FEDERAL COURT OF AUSTRALIA

Seller v Deputy Commissioner of Taxation [2011] FCA 865

| IN THE FEDERAL COURT OF AUSTRALIA | |

| Applicant | |

| AND: | DEPUTY COMMISSIONER OF TAXATION Respondent |

| DATE OF ORDER: | |

| WHERE MADE: |

THE COURT ORDERS THAT:

1. The Application as filed on 24 May 2011 is dismissed.

2. The Applicant is to pay the costs of the Respondent.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011. The text of entered orders can be located using Federal Law Search on the Court’s website.

| NSW DISTRICT REGISTRY | |

| GENERAL DIVISION | NSD 716 of 2011 |

| BETWEEN: | ROSS EDWARD SELLER Applicant |

| AND: | DEPUTY COMMISSIONER OF TAXATION Respondent |

| JUDGE: | FLICK J |

| DATE: | 3 AUGUST 2011 |

| PLACE: | SYDNEY |

REASONS FOR JUDGMENT

1 On 24 May 2011 an Application was filed in this Court seeking to set aside a Bankruptcy Notice that had been issued on 4 March 2011.

2 The proceeding first came before the Court on 23 June 2011. On that occasion, Counsel then appearing for the Applicant explained that there were two grounds upon which it was sought to have the Bankruptcy Notice set aside, namely:

as served, the Bankruptcy Notice did not annex a complete copy of the judgment relied upon, namely a default judgment issued by the Supreme Court of New South Wales on 24 December 2010 – but only a part of that judgment; and

an abuse of process said to have been engaged in by the Deputy Commissioner in issuing the Bankruptcy Notice.

Both parties wanted the proceeding stood over to a future date to enable a proceeding that had been commenced in the Supreme Court of New South Wales to proceed first. Little was known as to the nature of that proceeding other than that it was apparently an application to stay the judgment. That proceeding was to come back before that Court on 1 August 2011 with a view to a hearing date being set. The Applicant submitted that to defer the resolution of the proceeding in this Court would avoid incurring unnecessary legal costs.

3 On that first occasion, an indication was given to the parties that there was no reason why such issues as arose from the form in which the Bankruptcy Notice was said to have been served could not be heard and determined on either 30 June or 1 July 2011. The ambit of any factual dispute was confined, the evidence relevant to that issue had been filed and served and the ambit of the legal issues to be resolved was also within a confined ambit. The matter was stood over to 24 June 2011 with a view to the parties considering whether any of the witnesses would be required for cross-examination and the availability of Counsel.

4 On the following day, Counsel appeared for the Applicant and explained that no reliance was to be placed upon the form in which the Bankruptcy Notice had been served. It emerged that a copy of the judgment – and not a mere part of it – had in fact been annexed to the Bankruptcy Notice. Given the abandonment of that part of the Applicant’s case, attention was then directed to the abuse of process ground. Again, both parties wanted that part of the case stood over until after the conclusion of the Supreme Court proceeding. But, again, even that part of the case ultimately depended upon:

a chronology of events which was largely uncontroversial;

submissions as to the factual inferences to be drawn from that chronology; and

submissions as to the legal consequences that would flow, depending upon what inferences (if any) should be drawn.

The preferable course, it was considered, was to proceed to hear and determine the Application that had been commenced in this Court. A certain hearing date could be provided to the parties and such costs as would be incurred were costs confined to a limited factual and legal dispute. Senior Counsel for the Respondent was contacted with a view to determining his availability. He was in fact available, as was Counsel for the Applicant.

The Form of Judgment Annexed to the Bankruptcy Notice

5 Although reliance upon this ground of challenge to the validity of the Bankruptcy Notice was abandoned, it should be briefly addressed.

6 The Applicant in the proceeding, Mr Ross Edward Seller, is a solicitor – and hence an officer of the Court.

7 He filed his Application in this Court on 24 May 2011. The Affidavit he filed in support of his Application was sworn on 24 May 2011. In that Affidavit he referred to the Bankruptcy Notice which had been issued on 4 March 2011 and served on him on 3 May 2011 and relevantly stated on oath as follows:

The Bankruptcy Notice

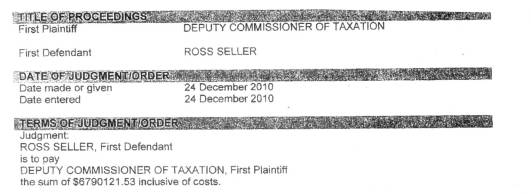

2. On 3 May 2011 I was served with Bankruptcy Notice 1520 issued on 4 March 2011 (“the Bankruptcy Notice”). Annexed hereto and marked “A” is a true copy of the Bankruptcy Notice as it was served on me.

3. At the top of the final page of the Bankruptcy Notice is what appears to be part of a copy of the judgment the Respondent (“The DCT”) relies on for the issue of the Bankruptcy Notice. I am not sure what court or proceedings that judgment was obtained in.

4. The reason why I am not sure what court or proceedings the judgment the DCT relies on to have the Bankruptcy Notice issued was obtained in is because the judgment in the form it is attached to the Bankruptcy Notice is not sealed, does not indicate the court it was obtained in, and does not state the proceeding number in the court it was obtained in. Without that information I cannot determine if I was served with the originating process or the nature of the proceedings.

Annexure A, being the form of judgment said to have been annexed to the Bankruptcy Notice, appeared as follows:

Given the information in fact disclosed, even in that part of the judgment that was annexed to the 24 May 2011 Affidavit, it is perhaps curious that Mr Seller stated he was “not sure” which Court issued the judgment or the proceeding in which the judgment had been obtained. But such matters may be left to one side.

8 On 16 June 2011, Mr Seller swore a further Affidavit in this proceeding. In that Affidavit he made a series of what he termed “correction[s].” But no “correction” was made to paragraphs [2], [3] or [4] of his earlier Affidavit.

9 Presumably the argument that Mr Seller had sought to advance was (in summary form) that the form of Bankruptcy Notice which had been served was not in the form prescribed in Regulation 4.02(1) of the Bankruptcy Regulations and, accordingly, there had been non-compliance with ss 40(1)(g) and 41 of the Bankruptcy Act 1966 (Cth). And, presumably, Mr Seller would also have submitted that such non-compliance was not a “formal defect or… irregularity” for the purposes of s 306 of the Act. A series of decisions have addressed the consequences flowing from defects in the form of a bankruptcy notice: e.g., Re Scerri (1998) 82 FCR 146; Commonwealth Bank of Australia v Horvath [1999] FCA 143; Bendigo Bank v Williams [2000] FCA 482, 98 FCR 377. A series of decisions have also addressed the question as to whether a defect is substantive and not formal. A defect is substantive where a bankruptcy notice fails to meet a requirement made essential by the Act: e.g., Kleinwort Benson Australia Limited v Crowl (1988) 165 CLR 71 at 79 to 80 Mason CJ, Wilson, Brennan and Gaudron JJ; American Express International Inc v Held [1999] FCA 321 at [13], 87 FCR 583 at 585 per Kenny J.

10 The abandonment by Mr Seller of these arguments necessarily means that the application of these decisions to the facts previously relied upon need not be further pursued.

11 But that which should be briefly mentioned is the explanation provided by Mr Seller by way of oral evidence as to how the 24 May 2011 Affidavit came to be sworn. That explanation was that he had scanned the Bankruptcy Notice which had been served upon him into his computer and thereafter relied upon the scanned copy – and not the original – when preparing his evidence. The copy was, it was said, not scanned in its entirety. The original copy only came to light when Mr Seller’s legal advisors shortly before the hearing asked for it to be provided. Even that explanation, if accepted, left unexplained why proper care had not been taken when preparing the 24 May 2011 Affidavit to ensure that it was factually accurate. The form of the Bankruptcy Notice said to have been served was not an incidental part of the case sought to be advanced; it was a fundamental part of the argument as to why it should be set aside.

12 The importance of ensuring that an affidavit presents to the Court – and an opposing party – a factually accurate account of the facts is fundamental to the administration of justice. An affidavit may be either “sworn or affirmed”: Federal Court of Australia Act 1976 (Cth), s 45(1). There are important obligations assumed by both a deponent to an affidavit and by the person who prepares an affidavit and before whom an affidavit is sworn or affirmed: Justice Arthur Emmett, ‘Practical Litigation in the Federal Court of Australia: Affidavits’ (2001) 20 Australian Bar Review 28 at 33 to 36.

13 Any deponent, especially a solicitor, should know the importance of taking proper steps to ensure an affidavit is factually correct before it is sworn. Mr Seller, even on his own account, obviously failed to do so. Given the importance as to the form of the Bankruptcy Notice as served to the Application being brought, the steps belatedly taken immediately prior to the proceeding coming on for hearing should have been undertaken far earlier by those before whom the Affidavit was first sworn on 24 May 2011.

Abuse of Process — relevant principles

14 The abandonment of Mr Seller’s first argument nevertheless left for resolution his contention as to an abuse of process.

15 The jurisdiction of this Court to set aside a bankruptcy notice as an abuse of process was not put in issue: Re Sterling; Ex parte Esanda Ltd (1980) 44 FLR 125 at 129 per Lockhart J. In identifying some of the circumstances in which the power may be exercised, His Honour said:

This Court and the Federal Court of Bankruptcy before it, have set aside bankruptcy notices over many years on various grounds. Instances of the exercise of this power are where the notice is not in accordance with the terms of the judgment and is calculated to perplex the debtor; the notice is issued for the whole of a judgment debt, yet the judgment debtor has paid into court in part satisfaction of the debt; in truth no debt lies behind the judgment … and the sum of which payment is required by the terms of a notice has in fact been paid by the debtor …: [(1980) 44 FLR 125 at 129]

His Honour continued on to state:

I mentioned earlier some instances of the exercise of the power to set aside bankruptcy notices by this court and the Federal Court of Bankruptcy. They are not exhaustive of the occasions on which the power will be exercised: [(1980) 44 FLR 125 at 131]

Lockhart J again referred to the circumstances in which a bankruptcy notice may be set aside in Clyne v Deputy Commissioner of Taxation (NSW) (No 4) (1982) 66 FLR 301 at 307 where His Honour said:

As I observed in Re Sterling; Ex parte Esanda Ltd (1980) 44 FLR 125, the court’s power to set aside bankruptcy notices is not conferred specifically by any provision of the Act, although it is assumed (see, for example, s 41(6a), (6b) and (6c)). Courts exercising bankruptcy jurisdiction have set aside bankruptcy notices over many years and on various grounds. The circumstances in which notices may be set aside are not governed by rigid rules and do not fall into fixed categories. The power may be exercised if warranted on the facts of a particular case. The source of this power is s 30(1) of the Act. That sub-section has been liberally construed by the courts. The circumstances which may give rise to questions or problems in matters of bankruptcy are so multifarious that it is impossible to confer powers upon the court to deal with them other than in general terms. Such powers must not be given any narrow or mean construction. Non-compliance with the requirements of a bankruptcy notice is an act of bankruptcy on which almost every petition is based which comes before the court. A bankruptcy notice is the foundation of a bankruptcy and involves quasi penal consequences. The court must be able to supervise bankruptcy notices at all stages of their existence. If an alternative source of power were needed, however, it would be found in the court’s inherent jurisdiction. In my opinion fairness requires that the bankruptcy notice be set aside.

The Court has “a wide discretion to set aside a bankruptcy notice where it is satisfied that the interests of justice require it to do so”: Re Lentini; Ex parte Lentini v CSR Limited (1991) 29 FCR 363 at 372 per Neaves J. See also Rixon v Bryett [2001] FCA 963 at [26], 112 FCR 295 at 303 per Moore J.

16 One instance of an abuse of process is where the purpose in issuing a bankruptcy notice is to put pressure on a debtor to pay the debt rather than to genuinely invoke the Court’s jurisdiction in relation to insolvency: Brunninghausen v Glavanics [1998] FCA 230. In Killoran v Duncan [1999] FCA 1574, Gyles J observed:

[12] Whilst there is no debate about the jurisdiction of the Court to set aside a bankruptcy notice as an abuse of process where it can be concluded that it was simply to put pressure on the debtor rather than to genuinely invoke the Court’s jurisdiction, I am not satisfied that that is the position here. There is nothing to indicate that the respondent creditor does not genuinely intend to pursue the matter if there is default in complying with the notice. In my opinion, there is nothing special about abuse of process in this field, and, if a person wishes to resort to the jurisdiction of the Court for appropriate orders, then it will be an unusual case in which that will be prevented.

[13] There is no evidence here of any collateral purpose or of any undue pressure being applied. It is correct, I think, that the time to judge abuse of process is the time that the bankruptcy notice is issued and that subsequent events have relatively slight relevance. They may be relevant insofar as they throw light upon circumstances which might have been appreciated and foreseen at the time of the issue of the notice.

[14] If, contrary to my view, however, there were a prima facie case of abuse of process, the remedy is discretionary and, in my view, if circumstances following that time had altered significantly so that it would not be appropriate to set aside the notice, I think that the jurisdiction of the Court is wide enough to give effect to that. I have in mind here that whilst the immediate parties to the application are those with the most interest in the matter, the body of creditors generally also have an interest and I cannot be certain one way or the other about the position of solvency. It may be most unfortunate if a bankruptcy notice were set aside in circumstances where the debtor is in fact insolvent.

See also: Maxwell-Smith v S & E Hall Pty Ltd [2006] FCA 825, 233 ALR 81; Cavoli v Etl [2007] FCA 1191 at [17] per Heerey J; Slack v Bottoms English Solicitors [2002] FCA 1445 at [15] to [18] per Spender J; Davidova v Murphy [2009] FCA 601 at [88]. It is also an abuse of process for a judgment creditor to pursue bankruptcy proceedings “for the purpose of stifling litigation”: Bayne v Baillieu; Bayne v Riggall (1908) 6 CLR 382 at 396 per Griffith CJ.

17 In Rankine v Lord [2011] FCA 478 at [29] to [30], 121 ALD 258 at 262 Marshall J rejected a submission that litigants who claim that a bankruptcy notice has been issued for an improper purpose “bear a heavy onus”. His Honour continued on to state that a “court considering such an issue will examine that matter objectively having regard to the entire relevant factual matrix and if it forms the view that the issuing of the notice is an abuse of process it ought not feel timid about saying so”. But “more than mere assertion would be required to set aside [a] bankruptcy notice … upon the footing that it was an abuse of process”: Watts v Adelaide Bank Ltd [2009] FCA 420 at [18] per Buchanan J. See also: Davidova v Murphy [2009] FCA 601 at [91].

18 Many cases have arisen comparable to the present where the Deputy Commissioner of Taxation has sought to enforce by way of bankruptcy proceedings a failure to comply with a notice of assessment.

19 One case was Clyne v Deputy Commissioner of Taxation (NSW) (No 3) (1982) 82 ATC 4484. Orders were there sought, including an order setting aside a bankruptcy notice. Lockhart J introduced the case as “yet another round in the fight between Peter Leopold Clyne … and the Deputy Commissioner of Taxation”. In declining to set aside the bankruptcy notice, His Honour observed:

The applicant must comply with the requirements of the notice or commit an act of bankruptcy. To defer the operation of the notice would merely place another weapon in his hands to delay and defeat the respondent (according to the applicant, until about 1989 or 1990), who is a creditor in a substantial sum and entitled to obtain payment of the tax which is due and payable.

The proper time for the Court to consider whether its discretion should be exercised in favour of the respondent is upon the hearing of any petition to sequestrate his estate which the respondent, or any other creditor, may present. The Court will then have a more recent knowledge of the stage reached in the litigation between the parties in the Court of Appeal and Board of Review or any other court or tribunal then involved in the battle. The applicant’s financial position and the views of any other creditors can be ascertained.

In the meantime an act of bankruptcy may be committed and a petition for sequestration presented, so that if a sequestration order is made the rights of creditors will be better preserved.

…

Of course, the applicant may not become bankrupt. He may satisfy or secure his indebtedness to the respondent. He may succeed in the litigation before the Court of Appeal or the Board of Review and not be made bankrupt in the meantime. In balancing the conflicting interests of the applicant and the respondent it is preferable that no indulgence is granted to the applicant at this stage. The proper time to consider any adjournment of any relevant bankruptcy process or proceeding is upon the hearing of a bankruptcy petition, and not before: [82 ATC 4484 at 4492].

An appeal was dismissed: Clyne v Deputy Commissioner of Taxation (1982) 69 FLR 1. The matter then came before the High Court: Clyne v Deputy Commissioner of Taxation (1983) 48 ALR 545. The taxpayer had lodged security in the sum of $100 and that operated as an automatic stay of execution. Mason ACJ removed the stay: Clyne v Deputy Commissioner of Taxation (No 4) (1982) 43 ALR 342. In the course of so doing, His Honour noted:

I was informed that it is a somewhat unusual course for the Deputy Commissioner to commence proceedings for recovery in a court relying on a notice of assessment which is under challenge in proceedings under Pt V of the Assessment Act. It is to be hoped that this is so. The institution of proceedings for recovery on a notice of assessment which is challenged in proceedings under Pt V may operate oppressively and unfairly to a taxpayer. Fortunately, and this is conceded by Mr Priestley QC for the Deputy Commissioner, the courts in which recovery is sought have a jurisdiction to stay or adjourn recovery proceedings when the notice of assessment is under challenge in Pt V proceedings, insisting, if it be appropriate, on the taxpayer giving suitable security or a suitable undertaking to meet the exigencies of the situation.

In removing the stay, Mason ACJ concluded in respect to the appeal that the “prospects of success are at best slight”.

20 There is no “general principle of fairness, according to which a bankruptcy notice will be set aside if in some way the notice is unfair to the debtor”: Re Briggs; Ex parte Briggs v Deputy Commissioner of Taxation (WA) (1986) 12 FCR 310 at 312 per Toohey J.

An Abuse of Process – The Facts of The Present Case

21 The chronology of facts relevant to the resolution of the abuse of process argument is as follows:

| DATE | EVENT |

| 10 June 2009 | Mr Seller is served with assessments to income tax, goods and services tax and penalties by the Deputy Commissioner. |

| 3-6 August 2009 | Mr Seller raises his objections to the Assessments. |

| 17 December 2009 | The Statement of Claim is filed by the Deputy Commissioner in the Supreme Court (for approx. $6m). |

| 10 June 2010 | Mr Seller is served with the Statement of Claim filed by the Deputy Commissioner in the Supreme Court of NSW seeking judgment for the amounts assessed by the Deputy Commissioner. |

| July to December 2010 | Mr Seller liaises with the Deputy Commissioner in respect of the Assessments and the Supreme Court Proceedings. |

| 13 December 2010 | Mr Seller’s father passes away. |

| 20 December 2010 | Mr Seller’s father’s funeral is held. |

| 24 December 2010 | The Deputy Commissioner moves for and obtains the default judgment against Mr Seller in the Supreme Court Proceedings. The default judgment is entered for the Deputy Commissioner. |

| 14 February 2011 | Mr Seller presses the Deputy Commissioner for determination of the Objections serving a notice under s 14ZYA of the Taxation Administration Act 1953 and, by letter, asks for a stay of enforcement of the Judgment. |

| 4 March 2011 | The Deputy Commissioner requests and obtains issue of the Bankruptcy Notice from the Official Receiver. |

| 15 April 2011 | Objection decisions made by the Deputy Commissioner on GST Assessments and Income Tax Assessments. The Deputy Commissioner serves Mr Seller with his notice that the Objections are disallowed. |

| 3 May 2011 | Mr Seller is served with the Bankruptcy Notice. |

| 17 May 2011 | Mr Seller files proceedings pursuant to Part IVC of the Taxation Administration Act in the Federal Court appealing against the Deputy Commissioner’s disallowance of the Objections. |

| 24 May 2011 | The present proceeding seeking to have the Bankruptcy Notice set aside commences. |

| 14 June 2011 | The Notice of Motion to stay the Judgment is filed by Mr Seller. |

22 This chronology of events, it was contended on behalf of Mr Seller, was to be considered (inter alia) against the background of the relevant policy of the Australian Taxation Office, namely Chapter 28 of the “ATO Receivables Policy” entitled “Recovering Disputed Debts”. In part that policy contains the following provisions:

Where 50/50 arrangement not accepted

28. Should the tax debtor choose not to enter into a 50/50 arrangement, collection action is unlikely to be commenced prior to the determination of the objection unless the circumstances of the case indicate an unacceptable level of risk.

29. Similarly, at review or appeals stage, collection action is unlikely to be commenced prior to the decision of the AAT or Court, unless the circumstances of the case indicate an unacceptable level of risk.

30. It should be noted, however, that the fact that the Commissioner has not instigated collection action for whatever reason while an objection, Tribunal review or appeal remains unresolved does not in itself amount to an agreement by the Commissioner to defer recovery of the disputed debt under section 255-5 of the TAA.

31. The Commissioner will only agree to a deferral of recovery action where:

• the tax debtor has entered into a 50/50 arrangement

• the Commissioner considers that a genuine dispute exists in regard to the assessability of an amount, or

• the Commissioner is pursuing arguments which are inconsistent with a previous Public or Private Ruling/Binding Oral Advice, or going against the weight of precedent cases (that is, the Commissioner is challenging the previously accepted position).

Such an agreement will usually be expressed in writing.

32. Where a 50/50 arrangement has not been accepted, GIC will accrue at the statutory rate on any of the disputed debt that remains unpaid after its due date.

Submissions proceeded upon the basis that Mr Seller had not chosen to enter into a “50/50 arrangement”.

23 Such evidence as there was as to consideration being given to the application of this policy or the consideration given to whether a bankruptcy notice should issue was within a limited compass. A Notice to Produce had been given to the Respondent and documents were produced at the hearing. The terms of the Notice to Produce, however, were unknown. But documents produced were for the period from February to May 2011 and entitled “Case Comments Report”. The “Report” for 3 February 2011 stated in part as follows:

Approval required for a Bankruptcy Notice:

On 24 December 2010 default judgment has been obtained in Supreme Court of NSW for the amount of $6,790,121.53 (IT $6,270,490.39, CAC $518,828.14 and $803 court costs).

I now recommend that a Bankruptcy notice be issued to Mr Ross Seller based on the following:

• The disputed debt is a significant amount and will continue to escalate while his level of compliance will deteriorate;

• The taxpayer did not wish to enter into a 50/50 arrangement;

• Section 260-5 of Schedule 1 to the TAA were issued to banks as well as companies that the taxpayer is a director of. The Commissioner was only able to receive an amount of $1,226.26 from CBA as most of the bank accounts are in joint names or in the name of his companies;

• There is also a concern that the taxpayer is limiting his liability to pay by transferring assets in the name of his partner or his companies. The assets that the debtor has transferred my [sic] be recoverable by the bankruptcy trustee; and

• Bankruptcy, will enable the trustee to conduct a public examination into the affairs of the taxpayer.

• 1. final judgment(s) / final order(s) $6790121.53

• 2. legal costs $803 ($749 filing fee & $54 service fee) - included in final order

• 3. judgment interest $78,123.64

• 4. sub total $6,868,245.17

• 5. payments/credits

• 6. total. $6,868,245.17

What other “Reports” stated is also not known.

24 At the outset of his submissions as to an abuse of process, Counsel on behalf of Mr Seller accepted that it was open to the Deputy Commissioner to commence proceedings in the Supreme Court as a step in seeking to enforce the assessment that had been issued. He also accepted that the mere fact that review had been sought of the assessment was not in itself a reason to conclude that the subsequent issue of a bankruptcy notice constituted an abuse of process. Indeed, in respect to those cases where review is sought before the Administrative Appeals Tribunal, s 14ZZM of the Taxation Administration Act 1953 (Cth) provides as follows:

Pending review not to affect implementation of taxation decisions

The fact that a review is pending in relation to a taxation decision does not in the meantime interfere with, or affect, the decision and any tax, additional tax or other amount may be recovered as if no review were pending.

Where an appeal has been brought in this Court, similar provision is made in s 14ZZR.

25 To make out an abuse of process, Counsel for Mr Seller accepted that he must establish more than the mere obtaining of a judgment; the issue of a bankruptcy notice and the existence of a proceeding in this Court challenging the decision disallowing his objections.

26 To lay the foundations for his abuse of process argument, repeated emphasis was placed upon:

the severe impact that a bankruptcy notice may have upon a debtor.

Although Counsel frequently elided the impact that the making of a sequestration order may have, as opposed to the impact that a bankruptcy notice may have, the severe consequences that follow from a failure to comply with a bankruptcy notice may readily be accepted. Those consequences may not be confined to those set forth in the Bankruptcy Act itself; they may also prejudice (for example) credit facilities that a debtor may have: cf. Conway v Jackson [2001] FCA 230 at [19], 107 FCR 201 at 207 per Moore, Mathews and Mansfield JJ. The fact, however, remains that “the commission of an act of bankruptcy is ... of a different order of gravity from the change of status brought about by the making of a sequestration order”: Byron v Southern Star Group Pty Ltd (1997) 73 FCR 264 at 270 per Lehane J.

27 In addition to reliance placed upon the impact on Mr Seller of a failure to set aside the Bankruptcy Notice, Counsel further submitted that an “abuse of process” – or perhaps an “abuse of power” – should be inferred from the following matters, namely:

non-compliance with paragraphs [28] and [29] of the “ATO Receivables Policy”;

a failure to consider the “ATO Receivables Policy” when approval was sought to have a bankruptcy notice issued;

a failure to consider the impact of a bankruptcy notice upon Mr Seller when approval was sought to have a bankruptcy notice issued; and

the delay that had occurred between the making of objections to the assessments and the resolution of those objections, and action being taken only when the Deputy Commissioner was “pressed” by Mr Seller’s legal representatives to make a decision.

The “abuse of process” in taking the course that was pursued by the Deputy Commissioner is said to be further supported by the observations of Mason ACJ in Clyne (No 4) (1982) 43 ALR 342.

28 From such limited evidence as was available, it is not considered that there was any failure to take into account the policy of the Australian Taxation Office to recover debts where a debtor had chosen not to enter into a “50/50 arrangement”. Nor is it open to conclude that the personal impact of the issue of a bankruptcy notice upon Mr Seller was not taken into account.

29 It is not considered that Mr Seller has established any abuse of process on the part of the Deputy Commissioner. No inference should be drawn that the Deputy Commissioner was doing anything other than bona fide invoking the bankruptcy regime set forth in the Bankruptcy Act. No inference should be drawn that the Deputy Commissioner was only seeking to invoke that regime to exert pressure upon Mr Seller to satisfy the monies said to be due and payable under the assessment. Nor should any inference be drawn that the Deputy Commissioner was otherwise abusing the power vested in him to recover monies said to be due and payable. Even if it be accepted that a failure to comply with paragraphs [28] and [29] of the “ATO Receivables Policy” goes some way towards establishing an abuse of process, such consideration as was given to the particular circumstances of Mr Seller in the “Case Comments Report” for 3 February 2011 exposes to a limited extent the basis upon which approval was sought for the issue of a bankruptcy notice. In the absence of further evidence, there is no basis for concluding that proper consideration was not given to the “ATO Receivables Policy” and the particular circumstances relevant to Mr Seller.

30 The drawing of any such inference is made even more difficult when, as is submitted on behalf of the Deputy Commissioner:

the solicitors for Mr Seller wrote on 14 February 2011 seeking a “stay of enforcement of your judgment” and where that request was denied on 17 February 2011;

and it was not until thereafter that:

applications were filed in this Court challenging the objection decisions; and

an application was made to stay the Supreme Court judgment.

Mr Seller was plainly put on notice that his request for a stay of enforcement action had been refused. The letter dated 17 February 2011 expressly “reserve[d] all rights to commence enforcement of the Judgment after 25 February 2011 without further notice”. It was only thereafter that the Bankruptcy Notice was served and served prior to the applications filed in this Court and the Supreme Court. Presumably the application made in June 2011 for a stay of the proceedings in the Supreme Court was brought in full knowledge of the fact that the power to grant such a stay is a power which “must be exercised sparingly”: Snow v Deputy Commissioner of Taxation (1987) 14 FCR 119 at 135 per French J (as His Honour then was). The legislative scheme, His Honour there noted, “reflects a clear policy favouring the revenue against the taxpayer… [T]he Commissioner is placed by the legislature in a position of special advantage”. See also: Federal Commissioner of Taxation v Mackey (1982) 64 FLR 432; Cywinski v Deputy Commissioner of Taxation [1990] VR 193.

31 Given the response communicated in the 17 February 2011 letter it is surprising that an application to stay the Supreme Court judgment was only made after the Bankruptcy Notice had been issued and served. Section 40(1) of the Bankruptcy Act, it will be recalled, sets forth the circumstances in which an act of bankruptcy is committed and s 40(1)(g) refers to those circumstances in which a judgment creditor has obtained “a final judgment or final order, being a judgment or order the execution of which has not been stayed …”. Whatever prospects a judgment debtor may have in seeking a stay of a judgment obtained by the Deputy Commissioner in reliance upon an assessment may be left to one side; that which is presently of importance is that the Deputy Commissioner did not seek to issue a bankruptcy notice without putting Mr Seller on notice that he reserved his “rights to commence enforcement”. The provision of such advance notice is not the hallmark of a creditor seeking to engage in an abuse of process. Different considerations may have applied had a bankruptcy notice been sought after an application had been made to stay the judgment or order relied upon and prior to that application being heard and determined.

32 It must, however, be noted that the Deputy Commissioner exercises considerable power. He occupies a position very different to that of any other creditor by reason of the extensive powers vested in him by the Legislature: W Gumley and K Wyatt, ‘Are the Commissioner’s Debt Recovery Powers Excessive?’ (1996) 25 Australian Tax Review 186. Assessments, for example, may be issued and are rendered conclusive (Income Tax Assessment Act 1936 (Cth), s 177) thereby facilitating applications for summary judgment. See also: F J Bloemen Pty Ltd v Federal Commissioner of Taxation (1981) 147 CLR 360; Deputy Commissioner of Taxation v Richard Walter Pty Ltd (1995) 183 CLR 168. Given the extensive powers that may be exercised, it is to be expected that this Court will carefully scrutinise the conduct of the Deputy Commissioner where he does seek to issue a bankruptcy notice. Subject to the supervisory jurisdiction of this Court to ensure that there has been no abuse of process in issuing a bankruptcy notice, the Deputy Commissioner may nevertheless do so – just as any other creditor may do so.

33 Notwithstanding that degree of scrutiny, no finding should be made in the present proceeding that the Deputy Commissioner issued the Bankruptcy Notice for the purpose of pressuring Mr Seller into paying the amount claimed rather than issuing it for the purpose of genuinely invoking this Court’s jurisdiction in respect to bankruptcy. No finding as to an abuse of process – or an abuse of power – is open on the facts presented.

34 Different considerations may well apply should the point be reached where a sequestration order is sought. It is at that stage when more detailed consideration may have to be given (for example) to the consequences of Mr Seller being deprived of an entitlement to pursue his objections to the assessments and the prospect of a trustee not pursuing those proceedings: Cummings v Claremont Petroleum NL (1996) 185 CLR 124; McCallum v Commissioner of Taxation (1997) 75 FCR 458. Although that consideration more immediately arises when a sequestration order may be sought, it nevertheless remains of some relevance to an assessment as to there being an existing abuse of process. Its relevance in the present proceeding, it is concluded, is marginal.

35 When prior reliance upon the form of the Bankruptcy Notice was abandoned, an abuse of process remained the only basis upon which the application to have the Bankruptcy Notice set aside was advanced. That application so advanced is rejected.

An Extension of Time — Section 41(6a)

36 In the event that the Bankruptcy Notice was not set aside, Mr Seller sought an extension of time within which to comply.

37 The power to extend time is to be found within s 41 of the Bankruptcy Act. Sub-sections (6A) and (6C) of s 41 provide as follows:

(6A) Where, before the expiration of the time fixed for compliance with the requirements of a bankruptcy notice:

(a) proceedings to set aside a judgment or order in respect of which the bankruptcy notice was issued have been instituted by the debtor; or

(b) an application has been made to the Court to set aside the bankruptcy notice;

the Court may, subject to subsection (6C), extend the time for compliance with the bankruptcy notice.

(6C) Where:

(a) a debtor applies to the Court for an extension of the time for complying with a bankruptcy notice on the ground that proceedings to set aside a judgment or order in respect of which the bankruptcy notice was issued have been instituted by the debtor; and

(b) the Court is of the opinion that the proceedings to set aside the judgment or order:

(i) have not been instituted bona fide ; or

(ii) are not being prosecuted with due diligence;

the Court shall not extend the time for compliance with the bankruptcy notice.

38 Section 41(6A), it will be noticed, sets forth in paragraphs (a) and (b) the conditions precedent that must be satisfied before the discretion is thereafter called upon to be exercised. An applicant who seeks to invoke s 41(6A) must bring himself within either s 41(6A)(a) or (b) before any question arises as to the manner in which the discretion may be exercised. Other than pursuant to s 41(6A), there is no statutory grant of power and no general inherent power in the Court to extend time for compliance with a bankruptcy notice: James v Abrahams (1981) 51 FLR 16 at 22 per Deane and Lockhart JJ. Section 41(6A) is thus the “sole source of power in the court to extend the time for compliance with the requirements of a bankruptcy notice”: Re Dalco; Ex parte Dalco v Deputy Commissioner of Taxation (1986) 67 ALR 605 at 613 per Neaves J.

39 The “power to extend time for compliance is in aid of the power to set aside the notice itself”: Re Sterling (1980) 44 FLR 125 at 130; Byron (1997) 73 FCR 264 at 268. And, “[o]nce the application to set aside the judgment or the bankruptcy notice has been finally determined … there is no aid which the power to extend time for compliance can give to the determined application”: Shephard v Chiquita Brands (South Pacific) Ltd [2004] FCAFC 76 at [40] per Hill and Marshall JJ.

40 Section 41(6A)(a) is not to be given a narrow meaning and includes an appeal from the judgment or order in respect of which the bankruptcy notice was issued where that appeal does in reality seek to have that judgment or order set aside. In Conway v Jackson, Moore, Mathews and Mansfield JJ observed:

[18] There is nothing in the language or the context of s41(6A)(a) which indicates that a narrow meaning should be given to the expression “proceedings to set aside judgment”. It contemplates circumstances where the judgment debtor is seeking to set aside the judgment. In certain circumstances, that may be done by application to the Court or the judge who entered the judgment. The clearest example of that arises where judgment has been entered in default of appearance or for some other procedural failure on the part of the judgment debtor. Commonly, in such cases, there has been no adjudication on the merits of the claim or on some part of the merits of the claim. But the language of s41(6A)(a) does not indicate any intention to limit its application to such circumstances. It would have been easy for such an intention to have been expressed. …

[19] We also consider that the purpose of s41(6A) would more usefully be served by adopting the construction of the relevant words which includes an appeal from the judgment on which the bankruptcy notice if founded, where that appeal in fact seeks to set aside the judgment. The commission of an act of bankruptcy has serious consequences. Apart from the obvious consequence of exposure to the making of a sequestration order, an act of bankruptcy itself commonly constitutes an act of default under security instruments and so exposes the person who has committed the act of bankruptcy to the crystallisation and calling up of other debts. It is also an event which, at least anecdotally, causes those providing unsecured credit to the judgment debtor, such as trade creditors in the case of a business operated by the judgment debtor, to alter or withdraw the terms upon which credit is or continues to be provided. S41(6A)(a) would appear to recognise the consequences of the commission of an act of bankruptcy, and to empower the Court in appropriate circumstances to protect a judgment debtor from those consequences. That policy would not be served by restricting the ability to exercise that power so as to exclude its exercise in all cases where the judgment debtor has appealed from the judgment at first instance and seeks to set it aside. …

In so concluding their Honours expressly disagreed with a contrary view expressed in some decisions (e.g., Re Lentini; Ex parte Lentini v CSR Limited (1991) 29 FCR 363 at 366 to 367 per Neaves J) that “the language of s 41(6A)(a) is apt only to encompass an application to set aside a judgment or order where there has been a failure to follow the rules of procedure or where there is shown to be some defect or irregularity or some other circumstance which renders it desirable that the debtor should be given an opportunity to have the issue further litigated, and so as to exclude proceedings by way of appeal which may result in the judgment being set aside”: Conway v Jackson [2001] FCA 230 at [29], 107 FCR 201 at 210.

41 An application for special leave to appeal to the High Court from a decision founding a bankruptcy notice also constitutes a proceeding to set aside a judgment: O’Loughlin v Glenmont Investments Pty Ltd [2001] FCA 925 at [4], 191 ALR 336 at 337 per Mansfield J.

42 Where either s 41(6A)(a) or (b) has been satisfied there is power to extend time for compliance and the discretion to do so is said to be “at large”: Re Taylor; Ex parte Deputy Commissioner of Taxation (1983) 74 FLR 377 at 379 per Sheppard J; Byron (1997) 73 FCR 264 at 270.

43 In Byron v Southern Star Group Pty Ltd, Lehane J considered what he referred to as “some difference of opinion in the cases as to the principles which will guide the court in exercising its discretion to extend time”: (1997) 73 FCR 264 at 268. His Honour thereafter referred to the decision of Kiefel J in Re Baker; Ex parte Baker v Staples (Unreported, Federal Court of Australia, Kiefel J, 4 September 1995) and to the decision of Sheppard J in Re Geard; Ex parte Reid (Unreported, Federal Court of Australia, Sheppard J, 11 February 1994). Lehane J then concluded:

Although I was referred, in argument, to both Baker and Geard, little attention was given to the difference of approach which, in my view, the passages which I have quoted clearly display. Because there is such a difference, I must consider for myself the approach appropriately to be adopted in a case such as this. In my view the considerations to which Sheppard J refers indicate that the principles to be applied where the question is whether a petition should be adjourned or dismissed are not necessarily those which should guide the exercise of the discretion to set aside, or extend time for compliance with, a bankruptcy notice. The commission of an act of bankruptcy is, undoubtedly, a serious matter; it is, however, of a different order of gravity from the change of status brought about by the making of a sequestration order; and there is also to be taken into account the interest of both the judgment creditor and other creditors of the judgment debtor in ensuring that, if ultimately a sequestration order is made, the relevant act of bankruptcy occurs earlier rather than later: [(1997) 73 FCR 264 at 270.]

This decision was distinguished by Edmonds J in Coshott v Barry [2009] FCA 1521, 113 ALD 358. It is, however, unnecessary to pursue any difference in the principles to be applied any further.

The Refusal of an Extension of Time

44 In opposing any extension of time for compliance, Senior Counsel on behalf of the Deputy Commissioner contended that s 41(6A) had “no scope to operate in the current context” because for the purposes of s 41(6A):

the judgment “… in respect of which the bankruptcy notice was issued” was the judgment of the Supreme Court and no application had been made to “set aside” that judgment; and

the Part IVC proceeding commenced in this Court does not constitute a proceeding to “set aside” the judgment of the Supreme Court.

The Deputy Commissioner further contended that:

once a decision has been made not to set aside a bankruptcy notice, the power to extend time is “spent”.

All three submissions are accepted.

45 No application has been made to “set aside” the decision of the Supreme Court. Given the conclusiveness of the assessments upon which the judgment was obtained, it is perhaps not surprising that no such application has been made. The conclusiveness of the assessments, it is respectfully considered, places those administering the taxation legislation in a position of unique power – especially in the restricted context of s 41(6A)(a). The conclusiveness of an assessment makes recourse by any judgment debtor to s 41(6A)(a) virtually an exercise in futility. Judgment is entered because an assessment is conclusive; any application to have that judgment “set aside” would in most cases meet with failure by reason of the same conclusiveness given to the assessment. To in effect deny a debtor who is the subject of a judgment obtained by a Deputy Commissioner recourse to s 41(6A)(a) is to deny him recourse to a valuable safeguard available to all other judgment debtors. This imbalance of power, and the serious consequences that committing an act of bankruptcy has upon a judgment debtor, needs to be addressed by the legislature. A submission that a judgment debtor may apply to the Supreme Court to have a judgment “set aside” by reason of “extreme financial hardship” or perhaps on the basis that the “assessment” is not an assessment which would attract the cloak of conclusiveness extended by s 177 of the Income Tax Assessment Act 1936 (Cth) provides little real comfort to the overwhelming number of judgment debtors who confront the Deputy Commissioner as a creditor. Without detracting from the conclusiveness of an assessment, consideration could be given by the legislature to separately addressing the relatively unique position a judgment debtor faces when seeking an extension of time to comply with a bankruptcy notice issued by the Deputy Commissioner.

46 An application to “stay” a judgment is not an application to have that judgment “set aside”. The submission advanced on behalf of Mr Seller that the Part IVC proceeding in this Court constitutes a proceeding to “set aside” the judgment of the Supreme Court is rejected. No authority was cited to support such a proposition. Mr Seller can thus not bring himself within s 41(6A)(a).

47 And, once the application to set aside the Bankruptcy Notice has been resolved and rejected, he cannot bring himself within s 41(6A)(b): Re Sterling (1980) 44 FLR 125 at 131.

48 No question for the exercise of any discretion conferred by s 41(6A) to extend the time for compliance thus arises.

49 An alternative source of power to extend time, it was contended on behalf of Mr Seller, was to be found in s 32 of the Federal Court of Australia Act 1976 (Cth). Again, no authority was provided in support of such a proposition. It is rejected. The sole source of power to extend time for compliance with a bankruptcy notice, it is concluded, is to be found within s 41(6A) of the Bankruptcy Act. That conclusion is only further supported by the terms of s 33(1)(c) of the Bankruptcy Act.

50 The acceptance of the Deputy Commissioner’s present submissions, however, may only serve to underline the importance of separately considering – if the need arises – whether a sequestration order should be later made.

Conclusions

51 The Bankruptcy Notice is not to be set aside. No abuse of process has been made out.

52 Mr Seller cannot bring himself within either s 41(6A)(a) or (b). The Court has no power to extend time for compliance with the Bankruptcy Notice and no question arises as to the manner in which any discretion to extend time may have been exercised. Had any question as to discretion arisen, it is unlikely on the limited factual basis presently advanced on behalf of Mr Seller than any discretion would in any event have been exercised in his favour.

53 There is no reason why the Deputy Commissioner should not have his costs, including those thrown away by reason of the abandonment by Mr Seller of any reliance upon an argument that the Bankruptcy Notice as served did not annex a copy of the judgment.

ORDERS

The Orders of the Court are:

1. The Application as filed on 24 May 2011 is dismissed.

2. The Applicant is to pay the costs of the Respondent.

| I certify that the preceding fifty-three (53) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Flick. |

Associate: