FEDERAL COURT OF AUSTRALIA

Betfair Pty Ltd v Racing New South Wales [2010] FCA 603

|

Citation: |

Betfair Pty Ltd v Racing New South Wales [2010] FCA 603 |

|

|

Parties: |

||

|

File number: |

NSD 1566 of 2008 |

|

|

Judge: |

PERRAM J |

|

|

Date of judgment: |

16 June 2010 |

|

|

Catchwords: |

||

|

Legislation: |

Australian Jockey Club Act 1873 (NSW) Betting Tax Act 2001 (NSW) ss 5A, 8, 9, 10 Constitution ss 90, 92 Copyright Act 1968 (Cth) Corporations Act 2001 (Cth) Crimes Act 1900 (NSW) ss 316, 545B Crimes (Sentencing Procedure) Act 1999 (NSW) s 17 Federal Court of Australia Act 1976 (Cth) s 50 Gaming Control Act 1993 (Tas) ss 3, 76I, 76N, 76VA, 76ZDB, 76ZDD, 150A, 150AC Gaming Control Regulations 2004 (Tas) r 5A Harness Racing Act 2002 (NSW) Harness Racing Act 2009 (NSW) ss 5, 9 Interactive Gambling Act 2001 (Cth) ss 5, 8A, 15, 15A Racing Administration Act 1998 (NSW) ss 4, 16, 18, 24, 27, 32A, 33, 33A, 33B, 33D, 33E; Sch 1 [1] Racing Administration Amendment Act 2008 (NSW) Sch 1[11] Racing Administration Regulation 2005 (NSW) rs 14, 16, 25 Racing Legislation Amendment Act 2006 (NSW) s 2 Recovery of Imposts Act 1963 (NSW) s 4 State Revenue Legislation Amendment (Budget) Act 2002 (NSW) Sch 2 Statute Law (Miscellaneous Provisions) Act 2008 (NSW) Sch 2[2] Statutory and Other Offices Remuneration Act 1975 (NSW) Sydney Turf Club Act 1943 (NSW) s 3 Thoroughbred Racing Act 1996 (NSW) Pt 2A; ss 4, 5, 6, 7, 10, 13, 15, 29, 29M, Totalizator Act 1997 (NSW) ss 6, 11, 13, 14, 15, 17, 21A, 69 Trade Practices Act 1974 (Cth) s 52 Unlawful Gambling Act 1998 (NSW) ss 4, 8, 9 |

|

|

Cases cited: |

Automatic Totalisators Ltd v Federal Commissioner of Taxation (1920) 27 CLR 513 cited Bath v Alston Holdings Pty Ltd (1988) 165 CLR 411 applied Betfair Pty Ltd v Racing New South Wales (No 1) [2009] FCA 111 cited Betfair Pty Ltd v Western Australia (2008) 234 CLR 418 applied Campomar Sociedad Limitada v Nike International Ltd (2000) 202 CLR 45 cited Castlemaine Tooheys Ltd v South Australia (1990) 169 CLR 436 applied Cole v Whitfield (1988) 165 CLR 360 applied Fingleton v Lowen (1979) 20 SASR 312 cited IceTV Pty Ltd v Nine Network Australia Pty Ltd (2009) 239 CLR 458 cited James v Cowan (1930) 43 CLR 386 cited Public Services Board (NSW) v Osmond (1986) 159 CLR 656 cited Sportsbet Pty Ltd v New South Wales [2010] FCA 604 cited Telstra Corporation Ltd v Hurstville City Council (2002) 118 FCR 198 cited Telstra Corporation Ltd v Phone Directories Co Pty Ltd (2010) 264 ALR 617 cited Tom & Bill Waterhouse Pty Ltd v Racing New South Wales (2008) 72 NSWLR 577 cited Totalisator Agency Board v Wagner [1963] WAR 180 cited Victoria Park Racing and Recreation Grounds Co Ltd v Taylor (1937) 58 CLR 479 cited |

|

|

|

|

|

|

Texts cited: |

J Kirk, “Constitutional Guarantees, Characterisation and the Concept of Proportionality” (1997) 21 Melbourne University Law Review 1 R I Palgrave (ed), Dictionary of Political Economy (1896) vol 2 C Ward, “The margin of appreciation in Australian Jurisprudence” (2003) 23 Australian Bar Review 189 |

|

|

|

|

|

|

Date of hearing: |

18-20, 23-24, 26-27, 30 November & 1-2 December 2009 |

|

|

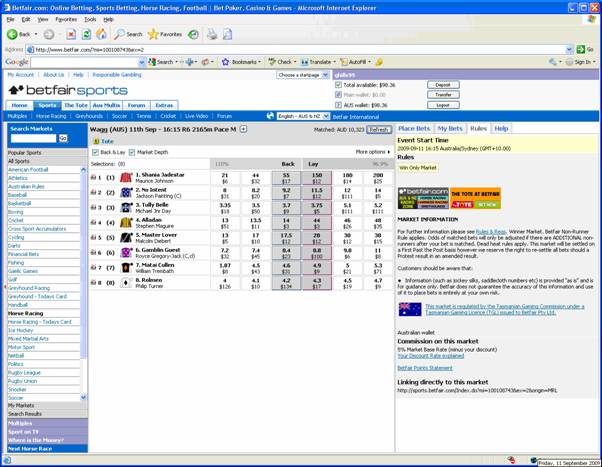

|

|

|

|

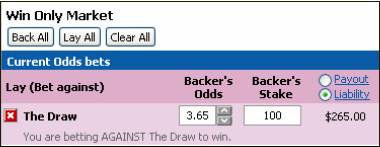

Date of last submissions: |

4 June 2010 |

|

|

|

|

|

|

Place: |

Sydney |

|

|

|

|

|

|

Division: |

GENERAL DIVISION |

|

|

|

|

|

|

Category: |

Catchwords |

|

|

|

|

|

|

Number of paragraphs: |

335 |

|

|

|

|

|

|

Counsel for the Applicant: |

Mr A Robertson SC with Mr A J Meagher SC, Ms K C Morgan |

|

|

|

|

|

|

Solicitor for the Applicant: |

Gilbert & Tobin |

|

|

|

|

|

|

Counsel for the First and Second Respondents: |

Mr J T Gleeson SC with Mr S A Kerr SC, Mr J Emmett and Mr S Robertson |

|

|

|

|

|

|

Solicitor for the First and Second Respondents: |

Yeldham Price O'Brien Lusk |

|

|

|

|

|

|

Counsel for the Intervenor: |

Mr J Kirk with Ms A Mitchelmore |

|

|

|

|

|

|

Solicitor for the Intervenor: |

New South Wales Crown Solicitor's Office |

|

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 1566 of 2008 |

|

BETFAIR PTY LTD Applicant

|

|

|

AND: |

RACING NEW SOUTH WALES First Respondent

HARNESS RACING NEW SOUTH WALES Second Respondent

ATTORNEY-GENERAL (NEW SOUTH WALES) Intervenor

|

|

JUDGE: |

|

|

DATE OF ORDER: |

16 JUNE 2010 |

|

WHERE MADE: |

SYDNEY |

THE COURT ORDERS THAT:

1. The application be dismissed.

2. These orders not be taken out without the leave of a Judge of the Court.

3. Vary all pre-existing orders made pursuant to s 50 of the Federal Court of Australia Act 1976 (Cth) to permit the publication of these reasons.

4. Stand over for further directions at 9.30 am on 24 June 2010.

Note:Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

The text of entered orders can be located using Federal Law Search on the Court’s website.

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

NSD 1566 of 2008 |

|

BETWEEN: |

BETFAIR PTY LTD Applicant

|

|

AND: |

RACING NEW SOUTH WALES First Respondent

HARNESS RACING NEW SOUTH WALES Second Respondent

ATTORNEY-GENERAL (NEW SOUTH WALES) Intervenor

|

|

JUDGE: |

PERRAM J |

|

DATE: |

16 JUNE 2010 |

|

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

These reasons for judgment are divided as follows:

|

I |

Introduction...................................................................................................... |

[1] |

|

II |

Backing and laying............................................................................................ |

[6] |

|

III |

Bookmakers..................................................................................................... |

[15] |

|

IV |

Totalizators....................................................................................................... |

[30] |

|

V |

Betting Exchanges............................................................................................. |

[38] |

|

VI |

The relationship between Betfair and the respondents........................................ |

[60] |

|

VII |

The race fields fee............................................................................................. |

[70] |

|

VIII |

Betfair’s case and the principal questions to be resolved.................................... |

[101] |

|

IX |

Is the fee discriminatory?................................................................................... |

[118] |

|

X |

Is the fee protectionist?..................................................................................... |

[154] |

|

XI |

Are the motives of the respondents relevant to s 92?.......................................... |

[207] |

|

XII |

Is the fee reasonably and appropriately adapted to some legitimate end?............ |

[238] |

|

XIII |

What relief, if any, should be granted?............................................................... |

[253] |

|

XIV |

Particular findings of fact................................................................................... |

[262] |

|

XV |

Rulings on interlocutory matters......................................................................... |

[324] |

I – Introduction

1 Section 92 of the Constitution provides, relevantly, that “trade, commerce and intercourse among the States…shall be absolutely free”. Perhaps somewhat unfortunately, the provision does not descend to the more mundane topic of the identity of the mischief from which the founding fathers were so very emphatic that interstate trade, commerce and intercourse was to be kept “absolutely free”. Early in the Federation’s history the obscurity of the immunity thus conferred was famously lamented by Rich J in James v Cowan (1930) 43 CLR 386 at 422 who only wished that:

Some hint at least might have been dropped, some distant allusion made, from which the nature of the immunity intended could afterwards have been deduced by those whose lot it is to explain the elliptical and expound the unexpressed.

2 For most of the last century s 92 was a continuing source of uncertainty. That state of affairs, however, came to an end with the High Court’s unanimous decision in Cole v Whitfield (1988) 165 CLR 360 which held that s 92 is concerned to stamp out discriminatory protectionism by the States and the Commonwealth within Australia. The Federation arising from the Constitution was, therefore, not merely a political union but was to be seen as a commercial union as well. As the editor (1877-1883) of The Economist noted in 1896 “[f]ree commercial intercourse, indeed, seems one of the most distinctive marks of national unity” (Sir Robert Inglis Palgrave (ed), Dictionary of Political Economy (1896) vol 2, pp 45-46, cited in Betfair Pty Ltd v Western Australia (2008) 234 CLR 418 at 455 [23] per Gleeson CJ, Gummow, Kirby, Hayne, Crennan and Kiefel JJ) (hereafter “Betfair”).

3 The Constitution itself, by s 90, banned the States from levying their own excise taxes and thereby did away with the potential for explicitly protective tax regimes on the free trade of goods. But s 92 goes far beyond the trading in goods and applies to all forms of trade, commerce and intercourse among the States and so operating extirpates from the Federation the almost infinite variety of forms by which protectionism may manifest itself.

4 The applicant, Betfair, conducts business from Hobart in Tasmania. Its complaint is against the regulators of thoroughbred racing and harness racing in New South Wales who are the first and second respondents and to whom I shall refer as “RNSW” and “HRNSW” respectively. It claims that a particular fee imposed by RNSW and HRNSW for the right to use “race fields information” discriminates against it and in favour of a New South Wales trader, TAB Limited (“the TAB”), and that the fee does so in a way which is properly to be characterised as protectionist. It seeks relief from the obligation to pay the fee and the return to it of so much of the fee as it has already paid. The questions to be determined are many but the important ones are:

(a) does the fee discriminate against Betfair and in favour of the TAB?

(b) if it does, is the fee to be seen as protectionist in character?

(c) if it is, is there some legitimate purpose which the fee can be seen as serving?

(d) if there is, are the means adopted to achieve that end reasonably appropriate and adapted for that purpose?

(e) can the intentions of officials of RNSW and HRNSW who made the decision to impose the fee be relevant to the questions posed by s 92 of the Constitution?

(f) if they can be, did some or all of the members of the boards of the regulators put the fee in place intending it to hinder Betfair from competing with the TAB?

(g) assuming all of these questions are answered in Betfair’s favour are RNSW and HRNSW obliged to refund the fee?

5 I have come to the clear conclusion that the race fields fee imposed by the respondents discriminates in favour of the TAB and against Betfair. However, I have also come to the conclusion that Betfair has failed to prove that the fee is protectionist in nature. The authorities indicate that protectionism is generally to be demonstrated by a close examination of the competitive consequences of the impugned measure. In this case, Betfair eschewed showing that the adverse discriminatory effect which the race fields fee undoubtedly burdens it with is protectionist in kind. It did not seek, for example, to demonstrate that the discriminatory adverse effect of the fee decreased some competitive advantage it had over the TAB consisting of the fact that it was required to pay lower betting taxes in Tasmania than the TAB was obliged to pay in New South Wales. Nor did it seek to show, for example, that the discriminatory effect of the fee might be seen as neutralising some competitive disadvantage that the TAB might have had by reason of its need to incur the substantial expenditure in running a retail network when Betfair was an internet operator. Nor did Betfair allege, as it was alleged in Sportsbet Pty Ltd v New South Wales [2010] FCA 604 (hereafter “Sportsbet”), that the fee was discriminatory in a protectionist sense because the TAB had the fee paid by it returned or that NSW on-course bookmakers were also relieved of their obligation to pay the fee. In the end, Betfair’s case was simply that the fee discriminated against it. Although it formally alleged protectionism it was plain from the way its case was pleaded that it meant by that allegation no more than that the fee discriminated against it. The authorities required Betfair to allege and prove discriminatory protectionism; in the end, all that it proved was discrimination. Structured in that way, Betfair’s case was bound to fail and I so conclude. The application should be dismissed.

II – Backing and laying

6 The fee which lies at the heart of this case is a fee imposed upon persons who derive revenue from those members of the public who gamble on the outcome of horse races and harness races held in New South Wales. In order to understand the fee it is necessary, in the first instance, to understand some basic concepts involved in betting and, in particular, the difference between the bet involved in “backing” an event and the bet involved in “laying” or accepting such a bet from another person.

7 A wagering operator, such as a bookmaker, accepts wagers from members of the public who wish to bet on the outcome of an event. Those persons are generally referred to as “punters”. The punter will place a bet with the wagering operator and will put up an amount of money known as the stake which he or she agrees will become the operator’s in the event that the final outcome is not the one backed by the punter. On the other hand, should the event backed by the punter also be the final outcome then the operator, in turn, agrees to return the stake to the punter together with an agreed return on the stake, sometimes referred to as the “price” or the “premium”.

8 In this litigation the parties have referred to the kind of wager placed by the punter in such a situation as a “back bet” and the kind of wager accepted by the operator as a “lay bet”. The parties were in agreement on the pleadings that a back bet was a bet that something would occur whereas a lay bet was a bet that something would not occur. That view of things is consistent with some statements made by the High Court in Betfair 234 CLR at 465 [52]. Similar was the description of backing and laying contained in Betfair’s “Punters’ Guide”, which it publishes on its website and which was placed into evidence. It explained the difference between the positions as following:

9 For reasons which will become apparent later in this judgment, I do not think that either of those descriptions fully captures the relevant difference. There are a number of critical matters which deserve emphasis. First, a back bet is not inevitably linked to whether an event occurs. A back bet can just as easily be made that an event does not occur. For example, one might place a back bet with a bookmaker that a particular test match is not drawn or that a particular tennis player does not proceed to the finals of a tennis tournament. As such, the laying of a bet is not inevitably linked to the non-occurrence of that event as the laying of the bets corresponding to the above examples reveals. Thus the bookmaker who accepts a bet from a punter that a test match is not drawn is, in substance, betting that the game is drawn. The essence of the difference between backing and laying is not therefore winning and losing or occurring or not occurring. Rather, it is that the backer and the layer always have opposite positions on an event’s outcome: if the punter backs a particular outcome then the layer is betting on the opposite outcome. However, that statement says nothing about whether the outcome is an event of occurrence or non-occurrence.

10 Secondly, the critical difference between a back and lay bet lies not in the occurrence or non-occurrence of an event but rather in the terms of the single contract which the lay and the back bet together constitute. The punter, on the one hand, promises to give the layer the stake on one outcome. The layer, on the other hand, promises to return the stake with a premium on the stake on the opposite outcome. These are two ends of the same contract but, as such, they are structurally and financially different. The backer’s maximum exposure under the single contract is the amount of the stake whereas the layer’s maximum exposure is the amount of the premium. On the other hand, the backer’s maximum gain is the premium whereas the layer’s maximum gain is the amount of the stake. What flows from that observation is that the backer’s profits are a function of the price but his losses are not whereas the layer’s losses are a function of price but his profits are not.

11 What is important to grasp is that every back bet is connected to a lay bet and vice versa and that together such pairs form one single contract. There is no such thing as a back bet disconnected from a lay bet just as there is no shadow without light. When an offer to lay an event is accepted by a backer (or an offer by a backer accepted by a layer) a wagering contract comes into existence between the two of them. Each such contract contains terms dealing with the stake placed by the backer with the layer and the premium offered on the stake in return. But there is no amount of money staked by the layer as there is in the case of the backer. It is possible to imagine a world in which layers do put up a stake with backers consisting of the premium which is returned to the layer if the backer loses and combined with the backer’s original stake which is already being held by the layer. However, there was no evidence before me that any wagering market operates in that mirror image way. No doubt, this is because the layers tend to be professional businesses (such as bookmakers) whereas backers tend to be members of the public in respect of whom questions of credit may arise.

12 I emphasise these matters because the submissions of all parties in this litigation often assumed that there was such a thing as a layer’s stake. For example, in paragraph 104(e) of RNSW and HRNSW’s closing submissions it was said that Betfair received “both the backer’s stake and the layer’s stake” and in paragraph 180 of the closing submissions on behalf of New South Wales it was said:

The one qualification is that it is only back bet turnover that is counted. In other words, half of the transactions engaged in by Betfair are not subject to the turnover fee. And that is so even though that consumer on the lay side themselves opened their wallet to Betfair, where they might otherwise have spent the money on other wagering products with other wagering operators who would have had to pay the fee. The qualification is thus which favours Betfair.

13 The consumers on the lay side (scil. the layers) did not open their wallets. They receive the backer’s stake. Half the transactions were not overlooked. Every lay bet is the other half of a back bet.

14 It is necessary then to turn to the differing wagering operators which exist. For present purposes, there are three kinds of operators: bookmakers, totalizators and betting exchanges. It is useful to deal with bookmakers first.

III – Bookmakers

15 The issues in this case are concerned with the operation of New South Wales law. Whilst the law of that State does define the term “bookmaker” in various statutes, none of those definitions contributes much in the way of content. Section 4 of the Racing Administration Act 1998 (NSW) helpfully defines a bookmaker to include a person who carries on the business of a bookmaker or endeavours to gain a livelihood by betting or making wagers. The same definition can be found in s 4 of the Unlawful Gambling Act 1998 (NSW) and s 3 of the Sydney Turf Club Act 1943 (NSW).

16 In Betfair (234 CLR at 465 [51]) the plurality adopted a statement by Zelling J in Fingleton v Lowen (1979) 20 SASR 312 at 314 as to the original meaning of the expression “bookmaker”:

A bookmaker was one who made up a book on all the horses in a given race, adjusting the odds and the volume of money he took on any particular horse, so that if his calculations were correct, at the end of the race, no matter what horse won, the book would show a profit to the bookmaker.

17 The evidence before me took the matter a little further. All parties agreed that in substance bookmakers generally engaged in fixed price betting which meant that the price to be paid to the successful punter was agreed at the time the bet was placed rather than being determined after the winner was ascertained (as happens with pari-mutuel or totalizator betting discussed infra at Section IV). The parties were also in agreement that bookmakers generally sought to make their money through what is known as “overround”. To understand the nature of overround one needs to understand the relationship between prices and odds. A bookmaker and a punter may agree that the wager on a particular horse is to be at a price of 5-1. What this means is that if that horse wins the race then the bookmaker will return the punter’s stake to him together with a premium which is five times the stake. Thus, if a punter places a $100 fixed price bet on Dred Scott with a bookmaker at 5-1 and Dred Scott wins the race then the bookmaker will pay the punter $600 consisting of the return of the $100 stake initially advanced by the punter to the bookmaker together with a $500 premium (being five times the stake of $100).

18 Yet another common way of expressing the same relationship is as a price expressed as a dollar rate of return such that when the rate is multiplied by the initial stake the product is the full payout by the bookmaker to the punter including the return of the initial stake. Using the above example, the price would be $6 which tells one that a winning $100 bet results in a payout of $6 x $100 = $600. Of course, so expressed, the price does not express the profit made for it includes the initial stake in the payout. To obtain the rate of profit one needs to deduct $1 from the price.

19 Another way of looking at the odds offered is to convert them into a number between 0 and 1 which has the appearance of being a measure of probability. Thus 5-1 means 1 chance in 6 (i.e. 1 chance of winning in (5+1)) or 0.1666. This can also be expressed as a percentage, 16.66%. Generally, the probability implied by a price is its reciprocal (ie. $6 implies a probability of 1/6 = 0.1666 or 16.66%). Necessarily, the price is the reciprocal of the probability expressed as a decimal. For example, race odds of 9-1 suggest one chance in ten of winning, i.e. 10%, or, in decimal notation, 0.1. The corresponding price is 1/0.1 = $10.

20 Odds may be short or they may be long. Thus a horse running at 50-1 is at long odds as it implies a probability of winning of 1 in 51 and correspondingly a high price of $51 (the inverse of the decimal odds). Further, odds may be expressed in favour (“odd on”) or against (“odds against”) a particular event. “Odds against” are displayed, for example, as 6-1 and their conversion into price and probability has been demonstrated above. Such odds are expressed this way as the first number (six) represents the number of possible outcomes that are against the backed event, whilst the second number (one), represents the number of possible ways the backed outcome may arise (i.e. six against, one on). Conversely, “odds on” are displayed, for example, as 15-1 on, which reflects a 1 in 16 chance of the backed event not being the final outcome (i.e. 15 on, one against). Their expression this way is for the same reason given above, that is, the second number (one) represents the number of possible outcomes against the backed event, whilst the first number (15), represents the number of possible ways the backed event may arise. This can also be expressed as a price by adding one to the offered odds of 15-1 on (that is 1 + (1/16)), resulting in a price of $1.06. This format is often used to express short odds on an event, for instance, the odds that a favourite horse will win a race. Lastly, since the price is always $1 plus a positive number of cents (no matter how short the odds are) the price must always be more than $1. The $1 itself, of course, reflects the 100% rate of return the backer gets on his own stake (if he or she wins). Correspondingly, there is no theoretical upper bound capping the level to which prices may go.

21 I turn then to the question of overround. The business of bookmaking is largely arithmetical and not complex. At its core is a straightforward concept, an explanation of which follows. It is to be noted that the explanation is simplified and, to an extent, idealised.

22 Let it be assumed that there is a three horse race between Grumpy, Dopey and Doc. It is a certainty that one of these horses will win the race so the probability of that event occurring is 100%. If the bookmaker ensures that all of the prices he offers imply probabilities which add up to 100% and he ensures that his exposure for each horse – that is, how much he will have to pay if the particular horse wins – is the same then he will neither win nor lose but will break even. However, to ensure that his exposure to the risk of each horse winning is the same he must adjust the size of the bet he takes to the price he is offering on that horse, for his exposure is the product of the price he has offered and the stake wagered. Thus, if the bookmaker assigns probabilities to Grumpy, Dopey and Doc of 50%, 35% and 15% then the prices will be $2.00, $2.86 and $6.67 (that is 1/0.5, 1/0.35 and 1/0.15). He will be indifferent to the outcome of the race (a state of affairs referred to as having a “square book”) if he budgets on a payout on any horse of $100. To square the book he must accept, therefore, bets totalling $50 on Grumpy ($2 x $50 = $100), $34.96 on Dopey ($2.86 x $34.96 = $100) and $14.99 on Doc ($6.67 x $14.99 = $100). The following table indicates the outcome:

|

Horse |

Implied probability |

Price |

Wagers accepted |

Potential payout |

|

Grumpy |

50% |

$2.00 |

$50.00 |

$100 |

|

Dopey |

35% |

$2.86 |

$34.96 |

$100 |

|

Doc |

15% |

$6.67 |

$14.99 |

$100 |

|

Total |

100% |

|

$99.95 |

|

|

Maximum payout |

|

|

|

$100 |

23 In this case, a guaranteed loss of five cents occurs generated by rounding errors. The book thus depicted is essentially square. If the bookmaker then structures his book such that the sum of the implied probabilities exceeds 100% this will imply from the backers’ perspective acceptance by them (viewed as a class) of a set of prices which means that the probability that one of the horses in the race will win is more than 100% (when, in fact, it is precisely 100% – one of the horses is bound to win). Viewed from that perspective such a set of prices ensures a guaranteed loss by them and, for that reason, a guaranteed profit by the bookmaker. One intuitive explanation for why this is so may be gleaned by observing that a person who bets $1 on the toss of a coin at a price implying a probability of 66.6%, that is, a price of 2-1 on or $1.50, will lose in the long run. Each successful toss of a coin will net 50 cents but each unsuccessful toss will lose $1. Since, in the long run, these outcomes are equally frequent a guaranteed loss ensues.

24 The amount by which the bookmaker’s probabilities exceed 100% is known as the overround. These concepts are a little abstract but are clearer if an example is given. If the overround on the race above is 4% then the bookmaker’s odds will need to total 104%. If the chances of Doc in the above example are increased from 15% ($6.67) to 19% ($5.26) this will achieve an overround of 4% as the following table illustrates:

|

Horse |

Implied probability |

Price |

Wagers accepted |

Potential payout |

|

Grumpy |

50% |

$2.00 |

$50.00 |

$100 |

|

Dopey |

35% |

$2.86 |

$34.96 |

$100 |

|

Doc |

19% |

$5.26 |

$19.01 |

$100 |

|

Total |

104% |

|

$103.97 |

|

|

Maximum payout |

|

|

|

$100 |

25 The bookmaker therefore is bound to make $3.97. It will be seen that the $3.97 profit arises from adjusting the price of Doc downwards from $6.67 to $5.26 which suggests the greater the bookmaker’s overround the lower his prices will be. In a betting ring bookmakers compete with each other and are exposed to twin opposing forces. Their own commercial interests will naturally incline them to increase their overround and, therefore, decrease their prices. But punters in the ring are inclined to self-interest in the opposite direction and are inclined to place their wagers with the bookmaker offering the highest price.

26 The example just given is very simplified and not just because there are only three horses. In practice, bookmakers are confronted with problems of liquidity, volume and sometimes the placing of bets with them by punters which exceed the volumes implied by their prices. The above example is to be taken only as a general indication of what overround is. When those kinds of considerations intrude the process becomes more complex. However, the above basic outline suffices for the purposes of these reasons.

27 There are a number of different kinds of bookmakers. In New South Wales the conduct of fixed price betting by bookmakers was originally confined to racecourses. Off-course bookmaking did occur but was a criminal enterprise. In 1994 a decision was made to permit bookmakers who were physically located at racecourses to accept bets by means of a telephone from customers not at the track. Later there came to be permitted corporate bookmakers who could take bets from customers off-course via the telephone or the internet. However, the law of New South Wales required (and still requires) that such businesses be conducted only from racecourses and only during the time at which the race meeting being held at the racecourse was underway: s 8 Unlawful Gambling Act 1998. The practical effect of that prohibition is that bookmakers are confined to racecourses and to trading times associated with race meetings. Unlike many countries, there are no shop-front bookmakers in New South Wales.

28 Independently, in the mid-1990s the Northern Territory and the Australian Capital Territory established different regimes governing “stand up” bookmakers at racecourses and corporate bookmakers. The latter were licensed to conduct an operation 7 days per week from a racecourse, providing wagering markets via the internet and telephone.

29 Having described the nature of the bookmaking business it is useful then to turn to the dominant form of wagering operator in this country, the totalizator.

IV – Totalizators

30 Totalizator betting or pari mutuel betting is a system of betting in which persons wishing to back an event or contingency do so by placing the bet with an operator who then pools all of the bets together. When the outcome is known the operator deducts a commission and the remainder of the pool is divided amongst the successful punters. The prices which result are not fixed and necessarily cannot be known before the outcome of the event in question. In that sense totalizator betting differs in obvious ways from the fixed price wagering offered by bookmakers.

31 Pari mutuel means mutual bet and reflects its French origins. Pari mutuel betting was invented in about 1867 by the Catalan, Joseph Oller, who is perhaps better known as one of the founders of the Moulin Rouge, a fact disappointingly omitted from the parties’ submissions. As a style of betting it spread rapidly around the world. In Totalisator Agency Board v Wagner [1963] WAR 180, Hale J referenced (at 190) the then Oxford English Dictionary whose entry for the word cited a passage from the Standard newspaper for 7 September 1881, which had stated that “Pari mutuels would perhaps be better understood by English people under their other appellation of totalisators, instruments much in vogue on the race-courses of Australia”. One of the practical difficulties originally encountered in operating pari mutuel betting was the extensive calculations which needed to be made. The totalizator was originally a mechanical computer directed to that end and was invented in about 1913. The first was apparently installed at the Ellerslie Racecourse in Auckland, New Zealand. The calculations involved in the process of conducting a totalizator are significant in number although not in sophistication. In an age prior to the rise of the computer, elaborate machinery was necessary to carry them out which gave rise to what Hale J described in Totalizator Agency Board v Wagner [1963] WAR at 191 as “a highly complex machine”. As calculating dividends from pools has become less onerous the word “totalizator” now does little more than denote a pari mutuel arrangement.

32 Consistent with the concept of pari mutuel s 6 of the Totalizator Act 1997 (NSW) defines “totalizator” in s 6 in these terms:

For the purposes of this Act, “totalizator” means:

(a) a system used to enable persons to invest money on events or contingencies with a view to successfully predicting specified outcomes of those events or contingencies and to enable the money left after the deduction of commission to be divided and distributed among those persons who successfully predict those outcomes, and

(b) any instrument, machine or device through or by which the system is operated.

33 The two key concepts here are the deduction by the totalizator operator of what s 6 calls a “commission” and the division of the remaining pool amongst the successful punters. The industry refers to the commission in s 6 as the “take out”.

34 There are similarities between a lottery and a totalizator. In both cases the punters share amongst themselves their pooled contributions and in both cases the operator takes out a commission prior to distribution. However, in Automatic Totalisators Ltd v Federal Commissioner of Taxation (1920) 27 CLR 513 at 518 per Knox CJ, Gavan Duffy and Starke JJ, the High Court concluded that a lottery was a game of “chance and nothing but chance” whereas the distribution of moneys to punters on a totalizator was not “determined purely by chance”. Another view might be that in a lottery all outcomes are equally probable but this is not so with animal racing.

35 There are three kinds of totalizators being conducted on New South Wales horse races. First, there are on-course totalizators operated by racing clubs such as the Australian Jockey Club (AJC), which operates Randwick Racecourse, or the Sydney Turf Club (STC), which operates Rose Hill Racecourse. The TAB is also permitted to operate on-course totalizators: s 15 Totalizator Act 1997. Secondly, there are totalizators operating from interstate; thirdly, there is a single off-course totalizator operated by the TAB. This third totalizator is a monopoly; s 14(2) of the Totalizator Act 1997 prohibits the grant at present of any more than one licence to conduct an off-course totalizator in NSW. Additionally, when the TAB operates its off-course totalizator on an event which is also being offered by an on-course totalizator, the latter acts as the TAB’s agent and pays any money collected by it into the TAB’s totalizator: s 17(3) Totalizator Act 1997. Thus, because bookmakers in New South Wales are confined to racecourses and are only able to operate during race meetings the TAB’s off-course totalizator monopoly is not only free from competition from other on-course totalizators but also any intrastate off-course bookmakers.

36 The TAB was formerly a government monopoly but was privatised in 1998. It is presently owned by Tabcorp Holdings Limited. The TAB is the dominant operator in New South Wales. For those unfamiliar with the size of the racing industry the amounts of money involved may be surprising. The Australian Racing Fact Book for 2007/2008 reveals that the total wagering turnover on thoroughbred racing in New South Wales for the 2007 and 2008 racing season was $3,505,370,000 of which $2,767,870,000 was placed through the off-course totalizator conducted by the TAB in New South Wales; put another way, 78.96% of all money wagered on New South Wales thoroughbred races was wagered on the TAB’s off-course totalizator. These figures leave out of account the betting on harness racing and greyhound racing. A report prepared for persons including HRNSW by BIS Shrapnel Pty Ltd entitled “Revenue Outlook for TAB Limited” suggested that in the preceding three years the TAB had collected 95% of the amount wagered on New South Wales thoroughbred, harness and greyhound racing across Australia and overseas, although it is not clear whether this related solely to the operations of its off-course totalizator.

37 The TAB’s off-course totalizator is a very significant undertaking. It is conducted through 1,971 retail agencies throughout the State and its green and yellow livery is a familiar sight in retail shopping areas. Moreover, it has a significant presence in the public hotels of New South Wales in which it often maintains betting facilities and television screens offering live footage of racing events. Because it is not lawful to conduct a totalizator or the business of a bookmaker from anywhere but a racecourse in New South Wales, it follows that the TAB has an unchallenged high street monopoly on betting shops. The encounter of that high street monopoly with the internet sets the stage for the present litigation.

V – Betting Exchanges

38 As has already been noted the business of bookmakers is the making of an overround by, in theory, the judicious laying of back bets. This endeavour is not always successful. On occasions, the bookmaker may be driven by the market to have a negative overround, or in other words, a guaranteed loss. At other times, the bookmaker may accept a wager which unbalances his book on account of its size leading to the possible result that if the wager succeeds the stakes collected on the remaining bets will not be sufficient to cover the payout arising on that event. It is not unusual in such situations for a bookmaker to seek to remove or ameliorate that risk by himself making a wager on the same event such that the amount to be won on the second wager will cover the outstanding liability on the first. This practice is called laying off. Its relevance for present purposes is to demonstrate that the business of a bookmaker includes not only the laying of back bets from punters but also, when the pressing need arises, the making of back bets with other bookmakers or sometimes totalizators.

39 A betting exchange, by contrast, involves the idea of providing a facility to punters so that they can bet with each other on a fixed price basis. Although totalizator betting is, in a sense, a mode of wagering where the punters are betting with each other because the successful punters take their winnings from the bets placed by other punters, they are not doing so as a matter of contract and the prize cannot be known until the identity of the winning horse is ascertained and the number of successful punters determined.

40 If punters are permitted to lay bets from each other then the possibility of matching back bets with lay bets becomes possible. A betting exchange is a facility whereby persons wishing to wager on the outcome of an event may make and accept offers to do so. Since each wager has a backer and a layer, the offers which may be made are necessarily offers to back and offers to lay. An offer to lay an occurrence would be open to acceptance by a person who wished to back that occurrence. Correspondingly, an offer to back an occurrence would be open for acceptance by a person wishing to lay it. The exchange model facilitates the making and acceptance of such offers.

41 Those familiar with the operations of futures and options markets will notice a similarity between these two kinds of operations. For example, a futures trader may offer to sell 1000 tonnes of wheat at $200 per tonne on 1 August 2010. Such an offer is an offer to sell. It is open for acceptance by a person who may wish to buy at that price and at that time. On the other hand, a purchaser may offer to enter into a contract to buy wheat at a different price and time. Such an offer is an offer to buy.

42 The making of back and lay bet offers is similar to such offers to buy and sell, although not identical. Both are offers to enter into contracts – one a contract of sale, the other a contract of wager – both inherently have two parties – the vendor and purchaser, the backer and layer. Both contractual positions have fluctuating values depending on an uncertain outcome in the future. If the price of wheat in the above example is trading above $200 per tonne on 1 August 2010 then the trader who previously agreed to sell the wheat will make a loss and the counterparty a corresponding profit. But this will not be known until 1 August 2010. Similarly, the precise value of a back bet of $100 at 6-1 on Crayfish will not be known until the outcome of the race.

43 Likewise, in both situations a party may exit his or her position by entry into the opposing contract. The wheat trader may crystallise his position in the example above by entering into a contract to buy on 1 August 2010 what he has offered to sell under the first contract. Once he has done that the price of wheat on 1 August 2010 will no longer be of concern to him. This is because his net economic position will be driven entirely by the difference between his agreed sale price (under the first contract) and his agreed purchase price (under the second contract). So too, a person who has entered into a wagering contract to back Equine Derivative on the first at Randwick on Saturday for $10 may crystallise his position by laying a bet on the same horse. In both situations, the crystallisation which occurs by entry into the opposing contract may result in a profit or a loss depending upon the price at which the second contract is entered into. But the example illustrates the structural similarity between the two arrangements nevertheless. There are of course obvious differences between futures and wagering contracts. For instance, the final payoffs for both parties on a wagering contract are distinctly known at the time of entry whilst the same is not true for parties to a futures contract. This significantly differentiates the potential profit and liability of a backer and layer of a bet as opposed to counterparties on a futures exchange, the latter of whom can theoretically face infinite profit or loss.

44 As with a futures exchange, a market on events will not operate efficiently, or probably at all, unless counterparty risk is removed. In a futures exchange, this is done by the exchange operator assuming the position of principal on all contracts and ensuring that its members maintain with it sufficient security to cover their outstanding positions (most commonly accomplished by requiring sufficient funds to be kept in a “margin account”). No different principle pertains to the case of a betting exchange. Since punters may be in different jurisdictions, the model is unlikely to work unless the exchange operator assumes the position of principal on all wagers. For those reasons at least one model of a betting exchange will have the following features.

(a) a market will be provided on a particular event upon which wagering is to take place, e.g. the winner of a horse race, the outcome of a tennis match, the outcome of a federal election, the place getters on a horse race and so on;

(b) the exchange operator will facilitate through some kind of platform the making of offers to lay and back bets and also for the acceptance of such offers as have been made;

(c) the exchange operator will assume the position of principal on all successfully formed wagers;

(d) the exchange operator will ensure that it is sufficiently in funds from the punters using the exchange to avoid credit risk to it; and

(e) the exchange will make its profit by charging, on some basis, a commission on transactions.

45 Having sketched the essential features of a betting exchange, it is useful then to note some similarities and differences between, on the one hand, betting exchanges and, on the other, bookmakers and totalizators. One thing which may at once be observed is that by reason of its position as a principal, the exchange operator enters into both back and lay wagers. As has already been noted, the nature of a bookmaker’s business also involves entry into back and lay wagers. However, this does not mean that the business of a betting exchange is the same as the business of a bookmaker. The bookmaker lays bets and backs bets with a view to generating an overround. A betting exchange, on the other hand, backs and lays in precisely equal proportions and is not seeking its profit by way of overround. Its profit derives not from winning more than it loses – as a bookmaker does – but from charging a commission. For the same reasons that a futures exchange cannot really be said to be in the business of trading futures contracts on its own behalf, so too a betting exchange is not in substance a bookmaker.

46 A comparison with the business of a totalizator operator results in a similar conclusion. It is true that Joseph Oller’s insight was to facilitate betting between the punters pari mutuel in an economic sense. But in a contractual sense the punters never wager with each other on a totalizator and, on any view, no punter enters, either contractually or financially, into the lay side of any wager. However, just as a betting exchange charges a commission, for instance, on the winnings of successful punters, so too a totalizator can be seen as doing something similar. The pool collected by a totalizator operator goes to the winning punters but only after the totalizator’s commission has been deducted. In a sense, a totalizator and a betting exchange have those two things in common: the earning of positive amounts of revenue does not depend on the outcome of the event and both effectively charge a commission which is deducted from the winnings of punters.

47 Having made those general observations about betting exchanges, it is useful to turn to the case of Betfair itself. In Australia, Betfair operates an exchange along the lines set out above. Its commission is charged upon the net winning positions held by customers in any particular market. It offers markets on sporting and other events and, in particular, offers markets on New South Wales horse races both of the thoroughbred and harness racing kind. For a given race there is a market conducted for the winner of the race. There is also usually a separate market conducted for place getters.

48 In keeping with the exchange model punters may back or lay an event. This they may do either by making offers to back or lay an event or by accepting offers which have already been made to back and/or lay an event by other punters. The exchange is operated over the internet and may be accessed via www.betfair.com.au. Betfair Australia itself is a joint venture essentially between Crown Ltd and the English company Betfair Group Ltd, whose wholly owned subsidiary, The Sporting Exchange Ltd (TSEL), was the innovator of internet-based betting exchanges. That group, using the Betfair brand, conducts an international betting exchange the website for which is connected directly to www.betfair.com.au. Generally, all exchange operations on Australian events are done through Betfair’s Australian website.

49 To utilise the exchange a customer must first be registered which involves a verification of identification procedure and the allotment of a user name and password. Before any betting can take place a customer must put his or her account in credit and funds thus deposited are held in trust by a company related to Betfair as security for exposures entered into by the customer. The exchange does not permit the entry into wagers for which sufficient funds are not held. All customers agree to be bound by the rules of the exchange. When a customer views the market for a particular event he or she sees a screen as follows (being a market on the 4.15 pm harness race at Wagga Wagga on 11 September 2009):

50 There are a number of features of the screenshot to be noted. The blue lined boxes indicate back wagers which are presently on offer (that is being layed) and which may be accepted by clicking on the relevant blue lined box. It is implicit that the blue lined boxes actually indicate offers by persons to lay a bet for it is the acceptance of a lay offer which gives rise to a back bet. The price on the blue lined box is the offered price which, if one is so minded, can be converted into odds and probabilities – $2 is 1:1 (50%), $3 is 2:1 (33.3%) and so on. The figure underneath the price in each blue lined box is the total amount which the layer or layers have indicated a willingness to accept as a stake. There may in fact be multiple layers at one price and the exchange may match a single lay offer with many back bets or a vice versa (just as in a futures market).

51 The boxes running to the left are also offers, but it will be seen, the prices trend down. The existence of these boxes indicates the depth of the market. On the right hand side there appear pink lined boxes which are lay wagers presently capable of acceptance. Again, those pink lined boxes reflect offers to back which have been made. The boxes to the right show increasing prices. Useful comparison with what is going on may be made with the system of bids and offers obtaining on stock exchanges. In many markets, particularly the larger ones, these prices are given to moving at considerable speed, with smaller price intervals between each box as well as greater amounts capable of being accepted by a backer or layer.

52 On the top right hand corner there is a figure following the word “matched” which indicates the amount staked in wagers which have been formed. It will be noted that the prices on the back side are lower than those on the lay side. Keeping in mind that the offers on the back side are made by layers and that the offers on the lay side are made by backers it will be seen that layers offer lower prices than the backers. This accords with common sense. The layers profit from lower pay-outs; the backers from higher ones. The percentage figures appearing on the backers’ and layers’ side are a measure of the probabilities implicit in the prices presently being offered. In the example shown, the prices being offered by the layers (that is the back prices on offer) reflect a probability exceeding 100%. On the other hand, the prices being offered by the backers (that is the lay prices on offer) reflect a probability below 100%. This curious result indicates that, taken as a class altogether, the layers are bound to make a profit and the backers, again taken as a class altogether, a loss at the indicated market prices. This phenomenon – which appears in most of the markets conducted on the exchange – was discussed during argument but there was no evidence which explained why it occurred.

53 When a back bet is accepted, the customer is presented with the following screen (being a market on a cricket match between Australian and South Africa):

54 When a lay bet offer is accepted (on the same market) the customer is presented with the following screen:

55 As has previously been noted, the mechanics of lay and back bets are different. In particular, there is no stake put up by the person laying a bet although Betfair does require there to be sufficient funds to cover any liability.

56 Not every offer is matched. Sometimes, particularly in the smaller markets, there is no liquidity. At other times the price offered is not consistent with the then prevailing market price and will languish unaccepted. Although the platform permits the placing of bets over the internet there is also a facility for the placing of bets by telephone. That facility is provided presumably to permit betting on events which are already in play such as cricket test matches. For reasons which are not altogether clear the Interactive Gambling Act 2001 (Cth) prohibits betting on events which are “in play” – that is, actually underway – where the bets are placed via the internet but not where they are placed via the telephone: ss 5(1), 5(3)(a), 5(3)(aa), 8A(1), 8A(2), 15 and 15A.

57 Betfair operates from premises in Glenorchy, north-west Hobart. It holds a gaming licence from the State of Tasmania issued under the Gaming Control Act 1993 (Tas). That licence permits Betfair to conduct its betting exchange from various locales including Glenorchy. The precise terms of that licence are set out in Section XIV below.

58 Nice questions may be posed by Betfair’s authority under Tasmanian law to conduct a business rendered unlawful by the laws of other States (for why this is so in New South Wales, see infra [79]-[84]). The Constitution does not provide an immediate resolution to the difficulties arising from such conflicts. However, no such issue arises in this litigation. No party suggested that the conduct of Betfair’s exchange in Glenorchy on New South Wales races infringed New South Wales’ or any other State’s law.

59 The original Betfair exchange commenced operations in June 2000 and was conducted by TSEL in the United Kingdom. Subsequently the operational parts of that business were transferred to Betfair Group Limited, which as stated before is the sole shareholder of TSEL. No other betting exchanges operate in Australia. There was no direct evidence before me of the identity of any other betting exchanges although it was plain enough from the “Report of the Betting Exchange Taskforce” (10 July 2003) that other exchanges residing internationally do exist.

VI – The relationship between Betfair and the respondents

60 As has already been mentioned, the TAB was privatised in 1998 and now holds the exclusive off-course totalizator licence by reason of s 14 of the Totalizator Act 1997. Section 21A of that Act prohibited the Minister from granting an exclusive off-course totalizator licence to the TAB unless he was satisfied that it had entered into a commercial relationship with the racing industry that was satisfactory to that industry. On 11 December 1997 an agreement was entered into between the TAB, RNSW, HRNSW, Greyhound Racing New South Wales (“GRNSW”) and another body corporate which was entitled the “Racing Distribution Agreement” (“the RDA”). That agreement has been changed over time. My references to it are to it in its current form. The TAB carries on a number of businesses. One is the off-course totalizator to which reference has already been made. However, it also provides fixed price betting on New South Wales racing events and fixed price and totalizator betting on non-racing events (such as the tennis). Under the RDA the TAB is obliged to pay fees to RNSW, HRNSW and GRNSW in respect of all of these revenue streams even though some of them have nothing to do with the racing of horses or hounds. The fees payable by the TAB under the agreement were usefully summarised in a report prepared for the New South Wales Minister for Gaming and Racing by Mr Alan Cameron AM as follows:

|

Wagering category |

Type of payment |

Basis of payment |

|

Totalizator |

Product fee |

21.9965% of net wagering revenue |

|

race wagering |

Fixed product fee |

$12m payable in FY07 indexed at CPI thereafter |

|

|

Wagering Incentive fee |

25% of notional wagering earnings of the NSW wagering business |

|

Totalizator |

Product fee |

21.9965% of net wagering revenue |

|

sports wagering |

Wagering Incentive fee |

25% of notional wagering earnings of the NSW wagering business |

|

Fixed odds race wagering |

Fixed odds product fee |

21.9965% of fixed odds revenue

|

|

|

Wagering Incentive fee |

25% of notional wagering earnings of the NSW wagering business |

|

Fixed odds sports betting |

Wagering Incentive fee |

25% of notional wagering earnings of the NSW wagering business |

|

Virtual racing games |

Wagering Incentive fee |

25% of notional wagering earnings of the NSW wagering business |

Source: Tabcorp

61 It is important to be clear, I think, about what this means. It signifies that the NSW racing industry, in its various forms, derives profit not only from the gambling public’s fascination with hound and horse races but also from the same public’s gambling interests in other sporting activities having no connexion whatsoever with horse or hound. The amounts of money distributed are very large. In the years 2005 to 2008 the TAB distributed close to $900 million to the New South Wales racing industry as the following table, drawn from paragraph 66 of the respondents’ submissions, illustrates:

|

Financial Year |

Amount Distributed |

|

2005 |

$220.5 million |

|

2006 |

$215 million |

|

2007 |

$221 million |

|

2008 |

$206.9 million |

62 It is useful then to note the identity of the other persons partaking in the rich harvest which is the TAB’s totalizator business. They are, first, the State of New South Wales which obtains the proceeds of a betting tax of either 10.91% or 19.11% (see ss 8-10 Betting Tax Act 2001 (NSW)) on each bet, the Commonwealth which obtains GST of 9.09% on each bet, the racing industry which appears to obtain about 30% and, finally, the TAB itself which gets the balance of about 40%. It will be seen, therefore, that the racing industry has nearly as much economic interest in the profitability of the TAB as the TAB does. The revenues derived by the three codes is split between them by an arrangement called the “Intercode Agreement”.

63 It has been convenient until now to describe the payments made by the TAB as being made to the racing industry. However, this is not a precise statement. The parties to the RDA include, inter alia, RNSW, HRNSW and GRNSW. RNSW is a body corporate established by s 4 of the Thoroughbred Racing Act 1996 (NSW). Before 1996 the Australian Jockey Club, itself established originally under the Australian Jockey Club Act 1873 (NSW), exercised a number of regulatory functions for thoroughbred horse racing in New South Wales. Those functions were taken from it in 1996 and conferred upon RNSW. Section 13 of the Thoroughbred Racing Act provides:

13 Functions of Racing NSW

(1) Racing NSW has the following functions:

(a) all the functions of the principal club for New South Wales and committee of the principal club for New South Wales under the Australian Rules of Racing,

(b) to control, supervise and regulate horse racing in the State,

(b1) such functions in relation to the business, economic development and strategic development of the horse racing industry in the State as are conferred or imposed by this Act,

(c) to initiate, develop and implement policies considered conducive to the promotion, strategic development and welfare of the horse racing industry in the State and the protection of the public interest as it relates to the horse racing industry,

(d) functions with respect to the insuring of participants in the horse racing industry, being functions of the kind exercised by the AJC on the commencement of this section, and such other functions with respect to insurance in the horse racing industry as may be prescribed by the regulations,

(e) such functions as may be conferred or imposed on Racing NSW by or under the Australian Rules of Racing or any other Act,

(f) such functions with respect to horse racing in New South Wales as may be prescribed by the regulations.

(2) The functions of Racing NSW are not limited by the Australian Rules of Racing and are to be exercised independently of the Australian Racing Board.

(3) The AJC ceases to have the functions that are solely the functions of the principal club for New South Wales or committee of the principal club for New South Wales under the Australian Rules of Racing.

(4) In this section:

“AJC” means the club known as the Australian Jockey Club as referred to in the Australian Jockey Club Act 1873 on the commencement of this section.

64 Section 5 of the Thoroughbred Racing Act declares that RNSW does not represent the Crown and that it is not subject to direction by or on behalf of the government. Other provisions in the Act, however, suggest a less than exiguous connexion with the State of New South Wales. Section 6 provides that RNSW is to consist of a chief executive officer and five appointed members. Those five members are appointed by the Minister acting on the recommendation of “the Selection Panel”: s 6(1)(a). However, the selection panel is established by the Minister: s 7(1). The base amount of a member’s remuneration is determined by the Statutory and Other Offices Remuneration Tribunal (s 10), a body established under the Statutory and Other Offices Remuneration Act 1975 (NSW). RNSW is obliged to give its annual report to the Minister and the Minister, in turn, must lay the report before both Houses of Parliament: s 29. Certain decisions of RNSW may be appealed to the Administrative Decisions Tribunal of New South Wales: s 29M(3). Likewise, the Minister may remove a member of RNSW from office for misbehaviour: s 15(2). The position of HRNSW is broadly similar. It is now incorporated under the provisions of the Harness Racing Act 2009 (NSW) although at the commencement of this litigation it existed under the Harness Racing Act 2002 (NSW). Its functions are set out in s 9 in these terms:

9 Functions of HRNSW

(1) HRNSW has the functions conferred or imposed on it by or under this or any other Act or law.

(2) Without limiting subsection (1), the functions of HRNSW include the following:

(a) to control, supervise and regulate harness racing in the State,

(b) to register harness racing clubs, harness racing horses, owners, trainers and drivers of harness racing horses, bookmakers for harness racing and other persons associated with harness racing,

(c) to initiate, develop and implement policies considered conducive to the promotion, strategic development and welfare of the harness racing industry in the State,

(d) to distribute money received as a result of commercial arrangements required by the Totalizator Act 1997,

(e) to allocate to harness racing clubs the dates on which they may conduct harness racing meetings.

(3) HRNSW may affiliate with such organisations, whether in or out of New South Wales, as HRNSW considers appropriate.

(4) The functions of HRNSW are not limited by the rules and are to be exercised independently of Harness Racing Australia or any successor.

65 Like RNSW it is said to be independent of the New South Wales government: s 5. But, also like RNSW, its structure indicates a substantial connexion with the State of New South Wales. In my opinion, the correct characterisation of both bodies is that they are independent statutory authorities which are part of, but do not represent, the State.

66 RNSW also has conferred upon it a number of “special functions” by Part 2A of the Thoroughbred Racing Act 1996. For example, it is empowered to provide minimum standards for the conduct of race meetings (Division 1); to regulate the radio broadcast of race meetings (Division 2); and, importantly, for present purposes, to enter into “Totalizator distribution arrangements” (Division 3). That division contemplates the existence of an intra-code agreement regulating the distribution of totalizator funds between different thoroughbred organisations, effectively, race clubs. RNSW is also party to the Intercode Agreement, to which reference has already been made, and which regulates the distribution of totalizator revenues between thoroughbred racing, harness racing and greyhound racing. The parties to the Intercode Agreement are RNSW, HRNSW, GRNSW and Racingcorp which acts as their agent for the purposes of receiving funds from the TAB. The sharing formula is rather complex but, for example, in the financial year 2006-2007 the $220.8 million distributed by the TAB to the industry was split 72.3%, 14.6% and 13.1% to RNSW, HRNSW and GRNSW respectively, ie, $159.63 million, $32.24 million and $28.92 million.

67 The profound economic dependency thereby exhibited is not just one way. The different codes are bound under the RDA to provide a New South Wales racing programme which is to consist at a minimum of 123 metropolitan thoroughbred meetings, 127 provincial thoroughbred meetings, 186 major country thoroughbred meetings, 55 minor country thoroughbred meetings, 342 harness meetings and 593 greyhound meetings. For each such meeting the TAB likewise must conduct its off-course totalizator and must pay liquidated damages if it does not. On the other hand, if a race meeting is not conducted which should have been under the New South Wales racing programme then Racingcorp must correspondingly pay to TAB liquidated damages.

68 What is presented therefore, is very close in an economic sense to a joint venture. The industry promises to provide, on pain of damages, races; the TAB promises to provide, on pain of damages, its off-course totalizator on each such race meeting. The parties share the bounty. Consistent with such a view there are clauses in the RDA designed to foster co-operation. The agreement provides for the establishment of a business and strategy committee made up of four representatives from the TAB and four from Racingcorp with at least one representative from each code. That committee is to make, as might naturally be expected, recommendations on strategic and business issues relating to wagering.

69 It follows that it is deeply contrary to the interests of RNSW and HRNSW that the revenue of the TAB from its off-course totalizator business be decreased. Below I conclude that the TAB’s average take out or commission from its off-course totalizator is about 16% of the quantum of all bets placed. On this view, for every $100 bet on that totalizator, $16 of take out or commission is thereby generated of which about 30% – $4.50 – goes to the industry. Each time, therefore, $100 of the punters’ money migrates from the TAB to a non-TAB wagering operator, the industry loses $4.50. No person involved in the funding and administration of the New South Wales racing industry could rationally ignore a substantial threat to the revenues of the TAB. This is not a criticism but, rather, a recognition of the commercial realities of the situation. It is also a sign that the New South Wales Parliament has created a regulatory structure with an in-built conflict of interest.

VII – The Race Fields Fee

70 In order for two people to have a wager upon the outcome of a horse race it is necessary for them to know the name or number of the horse, the race it is running in and whether it has been scratched from the racing event or not. It is convenient to refer to this information as race fields information. With that information they may then agree a price and stake and thereby conclude the wagering contract. Generally speaking it is only with those integers that such a wagering contract may be formed. It is theoretically possible that certain kinds of wagers can be concluded without the relevant race field information. For example, it is not needed for a wager that horses trained by a particular trainer will win at least ten races in a given year. However, there was no evidence that there is any market for wagers of that kind.

71 It is not clear whether, and if so, what kind of property rights may subsist in this sort of information or, assuming that property rights do subsist, who might own them. It may be that a collation of such information into a race guide constitutes some species of literary work protected under the Copyright Act 1968 (Cth) although there may be difficulties reconciling that proposition with the High Court’s decision in IceTV Pty Ltd v Nine Network Australia Pty Ltd (2009) 239 CLR 458 which holds there to be no copyright in the weekly schedules of television programming prepared by a free-to-air broadcaster. Recently, that principle has been applied to conclude, inter alia, that the publishers of the yellow and white pages do not own copyright therein: Telstra Corporation Ltd v Phone Directories Co Pty Ltd (2010) 264 ALR 617. How race fields information collated by racing clubs might be usefully distinguished from either of those scenarios is not an issue which need presently be further pursued. Nor, is it necessary to determine how the High Court’s decision in Victoria Park Racing and Recreation Grounds Co Ltd v Taylor (1937) 58 CLR 479 at 498 per Latham CJ, 511 per Dixon J and 527 per McTiernan J which denied that race fields information was the subject of copyright might be usefully distinguished.

72 On 1 July 2008 there commenced in New South Wales amendments to the Racing Administration Act 1998 designed to regulate the use of information identifying the competing horses and hounds in races. The amendments were brought about by the Racing Legislation Amendment Act 2006 (NSW). There were some subsequent amendments to that legislation to which it will be necessary to return. However, the present form of the Racing Administration Act 1998 has the following important features. The expression “ NSW race field information” is defined in s 27 to mean:

“NSW race field information” means information that identifies, or is capable of identifying, the name or number of a horse or greyhound:

(a) as a horse or greyhound that has been nominated for, or is otherwise taking part in, an intended race to be held at any race meeting on a licensed racecourse in New South Wales, or

(b) as a horse or greyhound that has been scratched or withdrawn from an intended race to be held at any race meeting on a licensed racecourse in New South Wales.

73 The “use” of New South Wales race fields information is an offence. Section 33(1) of the Act provides:

33 Use of NSW race field information restricted

(1) A wagering operator or prescribed person must not use NSW race field information unless the wagering operator or person:

(a) is authorised to do so by a race field information use approval and complies with the conditions (if any) to which the approval is subject, or

(b) is authorised to do so by or under the regulations.

Maximum penalty:

(a) in the case of a corporation – 500 penalty units, or

(b) in any other case:

(i) for a first offence – 50 penalty units or imprisonment for 12 months (or both), and

(ii) for a second or subsequent offence – 100 penalty units or imprisonment for 2 years (or both).

74 A penalty unit is presently defined by s 17 of the Crimes (Sentencing Procedure) Act 1999 (NSW) to be $110. Section 33(1) therefore imposes a fine of $55,000 on corporations, $5,500 for individuals on a first offence and $11,000 on individuals for subsequent offences with a possibility of two years imprisonment. In that regard it is to be compared with other offences in New South Wales carrying the same penalty such as, for example, concealing a serious indictable offence (s 316(1) Crimes Act 1900 (NSW)) and violent intimidation (s 545B Crimes Act 1900). Just why the offence of using New South Wales race fields information is regarded as such a social menace was not explained in the evidence before me but it is, I think, unlikely to be connected to any desire on the part of the Parliament to address the social ills attending gambling. Whatever the source of the legislative animus against the unauthorised use of race fields information it suffices to observe that the concern is such that New South Wales not only prohibits its use within that State but, in fact, throughout the world. So much emerges from s 32A which defines the expression “use NSW race field information” in these terms:

32A Meaning of “use NSW race field information

For the purposes of this Division, a person “uses NSW race field information” only if the person, whether in Australia or elsewhere:

(a) publishes any NSW race field information, or

(b) communicates any NSW race field information to a person (regardless of whether the person already knew the information), or

(c) acknowledges or confirms any NSW race field information communicated to the person (including acknowledging or confirming the information by accepting, or facilitating the making of, a bet), or

(d) makes a written or electronic record (such as a betting ticket, statement of account or notice) that contains or refers to any NSW race field information (regardless of whether the record is communicated to any person), or

(e) uses any NSW race field information in a manner prescribed by the regulations, or

(f) causes any of the activities referred to in paragraphs (a)-(e) to occur.

75 To reiterate, the prohibition only applies to “wagering operators” and “prescribed persons”. There are presently no prescribed persons. “Wagering operator” is defined in s 27 to mean:

“wagering operator” means a bookmaker, a person who operates a totalizator or a person who operates a betting exchange.

76 “Betting exchange” is defined in the same provision to mean:

… a facility, electronic or otherwise, that enables persons:

(a) to place or accept, through the operator of the facility, wagers with other persons, or

(b) to place with the operator of the facility wagers that, on acceptance, are matched with opposing wagers placed with and accepted by the operator,

but does not include a facility, electronic or otherwise, that enables persons to place wagers only with a bookmaker or a totalizator.

77 At various points during the argument it was submitted that Betfair was essentially a bookmaker with a perfectly balanced book. This was because its rôle as a principal in every wager made meant that for every back bet placed with it there was a corresponding lay bet (or bets). I have already rejected that argument above.

78 This is an additional reason for rejecting the argument which arises from the definition of “betting exchange”. It excludes facilities which permit persons to place wagers with bookmakers and totalizators. If the respondents were correct and Betfair were a bookmaker it would follow that it would thereby be providing a “facility … that enables persons to place wagers only with a bookmaker” and hence would be within the exception to the definition of a “betting exchange” which is internally inconsistent. The Act contemplates that whatever a betting exchange might be, it is not a facility for dealing with a bookmaker or totalizator. The law of New South Wales does not admit of the concept of a betting exchange which is a bookmaker or a totalizator.

79 A related issue which arose was whether it was lawful to conduct a betting exchange in New South Wales at all. Betfair submitted that it was not; RNSW and HRNSW that it was; the State of New South Wales adopted a position of studied silence. Section 8 of the Unlawful Gambling Act 1998 provides:

8 Offences relating to unlawful betting

(1) For the purposes of this section, the following forms of betting are prohibited:

(a) betting on any event or contingency if the person is not present at a licensed racecourse and the bet is made with a bookmaker,

(b) betting on any event or contingency (other than a horse race, harness race, greyhound race or sports betting event) when the person is present at a licensed racecourse,

(c) betting on any event or contingency when the person is present at a racecourse and a trial meeting (within the meaning of the Racing Administration Act 1998 ) is being held at that racecourse,

(d) betting on any event or contingency when the person is present at a racecourse and a race meeting is being held at that racecourse in contravention of the Racing Administration Act 1998.

(2) A person who engages in betting that is prohibited by subsection (1) is guilty of an offence.

Maximum penalty: 50 penalty units or imprisonment for 12 months (or both).

(3) A person must not make a bet on any horse race, harness race or greyhound race that is to be held anywhere in Australia if:

(a) the bet is made by telephone or electronically by means of the Internet, subscription TV or other on-line communications system, and

(b) the bet is made with another person whom the person making the bet knows (or would be reasonably expected to know):

(i) is not a legal bookmaker, or

(ii) is not a person who is authorised under the law of any State or Territory to conduct totalizator betting.

Maximum penalty: 50 penalty units or imprisonment for 12 months (or both).

(4) For the purposes of subsection (3):

“legal bookmaker” means:

(a) a licensed bookmaker, or