FEDERAL COURT OF AUSTRALIA

Tax Practitioners Board v Hogan [2012] FCA 642

| IN THE FEDERAL COURT OF AUSTRALIA | |

| Applicant | |

| AND: | Respondent |

| DATE OF ORDER: | |

| WHERE MADE: |

1. On 26 separate occasions detailed in Schedule A to this order, between about July 2010 and about October 2010 and in relation to the persons respectively described in Schedule A to this order in respect of a particular occasion, the respondent by providing to that person a service:

1.1 that involved the respondent doing one or more of the following:

1.1.1 giving advice to the person in relation to the person's income tax return;

1.1.2 completing details of the person's income tax return in preparation for lodgement;

1.1.3 lodging the person's income tax return with the Commissioner of Taxation;

1.2 for which the respondent received a monetary payment for providing the said service;

1.3 with knowledge of the matters referred to in sub-paragraphs 1.1 and 1.2 above;

1.4 while the respondent was not a registered tax agent pursuant to the Tax Agent Services Act 2009 (Cth) (the Act);

1.5 which was not a service relating to a business activity statement; and

1.6 which was not provided as a legal service;

in each case:

1.7 by reason of the matters referred to in sub-paragraphs 1.1 and 1.2 above, provided a service that the person could reasonably be expected to rely upon to satisfy liabilities or obligations, or claim entitlements, that arise, or could arise, under a taxation law; and

1.8 by reason of the matters referred to in sub-paragraphs 1.1 to 1.7 above, supplied a tax agent service in contravention of subsection 50-5(1) of the Act.

THE COURT ORDERS THAT:

2. In respect of the 26 separate contraventions of the Act one pecuniary penalty in the amount of $30,000 is imposed on the respondent.

3. The respondent pay the pecuniary penalty of $30,000 to the Commissioner of Taxation on behalf of the Commonwealth of Australia, such penalty to be paid as follows:

3.1 $5,000.00 on or before 30 November 2012;

3.2 $10,000.00 on or before 30 November 2013;

3.3 $10,000.00 on or before 30 November 2014;

3.4 the balance on or before 10 May 2015.

4. The respondent have liberty to apply in respect of the extension of any of the times provided for payment of the pecuniary penalty by order 3 herein.

5. For a period of 3 years from the date of this order, if she is requested to provide to another person or entity a service relating to one or more of:

5.1 advising another person or entity in relation to their entitlements, liabilities or obligations in relation to an Australian taxation law;

5.2 completing for another person or entity a return or statement in relation to an Australian taxation law; or

5.3 lodging for another person or entity a return or statement in relation to a taxation law with the Australian Taxation Office;

the respondent must, before providing or agreeing to provide the said service, and unless then registered as a tax agent pursuant to the Act, inform the person or entity of the matters referred to in paragraphs 1 to 8 in Form A in Schedule B to the Order and, if the person or entity still requests the service be performed by the respondent:

5.4 have the person or entity complete and sign Form A annexed hereto;

5.5 retain a copy of the form for a period of 3 years; and

5.6 provide any such signed forms to the Tax Practitioners Board within 14 days of its request.

6. The respondent pay the costs of the applicant on a party and party basis to be taxed if not agreed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011

