HNA Irish Nominee Ltd v Kinghorn (No 2) [2012] FCA 228

| IN THE FEDERAL COURT OF AUSTRALIA | |

| First Plaintiff HNA GROUP (HONG KONG) CO LIMITED Second Plaintiff | |

| AND: | First Defendant DAVID LLOYD VEAL Second Defendant KV AVIATION HOLDINGS PTY LIMITED (ACN 054 680 376) (FORMERLY CALLED AAHL PTY LIMITED) Third Defendant RIL AVIATION VQZ PTY LIMITED (ACN 110 563 007) AND OTHERS Fourth to Forty-First Defendants (as set out in the attached schedule) |

| DATE OF ORDER: | 15 March 2012 |

| WHERE MADE: |

1. Within 14 days, the plaintiffs file and serve proposed short minutes of orders reflecting these reasons.

2. Within 28 days, the defendants notify the plaintiffs and the Court whether they accept that the plaintiffs’ proposed short minutes reflect these reasons, and, if they do not, what amendments they propose to the plaintiffs’ proposed short minutes.

3. The proceeding be listed for further directions at 9.30am on Friday, 20 April 2012.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011. The text of entered orders can be located using Federal Law Search on the Court’s website.

| NEW SOUTH WALES DISTRICT REGISTRY | |

| GENERAL DIVISION | NSD 94 of 2010 |

| BETWEEN: | HNA IRISH NOMINEE LIMITED First Plaintiff HNA GROUP (HONG KONG) CO LIMITED Second Plaintiff |

| AND: | GEOFFREY ANDREW KINGHORN First Defendant DAVID LLOYD VEAL Second Defendant KV AVIATION HOLDINGS PTY LIMITED (ACN 054 680 376) (FORMERLY CALLED AAHL PTY LIMITED) Third Defendant RIL AVIATION VQZ PTY LIMITED (ACN 110 563 007) AND OTHERS Fourth to Forty-First Defendants (as set out in the attached schedule) |

| JUDGE: | EMMETT J |

| DATE: | 15 March 2012 |

| PLACE: | SYDNEY |

REASONS FOR JUDGMENT

1 This proceeding is concerned with the internal management of some 38 companies (the defendant RILAs), each of which is the owner of an aircraft. Each of the defendant RILAs is part of a somewhat complex aircraft financing arrangement (together the Aviation Transactions). Each Aviation Transaction involves, amongst other things, the defendant RILA leasing to an airline the aircraft owned by that defendant RILA. At the end of the lease, the aircraft might be sold, or, following a refinancing, it might be re-leased. Each Aviation Transaction also involves the allotment of preference shares in the relevant defendant RILA to investors who lend money as part of the overall arrangements.

2 As I shall explain further below, each Aviation Transaction involves two companies especially formed for that specific Aviation Transaction. One (the RILA) is the owner of the relevant aircraft. The other (the Financing SPC) is a financing vehicle. The full name of each RILA is RIL Aviation [XXX] Pty Limited. RIL is an acronym, and stands for Record Investments Limited. I shall refer to the company Record Investments Limited (Record) below. The full name of each Financing SPC is Allco [XXX] Financing Pty Limited. For both the RILAs and the Financing SPCs, the registration details of the relevant aircraft appear in place of [XXX]. For example, RIL Aviation VQZ Pty Limited (RILA VQZ), one of the defendant RILAs, is the owner of aircraft VH-VQZ, and the Financing SPC associated with RIL Aviation VQZ Pty Limited is Allco VQZ Financing Pty Limited (VQZ Financing SPC).

3 The defendant RILAs are the fourth to forty-first defendants in the proceeding. The first plaintiff, HNA Irish Nominee Limited (HNA Irish), is the holder of preference shares in each of the defendant RILAs. HNA Irish is a wholly owned subsidiary of the second plaintiff, HNA Group (Hong Kong) Co Limited (HNA Group).

4 The first and second defendants, Messrs Geoffrey Kinghorn and David Veal, are the only directors of each of the defendant RILAs. They are also the only directors of the third defendant, KV Aviation Holdings Pty Limited (KV Aviation). KV Aviation holds all of the ordinary shares in the capital of each of the defendant RILAs. The present shareholders of KV Aviation are Mr Veal, Mr Kinghorn and Niab Capital Markets Pty Limited (Niab). Messrs Veal and Kinghorn together hold the majority of the shares in KV Aviation.

5 In these reasons, references to submissions or contentions advanced on behalf of HNA Irish may be taken to be references to submissions or contentions advanced on behalf of both plaintiffs. Similarly, references to submissions or contentions advanced on behalf of KV Aviation may generally be taken to be references to submissions or contentions advanced on behalf of KV Aviation, Messrs Veal and Kinghorn, and the defendant RILAs. Occasionally, however, it will be appropriate to associate particular defendants more specifically with particular submissions or contentions.

6 The first broad issue raised in the proceeding (the Redemption Issue) is whether the preference shares held by HNA Irish in the defendant RILAs are redeemable, and, if so, in what circumstances they are redeemable and upon what terms they may be redeemed. The constitutions of the defendant RILAs are generally in similar terms, but are not identical. The constitutions of the RILAs generally provide that the preference shares may ony be redeemed out of Aircraft Profits, as that term is defined in the constitutions (see paragraph [56] below), and that the preference shares are entitled to a preferred dividend payable in cash out of Aircraft Profits. KV Aviation contends that the preferred dividend may be paid, and the preference shares redeemed, at any time, upon the amount of the preferred dividend being determined by the defendant RILA, by the assessment of Aircraft Profits according to proper accounting principles based on a revaluation of the aircraft at that time. HNA Irish, on the other hand, says that Aircraft Profits cannot be determined until the aircraft is sold or otherwise realised by the defendant RILA, and, accordingly, that the preference shares, if they can be redeemed at all, cannot be redeemed without the consent of the holder, until the aircraft is sold or realised.

7 If the questions as to redemption are decided unfavourably to HNA Irish and HNA Group, further questions arise (the Misrepresentation Issues) as to the availability of estoppels against asserting any rights of redemption and as to the availability of relief, under the Corporations Act 2001 (Cth) (the Corporations Act) and the Australian Securities and Investments Commission Act 2001 (Cth) (the ASIC Act), in respect of alleged misleading and deceptive conduct concerning the rights attached to preference shares. HNA Irish asserts that representations were made that are inconsistent with the construction of the constitutions of the defendant RILAs now contended for by KV Aviation.

8 The third broad issue raised in the proceeding (the Oppression Issue) is whether the affairs of the defendant RILAs have been conducted, and are likely to be conducted, contrary to the interests of the members of the defendant RILAs as a whole, and in a manner that is oppressive to, unfairly prejudicial to, or unfairly discriminatory against HNA Irish, as the holder of preference shares, within the meaning of s 232 of the Corporations Act, so as to justify the making of orders under s 233 of the Corporations Act. HNA Irish and HNA Group seek orders under s 233 divesting KV Aviation of its ordinary shares in the defendant RILAs, and orders for the appointment of persons nominated by HNA Irish to the board of directors of each defendant RILA. Such orders would effectively deprive Messrs Veal and Kinghorn of any say in the affairs of the defendant RILAs.

9 Before dealing with the issues I have just described, it is necessary to say something about the background and formation of the defendant RILAs. That will require an examination of the history of the business known as Allco Finance Group, whose Aviation Division Mr Veal headed from late 2002 onwards, as well as the history of KV Aviation and its connection with Allco Finance Group. It will also require an examination of the workings of the Aviation Transactions, which were effected by a series of complex instruments collectively referred to as Transaction Documents.

10 After saying something about those matters, I shall deal with the Redemption Issue, which will involve a detailed examination of the constitution of one of the defendant RILAs, in the light of the part that the RILA plays in the relevant Aviation Transaction. After that, I shall deal with the Misrepresentation Issues, which will require an examination of the circumstances in which preference shares were issued by the defendant RILAs to various investors, and the circumstances that led to the acquisition of preference shares by HNA Irish. Finally, I shall deal with the Oppression Issue, which will require an examination of events that followed the appointment of receivers to certain companies in Allco Finance Group.

11 The business known as Allco Finance Group was founded in 1979. Allco is an acronym, and stands for Australian Leveraged Leasing Company. Allco Finance Group specialised in large equity and leveraged leasing of plant and equipment, principally in the government sector. Subsequently, Allco Finance Group diversified its activities and expanded into structured property finance, cross-border finance and specialised vendor finance facilities, including financing within the aviation industry.

12 The Allco Finance Group business was initially conducted through a series of joint ventures. However, in June 1987, Allco Finance Group Limited (Old AFGL) was incorporated. The relationship between the joint ventures of Allco Finance Group and the members of Old AFGL is not entirely clear. However, I do not understand anything to turn on that. References are frequently made to Allco Finance Group as describing the overall group of entities, without identifying a specific entity such as Old AFGL. References in these reasons to Allco Finance Group are intended to refer to the overall business structure rather than to a specific entity.

13 Mr Veal joined Allco Finance Group in 1987 and became a senior partner in 1998. The other senior partners at that time included Mr John Kinghorn (Mr Geoffrey Kinghorn’s father), as well as Messrs John Bennett, David Coe and Brian Holmes. Prior to his appointment as a senior partner, Mr Veal reported to Mr John Kinghorn.

14 In 2001, Record was established to provide a source of equity funding for transactions undertaken by Old AFGL. Record was listed on the Australian Securities Exchange (ASX) and Old AFGL was a major shareholder of Record. In 2006, there was a merger of Old AFGL and Record (the Record Merger), under which Record acquired all the issued shares in Old AFGL. Record then changed its name to Allco Finance Group Limited (Public AFGL), and Old AFGL changed its name to Allco Finance (Australia) Limited. Public AFGL continued to be listed on the ASX. The partners of Allco Finance Group were not directors of Public AFGL.

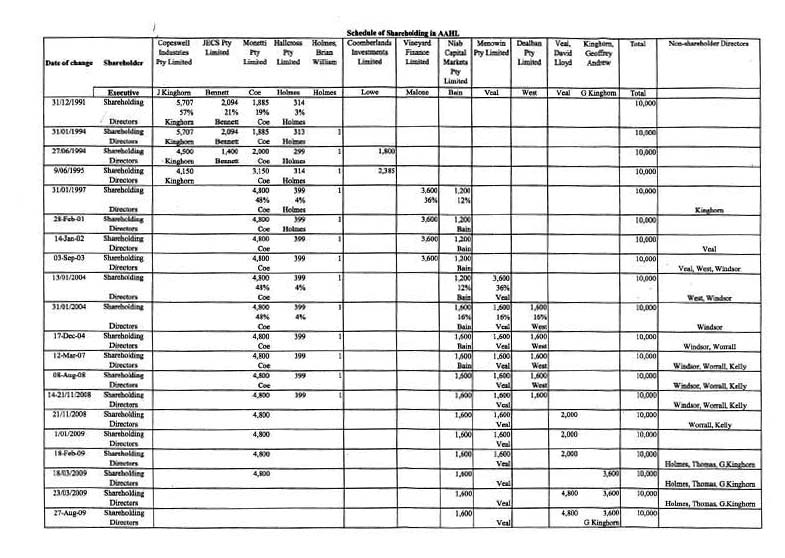

15 KV Aviation was incorporated in 1991. It was originally called Allco Australian Holdings Limited, and, subsequently, its name was changed to AAHL Limited. Its present name was adopted in January 2010. A document that purports to tabulate the historical directorship of and shareholding in KV Aviation appears as Appendix 1 to these reasons.

16 Historically, the respective directorships of KV Aviation and Old AFGL have been closely aligned. When KV Aviation was incorporated in 1991, its directors were Messrs John Kinghorn, Coe, Bennett and Holmes. The directors of Old AFGL at that time were also Messrs John Kinghorn, Coe, Bennett and Holmes. The shareholders of KV Aviation and Old AFGL were at that time the same, being Mr John Kinghorn (as to 57.07 per cent), Mr Coe (as to 18.85 per cent), Mr Bennett (as to 20.94 per cent) and Mr Holmes (as to 3.14 per cent).

17 That shareholding, as at 1991, reflected the shareholders’ respective interests in the senior joint venture partner in the operating joint ventures of Allco Finance Group. Messrs John Kinghorn, Coe, Bennett and Holmes were the senior partners of Allco Finance Group at that time. Thus, the initial directors and shareholders of KV Aviation and the directors of and shareholders in Old AFGL matched the participation, through joint ventures, of the senior partners of Allco Finance Group.

18 In 1998, new joint venture arrangements were entered into, as a consequence of which the senior partners of Allco Finance Group were Messrs Coe, Veal and Holmes, along with Messrs Nicholas Bain and Gary Cohen. The position within KV Aviation continued to reflect the position that had existed within Old AFGL prior to the new arrangements. That is to say, the shareholders of KV Aviation consisted of interests associated with Messrs Coe (as to 48 per cent), Bain (as to 12 per cent), Tom Malone (as to 36 per cent) and Holmes (as to 4 per cent).

19 On 14 January 2002, Mr Veal was appointed as a director of KV Aviation. The directors of KV Aviation were then Messrs Coe, Bain and Veal, the same as Old AFGL. As at 31 January 2004, the shareholders of KV Aviation were companies associated with Messrs Coe (as to 48 per cent), Bain (as to 16 per cent), Veal (as to 16 per cent), Christopher West (as to 16 per cent) and Holmes (4 per cent). At that time, the shareholding in KV Aviation reflected the shareholding in Old AFGL, involving Messrs Coe, Bain, Veal and West, with Mr Holmes also holding 4 per cent of the shares in KV Aviation. The shareholding in KV Aviation then remained unchanged until November 2008.

20 Following the Record Merger in 2006, 47.8 per cent of the shareholding in Public AFGL was controlled by ten senior executives of Old AFGL, including Messrs Coe, Bain, Veal and West. Mr Veal received 9,602,907 shares, representing approximately 3.3 per cent of Public AFGL.

21 On 4 November 2008, voluntary administrators were appointed to Public AFGL and certain of its subsidiaries. Later on the same day, Messrs Peter Gothard and Steven Sherman (the Receivers) were appointed as receivers and managers of Public AFGL and certain of its subsidiaries, including Allco Management Limited (Allco Management) and Allco Asset Finance Limited (Allco Asset Finance), which had been appointed as managers of the RILAs under the Transaction Documents (together the Managers). The Receivers were also appointed to Allco Managed Investments Limited (Allco Managed Investments), the trustee of unit trusts established by Allco Finance Group known as the Aircraft Holdings Trust and the Allco Aviation Fund. The investments made by those unit trusts include investments in preference shares in defendant RILAs. More will be said about those entities below. No administrators, and no receivers or managers, were appointed to KV Aviation or to any of the RILAs or the Financing SPCs.

22 Shortly after the appointment of the Receivers, Mr Veal decided to attempt to acquire the ordinary shares in KV Aviation that he, or a company controlled by him, did not already own. Mr Veal approached Messrs West, Holmes and Coe with a view to acquiring from them, or from companies associated with them, the shares in KV Aviation that they held. By the last week of November 2008, he had obtained executed share transfers from Mr West and Mr Holmes and had made an oral arrangement with Mr Coe for the transfer of the shares controlled by him. Mr Veal and Mr Geoffrey Kinghorn then entered into a series of transactions in relation to KV Aviation shares. Their acquisition of shares in KV Aviation for a price of $1 per share, or very close to $1 per share, took place as follows:

21 November 2008: Mr Veal acquired one share from Mr Holmes;

21 November 2008: Mr Veal acquired 399 shares from Mr Holmes’ company;

21 November 2008: Mr Veal acquired 1,600 shares from Mr West’s company;

18 March 2009: Mr Kinghorn acquired 1,600 shares from Mr Veal’s company;

18 March 2009: Mr Kinghorn acquired 2,000 shares from Mr Veal;

23 March 2009: Mr Veal acquired 4,800 shares from Mr Coe’s company.

23 Those transfers were approved at meetings of KV Aviation held on 20 March 2009 and 23 March 2009. The total issued share capital at all times was 10,000 shares. After 23 March 2009 the shareholding in KV Aviation was as follows:

4,800 shares controlled by Mr Veal;

3,600 shares controlled by Mr Geoffrey Kinghorn;

1,600 shares controlled by Mr Bain’s company, Niab (see paragraph [4] above).

SALE OF ASSETS OF THE AVIATION DIVISION

24 During November 2008, the Receivers commenced a sale process in respect of assets of the Aviation Division. Information was provided to prospective buyers in the form of various documents (the Sale Information Documents), which consisted of:

a document entitled “Allco Aviation Overview” (the Aviation Overview);

a document dated 19 December 2008 and entitled “Allco Aviation Information Memorandum” (the Sale Information Memorandum);

a written list of questions from bidders for the Aviation Division (the Q&A Document); and

a management presentation to shortlisted bidders dated January 2009 (the Management Presentation).

25 Bravia Capital Partners Inc (Bravia) is an adviser to, and co-investor with, HNA Group. Bravia received a copy of the Sale Information Memorandum and a copy of the Aviation Overview. On 23 January 2009, HNA Group submitted its first bid, and was included on the short list of bidders. It submitted two revised bids on 23 February 2009. One of the revised bids was subject to further due diligence and the other revised bid, a much lower one, was without due diligence. HNA Group submitted its final bid on 26 March 2009, in the sum of US $120 million.

26 Mr Veal resigned from the Aviation Division on 29 January 2009, with effect on the following day. He immediately held discussions with Mr John Kinghorn and Mr Geoffrey Kinghorn about a joint venture with them. Mr Veal said that discussions about participation in a joint venture with the Kinghorns first occurred in November 2008. The outline of a joint venture was substantially agreed between Mr Veal and the Kinghorns on or around 1 February 2009. As part of the arrangement, KV Aviation granted to Mr John Kinghorn a call option (the Call Option), executed on 23 February 2009, in respect of its ordinary shares in the RILAs. Also on 23 February 2009, the Kinghorns made an offer to the Receivers for assets of the Aviation Division. Although their offer was subsequently increased, the Kinghorns were notified that the Receivers did not wish to proceed with their bid.

27 During March 2009, Mr Veal and the Kinghorns gave their proposed new aircraft leasing joint venture the working name “KV Aviation”. On 27 May 2009, they arranged for KV Management Pty Limited (KV Management) to be incorporated as an aircraft lease management company.

28 On 5 May 2009, HNA Group entered into an agreement to acquire certain assets of the Aviation Division for a purchase price of approximately US $116.3 million (the May Sale Agreement). HNA Group had proposed that a component of the purchase price be structured as a control payment, payable in the event that the Receivers could deliver full control over the assets being sold. HNA Group regarded the control payment as an incentive for the Receivers to deal with any potential controversy as to the rights attached to the ordinary shares in the RILAs and the Financing SPCs. That controversy was generally referred to as the David Veal issue. Accordingly, in conjunction with the May Sale Agreement, a further instrument (the Control Payment Deed) was executed, which provided for a control payment of approximately US $24.3 million.

29 Because of changes in the structure of the proposed transaction and the expiration of the May Sale Agreement, HNA Group renegotiated the purchase with the Receivers in October and November 2009. The negotiations began with a purchase price of US $116.3 million, and involved bargaining over discounts from that figure to take account of a reduction in management fees by reason of the passing of time, an allowance for the costs and risks involved in the new structure, the fact that some assets were not going to be acquired, and an allowance to deal with the David Veal issue. The control payment was dropped in the course of those negotiations, such that HNA Group was to take responsibility for solving and funding the David Veal issue. The purchase price finally agreed was US $85.8 million, subject to adjustment. A final sale and purchase agreement (the Final Sale Agreement) was executed and completed on 6 January 2010.

30 The Control Payment Deed was terminated as part of the Final Sale Agreement. Instead, HNA Group received an assurance from 24 of the 28 investors involved in Aviation Transactions that they would not take any action to remove or replace the Managers if the relevant RILA sought to exercise a right of removal. On the basis of that assurance, HNA Group and HNA Irish completed the Final Sale Agreement in relation to 64 of the 68 Aviation Transactions that were in the portfolio of the Aviation Division. HNA Group and the investors also agreed to work together to effect a transfer of the ultimate ownership of the RILAs and the Financing SPCs “to independent trustees on behalf of an orphan trust”.

31 On 6 January 2010, upon completion of the Final Sale Agreement, HNA Irish became the owner of preference shares in the defendant RILAs, and HNA Group became the parent company of the Managers, Allco Management and Allco Asset Finance. The holder of the preference shares immediately prior to the acquisition by HNA Irish was, in most cases, either Allco Managed Investments or Allco Asset Finance. Allco Asset Finance also held units in the Allco Aviation Fund. Those units were transferred to HNA Irish under the Final Sale Agreement.

32 In 2002, following the events of 11 September 2001 in the United States, the aviation market and aircraft values were depressed. At the same time, financing markets were available for strong airline credit transactions. Mr Veal considered, at that time, that both debt finance and equity finance were available on terms that would allow the generation of significant income by structuring new financing transactions for aircraft. He concluded that it was an ideal time to engage in aircraft leasing transactions, so as to take advantage of the business opportunities that he considered were available.

33 Mr Veal therefore instigated a transaction analysis process, which included the commissioning of industry experts to assist in his evaluation of the current and future market value of aircraft, the opportunities available for an aircraft at the end of the term of a proposed lease, and the acceptable terms required to govern the ongoing maintenance and return conditions of the aircraft. He worked with solicitors and tax advisors in developing a financial structure for such transactions. That included the creation and development of appropriate tax and accounting structures, obtaining necessary tax and legal advice in relation to the relevant structures, and achieving bankruptcy remoteness for individual transactions.

34 The first Aviation Transaction was completed in December 2002, and involved Qantas Airways Limited (Qantas). Another Aviation Transaction involving Qantas was completed in February 2003. Mr Veal concluded that, having regard to the state of the market, the availability of similar aircraft on leases that were about to terminate, and the availability of debt and equity finance on acceptable terms, such transactions could be replicated. As a consequence, at about the end of 2002, the Aviation Division of Allco Finance Group was established, with Mr Veal at its head. The Aviation Transactions subsequently effected by the Aviation Division followed similar patterns to the two involving Qantas that I have just mentioned. Mr Veal remained as head of the Aviation Division until he resigned on 29 January 2009.

35 Allco Management and Allco Asset Finance, two companies to which I have referred above, were generally appointed under the Transaction Documents as Managers of Aviation Transactions. Mr Veal intended that the structures used in the Aviation Transactions would result in bankruptcy remoteness from the Managers, thus ensuring that failure of the Managers would not result in a failure of the security of an investor or financier involved in an Aviation Transaction, and thus of the ability of that investor or financier to continue to receive rental proceeds and full repayment of debt at the conclusion of the relevant aircraft lease. He intended that the separation of each Aviation Transaction from every other Aviation Transaction would ensure that the failure of one would not impact on any other, since there were invariably different investors and financiers involved. Mr Veal also intended, through the Aviation Transaction structures, to achieve a known tax treatment that would deal with payments of rental, principal and interest across the multiple tax jurisdictions of the airlines and other entities involved.

Structure of Aviation Transactions

36 An important characteristic of the Aviation Transactions is that they involved several layers of financing, each with a different level of risk. The most secure investors were the Senior Financiers. The next most secure were the Mezzanine Financiers. The Junior Financiers were the least secure. However, the Junior Financiers were compensated by an equity interest, which underlies the present dispute, and about which I shall say more shortly. In addition to the distinction between Senior Financiers, Mezzanine Financiers and Junior Financiers, there was also a distinction, within each of the categories of financier, between Asset Financiers and Receivables Financiers. The distinction will be explained below.

37 While there were some differences between the various Aviation Transactions, the structure that was adopted was generally the same. The features of that common structure, may be summarised as follows:

On a specified date, usually known as the Delivery Date, Allco Rentals Pty Limited (Allco Rentals), a subsidiary of KV Aviation, acquired legal ownership of the relevant aircraft from the manufacturer or from an airline, under a Master Aircraft Purchase Agreement and a Bill of Sale.

On the Delivery Date, Allco Rentals entered into an Operating Lease with the airline that was to use the aircraft, usually for a term of between seven and twelve years, under a Master Operating Lease Deed.

On the Delivery Date, Allco Rentals, under a Residuary Interest Sale Deed and a Bill of Sale, sold the aircraft to the relevant RILA, subject to the Operating Lease. The consideration that the RILA agreed to pay to Allco Rentals was the Residual Purchase Price, which was payable in three instalments. The first instalment was payable on the Delivery Date, the second instalment was payable from the proceeds of the loan by the Junior Financier, and the third instalment was payable from the proceeds of the sale or re-lease of the aircraft at the end of the term of the Operating Lease, or from casualty proceeds.

On the Delivery Date, under a Terms of Sale Receivables Deed, Allco Rentals sold to the related Financing SPC the right to payments of rental under the Operating Lease, and the right to receive from the RILA the third instalment of the Residual Purchase Price (the Terms of Sale Payment Rights).

Allco Management or Allco Asset Finance was appointed Manager under a document known as the Financing Deed.

Preference shares in the RILA were issued to the Junior Asset Financier.

Under the senior loan agreement, the Senior Receivables Financier agreed to provide the senior receivables facility and the Senior Asset Financier agreed to provide the senior asset facility.

Under the mezzanine loan agreement, the Mezzanine Receivables Financier agreed to provide the mezzanine receivables facility and the Mezzanine Asset Financier agreed to provide the mezzanine asset facility.

Under the junior loan agreement, the Junior Receivables Financier agreed to provide the junior receivables facility and the Junior Asset Financier agreed to provide the junior asset facility.

Each of the instruments described above is one of the Transaction Documents in relation to the particular Aviation Transaction.

38 As I have said, the third instalment of the Residual Purchase Price was payable from the proceeds of the sale or re-lease of the aircraft at the end of the term of the Operating Lease, or from casualty proceeds. The third instalment represented the amount required to repay the Senior Asset Financier and the Mezzanine Asset Financier. The effect of the structure was that the Junior Financiers held the riskiest or lowest-ranking investments in the Aviation Transactions, in the form of the junior loans and the preference shares in the RILA.

39 Each Aviation Transaction entered into along those lines resulted in a profit for Allco Rentals equal to:

the proceeds received from the first instalment of the Residual Purchase Price;

plus the proceeds received from the sale of the right to receive rental payments under the Operating Lease and the right to receive the third instalment of the Residual Purchase Price;

less the price paid for the acquisition of the aircraft.

From that profit, Allco Rentals paid an arrangement fee to a subsidiary of Old AFGL or Public AFGL, as relevant. The fee was typically an amount equal to the profit, less $10,000. Thus, Allco Rentals derived a fee of $10,000 from each Aviation Transaction.

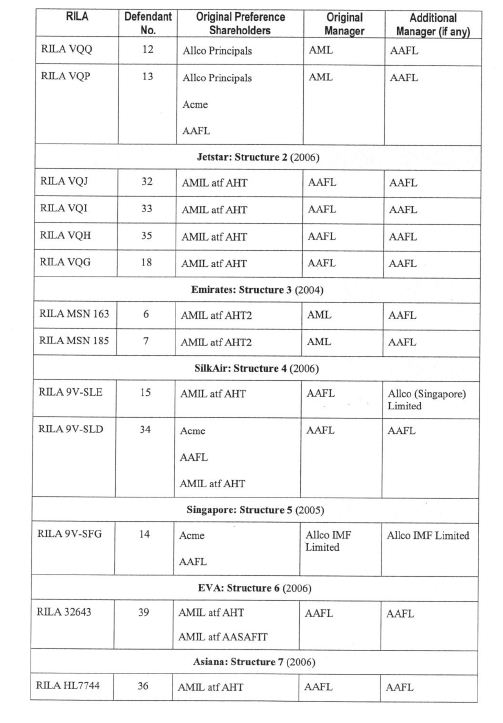

40 Aviation Transactions were structured so that term of the loans under the receivables facilities matched the term of the Operating Lease. The Receivables Financiers received monthly or quarterly payments of principal and interest sourced from the rental payments under the Operating Lease. The terms of the loans under the asset facilities also matched the term of the Operating Lease. However, the Asset Financiers typically received no payments of principal or interest until the final maturity date. Thus, the asset loans were future value or zero coupon loans. A future value loan or zero coupon loan is one under which no interest payments are made during the term of the loan. Rather, interest accrues and capitalises during the term of the loan, and is payable at the end of the term from (in the case of an Aviation Transaction) the proceeds of realisation of the relevant aircraft.

41 The source of funds for repayment of the asset loans was intended to be the proceeds from the sale or re-lease of the aircraft, or casualty proceeds. That is to say, the Asset Financiers typically lent to the relevant RILAs and were repaid from the realisation or refinancing of the relevant aircraft, while the Receivables Financiers typically lent to the Financing SPCs and were repaid from rental payments under the Operating Lease. The term of the loans under the asset facilities could be extended at the option of the preference shareholders, in certain circumstances.

42 The Junior Receivables Financier and the Junior Asset Financier were typically Allco Finance Group entities, most commonly Allco Managed Investments, as trustee of the Aircraft Holdings Trust. Allco Managed Investments was also usually the initial holder of some or all of the preference shares in the RILA. The surplus, if any, that remained from the proceeds of sale or re-lease of the aircraft, after payment of the loans under the receivables facilities and the loans under the asset facilities, was paid to the preference shareholders of the RILA. That surplus is generally referred to as the Upside. Thus, Old AFGL or Public AFGL, as relevant, as the holder of interests in the Aviation Holdings Trust, had an incentive to ensure that all loans were repaid in full and to maximise the proceeds from the sale or re-lease of the aircraft at the end of the term of the Operating Lease.

43 Allco Management or Allco Asset Finance, as the Managers, were paid a monthly or quarterly fee. That fee was also sourced from the rental payments under the relevant Operating Leases.

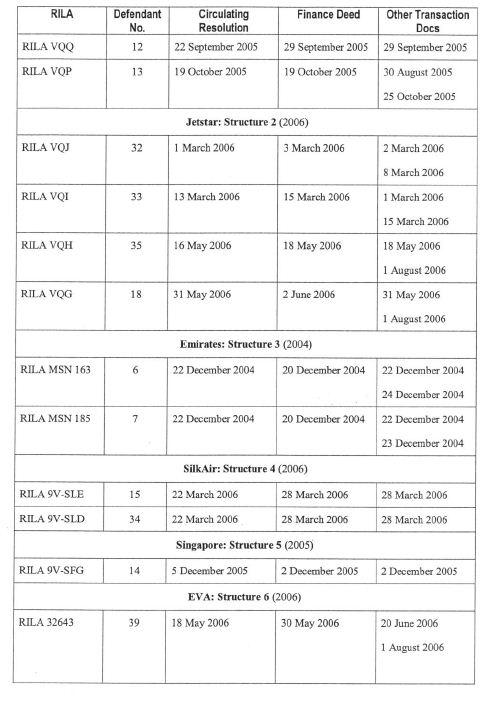

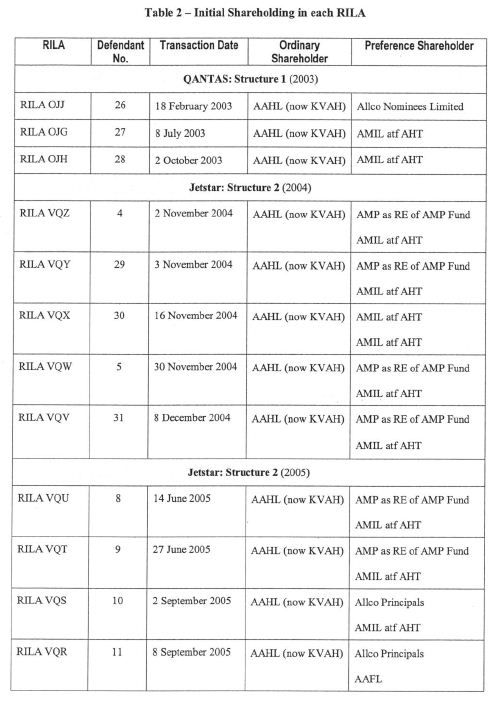

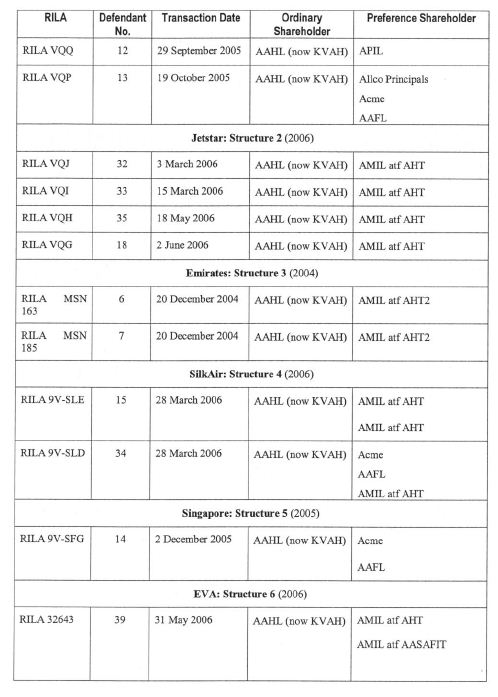

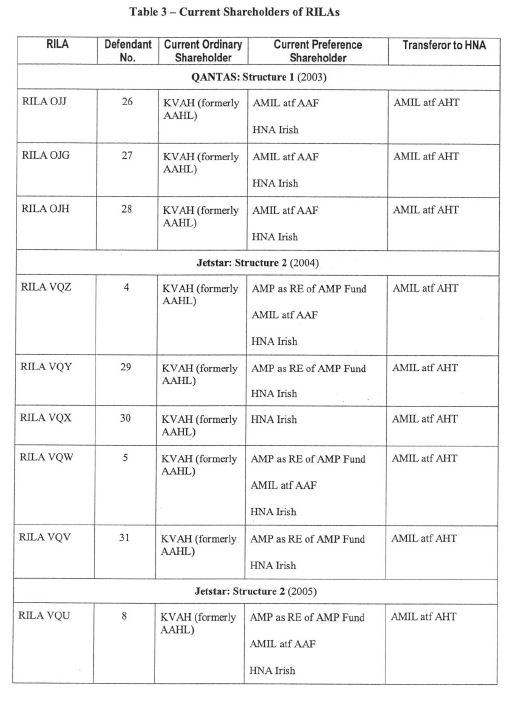

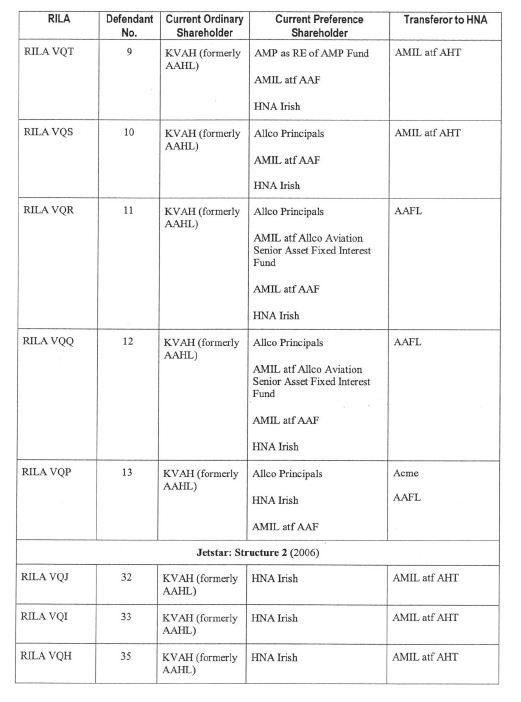

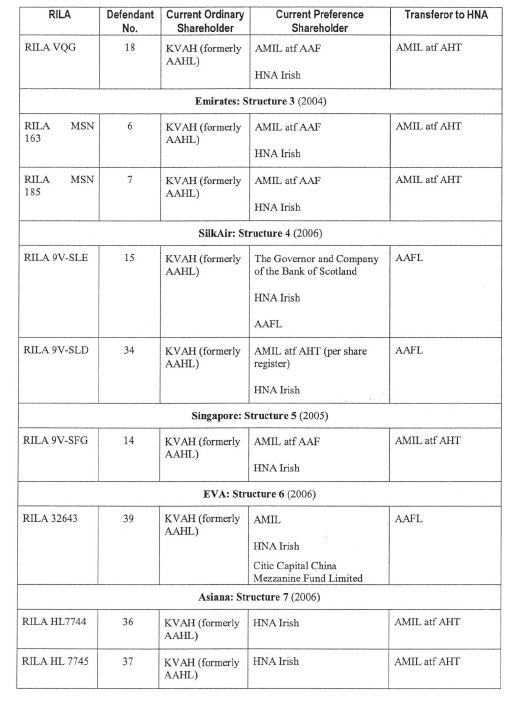

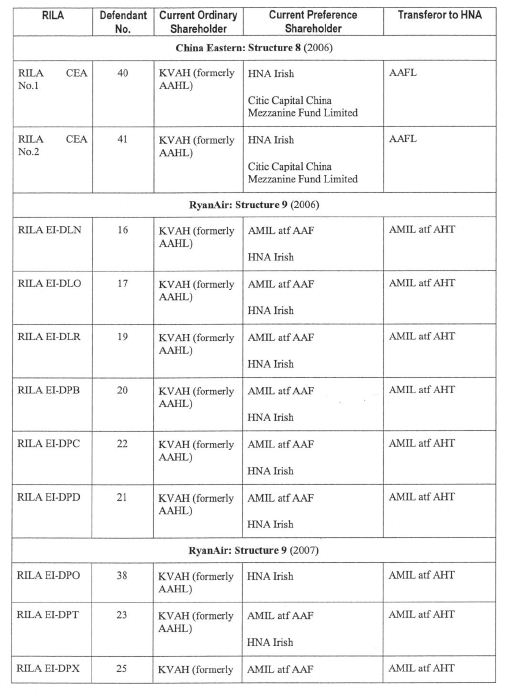

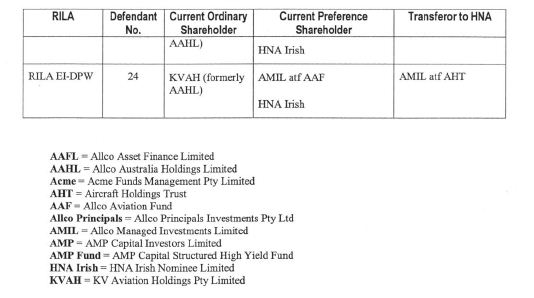

44 Thus, the Aviation Division had three sources of revenue from a given Aviation Transaction, as follows:

the arrangement fee earned when the Aviation Transaction was entered into, funded from the debt raised to finance the purchase of the aircraft;

management fees paid to the Managers, funded from the rental payments under the Operating Lease; and

the Upside, if any, at the end of the Operating Lease, which was payable to the preference shareholders of the RILA.

45 Except in two Aviation Transactions, where there was no junior loan, the borrower of the junior loans was the RILA. The borrower of the senior loans and the mezzanine loans was the Financing SPC. In all cases, the RILA and the Financing SPC each guaranteed the liabilities of the other and provided indemnities in respect of the obligations of the other. All relevant assets, including everything owned by the RILA and everything owned by the Financing SPC, were charged as security for the performance of the obligations arising under the various guarantees and indemnities. The assets included the aircraft and the rental payable under the Operating Lease. The charges were given to the Security Trustee. The role of the Security Trustee in the transactions is largely set out in cl 3 of a document known as the Master Financing Deed. In the case of RILA VQZ, JP Morgan Institutional Services Australia Limited was the Security Trustee.

46 In the course of negotiations with an airline or a bank in relation to an Aviation Transaction, the airline or the bank would usually be provided by Allco Finance Group with a written assurance (Comfort Letter). The Comfort Letters confirmed that KV Aviation (in its earlier guise as Allco Australian Holdings Limited) was the owner of the ordinary shares in the relevant RILA and Financing SPC. The Comfort Letters typically also contained an undertaking, from Old AFGL or Public AFGL, as relevant, to procure that either it or KV Aviation would continue to be the owner of those ordinary shares throughout the term of the Operating Lease. The assurances given in the Comfort Letters may have some significance, as will appear below.

47 Mr Benjamin Wilson, who was “Director – Aviation” with Public AFGL, was told by Mr Veal how to respond when asked by banks and airlines about the shareholding of KV Aviation in the RILAs. Mr Veal told Mr Wilson to tell those enquirers that KV Aviation was owned by the family trusts of executives of Old AFGL or Public AFGL, as relevant, which could always get the consent of KV Aviation and could procure any consents needed at the level of the RILAs and the Finance SPCs, because KV Aviation was controlled by Mr Coe and two other senior executives.

48 The constitutions of the RILAs, together with two of the Transaction Documents, the Remarketing Agreement and the Financing Deed, are of particular significance to the issues raised in this proceeding. The Remarketing Agreement provides for the realisation and application of proceeds from the sale or re-lease of the aircraft. The Managers are appointed under the Financing Deed. I shall describe the constitutions of the RILAs, the Financing Deed and the Remarketing Agreement in more detail.

The Constitutions of the RILAs

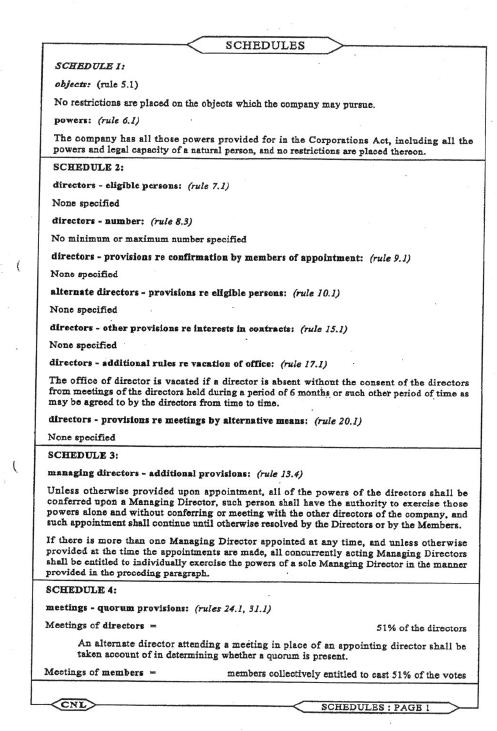

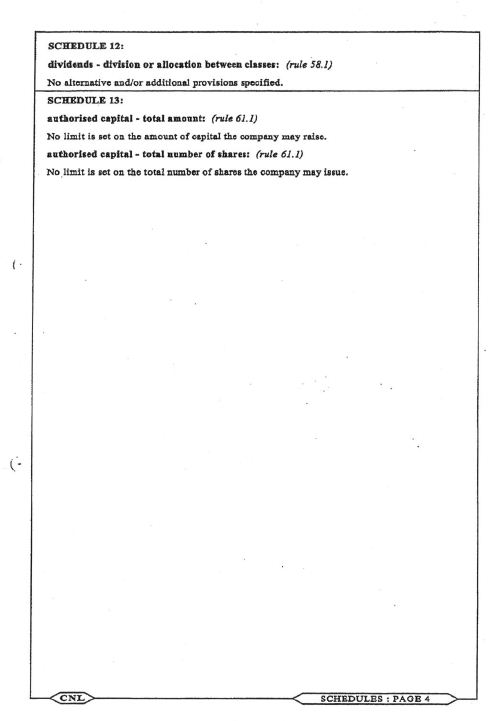

49 The constitutions of many of the defendant RILAs are in terms that are the same in relevant respects. Accordingly, the argument has, with a limited number of exceptions, been conducted on the basis that the constitutions of certain defendant RILAs exemplify others in the same form. The example that has been taken to represent the standard structure that applied in relation to the Aviation Transactions is the constitution of RILA VQZ. The Financing SPC associated with RILA VQZ was VQZ Financing SPC (see paragraph [2] above).

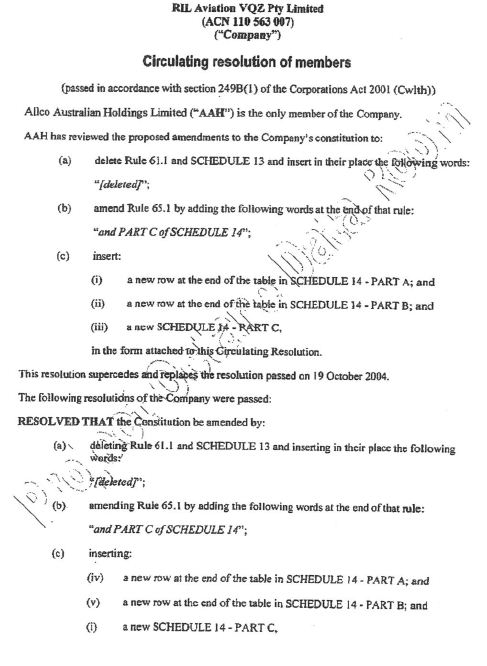

50 RILA VQZ was incorporated on 18 August 2004. Its constitution consisted of 66 clauses and 16 schedules. On 3 November 2004, the constitution of RILA VQZ was amended in a number of respects by a resolution passed in accordance with s 249B(1) of the Corporations Act by KV Aviation, which at that time was the only member of RILA VQZ. The original constitution and the resolution are set out in Appendix 2 to these reasons.

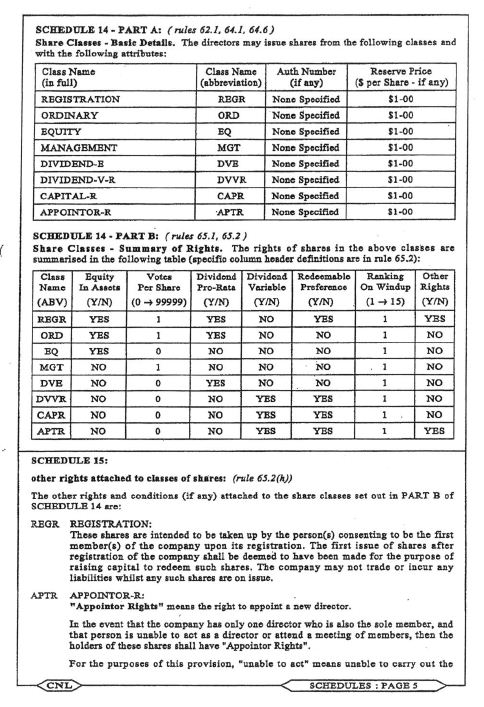

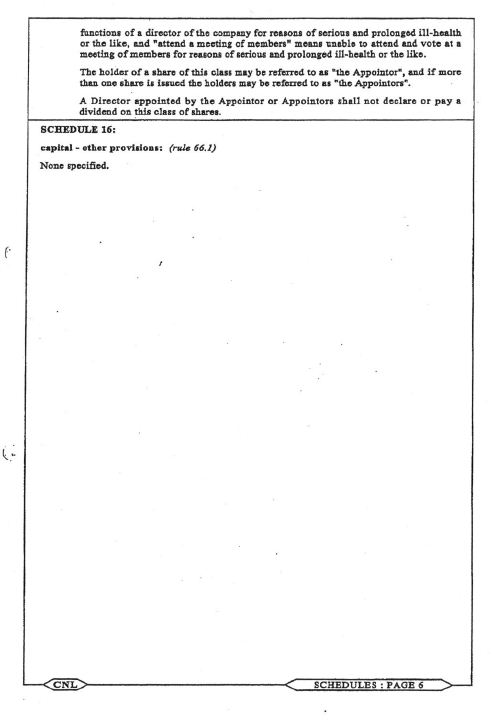

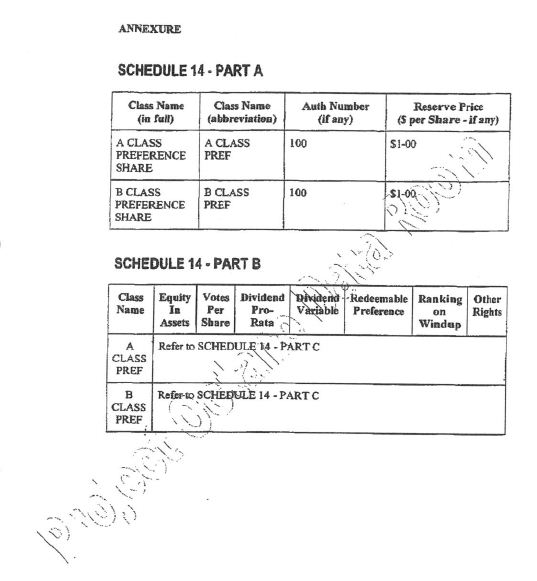

51 Clauses 60 to 66 of the constitution of RILA VQZ deal with capital, and Schedules 14 to 16 deal with share classes. Clause 60.1 provides that shares in RILA VQZ may be issued by the directors, and may be issued with such preferred, deferred, or other special rights, or with such restrictions, as the directors by resolution determine. Clause 64.1 provides that the directors may issue shares in the capital of RILA VQZ from the classes set out in Part A of Schedule 14. Clause 65.1, as amended, provides that the rights and conditions of the shares and the classes set out in Part A of Schedule 14 are summarised in Parts B and C of Schedule 14. Part C of Schedule 14 was added to the constitution of RILA VQZ by the resolution of 3 November 2004.

52 Part B of Schedule 14, as amended, consists of a table with eight columns. The headings of the eight columns may be seen in Appendix 2. The first column consists of abbreviated references to each class of share. A note to cl 65.1 states that the rights and conditions attached to a class of share in the table are to be determined by reading the row for each class horizontally, and reading the headings of the remaining vertical columns in accordance with the definitions supplied in cl 65.2. The effect is that Schedule 14 specifies, in relation to each class of share:

whether there is an entitlement to share in surplus assets on a winding up;

the number of votes per share;

whether there is a right to share equally with other holders of shares in the class in dividends;

whether there is a right to share in dividends;

whether the shares in the class are redeemable, in accordance with the general rights specified in cl 65.2(e);

the priority and ranking of the class, on a winding up, in respect of repayment of capital and the distribution of surplus assets and profits; and

whether other rights, referred to in Schedule 15, are attached to the class.

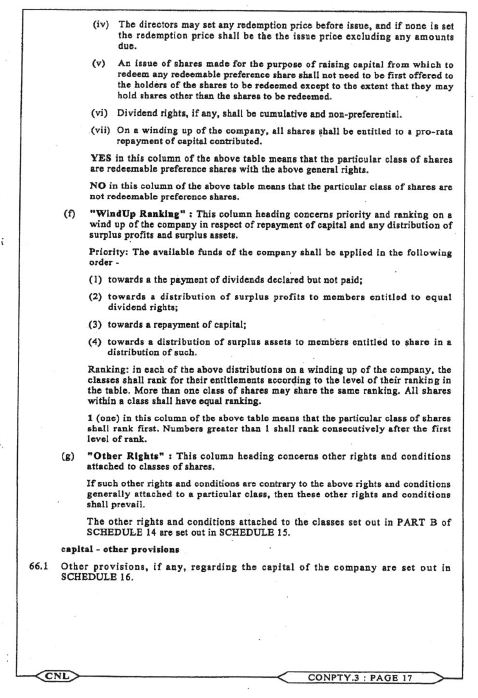

53 The general rights of redeemable preference shares set out in cl 65.2(e) are as follows:

(i) they are issued on the terms that they are liable to be redeemed;

(ii) the directors in their absolute discretion may redeem any one or more redeemable preference shares of this class to the exclusion of other shares;

(iii) they may be redeemed without notice to the holders;

(iv) the directors may set any redemption price before issue, and, if none is set, the redemption price is to be the issue price, excluding any amounts due;

(v) an issue of shares made for the purpose of raising capital from which to redeem any redeemable preference share does not need to be first offered to the holders of the shares to be redeemed, except to the extent that they may hold shares other than the shares to be redeemed;

(vi) dividend rights, if any, are to be cumulative and non-preferential;

(vii) on a winding up of the company, all shares are entitled to a pro-rata repayment of capital contributed.

54 The amendment made to Part A of Schedule 14 by the resolution of 3 November 2004 inserted two additional classes of shares, being A class preference shares and B class preference shares. The amendment made by the resolution to Part B of Schedule 14 was to insert two additional rows, one for each of those two additional classes of shares. However, whereas the table in Part B contains an entry for each of the original eight classes under each of the other seven column headings, the material inserted under all seven column headings in the row for each of the A class preference shares and B class preference shares simply refers to Part C of Schedule 14. Part C of Schedule 14 is set out in Appendix 2.

55 The summary of rights in relation to preference shares set out in Part C of Schedule 14 deals with the rights under the following headings:

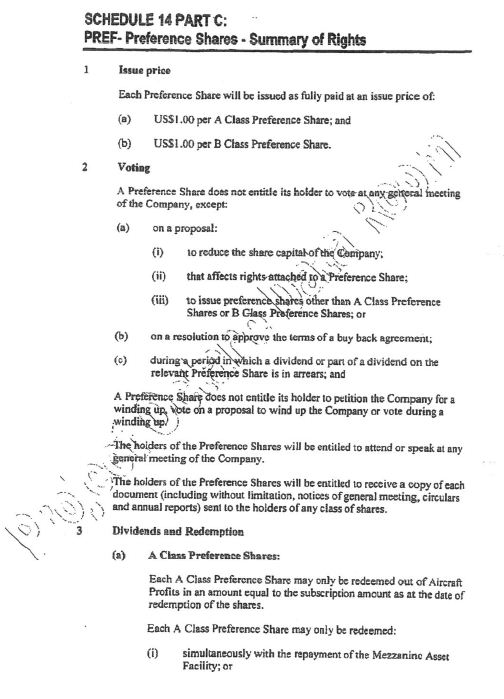

1. Issue price

2. Voting

3. Dividends and Redemption

(a) A Class Preference Shares

(b) B Class Preference Shares

4. Dividend lock-up

5. Variation of rights

6. Conversion

7. Ranking of Preference Shares

8. Transfer

9. Registration

10. Definitions

56 Where necessary, I shall refer to the precise language of the constitution of RILA VQZ in dealing with the contentions of the parties as to its proper construction. For present purposes, it will suffice to summarise the rights of the holders of preference shares, as follows:

The holder is not entitled to vote at any general meeting, except in relation to certain specified matters, which include a proposal affecting rights attached to either class of preference share.

The A class preference shares may only be redeemed out of Aircraft Profits in an amount equal to the subscription amount as at the date of redemption of the shares. The term Aircraft Profits is defined to mean all profit derived by RILA VQZ from:

(i) the sale or use of the aircraft;

(ii) any casualty or termination value, as defined in the relevant Operating Lease; and

(iii) any insurance proceeds received in relation to the aircraft.

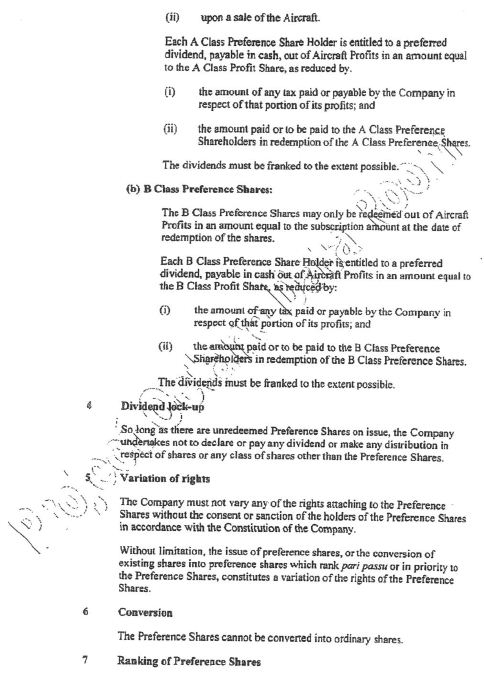

The A class preference shares may only be redeemed simultaneously with the repayment of the Mezzanine Asset Facility, or upon a sale of the aircraft.

Each holder of A class preference shares is entitled to a preferred dividend, payable in cash out of Aircraft Profits, in an amount equal to the A Class Profit Share, as reduced by:

(i) the amount of any tax paid or payable by the RILA in respect of that portion of its profits; and

(ii) the amount paid or to be paid to the holders of A class preference shares in redemption of the A class preference shares.

The B class preference shares may only be redeemed out of Aircraft Profits in an amount equal to the subscription amount as at the date of redemption of the shares.

Each holder of B class preference shares is entitled to a preferred dividend, payable in cash out of Aircraft Profits, in an amount equal to the B Class Profit Share, as reduced by:

(i) the amount of any tax paid or payable by RILA VQZ in respect of that portion of its profits; and

(ii) the amount paid or to be paid to the holders of B class preference shares in redemption of the B class preference shares.

So long as there are unredeemed preference shares on issue, RILA VQZ may not declare or pay any dividend or make any distribution in respect of shares or any class of shares other than preference shares.

RILA VQZ must not vary any of the rights attached to the preference shares without the consent or sanction of the holders of the preference shares in accordance with the constitution. The issue of preference shares, or the conversion of existing shares into preference shares which rank pari passu or in priority to the preference shares, constitutes a variation of the rights of the preference shares.

The preference shares cannot be converted into ordinary shares.

The preference shares rank in priority to ordinary shares in all respects. If there is a return or distribution of capital, the holders of the preference shares will be entitled to receive, in respect of each preference share held, a sum equal to the aggregate of:

(i) the amount of any dividend, whether declared or not, that is due and payable on the preference shares up to but excluding the date of the winding up;

(ii) all arrears of dividends described in (i) above; and

(iii) all surplus assets and capital of RILA VQZ;

divided by the number of preference shares on issue. The holders of the ordinary shares will be entitled to receive, in respect of each ordinary share, the return of their initial contribution.

The preference shares are transferable at the holder’s option with the prior consent of RILA VQZ, which consent must not be unreasonably withheld, delayed or conditional.

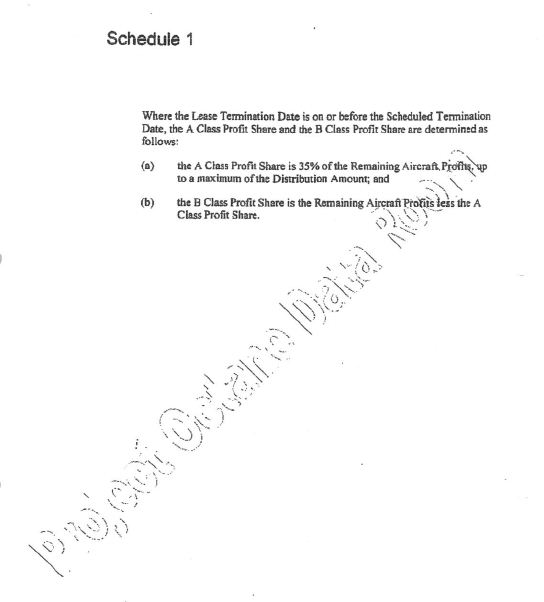

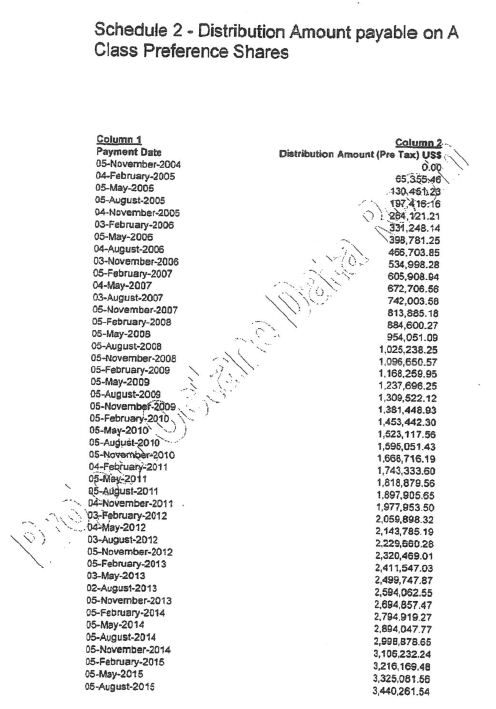

57 Schedules 1 and 2 to Part C of Schedule 14 specify the method by which the A Class Profit Share and B Class Profit Share are to be calculated. Where the Lease Termination Date is on or before the Scheduled Termination Date, the A Class Profit Share is 35 per cent of Remaining Aircraft Profits, up to a fixed amount that varies according to the payment date from 5 November 2004 to 5 August 2015. The B Class Profit Share is the Remaining Aircraft Profits less the A Class Profit Share. The Lease Termination Date is the date on which the Operating Lease is terminated. The Scheduled Termination Date is the expiry date of the Operating Lease. The term Remaining Aircraft Profits is defined as the remainder of Aircraft Profits following satisfaction of the RILA’s obligations under the Transaction Documents. Thus, the amount of the preferred dividend is determined by reference to the amount of Aircraft Profits.

58 The Remarketing Agreement relating to aircraft VH-VQZ is dated 3 November 2004. It may be summarised as follows:

The parties to the Remarketing Agreement include the Senior, Mezzanine and Junior Financiers, the holders of A class preference shares and B class preference shares, Allco Management (which is described as the Remarketing Agent) and RILA VQZ.

By cl 1.1(a), RILA VQZ irrevocably appoints the Remarketing Agent to act as agent for RILA VQZ during the remarketing period, which, ordinarily, is the last 18 months of the term of the Operating Lease. The appointment under cl 1.1(a) does not define the extent of the authority given to the Remarketing Agent.

By cl 1.2(a), the Remarketing Agent must, in the exercise of all rights, powers and discretions on behalf of RILA VQZ under the Remarketing Agreement, act in accordance with any instructions from the Instructing Group. The rights, powers and discretions that may be exercised are not set out.

By the operation of cl 1.2(d), any action taken by the Remarketing Agent in accordance with the Remarketing Agreement binds RILA VQZ.

Assuming that there has been no default, the Instructing Group is the B class preference shareholder. However, where the Junior Financier will not be repaid in full, the A class preference shareholder is the Instructing Group.

Under cl 3.1, the Remarketing Agent must appoint an aircraft agent in relation to the remarketing of the aircraft, and, under cl 3.3, must instruct the aircraft agent to prepare a market value of the aircraft and a lease value of the aircraft. The market value is a prediction of the net proceeds from sale of the aircraft and is to reflect the likely price to be obtainable for the aircraft on a sale. The lease value is a prediction of the proceeds to be received from a lease of the aircraft and is to reflect the market rent or other amount payable for a lease of the aircraft.

Under cl 3.3(c)(i), upon receipt of the report on the market value and the lease value, the Remarketing Agent must instruct the aircraft agent to solicit offers from responsible parties for the purchase or lease of the aircraft. A responsible party is an offeror with sufficient financial resources to be in a position either to complete the purchase or lease transaction pursuant to the offer, or to arrange for all financing within the terms of the offer. Thus, it is the duty of the Remarketing Agent to solicit offers from parties that are in a position to provide the necessary financing associated with their offers.

Under cl 3.3(d), the Remarketing Agent must use all reasonable endeavours either to sell the aircraft for the highest possible price or to lease the aircraft for the highest rent or other amount payable. While that provision stipulates what the Remarketing Agent is required to do, it is arguable that it is not a grant of authority to sell or lease the aircraft on behalf of RILA VQZ.

Under cl 3.4, each of the Financiers, RILA VQZ and the preference shareholders may, though none is obliged to, introduce responsible parties to the Remarketing Agent. There is no mention of RILA VQZ obtaining a fee or any other remuneration for introducing a responsible party.

Under cl 4, if the Remarketing Agent receives an offer from a responsible party, it must, within three days of receipt of the offer, notify each of the Financiers, RILA VQZ and the preference shareholders, stating the offered price.

Clause 5 deals with decision-making procedures during the remarketing period. Clause 5.3 provides a cascading regime for approving the acceptance of offers for the purchase or lease of the aircraft, as follows:

(a) if an offer will result in Net Sale Proceeds, a term defined in the Financing Deed, of less than or equal to the Senior Financier Threshold Amount, RILA VQZ may not direct the Remarketing Agent to accept that offer without the consent of the Senior Asset Financier, the Mezzanine Asset Financier and the Junior Asset Financier;

(b) if an offer will result in net sale proceeds of greater than the Senior Financier Threshold Amount, but less than or equal to the Mezzanine Financier Threshold Amount, RILA VQZ may not direct the Remarketing Agent to accept that offer without the consent of each of the Mezzanine Asset Financier and the Junior Asset Financier, but the consent of the Senior Asset Financier is not required;

(c) if an offer will result in net sale proceeds of greater than the Mezzanine Financier Threshold Amount, but less than or equal to the Junior Financier Threshold Amount, RILA VQZ may not direct the Remarketing Agent to accept that offer without the consent of the Junior Asset Financier, but the consents of the Senior Asset Financier and the Mezzanine Asset Financier are not required;

(d) if an offer will result in the net sale proceeds of greater than the Junior Financier Threshold Amount, RILA VQZ may direct the Remarketing Agent to accept that offer without the consent of any of the Asset Financiers.

The Threshold Amounts are the amounts necessary to discharge all amounts payable to the relevant Financier.

Clause 4 gives power to the Instructing Group to instruct the Remarketing Agent to accept or not accept an offer. That power is expressed to be subject to cl 5. Under cl 5.4, the preference shareholders may request a six month extension of the remarketing period. The remarketing period may be further extended with the consent of the Asset Financiers. However, under cl 5.4(c), certain conditions must be met before any extension is effective. The conditions are that RILA VQZ or the associated Financing SPC has provided satisfactory additional security to the Security Trustee and has made appropriate arrangements to preserve the value of the aircraft. That provision gives RILA VQZ a separate role in the process.

Under cl 5.6, RILA VQZ must not enter into leasing arrangements in respect of the aircraft during the remarketing period without the prior written consent of all of the Asset Financiers. If the lease value of the aircraft exceeds the market value of the aircraft, the parties agree to enter into discussions in good faith in relation to the most appropriate and beneficial way to remarket the aircraft.

Under cl 1.2(a), the entry into a new lease by RILA VQZ can only occur on instructions from the Instructing Group. That is confirmed by cl 9(c), which provides that the Remarketing Agent must not execute any documents on behalf of RILA VQZ unless so instructed by the Instructing Group.

Under cl 6, the preference shareholders must share additional costs during any extended remarketing period.

Clause 7 deals with the circumstances in which the Senior Asset Financier and the Mezzanine Asset Financier may be paid out. Thus, RILA VQZ is granted a right to acquire the interest of the Senior Asset Financier and the interest of the Mezzanine Asset Financier by paying all of the amounts owing to them. That right does not involve any prepayment fee, as RILA VQZ’s entitlement only arises at the end of the term of the Operating Lease. The entitlement of RILA VQZ to acquire those interests does not exclude the right of the Financing SPC, as the borrower from those Financiers, to prepay the loans. RILA VQZ is not given a right to acquire the interest of the Junior Asset Financier in that way. However, RILA VQZ, as the borrower from the Junior Asset Financier, can exercise the right to prepay that loan.

Under cl 7.2, RILA VQZ may only acquire all of the Mezzanine Asset Financier’s interest in the way just described if RILA VQZ simultaneously procures a purchase by a third party of all A class preference shares held by the Mezzanine Asset Financier for a purchase price equal to the amount that the Mezzanine Asset Financier would be entitled to receive by way of dividend and redemption proceeds if the aircraft were sold for a price equal to the best offer actually received for the aircraft that the Mezzanine Asset Financier is prepared to accept. If the Mezzanine Asset Financier is not prepared to accept any offer actually received for the aircraft, it must co-operate with RILA VQZ and use reasonable endeavours to assist RILA VQZ to enter into a refinancing of the aircraft, or other arrangement in respect of the aircraft, in a manner acceptable to RILA VQZ, so as to maximise the value of the aircraft for the A class preference shareholders and the B class preference shareholders.

59 KV Aviation claims that it has, through its holding of the ordinary shares in the defendant RILAs, valuable control rights in relation to the restructuring of Aviation Transactions at the end of the terms of the relevant Operating Leases. HNA Irish relies on the Remarketing Agreement as demonstrating that that claim lacks foundation. It contends that the control rights that exist at the end of the term of the Operating Lease are vested in the preference shareholders, and that there is no potentially profitable business opportunity available to be exploited by the ordinary shareholders of the defendant RILAs. It says that the vesting of control rights in the preference shareholders is consistent with their interest being the lowest ranking, or highest risk, investment in an Aviation Transaction. It says that vesting control rights in the preference shareholders creates an incentive for the proceeds from the sale or re-leasing of the aircraft to be maximised.

60 HNA Irish contends that the function of the Remarketing Agent is important, because it allows the party empowered to give instructions to the Remarketing Agent to control the sale or re-lease of the aircraft and thereby keep within its control the efforts to maximise the proceeds. That party, it says, was the holder of the preference shares, not RILA VQZ. Thus, HNA Irish contends that the provisions of the Remarketing Agreement reflect a clear intention that the holder of preference shares, and not the board of RILA VQZ, is to control the remarketing of the aircraft. KV Aviation, however, contends that that overstates the effect of the Remarketing Agreement. I shall return to that question below.

61 The parties to the Financing Deed of 2 November 2004, relating to aircraft VH-VQZ, apart from RILA VQZ and VQZ Financing SPC, are the Security Trustee, the Senior, Mezzanine and Junior Financiers and Facility Agents, and Allco Management as the Manager. By Part A, the Security Trustee declares that, at any time, it holds the trust fund, as defined, on trust for itself, the Facility Agents and the persons who are Financiers at that time. Under cl 1.3, the trust ends on the day before the 80th anniversary of the date of the Financing Deed, unless ended earlier. The trust fund consisted of the sum of $10, together with any other property that the Security Trustee acquired on the trusts of the Financing Deed, including any security for the payment of money or performance of obligations.

62 Clause 10.1 of the Financing Deed provides that the liability of each of RILA VQZ and VQZ Financing SPC is limited to the lesser of the amount owing by it and the proceeds of sale of the aircraft. The recourse of the Financiers is limited to the property charged under the charges given to the Security Trustee by RILA VQZ and VQZ Financing SPC.

63 Clause 14.1(i) of the Financing Deed contains undertakings about RILA VQZ and VQZ Financing SPC. The relevant undertakings (the Single Purpose Undertakings) are that each of RILA VQZ and VQZ Financing SPC will not:

(i) engage in any business or other activity other than as contemplated in the Transaction Documents;

(ii) have any liabilities, other than its liabilities under the Transaction Documents, liability to its shareholders in accordance with its constitution, and other liabilities required to maintain its existence or comply with any law relating to companies generally;

(iii) have any assets other than those under, or derived from, the Transaction Documents, and its share capital;

(iv) have any employees; or

(v) enter into any agreements other than the Transaction Documents or agreements in connection with any issue of ordinary or preference shares and agreements with the holders of such shares.

64 There is no provision for the termination of the provisions of the Financing Deed or the Single Purpose Undertakings before the end of the trust established by the Financing Deed. Specifically, there is no express provision in the Financing Deed that the Single Purpose Undertakings are to come to an end upon the repayment of the loans that are the subject of the financing documents. That is of some significance, and I shall return to that question below.

65 Clause 8.6 of the Financing Deed provides that the Manager may, with the prior written consent of all of the parties, terminate its appointment. Clause 8.7 of the Financing Deed provides that RILA VQZ, VQZ Financing SPC and Allco Rentals may remove the Manager from office if:

the Manager is insolvent; or

the Manager breaches its obligations under the Financing Deed.

The Security Trustee, acting on instructions of the Financiers, may also remove the Manager in those circumstances. Each of RILA VQZ, VQZ Financing SPC and Allco Rentals may also remove the Manager at the expiration of three months after it gives notice to the Manager that it requires the Manager to cease acting as the Manager.

66 However, cl 8.9 of the Financing Deed provides that neither the termination of the Manager under cl 8.6 nor the removal of the Manager under cl 8.7 is effective unless certain prerequisites are satisfied. First, a replacement Manager must have been identified and approved by both the Security Trustee and entities associated with the Financiers. Secondly, that replacement Manager must have executed documents reasonably satisfactory to the Security Trustee to become the replacement Manager for the purposes of the Transaction Documents.

67 The proceeding was commenced by way of originating process. A fourth further amended originating process was filed on 25 March 2011 (the Originating Process). The amended statement of claim, filed on 20 October 2010 (the Statement of Claim), runs to 168 paragraphs. An amended defence (the Defence) was filed on 21 June 2011. I shall first say something about the Originating Process and the defendant RILAs. I shall then say something about the Statement of Claim, the Defence, and the witnesses.

68 Some of the factual background to the proceeding is set out in the Statement of Claim. However, it is appropriate at this stage to provide a brief summary of certain aspects of the procedural history.

69 The proceeding was commenced during the afternoon of 3 February 2010. The timing is significant, as the commencement of the proceeding formed part of a broader struggle for control of the defendant RILAs that was taking place at that time. On the morning of 3 February 2010, HNA Irish arranged to hold general meetings of certain defendant RILAs. The meetings for ten of the defendant RILAs were to be held that day, and the meetings for another 24 defendant RILAs were to be held on 25 February 2010. Those meetings were arranged with the aim of passing resolutions to amend the constitutions of those defendant RILAs to strengthen the position of preference shareholders, and resolutions to appoint new directors to represent the interests of preference shareholders. At approximately 11.12am on 3 February 2010, the solicitors for HNA Irish sought undertakings from KV Aviation and Messrs Veal and Kinghorn that they would not take any steps to change the share capital of the defendant RILAs without first giving five business days’ notice.

70 The undertakings sought were not provided. Rather, Messrs Kinghorn and Veal responded by immediately convening meetings of the defendant RILAs, at which resolutions were passed to issue further ordinary shares in each of the defendant RILAs to KV Aviation. However, the passing of those resolutions was not disclosed to HNA Irish and HNA Group until 11 February 2010.

71 On the afternoon of 3 February 2010, HNA Irish sought and obtained urgent interlocutory relief. The orders made by the Court included an order that KV Aviation and Messrs Veal and Kinghorn be restrained from taking any action directed to the issue of further shares or securities in the 24 RILAs that were at that time named as defendants, without providing five business days’ notice in writing to HNA Irish and HNA Group. On 5 February 2010, the Court made further orders continuing that restraint until further order.

72 The Court was not told, on 5 February 2010, about the purported issue of ordinary shares in the defendant RILAs on 3 February 2010. On 23 March 2010, after it was accepted on behalf of KV Aviation and Messrs Veal and Kinghorn that that purported issue of ordinary shares was not valid, the Court made declarations to that effect.

73 The Court also ordered that certain questions relating to the resolutions that had been proposed on behalf of HNA Irish be determined separately. On 31 March 2010, the Court answered those questions, determining that the constitutions of the defendant RILAs did not entitle a holder of preference shares to vote on a resolution to insert a provision permitting the preference shareholders to appoint directors (see HNA Irish Nominee Limited v Kinghorn [2010] FCA 311). An appeal from that determination was dismissed (see HNA Irish Nominee Limited v Kinghorn (2010) 78 ACSR 553). Thus, the resolution purporting to insert such a provision and the resolution purporting to appoint new directors were each invalid. The consequence is that, other than for RILA 9V-SLE, about which I shall say something below, the preference shareholders do not have any right under the constitutions of the defendant RILAs to vote at a general meeting on resolutions to appoint directors. Only the holders of ordinary shares are entitled to vote on those questions.

74 By the Originating Process, HNA Irish and HNA Group seek:

declaratory relief in relation to the proper construction of the constitutions of the defendant RILAs;

final injunctive relief with respect to conduct or proposed conduct of Messrs Veal and Geoffrey Kinghorn on behalf of the defendant RILAs that affects the interests of HNA Irish as holder of preference shares;

relief under ss 232 and 233 of the Corporations Act with respect to the conduct of the affairs of the defendant RILAs; and

relief under ss 1324 and 1325 of the Corporations Act, and s 12GD and s 12GM of the ASIC Act, with respect to alleged contraventions of s 1041H of the Corporations Act and s 12DA of the ASIC Act.

75 Section 233 of the Corporations Act relevantly provides that the Court may make such order in relation to a company as it considers appropriate, including an order:

that the company’s existing constitution be modified or repealed;

regulating the conduct of the company’s affairs in the future;

for the purchase of any shares by any member;

restraining a person from engaging in specified conduct; or

requiring a person to do a specified act.

Under s 234, an application for an order under s 233 in relation to a company may be made by a member of the company. Under s 232, the Court may make an order under s 233 if, relevantly, the conduct of the company’s affairs is either:

contrary to the interests of the members as a whole; or

oppressive to, unfairly prejudicial to, or unfairly discriminatory against a member or members, whether in that capacity or in any other capacity.

76 Section 1324 of the Corporations Act relevantly provides that, where a person has engaged, is engaging, or is proposing to engage, in conduct that constituted, constitutes, or would constitute a contravention of the Act, the Court may, on the application of a person whose interests have been, are, or would be affected by the conduct, grant an injunction restraining the first-mentioned person from engaging in the conduct. Under s 1325, where, in a proceeding instituted under, or for a contravention of, certain provisions of the Corporations Act, the Court finds that a person who is a party to the proceeding has suffered, or is likely to suffer, loss or damage because of conduct that was engaged in in contravention of those provisions, the Court may, whether or not it grants an injunction or makes an order under any other provision of the Corporations Act, make such order or orders as it thinks appropriate, if the Court considers that the order or orders will compensate that person in whole or in part for the loss or damage, or will prevent or reduce the loss or damage.

77 One of the provisions referred to in s 1325 is s 1041H. Under s 1041H, a person must not engage in conduct in relation to a financial product or a financial service that is misleading or deceptive or is likely to mislead or deceive. Under s 763A, financial product includes a facility through which, or through the acquisition of which, a person makes a financial investment. Under s 763B, a person makes a financial investment if the person gives money or money’s worth to another person, intending that person to use it to generate a financial return. An example is the payment of money to a company for the issue of shares in the company.

78 Section 12DA of the ASIC Act provides that a person must not, in trade or commerce, engage in conduct in relation to financial services that is misleading or deceptive or is likely to mislead or deceive. Under s 12BAB of the ASIC Act, a person provides a financial service if that person deals in a financial product or provides a service that is otherwise supplied in relation to a financial product. Under s 12BAB(7), issuing a financial product constitutes dealing in a financial product.

79 Section 12GD of the ASIC Act provides that if, on the application of any person, the Court is satisfied that another person has engaged, or is proposing to engage, in conduct that constitutes or would constitute a contravention of a provision such as s 12DA, the Court may grant an injunction in such terms as it determines to be appropriate. Section 12GM provides, without limiting the generality of s 12GD, that if, in a proceeding instituted under or for an offence against a provision such as s 12DA, the Court finds that a person who is a party to the proceeding has suffered, or is likely to suffer, loss or damage, the Court may, whether or not it grants an injunction under s 12GD, make such order or orders as it thinks appropriate against a person who has engaged in conduct in contravention of that provision, if the Court considers that the order or orders concerned will compensate the first-mentioned person in whole or in part for the damage, or will prevent or reduce the loss or damage.

80 The specific relief claimed in the Originating Process is as follows:

an order that the ordinary shares in the defendant RILAs be transferred by KV Aviation to a party nominated by HNA Irish, for consideration of one dollar per share;

further, or in the alternative, an order that the ordinary shares in the defendant RILAs be transferred by KV Aviation to a charitable trust, to be maintainable at the cost of HNA Irish and HNA Group, for consideration of one dollar per share;

further, or in the alternative, an order that Messrs Stewart Smith, Nick Hardge and Mathis Shinnick each be appointed as directors of each of the defendant RILAs, to represent the interests of preference shareholders;

further, or in the alternative, an order that a minimum of three persons nominated by either HNA Irish or any of the other holders of preference shares in the defendant RILAs each be appointed as directors of each of the defendant RILAs, to represent the interests of preference shareholders.

81 In addition, HNA Irish and HNA Group claim declarations as follows:

that, on the proper construction of the constitutions of RILA OJG, RILA OJH and RILA OJJ, the preference shares owned by HNA Irish may not be redeemed by the relevant RILA;

that, on the proper construction of the constitution of RILA 9V–SLE, the preference shares owned by HNA Irish may only be redeemed by the relevant RILA with the consent of HNA Irish; and

that, on the proper construction of the constitutions of the remaining defendant RILAs, the preference shares owned by HNA Irish may only be redeemed by the relevant RILA:

(a) upon or after HNA Irish receiving its relevant share of all Remaining Aircraft Profits (as defined in the constitution of the relevant RILA), or, in the alternative,

(b) at the option of HNA Irish.

Further, or alternatively, they claim:

an injunction restraining each of the defendant RILAs from redeeming the preference shares owned by HNA Irish, except with the prior consent of HNA Irish; and

an order that any right of the defendant RILAs to redeem the preference shares that are owned by HNA Irish is void or unenforceable.

82 The argument before me proceeded on the basis that, with the exception of RILA OJG, RILA OJH, RILA OJJ and RILA 9V-SLE, whose particular circumstances are described below, the resolution of the Redemption Issue in respect of RILA VQZ will also resolve the Redemption Issue in respect of all of the other defendant RILAs.

83 Not all RILAs are defendant RILAs. As at November 2008, the portfolio of the Aviation Division consisted of some 68 Aviation Transactions, of which 38 involved RILAs that are named in the proceeding as defendants. It is possible to group Aviation Transactions together in tranches, with the Aviation Transactions in any given tranche generally having a similar overall structure and involving the same airline. The first three Aviation Transactions, entered into in 2002 and 2003, related to Qantas aircraft. The RILAs involved in those transactions were RILA OGG, RILA OGK and RILA OGL. None of those three RILAs is a defendant RILA.

84 The Aviation Transactions in which the defendant RILAs were involved were entered into from 2003 to 2007. Three further Aviation Transactions, involving defendant RILAs that related to aircraft leased to Qantas, were entered into in 2003. RILA OJG, RILA OJH and RILA OJJ were involved in those Aviation Transactions. By amendment made to the Defence with the leave of the Court after the start of the hearing, KV Aviation conceded that the preference shares of those three defendant RILAs are not redeemable at the option of the relevant RILA. KV Aviation further conceded that it could never receive a dividend in its capacity as the holder of ordinary shares in RILA OJG, RILA OJH and RILA OJJ. It conceded that the holders of preference shares in those three defendant RILAs are entitled to preferred dividends equal to all profits made by the RILAs on any account. The Redemption Issue is therefore not controversial in respect of those three defendant RILAs. In the Originating Process, HNA Irish seeks a declaration that, on the proper construction of the constitutions of RILA OJG, RILA OJH and RILA OJJ, the preference shares that are owned by HNA Irish may not be redeemed by the relevant RILA. It now appears to be common ground that such a declaration should be made.

85 Two Aviation Transactions relating to aircraft leased to SilkAir were entered into in 2006. Two defendant RILAs, namely RILA 9V-SLE and RILA 9V-SLD, were involved. RILA 9V-SLE is the fourth defendant RILA in respect of which the Redemption Issue is not controversial. In the Defence, as amended with leave, KV Aviation conceded that the right to redeem preference shares in accordance with the constitution of RILA 9V-SLE may only be exercised with the consent of the holder of the preference shares. In the Originating Process, HNA Irish seeks a declaration that, on the proper construction of the constitution of RILA 9V-SLE, the preference shares that are owned by HNA Irish may only be redeemed with the consent of HNA Irish. It now appears to be common ground that such a declaration should be made.

86 Aviation Transactions relating to aircraft leased to Jetstar Airways Pty Limited (Jetstar), a subsidiary of Qantas, were entered into in 2004, 2005 and 2006. That tranche of Aviation transactions involved 15 defendant RILAs. In order of their date of entry into their respective Aviation Transactions, those defendant RILAs are RILA VQZ, RILA VQY, RILA VQX, RILA VQW, RILA VQV, RILA VQU, RILA VQT, RILA VQS, RILA VQR, RILA VQQ, RILA VQP, RILA VQJ, RILA VQI, RILA VQH and RILA VQG.

87 Two Aviation Transactions relating to aircraft leased to Emirates were entered into in 2004. Two defendant RILAs, namely RILA MSN 163 and RILA MSN 185, were involved.

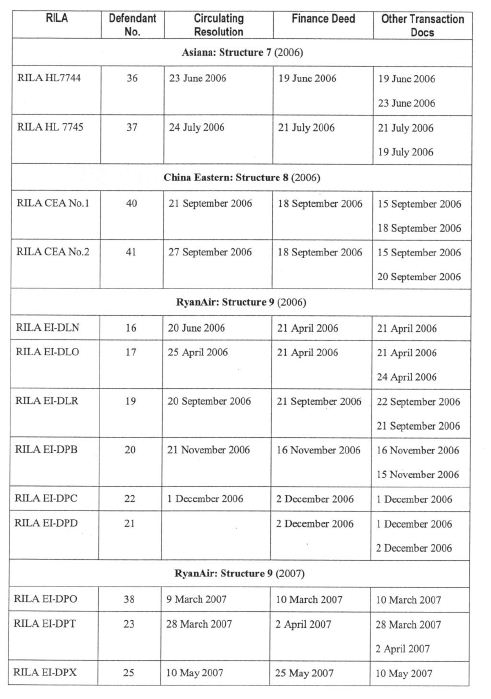

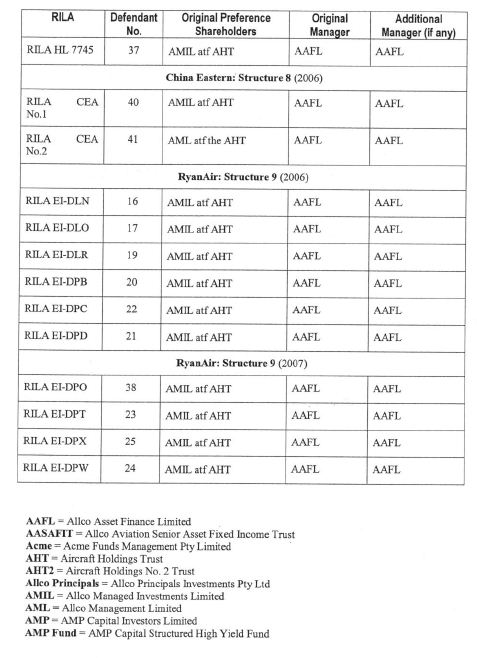

88 Two Aviation Transactions relating to aircraft leased to Singapore Airlines and EVA Airways were entered into in 2005 and 2006. Each involved a defendant RILA, being RILA 9V-SFG and RILA 32643. Two Aviation Transactions relating to aircraft leased to Asiana were entered into in 2006. Each involved a defendant RILA, being RILA HL 7744 and RILA HL 7745. Two Aviation Transactions involving aircraft leased to China Eastern were entered into in 2006. Each involved a defendant RILA, being RILA CEA No. 1 and RILA CEA No. 2.

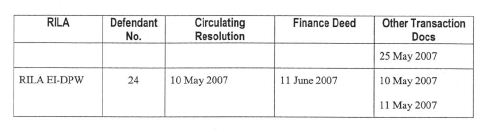

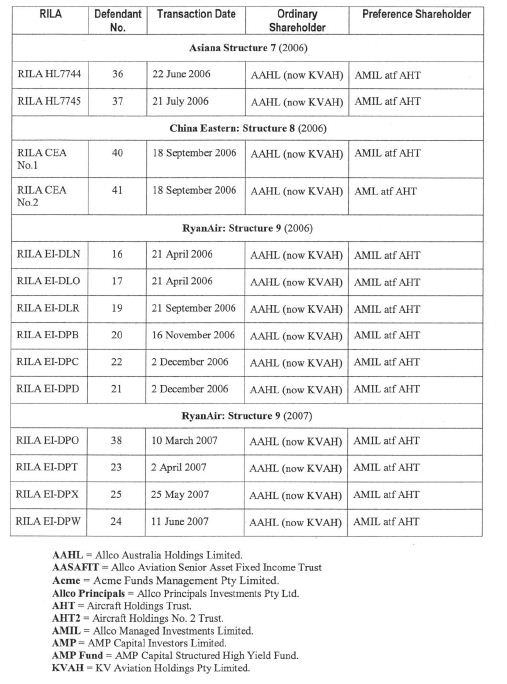

89 Ten Aviation Transactions involving aircraft leased to RyanAir were entered into in 2006 and 2007. Each of those Aviation Transactions involved a defendant RILA, being RILA EI-DLN, RILA EI-DLO, RILA EI-DLR, RILA EI-DPB, RILA EI-DPC, RILA EI-DPD, RILA EI-DPO, RILA EI-DPT, RILA EI-DPX and RILA EI-DPW.

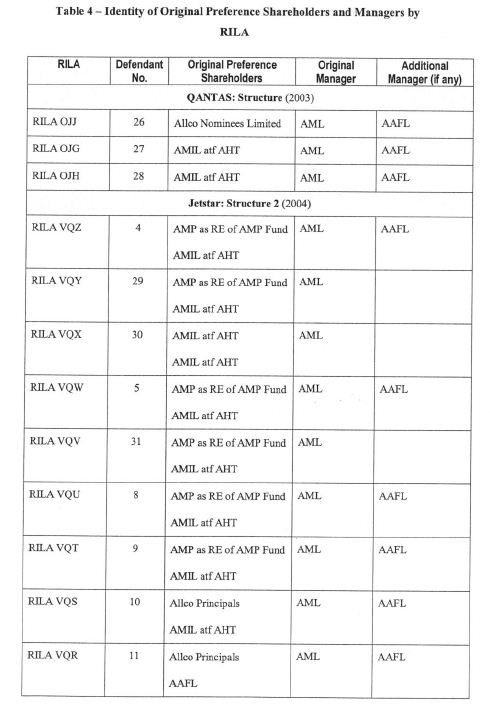

90 Set out in Appendix 3 to these reasons are tables, which were in evidence in the proceeding, that are said to show the dates of the various Transaction Documents in the Aviation Transactions involving defendant RILAs, the initial shareholding in each defendant RILA, and the current shareholding in each defendant RILA. It is apparent from that material that Aircraft Holdings Trust, through its trustee (initially Allco Nominees Limited (Allco Nominees) and subsequently Allco Managed Investments), frequently made the junior loan in Aviation Transactions involving defendant RILAs. For example, in the Aviation Transaction involving RILA OJJ, RILA OJJ issued 100 preference shares to Aircraft Holdings Trust, which were expressed to entitle Aircraft Holdings Trust to receive 100 per cent of the net income of the RILA.

91 Thus, third party investors in Aviation Transactions often made their investments by acquiring units in Aircraft Holdings Trust. Those investors thereby acquired indirect interests in the preference shares of the relevant RILAs. On 28 June 2007, the Allco Aviation Fund (see paragraph [21] above) was established to acquire certain of the interests in Aviation Transactions held by Aircraft Holdings Trust. The Allco Aviation Fund was to have two sub-funds, being the Senior Asset Fund (or Senior Secured Aircraft Investments Trust) and a newly established Junior Asset Fund, later renamed High Return Aircraft Investments Trust. The Junior Asset Fund was intended to hold junior loans and, less frequently, mezzanine loans, together with a portion of the preference shares issued in connection with Aviation Transactions. Allco Managed Investments was the trustee of the Allco Aviation Fund, as well as being trustee of the Senior Secured Aircraft Investment Trust and the High Return Aircraft Investments Trust. The Allco Aviation Fund was initially seeded with investments in 15 Aviation Transactions.

92 The holdings of preference shares vary somewhat as between the 38 defendant RILAs, and it is appropriate to say something about those holdings. In the unique case of RILA 9V-SLE, the Bank of Scotland is a 12.5 per cent preference shareholder. However, as I have indicated, there is no dispute as to the preference shares in RILA 9V-SLE.

93 There are seven defendant RILAs whose preference shareholding consists of a single class with a single member, namely HNA Irish. Those RILAs are RILA VQX, RILA VQJ, RILA VQI, RILA VQH, RILA HL 7744, RILA HL 7745, and RILA EI-DPO.

94 There are multiple preference shareholders in the remaining 30 defendant RILAs, including RILA OJG, RILA OJH and RILA OJJ. Each of those 30 RILAs has other preference shareholders owning the same class of preference share owned by HNA Irish. In the case of 20 of the defendant RILAs, that single class with multiple members accounts for the entire preference shareholding. However, ten of the 30 RILAs have a preference shareholding split across two classes. In those cases, the defendant RILAs also issued A class preference shares to Mezzanine Financiers. Those ten RILAs are RILA VQZ, RILA VQW, RILA VQU, RILA VQT, RILA VQS, RILA VQR, RILA VQQ, RILA VQP, RILA VQY and RILA VQV. I have said something about A class preference shares and B class preference shares above, in describing the constitution of RILA VQZ.

95 In the case of 27 of the 30 defendant RILAs with multiple preference shareholders, the owner of preference shares in the same class as those owned by HNA Irish is Allco Managed Investments, as trustee of the Allco Aviation Fund. I shall say something below, in considering the Misrepresentation Issues, about the various investors in the Allco Aviation Fund and its predecessor. In the case of the remaining three RILAs, namely RILA 32643, RILA CEA No. 1 and RILA CEA No. 2, Citic Allco Investments Limited (Citic) acquired preference shares as part of a selldown process in December 2007.