FEDERAL COURT OF AUSTRALIA

Quality Publications Australia Pty Limited v Commissioner of Taxation [2012] FCA 256

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

QUALITY PUBLICATIONS AUSTRALIA PTY LIMITED (ACN 096 396 593) Applicant | |

|

AND: |

Respondent |

|

DATE OF ORDER: |

|

|

WHERE MADE: |

THE COURT ORDERS THAT:

2. The applicant pay the respondent’s costs as agreed or taxed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

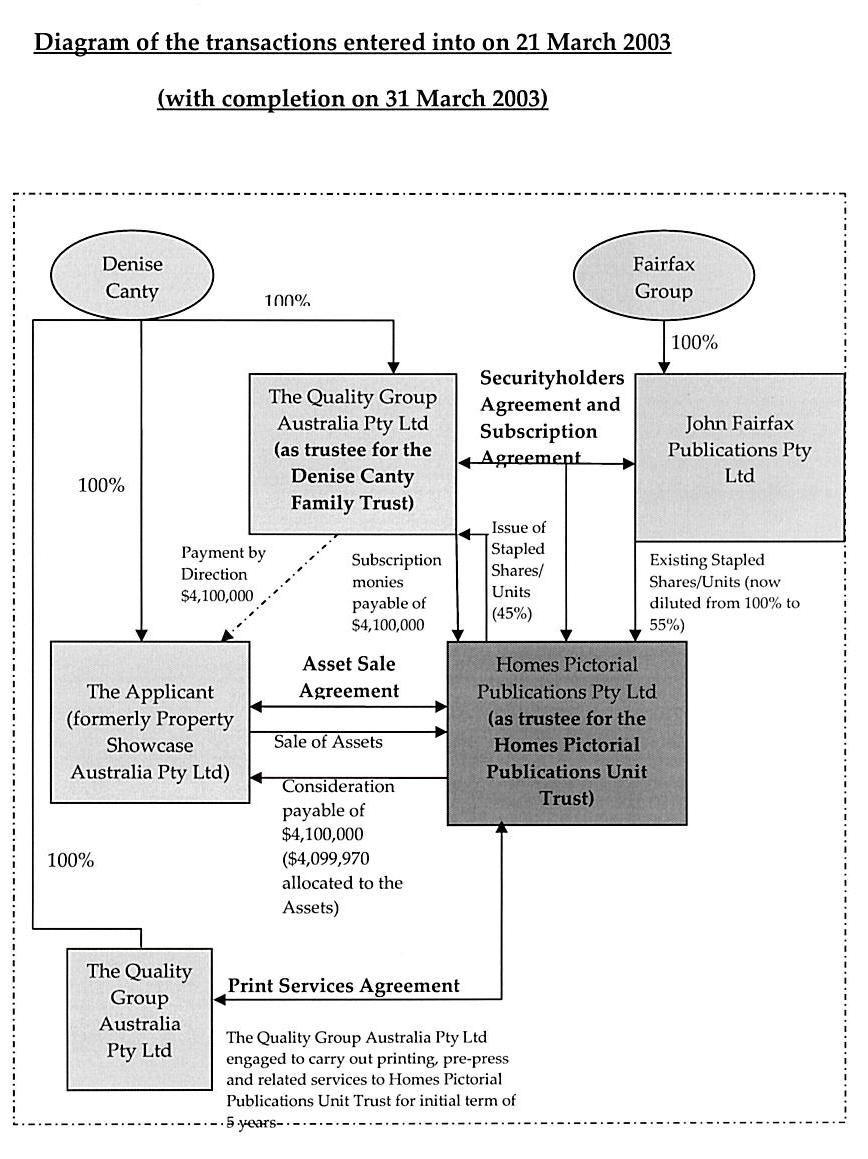

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 275 of 2009 |

|

BETWEEN: |

QUALITY PUBLICATIONS AUSTRALIA PTY LIMITED (ACN 096 396 593) Applicant |

|

AND: |

COMMISSIONER OF TAXATION Respondent |

|

JUDGE: |

EDMONDS J |

|

DATE: |

28 MARCH 2012 |

|

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

INTRODUCTION

1 This is an application by way of appeal pursuant to s 14ZZ of the Taxation Administration Act 1953 (Cth) (“TAA 1953”) against an objection decision of the respondent (“the Commissioner”) disallowing the applicant’s (“the taxpayer”) objection against an amended assessment of income tax issued to the taxpayer for the income year ended 30 June 2003.

2 The amended assessment included a sum of $3,100,000 in the taxpayer’s assessable income as the net capital gain arising on a disposal by the taxpayer (then called Property Showcase Australia Pty Ltd) of certain assets, including the masthead, “Property Showcase”, to Homes Pictorial Publications Pty Ltd (“Homes Pictorial”) as trustee of Homes Pictorial Publications Unit Trust (“Homes Pictorial Unit Trust”), pursuant to an Asset Sale Agreement dated 21 March 2003. The ultimate issue on this appeal is whether the net capital gain was that amount or, as the taxpayer contended, some lesser amount.

3 It is common ground that CGT Event A1 (s 104-10 of the Income Tax Assessment Act 1997 (Cth) (“ITAA 1997”)) occurred at the time the taxpayer entered into the Asset Sale Agreement on 21 March 2003.

THE ISSUES

4 The ultimate issue raised on the appeal, namely, whether the net capital gain to be included in the taxpayer’s assessable income pursuant to s 102-5 of the ITAA 1997 for the income year ended 30 June 2003 in respect of the disposal of the assets was the amount of $3,100,000 or some lesser amount, involves the determination of up to four anterior issues:

(1) Whether the cost base of the assets (for the purposes of Div 110 of the ITAA 1997) was greater than the cost base upon which the net capital gain was assessed, namely, $1 million.

(2) Whether the capital proceeds in respect of the disposal of the assets was in the amount of $4,100,000, being money the taxpayer received or was entitled to receive pursuant to s 116-20(1)(a) of the ITAA 199.

(3) Alternatively, whether the capital proceeds in respect of the disposal of the assets was some other amount by virtue of the operation of s 116-20(1)(b) of the ITAA 1997. In context, the issue here was whether the taxpayer received or was entitled to receive “other property” in respect of the disposal of the assets and, if so, what was the “market value” of the “other property” for the purpose of calculating the capital proceeds.

(4) Alternatively, whether the capital proceeds from the disposal of the assets was some other amount by virtue of the operation of s 116-30(2)(b)(i) of the ITAA 1997. In context, the issue here was whether the taxpayer and Homes Pictorial, as trustee of Homes Pictorial Unit Trust, dealt with each other at arm’s length in connection with the disposal of the assets and, if they did not, whether the capital proceeds exceeded the market value of the assets for the purposes of s 116-30(2)(b) of the ITAA 1997 so as to actuate the operation of the “market value substitution rule”.

Finally, there was the issue of whether the administrative penalty of $93,000 was properly payable by the taxpayer pursuant to s 284-75(1) of Sch 1 to the TAA 1953.

5 As to anterior issue (1), it is common ground that in assessing the taxpayer to a net capital gain of $3,100,000 on the sale of the assets, the Commissioner’s starting point, based on information provided to the Commissioner by the taxpayer during the course of the audit, was that the taxpayer’s cost base (see s 110-25 and s 110-35 of the ITAA 1997) in the assets was $1,000,000. The taxpayer led no evidence to suggest that the taxpayer’s cost base in the assets was greater than $1,000,000; indeed, such evidence as was led would point to the taxpayer’s cost base in the assets being less than $1,000,000. This no doubt explains the taxpayer’s acceptance of the Commissioner’s starting point (para (10) of the taxpayer’s preliminary outline of submissions). It is not open to this Court to increase the amount assessed. Moreover, having regard to my conclusions on other anterior issues, my conclusion on the ultimate issue is that the amended assessment is not excessive and issues going to the extent to which the amended assessment might be excessive do not arise. As such, anterior issue (1) need not be considered further.

THE FACTUAL CONTEXT

The purchase of the property magazine business by the taxpayer in 2001

6 The taxpayer was incorporated on 30 March 2001. From 9 November 2001 (and therefore, at all relevant times for the purposes of these proceedings) the shares in the taxpayer were wholly owned by Denise Irene Canty and the sole director of the company was Paul Brian Canty. Paul and Denise Canty are husband and wife.

7 In or around October 2001, the taxpayer purchased a property magazine publishing business from a company called Roblyn Products Pty Limited (“Roblyn”) pursuant to a contract for sale dated 4 July 2001. The contract stated that the purchase price was $850,000. An unstamped copy of the contract was admitted into evidence subject to compliance with the requirements of s 304(2)(b) of the Duties Act 1997 (NSW).

The background factual matrix as to sale of the property magazine business by the taxpayer

8 In or around April / May 2002, Paul Canty (on behalf of the taxpayer) was approached by Mr Ian Crowther, the General Manager of Fairfax Community Newspapers Liverpool, a subsidiary of Fairfax Media Limited (“Fairfax”), regarding whether the taxpayer was interested in selling the Property Showcase business to Fairfax.

9 There then followed several face to face meetings and telephone calls between representatives of the taxpayer and representatives of the Fairfax group concerning this matter, culminating in a presentation by representatives of the taxpayer of the Property Showcase business (and its value) to the Fairfax group in September 2002.

10 From as early as July 2002, Matthew Bradfield (a partner of Bradfield Partners) had been engaged by Fairfax Regional Newspapers to assist in carrying out a due diligence of the taxpayer’s business, including assessing the relative values of the business carried on by the taxpayer and that being carried on by Homes Pictorial as trustee of the Homes Pictorial Unit Trust, in order to assist Fairfax in negotiations with the taxpayer’s representatives. Mr Bradfield’s involvement expanded as the transaction developed and he was later asked to value the taxpayer’s business for stamp duty purposes (see [29] below).

11 The Homes Pictorial Unit Trust was constituted under a trust deed dated 28 November 1986. The trustee was Homes Pictorial. Prior to the transactions that occurred on 21 March 2003, both the shares in the trustee and the units in the Homes Pictorial Unit Trust were owned by John Fairfax Publications Pty Ltd (a member of the Fairfax Group). The Homes Pictorial Unit Trust published a magazine called “Homes Pictorial” that, like “Property Showcase”, advertised properties for sale.

12 On or about 12 September 2002, a “Homes Pictorial/Showcase Transaction Timetable” was prepared and issued by Minter Ellison (the solicitors acting for the Fairfax Group including the Homes Pictorial Unit Trust) to the taxpayer. The timetable referred, inter alia, to the due diligence process to occur, made reference to a possible approach to the Australian Competition & Consumer Commission (“ACCC”), provided for a series of scheduled meetings between the parties and referred to certain target dates for agreement on business plans, draft contracts, printing tender and other events to occur.

13 Various meetings (as scheduled in the timetable) took place between representatives of the taxpayer, Homes Pictorial and Fairfax Legal on 17 September 2002, 24 September 2002, 8 October 2002 and 17 October 2002. The minutes for the meetings indicate that discussion occurred between the parties regarding, inter alia, the timetable, due diligence, commercial terms, administration agreement, shareholders agreement, staffing issues and valuation. The minutes for the meeting on 8 October 2002 referred to an internal Fairfax presentation to be made to Mr Fred Hilmer (the then Chief Executive Officer of the Fairfax Group). The minutes for the meeting on 17 October 2002 recorded, inter alia, that Mr Hilmer had signed off on the business case as presented and agreed to a 55/45 split.

14 The representatives of the taxpayer during the negotiations included Paul Canty and his brother, Michael Canty, as well as Scott Nicholls from Sullivan Dewing Chartered Accountants. The taxpayer also received legal advice in relation to the transaction from Evangelos Patakas, solicitor, and later Matthew Rowe, a partner of Coleman & Greig.

15 In November and December 2002, various draft Asset Sale Agreements were prepared by the solicitors acting for the Fairfax Group and circulated to the parties.

16 On or around 29 November 2002, a paper entitled “Homes Pictorial/Showcase transaction – Current Issues as at 29 November 2002” was prepared internally by Fairfax. The document contained, inter alia, a discussion in relation to the Fairfax position in respect of the relative equity positions of the parties in the joint venture and Fairfax’s preliminary view at that time of the value of the Property Showcase business (i.e. that the valuation of 45% of the business going forward was between $2.4 and $2.5 million).

17 Further negotiations took place between the parties in early February 2003. It appears there were further drafts of the Asset Sale Agreement on 6 March 2003, 14 March 2003 and 19 March 2003 that were circulated to and reviewed by the parties.

The documents executed on 21 March 2003

18 On 21 March 2003, a suite of documents (“the agreements”) were executed by various parties to implement the transaction, as follows:

(1) An Asset Sale Agreement between the taxpayer, Homes Pictorial (as trustee of Homes Pictorial Unit Trust) and Paul and Denise Canty (“Asset Sale Agreement”).

(2) A Subscription Agreement between Homes Pictorial (as trustee of Homes Pictorial Unit Trust), John Fairfax Publications Pty Limited and The Quality Group Australia Pty Limited (“Quality Group”) (as trustee of the Denise Canty Family Trust) (“Subscription Agreement”).

(3) A Securityholders Agreement between Homes Pictorial (as trustee of Homes Pictorial Unit Trust), John Fairfax Publications Pty Limited and Quality Group (as trustee of the Denise Canty Family Trust) (“Securityholders Agreement”).

(4) A Print Services Agreement between Home Pictorial and the Quality Group (“Print Services Agreement”).

19 Quality Group (now called Quality Logistics Australia Pty Ltd) was incorporated on 28 June 2002 and at all relevant times was wholly owned by Denise Canty. At the relevant time to the proceedings, its sole director was Paul Brian Canty.

20 The Denise Canty Family Trust was settled on 24 January 2003 and is a discretionary trust. The Trustee is Quality Group and the primary discretionary objects (called “Nominated Beneficiaries”) are Denise Canty and the taxpayer. Denise Canty is also the Nominator and is thereby empowered to remove the trustee.

21 On 31 March 2003, a Loan Agreement was also executed between John Fairfax Group Finance Pty Ltd (as lender), Homes Pictorial (as borrower), Quality Group and John Fairfax Publications Pty Limited. The Loan amount was $1,000,000 (or such other amount as agreed before Completion by the parties) and $500,000 was to be made available in cash on Completion and $410,000 made available in cash in sufficient time for the borrower to pay the GST element of the Consideration under the Asset Sale Agreement. The Completion date was as defined in the Asset Sale Agreement.

Asset Sale Agreement

22 The salient clauses of the Asset Sale Agreement for present purposes are as follows:

(1) Clause 2 provided that the taxpayer agreed to sell the “Assets” (defined below) for Consideration to Homes Pictorial (as trustee for Homes Pictorial Unit Trust).

(2) Clause 1.1 defined the “Assets” as:

(i) the Masthead (meaning the masthead publications as set out in Sch 1 – Property Showcase Hawkesbury/Nepean, Property Showcase Hills District and Property Showcase Central Coast);

(ii) the Business Names (as set out in Sch 3);

(iii) the Intellectual Property (defined in cl 1.1);

(iv) the Trade Marks (meaning the registered and unregistered trade marks used by the taxpayer, as set out in Sch 3, and all associated goodwill); and

(v) Goodwill (defined in cl 1.1).

(3) Clause 3.1 provided that the “Consideration” was the amount of $4,100,000 apportioned as set out in that clause. Relevantly, the amount of $4,099,970 was apportioned to the Assets and the remaining $30 to the restrictive covenants referred to below.

(4) Clause 6.3 required Homes Pictorial to pay the Consideration to the taxpayer on Completion. Importantly, cl 6.4 provided that Homes Pictorial may pay the Consideration by directing Quality Group (as trustee of the Denise Canty Family Trust) to pay the subscription price ($4,100,000) due from it to Homes Pictorial under the Subscription Agreement, directly to the taxpayer (on behalf of Homes Pictorial).

(5) Clause 10 provided for the taxpayer, Paul Canty (being the sole director of the taxpayer) and Denise Canty (being the sole shareholder of the taxpayer) to enter into restrictive covenants for the benefit of Homes Pictorial as trustee of the Homes Pictorial Unit Trust. The amount of the Consideration apportioned under cl 3.1 to each of the restrictive covenants was in the amount of $10.

(6) Clause 15.9 provided that the Asset Sale Agreement constituted the entire agreement between the parties in connection with its subject matter and superseded all previous agreements or understandings between the parties in connection with its subject matter. The entire agreement clause amounts to an express avowal by the parties that all the terms regarding the sale of the Assets were contained in the agreement: Branir Pty Ltd v Owston Nominees (No. 2) Pty Ltd (2001) 117 FCR 424 at [440] per Allsop J.

(7) Completion (being the completion of the sale and purchase of the Assets contemplated in the Asset Sale Agreement (cl 1.1) was to take place on 31 March 2003 (or such other date agreed by the parties) as part of the completion of the Subscription Agreement: (cl 6.1 and cl 1.1). Further, in respect of Completion, no party was obliged to comply with its obligations for Completion unless all parties required to undertake completion obligations under the Subscription Agreement were ready, willing and able to do so: (cl 6.5(c)).

Subscription Agreement

23 The salient clauses of the Subscription Agreement for present purposes are as follows:

(a) Clause 2 provided for the issue to Quality Group (as trustee of the Denise Canty Family Trust) of “Stapled Securities” (being 45% of the ordinary shares in Homes Pictorial and 45% of the units in the Homes Pictorial Unit Trust) for “subscription monies” in the amount of $4,100,000.

(b) Clause 2.1(b) required Homes Pictorial to direct Quality Group (as trustee of the Denise Canty Family Trust) to pay to the taxpayer $4,100,000, being the subscription monies payable under the Subscription Agreement

Securityholders Agreement

24 The Securityholders Agreement set out the terms and conditions for the management and control of the Homes Pictorial Unit Trust and the conduct of its business.

Print Services Agreement

25 The Print Services Agreement set out the terms on which Quality Group would perform printing and related services for the magazines published by the Homes Pictorial Unit Trust, including relevantly “Homes Pictorial” (for which Fairfax had previously performed such services) and the magazines previously published by the taxpayer (cl 3) for the fees set out in cl 5. The term of the agreement was 5 years: (cl 4.1).

The result of the Agreements

26 A diagram of the relevant entities and the agreements, provided in the Commissioner’s outline of submissions, is set out below.

27 As a result of the execution of the agreements:

(1) The Assets of the taxpayer were sold for consideration of $4,099,970 to Homes Pictorial (as trustee of Homes Pictorial Unit Trust). In consideration for the giving of the restrictive covenants, the taxpayer and Paul and Denise Canty each received $10.00. The total consideration payable under the Asset Sale Agreement was $4,100,000.

(2) The Consideration of $4,100,000 payable under the Asset Sale Agreement was paid to the taxpayer by a direction given by Homes Pictorial (as trustee of Homes Pictorial Unit Trust) to Quality Group (as trustee for Denise Canty Family Trust) for payment by the latter to the taxpayer in the amount of $4,100,000 (being the subscription monies payable by Quality Group (as trustee of the Denise Canty Family Trust) under the Subscription Agreement.

(3) Quality Group (as trustee of the Denise Canty Family Trust) thereafter owed the taxpayer a debt of $4,100,000.

(4) Quality Group took over the printing of both the magazines previously published by the taxpayer and the “Homes Pictorial” magazine.

The valuation of the business assets of the taxpayer

28 On or about 7 May 2003, an independent written valuation of the business assets of the taxpayer that had been sold pursuant to the Asset Sale Agreement was obtained by the Directors of Homes Pictorial (as trustee of the Homes Pictorial Unit Trust) for the purposes of calculating stamp duty.

29 The opinion of the valuer, Matthew Bradfield, was that the fair value of the business assets sold by the taxpayer to Homes Pictorial was in the range of $2,460,000 to $5,740,000 and he recommended that the fair valuation for the calculation of stamp duty was $4,100,000 (in other words, the mid-point of the relevant range).

The 2003 income tax return of the taxpayer and the amended notice of assessment

30 The taxpayer did not include any capital gain as a result of disposing of the Assets in its income tax return as lodged for the income year ended 30 June 2003. In this regard, the taxpayer made a representation that no CGT event had occurred during the year of income.

31 Following an income tax audit in 2006 and 2007, an amended assessment was issued to the taxpayer on 13 November 2007. The taxpayer’s assessable income was increased by an amount of $3,100,000 pursuant to s 102-5 of the ITAA 1997 as a result of the disposal of the Assets (CGT Event A1). The net capital gain was calculated on the basis of capital proceeds of $4,100,000 and a cost base of $1,000,000 in the Assets.

32 A tax shortfall penalty was also imposed on the taxpayer of 50% for “recklessness” in the amount of $465,000 pursuant to Div 284 of Sch 1 of the TAA 1953. As a result of the taxpayer making a voluntary disclosure, the Commissioner reduced the tax shortfall penalty by 80% to the amount of $93,000.

33 On 3 January 2008, the taxpayer objected to the amended assessment and the imposition of a tax shortfall penalty.

34 By a notice of decision on objection dated 4 February 2009, the Commissioner wholly disallowed the taxpayer’s objection.

ANTERIOR ISSUE (2): Whether the capital proceeds in respect of the disposal of the assets was in the amount of $4,100,000 pursuant to s 116-20(1)(a) of the ITAA 1997?

Statutory Context

35 Section 116-20(1) provides the general rule for determining the capital proceeds from a CGT event as follows (relevantly for the 2003 income year):

“116-20 General rules about capital proceeds

(1) The capital proceeds from a *CGT event are the total of:

(a) the money you have received, or are entitled to receive, in respect of the event happening; and

(b) the *market value of any other property you have received, or are entitled to receive, in respect of the event happening (worked out as at the time of the event).

Note 1: The timing rules for each event are in Division 104.

Note 2: In some situations you are treated as having received money or other property, or being entitled to receive it: see section 103-10.

Note 3: If you dispose of shares in a buy-back, the capital proceeds are worked out under Division 16K of the Income Tax Assessment Act 1936.”

Analysis

36 In the present case, CGT A1 event happened by reason of the disposal of the Assets by the taxpayer. The time of the event was at the time of execution of the Asset Sale Agreement by the parties; relevantly, 21 March 2003. The Asset Sale Agreement plainly expressed the agreement of the contracting parties that:

(1) The taxpayer agreed to sell the Assets to the Purchaser (Homes Pictorial as trustee of the Homes Pictorial Unit Trust) and the Purchaser agreed to buy the Assets for the Consideration (cl 2(a)). The Consideration for the Assets was stated to be $4,099,970, that is, an amount of money (cl 3.1); and

(2) the payment of the Consideration (due to be paid at Completion – cl 6.3) by the Purchaser may be made by way of a direction to Quality Group (as trustee of the Denise Canty Family Trust) to pay the subscription price due by it to the Purchaser under the Subscription Agreement direct to the taxpayer on the Purchaser’s behalf in satisfaction of the Consideration (cl 6.4).

37 The Subscription Agreement plainly expressed the agreement of the parties that:

(1) Homes Pictorial (as trustee of the Homes Pictorial Unit Trust) must direct the Investor (being Quality Group as trustee of the Denise Canty Family Trust) to pay to the taxpayer an amount of money of $4,100,000 (cl 2.1). This sum was in fact explicitly referred to as the “subscription monies” for the Stapled Securities to be subscribed for by the Investor.

(2) The amount of $4,100,000 was to be paid in satisfaction of the GST exclusive consideration payable by Homes Pictorial (as trustee of the Homes Pictorial Unit Trust) for assets sold pursuant to the Asset Sale Agreement (such that a debt was created owing by the Investor to the taxpayer).

38 A mechanism for a “payment by direction” of the Consideration to the taxpayer, on behalf of Homes Pictorial as trustee, did not have the effect of changing or extinguishing the entitlement of the taxpayer to receive an amount of money in the sum of $4,100,000 in respect of the disposal of the Assets. The entitlement to this sum of money arose directly pursuant to the Asset Sale Agreement executed by the parties on 21 March 2003.

39 Further, the payment by direction in cl 2.1 of the Subscription Agreement explicitly stated that an amount of money ($4,100,000) was to be paid by Quality Group (as trustee of the Denise Canty Family Trust) to the taxpayer. The taxpayer remained at all times entitled to receive an amount of money.

40 Recently, in Commissioner of Taxation v Rozman (2010) 186 FCR 1, Perram J had cause to consider whether a direction to a debtor by a private company, to discharge a debt by payment to a third party amounted to a “payment” by the company for the purposes of s 109C(1) of the ITAA 1936. In that case, the private company (Tredex) directed two of its debtors (Fibre and Triton) to pay to the taxpayer moneys owed by them to the company. His Honour held that the payment of the amounts to the taxpayer constituted payment by the company and made the following observations regarding payments by direction generally (at [19]–[24]):

“[19] … The question which arises, therefore, is whether a direction by a private company to a debtor to discharge the debt by payment to a shareholder can be described as being a situation in which ‘a private company pays an amount to an entity’.

[20] I have no doubt that it does. As a matter of ordinary English, the verb ‘to pay’ includes amongst its many meanings notions of satisfaction and discharge. Thus, only a pedant would protest that a woman who buys a pair of shoes on a credit card has not paid for them; and this is so notwithstanding that every credit card purchase conceals at least one payment by direction: Visa International Service Association v Reserve Bank of Australia (2003) 131 FCR 300 at [71]-[74] per Tamberlin J. So too, it would be idle to suggest that a man who buys a hat by cheque has not paid for it simply because a cheque is a direction to a financial institution to pay a sum certain to another person: s 10 of the Cheques Act 1986 (Cth).

[21] In this case it could scarcely be suggested that had Tredex drawn a cheque upon its bankers in favour of Ms Rozman and delivered that cheque to her that it would not have paid her any money because the true flow of funds was from its bankers to hers. Yet, if that be not so, there is no plausible way of distinguishing other kinds of payment by direction. If a direction to pay given by cheque can be a payment why not a direction given by letter, email or telephone call? If a direction given to a bank is a payment, why not a direction given to some other kind of business, such as Fibre or Triton?

[22] In truth, there is no reason to construe ‘pay’ as requiring a direct flow of money from payer to payee. Only in a world in which the concept of money was confined to cash and coin could such a notion even begin to work, for once it be accepted that that concept includes debts and other choses of action, it becomes nonsensical to speak about money literally moving from the payer to the payee. Ms Rozman’s construction of the word ‘pay’ is, therefore, to be rejected. It ignores ordinary usage and it does so for no good reason.

[23] Ms Rozman’s attempt to confine the word ‘pay’ to situations where actual money changes hand is not novel and, when raised, has generally been rejected. Thus, for example, the rule in Spargo’s Case (Re Harmony and Montague Tin and Copper Mining Company (1873) LR 8 Ch App 407 at 412 per Sir James LJ) holds that, for the purposes of company law, when a liability upon shares and a liability on a cross-demand against the company of a sum certain immediately payable are set-off against each other this constitutes payment for the shares in cash: see also Whim Creek Consolidated NL v Federal Commissioner of Taxation (1977) 8 ATR 154 at 156-157; 17 ALR 421 at 425 per Bowen CJ, Franki and Deane JJ; Federal Commissioner of Taxation v P Iori and Sons Pty Ltd (1987) 15 FCR 363 at 368 per Fox J. The rule in Spargo’s Case is ‘not a principle confined merely to the company law context in which it was decided’: East Finchley Pty Ltd v Federal Commissioner of Taxation (1989) 20 ATR 1623 at 1634-1635; 90 ALR 457 at 469 per Hill J. Thus ‘payment of a dividend may occur in a variety of ways not involving payment in cash or by bill of exchange, as, for example, by an agreed set-off, account stated or an agreement which acknowledges that the amount of the dividend is to be lent by the shareholder to the company and is to be repaid to the shareholder in accordance with the terms of that agreement’: Brookton Co-operative Society Ltd v Federal Commissioner of Taxation (1981) 147 CLR 441 at 455 per Mason J (with whom on this point, each of the other Justices agreed). It is difficult to identify how payments by direction might be distinguished from any of those arrangements: cf Fruehauf Finance Corporation Pty Ltd v Zurich Australia Insurance Ltd (1993) 32 NSWLR 735 at 740 per Giles J; Skourdoumbis v Findlay (2002) 114 IR 318; 190 ALR 554 at [83]-[84] per Gray J. The statement of de Jersey CJ in an obiter dictum in Starco Developments Pty Ltd v Ladd [1999] 2 Qd R 542 at [4] that a party directing a debtor to pay another ‘is to be regarded as making the payment’ is, in those circumstances, hardly surprising. There is, therefore, no reason to read ‘the private company pays’ in s 109C(1) as precluding payment by direction.

[24] The Tribunal, it will be recalled, also concluded that there was a transfer of property to Ms Rozman from Tredex. If that were right it would fall within s 109C(3)(c) and be deemed thereby to be a payment. Ms Rozman submitted, and I accept, that no such a transfer took place. The only property involved was the debts owned by Tredex to Fibre and Triton. The payment or discharge of those debts did not operate as a transfer of them, rather, it extinguished them.”

41 The last paragraph of this passage is significant because his Honour drew a distinction between a payment by direction and the transfer (or assignment) of a debt. Similarly here, the payment by direction given by Homes Pictorial (as trustee) to Quality Group (as trustee) to pay the subscription monies of $4,100,000 to the taxpayer did not constitute an assignment or transfer of the debt owed by Quality Group (as trustee) to pay the amount of $4,100,000, but, rather, the discharge of it.

42 The reason why there is a distinction between a payment by direction and an assignment of a debt has to do with the nature of assignments. An assignment is “the immediate transfer of an existing proprietary right, vested or contingent, from the assignor to the assignee”: Norman v Commissioner of Taxation (1963) 109 CLR 9 at 26 per Windeyer J. In an appropriate case, an order to a debtor to pay the debt to a third party can constitute an assignment of the debt to the third party, but whether this is so depends on whether the debtor has been “given to understand that the debt has been made over by the creditor to some third person”: William Brandt’s Sons & Company Limited v Dunlop Rubber Co Ltd [1905] AC 454 at 462 per Lord Macnaghten.

43 In contrast, by way of example, where B is indebted to A and A simply directs B to make payment to C (on A’s behalf), there is no assignment of the debt owing by B to A because the intention of A is not to “make over” the debt to C. There are a number of bankruptcy cases in which it was accepted that B’s payment to C in that situation was a payment by A for the purpose of the bankruptcy preference section: Re Stevens (1929) 1 ABC 90; Re Ruwaldt (1931) 3 ABC 245; Re Smith (1933) 6 ABC 49, 51–52. This was recognised by Dawson, Gaudron and Gummow JJ in Sheahan v Carrier Air Conditioning Pty Limited (1997) 189 CLR 407 at 437:

“No doubt, as the authorities indicate, there may be a payment made by the debtor within the meaning of s122(1) [of the Bankruptcy Act 1966 (Cth)] where the debtor directs a third party who holds funds at the direction of the debtor or is otherwise obliged to the debtor to account to the debtor not by payment to the debtor but to a creditor of the debtor.”

44 One of the bankruptcy cases referred to by their Honours was Re Stevens where a debtor (A) authorised the purchaser of his property (B) to issue a promissory note to a creditor (C) in part payment of the purchase price, the creditor accepting the note in discharge of A’s debt to him. Moule J said (at 93) that A –

“…has parted with his assets, and the payment which he himself should have received he has authorised to be made to the creditor, and it is just the same as if he had received payment himself and had himself handed such payment to [C].”

45 Dawson, Gaudron and Gummow JJ in Sheahan approved this statement and explained (at 437) that the result in Re Stevens was “that the third party was to be treated as having acted on behalf of the debtor”. In other words, where B is acting on behalf of A, B’s payment to C is regarded as the same as if A had received payment from B and himself had paid C, thereby discharging the debtor (A).

46 Similarly here, the third party (Quality Group (as trustee)) is to be treated as having acted on behalf of the debtor (Homes Pictorial (as trustee)) in making payment to the taxpayer at the direction of the debtor (Homes Pictorial (as trustee)). That the third party here was acting on behalf of the debtor is made clear by cl 6.4 of the Asset Sale Agreement, which provides for payment by the third party “direct to the Vendor, on the Purchaser’s behalf, in satisfaction of the Consideration” (emphasis added).

47 On any reading of the Asset Sale Agreement or the Subscription Agreement, there is neither any intention to make over (i.e. assign), nor the effect of making over (i.e. assigning), a debt to the taxpayer. All that happened was the purchaser (Homes Pictorial (as trustee)) gave a third party (Quality Group (as trustee)) a direction to pay the taxpayer. The purchaser had the right to receive $4,100,000 from the third party, and directed it to make the payment to the taxpayer.

48 The third party (Quality Group (as trustee)) did not pay cash to the taxpayer, but rather assumed a liability to pay $4,100,000 to the taxpayer. Nevertheless, this constituted payment to the taxpayer, as illustrated by Re Stevens (where payment was constituted, in part, by the delivery of a promissory note by the third party to the creditor): see also Rozman supra at [23]. As noted in Proctor C (Ed), Goode On Payment Obligations in Commercial and Financial Transactions (2nd ed, Sweet & Maxwell, 2009) at 9:

“Payment in the legal sense means a gift or loan of money or any act offered and accepted in performance of a money obligation. So an act cannot constitute payment unless money is involved, but this requirement may be satisfied not only by the transfer of money but also by the performance of some other act in fulfilment of an obligation to pay money. The most common method of satisfying a money obligation—and that on which the creditor is entitled to insist unless otherwise expressly or impliedly agreed—is, of course, by the transfer of coins and notes by way of legal tender. This, however, is highly inconvenient, not to say risky, where substantial sums are involved, and the court will readily infer an agreement to pay by some other method which is equally acceptable commercially.” (Emphasis added.)

49 Accordingly, the capital proceeds from the disposal of the Assets was the sum of $4,099,970 pursuant to s 116-20(1)(a) of the ITAA 1997. Section 116-20(1)(b) simply does not apply in the present case because the taxpayer was entitled at all times to receive money pursuant to the Asset Sale Agreement and not “other property” in respect of CGT event A1 happening.

50 The taxpayer’s contention that the amount of $4,100,000 was merely a “notional” consideration must be rejected because:

(1) To the extent that there was a debt created between the taxpayer and Quality Group (as trustee of the Denise Canty Family Trust), the quantum of the debt was directly relevant to the relative values of these separate legal entities in the Quality group;

(2) The Consideration of $4,100,000 was the agreed maximum aggregate liability of the taxpayer (as vendor) as a result of Claims for breach of Warranties under the Asset Sale Agreement: (cl 9.7). Provision was also made in the agreement that a payment made for a breach of Warranty was to be treated as a reduction in the purchase price attributed to each relevant Asset: (cl 9.11).

(3) The Consideration of $4,100,000 was relevant for the purposes of payment of GST and stamp duty by the Purchaser (i.e. Homes Pictorial as trustee), as well as the books, records and financial statements of both entities.

(4) The Consideration was also important for the purposes of the cost base of the Assets (for CGT purposes) in the hands of Homes Pictorial as trustee as well as the cost base of the Stapled Securities in the hands of Quality Group as trustee.

(5) The Asset Sale Agreement also contained a specific clause that provided that it constituted the entire agreement between the parties in connection with the subject matter and superseded all prior agreements or understandings between the parties in connection with the subject matter: (cl 15.9).

51 The taxpayer sought in these proceedings to adduce a considerable amount of evidence containing the subjective intent or understanding of various witnesses in relation to the meaning of the Asset Sale Agreement and, in particular, the clause dealing with consideration. This material is not relevant to the proper construction of the agreements entered into. The relevant principles regarding the construction of contracts were summarised by Allsop P in Franklins Pty Ltd v Metcash Trading Ltd (2009) 264 ALR 15 at [4]-[24] (“Franklins”) as follows:

(1) The construction and meaning of the Asset Sale Agreement or indeed any other agreement (to the extent this is required for the purposes of the identification of the relevant capital proceeds) is an objective question for the Court (Pacific Carriers Limited v BNP Paribas (2004) 218 CLR 451 at 462.10 [22] (“Pacific”); Toll (FGCT) Pty Limited v Alphapharm Pty Ltd (2004) 219 CLR 165 at 179 [40]–[46] (“Toll”).

(2) Evidence, whether of negotiations, drafts or otherwise, which is probative of, or led so as to understand the actual intentions of the parties is impermissible (Pacific (supra), Toll (supra), Franklins at [24]).

(3) Evidence as to surrounding circumstances, to be admissible, must be relevant to a fact in issue, probative of the surrounding circumstances known to the parties or of the purpose or object of the transaction, including its genesis, background, context and market in which the parties are operating (Pacific (supra), Toll (supra), Franklins at [24])).

ANTERIOR ISSUE (3): Alternatively, whether the capital proceeds in respect of the disposal of the assets was some other amount by virtue of s 116-20(1)(b) of the ITAA 1997?

52 On the view I take of anterior issue (2) (see [49] above), anterior issue (3) does not arise; the taxpayer did not receive, nor was it entitled to receive, property other than money from the disposal of the Assets, such that the market value of that other property was the capital proceeds from such disposal.

53 However, in deference to the submissions that were made on behalf of the taxpayer, and in the event that these proceedings go further, it is appropriate that I should set out my views.

54 According to the taxpayer, what it received for the disposal of the Assets was the receivable due by Quality Group as trustee of the Denise Canty Family Trust. According to the taxpayer, that receivable is property other than money and therefore “other property” within s 116-20(1)(b) and it is the market value of that receivable that constitutes the capital proceeds in respect of the disposal of the Assets.

55 The taxpayer contended that it is permissible for the Court to go behind the obligor of the receivable, namely, Quality Group as trustee of the Denise Canty Family Trust and, in determining the market value of the receivable, make an assessment of the obligor’s capacity to pay. According to the taxpayer, as the only asset of the Denise Canty Family Trust were the Stapled Securities in Homes Pictorial and the Homes Pictorial Unit Trust, the market value of the receivables could not be greater than the market value of the Stapled Securities.

56 There are, at least, two problems with this contention. First, there was no evidence as to what were the assets and liabilities of the Denise Canty Family Trust at the relevant time; there was certainly no evidence to support the contention that the only assets of the Denise Canty Family Trust at the relevant time were the Stapled Securities in Homes Pictorial and the Homes Pictorial Unit Trust.

57 Second, the clear weight of authority is that in valuing a promise to pay or repay, it is not right to consider the financial capacity of the obligor. In Fadden v Commissioner of Taxation (1945) 70 CLR 555, it was unsuccessfully argued that a transfer of shares in consideration of an immediately enforceable promise to pay for them was a gift. At 559 Latham CJ said:

“In my opinion, it is impossible to say that such a promise is an inadequate consideration and it has not hitherto been suggested that a distinction should be drawn between such promises as consideration by reference to the financial capacity of the promisor to pay. Entry into such matters to determine the ‘real consideration’ or the ‘adequacy’ of the consideration under such provisions as those now under consideration would open up an entirely new field of inquiry, an inquiry which there appears to be no authority for making.”

58 In Pro-Image Studios Ltd v Commonwealth Bank of Australia (1991) 4 ASCR 586, Fullagar J of the Victoria Supreme Court said (at 590):

“In my opinion, the same applies to the present case. The value of a debt for all purposes of the present case is the face value of the legally and immediately enforceable obligation constituted by the debt itself.”

59 In Bray v Commissioner of Taxation (No 2) (1971) 123 CLR 348, Gibbs J, as his Honour then was, said (at 357):

“[Fadden] establishes not only that a promise to pay may be good consideration for gift duty purposes but also that it is immaterial that the promise has not been enforced, and that there might be difficulty in fact in enforcing it, provided of course that the transaction was bona fide. It follows that what has to be valued is the promise itself, and, once it is decided that the promise is not merely colourable, questions whether the promisor will be required, or able, to fulfil it are not to the point.”

And relevantly, at 360 his Honour said:

“The passage which I have already quoted from Fadden [at 559 per Latham CJ] shows that in valuing a promise to repay, it is not right to consider the financial capacity of the promisor to repay, but it does not follow that the value of the security is irrelevant in fixing an appropriate interest rate.”

60 It follows that if, contrary to my view, the taxpayer received, or was entitled to receive, property other than money on the disposal of the Assets, namely, the receivable from Quality Group as trustee of the Denise Canty Family Trust, so as to trigger s 116-20(1)(b) of the ITAA 1997, the market value of the receivable was, on the evidence in this case, equal to the face amount of the receivable, viz., $4,100,000.

ANTERIOR ISSUE (4): Alternatively, whether the capital proceeds in respect of the disposal of the assets was some other amount by virtue of the operation of s 116-30(2)(b)(i) of the ITAA 1997?

Statutory Context

61 In the 2003 income year, s 116-30(2)(b)(i) was relevantly in the following terms:

“116-30 Market value substitution rule: modification 1

No capital proceeds

(1) …

There are capital proceeds

(2) The *capital proceeds from a *CGT event are replaced with the *market value of the *CGT asset that is the subject of the event if:

(a) some or all of those proceeds cannot be valued; or

(b) those capital proceeds are more or less than the market value of the asset and:

(i) you and the entity that *acquired the asset from you did not deal with each other at arm’s length in connection with the event; or

(ii) the CGT event is CGT event C2 (about cancellation, surrender and similar endings).

(The market value is worked out as at the time of the event.)”

62 Section 116-20(1) sets out the prima facie rule for determining the capital proceeds from a CGT event happening to an asset where, as in the present case, the taxpayer receives (or is entitled to receive) an amount of money in respect of the relevant CGT event. That is, the capital proceeds will be the amount of money received or entitled to be received. However, s 116-30(2) modifies this general rule to substitute the market value of the CGT asset disposed of where the parties are not dealing with each other at arm’s length in relation to the disposal.

Analysis

63 The expression “did not deal with each other at arm’s length” in the context of s 124-780(4) of the ITAA 1997 (i.e. “scrip for scrip roll-over”) was considered at length by a Full Court of this Court in Commissioner of Taxation v AXA Asia Pacific Holdings Ltd (2010) 189 FCR 204. The majority (Edmonds and Gordon JJ) summarised the relevant legal principles as follows at [105] ff:

“[105] Any assessment of whether parties were dealing at arm’s length involves ‘an assessment [of] whether in respect of that dealing they dealt with each other as arm’s length parties would normally do, so that the outcome of their dealing is a matter of real bargaining’: Trustee for the Estate of AW Furse No 5 Will Trust v Federal Commissioner of Taxation (1990) 21 ATR 1123 at 1132 per Hill J. The reference in Furse 21 ATR 1123 to ‘real bargaining’ is significant. It focuses on actual dealing between the parties: see also Re Hains (deceased); Barnsdall v Federal Commissioner of Taxation (1988) 81 ATR 1352. That is not surprising. It is the same mental process as that described by Griffith CJ in Spencer v Commonwealth (1907) 5 CLR 418 at 432.

[106] The question of whether parties dealt with each other at arm’s length in respect of a particular dealing is one of fact in each case: Granby Pty Ltd v Federal Commissioner of Taxation (1995) 30 ATR 400 at 403. What is required is that ‘parties to a transaction have acted severally and independently in forming their bargain’: Granby at 403. Put another way, it requires consideration of how ‘unrelated parties, each acting in his or her own best interest, would carry out a particular transaction’: Australian Trade Commission v WA Meat Exports Pty Ltd (1987) 7 AAR 248 at 252; 75 ALR 287 at 291.

[107] Consistent with those principles, there is no presumption that parties at arm’s length dealt with each other at arm’s length: Hains and Furse at 1132. Parties may be at arm’s length generally yet not deal with each other at arm’s length in respect of a particular matter: Re RAL and Federal Commissioner of Taxation (2002) 50 ATR 1076 at [45]-[51]. So, for example, even where parties to a transaction are at arm’s length, they will not ‘be dealing with each other at arm’s length in a transaction in which they collude to achieve a particular result, or in which one of the parties submits the exercise of its will to the discretion of the other, perhaps, to promote the interests of the other’: Granby at 404.

[108] Similarly, where one party to a transaction seeks only an overall result and is indifferent to the outcome of a particular aspect on which the statute focuses, the parties will be found not to have dealt with each other at arm’s length on that particular aspect: Collis v Federal Commissioner of Taxation (1996) 33 ATR 438 at 443. In Collis, there was a question as to whether a vendor (the taxpayer) and purchaser of land had dealt at arm’s length in connection with the signing of two contracts of sale in relation to four parcels of land which had been sold at auction in a single bid. The purchaser who made the single bid for all blocks did not enquire as to why the contracts were apportioned between the blocks in the manner proposed by the taxpayer. Jenkinson J considered that this failure to enquire suggested ‘indifference’ on the part of the purchaser such as to indicate that the dealing was not at arm’s length. The taxpayer in Collis argued that not all arm’s length dealings involve a discussion or enquiry as to price (using an analogy of purchasing items of stock in a food store) and that the absence of such discussions or enquiries did not suggest indifference by the taxpayer. His Honour rejected that submission, noting that (at 443):

A parcel of land is not ordinarily dealt with in commerce as is a can of beans in a food store.

In Baxter v Commissioner of Taxation (2002) 51 ATR 209, a sales tax case, Gyles J held that a lease devised in order to obtain a revenue advantage did not make it a non-arm’s length transaction, ‘no matter how widely that concept is construed’: at [38]. (Baxter was considered the ‘most obviously helpful’ by the trial judge when determining whether the transaction was an arm’s length one: see [105] of the trial judge’s reasons for decision).”

64 To this summary of the relevant principles it may be added that the mere fact that there is a commercial relationship between the buyer and seller that influences the price does not necessarily mean that the parties are not dealing at arm’s length in the purchase or sale transaction: Commissioner of Taxation v BHP Billiton Limited (2011) 277 ALR 224 at [95] per Gummow J.

65 It is common ground that the taxpayer and Homes Pictorial (as trustee) were themselves at arm’s length up to the date of entering into the Asset Sale Agreement and other agreements. Up until that date, the shares in Homes Pictorial (as trustee) and units in the Homes Pictorial Unit Trust were wholly owned by the Fairfax Group and shares in the taxpayer were wholly owned by Denise Canty.

66 In respect of the crucial question under s 116-30(2)(b)(i) ITAA of the 1997 as to whether the taxpayer and Homes Pictorial (as trustee) dealt with each other at arm’s length in connection with CGT Event A1 (the disposal of the Assets), the evidence indicated that the parties acted in their own interests and severally and independently in forming their bargain:

(1) The transaction took the best part of one year from the initial meeting between Paul Canty and representatives of Fairfax (in April/May 2002) and the entry into the Asset Sale Agreement and other agreements on 21 March 2003. The minutes of the meetings and correspondence between the parties indicate hard-headed bargaining over the course of that period between the parties on a wide range of commercial, legal and valuation issues. Both parties were represented and assisted throughout the course of the negotiations by accounting and legal advisors.

(2) The correspondence clearly indicates that there was conscious consideration by the legal advisers (acting on the instructions of the parties) in respect of the figure to be inserted in the Asset Sale Agreement for Consideration. The evidence also reveals the relevant (and possibly) competing interests of the parties in this regard (i.e. capital gains issues for the taxpayer and accounting, corporate governance and taxation issues for the Fairfax Group).

(3) The Consideration of $4,100,000 was the basis for both GST and ad valorem stamp duty paid by Homes Pictorial. It therefore had no interest in over-stating the Consideration.

(4) The Consideration was also the maximum aggregate liability of the taxpayer (as Vendor) in respect of any Claims for breach of Warranties. It was clearly an amount of money that the parties had, in the ordinary commercial manner, agreed as between themselves.

(5) The Consideration was adopted as the value of the “Property Showcase” masthead in the accounting records of the Homes Pictorial Unit Trust following the transaction.

(6) The Asset Sale Agreement was part of a wider transaction that conferred benefits and burdens on the respective parties of an entirely commercial nature.

67 In the circumstances, s 116-30(2)(b)(i) does not apply because the taxpayer has failed to discharge its onus that it and Homes Pictorial (as trustee) did not deal with each other at arm’s length in connection with CGT Event A1.

CONCLUSION ON ULTIMATE ISSUE

68 For the foregoing reasons, I have come to the conclusion that the net capital gain to be included in the taxpayer’s assessable income pursuant to s 102-5 of the ITAA 1997 for the income year ended 30 June 2003 in respect of the disposal of the assets was the amount of $3,100,000 and that the taxpayer has not shown the amended assessment of income tax to be excessive.

ADMINISTRATIVE PENALTY

69 On the assumption that the Court found that the taxpayer failed to properly calculate the net capital gain it realised in the 2003 income year and include the net capital gain in its assessable income, the Commissioner submitted that this is a clear case within item 2 of the table in s 284-90(1) of Sch 1 to the TAA, item 2 being applicable where the shortfall resulted from “recklessness” by the taxpayer or its tax agent as to the operation of the ITAA 1997. I agree.

70 In Commissioner of Taxation v R&D Holdings Pty Ltd (2007) 160 FCR 248, the joint judgment of Heerey and Edmonds JJ (with whom Stone J agreed at [108]) stated at [70]:

“In Hart…at [44] Hill and Hely JJ said that recklessness in the context of s 226H means something more than failure to exercise reasonable care, but less than an intentional disregard of the Act. Their Honours cited with approval what was said by Cooper J in BRK (Brisbane) Pty Ltd v Federal Commissioner of Taxation 46 ATR 347 at 364:

Recklessness in this context means to include in a tax statement material upon which the Act or regulations are to operate, knowing that there is a real, as opposed to a fanciful, risk that the material may be incorrect, or be grossly indifferent as to whether or not the material is true and correct, and that a reasonable person in the position of the statement-maker would see that there was a real risk that the Act and regulations may not operate correctly to lead to the assessment of the proper tax payable because of the content of the tax statement. So understood, the proscribed conduct is more than mere negligence and must amount to gross carelessness.”

71 The evidence in the present case indicates that the shortfall amount did result from the recklessness of the taxpayer and/or its tax agent within the meaning in s 284-90(1)(item 2) of Sch 1 to the TAA:

(1) The taxpayer disposed of its entire business in the 2003 income year – a major event for the company that would have prompted a reasonable person in the position of the taxpayer and/or its tax agent to examine the transaction documents and consider the relevant capital gains implications.

(2) The Asset Sale Agreement explicitly stated that the consideration for the sale was an amount of $4,100,000.

(3) The taxpayer collected an amount of $410,000 in GST paid by the Purchaser, Homes Pictorial as trustee, that was clearly based on a consideration for the supply of the Assets of $4,100,000.

(4) The evidence indicates that capital gains considerations were specifically brought to the attention of the taxpayer (through its director, Paul Canty) by his accounting adviser, Scott Nicholls, during the course of the negotiations and prior to execution of the Asset Sale Agreement on 21 March 2003 and therefore lodgement of the 2003 income tax return on 18 February 2004.

(5) Despite the above, the taxpayer and/or its tax agent did not include any net capital gain in respect of the disposal of the Assets in its income tax return for the 2003 income year. Further, there was no disclosure by the taxpayer in the income tax return that a CGT event had even taken place during the year of income. In fact a representation was made to the contrary that no CGT event had occurred during the year of income.

72 In the present case the penalty was reduced (pursuant to s 284-225(3) and/or s 298- 20 of Sch 1 TAA) by 80% in light of a voluntary disclosure made to the Commissioner on 6 October 2007.

73 The taxpayer has not suggested any error on the part of the Commissioner in relation to the penalty remission decision and has not discharged its onus as to why the penalty remission decision ought to have been made differently.

PROPOSED ORDERS

74 The appeal must be dismissed. The taxpayer must pay the Commissioner’s costs as agreed or taxed.

|

I certify that the preceding seventy-four (74) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Edmonds. |

A/g Associate: