FEDERAL COURT OF AUSTRALIA

Citigroup Pty Limited v Commissioner of Taxation [2010] FCA 826

| Citation: | Citigroup Pty Limited v Commissioner of Taxation [2010] FCA 826 | |

|

| | |

| Parties: | ||

| | | |

| File number(s): | NSD 45 of 2009 | |

| | | |

| Judge: | EDMONDS J | |

| | | |

| Date of judgment: | 9 August 2010 | |

| | | |

| Catchwords: | Held: Part IVA applied. Section 204(3) of ITAA 1936 – general interest charge – whether taxpayer liable for general interest charge between date tax due and payable and date of amended determination of foreign tax credits allowed. Held: general interest charge did not apply

| |

| | | |

| Legislation: | ||

| | | |

| Cases cited: | Commissioner of Taxation v Consolidated Press Holdings Ltd (2001) 207 CLR 235 cited

| |

|

|

| |

| Date of hearing: | 8, 9, 10, 11 and 12 March 2010 | |

|

|

| |

| Place: | Sydney | |

|

|

| |

| Division: | GENERAL DIVISION | |

|

|

| |

| Category: | Catchwords | |

|

|

| |

| Number of paragraphs: | 197 | |

|

|

| |

| Counsel for the Applicant: | Mr AC Archibald QC, Mr SHP Steward SC, Ms CA Burnett | |

|

|

| |

| Solicitor for the Applicant: | Freehills | |

|

|

| |

| Counsel for the Respondent: | Mr NJ Williams SC, Ms E Collins, Mr J Kay Hoyle | |

|

|

| |

| Solicitor for the Respondent: | Maddocks Lawyers | |

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| NEW SOUTH WALES DISTRICT REGISTRY |

|

| GENERAL DIVISION | NSD 47 of 2009 |

| BETWEEN: | CITIGROUP PTY LIMITED Applicant

|

| AND: | COMMISSIONER OF TAXATION Respondent

|

| JUDGE: | EDMONDS J |

| DATE OF ORDER: | 9 AUGUST 2010 |

| WHERE MADE: | SYDNEY |

THE COURT ORDERS THAT:

2. The applicant pay the respondent’s costs, as taxed or agreed.

Note:Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

The text of entered orders can be located using Federal Law Search on the Court’s website.

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| NEW SOUTH WALES DISTRICT REGISTRY |

|

| GENERAL DIVISION | NSD 45 of 2009

|

| BETWEEN: | CITIGROUP PTY LIMITED (ABN 88 004 325 080) Applicant

|

| AND: | COMMISSIONER OF TAXATION Respondent

|

| JUDGE: | EDMONDS J |

| DATE OF ORDER: | 9 AUGUST 2010 |

| WHERE MADE: | SYDNEY |

THE COURT DECLARES THAT:

1. The applicant was not liable pursuant to s 204(3) of the Income Tax Assessment Act 1936 (Cth) (1936 Act), or otherwise, to pay General Interest Charge (GIC) for the period 1 June 2004 to 26 June 2008 on the liability to the respondent that arises by reason of s 160AN(5) of the 1936 Act on the difference between:

(a) the amount of $12,421,815, being the amount applied as a credit pursuant to ss 160AI and 160AJA of the 1936 Act in discharge of the applicant’s liability to pay income tax as assessed for the income year ended 31 December 2003 (Income Year); and

(b) the amount of $547,825, being the amount of foreign tax credits which the respondent determined by Notice of Amended Determination dated 27 June 2008 should be allowed to the respondent in respect of the Income Year.

2. The applicant was not liable pursuant to s 204(3) of the Income Tax Assessment Act 1936 (Cth) (1936 Act), or otherwise, to pay General Interest Charge (GIC) for the period 1 June 2005 to 22 April 2009 on the liability to the respondent that arises by reason of s 160AN(5) of the 1936 Act on the difference between:

(a) the amount of $12,467,760, being the amount applied as a credit pursuant to ss 160AI and 160AJA of the 1936 Act in discharge of the applicant’s liability to pay income tax as assessed for the income year ended 31 December 2004 (Income Year); and

(b) the amount of $729,096, being the amount of foreign tax credits which the respondent determined by Notice of Amended Determination dated 23 April 2009 should be allowed to the respondent in respect of the Income Year.

THE COURT orders THAT:

3. The respondent pay the applicant’s costs, as taxed or agreed.

Note:Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

The text of entered orders can be located using Federal Law Search on the Court’s website.

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| NEW SOUTH WALES DISTRICT REGISTRY |

|

| GENERAL DIVISION | NSD 45 of 2009 |

| BETWEEN: | CITIGROUP PTY LIMITED Applicant

|

| AND: | COMMISSIONER OF TAXATION Respondent

|

| JUDGE: | EDMONDS J |

| DATE: | 9 August 2010 |

| PLACE: | SYDNEY |

REASONS FOR JUDGMENT

THE ISSUEs

1 There is only one substantive issue in this case; relevantly, whether the provisions of Part IVA of the Income Tax Assessment Act 1936 (Cth) (‘the 1936 Act’) apply to entitle the respondent (‘the Commissioner’) to cancel foreign tax credits to which the applicant (‘CPL’) is otherwise entitled for the year ended 31 December 2003 (in lieu of the year ending 30 June 2004) and for the year ended 31 December 2004 (in lieu of the year ending 30 June 2005) in consequence of its participation in two Hong Kong bond transactions, the first on 31 December 2003 (‘HKBT 2003’) and the second on 2 November 2004 (‘HKBT 2004’).

2 There is no issue in this case that, absent the application of Part IVA, CPL is entitled to foreign tax credits arising out of HKBT 2003 and HKBT 2004.

3 If the Court finds that the Commissioner is entitled to cancel the foreign tax credits in reliance on Part IVA, a consequential issue arises as to whether CPL is liable to pay the general interest charge (‘GIC’) pursuant to s 204(3) of the 1936 Act or otherwise:

(1) for the period 1 June 2004 (the date that tax for the year ended 31 December 2003 was payable) to 26 June 2008 on the liability to the Commissioner that arises by reason of s 160AN(5) of the 1936 Act on the difference between:

(a) the amount of AUD12,421,815, being the amount applied as a foreign tax credit pursuant to ss 160AI and 160AJA of the 1936 Act in discharge of CPL’s liability to pay income tax as self-assessed for the year ended 31 December 2003; and

(b) the amount of AUD547,825, being the amount of foreign tax credit which the Commissioner determined by notice of amended determination dated 27 June 2008 should be allowed to CPL in respect of that year.

(2) for the period 1 June 2005 (the date that tax for the year ended 31 December 2004 was payable) to 22 April 2009 on the liability to the Commissioner that arises by reason of s 160AN(5) of the 1936 Act on the difference between:

(a) the amount of AUD12,467,760, being the amount applied as a foreign tax credit pursuant to ss 160AI and 160AJA of the 1936 Act in discharge of CPL’s liability to pay income tax as self-assessed for the year ended 31 December 2004; and

(b) the amount of AUD729,096, being the amount of foreign tax credit which the Commissioner determined by notice of amended determination dated 23 April 2009 should be allowed to CPL in respect of that year.

4 I return to this consequential issue later in these reasons.

Part IVA: Legislative Scheme and Background

5 Part IVA of the 1936 Act embodies Australia’s general anti-avoidance rules. By s 177D, Pt IVA applies to any scheme that has been or is entered into after 27 May 1981, and to any scheme that has been or is carried out or commenced to be carried out after that date (other than a scheme that was entered into on or before that date), whether the scheme has been or is entered into or carried out in Australia or outside Australia or partly in Australia and partly outside Australia, where –

(1) a taxpayer (referred to as the ‘relevant taxpayer’) has obtained, or would but for s 177F obtain, a tax benefit in connection with the scheme; and

(2) having regard to eight matters or considerations, it would be concluded that the person, or one of the persons, who entered into or carried out the scheme or any part of the scheme did so for the sole or dominant purpose of enabling the relevant taxpayer to obtain a tax benefit in connection with scheme or of enabling the relevant taxpayer and another taxpayer or other taxpayers each to obtain a tax benefit in connection with the scheme (whether or not that person who entered into or carried out the scheme or any part of the scheme is the relevant taxpayer or is the other taxpayer or one of the other taxpayers).

6 By s 177C(1), reference in Pt IVA to the obtaining by a taxpayer of a tax benefit in connection with a scheme originally read as a reference to:

‘(a) an amount not being included in the assessable income of the taxpayer of a year of income where that amount would have been included, or might reasonably be expected to have been included, in the assessable income of the taxpayer of that year of income if the scheme had not been entered into or carried out; or

(b) a deduction being allowable to the taxpayer in relation to a year of income where the whole or a part of that deduction would not have been allowable, or might reasonably be expected not to have been allowable, to the taxpayer in relation to that year of income if the scheme had not been entered into or carried out …’

Section 177C(1) further deems, for the purposes of Pt IVA, the amount of the tax benefit in each case.

