FEDERAL COURT OF AUSTRALIA

McCluskey v Wieselmann, in the matter of Westmeats (Export) Pty Ltd (Receivers and Managers Appointed) (In Liq) [2011] FCA 1340

VICTORIA DISTRICT REGISTRY | |

GENERAL DIVISION | VID 850 of 2010 |

BETWEEN: | PETER DAMIEN MCCLUSKEY AND JAMES HENRY STEWART IN THEIR CAPACITY AS RECEIVERS AND MANAGERS OF WESTMEATS (EXPORT) PTY LTD (IN LIQUIDATION) (ACN 005 096 677) AND AS CONTROLLERS OF MARTMAN NOMINEES PTY LTD (IN LIQUIDATION) (ACN 005 996 190) AND OF CROWN MEATS PTY LTD (ACN 007 311 140) Plaintiff MARTMAN NOMINEES PTY LTD (IN LIQUIDATION) (ACN 005 996 190) Cross-Claimant

|

AND: | EILEEN WIESELMANN First Respondent MARTMAN NOMINEES PTY LTD (IN LIQUIDATION) (ACN 005 996 190) Second Respondent DAKIRI PTY LTD (ACN 005 709 517) Third Respondent CROWN MEATS PTY LTD (ACN 007 311 140) Fourth Respondent MARTIN WIESELMANN (AS EXECUTOR OF THE DECEASED ESTATE OF VICTOR WIESELMANN) Fifth Respondent HELEN BECK (AS EXECUTOR OF THE DECEASED ESTATE OF VICTOR WIESELMANN) Sixth Respondent ANEND PTY LTD (ACN 006 455 429) First Cross-Respondent CCM MANAGEMENT PTY LTD (ACN 079 333 378) Second Cross-Respondent CROWN MEATS PTY LTD (ACN 007 311 140) Third Cross-Respondent DAKIRI PTY LTD (ACN 005 709 517) Fourth Cross-Respondent OXHILL PASTORAL COMPANY PTY LTD (ACN 006 588 085) (IN LIQUIDATION) Fifth Cross-Respondent SOUTHERN CROSS FROZEN FOODS (VIC) PTY LTD (ACN 006 373 753) Sixth Cross-Respondent WESTMEATS (EXPORT) PTY LTD (ACN 005 096 677) (IN LIQUIDATION) Seventh Cross-Respondent WESTMEATS PTY LTD (ACN 004 879 136 (IN LIQUIDATION) Eighth Cross-Respondent MARTIN WIESELMANN Ninth Cross-Respondent |

JUDGE: | DODDS-STREETON J |

DATE: | 23 NOVEMBER 2011 |

PLACE: | MELBOURNE |

REASONS FOR JUDGMENT

Introduction

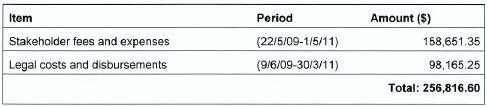

1 The applicants, Gess Rambaldi and David Vasudevan (“the liquidators”), as joint and several liquidators of Westmeats (Export) Pty Ltd (in liq) (“Export”), apply in proceeding VID 850 of 2010 for payment on an indemnity basis of their costs, fees and expenses for acting as stakeholders in a total sum of $256,816.60 excluding GST, made up as follows:

Category | Work commenced | Work finished | Amount claimed | Rambaldi affidavit | |

1. | Pre-litigation | 22/05/2009 | 11/10/2010 | $75,111.85 | [21]-[26] |

2. | Arrangements with receivers | 22/05/2009 | 11/10/2010 | $15,132.70 | [19] |

3. | Legal fees | 09/06/2009 | 06/10/2010 | $31,930.14 | [35] |

4. | Legal fees | 10/2009 | to date | $5,114.45 | [36] |

5. | Legal fees | 06/10/2010 | 30/03/2011 | $61,120.66 | [35] |

6. | This litigation | 12/10/2010 | 01/05/2011 | $53,587.60 | [31]-[34] |

7. | Re Broome properties | 12/10/2010 | 01/05/2011 | $13,004.20 | [27]-[30] |

8. | Receivers re Interpleader Orders | 12/10/2010 | 01/05/2011 | $1,815.00 | [16] |

2 An additional claim (category 9) related to legal fees incurred between 31 March 2011 and 31 August 2011 in the amount of $17,663.80. A claim for a further amount of $12,452.00 referred to in para [34] of the affidavit of Gess Rambaldi, discussed below, was not pressed.

