FEDERAL COURT OF AUSTRALIA

Commissioner of Taxation v Interhealth Energies Pty Ltd as Trustee of the Interhealth Superannuation Fund [2011] FCA 1365

IN THE FEDERAL COURT OF AUSTRALIA | |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

Pending the determination of this proceeding or further earlier order, and without prejudice to the rights of the fourth respondent under ASIC Charge number 2111887 granted by the second respondent:

1. The second respondent shall take all steps necessary to keep, maintain and preserve any moneys payable to it either from the sale of the second respondent’s units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments Pty Ltd or from moneys payable from any other party including Probiotic Technologies Pty Ltd.

2. The second respondent shall not pay, disperse, encumber or dispose of in any way (other than by paying the same into a bank account in the name of the second respondent established for this purpose) any and all moneys received by it from:

2.1. the sale of the second respondent’s units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments Pty Ltd; or

2.2. any moneys payable to it from any other party including Probiotic Technologies Pty Ltd.

3. The second and third respondents shall not give any direction to any person or entity be they Tweed Mortgage and Investments Pty Ltd or Probiotic Investments Pty Ltd, the fourth respondent or otherwise which would or would have the effect of:

3.1. preventing or inhibiting the payment of moneys due to the first respondent from the sale of the second respondent’s units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments Pty Ltd; or

3.2. preventing or inhibiting the payment of moneys due to the first respondent from any other entity including Probiotic Investments Pty Ltd.

4. Save than other in compliance with one of the orders herein, the third respondent, in her private capacity as well as in her capacity as a Director or shareholder of any entity, be restrained from entering into any arrangement or giving any direction which would prevent any sum being paid to the first respondent from the sale of the second respondent’s units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments Pty Ltd or from any other entity including Probiotic Investments Pty Ltd.

5. The first respondent not to seek any indemnity from, or from the assets of the Interhealth Superannuation Fund or any other entity for any cost incurred including legal costs as trustee of that fund.

6. The application against the fourth respondent be dismissed.

7. With respect to the oral application by Ivor Worrell and Jason Bettles in their capacity as joint and several trustees of the bankrupt estate of Patrick Shaun Wilson to intervene in this application made pursuant to Rule 9.12(1).

7.1. The oral application is deemed to be sufficient.

7.2. Pursuant to Rule 1.34, the filing of an application for leave to intervene is dispensed with.

7.3. Leave to intervene as second intervenor is granted.

7.4. Leave is granted to the second intervenor for the filing of:

7.4.1 a notice of address for service on behalf of the intervenor; and the

7.4.2 affidavit of Ivor Worrell sworn 10 November 2011.

7.5 The second intervenor’s right of intervention in this proceeding is limited to the making of submissions in respect of the form of the orders (if any) which the Court should make in respect of this proceeding.

7.6. Liberty is granted to the second intervenor to apply in respect of the granting of a wider right of intervention.

7.7 Leave is granted to the second intervenor to inspect and copy any material filed by the parties in this proceeding.

8. The applicant to pay the fourth respondent’s costs of and incidental to the application to be taxed if not agreed.

9. Save as aforesaid the costs of each of the parties including the second intervenor are reserved.

10. The originating application in QUD461/2011 is deemed to be an interlocutory application in the principal proceeding, QUD221/2010 – Commissioner of Taxation v Interhealth Energies Pty Ltd ATF the Interhealth Superannuation Fund.

11. Any affidavit, application or submissions filed by leave or otherwise in proceeding number QUD461/11 be uplifted from that file and filed in QUD221/10 and that there be no further material on file QUD461/11.

12. The applicant serve upon the first intervenor, Patrick Shaun Wilson a copy of the following:

12.1. Originating application filed 9 November 2011 (in QUD461/11);

12.2. Affidavit of Linda Gilligan sworn on 8 November 2011 (in QUD461/11);

12.3. A copy of these orders; and

12.4. Reasons for Judgment.

13. Liberty is granted to the first intervenor to apply in respect of these orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011

IN THE FEDERAL COURT OF AUSTRALIA | |

QUEENSLAND DISTRICT REGISTRY | |

GENERAL DIVISION | QUD 221 of 2010 |

BETWEEN: | COMMISSIONER OF TAXATION Applicant |

AND: | INTERHEALTH ENERGIES PTY LTD (ACN 003 104 505) AS TRUSTEE OF THE INTERHEALTH SUPERANNUATION FUND First Respondent GHUT HOLDINGS PTY LTD (ACN 146 608 933) AS TRUSTEE OF THE GREENHAVEN UNIT TRUST Second Respondent JOANNE HAMBROOK Third Respondent MERTHYR LAW PTY LTD (ACN 136 260 994) Fourth Respondent |

JUDGE: | LOGAN J |

DATE OF ORDER: | 11 NOVEMBER 2011 |

WHERE MADE: | BRISBANE |

THE COURT ORDERS THAT:

Pending the determination of this proceeding or further earlier order, and without prejudice to the rights of the fourth respondent under ASIC Charge number 2111887 granted by the second respondent:

1. The second respondent shall take all steps necessary to keep, maintain and preserve any moneys payable to it either from the sale of the second respondent’s units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments Pty Ltd or from moneys payable from any other party including Probiotic Technologies Pty Ltd.

2. The second respondent shall not pay, disperse, encumber or dispose of in any way (other than by paying the same into a bank account in the name of the second respondent established for this purpose) any and all moneys received by it from:

2.1. the sale of the second respondent’s units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments Pty Ltd; or

2.2. any moneys payable to it from any other party including Probiotic Technologies Pty Ltd.

3. The second and third respondents shall not give any direction to any person or entity be they Tweed Mortgage and Investments Pty Ltd or Probiotic Investments Pty Ltd, the fourth respondent or otherwise which would or would have the effect of:

3.1. preventing or inhibiting the payment of moneys due to the first respondent from the sale of the second respondent’s units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments Pty Ltd; or

3.2. preventing or inhibiting the payment of moneys due to the first respondent from any other entity including Probiotic Investments Pty Ltd.

4. Save than other in compliance with one of the orders herein, the third respondent, in her private capacity as well as in her capacity as a Director or shareholder of any entity, be restrained from entering into any arrangement or giving any direction which would prevent any sum being paid to the first respondent from the sale of the second respondent’s units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments Pty Ltd or from any other entity including Probiotic Investments Pty Ltd.

5. The first respondent not to seek any indemnity from, or from the assets of the Interhealth Superannuation Fund or any other entity for any cost incurred including legal costs as trustee of that fund.

6. The application against the fourth respondent be dismissed.

7. With respect to the oral application by Ivor Worrell and Jason Bettles in their capacity as joint and several trustees of the bankrupt estate of Patrick Shaun Wilson to intervene in this application made pursuant to Rule 9.12(1).

7.1. The oral application is deemed to be sufficient.

7.2. Pursuant to Rule 1.34, the filing of an application for leave to intervene is dispensed with.

7.3. Leave to intervene as second intervenor is granted.

7.4. Leave is granted to the second intervenor for the filing of:

7.4.1 a notice of address for service on behalf of the intervenor; and the

7.4.2 affidavit of Ivor Worrell sworn 10 November 2011.

7.5 The second intervenor’s right of intervention in this proceeding is limited to the making of submissions in respect of the form of the orders (if any) which the Court should make in respect of this proceeding.

7.6. Liberty is granted to the second intervenor to apply in respect of the granting of a wider right of intervention.

7.7 Leave is granted to the second intervenor to inspect and copy any material filed by the parties in this proceeding.

8. The applicant to pay the fourth respondent’s costs of and incidental to the application to be taxed if not agreed.

9. Save as aforesaid the costs of each of the parties including the second intervenor are reserved.

10. The originating application in QUD461/2011 is deemed to be an interlocutory application in the principal proceeding, QUD221/2010 – Commissioner of Taxation v Interhealth Energies Pty Ltd ATF the Interhealth Superannuation Fund.

11. Any affidavit, application or submissions filed by leave or otherwise in proceeding number QUD461/11 be uplifted from that file and filed in QUD221/10 and that there be no further material on file QUD461/11.

12. The applicant serve upon the first intervenor, Patrick Shaun Wilson a copy of the following:

12.1. Originating application filed 9 November 2011 (in QUD461/11);

12.2. Affidavit of Linda Gilligan sworn on 8 November 2011 (in QUD461/11);

12.3. A copy of these orders; and

12.4. Reasons for Judgment.

13. Liberty is granted to the first intervenor to apply in respect of these orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011

QUEENSLAND DISTRICT REGISTRY | |

GENERAL DIVISION | QUD 461 of 2011 QUD 221 of 2010 |

BETWEEN: | COMMISSIONER OF TAXATION Applicant

|

AND: | INTERHEALTH ENERGIES PTY LTD (ACN 003 104 505) AS TRUSTEE OF THE INTERHEALTH SUPERANNUATION FUND First Respondent GHUT HOLDINGS PTY LTD (ACN 146 608 933) AS TRUSTEE OF THE GREENHAVEN UNIT TRUST Second Respondent JOANNE HAMBROOK Third Respondent MERTHYR LAW PTY LTD (ACN 136 260 994) Fourth Respondent

|

JUDGE: | LOGAN J |

DATE: | 11 NOVEMBER 2011 |

PLACE: | BRISBANE |

REASONS FOR JUDGMENT

1 Proceeding QUD 221 of 2010 as between the Commissioner of Taxation, in his role as regulator under the Superannuation Industry (Supervision) Act 1993 (Cth) (SIS Act), and Interhealth Energies Pty Ltd (ACN 003 104 505) (Interhealth) as Trustee of the Interhealth Superannuation Fund (ISF) presently stands in the list for judgment.

2 In that proceeding, Mr Patrick Shaun Wilson (Mr Wilson) has been given leave to intervene in respect of orders that might be made in the event that the Commissioner establishes a case for relief.

3 The relief sought by the Commissioner in the proceeding arises from the giving of an undertaking by Interhealth pursuant to s 262A of the SIS Act. The Commissioner, as regulator, has formed the view that Interhealth has breached the terms of the undertaking which it gave. Section 262A(3) permits the making of an application to the Court for an order under subs (4). By s 262A(4), if the Court is satisfied that a person, in this case Interhealth, has breached a term of the undertaking, the Court may make all or any of the following orders:

(a) An order directing the person to comply with that term of the undertaking;

(b) An order directing the person to pay to the Commonwealth an amount up to the amount of any financial benefit that the person has obtained directly or indirectly and that is reasonably attributable to the breach;

(c) Any order that the Court considers appropriate directing the person to compensate any other person who has suffered loss or damage as a result of the breach;

(d) Any other order that the Court considers appropriate.

4 Recalling the nature of the substantive proceeding is helpful in the resolution of the application which has been made today by the Commissioner.

5 There are two beneficiaries of the ISF, Mr Wilson and Ms Joanne Hambrook. Mr Wilson was once, but has not been for many years, a director of Interhealth. That event, in itself, occasioned the ISF to become a non-complying superannuation fund under the SIS Act unless it had the benefit of a notice from the Commissioner. The reason why that is so is that the effect of the SIS Act, and regulations made thereunder, in relation to small superannuation funds, is that the trustee of such a fund, if a corporate trustee, must have as its directors those who are members of the fund.

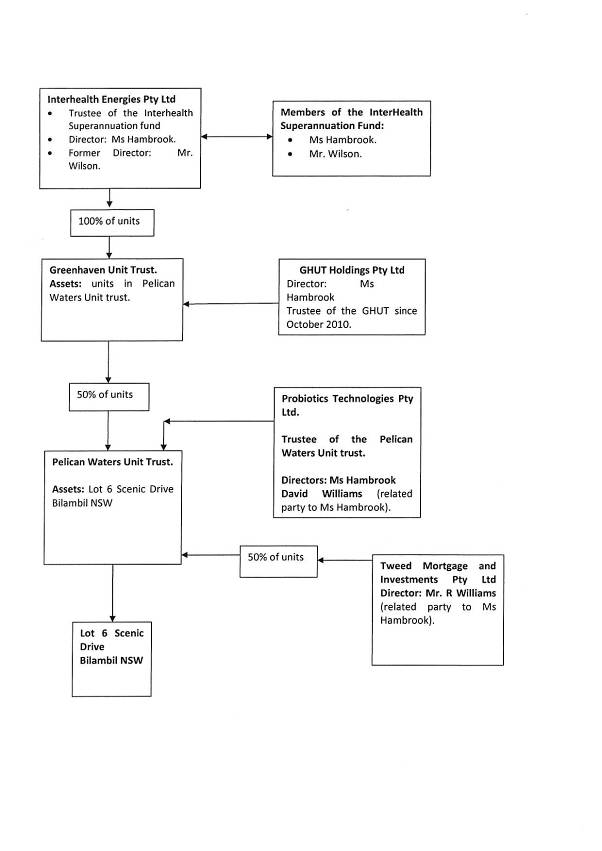

6 In effect, for many years Ms Hambrook has been in control of the trustee, Interhealth, and of the ISF. Ms Hambrook wears a number of other hats including, materially for the purposes of today, the office of director of another corporate trustee, GHUT Holdings Pty Ltd (GHUT Holdings). GHUT Holdings is the trustee of a unit trust known as the Greenhaven Unit Trust. Units in that trust are an asset of the ISF. Ms Hambrook also has other roles in relation to trusts which are a subsidiary of the Greenhaven Unit Trust.

7 The most convenient way of describing that inter-relationship between the ISF and what I have termed subsidiary trusts is diagrammatically. Such a diagram has helpfully been annexed to the Commissioner’s written outline of submissions and I annex that diagram, in turn, to this judgment: see Schedule attached. That diagrammatic summary confirms what the evidence led before me at trial established, which is that GHUT Holdings as trustee has 50% of the units in another unit trust known as the Pelican Waters Unit Trust of which a company Probiotic Technologies Pty Ltd is trustee. Ms Hambrook is one director of that company, Probiotic Technologies; another is a Mr David Williams. The other 50% of the units in the Pelican Waters Unit Trust are held by yet a further company, Tweed Mortgage and Investments Pty Ltd (Tweed Mortgage and Investments), of which the director is Mr R Williams.

8 The principal asset of the Pelican Waters Unit Trust is land at Lot 6, Scenic Drive, Bilambil in New South Wales. It is proposed that a sale occur next week which would see the units in the Pelican Waters Unit Trust sold and the consequential sale proceeds flowing through to the trusts which I have mentioned.

9 The Commissioner has sought interlocutory injunctive relief which would prevent the trustee of the Greenhaven Unit Trust in particular from dissipating any moneys which become payable to it either from the sale of its units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments or from moneys payable from any other party, including Probiotic Technologies.

10 That application was originally bought as a separate originating application. Upon reflection in the course of the proceedings today, the Commissioner sought that that originating application be treated instead as an interlocutory application made in QUD 221 of 2010. That seems to me to be the more appropriate way to deal with that application, it being one in the nature of an application to preserve the integrity of the jurisdiction that the Commissioner has invoked under s 262A of the SIS Act and, in particular, to preserve the efficacy of such orders as may be made under s 262A(4). So doing, ie, treating the originating application as an interlocutory application, will not do any injustice to any of the parties to the principal proceeding, QUD 221 of 2010, nor, for that matter, will it do any injustice to those who have been named as respondents to the application heard today.

11 Those respondents, apart from Interhealth, are GHUT Holdings, the second respondent, in its capacity as trustee of the Greenhaven Unit Trust, Ms Joanne Hambrook, personally, as third respondent and Merthyr Law Pty Ltd (Merthyr Law) as fourth respondent. It will be necessary later to give some explanation as to how Merthyr Law becomes relevant as a respondent.

12 It should also be recorded that in the interval which has passed between when judgment was reserved and today, Mr Wilson has become bankrupt. He was made bankrupt by order of the Federal Magistrates Court on 22 June 2011. Mr Jason Bettles and Mr Ivor Worrell were appointed as the joint and several trustees of his bankrupt estate.

13 Depending upon whether or not the ISF is a regulated superannuation fund, the interest which Mr Wilson has in that fund may or may not form part of the property divisible amongst his creditors: see s 116(2)(d)(iii)(A) of the Bankruptcy Act 1966 (Cth). It is not necessary to, in any way, reach a conclusion in respect of whether Mr Wilson’s interest does form part of the property divisible amongst his creditors today. It is necessary only to observe that there is, at least at present, a very real interest on the part of the trustees in whatever might be the fate of the orders made in the substantive proceeding given the potential for there to be property divisible amongst the bankrupt’s creditors.

14 Mr Wilson was given leave, as I have earlier noted, to intervene in the substantive proceeding. It seems to me in the interests of justice that the bankruptcy trustee be given like leave. The occasion for hearing submissions from the bankruptcy trustees as to the orders which might be made has not yet arisen, as was acknowledged on behalf of the trustees, but will instead arise once the reasons for judgment in the substantive proceeding have been delivered. At present, the bankruptcy trustee’s interest is only to preserve such benefit, if any, as the bankrupt estate may obtain from the proceeding brought by the regulator. Their stance, again an appropriate one, was to support the obtaining of orders at the behest of the Commissioner as regulator.

15 Mr Wilson himself, of course, might have an interest in his own right as was acknowledged by his being granted leave to intervene, and that potential remains, at least at present, notwithstanding his bankruptcy. In those circumstances, it is perhaps unfortunate that he was not, of all of those who were named as respondents, additionally named as a respondent. Be that as it may, there is an urgency about the interlocutory application given the pending sale. That means that the case needs to be dealt with today. It will, in my view, sufficiently recognise Mr Wilson’s interests if I direct that the Commissioner serve Mr Wilson with a copy of the orders made today and with a copy of the reasons for judgment. The orders made today will expressly reserve liberty to apply including liberty to apply on the part of Mr Wilson.

16 What then of Merthyr Law? Merthyr Law acted for Interhealth at the trial of the substantive proceeding. A Mr Noel Davis of the Sydney Bar appeared on behalf of Interhealth on that firm’s instructions. On 12 December 2010, GHUT Holdings, as chargor, gave to Merthyr Law, as chargee, by deed dated that day, a charge by way of a floating charge over charged property as defined in clause 8.1 of the deed of charge. The charged property is there defined, materially, to mean all of the chargor’s assets and undertakings whatsoever and wheresoever, both present and future including, materially, in paragraph (b), the holder of the chargor’s right, title and interest in any marketable securities for units in any unlisted unit trust.

17 The prospective liability under the charge is by cl 7.1 of that deed, stated for the purposes of s 282(3) of the Corporations Act 2001 (Cth) (Corporations Act) to be a maximum of $200,000. There is, in the deed of charge, reference to a “collateral agreement” as defined. That definition makes reference, amongst other things, to a deed of guarantee by the chargor in favour of the chargee to secure amounts owing from Interhealth Energies Pty Ltd as trustee for the Interhealth Superannuation Fund. It thus appears that GHUT Holdings has given a guarantee in favour of Merthyr Law to secure amounts owing from Interhealth Energies as trustee of the ISF.

18 Section 313 of the SIS Act provides inter alia:

Power of Court to prohibit payment or transfer of money or property

Court's power to protect interests of certain creditors etc.

(1) If:

(a) any of the following applies:

(i) an investigation is being carried out under this Act in relation to an act or omission by a person (the contravening person ), being an act or omission that constitutes or may constitute a contravention of this Act; or

(ii) a prosecution has begun against a person (also the contravening person ) for a contravention of this Act or under the Financial Sector (Collection of Data) Act 2001 in connection with a superannuation entity; or

(iii) a civil proceeding has begun against a person (also the contravening person ) under this Act; and

(b) the Regulator or a person (an aggrieved person ) to whom the contravening person is liable, or may become liable:

(i) to pay money (whether in respect of a debt, by way of damages or compensation or otherwise); or

(ii) to account for property;

applies to the Court; and

(c) the Court considers it necessary or desirable to do so for the purpose of protecting the interests of an aggrieved person;

the Court may make one or more of the orders specified in subsection (2).

Court's power to protect the interests of beneficiaries

(1A) If:

(a) the Regulator is of the opinion that it is necessary for the Court to make one or more of the orders specified in subsection (2) to protect the interests of any or all of the beneficiaries of a superannuation entity; and

(b) the Regulator applies to the Court for such an order in relation to a trustee of the entity; and

(c) the Court considers it necessary or desirable to protect the interests of any or all of the beneficiaries;

the Court may make one or more of the orders specified in subsection (2).

Any reference to the contravening person is a reference to the trustee

(1B) For the purposes of subsection (1A), subsection (2) has effect as if any reference to the contravening person were a reference to the trustee.

Orders that Court may make

(2) The orders that the Court may make are:

(a) an order prohibiting a person who is indebted to the contravening person or to an associate of the contravening person from making a payment in total or partial discharge of the debt to:

(i) the contravening person or associate; or

(ii) another person at the direction or request of the contravening person or associate;

(b) an order prohibiting a person holding money or property on behalf of the contravening person or of an associate of the contravening person from:

(i) paying all or any of the money; or

(ii) transferring or otherwise parting with possession of the property;

to:

(iii) the contravening person or associate; or

(iv) another person at the direction or request of the contravening person or associate;

(c) an order prohibiting the taking or sending out of Australia by a person of money of the contravening person or of an associate of the contravening person;

(d) an order prohibiting the taking, sending or transfer by a person of property of the contravening person, or of an associate of the contravening person from a place in Australia to a place outside Australia (including the transfer of interests from a register in Australia to a register outside Australia);

(e) an order appointing:

(i) if the contravening person is an individual--a receiver or trustee, having such powers as the Court orders, of the property or of part of the property of that person; or

(ii) if the contravening person is a body corporate--a receiver or receiver and manager, having such powers as the Court orders, of the property or of part of the property of that person;

(f) if the contravening person is an individual--an order requiring that person to deliver up to the Court his or her passport and such other documents as the Court thinks fit;

(g) if the contravening person is an individual--an order prohibiting that person from leaving Australia without the consent of the Court.

19 Suffice it to say, s 313(2) confers very wide powers indeed to preserve the subject matter materially of a proceeding under s 262A(3).

20 It is a noteworthy feature of s 313(7) provides that:

On an application under subsection (1) or (1A), the Court must not require the applicant or any other person, as a condition of granting an interim order under subsection (6), to give an undertaking as to damages.

21 There is a disposition on the part of Merthyr Law, on the evidence before me, to take advantage of its charge and, in particular, not to release it and not to allow a sale of units to occur. Unsurprisingly, the evidence before me establishes that the purchaser has already given notice that it requires clear title to the units and has reserved its rights in the event that clear title is not given at settlement. The sale of the units is due to occur on 17 November 2011. Apart from the power conferred by s 313 of the SIS Act, expressly, this Court has a more general power to make orders conferred upon it by s 23 of the Federal Court of Australia Act 1976 (Cth).

22 Whilst s 313 has not been the subject of judicial attention it does as the submissions helpfully made on behalf of Merthyr Law highlight, bear resemblance to s 1323 of the Corporations Act. In particular, in the use of “necessary” and “desirable” in that provision, Barrett J observed in ASIC v Sigalla [2010] NSWSC 1423 at [17] to [20]:

17 … is it “necessary” or “desirable” that the court impinge upon the freedom of disposition that the person concerned enjoys in relation to his, her or its property and impose a regime that denies that freedom? The court’s ordinary jurisdiction to appoint a receiver aims to protect assets that may turn out to belong to someone else. The purpose is protective. The same protective purpose is served, for the same reason, by a freezing order.

18 In addressing the “necessary or desirable” question in relation to the “alternative or lesser” freezing order, the court is dealing with an explicit statutory criterion. The approach is not the same as that adopted in relation to an application in equity for a freezing order of a Mareva kind. But factors typically taken into account in the exercise of equitable jurisdiction may well be relevant to questions of what is “necessary” or “desirable” in the interests of aggrieved persons.

19 The court may thus take into account all relevant discretionary factors, including those identified by Santow J in Re HIH Insurance Ltd; Australian Securities and Investments Commission v Adler (2001) 38 ACSR 266; [2001] NSWSC 451 at [4] to [7]. Santow J there observed that the public interest role of ASIC may warrant an order in circumstances where it might be denied to a private litigant. At the same time, however, any order the court makes must, as Santow J said “operate in a manner that is proportionate and not more intrusive than is necessary in the circumstances, recognising that it is inevitable that such orders will intrude upon private rights”. Santow J also pointed to the significance of the legislative exemption that ASIC enjoys from the requirement to give an undertaking as to damages.

20 In the end, the court’s task is as described, in relation to an application under s 1323(1)(j) and (k), by Nicholson J in Australian Securities and Investments Commission v Ivey (1998) 29 ACSR 391:

“The Court is required to engage in a balancing exercise which includes a balancing of public and private rights.”

(with the substitution for the ASIC of the Commissioner as regulator)

23 Those same sentiments, in my opinion, attend the exercise of the powers conferred upon this Court by s 313 of the SIS Act.

24 Further, it is a feature of other legislation where injunctions may be granted at the behest of a public official or commission that there is often a provision that an undertaking as to damages is not to be required. Such provision was found in the Trade Practices Act 1974 (Cth). That does not mean that the absence of an undertaking as to damages thereby becomes an irrelevant consideration in the context of the balancing exercise to which Nicholson J made reference in the passage quoted by Barrett J which I have set out.

25 There are a number of valuations in respect of the land at Bilambil Drive which are in evidence before me including in that regard the evidence given at trial. They provide on their face and if accepted, differing views as to the value of the land at differing times. It is that land that gives substance to the value in the units in the unit trust which are for sale. It is also that land which ultimately gives value to the worth of the superannuation fund interest of Mr Wilson which is the subject of the undertaking and in turn the proceeding brought by the Commissioner.

26 Another point which needs to be borne in mind in relation to the granting of any interlocutory injunctive relief arises from an observation made by Brennan J in Jackson v Sterling Industries Ltd (1987) 162 CLR 612 at 621:

The power to grant such an injunction does not support the making of an order which goes beyond what is in reasonable protection of a legal or equitable right which the court may enforce by judgment. To make an order giving an applicant, who has no more than a personal claim for damages, security for payment of an amount that might be awarded is to go beyond what is in reasonable protection of his right, for it would convert him from an unsecured creditor to a secured creditor.

[references omitted]

27 Against that background, it is worth recalling the terms of the undertaking which is the subject of the principal proceeding. Pursuant to that undertaking Interhealth undertook to do the following:

(a) Collect payment of unpaid distributions owed to the Interhealth Superannuation Fund by Greenhaven Unit Trust by 30 May 2008.

(b) Pay to Patrick Shaun Wilson his full superannuation entitlement by 30 May 2008.

(c) Provide evidence of the above to the Commissioner as regulator on or before 6 June 2008.

28 A principal issue in the substantive proceeding is whether or not those undertakings were complied with. It is neither necessary nor in any way desirable given that judgment is reserved to make any pronouncement as to whether those undertakings were or were not complied with. It is enough to observe that the Commissioner has on the evidence raised at the very least a serious question to be tried in relation to each of those issues, if not also a prima facie case at least. The question then becomes, having regard to the relief that might be given in the substantive proceeding under s 262A(4) of the SIS Act what is necessary or desirable in terms of s 313, if anything at all, to preserve the efficacy of the right that the Commissioner has sought to invoke.

29 What is to occur is a change in the composition of the assets which underlie the assets of the superannuation of the ISF. The undertaking was to collect unpaid distributions owed to Interhealth by the Greenhaven Unit Trust. In those circumstances it seems to me that a requirement pending the determination of the substantive proceeding or further earlier order that the second respondent, in other words the trustee of the Greenhaven Unit Trust, shall take all steps necessary to keep, maintain, preserve any moneys payable to it either from the sale of its units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments or from moneys payable from any other party including Probiotics Technologies Pty Ltd is necessary and desirable.

30 It likewise seems necessary and desirable, again pending the determination of the substantive proceeding or further earlier order to enjoin the second respondent as trustee of the Greenhaven Unit Trust from paying, disbursing, encumbering or disposing of in any way, other than by paying the same into a bank account in its name established for this purpose, any and all moneys received by it from the sale of its units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments or any moneys payable to it from any other party including Probiotic Technologies Pty Ltd. Given the very particular role which Ms Hambrook has in relation both to Interhealth and GHUT Holdings it seems to me necessary and desirable to order that not only the second respondent but also that she shall not give any direction to any person or entity be they Tweed Mortgage and Investments or Probiotic Investments Pty Ltd, the fourth respondent or otherwise, which would or would have the effect of preventing or inhibiting the payment of moneys due to Interhealth from the sale of GHUT Holding’s units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments Pty Ltd or preventing or inhibiting the payment of moneys due to Interhealth from any other entity including Probiotics Investments Pty Ltd.

31 Again, given the very particular roles which Ms Hambrook has, it seems to me necessary and desirable to order that, save in compliance with one of the orders herein, she in her private capacity as well as in her capacity as director or shareholder of any entity be restrained from entering into any arrangement or giving any direction which would prevent any sum being paid to Interhealth from the sale of GHUT Holding’s units in the Pelican Waters Unit Trust to Tweed Mortgage and Investments or from any other entity including Probiotics Investments Pty Ltd.

32 It also seems to me necessary and desirable, again subject to the limitation as depending on the determination of the substantive proceeding or further earlier order, that Interhealth should be ordered not to seek any indemnity from or from the assets of the Interhealth Superannuation Fund or any other entity for any cost incurred including legal costs as trustee of that fund.

33 The question then becomes as to whether additionally the fourth respondent, Merthyr Law, should be restrained from seeking or receiving any payment from the second respondent of any moneys otherwise due and owing under the charge that I identified. It is not for me today or even in the substantive proceeding to make any order in respect of the efficacy of that charge. The order that is sought in paragraph 7 of the draft orders by way of the restraint which I have mentioned seems to me not to be necessary or desirable in the sense that it would overreach the orders which may be made in the substantive proceeding and in effect convert an unsecured interest into a secured interest which took priority over a security which is in place pursuant to the deed of charge. Whether or not that deed of charge is in any way defective is a question which, if raised, would be one for determination in other proceedings. Those who are parties to that deed would take whatever moneys may come pursuant to it with that possibility existing. It would then become a matter for their prudent value judgment as to whether it was desirable to seek to rely upon that deed of charge.

34 I do not propose to make an order in terms of order 7 of the draft.

35 The intent therefore is that these orders do not prevent such payment, if any, as may be sought pursuant to that deed of charge from GHUT Holdings by Merthyr Law as chargee.

36 I should record as well that, in making the orders that I have, I have taken into account that the members of the superannuation fund concerned are twofold, Ms Hambrook as well as Mr Wilson. However, it is Mr Wilson’s interest in that fund which is the subject of the undertaking and which is in turn the subject of the relief sought in the substantive proceeding. The intention of the orders which I have made is to preserve the efficacy of whatever orders I may come to regard the Commissioner as regulator is entitled to and also to preserve thereby whatever benefit Mr Wilson or perhaps Mr Wilson’s bankrupt estate may gain from those orders.

37 I am otherwise minded just to order that the costs of each of the parties including the Commissioner be reserved but it does seem to me, having regard to the view that I have reached that the charge ought not to be subverted by an interlocutory order today that this requires separate provision. The Commissioner having sought in effect to do that, costs should follow that event in respect of that respondent to the interlocutory application. So the orders in respect of costs are that the Commissioner is to pay Merthyr Law’s costs of and incidental to the application to be taxed if not agreed and, save as aforesaid, the costs of each of the parties including the intervener are reserved.

38 I further order that all affidavits filed by leave or otherwise in the file which is presently QUD 461 of 2011 be uplifted from that file and filed in QUD 221 of 2010; that all affidavits and all applications and all outlines of submissions be uplifted and filed in 221; and that there be no further material filed in QUD 461 of 2011.

I certify that the preceding thirty-eight (38) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Logan. |

Associate:

SCHEDULE