FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Letten (No 12)

[2011] FCA 500

|

|

|

|

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | |

|

AND: |

First Defendant (and others according to the attached schedule) |

|

DATE OF ORDER: |

|

|

WHERE MADE: |

NOTE: For the purpose of this order:

(a) “Receivers” has the meaning ascribed to it in the Orders of Justice Gordon made in this proceeding on 25 February 2010, 4 March 2010 and 30 July 2010;

(b) “YVG Properties” has the meaning ascribed to it in the Orders of Justice Gordon made in this proceeding on 4 June 2010.

THE COURT ORDERS THAT:

1. The Receivers are justified in settling the contracts of sale entered into by the Receivers on 23 December 2010 in relation to the YVG Properties and the Glenbelle Retreat & Spa, comprising exhibits DJT-108, DJT-109, DJT-110, DJT-111 and DJT-112 (as varied by the letter agreements exhibited at DJT-113, DJT-114 and DJT-115) to the Twenty Fifth affidavit of Damian John Templeton sworn 21 April 2011.

2. Until further order, Confidential Exhibit DJT-103 and Exhibit DJT-112A to the Twenty Fifth Affidavit of Damian John Templeton sworn 21 April 2011 be placed in a sealed envelope and marked “Confidential: No access without leave of a judge of the Court”.

3. Until further order, pursuant to s 50 of the Federal Court of Australia Act 1976 (Cth), there be no publication of Confidential Exhibit DJT-103 or Exhibit DJT-112A to the Twenty Fifth Affidavit of Damian John Templeton sworn 21 April 2011 other than to ASIC and its legal representatives, the legal representatives of the defendants, judges of the Court, judges’ associates and executive assistants and the Receivers and their legal representatives and staff.

4. The proceedings otherwise be adjourned to a date to be fixed.

5. Costs reserved.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules. The text of entered orders can be located using Federal Law Search on the Court’s website.

|

VICTORIA DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

VID 95 of 2010 |

|

BETWEEN: |

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff |

|

AND: |

MARK RONALD LETTEN First Defendant (and others according to the attached schedule) |

|

JUDGE: |

GORDON J |

|

DATE: |

17 MAY 2011 |

|

PLACE: |

MELBOURNE |

REASONS FOR JUDGMENT

1 On 25 February 2010, the schemes numbered 1, 4 to 9 and 13 to 16 in Annexure A to these reasons for decision were wound up pursuant to s 601EE(1) of the Corporations Act 2001 (Cth) (the Corporations Act). Also on 25 February 2010, Mr Damian Templeton and Mr Phillip Hennessy of KPMG (the Receivers) were appointed as joint and several receivers and managers of certain property of each of the second to sixteenth and eighteenth to forty-fifth defendants (the Corporate Defendants) and as joint and several receivers and managers of identified property of each of the schemes listed in Annexure A (the Schemes) except for the scheme numbered 12: Australian Securities and Investments Commission v Letten [2010] FCA 140 (the 25 February Orders).

2 The 25 February Orders required the Receivers to file and serve a report in respect of, inter alia, the nature and identity of the property of each Scheme, any claims by third parties in relation to the property of the Scheme, the identities of investors and the nature of their investment (the Disclosure Reports).

3 On 13 April 2010, the Receivers filed Disclosure Reports in relation to each Scheme listed in Annexure A except for schemes numbered 6, 15 and 16. The Disclosure Reports for schemes numbered 6, 15 and 16 were filed on 28 April 2010.

4 This judgment concerns Schemes 15 (the Yarra Valley Golf Joint Venture Scheme) and 16 (the Glenbelle Project Scheme).

5 On 25 February 2010, the Court ordered that:

1. Pursuant to s 1323(1)(h)(ii) of the Act the Receivers be appointed to the property of, inter alia, the twenty-first to forty-fifth defendants (the YVG Parties) and the twenty-ninth and thirty-sixth defendants (the Glenbelle Parties), other than property that constitutes property of a Scheme as defined in Annexure A to the Order;

2. the Yarra Valley Golf Joint Venture Scheme and the Glenbelle Project Scheme (being Schemes identified in Annexure A) be wound up pursuant to s 60IEE(1) of the Act; and

3. the Receivers be appointed as receivers and managers of the Property of, inter alia, the Yarra Valley Golf Joint Venture Scheme and the Glenbelle Project Scheme.

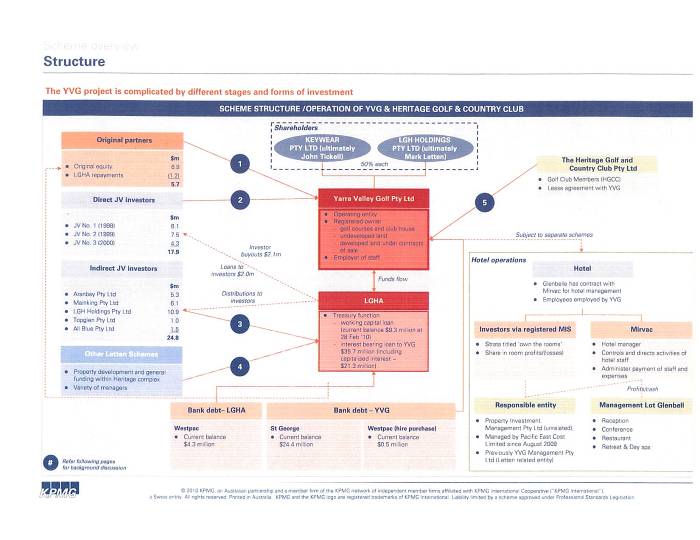

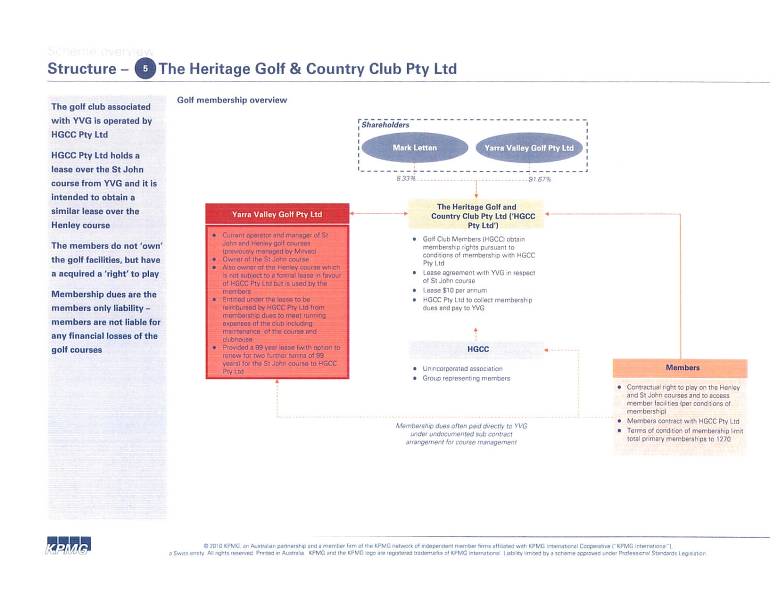

6 In his disclosure report in relation to the Yarra Valley Golf Joint Venture Scheme, Mr Templeton (one of the Receivers) provided a diagrammatic and descriptive overview of the scheme structure and the relationship with key stakeholders (the Yarra Valley Overview). A copy of the Yarra Valley Overview is Annexure B to these reasons for decision.

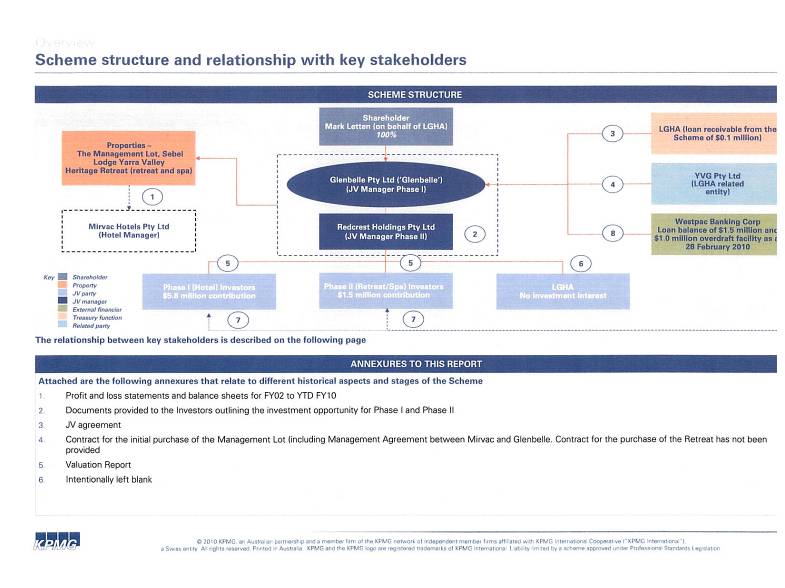

7 In his disclosure report in relation to the Glenbelle Project, Mr Templeton provided a diagrammatic and descriptive overview of the scheme structure and the relationship with key stakeholders (the Glenbelle Overview). A copy of the Glenbelle Overview is Annexure C to these reasons for decision.

8 On 4 June 2010, the Receivers were authorised to sell the YVG Properties and Glenbelle Properties, save that the Receivers were not authorised to enter into any contract of sale in respect of the YVG Properties and Glenbelle Properties which was not conditional upon approval of the Court. In the 4 June Orders, the “YVG Parties” were defined as the twenty-first to forty-fifth defendants and the “YVG Properties” were defined as:

(a) the land, buildings and fixtures, the legal title to which is held by any of the YVG Parties, located at The Heritage Golf and Country Club, Corner of Hughes and Yarraview Roads, Chirnside Park, Victoria (the Heritage Complex) including:

(i) the properties in respect of which there are existing contracts of sale, including:

(A) Lots 611 to 618 Botanica town houses;

(B) Lots 6 and 7 of the Henley Land;

(C) Lot 8 of the Henley Land,

(collectively, the Pre-sold Properties); and

(ii) all other developed and undeveloped land located at the Heritage Complex.

(b) the golf operations business located at the Heritage Complex including the YVG Parties’ interest in and rights in respect of:

(i) the Henley Golf Course;

(ii) the St John Golf Course;

(iii) the club house;

(iv) the members’ bar;

(v) the pro shop;

(vi) all maintenance sheds;

(vii) all ancillary property and plant and equipment used in the golf operations;

(viii) goodwill; and

(ix) debtors;

(c) all other rights, plant and equipment, vehicles and any other thing owned by the YVG Parties; and

(d) all shares held by Yarra Valley Golf Pty Ltd (receivers and managers appointed) in Heritage Golf and Country Club Pty Ltd,

(each a YVG Property and collectively the YVG Properties).

9 In the same orders, the “Glenbelle Parties” were defined as twenty-ninth and thirty-sixth defendants and the “Glenbelle Properties” were defined as:

(a) the land, buildings and fixtures, in respect of the Management Lot of The Sebel Lodge Yarra Valley located within the Heritage Complex;

(b) the land, building and fixtures, in respect of the Heritage Retreat recreation facility and day spa located within the Heritage Complex;

(c) The Sebel Lodge Yarra Valley business including the Glenbelle Parties’ interest in:

(i) the hotel operations;

(ii) the food and beverage operations;

(iii) the conference operations;

(iv) the associated goodwill;

(v) the debtors; and

(vi) all ancillary property and plant and equipment used in The Sebel Lodge Yarra Valley operations;

(d) the Heritage Retreat business including the Glenbelle Parties’ interest in;

(i) the spa operations;

(ii) the recreation facility operations;

(iii) the food and beverage operations;

(iv) the associated goodwill;

(v) the debtors;

(vi) all ancillary property and plant and equipment used in the Heritage Retreat operations;

(e) all other rights, plant and equipment, vehicles and any other thing owned by the Glenbelle Parties.

10 On 23 December 2010 the Receivers entered into various agreements for the sale of the YVG Properties and the retreat and day spa component of the Glenbelle Properties (the Glenbelle Retreat & Spa).

11 This application concerns the sale of the majority of the assets over which the Receivers have been appointed, comprising the land and businesses operated in the Yarra Valley where there is situated, generally speaking, golf courses, a substantial Clubhouse, a Hotel, a spa and pool complex, tennis courts and associated businesses that go to the operation of those assets and, in particular:

1. The St John Golf Course – an 18 hole championship course upon which there is a substantial club house;

2. The Henley Golf Course – an 18 hole championship course and further land surrounding it to be subdivided for sale;

3. The Retreat and Spa land – land upon which a spa and pool complex has been constructed, together with two tennis courts;

4. The business that operates the golf club known as the Heritage Golf and Country Club, the two golf courses, the clubhouse, a landscaping business and a property development business; and

5. The business that operated the Retreat and Spa.

The assets listed in paragraphs (1) to (5) have now been sold and are the subject of the current application.

12 On 27 April 2011, the Receivers filed an interlocutory process which, pursuant to ss 1323(5) and 601EE of the Corporations Act and paragraph 29 of the 25 February Orders, sought approval of the Receivers to enter into the following contracts of sale in relation to these assets:

1. The YVG Business Sale Agreement, whereby the Receivers, on behalf of Yarra Valley Golf Pty Ltd (Receivers and Managers Appointed) (YVG), entered into a business sale agreement for the sale of the assets of the business carried on by YVG in owning or operating the businesses conducted by and on behalf of the Heritage Golf and Country Club, two golf courses, the clubhouse, a landscaping business and YVG Development, a property development business conducted by YVG;

2. The Glenbelle Business Sale Agreement, whereby the Receivers, on behalf of Glenbelle Pty Ltd (Receivers and Managers Appointed) (Glenbelle), entered into a business sale agreement for the sale of the assets of the business carried on by Glenbelle in owning and operating the business conducted on the Management Lot and the Retreat and Day Spa businesses;

3. The St. John Golf Course land sale contract, whereby the Receivers, on behalf of YVG, entered into a contract for the sale of the land comprising the St. John Golf Course. Clause 25.6 of the Special Conditions makes completion of this sale contract conditional upon the completion of the YVG Business Sale Agreement, the YVG Property Agreement (Henley) sale contract, the Glenbelle Business Sale Agreement and the Retreat and Spa land sale contract;

4. The YVG Property Agreement (Henley) land sale contract, whereby the Receivers, on behalf of YVG, entered into a contract for the sale of the land comprising the Henley Golf Course. Clause 25.7 conditions the completion of this contract in the same way as referred to in relation to the St. John Golf Course land sale contract;

5. The Retreat and Spa of the Sebel Heritage Yarra Valley land sale contract, whereby the Receivers, on behalf of Glenbelle, entered into a land sale agreement comprising certain land upon which the Retreat and Spa business was operated. Clauses 21.5 and 21.6 make completion of this contract conditional upon completion of the other contracts the subject of this application.

(collectively, the Sale Contracts).

The interlocutory process was supported by affidavits sworn by Damian John Templeton on 21 April 2011 (the Twenty Fifth Templeton Affidavit), 12 May 2011 (the Twenty Sixth Templeton Affidavit) and 13 May 2011 (the Twenty Seventh Templeton Affidavit).

13 On 13 May, the interlocutory process came on for hearing. In addition to Counsel for the Receivers, a number of other parties appeared by Counsel including the Australian Securities and Investments Commission, the first defendant (Mr Letten) and the following interested parties (either by their legal representative or in person):

1. Westpac Banking Corporation (the secured lender) (Westpac);

2. Australian and Pacific Investment Corporation Pty Ltd and William Boerkamp;

3. Dr Tickell and Keywear Pty Ltd (Keywear) (the Tickell Interests);

4. Bridgehead Properties Pty Ltd (ACN 078 214 490) (Bridgehead), a creditor of Yarra Valley Golf Pty Ltd.

14 The only parties who opposed the orders sought by the Receivers were Bridgehead and the Tickell Interests. Bridgehead filed a number of affidavits in opposition to the claim and Mr Woodward SC made oral submissions in relation to Bridgehead’s opposition to the application. Dr Tickell (a guarantor) appeared in person and was given leave to appear on behalf of Keywear, another guarantor. Dr Tickell made written and oral submissions.

15 Their principal complaint was that a parcel of land included in the Sale Contracts (referred to during the submissions as “the undeveloped land)” was not marketed. It will be necessary to consider the substance of this argument in further detail later in these reasons for decision.

APPLICABLE PRINCIPLES

16 The applicable principles are summarised in ASIC v Letten (No 11) [2011] FCA 499 at [13] to [18] as follows:

The power to authorise the sale … is derived from various sources – s 601EE of the Corporations Act to the extent that the Properties are property of the Scheme and otherwise the Court’s inherent power to authorise the sale consequent upon the appointment of the Receivers by the Court: Letten (No 7) at [269] to [271]; Australian Securities and Investments Commission v Letten (No. 8) [2010] FCA 1458 at [10]; AIDC v Co-operative Farmers and Graziers Direct Meat Supply Ltd. [1978] VR 633 at 643.

The Receivers submitted (and I accept) that although the Court has a broad unfettered discretion (Letten (No 8) at [11] and AIDC at 647-8), the Court may take into account the interests of all creditors and other stakeholders. Letten (No 8) at [11].

As was stated in Letten (No 8) at [11], one way of approaching the current issue (but not the sole way) was to enquire whether the Receivers had discharged the duty imposed on them by s 420A of the Corporations Act. That section provides:

In exercising a power of sale in respect of property of a corporation, a controller must take all reasonable care to sell the property for:

(a) if, when it is sold, it has a market value – not less than the market value; or

(b) otherwise – the best price that is reasonably obtainable, having regard to the circumstances existing when the property is sold.

In ascertaining whether a controller has taken all reasonable care in the sale of a property pursuant to s 420A of the Corporations Act, the section necessitates an assessment or enquiry into the process adopted by the Receivers in selling the property: Florgale Uniforms Pty Ltd v Orders (2004) 11 VR 54 at [442] – [443] and Artistic Builders Pty Ltd v Elliot & Tuthill (Mortgages) Pty Ltd (2002) 10 BPR 19,565 at [126]. The actions of the controller in selling the property (in this case the Receivers) is of course a human endeavour which requires “the exercise of judgment, taking into account all the relevant variables and circumstances of the particular case”: Letten (No. 8) at [12] also referring to Florgale Uniforms Pty. Ltd. v Orders (2004) 11 VR 54 at [442] – [443] and Artistic Builders Pty. Ltd. v Elliott & Tuthill (Mortgages) Pty. Ltd. (2002) 10 BPR 19, 565 at [126].

The Receivers must act in good faith and not in a manner which is unconscionable. So, for example, the Court may refuse to authorise a sale if another course of action can be pursued to the benefit of all parties concerned: AIDC at 649 and 652 and see also Re Buenos Aires Port and City Tramways Limited (1920) 123 LT 748 at 750. However, a Court will usually sanction an immediate sale if the only alternative is for the Receiver to continue his or her management of the company indefinitely: see Company Receivers and Administrators by O’Donovan (Thomson Reuters) at [23.3510]. In the present case, the proposed course does not necessarily involve a sale but such a course will be permitted by the Court if that course is one which is sound in the all the circumstances.

A mortgagee in exercising a power of sale must act in good faith: Kennedy v De Trafford [1896] 1 Ch 762 at 772; MBF Investments Pty. Ltd. v Nolan [2011] VSCA 114 at [65]-[66]. That duty is, by analogy, very close to the exercise of a power of sale by a receiver: AIDC at 647. It is when a mortgagee’s conduct in a sale departs from such reasonable standards as to be unconscionable that the mortgagee’s power of sale may be impugned: Hawkesbury Valley Developments Pty. Ltd. v Custom Credit Corporation [1995] NSW Conv. R. 55-731 at 55,650.

OTHER RELEVANT FACTS

17 Before turning to consider the sale process, other facts relevant to the application should be noted at the outset.

18 Westpac is the secured creditor. Westpac has agreed to release its security over the properties the subject of the Sale Contracts if the contracts are settled and appropriate notice is given to the guarantors. If the Sale Contracts are settled the proceeds of sale, however, will not be sufficient to discharge the entire debt owed to Westpac. The shortfall to the secured lender is in excess of $10.393 million.

19 Secondly, there are substantial amounts of accruing interest and receivership costs. Finally, Westpac informed the Court that if the Sale Contracts are not settled by 30 June 2011, it will not provide further funding to the Receivers beyond that date.

SALE PROCESS

20 Against that background, I turn to the sale process undertaken by the Receivers.

21 On 23 July 2010, the Receivers engaged experienced estate agents – Knight Frank – to conduct the sale process, and, following extensive consultation with the relevant stakeholders, took the agent’s advice as how to best market and sell the YVG Properties and the Glenbelle Properties. The YVG Properties not included in the sale process were the Botanica townhouses that were subject to pre-existing contracts of sale and Lots 6, 7 and 8 of what is commonly referred to as the Henley Land as these lots are also subject to pre-existing contracts of sale.

22 The marketing of the YVG and Glenbelle Assets included an advertising campaign in Australian newspapers, advertising on the Knight Frank and RealCommercial websites, direct contact and emails by Knight Frank to potential local and international parties and the preparation of a marketing brochure in physical and e-brochure format. The newspaper advertisements appeared in The Age on 11, 18 and 25 August 2010, the Australian Financial Review on 12, 19 and 26 August 2010 and The Australian on 19 August 2010. The formal marketing campaign lasted for four weeks in accordance with the 4 June Orders.

23 During the marketing campaign, Knight Frank directly mailed approximately 1,750 copies of the brochure to their database of domestic and international companies and individuals involved in the golf industry and electronically distributed the e-brochure to Knight Frank’s database and a number of international companies identified by Dr Tickell who developed the original concept for the Heritage Golf and Country Club Complex. Knight Frank also utilised their Singapore office to further disseminate the marketing materials. By way of summary, approximately 1,750 brochures were distributed (1,600 domestically and 150 to international parties), 871 hits on the internet and 12 on-site inspections.

24 Separate information memoranda were prepared for the YVG assets and the Glenbelle assets. Each information memorandum stated that expressions of interest (EOI) would be considered on an individual asset or combined basis. Particular complaint was made by Bridgehead and Dr Tickell about the manner in which certain assets identified as “Other YVG developed and undeveloped land” were “marketed”. On page 37 of the Information Memorandum, these assets were described as follows:

In addition to the golf related assets of YVG and the shares in HGCC [Heritage Golf & Country Club] which are available for sale, YVG also owns further parcels of developed and undeveloped land at Heritage Golf & Country Club.

The Receivers … do not intend for this land to be sold (either in whole or in part) as part of this sale process. If interested parties, however, see the acquisition of either some or all of this land as fundamental to their bid, the Receivers and Managers will review each offer on an individual case by case basis and the Expressions of Interest lodged by the interested party must reflect the value being applied to the assets subject to the sale process as well as that which is being applied to the developed and undeveloped land.

The Receivers … note that there is no obligation for YVG to sell the developed and undeveloped land as part of this sale process.

25 Bridgehead described the land about which they made principal complaint as the “Development Land” comprising:

1. Stage 13 (land behind hotel);

2. Stage 11 (Augusta);

3. “Riverview”; and

4. Stages 24-26,

being all assets associated with the Heritage Golf & Country Club Complex (other than the YVG business and the Henley and St John golf courses).

26 Ten non-binding EOI were received by the date specified in the Information Memoranda – seven offers for the combined YVG and Glenbelle assets and three offers for the Glenbelle assets only. Five of the seven offers for the combined YVG and Glenbelle assets included the Development Land. Another party who made an offer for the combined YVG and Glenbelle assets sought an option over the Development Land. Six parties were shortlisted. Five had made combined offers for the YVG and Glenbelle assets including the Development Land.

27 There were extensive rounds of negotiation in four stages. The complexities and nuances in the negotiations and the degree of care performed by the Receivers in the conduct of the sale was provided to the Court in a confidential exhibit. In the end, the successful offer included the Development Land.

SUBMISSIONS

28 The Receivers submitted that they took all reasonable care in obtaining the market value of the YVG and Glenbelle Properties, being the price that a willing purchaser would have to pay a vendor willing but not anxious to sell in order to obtain the property.

29 What then are the complaints of Bridgehead and Dr Tickell? They fall into three categories. First, Dr Tickell submitted that the advertising campaign and the negotiations were not conducted in an appropriate manner. Secondly, contrary to the Receivers’ submissions, that the Development Land was not marketed, there was no market created and people were not provided and did not bid separately on the land. A third complaint concerned an alleged failure to allocate the sale price between YVG and Glenbelle may be dismissed.

30 The first and third complaints can be disposed of shortly. In relation to the first complaint, the Receivers took the agent’s advice as how to best market and sell the YVG Properties and the Glenbelle Properties. The agent’s advice was followed. The complaint is without foundation. Similarly, the third complaint should be dismissed. The purchaser, not the vendor, of the assets allocated the sale price.

31 The second complaint is more difficult. It is true that the Development Land was not marketed separately. It is true that the Information Memorandum said that it would not be sold. That statement was unsurprising because at that time the Receivers had made a conscious decision to market the land to ensure that the two golf courses, club house and gold memberships survived as a going concern. That strategy was important. Without the assets functioning as a going concern, all of the assets were primarily just pieces of land. Put another way, the value of the Development Land would be greater if the other assets were a going concern. The Information Memorandum, however, did go on to state that the Receivers would consider offers for the Development Land – and they did. Five of the shortlisted parties including the two final bidders bid for the assets including the Development Land.

32 The Receivers submitted that the Court should be wary of the submissions raised by Bridgehead and Dr Tickell because they go to matters of commercial judgment that the Receivers have made about how best to sell the assets. At one level, that is right. The actions of the controller in selling the property (in this case the Receivers) is of course a human endeavour which requires “the exercise of judgment, taking into account all the relevant variables and circumstances of the particular case”: Letten (No 8) at [12] also referring to Florgale Uniforms Pty. Ltd. v Orders (2004) 11 VR 54 at [442] – [443] and Artistic Builders Pty. Ltd. v Elliott & Tuthill (Mortgages) Pty. Ltd. (2002) 10 BPR 19, 565 at [126].

33 However, the Receivers must act in good faith and not in a manner which is unconscionable. It is when the conduct in a sale departs from such reasonable standards as to be unconscionable that the power of sale may be impugned. The question is whether they have done so in this case?

34 In all the circumstances, I am satisfied for the following reasons that the Receivers have acted in good faith and not in a manner which is unconscionable. I am satisfied that they took reasonable care in obtaining the market value of the properties the subject of the Sale Contracts (including the Development Land), being the price that a willing purchaser would have to pay a vendor willing but not anxious to sell in order to obtain the property.

35 First, contrary to Bridgehead’s submissions, there was an explanation as to why the Development Land was dealt with in the Information Memorandum in the manner set out in [24] above. As noted above, consistent with the advice the Receivers received from the experts, they adopted a flexible realisation strategy in relation to the assets with the golf courses as “the headline act”. The Information Memorandum made that position abundantly clear. Interestingly, that approach had been foreshadowed by the Receivers in the YVG Disclosure Report dated 27 April 2010.

36 Secondly, the evidence establishes that there was a robust competitive process for the entirety of the assets. Thirdly, there were no serious bids for the golf courses on a stand alone basis. Fourthly, as the Receivers submitted, care must be taken when seeking to compare the various offers to ensure that they are truly comparable. Many are not. Some contained offers for assets that are not the subject of this application. Others contained numerous and onerous conditions which the Receivers had to weigh up in assessing the various offers.

37 Fifthly, Westpac, the secured lender, supports the approval of the Sale Contracts notwithstanding the fact that the shortfall to the secured lender is in excess of $10.393 million. That fact is important because even if for the purposes of the argument propounded by Bridgehead and Dr Tickell the Development Land was able to be realised separately at say $7.8 million (the value allegedly ascribed to the land by one of the selling agents when speaking with one of the potential purchasers) or $10 million (the highest amount suggested by Dr Tickell), it would still be insufficient to pay out the secured creditor. Put another way, the unsecured creditors would not be disadvantaged by the approval of the Sale Contracts.

38 I will therefore make the following orders:

1. The Receivers are justified in settling the contracts of sale entered into by the Receivers on 23 December 2010 in relation to the YVG Properties and the Glenbelle Retreat & Spa, exhibited at exhibits DJT-108, DJT-109, DJT-110, DJT-111 and DJT-112 (as varied by the letter agreements exhibited at DJT-113, DJT-114 and DJT-115) to the Twenty Fifth affidavit of Damian John Templeton sworn 21 April 2011.

2. Until further order, Confidential Exhibit DJT-103 and Exhibit DJT-112A to the Twenty Fifth Affidavit of Damian John Templeton sworn 21 April 2011 be placed in a sealed envelope and marked “Confidential: No access without leave of a judge of the Court”.

3. Until further order, pursuant to s 50 of the Federal Court of Australia Act 1976 (Cth), there be no publication of Confidential Exhibit DJT-103 or Exhibit DJT-112A to the Twenty Fifth Affidavit of Damian John Templeton sworn 21 April 2011 other than to ASIC and its legal representatives, the legal representatives of the defendants, judges of the Court, judges’ associates and executive assistants and the Receivers and their legal representatives and staff.

|

I certify that the preceding thirty-eight (38) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gordon. |

Associate:

ANNEXURE A

|

Scheme |

Description of property |

Joint venture manager/s | |

|

1. |

211 Wellington Road Joint Venture |

211 Wellington Road, Mulgrave, Victoria |

211 Wellington Road Pty Ltd – Third Defendant |

|

2. |

Healesville Walk Shopping Centre Joint Venture |

251-263 Maroondah Highway, Healesville, Victoria |

Bluemist Holdings Pty Ltd – Fourth Defendant |

|

3. |

Howleys Road Joint Venture |

40-48 Howleys Road, Notting Hill, Victoria |

Dellwood Holdings Pty Ltd – Fifth Defendant |

|

4. |

George Street Joint Venture |

34 George Street, Launceston, Tasmania |

Enmore Enterprises Pty Ltd – Sixth Defendant |

|

5. |

Cimitiere House Joint Venture |

113 Cimitiere Street, Launceston, Tasmania |

Enmore Enterprises Pty Ltd – Sixth Defendant |

|

6. |

Reef House Resort |

99 Williams Esplanade Palm Cove, Qld – The Sebel Reef House Resort |

Firbank Arch Pty Ltd – Seventh Defendant Glenline Pty Ltd – Eighth Defendants |

|

7. |

Queen Street Joint Venture |

118 Queen Street, Melbourne, Victoria |

Gerling Holdings Pty Ltd – Ninth Defendant |

|

8. |

Low Head Joint Venture |

136 Low Head Road George Town, Tasmania, 142 Low Head Road, George Town, Tasmania & 40 Gunn Parade, George Town, Tasmania |

Low Head Village Pty Ltd – Twelfth Defendant |

|

9. |

Nicholson Street Joint Venture |

127-137 Nicholson Street, East Brunswick, Victoria |

Nicholson Street Pty Ltd – Thirteenth Defendant Holloway Crest Pty Ltd – Fourteenth Defendant Rosebery Enterprises Pty Ltd – Fifteenth Defendant |

|

10. |

National Boulevard Joint Venture |

144 National Boulevard, Campbellfield, Victoria |

Rosebery Enterprises Pty Ltd – Fifteenth Defendant |

|

11. |

Simms Investment Project |

626 Pittwater Road, Brookvale, NSW |

Simms Investments Pty Ltd – Sixteenth Defendant |

|

12. |

SY21 Retail Complex Project |

||

|

13. |

The Glen Centre Joint Venture |

673–681 Glenferrie Road, Hawthorn, Victoria |

The Glen Centre Hawthorn Pty Ltd – Eighteenth Defendant Castello Holdings Pty Ltd – Nineteenth Defendant |

|

14. |

Twinview Joint Venture |

167 Flinders Lane, Melbourne, Victoria |

Twinview Nominees – Twentieth Defendant |

|

15. |

Yarra Valley Golf Joint Venture |

St John of God's Seminary and Henley Farm, Chirnside Park, Victoria |

Yarra Valley Golf Pty Ltd – Twenty-First Defendant Adina Rise Pty Ltd – Twenty-Second Defendant Albright Investments Pty Ltd – Twenty-Third Defendant Ashfield Rise Pty Ltd – Twenty-Fourth Defendant Bradfield Corporation Pty Ltd – Twenty-Fifth Defendant Copeland Enterprises Pty Ltd – Twenty-Sixth Defendant Devlin Way Pty Ltd – Twenty-Seventh Defendant First Hazelwood Pty Ltd – Twenty-Eighth Defendant Glenbelle Pty Ltd – Twenty-Ninth Defendant Glenvale Way Pty Ltd – Thirtieth Defendant Greenview Lane Pty Ltd – Thirty-First Defendant Hallmark Corporation Pty Ltd – Thirty-Second Defendant Moorleigh Holdings Pty Ltd – Thirty-Third Defendant Norton Ridge Pty Ltd – Thirty-Fourth Defendant Raleigh Glen Pty Ltd – Thirty-Fifth Defendant Redcrest Holdings Pty Ltd – Thirty-Sixth Defendant Suri Corporation Pty Ltd – Thirty-Seventh Defendant Sutton Rise Pty Ltd – Thirty-Eighth Defendant The Virtual Mlmer Pty Ltd – Thirty-Ninth Defendant Tivendale Pty Ltd – Fortieth Defendant Tulloch Downes Pty Ltd – Forty-First Defendant Mainking Pty Ltd – Forty-Second Defendant Topglen Pty Ltd – Forty-Third Defendant Allblue Pty Ltd – Forty-Fourth Defendant Aranbay Pty Ltd – Forty-Fifth Defendant |

|

16. |

Glenbelle Project |

Sebel Heritage Lodge Management Lot, Yarra Valley Golf Course, Chirnside Park, Victoria |

Glenbelle Pty Ltd – Twenty-Ninth Defendant Redcrest Holdings Pty Ltd – Thirty-Sixth Defendant |

ANNEXURE B

ANNEXURE C

SCHEDULE OF PARTIES

LGH HOLDINGS LIMITED (ACN 077 191 943)

Second Defendant

211 WELLINGTON ROAD PTY LTD (ACN 092 663 860)

Third Defendant

BLUEMIST HOLDINGS PTY LTD (ACN 097 306 922)

Fourth Defendant

DELLWOOD HOLDINGS PTY LTD (ACN 098 505 803)

Fifth Defendant

ENMORE ENTERPRISES PTY LTD (ACN 082 158 487)

Sixth Defendant

FIRBANK ARCH PTY LTD (ACN 059 464 381)

Seventh Defendant

GLENLINE PTY LTD (ACN 098 532 364)

Eighth Defendant

GERLING HOLDINGS PTY LTD (ACN 091 726 457)

Ninth Defendant

LGH ADMINISTRATION PTY LTD (ACN 007 165 069)

Tenth Defendant

LGH FINANCE PTY LTD (ACN 078 859 248)

Eleventh Defendant

LOW HEAD VILLAGE PTY LTD (ACN 091 731 958)

Twelfth Defendant

NICHOLSON STREET PTY LTD (ACN 069 104 089)

Thirteenth Defendant

HOLLOWAY CREST PTY LTD (ACN 091 731 967)

Fourteenth Defendant

ROSEBERY ENTERPRISES PTY LTD (ACN 091 826 229)

Fifteenth Defendant

SIMMS INVESTMENTS PTY LTD (ACN 093 504 511)

Sixteenth Defendant

SY21 RETAIL PTY LTD (ACN 107 874 564)

Seventeenth Defendant

THE GLEN CENTRE HAWTHORN PTY LTD (ACN 089 906 543)

Eighteenth Defendant

CASTELLO HOLDINGS PTY LTD (ACN 088 204 175)

Nineteenth Defendant

TWINVIEW NOMINEES PTY LTD (ACN 097 307 278)

Twentieth Defendant

YARRA VALLEY GOLF PTY LTD (ACN 066 632 479)

Twenty-First Defendant

ADINA RISE PTY LTD (ACN 083 181 122)

Twenty-Second Defendant

ALBRIGHT INVESTMENTS PTY LTD (ACN 088 204 166)

Twenty-Third Defendant

ASHFIELD RISE PTY LTD (ACN 093 504 806)

Twenty-Fourth Defendant

BRADFIELD CORPORATION PTY LTD (ACN 088 204 371)

Twenty-Fifth Defendant

COPELAND ENTERPRISES PTY LTD (ACN 093 504 824)

Twenty-Sixth Defendant

DEVLIN WAY PTY LTD (ACN 088 264 813)

Twenty-Seventh Defendant

FIRST HAZELWOOD PTY LTD (ACN 093 505 303)

Twenty-Eighth Defendant

GLENBELLE PTY LTD (ACN 097 306 646)

Twenty-Ninth Defendant

GLENVALE WAY PTY LTD (ACN 088 287 021)

Thirtieth Defendant

GREENVIEW LANE PTY LTD (ACN 093 505 312)

Thirty-First Defendant

HALLMARK CORPORATION PTY LTD (ACN 093 505 312)

Thirty-Second Defendant

MOORLEIGH HOLDINGS PTY LTD (ACN 088 287 058)

Thirty-Third Defendant

NORTON RIDGE PTY LTD (ACN 078 821 066)

Thirty-Fourth Defendant

RALEIGH GLEN PTY LTD (ACN 088 204 380)

Thirty-Fifth Defendant

REDCREST HOLDINGS PTY LTD (ACN 100 836 486)

Thirty-Sixth Defendant

SURI CORPORATION PTY LTD (ACN 093 505 321)

Thirty-Seventh Defendant

SUTTON RISE PTY LTD (ACN 088 204 399)

Thirty-Eighth Defendant

THE VIRTUAL MLMER PTY LTD (ACN 065 374 665)

Thirty-Ninth Defendant

TIVENDALE PTY LTD (ACN 093 505 349)

Fortieth Defendant

TULLOCH DOWNES PTY LTD (ACN 078 895 048)

Forty-First Defendant

MAINKING PTY LTD (ACN 100 790 485)

Forty-Second Defendant

TOPGLEN PTY LTD (ACN 096 857 564)

Forty-Third Defendant

ALLBLUE PTY LTD (ACN 100 836 388)

Forty-Fourth Defendant

ARANBAY PTY LTD (ACN 098 532 319)

Forty-Fifth Defendant

MELVILLE CORPORATION PTY LTD (ACN 091 911 045)

Forty-Sixth Defendant

TILLEY LANE PTY LTD (ACN 086 136 361)

Forty-Seventh Defendant

HPSC PTY LTD (ACN 059 930 139

Forty-Eighth Defendant

JENSDALE PTY LTD (ACN 098 367 974)

Forty-Ninth Defendant

OAKDALE RISE PTY LTD (ACN 091 598 908)

Fiftieth Defendant

MAYWOOD INVESTMENTS PTY LTD (ACN 091 599 218)

Fifty-First Defendant

ACETRAIN PTY LTD (ACN 100 820 282)

Fifty-Second Defendant

SAGE BAY PTY LTD (ACN 097 306 628)

Fifty-Third Defendant

TOBAGO HOLDINGS PTY LTD (ACN 093 504 520)

Fifty-Fourth Defendant