FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Letten (No 16)

[2011] FCA 1308

IN THE FEDERAL COURT OF AUSTRALIA | |

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

AND: | First Defendant (and others according to the attached schedule) |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

1. By 4:00pm on 18 November 2011, the parties bring in orders to give effect to these reasons for decision.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

VICTORIA DISTRICT REGISTRY | |

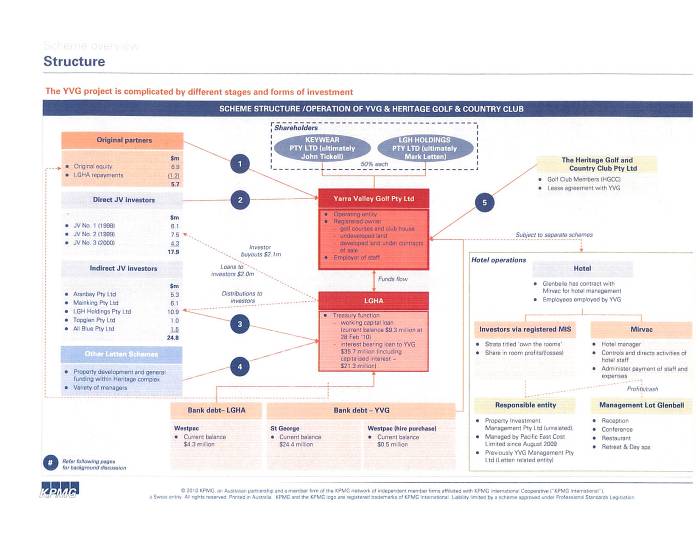

GENERAL DIVISION | VID 95 of 2010 |

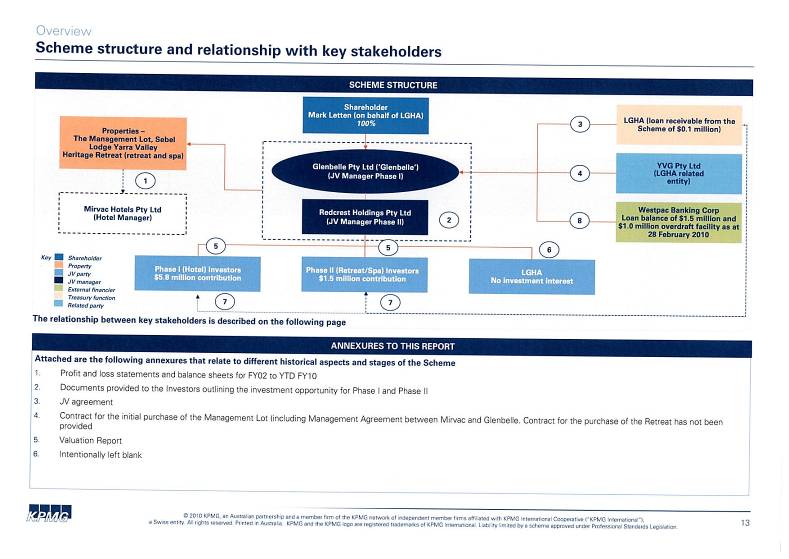

BETWEEN: | AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff

|

AND: | MARK RONALD LETTEN First Defendant (and others according to the attached schedule) |

JUDGE: | GORDON J |

DATE: | 16 NOVEMBER 2011 |

PLACE: | MELBOURNE |

REASONS FOR JUDGMENT

INTRODUCTION

1 By a contract of sale dated 18 February 2011, Mr Damian Templeton and Mr Phillip Hennessy of KPMG as the receivers and managers of Glenbelle Pty Ltd (Receivers and Managers Appointed) (in liquidation) (the Receivers) sold to Golden Heritage Golf Pty Ltd (GHG) the Management Lot of The Sebel Heritage Yarra Valley for $4 million subject to a number of special conditions (the Contingency Contract).

2 Special condition 24.2 of the Contingency Contract provided:

This contract is subject to the conditions subsequent that:

(a) the Existing Contract [defined to mean the contract of sale of the Management Lot between the Vendor and Wilhelmus Boerkamp dated 3 February 2011] is validly terminated in circumstances where the Vendor, acting reasonably, considers that termination of the Existing Contract is unlikely to be the subject of dispute, including the subject of court proceedings; and

(b) the Responsible Entity:

(i) waives its rights under clause 22.6 of the Hotel Management Agreement in respect of this contract, on terms to the reasonable satisfaction of the Vendor; or

(ii) fails to accept an offer made by the Vendor in accordance with clause 22.6(a) of the Hotel Management Agreement within the relevant time period,

or there is a combination of the matters referred to in paragraphs (i) and (ii).

Throughout these Reasons for Judgment, the “Existing Contract” is referred to as the “Boerkamp Contract”.

3 As Senior Counsel for GHG put at it the first directions hearing, GHG “don’t have an interest in completing under the Contingency Contract”. GHG initially contended that special condition 24.2(a) had not been fulfilled. In particular, GHG contended that:

1. the Boerkamp Contract had not been validly terminated; or

2. if the Boerkamp Contract had been validly terminated, it was not terminated in circumstances where the Receivers (as Vendor), acting reasonably, considered that termination of the Boerkamp Contract was unlikely to be the subject of dispute, including the subject of court proceedings.

4 Further, GHG contended that on the proper construction of the Contingency Contract it was not obliged to perform any obligations under special condition 24 (that it must use reasonable endeavours to assist the Receivers to satisfy the conditions referred to in special condition 23.1, including consent from the Responsible Entity) until the conditions contained in special condition 24.2 have been fulfilled, which has not yet occurred.

5 Just before the hearing, GHG filed an amended statement of case in which it “no longer pressed” the contentions in [3(1)] and [4] above. For the reasons that follow, I reject GHG’s remaining contention.

facts

6 The facts are addressed under the following headings:

1. The Schemes and the Receiverships: [7] to [17];

2. The Management Lot: [18] to [31];

3. The Contingency Contract: [32] to [35]; and

4. Steps after Day of Sale and execution of contracts: [36] to [46].

(1) The Schemes and the Receiverships

7 On 25 February 2010, the schemes numbered 1, 4 to 9 and 13 to 16 in Annexure A to the Order made on 25 February 2010 were wound up pursuant to s 601EE(1) of the Corporations Act 2001 (Cth) (the Corporations Act). Also on 25 February 2010, the Receivers were appointed as joint and several receivers and managers of certain property of each of the second to sixteenth and eighteenth to forty-fifth defendants (the Corporate Defendants) and as joint and several receivers and managers of identified property of each of the schemes listed in Annexure A (the Schemes) except for the scheme numbered 12: Australian Securities and Investments Commission v Letten [2010] FCA 140 (the 25 February Orders).

8 The 25 February Orders required the Receivers to file and serve a report in respect of, inter alia, the nature and identity of the property of each Scheme, any claims by third parties in relation to the property of each Scheme and the identities of investors and the nature of their investments (the Disclosure Reports).

9 On 13 April 2010, the Receivers filed Disclosure Reports in relation to each Scheme except for Schemes numbered 6, 15 and 16. The Disclosure Reports for Schemes numbered 6, 15 and 16 were filed on 28 April 2010.

10 This judgment concerns Schemes 15 (the Yarra Valley Golf Joint Venture Scheme) and 16 (the Glenbelle Project Scheme).

11 On 25 February 2010, the Court ordered that:

1. pursuant to s 1323(1)(h)(ii) of the Act the Receivers be appointed to the property of, inter alia, the twenty-first to forty-fifth defendants (the YVG Parties) and the twenty-ninth and thirty-sixth defendants (the Glenbelle Parties), other than property that constitutes property of a Scheme as defined in Annexure A to the Order;

2. the Yarra Valley Golf Joint Venture Scheme and the Glenbelle Project Scheme (each a Scheme) be wound up pursuant to s 60IEE(1) of the Act; and

3. the Receivers be appointed as receivers and managers of the Property of, inter alia, the Yarra Valley Golf Joint Venture Scheme and the Glenbelle Project Scheme.

12 In his disclosure report in relation to the Yarra Valley Golf Joint Venture Scheme, Mr Templeton (one of the Receivers) provided a diagrammatic and descriptive overview of the scheme structure and the relationship with key stakeholders (the Yarra Valley Overview). A copy of the Yarra Valley Overview is Annexure A to these reasons for decision.

13 In his disclosure report in relation to the Glenbelle Project, Mr Templeton provided a diagrammatic and descriptive overview of the scheme structure and the relationship with key stakeholders (the Glenbelle Overview). A copy of the Glenbelle Overview is Annexure B to these reasons for decision.

14 On 4 June 2010, the Receivers were authorised to sell the “YVG Properties” and “Glenbelle Properties”, save that the Receivers were not authorised to enter into any contract of sale in respect of the YVG Properties and Glenbelle Properties which was not conditional upon approval of the Court.

15 In the 4 June Orders, the “YVG Parties” were defined as the twenty-first to forty-fifth defendants and the “YVG Properties” were defined as:

(a) the land, buildings and fixtures, the legal title to which is held by any of the YVG Parties, located at The Heritage Golf and Country Club, Corner of Hughes and Yarraview Roads, Chirnside Park, Victoria (the Heritage Complex) including:

(i) the properties in respect of which there are existing contracts of sale, including:

(A) Lots 611 to 618 Botanica town houses;

(B) Lots 6 and 7 of the Henley Land;

(C) Lot 8 of the Henley Land,

(collectively, the Pre-sold Properties); and

(ii) all other developed and undeveloped land located at the Heritage Complex.

(b) the golf operations business located at the Heritage Complex including the YVG Parties’ interest in and rights in respect of:

(i) the Henley Golf Course;

(ii) the St John Golf Course;

(iii) the club house;

(iv) the members’ bar;

(v) the pro shop;

(vi) all maintenance sheds;

(vii) all ancillary property and plant and equipment used in the golf operations;

(viii) goodwill; and

(ix) debtors;

(c) all other rights, plant and equipment, vehicles and any other thing owned by the YVG Parties; and

(d) all shares held by Yarra Valley Golf Pty Ltd (receivers and managers appointed) in Heritage Golf and Country Club Pty Ltd.

16 In the same orders, the “Glenbelle Parties” were defined as the twenty-ninth and thirty-sixth defendants and the “Glenbelle Properties” were defined as:

(a) the land, buildings and fixtures, in respect of the Management Lot of The Sebel Lodge Yarra Valley located within the Heritage Complex;

(b) the land, building and fixtures, in respect of the Heritage Retreat recreation facility and day spa located within the Heritage Complex;

(c) The Sebel Lodge Yarra Valley business including the Glenbelle Parties’ interest in:

(i) the hotel operations;

(ii) the food and beverage operations;

(iii) the conference operations;

(iv) the associated goodwill;

(v) the debtors; and

(vi) all ancillary property and plant and equipment used in The Sebel Lodge Yarra Valley operations;

(d) the Heritage Retreat business including the Glenbelle Parties’ interest in;

(i) the spa operations;

(ii) the recreation facility operations;

(iii) the food and beverage operations;

(iv) the associated goodwill;

(v) the debtors;

(vi) all ancillary property and plant and equipment used in the Heritage Retreat operations;

(e) all other rights, plant and equipment, vehicles and any other thing owned by the Glenbelle Parties.

(Emphasis added.)

17 On 23 December 2010 the Receivers entered into various agreements for the sale of the YVG Properties and the retreat and day spa component of the Glenbelle Properties (the Glenbelle Retreat & Spa). On 17 May 2011, the Court directed that the Receivers were justified in settling the contracts of sale entered into by the Receivers on 23 December 2010.

(2) The Management Lot

18 This application concerns the sale of the Management Lot, which formed part of the “Glenbelle Properties”: see [16] above. The Management Lot was marketed as available to be purchased together with the YVG Assets and Glenbelle Assets or separately from them: see Australian Securities and Investments Commission (No 12) v Letten [2011] FCA 500. The sale of a portion of the Sebel Heritage Yarra Valley Hotel (Hotel) business itself was the subject of the previous YVG Application: see Australian Securities and Investments Commission (No 12) v Letten [2011] FCA 500. The Hotel real estate, however, comprises two aspects, neither of which were the subject of the YVG Application:

1. The Hotel rooms themselves (and associated business), which are owned by members of a properly registered, and continuing, managed investment scheme (the Hotel Scheme); and

2. The Management Lot, which comprises the balance of the real estate of the Hotel, including the conference areas, kitchen, restaurant, bar, storage areas, back of house office and reception desk.

19 The operations of the Hotel are governed by a Hotel Management Agreement dated 28 June 2002 (the HMA). The parties to the HMA are:

1. the responsible entity (RE) of the Hotel Scheme;

2. the owner of the Management Lot (Glenbelle); and

3. the Hotel manager, Mirvac Hotels Pty Ltd (Mirvac).

20 YVG Management Limited was the original party to the HMA in the role of RE. Pursuant to cl 22.2 of the HMA, YVG Management Limited was entitled to assign or novate its rights and responsibilities under the HMA to another RE. In or around 2009, prior to the Receivership, YVG Management Limited assigned its rights and responsibilities under the HMA to Pacific Investment Management Ltd (PIML), when PIML replaced YVG Management Limited as the RE. For present purposes, it is relevant to note that Austpac Funds Management Limited (AFML) became the RE on 6 July 2011.

21 Under the HMA, the “Management Lot” was defined to mean “Lot L34 on the Plan of Subdivision [PS415064K]”. It did not include the Glenbelle Business Assets. Other terms of the HMA are important.

22 Clause 22.4 entitled “Restriction on disposals during Initial Term” relevantly provided:

…

(b) Glenbelle shall not be entitled to dispose of its interests in the Management Lot except to a Related body corporate:

…

(ii) at any later date without receiving the prior written consent of [the RE]. [The RE’s] consent shall not be unreasonably withheld where:

(A) Glenbelle demonstrates to [the RE’s] reasonable satisfaction that the proposed purchaser (Proposed Transferee) is a responsible, respectable and solvent person capable of meeting the ongoing obligations of the Management Lot Proprietor under this Agreement;

(B) the Proposed Transferee enters into an agreement with Mirvac and [the RE] pursuant to which it agrees to fulfil the obligations of the Management Lot Proprietor which relate to the Management Lot as set out in this Agreement and, in particular, the obligations set out in clause 22.12 or otherwise accedes to this agreement;

(C) the Proposed Transferee provides [the RE] with a reasonably acceptable guarantee of performance of its obligations on this agreement if [the RE] so requests;

(D) Glenbelle agrees to pay the reasonable costs of [the RE] and Mirvac incurred in giving its consent and in the production or negotiation of any documentation related to the change of ownership of the Management Lot.

(Emphasis added.)

23 Clause 22.6 of the HMA entitled “First Right of Refusal over Management Lot” provided that:

Glenbelle must procure that neither it nor any of its Related bodies corporate (‘Vendor’) disposes of the Management Lot to any person other than the Owners or [the RE] as agent for the Owners unless:

(a) 90 days before the disposal the Vendor has offered its interests in the Management Lot to the Owners or [the RE] as agent for the Owners on terms no less favourable than the terms of the proposed sale to that other person; or

(b) that disposal is the result of the sale of the interests:

(i) by public auction; or

(ii) by private treaty within 1 Business Day after a public auction at which the sale was passed in and at a price no lower than that at which the Management Lot was passed in and, at least 30 days before the public auction, the Vendor gave [the RE]:

(A) notice of the date, time and place of that public auction; and

(B) a copy of the agreement under which the interest is offered for sale at that public auction.

24 Thus, the Management Lot could not be sold to the purchaser of the YVG Assets (being GHG) as part of the same contracts of sale which were the subject of the YVG Application (which included the assets comprising the catering and conference business conducted by Glenbelle (the Glenbelle Business Assets)).

25 In accordance with cl 22.6(b)(i) of the HMA, the Management Lot was auctioned. In addition to the marketing of the Glenbelle Assets (which included the Management Lot), to enable the auction of the Management Lot to occur, the Management Lot was also marketed as a stand alone asset.

26 In or about January 2011, Knight Frank issued an Information Memorandum for the sale of the Management Lot to all parties who had previously expressed interest in the YVG Assets or the Glenbelle Assets and who had executed a confidentiality undertaking. The Information Memorandum indicated that a public auction would take place on 3 February 2011 at the offices of Mallesons Stephen Jaques, solicitors for the Receivers (Mallesons). Advertisements were also placed in The Age on 29 December 2010, 12 January 2011 and 19 January 2011. Additionally around the time of the advertisements, an eBrochure was emailed by Knight Frank to all parties who had registered interest in the sale of the wider YVG and Glenbelle assets.

27 In addition, on or about 28 December 2010, a copy of the Information Memorandum and proposed sale contract to be used in the auction of the Management Lot was provided to PIML as the then RE of the Hotel Scheme. A day or two prior to the auction, Knight Frank also produced a two page document providing confirmatory information for interested parties for the public auction. The information was sent to eight parties who had expressed interest in the Management Lot or other Glenbelle assets previously (including Mr Boerkamp and GHG, amongst others).

28 The Management Lot was auctioned on 3 February 2011. The auction took place at Mallesons’ office and was attended by Mr Templeton (one of the Receivers); representatives of KPMG; representatives of the secured lenders; Mr Ken Smirk the auctioneer, from Knight Frank and another sales agent from Knight Frank; Mr Tony Troiani and Mr Andrew Norman both Partners of Mallesons; Mr Wilhelmus (Bill) Boerkamp (Mr Boerkamp) and his solicitor; Mr Erik Stuebe (CEO of Chateau Elan Hotels & Resorts), representing the Taggart Consortium who were an under-bidder for the assets that were the subject of the YVG Application; Mr Greg McPherson of Falcon Corporate Advisory, on behalf of GHG; a solicitor for GHG; and Mr Alan Severino, a representative of PIML.

29 Prior to the auctioneer presenting the property to bidders, he read out to those present at the auction a letter dated 3 February 2011, addressed to Mr Templeton, from Falcon Corporate Advisory (advisers to GHG) which stated, amongst other things, that GHG:

1. would not enter into any agreement with a purchaser of the Management Lot:

(a) to sell any of the Glenbelle Assets which were currently used by Glenbelle in the provision of hospitality services;

(b) in respect of access rights for the retreat and spa; and

(c) in relation to the utilisation of any of the other assets that had been purchased by GHG;

2. had the capability:

(a) to enter into an arrangement with Mirvac to service their hospitality requirements in the event that a purchaser of the Management Lot could not fulfil the HMA; and

(b) to establish competing hospitality services to those currently provided from the Management Lot.

Mr Templeton gave evidence that the Receivers had nothing to do with the letter, other than the fact that it was directed to him and that because he considered the letter relevant to bidders who were interested in acquiring the Management Lot, he asked the auctioneer to read the letter to the attendees at the auction.

30 Mr Templeton’s evidence was that just prior to the auctioneer presenting the Management Lot to bidders, Mr Boerkamp said words to the effect that the Management Lot was “worth $250,000”. At the auction, Mr Boerkamp bid to in excess of $4.5 million. Each bid placed by GHG (who was the under-bidder) was exceeded by an additional bid of $10,000 by Mr Boerkamp. Mr Boerkamp was ultimately the successful bidder at the auction, with a final bid of $4.51 million. The only other bidder was GHG.

31 On 3 February 2011, following the auction, the Receivers caused Glenbelle to enter into a conditional contract of sale in relation to the Management Lot with Mr Boerkamp (the Boerkamp Contract). The conditions subsequent included Court approval and (as contemplated by the HMA) approval of the purchaser by the RE: see [22] above.

(3) The Contingency Contract

32 Mr Templeton gave evidence that the Receivers perceived a significant risk that the Boerkamp Contract may not be completed. In light of their concerns, and in the interests of creditors and investors, on 18 February 2011 the Receivers caused Glenbelle to enter into the Contingency Contract with the under-bidder, GHG, whereby GHG would purchase the Management Lot in the event that, amongst other things, the Boerkamp Contract did not complete. The Contingency Contract has a sunset clause such that it expires on the earlier of:

1. 12 months after the date of the Contingency Contract; and

2. if completion has occurred on the assets that were the subject of the YVG Application, the date which is six months after the date of completion.

The sale of the assets the subject of the YVG Application to GHG settled on 15 July 2011. It is common ground that the sunset date for the Contingency Contract is 15 January 2012 and that after that date, the contract is able to be terminated by either party, unless stipulated conditions subsequent have been satisfied.

33 It is necessary to set out a number of the Special Conditions of the Contingency Contract. First, special condition 24 provided:

24.1 [GHG] acknowledges that:

(a) it has received a copy of, and has reviewed, the Existing Contract;

(b) it is aware that the Existing Contract is subject to the conditions subsequent:

(i) that the [RE] provides to [Glenbelle] the consent referred to in clause 22.4(b)(ii) of the [HMA]; and

(ii) of the purchaser under the Existing Contract, the [RE] and Mirvac entering into the Accession Deed and those parties agreeing the amount which the purchaser under the Existing Contract is required to contribute to the Owners FF&E Account, as defined in the [HMA], for the purposes of clause 22.10(c) of the Hotel Management Agreement.copy 23.1(b) [sic]; and

(c) it may be difficult for the purchaser under the Existing Contract to satisfy the conditions subsequent referred to in special condition 24.1(b).

24.2 This contract is subject to the conditions subsequent that:

(a) the Existing Contract [between Glenbelle and Mr Boerkamp] is validly terminated in circumstances where [Glenbelle], acting reasonably, considers that termination of the Existing Contract is unlikely to be the subject of dispute, including the subject of court proceedings; and

(b) the [RE]:

(i) waives its rights under clause 22.6 of the [HMA] in respect of this contract, on terms to the reasonable satisfaction of [Glenbelle]; or

(ii) fails to accept an offer made by [Glenbelle] in accordance with clause 22.6(a) of the [HMA] within the relevant time period,

or there is a combination of the matters referred to in paragraphs (i) and (ii).

24.3 [Glenbelle] must give [GHG] written notice immediately after the conditions subsequent referred to in special condition 24.2 have been satisfied.

24.4 If the conditions subsequent referred to in special condition 24.2 have not been satisfied by the Sunset Date then, at any time until the conditions subsequent have been satisfied, either [Glenbelle] or [GHG] may terminate this contract by written notice to the other and if the contract is terminated in those circumstances, [Glenbelle] must repay to [GHG], as soon as possible, the Deposit and Interest earned on the Deposit.

24.5 The termination of this contract by either party under special condition 24.4 shall not affect the rights of either party for a breach by the other party of this contract before the termination.

24.6 [Glenbelle] must give [GHG] written notice immediately after the Existing Contract has been terminated.

(Emphasis added.)

34 Next, special condition 23 entitled “conditions subsequent” provided:

23.1 This contract is subject to the conditions subsequent:

(a) that the [RE] provides to [Glenbelle] the consent referred to in clause 22.4(b)(ii) of the [HMA]; and

(b) of [GHG], the [RE] and Mirvac entering into the Accession Deed and those parties agreeing the amount which [GHG] is required to contribute to the Owners FF&E Account, as defined in the [HMA], for the purposes of clause 22.10(c) of the [HMA].

23.2 [Glenbelle] must give [GHG] written notice immediately after the conditions subsequent referred to in special condition 23.1 have been satisfied.

23.3 [GHG] acknowledges that:

(a) it has received a copy of, and has reviewed, the [HMA];

(b) it is aware that, under clause 22.4(b) of the [HMA], [Glenbelle] is not entitled to dispose of its interests in the Property without receiving the prior written consent of YVG Management Limited; and

(c) the [RE] has replaced YVG Management Limited as the responsible entity of the Scheme, as defined in the [HMA] and, as a result, under section 601FS(1) of the Corporations Ad 2001 (Cth), has assumed the rights, obligations and liabilities of YVG Management Limited under the [HMA].

23.4 [GHG] must use reasonable endeavours to assist [Glenbelle] to satisfy the conditions subsequent referred to in special condition 23.1 as soon as practicable.

23.5 Without limiting special condition 23.4, [GHG] must:

(a) do anything reasonably requested by [Glenbelle] to assist [Glenbelle] to demonstrate to the [RE’s] reasonable satisfaction that [GHG] is a responsible, respectable and solvent person capable of meeting the ongoing obligations of [Glenbelle] under the [HMA], in accordance with clause 22.4(b)(ii)(A) of the [HMA];

…

(c) if requested by the [RE], provide the [RE] with a reasonably acceptable guarantee of performance of its obligations under the [HMA] in accordance with clause 22.4(b)(ii)(C) of the [HMA];

(d) …

23.6 Without limiting [GHG’s] obligations under special condition 23.4, [Glenbelle] must:

(a) request the Responsible Entity’s written consent to this contract for the purposes of clause 22.4(b)(iii) of the [HMA] as soon as practicable after the Day of Sale:

(b) use reasonable endeavours to demonstrate to the [RE] reasonable satisfaction that [GHG] is a responsible, respectable and solvent person capable of meeting the ongoing obligations of [Glenbelle] under the [HMA] for the purposes of clause 22.4(b)(ii)(A) of the [HMA];

(c) if requested by the [RE], assist [GHG] to provide the [RE] with a reasonably acceptable guarantee of performance of [GHG’s] obligations under the [HMA];

(d) agree with the [RE] to pay the reasonable costs of the [RE] and Mirvac incurred in giving its consent and in the production or negotiation of any documentation related to the change of ownership of the Property, for the purposes of clause 22.4(b)(ii)(D) of the [HMA];

…

…

(g) use reasonable endeavours to enforce its rights under the [HMA] in connection with the conditions subsequent referred to in special condition 23.1.

…

23.9 If the conditions subsequent referred to in special condition 23.1 have not been satisfied by the Sunset Date then, at any time until the conditions subsequent have been satisfied, either [Glenbelle] or [GHG] may terminate this contract by written notice to the other.

23.10 The termination of this contract by either party under special condition 23.9 shall not affect the rights of either party for a breach by the other party of this contract before the termination.

35 On 11 May 2011, GHG executed a Deed Poll in favour of members of the Heritage Golf and Country Club which provided, amongst other things, recognition and assurances in respect of the members’ contractual rights and interests. The terms of the Deed Poll were consistent with previous representations made by GHG to the Receivers that they would honour members’ rights. As part of the settlement process, a copy of this Deed Poll was provided to the Committee of Members for the Heritage Golf and Country Club in or about July 2011, prior to the settlement of the assets which were the subject of the YVG Application.

(4) Steps after Day of Sale and execution of contracts

36 On 11 February 2011, the Receivers wrote to PIML (then the RE) seeking the RE’s consent to Mr Boerkamp as purchaser. A copy of the Boerkamp Contract had been provided to the RE more than 30 days prior to the auction, as required under the HMA: see [23] above.

37 Also on 11 February 2011, Mallesons (the Receivers’ solicitors) sent a letter to Hall & Wilcox (Mr Boerkamp’s solicitors) requesting, amongst other things, documents and information from Mr Boerkamp to assist Glenbelle to demonstrate to the RE’s reasonable satisfaction that Mr Boerkamp was a “responsible, respectable and solvent person capable of meeting the ongoing obligations” of the Management Lot owner under the HMA for the purposes of cl 22.4(b)(ii)(A) of the HMA. The evidence disclosed that there were delays in obtaining the necessary consent. For the purposes of the present application, it is unnecessary to canvass what transpired, or for that matter, did not transpire.

38 Events then move to June 2011. On or about 6 June 2011, by a Deed Poll signed by Mr Boerkamp and Mr Andrew Patrick, in favour of the lot-holders of the Heritage Lodge ARSN 089 099 246 (being the members of the Hotel Scheme), AFML provided certain undertakings in the event that it was to be installed as RE of the Scheme in the place of PIML. And, on 29 June 2011, AFML replaced PIML as RE and assumed all of the rights, duties and obligations of RE under the HMA. Mr Boerkamp is a director and secretary of AFML and a 50% shareholder of Austpac Group Pty Ltd, the ultimate holding company of AFML. On 21 July 2011, in accordance with cl 23.6(b) of the Boerkamp Contract, the Receivers provided certain information to AFML in order to demonstrate to AFML Mr Boerkamp’s responsibility, respectability and solvency and his capacity to meet the on-going obligations of the Management Lot owner, under the HMA, in accordance with cl 22.4(b)(ii)(A) of the HMA.

39 On or about 9 September 2011, AFML resolved to refuse its consent to the disposition of the Management Lot to Mr Boerkamp and, on 13 September 2011, DLA Piper (AFML’s solicitors) notified Mallesons (the Receivers’ solicitors), of that refusal. The reasons for AFML’s refusal to consent to Mr Boerkamp as purchaser of the Management Lot, as stated in the letter dated 13 September 2011, included that:

1. pursuant to cl 28 of the HMA, Glenbelle was bound to use its best endeavours to do all things necessary or desirable to give effect to the HMA and to refrain from doing anything which may hinder the performance of the HMA;

2. the way the Receivers structured the sale of the Management Lot was in breach of the obligation contained in cl 28 of the HMA;

3. both PIML and Mirvac should have acted to prevent the sale occurring in the manner in which it happened and, by failing to do this, and by virtue of their subsequent conduct, have been in breach of their respective obligations under the HMA;

4. AFML was aware that, in a Deed Poll dated 11 May 2011 executed by GHG, it was stated that GHG had agreed with Glenbelle to purchase the Management Lot if a presently existing contract between Glenbelle and another purchaser comes to an end or cannot be completed; and

5. it was concerned by the written and verbal threats from GHG, and from Falcon Corporate Advisory on behalf of GHG, and the effect that these may have if carried out upon Mr Boerkamp becoming the owner of the Management Lot.

40 In response, Mallesons wrote to Hall & Wilcox (Mr Boerkamp’s solicitors) on 16 September 2011 summarising Mr Boerkamp’s activities in allegedly “seeking to (and ultimately succeeding in) frustrating [sic] the approval process” and preserving the Receivers’ rights to pursue Mr Boerkamp for damages in the event that damage was suffered as a consequence of the termination.

41 By a letter dated 20 September 2011, Hall & Wilcox (Mr Boerkamp’s solicitors), wrote to Mallesons as follows:

We refer to your letter dated 16 September 2011 and the DLA Piper letter dated 13 September 2011 (DLA Letter).

…

4. Our client has at all times used his reasonable endeavours to assist your clients to obtain the Reasonable Entity’s consent.

5. If your clients purport to terminate the contract of sale other than in accordance with special condition 23 and do not refund our client’s deposit together with all interest earned thereon, that conduct will constitute a fundamental breach and repudiation of the contract of sale. Our client reserves all rights in relation to any breach of the contract of sale by your clients.

…

It appears that AFML has not provided consent due to the manner in which your clients’ [sic] structured the sale of the Management Lot. Given that AFML has now rejected your clients’ application for consent, please urgently advise of the steps your clients intend to take to satisfy the conditions subsequent.

If you do not intend to take any further steps, we assume that the condition subsequent at special condition 23.1 cannot be fulfilled, that the contract of sale will terminate and our client’s deposit will be refunded.

We look forward to hearing from you.

42 On 27 September 2011, Mallesons provided the Receivers with a Memorandum of Legal Advice entitled “Sale of Management Lot – Options”. The memorandum was tendered in evidence and the subject of extensive cross-examination. It provided as follows:

[REDACTED]

43 On 30 September 2011, Mallesons responded to Hall & Wilcox’s letter of 20 September 2011 (see [41] above) as follows:

We refer to your letter dated 20 September 2011 directed to Tony Troiani of this office.

In particular, we refer to your assumption that the condition subsequent in special condition 23.1 of the Contract cannot be fulfilled, that the Contract will terminate and that your client’s deposit will be refunded.

In accordance with the Contract and with your assumption, please find enclosed:

(a) a notice of termination of the Contract; and

(b) a bank cheque in the amount of $464,562.03 (being the deposit in the amount of $451,000 plus interest) payable to your client.

Our client reserves all of its rights under the Contract including under special condition 23.10 of the Contract.

On 30 September 2011, Mr Boerkamp presented the cheque to his bank for collection.

44 On 7 October 2011, in accordance with cl 22.6(a) of the HMA, the Receivers then provided a form of contract of sale for the Management Lot to AFML on terms no less favourable than those contained in the Contingency Contract (the AFML Pre-emption Contract) thereby providing notice to AFML to enable it to exercise its right of pre-emption.

45 Then things turned odd. On 7 October 2011, the solicitors for Mr Boerkamp, Hall & Wilcox, disputed the Receivers’ termination of the Boerkamp Contract and asserted that it was only capable of termination after the Boerkamp Sunset Date and alleged that the termination of the Boerkamp Contract by the Receivers was therefore invalid. Then, on 12 October 2011, the solicitors for GHG wrote to the solicitors for the Receivers contending that absent a valid termination of the Boerkamp Contract and in the circumstance of a dispute about that termination, special condition 24.2(a) of the Contingency Contract had not been met.

46 Ultimately, the Receivers sought directions about the status of the Boerkamp Contract. The parties attended mediation and, on 8 November 2011, Mr Boerkamp filed a defence in which he admitted each of the following pleaded points of claim:

[34] An agreement was made for the termination of the Boerkamp [C]ontract (“the Boerkamp Termination Agreement”).

Particulars

(i) The Boerkamp Termination Agreement was partly in writing and partly implied.

(ii) Insofar as it was in writing it was constituted by the Hall and Willcox [sic] letter of 20 September 2011, the letter from Mallesons dated 30 September 2011 and the Notice of Termination.

(iii) Insofar as it was implied it was implied by the tender of the Deposit Refund Cheque; alternatively the banking of the Deposit Refund Cheque.

[35] The Boerkamp Termination Agreement was made by:

(a) the making of an offer to terminate the Boerkamp Contract by Mr Boerkamp by his solicitors, Hall and Willcox [sic], by their letter of 20 September 2011, stating that “if you do not intend to take any further steps we assume that the condition subsequent at special condition cannot be fulfilled, that the contract of sale will terminate and our client’s deposit will be refunded”;

(b) the granting of acceptance by the Receivers by the terms of the letter of their solicitors, Mallesons, dated 30 September 2011, terminating the Boerkamp Contract, enclosing a Notice of Termination and tendering the Deposit Refund Cheque; and

(c) the mutual release of the primary obligations under the Boerkamp Contract.

[36] Alternatively to paragraph 35, the Boerkamp Termination Agreement was made by:

(a) the making of an offer to terminate the Boerkamp Contract by the Receivers by their solicitors, Mallesons, by their letter of 30 September 2011, terminating the Boerkamp Contract, enclosing a Notice of Termination and tendering the Deposit Refund Cheque;

(b) the granting of acceptance by Mr Boerkamp by the banking of the Deposit Refund Cheque, without reservation; and

(c) the mutual release of the primary obligations under the Boerkamp Contract.

[37] The term of the Boerkamp Termination Agreement was that the Boerkamp Contract be terminated.

[38] By reason of the making of the Boerkamp Termination Agreement, the Boerkamp contract is terminated.

issues

47 As noted above, there is now one issue left in dispute between the Receivers and GHG. Before turning to that issue it is necessary to say something about the termination of the Boerkamp Contact.

(1) Termination of the Boerkamp Contract

48 The parties to the Boerkamp Contact now agree that the Boerkamp Contract is terminated: see [46] above. By email dated 10 November 2011, GHG informed the Court and the parties that it no longer pressed the argument that the Boerkamp Contract was not validly terminated: see [5] above. The facts and circumstances of this case including the exchange of letters dated 20 and 30 September 2011 and the parties’ conduct (including Mr Boerkamp’s conduct in promptly banking the Deposit Refund Cheque) is consistent with no other conclusion than that the Boerkamp Contract has been validly terminated. Notwithstanding the apparent resolution of this aspect of the dispute, the Receivers initially sought a declaration in the following terms:

That the contract of sale entered into by Mr Damian Templeton and Mr Phillip Hennessy of KPMG as the receivers and managers of Glenbelle Pty Ltd (Receivers and Managers Appointed)(in liquidation) (the Receivers) on 3 February 2011 in relation to Lot L34 on the Plan of Subdivision PS415064K (the Management Lot) with Wilhelmus Boerkamp has been terminated.

49 After the hearing, the Receivers informed the Court that they no longer sought the declaration.

(2) Termination likely to be subject of dispute

50 I now turn to the remaining issue in dispute. Special condition 24.2(a) of the Contingency Contract provided that it was a condition subsequent to the Contingency Contract that the Boerkamp Contract (between the Receivers and Mr Boerkamp) be validly terminated in circumstances where the Receivers (as Vendor), acting reasonably, considered that termination of the Boerkamp Contract was unlikely to be the subject of dispute, including the subject of court proceedings: see [33] above.

51 The parties to the Boerkamp Contract agree that termination of the Boerkamp Contract was effectuated by the Receivers accepting (by its letter and accompanying notice of termination and Deposit Refund Cheque) Mr Boerkamp’s offer to terminate, or alternatively by Mr Boerkamp accepting (by his conduct in banking the Deposit Refund Cheque) the Receivers’ offer to terminate. In either case, the Boerkamp Contract was terminated on 30 September 2011: see [41] and [43].

52 However, as noted earlier (see [3(2)] above), GHG submitted that even if the termination was valid, the question still remains whether the second limb of special condition 24.2(a) was fulfilled. In their initial submissions GHG submitted that the second limb of special condition 24.2(a) involved a purely objective test of whether the Boerkamp Contract was terminated in circumstances where the Receivers, acting reasonably, considered that termination was unlikely to be the subject of dispute, including the subject of court proceedings. That contention was not pursued at the hearing. Instead, GHG sought to challenge Mr Templeton’s state of mind in support of its contention that the Boerkamp Contract was not terminated in circumstances where the Receivers, acting reasonably, considered that termination of the Boerkamp Contract was unlikely to be the subject of dispute, including the subject of court proceedings. Specifically, GHG referred to the following facts and matters:

1. the history of disputes between the Receivers and Mr Boerkamp, as set out in an affidavit sworn by Mr Templeton on 21 October 2011 (Templeton’s 31st affidavit);

2. the appointment of Mr Boerkamp’s company, AFML, as the RE in respect of which Mr Templeton says, “It appeared … that Mr Boerkamp had put himself in a position to influence the [RE]”;

3. correspondence leading up to 30 September 2011, being:

3.1 the letter from DLA Piper to Mallesons dated 13 September 2011 by which AFML’s refusal to consent to the Boerkamp Contract was conveyed: see [39] above;

3.2 the letter from Mallesons to Hall & Wilcox dated 16 September 2011: see [40] above;

3.3 the letter from Hall & Wilcox to Mallesons dated 20 September 2011: see [41] above; and

4. the failure of the Receivers to consider the fact that Mr Boerkamp had an exposure to damages under the reservation of rights in the letter of 30 September 2011 (see [43] above) and might therefore seek to challenge the termination.

53 In general terms, GHG submitted that based upon a literal construction of special condition 24.2(a) (and in particular the phrase “in circumstances where” in 24.2(a)), the facts giving rise to termination and the reasonable belief that a dispute was unlikely must occur at the same moment in time and that the Boerkamp Contract was not terminated in circumstances where the Receivers, acting reasonably, considered that termination of the Boerkamp Contract was unlikely to be the subject of dispute.

54 For the reasons that follow, I do not accept that as a matter of construction, the facts giving rise to termination and the reasonable belief that dispute is unlikely must occur at the same moment in time. Moreover, even if GHG’s construction of the Contingency Contract is the preferred construction (a view I do not accept), the evidence does not support the contention that the Receivers, acting reasonably at the time of termination of the Boerkamp Contract, did not consider that termination was unlikely to be the subject of dispute.

55 As the factual finding does not change even if GHG’s construction of the Contingency Contract is the preferred construction (a view I do not accept), it is strictly unnecessary to address the construction question. Nonetheless, given the parties’ submissions on the issue, it is appropriate to set out the factual matters and then say something about the construction question.

Factual Matters

56 GHG submitted that to satisfy that special condition 24.2(a), it was necessary for the Receivers, having reasonably assessed the facts and circumstances existing at the time the Boerkamp Contract was terminated, to have actually considered that the termination was unlikely to be disputed or challenged, such that the parties to the Contingency Contract could proceed to completion with as much certainty as possible. GHG’s submissions went so far as to contend that the Receivers did not undertake that exercise.

57 As the following reasons for decision will demonstrate, the Receivers undertook the relevant exercise and, secondly, the Boerkamp Contract was terminated in circumstances where the Receivers, acting reasonably, considered that termination of the Boerkamp Contract was unlikely to be the subject of dispute, including the subject of court proceedings. As noted earlier, those factual findings do not change if GHG’s construction of the Contingency Contract is the preferred construction (a view I do not accept).

58 Mr Templeton (being the Receiver and governing mind of Glenbelle, the Vendor) was called to give evidence and was extensively cross-examined by Senior Counsel for GHG. Mr Templeton’s evidence was that at the time of delivery of the notice of termination and the return of the deposit cheque, he considered that whilst a dispute with Mr Boerkamp in relation to the termination was possible, it was unlikely. In support of that view, Mr Templeton submitted that he had sound (and reasonable) grounds for that belief and referred to the following facts and matters:

1. at the auction, Mr Boerkamp bid to $4.51 million after announcing to all present that he believed the Management Lot was worth $250,000;

2. Mr Boerkamp stated publicly that he had been “forced to pay $4.5 million for something that had a negative value”;

3. Mr Boerkamp had taken extraordinary steps to secure the role of RE for the Hotel Scheme (which, in Mr Templeton’s view, was in order to give Mr Boerkamp influence over the approval process);

4. Mr Boerkamp had attended a meeting with Mr Templeton in which Mr Boerkamp said, in the presence of representatives of the RE, that the RE should reject him as buyer of the Management Lot and that Mr Boerkamp was going to ensure the RE carried out its function properly;

5. on 13 September, he received the letter set out at [39] above;

6. on 20 September, he received the letter from Mr Boerkamp’s solicitors: see [41] above;

7. the Receivers agreed with Mr Boerkamp about termination of the Boerkamp Contract and provided him with a notice of termination of the Boerkamp Contract and the Deposit Refund Cheque. That Deposit Refund Cheque was promptly banked by Mr Boerkamp;

8. at all relevant times, Mr Boerkamp’s conduct was consistent with him not wanting to complete the Boerkamp Contract;

9. the contents of the Options Paper: see [42] above; and

10. the Receivers needed to be satisfied that the Boerkamp Contract had in fact “gone away” and that its termination was unlikely to be challenged, because they needed to put forward an unconditional contract to the RE, pursuant to their pre-emptive rights under the AFML Pre-emption Contract: see [44] above.

59 What then were the facts and circumstances relied upon by GHG in support of the contrary contention? They may be summarised as follows:

1. in response to a request for discoverable documents which recorded the Receivers’ view under special condition 24.2(a), and the reasons for holding that view, no file note was produced by the Receivers or their legal advisers;

2. there was nothing in the Options Paper (prepared just three days before the 30 September 2011 letter (see [42] above)) that suggested that Mr Templeton was required to undertake that exercise and form a concluded view;

3. paragraph 1.3 of the Options Paper (see [42] above) misstated the test that was to be satisfied under special condition 24.2(a) and, indeed, the previous correspondence and submissions relied upon by the Receivers all appeared to proceed on the same mistaken basis that all that was required for special condition 24.2(a) was a valid termination;

4. the relevant partners from Mallesons were not called to give evidence;

5. the Receivers failed to take one of two obvious means of putting the issue beyond all doubt, namely seeking to terminate the Boerkamp Contract by agreement with mutual releases and / or applying to the Court for directions regarding termination of the Boerkamp Contract.

60 There was no file note. That is surprising. And the Options Paper did not, in terms, suggest that Mr Templeton was required to undertake the exercise and form a concluded view in the manner contended for by GHG. However, the Options Paper clearly addressed special condition 24.2(a) in options (b)(i) and (b)(ii) (see [42] above) and, in addressing those options, the paper identified at least some of the perceived disadvantages in adopting those options. As Counsel for the Receivers submitted, the only explanation for why the advantages and disadvantages are listed in the Options Paper is as a consequence of special condition 24.2(a) and, in particular, the kind of exercise which GHG submitted had not been addressed. Indeed, in reply, Senior Counsel for GHG accepted that the author of the Options Paper was aware of special condition 24.2(a) because it was expressly referred to in that paper. It must then be recalled that the evidence given by Mr Templeton (which I accept) that it was the Options Paper that formed the basis of his numerous discussions with his legal advisers about what to do in relation to the Boerkamp Contract. It therefore cannot be said that Mr Templeton did not turn his mind to the exercise he was required to undertake under special condition 24.2(a). His evidence on this aspect of the matter should be accepted.

61 The last remaining issue to address is GHG’s contention that Mr Templeton, acting reasonably, could not have considered that termination of the Boerkamp Contract was unlikely to be the subject of dispute, including the subject of court proceedings. In support of that contention, GHG submitted that because Mr Templeton conceded that he did not have regard to the damages risk that Mr Boerkamp faced when forming his view that termination of the Boerkamp Contract was unlikely to be the subject of dispute, including the subject of court proceedings, he did not act reasonably. The damages risk was said to be the difference between the contract price for the Management Lot under the Boerkamp Contract and the ultimate sale price of the Management Lot. There is, in my view, a complete answer to this contention. That answer is found in the express language of special condition 24.2(a).

62 Special condition 24.2(a) required the Receiver, acting reasonably, to have considered that termination of the Boerkamp Contract was unlikely to be the subject of dispute, including the subject of court proceedings. As is apparent, the subject matter of the exercise was not litigation at large but whether “termination of the [Boerkamp] Contract” was unlikely to be the subject of dispute. For the reasons stated earlier, I consider that the Receiver, acting reasonably, was entitled to form that view. Put another way, the damages risk for Mr Boerkamp was not and is not a dispute about the “termination of the [Boerkamp] Contract”. At its highest, it is a potential claim for damages which has as its origin a termination of the Boerkamp Contract.

63 In those circumstances, I accept that Mr Templeton formed the view that Mr Boerkamp did not want to complete his contract and, therefore, that the return of the deposit to Mr Boerkamp would likely bring an end to any potential dispute. To adopt the language used by Mallesons in the Options Paper given to the Receivers, it provided a “clean exit” from the Boerkamp Contract so that the precondition to completion in special condition 24.2(a) was met: see [42] above.

CONSTRUCTION OF THE CONTINGENCY CONTRACT

64 The essential submission of GHG is that, on a literal construction of special condition 24.2(a) (see [33] above), given the words “in circumstances where”, the facts giving rise to termination, and the reasonable belief that dispute about the termination is unlikely, must occur at the same moment in time.

65 The Receivers submitted and I accept that the proper construction of special condition 24.2(a) does not require the coincidence in time of the facts constituting the termination and the Vendor forming a reasonable opinion that dispute as to termination is unlikely. For the reasons that follow, I consider the preferable construction of special condition 24.2(a) is that the Boerkamp Contract must be in a state of valid termination at the time when the Vendor considers, acting reasonably, that a dispute about termination is unlikely and the coincidence of those two matters must occur prior to the Sunset Date (and not necessarily at the time of termination of the Boerkamp Contract).

66 First, the express words of the Contingency Contract. It contains a number of “conditions subsequent”, being conditions required to be satisfied before either party has an obligation to settle the Contingency Contract (primarily by way of Glenbelle delivering title and the purchaser paying the balance of the purchase price). These conditions subsequent are contained in special conditions 22.1 (Court approval), 23.1 (RE approval and Accession Deed) and 24.2 (Boerkamp Contract Termination and no RE pre-emption).

67 The satisfaction of each condition subsequent mandates an obligation on the Vendor to serve a notice on GHG that the condition has been satisfied – see special conditions 22.2, 23.2 and 24.3. Looking at page 2 of the Particulars of Sale under the Contingency Contract, the balance of the purchase price (defined as the Residue) is payable 45 days after the last notice is served on GHG (i.e. the completion date is set).

68 The Sunset Date defines the period during which all conditions subsequent must be satisfied, failing which the contract may be terminated at the will of either party: see special conditions 22.3, 23.9 and 24.4. Special condition 24.2(a), in its express terms, does not (and cannot) oust the concept that the whole of the period until the Sunset Date is available to the parties for the satisfaction of the conditions subsequent, and the objective intention of the parties was that this period be available for satisfaction of the specific condition subsequent in special condition 24.2(a).

69 The Receivers further submitted (and I accept) that their construction is supported by the existence of the notice obligation in special condition 24.6. This requires notification of termination immediately upon termination occurring, whether or not, at that time, there is any apprehension of potential dispute. The Contingency Contract expressly contemplates the possibility of a temporal disconnect between the moment of termination and the forming of a view that no dispute about it was likely. The existence of a separate notice requirement under special condition 24.3 makes that clear. In addition, that construction is supported by the express terms of special condition 24.4 which deals with what is to occur if special condition 24.2 is not satisfied by the Sunset Date.

70 Finally, the Receivers submitted and I accept that the primary purpose of the Contingency Contract was to provide for sale to GHG (being the under-bidder) in the event that completion of the Boerkamp Contract did not occur. As is readily apparent, neither the Vendor (the Receivers) nor GHG wished to face a risk that Mr Boerkamp subsequently asserted an interest in the property under the Boerkamp Contract. Put another way, special condition 24.2(a) protected the parties to the Contingency Contract. It protected against completing the Contingency Contract unless there was reasonable confidence that the risk (that the Boerkamp Contract was unlikely to be the subject of dispute, including the subject of court proceedings) did not exist.

71 Here, the critical matters were, relevantly, that the Boerkamp Contract was terminated and there was no reasonable apprehension of the risk such identified. They are and remain separate concepts. There was a requirement that both elements be satisfied prior to completion; it was not necessary for both elements to occur simultaneously.

72 The construction of special condition 24.2(a) contended for by GHG should be rejected. It is uncommercial. There are numerous mechanisms whereby a contract could be terminated which might well be disputed; for example, a rescission based upon an alleged repudiation. It might be some time after the purported termination, in those circumstances, before the vendor will know whether or not the termination is disputed. That is why the parties to the GHG contract allowed the period up until the Sunset Date for the condition to be satisfied. The construction of special condition 24.2(a) which has been adopted achieves a commercial and sensible construction. It provides a period of time (being the period until the Sunset Date) for disputes to be resolved.

Conclusion

73 For those reasons, I reject GHG’s submission that the special condition 24.2(a) has not been satisfied.

The enforceability of special condition 23.4 against GHG at this time

74 GHG initially submitted that on the proper construction of the Contingency Contract, GHG was not obliged to perform any obligations under special condition 23.4 (see [34] above) (that it must use reasonable endeavours to assist the Receivers to satisfy the conditions referred to in special condition 23.1, including consent from the Responsible Entity) until the conditions contained in special condition 24.2 (see [33] above) had been fulfilled, which has not yet occurred. Its central construction point was that as special condition 24.2 provides that “This contract is subject to”, the whole of the contract, including special condition 23.4, is subject to the special conditions.

75 Just prior to the hearing on 12 November 2011, GHG abandoned this argument and, consistent with that decision, filed and served an Amended Case. For that reason, it is unnecessary to address the parties’ respective submissions.

I certify that the preceding seventy-five (75) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gordon. |

Associate:

ANNEXURE A

ANNEXURE B

SCHEDULE OF PARTIES

LGH HOLDINGS LIMITED (ACN 007 191 943)

Second Defendant

211 WELLINGTON ROAD PTY LTD (ACN 092 663 860)

Third Defendant

BLUEMIST HOLDINGS PTY LTD (ACN 097 306 922)

Fourth Defendant

DELLWOOD HOLDINGS PTY LTD (ACN 098 505 803)

Fifth Defendant

ENMORE ENTERPRISES PTY LTD (ACN 082 158 487)

Sixth Defendant

FIRBANK ARCH PTY LTD (ACN 059 464 381)

Seventh Defendant

GLENLINE PTY LTD (ACN 098 532 364)

Eighth Defendant

GERLING HOLDINGS PTY LTD (ACN 091 726 457)

Ninth Defendant

LGH ADMINISTRATION PTY LTD (ACN 007 165 069)

Tenth Defendant

LGH FINANCE PTY LTD (ACN 078 859 248)

Eleventh Defendant

LOW HEAD VILLAGE PTY LTD (ACN 091 731 958)

Twelfth Defendant

NICHOLSON STREET PTY LTD (ACN 069 104 089)

Thirteenth Defendant

HOLLOWAY CREST PTY LTD (ACN 091 731 967)

Fourteenth Defendant

ROSEBERY ENTERPRISES PTY LTD (ACN 091 826 229)

Fifteenth Defendant

SIMMS INVESTMENTS PTY LTD (ACN 093 504 511)

Sixteenth Defendant

SY21 RETAIL PTY LTD (ACN 107 874 564)

Seventeenth Defendant

THE GLEN CENTRE HAWTHORN PTY LTD (ACN 089 906 543)

Eighteenth Defendant

CASTELLO HOLDINGS PTY LTD (ACN 088 204 175)

Nineteenth Defendant

TWINVIEW NOMINEES PTY LTD (ACN 097 307 278)

Twentieth Defendant

YARRA VALLEY GOLF PTY LTD (ACN 066 632 479)

Twenty-First Defendant

ADINA RISE PTY LTD (ACN 083 181 122)

Twenty-Second Defendant

ALBRIGHT INVESTMENTS PTY LTD (ACN 088 204 166)

Twenty-Third Defendant

ASHFIELD RISE PTY LTD (ACN 093 504 806)

Twenty-Fourth Defendant

BRADFIELD CORPORATION PTY LTD (ACN 088 204 371)

Twenty-Fifth Defendant

COPELAND ENTERPRISES PTY LTD (ACN 093 504 824)

Twenty-Sixth Defendant

DEVLIN WAY PTY LTD (ACN 088 264 813)

Twenty-Seventh Defendant

FIRST HAZELWOOD PTY LTD (ACN 093 505 303)

Twenty-Eighth Defendant

GLENBELLE PTY LTD (ACN 097 306 646)

Twenty-Ninth Defendant

GLENVALE WAY PTY LTD (ACN 088 287 021)

Thirtieth Defendant

GREENVIEW LANE PTY LTD (ACN 093 505 312)

Thirty-First Defendant

HALLMARK CORPORATION PTY LTD (ACN 093 505 312)

Thirty-Second Defendant

MOORLEIGH HOLDINGS PTY LTD (ACN 088 287 058)

Thirty-Third Defendant

NORTON RIDGE PTY LTD (ACN 078 821 066)

Thirty-Fourth Defendant

RALEIGH GLEN PTY LTD (ACN 088 204 380)

Thirty-Fifth Defendant

REDCREST HOLDINGS PTY LTD (ACN 100 836 486)

Thirty-Sixth Defendant

SURI CORPORATION PTY LTD (ACN 093 505 321)

Thirty-Seventh Defendant

SUTTON RISE PTY LTD (ACN 088 204 399)

Thirty-Eighth Defendant

THE VIRTUAL MLMER PTY LTD (ACN 065 374 665)

Thirty-Ninth Defendant

TIVENDALE PTY LTD (ACN 093 505 349)

Fortieth Defendant

TULLOCH DOWNES PTY LTD (ACN 078 895 048)

Forty-First Defendant

MAINKING PTY LTD (ACN 100 790 485)

Forty-Second Defendant

TOPGLEN PTY LTD (ACN 096 857 564)

Forty-Third Defendant

ALLBLUE PTY LTD (ACN 100 836 388)

Forty-Fourth Defendant

ARANBAY PTY LTD (ACN 098 532 319)

Forty-Fifth Defendant

MELVILLE CORPORATION PTY LTD (ACN 091 911 045)

Forty-Sixth Defendant

TILLEY LANE PTY LTD (ACN 086 136 361)

Forty-Seventh Defendant

HPSC PTY LTD (ACN 059 930 139

Forty-Eighth Defendant

JENSDALE PTY LTD (ACN 098 367 974)

Forty-Ninth Defendant

OAKDALE RISE PTY LTD (ACN 091 598 908)

Fiftieth Defendant

MAYWOOD INVESTMENTS PTY LTD (ACN 091 599 218)

Fifty-First Defendant

ACETRAIN PTY LTD (ACN 100 820 282)

Fifty-Second Defendant

SAGE BAY PTY LTD (ACN 097 306 628)

Fifty-Third Defendant

TOBAGO HOLDINGS PTY LTD (ACN 093 504 520)

Fifty-Fourth Defendant

WILHELMUS ANTONIUS JOANNES BOERKAMP

Fifty-Fifth Defendant

AUSTPAC FUNDS MANAGEMENT LIMITED

Fifty-Sixth Defendant

GOLDEN HERITAGE GOLF PTY LTD

Fifty-Seventh Defendant