FEDERAL COURT OF AUSTRALIA

Australian Energy Regulator v Stanwell Corporation Limited

[2011] FCA 991

IN THE FEDERAL COURT OF AUSTRALIA | |

| Applicant | |

AND: | STANWELL CORPORATION LIMITED (ACN 078 848 674) Respondent |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

1. the application be dismissed; and

2. in the absence of any application, within 7 days, for any other order as to costs, the applicant pay the respondent’s costs of the proceedings, including reserved costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

QUEENSLAND DISTRICT REGISTRY | |

GENERAL DIVISION | QUD 186 of 2009 |

BETWEEN: | AUSTRALIAN ENERGY REGULATOR Applicant

|

AND: | STANWELL CORPORATION LIMITED (ACN 078 848 674) Respondent

|

JUDGE: | DOWSETT J |

DATE: | 30 AUGUST 2011 |

PLACE: | BRISBANE |

REASONS FOR JUDGMENT

1 The National Electricity Market (the “NEM”) is a market for the sale and acquisition of electricity. The NEM is established pursuant to the National Electricity Law (the “Law”), originally enacted by the Parliament of South Australia and subsequently adopted by Commonwealth, New South Wales, Victorian, Queensland, Tasmanian and Australian Capital Territory legislation. The Law provides that:

The objective of this Law is to promote efficient investment in, and efficient operation and use of, electricity services for the long term interests of consumers of electricity with respect to −

(a) price, quality, safety, reliability and security of supply of electricity; and

(b) the reliability, safety and security of the national electricity system.

2 The National Electricity Rules (the “Rules”) govern the operation of the NEM. They have the force of law. There are five regions in the NEM, of which the State of Queensland is one. Although the demand for electricity within Queensland is generally met from local sources, electricity can be obtained from, and supplied to New South Wales. The NEM operates electronically. This case primarily concerns the Queensland region of the NEM in which there were, at the relevant time, effectively, nine suppliers of electricity. Although there were numerous purchasers of electricity in the market, mainly retail suppliers of electricity, decisions to purchase were, for present purposes, effectively made by the National Electronic Market Management Company Limited. That corporation is generally referred to in the evidence as “NEMMCO”, although the acronym “AEMO” is also used as its name is now Australian Energy Market Operator Limited. In these reasons I shall refer to it as the “Operator”. It was responsible for operation of the NEM.

ELECTRICITY GENERATION AND SUPPLY

3 The structure and operation of the NEM reflect certain characteristics of electricity and the mechanisms by which it is generated and supplied to end users. These matters are dealt with in detail in the affidavit of Gregory Harold Thorpe filed by the applicant on 26 February 2010. Mr Thorpe is an electrical engineer with considerable experience in the electricity industry, including industry regulation and marketing. Dr Ian Athol Rose was called by the respondent. He is an engineer, also eminently qualified to give evidence in respect of both technical and market matters. In his evidence Dr Rose avoided unnecessary repetition of the very detailed and helpful description of the market and of technical matters given by Mr Thorpe. He chose rather to comment upon aspects of Mr Thorpe’s report and to provide other, in most cases more detailed information concerning such matters. Much of this part of my reasons comes from Mr Thorpe’s evidence. I shall consider Dr Rose’s evidence separately.

4 In these reasons, I shall use the term “generating unit” to identify one set of equipment which is capable of generating electricity. I shall use the word “generator” to describe a legal entity which operates a generating unit. Generators usually operate power stations which house more than one generating unit. Electricity produced by generating units is, in the case of larger generators, transported to consumers through shared bulk transmission networks and local distribution networks. Some smaller or local generators supply electricity directly to local distribution networks.

5 Electricity is generated by converting other forms of energy into electrical energy. This may involve the conversion of energy stored in fuel such as coal or gas. Running water, the wind and the sun are other sources of energy used in generating electricity. Consumers convert electrical energy into other forms of energy such as light, heat and motion. The rate at which electrical energy is produced, transported or used at any point in time is described as “electrical power” and is measured in Watts (“W”). Applications which require substantial amounts of energy in short periods are said to have high power demand. The amount of energy produced or consumed in a given time is found by multiplying the power (that is the rate at which energy was delivered) by the length of time for which it was delivered and is measured in Watt-hours (“Wh”). Multiples of one thousand, one million and one thousand million units of power and energy are termed “kilowatts” and “kilowatt hours”, “megawatts” and “megawatt hours” and “gigawatts” and “gigawatt hours” respectively. The abbreviations “kW” and “kWh”, “MW” and “MWh” and “GW” and “GWh” are in common use. In this case it is not necessary to distinguish between Watts and Watt-hours.

6 In an electrical power system the aggregate power and energy requirements of individual consumers create the system demand for power and energy. Demand is sometimes described as “load”. That term may also be used to nominate the level at which generators are operating. This ambiguity is best avoided by referring to energy requirements of individual consumers and the aggregate of such requirements as “demand”.

7 Demand within any system will vary from second to second as users (including major users) switch appliances on and off. Demand tends to vary across each day and seasonally. Over a 24 hour period from midnight to midnight, demand typically falls to a low between 4.00 am and 6.00 am. Overnight demand includes 24 hour industry, security, street lighting and refrigeration. Demand rises as industrial, domestic and commercial activities commence for the day. Depending on the time of year and the location, early morning demand may reflect lighting, cooking, heating or air conditioning and public transport needs. During daylight hours, demand generally continues to rise to one or more peaks, and then begins to fall as commercial and industrial activity winds down. In hot weather air conditioning demand falls as the sun goes down. In cooler locations heating may drop as commerce and retailing close down for the day. Around 6.00 pm demand for cooking is high. Demand for lighting and for uses such as domestic television also increases until the daily cycle repeats.

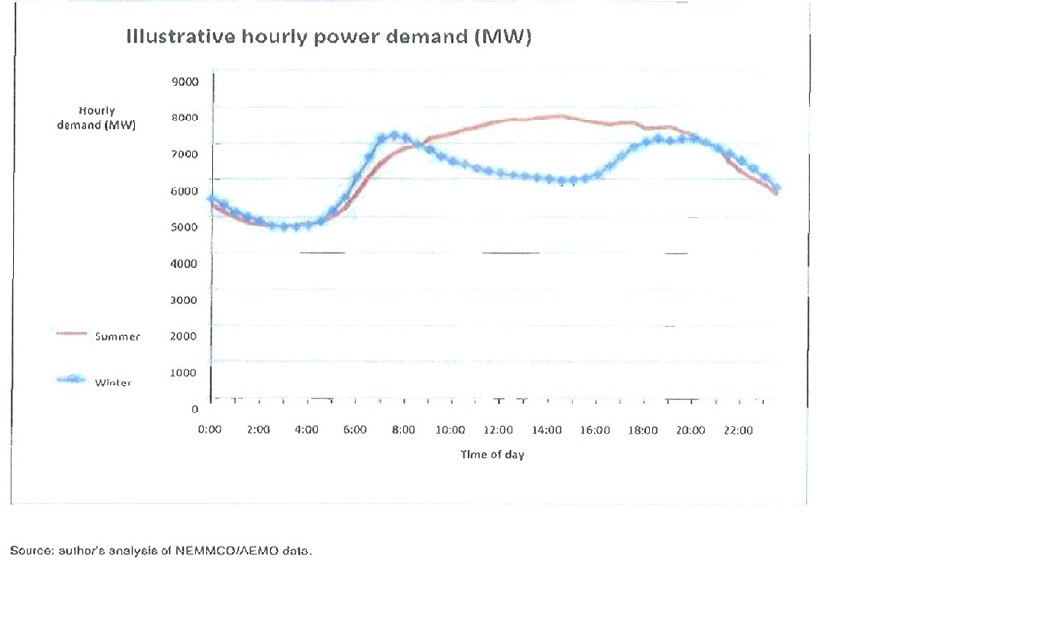

8 Figure 2 in Mr Thorpe’s report appears below. It shows typical daily fluctuation in demand for summer and winter days. Winter demand reflects lighting and heating requirements at the start and end of daylight hours, whilst summer demand reflects air conditioning requirements during the day and into the evening.

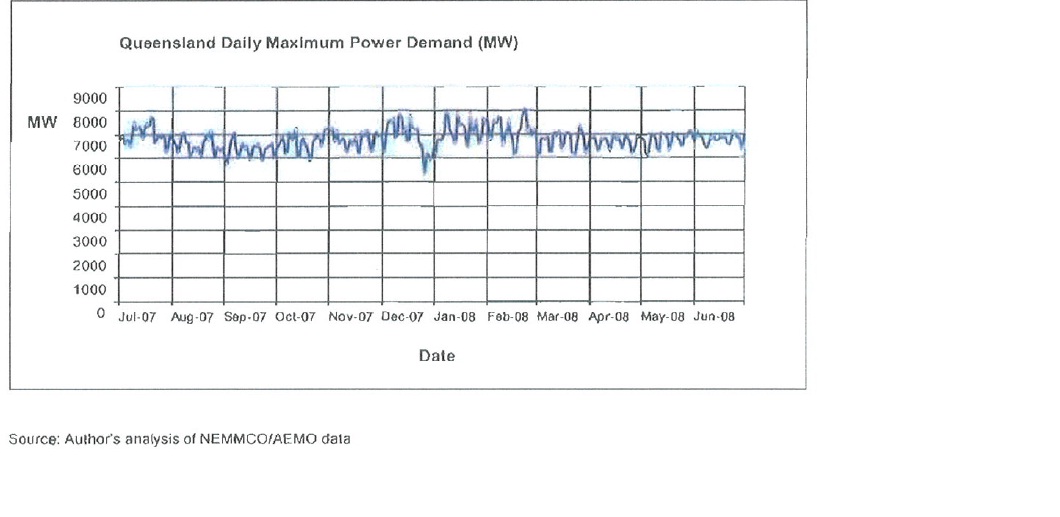

9 In Figure 3 (below) Mr Thorpe demonstrates the maximum or peak levels of power demand occurring during the 2007-2008 year in Queensland. Seasonal variations can be seen. The lowest peak demand was on Boxing Day. The Christmas and New Year period is generally the lowest demand period because of summer holidays and reduced industrial and commercial activity. This period of low demand is generally followed, later in January and February, by elevated demand due to air conditioning use. In general, there are higher peak demand periods in mid-winter and summer than in the rest of the year. In Australia demand is highly sensitive to weather conditions and associated heating and air conditioning requirements, resulting in significant day-to-day variations. In some other states there are even greater seasonal and daily variations than in Queensland.

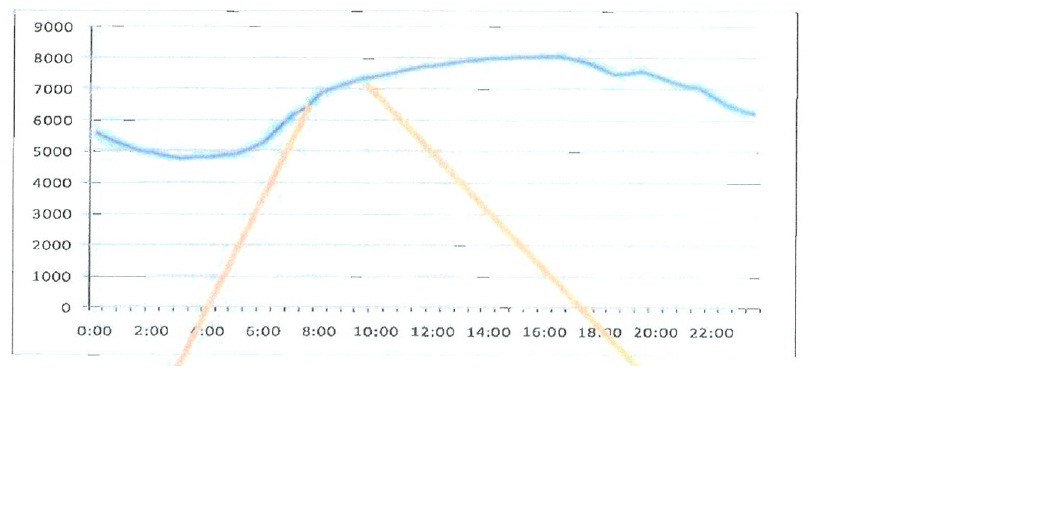

10 In Figure 4 (below) Mr Thorpe demonstrates the half-hourly demand trend in Queensland on 22 February 2008. It is typical of the variations experienced on a summer’s day.

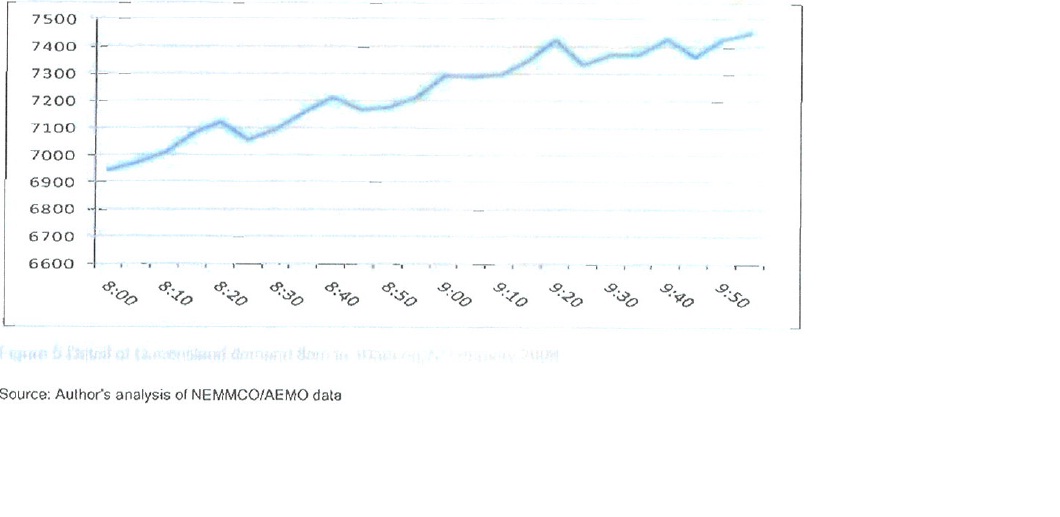

11 The diagonal lines indicate the part of the trend line (from 8.00 am to 10.00 am) which is considered in more detail in Figure 5 (below). Mr Thorpe says that there may be significant fluctuations within the general demand trend. Figure 5 shows demand for the 5 minute periods between 8.00 am and 10.00 am on 22 February 2008.

12 The “saw tooth” effect in Figure 5 cannot be seen in Figure 4. As I understand it, that effect demonstrates very rapid rises and falls in demand which the electricity generating and distribution system must meet. Such variation in demand imposes a number of constraints on the operation of power systems. In particular the Operator and generators need detailed knowledge of prevailing conditions and resources to manage the technical implications of fluctuations in demand.

13 Electricity, once generated, cannot be stored in any meaningful quantities. This characteristic has great significance in the technical and commercial operation of electrical power systems and the NEM. Electricity must generally be produced as it is needed by users. Hence aggregate production must track the short-term, saw-tooth shape of demand as it occurs. If the aggregate supply from all generators is not closely balanced with the aggregate level of demand from all users, the power system can become unstable. In extreme circumstances such instability may result in a complete shutdown of the power system with consequential interruption of supply. Widespread shutdowns are rare. Systems are designed and operated to avoid such occurrences to the extent that this is possible. However even a few seconds of imbalance between aggregate generation and aggregate demand can lead to instability. Stability of a system is indicated by fluctuations in its operating frequency measured in Hertz (Hz). The standard frequency in Australia is 50 Hz. If the frequency varies from 50 Hertz by more than one or two per cent, there is a risk of instability. Mr Thorpe explains this instability as follows:

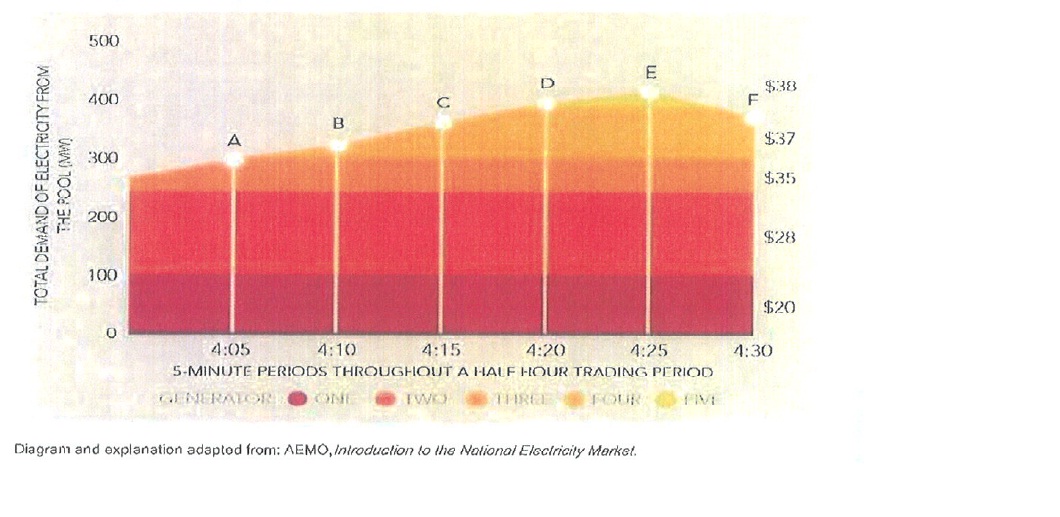

a. The electrical frequency at which a generating unit produces electricity is determined by the speed of rotation (rpm) and the construction of each turbine-generator unit;

b. Instability can occur because the rotating parts of power generating units are generally only able to operate safely within a relatively narrow range of speed of rotation and hence output electrical frequency;

c. If there is too much supply, for example due to the sudden disconnection of a block of customer demand when a transmission line is taken out of service due to a fault, the rotating machines may speed up to dangerous levels and potentially fail;

d. Conversely if there is too little aggregate supply, for example if a large generator is suddenly shutdown because of a fault, the remaining generators will slow down as they attempt to meet the full customer demand; and

e. Self-protection devices are built into turbine-generating plant [sic] to disconnect the units from the power system to avoid the plants running at unsafe speeds. In the case of under-supply, the failure or disconnection of a generating unit will exacerbate the under-supply and could lead to a cascading situation and eventual collapse of the power system.

14 As with any mechanical or electrical equipment, faults sometimes occur in generating units and in transmission and distribution networks. They may have to be taken off line for repair. There must be available reserve capacity in appropriate locations, with suitable response times, in order to keep power system frequency within safe bounds. Some generating systems have very short response times or other characteristics which make them especially suitable for use in the reserve role. Mr Thorpe says that some such systems are referred to as “ancillary services”. That term is defined in cl 3.11.1 of the Rules as:

… services that are essential to the management of power system security, facilitate orderly trading in electricity and ensure that electricity supplies are of acceptable quality.

15 In other words such services are vital aspects of the operation of the electricity supply system as a whole. Mr Thorpe presumably uses the term to describe generating units suitable for use in ensuring that such services are available as required. Other evidence suggests that there are special arrangements designed to guarantee the electricity supply necessary to maintain ancillary services, including arrangements concerning payments to generators for supplying such electricity. Mr Gnanananthan, formerly a trader employed by the respondent, gave further information concerning ancillary services. There are eight ancillary services markets. One such market is for power used in fine-balancing supply and demand. The markets are organized on the basis of 5 minute supply periods. Those periods are, themselves, divided into four second intervals. Although ancillary services are mentioned fairly frequently in the evidence, they are not of great importance in the case.

16 The generating units used to guarantee reserve and ancillary services are sometimes less cost effective than other units, and so may not always be in use when demand is low, and other sources are available. To guard against the risk that all available reserves may not be adequate to meet the demand created by a particular incident, systems are usually designed to permit disconnection of controlled amounts of customer demand. Similarly, to guard against a sudden drop in demand, systems are designed to permit disconnection of generating units. These mechanisms also provide a method of monitoring and recording changes in demand on a minute-to-minute or hour-to-hour basis.

17 The applicant was established pursuant to s 44AE of the Trade Practices Act 1974 (Cth), now the Competition and Consumer Act 2010 (Cth). Its functions are prescribed by the Law. They include the investigation of possible breaches of the Law, associated Regulations and the Rules and the conduct of proceedings in connection with any such breaches.

18 The Operator is responsible for various aspects of the electricity distribution system, including the NEM. In that capacity it effectively makes decisions as to the acceptance of offers by generators to supply electricity to the NEM. It is also responsible for power system security and for planning the development of the national transmission grid.

THE GENERATORS, INCLUDING THE RESPONDENT

19 At the relevant time there were nine generators selling electricity in the Queensland region of the NEM. The respondent was the largest single supplier, operating generating units at Stanwell, Gladstone, Kareeya, the Barron Gorge, and Mackay power stations. For present purposes the Stanwell and Gladstone power stations are of particular importance. At Stanwell there were four coal-fired, thermal, 350 MW generating units and at Gladstone, six coal-fired, thermal, 280 MW generating units. As I have said, electricity could also be acquired from the New South Wales generating system, using interstate connectors.

20 Some electricity generators sold electricity directly to larger end users pursuant to long term contracts. However much of the electricity produced was sold in the Spot Market which is part of the NEM. Operation of the NEM required that demand be tracked in order to match it with economical supply in prevailing conditions. This “dispatch process” had, as its dual objectives, reliable technical operation and economic use of resources. In order to manage the process the Operator had to predict future demand for electricity and have knowledge of available generating capacity. In particular, it had to know the quantities of electricity offered by the various generators at any point in time. Mr Thorpe suggests that the Operator had to “… judge the relative economic merits of calling different generators into service as demand rises and falls on the basis of the ‘dispatch cost’ presented to [the Operator]”. Mr Thorpe argues that the generators, in effect, would bid for shares of market demand by offering quantities of electricity at particular prices. Whilst the Operator sought to ensure continuity of supply to users at the lowest cost, generators sought to ensure that the amounts of electricity which they generated were disposed of and to maximise their returns. I have previously identified the need for reserve capacity, that such capacity might be provided by generating units which could be brought on line quite quickly and that those units may be more expensive to operate than other units. In periods of high demand, the cheaper generating units would be unable to meet demand, and so more expensive units would be brought on line. Only the prospect of higher prices would entice a generator to bring such units on line. A generator would seek to ensure that the electricity produced by its cheaper units was sold, whilst seeking to maximise its return by activating the more expensive units when the price was sufficiently high to justify their engagement. As will be seen, when the Operator acquired electricity at a higher price, all generators supplying electricity at the relevant time received the benefit of that price.

21 In discussing the market it is important to note one curiosity in its terminology. The regulations distinguished between dispatch bids, which reflected customer demand, and dispatch offers made by generators. However, in common parlance within the industry, both bids and offers were referred to generically as “bids”. Subsequent variations to either dispatch offers or dispatch bids were described as “rebids”. This latter usage was recognized in the definition provisions contained in Ch 10 of the Rules.

22 As I have said, trading of electricity in the NEM occurred in two broad forms, “spot” and “contract”. This case primarily concerns spot trading. Mr Thorpe described the NEM as occurring in a “mandatory gross spot market”, saying that:

a. It is mandatory as, with a limited number of exceptions … all wholesale quantities of electricity must be bought and sold through the Spot Market;

b. It is a gross arrangement as settlement of trading is for the entire amount of electricity produced by generators and consumed by retailers and large users;

c. It is a spot market as the trading occurs at Spot Prices determined on the basis of prevailing market conditions each half hour, although the design presumes market participants are likely to enter into bilateral contracts outside of the auspices of the [Rules]; and

d. The points of connection to the transmission networks of generators and wholesale buyers are grouped into geographic price regions and a separate Spot Price is set for each region. …

23 Contract trading occurred between buyers and sellers in parallel with spot trading, generally in the form of “contracts for difference”. Such contracts were made in advance and may have covered periods of some years. These contracts were, as Mr Thorpe puts it, “financial in nature”. The parties were free to agree on the contract price and other terms on a bilateral basis. However such trading was subject to legislative and regulatory oversight outside of the Rules. A contract for difference guaranteed that the generator would dispose of at least part of its capacity at a fixed price. Similarly, the end user had a guaranteed supply at that price. These contracts were generally performed by the payment of money by one party to the other, representing the difference between the relevant contract price and the spot price at the time of supply. Electricity was transferred between generators and contract customers using the various distribution networks. In the evidence these contracts are often referred to as “hedge contracts”.

24 The prices at which electricity was supplied reflected differences in generating technology. A turbine generating unit comprises a generating mechanism mounted on one end of a shaft. The shaft is made to rotate by a force acting on the blades of the turbine mounted on the other end of the shaft. When the turbine rotates, the generating mechanism produces electricity. Numerous technologies and fuels are used to drive turbines. They include:

steam produced by heating water in a boiler fuelled by gas, coal or other fuels;

hot exhaust gas from the combustion of fuels such as gas in gas turbines;

wind passing over the blades of wind turbines;

water falling from a height or flowing into a hydro-power station; and

emerging technologies, in various stages of development, including hot rocks as a source of energy to create steam, wave power and air heated in solar towers.

25 These technologies have different capital and operating cost structures which affect the cost of using them in producing electricity. Different technologies have different characteristics, affecting the rapidity with which they can be brought from standby mode to operating mode in order to respond to dispatch instructions. Generators were permitted only to submit bids for supply by generating units which were in operating mode and able so to respond. Relevant characteristics of different technologies are discussed below.

26 Steam boilers take between six and twenty hours to heat in order to produce sufficient steam to drive turbines and thus produce electricity. Hence there is a significant delay between a decision to call on an inactive steam generating unit and actual supply. Boilers have high capital costs which add significantly to the cost of thermal steam generating units. However they are often built in locations at which there is ample low cost fuel, so that operating costs can be lower than for other technologies. Typical average cost of electricity from a boiler-based generating unit using coal is $40.00 per MWh, of which approximately $25.00 to $35.00 per MWh is due to capital cost.

27 Gas turbine technology is less capital-intensive than thermal steam generation but makes less efficient use of fuel. As a result gas turbines generally have relatively low capital costs, but higher operating costs per unit of electricity produced. Gas turbines are very responsive. They can be brought from standby to dispatch in between 5 and 20 minutes. Because of the lower capital cost and relatively short response time, a gas turbine system is well suited to functioning as a reserve plant. It may be operated cost-effectively to meet short duration peaks in power demand.

28 Combined cycle generation technology is a combination of boiler and gas turbine technologies. The energy in hot exhaust gas from the gas turbine is used to heat water in a boiler in order to make steam to drive another turbine. Electricity is produced by generating units driven by both turbines, resulting in a greater electrical output for the same fuel input, and therefore lower cost per unit of electricity. Many new, gas-fired generating units use combined technology and are, as a result, cost-effective over a relatively wide range of operating roles. Some designs allow each part of the plant to be used separately. The plant is less efficient when so operated.

29 Hydro-generating units are generally more flexible than gas turbine units. Output can be changed by increasing or decreasing the flow of water through the turbine, using control valves. Operating costs are low, absent any external charge for the use of water. However hydro-facilities are generally capital-intensive. This is especially so for facilities associated with large water storage. Smaller facilities can be constructed at lower cost if located in the path of a rapidly flowing river. Larger facilities typically have high capital cost but low operating cost, again absent any external charge for the use of water. They have very short response times, in some cases, seconds, but in others, up to ten minutes. As a result such generating units can provide reserve services over varying timeframes. The amount of water available to drive such units may, from time to time, be limited, for example where the availability of water is affected by seasonal irrigation or annual snowmelt. In Queensland, there is a hydro-generator at the Wivenhoe power station. It is a “pumped storage facility”. Water is pumped into a high-level reservoir at times when the cost of electricity from other generators is low. The water is released through the turbine when higher-cost generation is needed. There are similar units elsewhere in Australia.

30 In 2008 generation in the NEM was distributed amongst fuel type as follows:

black coal – 49%;

brown coal – 17%;

hydro – 17%;

gas – 15%;

wind – 1%; and

other – 1%.

31 In Queensland black coal was by far the most significant fuel source used in the supply of electricity. There was also significant use of gas.

32 The Rules permitted generators to offer electricity at any point within a range from a high point of $10,000.00 per MW to a low point of minus $1,000.00 per MW meaning, in the latter case, that the generator would actually pay for electricity to be taken from it. This curiosity reflects the lack of capacity for storing electricity and the length of time taken to bring relatively cheap generating units on line. In general, generators prefer to keep units operating rather than to close them down, and then to re-activate them when needed. Thus, for presumably short periods of time, a generator might have chosen to pay the Operator to take electricity, ensuring that its load was consumed in advance of that offered by generators who had bid at higher prices, and avoiding the need to close down generating units. A generator was permitted to bid by offering dispatch volume in up to ten price bands, each having a specified price at which the generator was willing to supply an identified volume. In principle these bids were then ranked in merit order with the lowest price at the bottom of the list and the highest, at the top. In theory one would have expected the Operator to accept bids from the bottom upwards, until it had satisfied the aggregate demand of all customers for the relevant period. In fact the merit order was not so strictly applied for reasons associated with the structure of the power distribution networks and the geographical locations of various generators. The operation of the price bands can be demonstrated by this example taken from the applicant’s submissions:

Thus, if a [generator] is offering 10MW in price band 1, 10MW in price band 2 and 10MW in price band 3, it is in effect offering 30MW if the dispatch price reaches price band 3, 20MW if it only reaches price band 2 and 10MW if it reaches only price band 1.

33 The bidding process was conducted on a day-by-day basis. Each 24 hour cycle commenced at 4.00 am, the expected low point of daily demand. It was divided into 48 thirty minute Trading Intervals. Each Trading Interval was divided into six 5 minute Dispatch Intervals. Each Trading Interval was identified by its last minute. Dispatch Intervals were similarly identified. Thus “Trading Interval 13:00” was the Trading Interval between 12:30 and 13:00, using the 24 hour clock. “Dispatch Interval 13:00” was the Dispatch Interval between 12:55 and 13:00. Generators made offers in respect of each Trading Interval in a Trading Day. The bids were offers to supply fixed amounts of electricity for each Trading Interval. At the relevant time the Operator employed computing software known as the National Electricity Market Dispatch Engine (“NEMDE”) in calculating the way in which electricity was acquired and dispatched. The programme was run every five minutes and issued dispatch instructions to the various generating units in respect of which it had accepted bids. In effect the NEMDE programme was run at the beginning of each Dispatch Interval based on information received prior to its commencement, in order to calculate the Dispatch Price for that Dispatch Interval. The Dispatch Price was, in effect, that of the highest bid accepted for that Dispatch Interval. The evidence suggests that the Dispatch Price was published within one to two minutes of the commencement of the Dispatch Interval to which it related.

34 Each generator would submit its bids for each 24 hour period by 12.30 pm on the previous day. Generators could thereafter vary the amount of generation made available in each band but could not vary the price applicable to each band. Such “rebids” were permitted throughout the day. There was no formal cut-off time after which rebids would not be permitted. There was a working arrangement pursuant to which rebids were accepted as late as practicable. In practice rebids were allowed until one or two minutes before each NEMDE program run. The Spot Price for a particular Trading Interval was the average of the six Dispatch Prices for that Trading Interval. The Spot Price was the basis for financial settlements between generators and consumers in the NEM. All electricity acquired in the relevant Trading Interval was purchased at the Spot Price. The evidence suggests that the Spot Price for a Trading Interval was published shortly after the publication of the Dispatch Price for the last Dispatch Interval in that Trading Interval.

35 In order to perform its own functions and to assist generators in the bidding process, the Operator assembled and published substantial amounts of information relevant to NEM operations, including Dispatch and Spot Prices. Clauses 3.13.1 to 3.13.13 of the Rules identified other market information which it was obliged to distribute, including predictions concerning demand, available supply and price, based largely upon supply and demand bids already received. Information concerning the previous trading day was also made available. In addition to this very large amount of information, a generator also had information concerning its own generating capacity and current conditions, particularly weather conditions, which might affect demand. Forecasts were upgraded during the day. Actual and forecast dispatch generation levels for generating units in each region were available on an aggregate basis. Details of rebids were not published to other generators during the trading day in which they occurred. However the respondent’s evidence suggests that its operators had some knowledge of the pricing patterns of competitors. Information concerning rebids which had been accepted on a trading day were published on the following day.

36 Rebidding was regulated by cl 3.8.22 of the Rules as follows:

(a) Prices for each price band that are specified in dispatch bids, dispatch offers and market ancillary service offers are firm and no changes to the price for any price band are to be accepted under any circumstances.

(b) Subject to clauses 3.8.22(c) and 3.8.22A, a Scheduled Generator or Market Participant may vary its available capacity, daily energy constraints, dispatch inflexibilities and ramp rates of generating units, scheduled network services and scheduled loads, and the response breakpoints, enablement limits and response limits of market ancillary services.

(c) A Scheduled Generator or Market Participant must provide:

(1) all rebids to [the Operator] electronically unless otherwise approved by [the Operator];

(2) to [the Operator], at the same time as the rebid is made:

(i) a brief, verifiable and specific reason for the rebid; and

(ii) the time at which the event(s) or other occurrence(s) adduced by the Scheduled Generator or Market Participant as the reason for the rebid occurred;

(3) to the [applicant], upon written request, in accordance with guidelines published by the [applicant] from time to time under this clause 3.8.22 in accordance with the Rules consultation procedures such additional information to substantiate and verify the reason for a rebid as the [applicant] may require from time to time. The [applicant] must provide information provided to it in accordance with this clause 3.8.22(c)(3) to any Scheduled Generator or Market Participant that requests such information, except to the extent that the information can be reasonably claimed to be confidential information. The guidelines developed by the [applicant] under this clause 3.8.22(c)(3) must include:

(i) the amount of detail to be included in the information provided to [the Operator] under clause 3.8.22(c)(2); and

(ii) procedures for handling claims by Scheduled Generators or Market Participants in accordance with clause 3.8.22(c)(3) or 3.8.19(b)(2) that information provided to the [the applicant] by such Scheduled Generators or Market Participants under those clauses is confidential information.

The [applicant] must publish the guidelines developed under this clause 3.8.22 and may amend such guidelines from time to time.

(d) [The Operator] must:

(1) subject to the Scheduled Generator or Market Participant complying with clause 3.8.22(c)(1) and (c)(2)(i) and (ii), accept the rebid; and

(2) publish, in accordance with clause 3.13.4(p), the time the rebid was made and the reason provided by the Scheduled Generator or Market Participant under clause 3.8.22(c)(2)(i).

37 Clause 3.8.22A is critical to this case. It provided that:

(a) Scheduled Generators and Market Participants must make dispatch offers, dispatch bids and rebids in good faith.

(b) In clause 3.8.22A(a) a dispatch offer, dispatch bid or rebid is taken to be made in good faith if, at the time of making such an offer, bid or rebid, a Scheduled Generator or Market Participant has a genuine intention to honour that offer, bid or rebid, if the material conditions and circumstances upon which the offer, bid or rebid were based remain unchanged until the relevant dispatch interval.

(c) A Scheduled Generator or Market Participant may be taken to have contravened clause 3.8.22A(a) notwithstanding that, after all the evidence has been considered, the intention of the Scheduled Generator or Market Participant is ascertainable only by inference from the conduct of the Scheduled Generator or Market Participant, or of any other person, or from relevant circumstances.

38 The basis for remuneration of generators for electricity supplied was the Spot Price which was calculated for each Trading Interval, based upon the Dispatch Price for each Dispatch Interval comprising that Trading Interval. Pursuant to cl 3.9.2(d) of the Rules, the Dispatch Price “represented the marginal value of supply at that location and time, this being determined as the price of meeting an incremental change in load at that location and time in accordance with clause 3.8.1(b)”.

39 In para 109 of his report, Mr Thorpe gives a general indication of the way in which the process worked. He said:

Figure 12 presents the conceptual steps in scheduling process over a 30 minute period showing how the bands for a number of generating units are assembled and called in price order and the Dispatch Price for each 5 minute period determined by the price of the band at the margin, that is, the dispatch cost/price of the last band called. [The Operator] uses the most recent bid or rebid as appropriate relevant to the time.

a. The generator bands within bids and relevant rebids of different generators offering to produce electricity at any particular time (or in the case of scheduled loads to reduce consumption) can be visualised as being stacked in ascending order of dispatch price/cost.

b. Note that, although the example labels the bands as being from different generators, two or more of the bands may be from the same generating unit.

c. [The Operator] then calls or schedules for the lowest price/cost options to meet the prevailing demand. In the example shown:

i. In order to meet the demand at 4:05 (point A) [the Operator] will schedule generators one, two and three to the full availability offered. The Dispatch Price is based on the price of generator three at $35/MWh.

ii. At 4:10 (point B), in order to meet the increased demand at this time bands from generators one, two and three are fully scheduled and availability from generator four is partially scheduled and the Dispatch Price is based on the dispatch price/cost of generator four at $37/MWh.

iii. Similarly at 4:15 (point C), more of generator four is scheduled and the Dispatch Price remains at $37/MWh.

iv. By 4:20 (point D) a small amount of generator five is required and the Dispatch Price rises to $38/MWh.

v. By 4:25 (point E) more of generator five is required and the Dispatch Price continues to be set from it at $38/MWh.

vi. In the final 5-minute period of the half hour demand has fallen from its peak and none of generator five is needed and only part of generator four is required meaning the Dispatch Price is set from generator 4 at $37/MWh.

vii. The Spot Price for the half hour overall is the arithmetic average of the Dispatch Price in each of the 5-minute periods at $37/MWh.

40 Concerning the design of the NEM, Mr Thorpe says, at paras 122-124 of his report:

122. Amounts paid to generators, and by wholesale buyers, in the NEM are based on the Spot Price for the region in which they are located after adjustment for the effect of losses incurred in the transmission system.

123. This form of market design is known as an energy-only market.

124. The energy-only mechanism in the NEM is based on the well established economic principle of marginal pricing and is designed to enable market participants to establish the value of electricity over time through competitive pricing of their product to market. As a result Spot Prices can fall when there is a surplus and rise as demand approaches the available supply.

41 Paragraph 122 reflects the fact that in the course of transmitting electricity over the supply networks, there is some loss of energy. The Spot Price was adjusted to reflect the varying losses incurred, depending upon the location of each generating unit.

42 In a footnote to para 124 Mr Thorpe adds:

An objective of the design is that each generator will receive sufficient revenue to recover its capital costs and operating [costs] and a commercial level of profit but only if the overall portfolio of generating types and sizes is economically optimum. If it is not optimum one or more generation types may recover more or less than the “correct” amount. The over or under recovery is intended to create incentives for participants to either increase investment in a particular technology type that is currently recovering more than its costs, or to retire or reduce capability on those recovering less than the “correct” amount, in order that the overall portfolio of generation plant self corrects to the optimum over time.

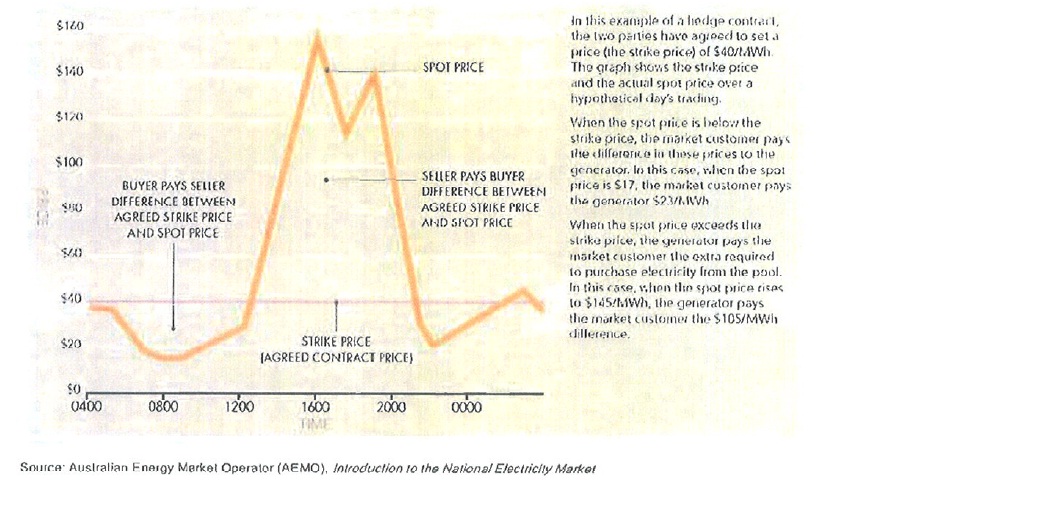

43 I have already referred to the practice of hedging adopted by generators and large consumers, often by “contracts of difference”. Mr Thorpe demonstrates the operation of such arrangements at paras 139-143 as follows:

139. In the following paragraphs I outline the operation of a number of the financial risk management instruments available in the NEM including hedge contracts introduced earlier at paragraph 63.

140. Depending on the volume of hedge contract each party enters into, typical contract forms provide stability of the net price paid by wholesale customers and received by generators for the contracted volume, irrespective of the Spot Price.

141. Figure 14 illustrates the effect of a hedge contract where the parties have agreed to a price of $40/MWh (i.e. in Figure 8 the value for $C is $40/MWh). Generators continue to receive the prevailing Spot Price (adjusted by the relevant loss factor for each participant) from [the Operator] for all of the energy they deliver to the network and the customer continues to pay [the Operator] at that price for all of their consumption. Under the terms of the hedge contract the parties also make or receive additional payments between themselves that results in the generator receiving and the customer paying net $40/MWh for the contracted quantity and the Spot Price for amounts in excess of the contract volume.

142. Note that generators face significant financial risk at high prices depending on the level of generation actually dispatched. This is because when the Spot Price is above the contract strike price and as [the Operator] only pays for the amount of electricity a generator actually delivers, but a typical contract obligates generators to make contract payments to counterparties for the difference between the Spot Price and the Contract Price for the contracted volume regardless of the amount the relevant generator(s) dispatches.

143. Accordingly there is a strong incentive for generators to ensure they achieve dispatch sufficient to cover contracted volumes, at a minimum. Generators also have an opportunity-cost incentive to generate above their contracted volumes whenever the spot price is above their actual [short run marginal cost], particularly if price is high. However, there will generally be a price-volume trade-off as price commonly falls if more generation is offered to market.

44 A generator’s need to cover its contract position is of some importance in this case. At a later stage, I shall discuss the matter in more detail. For the moment, I observe that for a generator, there was a tension between maximizing price and dispatching a particular volume of electricity. The process for resolving that tension is referred to in the evidence as a “price/volume trade off”.

45 Mr Thorpe discusses the relationship between price and investment, commencing with the proposition that in a market such as the NEM, very high prices might be efficient and necessary in order to provide a commercial return to generation investors. At paras 152-163 he observes:

152. Because customer demand is highly dependent on the weather and because electricity cannot be stored, some generation plants may only be called on to deliver energy for a very limited number of hours per year in periods of peak demand or following breakdown of other generators. These are termed peaking or peak load generators.

153. Although customer demand rises and falls across the day there is always some demand from customers and a need for a matching level of generation 24 hours per day. Generators that can cost effectively run 24 hours per day, termed base load generators, will generally offer bids and rebids that position them at the bottom of the dispatch merit order. In the NEM base load generators are predominantly coal fired thermal units.

154. In an energy-only market peaking generators can only cover their annual fixed costs and operating costs if they receive very high revenue from the spot market for the short time they are dispatched, or alternatively can arrange to receive at least some revenue from other sources, such as from the sale of hedging contracts to wholesale customers.

155. Typical hedging contracts provide a stable revenue stream for the generators as customers will make steady payments who in turn will be protected from the effects of volatile Spot Prices (for the contracted volume).

156. In principle the price a wholesale customer will pay a generator for a contract will be related to the likely expense the customer would be exposed to at Spot Price alone. Similarly a generator would seek a contract arrangement that at least covered its fixed and variable costs and reflected the amount it might receive from the spot market alone. Accordingly the potential exposure to Spot Price is a key factor in contract pricing.

157. Spot Price in the NEM can rise up to the maximum allowed level of $10,000/MWh. The following example illustrates why this relatively high amount aligns with the potential costs of low utilisation peaking generators:

a. Consider a hypothetical generating unit with typical cost parameters that requires revenue of $150,000/MW per annum of installed capacity to repay capital costs over its operating life, plus operating costs such as for fuel consumed when it is dispatched;

b. If this unit were operated in a base load role for 90% of the possible 8760 hours in a year (assuming it was undergoing maintenance for 10% of the time) each MW would produce 8760 [y multiplied by] 0.9 MWhs of electrical energy and require to be paid at an average wholesale price of 150,000 [divided by] 8760/0.9 = $19.0/MWh plus operating costs, in order to recover costs;

c. On the other hand, if this same generator operated as a peak load generator and ran only for 15 hours per year it would require a wholesale price of 150,000/15 = $10,000/MWh plus operating costs for every hour it ran; and

d. In practice the same technology would be unlikely to be cost effective for both peaking and baseload roles and thus the two types would require somewhat different prices – but not markedly so. The example is intended to illustrate the very significant effect that the duty cycle or number of hours of operation has on the revenue and price requirements for generators and to provide context for the occasionally very high Spot Prices.

158. Except for the peak hours of the year, generally there is more than enough capacity to meet demand in each region, although breakdowns of generators and periods of planned outages for maintenance can result in the demand approaching the level of capacity available for service at any time.

159. As a result Spot Price is moderate most of the time, for example Figure 13 presented earlier shows the Queensland region Spot Price was less than $100/MWh for 96.8% of 2007 – 08, but occasionally the Spot Price spikes to high levels and as noted earlier up to over $8,000/MWh in February 2008.

160. The prices in bids and rebids and the level of demand are key determinants of the Spot Price. However, the probability of any particular price band being called in the dispatch process is strongly impacted by the volume of relatively lower priced bands that are immediately available for dispatch by [the Operator].

161. Availability of lower priced bands is determined by the physical availability of different technology generators and the prices and volumes assigned to the bands of bids and rebids by participants to the extent permitted by the [Rules].

162. Ancillary service prices can vary over a similar range to energy. Historically ancillary service prices have been very low for most of the time but very occasionally spike to very high levels reflecting the opportunity cost that a generator forgoes from energy production when it provides an ancillary service at times when energy prices are very high.

163. In general generators will make decisions about the level at which they set “dispatch cost/prices” in bids and indirectly for rebids (through the volume in different price bands) depending on their actual costs, levels of hedge contract that they have negotiated with customers or other generators, market conditions and power system conditions. Generally they will also use the price bands to position different levels of output of generating units at different points of the merit order: for example where a generator operating a coal unit wishes to ensure that its unit is called to dispatch the minimum level that it can safely operate the unit at it will often set the price for its first bands relatively low. Similarly an operator of a gas turbine plant may wish to avoid short runs with marginal returns that might occur if it sets its price too low and thus sets a relatively high price so that it is only called if it is clearly profitable.

46 One might infer from the above explanation that generating units were either base load units or peak load units, and that the higher spot prices, which were occasionally available, were really designed to compensate the generators operating the latter category for only limited periods of time. However Dr Rose argues that generators operating base load units also needed the benefit of higher spot prices in order to operate on a viable financial basis. I do not understand the applicant to dispute that view.

47 At paras 167-183 Mr Thorpe addresses the role of information in the NEM. Again it is convenient that I set out the relevant paragraphs in full.

167. While the calculations for actual dispatch and price and the issue of instructions to generators are of necessity undertaken in the final minutes and seconds before the time electricity is consumed, preparation for dispatch and its associated trading commences a number of years before.

168. In the NEM many of the preparatory decisions are taken by market participants. However, [the Operator] has an oversight role and publishes aggregated information about future conditions to inform participants’ decisions. Relevant decisions and information includes:

a. Forecasts of demand for between the next 5 minutes and up to a number of years in advance;

b. Decisions about amount, location and type of generating capacity taken far enough in advance to allow new generation to be constructed;

c. Decisions about the timing of major shutdowns for maintenance;

d. Decisions about fuel supply;

e. Forecasts of likely wholesale price based on analysis of expected supply and demand;

f. Agreements between market participants about financial contracts;

g. Decisions about prices to be bid for dispatch; and

h. Decisions about rebids.

169. Efficient and effective decisions rely on the decision makers having timely, accurate and relevant information and forecasts. The [Rules] includes provisions designed to provide information to inform a number of the decisions taken by participants. Information published in accordance with cl 3.13 of the [Rules] is particularly relevant to decisions about rebidding.

170. Relevant provisions include a requirement for [the Operator] to prepare and publish a schedule with a resolution of 30 minutes for approximately one day ahead (30 minute predispatch schedule) showing:

a. Expected demands and prices in the different price regions;

b. Demand estimates (formed by [the Operator]);

c. Network capacity and ancillary service requirements current at the time of the preparation of the schedule; and

d. Details of the expected generation from each generator in the 30 minute predispatch schedule which are made available to the relevant generators, but not to other generators.

171. Information about the prices and volumes bid and rebid by each generator are not included in the 30 minute predispatch schedule but details of the final bids and rebids used for dispatch are published in full the following day (in accordance with [the Rules] cl 3.13).

172. [The Operator] updates the 30 minute predispatch schedule each 30 minutes and may also issue updates more frequently if circumstances change materially between routine updates.

173. After consultation with market participants, each 5 minutes [the Operator] also publishes a forecast for each 5 minutes of the next hour (5 minute predispatch schedule). Other than being calculated each 5 minutes and providing a 5 minute resolution, the 5 minute predispatch schedules contain information of the same form as 30 minute predispatch schedules.

174. Calculations in relation to 30 minute predispatch schedules, 5 minute predispatch schedules and for dispatch instructions (for the next 5 minute period) use the most recent bid or rebid available at the time of each calculation. Accordingly, rebids made less than 30 minutes before the time of dispatch may not appear in the last 30 minute predispatch, but will be taken into account in calculation of each 5 minute predispatch and dispatch instruction.

175. Rebids by generators are often the source of change in information provided in updates of 30 minute predispatch schedules and 5 minute predispatch schedules.

176. The NEM design places decisions with generators about how any limited amounts of fuel should be rationed and when a generator should begin preparations to present availability for future dispatch periods. Similar considerations apply for scheduled loads.

177. Consequently, the NEM also places decisions with generators about when it is efficient to not present capacity for dispatch, for example in order to undertake short term maintenance work, or because the value of a particular generator as evidenced by the forecast market price does not warrant it operating at that time.

178. The volumes and prices in bids and rebids are the primary means generators have to communicate their decisions to [the Operator]. The market forecasts that [the Operator] subsequently publish are a key mechanism by which [the Operator] disseminates relevant market consequences of those decisions – effectively inviting rebid(s) if appropriate.

179. I say inviting a rebid because I am aware from my experience that because of the potential for market and power system conditions to change rapidly it is normal and efficient practice for decisions to be reviewed and amended in the lead up to dispatch.

180. I am also aware from my experience that it is very difficult to design a set of conditions to limit the basis for rebids without excluding amendments that increase efficiency and therefore reduce the cost of production of electricity.

181. Similarly, decisions taken by [the Operator] as it prepares for dispatch and assesses the level of reserve and ancillary services and the likely loading on networks also require information.

182. [The Operator] has obligations under the [Rules] and [the Law] to ensure safe operation of the power system and has a power to intervene in the operation of the market in the event sufficient generating capacity is not presented to it through the bidding processes. To fulfil this obligation [the Operator] therefore must continually assess the outlook for security of the power system and determine if security standards are likely to be met or whether it should consider intervention. Intervention is a relatively rare occurrence.

183. Together, the provisions for bids and rebids, 30 minute predispatch schedules, 5 minute predispatch schedules and assessments of the security of operation, spot pricing and financial contracting are designed to elicit decisions by participants based on commercial incentives that deliver cost effective, reliable and secure operation of the wholesale market and allow [the Operator] to assess if it needs to intervene.

48 Although the Operator may have had both short and long term responsibilities and required information to perform those duties, paras 175 et seq demonstrate that rebids were primarily to reflect commercial considerations, and that it was difficult to design limitations which would accommodate that fact.

49 At paras 184-194 Mr Thorpe describes “underlying principles” which reflect his views as to the way in which the market was designed in order to achieve efficiency in the supply of electricity as follows:

184. Earlier sections have presented descriptions of the relatively detailed measures for bidding and rebidding and operation of the dispatch process and how they interact and accommodate the complex technical characteristics of electricity. This section aims to very briefly set these arrangements in the context of a market designed to deliver reliable and cost effective electricity in order to address the final questions put to me concerning inaccuracy in bids and rebids (dispatch offers).

185. In very general terms an efficient market will see buyers and sellers identify a fair value for the commodity being traded.

186. Information about future prices and market conditions is crucial in this regard. In the electricity sector this is complex as conditions vary continuously because electricity is not storable and demand varies markedly over a day. As a result different generators must be brought in and out of service across the daily cycle of operation as part of the dispatch process.

187. As different generating technologies have different operating costs (see Section 4) and need to recover different fixed costs, the cost to supply varies significantly.

188. In the longer term, economies of scale can be significant as well, meaning that investment and retirement is “lumpy” and the cost effective size of new generating units will be somewhat larger than is needed immediately – creating a short term surplus. As a result the supply/demand balance often will move from just sufficient to a surplus which will be eroded over time as demand grows or old generators are retired from service until the investment cycle repeats.

189. In the NEM buyers and sellers are expected to find an agreed set of prices and volumes in a mix of short term spot and longer term contract trading. However, there are strong linkages between the two forms of trading. If either is distorted the other is likely to be distorted also and distortion will generally mean lower efficiency and higher cost, which is eventually borne by consumers.

190. The bidding and rebidding provisions are a key element of the overall functioning of the NEM and are designed to assist the participants find an agreed set of spot and contact positions and in particular to respond to changing circumstances.

191. The different characteristics of different generating technologies noted earlier affect the practical capability for amendment via rebids for the different technologies – for example a technology with a long start up time cannot change a decision not to offer capacity at just a few hours notice.

192. As a result:

a. Only those generation plants already in a condition to increase production, such as a boiler fired steam turbine plant that had been started previously or generation plants with rapid start up time can respond to changing conditions close to the time of dispatch; and

b. It is generally the case that closer to the time of dispatch fewer generators can physically increase their total capacity available to the market (that is the sum of all price bands), but all that are available are able to adjust the volume within each price band (up to the capacity that is available).

193. Similarly, any arrangements for demand side response may require a number of hours notice to arrange.

194. Information is a key part of most markets establishing a fair and reasonable price and is the basis for the requirements for [the Operator] to publish forecasts and historical information discussed earlier (see paragraph 167).

INACCURACIES IN THE BIDDING PROCESS

50 At section 7.4 of his report Mr Thorpe offers his views as to the effects of inaccuracy in the bidding process as follows:

7.4 Forecast inaccuracy and dispatch inaccuracy

195. I now turn to the consequences of inaccurate bids and rebids.

196. Bids and rebids may be seen to be inaccurate in two ways, which for the purposes of this report I will term Forecast Inaccuracy and Dispatch Inaccuracy. Both forms can have physical and commercial impacts on the market as a whole and on individual participants.

7.4.1 Forecast inaccuracy

197. Forecast Inaccuracy occurs when subsequent to a bid or rebid being made, a participant submits a rebid (or further rebid) before the time of dispatch. To the extent that information in the first bid or rebid(s) is altered by the final rebid, the information in the first bid or rebid will have been inaccurate.

198. This may seem a harsh term to apply to a situation where new information comes to light and the information in both the first and any subsequent bids and rebids was accurate at the time it was presented.

199. However, the earlier information will have been the basis for a number of forecast and decisions, in particular:

a. [The Operator] will have counted now inaccurate capacity foreshadowed in the earlier bid or rebid in their planning for power system operation, including provision of reserve needed to maintain system security;

b. [The Operator] may have made decisions to allow or disallow planned network outages or to issue, or not issue, low reserve notices in accordance with cl 4.8 of the [Rules]; and

c. [The Operator] will have prepared and issued 30 minute predispatch schedules and 5 minute predispatch schedules including information for:

1. power system operation;

2. dispatch of all schedulable generation and demand side blocks;

3. predictions of network flows;

4. forecasts of Spot Price; and

5. forecasts of Dispatch Price.

200. Each of these items may therefore be inaccurate although the degree of error will be dependent on the circumstances and may range from very large to immaterial.

201. Participants may have acted on the forecasts of dispatch volumes and prices in forming any rebids they have made.

202. End users who are not market participants in their own right may arrange to buy from a retailer that is a participant under an arrangement that passes through all or part of the relevant Spot Price.

203. End users may wish to do this where they manage controllable demand (or small non market in-house generators that can be used to reduce the users net demand) and I would expect they will then actively monitor market conditions and make decisions about their operations – although I would expect these to be limited to situations where only extreme prices had been forecast on the basis of the first bid and rebid.

204. The final rebid may also be inaccurate at the time of dispatch giving rise to Dispatch Inaccuracy.

7.4.2 Dispatch inaccuracy

205. Dispatch Inaccuracy occurs when bids or rebids contain inaccurate information about the physical capability to respond to a dispatch instruction.

206. As noted earlier, [the Operator] uses the information contained in the bid or last rebid it receives before undertaking a dispatch calculation and issues associated dispatch instructions on the assumption all scheduled generators and scheduled loads can comply with the instructions. However, if a scheduled generator or scheduled load receiving a dispatch instruction finds that they cannot comply with their instructions because their particular plant is not able to operate to the level envisaged when they formed the bid or rebid due to an unexpected technical problem with their plant, by default that bid or rebid therefore will be shown to be inaccurate.

207. The consequences of a dispatch based on bids or rebids that lead to Dispatch Inaccuracy may include:

a. Ancillary Services will automatically compensate for the scheduled unit that does not respond as expected – for example if a generator had been instructed to increase in accordance with an inaccurate bid Ancillary Services will detect that this has not occurred and increase in its place;

b. [The Operator] may have over or under provided for different forms of operating reserves leading to increased costs or risks to operating security, or both;

c. [The Operator] may have made different decisions about allowing network outages to proceed leading to increased costs to network operators (and thus eventually to customers who pay those costs); and

d. Other participants may have made different decisions about their rebids had they been aware of the consequences of the inaccuracy in a bid and therefore suffer an opportunity loss.

208. It is important to note that both Forecast and Dispatch Inaccuracies also can occur in the normal course of operation of a power system and market operation. Unexpected technical problems that limit responses from generators in particular do occur.

209. Further, efficient operation of the NEM is premised on participants responding to forecasts of future market outcomes for both dispatch volumes and prices. For example, initial bids would normally be developed on the basis of expectations of market outcomes on the basis of experience and contracting prices.

210. However, if a price forecast in a 30 minute predispatch schedule and 5 minute predispatch schedule shows a higher or lower price than was expected, all participants would normally review their operation to consider if, subject to cl 3.8.22 and 3.8.22A, they should rebid. For example:

a. To offer increased capacity in response to a high price due to shutdown of another participant or because they perceive the market value has changed;

b. To offer less capacity in response to a lower than expected price due to early return to service of a low cost generator or changes in volumes offered in low priced bands of another generator; or

c. To offer different amounts of capacity at the prices of the bands established at the time of the initial bid.

51 I note that Mr Thorpe’s category of “forecast inaccuracies” includes any bid or rebid which was superseded by a rebid or further rebid. However the Rules permitted rebids and further rebids. The evidence suggests that rebids were accepted up until very shortly before the commencement of a relevant Dispatch Interval. Thus it would seem to be at least arguable that the Rules recognized the value of late bids or rebids, whatever the effect on the integrity of decisions made on the basis of any earlier bid or rebid. Further, as Mr Thorpe demonstrates at paras 175-183, rebids were intended to reflect commercial considerations. They occurred in a very complex structure, designed to collect, supply and analyse an enormous amount of information in a very short time. It is, perhaps, implicit in Mr Thorpe’s evidence that even a small “inaccuracy” may have had surprising consequences, or that the combined consequences of numerous “inaccuracies” may have been surprising. One must, however, question his use of the term “inaccuracy”. Forecasts are, after all, by definition, subject to change, particularly where they are based upon such a wide range of information which, itself, is subject to change. Use of the word “inaccuracy” to describe an earlier bid or rebid simply because a later bid varies it is not only “harsh”, to use Mr Thorpe’s description, but also, itself, inaccurate. Both earlier and later bids and rebids might reflect bona fide assessments of conditions at the relevant times. Mr Thorpe seems to say that changed conditions, as reflected in rebids or further rebids, might have led to the need to change earlier decisions. That situation seems to be contemplated by the market design.

52 Clearly, the vast amount of information available and supplied by the Operator was intended for use by generators in bidding and rebidding. As Mr Thorpe says, market participants acted on the basis of available information. During the trial I expressed the tentative view that the conduct which is impugned in this case may well be seen as an attempt to acquire further information about market conditions. If that characterization is correct, then it would be curious if the Rules were to be construed so as to prohibit such conduct, at least in the absence of any clear intention so to do.

53 I turn to Dr Rose’s evidence. First, Dr Rose dealt with the question of system instability, pointing out that the system was designed to remain stable, at least over a short period, even without intervention by the Operator. All generating units connected to the NEM were equipped with automatic governor mechanisms which provided a response to any sudden load increase or decrease. As most load changes would amount to only small percentages of total demand, and as such changes and resulting changes in frequency would be spread amongst all generating units, the individual effect would be small and co-ordinated amongst the units. There was also provision for automatic responses from the control centre or manual intervention by dispatchers. These responses would be slower. In general they were not dependent upon communication systems which might be subject to failure, resulting in a system-wide blackout.

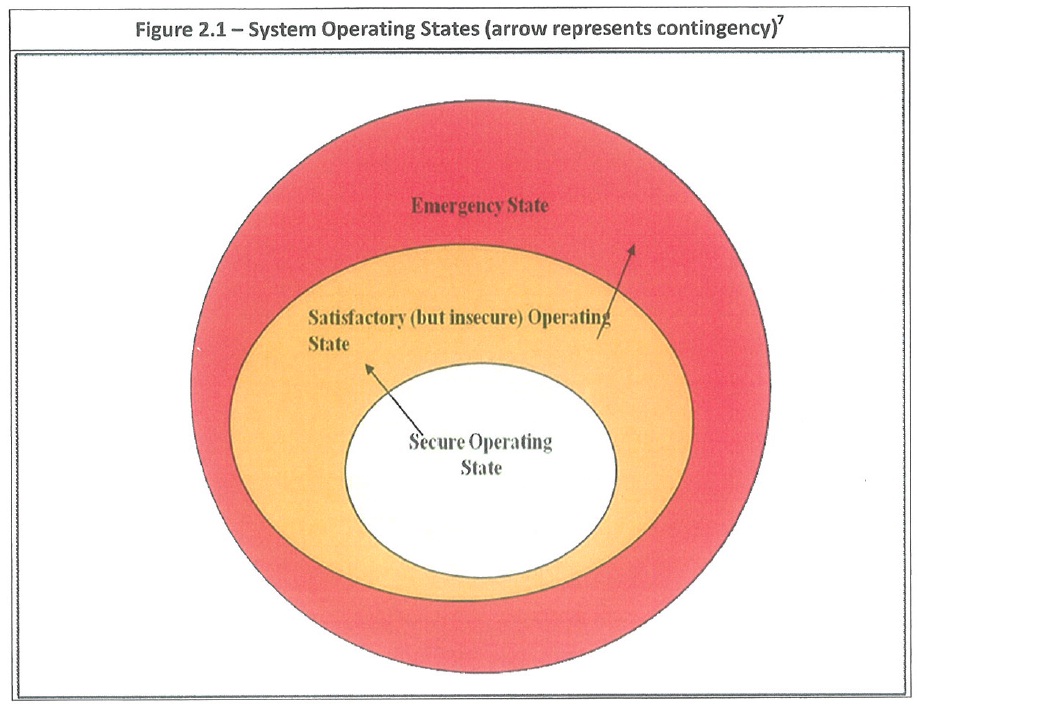

54 Dr Rose gives significant further information concerning system security, but I need not discuss it for present purposes. He stresses the proposition that system security should be seen as an “envelope” within which the system must be kept, rather than a sole “safe” point at which it must operate. Dr Rose demonstrates this point in his Figure 2.1, below. The “envelope” of secure operation is surrounded by a larger “envelope” of satisfactory, but insecure operation. The Operator’s role was to identify movement from the secure operating state to the satisfactory, but insecure state, to take action to prevent movement to the emergency state and to return the system to the secure state.

55 In Dr Rose’s view the Operator’s role was to oversee the NEM in order to ensure that it managed itself at five minute intervals throughout the bidding process, rather than to “control” the grid. The Operator had software tools which enabled it to assess the security of the system, whilst allowing generators to manage their production through their competitive bids. The 5 minute Dispatch Intervals facilitated such assessment. Dr Rose says that the system was designed to minimize the risk of instability, and to ensure that generating units operated within satisfactory boundaries, notwithstanding fluctuations in demand.

56 Dr Rose distinguishes between rebids which change total available capacity and rebids which move available capacity between price bands. As to changes in total capacity, Dr Rose points out that subject to one exception, any such rebid would reflect changes in the physical capability of the plant to provide the maximum level of capacity at any price. The exception was the case in which a generator withdrew capacity in the expectation that the Operator would direct it, pursuant to the Rules, to operate the generating unit in question. A generator might take that course if the generating unit was connected to a part of the network where additional generation was needed in order to avoid network overload, but the value of the Spot Price was lower than the price at which the generator was willing to operate the generating unit. That situation might arise as the result of local circumstances not generally prevailing throughout the network. If a generator withdrew a generating unit, the Operator could direct its re-instatement. Where such a direction was given and complied with, an investigation would be conducted, leading to the generator being paid a fair price for its generation. Dr Rose concedes that a reduction in available capacity may cause reduced security or stability within the system. However he considers that whether it is likely to do so depends upon the efficacy of the measures which are in place in order to deal with such changes. Elsewhere in his evidence he makes it clear that he considers that significant instability is unlikely.

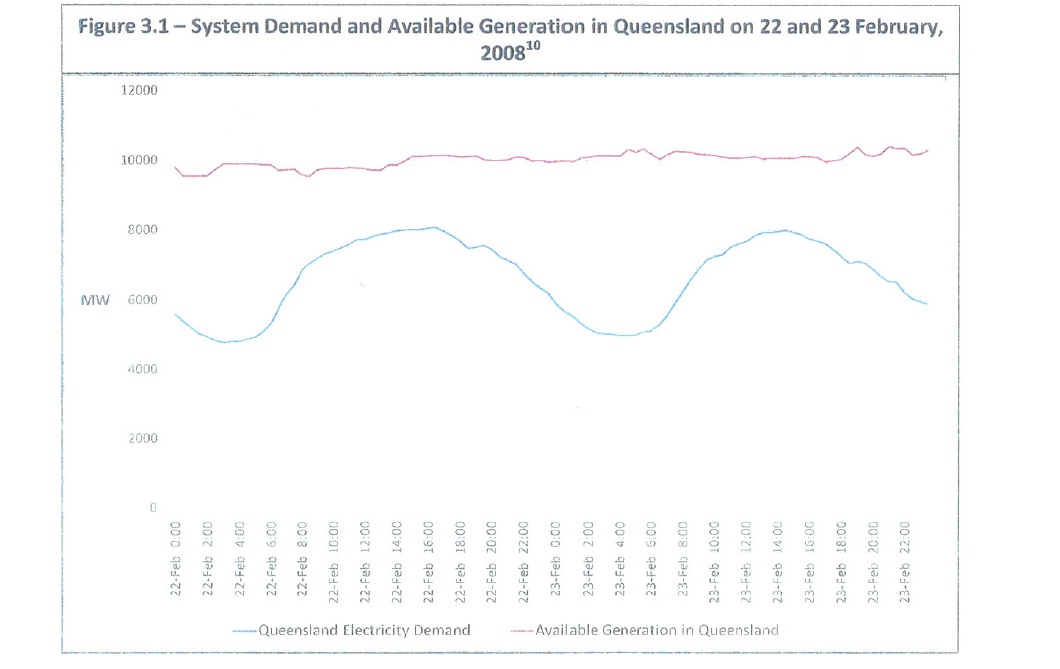

57 As to the movement of capacity between price bands, such action would affect the price at which power was available but not the level of supply. Each generator had up to ten price bands, any of which may have been setting the price at a point in time. Generators did not have access to competitors’ rebids as they were submitted, although some aggregated information was available. Dr Rose observes that on 22 and 23 February 2008, the dates with which this case is concerned, even at peak load periods, there was spare capacity in Queensland of approximately 2,000 MW. See Figure 3.1 below. In those circumstances a single generator could not have been sure that its rebidding would have resulted in an increase in the Spot Price rather than non-sale. That observation is of some importance in this case in connection with price/volume trade off.

58 This Figure shows that, for 22 and 23 February 2008, available generation was fairly constant at about 10,000 MW. Demand fluctuated between about 5,000 MW and 8,000 MW, with the low points being early in each morning, and the high points being around the middle of the day.

59 Information acquired in the 5 minute dispatch process was used by generators and was also available for use in ensuring system security. However Dr Rose asserts that the Operator’s dispatcher focused on the next 5 minute Dispatch Interval and did not attempt to manage energy resources over longer periods of time. In this respect, his evidence differs in emphasis from Mr Thorpe’s. I do not understand Dr Rose to be saying that planning and security were not the Operator’s concern. Rather, he is saying that rebids did not raise the need for human decision-making which might require time and distract the decision-maker from other duties. The NEMDE programme was designed to deal with such rebids, both in accepting bids and in ensuring system security. He also points out that at all material times the market was functioning within a comfortable margin as between supply and demand, notwithstanding the fact that demand was unusually high. At paras 32-34 Dr Rose describes the system as follows:

32 The bids and rebids for MW outputs of the generators, together with the system load, are therefore the primary tools for managing security, and are automatically processed by the NEMDE dispatch system to maintain the technical envelope.

33 The market works in this way. The generators send their MW preferences each 5 minutes for the next 5 minutes through their bids and rebids. It is not necessary for a generator to submit rebids for each 5 minutes unless they choose to do so. They are then sorted at the control centre on the basis of ascending prices and dispatched MW.

34 The control centre software sorts the bids into an ascending list from the lowest price to the highest price called a ‘bid stack’, which will be used to dispatch the bid bands for all generators in order, and assesses it for security implications. If the generator ‘bid stack’ will result in line overloads or other actual or contingent breaches in security, the bid stack is adjusted by NEMDE at the least increase in market cost, to meet the security criteria. NEMDE does this by replacing lower priced bids by higher priced bids such that the dispatch objective of maximising the efficiency of market dispatch is achieved without compromising security.

(Emphasis in original.)

60 As I understand it, Dr Rose is here dealing with the way in which the Operator, through its dispatchers, addressed bids received from generators in order to meet demand and maintain system security. In some circumstances, it may have been necessary that a higher bid be accepted over a lower bid in order to maintain system security. As the Dispatch Price for the Dispatch Interval would be, in effect, the highest bid accepted, that price would be increased by acceptance of a higher bid. Dr Rose then discusses various aspects of the systems used for maintaining security in the market. It is not necessary that I deal with those aspects. Dr Rose considers that neither rebids as to capacity nor those as to price band allocation would cause any disturbance to the grid or reduction in security, other than in exceptional circumstances. Dr Rose is not aware of any incident where rebidding behaviour has led to instability and widespread shutdowns.

Generating technologies and costs

61 Dr Rose then addresses the various generating technologies, highlighting some of their economic characteristics. Dr Rose considers that the role of coal-fired generating units was closely related to their short-run marginal cost (“SRMC”) for most of the time. He considers that market design dictated that for a large percentage of time, a generator would bid at just above its marginal cost, that is the cost of producing additional electricity. He further suggests that a generator would tend to bid the “shadow price” which is the SRMC of the next generator in order of ascending SRMCs. This bidding practice enabled a generator to increase bid price slightly without sacrificing production volume. Dr Rose observes that coal-fired generators tended to bid in merit order, that is in a band between SRMC and the shadow price in order of ascending SRMCs. This had a marked effect on what is called the “capacity factor”, in effect the percentage relationship between average production level of a generating unit and its maximum production level. The average production level was, of course, dictated by market forces.

62 The coal-fired generating unit in each region which had the lowest SRMC would operate at or near base load whenever it was available to do so. Coal-fired generating units with higher SRMCs would operate progressively less frequently because of the difference demonstrated in Fig 3.1 (see earlier) between power demand and available generation. By definition a generator which bid its SRMC would not be able to recover any of its fixed costs unless other generators were bidding higher prices and setting a higher Spot Price. The result was that the lower SRMC base load generators would be on line at all times. Whenever higher SRMC generating units were running, the lower SRMC units would recover their SRMCs and part of their fixed costs, as the higher SRMC generating units would be forcing up the Spot Price. However the higher SRMC generating units would be off-line or operating at reduced levels for most of the time. When they were on line they would tend to be setting prices at or near their own SRMCs and would not be able to recover their fixed costs, except for periods when prices were very high, and peak load generators were setting the price. These periods were rare and of considerable importance to the less competitive coal-fired generators in meeting their fixed costs.