FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Letten (No 17)

[2011] FCA 1420

IN THE FEDERAL COURT OF AUSTRALIA | |

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | First Defendant (and others according to the attached schedule) |

DATE OF ORDER: | |

WHERE MADE: |

NOTE: For the purposes of these Orders, Receivers has the meaning ascribed to it in the Orders made in this proceeding on 25 February 2010.

THE COURT ORDERS THAT:

1. For the purposes of paragraph 1(a)(iii) of the Orders dated 11 November 2010 (the Pooling Orders), the Receivers are not justified in paying to the liquidators of Twinview Nominees Pty Ltd (Receivers and Managers Appointed) (in liq) the amount of any of the creditor claims contained in the proofs of debt lodged with the liquidators and exhibited as “DJT-140” to the Thirtieth Affidavit of Damian John Templeton sworn on 29 August 2011 (the 30th Templeton Affidavit).

2. For the purposes of paragraph 1(a)(iii) of the Pooling Orders, the Receivers are justified in refusing to pay to the liquidators of The Glen Centre Hawthorn Pty Ltd (Receivers and Managers Appointed) (in liq) the amount of any of the creditor claims contained in the proofs of debt lodged with the liquidators and exhibited as “DJT-139” to the 30th Templeton Affidavit.

3. For the purposes of paragraph 1(b)(iii)(A) of the Pooling Orders, the Receivers’ costs of this application are costs of the receiverships.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

VICTORIA DISTRICT REGISTRY | |

GENERAL DIVISION | VID 95 of 2010 |

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff

|

AND: | MARK RONALD LETTEN First Defendant (and others according to the attached schedule) |

JUDGE: | GORDON J |

DATE: | 12 DECEMBER 2011 |

PLACE: | MELBOURNE |

REASONS FOR JUDGMENT

INTRODUCTION

1 By an amended interlocutory process dated 23 November 2011, Mr Damian Templeton and Mr Phillip Hennessy of KPMG as the receivers and managers of Twinview Nominees Pty Ltd (Receivers and Managers Appointed) (in liq) and The Glen Centre Hawthorn Pty Ltd (Receivers and Managers Appointed) (in liq) (the Receivers) sought directions in the receivership of the Twinview Joint Venture and The Glen Centre Joint Venture (as defined in the orders made in this proceeding on 25 February 2010 (the Appointment Orders)) as follows:

1. for the purposes of paragraph 1(a)(iii) of the Orders dated 11 November 2010 (the Pooling Orders), are the Receivers justified in paying to the Liquidators of Twinview Nominees Pty Ltd (Twinview) the amount of any, and if so which, of the creditor claims contained in the proofs of debt lodged with the liquidators of Twinview in Exhibit “DJT-140” to the Thirtieth Affidavit of Damian John Templeton sworn on 29 August 2011 and filed in this proceeding (the 30th Templeton Affidavit);

2. for the purposes of paragraph 1(a)(iii) of the Pooling Orders, are the Receivers justified in paying to the Liquidators of The Glen Centre Hawthorn Pty Ltd (TGCH) the amount of any, and if so which, of the creditor claims contained in the proofs of debt lodged with the liquidators of TGCH in Exhibit “DJT-139” to the 30th Templeton Affidavit?

The “creditor claims” may be divided into two categories – trade creditor claims and investor claimant claims. It will be necessary to return to consider those categories in further detail later in these reasons for decision.

2 The background to these proceedings is relevantly summarised in Australian Securities and Investments Commission v Letten (No 7) (2010) 80 ACSR 401 at [7]-[12]. Three stages of the receivership are relevant – the appointment (recorded in the Appointment Orders), the power of sale of property (recorded in the Sale Orders made in this proceeding on 25 May 2010) and the pooling of assets (recorded in the Pooling Orders).

3 In the Appointment Orders, the Court made orders that:

1. pursuant to s 1323(l)(h)(ii) of the Corporations Act 2001 (Cth) (the Corporations Act), the Receivers be appointed to the property of, inter alia, TGCH and Twinview (other than property that constituted property of a Scheme as defined in Annexure A to the Appointment Orders);

2. The Glen Centre Joint Venture Scheme and the Twinview Joint Venture Scheme (each a Scheme defined in Annexure A to the Appointment Orders) be wound up pursuant to s 601EE(1) of the Corporations Act; and

3. the Receivers be appointed as receivers and managers of the property of, inter alia, The Glen Centre Joint Venture Scheme and the Twinview Joint Venture Scheme.

4 In the Sale Orders, the Court made orders that:

1. the Appointment Orders be varied with respect to The Glen Centre Joint Venture and TGCH so that the Receivers had the power to sell The Glen Centre Property;

2. the Receivers were justified in paying all agent’s reasonable fees and other reasonable expenses associated with the sale of The Glen Centre Property;

3. the remaining proceeds of sale of The Glen Centre Property be paid into the bank account established by the Receivers in relation to The Glen Centre Joint Venture;

4. the Appointment Orders be varied with respect to the Twinview Joint Venture and Twinview so that the Receivers had the power to sell the Twinview Property;

5. the Receivers were justified in paying all agent’s reasonable fees and other reasonable expenses associated with the sale of the Twinview Property; and

6. the remaining proceeds of sale of the Twinview Property be paid into the bank account established by the Receivers in relation to the Twinview Joint Venture.

5 In the Pooling Orders (see also Letten (No 7)), the Court ordered, inter alia, that the Receivers were justified in paying the following amounts out of the proceeds of sale of each asset of the Schemes and the Corporate Defendants (as defined in the Appointment Orders), in the following order of priority:

1. priority receivership costs, as fixed by the Court, to the Receivers;

2. any liabilities secured by that asset, to the relevant Secured Lender;

3. the amount of trust creditor claims in respect of the relevant Corporate Defendant (if any) in respect of which the relevant Corporate Defendant has a right of indemnity and lien, to the relevant Corporate Defendant; and

4. the balance (if any) into a bank account held in the name of the Receivers and designated as the “Common Fund” account.

6 The Receivers have now sold The Glen Centre Property and the Twinview Property. TGCH and Twinview and the Thirteenth Defendant, Nicholson Street Pty Ltd, are the only Scheme Companies which, to date, have surplus cash after realisation of assets and discharge of any secured debt. Accordingly, at present they are the only Scheme Companies in respect of which the order referred to in [5(3)] above might be relevant. (The Receivers currently believe that the Twenty Ninth Defendant (Glenbelle) may ultimately also have a cash surplus.)

7 On 13 May 2011, the Receivers were appointed as Liquidators of a number of the Corporate Defendants, including TGCH and Twinview. On 10 June 2011, the Liquidators called for proofs of debt from creditors of TGCH and Twinview. The Liquidators received nine proofs of debt from persons claiming to be creditors of TGCH and six proofs of debt from persons claiming to be creditors of Twinview. As noted earlier, the creditors’ claims may be divided into two categories – trade creditor claims and investor claimant claims.

8 The questions raised for determination by the Court are whether the Receivers are justified in refusing to accept any of the claims of trade creditors or investor claimants as “trust creditor claims” for the purposes of the Pooling Orders. That, in turn, raises the question whether TGCH and Twinview are entitled to a right of indemnity out of the proceeds of sale for any of the claims of the trade creditors or the investors. It was common ground that each of TGCH and Twinview held their property on trust for the relevant Scheme investors.

9 The application for directions was served on Westpac Banking Corporation (the secured lender), the Australian Securities and Investments Commission and Mr Letten. In addition, the application for directions was served on the Australian Taxation Office, Baker & McKenzie, Breese Pitt Dixon Pty Ltd, Bridgehead Properties Pty Ltd (Bridgehead), Gross Waddell Pty Ltd, llario G Cortese Architects Pty Ltd, Metropolitan Fire and Emergency Services Board, ABK Group Pty Ltd, Louton Pty Ltd, Robuck Metals Pty Ltd, Resolve Air Conditioning and Mechanical Services Pty Ltd (each of which had lodged a proof of debt in one or both of Twinview and TGCH). The relevant Scheme investors were also given notice of the application.

10 Bridgehead appeared by Counsel to oppose the directions sought by the Receivers. The issues to be determined and the conclusions reached in relation to them are as follows:

1. Issue 1: Are Twinview and / or TGCH liable as trustees for losses to their respective trust estates such that any right of exoneration which might otherwise have subsisted in respect of either trade creditors or investor claimants is extinguished by the operation of the so-called clear accounts rule?

Answer: Yes.

2. Issue 2: Are Twinview and / or TGCH otherwise entitled to exoneration in respect of:

(a) trade creditors;

(b) investor claims,

having regard to the circumstances in which those debts and liabilities were incurred?

Answer: No.

3. Issue 3: Are Twinview and / or TGCH entitled to exoneration in respect of the investor claims at all?

Answer: No.

RELEVANT LEGAL PRINCIPLES – TRUSTEE’S INDEMNITY

11 The parties submitted that the current state of the law about the scope of a trustee’s indemnity was settled. The reference to the “current state of the law” is necessary because although Bridgehead accepted that this Court lacked the necessary authority to substantially rewrite the applicable principles, it submitted that the principles should be revisited and fundamentally changed.

12 A trustee must be diligent in discharging its duties and obligations and, in doing so, must give careful consideration to the exercise of discretions under the trust deed and refrain from doing anything beyond the terms of the trust deed and relevant statutory or other legal or equitable obligation: Grossman v E Katz Manufacturing Jewellers (ACT) Pty Ltd (2004) 52 ACSR 198 at [4] and Bruton Holdings Pty Ltd (in liq) v Federal Commissioner of Taxation (2011) 193 FCR 442 at [21]. As a result, a trustee is personally liable for liabilities incurred in the discharge of the trust but is entitled to be indemnified against those liabilities from trust assets: Octavo Investments Pty Ltd v Knight (1979) 27 ALR 129 at 134-135.

13 As Austin J said in Trim Perfect Australia v Albrook Constructions [2006] NSWSC 153 at [20]:

(1) A trustee is personally liable for the debts it incurs as trustee, notwithstanding any such provision as cl 16 of the present trust instrument purporting to relieve it of that liability: Vacuum Oil Co Pty Limited v Wiltshire (1945) 72 CLR 319; Octavo Investments Pty Limited v Knight (1979) 144 CLR 360 at 367.

(2) Where a trustee incurs expenses or becomes subject to liability in the course of performing the duties of the trust, it has a right of indemnity out of assets of the trust in respect of those expenses or that liability, the right of indemnity taking the form of a right of recoupment of expenditure made by the trustee and a right of exoneration from the liability to make expenditure which has not yet been expended: Octavo Investments at 367; Chief Commissioner of Stamp Duties for New South Wales v Buckle (1998) 192 CLR 226 at 245.

(3) The right of indemnity, recoupment and exoneration is supported by security in favour of the trustee over the trust assets in the form of an equitable lien (sometimes referred to as an equitable charge, though it arises as a matter of law rather than by agreement inter parties): Octavo Investments at 367; Buckle at 246.

(4) The trustee’s equitable lien confers on it a proprietary interest in the trust property, which can be asserted in priority to the claims of the cestuis que trust: Octavo Investments at 370.

(5) The trustee’s proprietary interest is enforceable by judicial sale or the appointment of a receiver, and ancillary orders such as an order to recover possession of trust property to permit these primary remedies to take effect, but foreclosure is not available: Tennant v Trenchard (1869) LR 4 Eq 537; Seton’s Judgments and Orders, 7th ed, 1912, vol 3 pp 2220 to 2225; see also Ashburner’s Principles of Equity, 2nd ed, 1983, p 248; EL Sykes and S Walker, The Law of Securities, 5th ed, 1993, p 198; Fisher and Lightwood’s Law of Mortgages, Australian ed, 1995 by E L G Tyler, P W Young and C W Croft, p 44; ANZ Banking Group Limited v Intagro Projects Pty Limited [2004] NSWSC 1054 [at 14].

(6) The trustee’s proprietary interest may only be enforced by judicial sale or the appointment of a receiver (and ancillary orders) and not merely by sale without curial intervention: The Melbourne Tramways Trust v The Melbourne Tramway and Omnibus Co Ltd (1887) 13 VLR 487 at 490; Re Pumfrey (deceased); The Worcester City and County Banking Co Ltd v Blick (1883) 22 ChD 255 at 265; Re Stucley; Stucley v Kekewich [1905] 1 ChD 67; Davies v Littlejohn (1923) 34 CLR 174 at 184; Hewett v Court (1983) 149 CLR 639 at 663.

(7) The right of indemnity accrues at the time the obligation is incurred, although it may subsequently become either a right of recoupment or a right of exoneration, depending on how the trustee responds: Xebec Pty Limited (in liq) v Enthe Pty Limited (1987) 18 ATR 893; Southern Wine Corporation (in liq) v Frankland River Olive Co Ltd [2005] WASCA 236 at [30].

(8) Loss of office by the trustee (whether by retirement or removal) does not deprive the trustee of an accrued right of indemnity, recoupment or exoneration: Coates v McInerney (1992) 7 WAR 537; Xebec v Enthe [at 898]; Southern Wines [at 30].

See also JA Pty Ltd v Jonco Holdings Pty Ltd (2000) 33 ACSR 691 at [50].

14 The trustee’s right of indemnity against trust assets, however, is qualified. In general terms, it depends on whether the trustee has strictly adhered to the terms of its mandate. So, for example, the indemnity is not available if the activity which generated the liability involved a breach of trust or a breach of a duty by the trustee, was beyond the powers given to the trustee or was criminal or fraudulent in nature: Gatsios Holdings Pty Ltd v Kritharas Holdings Pty Ltd (in liq) (2002) ATPR 41-864. The indemnity is also not available where the liability is “unreasonable or unnecessary” and therefore is not “properly incurred”: O’Keeffe v Hayes Knight GTO Pty Ltd (2005) 218 ALR 604 at [14] and Nolan v Collie (2003) 7 VR 287 at [51] and [53].

15 Although those principles appear relatively straightforward, the scope and nature of a trustee’s right of indemnity has been the subject of judicial comment and academic debate: see, for example, Nolan v Collie [2004] HCATrans 22 and Aitken L, “A liability ‘properly incurred’? – The trustee’s right to indemnity, and exemption from liability for breach of trust” (2011) 35 Australian Bar Review 53 at 54. At the core of the debate is identifying when a trustee’s liability has been “properly incurred”. As has been noted on more than one occasion, the word “properly” or “improperly” is less than helpful: see, for example, Gatsios at [8]. The negative test is the relevant test; that is to allow indemnification for what has not been shown to have been improperly incurred: Nolan at [51] and [53] citing Lindley LJ in Re Beddoe [1893] 1 Ch 547.

16 To determine what is “improperly incurred” it is necessary to consider whether the conduct of the trustee was (Nolan at [53]):

1. done in bad faith;

2. outside the relevant power (that is, outside the terms of the trust deed); and/or

3. exercised with an absence of the care and diligence that a person of ordinary prudence should exercise. If it concerns the management of trust property, the equitable standard applies: Speight v Gaunt (1883) 9 App Cas 1. If it concerns investment of trust property, the statutory standard applies, namely the duties under the relevant provisions of the Trustee Act of each State and Territory.

17 Of course, not all breaches of duty result in a trustee losing the right of indemnity. Duties that require strict adherence, if breached, will result in loss of the right of indemnity: Nolan at [51]. In Nolan, the following examples were given at [52]:

1. duty to keep and render accounts;

2. the duty not to allow a conflict between duty and interest;

3. the duty not to obtain an unauthorised benefit from the trust; and

4. the duty to adhere and carry out the terms of the trust deed.

The list is, of course, not exhaustive. On the other hand, duties that concern the day to day management of the trust, if breached, will not result in a loss of the right of indemnity: Nolan at [51].

18 At a practical level, a breach of certain “core” duties will as a matter of course result in a loss of the right of indemnity. For all other breaches, the answer will depend on the terms of the trust deed and whether that breach was in bad faith, outside the relevant power and exercised with an absence of care and diligence that a person or ordinary prudence should exercise.

19 A trustee’s right of indemnification is also subject to a condition precedent – that the trustee make good any loss it caused to the estate (the clear accounts rule). That rule was described and analysed by Brooking J in RWG Management Ltd v Commissioner for Corporate Affairs [1985] VR 385 where his Honour said (at 397-398):

… a balance is to be struck between what is due by way of compensation and what is due by way of indemnity and … if the balance is in favour of trustee he may recover from the estate to that extent.

See also Warne v GDK Financial Solutions Pty Ltd; Billingham v Parbery [2006] NSWSC 259 at [192].

20 The Receivers submitted, and I accept, that the clear accounts rule is essentially a mathematical exercise setting off the trustee’s right to indemnity against its liability with respect to previous breaches of trust: RWG Management at 397; CB Darvall & Darvall v Moloney (No 2) [2007] QSC 337 at [19] and Holli Managed Investments Pty Ltd v Australian Securities Commission (1998) 30 ACSR 113 at 124. Put another way, the quantum of the trustee’s right to indemnity may be diminished by breaches unrelated to the liabilities for which the right of indemnity is claimed. Indeed, it was common ground that the clear accounts rule will apply if it can be established that Twinview or TGCH (as the case may be) can be shown to have acted in breach of trust or duty such as to give rise to a liability to pay compensation to the relevant trust fund in an amount equal to or in excess of the present value of the fund.

21 The area of dispute is the application of these principles to the facts. Bridgehead contended there was no relevant breach of trust or duty. The Receivers contended otherwise.

22 Before turning to the facts, it is necessary to address Bridgehead’s submission that “guided by US jurisprudence, the High Court could deliver the desired outcome of a direct route of access to trust assets which bypasses the clear accounts rule …”. The extent of the “revisiting” required is beyond the capacity of a Judge at first instance and possibly also an intermediate appellate court. If the fundamental principles are to be rewritten (which must extend to the principle that an unsecured creditor of a trustee company will not be entitled to subrogate the trustee’s right of indemnity where the trustee has engaged in unrelated breaches of trust), then that would appear to be a matter for the High Court, or more likely, Parliament as has occurred in a number of the States in the United States of America.

RELEVANT FACTS

23 Consistent with the Appointment Orders, the Receivers prepared and filed a Disclosure Report for each of The Glen Centre Joint Venture and the Twinview Joint Venture.

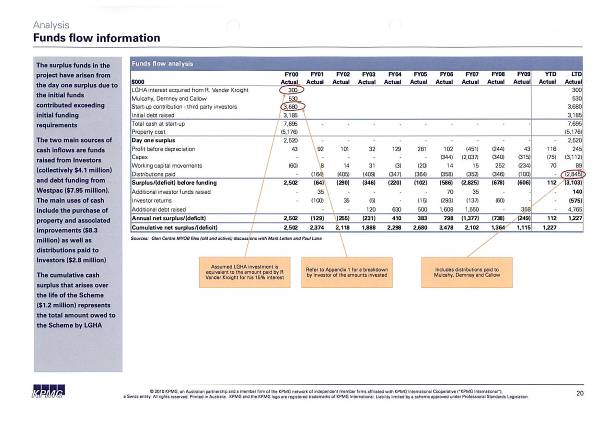

24 The Disclosure Report for The Glen Centre Joint Venture stated that initial investors contributed $4.51 million, the initial debt raised was $3.185 million, the property acquisition cost was $5.176 million and there was therefore an initial cash surplus of $2.520 million. Up to the date of the Disclosure Report, allowing for profits and losses, capital expenditure, working capital movements and distributions paid to investors, there was a deficit before funding of $3.103 million. Additional funds raised from investors totalled $0.14 million and additional debt of $4.765 million was incurred. After capital repayments to some investors, the cumulative net cash position should have been $1.227 million but was in fact $74,000 as at the date of the appointment of the Receivers.

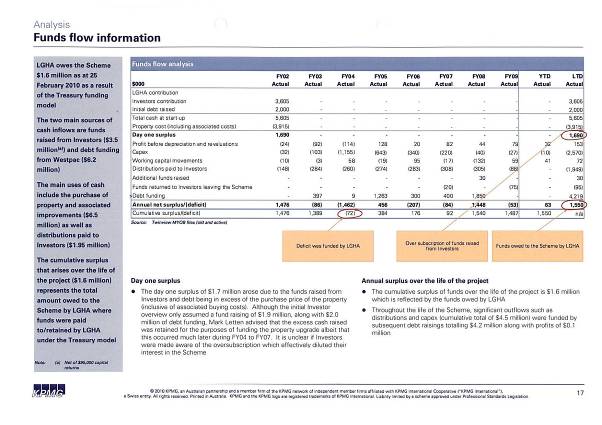

25 The Disclosure Report for the Twinview Joint Venture stated that initial investors contributed $3.605 million, the initial debt raised was $2 million, the property acquisition cost was $3.915 million and there was therefore an initial cash surplus of $1.69 million. Up to the date of the Disclosure Report, allowing for profits and losses, capital expenditure, working capital movements, distributions paid to investors, additional funds raised from investors, capital repayments to some investors and additional debt, the cumulative net cash position should have been $1.55 million but was in fact $26,000 as at the date of the appointment of the Receivers.

26 A separate Disclosure Report in relation to LGH Administration Pty Ltd (LGHA), LGH Holdings Ltd and LGH Finance Pty Ltd (Receivers and Managers appointed) (collectively the LGH Companies) is also relevant. It included the following conclusions:

1. funds contributed by investors in each of the Schemes were mixed and co-mingled in common bank accounts of LGHA;

2. the proceeds of sale of a number of the Scheme properties which were sold prior to the appointment of the Receivers were also paid to the LGH Companies and were mixed and co-mingled in the bank accounts of LGHA;

3. the LGH Companies applied the mixed investor funds and the proceeds of sale of various Scheme properties to the assets of the Schemes by way of:

3.1 the purchase and development of individual properties;

3.2 the operation and maintenance of individual properties;

3.3 the payment of distributions to investors; and

3.4 some limited returns of capital to certain investors;

4. the property of the Schemes was irretrievably intermingled owing to the central treasury role played by LGHA.

27 The Pooling Orders were made, among other reasons, because of the complexity and probable impossibility in reconciling the flow of funds between Schemes: see Letten (No 7). Put simply, the funds contributed by investors, and the property of the various Schemes, were and remain irretrievably intermingled with the result that there was no certainty that the trust fund or estate of any particular Scheme truly represented the funds that were contributed by investors with an intention that they be applied to that particular Scheme. So, for example, the trust fund for the Twinview Joint Venture Scheme may include funds from other Schemes that have been inappropriately directed to it.

28 Letten (No 7) considered both The Glen Centre Joint Venture and the Twinview Joint Venture. The Glen Centre Joint Venture was described (at [85]-[91]) in the following terms:

[85] The Glen Centre joint venture was wound up on 25 February 2010. The property was described by the receivers as a retail complex comprising 16 shops, a restaurant and dance studio at 673-681 Glenferrie Road, Hawthorn (the Glen Centre Property). At the time of the appointment of the receivers, Westpac had a secured claim over the property of $7.95 million. The receivers were granted the power of sale and orders were made governing the receivers’ dealing with the proceeds from the disposal of the assets of the scheme: see [11] above.

[86] According to the receivers, the Glen Centre Property was purchased by The Glen Centre Hawthorn Pty Ltd, the eighteenth defendant (Glen Centre), in October 1999. The deposit was paid by LGHA. Prior to inviting investors to participate in the scheme, Mr Letten sold a 15% interest in the Glen Centre Property to one investor and a further 15% to a group of three investors. Of the remaining 70% of the project, 65% was initially sold to approximately 92 investors, with the remaining 5% held by LGHA. Mr Letten informed the receivers that LGHA purchased the 15% interest from the investor which increased LGHA’s share in the scheme to 20%. No agreement was signed recording that subsequent arrangement.

[87] Investments in the scheme occurred through by following means:

(1) execution of a joint venture agreement;

(2) roll over from another scheme;

(3) payment of funds without execution of a joint venture agreement or any other document.

[88] The joint venture agreements were largely entered into between the investor and Glen Centre, the manager of the scheme. However, the receivers identified a small number of joint venture agreements for the scheme that were entered into between individual investors and Castello Holdings Pty Ltd, the nineteenth defendant, whose relationship to the scheme is not clear. The recitals to the joint venture agreement provided:

The Investors and the Manager have agreed to associate themselves as Joint Venturers for the purpose of acquiring an Interest in the Glen Centre Hawthorn (hereinafter defined) and to hold the same as an investment and to earn income therefrom (“the Project”). [Emphasis added.]

“Interest” was defined as a “share or interest in the investment known as ‘The Glen Centre Hawthorn’”. “The Glen Centre Hawthorn” was not defined. The joint venture agreement only provided for capital growth and not an income return. Notwithstanding that term of the joint venture agreement, over the life of the scheme, investors received distributions.

[89] The promotional material for the scheme produced by the receivers described the investment proposal in vague terms. It provided:

The proposal is to hold the property for a medium to long term period and in the process, steadily improve the asset by:

- Replacing shop fronts and mall.

- Renewing facade and awnings to Glenferrie Road frontage.

- Changing tenant mix.

- Improve trading conditions to car park and mall tenancies.

with the ultimate aim to subdivide the property and “sell off” the individual tenancies on very firm yields which are currently being evidenced and improving dramatically in this retail precinct.

[90] There were initially 92 investors in the scheme who contributed $4,779,000. Twenty-two initial investors have left the scheme. The receivers were informed by Mr Letten that, upon leaving, these investors may have agreed a “handshake” agreement with Mr Letten whereby the investors were entitled to share in any capital gain on wind-up of the scheme. However, no documentation has been produced to the receivers to support such an agreement. A total of $530,000 was returned to investors exiting the scheme and $45,000 was transferred to other schemes. Further, a total of $2,844,921 in distributions was made to investors from the inception of the scheme until October 2008. Those distributions were funded by LGHA.

[91] As at 25 February 2010, the scheme has 70 investors who have contributed $3,775,000 to the scheme. In addition to that sum, there is an additional $0.3 million that was acquired by LGHA from another investor, increasing the total funds from active investors to $4,075,000. There is also a secured loan from Westpac for $7.95 million. The estimated surplus for the scheme is only $1,227,000 which represents the total amount owed to the scheme by LGHA given the central treasury funding model adopted by this scheme. According to the receivers, the main uses of cash during the life of the scheme included the purchase of property and associated improvements ($8.3 million) as well as distributions paid to investors ($2.8 million). Although the distributions paid were higher than the retained profits during the life of the scheme (and therefore had to be funded from another source), the receivers noted that once property revaluations were taken into account, the scheme appeared to have sufficient retained profits to pay those distributions.

29 Twinview was described (at [130]-[137]) in the following terms:

[130] Receivers were appointed to the Twinview joint venture on 25 February 2010 and the scheme was wound up pursuant to s 601EE of the Act. The property at 167-173 Flinders Lane, Melbourne, Victoria was a retail/commercial complex which was acquired by Twinview Nominees Pty Ltd, the twentieth defendant (Twinview), in September 2001 for $3.9 million.

[131] Investments in the scheme through LGHA came about by the following means:

(1) execution of a joint venture agreement (35 investors);

(2) roll over from another scheme (four investors);

(3) payment of funds without execution of a joint venture agreement or any other document (43 investors).

Of the 82 investors, 74 were initial investors. There was one subsequent third party investor, six were transfers between investors and one investor left the scheme.

[132] A screed for investors in the scheme dated 25 September 2001 was issued by LGHH. Investors were offered the opportunity to “join with [LGHH]” in the purchase of the property. The investment offered two types of return: an “income” return to be paid monthly during the life of the project (7.46% in 2001, 7.46% in 2002, 7.41% in 2003, 9.37% in 2004, 11.26% in 2005 and 12.25% in 2006) and a capital return upon sale of the property. However, one of the “2002” joint venture agreements produced by the receivers only provided for the latter (a capital return). Notwithstanding that term of that joint venture agreement, over the life of the scheme, investors received distributions of $1.95 million.

[133] In the joint venture agreement, the recitals provided that:

The Investors and the Manager have agreed to associate themselves as Joint Venturers for the purpose of acquiring an Interest in the 167 Flinders Lane Project (hereinafter defined) and to hold the same as an investment and to earn income therefrom (“the Project”). [Emphasis added.]

As with other schemes, the phrase “167 Flinders Lane Project” was not defined. “Interest” was defined as a “share or interest in the investment known as ‘the Project’”. The manager of the joint venture was Twinview.

[134] LGHA may be understood to have performed a central treasury function on behalf of Twinview. LGHA collected all receipts from any debt or investment raising. It also funded distributions to investors, received rental income receipts from tenants and settled amounts owing to third party suppliers / financiers of Twinview.

[135] The receivers determined that approximately $3.540 million was raised from investors. Cash investments were made through LGHA by cheque payable to LGHA. At the start of the scheme, there was a surplus of $1.7 million because the funds raised from investors and debt exceeded the purchase price of the property. This was contrary to what investors had been told, namely fund raising of $1.9 million along with debt raising of $2 million. It is not known whether investors were told about the over-funding.

[136] Over the life of the scheme, distributions to investors totalled $1.95 million and capital expenditure totalled $2.570 million. Although these amounts were capable of being funded through subsequent debt raisings of $4.2 million and profits of $0.1 million, the source of funding was LGHA.

[137] As at 25 February 2010, LGHA owed the scheme $1.6 million (the scheme’s estimated surplus cash as at that date) and Twinview had a loan payable to Westpac of $6.2 million.

30 Bridgehead placed considerable reliance upon the joint venture agreements (the JVAs) entered into between Twinview and TGCH (respectively) and certain investors in the Projects (as that term was defined in the JVAs). Bridgehead submitted that the JVAs were the only document that could be said to define the scope of each of Twinview and TGCH’s obligations in respect of the Projects and that:

1. the trust estates for TGCH and Twinview were confined to The Glen Centre Property and the Twinview Property respectively;

2. TGCH and Twinview were not obliged, under the relevant JVAs or otherwise, to get in and receive Capital Contributions (as that term was defined in the JVAs); and

3. there was no relevant breach of trust or other conduct on the part of TGCH or Twinview that would give rise to an obligation to compensate that trust estate.

For the reasons that follow, I reject those contentions.

31 A sample of the JVAs for each of Twinview and TGCH was in evidence. The sample JVAs were relevantly the same and included the following provisions:

1. Recital A – “The Investors and the Manager have agreed to associate themselves as Joint Venturers for the purposes of acquiring an Interest in the [relevant Project] and to hold the same as an investment and to earn income therefrom (“the Project”)”.

2. Recital B – “The Manager has agreed to act as nominee of the Investors and as Manager of the Joint Venture and has entered or will enter into the Contract of Sale for the purchase of the Project and agrees to enter into all other contracts on behalf of and nominee [sic] for the Investors”.

3. Clause 1.1(c) – “‘Capital Contribution’ means the aggregate of the Equity Contribution which each Investor contributes to the capital of the Joint Venture as set out opposite each Investor’s name in column 4 of the Schedule together with any further amounts so contributed from time to time”. (There was no schedule in the TGCH JVA. The Schedule in the Twinview JVA provided that the “Capital Contribution” was the aggregate of the “Equity Contribution” and the “Debt Contribution”).

4. Clause 1.1(i) – “‘Participating Interest’ means the interest which an Investor holds from time to time in the Joint Venture, which interest shall be equal to the proportion that the Capital Contribution of that Investor bears to the aggregate of the Capital Contributions of all Investors”.

5. Clause 1.1(j) – “‘Interest’ means a share or interest in the investment known as ‘the Project’”.

6. Clause 2.2 – “The assets of the Joint Venture shall be held by the Manager on trust for the Investors and the Investors shall own the beneficial interest in those assets as tenants-in-common in accordance with their respective Participating Interests. The expression “assets of the Joint Venture” was not defined in the JVA.

7. Clause 3.2 – “The Manager shall hold all assets of the Joint Venture including the Interest on behalf of the Investors in accordance with the terms and conditions of this Agreement, particularly clause 2.2”.

8. Clause 4.2 – “In carrying out its duties and obligations under or pursuant to this Agreement, the Manager shall … (f) keep full accurate and proper books of account and records of all expenditure incurred in the course of the Project and of all income received by the Manager in the course of the Project and keep all documents supporting and evidencing all entries in those books of account and records.”

9. Clause 4.3(a) – “A bank account, if required, for the Joint Venture shall be established by the Manager in the name of the Manager and the Joint Venture with a Bank selected by the Manager. Subject as hereafter provided in this clause 4.3, all Capital Contributions and other money of the Joint Venture shall be paid to or deposited into that account or into a solicitors’ or accountants’ trust account as notified to the Investors by the Manager. Moneys of the Joint Venture may also be paid direct to or applied at the direction of any creditor of the Joint Venture without the need to first deposit those monies into an account.”

10. Clause 4.3(b):

The Manager shall furnish to each Investor within three months after the end of each financial year a signed statement of account, reflecting for that financial year:

(i) all transactions in connection with the Project during the financial year, as disclosed by the records and accounts kept or caused to be kept by the Manager;

(ii) all Project expenses incurred or accrued during the financial year; and

(iii) all Joint Venture assets as at the end of the financial year.

11. Clause 5.1 – “Each Investor agrees to contribute to the Joint Venture its Capital Contribution to be held and used by the Manager in accordance with the terms and conditions of this Agreement”.

12. Clause 5.2 – “Immediately upon signing this Agreement, each Investor shall pay its Equity Contribution to the Manager”.

13. Clause 9.1 – “Each party covenants and agrees with each other party to indemnify and keep indemnified that other party from and against all liabilities, losses and damages which may arise in respect of any breach of the obligations imposed on the first party under this Agreement and, without in any way limiting the generality of the foregoing and where the first party is the Manager, any losses and damages which may arise from the Manager, in breach of its obligations under this Agreement, entering into any obligations or making any warranties or representations whatsoever for or on behalf of the Joint Venture without the necessary power or authority to do so.”

32 Where a JVA was executed, its terms were far from clear. Generally (but not always), the JVA did not identify the putative “Manager” by name and indeed failed to accurately identify what comprised “the Project” and, therefore, an “Interest” in “the Project”. There are additional complicating facts. First, the “screeds” seen by at least some of the investors (see [29] above) described arrangements inconsistent with the JVA and, secondly, the payments received by some of the investors were inconsistent with the “screeds” and / or the JVAs.

33 Thirdly, as discussed in the extracts from Letten (No 7) (at [28] and [29] above), a JVA was not always executed. Indeed, close to half of the investments in the case of Twinview and the vast majority of investments in the case of TGCH, appear to have been made in circumstances where there were no written terms governing the relationship (if any) between Twinview / TGCH and the investors. In Letten (No 7) at [248], the conclusion reached in those cases was that “a trust was created when the moneys were received by LGHA … to hold that money and apply it for the purposes of a joint venture in which the property or project was sufficiently identified to form the subject matter of a trust”.

34 That leads to a fourth complicating factor – the central treasury function performed by LGHA. The Disclosure Report for Twinview, under the heading “Scheme structure and relationship with key stakeholders”, described it as follows:

2. LGHA performed as a treasury function on behalf of Twinview. LGHA collected all receipts from any debt and/or equity raising undertaken by Twinview…

3. Third party Investors have contributed $3.6 million to the Scheme. Cash investments made by Investors were via LGHA (i.e. Investor cheque made payable to LGHA)…

35 In the Disclosure Report for TGCH, there was a diagrammatic representation of the Scheme Structure in similar terms. The Disclosure Report for TGCH did not specifically assert that investor cheques were made payable to LGHA. Notwithstanding that fact, the Disclosure Report for TGCH stated that LGHA collected all receipts, and TGCH did not itself have a bank account into which cheques or deposits payable to TGCH could be paid. Thus, and in the absence of any evidence to the contrary (and there was none), it appears all investors who made out cheques or otherwise deposited funds for investment into a Project did so knowing that the funds were being paid (at least in the first instance) to LGHA.

BRIDGEHEAD’S CONTENTIONS

36 Bridgehead’s submissions dealt with the two categories of investors separately – those who executed a JVA and those who did not. In cases where the parties executed a JVA, Bridgehead submitted that identifying the nature and extent of the obligations of Twinview and TGCH to the investors was essentially a question of construction of the JVA. In particular, Bridgehead submitted that:

1. there was nothing in the terms of the JVAs nor any relevant surrounding circumstances (to the extent they are known) that imposed on Twinview and TGCH any obligation to get in and receive Capital Contributions, either expressly or by implication;

2. the expression “assets of the Joint Venture” as referred to in cll 2.2 and 3.2 of the JVAs was not defined to include the Capital Contributions or any other money paid by investors;

3. having regard to cl 4.3 of the JVAs which expressly contemplated that Capital Contributions could be paid to a third party to be held on trust or used to pay creditors of the Joint Venture directly, “assets of the Joint Venture” should be construed as referring only to assets that came under the direct control of Twinview and TGCH being (respectively) the Twinview Property and The Glen Centre Property;

4. further, the JVAs specifically contemplated (cl 4.3) that a bank account for the deposit of Capital Contributions would be established by the Manager only “if required” and went on to expressly provide that Capital Contributions could be paid to or deposited into “... a solicitors’ or accountants’ trust account as notified to the Investors by the Manager”.

37 Further, Bridgehead placed considerable reliance upon the following facts:

1. the funds paid to LGHA were in fact held on trust by LGHA (not Twinview or TGCH, either alone or together with LGHA) for the investors for investment in the relevant Project: see Letten (No 7) at [248];

2. there was no evidence concerning the circumstances in which investors came to make payments to LGHA, including whether investors were notified or understood that by making cheques payable to LGHA they were paying their Capital Contributions to an “accountants’ trust account”;

38 Having regard to the terms of the JVAs and the additional facts in the preceding paragraph, to the extent that funds were misapplied, Bridgehead submitted that the misapplication was by LGHA, giving rise to a liability in LGHA (not Twinview or TGCH) to compensate the relevant trust estate (being the pool of investor funds provided to LGHA for the purposes of investment in the relevant Project). Thus, according to Bridgehead, the assets of the Joint Venture held by Twinview and TGCH subject to the trust established under cl 2.2 of the JVAs (and thus the trust estate for which Twinview and TGCH were accountable) were at all times limited to (respectively) the Twinview Property and The Glen Centre Property in respect of which there has not been, as far as the Receivers are aware, any relevant loss.

39 To the extent that investors made payments purportedly in respect of a particular Project otherwise than pursuant to a JVA (that is, where no JVA was executed or by rolling over from an earlier investment), Bridgehead submitted that there was no document or other basis for imposing any obligation on either Twinview or TGCH to get in or take control of those funds and, thus, no liability in either Twinview or TGCH.

ANALYSIS

40 Three related questions arise – what is the trust estate, what are the duties and obligations of the trustee of that estate and what is the nature of the breaches of trust (if any)?

41 Letten (No 7) included the following passages at [239]-[248]:

[239] It was common ground that each of the schemes was established as a trust or a number of trusts. That requires more explanation and in particular, requires a distinction to be drawn between the various ways investors invested in the schemes.

(a) Investments pursuant to joint venture agreements

[240] Many investors executed joint venture agreements (including for the equity deposit bonds) pursuant to which:

(1) one or more of the Letten Entities were appointed as manager of one or more of the joint ventures;

(2) the investors and the manager agreed to associate themselves as joint venturers for the purposes of carrying out the relevant “project”;

(3) the assets of the joint venture were held by the manager on trust for the investors and the investors owned the beneficial interest in those assets in accordance with their respective participating interests; and

(4) the profits of the joint venture were owned by the investors in proportion to their respective interests with investors each liable to contribute to any losses of the joint venture in the same proportion.

[241] On that basis, each of the schemes involving a joint venture agreement appears to be a trust created under the relevant joint venture agreement (or possibly a number of trusts in the case of YVG) with the relevant corporate defendant appointed pursuant to the joint venture agreement acting as the operator of the relevant scheme and trustee of the relevant trust.

…

[246] The receivers also relied on the following propositions:

(1) The responsible entity of a registered managed investment scheme is required, pursuant to s 601FC(2) of the [Corporations Act (2001) (Cth)], to hold scheme property on trust for scheme members.

(2) The Full Court of this court commented in Brookfield Multiplex Ltd v International Litigation Funding Partners Pty Ltd (2009) 180 FCR 11; 260 ALR 643; 74 ACSR 447; [2009] FCAFC 147 at [64] that, if an arrangement is required to be registered as a managed investment scheme, then “by force of the legislation, scheme property is to be held on trust by the responsible entity”.

[247] On those bases, the receivers submitted that investors’ contributions in respect of the other forms of investment should be deemed to have been received by LGHA (or the relevant Letten entity) subject to a trust in favour of the investors. The receivers submitted that conclusion was further reinforced because the funds contributed by the alternative forms of investment were most likely paid to LGHA and will have been applied in the same manner as investors’ contributions pursuant to joint venture agreements.

[248] I accept that submission. In all circumstances, notwithstanding the deficiencies in the screeds and the joint venture agreements, a trust was created when the moneys were received by LGHA or the relevant Letten Entity (as the case may be) to hold that money and apply it for the purposes of a joint venture in which the property or project was sufficiently identified to form the subject matter of a trust: Lehman Brothers International (Europe) (in admin) v CRC Credit Fund Ltd [2010] EWCA Civ 917 at [171] …

42 In identifying the trust estate for which TGCH and Twinview are accountable, three possibilities were suggested. First, that the trust estate is (or was) confined to The Glen Centre Property and the Twinview Property respectively. Secondly, that it extended to all monies received by LGHA for application (as described in [248] of Letten (No 7)) to The Glen Centre Property and the Twinview Property (or the relevant Project) respectively. The third possibility, which the Receivers submitted to be the better view, was that the funds of all Schemes ought to be viewed as a single “master trust” of which the various corporate defendants constitute joint trustees. The Receivers submitted that this would be consistent with the rationale which led to the making of the Pooling Orders. In support of the “master trust” proposition, the Receivers submitted that given the way in which the funds of the various Schemes were dealt with, the other approaches were artificial because there is no way of determining whether the estate truly represented the funds referable to that particular Scheme.

43 As at 11 February 2011, the expected dividend return to investors upon finalisation of the winding up of the Schemes was in the order of 8-10 cents in the dollar. That remains the position. Thus, the losses to investors are anticipated to be not less than 90 cents in the dollar. If the clear accounts rule is to be assessed by reference to the single, master trust, there will be no indemnity available for trust creditor claims as the loss caused by the large scale breaches of trust committed by the various corporate trustee defendants would be far in excess of the value of those creditor claims. In the case of TGCH, the total of investor claims is $3,245,000, so investor losses (at 90 cents in the dollar) are not less than $2,920,500. In the case of Twinview, the total of investor claims is $3,540,000, so investor losses (at 90 cents in the dollar) are not less than $3,186,000. These amounts represent total investor contributions, less returns of capital.

44 A number of undisputed facts must be stated at the outset. First, each of TGCH and Twinview were trustees – they held property on trust for investors: see [31(6)] above. Secondly, at the very least, the trust estate included The Glen Centre Property and the Twinview Property respectively. Thirdly, Mr Letten was at all relevant times the sole director of each of the TGCH and Twinview. Fourthly, Mr Letten was the controlling mind of each entity and of LGHA.

45 The Receivers submitted that the actions of Twinview and TGCH were not taken in good faith and were thus “improperly incurred”, such that the right of indemnity is unavailable. Bridgehead did not address this issue. Given the views that I have formed, that issue may be put to one side.

46 The critical question is whether, assuming the liabilities the subject of the claims were “properly incurred”, each trustee lost its right of indemnity against the trust assets for the trade creditor and investor liabilities because of the operation of the clear accounts rule. That is, as noted earlier, the quantum of the trustee’s right to indemnity may be diminished by breaches unrelated to the liabilities for which the right of indemnity is claimed: at [19]-]20] above. That brings in to sharp focus the need to identify the trust fund, the trustee’s duties and obligations in relation to that fund and the alleged breaches of duty.

47 It is necessary to address the duties owed by each of TGCH and Twinview by reference to two classes of beneficiaries; those that signed JVAs and those that did not.

Investors that signed a JVA

48 In relation to those investors that signed a JVA, the JVAs expressly stated that the assets of the joint venture were held by the Manager on trust for the investors: cl 2.2. In the case of The Glen Centre Joint Venture and Twinview Joint Venture, the Managers were TGCH and Twinview respectively. They were named in the JVAs as “Manager” and that was the capacity in which they acted. For the sake of completeness, it should be noted that for some of the JVAs for The Glen Centre Joint Venture, Castello Holdings Pty Ltd (Castello) (rather than TGCH) was appointed as Manager. There was no evidence that Castello held any assets, incurred any liabilities as Manager, or had any written arrangement with TGCH.

49 The phrase “assets of the Joint Venture” was not defined in the JVAs. However, under the JVAs, the Manager was obliged to “hold all assets of the Joint Venture including the Interest on behalf of the Investors in accordance with the terms and conditions of [the JVA], particularly clause 2.2”: cl 3.2 (emphasis added). “Interest” was defined to mean “a share or interest in the investment known as ‘the Project’”: cl 1.1(j).

50 As those, and other, provisions of the JVAs make clear, the assets of the trust were not limited to The Glen Centre Property or the Twinview Property. The JVAs expressly acknowledged that there would be other assets of the trust and that those assets were to be held, managed and developed by the manager for and on behalf of the investors. For example, under the JVAs:

1. not only did the investors and the manager associate themselves as joint venturers for the purposes of acquiring an Interest in the Project, they agreed to hold that investment and earn income from it: Recital A;

2. the Manager was appointed as nominee to enter into all other contracts (not just the contract of sale for the purchase of the “Project”) on behalf of the investors: Recital B;

3. each investor agreed to contribute to the Joint Venture, not to the purchase of the Project, its Capital Contribution (defined to include an equity contribution and a debt contribution) to be held and used by the Manager in accordance with the terms of the JVA: cl 5.1.

51 The distinction sought to be drawn by Bridgehead (between the real properties in the hands of Twinview and TGCH on the one hand, and the Capital Contributions in the hands of LGHA on the other hand), whilst superficially attractive, has an air of unreality about it, in the context of all of the circumstances surrounding the Schemes. As noted at [44] above, the controlling mind of each of Twinview, TGCH and LGHA was Mr Letten. Investors gave their money to Mr Letten on the assumption (and with the intention) that it would be used to acquire and / or improve a specified piece of real property. The real property was acquired and / or improved with a mixed fund which included some of the funds contributed for that intended purpose, along with funds improperly diverted from other purposes.

52 Thus, the trust estate extended to include not only The Glen Centre Property or the Twinview Property but also, without limitation, the Capital Contributions, any income generated and the benefit of any contracts entered into by the manager. That list is not exhaustive. To the extent that surplus funds were received by LGHA for the Project (or an investment proposal), those funds should be regarded as having been received on behalf of Twinview or TGCH (as the case may be); LGHA being, in effect, the central banker or treasurer for the Schemes: see [34] above.

53 As noted above, Bridgehead submitted that there was nothing in the terms of the JVAs or any relevant surrounding circumstances (to the extent they are known) that imposed on Twinview and TGCH any obligation to get in and receive Capital Contributions, either expressly or by implication and, secondly, that the expression “assets of the Joint Venture” as referred to in cll 2.2 and 3.2 of the JVAs was not defined to include the Capital Contributions or any other money paid by investors. I reject those submissions. They are contrary to the express terms of the JVAs. First, as noted at [31(6)] and [44] above, the Manager held the assets of the Joint Venture on trust for the investors (cl 2.2) and the Manager was obliged to “hold all assets of the Joint Venture including the Interest on behalf of the Investors in accordance with the terms and conditions of [the JVA]” (cl 3.2). The assets of the Joint Venture were not limited to the Interest (defined to mean a share or interest in the investment known as “the Project”) but included it. There were other assets identified in the JVAs that were to be held by the Manager.

54 Bridgehead also sought to rely upon cl 4.3 of the JVA in support of its contention that the phrase the “assets of the Joint Venture” should be construed as referring only to assets that came under the direct control of Twinview and TGCH being (respectively) the Twinview Property and The Glen Centre Property. In particular, Bridgehead relied upon the fact that cl 4.3 expressly contemplated that Capital Contributions could be paid to a third party to be held on trust or used to pay creditors of the Joint Venture directly, secondly contemplated that a bank account for the deposit of Capital Contributions would be established by the Manager only “if required” and, thirdly, went on to expressly provide that Capital Contributions could be paid to or deposited into “... a solicitors’ or accountants’ trust account as notified to the Investors by the Manager”. In my view, the express terms of cl 4.3 do not detract from the construction of the JVA that I have adopted. What cl 4.3 did was to set out one aspect of the metes and bounds of the trustee’s obligations in relation to the manner in which the Capital Contributions could be held and dealt with. It must be recalled that under cl 4.2(f) of the JVA, the Manager was required to “… keep full accurate and proper books of account and records of all expenditure incurred in the course of the Project and of all income received by the Manager in the course of the Project and keep all documents supporting and evidencing all entries in those books of account and records” and under cl 4.3(b) of the JVA, to furnish a statement of account reflecting, inter alia, “all transactions in connection with the Project”. Those clauses logically applied to all Capital Contributions made in connection with the Projects and Capital Contributions which have, to TGCH and Twinview’s knowledge or direction, been deposited with LGHA. It would be practically impossible for the Manager to comply with cll 4.2(f) and 4.3(b) if the trust estate was limited in the manner contended for by Bridgehead.

55 It must be recalled that it was the Capital Contributions that the investors agreed to contribute to the Joint Venture “to be held and used by the Manager” in accordance with the terms of the JVA: cl 5.1. It was TGCH or Twinview (as the case may be) that were the relevant parties to JVAs, such that the funds could only have been placed under LGHA’s control with TGCH or Twinview’s explicit or implied sanction. Regardless of whether the Capital Contributions were deposited into a TGCH or Twinview bank account, a solicitor’s trust fund or, as was the case, the LGHA account, TGCH or Twinview remained ultimately responsible for those funds.

56 For the reasons stated above, I accept the Receivers’ submission that cl 4.3 does not support the contention that the trust fund is confined merely to The Glen Centre Property and the Twinview Property. On the contrary, it strongly suggests that it also extends to all monies contributed by the relevant investors.

57 The next question is, having been appointed trustee of the assets of the Joint Venture, what then were the duties, were those duties breached and, if so, were they subject to the clear accounts rule? As Counsel for Bridgehead submitted, the questions to be determined are whether there were unrelated breaches of trust and, if so, the accounting value of the losses to each trust attributable to those unrelated breaches of trust? As the Receivers submitted, the trustee’s right of indemnity is reduced pro tanto by the amount of any losses caused by its breach of trust: see also [20] above. It was common ground that the amount or value of the breaches needed to be no more than approximately $500,000 in the case of Twinview and $480,000 in the case of TGCH (being the total unsecured creditor claims excluding the claims submitted by investors).

58 The Receivers submitted that the following were unrelated breaches that gave rise to losses to the estate that the trustee should first make good before being entitled to exercise its right of indemnity:

1. a failure to get in and / or secure that part of the trust fund comprising surplus investor funds collected by LGHA but not applied to the Project;

2. a failure to properly account for income generated by the Project and / or additional debt funding secured against the Property;

3. a failure to properly account for distributions to investors; and

4. a failure to comply with the law.

59 It will be necessary to take each in turn. A funds flow analysis for each joint venture (based on the Disclosure Reports) and prepared by the Receivers is annexed to these Reasons for Decision.

60 The Receivers submitted, and I accept, that each of Twinview and TGCH were placed in a position equivalent to a responsible entity of a managed investment scheme with a duty to collect, or at the very least secure, the monies that each knew had been paid to LGHA by investors to obtain rights and benefits under the respective Schemes: eg Letten (No 7) at [264]-[265]. They did neither. They knowingly permitted investor funds to be used by LGHA for purposes other than that connected with the identified Project. That money cannot be recovered from LGHA. Were it not for the loss, the surplus available, in each case, would have been greater.

61 The fact that Twinview and TGCH were under a duty to get in and / or secure that part of the trust fund comprising surplus investor funds collected by LGHA but not applied to the Project is fortified by cl 4.2 of the JVAs which provided that:

In carrying out its duties and obligations under or pursuant to this Agreement, the Manager shall:

(a) faithfully, dutifully and punctually carry out its duties and exercise its responsibilities in the best interests of the Investors with all due skill, care and diligence;

It was plainly in the best interests of the Project (as defined by the JVAs), and therefore the investors, to get in and receive all Capital Contributions that were intended for that Project.

62 As the attached funds analysis records, the amount not collected, or secured, from LGHA was at least $1.69 million for Twinview and $2.52 for TGCH. These amounts represented the investor monies collected by LGHA which were not applied to the Project.

63 Bridgehead submitted that because there was no evidence that the surplus funds ever reached Twinview or TGCH, each entity was somehow absolved from liability. I reject that submission. Under the JVAs and the obligations imposed on each entity as an entity in a position equivalent to a responsible entity of a managed investment scheme (see Letten (No 7) at [263]-[268]), the identified property of each Scheme was held on trust for the investors. That obligation placed each entity in a fiduciary position. As stated in Letten (No 7) at [265], in the context of an unregistered managed investment scheme (a fact not in dispute), the essential elements of which are:

… a coherent and defined purpose, in the form of a “programme” or “plan of action”, coupled with a series of steps or course of conduct to effectuate the purpose and pursue the programme or plan and a pooling of contributors’ funds or of a “common enterprise” as between the contributors[,]

… pooled funds were received by the Manager (in this case Twinview or TGCH) in a fiduciary capacity.

64 As Keane JA explained in Mier v FN Management Pty Ltd (2005) 56 ACSR 93 at [26]:

… [T]here can be no doubt that the scheme property of an unregistered scheme is to be identified by reference to the terms of the scheme in relation to the contribution of assets to the enterprise involved in the scheme.

(Emphasis added.)

65 To the extent that surplus funds were received for the “enterprise” (that is, the Project), by LGHA as the central banker or treasurer for the Schemes (see [34] above), those funds were “scheme property” which Twinview and TGCH were obliged to get in and / or secure.

66 Next, the failure to properly account for income generated by the Project and / or additional debt funding secured against the Property. As discussed above (see [54]), Twinview and TGCH were obliged under cll 4.2(f) and 4.3(b) to properly account for the Project. Bridgehead submitted that in relation to the profits, the investors cannot prove on the balance of probabilities that these were paid to LGHA and not used to fund, for example, investor contributions or returns of capital to investors. I reject that submission. As the Disclosure Reports provided, LGHA collected all receipts from any debt and / or equity raising undertaken by Twinview or TGCH (as the case may be): see [34] above. That evidence, on the balance of probabilities, is sufficient to establish that both profits and the proceeds of additional debt funding secured on the property were paid to LGHA. As the attached funds analysis records, the total amounts so paid to LGHA by Twinview are $1.876 million and by TGCH $1.986 million. It was a clear breach of trust for Twinview and TGCH to hand these monies over to LGHA for LGHA to use for its own purposes, and given the value of the capital expenditure on the properties (which has been deducted from these figures), there is no countervailing benefit to the trust estate. On the face of it, these amounts represent a loss to the estate.

67 Bridgehead also submitted that there was insufficient evidence to establish that the debt funding was for unauthorised purposes. It submitted that given that the bank was “presumably” monitoring the application of its funds in respect of each Project, it was “inherently more likely” that the debt funding was applied in full to the Project. There are two answers to this contention. First, the obligation on Twinview and TGCH as trustees was to “properly account” for income generated by the Project and / or additional debt funding secured against the Property. As the Disclosure Reports and the attached funds analysis record, that did not occur. Secondly, Bridgehead’s contention that it was “inherently more likely” that the debt funding was applied in full to the Project itself rises no higher than a “presumption” and an “inherent likelihood”.

68 Next, the failure to properly account for distributions to investors. As the attached funds analysis records, distributions to investors were approximately $1.950 million for Twinview and $2.845 million for TGCH. Bridgehead submitted that these investor distributions were not unauthorised, because the “screeds” either expressly provided that investors will receive a monthly income from the property (in the case of Twinview) or contemplated income returns to investors (in the case of TGCH), and the JVAs did not prohibit or otherwise preclude the payment of distributions to investors. That may be so, but the obligation was to “properly account” for distributions to investors. As the attached funds analysis shows, there was no relationship between the amounts paid by LGHA to investors and the amounts received from Twinview and TGCH. This is consistent with the general modus operandi of LGHA, which was to raise funds from investors, on the basis of specific property proposals, but with a representation of annual income on that investment which bore no relationship with the actual returns on the property concerned, and which were paid regardless of the amount of any such returns: see Letten (No 7) at [94], [195] and [244]-[251].

69 There is thus no prospect of tracing the monies paid by Twinview and TGCH to LGHA into the hands of investors in the Twinview or Glen Centre Schemes. The funds were simply merged into the mixed and untraceable funds of LGHA. The liability of Twinview and TGCH is to restore the estate of which they were respectively trustees to the position it would have been in if there had been no breach of trust: Pilmer v The Duke Group (in liq) (2001) 207 CLR 165 and Breen v Williams (1996) 186 CLR 71. In the absence of a breach of trust, the amounts of $1.876 million and $1.986 million would not have been paid to LGHA.

70 Finally, the failure to comply with the law. Clause 4.2 of the JVA provided that:

In carrying out its duties and obligations under or pursuant to this Agreement, the Manager shall:

…

(e) use all reasonable endeavours to comply with all applicable laws, regulations and similar requirements in relation to the Project;

In contravention of the above clause, at all material times TGCH and Twinview were operating illegal, unregistered managed investment schemes such that the Projects were not complying with all applicable laws: see Australian Securities and Investments Commission v Letten [2010] FCA 140.

71 Bridgehead placed considerable emphasis on Twinview and TGCH occupying the “dual roles” of trustee of the joint venture property and manager of the joint venture. Accepting that there may be contractual duties that Twinview and TGCH had as managers which would not be regarded as a breach of trust or of a duty as trustee, the breaches of duty referred to above were plainly occasioned by a breach of trust.

72 Finally, it is necessary to say something about management fees. The “Investment Analysis” forming part of the “screeds” provided for management fees totalling $80,000 for Twinview and totalling $225,000 for TGCH. It appears from the attached funds analysis that no management fees have been paid. Bridgehead submitted that Twinview and TGCH were entitled to pay those management fees themselves, not out of trust assets pursuant to any right of exoneration, but pursuant to the JVAs independently of their powers as trustee. That submission is rejected. The contention that Twinview and TGCH are entitled to apply the trust assets to pay management fees without regard to their liability to the trustee estate is completely contrary to the principle that underlies the clear accounts rule. As Brooking J stated in RWG Management at 398:

… the rule that a defaulting trustee cannot claim a share in the estate unless and until he has made good his default is founded on the principle that where there is an aggregate fund in which the trustee is beneficially interested and to which he owes something, he must be taken to have paid himself that amount on account of his share.

It is immaterial whether the trustee’s claim on the fund arises from a liability that it has incurred, or from a management or other fee to which it is entitled, or even from the fact of also being a beneficiary of the trust. In every case, equity requires that the trustee be regarded as applying its share of the fund to the payment of its debt to the fund. The debts in this case exceed by a considerable margin the total of the possible claims by the trustee companies upon the respective funds.

Investors that did not sign a JVA

73 The position of those investors that did not sign a JVA is not substantially different to those that did sign a JVA. Why? First, the written record of the trust obligation was limited to the “screeds” (see [29] above) and to the fact that each of Twinview and TGCH were placed in a position equivalent to a responsible entity of a managed investment scheme. Second, the duties and obligations imposed by both the “screeds” and the relevant sections of Ch 5C of the Corporations Act included, at the very least, a duty to collect, or at the very least secure, the monies that each knew had been paid to LGHA by investors to obtain rights and benefits under the respective Schemes: eg Letten (No 7) at [264]-[265] and [60]-[72] above. Third, the duty imposed under cl 4.2(a) of the JVAs reflects the duties imposed by law on responsible entities under s 601FC in Ch 5C of the Corporations Act, and the duty imposed under cl 4.2(e) essentially obliged Twinview and TGCH to do what it was legally required to do – comply with Ch 5C of the Corporations Act.

74 In breach of those duties, each of Twinview and TGCH knowingly (through the controlling mind and will of Mr Letten) permitted investor funds to be used by LGHA (which Mr Letten also controlled) for purposes other than that connected with the identified Project, failed to properly account for income generated by the Project and / or additional debt funding secured against the Property and failed to properly account for distributions to investors. None of that can be recovered. Were it not for those losses, the surplus available, in each case, would have been greater.

The Master Trust

75 The third basis of the Receivers’ submissions was that the various corporate defendants were joint trustees of all the funds of the Schemes. That submission, in turn, depended on a finding that the special purpose corporate defendants (such as Twinview and TGCH) were trustees of funds deposited directly with LGHA for investment in the relevant Project, which then became irretrievably intermingled with funds deposited with LGHA for investment in other Projects. The Receivers accepted that there was no other basis on which Twinview and TGCH could be elevated to the position of joint trustee of funds paid to LGHA. Given the views that I have formed, it is unnecessary to resolve this issue.

Availability of the right of indemnity

76 As noted at [46] above, the Receivers submitted that because the Schemes were unlawful enterprises, having regard to way the Schemes were conducted, and the manner in which investors were induced to invest funds, the Schemes can also be characterised as being fraudulent in nature, such that no right of indemnity is available to Twinview and TGCH.

77 In RWG Management at 396, Brooking J stated that a trustee is:

… entitled to be indemnified in respect of a liability improperly incurred to the extent to which, acting in good faith, he has benefited the trust estate.

(Emphasis added.)

78 The Receivers submitted that the actions of Twinview and TGCH in furtherance of the Schemes cannot be characterised as having been taken in good faith because they constitute steps taken in furtherance of an illegal and (arguably) fraudulent enterprise, with knowledge of its illegality at all relevant times through the controlling mind and will of Mr Letten. Therefore, the Receivers submitted, any liabilities incurred in furtherance of this enterprise should not be subject to a trustee’s right of indemnity. Given the views that I have formed, it is unnecessary to resolve this issue.

Investor Claims

79 The proofs of debt received from investors are generally poorly articulated. In general terms, they appear to be damages claims for misrepresentation against the trustees in which the damages alleged to result are said to be the loss of the alleged creditor’s investment. Presumably the investors will assert that, had they known that their funds would be deployed for purposes beyond that of The Glen Centre Joint Venture and Twinview Joint Venture, they would not have invested the monies. The other matters raised in the proofs of debt appear to be unrelated to the Schemes in issue or simply annex a copy of the relevant JVA.

80 While the authorities do provide that a trustee can have a right for indemnity for damages claims, those damages must be incurred during the course of carrying on the trust business: see [11]-[18] above and Re Raybould [1900] 1 Ch 199 and Gatsios at [46]. Further, the claim for indemnity is also subject to the overarching consideration of whether the liability was properly incurred.

81 In the circumstances outlined above, the investor damages claims are not claims for which TGCH or Twinview could claim a right of indemnity as the liabilities were either:

1. incurred in breach of trust;

2. improperly incurred; and / or

3. arguably unlawful in nature, at least to the extent that they relate to the raising of capital for an unregistered management investment scheme.

Costs

82 Where an application for directions in the course of a receivership or a winding up is complex, or involves a relatively novel proposition in law, the starting point is that the costs of a “proper contradictor” are paid out of the assets of the company: Farrow Finance Company Ltd (in liq) v ANZ Executors and Trustee Company Ltd (1997) 23 ACSR 521 at 527.

83 Bridgehead submitted that it acted as a “proper contradictor” for the benefit of all proper trust creditors of Twinview and TGCH (and possibly creditors of other Schemes where funds become available to meet trust creditor claims), and that its costs should therefore be borne by the Receivers out of the fund held by them.

84 While Bridgehead acknowledged that it had acted in its own self-interest, it submitted that it is almost invariably the case that a contradictor takes a position in an application of this kind that is consistent with its own interest, and that its interest is shared by a number of other creditors.

85 Bridgehead’s interest represents 94% of the total value of the proofs of debt submitted (other than by investors purporting to claim as creditors) in respect of both Twinview and TGCH. Bridgehead has acted in its own self-interest in what was essentially a priority dispute. Through the forum of the application for directions, Bridgehead has been afforded a unique opportunity to advance its interests in this matter. If the Receivers had not sought directions, but rather decided unilaterally that the right of indemnity was wiped out by operation of the clear accounts rule, Bridgehead’s only recourse would have been to fund a challenge of this decision by the Liquidators. In that case, they would be exposed to the risk of paying the Receivers’ costs in the event of an unsuccessful challenge. For those reasons, I consider that Bridgehead should bear its own costs of the application. The Receivers’ costs of the application, will be costs of the receiverships.

I certify that the preceding eighty-five (85) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gordon. |

Associate:

ANNEXURE

The Glen Centre Joint Venture

ANNEXURE

Twinview Joint Venture

SCHEDULE OF PARTIES

LGH HOLDINGS LIMITED (ACN 007 191 943)

Second Defendant

211 WELLINGTON ROAD PTY LTD (ACN 092 663 860)

Third Defendant

BLUEMIST HOLDINGS PTY LTD (ACN 097 306 922)

Fourth Defendant

DELLWOOD HOLDINGS PTY LTD (ACN 098 505 803)

Fifth Defendant

ENMORE ENTERPRISES PTY LTD (ACN 082 158 487)

Sixth Defendant

FIRBANK ARCH PTY LTD (ACN 059 464 381)

Seventh Defendant

GLENLINE PTY LTD (ACN 098 532 364)

Eighth Defendant

GERLING HOLDINGS PTY LTD (ACN 091 726 457)

Ninth Defendant

LGH ADMINISTRATION PTY LTD (ACN 007 165 069)

Tenth Defendant

LGH FINANCE PTY LTD (ACN 078 859 248)

Eleventh Defendant

LOW HEAD VILLAGE PTY LTD (ACN 091 731 958)

Twelfth Defendant

NICHOLSON STREET PTY LTD (ACN 069 104 089)

Thirteenth Defendant

HOLLOWAY CREST PTY LTD (ACN 091 731 967)

Fourteenth Defendant

ROSEBERY ENTERPRISES PTY LTD (ACN 091 826 229)

Fifteenth Defendant

SIMMS INVESTMENTS PTY LTD (ACN 093 504 511)

Sixteenth Defendant

SY21 RETAIL PTY LTD (ACN 107 874 564)

Seventeenth Defendant

THE GLEN CENTRE HAWTHORN PTY LTD (ACN 089 906 543)

Eighteenth Defendant

CASTELLO HOLDINGS PTY LTD (ACN 088 204 175)