FEDERAL COURT OF AUSTRALIA

Telstra Corporation Limited v Phone Directories Company Pty Ltd

[2011] FCA 1463

IN THE FEDERAL COURT OF AUSTRALIA |

|

DATE OF ORDER: |

|

WHERE MADE: |

THE COURT ORDERS THAT:

1. Pursuant to r 40.02(b) of the Federal Court Rules 2011, the Applicants pay the Respondents’ costs by way of a gross costs sum order, for the period from 16 June 2009 to 8 February 2010 inclusive, in the sum of $326,931.75.

2. Costs of the interlocutory application be reserved.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

VICTORIA DISTRICT REGISTRY |

|

GENERAL DIVISION |

VID 276 of 2007 |

BETWEEN: |

TELSTRA CORPORATION LIMITED (ACN 051 775 556) First Applicant SENSIS PTY LTD (ACN 007 423 913) Second Applicant

|

AND: |

PHONE DIRECTORIES COMPANY PTY LTD (ACN 059 776 091) First Respondent AUSTRALIAN LOCAL DIRECTORIES PTY LTD (ACN 078 856 318) Second Respondent ADAM HARGRAVES Third Respondent GLENN HARGRAVES Fourth Respondent DANIEL STOTEN Fifth Respondent LOCAL DIRECTORIES PTY LTD (ACN 130 550 971) Sixth Respondent

|

JUDGE: |

GORDON J |

DATE: |

14 DECEMBER 2011 |

PLACE: |

MELBOURNE |

REASONS FOR JUDGMENT

INTRODUCTION

1 By Notice of Motion dated 30 June 2011, the respondents sought an order that the applicants pay their costs, on a party and party basis, by way of a gross costs order. Since then, the parties have agreed that the respondents should have a gross costs sum order for the period from 16 June 2009 to 8 February 2010. (I leave to one side the application for a gross costs sum order for other periods.) For the period in issue, the parties are unable to agree on the fixed sum. The respondents seek an order for $364,694, or 83.66% of the amount claimed for the total professional fees and disbursements for the period estimated to relate to the copyright issues of $435,909. On the other hand, the applicants submit that the lump sum should be only $291,324 or 66.83% of $435,909.

RELEVANT PRINCIPLES

2 What are the applicable principles? In Ginos Engineers Pty Ltd v Autodesk Australia Pty Ltd (2008) 249 ALR 371 at [22]-[24], Finn J described them as follows:

22 Rules of Court such as r 21.02(2)(a) of the FMC Rules and O 62 r 4(2)(c) of the Federal Court Rules, which empower a court to order a gross amount in costs instead of an amount determined after taxation, are well accepted as being directed to the avoidance of expense, delay and the protraction of litigation, whether the case be a complex or a simple one: see Beach Petroleum NL v Johnson (No 2) (1995) 57 FCR 119 at 120 (Beach Petroleum NL); Australasian Performing Rights Association Ltd v Marlin [1999] FCA 1006; Nine Films & Television Pty Ltd v Ninox Television Ltd [2006] FCA 1046 (Nine Films & Television); see generally on fixing of costs by courts, GE Dal Pont, Law of Costs, Butterworths, Sydney (2003) para [15.14] and following R Quick and DJ Garnsworthy, Quick on Costs, looseleaf, LBS Information Services, Sydney, para [6.20].

23 It is inconsistent both with the terms of r 21.02(2)(a) and to the clear objective in making a lump sum order that the costs in issue be subjected to the detailed scrutiny often applied in taxations: Leary v Leary [1987] 1 All ER 261 at 265; Dal Pont, 2003 para [15.17] and [15.19]. In specifying a lump sum, it is well accepted that it is appropriate to apply a “much broader brush” than would be applied on a taxation: see Sony Entertainment (Australia) Ltd v Smith (2005) 215 ALR 788 at [196] – [200] (Sony Entertainment). Nonetheless, the discretion to make a lump sum order, no less than the general discretion to order costs, must be exercised judicially and in accordance with principle. In particular in making a lump sum estimate the approach of the court should be “logical, fair and reasonable”: Beach Petroleum NL at CLR 123; ALR 164; Nine Films & Television Pty Ltd at [8].

24. It is not uncommon, particularly, but not only, in intellectual property cases, for the court to take as its starting point the evidence of the charges for professional costs incurred and disbursements made by the lawyers of the party awarded costs – and this irrespective of whether the costs are to be estimated on an indemnity basis: compare Beach Petroleum NL at CLR 120; ALR 162; or on a party and party basis: compare Universal Music Australia Pty Ltd v Miyamoto [2003] FCA 812 at [29] and following. That figure is then characteristically adjusted to take account of the acceptability of the charges made, the conduct of the proceeding, the measure of success on issues and so on, to produce a sum which as a matter of judgment is neither overcompensatory nor prejudicial to the successful party. Consistent with the broad brush approach, that adjustment ordinarily is effected through the application of a discount to the figure accepted by the court on the available evidence as appropriately reflecting actual professional costs charged and disbursements made. The case law evidences wide variations in the percentages of discount sought and/or applied to reflect the exigencies of the matter in question: compare Sony Entertainment, 60%; Beach Petroleum NL, 39%, Nine Films & Television, 23%. What is clear is that a lump sum award may be in an amount that is greater or smaller than would have been the taxed costs payable: see Dal Pont, 2003, para [15.20].

See also GM Holden Ltd v Paine (No 3) [2011] FCA 693; Playcorp Group of Companies Ltd v Peter Bodum A/S (No 2) [2010] FCA 455 and Seven Network Limited v News Limited [2007] FCA 2059.

3 Against that background, I turn to consider the circumstances of the present case.

4 There is no doubt that a taxation of the respondents’ costs against the applicants under r 40.02(b) of the Federal Court Rules 2011 for the period in issue would be complex, costly and time consuming.

5 It is also common ground that the method for calculating a gross sum costs order is not rigid. As noted, above, a starting point may be evidence of professional costs and disbursements charged by the lawyers for the party awarded costs (irrespective of whether costs were to be estimated on an indemnity basis) adjusted to produce a sum which was neither over compensatory nor prejudicial to the successful party: see [2] above. It is also trite that a judge’s experience in taxing costs is limited: see, by way of example, Re Clynton Court Pty Ltd (2005) 53 ACSR 432 at [21]. In the Federal Court, taxation of costs is conducted by Registrars of the Court. They have substantial experience in taxation of costs covering a wide range of matters (both in terms of substance and size). By reference to the Court’s scale of costs allowable for work done and services performed and the bills of costs filed by the parties in whose favour a costs order was made, Registrars make an estimate of the approximate totals for which (if the bill were taxed) a certificate of taxation would be likely to issue. The process of estimation is important because, at one level, that is what the respondents seek from the Court on a final basis. Although the estimates by Registrars vary, it is not uncommon that approximately 25% of the bill is taxed off.

6 Other matters are self evident. First, the costs recovered on a party and party basis are not a complete indemnity. There was no such order for costs to be paid on an indemnity basis in this case. Second, there is usually a discount applied to the fees and that discount reflects a range of matters including, but not limited to, the rates charged, the nature of the work done, the time taken to complete the work, the seniority of the practitioners. The list is not limited.

7 Third, as Ms Egan for the respondents submitted, the relevant scale of costs also includes item 41 which provides for an uploading of relevant professional fees for such matters as the complexity of issues, the difficulty and novelty of questions raised, the importance of the matter to a party, the amount involved and the skill, labour and specialised knowledge and responsibility on the part of the solicitor. This list is not exhaustive.

8 Fourth, in relation to disbursements, there is a “National Guide to Counsel Fees” published by the Federal Court with effect from 4 January 2010. The guide provides a range of fees for junior and senior Counsel, by type of application and appeal. If the fees fall within the guide, then in the absence of some other fact or matter, Counsel’s fees would not be reduced substantively.

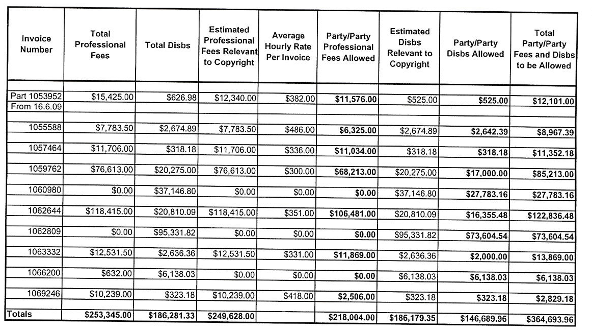

9 The respondents seek a gross sum costs order on the basis of an analysis undertaken by Judith Hedstrom, a costs consultant with extensive experience. As the basis for her report, Ms Hedstrom referred to the invoices issued by the respondents’ solicitors, for the relevant period that were said to relate to the copyright issues as follows:

A careful reader will notice that the respondents have already discounted the fees and disbursements. Discounts were made by Ms Hedstrom in two ways. First, to identify what amount of the fees and disbursements related to the copyright issues and, second, a further discount taking into account what would be expected to be allowed on a party and party basis.

10 Contrary to the submissions of the applicants, I do not accept that there is anything wrong with the approach adopted by Ms Hedstrom. First, all but the first invoice relied on by Ms Hedstrom related entirely to the copyright issues. The only part invoice was the invoice issued in relation to the period at the beginning of the period in issue, being the invoice dated 16 June 2009. Secondly, Ms Hedstrom did not simply accept the invoices at face value. She explained the process she undertook as follows:

A. Professional charges of the lawyers:

1. In assessing the lawyers professional charges I have had recourse to Schedule 2 of Order 62 Federal Court Rules and in assessing Counsels’ fees I have had recourse to the Federal Court “National Guide” to Counsels’ Fees.

2. I have examined all of the lawyers’ invoices including counsels’ memoranda of fees and have allowed, in my assessment of the party/party professional charges and disbursements “all such costs charges and expenses as appear to have been necessary or proper for the attainment of justice” – Federal Court Rules Order 62 Rule 19.

3. I am instructed that until 16 June 2009 the majority of the work carried out by the law firms and Counsel related to all issues in the proceeding and I have accordingly relied upon the table of apportionment provided to me by my instructing solicitors.

4. I noted that Middleton’s Melbourne commenced acting for the Respondents in June 2008 the Respondents having previously been represented by DLA Phillips Fox Brisbane. I have taken this into account in assessing the party/party costs by disallowing work that appeared to duplicate work carried out by DLA Phillips Fox particularly work carried out by Middelton’s lawyers to acquaint themselves with the proceeding i.e. I have not allowed “reading in” time.

5. Good & Services Tax – As the Respondents can claim an input credit for GST I have not included any such amounts in the claims for disbursements.

6. To assess the party/ party charges of the lawyers I perused each invoice rendered by the lawyers to identify the work that would not be allowed on a party/party taxation of the costs.

The amounts I then allowed took into account the percentage that the lawyers had calculated applied to the work solely relating to the copyright issues.

1. Counsels’ Fees

To assess amounts that would be allowed for Counsels’ fees on a party/party taxation I considered the details of work carried out by the various Counsel and their respective charge out rates assessing the amounts that would be allowed on taxation. I also took into account the percentage apportionment that the lawyers had calculated applied to Counsels’ fees in relation to the copyright issue.

2. Other disbursements

In relation to all other disbursements I have only included those I consider would be allowed on taxation and have reduced the quantum of some such disbursements.

11 Against that background, what is the appropriate order? As noted earlier, the parties agree that there should be a gross costs sum order. The issue between them is the discount to be applied to the recoverable costs. The applicants submitted that the discount should be 33%. The respondents submitted that the discount should be 16%, that proposed by Ms Hedstrom. It is important to note that both parties proposed that a discount be applied to professional fees and disbursements.

12 The cases that have considered a gross costs order have not adopted a consistent approach in relation to the size of the discount. That is not surprising – each case must be determined taking into account the facts and circumstances of the particular case and the assessment of a gross sum costs order requires a broad brush. It inevitably involves matters of evaluation and judgment.

13 In the circumstances of the present case, I propose to make an order under r 40.02(b) of the Federal Court Rules 2011 that the applicants pay the respondents 75% of the party and party fees and disbursements claimed by the respondents for the period from 16 June 2009 to 8 February 2010. That amount is $326,931.75. As Sackville J said in Seven Network, if the matter is viewed simply as an assessment by reference to the percentage of total costs, an award of approximately 75% seems to me well within the appropriate range, taking into account the particular circumstances of this case.

I certify that the preceding thirteen (13) numbered paragraph are a true copy of the Reasons for Judgment herein of the Honourable Justice Gordon. |

Associate: