FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Letten (No 4)

[2010] FCA 571

|

Citation: |

Australian Securities and Investments Commission v Letten (No 4) [2010] FCA 571 | |

|

Parties: |

||

|

File number: |

VID 95 of 2010 | |

|

Judge: |

GORDON J | |

|

Date of judgment: |

4 June 2010 | |

|

Legislation: |

||

|

Cases cited: |

Australian Securities and Investments Commission v Letten (No 3) [2010] FCA 512 | |

|

|

| |

|

Date of hearing: |

28 May 2010 | |

|

|

| |

|

Date of last submissions: |

2 June 2010 | |

|

|

| |

|

Place: |

Melbourne | |

|

|

| |

|

Division: |

GENERAL DIVISION | |

|

|

| |

|

Category: |

No Catchwords | |

|

|

| |

|

Number of paragraphs: |

33 | |

|

|

| |

|

Counsel for the Plaintiff: |

AP Trichardt | |

|

|

| |

|

Solicitor for the Plaintiff: |

Australian Securities and Investments Commission | |

|

|

| |

|

Counsel for the First Defendant: |

SJ Hibble | |

|

|

| |

|

Solicitor for the First Defendant: |

Baker & McKenzie | |

|

|

| |

|

Counsel for the Receivers: |

R Strong | |

|

|

| |

|

Solicitor for the Receivers: |

Mallesons Stephen Jaques | |

|

|

| |

|

Solicitor for Westpac Banking Corporation: |

C Hinchen for Allens Arthur Robinson | |

|

|

| |

|

Counsel for Keywear Pty Ltd and Montana Ena Holdings Pty Ltd: |

C Brown | |

|

|

| |

|

Solicitor for Keywear Pty Ltd and Montana Ena Holdings Pty Ltd: |

Hall and Wilcox | |

|

|

| |

|

Counsel for the Committee of Members of the Heritage Golf and Country Club: |

M Goldblatt | |

|

|

| |

|

Solicitor for the Committee of Members of the Heritage Golf and Country Club: |

Gadens Lawyers | |

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

VICTORIA DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

VID 95 of 2010 |

|

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff

|

|

AND: |

MARK RONALD LETTEN First Defendant (and others according to the attached schedule)

|

|

JUDGE: |

|

|

DATE OF ORDER: |

4 JUNE 2010 |

|

WHERE MADE: |

MELBOURNE |

NOTE: For the purposes of this order, “Property”, “Receivers”, “Scheme” and “Secured Lender” have the meanings ascribed to them respectively in the Orders of Justice Gordon in this proceeding made on 25 February 2010 (25 February Orders).

THE COURT ORDERS THAT:

A. Scheme Number 6: Reef House Resort, Seventh Defendant: Firbank Arch Pty Ltd and Eighth Defendant: Glenline Pty Ltd

1. Paragraphs 3 and 8(c) of the 25 February Orders be varied with respect to the Reef House Resort and the Seventh and Eighth Defendants (the Reef House Parties) so that the Receivers shall have the power to sell:

(a) the land, buildings and fixtures, in respect of the Sebel Reef House Resort, the Esplanade, Palm Cove, Queensland;

(b) the Sebel Reef House Resort business including:

(i) hotel operations;

(ii) food and beverage operations;

(iii) conference operations;

(iv) associated goodwill;

(v) debtors; and

(vi) all ancillary property and plant and equipment used in the Sebel Reef House Resort operations; and

(c) all other rights, plant and equipment, vehicles and any other thing owned by the Reef House Parties,

(each a Reef House Property and collectively the Reef House Properties),

save that the Receivers shall not enter into any contract of sale in respect of the Reef House Properties which is not conditional upon approval of the Court.

2. In selling the Reef House Properties the Receivers, consistent with their duties as receivers and managers:

(a) may sell each Reef House Property together with or separately from the other Reef House Properties;

(b) shall obtain proposals from at least three real estate agents or other agent(s) in relation to the sale of the Reef House Properties;

(c) shall select and appoint that real estate or other agent(s) to sell the Reef House Properties or any of them which the Receivers believe, on the basis of the proposals submitted, to be the most appropriate in all of the circumstances (and as consented to by the Secured Lender), provided that the sales commission payable to the selling agent shall not exceed 1.5% (plus GST), exclusive of disbursements, of the achieved sale price;

(d) shall conduct a marketing campaign for the Reef House Properties or any of them for a period of not less than four weeks;

(e) may sell the Reef House Properties or any of them either by auction, tender or expressions of interest as agreed with the appointed agent(s);

(f) may undertake any capital works which the Receivers consider to be necessary or appropriate in order to sell any of the Reef House Properties; and

(g) shall, upon commencement of the sale process, write to all investors in the Reef House Resort (either by email where email addresses of the investors are known or by mail in all other cases) and Tercar Pty Ltd, setting out:

(i) the identity of the appointed agent(s); and

(ii) the process (in general terms) which will be adopted by the Receivers in selling the Reef House Properties.

3. Subject to paragraph 2(c) above, the Receivers are justified in paying all agent’s reasonable fees and other reasonable expenses associated with the sale of the Reef House Properties.

4. Notwithstanding paragraphs 3 and 5 of the 25 February Orders, and subject to paragraphs 20 and 21 of the 25 February Orders, the Receivers are justified in:

(a) paying the proceeds of the realisation of the Reef HouseProperties to the relevant Secured Lender, in reduction or extinguishment of the secured liabilities to the Secured Lender (without prejudice to the relevant defendants’ rights to dispute any of the Secured Lender’s claim), after deduction of the reasonable selling expenses of the Receivers and the reasonable fees and expenses of the Receivers in respect of getting in, preserving and realising the Reef House Properties (as agreed with the Secured Lender);

(b) paying the remaining proceeds of the realisation of the Reef House Properties (after payment of any Secured Lender), including any amounts deducted from the amount paid to any Secured Lender in accordance with paragraph 4(a) above, into the bank account established by the Receivers in relation to the Reef House Resort.

B. Scheme Number 15: Yarra Valley Golf Joint Venture, Twenty-First Defendant: Yarra Valley Golf Pty Ltd, Twenty-Second Defendant: Adina Rise Pty Ltd, Twenty-Third Defendant: Albright Investments Pty Ltd, Twenty-Fourth Defendant: Ashfield Rise Pty Ltd, Twenty-Fifth Defendant: Bradfield Corporation Pty Ltd, Twenty-Sixth Defendant: Copeland Enterprises Pty Ltd, Twenty-Seventh Defendant: Devlin Way Pty Ltd, Twenty-Eighth Defendant: First Hazelwood Pty Ltd, Twenty-Ninth Defendant: Glenbelle Pty Ltd, Thirtieth Defendant: Glenvale Way Pty Ltd, Thirty-First Defendant: Greenview Lane Pty Ltd, Thirty-Second Defendant: Hallmark Corporation Pty Ltd, Thirty-Third Defendant: Moorleigh Holdings Pty Ltd, Thirty-Fourth Defendant: Norton Ridge Pty Ltd, Thirty-Fifth Defendant: Raleigh Glen Pty Ltd, Thirty-Sixth Defendant: Redcrest Holdings Pty Ltd, Thirty-Seventh Defendant: Suri Corporation Pty Ltd, Thirty-Eighth Defendant: Sutton Rise Pty Ltd, Thirty-Ninth Defendant: The Virtual Mlmer Pty Ltd, Fortieth Defendant: Tivendale Pty Ltd, Forty-First Defendant: Tulloch Downes Pty Ltd, Forty-Second Defendant: Mainking Pty Ltd, Forty-Third Defendant: Topglen Pty Ltd, Forty-Fourth Defendant: Allblue Pty Ltd and Forty-Fifth Defendant: Aranbay Pty Ltd

5. Paragraphs 3 and 8(c) of the 25 February Orders be varied with respect to the Yarra Valley GolfJoint Venture and the Twenty-First, Twenty-Second, Twenty-Third, Twenty-Fourth, Twenty-Fifth, Twenty-Sixth, Twenty-Seventh, Twenty-Eighth, Twenty-Ninth, Thirtieth, Thirty-First, Thirty-Second, Thirty-Third, Thirty-Fourth, Thirty-Fifth, Thirty-Sixth, Thirty-Seventh, Thirty-Eighth, Thirty-Ninth, Fortieth, Forty-First, Forty-Second, Forty-Third, Forty-Fourth and Forty-Fifth Defendants (the YVG Parties) so that the Receivers shall have the power to sell:

(a) the land, buildings and fixtures, the legal title to which is held by any of the YVG Parties, located at The Heritage Golf and Country Club, Corner of Hughes and Yarraview Roads, Chirnside Park, Victoria (the Heritage Complex) including:

(i) the properties in respect of which there are existing contracts of sale, including:

(A) Lots 611 to 618 Botanica town houses;

(B) Lots 6 and 7 of the Henley Land;

(C) Lot 8 of the Henley Land,

(collectively, the Pre-sold Properties); and

(ii) all other developed and undeveloped land located at the Heritage Complex.

(b) the golf operations business located at the Heritage Complex including the YVG Parties’ interest in and rights in respect of:

(i) the Henley Golf Course;

(ii) the St John Golf Course;

(iii) the club house;

(iv) the members’ bar;

(v) the pro shop;

(vi) all maintenance sheds;

(vii) all ancillary property and plant and equipment used in the golf operations;

(viii) goodwill; and

(ix) debtors;

(c) all other rights, plant and equipment, vehicles and any other thing owned by the YVG Parties; and

(d) all shares held by Yarra Valley Golf Pty Ltd (receivers and managers appointed) in Heritage Golf and Country Club Pty Ltd,

(each a YVG Property and collectively the YVG Properties),

save that the Receivers shall not enter into any contract of sale in respect of the YVG Properties which is not conditional upon approval of the Court.

6. In selling the YVG Properties, except for the Pre-sold Properties, the Receivers, consistent with their duties as receivers and managers:

(a) may sell each YVG Property together with or separately from the other YVG Properties and the Glenbelle Property (as defined in order 10 below);

(b) shall obtain proposals from at least two real estate agents or other agent(s) in relation to the sale of the YVG Properties;

(c) shall select and appoint that real estate or other agent(s) to sell the YVG Properties which the Receivers believe, on the basis of the proposals submitted, to be the most appropriate in all of the circumstances (and as consented to by the Secured Lender), provided that the sales commission payable to the selling agent shall not exceed 1.5% (plus GST), exclusive of disbursements, of the achieved sale price;

(d) shall conduct a marketing campaign for the YVG Properties or any of them for a period of not less than four weeks;

(e) may sell the YVG Properties or any of them either by auction, tender or expressions of interest as agreed with the appointed agent(s);

(f) may undertake any capital works which the Receivers consider to be necessary or appropriate in order to sell any of the YVG Properties; and

(g) shall, upon commencement of the sale process, write to all investors in the Yarra Valley Golf Joint Venture and any other person or entity known to the Receivers, or their partners or staff, to be actual or potential investors, directly or indirectly, in the Yarra Valley Golf Joint Venture or any of the YVG Properties (either by email where email addresses of the investors are known or by mail in all other cases) setting out:

(i) the identity of the appointed agent(s); and

(ii) the process (in general terms) which will be adopted by the Receivers in selling the YVG Properties.

7. In relation to the Pre-sold Properties, the Receivers, consistent with their duties as receivers and managers:

(a) may settle the existing contracts of sale in respect of those properties; and

(b) may undertake any capital works in relation to the Pre-sold Properties which the Receivers consider to be necessary or appropriate in order to settle the existing contracts of sale in respect of the Pre-sold Properties.

8. Subject to paragraph 6(c) above, the Receivers are justified in paying all agent’s reasonable fees and other reasonable expenses associated with the sale of the YVG Properties.

9. Notwithstanding paragraphs 3 and 5 of the 25 February Orders, and subject to paragraphs 20 and 21 of the 25 February Orders, the Receivers are justified in:

(a) paying the proceeds of the realisation of the YVGProperties to the relevant Secured Lender, in reduction or extinguishment of the secured liabilities to the Secured Lender (without prejudice to the relevant defendants’ rights to dispute any of the Secured Lender’s claim), after deduction of the reasonable selling expenses of the Receivers and the reasonable fees and expenses of the Receivers in respect of getting in, preserving and realising the YVG Properties (as agreed with the Secured Lender);

(b) paying the remaining proceeds of the realisation of the YVGProperties (after payment of any Secured Lender), including any amounts deducted from the amount paid to any Secured Lender in accordance with paragraph 9(a) above, into the bank account established by the Receivers in relation to the Yarra Valley GolfJoint Venture.

C. Scheme Number 16: Glenbelle Project, Twenty-Ninth Defendant: Glenbelle Pty Ltd and Thirty-Sixth Defendant: Redcrest Holdings Pty Ltd

10. Paragraphs 3 and 8(c) of the 25 February Orders be varied with respect to the Glenbelle Project and the Twenty-Ninth and Thirty-Sixth Defendants (Glenbelle Parties) so that the Receivers shall have the power to sell:

(a) the land, buildings and fixtures, in respect of the Management Lot of The Sebel Lodge Yarra Valley located within the Heritage Complex;

(b) the land, building and fixtures, in respect of the Heritage Retreat recreation facility and day spa located within the Heritage Complex;

(c) The Sebel Lodge Yarra Valley business including the Glenbelle Parties’ interest in:

(i) the hotel operations;

(ii) the food and beverage operations;

(iii) the conference operations;

(iv) the associated goodwill;

(v) the debtors; and

(vi) all ancillary property and plant and equipment used in The Sebel Lodge Yarra Valley operations;

(d) the Heritage Retreat business including the Glenbelle Parties’ interest in;

(i) the spa operations;

(ii) the recreation facility operations;

(iii) the food and beverage operations;

(iv) the associated goodwill;

(v) the debtors;

(vi) all ancillary property and plant and equipment used in the Heritage Retreat operations;

(e) all other rights, plant and equipment, vehicles and any other thing owned by the Glenbelle Parties,

(each a Glenbelle Property and collectively the Glenbelle Properties),

save that the Receivers shall not enter into any contract of sale in respect of the Glenbelle Properties which is not conditional upon approval of the Court.

11. In selling the Glenbelle Properties the Receivers, consistent with their duties as receivers and managers:

(a) may sell each Glenbelle Property together with or separately from the other Glenbelle Properties and the YVG Properties;

(b) shall obtain proposals from at least two real estate agents or other agent(s) in relation to the sale of the Glenbelle Properties;

(c) shall select and appoint that real estate or other agent(s) to sell the Glenbelle Properties or any of them which the Receivers believe, on the basis of the proposals submitted, to be the most appropriate in all of the circumstances (and as consented to by the Secured Lender), provided that the sales commission payable to the selling agent shall not exceed 1.5% (plus GST), exclusive of disbursements, of the achieved sale price;

(d) shall conduct a marketing campaign for the Glenbelle Properties or any of them for a period of not less than four weeks;

(e) may sell the Glenbelle Properties or any of them either by auction, tender or expressions of interest as agreed with the appointed agent(s);

(f) may undertake any capital works which the Receivers consider to be necessary or appropriate in order to sell any of the Glenbelle Properties; and

(g) shall, upon commencement of the sale process, write to all investors in the Glenbelle Project (either by email where email addresses of the investors are known or by mail in all other cases) setting out:

(i) the identity of the appointed agent(s); and

(ii) the process (in general terms) which will be adopted by the Receivers in selling the Glenbelle Properties.

12. Subject to paragraph 11(c) above, the Receivers are justified in paying all agent’s reasonable fees and other reasonable expenses associated with the sale of the Glenbelle Properties.

13. Notwithstanding paragraphs 3 and 5 of the 25 February Orders, and subject to paragraphs 20 and 21 of the 25 February Orders, the Receivers are justified in:

(a) paying the proceeds of the realisation of the GlenbelleProperties to the relevant Secured Lender, in reduction or extinguishment of the secured liabilities to the Secured Lender (without prejudice to the relevant defendants’ rights to dispute any of the Secured Lender’s claim), after deduction of the reasonable selling expenses of the Receivers and the reasonable fees and expenses of the Receivers in respect of getting in, preserving and realising the Glenbelle Properties (as agreed with the Secured Lender);

(b) paying the remaining proceeds of the realisation of the Glenbelle Properties (after payment of any Secured Lender), including any amounts deducted from the amount paid to any Secured Lender in accordance with paragraph 13(a) above, into the bank account established by the Receivers in relation to the Glenbelle Project.

D. LGH Companies’ Report

14. Paragraph 11 of the Orders made on 6 May 2010 be varied to extend the date for compliance to 8 June 2010.

15. Paragraph 12 of the Orders made on 6 May 2010 be varied so as to provide that “The Receivers shall provide on a “strictly confidential basis: for personal use only” a copy of the LGH Companies’ Report to the Investors in each Scheme and each Secured Lender on or before 10 June 2010”.

E. General matters

16. The further hearing of the matter be adjourned to 30 July 2010 at 9:30am.

17. Costs be reserved.

Note:Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

The text of entered orders can be located using Federal Law Search on the Court’s website.

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

VICTORIA DISTRICT REGISTRY |

|

|

GENERAL DIVISION |

VID 95 of 2010 |

|

BETWEEN: |

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff

|

|

AND: |

MARK RONALD LETTEN First Defendant (and others according to the attached schedule) |

|

JUDGE: |

GORDON J |

|

DATE: |

4 JUNE 2010 |

|

PLACE: |

MELBOURNE |

REASONS FOR JUDGMENT

INTRODUCTION

1 This is the fourth judgment in relation to a number of commercial projects in which Mr Mark Ronald Letten (Mr Letten), the first defendant, has been involved. The history of the proceedings are summarised in Australian Securities and Investments Commission v Letten (No 3) [2010] FCA 512 at paragraphs [1] – [4] in the following terms:

2 On 4 March 2010, Orders were made appointing the Receivers as joint and several receivers and managers of the property of the scheme defined in those orders as “the funds invested, contributed or deposited by investors for the purpose of acquiring an interest in the project known as SY21 Retail Complex Project” (the SY21 Scheme), being the scheme numbered 12 in Annexure A (the 4 March Orders). The 4 March Orders also provided the SY21 Scheme be wound up pursuant to s 601EE(1) of the Act.

3 On 31 March 2010, Orders were made providing that the Receivers were justified in causing certain Corporate Defendants which owned or operated the schemes numbered 4, 5, 6, 9, 13, 14, 15 and 16 in Annexure A to borrow funds from Westpac Banking Corporation Limited (Westpac) on certain conditions to maintain the status quo: see Australian Securities and Investments Commission v Letten (No 2) [2010] FCA 307.

4 The 25 February Orders required the Receivers to do a number of things. Two aspects of the 25 February Orders should be noted. First, the 25 February Orders required the Receivers to file and serve a report in respect of, inter alia, the nature and identity of the property of each Scheme, any claims by third parties in relation to the property of the Scheme, the identities of investors and the nature of their investment (the Disclosure Reports). Secondly, the 25 February Orders required the Receivers to provide a copy of a Disclosure Report in respect of a Scheme to the investors in that Scheme.

These reasons for decision adopt the same abbreviations.

2 On 13 April 2010, the Receivers filed Disclosure Reports in relation to each Scheme listed in Annexure A to these reasons for decision except for schemes numbered 6, 15 and 16. The Disclosure Reports for schemes numbered 6, 15 and 16 were filed on 28 April 2010. Letten (No 3) [2010] FCA 512 determined the Receivers application for the power of sale in relation to schemes numbered 4, 5, 8, 9, 13 and 14 in Annexure A.

3 These reasons for decision concern two matters. First, consideration of an application by the Receivers as to the manner in which they may initially deal with any proceeds from any disposal of the assets of the schemes numbered 4, 5, 9, 13 and 14 in Annexure A and, secondly, the Receivers’ application for a power of sale in relation to assets of the schemes numbered 6, 15 and 16.

4 Before turning to consider each matter in turn, it is necessary to refer to the matters summarised in paragraph [8] of Letten (No 3) [2010] FCA 512 which the Receivers submitted remained the position in relation to the schemes numbered 4, 5, 9, 13 and 14 and were equally applicable to the schemes numbered 6, 15 and 16, namely:

1. on 25 February 2010, the Court ordered the scheme be wound up pursuant to s 601EE of the Act;

2. the property of the scheme is subject to mortgages and charges which secure substantial debts, and the scheme does not have the resources to pay the debts otherwise than out of the proceeds of the sale of the property of the scheme;

3. the Secured Lender (as defined in the 25 February Orders) has reserved its rights in relation to its securities in respect of the scheme;

4. interest is presently accruing on the secured debt in respect of the scheme in favour of the Secured Lender which is diminishing any equity which may be available for distribution to investors in the scheme;

5. exercising the power of sale would minimise the ongoing operating costs in relation to the property of the scheme;

6. investors will only become entitled to repayment of their principal investment in the scheme or to a share in the net profits of the joint venture when the property of the scheme is sold; and

7. there is no practical means of winding up the schemes otherwise than by realisation of the property of the scheme.

5 Against that background, I turn to consider each application.

I. INITIAL DEALING WITH PROCEEDS OF SALE OF SCHEMES NUMBERED 4, 5, 9, 13 AND 14 IN ANNEXURE A

6 On 28 May 2010, Orders were made in the following terms:

NOTE: For the purposes of this order, “Property”, “Receivers”, “Scheme” and “Secured Lender” have the meanings ascribed to them respectively in the Orders of Justice Gordon in this proceeding made on 25 February 2010 (25 February Orders). For the purposes of this order “George Street Property”, “Cimitiere House Property”, “Low Head Property”, “Nicholson Street Property”, “The Glen Centre Property” and “Twinview Property” have the meanings ascribed to them respectively in the Orders of Justice Gordon in this proceeding made on 25 May 2010 (25 May Orders).

A. Scheme number 4: George Street Joint Venture, Sixth Defendant: Enmore Enterprises Pty Ltd

1 Notwithstanding paragraphs 3 and 5 of the 25 February Orders and paragraph 4 of the 25 May Orders, and subject to paragraphs 20 and 21 of the 25 February Orders, the Receivers are justified in:

(a) paying the proceeds of the realisation of the George Street Property to the relevant Secured Lender, in reduction or extinguishment of the secured liabilities to the Secured Lender (without prejudice to the relevant defendants’ rights to dispute any of the Secured Lender’s claim), after deduction of the reasonable selling expenses of the Receivers and the reasonable fees and expenses of the Receivers in respect of getting in, preserving and realising the relevant Property (as agreed with the Secured Lender);

(b) paying the remaining proceeds of the realisation of the George Street Property (after payment of any Secured Lender), including any amounts deducted from the amount paid to any Secured Lender in accordance with paragraph 1(a) above, into the bank account established by the Receivers in relation to the George Street Joint Venture.

B. Scheme number 5: Cimitiere House Joint Venture, Sixth Defendant: Enmore Enterprises Pty Ltd

2 Notwithstanding paragraphs 3 and 5 of the 25 February Orders and paragraph 8 of the 25 May Orders, and subject to paragraphs 20 and 21 of the 25 February Orders, the Receivers are justified in:

(a) paying the proceeds of the realisation of the Cimitiere House Property to the relevant Secured Lender, in reduction or extinguishment of the secured liabilities to the Secured Lender (without prejudice to the relevant defendants’ rights to dispute any of the Secured Lender’s claim), after deduction of the reasonable selling expenses of the Receivers and the reasonable fees and expenses of the Receivers in respect of getting in, preserving and realising the relevant Property (as agreed with the Secured Lender).

(b) paying the remaining proceeds of the realisation of the Cimitiere House Property (after payment of any Secured Lender), including any amounts deducted from the amount paid to any Secured Lender in accordance with paragraph 2(a) above, into the bank account established by the Receivers in relation to the Cimitiere House Joint Venture.

C. Scheme number 9: Nicholson Street Joint Venture, Thirteenth Defendant: Nicholson Street Pty Ltd, Fourteenth Defendant: Holloway Crest Pty Ltd and Fifteenth Defendant: Rosebery Enterprises Pty Ltd

3 Notwithstanding paragraphs 3 and 5 of the 25 February Orders and paragraph 16 of the 25 May Orders, and subject to paragraphs 20 and 21 of the 25 February Orders, the Receivers are justified in:

(a) paying the proceeds of the realisation of the Nicholson StreetProperty to the relevant Secured Lender, in reduction or extinguishment of the secured liabilities to the Secured Lender (without prejudice to the relevant defendants’ rights to dispute any of the Secured Lender’s claim), after deduction of the reasonable selling expenses of the Receivers and the reasonable fees and expenses of the Receivers in respect of getting in, preserving and realising the Nicholson Street Property (as agreed with the Secured Lender).

(b) paying the remaining proceeds of the realisation of the Nicholson Street Property (after payment of any Secured Lender), including any amounts deducted from the amount paid to any Secured Lender in accordance with paragraph 3(a) above, into the bank account established by the Receivers in relation to the Nicholson Street Joint Venture.

D. Scheme number 13: The Glen Centre Joint Venture, Eighteenth Defendant: The Glen Centre Hawthorn Pty Ltd, Nineteenth Defendant: Castello Holdings Pty Ltd

4 Notwithstanding paragraphs 3 and 5 of the 25 February Orders and paragraph 20 of the 25 May Orders, and subject to paragraphs 20 and 21 of the 25 February Orders, the Receivers are justified in:

(a) paying the proceeds of the realisation of The Glen Centre Property to the relevant Secured Lender, in reduction or extinguishment of the secured liabilities to the Secured Lender (without prejudice to the relevant defendants’ rights to dispute any of the Secured Lender’s claim), after deduction of the reasonable selling expenses of the Receivers and the reasonable fees and expenses of the Receivers in respect of getting in, preserving and realising The Glen Centre Property (as agreed with the Secured Lender).

(b) paying the remaining proceeds of the realisation of The Glen Centre Property (after payment of any Secured Lenders), including any amounts deducted from the amount paid to any Secured Lender in accordance with paragraph 4(a) above, into the bank account established by the Receivers in relation to The Glen Centre Joint Venture.

E. Scheme number 14: Twinview Joint Venture, Twentieth Defendant: Twinview Nominees Pty Ltd

5 Notwithstanding paragraphs 3 and 5 of the 25 February Orders and paragraph 24 of the 25 May Orders, and subject to paragraphs 20 and 21 of the 25 February Orders, the Receivers are justified in:

(a) paying the proceeds of the realisation of the TwinviewProperty to the relevant Secured Lender, in reduction or extinguishment of the secured liabilities to the Secured Lender (without prejudice to the relevant defendants’ rights to dispute any of the Secured Lender’s claim), after deduction of the reasonable selling expenses of the Receivers and the reasonable fees and expenses of the Receivers in respect of getting in, preserving and realising the relevant Property (as agreed with the Secured Lender).

(b) paying the remaining proceeds of the realisation of the TwinviewProperty (after payment of any Secured Lenders), including any amounts deducted from the amount paid to any Secured Lender in accordance with paragraph 5(a) above, into the bank account established by the Receivers in relation to the TwinviewJoint Venture.

F. General matters

6 The further hearing of the matter be adjourned to 30 July 2010.

7 Costs be reserved

(In each of the schemes numbered 4, 5, 9, 13 and 14, the Secured Lender was Westpac Banking Corporation (Westpac)).

7 These reasons for decision record why Orders were made in those terms.

8 Having regard to the matters identified in paragraph [4] above, the Receivers and Westpac executed a Deed of Priority. In general terms, that Deed of Priority records an agreement reached between them, inter alia, that:

1. certain costs of the Receivers (defined as Receivers’ Priority Costs) will have priority over Westpac’s Secured Debt;

2. at least three business days prior to the settlement of the sale of an asset which is subject to security in favour of Westpac, the Receivers will give notice to Westpac of the Receivership Costs together with the details of those costs and Westpac will identify which costs are disputed and which ones are not;

3. upon settlement of sale of an asset which is subject to security in favour of Westpac, the Receivers’ disputed costs and undisputed costs will be placed in separate accounts;

4. all amounts will be held by the Receivers pending approval of their costs by the Court;

5. the Receivers reserve all their rights and the rights of the entities in relation to the validity of the securities claimed by Westpac (defined as Westpac Securities) and the amount secured by the Westpac Securities.

9 These arrangements are intended to reduce the impact of the facts and matters identified in paragraph [4(4)] and [4(5)] above whilst at the same time preserving the Receivers’ rights to contest Westpac’s position in relation to its security and the amount of its secured debt. In the circumstances of each of these schemes, I concluded and remain of the view it was appropriate for the Court to grant the Orders in paragraph [6] above.

10 Finally, during the course of the hearing, the Receivers properly conceded that it was not appropriate for the Court to grant similar orders in relation to scheme 8 or in relation to the second and 10th defendants. In relation to scheme 8, the orders sought were not appropriate because there was another secured lender involved in that scheme who was not represented at the hearing and had not entered into any formal arrangements with the Receivers to protect the available proceeds of sale from the investors’ perspective whilst at the same time reducing the secured debt which was not being serviced. In relation to the second and 10th defendants, the reasons were different. A form of disclosure report in relation to those entities had not yet been provided to the Court by the Receivers and therefore it was not possible to identify whether any investors or any third parties should be provided with notice of the application and given an opportunity to make submissions in relation to the proposed sale of what can only be described as some minor assets. The Receivers have liberty to apply in relation to those matters if it becomes necessary for them to do so.

II. POWER OF SALE IN RELATION TO SCHEMES 6, 15 AND 16 IN ANNEXURE A

11 On 6 May 2010, the Receivers were directed to send a circular to all investors clarifying the way in which investors could make submissions to the Court in relation to the future of any of the Schemes. Between 11 and 27 May 2010, submissions were received from 30 investors or groups of investors in relation to the schemes numbered 6, 15 and 16 in Annexure A. These submissions will be addressed in further detail below.

12 Before turning to consider each scheme, there are a number of matters to be noted. First, each of the matters summarised in paragraph [8] of Letten (No 3) [2010] FCA 512 (see [4] above) apply to the schemes numbered 6, 15 and 16. Any particular facts and matters relevant to any scheme are addressed under the specific scheme headings below.

13 Secondly, I have read each submission filed by the investors. However, although I have read and considered each submission filed by an investor in relation to a particular scheme, it is again both unnecessary and inappropriate for me to determine whether that person is in fact an investor in that scheme. Thirdly, for the purposes of the present application, I have deferred consideration of those submissions dealing with the distribution of any proceeds from the sale of any scheme property. Those issues will be substantively addressed if and when any property is sold. Finally, because of the complicated nature of some aspects of the schemes numbered 6, 15 and 16, I refused to consider the Receivers’ application for a power of sale in relation to the property of each of the schemes until the Receivers provided the Court with evidence that each person and entity known to the Receivers who might be affected by the exercise of the power of sale received notification of the application and was provided with an opportunity to file a submission with the Court in relation to the application. As the following analysis will demonstrate, that required a review by the Receivers of the notice they had given and, where appropriate, required notice to be given to a number of other persons and entities. On 2 June 2010, the Receivers filed a further affidavit with the Court (the Ninth Templeton Affidavit) which:

1. identified the other persons and entities who were presently known to them and may be affected by the Court granting the Receivers the power of sale;

2. established that each of the persons and entities in (1) were notified of the Receivers’ application for a power of sale and given an opportunity to make submissions to the Court in relation to the application; and

3. confirmed that those persons notified supported the Receivers’ proposed exercise of the power of sale but, like many investors, expressed the view that the property of the schemes should be sold in an orderly manner and not on a fire sale basis.

SCHEME 6: REEF HOUSE RESORT

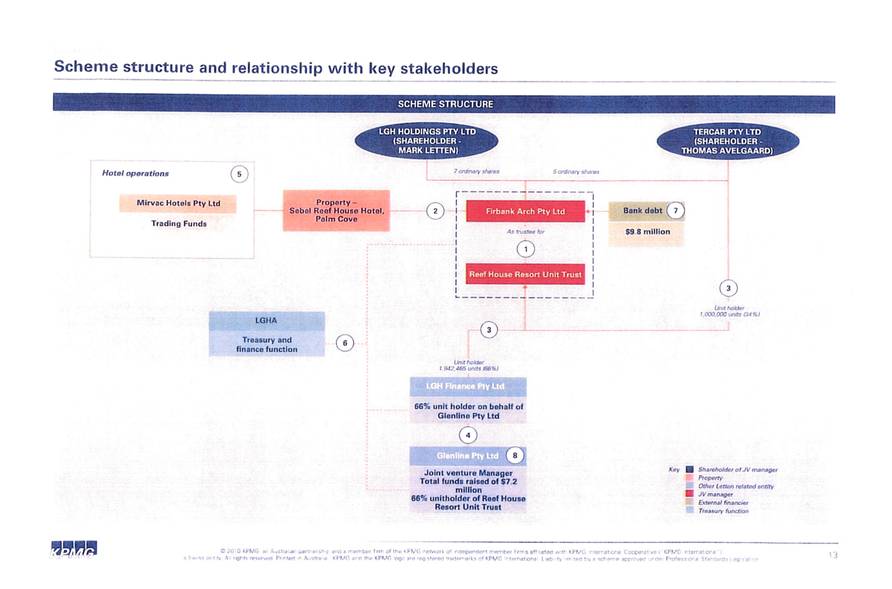

14 The Disclosure Report identifies the property as the Sebel Reef House Resort, the Esplanade, Palm Cove, Queensland (the Resort) with the Resort’s operations being managed by Mirvac Hotels. The whole of the real property is mortgaged to Westpac together with a fixed and floating charge over the assets of Firbank Arch Pty Ltd (receiver and manager appointed) (Firbank). Firbank is the seventh defendant and the trustee of the Reef House Resort Unit Trust (the Trust).

15 The Disclosure Report also records that:

1. LGH Finance Pty Ltd (the 11th defendant) holds 66% of the units in the Trust on behalf of Glenline Pty Ltd (the eighth defendant) which in turn holds the units as joint venture manager for the scheme;

2. the balance of the units in the Trust (34%) are held by Tercar Pty Ltd (Tercar) and that Mr Thomas Avelsgaard is a director and shareholder in Tercar;

3. in addition to the Westpac mortgage, the scheme owes an amount to LGH Administration Pty Ltd (LGHA), the 10th defendant, of approximately $5.0 million, and to Tercar of $1.37 million.

A flow chart included by the Receivers in the Disclosure Report summarising the arrangements is attached as Annexure B to these reasons for decision.

16 The Ninth Templeton Affidavit disclosed that Tercar had been provided with a copy of the relevant disclosure report through Mr Avelsgaard. Tercar also received notification of the Receivers’ proposal to sell the assets and had expressed the view that it wanted to obtain from the realisation of the assets whatever return it could so that it could begin to reinvest its capital.

17 The financial history and performance of the business and assets of the scheme is more complicated than that considered in Letten (No 3) [2010] FCA 512. So, for example, at present, the Resort is trading marginally profitably, the cash flow is sufficient to meet the costs of operating the business but insufficient to service the interest on the debt, the adjusted balance sheet shows negative assets of $500,000 and the funds flow analysis shows an accumulated deficit of approximately $5 million. In relation to the physical assets, the Resort consists of a number of buildings of various ages and conditions. Some capital works have been identified. At present, the Receivers have not yet determined whether those works should be undertaken prior to sale. In any event, the Receivers do not have the necessary funding to complete capital works. Counsel for the Receivers informed the Court that should the Receivers consider that capital works are necessary to be undertaken prior to sale for which they require funding, they would make a separate application to the Court.

18 Submissions were received from eight investors or groups of investors: Warren Appleton, Marion and Ray Borycewicz, Roger Smith, Wayne and Lesley Kelly, Geoffrey and Veronica Keogh, Douglas Mitchell, Sally Jeanette Carlton of the BACS Group Trust and Anthony John Light on behalf of Light Investments Pty Ltd and Light Carden Investments Pty Ltd. Concern was expressed by a number of investors that the sale should proceed in an orderly fashion and not on a fire sale basis. Other investors submitted that the sale should be deferred until the market for resorts improved.

19 For the reasons set out in paragraphs [4] and [14] – [17] above, the Receivers sought a power of sale of the property of the scheme numbered 6. The Receivers have proposed that they shall not enter into any contract of sale which is not conditional upon approval of the Court. In the circumstances, I would grant the Receivers the power of sale. I am satisfied that the concerns of the investors and Tercar are adequately addressed by the form of orders I propose to make in relation to the power of sale.

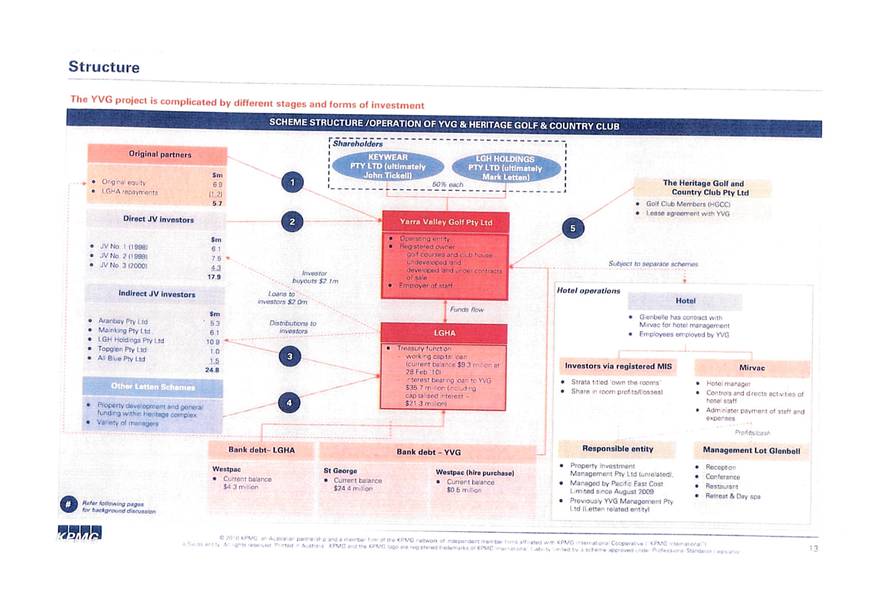

SCHEME 15: YARRA VALLEY GOLF JOINT VENTURE

20 The Disclosure Report identifies the property of the scheme numbered 15 as the Heritage Golf Club and Country Club, Corner of Hughes and Yarraview Roads, Chirnside Park, Victoria (the YVG Property). The YVG Property is described by the Receivers as follows:

The … property is situated within the Heritage Golf Club and Country Club Complex. This includes residential, hotel, day spa, conference and golf facilities (albeit these have different owners)

The … property comprises the two golf courses (St John & Henley), clubhouse, residential development land and 92% of the shares in HGCC Pty Ltd. HGCC Pty Ltd in turn operates the Heritage Golf Club and Country Club (an unincorporated association). The St John course is subject to a lease to HGCC Pty Ltd. It was originally intended that a similar lease be provided to HGCC Pty Ltd once the subdivision of the relevant land occurs

[Yarra Valley Golf Pty Ltd] is responsible for the day to day management of the golf operations and the development, marketing and sale of the residential land. The hotel operations including conference and day spa facilities are not owned by [Yarra Valley Golf Pty Ltd]

21 The Disclosure Report set out the “key” steps and processes by which the project was established. For present purposes, it is sufficient to note that the Receivers stated that:

The investor funding for the development of [Yarra Valley Golf Pty Ltd] has been sourced from many different investors and in different forms over a long period of time and as such may constitute separate schemes

There are a number of issues which make it difficult to identify the scheme property for each of the schemes. These include:

· The fact that a number of [Joint Venture Agreements] appear to relate to the same physical assets (even though different corporate managers were appointed pursuant to the [Joint Venture Agreements])

· Any separate schemes are effectively ‘cross collaterised’ as the secured finance in relation to [Yarra Valley Golf Pty Ltd] has not been quarantined to particular assets of the schemes

· The substantial number of investors who invested in various aspects of the [Yarra Valley Golf Pty Ltd] development

On any view, the arrangements are complicated. So, for example, the initial source appears to have been provided in the mid 1990’s with the creation of a partnership and the acquisition of the St John and Henley land. The current status of that partnership is an issue which remains unresolved.

22 A flow chart included by the Receivers in the Disclosure Report summarising the arrangements is attached as Annexure C to these reasons for decision. As that flow chart illustrates, there are a number of other entities and persons that are likely to be affected by this application. As noted above, at the time of the hearing, the Receivers could not establish that all of those persons and entities had received notice of the application and been given an opportunity to make submissions in relation to it. I directed the Receivers to rectify that position. In addition, Mr Brown of Counsel appeared for Keywear Pty Ltd and Montana Ena Holdings Pty Ltd. Keywear Pty Ltd was identified in the Disclosure Report as an original partner. Montana Ena Holdings Pty Ltd was not disclosed but asserts an interest in the assets the subject of the application. Mr Brown informed the Court that his instructions were not to delay the process but to seek liberty to apply. I directed that any further submissions in relation to the application should be provided forthwith. No further submissions were filed with the Court.

23 The Ninth Templeton Affidavit disclosed that the Receivers had provided to each of the other entities and persons who were likely to be affected by the application, and who were known to the Receivers, a copy of the relevant Disclosure Report and notification of the Receivers’ proposal to seek a power of sale of the assets. Most of the other entities and persons were provided with the circular approved by the Court on 6 May 2010 inviting them to make submissions. Those who did not receive the circular were contacted by the Receivers and were given the opportunity to make submissions concerning the proposed realisation strategy. The majority of the other entities and persons endorsed the Receivers’ proposed realisation strategy. Several of the other entities and persons expressed concern that the realisation of the assets be undertaken in an orderly manner, not on a fire sale basis and in a way that ensures the value of the property is maximised.

24 I turn to consider the financial position. Westpac (including St George Bank Limited) is a secured creditor. The debt owed to Westpac is secured by real property mortgages over numerous titles as well as fixed charges over identified items of equipment and a fixed and floating charge over the assets and undertaking of Yarra Valley Golf Pty Ltd, the 21st defendant (YVG). The trading summary indicates that the schemes have an accumulated deficit of about $38 million. The funds flow analysis forecasts a cash surplus for the year ended 30 June 2010 of approximately $600,000. The balance sheet shows equity of $4,850,000. That amount includes an amount of $35,650,000 under the heading “Loans and Borrowings” said to be owed to LGHA in respect of which it appears there have been no repayments and on which unpaid interest has been accumulating for a number of years.

25 The assets the subject of the Receivers’ application were divided into four categories: operating assets, assets under contract / available for immediate sale, subdivided land and land yet to be developed. YVG is the registered proprietor of those assets. Those assets are unable to generate sufficient revenue to service the debt. In relation to those assets, a number of assets were in fact sold prior to the appointment of the Receivers but remain to be completed. The unsettled contracts total approximately $18 million. The initial strategy identified by the Receivers is to seek to secure the future of the golf courses as operating assets through a sale process of one or both of them and move to completion on the unsettled contracts.

26 Submissions were received from 27 investors or groups of investors. It is unnecessary to name each of them. Again, concern was expressed by a number of investors that the sale should proceed in an orderly fashion and not on a fire sale basis. One investor submitted that the sale should be deferred until a “good price” could be obtained. Other investors supported the Receivers’ recommendations. A number of investors suggested that the “developments” should take place before the properties are sold. As I understand it, that is a reference to the last category of assets referred to in [25] above. Given the initial strategy identified by the Receivers (see [25]) and that the Receivers informed the Court they would seek Court approval if the advice they received was to sell that land “as is” in whole or in part with other assets, that issue appears to be unnecessary to immediately resolve.

27 For the reasons set out in paragraphs [4] and [20]-[25] above, the Receivers sought a power of sale of the YVG Property. As with the Reef House Resort, the Receivers have proposed to seek Court approval before any contract of sale is entered into. In the circumstances, I would grant the Receivers the power of sale. I am satisfied that the concerns of the investors and the other entities and persons identified in paragraphs [23] and [26] above are adequately addressed by the form of orders I propose to make in relation to the power of sale.

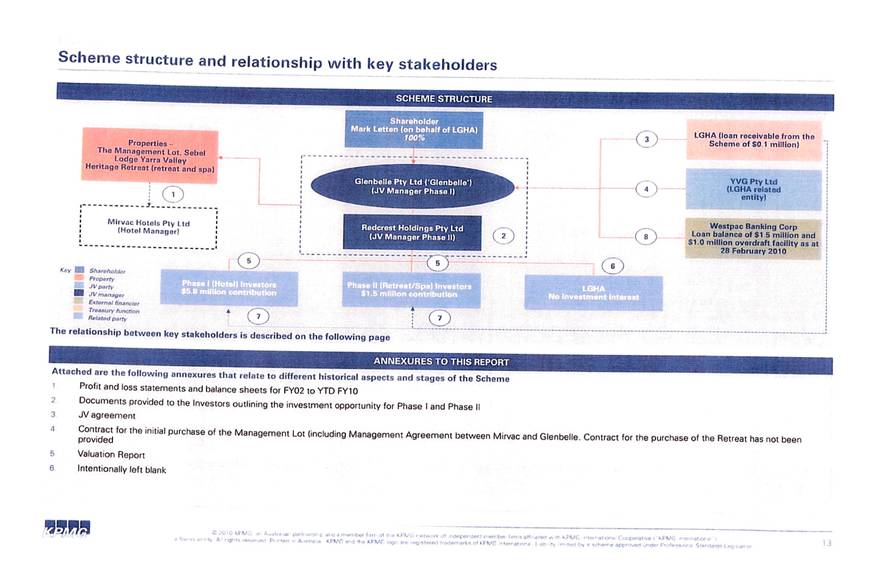

SCHEME 16: GLENBELLE PROJECT

28 The Disclosure Report identifies the property of the scheme numbered 16 as the Management Lot of The Sebel Lodge Yarra Valley, Corner of Hughes and Yarraview Roads, Chirnside Park, Victoria and the Heritage Retreat, in Wonga Park, Victoria. Careful readers will note that The Sebel Lodge Yarra Valley has the same address as the Heritage Golf Club and Country Club (that is, the YVG Property). The Sebel Lodge Yarra Valley is a hotel. The rooms in the hotel are strata titled and owned by individuals pursuant to a registered managed investment scheme which is not the subject of these proceedings. The “Management Lot” covers those areas of the hotel which are needed to operate the hotel as a business including kitchens, the reception and conference facilities. Mirvac Hotels is the manager of the hotel business.

29 A flow chart included by the Receivers in the Disclosure Report summarising the arrangements is attached as Annexure D to these reasons for decision. As that chart illustrates, there were two phases. Despite Redcrest Holdings Pty Ltd, the 36th defendant, being the joint venture manager for phase II, it does not appear to hold any assets. Instead, Glenbelle Pty Ltd, the 29th defendant (Glenbelle), the joint venture manager of phase I, holds all the assets. Whether there is one scheme or, in fact, two schemes has not yet been resolved. Moreover, it is unnecessary to resolve it at present. If that position changes, I expect the Receivers to make immediate application to the Court.

30 I turn to consider the financial position of scheme 16 as it is currently defined. Westpac is a secured creditor. The debt owed to Westpac is secured by real property mortgages over two titles as well as a fixed and floating charge over the assets and undertaking of Glenbelle. An amount is also owing to LGHA. The trading summary indicates that prior to the appointment of the Receivers a substantial sum was paid for services that were to be provided after the appointment of the Receivers. As a result, the available cash flow was negative. That position is expected to continue for the next few months. As a result, during that period at least insufficient revenue is being generated to service the debt.

31 Counsel for the Receivers submitted that after the initial period just described, it remained the position that future forecasted cash flows might be insufficient to service the debt especially when the costs of the receivership were taken into account.

32 Submissions were received from nine investors or groups of investors. It is unnecessary to name each of them. Again, concern was expressed by a number of investors that the sale should proceed in an orderly fashion and not on a fire sale basis. One investor submitted that the sale should be deferred until the market had improved. Other investors supported the Receivers’ recommendations.

33 For the reasons set out in paragraphs [4] and [28] – [31] above, the Receivers sought a power of sale of the property of the scheme numbered 16. Again, the Receivers have proposed that any contract of sale proposed to be entered into would be subject to Court approval. In the circumstances, I would grant the Receivers the power of sale. I am satisfied that the concerns of the investors identified in paragraph [32] above are adequately addressed by the form of orders I propose to make in relation to the power of sale.

|

I certify that the preceding thirty-three (33) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gordon. |

Associate:

Dated: 4 June 2010

Annexure A

|

|

Scheme |

Description of property |

Joint venture manager/s |

|

1. |

211 Wellington Road Joint Venture |

211 Wellington Road, Mulgrave, Victoria |

211 Wellington Road Pty Ltd – Third Defendant |

|

2. |

Healesville Walk Shopping Centre Joint Venture |

251-263 Maroondah Highway, Healesville, Victoria |

Bluemist Holdings Pty Ltd – Fourth Defendant |

|

3. |

Howleys Road Joint Venture |

40-48 Howleys Road, Notting Hill, Victoria |

Dellwood Holdings Pty Ltd – Fifth Defendant |

|

4. |

George Street Joint Venture |

34 George Street, Launceston, Tasmania |

Enmore Enterprises Pty Ltd – Sixth Defendant |

|

5. |

Cimitiere House Joint Venture |

113 Cimitiere Street, Launceston, Tasmania |

Enmore Enterprises Pty Ltd – Sixth Defendant |

|

6. |

Reef House Resort |

99 Williams Esplanade Palm Cove, Qld – The Sebel Reef House Resort |

Firbank Arch Pty Ltd – Seventh Defendant Glenline Pty Ltd – Eighth Defendants |

|

7. |

Queen Street Joint Venture |

118 Queen Street, Melbourne, Victoria |

Gerling Holdings Pty Ltd – Ninth Defendant |

|

8. |

Low Head Joint Venture |

136 Low Head Road George Town, Tasmania, 142 Low Head Road, George Town, Tasmania & 40 Gunn Parade, George Town, Tasmania |

Low Head Village Pty Ltd – Twelfth Defendant |

|

9. |

Nicholson Street Joint Venture |

127-137 Nicholson Street, East Brunswick, Victoria |

Nicholson Street Pty Ltd – Thirteenth Defendant Holloway Crest Pty Ltd – Fourteenth Defendant Rosebery Enterprises Pty Ltd – Fifteenth Defendant |

|

10. |

National Boulevard Joint Venture |

144 National Boulevard, Campbellfield, Victoria |

Rosebery Enterprises Pty Ltd – Fifteenth Defendant |

|

11. |

Simms Investment Project |

626 Pittwater Road, Brookvale, NSW |

Simms Investments Pty Ltd – Sixteenth Defendant |

|

12. |

SY21 Joint Venture |

720-760 Chapel Street, South Yarra, Victoria |

SY21 Retail Pty Ltd – Seventeenth Defendant |

|

13. |

The Glen Centre Joint Venture |

673–681 Glenferrie Road, Hawthorn, Victoria |

The Glen Centre Hawthorn Pty Ltd – Eighteenth Defendant Castello Holdings Pty Ltd – Nineteenth Defendant |

|

14. |

Twinview Joint Venture |

167 Flinders Lane, Melbourne, Victoria |

Twinview Nominees – Twentieth Defendant |

|

15. |

Yarra Valley Golf Joint Venture |

St John of God's Seminary and Henley Farm, Chirnside Park, Victoria |

Yarra Valley Golf Pty Ltd – Twenty-First Defendant Adina Rise Pty Ltd – Twenty-Second Defendant Albright Investments Pty Ltd – Twenty-Third Defendant Ashfield Rise Pty Ltd – Twenty-Fourth Defendant Bradfield Corporation Pty Ltd – Twenty-Fifth Defendant Copeland Enterprises Pty Ltd – Twenty-Sixth Defendant Devlin Way Pty Ltd – Twenty-Seventh Defendant First Hazelwood Pty Ltd – Twenty-Eighth Defendant Glenbelle Pty Ltd – Twenty-Ninth Defendant Glenvale Way Pty Ltd – Thirtieth Defendant Greenview Lane Pty Ltd – Thirty-First Defendant Hallmark Corporation Pty Ltd – Thirty-Second Defendant Moorleigh Holdings Pty Ltd – Thirty-Third Defendant Norton Ridge Pty Ltd – Thirty-Fourth Defendant Raleigh Glen Pty Ltd – Thirty-Fifth Defendant Redcrest Holdings Pty Ltd – Thirty-Sixth Defendant Suri Corporation Pty Ltd – Thirty-Seventh Defendant Sutton Rise Pty Ltd – Thirty-Eighth Defendant The Virtual Mlmer Pty Ltd – Thirty-Ninth Defendant Tivendale Pty Ltd – Fortieth Defendant Tulloch Downes Pty Ltd – Forty-First Defendant Mainking Pty Ltd – Forty-Second Defendant Topglen Pty Ltd – Forty-Third Defendant Allblue Pty Ltd – Forty-Fourth Defendant Aranbay Pty Ltd – Forty-Fifth Defendant |

|

16. |

Glenbelle Project |

Sebel Heritage Lodge Management Lot, Yarra Valley Golf Course, Chirnside Park, Victoria |

Glenbelle Pty Ltd – Twenty-Ninth Defendant Redcrest Holdings Pty Ltd – Thirty-Sixth Defendant |

Annexure B

Annexure C

Annexure D

SCHEDULE OF PARTIES

LGH HOLDINGS LIMITED (ACN 007 191 943)

Second Defendant

211 WELLINGTON ROAD PTY LTD (ACN 092 663 860)

Third Defendant

BLUEMIST HOLDINGS PTY LTD (ACN 097 306 922)

Fourth Defendant

DELLWOOD HOLDINGS PTY LTD (ACN 098 505 803)

Fifth Defendant

ENMORE ENTERPRISES PTY LTD (ACN 082 158 487)

Sixth Defendant

FIRBANK ARCH PTY LTD (ACN 059 464 381)

Seventh Defendant

GLENLINE PTY LTD (ACN 098 532 364)

Eighth Defendant

GERLING HOLDINGS PTY LTD (ACN 091 726 457)

Ninth Defendant

LGH ADMINISTRATION PTY LTD (ACN 007 165 069)

Tenth Defendant

LGH FINANCE PTY LTD (ACN 078 859 248)

Eleventh Defendant

LOW HEAD VILLAGE PTY LTD (ACN 091 731 958)

Twelfth Defendant

NICHOLSON STREET PTY LTD (ACN 069 104 089)

Thirteenth Defendant

HOLLOWAY CREST PTY LTD (ACN 091 731 967)

Fourteenth Defendant

ROSEBERY ENTERPRISES PTY LTD (ACN 091 826 229)

Fifteenth Defendant

SIMMS INVESTMENTS PTY LTD (ACN 093 504 511)

Sixteenth Defendant

SY21 RETAIL PTY LTD (ACN 107 874 564)

Seventeenth Defendant

THE GLEN CENTRE HAWTHORN PTY LTD (ACN 089 906 543)

Eighteenth Defendant

CASTELLO HOLDINGS PTY LTD (ACN 088 204 175)

Nineteenth Defendant

TWINVIEW NOMINEES PTY LTD (ACN 097 307 278)

Twentieth Defendant

YARRA VALLEY GOLF PTY LTD (ACN 066 632 479)

Twenty-First Defendant

ADINA RISE PTY LTD (ACN 083 181 122)

Twenty-Second Defendant

ALBRIGHT INVESTMENTS PTY LTD (ACN 088 204 166)

Twenty-Third Defendant

ASHFIELD RISE PTY LTD (ACN 093 504 806)

Twenty-Fourth Defendant

BRADFIELD CORPORATION PTY LTD (ACN 088 204 371)

Twenty-Fifth Defendant

COPELAND ENTERPRISES PTY LTD (ACN 093 504 824)

Twenty-Sixth Defendant

DEVLIN WAY PTY LTD (ACN 088 264 813)

Twenty-Seventh Defendant

FIRST HAZELWOOD PTY LTD (ACN 093 505 303)

Twenty-Eighth Defendant

GLENBELLE PTY LTD (ACN 097 306 646)

Twenty-Ninth Defendant

GLENVALE WAY PTY LTD (ACN 088 287 021)

Thirtieth Defendant

GREENVIEW LANE PTY LTD (ACN 093 505 312)

Thirty-First Defendant

HALLMARK CORPORATION PTY LTD (ACN 093 505 312)

Thirty-Second Defendant

MOORLEIGH HOLDINGS PTY LTD (ACN 088 287 058)

Thirty-Third Defendant

NORTON RIDGE PTY LTD (ACN 078 821 066)

Thirty-Fourth Defendant

RALEIGH GLEN PTY LTD (ACN 088 204 380)

Thirty-Fifth Defendant

REDCREST HOLDINGS PTY LTD (ACN 100 836 486)

Thirty-Sixth Defendant

SURI CORPORATION PTY LTD (ACN 093 505 321)

Thirty-Seventh Defendant

SUTTON RISE PTY LTD (ACN 088 204 399)

Thirty-Eighth Defendant

THE VIRTUAL MLMER PTY LTD (ACN 065 374 665)

Thirty-Ninth Defendant

TIVENDALE PTY LTD (ACN 093 505 349)

Fortieth Defendant

TULLOCH DOWNES PTY LTD (ACN 078 895 048)

Forty-First Defendant

MAINKING PTY LTD (ACN 100 790 485)

Forty-Second Defendant

TOPGLEN PTY LTD (ACN 096 857 564)

Forty-Third Defendant

ALLBLUE PTY LTD (ACN 100 836 388)

Forty-Fourth Defendant

ARANBAY PTY LTD (ACN 098 532 319)

Forty-Fifth Defendant