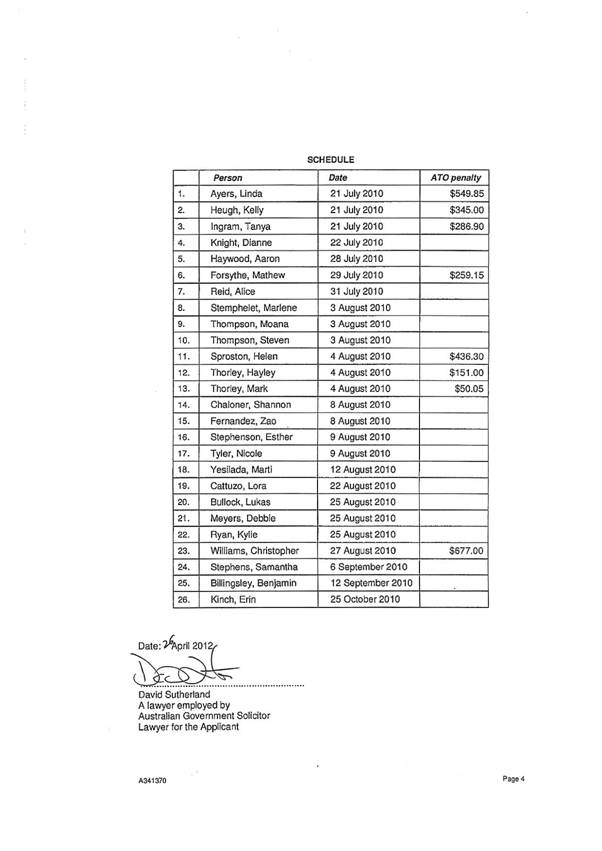

SCHEDULE A

TO ORDER OF 10 MAY 2012

| Person | Date | |

| 1. | Ayers, Linda | 21 July 2010 |

| 2. | Heugh, Kelly | 21 July 2010 |

| 3. | Ingram, Tanya | 21 July 2010 |

| 4. | Knight, Dianne | 22 July 2010 |

| 5. | Haywood, Aaron | 28 July 2010 |

| 6. | Forsythe, Mathew | 29 July 2010 |

| 7. | Reid, Alice | 31 July 2010 |

| 8. | Stemphelet, Marlene | 3 August 2010 |

| 9. | Thompson, Moana | 3 August 2010 |

| 10. | Thompson, Steven | 3 August 2010 |

| 11. | Sproston, Helen | 4 August 2010 |

| 12. | Thorley, Hayley | 4 August 2010 |

| 13. | Thorley, Mark | 4 August 2010 |

| 14. | Chaloner, Shannon | 8 August 2010 |

| 15. | Fernandez, Zao | 8 August 2010 |

| 16. | Stephenson, Esther | 9 August 2010 |

| 17. | Tyler, Nicole | 9 August 2010 |

| 18. | Yesilada, Marti | 12 August 2010 |

| 19. | Cattuzo, Lora | 22 August 2010 |

| 20. | Bullock, Lukas | 25 August 2010 |

| 21. | Meyers, Debbie | 25 August 2010 |

| 22. | Ryan, Kylie | 25 August 2010 |

| 23. | Williams, Christopher | 27 August 2010 |

| 24. | Stephens, Samantha | 6 September 2010 |

| 25. | Billingsley, Benjamin | 12 September 2010 |

| 26. | Kinch, Erin | 25 October 2010 |

SCHEDULE B

to the Order of 10 May 2012

Form A

| I, [print full name] ……….………………………….………..…………………….…………, having requested Avril Hogan to provide a service (i) to me / (ii) to the entity named: ………………………………………………..….….………. [delete whichever inapplicable] relating to one or more of the following: (a) giving advice concerning entitlements, liabilities or obligations that arise or could arise under a taxation law; (b) completing a return or statement in relation to a taxation law; or (c) lodging a return or statement in relation to a taxation law with the Australian Taxation Office; and having been informed that: 1. she is not a registered tax agent; 2. she may not have the educational qualifications to be a registered tax agent and could only finally ascertain whether she is eligible in terms of those qualifications to be registered if she were to apply to the Tax Practitioners Board for registration as a tax agent; 3. she may not have the relevant experience as required by the Tax Agent Services Regulations 2009 to become a registered tax agent; 4. she may not be a fit and proper person to be a registered agent so as to be able to provide a service relating to one or more of items (a), (b) or (c) above for a fee or other reward; 5. a person or entity should seek assistance from a registered tax agent for matters that relate to such services or for such services; 6. she does not wish to receive, and will not accept, any fee, benefit or reward of any kind for providing such a service; 7. she is likely to be contravening the Tax Agent Services Act 2009 if she receives a fee, benefit or reward for providing such a service; and 8. she is required by order of the Federal Court of Australia to inform me of these matters; still request her to provide the service. SIGNED: ……………………………… DATE: …………..…………. ………………………………………………………..……………………………………….. print full address |

| QUEENSLAND DISTRICT REGISTRY | |

| GENERAL DIVISION | QUD 136 of 2012 |

| BETWEEN: | TAX PRACTITIONERS BOARD Applicant |

| AND: | AVRIL HOGAN Respondent |

| JUDGE: | LOGAN J |

| DATE: | 10 MAY 2012 |

| PLACE: | BRISBANE |

REASONS FOR JUDGMENT

1 The Tax Practitioners Board, constituted under the Tax Agent Services Act 2009 (Cth) (Tax Agent Services Act), has made application to the Court for the imposition of pecuniary penalties and related declaratory and injunctive relief arising out of 26 specific alleged contraventions of s 50-5(1) of the Act.

2 That provision materially states that you contravene this subsection if:

(a) you provide a service that you know, or ought reasonably to know, is a tax agent service; and

(b) the tax agent service is not a BAS service, and

(c) you charge or receive a fee or other reward for providing the tax agent service; and

(d) you are not a registered tax agent

For an individual the penalty in respect of each contravention of that provision is a maximum of 250 penalty units. Having regard to the prescription in the Crimes Act 1914 (Cth), by s 4AA(1), that a penalty unit means $110, and by a process of mathematics, the maximum penalty per contravention for an individual is $27,500. Again by a process of mathematics, the total maximum penalty which could be imposed in respect of the alleged contraventions is therefore $715,500.

3 The case has proceeded upon an agreed statement of facts and upon affidavit evidence which is not controversial. The respondent, Mrs Avril Hogan (Mrs Hogan), admits the alleged contraventions. Further, and in the course of submissions, both on behalf of the Board and on behalf of Mrs Hogan, the position was reached whereby the parties agreed that an appropriate penalty in the circumstances of this case was the imposition of a single penalty in the sum of $30,000. For her part, Mrs Hogan had promoted before then that a penalty of $25,000 was appropriate while, for its part, the Board had promoted in submissions that a penalty of $35,000 was appropriate.

4 It may seem to some, therefore, that there has been something of a Solomon-like compromise reached between the parties as to the amount of penalty jointly to submit to the court as appropriate. Nonetheless, the existence of an agreement between the parties with respect to penalty is always, in civil penalty proceedings such as the present, a relevant consideration for the court to take into account in the exercise of a discretion as to the amount of penalty to impose: see NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission (1996) 71 FCR 285 (NW Frozen Foods).

5 That is not to say that an agreement fetters the exercise of a judicial discretion, but rather that it informs it. One ought not depart lightly from an agreed position as to penalty unless, having regard to the particular circumstances of a case, that agreed position would not accord with the just exercise of a judicial discretion. That is not the case here, for reasons which I shall develop.

6 As I have stated, the facts concerned are agreed. In those circumstances it seems to me that the most convenient course is to annex to these reasons for judgment the full text of the agreed statement, and then to make particular observations with respect to features of that agreed position relevant to an acceptance of the agreed penalty, as well as other relevant facts which emerge separately from affidavit evidence.

7 Before so doing it is desirable, particularly because, so I was informed by counsel on behalf of the Board, this is the first occasion when it has fallen to the Court to impose penalties under the current legislation in respect of this type of conduct, to make some observations of a general nature with respect to the regulation of tax agents and those who, for reward, act as a tax agent without registration, or otherwise contravene s 50-5.

8 Provision in federal law for the registration of tax agents is no new subject. In the successive Federal Income Tax Assessment Acts, the Income Tax Assessment Act 1915 (Cth), the Income Tax Assessment Act 1922 (Cth) and, as enacted, the Income Tax Assessment Act 1936 (Cth) (1936 Act), there was no provision for the registration of tax agents.

Such registration was first introduced by the Income Tax Assessment Act 1943 (Cth) (1943 Act), which introduced into the 1936 Act, a new part, Pt VIIA, directed to the registration of tax agents.

9 In his second reading speech, in respect of the Bill, which became the 1943 Act, the then Commonwealth Treasurer, the Honourable J.B. Chifley, made the following statement:

Honourable members may recall that the Royal Commission on Taxation 1932-1934, in a third report, expressed the opinion that the registration of tax agents would be in the best interests of both the tax payer and the Taxation Department. The Royal Commissioner said that registration would provide an assurance to both the tax payer and the Department – that a person authorised to act on behalf of a tax payer is reputable and competent. It would prevent exploitation of the tax payer by unscrupulous persons who may ultimately involve him in serious trouble and perhaps penalties. Moreover, it would also enable the Department to deal effectively with such unscrupulous persons.