3 The liquidators seek the payment of their remuneration and expenses from an amount of $300,000 (“fee escrow”) which was set aside for that purpose pursuant to consent orders made on 20 May 2011 (“Payment Orders”), which relevantly provided:

Payment from the fund

1. The liquidators of the seventh cross-respondent (Export), acting as stakeholders pursuant to the orders of the Honourable Justice Finkelstein dated 12 October 2010:

(a) by 20 May 2011, set aside $300,000 of the ‘Surplus’ referred to in that order (the fee escrow) for distribution in payment of their fees and expenses (including, for the avoidance of doubt, the stakeholder's legal costs and disbursements) (the stakeholders’ fees) by agreement of the respondents or order of the Court, with any remaining Surplus to be distributed in the manner set out in subparagraph (b) below;

(b) by 20 May 2011, distribute the remainder of the Surplus as is held in cash in the following manner:

(1) to the cross-claimant (Martman), 56.23%;

(2) to the fifth and sixth respondents, in their capacity as the executors of the deceased estate of Victor Weiselmann (Executors), 24.79%;

(3) to the third respondent (Dakiri), 12.19%; and

(4) to the fourth respondent (Crown), 6.78%;

(c) instruct a real estate agent, forthwith, to market and sell:

(1) the property known as unit 70, Cable Beach Sanctuary, 11 Oryx Road, Cable Beach in the state of Western Australia (described as volume 2615 folio 960) for no less than $260,000 on settlement terms of no longer than 60 days;

(2) the property known as unit 26, Cable Beach Sanctuary, 11 Oryx Road, Cable Beach in the state of Western Australia (described as volume 2609 folio 326) for no less than $300,000 on settlement terms of no longer than 60 days;

(d) in the event that either or both of those properties fails to sell in accordance with the terms set out in paragraph (c) within 90 days following the date of this order or as otherwise agreed by Dakiri, Crown, the Executors and Martman (the claimants), instruct the real estate agent to sell the properties at a public auction with a reserve price and by a date to be agreed by the claimants or set by order of the Court; and

(e) distribute the proceeds of sale of the properties in the manner set out in subparagraph (b) above.

4 The liquidators also seek liberty to apply in respect of any further fees and expenses incurred by them from 2 May 2011, as stakeholders, in accordance with the process contained in paragraph 10 of the Payment Orders.

5 The liquidators are not party to proceeding VID 850 of 2010 but are liquidators of the seventh cross-respondent in that proceeding.

6 The application was made and supported by:

(a) the affidavit of Gess Rambaldi sworn on 2 September 2011;

(b) the affidavit of David Vasudevan sworn on 22 September 2011;

(c) written submissions of the liquidators filed on 23 September 2011; and

(d) supplementary written submissions of the liquidators filed on 25 October 2011.

7 The liquidators’ application for payment in the amount claimed was opposed by Martman Nominees Pty Ltd (in liq) (“Martman”), the second respondent and cross-claimant in the proceeding.

8 Martman relied on:

(a) the affidavit of its liquidator, Kenneth Wayne Lamb, sworn on 21 September 2011;

(b) written submissions of Martman dated 21 September 2011; and

(c) further written submissions of Martman dated 31 October 2011.

Background and evidence

9 The background to the application, as appears from the materials filed, was largely undisputed.

10 Martman, Export and seven other entities were members of a corporate group (“the Westmeats Group”).

11 Between 1991 and 2008, Westpac advanced money to companies including Export, and was granted a number of mortgages and charges as security for the advances. In 2007, by two instruments of guarantee and indemnity, Export and others executed an Interlocking Guarantee and Indemnity with Westpac, whereby the guarantors guaranteed and indemnified Westpac in relation to the payment by Export of the guaranteed money and the performance of the guaranteed obligations.

12 In 2008, Export and other companies in the Westmeats Group defaulted in their payments due to Westpac. As at 28 August 2008, the Westmeats Group owed Westpac approximately $13,690,583. Each relevant member of the Westmeats Group failed to satisfy demands for payment.

13 On 29 August 2008, Peter McCluskey and James Stewart of Ferrier Hodgson (“the receivers”), were appointed by Westpac as, inter alia, receivers and managers of Export and controllers of various other companies in the Westmeats Group.

14 On 8 December 2008, liquidators were appointed to Export pursuant to a resolution of its creditors.

15 Following their appointment, the receivers began to realise certain assets of various companies in the Westmeats Group over which Westpac held security. After August 2008, the indebtedness of the Westmeats Group to Westpac was progressively reduced and ultimately discharged by application of the proceeds of sale of various properties. It was not disputed that the Westmeats Group liability to Westpac was discharged by June 2009.

16 By October 2009, the receivers also held a surplus of approximately $1,285,000 in cash on behalf of Westpac in relation to Export (“the surplus”). It was not disputed that Export owed Westpac the largest amount of any group member and that its debts had been met largely from the proceeds of sale of other group members’ assets. As a result, the surplus fund largely comprised the property of Export, but subject to the other group members’ claims of contribution and subrogation.

17 The receivers wished to retire from and terminate their remaining appointments including to Export, by transferring the surplus to the liquidators of Export but, as Mr McCluskey deposed, were prevented from doing so by an ongoing dispute between the guarantors and the receivers regarding the distribution of the surplus.

18 Between 22 May 2009 and 11 October 2010, the liquidators undertook activities pursuant to an arrangement with the receivers, including in relation to subrogation claims to the surplus fund, as Mr Rambaldi deposed in paragraphs 21 to 26 of his affidavit, for which they claim $75,111.85 (under category 1) and as deposed in paragraph 19 of his affidavit, for which they claim $15,132.70 (under category 2).

19 By a letter dated 16 September 2010, the solicitors for the receivers requested “unequivocal confirmation” from the relevant parties of their agreement to the proposal whereby the liquidators would hold the surplus funds and remaining assets on trust, in their capacity as stakeholders, failing which they would apply to the court for directions under the Corporations Act 2001 (Cth).

20 As the subrogation claims were not resolved, the receivers, by an originating process dated 5 October 2010, sought, inter alia, directions and declarations in respect to the subrogation claims and an order that they were justified in paying to the liquidators of Export the surplus of monies held by them upon realisation of the securities under which they were appointed.

21 Finkelstein J on 12 October 2010 ordered that the liquidators be appointed stakeholders of the surplus. His Honour also made directions for the interpleader application, requiring any person having a claim in respect of the surplus, inter alia, to file a notice with the court.

22 The receivers then retired and transferred the surplus to the liquidators as stakeholders.

23 In March 2011, Martman filed a cross-claim against certain Westmeats Group entities.

24 The interpleader and cross-claim within this proceeding were mediated on 1 April 2011 and the Payment Orders of 20 May 2011 were made.

25 Following the making of the Payment Orders, the liquidators:

(a) set aside $300,000.00 of the Surplus (the Fee Escrow) and distributed the balance of the surplus to the claimants; and

(b) instructed a real estate agent to market and sell the Broome Properties.

26 The Broome Properties were marketed, but failed to sell within 90 days of the Payment Orders.

Affidavit of Gess Rambaldi

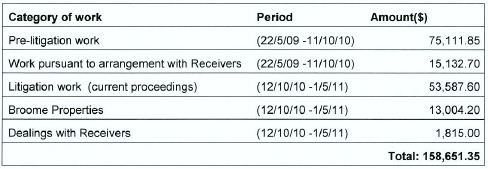

27 Mr Rambaldi deposed that the stakeholders’ fees and expenses to 1 May 2011 totalled $256,816.60 inclusive of GST, made up as follows:

28 Mr Rambaldi deposed that stakeholders’ fees and expenses in the sum of $158,650.80, including GST, fell into the following general categories:

Category 1 - $75,111.85 for the liquidators’ pre-litigation work

29 In paragraphs 21 to 26 of his affidavit, Mr Rambaldi deposed that between 22 May 2009 and 11 October 2010 (ie for about 18 months prior to the appointment of stakeholders), the liquidators incurred fees and expenses “in considering the merits of the subrogation claims and in corresponding, negotiating, conferencing and tendering proposals in relation to the same”.

30 Mr Rambaldi deposed that in that context, the liquidators made proposals and arranged various meetings and discussions throughout the relevant period with a view to facilitating the receivers’ retirement and dealing with the subrogation claims.

31 Mr Rambaldi exhibited relevant correspondence (Exhibit GMR12). The correspondence included Mr Rambaldi’s letter to the receivers dated 12 June 2009 noting their advice that the Westpac debt was paid in full, that the receivers were no longer being paid and wished to retire but were confronted by subrogation claims to the fund by related entities, and that a number of the company’s assets needed to be realised, including debtors, real estate in Western Australia and related party loan accounts. Mr Rambaldi’s letter proposed that the surplus funds be paid to the liquidators pending resolution of the subrogation and other claims and that the liquidators would realise the remaining assets, reserving the rights of related entities and other relevant creditors to the surplus funds on the basis that their costs directly attributable to the asset realisation would be deducted from the proceeds and be secured by a lien against such assets.

32 By a letter to the liquidators dated 15 September 2009, the receivers agreed that the liquidators should instruct valuers for the Broome properties, deal with the collection of outstanding trade debtors and could pursue recovery actions in respect of related party loans, which the receivers had not actively pursued. The letter declined to release the funds and stated that there was little information about subrogation claims at that stage.

33 In a letter to the liquidators dated 25 January 2010, Martman asserted a right of subrogation over the surplus and would not agree to any transfer of the surplus to the liquidators unless it were paid into a trust account controlled by the liquidator “as stakeholder and not as liquidator”.

