FEDERAL COURT OF AUSTRALIA

Benedict v Olde; in the matter of ATS (Asia Pacific) Pty Ltd [2011] FCA 1008

| IN THE FEDERAL COURT OF AUSTRALIA | |

| DATE OF ORDER: | |

| WHERE MADE: |

THE COURT NOTES THAT:

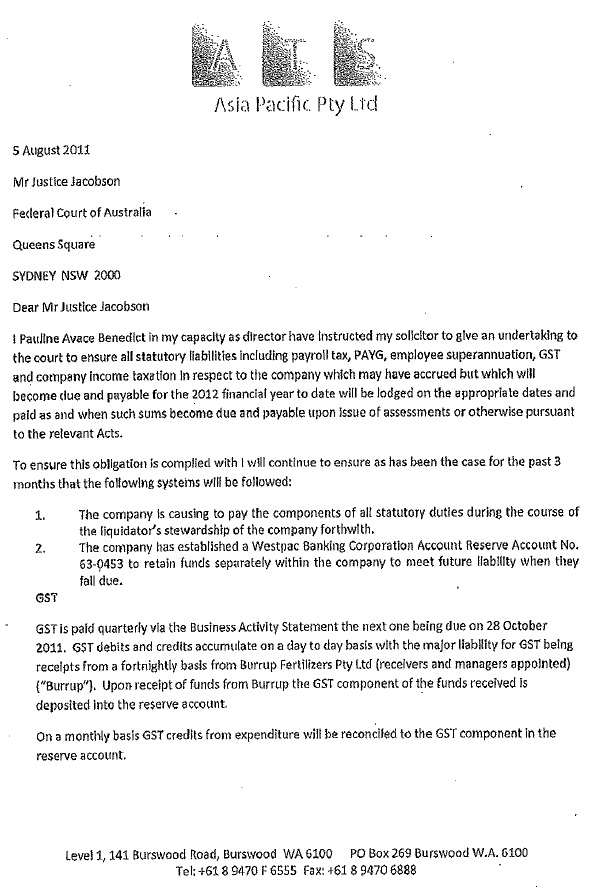

1. The undertaking to the Court of the Applicant in respect to accrued statutory entitlements to be paid when due and payable in terms of Exhibit A (copy attached).

2. The sum of $160,833.00 is to be remitted by Parry Carroll Lawyers from its trust account to ATS (Asia Pacific) Pty Ltd upon termination of the winding up of the company and is to be applied forthwith by the company for distribution to various employee superannuation funds or otherwise retained by the company pending receipt of employee superannuation details or otherwise paid to the Australian Taxation Office Unclaimed Superannuation Fund after a period of 12 months.

3. The sum of $16,500 is to be held by Parry Carroll Lawyers in a controlled monies account in the name of Parry Carroll atf ATS (Asia Pacific) Pty Ltd and Quentin Olde on account of potential income tax during the course of the liquidation of the company pending assessment and payment of company taxation for the year ended 30 June 2012 with such sum to be applied in payment of such tax or returned to the company once satisfactory evidence is provided to Quentin Olde that such tax has been paid in full.

THE COURT ORDERS THAT:

4. Conditional upon the making of the following payments (by the drawing and posting of cheques in favour of the relevant payee designated below and conditional upon the establishment of the controlled monies account referred to in Notation C above, the liquidation of ATS (Asia Pacific) Pty Ltd (in liquidation) be terminated pursuant to s 482 of the Corporations Act 2001 (Cth) (“the Act”) on 10 August 2011:

Trade Creditors

Telstra Limited $ 2,222.56 *

Seek Limited $ 236.50 *

Impact Financial Services $ 624.84 *

North West Training $ 5,382.20 *

Eco Springs $ 47.66 *

Mark Blewett (rent) $ 9,533.00 *

Statutory Obligations

Office of State Revenue (WA) $ 61,550.64 *

Australian Taxation Office (GST) $ 393,867.00 **

Australian Taxation Office (Dec GST) $ 38,544.00 *

Australian Taxation Office (PAYG) $ 544,816.54

Expenses incurred by the Liquidator during the Liquidation

ATO - Employee PAYG w/e 1 August 2011 $ 32,930.00

ATO - Employee PAYG w/e 8 August 2011 $ 24,660.00

ATO – GST on Burrup invoices $ 20,000.00

Employee superannuation – w/e 1 August $ 10,210.00

Employee superannuation – w/e 8 August $ 7,868.00

OSR (WA) – payroll tax w/e 1 August $ 6,240.00

OSR (WA) – payroll tax w/e 8 August $ 4,809.00

5. The sum of $171,100.26 be paid forthwith to Dun Oir Investments Pty Ltd from the funds held in the trust account of Parry Carroll Lawyers on account of the costs order in the winding up proceedings No. ACD 34 of 2011 in the sum of $6,100.26 and the amount claimed by Dun Oir Investments Pty Ltd in the sum of $165,000.00.

6. Pursuant to section 479(3) of the Act, the Court directs that, the First Respondent is justified in not opposing the making of the order for termination of the winding up of the Second Respondent, ATS (Asia Pacific) Pty Limited (In Liquidation) ACN 147 044 068, and in complying with the regime for payment of the obligations of the Second Respondent as set out in the orders and notations made by the Court today.

7. The Applicant pay the costs of these proceedings of the petitioning creditor, Dun Oir Investments Pty Ltd, as agreed or assessed.

8. That leave be granted to discontinue the Interlocutory Process filed in proceedings No. ACD 34 of 2011.

9. Liberty to restore the matter on the giving of 48 hours notice in writing.

Note: Settlement and entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011. The text of entered orders can be located using Federal Law Search on the Court’s website.

| NEW SOUTH WALES DISTRICT REGISTRY | |

| GENERAL DIVISION | NSD 1274 of 2011 |

| BETWEEN: | PAULINE AVACE BENEDICT Plaintiff |

| AND: | QUENTIN JAMES OLDE IN HIS CAPACITY AS LIQUIDATOR OF ATS (ASIA PACIFIC) PTY LTD (IN LIQUIDATION) ACN 147 044 068 First Defendant ATS (ASIA PACIFIC) PTY LTD (IN LIQUIDATION) ACN 147 044 068 Second Defendant |

| JUDGE: | JACOBSON J |

| DATE: | 9 AUGUST 2011 |

| PLACE: | SYDNEY |

REASONS FOR JUDGMENT

1 This is an application made under s 482(1) of the Corporations Act 2001 (Cth) (“the Act”) for an order that the winding up of ATS (Asia Pacific) Pty Limited (“the Company”) be terminated. The Company was placed in liquidation by order of the Federal Court of Australia on 25 July 2011 and Mr Quentin Olde was appointed as the liquidator. The winding up order was made on a presumption of insolvency on the basis of an unsatisfied statutory demand.

2 The Company operates a labour hire business providing staff to the oil, gas and pesticide industries in Karratha in the state of Western Australia. It is the only union authorised labour hire provider to Barrup Fertilisers Pty Limited (“Barrup”) which is in receivership and which is under the control of PPB Advisory. Barrup makes fertilisers and explosives on the Burrup Peninsula near Karratha.

3 The statutory demand was issued by Dun Oir Investments Pty Ltd on 5 June 2011. The debt stated in the statutory demand was for a sum $170,000 but it was paid in full by the Company in three instalments, the last instalment being paid on 22 July 2011. Notwithstanding the payment of the sum of $170,000, the petitioning creditor proceeded on 25 July 2011 to obtain a winding up order upon the basis of a claim for other moneys totalling approximately $165,000 said to be due to the petitioning creditor by the Company. The order was made by Registrar Wall in Canberra on 25 July 2011 without any appearance on behalf of the Company. Ms Benedict, to whom I refer below, has sufficiently explained the reason why the Company failed to attend before the Registrar.

4 The application for an order terminating the winding up is Ms Pauline Avace Benedict. She is the sole director and sole shareholder of the Company. She is a contributory of the Company and therefore has standing to bring the present application.

5 The jurisdiction to terminate a winding up under s 482 is discretionary. The court ordinarily has regard to a range of factors which were set out in the judgment of Master Lee QC in Re Warbler Pty Limited (1982) 6 ACLR 526. As Santow J said in Dubolo Pty Ltd (t/as Fender Signs) v Codrington Investment Corporation Pty Ltd (1998) 26 ACSR 723, those factors are not to be rigidly applied but it is well accepted that the eight factors listed by Master Lee provide useful guidance.

6 I do not propose to set out the so-called ‘Warbler factors’. They were set out by Barrett J in Metledge v Bambakit Pty Ltd (in liq) [2005] NSWSC 160 at [5] and have been applied and referred to on numerous occasions: see, for example, Gematech Pty Ltd v Bardi Investments Pty Ltd [2008] NSWSC 196 at [24]–[32] per Hammerschlag J; Velissaris v Fitzgerald [2011] FCA 197. I am satisfied that the relevant factors have been sufficiently complied with in the present case to make an order. The principal factors which the court considers are what is for the benefit of creditors including contingent creditors as well as the interests of members and the liquidator.

7 Questions of “commercial morality” and the public interest are also important factors. It has often been said that it’s a matter of public policy and commercial morality that the court will not countenance the return of an insolvent company to the mainstream of commercial life: see Re Data Homes Pty Limited [1971] 1 NSWLR 338; Re Data Homes Pty Limited [1972] 2 NSWLR 22 at 26-27 per Mason JA.

8 In the present case, on the critical issue of solvency I have a preliminary report given by Messrs Hall Chadwick on the solvency of the Company. Hall Chadwick have stated in their report, dated 4 August 2011, that on their preliminary analysis as set out in the report the Company is solvent for the purposes of the Act. Moreover, I have evidence which satisfies me as to the nature and extent of the creditors and whether or not their debts have been or will be discharged.

9 The position is succinctly recorded in a table, or a schedule, of the estimated statement of the Company’s financial position. That document was exhibit B in the present application. Although the exhibit indicated a net deficiency of approximately $108,000, the position now appears to be that the Company has a surplus which is evidenced by the fact of an additional payment of approximately $130,000 into the trust account of Messrs Parry Carroll Solicitors. At the time of the preparation of the estimated statement of position, Ms Parry had $450,000 in her trust account but she now holds $588,000, thereby disclosing the additional of $130,000 to which I have referred.

10 The order which is sought is a conditional order, the condition being set out in para 1 of the draft orders submitted to me this afternoon. The conditions address the question of payment of trade creditors, statutory obligations owing in particular to the Office of State Revenue of Western Australia and to the Australian Taxation Office, employee entitlements and expenses incurred by the liquidator during the liquidation.

11 Whilst I have not seen all of the evidence which sets forth the ability of the company to meet these payments, the fact that the termination of the winding up is to be conditional upon the payments is sufficient to satisfy me that I ought to exercise my discretion. In this regard it is important to note that the company and its solicitor, Ms Perry, have been in close contact and cooperation with the liquidator with a view to determining what amounts are owing and the ability of the company to meet those liabilities. In those circumstances it seems to me that the position of creditors is sufficiently satisfied to permit me to exercise the discretion. The effect of the schedule is that it should ensure that all creditors’ interests are met.

12 Importantly the petitioning creditor was served with notice of the present application. The amount that was due to the petitioning creditor together with legal costs is part of the funds held in Ms Perry’s trust account. The petitioning creditor does not oppose the order terminating the winding up. Also it is important that a major creditor of the company, the ATO, was served with notice of the application. I have evidence before me that the ATO does not object to the order that is sought. In addition ASIC was served with notice of the application and it also does not oppose the making of the order.

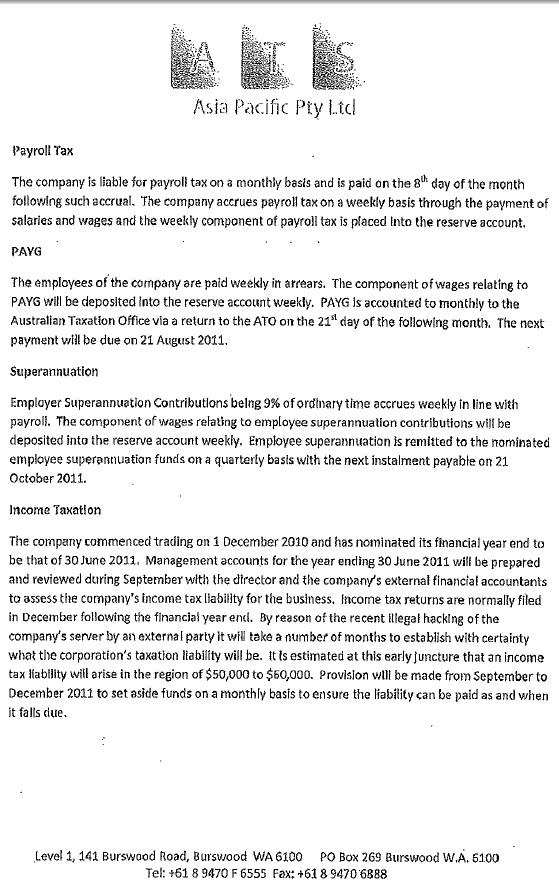

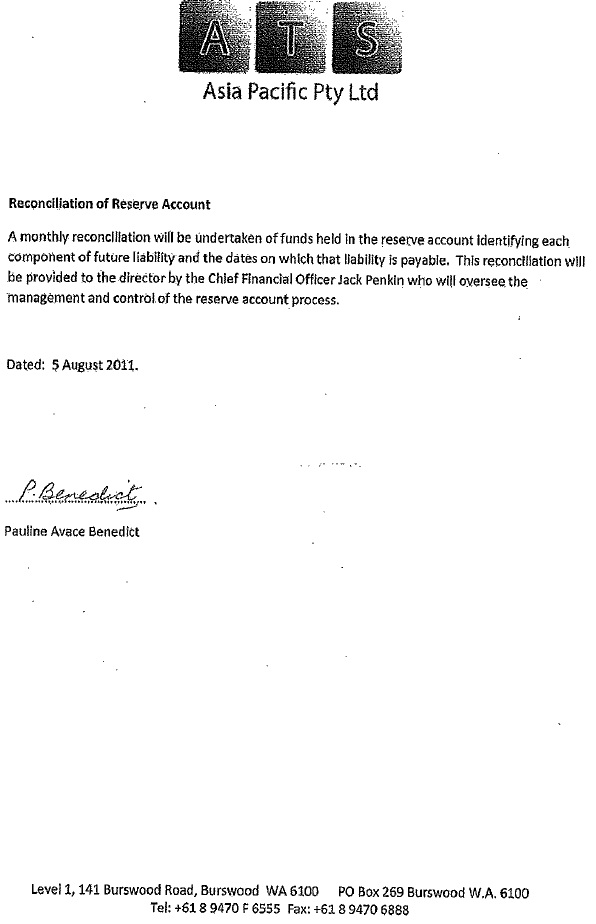

13 So far as accruing statutory entitlements are concerned this has been addressed by undertakings to the court given by Ms Benedict. The undertaking is contained in exhibit A. It is intended to ensure that the company will comply and continue to comply with its statutory obligations and provides for the establishment of a reserve account in which funds are to be retained separately to meet future liabilities as and when they fall due. I will note the undertaking to the court in the form of orders which I make.

14 The position of the liquidator is that he does not oppose the making of the order terminating the winding up, however, the liquidator seeks a direction from the court under s 479(3) of the Act. He does so because he is concerned that he may have a personal liability for tax payable in respect of the trading of the company during the period that it was in liquidation. Counsel for the liquidator, Mr Baird, referred me to an authority of the Court of Appeal of Queensland in a matter of Barkworth Olives Management Ltd v Deputy Commissioner of Taxation [2010] QCA 80, in particular at [29] (“Barkworth”).

15 Mr Baird submits that the position which arises in the present case is quite unusual because here a solvent company has traded profitable through the period of liquidation and the effect of the provisions of s 254 of the Income Tax Assessment Act may be to make the liquidator liable for the tax which may in due course become payable in respect of income earned during the period of the liquidation.

16 As Mr Baird points out there is no liability on the liquidator to lodge a tax return. The position appears to be that the effect of s 254 is that there was no liability on the liquidator to lodge the return because the liquidation is about to be terminated. However, the company would have and will have an obligation to lodge the return and there is a potential for liability for tax in respect of the trading undertaken during the period of liquidation.

17 Mr Baird submits that the position with regard to s 254 is not entirely clear. Notwithstanding the view of the Queensland Court of Appeal in Barkworth that case dealt with a different issue and the provisions of s 254 may expose the liquidator to a personal liability. In those circumstances Mr Baird submits that this is an appropriate case in which to give a direction under s 479(3) of the Act. The direction that he seeks is that the liquidator is justified in not opposing the making of the order for termination in the winding up of the company and in not opposing the regime for payment of the obligations of the company as set out in the draft short minutes of order which were handed up, as I have said, this afternoon.

18 It is true, as Ms Perry points out, that the potential liability of the liquidator is no more than hypothetical. The obligation to file a return will fall upon the company and the liability will relate to the full financial year of trading. The question of whether the company may or may not make a profit during the whole of the financial year is therefore entirely hypothetical. It would appear from the matters put to me today that the highest amount of tax liability which might possibly arise from the period of trading to which I have referred is $16,000.

19 I did have some doubts as to whether this is an appropriate case for the exercise of my discretion to make a direction. The authorities set out the relevant circumstances in which it is appropriate to give directions: see, for example, Re Adstone Pty Limited (in liq) (1997) 25 ACSR 357 and Re Ansett v Korda (2002) 40 ACSR 433 at 65.

20 Notwithstanding the reservations that I initially expressed, I am satisfied that this is a case in which there is sufficient uncertainty as to the legal position with respect to the liquidator’s potential liability that I ought to make the direction which he seeks. Of course, this direction is given upon the basis of the evidence which indicates how the regime has been put in place to provide for payment of creditors and the direction is only as good as the facts which support the application. Nonetheless it does seem to me that I can be satisfied there is some utility in giving the direction which I have stated.

21 The final form of the order will be substantially to the effect of the draft which I have considered but will include provision for the additional funds to be received into Ms Perry’s trust account. I will make orders in terms which reflect the final draft as soon as it is received by my associate.

22 The application came before me as a matter of some urgency, in particular because the company employs approximately 38 employees on the site in Western Australia. The employees were threatening to walk off the site. They are skilled personnel who are critical to the carrying out of the company’s business and the order was therefore sought as a matter of some urgency. This may explain some of the more unusual features of the way in which the proceeding has been dealt with by me.

| I certify that the preceding twenty-two (22) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Jacobson. |

Associate: