserve Bonds. Having regard to the stated purpose of each of those investments (see [27]-[30] above), it is appropriate to treat the investors in the War Chest and the Project Reserve Bonds as having a claim on the Common Fund. Those investments were subject to a trust, notwithstanding that the relevant instruments did not provide so expressly.

42 The second class includes two categories of investors; the investments that came about as the result of the rollover of an investment in one of the Schemes and a related category of investments waiting allocation to a particular joint venture project. Having regard to the stated purpose of those investments (see [27]-[31] above), and the new instructions provided by Mr Letten in relation to the LGH Development JVs, it is appropriate to treat investors in the LGH Development JVs and the LGH Joint Ventures as having a claim on the Common Fund. As was said in the Pooling Judgment (at [335]):

… In relation to investors whose contributions to Schemes are not governed by joint venture agreements, the claims are substantially equal to the claims of those who contributed by joint venture agreements. Their funds were treated on the same basis by LGHA (and the other Letten Entities) and by the other Corporate Defendants. To adopt the same language as the Court of Appeal in Lehman Brothers, the investors suffered a “common misfortune”, and any method of distribution should reflect that fact.

43 For those reasons, the Receivers are entitled to a direction that investors ought to be able to include their contributions to the War Chest, the Project Reserve Bonds, the LGH Development JVs or the LGH Joint Ventures in their Claims against the Common Fund for the purposes of the Pooling Orders. Investments in these non-Scheme specific investments ought to form part of investors’ “net contributions to the Schemes”.

PRIOR DISTRIBUTION CLAIMS

Introduction

44 This issue is complex. The facts are not in dispute. Significant amounts have been paid to many investors over the life of the Schemes, including:

1. approximately $38 million of “distributions” which were paid to investors over the life of the Schemes but which exceeded profits generated by the Schemes and may have been funded by other investors and/or other Schemes; and

2. approximately $18 million described as return of investor capital.

45 As a result of the overpayments of “distributions” to investors, investors in the Schemes have been receiving distributions from their own and from other investors’ money. In fact, the total payments received by many individual investors in respect of their investments in the Schemes are significant and far exceed the 8 to 10 cent in the dollar return which the Receivers have previously estimated that Claimants will receive on their Claims from the Common Fund. Indeed, in some cases, the amounts received by investors in respect of their investments in the Schemes exceed the amount initially contributed by the investors to the Schemes. So, for example, the evidence demonstrates that:

1. Investor K received total payments of:

1. $23,045.01 in respect of its initial investment of $60,000 in 211 Wellington Road (a return on investment of 38.4%);

2. $114,302.26 in respect of its initial investment of $80,000 in Aurora Park Project Lots 9 and 13 (a return on investment of 142.88%); and

3. $187,319.57 in respect of its initial investment of $126,562.50 in Heritage Stage 2A (a return on investment of 148%).

2. Investor L and Investor M received total payments of:

1. $32,681 in respect of their initial investment of $50,000 in The Glen Centre (a return on investment of 65.36%);

2. $15,510 in respect of their initial investment of $50,000 in George Street (a return on investment of 31.02%); and

3. NZ$22,280 in respect of their initial investment of NZ$20,000 in Moorhouse (a return on investment of 111.4%).

3. Investor N received total payments of:

1. $97,679 in respect of her initial investment of $135,000 in The Glen Centre (a return on investment of 72.35%);

2. $88,451 in respect of her initial investment of $100,000 in Healesville Walk Shopping Centre (a return on investment of 88.45%);

3. $45,484 in respect of her initial investment of $70,250 in Sebel Lodge (a return on investment of 64.75%);

4. $12,750 in respect of her initial investment of $30,000 in Yarra Valley St John’s clubhouse (a return on investment of 42.5%);

5. $5,950 in respect of her initial investment of $14,000 in Yarra Valley 16th fairway (a return on investment of 42.5%); and

6. $0 in respect of her initial investment of $3,000 in Yarra Valley HGCC S10 (a return on investment of 0%).

46 However, other investors are in a radically different position. Some investors in certain Schemes did not receive any “distributions” or “capital returns” over the life of their investments in the Schemes.

Receivers’ submissions

47 As noted at [3] above, the Pooling Orders provided that investors are only entitled to claim against the Common Fund for their “total net contributions to the Scheme or Schemes”. The Receivers submitted that, in identifying investors’ “total net contributions”, the Court ought to have regard to the principle that a person seeking to participate in the distribution of a fund must bring into hotchpot the benefits already received by that claimant from the fund: Re French Caledonia Travel Services Pty Ltd (in liq) (2003) 59 NSWLR 361.

48 In short, the issue is whether the investors are required to account for all payments received in respect of their investments in the Scheme (whether those payments were described by the Corporate Defendants as “distributions”, “income”, a “capital gain” or a “capital return”) in calculating their Claim on the Common Fund. The Receivers seek a direction to that effect.

Opposition to the direction sought

49 The Contradictor opposed the direction sought by the Receivers. Other investors also filed submissions opposing the directions. The substance of the objections was not substantially different. The Contradictor’s grounds of opposition were directed at identification of the Common Fund and, having determined that question, identification of what was the appropriate methodology to be adopted in distributing that fund.

50 In that context, the Contradictor submitted that none of the prior distributions formed or were capable of forming part of the Common Fund and, consistent with the rule in Cherry v Boultbee (1839) 41 ER 171 (the Cherry v Boultbee Rule), there was no legal right to consider them in the calculation of an investor’s “net contribution”. The flip side of the Contradictor’s submission was that “the so-called hotchpot principle” was little more than a label under which specific rules have been collected with a common thread: he who seeks equity must do equity. In fact, the Contradictor submitted that the hotchpot principle does not bear a sound juridical foundation and is no more than a label to address a variety of competing and complex issues.

51 One investor, Mrs Avelsgaard, appeared and made oral submissions. Her submissions were directed and poignant. She and her husband had been investors in Letten related entities since about 1983. Mrs Avelsgaard raised two concerns. Her first concern was that a declared and unpaid “capital gain” would not be included as a “contribution” in the proof of debt process. Mrs Avelsgaard’s second concern was that the periodic payments that they had received should not be deducted in the calculation of their “net contributions”. As Mrs Avelsgaard told the Court, they believed that they should be entitled to claim the whole of their initial investment (without deducting any actual distributions received) because any distribution they in fact received was an interest payment according to the documents sent to them by the Letten Entities.

Analysis

52 The issue is controversial. The investors (like Mrs Avelsgaard) who received periodic payments obviously want to retain those payments. Those investors who did not receive any periodic payments (such as the “direct” YVG investors) have an interest in the other investors giving up the advantage of the periodic payments received by them before participating rateably in the Common Fund.

53 The controversy is exacerbated in the minds of the Contradictor and the other investors who oppose the order because they contend there has been a radical change in the position adopted by the Receivers. The basis for this contention is that, in the submissions filed by the Receivers in September 2010 in support of the initial pooling orders:

Investors would not be required to bring any distributions into hotchpot in order to make a claim on the Common Fund in respect of their contributions.

(Emphasis added.)

54 The Contradictor and the other investors who opposed the order contrast that statement with the Receivers’ current submissions that:

… the Court ought to have regard to the principle that a person seeking to participate in the distribution of a fund must bring into hotchpot the benefits already received by that claimant from the fund.

and that:

… the Investors must account for all payments received in respect of their investments in the Schemes (whether described as “distributions” or as “capital gains”) before participating rateably in the Common Fund.

The Contradictor and the other investors who opposed the order asserted that the diametric change in position was inexplicable.

55 Before turning to the substantive objections raised by the Contradictor, it is appropriate to say something about this alleged change of position by the Receivers. In my view, the complaint is misplaced.

56 The question of accounting for distributions was addressed factually and legally in the Pooling Judgment: see [7] above. The Pooling Orders were made on the basis that:

1. some investors had received distributions;

2. the Receivers acknowledged the observations of Campbell J in Re French Caledonia at [179]-[185] that a person seeking to participate in the distribution of a fund must “bring to hotchpot” the benefits already received by that claimant from the fund;

3. the Receivers submitted that the resolution of the investors’ entitlements with respect to distributions may depend, to some extent, on the representations that were made to each individual investor.

As a result, the Receivers submitted (and the Court accepted) that the issue of distributions, and any residual uncertainties in respect of other entitlements, would best be resolved as part of the proof of debt process. That is what occurred and that is the reason (or at least one of the reasons) for this application for directions.

57 What then were the parties’ respective submissions on the substantive question of how to treat the distributions to investors? The Receivers placed considerable reliance on the decision of Barrett J in Australian Securities and Investments Commission (ASIC) v Idylic Solutions Ltd; Australian Securities and Investments Commission v PJCB International Ltd (2009) 76 ACSR 129 (Idylic). In that case, Barrett J held that investors who received a monthly 3.5% “return” on their investments in two unregistered managed investment schemes were required to bring any returns received by them into hotchpot in reduction of their claims in the winding up of the unregistered managed investment schemes. In that case, the Court held that the “returns” were not distributions of profits but payments to early investors of capital contributed by themselves, and perhaps some later investors, in order to satisfy expectations of periodic returns created by the promotional literature (which referred to a “return objective” of 3.5%). There was a “Ponzi” aspect to the schemes. It was also relevant that the “returns” were paid inconsistently and contrary to the documentation which set out the basis on which each scheme had been promoted and established.

58 As a result of those matters, Barrett J held at [77] that:

… The recipients of the “returns” must, as against the other persons interested in the pooled fund as a whole, do equity by giving up the advantage of the “returns” before participating rateably in what remains of the fund.

59 The Receivers submitted that the position in respect of the Schemes was not distinguishable from that considered in Idylic:

1. the distributions paid to investors in the Schemes were not typically paid out of the profits of the Schemes and the payment of the distributions depleted the Common Fund;

2. the amounts paid to investors in the Schemes in respect of alleged “capital gains” typically did not reflect any capital gains made by the Schemes and the payment of “capital gains” depleted the Common Fund;

3. as a result of the overpayments of “distributions” to investors, investors in the Schemes have been receiving distributions from their own and from other investors’ money;

4. the payments made to investors were paid to investors in the Schemes inconsistently, with some investors receiving more than 100% return on their investment in a Scheme and other investors receiving 0% return on their investment in a Scheme.

60 It was for those reasons that the Receivers submitted that the investors must account for all payments received in respect of their investments in the Schemes (whether described as “distributions” or as “capital gains”) before participating rateably in the Common Fund. Why? Because “personal equities” have arisen so that investors seeking to claim against the Common Fund must bring into hotchpot the benefits already received by that claimant from the fund: Re French Caledonia. Indeed, the Pooling Orders were expressed to ensure that occurred: see [7] above.

61 In the present case, there is a complicating factor. The adoption of any approach to the distribution of the assets of the Schemes which permitted investors to retain even legitimate actual profits of the relevant Scheme would be difficult to justify in circumstances where investors in other Schemes would also have claims in respect of those profits owing to the operation of the Schemes as a mixed fund. Unlike the case in Idylic, the tension between the investors is not simply between investors who received periodic payments and those that did not but also between investors in profitable Schemes and investors in Schemes which were not profitable but whose contributions subsidised the profitable Schemes. The Receivers submitted that this complication provided a further reason why investors ought to be required to bring all payments received in respect of their investments in the Schemes (including “distributions” and “capital gains”) into hotchpot so that those payments can, in effect, be pooled. I agree.

62 As noted above, the Contradictor’s submissions were that, consistent with the Cherry v Boultbee Rule, investors who received distributions of any description were not under a legal liability to pay or restore that amount to the Common Fund and therefore were not obliged to bring all payments received in respect of their investments in the Schemes (including “distributions” and “capital gains”) into hotchpot so that those payments could, in effect, be pooled.

63 The Contradictor’s focus on the Cherry v Boultbee Rule was misplaced. Even if the rule were able to be stated in such precise terms (a matter that does not need to be resolved in the present case), that rule does not, and cannot, apply to a case such as the present where the Court has determined that by reason of a complex web of equitable charges the assets of the Schemes should be pooled and that tracing should not occur.

64 As the Court stated in the Pooling Judgment:

258. Given the complexities associated with the financial and accounting data (or lack of it), the Receivers concluded that to attempt to reconstruct the LGHA accounts, the Investor Current Accounts and to attempt to trace the approximately 110,000 transactions which took place in relation to the LGHA bank accounts plus the distributions to investors would cost approximately $18 million. That cost is prohibitive. As the Receivers stated in the LGH Companies’ Disclosure Report it would not “be justifiable to incur any further costs in the tracing exercise in circumstances where it is clear that the tracing exercise cannot be completed”.

259. Even if the tracing exercise could be completed (and it cannot), in the circumstances of this case it is not justifiable to reduce the available funds for distribution to investors by $18 million (the approximate cost of the tracing exercise) out of a possible fund of $13 to 14 million (after payment of secured creditors) because:

1. The funds contributed by investors in each of the Schemes were paid directly by investors to LGHA or another Letten Entity rather than to the manager of the relevant Schemes;

2. None of the Corporate Defendants beneficially own any assets which are not property of one or more of the Schemes;

3. Funds contributed by investors in each of the Schemes were mixed and commingled in common bank accounts of LGHA;

4. The proceeds of sale of a number of the Scheme properties which were sold prior to the appointment of the Receivers were also paid to the Letten Entities and were mixed and commingled in the bank accounts of LGHA;

5. The Letten Entities applied the mixed investor funds and the proceeds of sale of various Scheme properties to the assets of other Schemes by way of:

5.1 the purchase and development of individual properties;

5.2 the operation and maintenance of individual properties;

5.3 the payment of distributions to investors; and

5.4 some limited returns of capital to certain investors;

6. The books and records of each of the Schemes (as interpreted and adjusted by the Receivers) describe the assets of each Scheme as an identified property development (unless that asset has been sold) with or without a loan receivable from LGHA;

7. The books and records of each of the Schemes (as interpreted and adjusted by the Receivers) describe the liabilities of each Scheme as the secured and unsecured debts of the relevant Corporate Defendant with or without a loan payable to LGHA;

8. The books and records of LGHA refer to LGHA as having net assets of $21.1 million which primarily relates to LGHA’s “net contributions in the projects” (NCIP) and some ancillary matters;

9. The books and records of each of the Schemes and the Corporate Defendants (including the Letten Entities) cannot be reconciled, the balances of the intercompany loans and the NCIP (as described in the relevant books and records) cannot be verified and individual investors’ contributions cannot be traced into particular properties because even with the expense of a full reconstruction, the accounts may not reconcile;

10. Any tracing exercise would confirm that various investors have an interest in common assets (such as the assets of the YVG Joint Venture) and various investors have an interest in funds or property in the hands of investors in other Schemes.

65 In other words, contrary to the Contradictor’s submissions, the prior distributions did form or were capable of forming part of the mixed fund (now defined as the Common Fund) and the Cherry v Boultbee Rule is inapplicable. The rule is inapplicable because, as was explained earlier, the investors’ claims against the mixed fund (now defined as the Common Fund) did not spring into existence when the Court appointed the Receivers or on the making of the Pooling Orders. The investors’ claims against the mixed fund arose immediately when moneys paid by the investors to the Letten entities on trust were mixed together with other moneys held on other trusts.

66 The mixing was complex: see [256] of the Pooling Judgment. As a result of the payment out of a distribution to an investor (and each subsequent distribution to an investor), the payment was out of property over which already existed a complex set of equitable charges in favour of a number of investors. On each distribution (and other uses of the mixed fund) by the Letten Entities, a different combination of equitable charges sprang into existence. The web of charges was necessarily complex. The fund was inextricably mixed. It was these facts that formed part of the foundation for the Pooling Orders. The Receivers have accepted for the purposes of the administration of these entities that there is no right on the part of the Receivers in their capacity as receivers of entities or funds to recover moneys that were paid, whether by way of distributions or capital returns, to investors. As Counsel for the Receivers submitted, that position has been adopted because it would not be possible to trace the moneys distributed to investors into some asset in the hands of the investors: cf Georges v Seaborn International (Trustee), Re; Sonray Capital Markets Pty Ltd (in liq) (2012) 87 ACSR 442 at [83].

67 The conclusion that the distributions formed part of the mixed fund from the outset may be tested as follows. If when money was paid to an investor, it was possible to stop the clock, that money would have been subject to a charge held by all the other investors who had directly and indirectly funded that payment. And if the clock had been stopped, it would have been possible to seek the return of that distribution to the mixed fund before the investor disposed of it. That did not occur. It is those facts, which have remained unchanged since each distribution was made, that provide the foundation for the personal equity of the kind described by Campbell J in Re French Caledonia at [179]-[185].

68 The Contradictor placed considerable reliance upon the decision of the Privy Council in Cleaver v Delta American Reinsurance Co (in liq) [2001] 2 AC 328 as authority for the proposition that the hotchpot requirement does not apply to assets that never formed part of the common fund. The decision in Cleaver is distinguishable on its facts. It concerned a company being wound up in liquidation. The identity of the fund was therefore important. The date of the existence of the fund, as well as the components of it, was prescribed by the relevant statutory framework. What was in issue was whether assets that were acquired before the commencement of the relevant fund and assets that never formed part of the fund were able to be included in a fund which sprang into existence on the winding up of the corporation. That is not this case. The situation addressed in Cleaver is factually and legally different.

69 One issue addressed in Cleaver was whether (in the circumstances of that case or at all) it was open to extend the hotchpot rule to cater for what were described as cases of “unfair advantage”: at [35]. Their lordships rejected extending the principle stating that to do so would “introduce inherent uncertainty into what ought to be, and at present is, a rule easy to understand and apply”. That raises the next limb of the Contradictor’s submission - that the hotchpot principle lacks a sound juridical basis and is little more than a label under which specific rules have been collected with a common thread: he who seeks equity must do equity.

70 In Re French Caledonia, Campbell J described the hotchpot principle as comprising the following elements at [176]-[185]:

1. each person who had made contributions to the fund had an interest in the fund (by way of contingent resulting trust) to the extent that it was not distributed according to the rules of the fund;

2. where the resulting fund was a “mixed fund” of every member’s contributions, each member had an equitable charge over the fund to support their interest;

3. each member was required to bring into hotchpot benefits from the fund;

4. the “requirement” that each member bring into hotchpot benefits from the fund was:

… an illustration of a personal equity which results in the charge which one contributor has being held to be of lower priority than the charge which another contributor has, though with the possibility of becoming of equal ranking if one of the chargees performed an action which he had no obligation to perform, but the performance of which was a precondition to his charge being accorded equal rank.

71 A similar issue was considered in Idylic. There the Court was concerned with the distribution of two funds which had operated over a three-year period. Towards the end of the three years there was a degree of intermingling between the two funds. As a result of that intermingling, the contributors to one of the funds obtained a benefit which the contributors to the other fund did not receive. In addition, during the life of each fund, the contributors had received “returns” which were not distributions of profits but, in effect, repayments of capital paid “in order to satisfy expectations of periodic returns generated by the promotional literature”. The rules of the two funds did not make any provision for the repayment of capital except upon notice of withdrawal given after the expiration of the minimum investment period. There were two hotchpot questions in Idylic; how to treat the disparity in benefits arising from the intermingling of the two funds and how to treat the payment of the returns. Barrett J dealt with the second question first.

72 Justice Barrett traced broadly the origins and development of the hotchpot principle through a number of disparate areas from the enactment of the Statute of Distributions 1670: at [54]-[60]. After referring to the fact that the returns with which he was dealing were not in truth distribution of profits and that their payment “was not in accordance with the basis upon which each scheme has been promoted and established”, he concluded at [77]:

… personal equities can be seen to exist between the recipients of “returns” and other contributors to a particular scheme causing those recipients to merit a lower priority as to participation in the fund, which relegation will, however, be eliminated if the “returns” are brought into hotchpot. ... there must be an account of the “returns” in order to ascertain the whole of each remaining fund to which the principle of division in proportion to contributions is to be applied. The recipients of the “returns” must, as against the other persons interested in the pooled fund as a whole, do equity by giving up the advantage of the “returns” before participating rateably in what remains of the fund.

73 The juridical foundation for the hotchpot principle is clear. It comprises the elements summarised at [70] above. Its rationale is simply stated – if Investor A received money from a mixed fund with the consequence that other peoples’ (Investors B to Z) property interests in that money were extinguished or diminished, it would be unconscionable for Investor A with knowledge of that fact to claim to rank equally with Investors B to Z in relation to the balance of the mixed fund whilst retaining all of the benefit of the payment from property over which Investors B to Z used to have, but no longer had, any proprietary claim.

74 What then is the position here? The property which is the subject matter of the directions sought by the Receivers is the Common Fund. What comprises the Common Fund was resolved in the Pooling Judgment. The remaining question is how are particular claims on that Common Fund to be determined? In particular, should those investors who received distributions or returns be asked to do equity in order to rank equally with investors who have not received distributions? In my view, they should. Personal equities exist between those investors who received distributions and those investors who did not receive distributions such that the equitable charge held by those investors who received the distributions should only be afforded an equal priority to the equitable charge held by investors who have not received distributions once all distributions have been brought into hotchpot.

75 As Barrett J stated in Idylic, “[t]he recipients of the “returns” must as against the other persons interested in the pooled fund as a whole do equity by giving up the advantage of the ‘returns’ before participating rateably in what remains of the fund”. Of course, investors who received distributions may elect not to share in the distribution of the Common Fund in which case the distributions they have already received will not form part of the Common Fund.

76 The Receivers’ submissions acknowledged that if the balance of the Common Fund is distributed in the manner outlined it does not recognise differences (if any) between the investors by reference to the period of time their moneys were contributed to the funds.

77 After the hearing, the Contradictor drew the Court’s attention to the recent decision of the High Court in Stanford v Stanford [2012] HCA 52 (15 November 2012). Stanford was a further illustration of the principle that statute may provide for orders affecting existing proprietary interests. The decision dealt with Part VIII (ss 71-90) of the Family Law Act 1975 (Cth) (the Family Law Act) and, in particular, the requirement in s 79(2) of the Family Law Act that a court shall not make a property settlement order unless satisfied that it is “just and equitable” to do so: see also s 79(4). The majority of the Court described the expression “just and equitable” in s 79(2) as follows:

36 The expression “just and equitable” is a qualitative description of a conclusion reached after examination of a range of potentially competing considerations. It does not admit of exhaustive definition. It is not possible to chart its metes and bounds. And while the power given by s 79 is not “to be exercised in accordance with fixed rules”, nevertheless, three fundamental propositions must not be obscured.

37 First, it is necessary to begin consideration of whether it is just and equitable to make a property settlement order by identifying, according to ordinary common law and equitable principles, the existing legal and equitable interests of the parties in the property. …

38 Second, although s 79 confers a broad power on a court exercising jurisdiction under the Act to make a property settlement order, it is not a power that is to be exercised according to an unguided judicial discretion. In Wirth v Wirth, Dixon CJ observed that a power to make such order with respect to property and costs “as [the judge] thinks fit”, in any question between husband and wife as to the title to or possession of property, is a power which “rests upon the law and not upon judicial discretion”.

…

40 Third, whether making a property settlement order is “just and equitable” is not to be answered by beginning from the assumption that one or other party has the right to have the property of the parties divided between them …. The power to make a property settlement order must be exercised “in accordance with legal principles, including the principles which the Act itself lays down”. To conclude that making an order is “just and equitable” only because of and by reference to various matters in s 79(4), without a separate consideration of s 79(2), would be to conflate the statutory requirements and ignore the principles laid down by the Act.

(footnotes omitted.)

78 The Contradictor submitted that this decision provides further support for the contention that the parties’ relevant contributions to the pool – including the alleged receipts rolled over – might be a relative, if not decisive, factor in determining what is just and equitable. In the present case, there are a number of answers to that contention. First, it is not just and equitable to include as a contribution amounts “rolled over”: see [18]-[25] above. Put simply, it is far from clear that there were amounts to “roll over”. Secondly, in relation to the so called “distributions”, it is apparent they were funded from a fund over which other investors had claims: see [73]-[74]. Thirdly, it is not appropriate or possible to seek to unravel the investors’ claims: see the Pooling Judgment. That third factual and legal finding is significant. It is significant because any task of unravelling would have necessarily included ascertaining an investor’s legal entitlement to interest over the period each investor held the investment or investments: cf Commissioner of Taxation v Broken Hill Pty Co Ltd (2000) 179 ALR 593 at [40] and Bond v Barrow Haematite Steel Co [1902] 1 Ch 353 at 363. That task would not have been straightforward – the existence of a right to interest was uncertain, the existence of a fund from which to pay any interest entitlement was uncertain because the profitability of each Scheme was and remains uncertain and finally, it is by no means certain that the Schemes would have continued with the Investors as members without the improper mixing of the funds.