These views of the Royal Commissioners, with which I agree, were approved by the government of the day but at the time, a system of registration was already in operation in the states of Queensland and South Australia and it was decided to leave the matter to the states in order to avoid duplication. In due course, the states of Tasmania and New South Wales, enacted legislation, requiring the registration of tax agents. Registration has not been required in Victoria or Western Australia. Since the passage of the uniform income tax legislation last year however, the state laws relating to income tax are in suspense and the establishment of a system of commonwealth registration becomes necessary.

10 As can be seen therefore, the origins of federal registration of tax agents are to be found in the rise of Commonwealth fiscal supremacy in the field of income tax and the co-relative need, having regard to a scheme of national income tax legislation, for national registration of tax agents. For all that, one sees in Pt VIIA of the 1936 Act, echoes of the former State regulatory past in the provision, in the now superseded regime, for separate, State registration boards for tax agents. That regime has been replaced by the Tax Agent Services Act which provides for a national board.

11 There are features of the current act which, so far as presently material, find echoes in earlier federal regulation. Thus, even as originally enacted, it was a feature of that regulation, by s 251L of the 1936 Act, that, a person other than a person exempted by a tax agents’ registration board, should not demand or receive any fee for or in relation to the preparation of any income tax return or objection or for or in relation to the transaction of any business on behalf of a tax payer in income tax matters, unless he is a registered tax agent. Interestingly, in providing scope for a board to exempt a person, Parliament conditioned that exemption upon a board being satisfied as to no more than a particular minimal level of income being derived by the person concerned as a tax agent. In other words, it was not part of the original regime that one could not without registration, act as a tax agent and act only gratuitously but, for all that, the threshold amount by reference to which exemption could be granted, was never high. In contrast, s 50-5(1)(c), speaks of fee or other award and there is not in that section, scope for an exemption of the kind previously found in Pt VIIA.

12 Nonetheless, the purposes of the Tax Agent Services Act are not so very different at all from those contemplated by Mr Chifley when first introducing a bill for Federal regulation of tax agents. Manifestly, there is discerned by Parliament, a public interest, both for members of the public and for the administration by the Commissioner of Taxation and his officers of federal revenue laws, in providing for the registration of duly qualified and fit and proper persons to carry on business as tax agents. Mr Chifley’s aim of protecting the public from the unscrupulous is also manifest in the Tax Agent Services Act as a continuing aim on the part of Parliament.

13 It is not, of course, only the unscrupulous who must be penalised. I do not, having regard to the agreed facts, regard Mrs Hogan as unscrupulous. Nevertheless, she has provided a service for which she is not qualified. There is force in the submission made on behalf of the Board that there is a section of the community, perhaps not sophisticated in matters of business and commerce, who are in particular need of being protected from the holding out and provision of services by persons who profess an ability to assist in the preparation and submission of tax returns for a fee but who have no qualification or registration. That particular class of persons may well find the task of preparing individually, a tax return, difficult but have difficulty in seeing the benefit of paying a little bit more for the services of a registered tax agent.

14 The jurisdiction the Court exercises is, in the first instance, in my opinion, a protective one in the public interest, with the penal aspects of the jurisdiction being subsidiary to that protective purpose of the legislation and designed to supplement that protective purpose by both specific and general deterrents in respect of contravening conduct.

15 It is a feature of this case that the 26 instances of contravention, detailed in the annexed agreed statement, are representative contraventions. By that, I mean that it is agreed that there was other conduct of a like kind. What the Board has done is to adopt a permissible course of laying representative charges. Equally, Mrs Hogan has, to her particular credit, acknowledged that they have that quality. I say that because, in theory, it was open to the Board to lay many other charges. That does not mean at all that Mrs Hogan is to be subject to penalties other than those applicable to the contraventions charged, only that the assessment of penalty must occur against the background that these are representative charges.

16 The considerations that are relevant in respect of the imposition of penalty in respect of this type of contravention are first and foremost the subject matter, scope and purpose of the Act, and in particular, s 50-5. As I have said, the view I take is that the legislative purpose is protective in respect of provision of tax agent services only by registered persons. Other considerations intrude. Considerations of a general nature of the kind identified in cases such as Trade Practices Commission v CSR Limited (1991) ATPR 41-075; NW Frozen Foods and Australian Communications Management Authority v Mobilegate Limited A Company Incorporated in Hong Kong (No 4) (2009) 180 FCR 467 are pertinent. In this case, it is not necessary to elaborate in detail in respect of the applicability of such general considerations because of the agreed position.

17 In respect of the 26 contraventions, the overall financial benefit derived by Mrs Hogan was in excess of $1200. She acknowledges that she has received other money in respect of the preparation of returns for which she has not been charged by the Board. It is important in the imposition of penalties, not just by reason of specific deterrents, but also general deterrence, to make it plain by the imposition of those penalties that there is no risk worth taking, having regard to the penalty applicable, by contravening s 50-5. In other words, it is important to pay due regard to the maximum, and not to trivialise the parliamentary intent. For all that, the penalty must nonetheless be appropriate to individual circumstances. There can be no template outcome. The range promoted by the parties was, as I observed in the course of the penalty hearing, a range which I regarded as an appropriate range having regard to the purposes of the Act and, further, general considerations with respect to penalty which emerge from the cases to which I have made reference. The range is one which, having regard to the particular conduct, is a range which serves the interests of both general and specific deterrence by underscoring that it is economically irrational, and a grave risk, for a person to seek to engage in this conduct in the hope that the rewards will be greater than the risk of detection and the penalty that will flow upon a proved contravention.

18 It is apparent from the evidence that individual tax payers have suffered by this conduct, by the imposition of additional tax as a result of incorrect returns. This also is a factor to take into account in relation to the imposition of penalty. So, too, is a particular attitude, evident in the agreed statement, on the part of Mrs Hogan in the initial investigation of clients by the audit staff of the Australian Taxation Office. The messages concerned arose in this way and was in these terms:

Mrs Hogan received from a client taxpayer, Ms Thorley, an SMS message regarding her 2010 return, then being audited by the tax office. Her reply messages were as follows:

“someone has told the ATO I’m doing tax returns from home”

“you only have to tell them a friend helped you, and that’s all you have to tell them”

“the whole point of these audits is to make people use tax agents. Ridiculous as they charge a fortune. You can do yourself”

Those were the three SMS messages sent by Mrs Hogan to Ms Thorley.

19 It must be said at once that the whole purpose of tax audits is to inquire as to whether taxation returns have been lodged according to law, and that the returns as lodged are compliant with the requirements of Federal revenue law. It must also be said that the point of audits is not to make people use tax agents. The Tax Agent Services Act does not have, as any part of its discernible purpose, the obliging of people to use tax agents. It leaves that to the good sense and judgment of individuals and corporations. Its purpose, overwhelmingly, is to ensure that, if persons do, as a matter of good sense and judgment, use tax agents, that they use only registered tax agents.

20 There is a benefit from using a registered tax agent, which may flow, in particular circumstances, to a taxpayer by virtue of the regime found in s 284-75 in Sch 1 to the Taxation Administration Act 1953 (Cth), which, in certain circumstances, provides for an exemption from administrative penalty by the engagement of a registered tax agent. That, though, can be seen to be a feature of a circumstance where a person has relied upon a registered tax agent to take a particular position. It is not to be regarded as in any way obliging people to use registered tax agents.

21 Mrs Hogan has been quite frank in her acknowledgement of the sending of the SMS messages. She has also been extremely frank in a letter exhibited to her affidavit. That letter is addressed to the Court. I have had particular regard to that letter. She makes in it an unqualified apology for her behaviour. It is quite apparent from her affidavit, which, as I have said, is not challenged, that these proceedings have had a scarifying effect on her and upon her family. I have no doubt at all, and the absence of that doubt is underscored by her cooperation with the administration of justice, that she is genuinely contrite in respect of the conduct in which she engaged. That, too, is a factor which I have taken into account in relation to deciding to regard the penalty agreed between the parties as one which is appropriate.

22 I do not propose to elaborate further on the circumstances of the case, as it would be if I had to explain why I had of my own motion fixed a particular penalty (as opposed to regarding it as appropriate to accept that promoted by the parties).

23 The Commissioner has also sought declaratory and injunctive relief. Whatever may have been the position beforehand, there is no doubt, having regard to Australian Competition and Consumer Commission v MSY Technology Pty Ltd [2012] FCAFC 56, that there is power in circumstances such as the present to grant declaratory relief. Power is one thing, whether the power should be exercised as a matter of discretion is another. Here, again, this is an appropriate case, in my opinion, for the exercise of that power. There is a very strong public interest in the recording formally by declaration of the contraventions. Reference might be made in that regard to an observation made by Spigelman CJ in New South Wales Bar Association v Cummins (2001) 52 NSWLR 279 at [32] where, with the agreement of Mason P and Handley JA, the Chief Justice stated:

In respect of an order removing a practitioner from the role of practitioners where it was additionally sought to have a declaration made that the person concerned was not a fit and proper person that “such a declaration serves the public interest not least by reaffirming the high regard the court has for the reputation and standing of the legal profession represented before the court by the Bar Association. A formal declaration will go some way to assuring the public that conduct of this character cannot and is not tolerated in the profession. Where as here, the public interest is involved the court should formally record the result.

In making that statement, his Honour made reference to Tobacco Institute of Australia Limited v Australian Federation of Consumer Organisations Inc No 2 (1993) 41 FCR 89 at 100, 106 and 107. Here, the making of a declaration will affirm in a public way the intolerance of contraventions of s 50-5 and more particularly the acceptance of the provision for a fee or reward of tax agent services by unregistered tax agents.

24 There is then a question of whether injunctive relief should go. Again, it is not a question of power but rather whether the relief sought by the Commissioner should be granted. In effect, the injunctions provide for a requirement of disclosure on the part of Mrs Hogan to those who would seek to engage her that she is not registered. There may well be, I apprehend, a protective element not just for the public but also for Mrs Hogan in this. I have a sense, upon reading her affidavit and the agreed statement, that at times she has come under informal pressure from those who have come to know of her undertaking these services further to provide them. The existence of an injunction will allow her to say that she must not for fee or reward and is obliged to tell people as well as informing then that she is not registered.

25 The time proposed for the length of the injunction is three years. That seems to me to be an apt length of time to subject Mrs Hogan to that obligation, having regard to the length of time in which she has engaged in contravening conduct and the likelihood that after that time, there will be no further need for her to be reminded of the obligations which are found in the Tax Agents Services Act.

26 There is also, manifestly, having regard to the financial circumstances not just of Mrs Hogan personally but also of her family a need to allow time for payment. It is not necessary to delve into the detail of those financial circumstances. Suffice it to say, it is not just for reasons of symmetry with the length of the injunction period but also because I believe it to be an apt balancing of a need to confront the requirement to pay a penalty with the ability to pay that penalty that she should be allowed in total a period of three years to pay the penalty in full.

27 That total period should be divided into instalment periods, so that the need to confront her requirement to pay a penalty is continually before Mrs Hogan and also so that any difficulty which she might face in so doing is drawn at as early a stage as possible to the attention of the Board.

28 The orders then in respect of penalty will provide for the payment of $5000 by 30 November 2012; a further $10,000 by 30 November 2013; a further $10,000 by 30 November 2014 with the balance being payable not later than three years from this date, in other words, upon the same date as the expiry of the injunctive relief that I propose to grant. The penalties concerned must, as is provided for by s 50-45 of the Tax Agent Services Act be paid to the Commissioner of Taxation who receives that penalty on behalf of the Commonwealth. In addition, the Board has made application for costs. Costs are able to be awarded in a civil penalty proceeding. There is no opposition to the awarding of costs to the Board on a party and party basis to be taxed if not agreed.

29 I shall also make provision in the orders for the allowance of liberty to apply in respect of an extension of times fixed by this order for payment. The occasion for making that provision is not to lead Mrs Hogan to the view that the amounts concerned are not payable and are not payable within the times specified but rather to accommodate the contingency, which is all too real in present economic circumstances, that, through no fault of her own or that of her husband, she may for good reason find it not reasonably possible at all notwithstanding her endeavours to make payment in full as and required. If so, she should in a timely way communicate fully and in detail to the Board why that is so. I should expect that in those circumstances if there is a genuine case made that the Board in turn would promote to the Court the making of orders by consent extending time.

30 There will be orders accordingly.

| I certify that the preceding thirty (30) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Logan. |

Associate:

ANNEXURE