FEDERAL COURT OF AUSTRALIA

Andrews v Australia and New Zealand Banking Group Ltd [2011] FCA 388

IN THE FEDERAL COURT OF AUSTRALIA | |

| First Applicant ANGELO JULIAN SALIBA Second Applicant GEOFFREY ALLAN FIELD Third Applicant | |

AND: | AUSTRALIA AND NEW ZEALAND BANKING GROUP LTD (ACN 005 357 522) Respondent |

DATE OF ORDER: | |

WHERE MADE: |

THE COURT ORDERS THAT:

1. The parties are to confer and bring in orders to give effect to these reasons for decision by 4:00pm on 28 April 2011.

2. The proceeding be listed for further directions at 9:30am on 5 May 2011.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules. The text of entered orders can be located using Federal Law Search on the Court’s website.

VICTORIA DISTRICT REGISTRY | |

GENERAL DIVISION | VID 811 of 2010 |

BETWEEN: | JOHN ANDREWS First Applicant ANGELO JULIAN SALIBA Second Applicant Third Applicant

|

AND: | AUSTRALIA AND NEW ZEALAND BANKING GROUP LTD (ACN 005 357 522) Respondent

|

JUDGE: | GORDON J |

DATE: | 19 APRIL 2011 |

PLACE: | MELBOURNE |

REASONS FOR JUDGMENT

1 This is a representative action. The Applicants are customers of Australia and New Zealand Banking Group Limited (ANZ). ANZ charged the Applicants a variety of fees for unauthorised overdrafts, overdrawn accounts, dishonour fees and over limit credit card accounts (defined collectively as Exception Fees). The contracts between the Applicants and ANZ entitled the ANZ to charge the Exception Fees (defined as Penalty Provisions).

2 The primary issue is whether ANZ is obliged to repay all or part of the Exception Fees charged to the Applicants (or to pay damages). The Applicants seek declarations that the Penalty Provisions and/or the Exception Fees are void or unenforceable as a penalty.

3 The Applicants’ claim that the Penalty Provisions and/or the Exception Fees are void or unenforceable as a penalty is put on two bases. First, they contend that the Exception Fees charged by ANZ were penalties or in the nature of penalties because of three matters: (1) the quantum of each Exception Fee was not a covenanted or agreed sum which could be regarded as a genuine pre-estimate of the damage likely to be caused by the breach; (2) upon any comparison, the quantum of each Exception Fee substantially exceeded what would be recoverable as unliquidated damages by ANZ upon breach; and/or (3) the quantum of each Exception Fee was extravagant and unconscionable in amount in comparison with the greatest loss that could conceivably be proved to have followed from the breach. The Applicants’ Amended Fast Track Statement (AFTS) particularised this third aspect by reference to, inter alia, publicly available information that they contend indicates that the cost to ANZ of responding to the circumstances giving rise to each Exception Fee was substantially less that the amount of the Exception Fees throughout the period in dispute. Alternatively, the Applicants contend that the Penalty Provisions and/or the “Exception Fee Charges”, as defined in paragraph 51 of the AFTS, are unenforceable and/or void as a penalty to the extent that the Exception Fees charged pursuant to them exceeded the loss or damage (if any) which ANZ can prove to have been caused by the breach in question. This is described by ANZ as the Applicants’ “Orthodox Penalty Case”.

4 Next, the Applicants contend that the Penalty Provisions are unenforceable and/or void as a penalty because the obligations set out in the Penalty Provisions, which were imposed on the Applicants, are properly to be characterised as lying within the area of obligation of the Applicants in that it was the Applicants’ responsibility to ensure that they did not cause an event that would trigger the application of the Penalty Provisions (defined as a Default Event). Further, the Applicants contend that upon or in default of the occurrence of a Default Event, the Exception Fees were out of all proportion or unrelated to the loss or damage which ANZ might reasonably have sustained by reason of the Default Event. This is described by ANZ as the Applicants’ “Expanded Penalty Case”.

5 ANZ denies the allegations. As a matter of legal analysis, ANZ denies that the Expanded Penalty Case is open on the current state of the law as propounded by the High Court in Ringrow Pty Ltd v BP Australia Pty Ltd (2005) 224 CLR 656. ANZ contends that the doctrine of penalties must be confined to a case of breach.

6 In relation to the factual disputes, in its Amended Fast Track Response (AFTR), ANZ identifies four factual questions for resolution. First, the contractual terms and conditions between ANZ and its customers, of which the Exception Fees formed part. This question of fact is no longer in dispute. A copy of each relevant contract was produced to the Court after the hearing (the Contracts). Moreover, the parties have identified and agreed on examples of the various Exception Fees in the Contracts that could be heard and determined as part of an initial hearing. The second factual question concerned the circumstances in which ANZ and its customers entered into the Contracts. Many of the factual allegations about the circumstances in which ANZ made contracts with its individual customers are disputed.

7 The third question of fact concerns the quantum of the Exception Fees and, in particular, whether the quantum was a genuine pre-estimate of damage, whether the quantum substantially exceeded what would be recoverable as unliquidated damages and whether the quantum was extravagant or unconscionable. ANZ admitted the quantum was not a genuine pre-estimate of a sum that would have been recoverable as unliquidated damages but ANZ disputed the other allegations. Finally, the fourth question of fact concerns the quantum of any amount to be paid to the Applicants if they are successful on any of their claims (including the non-penalty claims). That question of fact may also require consideration of the question of the costs incurred by, or the loss or damage suffered by, ANZ by reason of the events that gave rise to the charging of the Exception Fees.

8 The third and fourth questions of fact lie at the heart of the current application. Paragraph 52 of the AFTS provides:

The Exception Fees charged by ANZ to the applicants and Group Members upon breach of the Penalty Provisions were a penalty as:

(a) the quantum of each Exception Fee was not a covenanted or agreed sum which could be regarded as a genuine pre-estimate of the damage likely to be caused by the breach as:

(i) prior to entering into the Saving Contracts, Card Contracts, Commercial Card Contracts and the Business Contracts (Contracts), the parties did not reach a consensus or genuinely strike an agreement as to the pre-estimate of the likely damage or the comparative relationship between the likely damage and the proposed Exception Fee;

(ii) any amendment or change to the quantum of each Exception Fee during the course of the Contracts arose by reason of diktat of ANZ rather than by way of a consensus or a genuine agreement as to the pre-estimate of the likely damage or the comparative relationship between the likely damage and the proposed Exception Fee;

(iii) the quantum of each Exception Fee was determined by only one party to the Contract, being ANZ, without reference to a comparison of the Exception Fees with the sum that would have been recoverable as unliquidated damages payable upon breach; and/or

(b) upon any comparison, the quantum of each Exception Fee substantially exceeded what would be recoverable as unliquidated damages by ANZ upon breach; and/or

(c) the quantum of each Exception Fee was extravagant and unconscionable in amount in comparison with the greatest loss that could conceivably be proved to have followed from the breach.

Particulars

a. Publicly available material indicates that the cost to ANZ (or other banks in the position of ANZ) of responding to the circumstances giving rise to each Exception Fee (or similar fees in the case of other banks) was substantially less than the amount of the Exception Fees (or similar fees in the case of other banks) throughout the entirety of the period covered by this Amended Fast Track Statement. Such material includes:

i. Haberfield, R and Harrington, J, “Bounced Checks Boost Profits; NSF Fees and other revenue sources offer untapped potential, contends this checking account expert”, Savings Institutions, March 1991, at pp 33;

ii. Prices Surveillance Authority, Inquiry into Fees and Charges Imposed on Retail Accounts by Banks and Other Institutions and by Retailers on EFTPOS Transactions, 30 June 1995, at pp 205 and 206;

iii. Boston Consulting Group, The Untapped Power of Pricing: Opportunities for Action in Financial Services, 2002;

iv. Rich, Nicole, Unfair Fees: A report into penalty fees charged by Australian banks, Consumer Law Centre, December 2004.

b. The Exception Fees were in the order of four times the fee charged by ANZ in circumstances of an equivalent event, namely inward or inbound dishonour. See further Schedule 13 to this Amended Fast Track Statement. This particular is provided without admission that the inward or inbound dishonour fees were fair and reasonable, only that they represent a bound above which an Exception Fee cannot be readily justified.

c. The matters in paragraphs 19, 26, 33 and 40 are relied upon as evidencing the true character of the Exception Fees as a penalty.

d. Further particulars will be provided prior to the initial trial of the applicants’ claim, but following ANZ giving discovery and providing answers to any interrogatories allowed by leave.

9 ANZ responded in paragraph 55 of its AFTR. After admitting that the quantum of each relevant Exception Fee was determined by ANZ, it denied the allegations in paragraph 52 of the AFTS. However, its response continued as follows:

(c) [ANZ] says further that:

(i) the events that gave rise to each Exception Fee charged to each applicant and group member constituted the supply of one or more services by ANZ for the benefit of the applicant or group member (as applicable);

Particulars

(A) In the case of Saving Exception Fees and Business Exception Fees:

(I) the services supplied in connection with honour fees, dishonour fees and non-payment fees included the assessment of a request made by the customer for the supply of credit in amounts not previously agreed by ANZ;

(II) the services supplied in connection with dishonour fees and non-payment fees also included the assessment of a request for the processing of a payment instrument or method not previously agreed with ANZ;

(III) the services supplied in connection with honour fees also included the supply of credit at the request of the customer in amounts not previously agreed by ANZ;

(B) In the case of Card Exception Fees and Commercial Card Exception Fees:

(I) the services supplied in connection with late payment fees included the supply of credit at the request of the customer for periods of time not previously agreed by ANZ;

(II) the services supplied in connection with overlimit fees included the assessment of a request made by the customer for the supply of credit in amounts not previously agreed by ANZ;

(III) the services supplied in connection with overlimit fees included the supply of credit at the request of the customer in amounts not previously agreed by ANZ;

(ii) during the Relevant Period, the quantum of each Exception Fee did not substantially exceed, and was not extravagant and unconscionable in amount in comparison to:

(A) the costs that would or might be incurred by ANZ as a consequence of or in connection with the occurrence of the events that would or might have given rise to the Exception Fee; and

(B) the benefits that would or might be received by ANZ’s customers from the supply of the services that would or might be supplied by reason of the occurrence of the events that would or might give rise to the Exception Fee.

Particulars

The calculation of the costs and the valuation of the benefits referred to herein will be the subject of expert evidence.

(Emphasis added.)

10 The calculation exercise referred to in the particulars to paragraph 55(c)(ii) requires explanation. On 15 December 2010, one of ANZ’s solicitors filed an affidavit which informed the Court that ANZ intended to call evidence from an expert accountant as to the costs incurred by ANZ from or in connection with the customer conduct that gave rise to Exception Fees and any profitability analysis which might be relevant to Exception Fees.

11 The Court was told that:

Blake Dawson have retained Deloitte to assist with identification of the operational, capital allocation and other costs to ANZ of customer conduct that are associated with the customer conduct which gave rise to exception fees. Deloitte are developing a proposed programme of work necessary in order to estimate the costs associated with that customer conduct. It is anticipated that a UK partner of Deloitte, who will be appointed as [ANZ’s] independent expert, will review and approve the methodology for estimating the costs and will subsequently review and interpret the outputs of the cost modelling exercise.

12 What then followed under a heading “Programme of work for estimating the costs of exception fee processes” is important. First, ANZ’s solicitor summarised ANZ’s assessment (as at 14 December 2010) of the Deloitte exercise as follows:

Deloitte are developing a programme of work designed to enable an assessment to be made of the various operational, capital allocation and other costs to ANZ of customer conduct which gave rise to exception fees. Following a high level review of the bank’s processes that relate to or result from such customer conduct and consideration of the likely availability of costs information at the necessary level of detail to enable those processes to be costed, Deloitte have estimated the time necessary to complete the work programme to assess operational costs to be around 14 months and the time necessary to complete a separate work programme (to be undertaken at the same time) to assess capital allocation and other (eg funding) costs to be four to six months.

(Emphasis added.)

13 Twenty six paragraphs dealing with “Operational Costs” and “Credit risk and capital allocation” then followed. The section dealing with Operational Costs was itself divided into five sections: First phase: detailed process mapping; Second Phase: source data; Third Phase: master data; Fourth phase: costs model and Fifth phase: reporting. Each section outlined the work proposed to be undertaken in each phase. The solicitor for ANZ stated that the “work programme assume[d] that the team undertaking the work [would] be heavily resourced … so that as many tasks as possible will be undertaken simultaneously”.

14 Justice Finkelstein expressed concern about the proposal. Justice Finkelstein directed ANZ to arrange for Mr Will Inglis, from Deloitte, London (ANZ’s expert), to be available in Court on 10 February 2011. He expected he would speak to him by video link. Mr Inglis travelled to Australia. On 10 February 2011, Mr Inglis discussed what has become known as the “Inglis Exercise” with his Honour. No letter of instruction to Mr Inglis was produced to the Court in December 2010, at the hearing on 10 February 2011 or, for that matter, at the hearing on 7 March 2011. During the course of the directions hearing on 10 February, the following became evident as at 10 February 2011:

1. Mr Inglis had not read anything about the matter until some 10 days prior to the hearing, while on the aeroplane over to Australia;

2. a team from Deloitte, Australia, had been working on “planning” the Inglis Exercise for two or three months. That “planning” work was to set out the programs for how Deloitte Australia and Deloitte London propose to proceed;

3. a timeline had been prepared which estimated completion in 14 months but that no one could be quite sure how long in fact the exercise was going to take because, according to Mr Inglis, “it’s a task that no one has done before”;

4. although the objective was to cost every single step involved in one of these events – such as bouncing a cheque – realistically Mr Inglis was unable to say whether that could be achieved because:

4.1 ANZ is a large, complex organisation with many different systems and processes and “it has not, as part of its ordinary course of business, felt it necessary to measure the activities which go to these particular events”. Put another way, ANZ has “never gone down to a sufficient level of granularity in relation to the exception fee, as to be able to understand the exact costs”. ANZ “simply has not measured these in the past”;

4.2 Costing is very difficult to do for banks because they have a very, very high level of central cost and very little can be attributed specifically to a particular product line or service.

15 On 24 February 2011, ANZ’s solicitors wrote to Mr Inglis to enable an “update” to be provided to the Court on 7 March. Mr Inglis was asked 6 questions. The questions are in bold. So far as is relevant, his answers provided by letter dated 28 February 2011 follow each question:

1. How many cost centres does ANZ have?

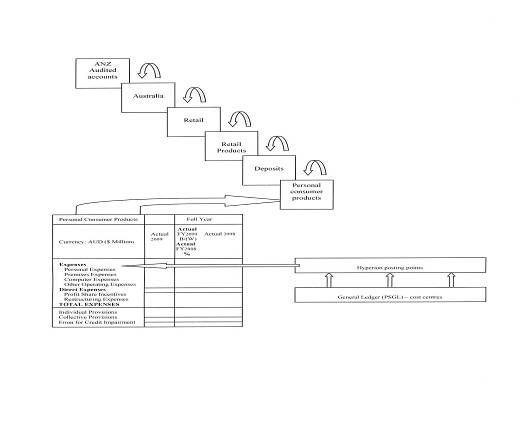

ANZ’s audited accounts are based on a financial reporting application called Hyperion. Hyperion gathers information from the general ledger … and other sources.

In 2009, ANZ used over 4,000 Hyperion reporting points of which approximately 950 related to the Australian division of ANZ and the related ANZ centralised areas. Based on an initial high level review of these reporting points, I currently expect that in the region 400 of these reporting points are, or may be, relevant to the costing of Exception Fees [footnote omitted].

2. What material information is recorded in respect of each cost centre?

The Hyperion reporting points are set up in a hierarchy or reporting point tree (illustrated below). It is therefore necessary to follow costs back down through this tree until there is sufficient detail to enable the relevant costs to be identified. Each Hyperion reporting point consists of the same direct expenses categories namely:

• Personnel Expenses;

• Premises Expenses;

• Computer Expenses;

• Other operating Expenses; and

• Net Intra Group Expenses …

To the extent that any particular Hyperion reporting point is considered relevant (i.e. approximately 400), all these categories of costs are relevant to this matter in that the reporting point will, to a greater or lesser degree, contain costs that are related to Exception Fees. Hyperion reporting points also contain a further breakdown for each category of costs. For example, “Personnel expenses” will consist of wages and salaries, employee taxes, annual leave and so on.

The general ledger (PSGL) maps into Hyperion reporting points known as posting points. PSGL provides an even greater level of granularity relative to Hyperion, with over 8,000 cost centres within PSGL. Each Hyperion posting point may have one or several PSGL cost centres mapped to it. I hope that in most instances it will not be necessary to go beyond the Hyperion posting points into PSGL, but I cannot rule out the possibility that on occasion it may be.

3. To what extent will the existing cost centre information allow you to calculate the costs referable to Exception Fees? What are the obstacles to calculating the costs referable to Exception Fees based upon ANZ’s existing cost centre information?

The existing cost centre information provides some assistance in calculating costs referable to Exception Fees. It is possible to immediately eliminate some areas of ANZ’s total cost base as not relevant, thus reducing the overall cost population that needs to be considered and also providing an overview of the areas where larger amounts of relevant costs may be recorded and which should be focused on.

However, as noted above, the costs that may be referable to Exception Fees cut across a significant proportion of the reporting points within Hyperion.

The reporting structure and accounting cost centres are designed for financial reporting purposes and not to capture costs associated with specific activities or operations. It is therefore necessary to review the Hyperion reporting points to identify the relevant costs. Each reporting point may have a large or small proportion of its costs that are relevant: few will have costs that relate only to activities connected to the Exception Fees.

4. To what extent do you consider you may be able to adopt ANZ’s own costs assessment or allocation work for the purposes of your assignment?

ANZ’s own existing costing models tend to have a number of limitations. Some do not go back very far, the methodologies have continued to be refined and changed over the years so each year will need to be reviewed, they tend to be based on plans rather than actual costs (although this may not necessarily be a significant issue on the assumption that ANZ’s forecasting is reasonably robust), and lastly, they do not look at costs in sufficient detail. … At best, these costing models may provide some form of high level sense check, but are unlikely to provide much more than this.

My other observation at this stage is that whilst the cost allocation work that ANZ has done in respect of overheads, premises and technology is helpful (for example, in considering the reallocation of costs) the over-riding issue remains that the fees that are central to this matter do not form part of the core activities. Consequently they do not answer the question I have been asked to address in relation to Exception Fees.

5. Do your answers to questions 3 or 4 have any impact on the work program?

The above analysis has tended to confirm the basis on which the proposed work programme has been prepared and I do not envisage any changes of note as a consequence. I note that in one area the matter is more problematic than I had initially thought. I understand that Hyperion does not record changes in the reporting structure over time and it is therefore not simply a case of applying the same methodology to a number of years as the same type of costs may have been reported in different place [sic]. It may therefore be necessary to reconstitute Hyperion for previous financial years. I do not yet know how significant an issue this may be when looking back over preceding years.

6. What is your current estimate of the time required to complete the assignment?

Based on the findings of the work carried out by me and my team since 10 February 2011 and my comments above, my view remains that the best estimate I am able to give, and clearly this can be no more than an estimate, is 13 months to complete the assignment on the basis we had originally planned.

The entirety of Mr Inglis’ responses is important and repays careful re-reading. In short, the construction exercise is enormous. Mr Inglis does not know the extent to which he needs to look at up to 8,000 cost centres and ANZ has never captured the information he needs for the construction exercise. In relation to the information ANZ in fact holds, its Hyperion system does not record changes in the reporting structure over time. The result – is that it might be necessary for the Inglis Exercise to reconstitute Hyperion for previous financial years. Mr Inglis’ best estimate is that it will take 13 months to complete the assignment.

16 In a further letter dated 28 February 2011 from Mr Inglis to ANZ’s solicitors he stated that:

1. the Inglis Exercise was one of construction – understanding the relevant processes, analysing the available financial data, designing and performing programmes to measure activities where existing financial and other data is insufficient, identifying costs relevant to activities relating to fee events, building a cost model sufficiently flexible to allow costs to be recalculated in the event that the court determined that certain costs should be treated differently and preparing an expert report;

2. there may be difficulties retrieving data in sufficient detail in relation to earlier years and that the task is likely to be harder because those involved in financial management at the time may have moved on or may not recall in detail how the systems worked at the relevant time;

3. limiting the number of fee types under examination to six fees across four fee types covering four or five financial years may result in “some marginal saving in time” which, in broad terms would expect to “lead to a decrease in the timetable of only a few weeks”.

17 It is against that factual background that the current applications come before the Court.

NOTICE OF MOTION

18 By a Notice of Motion filed on 22 February 2011, the Applicants seek two orders. First, an order pursuant to O 11 r 16 of the Federal Court Rules (FCR) and/or s 37P and/or s 33ZF of the Federal Court of Australia Act 1976 (Cth) (the FCA) that paragraph 55(c)(ii) of ANZ’s AFTR be struck out on the basis that it discloses no reasonable defence or allegation relevant to paragraph 52 of the Applicants’ AFTS.

19 Secondly, the Applicants seek an order pursuant to ss 33Z(1), 33ZF(1) and 37P(2) of the FCA and, further or alternatively, O 29 r 2 of the FCR, that the Court determine identified questions separately and before any other issue in the proceedings. On the morning of the hearing, the Applicants handed up identified questions which were substantively different to those attached to the Motion. The separate questions now sought by the Applicants were identified as:

1. In respect of each of the Exception Fees, are the amounts payable upon breach, so as to be capable of amounting to a penalty?

2. In respect of each of the Exception Fees, are the amounts otherwise payable on the occurrence of an event within the area of obligation of the customer, such that they are capable of amounting to a penalty?

20 I will deal with each application in turn.

A. APPLICATION to STRIKE OUT

21 As noted, the application to strike out paragraph 55(c)(ii) of the AFTR is made under O 11 r 16 of the FCR and/or ss 37P and/or 33ZF of the FCA.

Order 11 r 16 of the FCR

22 Order 11 r 16 of the FCR provides that:

Where a pleading:

(a) discloses no reasonable cause of action or defence or other case appropriate to the nature of the pleading;

(b) has a tendency to cause prejudice, embarrassment or delay in the proceeding; or

(c) is otherwise an abuse of the process of the Court,

the Court may at any stage of the proceeding order that the whole or any part of the pleading be struck out.

23 An order to strike out a pleading will “only be made in a plain and obvious case”: Davis v Commonwealth of Australia (1986) 68 ALR 18 at 23 and the authorities cited. It is a discretionary power to be exercised with caution: Trade Practices Commission v Pioneer Concrete (Qld) Pty Ltd (1994) 52 FCR 164. As Finkelstein J stated in Imobilari Pty Ltd (ACN 091 464 729) v Opes Prime Stockbroking Ltd (in liq) (recs and mgrs apptd) (ACN 086 294 028) (2008) 252 ALR 41 said (at [4] – [5]):

The fundamental thing to understand about the strike-out rule, which the language of O 11 r 16 itself makes clear, is that the rule is concerned only with the adequacy of the pleading (or to be more precise, the allegations and the causes of action asserted therein) as a matter of law. The rule does not permit or allow consideration of facts or evidence outside the pleadings: Dey v Victorian Railways Cmrs (1949) 78 CLR 62 at 91 and 109 … see also General Steel Industries Inc v Cmr for Railways (NSW) (1964) 112 CLR 125 at 129 … Indeed, as counsel for ANZ, Mr Archibald QC, correctly noted in his submissions, the court must, for purposes of deciding the strike-out motion and deciding whether a pleading discloses a reasonable cause of action, assume the truth of the allegations in the statement of claim and draw all inferences in favour of the non-moving party because the question is whether those allegations, even if proved, cannot succeed as a matter of law: General Steel at CLR 129.

The United States Supreme Court recently reexamined the standard for a strike-out motion (called a motion to dismiss in the US) in Bell-Atlantic Corp v Twombly 550 US 544 (2007) ... The Supreme Court reaffirmed that on a strike-out motion the court is required to assume the truth of all allegations. Proceeding on that assumption, the Supreme Court held the only question is whether the allegations are enough to raise the applicant’s right to relief above the speculative level. That is, the allegations must be plausible enough to create a reasonable expectation that discovery will reveal evidence to support the claim. This plausibility test is consistent with the strike-out test expressed by the High Court in General Steel, where Barwick CJ said (at CLR 129):

The test to be applied has been variously expressed; “so obviously untenable that it cannot possibly succeed”; “manifestly groundless”; “so manifestly faulty that it does not admit of argument”; “discloses a case which the Court is satisfied cannot succeed”; “under no possibility can there be a good cause of action”; “be manifest that to allow them” (the pleadings) “to stand would involve useless expense”… At times the test has been put as high as saying that the case must be so plain and obvious that the court can say at once that the statement of claim, even if proved, cannot succeed; or “so manifest on the view of the pleadings, merely reading through them, that it is a case that does not admit of reasonable argument”; “so to speak apparent at a glance”.

(Emphasis added.)

Consistent with that view, the Court will not usually decide a difficult question of law on a strike-out application unless resolution of the question of law will bring the proceedings to an end or else substantially reduce the scope of the trial: Traderight (NSW) Pty Ltd and Ors v Bank of Queensland Ltd [2008] NSWSC 543 and Williams and Humbert Ltd v W&H Trademarks (Jersey) Ltd [1986] AC 386, at 435-6.

24 Opinions have been expressed that some revision of the principles may be necessary in light of the ever increasing complexity of modern commercial litigation: cf AWA Limited v Daniels (unreported, Supreme Court of New South Wales, Rogers CJ Comm D, 8 October 1992,) and Re Elders Australia Ltd; Super John Pty Ltd & Ors v Futuris Rural Pty Ltd (No 2) [1997] FCA 1501. In my view, the principles have, at least to some extent, already been modified. That last statement requires explanation.

25 In 1993, the High Court reaffirmed the principles applicable to a strike out application without qualification: cf Webster v Lampard (1993) 177 CLR 598. Sixteen years later, the High Court expressed what must be described as the pragmatic modern view of litigation (albeit in the context of an amendment application): a view which proceeds from a number of fundamental premises. First, that case management is an essential and accepted aspect of our civil justice system: AON Risk Services Limited v Australian National University (2009) 239 CLR 175 at [92]. Secondly, the civil litigation rules no longer are considered as directed only to the resolution of the dispute between the parties to the proceeding: AON at [93]. Thirdly, that conduct of litigation is not merely a matter for the parties but also one for the Courts: AON at [93]. Fourthly, case management requires account to be taken of other litigants, not just the parties to the proceedings.

26 Of course “case management principles should not supplant the objective of doing justice between the parties according to law”: AON at [29], [30] and [57]. However, the High Court stated that “waste of public resources and undue delay, with the concomitant strain and uncertainty imposed on litigants”, together with the potential for loss of public confidence in the legal system, were factors able to be taken into account in the exercise of interlocutory discretions: AON at [30] and at [57]. The analysis of the plurality in AON is instructive. Their Honours (at [57], [94] and [95]) refer to The State of Queensland v JL Holdings Pty Limited (1997) 189 CLR 146 at 154, where after referring the Court’s previous decision in Sali v SPC Ltd (1993) 67 ALJR 841, the plurality in JL Holdings dealt with case management principles as follows:

… nothing in that case suggests that those principles might be employed, except perhaps in extreme circumstances, to shut a party out from litigating an issue which is fairly arguable. Case management is not an end in itself. It is an important and useful aid for ensuring the prompt and efficient disposal of litigation. But it ought always to be borne in mind, even in changing times, that the ultimate aim of a court is the attainment of justice and no principle of case management can be allowed to supplant that aim.

(Emphasis added.)

27 The High Court in AON then went further – their Honours acknowledged that it may be necessary in an appropriate case to make a decision which may produce a sense of injustice, for the sake of doing justice to the opponent or to other litigants: AON at [94]. Such an approach is consistent with the direction in s 37M(3) of the FCA that the Rules must be interpreted and applied, and any power conferred must be exercised or carried out, in a way that best promotes the overarching purpose – the just resolution of disputes according to law and as quickly, inexpensively and efficiently as possible: see s 37M of the FCA and AON at [97] – [98].

28 Put another way, “courts have an inherent power to prevent misuse of their procedures in a way, which although not inconsistent with a literal applications of the Rules, would nevertheless be unfair to a party to the litigation ‘or would otherwise being the administration of justice into disrepute among right-thinking people’”: AON at [33] and the authorities cited.

Apply to Fast Track?

29 Before turning to consider O 11 r 16 of the FCR, it is first necessary to enquire whether O 11 r 16 of the FCR which refers to “pleadings” applies to proceedings filed in Fast Track. ANZ did not contend that O 11 r 16 of the FCR was inapplicable.

30 “Pleading” is defined in O 1 r 4 of the FCR as including “a statement of claim and a cross-claim to which Order 5 applies and subsequent pleadings, but does not include an application, notice of motion or affidavit”. The definition is not exhaustive. That is not surprising. The mere labelling of a document as a “pleading” (or a particular type of pleading) will never be sufficient to ensure that a document is a pleading. More is required. Similarly, the fact that a document is not called, for example, a “statement of claim” does not preclude the operation of O 11 of the FCR.

31 The purpose of a pleading is to clearly define the issues to be tried, and to allow the other party an opportunity to know the case against them: Betfair Pty Limited v Racing New South Wales [2010] FCAFC 133 at [49] – [52]; Gould, Birbeck and Bacon v Mount Oxide Mines Limited. (In liquidation) (1916) 22 CLR 490, 517 and Australian Securities and Investments Commission v Sydney Investment House Equities Pty Ltd (2008) 69 ACSR 1 at [68]. That has been the role and purpose of pleadings at least since the Supreme Court of Judicature Act 1875 (UK): see AON at [10] – [13].

32 The Federal Court Practice Note “CM 8 – Fast Track” (CM 8) sets out the arrangements for the management of proceedings filed in Fast Track: cl 1.2 of Pt 1. Part 4 of CM 8 entitled “Fast Track Statements, Responses and Cross-Claims” addresses the fact that pleadings are replaced by Fast Track Statements, Responses and Cross-Claims (together, Fast Track documents) as follows:

No pleadings unless Court otherwise orders

4.1 Unless the Court otherwise orders, there will be no pleadings in a proceeding to be conducted in accordance with the Fast Track Directions. Instead, the parties will use Fast Track Statements, Fast Track Responses, Fast Track Cross-Claims and Fast Track Replies.

33 That statement must be read in context. Clauses 4.2 and 4.3 provide:

Fast Track Statement

4.2 The applicant in a proceeding to be conducted in accordance with the Fast Track Directions must file and serve a ‘Fast Track Statement’ in accordance with the form set out in the annexure to this Practice Note. The document must, avoiding undue formality, state in summary form:

(a) the nature of the dispute;

(b) the issues that the applicant believes are likely to arise in the proceeding;

(c) the applicant’s contentions, including the material facts upon which the applicant intends to rely (which must be stated with adequate particulars), the relief claimed and the legal grounds for that relief.

Fast Track Response

4.3 The respondent in a proceeding to be conducted in accordance with the Fast Track Directions must file and serve a ‘Fast Track Response’ in accordance with the form set out in the annexure to this Practice Note. The document must, avoiding undue formality, state in summary form:

(a) the nature of the dispute;

(b) the issues that are likely to arise in the proceeding;

(c) the respondent’s response to each of the applicant’s contentions including:

(i) the material facts upon which the respondent intends to rely, insofar as they are not included in the ‘Fast Track Statement’;

(ii) a reference to whether the respondent admits, does not admit or denies each allegation made by the applicant; and

(iii) the legal grounds for opposing the relief claimed by the applicant.

34 The Annexure to CM 8 requires a Fast Track Statement and a Fast Track Response to address the following matters:

Nature of the dispute

Issues Likely to Arise

Applicant’s [or Cross-Claimant’s] Contentions*

(which should include the material facts upon which the applicant intends to rely (which must be stated with adequate particulars) and the relief claimed and the legal grounds for that relief)

Respondent’s [or Cross-Respondent’s] Responses to Contentions*

(which should include the material facts upon which the respondent intends to rely, insofar as they are not included in the ‘Fast Track Statement’; a reference to each allegation that the respondent or cross-respondent admits, does not admit or denies; and the legal grounds for opposing the relief claimed by the applicant)

* Omit if inapplicable

35 As is apparent, fast track statements and responses are used instead of, or in substitution of, pleadings. They serve the same purpose as pleadings – to clearly define the issues to be tried, and to allow the other party an opportunity to know the case against them. In my view, they fall within the “inclusory nature of the definition of “pleading”” in the Rules: cf WR Carpenter Holdings Pty Ltd (ACN 008 401 796) v Commissioner of Taxation (2006) 234 ALR 451 at [35].

36 Before leaving this aspect of the matter, it is relevant to consider the tax jurisdiction of the Court where the relevant document is an “Appeal Statement”. An “Appeal Statement” is defined in the FCR to be a statement “outlining succinctly the Commissioner’s contentions and the facts and issues in the appeal as the Commissioner perceives them”: O 52B r 5(3) of the FCR. They take the place of pleadings, but they are not, in substance, pleadings: WR Carpenter at [35]; McDonald’s Australia Ltd v Commissioner of Taxation (No 2) (2008) 69 ATR 898 at [6]; see also Pacific Exchange Corporation Pty Ltd v Federal Commissioner of Taxation (2009) 180 FCR 300 at [3] (cf Rio Tinto Ltd v Federal Commissioner of Taxation (2004) 55 ATR 321 at [22] – [27] and [58]). Their stated purpose is different – to give each party and the Court a practical understanding of the parties’ positions and summarise the essential issues on appeal: BAE Systems Australia (NSW) Pty Ltd v Commissioner of Taxation for the Commonwealth of Australia (2008) 69 ATR 567 at [19]. Further, they are not subject to the same scrutiny as a pleading: BAE at [19].

37 Contrary to the form and content of the appeal statements, Fast Track documents do not have the principal purpose or intention of making the exchange between parties merely practical or informative. The Fast Track documents operate instead of pleadings: Pt 4, Cl 4.1 of CM 8. They ensure that they clearly define the issues to be tried and allow the other party an opportunity to know the case against them. They seek to achieve those ends in the most efficient manner.

Other sources of power

38 Further, if there is doubt about the applicability of O 11 r 16 (and I do not consider there is), there are two further answers. First, this is a case in which I should direct (and out of an abundance of caution I do direct, pursuant to O 1 r 9(1)) that O 11 r 16 is to apply to the parties’ Fast Track documents, thus engaging the provisions of O 11 r 16 for the purposes of considering the Applicants’ motion: O 1 r 9(1). Secondly, I consider that s 33ZF and/or s 37P of the FCA provide the Court with power to strike out a paragraph in the AFTR. Section 33ZF of the FCA confers wide power on the Court in a representative proceeding. It provides that by the Court’s own motion, or on an application by a party or a group member, the Court may “make any order the Court thinks appropriate or necessary to ensure that justice is done” in a proceeding under Pt IVA of the FCA. Finally and no less importantly, s 37P of the FCA confers power on the Court to give directions about practice and procedure to be followed in relation to a civil proceeding before the Court, in accordance with the overarching purpose under s 37M of the FCA: see [27] above.

Applicants’ case

39 The Applicants’ application to strike out paragraph 55(c)(ii) of the AFTR was put on a number of bases. First, the Applicants contend that a review of how the Applicants put their case and how issue is joined, demonstrates that the Inglis Exercise cannot be relevant to the Applicants’ penalty argument. Further and alternatively, the Applicants contend that the Inglis Exercise is an ex post rather than an ex ante analysis. And it is for that reason that it is going to take so long and cost so much – the expert has to start from scratch and to devise an entire system for measurement of a cost never contemporaneously employed by ANZ. That is, the construction exercise does not deal with reality but is a hypothetical enquiry: a construction of a way ANZ might have sought to conduct its business and to record its expenses, but in fact never undertook. Thirdly, the Applicants contend the construction exercise does not focus on the loss that did or might flow from breach, but seeks to identify the matters set out in paragraph 55(c)(ii): see [9] above. Fourthly, the Applicants contend that the Inglis Exercise is not only extravagant, costly, time consuming and productive of delay but will not produce evidence relevant or necessary for the quelling of the penalty argument. Fifthly, the Applicants contend that ANZ’s attempt to bring in “benefits” as well as costs into the Inglis Exercise (see [9] above) demonstrates that it is irrelevant to the penalty argument especially in light of the fact that in the AFTR, ANZ used the conjunctive “and” between the costs and the benefits allegations.

40 Finally, the Applicants contended that on the available material and without further explanation, it is open to conclude that the allegations in paragraph 55(c)(ii) have been made speculatively in order to generate an issue which ANZ cannot yet advance conscientiously.

ANZ’s response

41 ANZ submits that it cannot be said that paragraph 55(c)(ii) of ANZ’s AFTR is “manifestly groundless” or “so obviously untenable that it cannot possibly succeed”. ANZ submit that Mr Inglis is not starting from scratch but is using the material already available to ANZ including existing cost allocations and “other work”. As is apparent from the earlier analysis (see [11] to [16] above), that submission hides more than it reveals.

42 As noted, ANZ divides the Applicants’ alternative penalty cases into what it describes as the Orthodox Penalty Case and the Expanded Penalty Case. The Orthodox Penalty Case relies upon the principle that the doctrine of penalties is only invoked if a clause in a contract requires a payment or transfer of property as a result of breach or termination following breach. The Expanded Penalty Case is predicated not upon a finding of breach but, instead, on allegations that the Penalty Provisions were within the area of obligation of the Applicants as it was their responsibility to ensure that they did not cause an event that would trigger the application of the Penalty Provisions (defined as a Default Event) and that the Exception Fees were out of all proportion or unrelated to the loss or damage which ANZ might have sustained by reason of the Default Event. ANZ submitted that the Inglis Exercise was relevant to the Applicants’ Orthodox Penalty Case and to the Applicants’ Expanded Penalty Case.

ANALYSIS

43 For the reasons that follow, I would strike out paragraph 55(c)(ii) of ANZ’s AFTR pursuant to O 11 r 16 of the FCR and/or ss 33ZF and 37P of the Act.

44 The facts reveal (see [11] to [16] above) that the relevant sub-paragraph of ANZ’s Fast Track Response (FTR) (and AFTR) was prepared and filed without any material that would support any of the allegations made in it. The facts described show further that the Inglis Exercise is intended to provide some opinion evidence to support the allegation. But this is after the allegation has been made in the FTR and the AFTR. The Inglis Exercise is not intended to provide any evidence of fact. By its nature, it could not and that is admitted by ANZ when it admits that it does not have any of the records that are or would be relevant to establishing the matters alleged in paragraph 55(c)(ii) of the AFTR. Rather, the relevant paragraph of the AFTR was prepared and filed in the (then unsubstantiated) hope that facts and evidence to prove facts could later be found to make out what was alleged.

45 The Applicants seek to have paragraph 55(c)(ii) of ANZ’s AFTR struck out on the basis that it discloses no reasonable defence or allegation relevant to paragraph 52 of the Applicants’ AFTS. The facts set out above (see [6] – [16] above) require that step. To “plead”, without any factual foundation for the pleading is reason enough, at least in the circumstances of this case, to conclude that the pleading is an abuse of process. It is an abuse of process because the allegations are made in the AFTR without any foundation.

46 Abuse of process is a term that can be engaged in various circumstances. The High Court examined the use of the expression in Batistatos v Roads and Traffic Authority of New South Wales (2006) 226 CLR 256 at [9] – [16], especially at [15]. The particular species of abuse with which this application is concerned is where the Rules and procedures of the Court are being engaged for purposes and in ways that are foreign to the overall purposes of the Rules of Court – the fair, just and efficient determination of matters according to an adversarial mode of procedure.

47 The inclusion of paragraph 55(c)(ii) of the AFTR is a use of the processes of the Court for purposes foreign to the underlying and informing purposes of the Rules that govern the preparation of such documents. Paragraph 55(c)(ii) seeks to create a factual controversy where the party raising that controversy has no basis for doing so.

48 That is reason enough to conclude that the impugned sub-paragraph of ANZ’s AFTR should be struck out. This conclusion is reinforced by a further consideration that emerged in the course of the hearing.

49 In paragraph 55(c)(ii) it is alleged that the quantum of the Exception Fees is not extravagant or unconscionable in comparison to two identified matters: the costs that would or might be incurred by ANZ as a consequence of, or in connection with, the occurrence of the relevant events and the benefits that would or might be received by the customer from the supply of the services supplied as a result of the occurrence of the relevant events. In the course of oral argument it emerged that despite the form of the pleading in the AFTR, ANZ in fact sought to rely on these matters as alternative or cumulative considerations (or both alternative and cumulative). As Senior Counsel conceded, “it sets out part of the bank’s case”. It is evident then that the pleading, as it now stands, must be amended if it is to articulate the case which ANZ seeks to make at trial. But tellingly, when Senior Counsel for ANZ was asked whether he had instructions to put a case in the form that he had indicated was intended to be the effect of the pleading, he answered that he did not have “separate” instructions to do so. Again, it is necessary to observe that the case for ANZ, as revealed by the AFTR, is a case which is founded, in this respect as well, on the speculative hope that someone, somewhere (it may be assumed preferably Mr Inglis and Deloitte) might come up with evidence that would support the asserted defence to the claim that now is made against ANZ.

50 To permit a pleading which seeks to raise a factual controversy to stand, when there is no factual basis on which the controversy is raised, would be to permit a new form of fishing for a defence. It should not be permitted. When it is said by ANZ that its fishing expedition would take not less than 13 months (possibly longer) and cost many many thousands of dollars there is even stronger reason to strike out the pleading as an abuse of process. ANZ seeks to subject opposite parties to an extended period of delay in the prosecution of their claim in the hope that evidence might be obtained that would support an ex post facto rationalisation of the amounts of charges that have been levied under contractual terms which ANZ set for itself.

51 On the facts and circumstances now revealed, ANZ should be shut out from litigating the issue it seeks to raise by paragraph 55(c)(ii). I refer to the facts and circumstances as they are “now revealed” because as will become evident later in these reasons for decision, the parties have identified separate questions for determination. Determination of those questions will not involve the Inglis Exercise. It is hoped that the determination of those questions will provide the parties with a proper and better assessment of critical aspects of the Orthodox Penalty Case and the Expanded Penalty Case in a more expeditious and cost effective manner. Whether, after the hearing and determination of those preliminary questions, the facts and circumstances as they are then known to the parties would justify some amendment to the pleadings is a question that cannot now be answered.

52 It is, however, important to go on to consider the other ways in which the strike out application was put.

Other Grounds – Inglis Exercise Not Relevant to the Law in Relation to Penalties

53 The Applicants submitted that paragraph 55(c)(ii) of ANZ’s AFTR incorrectly gives rise to the contention that the Inglis Exercise may be of relevance to the penalty argument: see [39] above.

54 The principles in relation to the law of penalties have been considered on a number of occasions: see Ringrow; O’Dea v Allstates Leasing System (WA) Proprietary Limited (1983) 152 CLR 359; Acron Pacific Limited v Offshore Oil NL (1985) 157 CLR 514; Interstar Wholesale Finance Pty Ltd v Integral Home Loans Pty Ltd (2008) 257 ALR 292.

55 In Ringrow, the High Court referred to Dunlop Pneumatic Tyre Co Ltd v New Garage and Motor Co Ltd [1915] AC 79 where Lord Dunedin said (at 86-87):

2. The essence of a penalty is a payment of money stipulated as in terrorem of the offending party; the essence of liquidated damages is a genuine covenanted pre-estimate of damage …

3. The question whether a sum stipulated is penalty or liquidated damages is a question of construction to be decided upon the terms and inherent circumstances of each particular contract, judged of as at the time of the making of the contract, not as at the time of the breach …

4. To assist this task of construction various tests have been suggested, which if applicable to the case under consideration may prove helpful, or even conclusive. Such are:

(a) It will be held to be penalty if the sum stipulated for is extravagant and unconscionable in amount in comparison with the greatest loss that could conceivably be proved to have followed from the breach ...

(b) It will be held to be a penalty if the breach consists only in not paying a sum of money, and the sum stipulated is a sum greater than the sum which ought to have been paid ...

(c) There is a presumption (but no more) that it is a penalty when ‘a single lump sum is made payable by way of compensation, on the occurrence of one or more or all of several events, some of which may occasion serious and others but trifling damage’: Lord Elphinstone v Monkland Iron and Coal Co (1886) 11 App Cas 332 at 342 per Lord Watson.

56 As noted, the Applicants seek to advance alternative penalty cases – the Orthodox Penalty Case and the Expanded Penalty Case: see [42] above. The Applicants submit that the High Court has not authoritatively stated that the law of penalties must be confined to the case of breach and the doctrine of penalties should, in present times, be stated in broader terms. In support of the broader application of the law of penalties, the Applicants rely on Integral Home Loans Pty Ltd v Interstar Wholesale Finance Pty Ltd [2007] NSWSC 406 at first instance where Brereton J said:

[A] penalty is a contractual liability to pay or forfeit or suffer the retention of a sum of money or property … which is agreed in advance to be payable (or forfeited or retainable), by one party to the other, upon or in default of the occurrence of an event which can be seen, as a matter of substance, to have been treated by the parties as lying within the area of obligation of the first party, in the sense that it is his or her responsibility to see that the specified event does not occur, and where the stipulated payment is out of all proportion or unrelated to the damage which might be sustained by the other party by reason of the particular occurrence or default.

In these proceedings, the Applicants accept that their pleaded case about Exception Fees “will require consideration of the metes and bounds of the [penalty] doctrine as well as its orthodox application”.

57 Strike out applications cannot and should not address questions of substance except where the result is clear beyond question: Dorrough v Bank of Melbourne Ltd (1995) 8 ANZ Ins Cas 61-290 at 76,245 and Pioneer Concrete (Qld) Pty Ltd at 172. I do not propose now to address the questions of substance raised in this case. Whether or not the Inglis Exercise is relevant to the Orthodox Penalty Case and/or the Expanded Penalty Case is an issue which might become necessary to determine at any subsequent trial. It would not be right to decide in this application whether the Applicants or ANZ have the better of the legal argument about these matters. I proceed on the basis that the arguments which ANZ seeks to advance in paragraph 55 of its AFTR are legally tenable. I express no view, one way or the other, about their ultimate correctness as propositions of law. But the propositions of law which ANZ seeks to advance in paragraph 55(c)(ii) are founded on assertions of fact and it is the absence of any factual foundation for the allegations which is of determinative significance in this application.

58 As previously mentioned, ANZ did not make any pre-estimate of loss in relation to the Exception Fees. And, of most significance for the present application, ANZ does not now have a factual basis for asserting that there was any net outgoing incurred in respect of any of the events said to found a penalty or exception fee. If there was a net outgoing incurred by ANZ in respect of some or all of the events or breaches concerned, ANZ does not now have any factual basis for identifying what the amount of that outgoing, or those outgoings may have been, whether the outgoings are considered as a global amount or are considered by being broken up by category of transaction or on some other basis.

59 The Inglis Exercise is a task that is intended to provide an opinion on those matters. It is a task that has not been done before and it is a task that, in Mr Inglis’ words, “no one can be quite sure how long, in fact, it’s going to take”. Thirteen months is merely a best estimate provided by Mr Inglis in the circumstances. It is clear that the Inglis Exercise will result in substantial delay to these proceedings. Because the outcome of the exercise is not and cannot be known now, it is not possible to say that it will produce evidence that bears upon the issues which ANZ seeks to raise in the impugned paragraph of its AFTR.

60 There is one other matter that needs to be addressed. ANZ’s arguments appeared to proceed on the premise that because a step was taken in The Office of Fair Trading v Abbey National PLC & Others [2009] UKSC 6, it is a step which is open, or must, be taken by ANZ in this case. If that is the premise, then I reject it. Each case must be considered on its facts and by reference to the circumstances at the time of any decision. In Abbey National, the contracts between the customers and the banks (and one building society) were different and, of course, did not involve the ANZ. No less significantly, the parties did not suggest to the trial judge that he could determine on the evidence before him whether the amounts levied by the banks were extravagant or unconscionable and no more than a genuine pre-estimate of loss: The Office of Fair Trading v Abbey National PLC & Others [2008] EWHC 875 (Comm) at [296]. That issue was, if necessary, deferred for consideration on another occasion: at [296].

Substantial Delay

61 In this context, ANZ submitted that the proper test to be applied in deciding whether the allegation should be allowed to stand is whether the amount charged was extravagant or unconscionable by comparison with the greatest amount that could conceivably be proved to have followed from the breach, and that the law does not require that such a comparison should have been undertaken before the contract was entered into. ANZ referred to De Francesch Builders Pty Ltd v Rile [2000] WASC 301; Yarra Capital Group Pty Ltd v Sklash Pty Ltd [2006] VSCA 109 and Clydebank Engineering and Shipbuilding Company Limited v Don Jose Ramos Yzquierdo y Castaneda [1905] AC 6. Again, it would not be right to decide in this application whether the Applicants or ANZ have the better of the legal argument about these matters. However, one must not lose sight of the fact that because ANZ did not have a pre-estimate of loss in relation to the Exception Fees, they rely upon the Inglis Exercise. As previously mentioned, an exercise that has not been done before and that, in Mr Inglis’ words “no one can be quite sure how long, in fact, it’s going to take”. An exercise that, at best guess will take a minimum of 13 months and, regardless of the outcome will result in substantial delay to these proceedings. In my view, those facts would also provide a sufficient basis for striking out the paragraph under O 11 r 16 of the FCR and further or alternatively, under ss 33ZF and 37P of the FCA: see [43] to [51] above.

Publicly available information

62 On 8 March 2011, the day after the hearing, the Applicants filed and served a folder of publicly available documents produced between 1991 and 2006 (the public material). The folder included a copy of the documents listed in paragraph (a) of the particulars to paragraph 52(c) of the AFTS.

63 One of the documents listed in the particulars was a report by the Prices Surveillance Authority dated 30 June 1995 entitled “Inquiry Into Fees and Charges Imposed on Retail Accounts by Banks and Other Financial Institutions and by Retailers on EFTPOS Transactions” (the PSA Report). The Applicants submitted that the publicly available material (including the PSA Report) provides evidence that, inter alia, some bank charges exceed the costs of providing associated bank services and that the banks have not publicly contradicted the correctness of these materials. As noted above (see [23] above), applications to strike out a pleading (or a part of a pleading) under O 11 r 16 of the FCR is limited to the face of the pleading. I do not consider that these materials assist in the resolution of the motion.

CONCLUSION

64 For those reasons, I would strike out paragraph 55(c)(ii) of ANZ’s AFTR pursuant to O 11 r 16 of the FCR and further or alternatively, ss 33ZF and 37P of the FCA. As noted earlier, that does not preclude ANZ from making application on proper material for leave to amend its AFTR to raise such an allegation if and when it is in a position to do so. At present, its current state of preparation (or lack thereof) in relation to the Inglis Exercise should not, and cannot, be permitted to delay the hearing of the core issue in these proceedings for in excess of 18 months since the issue was first raised in the hope (as ANZ would have it) that a factual controversy might be enlivened and determined in its favour. To permit such a course would be contrary to s 37M of the FCA and make a mockery of the overarching purpose which underpins the work of the Federal Court – to facilitate the just resolution of disputes according to law and as quickly, inexpensively and efficiently as possible.

B. APPLICATION FOR SEPARATE DETERMINATION OF PENALTY ARGUMENT

65 As discussed previously, the Applicants sought a separate hearing of the questions identified in [19] above, namely:

1. In respect of each of the Exception Fees, are the amounts payable upon breach, so as to be capable of amounting to a penalty?

2. In respect of each of the Exception Fees, are the amounts otherwise payable on the occurrence of an event within the area of obligation of the customer, such that they are capable of amounting to a penalty?

(the Separate Questions).

66 On 10 March 2011, in accordance with directions made at the hearing, ANZ filed a response to the Applicants’ proposed orders. ANZ’s response was that “[i]f the Court is minded to order an initial trial of separate questions as proposed by the applicants, ANZ is content with the form of the questions …, on the understanding that both questions raise issues which correspond to the penalty and fee for service issues the subject of determination in Office of Fair Trading v Abbey National PLC & Others [2008] EWHC 875”. The reference to an understanding of what is encompassed by the questions is important. It suggests that further work must be done by the parties to articulate the questions in a form that is unequivocally clear.

67 On 16 March 2011, the Applicants filed a document entitled “Exception Fees Proposed by Applicants for Initial Hearing” (the Initial Hearing Schedule). The Initial Hearing Schedule was divided into Savings Contracts, Card Contracts, Commercial Card Contracts and Business Contracts and, in relation to each category, listed the types of fees charged, the relevant penalty provision and the relevant contractual documents. Fourteen separate “cases” were identified. The Applicants also identified an example of each fee or “case” that they proposed be determined at the separate hearing. On 21 March 2011, ANZ’s solicitors responded. There were two aspects to their response. ANZ proposed revisions to four cases. ANZ also identified what it described as “lack of conformity” between (1) the Initial Hearing Schedule and the AFTS and (2) the Initial Hearing Schedule and the Agreed Bundle of Contractual Documents. ANZ informed the Court that it would raise these matters with the Applicants’ solicitors. As noted earlier, the parties have now identified and agreed examples of the various Exception Fees in the Contracts that could be heard and determined as part of an initial hearing.

68 Subsequently, on 22 and 30 March 2011, the Applicants and ANZ respectively filed a list of factual propositions that they contend would be relevant to a hearing of the Separate Questions. The lists do not coincide. The parties are in dispute. ANZ contends that if, contrary to its primary position, a trial of the Separate Questions is ordered, then the question of whether and how an initial trial should proceed ought to be the subject of submission and determination at a further directions hearing.

Should there be a trial of the Separate Questions?

69 The Applicants seek the trial of the Separate Questions pursuant to ss 33Z(1), 33ZF(1) and/or s 37P(2) of the FCA and further or alternatively, O 29 r 2 of the FCR. ANZ opposes the application. ANZ submits that the separation of claims and allegations will lead to increased costs for the parties, prolong the litigation and is an inefficient use of the Court’s resources. ANZ further submits that a separate hearing will result in the proceeding becoming fragmented, cause litigation costs and judicial resources to escalate, and will further delay the final resolution of the litigation.

70 In Reading Australia Pty Ltd v Australian Mutual Provident Society (1999) 217 ALR 495 (at [8]), Branson J summarised the principles that govern circumstances in which an order will be made under O 29 r 2 of the FCR. The principles are well known and it is unnecessary to repeat them. They have been applied in numerous cases: see, most recently, Nunagin Holdings Pty Ltd v Evertop Investments Pty Ltd (No 2) [2010] FCA 1228 at [6] – [11] and the authorities cited.

71 In my view, consistent with those principles, it is appropriate that there be a trial of the Separate Questions. The determination of the Separate Questions will not lead to a disposal of the action. They will however provide a proper basis for the parties to better assess their risk and that will inevitably contribute to a better prospect of settlement. The issues raised will be narrower because the Applicants’ other causes of action will not be addressed. If the Separate Questions are determined adversely to the Applicants, the Applicants concede that they would need to reconsider whether to continue to press the broader and other causes of action. No less importantly, it is apparent that a trial of the Separate Questions could be prepared and brought to trial in the next 12 months.

72 Contrary to the submissions of ANZ, such an outcome is consistent with and will promote the overarching purpose in s 37 of the FCA. This proceeding is one where the “utility, economy and fairness to the parties” of a trial of the Separate Questions is beyond question: cf Tepko Pty Limited v Water Board (2001) 206 CLR 1 at [170].

73 The utility of a hearing of the Separate Questions is a determination of critical issues – the proper construction of the Contracts containing the Exception Fees (Questions 1 and 2). Economy and fairness considerations may be tested by posing a rhetorical question – what happens if the Court does not separately determine the Separate Questions? The trial of the Applicants’ proceedings (customers of ANZ) is delayed for a period of years while the Inglis Exercise is completed – a construction exercise which will take at least 13 months and probably longer, may not provide the facts and evidence that ANZ speculates might exist, will be expensive and, if and when finished, will necessitate further delays while the Applicants consider what is produced and then respond. Mr Inglis acknowledged that the model he is creating may be disputed: see [16] above. He talked about amendment by the Court. He does not refer to the fact that the model (in its entirety or in part) is likely to be the subject of challenge by the Applicants. If ANZ’s submissions were accepted, it would be a classic case of the tail wagging the dog. That cannot be permitted to occur. ANZ has obligations to its customers as their banker. ANZ and its lawyers have obligations to the Applicants and the Court under ss 37M and 37N of the FCA. ANZ’s response – it will do as much as it can as quickly as it can – does not provide an appropriate answer to those obligations.

74 In those circumstances, I do not accept that a Court should wait and conduct a trial of all issues in two or three years time. It is simply an inappropriate way in which to conduct this piece of litigation. I accept that the outcome is not perfect – it will not inevitably resolve all or a substantial part of the proceeding. But it might. And to adopt the alternative, is to permit ANZ to incur substantial costs (which if it is successful it will seek to cast on the Applicants) and necessarily to delay the hearing for years when the construction exercise we are asked to wait for has never been done before and there is no certainty that it can be done.

75 I will list the matter for further directions on 5 May 2011 to address the hearing of the Separate Questions. I will direct that the Applicants and ANZ confer prior to that directions hearing to seek to agree upon the form in which the Separate Questions should be identified, on the orders that are necessary to give effect to these reasons for decision and on orders to bring on the trial of the Separate Questions without delay.

I certify that the preceding seventy-five (75) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gordon. |

Associate:

Dated: 19 April 2011