34 The letter of Frenkel Partners (solicitors for the liquidators and Export) dated 21 May 2010 to the receivers’ solicitors confirmed that Westpac would assign Export’s fixed and floating charge to entities associated with Mr Weiselmann, and that the liquidators would continue to seek recovery of Export’s assets, would review the value of the security and would determine on submissions and evidence the value of the subrogated claims.

35 A letter of Harrick Lawyers (solicitors for Mr Wieselmann) dated 25 May 2010 to Frenkel Partners asserted its client’s right to be subrogated to Westpac’s rights and discussed the liquidators’ future role in continuing to recover Export’s assets.

36 Further exhibited correspondence between Frenkel Partners, the solicitors for the receivers and related parties occurred between June 2009 and September 2010 in relation to the liquidators’ proposed preliminary determination and quantification of subrogated claims, pending the payment of the surplus into a separate interest bearing account, and their continued recovery and realisation of remaining assets subject to the security, subject to their entitlement to reasonable costs and expenses.

37 By a letter of 9 September 2010, the liquidators, through their solicitors, confirmed that they would “hold the Surplus Funds and Remaining Assets in trust as stakeholders” pending the resolution of the claims for subrogation.

38 In relation to the liquidators’ activities during the period 22 May 2009 to 11 October 2010, Mr Rambaldi deposed:

25. I believe that this process was necessary to address the subrogation claims, it was conducive to the retirement of the Receivers, it assisted the parties in crystallising their positions and understanding their respective obligations and that it was the Liquidators' responsibility in all the circumstances to have ensured that the subrogation claims, the Surplus and remaining assets were dealt with appropriately, and, if possible, without the parties' incurring the costs of court proceedings.

26. Further, this work was also carried out by the Liquidators on the advice of the Receivers’ that their retirement was always imminent and subject to the finalisation of their accounts and administrative matters.

Category 2 - $15,132.70 for work pursuant to the arrangement with receivers from 22 May 2009 to 11 October 2010

39 In paragraph 19, Mr Rambaldi deposed that between June 2009 and September 2009 (prior to the commencement of the proceeding), the liquidators and receivers had arranged a strategy to realise Export’s remaining assets including its Broome properties, trade debtors and related party debtors, with Westpac’s consent. Under the arrangement, the liquidators were to commence recovery of the debts and obtain an independent valuation of the Broome properties. The activities of the liquidators and their lawyers would separately be recorded and the costs deducted from the recovery proceeds. Exhibits GMR9 to GMR11 related to this claim. Mr Rambaldi deposed that the liquidators had received no costs or expenses for any work performed pursuant to their arrangement with the receivers to date.

Categories 3, 4 and 5 –$98,165.25 for legal costs and disbursements for the period 9 June 2009 to 30 March 2011

Categories 3 and 5 – in relation to subrogation claims

40 Mr Rambaldi, in paragraph 35, exhibited a draft tax invoice of Frenkel Partners, the liquidators’ legal advisers, totalling $93,050.80 inclusive of GST for the period 9 June 2009 to 30 March 2011 “in respect of work carried out by [Frenkel Partners] in relation to the subrogation claims, excluding any work done or costs incurred in relation to Export’s debtor recoveries” (Exhibit GMR17). The amount was broken down as follows:

(a) $31,930.14 for the period from 9 June 2009 to 6 October 2010; and

(b) $61,120.66 for the period from 6 October 2010 to 30 March 2011.

Category 4 – in relation to debtor recoveries

41 In paragraph 36, Mr Rambaldi further deposed to and exhibited invoices in relation to $5,114.45, inclusive of GST, for work performed and disbursements incurred by Frenkel Partners in relation to the Export debtor recoveries pursuant to the agreement with the receivers (Exhibit GMR18).

Category 6 - $53,587.60 for liquidators’ work and expenses as stakeholders in current proceedings – from 12 October 2010 to 1 May 2011

42 Under the heading “litigation”, in relation to the periods 7 March to 27 March 2011 and 28 March 2011 to 1 May 2011, Mr Rambaldi exhibited, in GMR15 and GMR16, summaries of work which he deposed the liquidators performed and expenses they incurred as stakeholders in respect of the current proceedings, excluding legal costs.

Category 7 - $13,004.20 for the Broome properties

43 In paragraphs 27 to 30, Mr Rambaldi deposed in relation to the Broome properties:

27. Shortly after the Receivers retired pursuant to Justice Finkelstein's orders, made 12 October 2010, I wrote through my solicitors, Frenkel Partners, to the parties' solicitors proposing that the Broome Properties' ongoing expenses (i.e. utilities and body corporate fees) together with my professional fees in administering the properties, be paid from rental income generated from those properties (held in a special purpose account operated by me) and any shortfall from the Surplus…

28. I was unable to obtain agreement to this proposal from all parties.

44 Mr Rambaldi exhibited in GMR14 a detailed summary of tasks undertaken and costs (including expenses) which he deposed were incurred by him and his staff as stakeholders, for the period 12 October 2010 to 1 May 2011 relating to the maintenance and administration of the Broome properties, in respect of which the stakeholders have yet to receive payment.

45 He further deposed:

30. Since this time, additional fees and expenses have been incurred in maintaining and administering the Broome Properties in the sum of $5,683.00 plus GST (being the period 2 May 2011 to 21 August 2011) which is not included in the table subjoined to paragraph 16 of this my affidavit. Running expenses have been met from rental proceeds.

46 Martman did not dispute the liquidators’ entitlement to payment of category 7.

Category 8 - $1,815 for receivers’ claim in relation to interpleader orders

47 Martman did not dispute the liquidators’ entitlement to payment of category 8.

Category 9 - “additional $17,663.80” for legal fees for the period 31 March 2011 to 31 August 2011

48 In paragraph 37, Mr Rambaldi deposed that additional legal costs totalling $17,663.80, including GST and disbursements, but excluding counsel's fees, were incurred for the period from 1 April 2011 to 31 August 2011, which Frenkel Partners informed him did not include any costs associated with debtor recoveries, according to invoices exhibited in GMR19.

“Additional $12,452” – for stakeholders’ fees and expenses

49 In paragraph 34, Mr Rambaldi also deposed to fees and expenses (excluding legal costs) incurred by the stakeholders incurred since 1 May 2011 as follows:

34. Since 1 May 2011, the stakeholders have incurred further fees and expenses (excluding legal costs) in relation to the current proceedings in the sum of $12,452.00 plus GST (being for the period 2 May 2011 to 21 August 2011).

At the hearing of the application, senior counsel for the liquidators made clear that they made no claim for that amount.

50 Mr Rambaldi deposed that Export’s creditors approved payment of the administrators’ remuneration of $62,861 (from 29 August 2008 to the conclusion of the voluntary administration) and liquidators’ remuneration of a total of $148,872 (from 8 December 2008 to 31 October 2010), none of which had been paid.

Affidavit of David Vasudevan

51 Mr Vasudevan exhibited the Export liquidators’ report to creditors dated 10 November 2010 and a summary schedule of liquidators’ fees and expenses which he deposed were incurred by the liquidators in their capacity as liquidators of Export from 8 December 2008 to 1 May 2011, and excluded costs directly attributable to the maintenance and administration of the Broome properties. The liquidators’ remuneration of $219,585 plus GST, expenses of $6,352.40 plus GST, and the voluntary administration costs of $62,861 due to the liquidators, were wholly unpaid.

Affidavit of Wayne Lamb

52 Mr Lamb, the liquidator of Martman, in opposition to the liquidators’ application, deposed that the only claim which was clearly identifiable as part of the stakeholders’ fees and expenses was the sum of $13,004.20 covering the period 12 October 2010 to 1 May 2011 relating to the Broome properties.

53 Mr Lamb observed that the costs and expenses referred to in paragraphs 15, 16 and 35 of Mr Rambaldi’s affidavit were for a period which began prior to appointment as stakeholder. Further, the liquidators’ circular to creditors included a report dated 10 November 2010 which indicated that the liquidators were seeking advice and would take action as to their entitlement to the surplus funds and the unsecured creditors’ rights.

54 Mr Lamb deposed that in April 2011, Mr Rambaldi discussed with Mr Lamb his claim for professional fees and expenses and agreed to provide more detailed information of the breakdown directly related to his role as stakeholder.

DISCUSSION

55 In the present case, the liquidators claimed payment from the fee escrow on the potentially overlapping bases of entitlement as a stakeholder and the principle in Re Universal Distributing Co Ltd (in liq) (1933) 48 CLR 171 (“Universal Distributing”).

56 The liquidators acknowledged that some of the amounts claimed related to fees, costs, expenses and legal costs for work they performed prior to their appointment as stakeholders, but submitted that the relevant amounts directly related to and were necessarily incurred in their roles as stakeholders, and, or alternatively, in the care, preservation or realisation of the surplus fund in accordance with the Universal Distributing principle.

57 The liquidators bore the onus of establishing their entitlement to payment from the fee escrow in the amount claimed. In that context, it was necessary to establish that work or expenses of the general description in each major category satisfied the requirements of stakeholder entitlement discussed in relevant authority or the Universal Distributing principle, and, further, if so, that individual items of work or expenditure for which claims were made under each major category fell within it and were reasonably undertaken or incurred, and that the charges were reasonable.

58 In relation to their claim as stakeholders, the liquidators relied on McPherson Thom & Co v Coombie Pastoral Co Pty Ltd [1929] VLR 295 (“McPherson”), where an interpleader summons was taken out by stock auctioneers confronted with conflicting claims to the proceeds of sale of certain sheep. The auctioneers, who had “no interest whatever in the subject-matter of the claims” (at 299), sought a complete indemnity for their costs.

59 Lowe J acknowledged the dearth of specific authority, but accepted that the interpleader provision in the court’s rules conferred the power to make such orders as to costs as were just and equitable.

60 Lowe J stated at 301:

In my judgment, the rule to be deduced from these cases in regard to costs is that where the applicant on an interpleader summons has come promptly to the Court when faced with conflicting claims, and has been guilty of no conduct which has increased costs, prima facie he should have a complete indemnity, so far as the fund will permit, for his costs; that is to say, he is prima facie entitled in such circumstances to his costs as been solicitor and client. In most cases of interpleader, however, the proceedings on the part of the applicant are of the simplest nature, and his costs should not require to be taxed in order that he should have full indemnity. In such cases – and these I think will be the general rule – the Judge on the hearing will fix the costs of the applicant at an amount which will give that indemnity. The rule which I have now declared records with what, in my experience, has been the practice in the past.

61 In Kennett v Charlton [2007] NSWSC 190 (“Kennett”), a solicitor who had received conflicting instructions from disputing interested parties about the payment of certain funds he held, sought his costs of corresponding about the disposition of the funds, negotiating with the rival claimants and his interpleader summons issued when the matter failed to settle. Gzell J allowed the solicitor the costs of his dealings and negotiations with the parties prior to issuing the application and of the application itself on an indemnity basis. Gzell J stated that the solicitor (who prior to the payment into court was a trustee with a right to exoneration and reimbursement from the trust fund) fell within the McPherson stakeholder principle and should not be out of pocket as a result of dealing with the rival claims to the fund he held.

62 In Universal Distributing, the liquidator of an insolvent company realised its assets subject to a debenture charge. The proceeds of the realised assets subject to the charge were not sufficient to pay the debenture holder in full and it was unlikely that any funds would be available for unsecured creditors.

63 Dixon J stated that, while the security was paramount to the general costs and expenses incidental to the realisation of the assets, the expenses attendant upon the realisation of the fund affected by the security must be borne by it (at 174). The debenture holders were creditors of the company with a specific right to the property for the purpose of paying their debts, and if it were realised instead by the liquidator, “the proceeds must bear the cost of the realization just as if they had begun a suit for its realization or had themselves realized it without suit” (at 174).

64 Dixon J discussed relevant authority and further stated (at 174):

In applying this principle, only those expenses appear to have been thrown against the fund belonging to the debenture-holders which have been reasonably incurred in the care, preservation and realisation of the property. In the present case the liquidator has employed a material part of his time and energies in recovering moneys, both uncalled capital and debts, which enure for the debenture-holder, and in so far as these services increase the remuneration which he receives, I see no reason why the burden should not be thrown upon the proceeds. The question is not whether moneys available for unsecured creditors should be relieved at the expense of the security. In such a case it may be said that the service of collecting enough to discharge the debenture must in any event be performed in order that a surplus may then arise in which the unsecured creditors may participate. The question in the present case is whether the liquidator can charge against the fund passing through his hands, as between himself and the person to whom it is payable, so much of the remuneration fixed for work done in the winding up as is referable to the calling in and conversion of the assets producing the fund. I see no reason why remuneration for work done for the exclusive purpose of raising the fund should not be charged upon it.

65 In Re S&D International Pty Ltd (in liq) (recs and mgrs apptd) [2009] VSC 225 (“S&D”), Robson J analysed the decision in Universal Distributing extensively (at [255] to [257] and [261]).

66 His Honour stated (at [257] and [261]):

Dixon J speaks of the expenses as being “thrown against the fund.” The equitable claim is against the fund irrespective of those claiming an interest in the fund. The expenses incurred must have contributed to the funds realization, care or preservation. Dixon J recognised that this right against the fund is independent of any conduct of others laying claim to the fund which might otherwise have given rise to some claim as between the parties.

…

In Hewett v Court Deane J addressed the nature of an equitable lien generally. He said:

An equitable lien is a right against property which arises automatically by implication of equity to secure the discharge of an actual or potential indebtedness … Though called a lien, it is, in truth, a form of equitable charge over the subject property … in that it does not depend upon possession and may, in general, be enforced in the same way as any other equitable charge, namely, by sale in pursuance of court order or, where the lien is over a fund, by an order for payment thereout … (citations omitted).

Importantly, for this case, these principles confirm that the liquidator may assert a lien even though he is not in possession of the fund and may enforce it by an order for payment out.

(citation omitted)

67 Robson J discussed Commonwealth Bank of Australia v Butterell (1994) 35 NSWLR 64, where Young J reiterated at 71 that it was necessary to distinguish between the general costs of the administration and the costs of preservation of the property. If something fell within the general costs of administration because its sole purpose was not to preserve or realise the property, then the secured creditor would take in priority to the person whose efforts brought about the production of the fund.

68 Young J held at [72] to [73] that the administrators’ remuneration would not fall under the equitable lien unless their time was exclusively directed to the realisation of the fund passed over to the receivers. The administrators could not be remunerated for time spent on statutory duties and time spent on a heterogeneous group of problems.

69 In S&D, Robson J distilled the relevant principles at [273] as follows:

From these authorities the following principles referrable to a liquidator may be stated:

(a) At equity, an equitable lien arises in favour of a liquidator over the funds realised from the sale of company property for the costs he incurs for the care, preservation and realisation of the property in priority to those otherwise interested in the fund…

(b) The costs include those that the liquidator fairly incurs in the discharge of his duty to care, preserve and realise the property...

(c) The lien may arise whether or not the ultimate sale is affected by the liquidator and entitles the liquidator to be paid in priority out of the fund whether or not he is in possession of the fund…

(d) The costs and expenses secured by the lien must be incurred exclusively for the care, preservation or realisation of the property and not otherwise expended in the general administration of the mortgagor...

(e) The costs and expenses include the liquidator’s reasonable remuneration…

(citations omitted)

70 In S&D, the liquidator, who did not realise the fund himself, nevertheless recovered it from persons who would probably have dissipated it. Robson J found that the fund in specie would have been lost but for the liquidator’s actions. His Honour held that the liquidator’s costs and expenses directed exclusively towards recovering the fund and delivering it to the safety of the court were covered by a lien conferring priority to all other claimants. His Honour allowed the liquidator reasonable remuneration exclusively for that purpose.

71 Robson J did not consider that the lien covered the liquidator’s costs and expenses for his prior actions in investigating and making inquiries of the fund, or for general correspondence, which did not preserve the fund but merely sought to identify it, and were part of the liquidator’s general duties.

72 In the present case, while acknowledging the potential overlap between their concurrent roles as liquidators of Export and stakeholders, the liquidators submitted that the court should approach their present claim robustly. Senior counsel for the liquidators submitted that the evidence established that, independently of the work claimed for in this application, they had carried out a significant number of activities and incurred expenses in the general administration of Export, for which significant remuneration was approved, albeit it remained unpaid. Those costs and expenses, including of investigating whether the unsecured creditors had any entitlement to the surplus, were thus separately charged for and were excised from the present claims, which did not relate to the liquidators’ general administration duties incumbent on them in that capacity.

73 Martman conceded that the amounts of $13,004.20 and $1,815 including GST (categories 7 and 8) were properly incurred, reasonable in quantum and should be paid from the fund.

74 Martman nevertheless objected to payment of the claims comprising categories 1 and 2 (and, by necessary implication, to dependent claims under other categories). It submitted that, as a matter of principle, entitlement to payment of categories 1 and 2 from the fee escrow was not made out under either the stakeholder or the Universal Distributing principle, which applied only to costs exclusively incurred as a stakeholder or for the care, preservation and realisation of the relevant property. In Martman’s submission, the activities described in categories 1 and 2 fell within the general administration of Export.

75 As an alternative or subsidiary submission, Martman contended that if payment for categories 1 and 2 were justified as a matter of principle, the liquidators’ evidence did not establish the accuracy of their characterisation of their work and expenses, or exclude overlap with their general administration duties. Nor did the liquidators’ evidence establish the reasonableness of performing particular tasks, incurring particular expenses or the quantum claimed for them.

76 While in written submissions Martman conceded that the liquidators as stakeholders were effectively trustees of the surplus fund and entitled to remuneration and costs for work incurred in the proper administration of the trust under s 77 of the Trustee Act 1958 (Vic) or in equity, it submitted that there was no general rule entitling a stakeholder to remuneration or fees, and any such entitlement related only to the time that property was held pending resolution of the dispute. It relied, in that context, on De Rothschild Freres v Morrison, Kekewich & Co (1890) 24 QBD 750.

77 Before me, however, counsel for Martman conceded that the liquidators were entitled to payment for work carried out as a stakeholder before their formal appointment. Martman also acknowledged the potential overlapping application of the Universal Distributing principle, but submitted that it required the claimants’ efforts to increase the relevant fund. Martman submitted, however, that any injustice occasioned by the exclusivity requirement could be tempered by making a proportionate allowance.

Categories 1 and 2

78 In my opinion, the liquidators’ activities prior to 12 October 2010 in considering the subrogation claims and corresponding, negotiating, conferencing and tendering proposals to achieve an accommodation and avoid litigation fell, as a matter of substance, within the ambit of the stakeholder role, albeit performed by the liquidators as the de facto delegate of the receivers.

79 Prior to the liquidators’ formal appointment as stakeholders, the surplus fund, the remaining Broome properties, the related party debts and other uncollected debts were subject to the security and remained in the receivers’ control and possession. The receivers, once the debt to Westpac was discharged, essentially held the surplus fund and other assets in the character of stakeholders, who did not claim any interest on their client’s behalf. In such circumstances, contrary to Martman’s submission, the liquidators were not obliged and had no right (without the receivers’ authority and consent) to deal with or perform activities in relation to the surplus fund or other assets.

80 The competing subrogation claims to the surplus fund (and any unrealised assets which might enhance it) precluded the receivers’ retirement, and they assented to the liquidators’ role in attempting to resolve them.

81 While the liquidators were obliged, as an aspect of the general administration of Export, to investigate whether the unsecured creditors may have an interest in the surplus fund after satisfaction of the secured creditor’s and subrogation claims, the liquidators submitted that they claimed for such work separately, in the liquidation.

82 It was not suggested that the unsecured creditors of Export received any dividend or other advantage from the surplus fund or that funds were available to satisfy their claims or to pay the liquidators’ remuneration. Thus, as in Universal Distributing, “the service of collecting enough to discharge the debenture” (or the claims of those subrogated to the debenture holder) was not performed in order to achieve a surplus in which the unsecured creditors could share.

83 Martman submitted that the liquidators’ evidence, including the narratives in the exhibited summaries, did not clearly link their claims in categories 1 and 2 to work done as a stakeholder or to preserve the surplus fund, or sufficiently exclude work properly attributable to general administration.

84 Mr Rambaldi deposed, however, that the claim in category 1 was for considering the merits of the subrogation claims and corresponding, negotiating, conferencing and entering proposals in relation to them, where, on the liquidators’ evidence, they undertook separate work and incurred separate expenses in the general liquidation for the benefit of Export’s unsecured creditors.

85 Messrs Rambaldi and Vasudevan were not cross-examined. The documents they exhibited indicated that reports were provided, meetings held and other activities undertaken in the general administration of Export. Neither the exhibited documents nor any evidence filed on behalf of Martman negatived the liquidators’ evidence.

86 In the circumstances, the principles of stakeholder entitlement and, or alternatively, Universal Distributing, would apply to the costs, remuneration and expenses of the liquidators’ activities described under category 1 in relation to the subrogation claims, consistently with the analysis in Kennett, and under category 2 pursuant to the arrangement with the receivers to realise Export’s Broome properties, outstanding trade debtors and related party debtors subject to the security. There is, in my opinion, no requirement to demonstrate that the efforts increased the fund. Further, the evidence, when read in context, in my opinion sufficiently established that the liquidators performed the relevant work and incurred the expenses for the purposes they stated.

87 So to conclude does not, however, resolve the question whether each individual item claimed under categories 1 and 2 should be allowed at all or in the quantum claimed, as the performance of the work, the incurring of the expense and the quantum of the remuneration or charge must be reasonable. Those questions should be referred for determination to a Registrar who should fix the liquidators’ remuneration, costs and expenses in accordance with these reasons and who may make directions for the filing of any further evidence and written submissions and, if appropriate, a hearing.

Category 6

88 Consistently with the reasoning above, and in particular the analysis in McPherson, the liquidators are, as a matter of principle, entitled to payment from the fee escrow for work performed and expenses incurred by them (excluding legal costs) in respect of the current interpleader litigation from their appointment on 12 October 2010 to 1 May 2011 as described in category 6, subject to the proviso and referral discussed in paragraph [87] above.

Categories 3, 4, 5

89 The above comprise legal fees incurred by the liquidators in relation to particular activities during different periods. The liquidators’ entitlement as a matter of principle to payment for the legal costs in categories 3, 4 and 5 follow from the conclusions on category 1, to which they relate, but is subject to the proviso and referral discussed in paragraph [87].

Category 9

90 Mr Rambaldi’s affidavit did not clearly identify the purpose for which the legal fees in category 9 were incurred, but the exhibited summaries suggested that it was, inter alia, to establish, by the present application, the liquidators’ entitlement to the payment from fee escrow of their claims as stakeholder. Such costs are integrally connected with their role as stakeholders and, subject to the proviso and referral discussed in paragraph [87], would, in my opinion, be payable from the fee escrow.

CONCLUSION

91 For the reasons stated above, the liquidators are entitled as a matter of principle to payment of their remuneration, costs and expenses from the fee escrow for work and expenses claimed in categories 1 to 9 which was reasonably done or were reasonably incurred, in a reasonable quantum. The matter should be referred to a Registrar for the fixing, in accordance with these reasons, of the liquidators’ remuneration, costs and expenses.

I certify that the preceding ninety-one (91) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Dodds-Streeton. |

Associate: