FEDERAL COURT OF AUSTRALIA

ACE Insurance Limited v Trifunovski (No 2) [2012] FCA 793

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

Applicant |

|

AND: |

First Respondent HERACLEA PTY LIMITED ACN 007 437 372 Second Respondent JOSEPH VIVIL RIENZIE PERIES Third Respondent SHARE PEREZ Fourth Respondent WILLIAM DICINOSKI Fifth Respondent FETIE VICKI DICINOSKI Sixth Respondent |

DATE OF ORDER: |

|

WHERE MADE: |

THE COURT ORDERS THAT:

1. The parties bring in short minutes of order giving effect to these reasons by 7 August 2012.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

IN THE FEDERAL COURT OF AUSTRALIA |

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

GENERAL DIVISION |

NSD 643 OF 2009 |

BETWEEN: |

SHANE PEREZ Applicant |

AND: |

ACE INSURANCE LIMITED Respondent |

JUDGE: |

PERRAM J |

DATE OF ORDER: |

31 july 2012 |

WHERE MADE: |

SYDNEY |

THE COURT ORDERS THAT:

1. The parties bring in short minutes of order giving effect to these reasons by 7 August 2012.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

IN THE FEDERAL COURT OF AUSTRALIA |

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

GENERAL DIVISION |

NSD 644 OF 2009 |

BETWEEN: |

RIENZIE PERIES Applicant |

AND: |

ACE INSURANCE LIMITED Respondent |

JUDGE: |

PERRAM J |

DATE OF ORDER: |

31 july 2012 |

WHERE MADE: |

SYDNEY |

THE COURT ORDERS THAT:

1. The parties bring in short minutes of order giving effect to these reasons by 7 August 2012.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

IN THE FEDERAL COURT OF AUSTRALIA |

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

GENERAL DIVISION |

NSD 646 OF 2009 |

BETWEEN: |

FETIE DICINOSKI Applicant |

AND: |

ACE INSURANCE LIMITED Respondent |

JUDGE: |

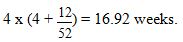

PERRAM J |

DATE OF ORDER: |

31 july 2012 |

WHERE MADE: |

SYDNEY |

THE COURT ORDERS THAT:

1. The parties bring in short minutes of order giving effect to these reasons by 7 August 2012.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

IN THE FEDERAL COURT OF AUSTRALIA |

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

GENERAL DIVISION |

NSD 647 OF 2009 |

BETWEEN: |

WILLIAM DICINOSKI Applicant |

AND: |

ACE INSURANCE LIMITED Respondent |

JUDGE: |

PERRAM J |

DATE OF ORDER: |

31 july 2012 |

WHERE MADE: |

SYDNEY |

THE COURT ORDERS THAT:

1. The parties bring in short minutes of order giving effect to these reasons by 7 August 2012.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

IN THE FEDERAL COURT OF AUSTRALIA |

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

GENERAL DIVISION |

NSD 649 OF 2009 |

BETWEEN: |

BLAGOJA TRIFUNOVSKI Applicant |

AND: |

ACE INSURANCE LIMITED Respondent |

JUDGE: |

PERRAM J |

DATE OF ORDER: |

31 july 2012 |

WHERE MADE: |

SYDNEY |

THE COURT ORDERS THAT:

1. The parties bring in short minutes of order giving effect to these reasons by 7 August 2012.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

NEW SOUTH WALES DISTRICT REGISTRY |

|

GENERAL DIVISION |

NSD 1860 OF 2008 |

BETWEEN: |

ACE INSURANCE LIMITED Applicant

|

AND: |

BLAGOJA TRIFUNOVSKI First Respondent HERACLEA PTY LIMITED ACN 007 437 372 Second Respondent JOSEPH VIVIL RIENZIE PERIES Third Respondent SHARE PEREZ Fourth Respondent WILLIAM DICINOSKI Fifth Respondent FETIE VICKI DICINOSKI Sixth Respondent

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

GENERAL DIVISION |

NSD 643 OF 2009 |

BETWEEN: |

SHANE PEREZ Applicant

|

AND: |

ACE INSURANCE LIMITED Respondent

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

GENERAL DIVISION |

NSD 644 OF 2009 |

BETWEEN: |

RIENZIE PERIES Applicant

|

AND: |

ACE INSURANCE LIMITED Respondent

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

GENERAL DIVISION |

NSD 646 OF 2009 |

BETWEEN: |

FETIE DICINOSKI Applicant

|

AND: |

ACE INSURANCE LIMITED Respondent

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

GENERAL DIVISION |

NSD 647 OF 2009 |

BETWEEN: |

william dicinoski Applicant

|

AND: |

ACE INSURANCE LIMITED Respondent

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

GENERAL DIVISION |

NSD 649 OF 2009 |

BETWEEN: |

blagoja trifunovski Applicant

|

AND: |

ACE INSURANCE LIMITED Respondent

|

JUDGE: |

PERRAM J |

DATE: |

31 July 2012 |

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

[4] |

|

[5] |

|

[17] |

|

[36] |

|

[40] |

|

[41] |

|

[52] |

|

[59] |

|

[61] |

|

[64] |

|

[66] |

|

[67] |

|

[74] |

|

[84] |

|

(a) The nature and extent of the conduct which led to the breaches |

[91] |

[95] |

|

(c) The nature and extent of any loss or damage sustained as a result of the breaches |

[108] |

(d) Whether there has been similar conduct by the respondent in the past |

[109] |

[110] |

|

[111] |

|

[112] |

|

[113] |

|

[116] |

|

[117] |

|

[118] |

|

[119] |

|

[120] |

|

[121] |

|

[124] |

|

[128] |

|

[130] |

|

[133] |

|

[134] |

1 On 25 October 2011 I determined that the relationship between Combined Insurance Company of America Ltd (‘Combined’) and five of its former insurance agents (‘the agents’) was one of employment: ACE Insurance Ltd v Trifunovski (2011) 200 FCR 532 (‘the first judgment’). That question arose as an issue in the agents’ claims against Combined for unpaid annual and long-service leave as well as in their pursuit of Combined for the imposition of civil penalties for failing to pay those entitlements. Shortly before judgment was delivered Combined’s insurance business (including its liabilities) was transferred to ACE Insurance Ltd (‘ACE’) under a scheme governed by the Insurance Act 1973 (Cth) giving rise to the proceedings’ present title. For consistency, I will continue to refer to ‘Combined’ (see the first judgment at [1]).

2 The parties seek now the resolution of two issues: first, the assessment of the entitlements of each of the agents to annual and long-service leave; secondly, the determination of an appropriate civil penalty for failing to pay those entitlements.

3 These reasons should be read with the reasons in the first judgment. For consistency the same nomenclature has been adopted. They are divided as follows:

I Annual Leave

II Long-service Leave

III Penalty

4 On the question of annual leave the parties had four debates calling for resolution. These were:

(a) whether the rate at which any accrued annual leave was to be paid was the rate the agents were receiving immediately prior to termination or, instead, the minimum rate provided for by the Award (‘the Rate Issue’);

(b) whether the territory and sub-regional representatives in fact took paid annual leave, thereby extinguishing the possibility of their having accrued annual leave (‘the Leave Issue’);

(c) whether Mr Perez was entitled to leave prior to 3 June 1998 (‘the Mr Perez Issue’); and

(d) the amounts determined to be due for annual leave (‘the Quantum Issue’).

5 In the first judgment I concluded that the employment of the five agents was governed by the former Insurance Industry Award 1998 (Cth) (‘the Award’). I also set out in Section II of the first judgment my reasons for accepting the enforceability of the Award. I will not repeat that analysis which applies equally in the present case. Not determined in the first judgment were two questions: (a) the source of the power to order the recovery of unpaid entitlements; and (b) whether the Award would itself apply or whether what was to be applied were the statutorily mandated minimum standards (here the question was which was more generous, the view being agreed that the more generous of the two would apply).

6 The answers to both of those questions were agreed between the parties in the present hearing. As to the first, it was common ground that the source of power was s 179 of the former Workplace Relations Act 1996 (Cth). As to the second, that the Award provided more than the statutorily mandated minimum entitlements which could, therefore, be put to one side.

7 Section 179(1) provided:

179 Recovery of wages etc.

(1) Where an employer is required by an award, order or certified agreement to pay an amount to an employee, the employee may, not later than 6 years after the employer was required to make the payment to the employee under the award, order or agreement, sue for the amount of the payment in the [Federal] Court or in any court of competent jurisdiction.

8 The obligation of Combined to pay its employees on termination any accrued annual leave arose from cl 22.9 of the Award. It provided:

22.1.1 Payment for leave on termination of employment

22.9.1 On the termination of employment of an employee an employer must pay the employee for any annual leave to which the employee became entitled during the period of employment with the employer to the extent that the annual leave was not taken.

22.1.1 The rate of pay at which the payment must be made is that actual salary rate the employee was receiving immediately prior to termination. Annual leave loading at the rate prescribed in 22.8.2(a) of this clause subject to the maximum prescribed in that subparagraph shall be paid on leave which has fallen due. Proportionate leave shall be treated as prescribed in 22.10.

(Emphasis added.)

9 The agents submitted that cl 22.9.2 and, in particular, the emphasised words ‘actual salary rate the employee was receiving immediately prior to termination’ directed attention to the final rate of pay of each agent. Combined submitted that this was not so principally because each agent’s remuneration consisted of a flow of fluctuating commission payments not aptly described as a ‘salary’. It pointed to various dictionary definitions of the word ‘salary’ to establish that, in ordinary parlance, the word connoted a fixed periodical payment for the performance of work, a proposition about usage which I accept.

10 Of course, the question which arises is not the meaning of the word ‘salary’ in general but instead its meaning in cl 22.9.2. Combined did not shy away, however, from that proposition. Indeed, it pointed to the terms of the Award as demonstrating, quite apart from the ordinary meaning of the word ‘salary’, that whatever ‘salary’ otherwise meant it could not include payments made by way of commission. Specific reference was made to the provisions dealing with long-service leave in cl 25 which, in general terms, provided for an entitlement to certain amounts of leave after 15 years service. The calculation of the entitlement turned, in part, on the expression ‘actual rates of pay’ (this is, in fact, not altogether clear but it is convenient to assume it to be so). ‘Actual rates of pay’ was defined in cl 25.5.1 to mean relevantly ‘the actual salary of the employee’. Importantly – and it was upon this which Combined fixed – cl 25.5.2 provided that ‘salary’ would not include ‘shift premiums, overtime, penalty rates, commissions, bonuses or allowances’ (emphasis added). Where the Award dealt with commissions, so the argument was developed, it did so in a way that made plain that they were not included in the concept of ‘salary’.

11 Despite some attractiveness this argument is not, I think, correct. The full text of cll 25.5.1 and 25.5.2 is as follows:

25.5.1 “Actual rates of pay” for the purpose of this clause, means the actual salary of the employee for a normal weekly number of hours of work immediately prior to the time of taking each period of long service leave.

25.5.2 Such salary will not include shift premiums, overtime, penalty rates, commissions, bonuses or allowances payable to the employee when working.

12 Contrary to Combined’s argument, cl 25.5.1 assumes that ‘salary’ includes shift premiums, overtime, penalty rates, commissions and bonuses; otherwise cl 25.5.2 would have no work to do. The absence of a provision such as cl 25.5.2 from the machinery in cl 22.9 tells against the argument that ‘salary’ does not include commission for annual leave purposes.

13 Another potential downside of Combined’s argument on this issue is that it would have the consequence, unless mediated by some other mechanism, that employees paid only by commission would not be entitled to receive payment in lieu for accrued annual leave. That would be a surprising reading of the Award and one whose rationality would not at once be obvious. Counsel for Combined were heedful of this unattractive consequence of the submission and, not without some considerable ingenuity, sought to moderate it in advance. They submitted that this would not be how cl 22.9.2 operated even if the concept of ‘salary’ were to have excised from it notions of commission. The reason for this lay in the words used in cl 22.9.2 – ‘actual salary rate’ – which, so it was submitted, was a reference not to the salary actually paid to the employee but, instead, to the minimum salaries specified in cl 14 of the Award (that clause specified a minimum annual salary for each grade or position covered by the Award). So viewed, no problem arose in the case of an employee paid only commission – cl 22.9 would, by default, cause such an employee to be deemed to be paid at the rate specified in cl 14 for the purpose of calculating annual leave.

14 This is not, however, a plausible reading of cl 22.9.2. The complete phrase used is ‘actual salary rate the employee was receiving immediately prior to termination’. The difficulty for Combined is the word ‘actual’ which suggests the presence of a reality and the words ‘was receiving’ which identifies that reality.

15 That being so, the consequence of Combined’s argument about the meaning of ‘salary’, if correct, is that employees paid only commission have no entitlement to payment in lieu for accrued annual leave. Given the nature of the instrument I would not accept such a reading unless compelled with some clarity to do so. Far from that clarity being present, however, it seems to me that the express excision of commission from the concept of salary in cl 25.5.2 is an indicator that, at least so far as the Award is concerned, the concept of salary embraces all forms of payment including overtime, bonuses and commission.

16 I therefore conclude that each agent was entitled to have his or her annual leave entitlement calculated on the basis of his or her salary, so understood, at termination.

17 The parties’ submissions about this were as follows: Combined noted that its obligation to give each agent annual leave arose from cl 22.1.1 which provided:

A period of four weeks (twenty working days) leave of absence on full pay must be allowed annually to an employee after twelve months continuous service which is to be granted and taken at a time agreed between the employer and the employee.

(Emphasis added.)

18 Each of the agents gave evidence at trial that there was a Christmas shutdown at Combined which lasted for two weeks from which, so Combined submitted, it was to be inferred that each took a ‘leave of absence’ for at least two weeks per year. Despite some misgivings I have about the effect on this argument of the Christmas Day, Boxing Day and New Years Day annual holidays I did not apprehend the agents to contest this aspect of it.

19 The agents’ attentions were instead focussed on the next step. Here Combined submitted that the agents had been on ‘full pay’ during that two week period. The submission was limited to the position of territory and sub-regional representatives because it was only those agents who were entitled to receive ‘override’ commission. The nature of override commission was explained at [49] in the first judgment but, in effect, it was a commission paid on the commissions earned by the door-to-door sales team. Combined’s point was that the territory and sub-regional representatives could continue to earn this override commission even when they were not working, including during the two-week Christmas shutdown.

20 The agents’ response to this argument was to deny that any override commission had been paid in discharge of Combined’s obligation to pay annual leave under cl 22.2.1. They did not submit that – and I need not consider whether – there were no override commissions earned in the two week Christmas break because the sales team was not working at that time either.

21 The agents instead rested their argument on a more general principle. Combined had two obligations, the first of which was contractual and derived from the written agreements it had executed with the agents. Under these agreements – and this was not in dispute – Combined had bound itself to pay override commission in accordance with the terms of the agreements when it became due. The second obligation sprang from cl 22.1.1 itself (above at [17]) which imposed the obligation on Combined to pay even though the employee was not working.

22 As Automatic Fire Sprinklers Pty Ltd v Watson (1946) 72 CLR 435 shows, an employer’s obligation to pay wages is generally dependent upon the employee’s performance of work. Ordinarily, therefore, where an employee does no work the employer’s obligation to pay wages is not engaged (see, for example, the judgment of Dixon J at 463-465). Provisions in contracts and awards of the genus of which cl 22.1.1 is a member overcome this problem by imposing an obligation on the employer to pay money which is not contingent on the work of the employee: an employee on annual leave is entitled to be paid even though performing no work.

23 Some difficulty attends that analysis in the present circumstance. Unlike the obligation to pay wages in an ordinary case, Combined’s obligation to pay override commission was not, in terms, dependent on the anterior performance of work by the employee. Instead, it was contingent on the performance of work by others. Consequently the obligation to pay override commission under the contract and the obligation to pay ‘full pay’ under cl 22.1.1 have conceptually distinct headwaters.

24 Combined’s submission was necessarily that its payment of override commission discharged its obligations under cl 22.1.1 notwithstanding its separate origin and different nature.

25 The agents submitted that Combined’s position was excluded by authority. They drew particular attention to the dissenting judgment of Sheldon J in Ray v Radano [1967] AR (NSW) 471 and the fact of its having been applied by successive Full Courts of this Court in Poletti v Ecob (No 2) (1989) 31 IR 321 at 329-333 per Kelly, Ryan and Gray JJ and Australian and New Zealand Banking Group Limited v Finance Sector Union of Australia (2001) 111 IR 227; [2001] FCA 1785 per Black CJ, Wilcox and von Doussa JJ at [47]. These authorities establish two propositions:

(a) if by the contract between the parties they have agreed that a payment will be made over and above an award payment or that a payment will be made that is extraneous to an award payment then the employer is prevented from claiming that the payment made pursuant to the contract may be set up as a discharge of its obligation under the award; and

(b) if in a situation of outstanding award entitlements an employer pays an employee a sum of money and designates it as being for a purpose other than the award payment the employer may not later claim that it has paid the award entitlement.

26 The agents were clear that they relied on (a) and not (b). As to (a), they submitted that the payment of override commission was ‘extraneous’ to the payment of full pay whilst on leave.

27 Mr Leopold SC, with whom Mr Saunders of counsel appeared for Combined, stressed the closeness of the relationship between override commission and the award entitlement to annual leave. In particular, he drew attention to cl 3(h) in the ‘Standard Agency Agreement’ entered into by Combined and Mr Trifunovski on 22 August 1994 (which was treated, without demur from the agents, as typical):

(h) In the event that the Territory Representative shall cease for any reason to be present in the Sales Territory or to actively perform the function of Territory Representative in the Sales Territory in either case for a period of more than thirty (30) days the Company shall be entitled:

(1) to cease to pay Override Commissions, Standard Commissions, Other Commissions and Bonuses to the Territory Representative on and from a date determined by the Company and notified to the Territory Representative;

(2) to appoint a Person (“Acting Territory Representative”) to act as Territory Representative in the Territory Representative’s place either for a specified or an indeterminate period;

(3) to pay to the Acting Territory Representative Override Commissions, Standard Commissions, Other Commissions and Bonuses relating to the Sales Territory in respect of the period during which the Acting Territory Representative so acts; and

(4) to terminate on a date determined by the Company and notified to the Acting Territory Representative the appointment of an Acting Territory Representative who has been appointed for an unspecified period;

for the purposes of paragraphs (1) and (4) of this Clause (3)(h) seven (7) days shall (notwithstanding any other provisions of this Agreement) be a sufficient period of notice.

28 Emphasis was placed on the reference to 30 days which, so it was submitted, matched the entitlement to annual leave under the Award. What this signified, according to Combined, was that the agreement contemplated that an agent could take four weeks off and continue to receive his or her override commission but no more. Viewed from that perspective, its operation was to be seen as being analogous, in substance, to the four weeks of annual leave provided for in cl 22.1.1 of the Award. This meant that the two clauses were effectively operating in the same domain of discourse so that payment of the override commission whilst an agent was away from work for a period of up to four weeks should be seen as a discharge of the obligation in cl 22.1.1.

29 The correctness of this submission is to be assessed by reference to its centrepiece which is the characterisation of cl 3(h)’s domain of operation as being analogous to that of cl 22.1.1 of the Award. However, for at least three reasons I do not think that that proposition should be accepted. To begin with, cl 3(h) confers no right upon an agent to receive, and imposes no obligation on Combined to make, any payment. The obligation to pay the override commission is to be found elsewhere, in cl 3(c). There is therefore no payment under cl 3(h) which can be utilised to form the basis of an argument that the clause is a member of the genus of annual leave provisions. The entitlement to receive override commission is, therefore, ‘extraneous’ to cl 3(h).

30 Another problem is the difference between the 30 days which cl 3(h) stipulates and the four weeks for which cl 22.1.1 provides. By that I do not mean the difference between 20 working days which cl 22.1.1 contemplates and the 30 calendar days which cl 3(h) operates on (although this, too, is not a small problem for the argument). Rather, it is the fact that cl 3(h) is not limited in its operation to 30 days per year. In fact, cl 3(h) will allow a territory representative to be away from work for any successive 30 day period so long as what is involved is a continuous sequence of 30 days. Theoretically, cl 3(h) would allow a territory representative to take 30 days away from work, come back to work for one day and then take another 30 days. Indeed, so long as each 30 day period is preceded and followed by a single day at work then such ‘leave’, if it can be so described, will be sanctioned by cl 3(h). There are 31 days in each such cycle (because the last day of each cycle could also serve as the first day of the next) and more than 11 such cycles in each year. Assuming – as Combined’s argument does – that 30 days is equivalent to four weeks annual leave, then the proposition that cl 3(h) operates analogously with, or in the same area as, cl 22.1.1 should be tested against the fact that it permits, in terms, more that 11 periods of four weeks leave in each year or, put it another way, more than 44 weeks of leave per year.

31 To that may be fairly raised the objection that, in practical terms, that would never be how cl 3(h) operated. A territory or subregional representative who sought to take 11 lots of 4 weeks away interspersed with single days at the office would not remotely be able to discharge the duties associated with her position and would surely have her agreement with Combined terminated in accordance with cl 6(a).

32 That objection – valid enough perhaps in itself – only points to the real question, which relates to the purpose of cl 3(h). Combined’s argument assumes implicitly that it operates as a conferral of a benefit on an agent and that the benefit is annual leave or something rather like annual leave. But this, in my opinion, is not what the clause is about. In truth, it is about Combined’s entitlement to have a workforce which is never away from work for more than four weeks at a time. An agent who is away for longer than that period, in effect, loses his position. Clause 3(h)(1) strips such agents of their remuneration and cll 3(h)(2) and 3(h)(3) allow their positions to be filled by others.

33 There is a third problem: cl 3(h) can be activated by one of two circumstances, neither of which is equivalent to the taking of leave. These are failing to be present in the relevant territory and failing actively to perform the functions of a territory representative. It is clear that the former is not leave. In the case of the latter there is a distinction to be drawn between being on leave and not actively performing duties. A person may not be actively performing duties even if he is not on leave. By contrast a person on leave has no active duties.

34 For those reasons I do not accept that cl 3(h) can fulfil the role that Combined’s submission requires. The payment by it of override commission whilst the agents were not working was not a payment which could discharge its obligation to pay full salary under cl 22.1.1.

35 It follows that the compensation issues are to be approached on the basis that annual leave was never taken and that the full amount accrued in each 12 month period.

36 In the primary judgment at [164] I determined that Mr Perez was entitled to annual leave between 29 October 1990 and 12 October 2006 notwithstanding that the Award did not exist prior to 3 June 1998. I did this because its non-existence was not pleaded against him (although it was pleaded against the other agents). It was not suggested that I should now approach the matter on a different basis.

37 Combined submitted that the evidence showed that he had taken, on average, at least four weeks off in each of the years in the period from 20 October 1990 to 3 June 1998. No submission was made to the contrary and, in my opinion, the evidence makes good this point.

38 Combined then submitted that Mr Perez bore the onus of proving that he satisfied the requirements of cl 22.1.1 and this, in turn, required him to prove that he had not taken leave of absence on full pay in terms of cl 22.1.1. Since the evidence established that he had taken at least four weeks leave it was for him to prove that he had not received full pay. Combined submitted that he could not discharge this burden because of the considerable override commissions he had received. Consequently, he had failed to prove his entitlement prior to 3 June 1998.

39 The difficulty with that submission is that assumes that the override commissions could be paid in discharge of the obligation under cl 22.1.1. For reasons already given that proposition should not be accepted.

40 It is convenient to deal with the position of each agent separately.

41 In the first judgment at [164], I concluded that Mr Trifunovski was entitled to annual leave for the period 3 June 1998 to 18 September 2005, a period of seven years, fifteen weeks and three days. By cl 22.1.1 he was entitled to four weeks per year for each whole year (that is, twenty-eight weeks). In his final year he worked only fifteen weeks. In the case of a partial year cl 22.10.1(b) of the Award required the four weeks leave to be subject to a pro-rata reduction on the basis of weeks worked. This results in an entitlement of  weeks. The result is that he has an entitlement to 29.15 weeks. This largely accords with Combined’s calculation of 29.1 weeks and is slightly larger than Mr Trifunovski’s own calculation of 28.8 weeks (though Mr Trifunovski accepted Combined’s calculation in his submissions in reply).

weeks. The result is that he has an entitlement to 29.15 weeks. This largely accords with Combined’s calculation of 29.1 weeks and is slightly larger than Mr Trifunovski’s own calculation of 28.8 weeks (though Mr Trifunovski accepted Combined’s calculation in his submissions in reply).

42 At the hearing the parties announced that there were only eleven issues between them. At the level of quantification, however, there regrettably appear to be some further differences which were not explored by counsel and were not the subject of any submission. The agents assumed that the rate of pay at termination for each agent was to be calculated from their tax returns. It was submitted on Mr Trifunovski’s behalf that his final rate of pay was $2,127.06 per week and that this could be gleaned from:

(a) his personal income tax return for 2005-2006;

(b) the income tax return for the Heraclea Trust (Mr Trifunovski’s company) for 2005-2006; and

(c) a document produced by Combined headed ‘Representative Income Summary and Details by Period’.

43 Mr Trifunovski’s personal tax return for the tax financial year ended 30 June 2006 shows $32,694 by way of income as a distribution from the Heraclea Trust. The return for the Heraclea Trust, on the other hand, records it as having earnt $127,683 by way of business income. The document generated by Combined in (c) suggests that Heraclea Pty Ltd earned $124,454.93 during periods ‘200441 to 200540’. I am prepared to assume that this was earned as trust income of the Heraclea Trust. However, I cannot identify what the period is.

44 The evidence at trial satisfied me that Mr Trifunovski’s commissions were paid to the trust and that its income represents the results of Mr Trifunovski’s labours for Combined (see the first judgment at [95] and [99]). It is, in that circumstance, appropriate to focus on its income rather than the amount distributed to him as a trust distribution. The distributed income of the trust does not reflect the fruits of his labours; more importantly, it was not paid to him by Combined.

45 Mr Trifunovski ceased working for Combined on 18 September 2005, only 11 weeks and three days into the financial year. I do not know what he did for the balance of the year; specifically, I do not know whether he was employed elsewhere. It seems to me unlikely that he was only employed by Combined in that financial year.

46 Combined submitted that it had paid Mr Trifunovski $127,683 in the 2005-2006 financial year, citing the Heraclea Trust tax returns. I take from that submission that which the evidence does not otherwise establish, namely, that income of the trust for the 2005-2006 income year is solely attributable to Mr Trifunovski’s work for Combined.

47 If Mr Trifunovski earned $127,683 in the first 11 weeks and three days of the financial year, this equates to weekly salary of $11,172.26. The submission made on Mr Trifunovski’s behalf was that his weekly salary was $2,127.06. Despite some industry, I am at a loss to understand whence that number came.

48 It may be that Mr Trifunovski knew that he was employed by other persons during the financial year and has reduced his claim to $2,127.06 (without explanation) to reflect this. That proposition is difficult to square, however, with Combined’s submission that the income in the Heraclea Trust tax return is attributable to it. Nor may it be easily reconciled with Mr Trifunovski’s submission that I should look to the tax returns.

49 Not without considerable misgivings, and certainly without any assistance, I have come to the conclusion that I should give Mr Trifunovski what the evidence appears to show, rather than what he appears to be asking for. I take that course because I believe that in some unfocussed way his submissions were trying to put forward such a case and because the figure is derived from Combined’s submissions about Mr Trifunovski’s earnings.

50 I conclude that Mr Trifunovski’s final salary was $11,172.26 per week.

51 On the basis of 29.15 weeks of accrued leave at that rate the amount for annual leave is $325,671.38.

52 Mr Perez was employed between 29 October 1990 and 12 October 2006. Unfortunately, this period straddles the commencement of substantial amendments to the Workplace Relations Act which occurred on 27 March 2006. The period after that date requires separate treatment. The first period is from 29 October 1990 to 26 March 2006, which is 15 whole years and a broken period of 21 weeks and two days. Under the Award, Mr Perez is entitled therefore to 60 weeks for the whole years (i.e. 4 x 15) and 1.62 weeks for the partial year  for a total of 61.62 weeks.

for a total of 61.62 weeks.

53 For the period between 27 March 2006 and 12 October 2006 the calculation is governed by s 232(2) of the former Workplace Relations Act which provides:

An employee is entitled to accrue an amount of paid annual leave, for each completed 4 week period of continuous service with an employer, on of the number of nominal hours worked by the employee for the employer during that 4 week period.

(Emphasis added.)

54 There were 28 weeks and four days between 27 March 2006 and 12 October 2006 (including the last day), which is seven completed four week periods. Mr Perez is therefore entitled to  or 2.15 weeks.

or 2.15 weeks.

55 In relation to the first period the question arises as to what his final salary was. The evidence about this issue is, as with Mr Trifunovski’s, not entirely satisfactory. Mr Perez’s evidence under cross-examination was that he started working for ‘Advanced Hair’ in April or May 2006 and that he had stopped working for Combined three months before the formal date of termination. Combined did not submit that this should be taken into account in calculating his annual leave entitlement; that is, it did not submit that some date other than 12 October 2006 should be used. Commonsense suggests that Mr Perez’s final rate of pay should be determined during a period in which he was actually working for Combined. That, so it seems to me, must be the financial year ending 30 June 2006. In that period Mr Perez earned $45,280. No submission was made to me that I should discount this by reference to wages received from other employers although the cross-examination of Mr Perez showed that he did work for others in that year. I proceed accordingly. Consequently, Mr Perez is entitled to $870.77 per week (i.e. $45,280 ÷ 52). For the first period he is entitled, therefore, to 61.62 x $870.77 which is $53,656.85.

56 In relation to the second period, I do not believe Mr Perez is entitled to succeed. The matter is governed by the former s 235 which provided:

235 Annual leave—payment rules

(1) If an employee takes annual leave during a period, the annual leave must be paid at a rate that is no less than the employee’s basic periodic rate of pay immediately before the period begins.

(2) If the employment of an employee who has not taken an amount of accrued annual leave ends at a particular time, the employee’s untaken accrued annual leave must be paid at a rate that is no less than the employee’s basic periodic rate of pay at that time.

(Emphasis added.)

The expression ‘basis periodic rate of pay’ was defined in s 178 as follows:

Basic periodic rate of pay means a rate of pay for a period worked (however the rate is described) that does not include incentive-based payments and bonuses, loadings, monetary allowances, penalty rates or other similar separately identifiable entitlements. The meaning of basic periodic rate of pay is also affected by section 210.

(Underlined emphasis added.)

57 Section 210 is not material. In my opinion the commission payments received by Mr Perez were, as Combined submitted, ‘incentive-based payments’ and hence excluded from this definition. No submission was made on Mr Perez’s behalf about this. In particular no submission was developed that there might be some continuing role for the Award. It would not be procedurally fair for me to consider that issue upon which Combined has not been heard.

58 It follows that Mr Perez has no entitlement for this period. If I am wrong in that conclusion, I would award him the period calculated above (2.15 weeks) multiplied by $870.77, i.e. $1,872.16.

59 Mr Peries was employed by Combined as a representative from 30 June 1998 to 15 December 2002. He was subsequently employed by Combined as a regional manager from 16 December 2002 to 15 December 2005. In respect of this second period it was not suggested that he had not been paid his entitlements (Combined having always accepted that the regional manager’s position was an employed one). Attention may then be confined to the first period. That period was four years, 24 weeks and one day in duration. He is entitled therefore to annual leave as follows:  = 17.85 weeks.

= 17.85 weeks.

60 It was submitted on Mr Peries behalf that his final rate of pay was $3,990.21. This was based on his pay in 2005 when he finished employment as a regional manager. Reference was made to his tax return for the 2005-2006 income years. Combined did not deny the appropriateness of using the 2005 figure but it did submit, correctly in my opinion, that his final pay in that year included a termination payment of $20,346 which ought be excised from the calculation. When this is done his earnings for that year are reduced from $95,765 to $75,419 for the period 1 July 2005 to 15 December 2005, a period of 24 working weeks. Consequently, his final rate of pay was $3,142.46 per week (i.e. $75,419 ÷ 24). Mr Peries is, therefore, entitled to $56,092.91 in respect of accrued annual leave (17.85 x $3,142.46).

61 Mr Dicinoski was employed between 30 September 2001 and 23 April 2005, a period of three years, 29 weeks and three days. He is therefore entitled to accrued annual leave as follows:  = 14.23 weeks.

= 14.23 weeks.

62 Mr Dicinoski submitted that his final rate of pay was to be derived from his income tax return for 2004-2005. This showed that he received $43,886 in the period 1 July 2004 to 23 April 2005, a period of 297 days. This equates to an annual salary of $53,933.97 ($43,886 ÷ 297 x 365) or a weekly rate of $1,037.19. The submissions prepared on Mr Dicinoski’s behalf suggested that the figure should be $674.73 per week. The only hint provided as to where this might be derived from was this inscrutable statement in the written submissions prepared on his behalf:

Personal Tax Return: 2004-5 (20/7377-7382)

Income Summary & Details: (16/5774-5775)

Insurance Industry Award – Grade 5 (s 14.5)

(The numbers in the first two sets of parentheses are references to volume and page numbers in the 28-volume Court Book. The number in the third is a reference to a clause in the Award.)

63 The first two references lead however to the figure $1,037.19 not $674.73. The third reference points one in the direction of the Award and the proposition that Mr Dicinoski was grade 5. In the end this submission – if it really amounted to a submission – was inaccessible, at least to me. Doing the best one can this seems to be the grade 5 rate that applied from 11 September 2005, after Mr Dicinoski left. Combined agreed that Mr Dicinoski was to be regarded as grade 5. This flowed from its earlier submission that it was the minimum salaries in the award for each grade which were to provide the final rate of pay. I have already rejected that submission. It submitted therefore that the minimum provided was $657.73. This is different to the $674.73 apparently claimed by Mr Dicinoski the origins of which are lost. I propose to proceed on the basis of the rate disclosed in the tax returns, $1,037.19, largely for the reasons I did in Mr Trifunovski’s case. On that basis Mr Dicinoski is entitled to $14,759.21 ($1,037.19 x 14.23) in respect of his accrued annual leave. I have taken this approach because I take the thrust of the submissions made on his behalf to have been directed at the ascertainment of his actual earnings, even if the ultimate submissions made on his behalf were almost entirely incomprehensible.

64 Mrs Dicinoski was employed from 1 October 2001 to 23 December 2005, a period of four years and 12 weeks. She is therefore entitled to accrued annual leave as follows:

65 In the financial year ending 30 June 2006, Mrs Dicinoski’s tax return discloses she earned $6,830 by way of income. On the other hand, Combined’s records appear to show that it paid her a net income of $52,015.08. The submission made on her behalf referred me to both of these documents and submitted that this justified the conclusion that her final rate of pay was $674.73 (the Award rate). I do not understand that submission nor how I might resolve the discrepancy between the tax return and Combined’s records. Combined also submitted that it was the Award rate which should be used (although for different reasons). The parties are ad idem that I should use the $674.73 figure and I will therefore use it (notwithstanding my misgivings). She is therefore entitled to 16.92 x $674.73, i.e., $11,416.43. I have been unable to take the position in relation to Mrs Dicinoski that I did with Mr Dicinoski and Mr Trifunovski because of the very large inconsistency between her tax return and Combined’s records. I cannot unscramble what was being put on her behalf. There is, in short, a limit to what a trial judge can be expected to do for persons who are represented.

66 These issues relate only to Mr Perez, Mr Peries and Mr Trifunovski. The parties informed me during the hearing that there were two issues requiring resolution:

(a) the Pro-rata Issue; and

(b) the Quantum Issue.

67 Clause 25.1 of the Award provides:

25.1 Long service leave entitlement after 15 years service

Subject to the provisions of this clause each employee will be entitled to thirteen weeks’ long service leave or an amount of leave as calculated in accordance with 25.3.1 of this subclause at actual rates of pay on the completion of fifteen years continuous employment within Australia with the same employer and thereafter an additional four and one-third weeks’ leave on completion of each additional five years of such employment.

68 It is convenient to illustrate the issue using the example of Mr Perez.

69 Mr Perez was employed from 29 October 1990 to 12 October 2006, a period of 15 years and 349 days. A question arises as to his entitlement to long-service leave in respect of the 349-day period. Combined submits that no further leave after 15 years accrues until the completion of a further five year period so that no entitlement arises in relation to this 349-day period.

70 Mr Perez submitted that account needed to be taken of cl 25.3.1. That clause needs to be read with cl 25.2. Together they provide:

25.2 Payment in lieu of leave on termination

25.2.1 Termination by employer – 10-15 years of service

After an employee has completed ten years but less than fifteen years of such employment and the employment is terminated by the employer for any cause other than serious misconduct, the employee will be entitled to payment in lieu of such long service leave less any long service leave which has already been granted to and taken by the employee under 25.9.1.

25.2.2 Termination by employee – 10-15 years of service

Where an employee terminates employment after having completed ten years but less than fifteen years of continuous employment the employee shall be entitled to payment in lieu of such leave less than [sic] any long service leave already granted to and taken by the employee.

25.2.3 Termination of employment – 15 or more years of service

After an employee has completed fifteen years of such employment and employment is terminated the employee will be entitled to payment in lieu of such leave less any long service leave which has already been granted to and taken by the employee under 25.9.1.

25.3 Method of calculation of entitlement

25.3.1 In the case of an employee whose period of continuous employment commenced before 1 August 1964, the amount of long service leave to which the employee will be entitled under 25.1 and 25.2.3 hereof for which the employee will be entitled to payment in lieu under that paragraph is the sum of the following –

25.3.1(a) For the period of employment prior to 1 August 1964 the amount calculated on the basis that leave accrues at the rate of 13 weeks for 20 years continuous service.

NOTE: TABLE 1 LONG SERVICE LEAVE CALCULATION TABLE ON THE BASIS OF 13 WEEKS LEAVE FOR 20 YEARS SERVICE at the end of this clause should be used to calculate the employee’s entitlement for service prior to 1 August 1964.

25.3.1(b) For the period of employment from 1 August 1964 onwards the amount calculated on the basis that leave accrues at the rate of 13 weeks for 15 years continuous service.

NOTE: TABLE 2 LONG SERVICE CALCULATION TABLE ON THE BASIS OF 13 WEEKS LEAVE FOR 15 YEARS SERVICE should be used to calculate the employee’s entitlement for service on and after 1 August 1964.

71 Mr Perez submitted that cl 25.3 demonstrated that a pro-rata amount in excess of 15 years could be awarded. I am not sure that this reading is correct but, in any event, it does not matter because I accept Combined’s submission that cl 25.3 is only concerned with persons whose employment commenced prior to 1 August 1964.

72 Clause 25.1 is clear in its terms. It does not generate a pro-rata obligation. The provision governing payment in lieu – cl 25.2.3 – does not give any entitlement to long-service leave which has not accrued under cl 25.1.

73 I therefore reject Mr Perez’s submission that he is entitled to long service leave for the additional 349 days.

74 Mr Peries was employed for the period 26 October 1981 to 15 December 2005, a period of just over 24 years. It will follow from the conclusion just reached that Mr Peries is entitled to be paid for 20 years of long-service entitlement. He is therefore entitled to 13 weeks for the first fifteen years and 4 weeks for the following five years, that is, a total of  weeks.

weeks.

75 Mr Perez, on the other hand, is entitled to only 13 weeks by reason of cl 25.1.

76 Mr Trifunovski was employed between 22 August 1994 and 13 September 2005, a period of 11 years and 23 days. Clause 25.1 appears to give him no entitlement since it requires at least 15 years service. The matter is, however, affected by cl 25.2.2 which gives him a right to payment in lieu. It was not submitted that Mr Trifunovski was not entitled to any payment in lieu because the leave entitlement had not accrued. Probably correctly, Combined proceeded on the basis that cl 25.2.2 had to do something. This would appear to require one to calculate the entitlement at the annual rate implicit in cl 25.2.2’s rate of 13 weeks per 15 years. This lends to an entitlement of 9.5333 weeks (disregarding the 23 days) which Combined submitted was the correct figure. Mr Trifunovski sought 9.6 weeks. I am not sure whether this results from using the same methodology (disregarding the 23 days) and rounding up or including the 23 days (in which case, on my reckoning, one gets 9.59 weeks). Combined withdrew [154] of its written submissions wherein it explained why the 23 days was not available. (Combined actually submitted that there were 22 days, but its method of calculation seems to have been non-inclusive.) I proceed on the basis that is accepted that the 23 days should be brought to account. I find Mr Trifunovski is entitled to 9.59 weeks of leave.

77 Clauses 25.5.1 and 25.5.2 are set out above at [11]. The definition of ‘salary’ in cl 25.5.2 specifically excludes commission. Combined submitted that this meant that Mr Peries’, Mr Perez’s and Mr Trifunovski’s commissions had to be excluded from the calculation of long service leave.

78 Combined went on to submit that it was appropriate to calculate the entitlement by reference to the minimum amounts specified in the award. The submissions in chief of Mr Perez, Mr Peries and Mr Trifunovski suggested that the appropriate rate of pay for long service leave would be their final rate of pay. However, in their submissions in reply they accepted that the appropriate rate was the award rate.

79 Having reached that consensus the parties then ignored it when coming to the question of calculation. Combined submitted that Mr Peries’ final rate of actual pay was $3,142.46 which Mr Peries accepted. But this figure was not, contrary to Combined’s submission and the agents’ concession, the rate set out in cl 14.5 of the Award.

80 Unguided by the parties, I propose to proceed as follows: as explained above at [10]-[12], the effect of cl 25.5.2 is to exclude commission from the concept of ‘salary’ for long-service purposes. The consequence of that is that Mr Peries, Mr Perez and Mr Trifunovski, in principle, should receive no payment. Combined submits that I should find that ‘actual salary’ means the salary rates set out in cl 14. I have rejected that argument at [13].

81 In principle Mr Peries, Mr Perez and Mr Trifunovski fail. However, Combined’s submission that I should impose the salary rates set out in cl 14 meant that they were not on notice – at least in relation to this part of the case – of an argument that they should receive nothing. Accordingly, it would be procedurally unfair to award less than the amount set out in cl 14. On the other hand, I cannot accept that any higher rate is justified because of the effect of cl 25.5.2.

82 In those circumstances, although it appears to lack internal legal logic, I feel bound to award Mr Peries, Mr Perez and Mr Trifunovski long-service leave at the rate under cl 14. In Mr Trifunovski’s case his final grade would have been grade 6 which equates to a weekly salary of $777.88. In Mr Peries’ case, his final position was also as a grade 6, which would have resulted in a weekly salary of $724.88. In Mr Perez’s case, he finished at the level of a grade 5 (as he was demoted to a grade 5/territory representative in 2005: see the first judgment at [64]). At the time of the end of his employment, this corresponded with a weekly salary of $674.73.

83 In those circumstances, the long leave entitlements are as follows:

(a) Mr Trifunovski – $777.88 x 9.59 = $7,459.87

(b) Mr Peries – $724.88 x 17 = $12,564.59

= $12,564.59

(c) Mr Perez – $674.73 x 13 = $8,771.49

84 The power to impose a penalty for breach of the award is to be found in s 178 of the Workplace Relations Act as it stood immediately prior to 27 March 2006. Insofar as Mr Perez is concerned the power to impose a penalty in relation to events after that day is to be found in s 719 of the Workplace Relations Act as it was on and after 22 March 2006. In both cases the maximum penalty for a contravention by a corporation is 300 penalty units (see ss 178(4)(a)(ii) and 719(4)). A penalty unit is defined in s 4AA of the Crimes Act 1914 (Cth) to mean $110. Consequently, the maximum penalty for any of the contraventions with which this case is concerned is $33,000.

85 What should the penalty be? In the realm of civil penalties it is accepted that their purpose includes both punishment and deterrence. In turn deterrence has two aspects, the particular and the general, and these reflect the concern that the penalty should operate not only so that the contravenor does not feel that it would be worthwhile to engage in the conduct again but also so that others feel the same way too. It is often said that penal laws – criminal laws in particular – serve another end too, namely, that of rehabilitation. ‘So one punishes not to efface the crime, but to transform a criminal (actual or potential); punishment must bring with it a certain corrective technique’ (M Foucault, Discipline and Punish: The Birth of the Prison (A Sheridan trans, Penguin, 1977) [trans of: Surveiller et punir: Naissance de la prison (first published 1975)] at 127). Doubts have sometimes been expressed as to whether the concept of rehabilitation has much to do with the punishment of corporations who find themselves in breach of civil penalty provisions: cf. Ponzio v B & P Caelli Constructions Pty Ltd (2007) 158 FCR 543 at [93]-[94] per Lander J (‘In some cases, although hardly in this type of contravention, rehabilitation is an important factor’). This may be so not only because corporations do not have minds of their own which may be successfully rehabilitated but because the kinds of matters typically made the subject of civil penalties little lend themselves to notions of rehabilitation. A corporation does not infringe such a provision because the shelf on which it was originally incorporated was in a bad neighbourhood. Correspondingly, beyond its actual deterrent effect it is difficult to identify the rehabilitative effect a civil penalty might be expected to have.

86 Apart from those matters, the penalty must be proportionate to the wrong which has been done and in accordance with prevailing standards of punishment: Ponzio at [93]. This aspect of the general law is reflected in the requirement that where a contravention arises out of a course of conduct it is to be taken as a single breach: ss 178(2)(b) and 719(2)(b).

87 These concepts are not necessarily distinct. The need to impose a penalty which is proportionate to the wrongdoing directs attention, in the first instance, to an assessment of the degree of wrongdoing involved and this, in turn, requires an assessment of how many contraventions there have been and whether what is involved is a single course of conduct. In Construction, Forestry, Mining and Energy Union v Cahill (2010) 194 IR 461; [2010] FCAFC 39, Middleton and Gordon JJ explained the course of conduct principle this way (at 473 [39]):

As the passages in Construction, Forestry, Mining and Energy Union v Williams (2009) 191 IR 445 explain, a “course of conduct” or the “one transaction principle” is not a concept peculiar to the industrial context. It is a concept which arises in the criminal context generally and one which may be relevant to the proper exercise of the sentencing discretion. The principle recognises that where there is an interrelationship between the legal and factual elements of two or more offences for which an offender has been charged, care must be taken to ensure that the offender is not punished twice for what is essentially the same criminality. That requires careful identification of what is “the same criminality” and that is necessarily a factually specific enquiry. Bare identity of motive for commission of separate offences will seldom suffice to establish the same criminality in separate and distinct offending acts or omissions.

(Emphasis in original.)

88 In this case both Combined and the agents accepted that Combined’s breaches of its annual leave obligations under the Award arose from a single course of conduct and they took the same position in relation to the long-service leave issues (see, lest there be doubt, Combined’s written submissions at [173]-[175]; agents’ written submissions in reply at [60]-[61]). The logic of that leads, as Combined submitted, to the conclusion that there were two contraventions. The agents submitted that there were one or two contraventions for each employee (depending on whether long-service leave was an issue). This was on the basis that there was a separate proceeding for each employee. I do not accept, however, that the procedural form that a civil penalty claim takes may have a substantive impact on the scope of the punishment. I should say I have considered whether the agents’ general concession that there was a single course of conduct for annual leave and another for long-service leave was a reasonable one which ought to be accepted. In my view, it was.

89 We are, in the circumstances, concerned with the imposition of two penalties: one for annual leave; one for long-service leave.

90 In assessing the appropriate penalty it is necessary to have regard to all of the relevant circumstances. In this case these are:

(a) The nature and extent of the conduct which led to the breaches

91 Combined submitted that the conduct in question was narrow in scope and had resulted from a single structural decision that agents were to be engaged as independent contractors. On the other hand the agents submitted that the breaches were extensive, demonstrated a failure to provide basic entitlements over a lengthy period and showed little regard for Commonwealth law.

92 The contraventions were certainly extensive in that they extended over a period between 1981 (when Mr Peries was hired) through to 2006 when Mr Perez left. I accept that the agents did not get their annual leave and this, no doubt, would have had a deleterious effect on the amenity of their lives. On the other hand, it should not be lost sight of that, whatever else it might be called, they obtained the benefit of the shutdown for two weeks over the Christmas/New Year season. I do not mean to suggest that one was a substitute for the other. But it does show, at least from an amenities perspective, that this was not a case where the employees were worked, as a matter of physical reality, 52 weeks per year. In that regard, I also take into account the evidence of some of the agents that they also took holidays from time to time during the year.

93 Of course, that is no answer to so much of the complaint as concerns a failure by Combined to pay its staff whilst on leave.

94 I reject the agents’ submission that Combined’s conduct shows a disregard for Commonwealth law. As I explain below Combined’s position was the result of having taken legal advice which advice, correct at the time, has been overtaken by later High Court authority. In such a state of affairs I detect no disregard for the law; indeed, quite the contrary.

(b) The circumstances in which the conduct took place

95 Combined drew attention to several matters. First, it submitted it had received legal advice that the relationship between itself and its agents was one of employment and this had occurred more than once. The first of these was an advice proffered by Messrs Allen Allen & Hemsley dated 13 December 1986. This advice was principally directed to the question of whether Combined was obliged to remit PAYE tax in respect of its agents. The advice was proffered in a context in which the Commissioner appeared to be making some inquiries about this issue.

96 Without dwelling on the employment question at length (there were other provisions at play beyond those dealing with employment) the advice suggested that the most recent redrafts of the contracts would probably be found not to give rise to a relationship of employment but there were unresolved issues about the earlier ones. The new agreements came into use in January 1987.

97 Secondly, Combined knew that its view that its agents were independent contractors had been accepted in 1987 by the Department of Industrial Relations. A file note prepared by a solicitor in Allens recorded that that Department’s representative had informed Combined and its lawyers that a claim by one of its former agents for holiday pay would be taken no further since it was satisfied that he was not an employee.

98 The third matter was an advice prepared by S.E.K. Hulme QC for the National Mutual Life Association of Australasia Limited on the question of the tax status of its agents. The advice was dated 20 March 1987. Mr Hulme based his advice on the National Mutual agency structure which was not very dissimilar to that obtaining at Combined. He examined the agency agreements and thought them indistinguishable from those in suit in Australian Mutual Provident Society v Allen (1978) 52 ALJR 407. His ultimate conclusion was that National Mutual’s agents were not employees.

99 This advice appears to have come into the possession of Combined in around May 1988. An internal memo describes it as a ‘very important submission’. It recorded that Allens were seeking to convene a meeting with Mr Murray Gleeson QC and Mr Richard Edmonds the latter of whom was, unfortunately, unavailable. There is no evidence that the meeting with Gleeson QC took place. Mr McDonald did say, however, that he had had regard to Mr Hulme’s advice.

100 I conclude that, as at May 1988, Combined had good reason to believe that, at least on the basis of the new agreements in place from January 1987, its agents were not employees. It is true that the advice it received was never directly focussed on the question. Nevertheless, it did receive such advice. Further, I do not think that reliance on Mr Hulme’s advice was unreasonable. On the other hand, the advice of 13 December 1986 proffered by Allens gave it reason to suspect that in the period 1981-1986 there was a risk that its agents were employees. The agents submitted that this advice was defective because it did not consider Stevens v Brodribb Sawmilling Company Pty Ltd (1986) 160 CLR 16. Stevens was decided on 13 February 1986, so this criticism of Allens’ advice may not be unwarranted. But that hardly affects the reasonableness of Combined’s reliance upon it. It might be noted that Mr Hulme’s advice did not refer to Stevens either. Although it is not strictly material since the question is the reasonableness of Combined’s conduct and not the correctness of the advice proffered to it, I do not think that the result in the present case would have happened before the High Court’s decision in Hollis v Vabu Pty Ltd (2001) 207 CLR 21. As that case illustrates, the concept of employment is a social concept subject to development.

101 The agents also criticised Combined because both advices pre-dated Hollis v Vabu. I do not understand how this can be a criticism of Combined in the period up to 9 August 2001 when that decision was delivered.

102 The agents submitted that it was reckless not to get further advice having received Mr Hulme’s advice. I do not accept this. Until Hollis v Vabu there was really no problem; further, Combined had been receiving advice that its structure, at least from 1987, did not generate any issue.

103 There is no evidence as to when Combined became aware of Hollis v Vabu or if it thereafter received advice about it. Given where the onus lies in the present case I proceed on the basis that nothing alerted Combined to any alteration in the law so as to cast doubt on the correctness of its previous advice.

104 At least so far as Mr Perez’s final period of employment is concerned there is an additional matter: on 28 March 2006 the Western Australian Industrial Relations Commission concluded that one of Combined’s agents was not an employee: Sehovic v Combined Insurance Company of Australia [2006] WAIRComm 4003. This decision, in my opinion, makes it difficult to describe Combined’s position after that date as unreasonable. If it mattered my view would be that that advice was correct until 9 August 2001, when Hollis v Vabu was decided.

105 In summary I conclude that in the period 1981-1986 there were doubts about the question but that from 1987 onwards Combined had been advised that its agents were not employees and its reliance on that advice was not unreasonable.

106 Combined also relied upon two other matters as being relevant. The first of these was the fact that both it and its agents had laboured under the same misapprehension as to their status. I found this to be the fact in the first judgment at [91]. I am not sure how the mutuality of the error reduces the seriousness of the matter when one has already concluded that the error occurred as a result of reasonable reliance on legal advice. I reject Combined’s contention that the agents’ claims were opportunistic: they do not seem to me to have that quality.

107 Combined also submitted that I should take into account the fact that, had the true position been known to the parties (i.e. that the agents were employees), their rates of pay would have been reduced to reflect their annual leave entitlements. To that extent they may well have been worse off financially. It is difficult, however, to assess the impact of this observation overall. It is not, after all, just a question of money. Annual leave is an aspect of lifestyle amenity. Few people would be willing to work 52 weeks per year in return for an extra four weeks’ pay. It may be possible, as Combined submits, to accept that perhaps the financial position of the agents was not so deleteriously affected but one would need to bring to account in that calculus some measure of what was lost too – i.e. the amenity of leave. Ultimately, I think both considerations are too speculative to be able to be brought to account in a way which would be just.

(c) The nature and extent of any loss or damage sustained as a result of the breaches

108 Combined submitted that it had, in substance if not in form, complied with the obligation to give annual leave. I certainly accept that the agents did receive around two weeks off at Christmas and that some of them took further time off during the year. Of course, this was leave without pay. But this is relevant because it shows that the default involved was more related to failing to pay for leave otherwise permitted to be taken rather than the more serious matter of not permitting leave to be taken at all. Although I accept this, I would hesitate necessarily to describe this as a case where Combined had in substance complied with its obligations. Those obligations consisted of a substantial element of payment. For reasons I have given above I do not accept that Combined did comply with that obligation either in substance or in form.

(d) Whether there has been similar conduct by the respondent in the past

109 There is no evidence that Combined has ever been found to have infringed the award or long service provisions before. Indeed, to the contrary, it was found not to have infringed them in Sehovic.

110 The business of Combined in Australia is substantial. This suggests that there is unlikely to be any hardship issue especially with a maximum civil penalty of $66,000. There are no issues of market size or definition which would tend to make the magnitude of the undertaking an aggravating matter.

(f) The deliberateness of the breaches

111 The conduct was deliberate in the sense that Combined intended to ensure, as best it could, that its agents were not employees. On the other hand, an assessment of the deliberateness of the conduct cannot take place without bringing to account Combined’s reasonable belief that what it was doing was lawful.

(g) Whether senior management was involved

112 The employment structure of Combined was conceived, as one would expect, at a senior level. In substance, this was not really disputed. Again, however, it must be seen as being tempered by management having acted on legal advice (in the sense discussed above).

113 It is not clear to me how an artificial construct such as a corporation can experience the complex human emotion of contrition made up, as it is, of an amalgam of distinctly human emotions such as regret, shame and sympathy. I do not doubt that a corporation may exhibit signs of regret but it is too much to expect that such an artificial construct can be meaningfully contrite.

114 For civil penalty cases involving corporations it would be more coherent to ask only whether the corporation has changed its behaviour. Nothing more can be expected; a person who does not literally or physically exist may not wear sackcloth.

115 In this case there is a difficulty generated by the bifurcated hearing which has occurred. In the first judgment I concluded that the agents were employees. That issue will certainly be tested on appeal. In the meantime Combined has done nothing to change its arrangements. Given the certainty of an appeal I do not regard this as showing an unwillingness to bend to the judgment. I will treat this matter as neutral.

116 This issue is subsumed in the previous one.

117 This is irrelevant in circumstances where no regulator has become involved.

(k) Ensuring compliance with minimum standards by provision of an effective means for investigation and enforcement of employee benefits

118 The present cases do not present as ones in which there has been flouting of the law. Rather, the position of Combined was derived from a reasonably held view based on advice. I do not think that this is a consideration calling for the imposition of a penalty.

(l) Magnitude of the entitlements

119 I do not accept Combined’s submission that the amounts involved were not large. For individuals they are. I accept that they must be seen in a context which includes them having been incurred over a substantial period but that does not lessen the seriousness of the matter.

120 I do not accept that Combined’s actions were, in any sense, reckless.

121 The evidence of Mr Downes indicates that if the first judgment is upheld the business will be restructured. I accept that this means that the risk of repeated contraventions is nil if the primary judgment is reversed on appeal. If, on the other had, the appeal is dismissed this presumably will guarantee further contraventions during the appeal process. The underscores why determining penalty in advance of the appeal is difficult.

122 Were this a minor matter I might be inclined to assign to Combined’s account the failure to act on the first judgment. But that decision fundamentally challenges its entire business model. I accept that it would be quite unjust for it to have to make those effectively irreversible changes before the correctness of the judgment has been ascertained.

123 In those circumstances, I regard this as a neutral matter.

124 Combined submitted, and I accept, that it has spent $1.656 million on these proceedings. I do not think that in doing so it has been driven by a desire to avoid the imposition of a civil penalty. Rather, its motive for such a trenchant approach to its defence is that the conclusion that its agents are employees represents a very serious threat to the manner in which it does its business. If Combined’s defence is unsuccessful its whole business model will need to be changed root and branch. Insofar as the past is concerned it has civil exposures potentially limited only by limitation periods.

125 Given those matters, its defence and the resources devoted to that defence are to be seen as directed towards protecting itself from challenge to its business model and not towards evading a civil penalty of $66,000.

126 There are risks in permitting the incurring of legal costs to count as an ameliorating factor in assessing a civil penalty. To do so may provide an economic incentive to a respondent to draw out a proceeding confident that money spent on its defence may result in a reduction in penalty. This, in turn, would conflict with the policy of encouraging early admission of wrongdoing by taking account of it in the process of penalty assessment as a positive matter: cf Minister for Sustainability, Environment, Water, Population and Communities v De Bono [2012] FCA 643 at [60], [73]; Secretary, Department of Health and Ageing v Export Corporation (Australia) Pty Ltd [2012] FCA 42 at [91].

127 Despite that there can be cases where it is appropriate to take the incurring of costs into account. This will be particularly so where it is obvious that the costs have been incurred in defending related civil proceedings rather than the penalty proceedings themselves. This is such a case and, in my opinion, it is a significant matter.

(p) Specific and general deterrence

128 I do not think that there is any risk of further contravention (should the appeal be dismissed). Indeed, there never was: Combined has always been willing to abide what it was advised its legal obligations were.

129 The issue of general deterrence is more difficult. The entity being held up as an example is one which I have determined behaved reasonably by taking advice. It is necessary then to identify what behaviour it is that it is sought to deter. If one were to criticise Combined’s conduct it would I think only be this: it did not take complete and comprehensive advice on the issue and it did not seek to keep itself abreast of significant developments in industrial law such as Hollis v Vabu.

130 The matters which predominate in my mind are Combined’s reliance upon advice; the likely correctness of that advice until Hollis v Vabu; and the size of its legal costs. In the somewhat unusual circumstances of this case I propose to impose a civil penalty of $5,000 for each of the two breaches. I do this largely for general deterrence. Apart from the need to ensure that employers get these questions right, I see little to punish in Combined’s conduct.

131 I pause to consider whether a civil penalty of $10,000 adequately captures the wrongdoing involved in the contraventions. Although seemingly at the low end, the significant exculpatory matters justify that conclusion.

132 In my opinion this civil penalty should be paid to the five agents. It is to be shared between them in equal shares.

133 The agents claimed interest in respect of each of the outstanding annual and long-service leave payments. Combined submitted that the interest should run from the point at which the right to receive such payments came into being (i.e. when each agent left the employment of Combined). I accept this. I will not accept, however, the calculations of either party, founded as they are on entitlements that I have varied. I will leave it to the parties to calculate the interest in accordance with Practice Note CM 16.

134 The parties will need to bring in short minutes of order giving effect to these reasons within seven days. Those short minutes should include a grant of leave to appeal both the orders the subject of this judgment and the earlier orders the subject of the first judgment. I will determine the question of costs on the papers. The short minutes should provide a timetable for that.

I certify that the preceding one hundred and thirty-four (134) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Perram. |

Associate: