FEDERAL COURT OF AUSTRALIA

Commissioner of Taxation v Interhealth Energies Pty Ltd as Trustee of the Interhealth Superannuation Fund [2012] FCA 120

IN THE FEDERAL COURT OF AUSTRALIA | |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT DECLARES THAT:

(a) the respondent breached the enforceable undertaking under the Superannuation Industry Supervision Act 1993 (Cth) (SIS Act) dated 28 February 2008 in that it failed by 30 May 2008:

(i) to collect a distribution payable to the Interhealth Superannuation Fund (ISF) by the Greenhaven Unit Trust by that date;

(ii) failed to pay in full to Mr Patrick Shaun Wilson, a member of the ISF the retirement benefit then due to him; and

(iii) failed to report the making of payment in full by the date specified in the undertaking.

(b) the respondent likewise failed to perform the actions referred to in paragraphs (a)(i) and (a)(ii) by 19 June 2008 and failed to report by 25 June 2008 its carrying out of those actions;

(c) the amount of Mr Patrick Shaun Wilson’s residual interest in the ISF as at 20 June 2008 was, after allowance for the payment to him by the respondent of the sum of $42,824.15 by cheque sent to him that day and earlier payments made to him or on his behalf by the respondent, $249,457.35;

(d) a reasonable time by which the respondent should have paid in full the amount of Mr Patrick Shaun Wilson’s residual interest in the ISF was 30 September 2008;

(e) the amount which the respondent should have paid to Mr Patrick Shaun Wilson by 30 September 2008 so as to pay in full his residual interest in the ISF was $249,457.35.

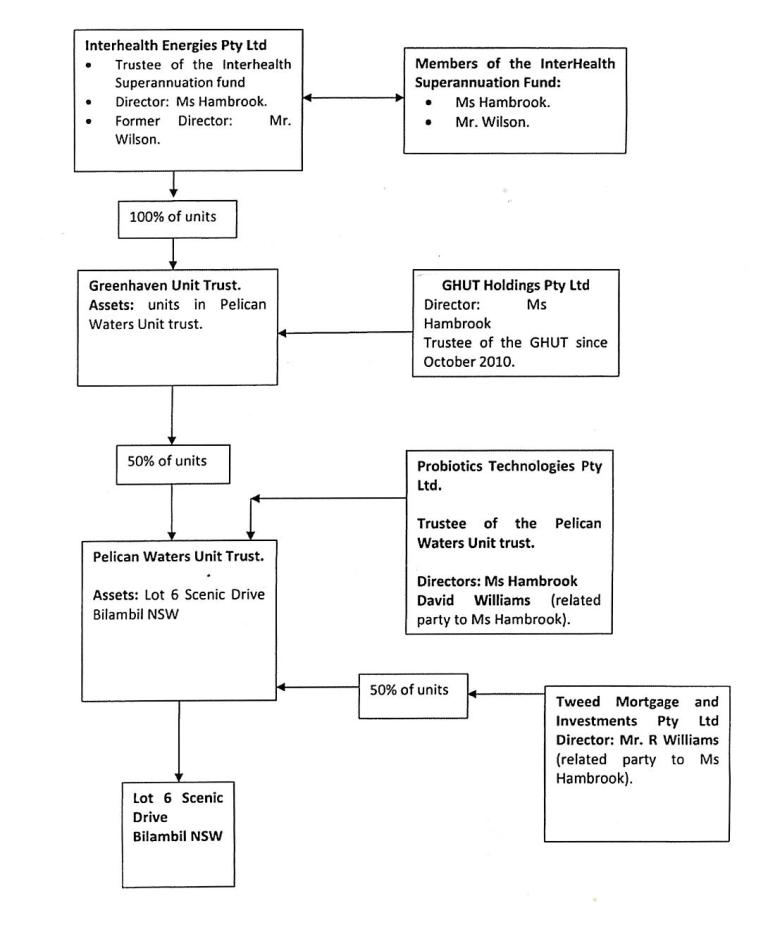

THE COURT ORDERS THAT:

1. The respondent pay to Mr Patrick Shaun Wilson the sum of $249,457.35.

2. Mr Patrick Shaun Wilson may enforce the order for payment in the same manner as a judgment obtained by him against the respondent for the sum of $249,457.35.

3. This proceeding be adjourned to a date to be fixed for further consideration as to what further or other orders, if any, having regard to the reasons for judgment published today, should be made, including whether interest can or should be awarded in respect of the sum ordered to be paid and, if so, for what period and at what rate, whether the respondent should be restrained from dealing with the ISF and, if so, on what terms and whether any charge over the ISF should be ordered.

4. All questions as to costs be reserved to a date fixed for further consideration of ancillary orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011

QUEENSLAND DISTRICT REGISTRY | |

GENERAL DIVISION | QUD 221 of 2010 |

BETWEEN: | COMMISSIONER OF TAXATION Applicant |

AND: | INTERHEALTH ENERGIES PTY LTD ACN 003 104 505 AS TRUSTEE OF THE INTERHEALTH SUPERANNUATION FUND First Respondent PATRICK SHAUN WILSON First Intervener IVOR WORRELL AND JASON BETTLES IN THEIR CAPACITY AS JOINT AND SEVERAL TRUSTEES OF THE BANKRUPT ESTATE OF PATRICK SHAUN WILSON Second Intervener |

JUDGE: | LOGAN J |

DATE: | 22 FEBRUARY 2012 |

PLACE: | BRISBANE |

REASONS FOR JUDGMENT

1 The respondent, Interhealth Energies Pty Ltd (Interhealth) is the trustee of a fund held pursuant to superannuation trust deed and settled on 23 June 1993. The trust as constituted by that deed was comprehensively varied by a further deed on 25 November 1994 so as to align the trust with the requirements of the Superannuation Industry Supervision Act 1993 (Cth) (SIS Act). The trust is known as the Interhealth Superannuation Fund (the ISF). At all material times there were two members of this superannuation fund, Ms Joanna Hambrook (Ms Hambrook) and Mr Patrick Shaun Wilson (Mr Wilson). Ms Hambrook and Mr Wilson were once involved with each other both commercially and, via a de facto relationship, personally. The ISF was established in the course of each of these relationships. Each of these relationships ceased some time ago in what seems on the evidence to have been acrimonious circumstances. Ms Hambrook and Mr Wilson each gave evidence before me. To my direct observation, their antipathy one for the other was palpable, mutual and enduring. The wider origins of this proceeding lie in the cessation of these relationships, commercial and personal, and in that antipathy.

2 The more immediate origin of this proceeding is an undertaking given to the Commissioner of Taxation (the Commissioner) by Interhealth, by its by then remaining director, Ms Hambrook, on 28 February 2008 pursuant to s 262A of the SIS Act. That provision allows a “Regulator” to accept a written undertaking given by a person in connection with a matter in relation to which that “Regulator” has a function or power under the SIS Act. The Commissioner is Regulator, for the purpose of the application of the SIS Act to Self Managed Superannuation Funds (SMSF). The Commissioner alleges that this undertaking has been breached by Interhealth. He seeks orders that the undertaking be enforced.

3 Section 17A of the SIS Act defines what constitutes a SMSF for the purposes of that Act. Materially, such a fund must have fewer than five members and where, as here, its trustee is a body corporate, each director of the body corporate must be a member of the fund. Ms Hambrook remains a director of Interhealth. Mr Wilson ceased to be a director of that company on 7 October 2004. The effect of Mr Wilson’s cessation of holding office as a director was that the Fund ceased to comply with a regulatory provision of the SIS Act namely, with the definition of self managed superannuation fund in s 17A. That, in turn, meant that the Fund could only meet the “compliance test” in s 42A of the SIS Act so as to constitute a complying superannuation fund if the Commissioner, as “Regulator”, having regard to the matters specified in s 42A(5)(b) of the SIS Act, “thinks that a notice should nonetheless be given stating that the entity is a complying superannuation fund in relation to the year of income concerned”.

4 Status as a complying superannuation fund has an important consequence for income tax purposes. A fund which has that status is subject to concessional rates of taxation whereas one which is not is taxed at the top marginal tax rate: Division 285 of the Income Tax Assessment Act 1997 (Cth) and, for the income years prior to the 2007/2008 year, Pt IX of the Income Tax Assessment Act 1936 (Cth).

5 It might perhaps be thought that there is a degree of tension between consigning to the Commissioner the function of “Regulator” with the power, relevantly, of granting a form of absolution to a fund from otherwise adverse fiscal consequences and his separate function as the Commonwealth’s chief revenue collection officer. Equally though, given the benign taxation regime enjoyed by complying superannuation funds, consigning that duality of function to the Commissioner might be considered a means of ensuring fiscal integrity. It is neither necessary nor appropriate further to delve into, much less to resolve, matters of public administration practice. What it is necessary to record is that the giving of an undertaking under s 262A of the SIS Act is relevant to the exercise of the discretion under s 42A(5)(b) of that Act to give a notice that a fund is a complying fund in relation to a year of income.

6 Interhealth resists the making of any enforcement order at all, contending that there has been no breach of the undertaking and that, as a matter of discretion, relief should be refused on the basis that the Commissioner as Regulator has not, so it is contended, adopted an “even handed” approach to his administration of the SIS Act and has, by the institution of this proceeding, favoured Mr Wilson over Ms Hambrook. As will be apparent from these reasons for judgment, the latter submission is but symptomatic of a comprehensive failure by Ms Hambrook to understand and to cause Interhealth to discharge the duties that fell on it as the trustee of a SMSF both under the general law and under the SIS Act. All that the Commissioner has done on the evidence is in good faith to carry out his duties as Regulator under the SIS Act. Interhealth also advances alternative submissions, summarised below, that relief in the terms proposed by the Commissioner should not be granted.

7 Because of the direct interest which he had as a member in the outcome of the proceeding I granted leave to Mr Wilson to make submissions as to the form of orders which the Court might make in the event that I found that the undertaking had been breached and that an enforcement order ought to be made. Later, as a result of the supervening bankruptcy of Mr Wilson, this grant of leave was extended to his trustee in bankruptcy.

8 By the undertaking, Interhealth undertook to the Commissioner that it would do the following:

(a) collect payments of unpaid distributions owed to the ISF by the Greenhaven Unit Trust by 30 May 2008;

(b) pay to Mr Wilson his full superannuation entitlement by 30 May 2008; and

(c) provide evidence of the above to the Commissioner by 6 June 2008.

9 Given the denial by Interhealth of any breach of the undertaking, the primary issue in this proceeding is whether it has breached one or more of the requirements of the undertaking. A related issue is whether particular legal expenses incurred by Interhealth since the 2006 financial year are expenses properly incurred in the administration of the ISF. A further issue is whether Mr Wilson was entitled to benefits under the ISF deed as a lump sum in the 2006 year.

10 To understand how the undertaking came to be given in the terms set out above, whether it has been breached and how issues as to the incurring of legal expenses and as to Mr Wilson’s entitlement in 2006 arise requires the making of detailed findings as to background facts. Before turning to this task it gives helpful context to make some reference to the duties of the trustee of a superannuation fund.

11 Used in a popular sense, the term “superannuation fund” means a retirement fund, especially one to which an employee and usually an employer make contributions during the period of employment so as to provide benefits after retirement (Macquarie Dictionary, Online Edition; Oxford English Dictionary, Online Edition). Just to refer to a “superannuation fund” can, by a conflation of a number of different concepts, be apt to distract from appreciating what, truly, are the legal entities involved, the legal relationships created and the trust property concerned. What in law occurs is the assumption of the office of trustee by a legal entity, in this case a body corporate, Interhealth, in respect of property settled on and accumulated by that trustee subject to particular trust obligations set out in a deed of trust. Strictly, the term “superannuation fund” refers not to the trustee but only to the property settled upon and accumulated by the trustee and held in terms of the trust. Further, a “superannuation fund” is not a legal entity, nor is “the trust” (although for revenue law purposes it is artificially treated as such). The only legal entity involved is the trustee.

12 Understanding this highlights that the duties which attend any trustee of property attend the office of trustee of a fund held on trust for the purposes of the provision of superannuation benefits. The price of benign taxation treatment for the assessable income of the fund is the assumption by its trustee of additional obligations, such as those for which the SIS Act provides. These supplement, rather than relieve a trustee from complying with, the general duties of a trustee. In the case of inconsistency, the SIS Act obligations prevail over whatever is otherwise specified in the governing trust deed.

13 A trustee’s most fundamental duty is to comply with the terms of the trust. In the case of Interhealth its obligation is to comply with the terms of the deed governing the ISF, as varied. In discharging that duty, the trustee must act as would an ordinary, prudent man of business managing his own affairs: Re Speight (1882) 22 Ch D 727 at 739-740. As that deed is varied, Interhealth’s obligation as trustee includes compliance with the SIS Act. A trustee is also subject to a range of fiduciary duties. These include a duty of impartiality. A trustee also has a duty to invest money held on trust. As varied, the deed governing the ISF confers a broad investment power on the trustee but expressly qualifies it in two ways (cl 9.1). The exercise of the investment power is subject to the provisions of the SIS Act. It is also subject to the proviso that trust investments are made on an arm’s length basis. More generally, the exercise of that power is subject to the prudential management duty mentioned earlier. Subject to those express qualifications, that general requirement will dictate that the investment power be exercised in a way that is in the best financial interests of the beneficiaries of the trust: Cowan v Scargill [1985] Ch 270 at 286-287.

14 The trust property which has constituted the ISF has comprised liquid funds and, materially, the whole of the units in a unit trust known as the Greenhaven Unit Trust (GHUT) and an amount receivable from that trust by the ISF by way of unpaid distributions. Since October 2010 the trustee of the GHUT has been GHUT Holdings Pty Ltd of which Ms Hambrook is the sole director. Before then, Probiotic Technologies Pty Ltd (Probiotic) was the trustee of the GHUT. The worth, if any, of the units in the GHUT is controversial. Resolving that controversy requires an understanding of a complicated cascade of trust interests which ultimately find expression in an interest in land at Lot 6 Scenic Drive Bilambil in New South Wales (the Bilambil property). The nature of that cascade of trust interests, the entities which are trustees of the trusts concerned and who are presently the directors of those entities are best described diagrammatically, as set out below:

15 The Bilambil property was purchased in 2000 for the sum of $210,000 with the aid of funds advanced by Interhealth from the ISF to Probiotic, the then trustee of the GHUT, which also then acted and continues to act as the trustee of the Pelican Waters Unit Trust (PWUT). The PWUT was constituted in April 2000, inferentially in conjunction with the decision to acquire the Bilambil property. At the time of the purchase in 2000, the directors of Probiotic were Ms Hambrook and Mr Wilson. They were then on good terms both personally and commercially. In effecting the purchase of the Bilambil property as trustee Probiotic acted via Mr Wilson. On its acquisition, and for reasons which remain unclear, Mr Wilson chose to cause the Bilambil property to be registered in his name rather than that of Probiotic. Ms Hambrook was not then aware that this property had been so registered. The Bilambil property was though shown in the accounts of the PWUT as an asset of that trust on and from its acquisition.

16 A number of critical events occurred in 2004.

17 In March 2004 Probiotic sold 50% of the units in the PWUT to Tweed Mortgage and Investments Pty Ltd (TMI) for the sum of $200,000. TMI was then and remains a company controlled by Mr Ronald Williams and his American resident brother, Dr David Williams. TMI controlled Lot 2 at Scenic Drive. The proximity of that property to the Bilambil property and perceived future development benefits were a motivating factor for all parties in this PWUT unit sale transaction. The other attraction for Probiotic was that it converted part of the PWUT property namely, the Bilambil property, into liquid funds without having to dispose of that land. At the time of the transaction, the value of the Bilambil property had been appraised by a local real estate agency as being between $380,000 and $420,000. Probiotic struck its sale price by reference to this appraisal.

18 The directors of Probiotic as at the time of the sale of the units to TMI were Ms Hambrook and Mr Wilson. Contrary to Ms Hambrook’s evidence, Mr Wilson denies participating in a meeting of directors of Probiotic on 25 March 2004 at which the sale of the units to TMI was approved. That a sale did occur as related in the preceding paragraph is undoubted.

19 Having regard to her later actions concerning the ISF and where Mr Wilson is concerned, I do not doubt that Ms Hambrook is well capable of expedient action in matters touching on her personal interest, even in circumstances which, viewed objectively, are redolent of a conflict of interest. She is an astute, determined woman, convinced of the righteousness of her actions with respect to the ISF and not hesitant to express that conviction (her affidavits are riddled with editorial self justifications). I am wary of acting on her uncorroborated evidence alone. That acknowledged, much bad blood, manifested by much litigation in which they have been on opposing sides, has passed between her and Mr Wilson (or related entities) since March 2004. Even after entering into a comprehensive deed of compromise, of which more shortly, he has demonstrated a degree of recalcitrance in carrying that agreement into effect both in letter and in spirit. However, the efficacy of the releases in that deed as against him are binding and fully apt definitively to eliminate any such residual recalcitrance. In fairness to him, that recalcitrance has been grounded in his perception that, via Ms Hambrook’s decision, Interhealth has continued unreasonably to pay out his superannuation benefit entitlement in full. Mr Wilson’s recollection of events in March 2004 and thereafter was, I thought, coloured by his recalling them through the prism of his antipathy for Ms Hambrook and that perception.

20 Dr David Williams related in his evidence the elaborate dealings, in which he and Mr Wilson were intimately involved, from 2000 to 2004, directed towards the bringing to fruition of a proposal which would have seen a development not only of Lot 2 and Lot 6 (Bilambil property) but also the intermediate block, Lot 4 Scenic Drive. It is not necessary in order to resolve this case to relate those dealings. His account, which I accept, corroborates Ms Hambrook’s recollection of Mr Wilson’s involvement in the disposal of the units. Further, the events and related antagonism and litigation, prompted by the discovery by Ms Hambrook and Dr Williams that Lot 6 was registered in Mr Wilson’s name, did not occur until later in 2004. I accept Dr Williams’ account even though he and his brother Ronald presently share with Ms Hambrook a community of interest in relation to the Bilambil property. The benefits which might potentially be found in a proposal which would have seen the co-operative development of contiguous Lots disparately held make his account inherently likely. I find that, in March 2004, Mr Wilson was not ignorant of the sale of units in the PWUT to TMI. He, along with Ms Hambrook, resolved that Probiotic should sell 50% of the PWUT units to TMI.

21 A consequence of TMI’s taking up units in the PWUT was that Dr David Williams joined Ms Hambrook and Mr Wilson on the board of Probiotic. Dr Williams became a director on 7 August 2004. That same month, as he recalls it, he and Ms Hambrook discovered that Lot 6 was not registered in the name of Probiotic but rather Mr Wilson. Ms Hambrook places her discovery of in whose name the Bilambil property was registered as having occurred in “August/September 2004”. It seems inherently likely that the occasion for this discovery was their receipt in August of a valuation of the Bilambil property which had been commissioned with a view to Probiotic selling it. That sale was proposed because by then it had become clear that a conjoint development of that property and Lots 2 and 4 Scenic Drive was not possible.

22 Shortly after Ms Hambrook and Dr Williams discovered in whose name the Bilambil property was registered they confronted Mr Wilson on that subject. He claimed that it was a mistake and that he would cause it to be corrected. Notwithstanding repeated requests of him made later in August, in September and in October 2004, he failed to do this. The present acrimony that exists between Mr Wilson and Ms Hambrook dates at least from this time so far as their business relations are concerned but has been much exacerbated by later events. Inferentially, whatever personal relationship they had ceased not later than this time also. It may be that the latter had ceased earlier but this is not clear on the evidence and not necessary in any event to determine for the purpose of resolving these proceedings.

23 An immediate consequence of Mr Wilson’s failure to cause the transfer of the Bilambil property to Probiotic was that Ms Hambrook and Dr Williams caused him to be removed as a director of Probiotic in late September 2004. That left the two of them as directors of that company. In November 2004 they caused Probiotic to institute proceedings in number 6294/04 against Mr Wilson in the Supreme Court of New South Wales seeking orders that he cause the Bilambil property to be registered in the name of that company as trustee of the PWUT. That New South Wales proceeding was later cross vested to the Supreme Court of Queensland.

24 As already noted, Mr Wilson ceased in October 2004 to be a director of Interhealth. Ms Hambrook attributed this cessation just to a need to replace Interhealth as trustee of the ISF because that company was also carrying on business in its own right. That is something a trustee of a SMSF should not do. There is certainly contemporaneous correspondence proposing a change of trustee of the ISF for just such a reason and with a replacement by another company of which Mr Wilson and Ms Hambrook would be directors. That proposal never came to pass. Further and in any event, such a reason does not explain why Mr Wilson was removed as a director of Interhealth while that company remained charged with trust and related statutory responsibilities in respect of the ISF. It is no coincidence that this removal occurred at a time of ever increasing acrimony between Ms Hambrook and Mr Wilson and also Dr Williams and Mr Wilson. She was then in a position to cause his removal as a director of Interhealth and did so. Interhealth’s shareholders were as to 99.9%, Mr Ron Williams and, as to 0.1%, A.H.A. Group Holdings Pty Ltd (Table 3, WMS Report). On the evidence, Mr Ron Williams and Dr David Williams act in concert in matters touching on Interhealth, Probiotic and the Bilambil property.

25 The effect of the removal of Mr Wilson from the boards of both Interhealth and Probiotic is that he was thereafter excluded from decision-making in respect of the ISF itself and its underlying assets. Between them, Ms Hambrook, Dr David Williams and Mr Ron Williams controlled all of the entities concerned with the ISF and its underlying assets.

26 Separate Queensland Supreme Court de facto relationship property related litigation, matter number BS482/05 was instituted by Mr Wilson in February 2005 against Ms Hambrook, Interhealth, Probiotic, TMI and many other corporate defendants.

27 In the proceeding cross vested to the Queensland Supreme Court, Atkinson J came in March 2006 to make an order, to the making of which Mr Wilson consented, providing for his transferring the Bilambil property to Probiotic. Also in March 2006. and not later than 3 March, Mr Wilson applied to Interhealth for his member’s benefit on the basis of age and retirement from employment. Those two events are inherently unlikely to have been coincidental actions on the part of Mr Wilson and I find that they were not.

28 Mr Wilson did not effect the transfer of the Bilambil property to Probiotic until September 2006. Nor for that matter, did Interhealth forthwith pay the member’s benefit for which Mr Wilson had applied. On 30 August 2006, Mr Wilson lodged a caveat over the Bilambil property. The basis cited for that caveat was a claimed entitlement on constructive trust arising from his former de facto relationship with Ms Hambrook. This later lapsed but was replaced by a further caveat lodged by relatives of Mr Wilson (his brother in law, Mr Stephen Fitzgerald and his wife and Mr Wilson’s sister, Mrs Frances Wilson-Fitzgerald).

29 On 23 August 2007 Mr Wilson instituted proceedings in this Court in matter QUD 271 of 2007 against Ms Hambrook and eventually also Interhealth (in substitution for an original respondent company, seemingly misidentified as the trustee of the ISF) by which he sought to compel payment of his claimed ISF entitlements. None had by then been paid to him by Interhealth. The Commissioner as “Regulator” was once but is no longer also a respondent party to that proceeding. He has though been granted leave to appear as amicus curiae in that proceeding.

30 On 12 November 2007 a comprehensive deed of compromise was made to which Ms Hambrook, Mr Wilson, Interhealth, the relatives of Mr Wilson who had lodged the substitute caveat in respect of the Bilambil property and Probiotic were each party. One of the recitals to that deed was an acceptance by Interhealth that Mr Wilson had retired and was the vested owner of what were described as “the entitlements” and that “subject to the quantum of the entitlements being determined, the entitlements can be paid to [him]”. Those entitlements were elsewhere (cl 1.1(p)) defined as “Wilson’s Superannuation Entitlements” as “the vested superannuation entitlements payable to Wilson as a consequence of Wilson’s retirement and his request that his vested superannuation entitlements be paid to him”. Under the deed (cl 5) Mr Wilson released Ms Hambrook, Interhealth and Probiotic from all claims in respect of the Bilambil property. Like comprehensive releases were given to these persons under the deed by Mr Wilson’s relatives. The deed further provided (cl 3.1) for the making of an interim distribution of Mr Wilson’s ISF superannuation entitlement by way of payment by Interhealth of:

(a) the sum of $150,000 directly to him; and

(b) (implicitly under the deed by Mr Wilson’s direction) the amount of a costs order made in favour of Probiotic against Mr Wilson which had become the subject of a Magistrates Court judgment against him together with related enforcement expenses.

31 The deed was also cast on the basis that Interhealth had made application to the Commissioner for the acceptance of an Enforceable Undertaking. What did not occur, prior to the making of interim payments by Interhealth, notwithstanding a qualification with respect to interim payment found in cl 3.1 and cl 3.2 of the deed of compromise, was the appointment of custodians for the purpose undertaking realisations as provided for by a deed of appointment of custodian, a draft of which was attached to the deed of compromise. Nothing was made of the absence of this occurrence in submissions by either party to the present proceeding, presumably on the basis that any such qualifying requirement had been waived by the conduct of all concerned and overtaken by the obligation assumed by Interhealth under the Enforceable Undertaking.

32 The deed of compromise also provided for the taking of accounts and for valuations of the assets of the ISF.

33 As to the taking of accounts and valuations, on 23 November 2007 Mr B McCracken, a registered valuer of Colliers International valued the Bilambil property as at 13 November 2007 at $800,000. This valuation formed part of a report dated 26 November 2007 given to Interhealth by a chartered accountant, Mr I Otto of WMS Legal Support Pty Ltd (the WMS Report), which assessed the value of the net assets of the ISF at $974,822 as at 14 November 2007. The WMS Report is comprehensive. It has been made against the background of Mr Otto’s having been briefed with the deed of compromise and details of the cascade of trust and other interests which underpin and intrude upon the superannuation fund’s holding of 100% of the units in the GHUT. I accept the opinions as to value contained in the WMS Report and in that of Colliers International, which underpins part of the WMS Report.

34 As disclosed by the WMS Report and as valued by him, the current assets of the ISF as at 14 November 2007 comprised:

(a) Funds in a bank account at the Macquarie Bank - $40,253.00;

(b) Funds held in a term deposit at that same bank - $534,952.00;

(c) A distribution to the ISF receivable from the GHUT - $122,766; and

(d) Amounts receivable from other debtors - $611.

The non-current asset of the ISF comprised the units in the GHUT. Apart from minor tax liabilities, the only then current liabilities of the ISF were the professional fees associated with the preparation of the Colliers valuation and the WMS report. There were no non-current liabilities. No liability in respect of legal expenses was shown in respect of the ISF.

35 In terms of underlying trusts within what I have described as the cascade, the value of the 50% holding by the trustee of the GHUT of the units in the PWUT was given as $337,443 in the WMS Report.

36 A feature of the WMS Report is that its author, Mr Otto, has expressly taken into account when assessing the worth of units in the GHUT a liability to which its trustee was said in its accounts to be subject in respect of legal expenses. Mr Otto proceeded on the basis that they related to the then current litigation in this Court (Para 86 of WMS Report). It may be, as the Commissioner submitted, that some at least of those costs came to be recovered via the payment made by direction as an interim payment under the deed of compromise. It is not necessary to determine that. It is enough to note that the impact of legal costs was taken into account when assessing the worth of what underpinned the assets of the ISF.

37 The accounts of the ISF for the years ended 30 June 2005, 2006, 2007 and 2008 are in evidence (the 2005 accounts also show the comparative 2004 position). For these four financial years, the position so far as the net assets of the ISF and the amounts of Mr Wilson’s benefit may be summarised in the following table, subject to the necessary qualification that the 2008 accounts are qualified by the auditors and cast on the basis of ongoing litigation such that there was an inability to pay member benefits. Inferentially, it seems likely that this qualification had its origins in instructions provided by Interhealth’s sole director, Ms Hambrook. In any event, I find it impossible to reconcile the qualification with the comprehensive releases contained in the deed of compromise. The 2008 accounts also record a financial year in which member and other payments, related below, were made from the ISF:

Year | Liability for Accrued Member’s Benefit – allocated to members’ account | Withdrawal benefit for Mr Wilson |

2004 | $823,418.17 | $431,747.71 |

2005 | $847,164.77 | $443,739.51 |

2006 | $876,481.57 | $455,440.56 |

2007 | $892,321.67 | $442,067.50 |

2008 | $46,832.02 | ($30.83) |

38 On 28 February 2008 the Enforceable Undertaking was executed by Ms Hambrook on behalf of Interhealth and then returned to the Commissioner. Its form had been settled in earlier exchanges of correspondence between those acting on behalf of Interhealth and Ms Hambrook and the Australian Government Solicitor (AGS) who acted for the Commissioner. Apart from the obligations entailed in the undertaking, the following recitals should be noted:

1.9 Trust distributions payable to the Fund from the GHUT have not been paid to the Fund since the income year ended 30 June 2003.

1.10 The balance of the unpaid distributions was $134,933.82.

1.11 Patrick Wilson’s date of birth is 26 July 1945. He is 62. The preservation age for people born before 1 July 1960 is 55 years. Patrick has reached his preservation age and has met a condition of release to access his benefits from the Fund.

39 The interim distribution for which the deed of compromise provided was not paid until 28 March 2008. On that date:

(a) $150,000 was paid to Mr Wilson; and

(b) $28,342.72 was paid by direction in respect of the judgment for legal costs payable by him.

Though the deed of compromise provided no authority for it, payment of a like total amount ($178,342.72) was also made, on Ms Hambrook’s behalf, from the ISF by Interhealth at the same time. It is described in an application later made to the Commissioner for variation of the Enforceable Undertaking as a “rollover” (inferentially, a payment into another superannuation fund on Ms Hambrook’s behalf). The payment was made after agreement between the solicitors then acting for Mr Wilson and those then acting for Ms Hambrook. It was no part of the Commissioner’s submissions that this distribution to Ms Hambrook was not authorised by the terms of the deed governing the ISF. I do not therefore consider that question.

40 Also paid out of the Fund in the 2008 financial year was, according to its audited accounts for that year, the sum of $184,456.26. These were said to be referable to the professional fees expenses entailed in litigation, particularly the earlier proceeding in this Court, to which Interhealth as trustee and Mr Wilson had been parties.

41 On 30 April 2008 Ms Hambrook, in her capacity as sole remaining director, resolved that Interhealth, as trustee of the ISF, should purchase further units in the GHUT for the sum of $121,071. To that end she signed on behalf of Interhealth that day an application for a further 79,898 units in the GHUT at a price of $1.5153. The issuing of these units was treated by Interhealth as discharging the obligation of the trustee of the GHUT, then Probiotic, to pay the then outstanding distributions to Interhealth. The expression used was “in lieu of unpaid trust distributions owed to it in the accounts of the Greenhaven Unit Trust”. The amount of those unpaid distributions as at that date was $121,071. Also on 30 April 2008, at a meeting of directors chaired by Ms Hambrook in which the other director of Probiotic participated, the issuing of the further units in the GHUT on the terms specified in Interhealth’s application was approved.

42 On 25 May 2008 Ms Hambrook caused Interhealth, via Cleary and Bentley (who describe themselves as “taxation specialists”), to seek a variation of the Enforceable Undertaking in terms of a document signed by her on 23 May 2008. On 17 June 2008 the Commissioner, via the AGS, advised Interhealth’s solicitors, Rodgers Barnes & Green, that this proposal was unacceptable. Also in that correspondence the AGS advised that the Commissioner would agree to a variation of that undertaking whereby Mr Wilson’s entitlement was paid out in full to him by close of business on 19 June 2008 with evidence of that payment being given to the Commissioner by close of business on 25 June 2008. Confirmation that Interhealth and Ms Hambrook “will accept and act in accordance with this revised requirement” was sought by the AGS in this correspondence. Neither by its solicitors nor otherwise did Interhealth directly respond to this request for confirmation. It did cause its solicitors in turn to cause Cleary & Bentley to forward by email on 20 June 2008 to the AGS a document which sought to “outline the difficulties that [Interhealth as trustee of the ISF] has encountered in its attempt to comply with its responsibilities”. Elaborate though that explanation is, a noteworthy feature of it is an absence of reference to the deed of compromise agreed in November 2007 and, especially, to the comprehensive releases for which that deed provided. That is a manifest absence of candour in a document intended to be relied upon by officers of the Commonwealth. The instructions for the preparation and despatch of the document must necessarily have come from Ms Hambrook, for Interhealth had no other officer. Interhealth never executed a revised Enforceable Undertaking incorporating the extensions the commissioner signified were acceptable. It did though act as if it had.

43 On 20 June 2008 Ms Hambrook signed and sent a letter to Mr Wilson enclosing an Interhealth cheque for $42,824.15. In that letter she described that amount as “Mr Wilson’s entitlement to 49.54% of the balance of the Interhealth Superannuation Fund”.

44 The preceding day, 19 June 2008, Ms Hambrook had by email and on behalf of Interhealth commissioned Mr Otto of WMS Legal Support to prepare, as a matter of urgency, a revaluation of the units in the PWUT. It is necessary to set out in full the instructions which she gave for that valuation.

Please revalue the units in the Pelican Waters Unit Trust that you have previously valued in the valuation dated 26 November 2008. The valuation should be on the basis of an urgent liquidation or a fire sale as the units have encumbrances on them and because of these encumbrances are not saleable. The encumbrances include:

1. Probiotic Technologies Pty Ltd (“Probiotics”) is included in the action in the Supreme Court of Queensland (BS 482/05);

2. Wilson has made statements that he reserves his right to take further action to claim an interest in Lot 6 Scenic Drive Bilambil Heights NSW;

3. Wilson has claimed that the sale of 50% of the units on issue to Tweed Mortgage and Investments Pty Ltd (“TMI”) was not legitimate;

4. refusal by Wilson to release from all claims, actions, suits and demands which Wilson considers he has now or may have in the future arising out of or in connection with Land, the units in PWUT, Probiotics and TMI and accounting profits derived from any and all dispositions of real and personal property by Probiotics and TMI.

Any potential purchaser would not be prepared to expose him or herself to the threat of being involved in litigation or the value of their investment being eroded by such litigation.

King regards

Joanne

45 A significant feature of these instructions is the absence of reference in them to the deed of compromise and to the releases for which it provided. Indeed, item 4 in the instructions is directly at odds with those releases. Another significant feature of those instructions is the absence of any reference by Ms Hambrook to legal costs for which Interhealth as trustee was responsible, being in excess of those set out in the WMS report. By virtue of her being a party to the deed of compromise and her office in Interhealth. Ms Hambrook then knew or ought to have known the position in respect of each of those subjects. Yet another feature of the instructions is the reference to “fire sale” in circumstances, where more than three months of realisation inaction had passed since Interhealth gave its undertaking to the Commissioner.

46 Mr Otto provided a supplementary report (the supplementary WMS report) that same day, indeed that same afternoon, for Ms Hambrook’s email was not sent until 2:45 pm on 19 June 2008. Based on the contentious picture painted by Ms Hambrook in her instructions, Mr Otto opined, “if an independent trustee sought to realise an immediate value for the units in PWUT from an arm’s length buyer, it is likely to be $NIL or an immaterial amount.” Significantly, he added this qualification, “Should all of the above issues be resolved in a timely and economical manner, then the values in my valuation report dated 26 November 2007 could remain as an indicator of the ‘fair market value’”.

47 On 25 June 2008, via a letter sent directly to the Commissioner by Cleary & Bentley, Interhealth advised that Mr Wilson’s member benefits had been paid in full.

48 On 3 July 2008, prompted by the forwarding to that office of a letter from Mr Wilson’s solicitors advising of his receipt of the sum $42,824.15, the AGS sought, via a letter directed to its solicitors, advice from Interhealth as to whether this payment was intended to be final payment of Mr Wilson’s superannuation entitlements and how the amount of this payment was to be reconciled with the figures presented in superannuation fund returns in respect of the ISF lodged with the Commissioner. No reply was made to this letter by or on behalf of Interhealth.

49 The AGS directed a further letter to Interhealth’s solicitors, Rodgers Barnes & Green, on 11 February 2009 which in substance repeated the inquiries made by the earlier letter of 3 July 2008. This time Interhealth did respond. By a letter dated 18 February 2009 its solicitors stated that Mr Wilson’s full entitlements had been paid out to him via the two payments made on 28 March 2008 and the further payment in June of $42,824.15. The latter was said to be in accordance with the revised date agreed to by the Commissioner via the AGS letter of 17 June 2008. The explanation provided in this letter for how and why these sums were paid to Mr Wilson and why they represented his full entitlement in substance repeated the explanation given in the explanation attached to the email which Cleary & Bentley sent to the AGS on 20 June 2008 and in the instructions which Ms Hambrook gave to Mr Otto on 19 June 2008. Even though the deed of compromise had, on its face been prepared by Rodgers Barnes & Green and even though that firm had sent a copy of that deed to the Commissioner under cover of a letter to the AGS dated 12 November 2007 and then quoted extensively from it, particularly the releases, in a further letter to the AGS dated 19 November 2007 enclosing for the Commissioner’s consideration of acceptance a proposed enforceable undertaking to be given by Interhealth, there is no reference at all to that deed of compromise or those releases in Rodgers Barnes & Green’s letter of 18 February 2009. Materially, what is stated is this:

You will also see that, in the accounts, provision of $70,000 has been made for legal fees and expenses that the trustee of the fund was advised is likely to be the minimum that will be incurred in the trustee defending, on behalf of the fund, Mr Wilson’s claim in the Federal Court that the fund is a non-complying fund. The trustee obtained legal advice on making that provision and was advised that, in order for the law trust obligation of fairness between members to be satisfied, it was necessary that that provision be made because, if Mr Wilson’s benefit was paid without taking account of it, the financial burden of the trustee defending the claim would fall solely on the member’s account of the remaining member.

It is necessary for the trustee of the fund, in carrying out its fiduciary duties, to defend the Federal Court proceedings.

This letter was sent on Interhealth’s instructions, which necessarily were those of Ms Hambrook.

50 This explanation was not regarded as satisfactory by the Commissioner and eventually resulted in the present proceeding.

51 Against this background, was the Enforceable Undertaking breached as alleged?

Were payments of unpaid distributions owed to the ISF by the Greenhaven Unit Trust collected by 30 May 2008?

52 Interhealth submits that, “the [GHUT] did not have the liquidity to pay the unpaid trust distributions … It was, therefore, necessary for the unpaid trust distributions to be applied as consideration for the issue to [Interhealth] of further units in the [GHUT], thus extinguishing the liability”. On this basis it submits that it has complied with the collection obligation in respect of unpaid GHUT distributions.

53 Interhealth has done no such thing.

54 In April 2008, Interhealth, as trustee of the ISF, already owned all of the issued units in the GHUT. The asset of the GHUT was its 50% holding of the issued units in the PWUT. In turn, the worth of units in the PWUT was whatever was able to be realised for the Bilambil property after allowing for expenses of sale. The acquisition of further units in the GHUT could not possibly have increased the value of the assets of the ISF. If the GHUT had paid the amount receivable, the ISF would still have owned all of the units in the GHUT. Far from increasing the worth of the ISF, the transaction on 30 April 2008 diminished that value. In return for extinguishing the liability which Probiotic as trustee of the GHUT had to pay then unpaid distributions to it as trustee of the ISF, Interhealth received worthless units. Worthless because before and after the transaction Interhealth held 100% of the issued units in the GHUT. Interhealth did not, as it had undertaken collect the unpaid distributions. It deliberately extinguished a subsisting obligation to pay them. A consequence of the collection of the unpaid distributions would have been that the liability was discharged, but nothing has been collected here. This was not an arm’s length transaction.

55 There is no doubt that Ms Hambrook caused Interhealth to acquire the additional units in the GHUT for the ISF. The imperative that fell on Interhealth was the result of an undertaking which she had signed on its behalf as a sequel to an obligation assumed in a deed of compromise to which she was a party personally and to which Mr Wilson, his relatives, Interhealth and Probiotic were also parties. Ms Hambrook was also one of the directors of Probiotic. There is nothing on the evidence to suggest that the initiative for the transaction of 30 April 2008 came from either Dr David Williams or Mr Ron Williams. There is a clear inference that it was Ms Hambrook who procured the participation of Probiotic in the transaction. The transaction of 30 April was one manifestly against the interests of the ISF and manifestly in the interests of Probiotic in its capacity as trustee of the GHUT. To record that is to highlight the serious conflict of interest which the transaction presented so far as Ms Hambrook’s involvement was concerned, given the positions which she held. That is to say nothing of the inherent conflict associated with Interhealth, when under Ms Hambrook’s control from October 2004, having failed earlier to collect the sum receivable from time to time from Probiotic, the then trustee of the GHUT, which sum always represented a not insubstantial proportion of the total assets of the ISF.

56 As recorded in the WMS Report in November 2007, the total amount of the unpaid distributions was $122,766. According to the recital in the Enforceable Undertaking signed on 28 February 2008 that amount was $134,933.82. The documents relative to the 30 April 2008 transaction record it as $121,071. The differences were not explained on the evidence but it does seem that the balance unpaid fluctuated over time. For all that, care does appear to have been taken with the 30 April transaction to ensure that all that then owed was extinguished.

57 I find that Ms Hambrook knowingly caused Interhealth to fail to collect unpaid distributions in the amount of $121,071 from Probiotic as trustee of the GHUT. In so doing, she caused that company to act completely contrary to how an “ordinary, prudent man of business managing his own affairs” would act and thus caused Interhealth to commit a breach of the obligations to which it was subject as trustee of the ISF. She also caused Interhealth to breach this requirement of the Enforceable Undertaking. Her actions were wilful, cynical and self interested.

58 The collection requirement in the Enforceable Undertaking was not to be read in isolation from the other principal requirement of the undertaking, which was to pay out in full Mr Wilson’s member entitlements by 30 May 2008. For this, liquid funds were needed, not worthless units. Ms Hambrook took no measures to cause Interhealth to raise these by causing the winding up of the cascade of trusts which underpinned the ISF. Her rationale for this was persistence, so she saw it, in obstruction by Mr Wilson. Yet he, like her and all other potentially interested parties, was bound by comprehensive releases in the deed of compromise. She had no warrant at that stage for not causing Interhealth as trustee to begin a process of realisation. In the event that a difficulty were encountered after that process had been initiated, it would then have been open to her to cause Interhealth to seek the Commissioner’s acceptance of whatever further extension or modification of the undertaking was then reasonably necessary.

59 I make these findings in relation to the causing of a breach of trust because it was a deliberate feature of Interhealth’s case that Ms Hambrook had done nothing wrong. Both having regard to the submissions made on behalf of Interhealth and by direct observation of her demeanour when giving evidence and throughout the trial, Ms Hambrook remains unrepentant, convinced of the righteousness of her actions and resentful of the involvement of the Commissioner, especially including his institution of this proceeding.

Was Mr Wilson paid his full superannuation entitlement by 30 May 2008?

60 The discretionary power conferred on the Commissioner as “Regulator” by s 262A of the SIS Act is to accept a written undertaking. The only written undertaking given by Interhealth and accepted by the Commissioner required payment of Mr Wilson’s full superannuation entitlement by 30 May 2008. Even assuming that Mr Wilson’s entitlement was as Interhealth came to calculate and pay it in June that year, the amount of that entitlement was not paid before 30 May 2008. The Commissioner did signify a disposition to extend the time for payment but that never became the subject of a written undertaking which he accepted. That the undertaking must be in writing has an obvious evidentiary importance but Interhealth did not even give such an undertaking orally. It did though act as if it had given a written undertaking incorporating the extension which the Commissioner stated would be acceptable.

61 In these circumstances, the question is really one of whether, the only accepted written undertaking having been breached in that payment was not made by 30 May 2008, should any relief be ordered? If Interhealth did pay Mr Wilson his full entitlement by 19 June 2008, the proposed extended date, or even by 20 June 2008, the date on which the letter enclosing the cheque for the alleged balance was sent, there would be no occasion for the granting of any relief.

62 According to the financial statements of the ISF as at 30 June 2006:

(a) the assets of the fund amounted in total to $873,123.58 of which:

(i) cash at bank was $516,705.76;

(ii) the distribution receivable from the GHUT was then $134,933.82; and

(iii) unit in managed funds, presumably the GHUT were valued at $221,484.00;

(b) the net assets available to pay benefits comprised $876,481.57.

As can be seen, the ISF then had minimal liabilities and almost 60% of its assets comprised liquid funds. Further, the value of the GHUT units was, on the evidence, a conservative one, being referable to an historic rather than the then likely contemporary value of the Bilambil property. I make that observation because, by 13 November 2007, the date of the Colliers valuation, that property was valued at $800,000. As noted above, Mr Wilson’s then withdrawal benefit was valued at $455,440.56. Also as noted above, it was in that financial year that Mr Wilson sought the payment from the ISF of his retirement benefit. There were then sufficient liquid funds in the ISF to pay that benefit.

63 Under the ISF deed (cl 41) a member’s retirement benefit was to be paid to a member who, having reached “Retiring Age” had ceased employment. The term “Retiring Age” was defined by the deed (cl 5.2) to mean either 65 years of age or such other age greater than 55 years of age as the trustee and employer agree on as being that member’s retiring age. (The trustee and employer were seemingly each Interhealth, although, after Mr Wilson’s expulsion as a removal as a director of Interhealth in October 2004, it is not clear how he fell even within the expanded definition of “Employee” in cl 5.2 of the ISF deed. This was not pursued by the parties who each proceeded on the basis that Mr Wilson remained an employee as at the date of his application for his retirement benefit. I also proceed on that basis.) Mr Wilson was born on 26 July 1945, which means he had not attained 65 years of age in the year ended 30 June 2006. He was though then over 55 years of age. In the period between when the retirement benefit was sought in March 2006 and November 2007 when the deed of compromise was signed there does not appear to have been any controversy that Mr Wilson had ceased employment and had reached what was to be regarded for the purposes of the ISF as his retiring age. That he was eligible to be paid his retirement benefit was acknowledged in the deed of compromise and, for that matter, in the recitals to the Enforceable Undertaking. He was eligible to be paid his full entitlement to a lump sum in 2006 following his application.

64 The ISF deed does not specify by when after application a member’s retirement benefit is to be paid. Neither, expressly, do either the SIS Act or the Superannuation Industry (Supervision) Regulations 1994 (SIS Regulations) made there under contain such a specification. As a matter of construction and inferentially, the trustee of that fund was obliged to pay that benefit as soon as reasonably practical. Section 52(2)(f) of the SIS Act required Interhealth as a superannuation fund trustee to formulate and give effect to an investment strategy which had regard to expected cash flow requirements, liquidity, and the ability of the fund to discharge existing and prospective liabilities. So much would have fallen for a trustee of such a fund to do in any event under general trust law. Necessarily such a strategy could not be immutable and would have to take into account, inter alios, the age profile of fund members and, ever increasingly on and from their turning 55 years of age, the contingency that some may decide to retire before age 65. The liquid reserves held as at 30 June 2006 appear to me to have been consistent with a looming contingency that the ISF might be called upon to pay a retirement benefit.

65 As at March 2006 and until the making of the deed of compromise, there had been no resolution of the litigation in the Supreme Court of Queensland. It was not until some six months later that Probiotic was able to achieve the registration of the Bilambil property in its name. Even then, controversy at Mr Wilson’s initiative attended that property. Further, there is some evidence, the accuracy of which in the acrimonious and litigious circumstances seems inherently likely, that in 2005 Mr Wilson had agitated with the ISF bankers, Macquarie Bank so as to prevent that bank from allowing drawings on the ISF account. There is also evidence that that bank came nonetheless to permit a translation of some of the monies held into an interest bearing term deposit. There is no reference in the WMS Report to any ongoing restriction of access to the ISF accounts at the Macquarie Bank. It seems inherently likely, given that instructions for the preparation of that report originated from Ms Hambrook, that, if there were then any such restriction, reference would have been made by Mr Otto to it in that report. I infer that, whatever was the nature of the restriction in 2005, it had long before then ceased.

66 The amount of Mr Wilson’s accrued member’s benefit was dependent to an extent upon the worth of the GHUT units and the worth of these was ultimately referable to the worth of the Bilambil property. Under the ISF deed, asset valuation was a matter for the trustee to determine (cl 12.2(a)). That task had to be undertaken honestly.

67 The Commissioner focussed his submission as to the amount which ought to have been paid to Mr Wilson by reference to the accounts of the ISF as at 30 June 2006. It is true that these disclose the financial position reasonably proximate to when Mr Wilson applied for his benefits. However, the worth of the GHUT component of that financial position was then uncertain. It may be accepted, as was the case advanced via Ms Hambrook’s evidence and submissions made on behalf of Interhealth, that the then litigation impacted upon the ability of Interhealth to pay in full Mr Wilson’s retirement benefit in the year ended 30 June 2006. It did not though prevent a portion of that benefit referable to liquid funds then held being paid in that financial year. This was not done.

68 No payment at all having been made to him from the ISF by 2007, it is by no means impossible to see how Mr Wilson was entitled to take steps to seek to compel Interhealth to make payment to him. That is so even though the litigation which he instituted in this Court in 2007 was, to say the least, unorthodox. Again though, the litigation did not, before the deed of compromise, prompt any interim payment of a retirement benefit to Mr Wilson even though, in the 2007 financial year, ample liquid funds remained in the ISF. I accept though that the array of litigation to which Interhealth was a party did, prior to the deed of compromise, provide a reasonable basis for why Mr Wilson’s benefit was not paid in full prior to the deed of compromise.

69 I have already referred to the interim payments to or on behalf of Mr Wilson which followed the deed of compromise. The final payment in June 2008 was struck by Ms Hambrook’s reference to a valuation which placed the worth of the Bilambil property and thus the trust units dependent upon it for value at nil. The instructions upon which that valuation was based were hers and hers alone. They painted a dramatic picture of ongoing serious disputation. They made no reference whatsoever to the deed of compromise and to the comprehensive releases it contained or that Mr Wilson remained bound by the deed of compromise. In that omission Mrs Hambrook was not merely reckless, she was deliberately misleading. Giving instructions of that nature provided a convenient, for her, and expeditious way of causing Interhealth to meet what she understood to be the extended time which the Commissioner had allowed in respect of the Enforceable Undertaking. It is true that Mr Otto had been briefed in November 2007 with a copy of the deed of compromise but nothing had occurred thereafter which warranted the dramatic nature of the instructions which Ms Hambrook chose to give him by her email. In causing Interhealth to adopt that valuation and to calculate what was said to be the amount of the instalment necessary to pay in full the amount of Mr Wilson’s retirement benefit Ms Hambrook did not act honestly. The valuation which she adopted was, to her knowledge, based on a false premise. That is no reflection on Mr Otto, who was careful to qualify the supplementary WMS report, only on Ms Hambrook.

70 This provides one reason for my conclusion that Interhealth did not then pay in full by 19 June 2008 Mr Wilson’s retirement benefit.

71 Apart from the valuation which Ms Hambrook procured from Mr Otto on a false premise, the other reason why the final payment to Mr Wilson was no more than $42,824.15 was because of legal expenses which Interhealth had incurred and paid by 1 June 2008, purportedly in the course of administering the ISF.

72 Mr Wilkinson, a chartered accountant, stated in evidence that, based on his examination of the accounts of the ISF, that fund had cash, bank securities and term deposits of $671,482 as at 30 June 2007. He further related that, by 1 June 2008, these had been reduced to approximately $140,000 prior to the making of the payment of $42,824.15 to Mr Wilson. Apart from the interim member benefit payments made to Ms Hambrook (rollover payment) and to or on behalf of Mr Wilson, the other reduction was, according to Mr Wilkinson (and so I find) referable to legal and other (presumably trust administration) expenses of approximately $176,000. This figure is broadly consistent with the figure of $184,456 for such expenses in respect of the 2008 financial year calculated by another accountant, Mr Lavell in auditing the ISF accounts.

73 As at 30 June 2007 and 14 November 2007 the total liabilities, current and otherwise, of the ISF were just $645 (WMS report, para 34, summary of the position of the ISF). Mr Wilkinson did not explain in his evidence how or why, by reference to the accounts of the ISF for the preceding financial year, still current as at 14 November 2007, legal costs of $176,000 had been incurred and paid by Interhealth as trustee of the ISF in the period between 14 November 2007 and 1 June 2008. Neither did Ms Hambrook. Nor was there an explanation offered as to how legal and other expenses of $176,000 could have been properly incurred by Interhealth as trustee of the ISF when, in the WMS report (para 86), the sum of $31,268, disclosed in the accounts of the GHUT (para 74), was described as referable to fees owing to Rogers Barnes and Green and barristers costs (which Mr Otto took to relate to the then current proceeding in this Court). It was not up to the Commissioner to resolve or explain such anomalies. It was Interhealth which pointed to legal and other expenses allegedly properly incurred in the administration of the ISF as one reason why payment in full was effected by the payment to Mr Wilson of the sum of $42,824.15 in June 2008.

74 As to this expenditure on legal and other expenses in the balance of the 2008 financial year, it was submitted on behalf of Interhealth that, “the logic of ignoring [it] is beyond comprehension”. It may readily be accepted that the expenditure should not be ignored; but nor should its propriety. As to the extant litigation:

(a) legal costs in respect of the NSW Supreme Court proceeding to secure the removal of the caveat in respect of the Bilambil property and the registration of Probiotic as proprietor were for Probiotic as trustee of the PWUT to incur and pay;

(b) the like may be said of the proceeding in the Supreme Court of Queensland in which Atkinson J came to make an order on 23 March 2006;

(c) the other Queensland Supreme Court litigation related to the former de facto relationship and initiated by Mr Wilson involved multiple defendants apart from Interhealth and included TMI and Probiotic;

(d) the 2007 litigation in the Federal Court to force the payment of Mr Wilson’s retirement benefit was referable to a failure of Interhealth to pay him anything at all for more than a year after he had applied for his benefit and in circumstances where there was no reasonable basis for not making at least an interim payment to him having regard to the assets of the ISF which comprised bank funds; and

(e) the expense incurred in respect of the obtaining of the supplementary WMS report was dishonestly incurred.

75 The rationale put forward for the payment of legal costs associated with the vindication and defence of Probiotic’s ownership as trustee of the PWUT, of the Bilambil property, was that the value of this property underpinned the worth of the ISF holding of GHUT trust units. This is true but it remains the case that Interhealth did not own that property. Further, even viewed indirectly, Interhealth as trustee of the ISF was not the only entity interested in the preservation of the Bilambil property as an asset of the PWUT. At all material times, TMI held 50% of the units in the PWUT. Paying legal costs on behalf of Probiotic advanced TMI’s interests just as much as, indirectly, there was any advancement of the interests of the ISF. There was no arrangement in place, as evidenced by the lack of reference to any such asset in the accounts of the ISF for the 2004 to 2008 financial years, whereby Probiotic incurred an indebtedness to the ISF to the extent that costs on its behalf were met from the ISF. The absence of any such arrangement was not the act of “an ordinary, prudent man of business managing his own affairs”. Neither under the general law of trusts nor, if there be any relevant distinction, the covenants taken by s 52(2)(b) of the SIS Act to form part of the trust charter for the ISF was the incurring of these legal and other expenses on behalf of Probiotic in such a manner warranted. That is to say nothing of the absence of ISF taking a charge over the assets of Probiotic to secure any indebtedness in respect of costs paid on its behalf.

76 That Interhealth allowed the liquid assets of the ISF to be diminished in this fashion is yet a further manifestation of the conflict of interest inherent in the roles that Ms Hambrook undertook on and from October 2004.

77 It is not possible on the evidence to apportion with any precision or confidence how much of the legal expenses incurred by Interhealth were attributable to its defence of proceedings to which it was a party as trustee of the ISF. An apportionment of sorts is contained in a letter sent to the AGS by Rodgers Barnes and Green on 10 December 2007 in the lead up to the course of the negotiations which led to the Enforceable Undertaking. It is there said that the GHUT had been “forced to pay the expenses of the [ISF]” because Mr Wilson had caused the Macquarie Bank to “freeze” the accounts of the ISF. It may be that this part of the costs is the sum of $31,268 said to have been incurred by the GHUT in relation to the litigation in this Court instituted by Mr Wilson to the end of compelling the payment of his retirement benefit (WMS Report, para 86). The letter of 10 December does not mention such a sum but rather apportions the costs to be:

(a) “expenses relating to the [Bilambil property]” of $74,210.40, less costs to be paid by Mr Wilson of $24,630.69 [leaving a net amount of $49,579.71]; and

(b) “costs incurred in relation to the dispute between Fund and Mr Wilson” of $92,520,50.

78 There is no detailing of what is embraced by “the dispute”. It seems inherently unlikely, given the lesser, other sum referred to in the WMS Report and that the litigation in this Court had only been instituted in 2007 and not proceeded to trial that all or perhaps even any of the $92,520.50 related to a proceeding in this Court. The total of costs specified in the letter of 10 December 2007 is $142,100.21.

79 Some of the ISF administration expenses are attributable to the obtaining for the WMS Report and that of Colliers International. These total $12,000 (WMS Report, para 97). On any view, these were necessary expenses in order to strike a value for the ISF and thus members’ benefits in the wake of the deed of compromise. They were reasonable administration expenses. Whatever the supplementary WMS Report cost, it was not a reasonable expense, having regard to the origin of the false premise which underpinned it.

80 It was Interhealth which had access to all records necessary to offer a detailed explanation as to how and why all of the sum of $176,000 paid in respect of legal expenses were expenses properly incurred in the administration of the ISF. It has not done this. Further, progressive accumulation of legal expenses of the order which came to be paid ought to have given a prudent trustee, well before this total was reached, substantial pause for thought not only about the absence of any security or indebtedness from Probiotic for them but whether, having regard to the overall assets of the ISF, costs should continue to be incurred. All in all, it is difficult to escape the conclusion (and I conclude) that, under Ms Hambrook’s control, Interhealth used the ISF in an uncritical way as a bank from which to fund legal expenses, most of which were not directly concerned with the administration of the ISF and, to the extent to which they were capable of being regarded as indirectly concerned, Interhealth incurred those expenses in an imprudent way.

81 Doing the best that I can on the evidence to hand, I am prepared to accept, at the risk, I suspect, of generosity, that the sum of $176,000 included the sum of $31,268 said to have been incurred by the GHUT on behalf of the ISF. To the extent that this is generous, I make allowance in it for any costs which might be regarded as referable to a proportion of costs referable to Interhealth as trustee of the ISF being a party to the Queensland Supreme Court litigation and in taking advice as to the deed of compromise and the undertaking for which it provided. I also make allowance for the sum of $12,000 referable to the obtaining of the WMS Report. This yields a total of $43,268. Of the sum of $176,000, I find therefore that the resultant balance of $132,732 did not constitute expenses prudently incurred in the administration of the ISF.

Reporting

82 Interhealth did cause Cleary and Bentley to make a report as to payment in full on 25 June 2008, but the instructions given to that firm for the purpose of making that report were necessarily predicated upon the making of a payment referable in amount to Interhealth’s failure to administer the ISF according to law. It is a corollary of my conclusion that he was not then paid in full that the report of 25 June was not truly as to a full payment. Also, on any view, Interhealth did not report a payment in full by the date specified in the Enforceable Undertaking. I am satisfied that this requirement of the Enforceable Undertaking was breached.

Relief

83 Having regard to the WMS Report, the deed of compromise and to the qualification which Mr Otto made in the supplementary WMS Report and adapting the assessed value of the ISF in the WMS Report to take account of findings which I have made, the worth of the ISF as at 19 June 2008, if Interhealth had managed that trust fund as with “the same degree of care, skill and diligence as an ordinary prudent person would exercise in dealing with property of another for whom the person felt morally bound to provide” ought to have been:

(a) Units GHUT - $288,939.00;

(b) Distribution receivable - $121,071

(c) Macquarie Bank and Term deposit - $174,553.56 (see note below)

Total: $584,563.00

Note: Item (c) is calculated as follows. The total of the Macquarie Bank and the Term Deposit amounts, as per the WMS Report, Table 15, equals $575,205. From this figure I have deducted the two payments of $178,342.72 made by Interhealth to Mr Wilson and Ms Hambrook, which total $356,685.44. This yields a net amount in funds held in a bank of $218,519.56. From this I have further deducted the sum of $12,698 shown on the WMS Report as an ISF liability (which includes the costs of that report) and the sum of $31,268 in respect of such legal expenses as I am prepared to find were properly incurred in the administration of the ISF, a total of $43,966. This yields (or should have left) a net amount at the bank of $174,553.56.

84 On this basis, I find that the residual amount of Mr Wilson’s interest in the ISF as at 19 June 2008, had the ISF been managed as required by law, was $292,281.50 (half of $584,563.00). Of this, he received $42,824.15 under cover of the letter of 20 June 2008. That was not payment in full of his entitlement. Based on the value of the ISF as at 19 June 2008 and Mr Wilson’s interest in that fund, the sum of $249,457.35 remains outstanding. However, even had that fund been properly administered, its then cash reserves would have been but $174,553.56. Time for realisation of assets was needed and some cash reserves needed to be held in reserve having regard to Ms Hambrook’s continued membership of the ISF and lawful and prudent administration expenses. Half of what should have been the cash reserves is $87,276.78. At least another $30,000 could then prudently have been paid, in my opinion with whatever proved to be the final balance following after an orderly realisation of the non-liquid assets of the ISF.

85 Even though Interhealth did not pay in full by 19 June the balance of Mr Wilson’s then interest in the ISF it does not automatically follow that compensation should be calculated by reference to that balance.

86 Theoretically, the final balance may well have been more or lower than $249,457.35 (less the further $30,000 to which I have referred), depending upon the fate of realisations. Interhealth took no steps from the signification of the Commissioner’s acceptance of the Enforceable Undertaking to effect those realisations. The realisation period to take into account should not run from 19 June but from this earlier date. In the Colliers International Report, (p 16), the following is stated in relation to the then state of the market:

Currently, there are limited vacant lots listed for sale in the suburb. Of these, agents are reporting strong buyer enquiry. Smaller lots located in steeper sites that have higher house construction costs, or are in what is considered to be a secondary location are achieving between $150,000 and $200,000. Lots priced over $200,000 are generally for level lots.

The value of $800,000 assigned to the Bilambil property in this report was assigned having regard to prevailing market conditions.

87 Having regard to the evidence concerning the then market, it seems inherently likely that the Bilambil property would have been able to be realised for its market value on or before September 2008, had Ms Hambrook promptly initiated a realisation of the non-liquid assets of the ISF. In making that finding I take into account the comprehensive releases contained in the deed of compromise. That being so, it is more likely than not that the remaining value of Mr Wilson’s interest in the ISF, in order for him to be paid out in full, would have then still been $249,457.35 (or $219,457.35, had a further $30,000 been paid to him in June 2008).

88 It was put on behalf of Interhealth that s 262A(4) of the SIS Act did not permit the making of any compensatory order based on what ought to have comprised the balance of Mr Wilson’s interest in the ISF had the ISF been administered according to law. The decision of the trustee, Interhealth as to the value of the assets of the ISF was, it was submitted, one for the exercise of its discretion alone, the discretion had been exercised and the result was that the payment to Mr Wilson of $42,824.15 finalised his interest in that superannuation fund. I reject this submission.

89 Section 262A(4) provides:

If the Court is satisfied that the person has breached a term of the undertaking, the Court may make all or any of the following orders:

(a) an order directing the person to comply with that term of the undertaking;

(b) an order directing the person to pay to the Commonwealth an amount up to the amount of any financial benefit that the person has obtained directly or indirectly and that is reasonably attributable to the breach;

(c) any order that the Court considers appropriate directing the person to compensate any other person who has suffered loss or damage as a result of the breach;

(d) any other order that the Court considers appropriate.

90 The jurisdiction conferred on the Court by s 262A(4) of the SIS Act depends on the proper construction of s 262A(4) of the SIS Act having regard to the language of that sub-section, context in which it appears and the purpose and scope both of the provision and of the SIS Act: Alexander v Perpetual Trustees WA Limited (2004) 216 CLR 109 at [26] per Gleeson CJ, Gummow and Hayne JJ. In respect of those superannuation funds to which the SIS Act has application, the section supplements the general law of trusts. It permits recourse to an exercise of judicial power by this Court in circumstances where the exercise of executive power by the Commissioner as Regulator in accepting an undertaking has proved insufficient to ensure that a particular superannuation fund is administered according to law. It is not just a remedial provision; its scope and purpose are designed to ensure the integrity of the administration of superannuation funds governed by the SIS Act. The fiscal incentive offered for such funds to be brought under that Act and to be complying funds is considerable, reflecting the public policy purpose of encouraging provision for superannuation evident by that fiscal incentive. For all of these reasons, the approach to construing nature of the jurisdiction which s 262A(4) confers should not be narrow. The language of s 262A(4)(c) and s 262A(4)(d) is commensurately broad.

91 The undertaking which Interhealth gave was one in the course of the administration of the ISF. Interhealth was not excused from complying with the general and statutory duties of the trustee of the ISF when it came to complying with that undertaking. The payment of Mr Wilson’s entitlements in full required payment of his entitlements in the ISF administered according to law. Interhealth did not so administer that fund. Section 262A(4) confers ample jurisdiction on the Court to order the compensation of Mr Wilson for the breaches of the Enforceable Undertaking which have occurred.

92 Another submission advanced on behalf of Interhealth was that Mr Wilson had not really retired in 2006 and therefore no obligation to pay him then had arisen. This was a novel contention, unevidenced at the time when Mr Wilson applied for his retirement benefit in 2006 and contrary to the acknowledgments in both the deed of compromise and the Enforceable Undertaking itself. In these circumstances, it was not the submission of a person exercising “the same degree of care, skill and diligence as an ordinary prudent person would exercise in dealing with property of another for whom the person felt morally bound to provide”. That it was made at all is but another indicator of Ms Hambrook’s lack of insight into her responsibilities with respect to the ISF. I reject the submission. For that reason, I do not explore the alternative, canvassed in submissions, of what would have been Mr Wilson’s position in any event had he merely been terminated prior to retirement age (cl 45 of the ISF deed and reg 6.18(1) and reg 6.01 of the SIS Regulations refer).

93 The Commissioner sought the payment of a sum to Mr Wilson calculated on the basis that he ought to have been paid in full his retirement benefit in 2006. For the reasons given, I do not accept that this is how the matter should be approached. Mr Wilson was eligible in 2006 for a lump sum payment, which ought to have been paid as soon as reasonably practical thereafter. However, the undertaking was given in 2008 and required payment by a specified time in 2008. It is just that, had the ISF been administered according to law before that time, the final payment resulting in payment in full of entitlements should have been more than it was said then by Interhealth to be.

94 The Commissioner did not seek any order that the amount of compensation carry any interest, even simple interest since 19 June 2008. It follows from the conclusions I have reached that Mr Wilson has been held out of the payment in full of his entitlements by the acts of Interhealth. Even had the ISF been properly administered, its cash reserves would not have been sufficient to pay in full by 19 June 2008 all that it was owed. Much more than $42,824.15 ought then to have been able to be paid; I have opined at least a further $30,000. The balance in order to achieve payment in full ought to have been able to have been paid by the end of September 2008.