7 Part IVA is not self-executing. Where a tax benefit has been obtained, or would but for s 177F be obtained, by a taxpayer in connection with a scheme (s 177C(1)) to which Pt IVA applies (s 177D), by s 177F(1) the Commissioner may –

‘(a) in the case of a tax benefit that is referable to an amount not being included in the assessable income of the taxpayer of a year of income—determine that the whole or a part of that amount shall be included in the assessable income of the taxpayer of that year of income; or

(b) in the case of a tax benefit that is referable to a deduction or a part of a deduction being allowable to the taxpayer in relation to a year of income—determine that the whole or a part of the deduction or of the part of the deduction, as the case may be, shall not be allowable to the taxpayer in relation to that year of income…’

and, where the Commissioner makes such a determination, he is required to take such action as he considers necessary to give effect to that determination.

8 On 13 August 1998 the Treasurer of the day announced that the provisions of Pt IVA of the 1936 Act would be amended with immediate effect in relation to schemes entered into after that time which are designed to acquire or generate foreign tax credits that can be used to shelter low-taxed foreign source income from Australian tax. The Treasurer went on to say:

‘These transactions generally are structured to yield little or no economic profit relative to the expected Australian tax benefits. Typically they involve the acquisition of an asset that generates an income stream subject to foreign withholding tax. An illustrative example of one such arrangement is attached.

Step 1: Foreign Resident Company (ForCo2) owes royalty payment to Foreign Resident (ForCo1) for the use of intellectual property.

Step 2: ForCo1 & AustCo enter into assignment agreement under which the right to receive the income stream in respect of the intellectual property is assigned to AusCo.

Step 3: AusCo makes payment to ForCo1 for the right to receive the income stream.

Step 4: The assigned income is paid to AusCo by ForCo2. Country B withholds 10% tax on the royalty.

AusCo includes the income stream in its assessable income. After “grossing up” to reflect the foreign tax, and claiming a deduction in respect of the cost of acquiring the income stream, only a small amount of net income is included in AusCo’s taxable income. AusCo claims a foreign tax credit for the full amount withheld by Country B. This amount is greater than the amount needed to offset the tax in respect of the net foreign income. The excess credit is used to reduce the Australian tax payable on other foreign income of the same class.’

9 This announcement found legislative expression by the addition of paras (bb) and (f) to s 177C(1), which, as outlined in [6] above, deals with what constitutes the obtaining by a taxpayer of a tax benefit in connection with a scheme for the purposes of Pt IVA and the amount of the tax benefit. Relevantly, the additional paragraphs read:

‘177C(1) Subject to this section, a reference in this Part to the obtaining by a taxpayer of a tax benefit in connection with a scheme shall be read as a reference to:

(a) ...

(b) …

(ba) …

(bb) a foreign tax credit being allowable to the taxpayer where the whole or a part of that foreign tax credit would not have been allowable, or might reasonably be expected not to have been allowable, to the taxpayer if the scheme had not been entered into or carried out;

and, for the purposes of this Part, the amount of the tax benefit shall be taken to be:

(c) …

(d) …

(e) ..

(f) in a case where paragraph (bb) applies – the amount of the whole of the foreign tax credit or of the part of the foreign tax credit, as the case may be, referred to in that paragraph.’

10 A new para 177F(1)(d) was inserted into s 177F(1) to enable the Commissioner to cancel a tax benefit which is referable, in whole or in part, to a foreign tax credit.

11 Other amendments to Pt IVA were made by the same amending legislation Taxation Laws Amendment Act (No 3) 1999 (Cth) (‘Act No 11 of 1999’), but they are not relevant for present purposes.

12 The Explanatory Memorandum (‘EM’) circulated by authority of the Treasurer, at the time the amending bill was introduced into the House of Representatives, relevantly provided:

‘Background to the legislation

2.4 Australian taxpayers are subject to Australian income tax on all Australian sourced and foreign sourced income, except where a specific exemption applies. Generally, Australian taxpayers with assessable foreign sourced income may claim a credit for tax imposed by foreign jurisdictions against their Australian income tax liability on that foreign sourced income.

2.5 Arrangements which promote the purported acquisition of foreign tax credits by Australian taxpayers have come to the attention of the Australian Taxation Office. These arrangements are structured to acquire or generate foreign tax credits to be offset against tax payable on other foreign sourced income of the Australian taxpayer.

2.6 A foreign tax credit scheme operates on the basis that foreign income is earned which gives rise to an entitlement to foreign tax credits. A scheme is entered into whereby a foreign income stream is acquired. Where the acquisition cost of the income stream is deductible, those deductions largely cancel out the foreign income received. The major portion of the foreign tax credits which relate to that foreign income stream are then available to offset tax payable on the taxpayer’s other foreign income of the same class or to carry forward any excess to future years.’

AN OVERVIEW OF Part IVA IN the Present Case

Scheme

13 In respect of the HKBTs, CPL accepts that the ‘wider scheme’ and the ‘narrow scheme’ identified by the Commissioner are each capable of constituting a ‘scheme’ within the s 177A definition of that word for the purpose of Pt IVA.

Tax Benefit

14 CPL does not contend, for the purposes of s 177C, that had it not entered into one or both of the HKBTs, it would have entered into some other transaction that would have resulted, or might reasonably be expected to have resulted, in the payment of foreign tax and an entitlement to a foreign tax credit in that amount. The Commissioner contends that it necessarily follows from this that CPL obtained a tax benefit in connection with each scheme, and that the tax benefit obtained in each case was its entitlement to the whole of the foreign tax credits resulting from each scheme. This must be right, although CPL apparently does not accept that it obtained a benefit in the sense of a reduction in the amount of tax payable by it either generally or in relation to the HKBTs. That may be so, but the fact that CPL did not obtain a benefit in the sense of a reduction in the amount of tax (foreign and Australian) payable by it either generally or in relation to the HKBTs is not relevant for the purposes of s 177C.

Dominant Purpose

15 The real issue between the parties is the conclusion that should be drawn, having regard to the eight matters or considerations in s 177D(b), as to the dominant purpose of CPL in entering into each of the schemes constituted by the HKBTs. CPL’s case is that it should not be concluded that its dominant purpose in entering into each of the schemes constituted by the HKBTs was to obtain a tax benefit; rather, it should be concluded that its dominant purpose was to obtain fee income, premium and the return on the bonds. The Commissioner’s case is that it should be concluded that CPL’s purpose in entering into each of the schemes constituted by the HKBTs was to obtain a tax benefit in the form of a foreign tax credit.

16 The Commissioner’s case against persons, other than CPL, who entered into or carried out each of the schemes or part of them, as to the conclusion that should be drawn as to their dominant purpose in doing so, appears to be no different from that alleged against CPL itself. Consequently, if it was not concluded that CPL had the requisite purpose under s 177D(b) of entering into or carrying out each of the schemes, it would follow, according to CPL, that no other relevant person had such a purpose. Again, I think this must be right; nor did the Commissioner press that if the Court should conclude that CPL did not have the requisite purpose, it was nevertheless open to the Court to find that another relevant person did have such a purpose.

The Opening Salvos

17 In opening, CPL contended that a reasonable person could not conclude that the dominant purpose of a person making an actual payment of foreign tax was the acquisition of foreign tax credits in the same amount. That is evident, so CPL contended, because no rational taxpayer would pay a dollar of foreign tax simply to avoid an obligation to pay an equal amount of tax in Australia: why, one might ask, would the rational taxpayer be anything other than indifferent as to where it paid that tax?

18 So much may be conceded where the foreign tax on the relevant income is equal to or less than the Australian tax on that income; it may also be conceded where the foreign tax on the relevant income is greater than the Australian tax on that income by reason only of a greater foreign tax rate. But where, as here, the foreign tax rate (17.5%) is less than the Australian tax rate (30%) but the foreign income base, in the years in which the relevant transactions are entered into, is considerably greater than the Australian income base by reason of the different computation of those bases, resulting in greater foreign tax payable than the Australian tax that would otherwise be payable, giving rise to excess foreign tax credits, the door of inquiry under s 177D(b) as to the dominant purpose of a person entering into a scheme giving rise to a tax benefit in the form of those foreign tax credits, is not foreclosed by recourse to arguments based on the rationality of a taxpayer. It has to be determined by reference to the relevant matters or considerations set out in s 177D(b) and one of those matters or considerations will be whether the person has other foreign source income which has not borne foreign tax, or has borne foreign tax in an amount less than the applicable Australian tax, against which the excess foreign tax credits can be applied, in whole or in part, to reduce or otherwise relieve the Australian tax liability on the other foreign source income.

19 CPL contended that the HKBTs exhibited none of the elements identified in the Treasury Press Release issued on 13 August 1998 (see [8] above) as being the target of the relevant amendments made to Part IVA by Act No 11 of 1999 (see [9] above) nor any of the elements identified in the EM circulated by authority of the Treasurer at the time the amending bill was introduced into the House of Representatives (see [12] above). The Commissioner responded by observing that such a contention sought to read the EM in substitution for the plain words of the Act, which do not contain the restriction on the operation of the section for which CPL contended. That is of course impermissible: Re Bolton; Ex parte Beane (1987) 162 CLR 514 at 518. Had the intention been to so restrict the section, it could easily have been expressed in the section itself. CPL responded by saying that it did not dispute that the text of the legislation has primacy, but that the EM aids the interpretative task of identifying the particular mischief against which the amendment was directed. The Commissioner’s suggestion that the EM be discarded entirely is, according to CPL, entirely inconsistent with the need to construe legislation by reference to its intended purpose.

20 Clearly, Pt IVA, in its form as extended by the amendments effected by Act No 11 of 1999, is not to be construed as being confined to the examples given in either the Treasury Press Release or in the EM; they are just that, examples. The examples given all involved the acquisition of an income stream which is taxed in the foreign jurisdiction on a gross basis but where, for Australian income tax purposes, the cost of acquisition is an allowable deduction thus reducing the income base to a net basis. In such a situation, the product of the foreign tax rate, even one less than the applicable Australian tax rate, and the gross income base is likely to give rise to a greater amount of foreign tax than the product of the higher Australian tax rate and the net income base, and in turn give rise to excess foreign tax credits ‘available to offset tax payable on the taxpayer’s other foreign income of the same class or to carry forward any excess to future years’.

21 As will be seen, the relevant facts relating to the HKBT’s did not give rise to any allowable deductions to CPL in Australia which were not available to it in Hong Kong, but the income base in Hong Kong in the year in which the transactions were consummated included the gross amount of the consideration received by the bond purchasing partnerships, of which CPL was a member, for the sale of the interest coupons (similar to the outcome in Commissioner of Taxation v The Myer Emporium Ltd (1987) 163 CLR 199) whereas the income base in Australia, while starting from the same point, was, by virtue of the application of the provisions of Div 16E of Pt III of the 1936 Act, spread over the life of the bonds to equate with their treatment for financial accounting purposes. This meant that the income base in Hong Kong for HKBT 2003 and HKBT 2004 in the years in which the transactions were consummated included AUD60,495,296 and AUD61,199,317 respectively, whereas no amount was included in the income base in Australia for HKBT 2003 pursuant to Div 16E in the year in which the transaction was consummated (it having been consummated on the last day of the year of income) and only AUD1,977,415 was included in the income base in Australia for HKBT 2004 pursuant to Div 16E in the year in which the transaction was consummated. It is true that over the next five years (or four years plus part of a year for HKBT 2004) the balance was brought to account pursuant to Div 16E and included in the Australian income base of CPL in those years, but my purpose in noting the consequence in the years the transactions were consummated is to illustrate that there is, indeed, a measure of common ground between the examples in the extrinsic material and the facts of the present case.

22 In opening, the Commissioner submitted that the authorities establish that the fact that a Pt IVA scheme can be justified commercially, does not prevent Pt IVA from operating, and to reason otherwise is to adopt a false dichotomy: reference was made to Commissioner of Taxation v Spotless Services Limited (1996) 186 CLR 404 at 415 – 416 per Brennan CJ, Dawson, Toohey, Gaudron, Gummow and Kirby JJ. Reference was also made to what Gummow and Hayne JJ said in Commissioner of Taxation v Hart (2004) 217 CLR 216 at [64]:

‘[A]s was held in Spotless, there is a false dichotomy between a “rational commercial decision” and “the obtaining of a tax benefit as ‘the dominant purpose of the taxpayers in making the investment’”. Pointing to the “commercial end” of the scheme reveals the adoption of the same, or at least a substantially similar, false dichotomy. The presence of a discernible commercial end does not determine the answer to the question posed by s 177D. As Hely J rightly said [Hart (2002) 121 FCR 206 at 230 [81]]:

“A particular course of action may be both tax driven, and bear the character of a rational commercial decision. The presence of the latter characteristic does not determine in favour of the taxpayer whether, within the meaning of Pt IVA, a person entered into or carried out a ‘scheme’ for the dominant purpose of enabling a taxpayer to obtain a tax benefit.”’

23 So much may be conceded, but in the very next breath, Hely J said (at [81]):

‘But nor does the fact that a taxpayer adopted one of two or more alternative courses of action, being the one that produces a tax benefit, determine the answer to that question in favour of the Commissioner: Metal Manufactures Ltd v Commissioner of Taxation (Cth) (1999) 43 ATR 375 at 427; 99 ATC 5229 at 5275 per Emmett J (on appeal Commissioner of Taxation (Cth) v Metal Manufactures Ltd (2001) 108 FCR 150; [2001] ATC 4152); Spotless at 425 per McHugh J; Inland Revenue Commissioners v Brebner [1967] 2 AC 18 at 30, per Lord Upjohn.’

This was taken up by Gleeson CJ and McHugh J in Hart, as follows (at [15]):

‘As Hely J correctly observed in the Full Court, the fact that a particular commercial transaction is chosen from a number of possible alternative courses of action because of tax benefits associated with its adoption does not of itself mean that there must be an affirmative answer to the question posed by s 177D. Taxation is part of the cost of doing business, and business transactions are normally influenced by cost considerations. Furthermore, even if a particular form of transaction carries a tax benefit, it does not follow that obtaining the tax benefit is the dominant purpose of the taxpayer in entering into the transaction. A taxpayer wishing to obtain the right to occupy premises for the purpose of carrying on a business enterprise might decide to lease real estate rather than to buy it. Depending upon a variety of circumstances, the potential deductibility of the rent may be an important factor in the decision. Yet, if there were nothing more to it than that, it would ordinarily be impossible to conclude, having regard to the factors listed in s 177D, that the dominant purpose of the lessee in leasing the land was to obtain a tax benefit. The dominant purpose would be to gain the right to occupy the premises, not to obtain a tax deduction for the rent, even if the availability of the tax deduction meant that leasing the premises was more cost-effective than buying them.’

24 What these extracts from their Honours’ reasons in Hart go to exemplify is that the task for the Court under s 177D(b) in drawing a conclusion as to the dominant purpose of a taxpayer in entering into or carrying out a scheme is not to be determined by reference to whether it represents a ‘rational commercial decision’ or that the scheme has a ‘commercial end’, any more than it is to be determined by reference to the fact, if it be a fact, that a taxpayer adopted one of two alternative courses of action, being the one that produces a tax benefit. Moreover, I do not read their Honours’ articulation of the test in Spotless at 423 namely ‘… that, viewed objectively, it was the obtaining of the tax benefit which directed the taxpayers in taking steps they otherwise would not have taken by entering into the scheme’, as embracing a ‘but for’ test; the requisite dominant purpose is not to be drawn merely because, as a matter of objective fact, it is to be concluded that ‘but for’ the tax benefit the course of action adopted would not have been adopted or that ‘but for’ the tax benefit, another course of action would have been adopted, although those considerations may be relevant to the conclusion as to the alternative postulate or hypothetical construct by reference to which the ‘tax benefit’, if any, may be measured.

25 The conclusion which the Court is required to draw under s 177D(b) is one which must be drawn having regard to such of the eight matters or considerations referred to therein as are relevant to the scheme under scrutiny (in many cases they may not all be relevant), and to no other matters. This does not exclude consideration of particular matters which fall within the wider umbrella of one or more of the eight matters or considerations referred to, but if they do not, they cannot be taken into account as part of the process of conclusion-drawing that the Court is required to undertake. In my view, this still leaves the Court with considerable latitude in the matters or considerations it can have regard to in the conclusion-drawing process.

The Facts

Introduction

26 The following glossary of terms, some of which have already been defined, will assist in a reading of these reasons, particularly the factual phase upon which I am about to embark. Hopefully, it will also simplify the narration of the transactions which, even post first blush, have an aura of complexity. To that end, I have also decided to incorporate in these reasons diagrammatic representations of the transactions, annotated by reference to the narration of them, with a view to facilitating, as best I can, a comprehension to the reader of what occurred. I am grateful to counsel for CPL for providing the Court with draft diagrammatic representations which, hopefully, I have been able to embellish without making them misleading.

Term Definition

AUD Australian dollars

BOC Bank of China (Hong Kong) Limited

BNP BNP Paribas

BPP BPP (Hong Kong) Partnership, the partners in which were CPL and OIPL

BPQ BPQ (Hong Kong) Partnership, the partners in which were CPL and OIPL

CIFS Citibank Ireland Financial Services plc, a company incorporated in the Republic of Ireland whose ultimate parent company is Citigroup Inc

Citibank NA Citibank NA is a company incorporated in the United States of America which carries on the businesses of lending money and of providing financial services throughout the world and whose ultimate parent company is Citigroup Inc

Citicorp Citicorp International Limited, a company incorporated in Hong Kong

International whose ultimate parent company is Citigroup Inc

Citicorp Life Citicorp Life Insurance Limited (formerly Metlife Insurance Limited)

CMAC Citigroup’s Capital Markets Approval Committee

CPL Citigroup Pty Limited

CPP CPP (Jersey) Limited Partnership, the partners in which were BOC and CIFS

CPQ CPQ (Jersey) Limited Partnership, the partners in which were BOC and CRC

CRC Citirealty China (BVI) Limited, a company incorporated in the British Virgin Islands whose ultimate parent company is Citigroup Inc

DBS DBS Bank Ltd, a bank incorporated in Singapore

GCS Global Capital Structuring division of Citigroup’s global group of companies

Guidelines Guidelines issued by the HKIRD on bond transactions of the kind exemplified by the HKBTs

Healthcote Healthcote Limited, a company incorporated in Hong Kong whose ultimate parent company is Citigroup Inc

HKIRD Hong Kong Inland Revenue Department

2003 HKBT or Hong Kong Bond Transaction entered into on 31 December 2003

HKBT 2003

2004 HKBT or Hong Kong Bond Transaction entered into on 2 November 2004

HKBT 2004

HKBTs HKBT 2003 and HKBT 2004

HKD Hong Kong dollars

KPMG KPMG Tax Limited, Hong Kong

Lenlyn Lenlyn Limited, a private company incorporated in Jersey

MSJ Mallesons Stephen Jaques, Sydney

OIPL Outsourcing Investments Pty Ltd, a wholly owned subsidiary of CPL

USD United States dollars

Background

27 CPL is the head company of the Citigroup Pty Limited consolidated group. It is, in turn, a member of the global group of companies headed by Citigroup Inc, a corporation listed on the New York stock exchange (the global group is referred to as Citigroup).

28 At the time the HKBTs were entered into, one of the business divisions of Citigroup was GCS. GCS was not associated with any one legal entity; its directors and other executives were located in various countries including Hong Kong, Australia, the United Kingdom, Ireland and the United States and were employed by various companies, including CPL. GCS earned revenue by arranging transactions for Citigroup’s large corporate clients.

29 Prior to the HKBTs, Citigroup had not done a Hong Kong bond transaction although a number of its clients had approached it about doing one. They were sufficiently common place that the HKIRD had issued Guidelines to assist those contemplating entering into such transactions with their advance ruling requests.

30 Citigroup hired Mr Patrick Pang to join GCS in 2002. He was employed by Citicorp International in Hong Kong. One of the reasons for his recruitment was to help Citigroup break into the Hong Kong bond transaction market, as Mr Pang had prior experience with such transactions.

31 In September 2003 Mr Pang instructed KPMG to notify the HKIRD that companies within Citigroup proposed to enter into one Hong Kong bond transaction in 2003 and two such transactions in 2004 with BOC.

32 On 24 October 2003 Mr Pang attended a ‘greenlight’ meeting in relation to the first of the proposed Hong Kong bond transactions and approval was granted to approach Group Tax within Citigroup to obtain approval to submit a Hong Kong Advance Ruling Application, and to continue to work towards getting CMAC approval. The memorandum provided to Group Tax described the transaction in summary:

‘The following describes a well-established HK structure … which, if closed, by Dec 31, 2003, would:

- raise US$56.5MM of net financing for 6 months for Citigroup, and

- deliver to Citigroup approximately US$6.4MM of pre-tax earnings (US$7.2MM received upfront less US$0.8MM of funding cost).’

It further observed that the transaction would lead to the payment of tax in Hong Kong of USD11.2 million shortly after closing.

33 That approval was apparently granted by Group Tax on 28 October 2003.

34 Also on 28 October 2003 Mr Pang was advised by Mr Chris Leung, a Citigroup employee within GCS based in Sydney, that as for the first time CGM will form part of the tax consolidated group of CPL, this meant that for Australian tax purposes a Hong Kong bond transaction ‘shouldn’t be too unusual given the tax return will contain the activities of CGM as well’.

35 On 7 November 2003 BOC advised Mr Pang that they agreed in principle to participate in the proposed transaction. On the same day KPMG submitted an Advance Ruling Request (‘Request’) to the HKIRD. The Request advised, inter alia, that BPP would be comprised of two wholly owned subsidiaries of CPL. It also advised that BPP would fund the acquisition of the bond from sources outside of Hong Kong and that BPP would not incur any funding costs. BPP would enter into a sale agreement to sell to CPP the right to all the bond interest receipts (‘the Interest Rights’) and would be subject to Hong Kong tax on those sale proceeds.

36 Appendix 3 to the Request set out the proposed cash flow and tax profile details. It advised that BPP was projected to pay tax equal to USD8,767,500 after taking into account a deduction in respect of legals of USD300,000 and CPP was projected to claim a tax deduction with a value of USD8,819,900.

37 On 24 November 2003 the HKIRD wrote to KPMG with reference to paragraph (A)(1) of Revised Guidelines, namely, ‘the bond issue must be motivated by a genuine commercial need to raise funds ...’ and observed that it appeared that the proposed transaction would not result in raising any external funds to Citigroup. This observation was undoubtedly correct on the material contained in the Request. As originally envisioned, the bond issuer was to be a third party acceptable to both Citigroup and BOC. However, as a result of a third party bank pulling out as bond issuer because it feared losing its relationship with another bank, the GCS executives decided that the bond issuer would be a Citigroup entity (Healthcote Limited) in order to complete the transaction on time and without obstruction.

38 On 2 December 2003 KPMG wrote to the HKIRD stating (or reiterating) that:

(a) The funding for the acquisition of the bond by BPP would be sourced from outside of Hong Kong and BPP would not incur any funding costs on the partnership capital or the interest free loan;

(b) the overall net funding raised by Citigroup or ‘real’ funding amounted to USD50.4 million, which was the effective loan funding taking into account all cash flows and the economic effect on the Citigroup entities;

(c) BPP and its partners were not seeking to raise funds through the transaction – it was the Issuer (Healthcote Ltd) who was seeking to take up a commercially significant amount of external debt funding. It wrote:

‘As noted, the Department in analysing the transaction, appears to have focused primarily on the partners in BPP and BPP itself. Given that the cash flows between these entities do not in themselves, show external funding raised, this may also have been the perception reached by the Department. However, it is important to note for the purpose of analysing the transaction that BPP and its partners are not seeking to raise funds through their participation in the transaction – rather, it is the Issuer, a Citigroup entity, which is seeking to take up a commercially significant amount of external debt funding based on arm’s length terms and conditions.’

(d) the partners in BPP will not carry on business in Hong Kong apart from the bond transaction, consequently the HKIRD could be satisfied that they would not be in a position to apply any losses sustained in another business carried on in Hong Kong to set off against its share of the profits from BPP.

39 On 9 December 2003 Mr Leung and Mr John Walker of GCS, Sydney, prepared a memorandum entitled ‘Hong Kong Transaction – FTC Utilisation’. The memorandum noted that the proposed transaction generated up front AUD11.95 million in Australian foreign tax credits and that CPL’s net investment in the bond principal replicated and was treated as an investment in a zero coupon bond for Australian tax purposes. On an assumption that the foreign sourced discount income was recognised on a straight line basis, the FTCs generated under the transaction would be fully applied against the foreign sourced income generated by the end of the third year.

40 On 11 December 2003 KPMG advised the HKIRD that in view of the concern raised by the HKIRD, and with a view to facilitating the completion of the transaction, the partners of BPP agreed that the estimated legal and professional fees (i.e. USD300,000) will no longer be incurred by BPP, to increase BPP’s profit tax payable from USD8,767,500 to USD8,820,000. This made the transaction slightly revenue positive for the HKIRD.

41 On 12 December 2003 the HKIRD issued a ruling pursuant to s 88A of the Inland Revenue Ordinance. In the ruling the HKIRD advised, inter alia, that the application of the taxation law meant that BPP shall be assessable on the whole of the sale of the Interest Rights as well as the fee of USD3 million and that the amount paid by CPP to BPP for the acquisition of the Interest Rights and the USD3 million fee would be deductible in full to CPP, as would the interest accrued by CPP on the limited recourse loan from the lender.

42 On 12 December 2003 Mr Walker and Mr Leung advised that they had met with all Citi-appointed directors of CPL (Roberts, Mattheson and O'Callaghan) and that it had been resolved that CPL and OIPL enter into the transactions subject to requisite internal approvals, and that approval not be sought from the two independent directors.

43 On 19 December 2003 CMAC approved the transaction.

44 The paper provided to CMAC under the heading: Transaction Rationale, stated:

‘IV. Transaction Rationale

The overall effect of the transaction is for Citigroup to raise approximately USD50 million of 5 year amortising funding through the sale of interest coupons to BoC.

From BoC’s perspective, the purpose of this transaction is to obtain an enhanced after-tax yield through its investment in the bond coupon strip. This is achieved because BoC will be entitled to an immediate tax deduction in Hong Kong for the cost of purchasing the bond coupons.

From Citigroup’s perspective, the purpose of the transaction is to realise an upfront benefit of circa USD5.5million through the sale of bond coupons to BoC, which reflects Citigroup’s share of the benefit obtained by BoC from the purchase of the coupons.’

Under heading: Transaction Economics, it stated:

‘[CPL] achieves funding of at least 75bps p.a. below its usual cost on comparable terms. In addition, an upfront fee of USD3 million will be received.’

45 The appendix to the CMAC paper states the following:

‘The Hong Kong Partnership [‘HKP’] transaction provides BoC with an enhanced after-tax yield through its investment in a bond coupon strip arranged by Citigroup. At the same time Citigroup, as the bond issuer, obtains funding at an attractive rate. The effect is to generate funding for Citigroup at approximately 75bps less than our normal cost of funds from conventional capital markets issues plus an upfront fee of US$3mm.’

..

The HKP transaction provides Citigroup with a total benefit of circa USD$5.5million, which as noted above will be received in the form of an upfront fee of USD$3million and a premium price from CPP for the coupons which additionally reduces the annual cost of the funding by a further 75bps below our typical cost of funds under comparable “plain vanilla” funding,

…

6. Other Transaction Issues

Tax Considerations

• HK profits tax: KPMG (HK) is providing a tax opinion addressing the HK profits tax implications of the transaction. Additionally, the IRD provided on 12 December 2003 a binding advance tax ruling in respect of the transaction. KPMG (HK) has provided a written confirmation that the transaction documents (currently advanced drafts) accord with the fact pattern disclosed in the IRD advance ruling.

• Australian income tax: Mallesons Stephen Jaques is providing a tax opinion addressing the Australian income tax issues. As a consequence of the transaction is that BPP will pay USD8.8million of Hong Kong tax in 2003, it is clearly vital that (a) this tax is capable of being credited against Australian tax liabilities of its partners, i.e.. CPL and OIL and (b) that projected results of Citigroup in Australia support the view that the tax will be absorbed in a relatively short period of time thereby permitting a deferred tax asset to be created for any unabsorbed credits at end-2003. [masked for legal professional privilege] the forecasts of Australian Tax and Fincon are favourable on both points.

• U.S. federal income tax: Skadden Arps is providing a tax opinion addressing the US federal income tax. Essentially this concludes [masked for legal professional privilege]’

46 The minutes of that meeting record:

‘The most important condition for the proposed transaction to work is the availability of foreign tax credit in Australia with respect to the income booked by BPP and hence CPL. Rodger Chippindale confirmed that they have received a “should” opinion from Mallesons that such tax credit would be available.’

HKBT 2003

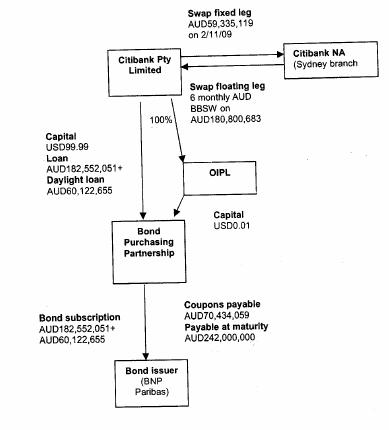

Step 1 – Bond issue

|

|

| Swap fixed leg AUD 60,495,295 on 31/12/08 |

| |||

|

| Citibank Pty Limited | (j) | Citibank NA (Sydney branch) | |||

|

| ||||||

| (j) | ||||||

|

USD99.99 Loan AUD169,504,704 |

(a) | |

100% | Swap floating leg 3 monthly AUD BBSW on AUD 169,504,704

|

| |

|

|

|

|

| |||

|

|

| OIPL |

| |||

|

|

|

|

| |||

|

|

| Capital USD0.01 |

| |||

|

| BPP Bond Purchasing Partnership |

|

| |||

|

AUD169,504,704 (Note 1) |

(c) |

|

(c) | Bond issued Coupons payable USD48,986,600 Payable at maturity AUD230,000,000 |

| |

|

| Bond issuer (Healthcote) |

|

| |||

|

AUD169,504,704 |

| (d) |

|

| ||

|

| Citibank NA (Singapore branch) |

|

| |||

Notes

(1) The balance of the bond subscription price (USD44,935,906) was funded from the proceeds of the coupon strip at step (h) below.

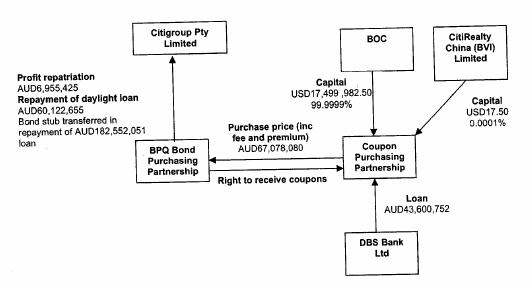

Step 2 – Coupon strip

|

| Citibank Pty Limited |

|

| BOC |

| Citibank Ireland Financial Services plc |

|

USD5,464,094 |

(i) |

| Capital USD17,639,982.36 99.9999% |

|

|

(f) |

|

Bond stub transferred in Repayment of AUD 169,504,704 loan |

|

| (f) |

| Capital USD17.64 0.0001% | |

|

|

| Purchase price (inc fee and premium) USD50,400,000 |

|

|

| |

|

| BPP Bond Purchasing Partnership | (h)

(h) |

| Coupon Purchasing Partnership |

|

|

|

|

| Right to receive coupons |

|

| Loan USD32,760,000 | |

| Balance of bond subscription USD 44,935,906 |

|

|

(g) |

|

| |

|

| Bond issuer (Healthcote) |

|

| DBS Band Ltd |

|

|

|

USD44,935,906 |

(d) |

|

|

|

|

|

|

| Citibank NA (Singapore branch) |

|

|

|

|

|

|

USD44,935,906 |

(e) |

|

|

|

|

|

|

| Citibank NA (Sydney branch) |

|

|

|

|

|

HKBT 2003 steps

47 On 31 December 2003:

(a) CPL lent AUD169,504,704 to BPP from its general pool of funds;

(b) CPL also made available a facility to BPP enabling it to draw down USD44,935,906;

(c) BPP paid AUD169,504,704 and USD44,935,906 to Healthcote in return for the issue of a five year AUD230,000,000 bond carrying the right to receive 10 fixed interest coupons payable at six-monthly intervals;

(d) Healthcote deposited AUD169,504,704 and USD44,935,906 to Citibank NA Singapore;

(e) Citibank NA Singapore deposited USD44,935,906 with Citibank NA Sydney;

(f) CPP was capitalised with USD17,639,982.36 from BOC and USD17.64 from the minority partner;

(g) CPP borrowed USD32,760,000 from DBS;

(h) CPP paid USD50,400,000 (including a fee of USD3,000,000) to BPP and in return received the right to receive the coupons on the Healthcote bond;

(i) BPP assigned the bond stub to CPL in repayment of the loan of AUD169,504,704; and

(j) CPL entered into a swap with Citibank NA, Sydney branch, pursuant to which it agreed to pay AUD60,495,296 on 31 December 2008 and in return received quarterly payments at three monthly AUD bank bill swap rate (BBSW) on AUD169,504,704.

48 The daylight loan of USD44,935,906 was not drawn on by BPP because it received USD50,400,000 from the sale of coupons of which:

(a) USD44,935,906 was paid to Healthcote as described in [47(c)] above; and

(b) the balance of USD5,464,094 was distributed to CPL (being the USD3,000,000 fee and a premium of USD2,464,094 on the sale of the coupons).

49 On 2 July 2004:

(a) DBS lent a further USD11,907,000 to a third party; and

(b) CPP assigned the right to receive the bond coupons to DBS in repayment of the two DBS loans.

HKBT 2003 Financial Consequences for CPL

50 The HKBT 2003 produced the following financial consequences for CPL (before tax is taken into account):

(a) CPL received the USD3,000,000 fee and USD2,464,094 premium in respect of the coupon sale. The total, USD5,464,094, translated into AUD7,356,211. On 30 March 2004 BPP ‘repatriated’ the profit of USD5,464,094 to CPL;

(b) CPL incurred transaction expenses of AUD863,699; and

(c) CPL paid AUD169,504,704 to acquire a bond which would pay AUD230,000,000 in five years on 31 December 2008, a return of AUD60,495,296, with that fixed return being swapped into a floating rate return equal to three monthly AUD BBSW on the amount invested of AUD169,504,704.

51 CPL submitted that it also derived a margin (or difference between the return on the bond investment taking into account the swap and the cost of funding the investment) of approximately AUD8,000,000, such that the net profit before tax approximated AUD14.5 million but the evidence in support of the funding cost, upon which the margin was calculated, was described as ‘notional’ and incapable of being ‘precisely identified’, and such a margin had not been taken into account by CPL in its decision to enter into the HKBT 2003. I return to this matter later in these reasons.

HKBT 2003 Other Benefits

52 In addition to those benefits to CPL, CPL identified that the transaction had the following benefits for the other participants:

(a) BOC was entitled to a Hong Kong tax deduction for the cost of acquiring the coupons;

(b) Citigroup:

(i) improved its client relationship with BOC and its commercial reputation in the Hong Kong finance sector;

(ii) having completed one HKBT in 2003, was in a position to complete two more in the following year;

(iii) raised five year amortising funding at market rates from DBS through Healthcote; and

(c) DBS earned a market rate of return on funds lent and an up-front loan establishment fee, also at the market rate.

Hong Kong Profits Tax

53 On 3 March 2004 the HKIRD issued an Assessment and Demand for Tax to BPP for Hong Kong Profits Tax of HKD68,558,742 (equivalent to AUD11,561,399) for the 2003/2004 Hong Kong tax year in respect of the coupon sale proceeds. On 1 April 2004 CPL remitted HKD68,558,742 (equivalent to AUD11,561,399) to Citibank HK and that amount was paid to the HKIRD on BPP’s behalf.

HKBT 2004

54 In early 2004 Mr Walker and Mr Leung began discussions with Australian banks about co-investing with CPL in the second bond transaction. It was not until June that BNP was identified as a potential issuer of the bond.

55 On 16 August 2004 KPMG sought a further Advance Ruling from the HKIRD in relation to HKBT 2004. KPMG provided further information to the HKIRD on 8 September 2004 and the HKIRD provided an Advance Ruling on 13 September 2004.

56 In an email Mr Pang sent to Mr Hal Davis and Ms Queenie Chong on 2 September 2004, he advised that one of the proposed co-investor banks (Westpac) had dropped out because they had losses in Hong Kong which made it difficult for them to have the Hong Kong tax payable creditable in Australia.

57 A CMAC meeting was held on 21 September 2004 in relation to the proposed second bond transaction. A memorandum provided to CMAC committee members dated 21 September 2004 described ‘Citigroup Benefits’ as follows:

‘The HKP transaction provides Citigroup with a total benefit of approximately A$[7.4]mm, which consists of a net upfront fee of A$[4.8]mm and a premium of A$[2.6]mm, equivalent to a margin of [30]bp p.a.’

The minutes of that meeting record under the heading ‘Motivation’:

‘CPL – Enhances relationship with BOC since the transaction provides an attractive benefit from their HK tax savings

- Australian jurisdiction chosen because of CPL is an APB23 entity whose earnings are indefinitely invested outside of the US, so does not directly affect Citigroup’s US tax return. Also, HK tax paid is neutral in HK, but a foreign tax credit can be claimed in Australia.

- Attractive upfront fees of AUD 4.8mm structuring fee and AUD 2.6mm in premium (margin approx. 30 bps p.a.)

BOC – Ability to secure in 2004, HK tax deductions based on half of bond coupons purchased, equivalent to approx. AUD 64mm x HK tax rate.

BNP – Ability to raise 3rd party funding from CPL and BOC at relatively attractive rates to their normal cost of funds.

Development Bank of Singapore (“DBS”) – Has a limited role lending to BOC for the coupon purchase. Attractively priced lending.’

Under the heading ‘Summary of Significant Issues/Concerns raised by Committee Members’ appears ‘tax’, and a note that the key tax risk is the utilisation of foreign tax credits in Australia.

58 On 24 September 2004 a meeting of the directors of CPL attended by Messrs Bunker, Craig, Matheson, Roberts, Scott and Walker resolved to approve the transaction on the basis that (i) global internal tax sign off was secured and (ii) Citibank NA in Hong Kong indemnified CPL if the tax credit was disallowed.

59 On 25 October 2004 a suite of transaction documents were apparently executed in Hong Kong and on 2 November 2004 certain funds were transferred between the participants in HKBT 2004.

60 Also around 2 November 2004 BPQ ‘repatriated’ the sum of AUD6,955,425 to CPL. On 30 March 2005 the HKIRD issued a profits tax return (final assessment and provisional payment) to BPQ recording assessable profits of HKD388,605,000 and tax payable of HKD68,005,875. As HKD68,250,000 had previously been paid on a provisional basis, a refund of HKD244,125 was due.

61 The only difference of significant between HKBT 2003 and HKBT 2004 is that the bond issuer in the HKBT 2004 was a third party, BNP, a bank incorporated in France. A third party bond issuer was critical in the 2004 transaction to ensure that CPL did not breach APRA limits on related party exposures and Citigroup had more time in developing the 2004 transaction to identify a third party bond issuer that was not subject to pressure from competitor banks.

62 The benefits of the HKBT 2004 for CPL, Citigroup and DBS were the same as those for the HKBT 2003, with the exception that, because the bond issuer was BNP rather than Citigroup raising funds from DBS, it invested funds in a bond issued by a third party and earned a market return on that bond. The benefit of the HKBT 2004 for BNP was a raising of funds at market rates.

HKBT 2004

Step 1 – Bond issue

Step 2 – Coupon strip

The Respective Cases

CPL

63 CPL’s case is that objectively considered, it should be concluded that its dominant purpose in entering into or carrying out the schemes, constituted by the HKBTs, was to obtain the fee income, premium and return on the bonds. It contends that this conclusion is compelling, especially when regard is had to the eight matters in s 177D(b). By reference to each of these matters, it makes the submissions set out in [64] to [87] below.

The manner in which the schemes were entered into or carried out

64 The manner in which the schemes were entered into or carried out was determined by the requirements of the Guidelines. They dictated the steps to be carried out, and, in large measure, the parties to them. The Guidelines thus required the use of special purpose vehicles, required that the partners in the BPP not otherwise carry on business in Hong Kong and set timing and gearing thresholds. The evident purpose of the manner in which the schemes were entered into was to secure for BOC a Hong Kong tax benefit. BOC had entered into transactions similar in structure to the HKBTs before. CPL wished to earn fee and premium income as well as the return on the bonds, court BOC's business and break a competitor bank’s monopoly in respect of this type of transaction.

65 The HKBTs were also entered into after substantial negotiation, and the obtaining of approvals and risk assessments. Thus, CPL followed its ordinary approvals process and all the constituent transactions were priced on an arm’s length basis.

66 In Commissioner of Taxation v Spotless Services Ltd (1996) 186 CLR 404, Brennan CJ, Dawson, Toomey, Gaudron, Gum mow and Kirby JJ, said at 416:

‘Much turns upon the identification, among various purposes, of that which is “dominant”. In its ordinary meaning, dominant indicates that purpose which was the ruling, prevailing, or most influential purpose. In the present case, if the taxpayers took steps which maximised their after-tax return and they did so in a manner indicating the presence of the “dominant purpose” to obtain a “tax benefit”, then the criteria which were to be met before the Commissioner might make determinations under s 177F were satisfied.’ ( Emphasis added.)

67 Their Honours went on to say of the facts of that case at 423:

‘In those circumstances, a reasonable person would conclude that the taxpayers in entering into and carrying out the particular scheme had, as their most influential and prevailing or ruling purpose, and thus their dominant purpose, the obtaining thereby of a tax benefit, in the statutory sense. The scheme was the particular means adopted by the taxpayers to obtain the maximum return on the money invested after payment of all applicable costs, including tax. The dominant purpose in the adoption of the particular scheme was the obtaining of a tax benefit ... It is true that the taxpayers were concerned with obtaining what was regarded as adequate security for an investment made “off-shore”. However, the circumstance that the Midland Letter of Credit afforded the necessary assurance to the taxpayers does not detract from the conclusion that, viewed objectively, it was the obtaining of the tax benefit which directed the taxpayers in taking steps they otherwise would not have taken by entering into the scheme.’ (Emphasis added)

68 There is no step or feature of the schemes alleged here which is explicable only or even partly by Australian tax consequences or which was inserted for Australian tax reasons, in contrast to the schemes in Spotless Services; Hart and Commissioner of Taxation v Consolidated Press Holdings Ltd (2001) 207 CLR 235. Nor has CPL taken specific steps, different from those dictated by the Guidelines, which are productive of the tax benefit which the Commissioner here seeks to cancel. Instead:

(a) The existence of the foreign tax credits is a necessary consequence of the payment of tax in Hong Kong and the application of Div 18 to that payment. CPL has not added any step to the HKBTs to cause Div 18 to so apply, or to enhance its application;

(b) the payment of tax in Hong Kong itself was a requirement of the Guidelines. It was not directed to the requirements of Div 18;

(c) CPL had no other expected foreign source income which it sought to shelter; and

(d) what attracted CPL to participate in what are otherwise wholly Hong Kong transactions was the fee and premium it received. All of the contemporaneous evidence identifies the fee and premium and the return on the bonds as the principal commercial rationale for CPL’s participation in the HKBTs.

The form and substance of the schemes

69 From CPL’s perspective, the form of the transactions was simple. It acquired two bonds and sold the right to receive the coupons on those bonds for a profit. The substance of the transactions was identical. That is, CPL in fact received fee and premium income for the sale of the coupons (which it returned as assessable income in Australia) and held the bonds to maturity, returning as income the difference between the deemed acquisition price and the face value, in accordance with Div 16E.

The time at which the schemes were entered into and the length of the period during which the schemes were carried out

70 The 2003 schemes commenced on 25 October 2003 and concluded around 2008. The 2004 schemes commenced on 31 May 2004 and concluded in 2009. CPL held the bond at the centre of each of the schemes for five years.

71 Aspects of the timing are indicative of Hong Kong tax requirements: hence, ensuring BOC obtained deductions that it could use to reduce its assessable profits in Hong Kong for the years ended 31 December 2003 and 31 December 2004.

72 Nothing in the timing or duration of the schemes supports a conclusion that a person entered into any of the alleged schemes for the dominant purpose of obtaining foreign tax credits for CPL. The 2003 HKBT was entered into at a time when it was expected that the Australian Citigroup consolidated group would have very little foreign source income.

The result in relation to the operation of this Act that, but for this Part, would be achieved by the schemes

73 Under Div 18, CPL obtained a FTC of AUD11,561,339 in relation to the HKBT 2003 and a FTC of AUD11,520,171 in relation to the HKBT 2004; neither would have been obtained absent the schemes.

74 But the fact that the taxpayer pays less tax under the scheme than under an alternative does not compel the conclusion that Pt IVA applies: Hart per Gleeson CJ and McHugh J at [15] and Gummow and Hayne JJ at [52], [53]; Macquarie Finance Ltd v Commissioner of Taxation (2005) 146 FCR 77 per Hely J at [232].

75 More fundamentally, the result obtained under the Act (being a reduction in domestic tax) cannot be considered in isolation. Each dollar of reduced liability flowed from the fact that CPL was required to pay a dollar of tax in Hong Kong. The payment of this foreign tax did not lead to a greater saving of tax in Australia. From CPL’s perspective, there was no reduction in its fiscal liability. From inception these were always going to be Hong Kong transactions which, as a condition for their performance, required the payment of Hong Kong tax. That payment, if anything, accelerated what would otherwise have been in Australia a payment of tax over five years.

76 This demonstrates that, objectively, the appeal of the HKBTs to CPL lay in the fee and premium income that CPL would derive, not in any Australian income tax consequence.

77 Further, an objective view of the facts shows that CPL’s foreign tax credits were never presented as a commercial or accounting benefit by CPL or any other person. The amount recorded in CPL’s accounts, on the basis of which the transactions were approved and undertaken, was CPL’s profit from the fee, premium and margin income.

Any change in the financial position of the relevant taxpayer that has resulted, will result, or may reasonably be expected to result, from the schemes

78 From the HKBT 2003, CPL derived a pre-tax profit of approximately $14.5 million, including a $4,038,772 fee and the $3,317,305 coupon premium and an approximately $8 million margin on the bond (less transaction costs of approximately $1 million). From the HKBT 2004, CPL could have expected, at the time it entered into the transaction, to derive a pre-tax profit of approximately $15 million, including a $4,517,812 fee, a $2,437,642 coupon premium and an approximately $9 million margin (less transaction costs of approximately $1 million).

79 The fee and premium from each transaction were described by Citigroup executives as attractive returns, and measured well against Citigroup’s Return on Tangible Equity rates.

80 The schemes were pre-tax positive for CPL. This is not a case such as Spotless where the rate at which the taxpayer earned interest in the Cook Islands was lower (even before Cook Islands withholding tax was subtracted) than the rate the taxpayer could obtain in Australia, or Hart where the taxpayer borrowed at a higher than market rate, with the difference in each case being compensated for by the tax benefit.

Any change in the financial position of any person who has, or has had, any connection (whether of a business, family or other nature) with the relevant taxpayer, being a chance that has resulted, will result or may reasonably be expected to result, from the schemes

81 Under the HKBT 2003, CPL raised USD44,935,906 from third party financiers at market rates, amortising over five years.

82 Under the HKBT 2004, BNP Paribas raised $242,000,000 for five years at market rates and a fee of $674,706.

83 Under the HKBTs:

(a) DBS lent funds at market rates and earned a loan establishment fee;

(b) professional advisers earned fee income; and

(c) BOC obtained Hong Kong tax deductions.

84 The transactions were pre-tax positive for every person other than BOC, and BOC’s Hong Kong deduction does not attract Pt IVA (it was also in conformity with a HKIRD Ruling).

Any other consequence for the relevant taxpayer, or for any person referred to in subparagraph (vi), of the scheme having been entered into or carried out

85 After CPL entered into the HKBT 2003, it was better placed to enter into and enjoy the benefits of two more similar transactions.

86 Citigroup considered that its participation in the HKBTs improved its relationship with BOC in Hong Kong, and that Citigroup’s reputation in the Hong Kong financial market was enhanced.

The nature of any connection (whether of a business, family or other nature) between the relevant taxpayer and any person referred to in subparagraph (vi)

87 Some of the parties to the HKBTs are in the same global group as CPL, but that is unsurprising given CPL’s GCS Division spanned legal entities. All the transactions were priced at arm’s length. Any connections between CPL and the other parties are neutral in arriving at a conclusion as to a person’s dominant purpose for entering into one of the schemes.

The Commissioner

88 The Commissioner’s contentions in response are embodied in [89] to [120] below:

The manner in which the schemes were entered into or carried out

89 The Commissioner contended that CPL’s contention that the manner in which the schemes were entered into or carried out were determined by the Guidelines was incorrect in a number of respects. Perhaps the most significant error is the inference (indeed the evidence of one former Citigroup employee) that it was a requirement of the Guidelines that the bond purchasing partnership be a foreign entity (that is, not from Hong Kong). There was no such requirement. It was a requirement of the Guidelines that the bond purchasing entity (or if it was a partnership, the partners) be a special purpose taxable entity that is not otherwise carrying on a business in Hong Kong. This requirement was capable of being satisfied by a non-trading Hong Kong registered entity. The selection of a foreign entity (CPL) is explicable by the taxation consequences of the selection. This is because, as explained below, from the bond purchasing entity’s perspective the transaction was loss making – the profit derived was less than the taxation liability. A foreign entity with appropriate recognition of tax paid overseas in the form of credits was essential to offset that loss.

The form and substance of the schemes

90 The Commissioner did not accept that the form of the transactions was simple. The complexity of the structure in fact adopted could have been avoided if, for instance, CPL was genuinely desirous of taking funds from its general pool and investing them elsewhere with a view to profit. The complex structure adopted was essential to both generate the desired tax deduction for BOC and to ensure that the BPP’s post-Hong Kong tax loss on the transaction was more than offset by a tax benefit in Australia.

91 The substance of the transaction was the acquisition of a tax deduction for BOC in Hong Kong, paid for by the BPP, and then the reimbursement of that cost to CPL as a member of the BPP plus a true ‘margin’ through a tax benefit in Australia. The Div 16E income expected to be returned in Australia over the life of the bond was wholly offset and hence neutralised by the funding cost deductions.

The time at which the schemes were entered into and the length of the period during which the schemes were carried out

92 While the bonds had a nominal life span of five years, in reality the transactions were one day transactions for CPL. CPL ensured, through its entry into the swaps, that the income to be accrued over the life of the bond was cancelled out by the value of its deduction in respect of payments made to Citibank NA.

93 Contrary to CPL’s submission, HKBT 2003 was not entered into at a time when it was expected that the CPL consolidated group would have very little foreign source income. The objective facts at the time of entering into HKBT 2003 were that Citicorp Life had returned foreign source income of AUD51 million in 2002; from 1 January 2003 Citicorp Life formed part of the MEC group headed by CPL; and in the year ended 31 December 2003 CPL itself had foreign source income in the form of interest income of AUD32,003,170 and Citicorp Life had foreign source income in the amount of AUD98,344,349.

94 CPL’s ‘expectation’ case is solely based upon incorrect information provided by Ms Marckatos to Ms Tan in December 2003. The evidence adduced in respect of the conversation between Ms Tan and Ms Marckatos falls short of establishing that Ms Tan positively expected that the CPL consolidated group would have no foreign source income in the 2003 year. However, even if she did, evidence of the expectation of one CPL employee is irrelevant in circumstances where the employee engaged on a fact finding mission in respect of such foreign source income has not been called, and clearly there would have been any number of employees who knew that Citicorp Life had returned substantial foreign source income in 2002 and continued to derive substantial foreign source income.

95 As at 31 December 2003 CPL had derived a pre-tax profit from HKBT 2003 of AUD6,493,512. It had paid tax in Hong Kong of AUD11,561,339. It had a liability for taxation in Australia of AUD1,948,058, but had foreign tax credits of AUD11,561,339. In other words, as at 31 December 2003 CPL had suffered a post tax loss of approximately AUD5 million. However, it had the balance of the foreign tax credits to be offset against its other foreign source income.

96 HKBT 2004 was entered into at a time when it was expected that the CPL consolidated group would have significant foreign source income. The objective facts at the time of entering into HKBT 2004 were that CPL had returned foreign source income of AUD137 million in 2003; from 1 January 2003 Citicorp Life formed part of the MEC group headed by CPL; and in the year ended 31 December 2003 CPL itself had foreign source income in the form of interest income of AUD32,003,170 and Citicorp Life had foreign source income in the amount of AUD98,344,349.

97 The evidence of Ms Tan was that the exercise she performed was dictated by the relevant financial accounting standard in relation to deferred tax assets. She knew that CPL had returned significant foreign source income in 2003 and had no reason to believe that significant foreign source income would not be received in the 2004 year. The objective facts at the time of entry into HKBT 2004 are that CPL had derived, and continued to derive, substantial foreign source income.

98 As at 2 November 2003 BPQ had derived a pre-tax profit from HKBT 2004 of AUD6,955,425. However, it expected to have, and did in fact have, an obligation to pay tax in Hong Kong of AUD11,520,171. CPL paid that tax on behalf of BPQ, and for the year ended 31 December 2004 returned AUD6,955,425, in Australia for which it incurred a liability for taxation in Australia of AUD1,867,008. As against that, CPL had foreign tax credits of AUD11,520,171. In other words, as at 2 November 2004 CPL knew it would have a post tax loss of approximately AUD4.6 million in relation to BPQ. However, it had the balance of the foreign tax credits to be offset against its other foreign source income.

99 In light of the implementation date of HKBT 2004, it can hardly be suggested that, having returned other foreign income of AUD137,693,730 four months earlier, CPL did not expect at that time that it would have any foreign source income against which the foreign tax credits arising out of HKBT 2004 could be applied.

The result in relation to the operation of this Act that, but for this Part, would be achieved by the schemes

100 It is common ground that the result obtained under the Act but for the application of Pt IVA was a reduction in CPL’s domestic tax; in both years, the reduction was in excess of AUD9.6 million, equal to the balance of the foreign tax credits available for each year.

Any change in the financial position of the relevant taxpayer that has resulted, will result, or may reasonably be expected to result, from the schemes

101 CPL initially contended that HKBT 2003 produced the following pre-tax financial consequences of the scheme for CPL – first, the USD3 million fee plus the USD2,464,094 in respect of the coupon sale, a total of USD5,464,094; and second, a return of AUD60,495,296 (AUD230 million less AUD169,504,704) which was swapped into the floating rate return equal to three monthly AUD BBSW on the sum of AUD169,504,704.

102 CPL next contended that the net profit before tax to CPL was or could have been expected to be approximately AUD14.5 million, comprising the fee and premium income of USD5,464,094 (AUD7,356,211) plus a margin (or difference between the return on the bond taking into account the swap and the cost of funding the investment) of approximately AUD8 million, less expenses of AUD862,699.

103 This alleged ‘margin’ is not referred to in the contemporaneous documents. Even if there was a margin, as Mr Walker admitted such a margin would have been earned on any investment by CPL of the funds employed, so that is not a change in the financial position that results from the scheme, since it would have occurred if the scheme had not been entered into. It is axiomatic that ‘the time for testing the dominant purpose must be the time at which the scheme was entered into or carried out...’: CPH Property Pty Limited v Commissioner of Taxation (1998) 88 FCR 21 at 42, per Hill J; Vincent v Commissioner of Taxation (2002) 124 FCR 350 at 372 [93] per Hill, Tamberlin and Hely JJ. It is also based on the evidence of Mr Russell, which in this respect is entirely inadmissible. While he is not put forward as an expert witness and was not apparently provided with the expert’s code of conduct he purports to give opinion evidence on a critical matter which is not based on his specialised knowledge, but rather upon his recollection (as the former audit partner) of CPL’s ‘accounting records’. Those records have not been produced and he does not explain what he means. Further, the assumption he makes is not made good by the lay evidence filed on CPL’s behalf.

104 The ‘return’ of AUD60,495,296 was swapped into three monthly AUD BBSW on the sum of AUD169,504,704 with Citibank NA. The sum paid to Citibank NA pursuant to the swap, that is, AUD60,495,296, was claimed as an allowable deduction. The amount CPL was obliged to pay Citibank NA exactly equalled the Div 16E income. The BBSW received by CPL under the swap was returned as income and CPL now says that its funding costs were approximately AUD8 million less than the BBSW income.

105 It follows that to be persuaded that CPL made or expected to make a margin on the bond of approximately $8 million the Court needs to be persuaded that the cost of funding the investment was about $8 million less than the BBSW received. The allegation is that CPL withdrew the funds loaned to BPP from its ‘general pool of funds’. The Commissioner submitted that the Court cannot reasonably be persuaded of either of these matters for essentially two reasons. First, there is no reference in the contemporaneous documentation to any expectation of such a margin, let alone of that magnitude. The first suggestion of such a margin is in the affidavits prepared for this hearing. Second, the evidence sought to be adduced by CPL to establish that in fact such a margin was made is speculative, unconvincing and (in the case of Mr Russell, assuming that his affidavits are proposed to be read) inadmissible.

106 It follows that the net profit before tax was at best the fee and premium income less the ‘expenses’, the sum of $6,493,512.

107 While BPP returned a profit in Hong Kong and funds were ‘repatriated’ to CPL in Sydney, in substance HKBT 2003 was a loss making transaction for BPP and CPL as the majority partner in the BPP in substance suffered an economic detriment as a consequence of the transaction. The plain fact of the matter is that the amount the partnership was obliged to pay by way of tax in Hong Kong substantially exceeded the amount of the ‘profit’ it made on the transaction. The tax in Hong Kong was akin to an additional transaction expense for BPP and hence CPL.

108 The Hong Kong tax paid equivalent to AUD11,561,339 was in fact paid by CPL. In other words, while a ‘profit’ was returned in Australia of AUD7,356,211 representing the profit made on the sale of coupons plus the structuring fee, Hong Kong tax equivalent to AUD11,561,339 plus transaction costs totalling AUD862,699 was then paid by CPL a day or two later. This means that the economic detriment to CPL amounted to AUD5,067,827, until account is taken of the foreign tax credits of AUD11,561,339.

109 The foreign tax credits of AUD11,561,339 were applied in Australia as follows:

(a) AUD1,948,054 against tax otherwise payable on the profit made by BPP of AUD6,493,512 (AUD7,356,211 less transaction cots of AUD862,699);

(b) AUD9,613,285 against tax otherwise payable on other foreign sourced income (which, as noted earlier, was substantial).

110 In other words, but for Pt IVA, the HKBT 2003 scheme delivered a financial consequence for CPL of a reduction in it’s fiscal liability of AUD9,613,285. Put another way, but for the scheme, CPL would have been liable to pay additional tax of AUD9,613,285 in Australia in respect of its other foreign income.