FEDERAL COURT OF AUSTRALIA

APF Properties Pty Ltd v Kestrel Holdings Pty Ltd (No 2) [2007] FCA 1561

Held:

1. Vendors made misleading and deceptive representations and were negligent in relation to the croppable area of the properties.

2. Valuer was negligent in relation to the croppable area and value of the properties.

3. In the circumstances valuer owed a duty of care to the purchasers.

4. Valuer’s disclaimer not effective to prevent liability to purchasers.

5. No fiduciary duty owed by vendor to purchasers.

6. Lease of homestead block should not be set aside.

7. Measure of damages was difference between price paid and true value at time of purchase.

8. Damages should include consumer price index adjustment.

9. Value at time of trial was not more than price paid; even if it had been, measure of damage would not be affected.

10. Purchaser’s cause of action arose before effective date of legislation for contributory negligence and proportionate liability.

11. Valuer entitled to full indemnity from vendors.

Trade Practices Act 1974 (Cth) ss 52, 53A(1)(b), 82(1B), 82(2), 84, 87CD

Fair Trading Act 1990 (Tas) ss 14, 17(1)(b)

Wrongs Act 1954 (Tas) ss 3, 4

Civil Liability Act 2002 (Tas) ss 4, 43B

Jones v Dunkel (1959) 101 CLR 298 applied

Australian Communications and Media Authority v Clarity 1 Pty Ltd (2006) 150 FCR 49 cited

Spencer v The Commonwealth (1907) 5 CLR 418 at 432 cited

Henville v Walker (2001) 206 CLR 459 cited

I & L Securities Pty Limited v HTW Valuers (Brisbane) Pty Ltd (2002) 210 CLR 109 applied

Norberg v Wynrib [1992] 2 SCR 226 applied

Pilmer v Duke Group Ltd (2001) 207 CLR 165 applied

Hospital Products Pty Ltd v United States Surgical Corporation (1984) 156 CLR 41 cited

News Ltd v Australian Rugby Football League Ltd (1996) 139 ALR 193 at 311 cited

New Zealand Netherlands Society “Oranje” Inc v Kuys [1973] 2 All ER 1222 applied

Flemington Properties Pty Ltd v Raine & Horne Commercial Pty Ltd (1997) 148 ALR 271 discussed

Potts v Miller (1940) 64 CLR 282 cited

Toteff v Antonas (1952) 87 CLR 647 cited

Gould v Vaggelas (1985) 157 CLR 215 cited

Gates v City Mutual Life Assurance Society Ltd (1986) 160 CLR 1 cited

Wardley Australia Ltd v Western Australia (1992) 175 CLR 514 cited

Kizbeau Pty Ltd v WG & B Pty Ltd (1995) 184 CLR 281 cited

Morgan Corporate Ltd v GWG Leviny Pty Ltd (1995) ATPR 41-414 cited

Munchies Management Pty Ltd v Belperio Pty Ltd (1988) 58 FCR 274 cited

Netaf Pty Ltd v Bikane Pty Ltd (1990) 26 FCR 30 cited

Kenny & Good Pty Ltd v MGICA (1992) Ltd (1999) 199 CLR 413 cited

Henderson v Amadio Pty Ltd (No 1) (1995) 62 FCR 1 cited

Banque Bruxelles Lambert SA v Eagle Star Insurance Co Ltd [1995] QB 375 cited

Banque Bruxelles Lambert SA v Eagle Star Insurance Co Ltd [1997] AC 191 cited

Esanda Finance Corporation Ltd v Peat Marwick Hungerfords (1997) 188 CLR 241 cited

Perre v Apand Pty Ltd (1999) 198 CLR 180 cited

Ta Ho Ma Pty Ltd v Allen (1999) 47 NSWLR 1 discussed

BT Australia Ltd v Raine & Horne Pty Ltd [1983] 3 NSWLR 221 applied

Glass Real Estate Pty Ltd v Karawi Constructions Pty Ltd (1993) ATPR 41-249 cited

Butcher v Lachlan Elder Realty Pty Ltd (2004) 218 CLR 592 cited

Orion Pet Products Pty Ltd v Royal Society for the Prevention of Cruelty to Animals (Vic) Inc (2002) 120 FCR 191 cited

MGICA (1992) Ltd v Kenny & Good Pty Ltd (1996) 140 ALR 313 followed

Baxter v F W Gapp Co Ltd [1939] 2 KB 271 followed

Wardley and King v Yurisich (2006) 153 FCR 78 cited

Burke v LFOT Pty Ltd (2002) 209 CLR 282 applied

C J Gross Land Capability Hand Book, Guidelines for the Classification of Agricultural Land in Tasmania, (2nd ed, Department Primary Industry Water Environment 1999)

W D Duncan (ed) Joint Ventures Law in Australia, (2nd ed, The Federation Press 2005)

TAD 27 OF 2005

HEEREY J

15 NOVEMBER 2007

MELBOURNE (HEARD IN HOBART)

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| TASMANIA DISTRICT REGISTRY | TAD 27 OF 2005 |

| BETWEEN: | APF PROPERTIES PTY LTD Applicant

|

| AND: | KESTREL HOLDINGS PTY LTD First Respondent

NICOLAS GRAEME ROBINSON Second Respondent

ROBINSON INVESTMENT CAPITAL PTY LTD Third Respondent

HALISBWYN PTY LTD TRADING AS MANTACH WHITMORE VALUATIONS Fourth Respondent

HARRISON HUMPHREYS PTY LTD Fifth Respondent

|

| HEEREY J | |

| DATE OF ORDER: | 15 november 2007 |

| WHERE MADE: | melbourne (heard IN HOBART) |

THE COURT ORDERS THAT:

1. Counsel bring in minutes of orders to give effect to these reasons.

2. Further hearing is adjourned to date to be fixed.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| TASMANIA DISTRICT REGISTRY | TAD 27 OF 2005 |

| BETWEEN: | APF PROPERTIES PTY LTD Applicant

|

| AND: | KESTREL HOLDINGS PTY LTD First Respondent

NICOLAS GRAEME ROBINSON Second Respondent

ROBINSON INVESTMENT CAPITAL PTY LTD Third Respondent

HALISBWYN PTY LTD TRADING AS MANTACH WHITMORE VALUATIONS Fourth Respondent

HARRISON HUMPHREYS PTY LTD Fifth Respondent

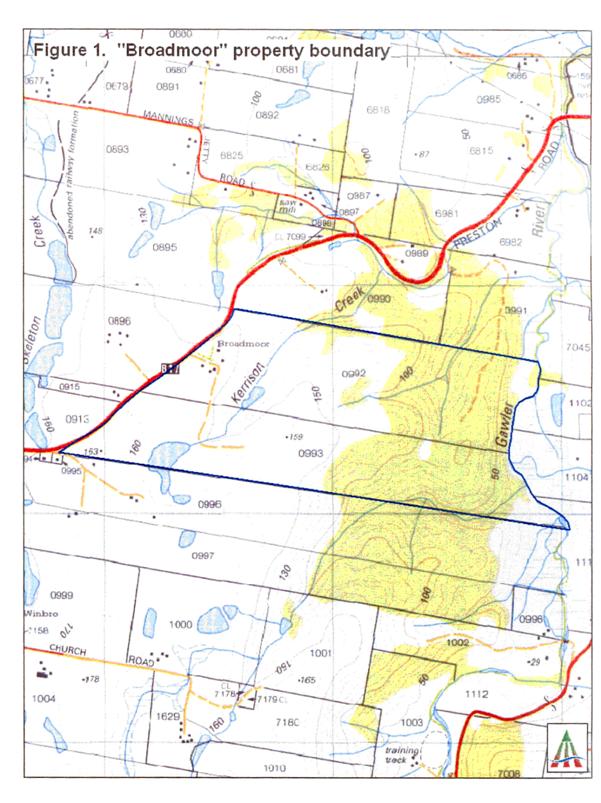

|

| JUDGE: | HEEREY J |

| DATE: | 15 NOVEMBER 2007 |

| PLACE: | MELBOURNE (HEARD IN HOBART) |

REASONS FOR JUDGMENT

TABLE OF CONTENTS

1....... INTRODUCTION........................................................................................................... [1]

2....... APPLICANT’S CLAIMS AGAINST ROBINSONS AND MANTACH........................ [6]

(i) Agtech Representations........................................................................................... [7]

(ii) Robinsons Value Representations.......................................................................... [11]

(iii) Robinsons Representations to Mantach.................................................................. [13]

(iv) Robinsons Price Representations........................................................................... [16]

(v) Robinsons Financial Difficulties.............................................................................. [20]

(vi) Misleading and deceptive conduct of Robinsons..................................................... [22]

(vii) Fiduciary duties..................................................................................................... [23]

(viii) Negligence of Robinsons....................................................................................... [26]

(ix) Damage suffered (as against Robinsons)................................................................. [28]

(x) Lease of Broadmoor homestead block................................................................... [31]

(xi) Misleading and deceptive conduct of Mantach....................................................... [35]

(xii) Negligence of Mantach.......................................................................................... [39]

(xiii) Damage suffered (as against Mantach)................................................................... [41]

3....... ROBINSONS’ DEFENCE TO THE APPLICANT’S CLAIMS.................................... [42]

4....... MANTACH DEFENCE TO THE APPLICANT’S CLAIMS........................................ [61]

5....... ROBINSONS’ CROSS-CLAIM AGAINST MANTACH............................................ [73]

6....... MANTACH CROSS-CLAIM AGAINST THE APPLICANT...................................... [74]

7....... MANTACH CROSS-CLAIM AGAINST THE ROBINSONS..................................... [80]

8....... APPLICANT’S DEFENCE TO MANTACH CROSS-CLAIM.................................... [85]

9....... A BRIEF NARRATIVE OF EVENTS........................................................................... [86]

(i) Earlier valuations of Robinson properties................................................................ [87]

(ii) Negotiations for APF joint venture......................................................................... [92]

(iii) Corporate structure............................................................................................... [99]

(iv) Purchase of Robinson properties.......................................................................... [102]

(v) Forestry leases.................................................................................................... [133]

(vi) Lease of the Broadmoor homestead block........................................................... [134]

(vii) Sale of Robinson properties................................................................................. [139]

10..... DID THE ROBINSONS ADVISE MANTACH OF THE CROPPING AREAS FOR BROADMOOR AND LOWER WILMOT? IF YES, DID NICOLAS ROBINSON HAVE A REASONABLE BASIS TO SO ADVISE?..................................................................................................................... [152]

11..... DID MANTACH RELY ON ADVICE FROM THE ROBINSONS AS TO CROPPING AREAS? WAS IT ENTITLED TO DO SO?............................................................................................. [163]

12..... SHOULD MANTACH HAVE REQUIRED A SOIL SURVEY OR AGRICULTURAL CONSULTANT’S REPORT?.................................................................................................................... [174]

13..... SHOULD THE APPLICANT HAVE SPECIFICALLY REQUESTED AN AGRICULTURAL CONSULTANT’S REPORT FOR CONSIDERATION BY MANTACH?................ [177]

14..... DID MANTACH RELEVANTLY RELY ON THE AGTECH REPORT?................... [178]

15..... WAS THE AGTECH REPORT PROVIDED TO MANTACH FALSE AND/OR MISLEADING? [183]

16..... DID MANTACH RELEVANTLY KNOW THAT THE VALUATIONS WERE REQUIRED FOR A PURCHASER (RATHER THAN A MORTGAGE FINANCIER)?............................. [185]

17..... WAS ROBINSON ACTING AS AGENT FOR BOYDS OR THE APPLICANT WHEN HE MADE ANY MISREPRESENTATION TO MANTACH?............................................................... [195]

18..... DID MANTACH HAVE A REASONABLE BASIS FOR ITS STATEMENT AS TO THE CROPPING AREA ON BROADMOOR AND LOWER WILMOT?.............................................. [198]

19..... DID MANTACH HAVE A REASONABLE BASIS FOR ITS EXPRESSION OF VALUE FOR BROADMOOR AND LOWER WILMOT?................................................................ [199]

20..... DID MANTACH HOLD THE OPINION OF VALUE FOR THOSE PROPERTIES AND WAS THERE SOME PROPER FOUNDATION FOR EACH OF THE EXPRESSIONS OF OPINION?[200]

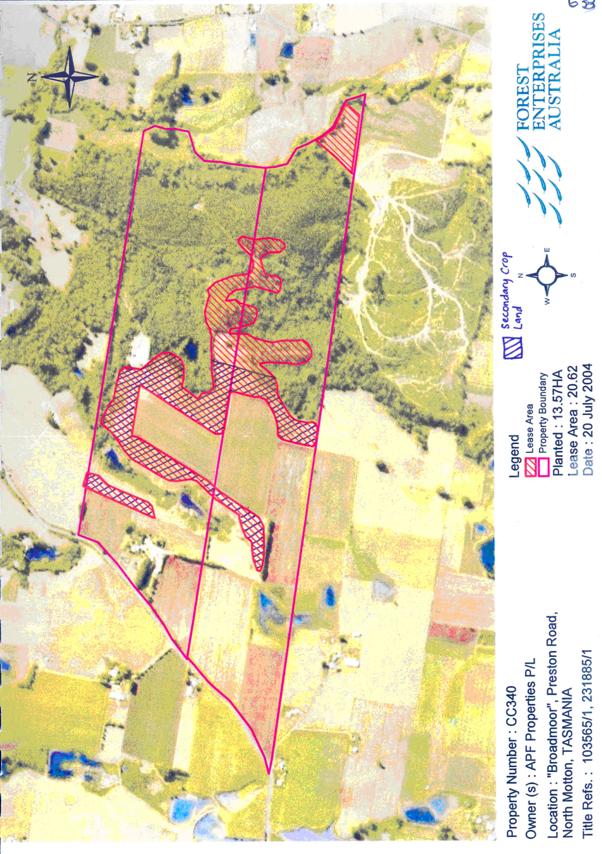

21..... WAS THE RATE PER HECTARE USED BY MANTACH FOR BROADMOOR AND LOWER WILMOT REASONABLE AND/OR WITHIN AN ACCEPTABLE RANGE?........................... [201]

(i) Broadmoor......................................................................................................... [201]

(ii) Lower Wilmot..................................................................................................... [208]

22..... WHAT WERE THE CROPPING AREAS OF BROADMOOR AND LOWER WILMOT?.... [209]

(i) Some background............................................................................................... [209]

(ii) Broadmoor......................................................................................................... [213]

(iii) Lower Wilmot..................................................................................................... [257]

23..... DID THE APPLICANT RELY ON THE MANTACH VALUATIONS IN ENTERING INTO AND SETTLING THE CONTRACT OF PURCHASE FOR BROADMOOR AND LOWER WILMOT? [274]

24..... DID THE APPLICANT RELY ON MANTACH’S OPINION AS TO CROPPING AREA? [280]

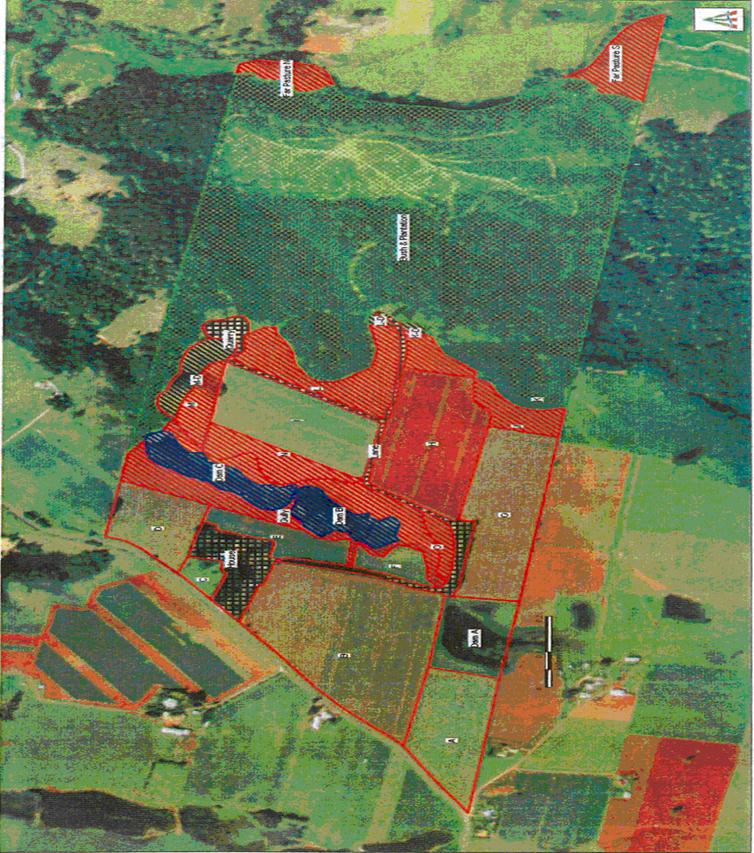

25..... DID THE APPLICANT AND APF KNOW, OR OUGHT THEY TO HAVE KNOWN, BEFORE THE CONTRACTS OF SALE OR SETTLEMENTS, THAT 155 HA OR LESS WAS AVAILABLE TO GROW PYRETHRUM ON THE ROBINSON PROPERTIES?............................................... [281]

26..... WOULD THE ROBINSONS HAVE SOLD THE PROPERTIES FOR LESS THAN THE MANTACH VALUATIONS?.......................................................................................................... [283]

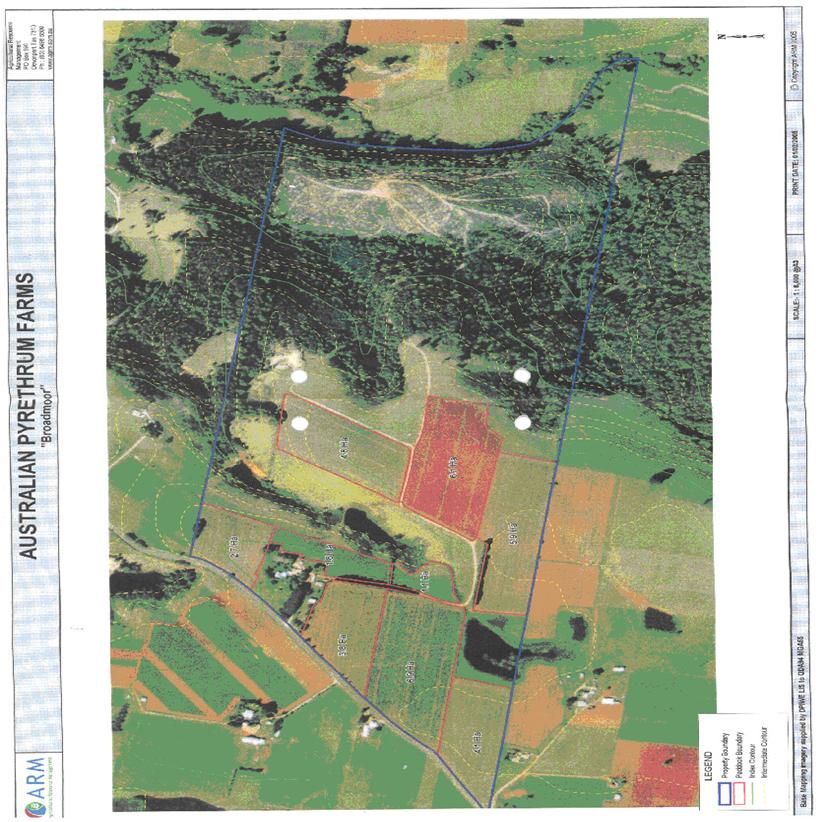

27..... WAS MANTACH’S OPINION AS TO THE APPLICABLE RATE PER HECTARE FOR THE SUBJECT PROPERTIES STILL AN ACCEPTABLE RATE THAT THE APPLICANT WOULD HAVE PAID ANYWAY?................................................................................................................. [286]

28..... DID KESTREL AND NICOLAS ROBINSON MAKE THE AGTECH REPRESENTATIONS AS PLEADED?................................................................................................................. [287]

29..... DID KESTREL AND NICOLAS ROBINSON MAKE THE ROBINSONS VALUE REPRESENTATIONS AS PLEADED?........................................................................................................... [288]

30..... DID KESTREL AND NICOLAS AND CHRISTOPHER ROBINSON MAKE THE REPRESENTATIONS AS TO PRICE AS PLEADED AND WERE THEY RELIED ON BY THE APPLICANT?[289]

31..... DID KESTREL AND NICOLAS ROBINSON OWE FIDUCIARY DUTIES TO THE APPLICANT?.................................................................................................................................... [291]

32..... DID KESTREL AND NICOLAS ROBINSON BREACH ANY FIDUCIARY DUTIES?[293]

33..... WERE THE ROBINSONS REPRESENTATIONS FALSE OR MISLEADING?....... [294]

34..... DID THE APPLICANT RELY ON THE ROBINSONS REPRESENTATIONS?...... [298]

35..... DID KESTREL AND NICOLAS ROBINSON FAIL TO DISCLOSE THE ROBINSONS’ FINANCIAL DIFFICULTIES TO THE APPLICANT?.................................................................... [299]

36..... BUT FOR THE REPRESENTATIONS MADE TO IT WOULD THE APPLICANT HAVE AGREED TO ALLOW ROBINSON INVESTMENTS TO LEASE THE HOMESTEAD BLOCK ON BROADMOOR?.................................................................................................................................... [300]

37..... DID THE REPRESENTATIONS OR BREACH OF FIDUCIARY DUTY CAUSE THE APPLICANT TO LEASE THE BROADMOOR HOMESTEAD BLOCK?............................................. [305]

38..... WHAT WAS THE VALUE OF BROADMOOR AT DECEMBER 2000/ JANUARY 2001? [306]

39..... WHAT WAS THE VALUE OF BROADMOOR AT JULY 2007?............................. [307]

40..... WHAT WAS THE VALUE OF LOWER WILMOT AT JANUARY 2001?............... [312]

41..... WHAT WAS THE VALUE OF LOWER WILMOT AT JULY 2007?........................ [313]

42..... SHOULD CPI BE ALLOWED ON INTEREST OR CAPITAL?................................ [314]

43..... LIABILITY OF ROBINSONS TO THE APPLICANT............................................... [317]

(i) Liability............................................................................................................... [317]

(ii) Damages............................................................................................................. [320]

44..... LIABILITY OF MANTACH TO THE APPLICANT.................................................. [335]

(i) Duty of care........................................................................................................ [335]

(ii) Disclaimer........................................................................................................... [347]

(iii) Misleading and deceptive conduct........................................................................ [351]

(iv) Untruth of representations; negligence.................................................................. [355]

(v) Was the applicant misled? Mr Wright’s role........................................................ [357]

(vi) Reliance and causation......................................................................................... [361]

45..... LIABILITY OF APPLICANT TO MANTACH.......................................................... [364]

46..... CONTRIBUTORY NEGLIGENCE............................................................................ [366]

47..... PROPORTIONATE LIABILITY................................................................................. [370]

48..... CONTRIBUTION BETWEEN RESPONDENTS....................................................... [373]

49..... CONCLUSION.......................................................................................................... [379]

1. INTRODUCTION

1 In 1999 members of the Robinson family owned, either directly or through the first respondent Kestrel Holdings Pty Ltd, three farming properties on the North West Coast of Tasmania. They were known as Broadmoor, Lower Wilmot and Mannings Jetty Road. For some time the Robinsons (a term which, unless the context otherwise indicates, means or includes the first three respondents Kestrel, Nicolas Robinson and Robinson Investment Capital Pty Ltd) had grown crops of pyrethrum on the properties. Pyrethrum, a perennial similar in appearance to a daisy bush, provides an ingredient used in the manufacture of insecticides. The Robinsons grew the crops under contracts to supply a company called Botanical Resources Australia Pty Ltd (BRA) which at the time had a monopoly over the production of pyrethrum in Tasmania.

2 The Robinsons wished to set up a pyrethrum farming operation in opposition to BRA. They engaged a merchant banker, Mr Haydn Wright, to advise and obtain investors. Mr Wright in turn through Boyd Partners Limited (Boyds), a Melbourne firm of Corporate Financial Advisors and Chartered Accountants, obtained investment funds from Mr Andrew Cottrell and Mr Gary Andriske who had farming interests in New South Wales.

3 Through a corporate and trust structure a joint venture called Australian Pyrethrum Farms (APF) was established. The individuals involved were brothers Nicolas and Christopher Robinson, Mr Wright, Messrs Cottrell and Andriske and Mr Andrew Youl whose family farmed at Symmons Plains in the Northern Midlands. The vehicle for the acquisition of the Robinson properties was the applicant company APF Properties Pty Ltd.

4 On 8 August 2001 the applicant completed the purchase of the three Robinson properties for the total sum of $2,193,000 made up as follows:

| Broadmoor | $1,040,000 |

| Lower Wilmot | $753,000 |

| Mannings Jetty Road | $400,000 |

The purchase was partly financed by a commercial bill facility of $1.5 million from the Bank of Melbourne.

5 In this litigation the applicant complains of misrepresentations by the Robinsons as to the value, price and available cropping area of Broadmoor and Lower Wilmot and breach of fiduciary duties and duties of care owed by the Robinsons to their joint venture partners. Negligence is alleged against the fourth respondent, a company carrying on a valuation practice as Mantach Whitmore Valuations (Mantach), in respect of valuations of those two properties provided to the purchaser. (No complaint is made about the purchase of Mannings Jetty Road.) An issue also arises as to the grant by the applicant to the third respondent of a 99 year lease over the homestead block on Broadmoor. The applicant seeks an order setting aside the lease.

2. APPLICANT’S CLAIMS AGAINST ROBINSONS AND MANTACH

6 In its fourth amended statement of claim the applicant raises a number of allegations which may be summarised as follows.

(i) Agtech Representations

7 On 15 January 2001 Nicolas Robinson sent to Mantach a document (the Agtech Report) described in the accompanying fax as “a report by Agtech on our properties”. The Agtech Report purported to come from a firm called Agtech Rural and Horticultural Consultants and to have been prepared for “potential joint venture partners of Australian Pyrethrum Farms (APF Ltd)”.

8 The Agtech Report included statements that Broadmoor had 80 hectares of cropping land and 40 hectares of bush and that Lower Wilmot had 80 hectares of cropping land and 66 hectares of bush and pasture. The Report made comments about other matters such as soils, weed control, irrigation systems and yield projections. It was said that Agtech Rural and Horticultural Consultants specialised in giving advice to agricultural businesses on the North West Coast of Tasmania and had “extensive experience in the Agricultural and Horticultural industry”.

9 In fact, the land available for cropping was 35.9 hectares on Broadmoor and 50.5 hectares on Lower Wilmot. Moreover, the entity Agtech Rural and Horticultural Consultants did not exist. The Agtech Report was the creation of Nicolas Robinson.

10 The Robinsons made the representations in the Agtech Report (the Agtech Representations) fraudulently in order to induce Messrs Cottrell and Andriske and the applicant to invest in the purchase of Broadmoor and Lower Wilmot.

(ii) Robinsons Value Representations

11 Between November 2000 and May 2001, in the course of negotiations for the joint venture proposal and the acquisition of the Robinson properties, the Robinsons represented (the Robinsons Value Representations) that Broadmoor was worth well in excess of $1 million and Lower Wilmot well in excess of $750,000.

12 In fact the value of Broadmoor was closer to $700,000 and that of Lower Wilmot closer to $450,000.

(iii) Robinsons Representations to Mantach

13 On 29 November 2000 Boyds on behalf of Messrs Cottrell and Andriske instructed Mantach to value Broadmoor and Lower Wilmot.

14 In the course of Mantach’s preparing its valuations the Robinsons (a) made representations to it that there were 80 hectares of land suitable for cropping pyrethrum on each of Broadmoor and Lower Wilmot (the Robinsons Representations to Mantach) and (b) provided the Agtech Report to Mantach.

15 The Robinsons intended, or knew or ought to have known (as in fact proved to be the case), that Mantach would rely on the Robinsons Representations to it and the Agtech Report in making its valuations of Broadmoor and Lower Wilmot.

(iv) Robinsons Price Representations

16 Between January and May 2001 the Robinsons represented to the applicant (a) that it was necessary for the benefit of the joint venture for the pyrethrum seed to be planted at Broadmoor and Lower Wilmot without delay, (b) that Mantach and another valuer Harrison Humphreys (the fifth respondent, against whom no relief is now sought) had undervalued the two properties, and (c) that the Robinsons would not sell the properties unless they received a higher price. They also procured Mr Wright to represent on their behalf to Boyds that there were certain defects in the Mantach and Harrison Humphreys valuations and that the price of Broadmoor and Lower Wilmot ought to be higher.

17 In January 2001 Christopher Robinson sent a letter to Mr Wright, with the intention that it be sent on to Boyds and their client investors, as in fact it was. In the letter Christopher stated that he was a registered valuer in Tasmania, number 1108, carrying on business as Christopher E Robinson Valuations, and that the value of Broadmoor was $1,363,686 and the value of Lower Wilmot was between $1,135,017 and $1,135,542.

18 In fact, Christopher Robinson was not a registered valuer in Tasmania and did not carry on the business alleged.

19 The representations alleged in [16]-[18] are herein referred to as “the Robinsons Price Representations”.

(v) Robinsons Financial Difficulties

20 At the time of the negotiations for the purchase of the properties the Robinsons were indebted to the Commonwealth Bank of Australia in the sum of approximately $2.1 million.

21 On 17 April 2001 the Bank appointed Paul John Cook as its agent as mortgagee in possession and as receiver and manager of the properties.

(vi) Misleading and deceptive conduct of Robinsons

22 By reason of the above-mentioned Representations, and their failure to disclose their financial difficulties, the Robinsons engaged in conduct that was misleading and/or deceptive contrary to ss 52 and 53A(1)(b) of the Trade Practices Act 1974 (Cth) and ss 14 and 17(1)(b) of the Fair Trading Act 1990 (Tas).

(vii) Fiduciary duties

23 As promoters of the joint venture the Robinsons owed fiduciary duties to the applicant (a) not to permit a conflict between their personal interests and their duty to carry out a task in the interests of the applicant, (b) to account to the applicant for any benefit obtained by them by use of their fiduciary position, and (c) to disclose to the applicant all knowledge relevant to the decision made by it to engage in the dealing with them.

24 In breach of their fiduciary duties the Robinsons made the Representations to the applicant.

25 In further breach of their fiduciary duties, the Robinsons procured for themselves prices for Broadmoor and Lower Wilmot in excess of the true value of those properties, failed to account to the applicant for that part of the purchase price which exceeded the true value of the properties and failed to disclose to the applicant their financial difficulties.

(viii) Negligence of Robinsons

26 The Robinsons owed the applicant a duty of care (a) to ensure the accuracy of material facts provided by them to it which might relate to it’s decision to purchase Broadmoor and Lower Wilmot and (b) to disclose all material facts which might relate to the decision to purchase the two properties.

27 The Robinsons breached their duty of care.

(ix) Damage suffered (as against Robinsons)

28 In purchasing Broadmoor and Lower Wilmot, the applicant relied on the Representations.

29 By reason of its reliance on the Representations and the misleading and deceptive conduct, breaches of fiduciary duty and negligence of the Robinsons, the applicant has suffered loss and damage in that it paid $303,000 and $340,000 in excess of the true value of, respectively, Broadmoor and Lower Wilmot. It has also incurred extra financing costs.

30 Alternatively, the applicant claims $643,000 from the Robinsons as money had and received, being the amount paid in excess of the true value of Broadmoor and Lower Wilmot.

(x) Lease of Broadmoor homestead block

31 By a lease dated 29 August 2003 the applicant leased the homestead and curtilage on Broadmoor consisting of 1.683 hectares to the third respondent Robinson Investment Capital Pty Ltd for a term of nine years with further options for a total of 99 years.

32 Robinson Investment Capital knew or ought to have known that the applicant had agreed to purchase Broadmoor, and lease the homestead block, as a result of the Representations. Had it not been for those Representations the applicant would not have leased the homestead block to Robinson Investment Capital.

33 In the premises Robinson Investment Capital engaged in misleading and deceptive conduct in contravention of s 52 of the Trade Practices Act and s 14 of the Fair Trading Act.

34 The lease of the homestead block contributes to the loss of value of Broadmoor and should be set aside.

(xi) Misleading and deceptive conduct of Mantach

35 In valuing Broadmoor and Lower Wilmot Mantach relied on the Robinson Representations to Mantach and the Agtech Report.

36 Mantach knew or ought to have known that Boyds would communicate the Mantach valuations to a client or clients who would rely on such valuations and statements in them in deciding whether to invest in or purchase the properties.

37 By written valuation reports dated January 2001 Mantach represented to Boyds that:

(a) the value of Broadmoor was $1,040,000;

(b) Broadmoor had 82 hectares of cropping land available;

(c) the value of Lower Wilmot was $753,000;

(d) Lower Wilmot had 70 hectares of cropping land available.

In fact:

(a) the value of Broadmoor was closer to $700,000;

(b) Broadmoor had 35.9 hectares of cropping land available;

(c) the value of Lower Wilmot was closer to $450,000;

(d) Lower Wilmot had 50.5 hectares of cropping land available.

38 In the premises Mantach has engaged in conduct which was misleading and/or deceptive contrary to ss 52 and 53A(1)(b) of the Trade Practices Act and ss 14 and 17(1)(b) of the Fair Trading Act.

(xii) Negligence of Mantach

39 Mantach owed the applicant a duty to make proper and diligent enquiries to determine the land available for cropping, to exercise the care, competence and diligence of a competent valuer and to give fair and accurate advice in relation to the value of the properties and the area available for cropping.

40 In breach of its duties Mantach:

(a) relied on the advice of the Robinsons and the Agtech Report to determine the area of land available for cropping;

(b) failed to make any or any adequate enquiries about the information in the Agtech Report;

(c) failed either to commission an agricultural report to accurately determine the land available for cropping or to advise Boyds or the applicant to commission such a report;

(d) relied on information contained in Tasmap 1:25,000 maps to determine the area of land available for cropping;

(e) failed to identify accurately the land available for cropping;

(f) failed to utilize accurately the comparable sales evidence available.

(xiii) Damage suffered (as against Mantach)

41 The applicant has suffered the same damage as that alleged against the Robinsons.

3. ROBINSONS’ DEFENCE TO THE APPLICANT’S CLAIMS

42 Unless otherwise indicated, the Robinsons put in issue the allegations made against them. In particular, they deny that any of the matters alleged against them had any causative effect on the decision of the applicant to purchase the Robinson properties or to lease the homestead block. Reliance is in issue.

43 The Robinsons admit that Nicolas Robinson prepared the Agtech Report. They deny they made the Agtech Representations fraudulently. They deny that they intended the Agtech Report to be accepted as professional advice in relation to the feasibility of successful pyrethrum farming on Broadmoor and Lower Wilmot.

44 They do not admit making the Robinsons Value Representations.

45 They admit that Boyds, on behalf of Messrs Cottrell and Andriske, instructed Mantach to value Broadmoor and Lower Wilmot.

46 They deny they made the Robinsons Representations to Mantach. They gave the Agtech Report to Mantach after it had completed its inspection and valuation and after it had, on 16 January 2001, provided its valuations to Boyds.

47 They deny that Mantach relied on the Robinsons Representations to Mantach or the Agtech Report in making its valuations of Broadmoor and Lower Wilmot.

48 Save that they admit that Mr Wright made representations on their behalf as to the price of Broadmoor and Lower Wilmot, they deny making the Robinsons Price Representations.

49 They deny that Christopher Robinson made any representations as to valuation qualifications and say that any cause of action arising therefrom is outside “the relevant limitations period”.

50 They put in issue all elements of the applicant’s claims of misleading and deceptive conduct and breach of fiduciary duties.

51 As to the negligence claim, the Robinsons deny the existence of any duty of care to the applicant, that they were in breach of any such duties, or that Messrs Cottrell and Andriske or the applicant relied on any of the Representations in their decision to purchase Broadmoor and Lower Wilmot.

52 Further, they say that the applicant devalued Broadmoor and Lower Wilmot by (a) granting, on 10 August 2004, forestry leases over portions of those properties and (b) requiring Robison Investment Capital to lease the homestead block on Broadmoor.

53 They say the applicant imposed as a condition of sale that Robinson Investment Capital purchase the Broadmoor homestead block. Subsequently local planning restrictions made subdivision impossible and the alternative of a 99 year lease was adopted.

54 They seek to set off against any amount for which they are found liable the amounts received by the applicant from Forest Enterprises Australia Ltd (FEA).

55 The Robinsons raise a plea of contributory negligence. They say the applicant

(a) limited its instructions to Mantach to a request for “a formal valuation of the freehold interest”;

(b) failed to clarify with Mantach the criteria of cropping land;

(c) failed to obtain, or instruct Mantach to obtain, a suitably qualified agricultural consultant to advise as to the area of croppable land;

(d) purchased the properties when it knew or ought to have known that the area of 155 hectares or less was available to grow pyrethrum on the three properties.

56 By reason of the contributory negligence of the applicant, the Robinsons are entitled to have their liability reduced by reason of s 82(1B) of the Trade Practices Act and s 4 of the Wrongs Act 1954 (Tas).

57 Any loss in relation to Broadmoor was caused or contributed to by (a) the 99 year lease of the homestead block and (b) by the creation of the forestry lease.

58 Any loss in relation to Lower Wilmot was caused or contributed to by the creation of the forestry lease.

59 The applicant sold Lower Wilmot in August 2004 for $450,000 whereas its true market value was at least $750,000. It failed to mitigate its loss. It failed to obtain a valuation to set a reserve, failed to allow a lengthy marketing and sale period and marketed the property too late in the cropping cycle. The Robinsons rely on s 82(1B) of the Trade Practices Act and s 4 of the Wrongs Act.

60 Any liability should be limited as between the Robinsons and Mantach as concurrent wrong doers having regard to their responsibility for the damage and loss under s 87CD of the Trade Practices Act and s 43B of the Civil Liability Act 2002 (Tas).

4. MANTACH DEFENCE TO THE APPLICANT’S CLAIMS

61 Mantach says that on 29 November 2000 it received instructions from Boyds to value the three properties in the belief and understanding that it was to prepare a valuation for mortgage lending purposes.

62 In the course of an inspection for an earlier valuation in March 1997 Nicolas Robinson represented to it that there were 80 or 82 hectares of land on Broadmoor and 70 hectares on Lower Wilmot used for cropping purposes. Those representations were repeated and/or not withdrawn by Nicolas Robinson at the time of the 2001 valuations.

63 Its valuation reports in 2001 were addressed to and intended for use by Boyds for mortgage lending purposes only. Its understanding was that if Boyds wanted a lender or any other person to rely on the valuation reports they would ask that person to write to Mantach to ask that the report be addressed to that other person.

64 The valuation reports were made subject to the following disclaimer:

We state that this report is for the use only of the party to whom it is addressed and for no other purpose, and no responsibility is accepted to any third party for the whole or part of its contents.

65 Mantach admits it considered the Robinson Representations and considered and relied on the Agtech Report in carrying out its valuations, along with other factors and information available to it. It denies knowing that either was inaccurate.

66 Any loss of the applicant was caused by its contributory negligence in:

(a) not instructing Boyds to clearly specify the intended recipient of and the purpose for which the Mantach valuations were to be used;

(b) relying on the Representations;

(c) failing to conduct due diligence regarding the ownership of the properties and regarding the joint venture;

(d) failing to instruct it to obtain an independent agricultural consultant’s report;

(e) failing to advise that the valuations were required for the purpose of potential purchases and not mortgage lending.

67 By reason of the contributory negligence of the Robinsons, Mantach is entitled to have its liability reduced by reason of s 82(1B) of the Trade Practices Act and s 4 of the Wrongs Act.

68 Any loss in relation to Broadmoor was caused or contributed to by (a) the 99 year lease of the homestead block and (b) by the creation of the forestry lease.

69 Any loss in relation to Lower Wilmot was caused or contributed to by the creation of the forestry lease.

70 Nicolas Robinson, as the agent of the applicant, knew the areas of land at Broadmoor and Lower Wilmot used for cropping purposes and was not misled as to anything to this effect in Mantach’s valuation reports. His knowledge is to be imputed to the applicant pursuant to s 84 of the Trade Practices Act and the general law.

71 The applicant sold Lower Wilmot in August 2004 for $450,000 whereas its true market value was at least $750,000. It failed to mitigate its loss. It failed to obtain a valuation to set a reserve, failed to allow a lengthy marketing and sale period and marketed the property too late in the cropping cycle. The Robinsons rely on s 82(1B) of the Trade Practices Act and s 4 of the Wrongs Act.

72 Any liability should be limited as between it and the Robinsons as concurrent wrong doers having regard to their responsibility for the damage and loss under s 87CD of the Trade Practices Act and s 43B of the Civil Liability Act.

5. ROBINSONS’ CROSS-CLAIM AGAINST MANTACH

73 Kestrel and Nicolas Robinson seek contribution from Mantach under s 3 of the Wrongs Act.

6. MANTACH CROSS-CLAIM AGAINST THE APPLICANT

74 The applicant represented to Mantach (a) that the valuations of Broadmoor and Lower Wilmot were required by the Robinsons and not for a potential purchaser of the properties, (b) that Mantach need not obtain an independent agricultural consultant’s report, and (c) that it was appropriate for Mantach to rely on the Robinsons’ statements as to the areas used for cropping purposes.

75 These representations were implied from the circumstances that:

(a) the applicant was aware that Mantach had prepared the 1997 and 1999 valuations for the Robinsons for mortgage lending purposes;

(b) the 2001 Mantach valuations expressly stated that no independent soil reports were being obtained;

(c) the 2001 valuations were sent to Boyds with a compliments slip addressed to Boyds “for your client Robinson”;

(d) the applicant did not tell Mantach that it required the valuations for the purpose of purchase of the properties.

76 If it is found (contrary to Mantach’s case) that the 2001 valuations were prepared for the purpose of potential purchase, that Mantach should have obtained an independent agricultural consultant’s report and/or that Mantach was not entitled to rely on the Robinsons’ statements as to the area of land used for cropping purposes, then the representations referred to in [75] were misleading.

77 In reliance on the representations Mantach valued the properties. Had it known the representations were misleading it would not have done the valuations at all or would have qualified its valuation reports.

78 The applicant has thus engaged in conduct that was misleading or deceptive or likely to mislead or deceive, contrary to s 52 of the Trade Practices Act.

79 Mantach has suffered loss and damage because in the absence of the representations Mantach would not have valued the properties at all, or would have placed appropriate qualifications or disclaimers on the valuations. In that event this proceeding would not have been brought against Mantach and it would not have been exposed to actual or potential loss, including liability for damages interest and costs.

7. MANTACH CROSS-CLAIM AGAINST THE ROBINSONS

80 In the event that the Court finds that Mantach is liable to the applicant, Mantach seeks from Kestrel and Nicolas Robinson contribution to an extent as shall seem just and equitable under s 3 of the Wrongs Act.

81 Further, Kestrel and Nicolas Robinson represented to Mantach that Broadmoor and Lower Wilmot had 80 and 70 hectares respectively used for cropping purposes.

82 These representations were made orally at the time Mantach carried out earlier valuations of the properties for the Robinsons in 1997 and 1999 and between 29 November 2000 and January 2001 when Mantach was carrying out the valuations the subject of this proceeding.

83 The representations were also made in the Agtech Report and are also to be implied from the fact that the Robinsons did not correct the areas recorded in the 1997 and 1999 valuations provided by Mantach.

84 If it is found that there were not 80 hectares of land suitable for cropping pyrethrum at Broadmoor and there were not 70 (or 80) hectares of such land at Lower Wilmot (all of which Mantach denies) then Kestrel and Nicolas Robinson were negligent and engaged in misleading and deceptive conduct contrary to s 52 of the Trade Practices Act and s 14 of the Fair Trading Act.

8. APPLICANT’S DEFENCE TO MANTACH CROSS-CLAIM

85 Mantach filed its cross claim after the expiration of the limitation period prescribed by s 82(2) of the Trade Practices Act.

9. A BRIEF NARRATIVE OF EVENTS

86 In this section I shall briefly outline the sequence of events. Following that I shall address the issues raised by the pleadings. The definition of legal and factual issues appearing hereafter in these reasons generally corresponds with a template prepared and agreed on by counsel at my request.

(i) Earlier valuations of Robinson properties

87 In August 1992 Mr Brian Chandler of Richardson & Wrench (Tas) Pty Ltd valued Broadmoor for the Westpac Bank. The Robinsons had a copy of the valuation. It valued Broadmoor at $560,000 and included the following

Areas Cleared

Approximately 52 hectares of cropping land.

Approximately 30 hectares of grazing slopes and flats.

Balance – bush, dams and waste areas.

88 In 1997 a finance broker Mr Ray Cross instructed Mantach to value the Robinson properties on behalf of the Hobart legal firm Piggott, Wood and Baker which was a prospective mortgagee. Mantach duly provided valuations of Broadmoor and Lower Wilmot dated March 1997. Mr Brian Mantach conducted an inspection of the property on 14 March 1997. He valued Broadmoor at $1,022,000. His report stated his instructions as follows:

My instructions are to establish the current fair market value of the property for mortgage security purposes. Instructions have been issued by Mr Ray Cross, Finance Broker of 88 Main Street, Sheffield, on behalf of the Robinson family. Lender is Piggott, Wood and Baker.

Under the heading “Description” there was a description of the land in the two titles which comprised the property. It was in these terms:

Description

P 0992 comprises approximately 42 ha of near level upper banks and gently sloping hillside ranging from the 150 metre contour down to the 100 metre contour. Kerrison Creek runs through this land forming a permanent water supply. The balance land in this title is steeper undulating land that remains as bush.

P 0993 contains approximately 40 ha of mostly near level banks and gentle slopes that is [sic] used for cropping purposes with the remainder of the property being undulating in nature and containing bush. The soils on the cleared land are red basalt in nature, mostly stone free and very suitable for cropping purposes. The area has an average rainfall of around 37 inches and predominant land use in the area, apart from cropping in its various forms is for dairying, fat lambs and beef cattle.

Under the heading “Site Improvements” there appeared the following:

The property is now exclusively used for cropping purposes. By scaling off a map and by discussions with the owners, there is [sic] approximately 82 ha of gently undulating banks and slopes that have been cleared and are used for cropping purposes. The remaining 40 ha of the property is bush. The boundary is fenced with standard post and wire fencing plus there is some internal fencing of a similar nature. A gravel roadway provides access through the property. [Emphasis added]

After detailing six comparable sales the valuation calculations were set out. Buildings and chattels totalled $142,000 (rounded). Land was $880,000 as follows:

82 ha of red cropping land @ $10,000/per ha 820,000

40 ha of bush @ $1,500/per ha 60,000

89 A valuation also dated March 1997 for Lower Wilmot was based on inspection of that property on the same date as Broadmoor. The valuation was $753,000. It included a figure for 70 ha of “cropping land” at $8000 per hectare.

90 In July 1999 Mantach provided further valuations of Broadmoor and Lower Wilmot for the Robinsons for mortgage lending purposes. The descriptions of cropping land and the values assessed were the same as in the 1997 valuations.

91 In November 1999 at the request of the Robinsons, Mantach “assigned” its valuations to the Commonwealth Bank, that is to say, Mantach made the valuations available to the Bank for its use, obviously enough for security purposes. Mantach did not charge the bank but did charge the Robinsons.

(ii) Negotiations for APF joint venture

92 In mid 1999 the Robinson brothers and Mr Andrew Youl commenced research into the possibility of establishing a company for the growing of pyrethrum. They had in mind securing a hybrid seed capable of producing high yields and securing holdings of 1000 ha cropping land.

93 In November 1999 Mr Haydn Wright was introduced to the Robinsons as a person who might assist them to find investors. On 24 November 1999 Australian Bio-Pharmaceuticals Pty Ltd (ABP) was incorporated. The founding members were the Robinson brothers, Mr Wright, Mr Youl and Mr Nigel Blair who had experience in insurance.

94 In July 2000 Messrs Cottrell and Andriske, clients of Boyds, were introduced to the project by Mr Joff Macleod of that firm. They were given an information memorandum which included two financial models prepared by Mr Wright. One was a “red” model and the other a “grey” model. The two models assumed operations on, respectively, the red soils of the North West Coast or the grey soils of the Northern Midlands.

95 Messrs Cottrell, Andriske and Macleod made several visits to Tasmania and had discussions with the Robinsons. Messrs Cottrell and Andriske told the Robinsons that in their view the grey model was far superior because the land was cheaper and could be operated more profitably. However, Nicolas Robinson persuaded them that red soil was preferable because it had better drainage properties. He told them the Robinson family had been growing pyrethrum for almost 10 years, were BRA’s biggest grower and had the top yielding crop. In answer to Messrs Cottrell and Andriske’s query as to why they were needed if pyrethrum farming was so easy and so profitable, Nicolas Robinson said that they had debt against their properties and could not raise extra money to buy new properties. They wanted to buy more properties through BRA, but BRA was inherently conservative and would not allow them to do that.

96 In the course of one of their trips to Tasmania, Messrs Cottrell and Andriske inspected the Robinson properties and other farming properties on the North West Coast. The Robinsons said that the price of red cropping land was about $7000 per hectare but their own land was worth more. However, no specific price was put on the Robinson land at this stage.

97 By November 2000 the various parties were committed to the project. Up until this stage the Robinsons did not wish their land to be considered for the project. However, in November this attitude changed and it was agreed that the Robinson properties should be purchased by the joint venture. Broadly speaking, the scheme was that the Robinsons would run operations under the overall direction of Mr Youl. Messrs Cottrell and Andriske would provide the equity capital.

98 About this time arrangements were made to import seed from a firm called Pyagra Inc in Arizona, USA. Importation was seen to introduce a note of urgency to finalise the sites for the venture.

(iii) Corporate structure

99 On 5 December 2000 the applicant and APF Investments Pty Ltd were incorporated. Mr Wright was appointed as sole director of the applicant and Mr Macleod as sole director of APF Investments.

100 Leaving aside, for the sake of clarity, trust arrangements, the structure of the joint venture was as follows. The operating company was Australian Pyrethrum Farms Pty Ltd. Its share capital was divided into equal numbers of A class and B class shares. The A class shares were held by APF Investments, in which the Cottrell and Andriske interests each had a 50 per cent shareholding. The B class shares were owned by ABP. That company’s shareholding was divided between the Robinsons and Messrs Wright, Youl and Blair. Holders of B class shares were not entitled to a share of profits until the return on investment to APF Investments reached 25 per cent.

101 Australian Pyrethrum Farms was to lease the properties from the applicant in which the beneficial interests, again via trusts, were shared between APF Investments and ABP, but with the latter having a deferred interest contingent on APF Investments obtaining a 25 per cent return.

(iv) Purchase of Robinson properties

102 In November 2000 a meeting was held at the office of Boyds in Melbourne. Present were the Robinson brothers and Messrs Wright, Macleod, Blair, Cottrell and Andriske. In his evidence Mr Cottrell described the meeting in these terms:

Right and what – was there any particular aspect of proceedings at that stage that sparked the discussion about the property purchase?---Yes, well, the discussion at that stage was that we knew we had seed coming and that they wanted to get it in straight away.

Right?---And it was pretty clear that Robinsons’ property was the only one we could practically get prepared in time to actually put the seed in, so that brought up how do we actually get the properties. It was agreed by everyone that we would buy them. It was agreed that the homestead would be subdivided as the Robinsons wanted to keep their family home, which we felt was fair enough. In the scope of what we were looking at then as well we weren’t looking at selling the property back and worrying about the homestead. That was going to be one of many properties we were going to buy over the next 12 months. We discussed the properties and the Robinsons weren’t keen on getting valuations, they didn’t like that idea, but we just couldn’t agree to just simply handing them over whatever price they wanted to put on it, and it was the only [way?] we could practically agree to getting a purchase. So it was agreed to get two valuations and it was agreed to abide by them.

103 On 29 November Boyds wrote to Mantach requesting a valuation of the three Robinson properties. The letter stated (formal parts omitted):

REQUEST FOR VALUATION IN RELATION TO THE FOLLOWING PROPERTIES:

□ P.2600 Mannings Jetty Road, North Motton,

□ P 0992 & P 0993 Broadmoor RA 403 Preston Main Road,

□ UPI Nos. 1155-1159 Wilmot Road, Lower Wilmot.

We hereby instruct Mantach Whitmore Valuations to prepare a formal valuation of the freehold interest in the above properties.

We require the following issues to be considered in performing this assignment:

□ The valuations is [sic] to be carried out in accordance with the definition of Market Value as defined by the International Assets Standards Committee;

□ The valuation should be based on an arms length market valuation;

□ The valuation reports must be signed by the undertaking Valuer and any other person duly required in relation to the Firm’s Professional Indemnity Insurance;

□ We require full disclosure of the Valuation Methodology including calculations, rationale and any assumptions; and

□ The valuation is urgent and must be completed without delay.

Prior to undertaking the assignment, would you please provide an indication of your fee for our approval together with the proposed completion date.

Should you have any queries or require any further information, please do not hesitate to contact us.

104 On 29 November Boyds gave instructions to Mr Andrew Cubbins of Harrison & Humphreys in similar terms.

105 On 5 January 2001 Mr Wright wrote to Pyagra confirming that ABP would plant 500 acres of land in January 2001 and that the land specified had a land volume in excess of 500 acres. The letter stated that the land was “owned by the Robinson Family who are known to Pyagra”.

106 On 9 January Mr Cubbins of Harrison & Humphreys wrote to Boyds advising of valuations of $820,000 for Broadmoor and $575,000 for Lower Wilmot and stating that full valuation reports would follow.

107 On 15 January Mantach wrote to Boyds stating that Mr Brian Mantach had inspected the three properties and that detailed valuation reports were being prepared. Figures were given as follows:

Mannings Jetty Road $400,000

Broadmoor $1,040,000

Lower Wilmot $753,000

The letter stated that at Broadmoor “(a)bout 82 hectares of … land comprises good red basalt type soils that are very suitable for intensive cropping purposes. The balance comprises land that was until recently bush but which has now been pushed and partly cleared”. Lower Wilmot had “about 70 hectares of good cropping land”.

108 On 16 January Nicolas Robinson faxed a copy of the Agtech Report to Mantach. The covering letter said:

Dear Brian,

Please find attached a report by Agtech on our properties.

Yours faithfully,

Nic

109 On the same day Boyds gave instructions to Mr Noel Ware of Ware & Otlowski, solicitors, to act on behalf of Cottrell and Andriske in relation to the purchase of the three properties. The letter enclosed contracts of sale which were “subject to the vendors providing final confirmation of clear title and final price negotiation”.

110 On 18 January Mr Wright emailed Boyds referring to their meeting of the same date and advising that subsequent discussions with the shareholders of ABP confirmed that the land would be sold to the applicant at $2,300,000 “unless reasonable argument can be shown to the contrary”. The email also stated that seed would be on hand within days and that ABP would commence planting “irrespective of the contemplated agreements being finalised”.

111 Some time in late January Mantach sent formal valuations of the properties to Boyds. They were accompanied with a compliments slip in these terms:

With Compliments

To: J J McLeod

Enclosed please find the Valuation Report as requested for your client, Robinson

Thank you for your instructions in this matter.

Regards

Brian Mantach

The words underlined were handwritten.

112 In the Broadmoor valuation under the heading “Client and Instructions” the report stated:

My instructions are to prepare a formal valuation of the freehold interest in the property. Instructions have been issued by Boyd Partners Limited.

The interest valued was stated to be “Freehold interest assuming vacant possession” and the valuation $1,040,000. The description of the land in each title was identical with that of the Mantach 1997 valuation (see [88] above), except that the title references themselves were different. The description under the heading “Site Improvements” was the same, except that the sentence italicised was replaced by “The remaining 40 ha of the property was bush much of which has recently been cleared”. Seven comparable sales showing brief details of improvements, cropping areas and price were set out. Another nine were noted in more summary form.

113 Under the heading “Summation Valuation” figures were attributed to various improvements and to 82 hectares of “Red cropping land” at $9500 per hectare.

114 Under the heading “Qualifications and Assumptions” it was said (par (j)) that while the valuer had “taken every reasonable care both during our inspection of the property and in making relevant enquiries, we have not undertaken or requested” a number of enquiries and searches, including “soil survey”. It was also stated (par l):

We state that this report is for the use only of the party to whom it is addressed and for no other purpose, and no responsibility is accepted to any third party for the whole or part of its contents.

115 The Lower Wilmot valuation was for the same figure ($753,000) as the 1997 valuation. It contained the same qualifications and assumptions as the 2001 Broadmoor valuation.

116 On 25 January Mr Wright wrote to Boyds criticising the valuations and in particular those of Cubbins. The letter concluded:

The Robinson’s [sic] have argued that a figure far in excess of the Mantach Whitmore valuation could be achieved on the open market given the cropping history and water systems on their properties would make them highly sought after. The consideration requested is $2,300,000 and this is obviously an issue that must now be dealt with to see how consensus on price can be achieved.

The letter enclosed what was described as a

separate analysis provided by Chris Robinson in respect of the comparable data noting in particular where the comparable is distinguishable by property use.

117 That letter is headed “Christopher E. Robinson Valuations” and is signed under a description “Christopher E. Robinson (BBUS PROP VAL, IM) REGISTERED VALUER NO: 1108”. After noting some favourable features of the Robinson properties and criticising the valuations, particularly those of Cubbins, it included the following:

Please note there is a long history of cropping land sales that show an overall rate above $9000 per hectare. If this rate is applied to the Robinson Group’s 315.38 hectares, $2,838,420 results.

118 After the Mantach and Cubbins valuations were received there was a meeting in Melbourne. According to Mr Cottrell, the Robinsons (or at least Nicolas, he could not be sure if Christopher was present) were very unhappy about the valuations. They felt they grossly under-valued their properties and that to agree to them would be to give away some of their family heritage cheaply and would be discounting all the work they had done on their farms.

119 The stand taken by Cottrell and Andriske was that without some reason they could not agree to pay more than the valuations, so they would pay the (higher) Mantach valuation. The original agreement had been that the parties would get two valuations and split the difference, but as it turned out the Robinsons were not happy with either valuation. After this meeting negotiations continued between Macleod on behalf of the Cottrell and Andriske side and Wright on behalf of the Robinsons.

120 On 29 January Mr Wright emailed Boyds confirming discussions to the effect that Nicolas Robinson would “need $2,300,000 [to] pay out family with reimbursement to investors at subdivision”.

121 On 1 February Mr Wright wrote to Boyds referring to a recent conversation confirming purchase for the price equal to the Mantach valuations on terms of 10 per cent deposit with 30 days settlement. The letter also stated:

That the Robinson Group will purchase the homestead property together with any land required for subdivision purposes from the applicant upon achieving subdivision. The purchase price will be equal to that stipulated in the Mantach Whitmore valuations. Any cleared land that is included in the subdivision will be purchased by the Robinson Group at the valuation price of $2,500.00. Any cropping land required for subdivision will be purchased for nil consideration subject to that land being leased to the applicant on a 99- year basis.

122 No mention had been made in the Mantach valuation of Broadmoor of any sale back of the homestead property. It is not suggested that this issue was raised with Mr Mantach.

123 On 15 February Boyds on the letterhead of APF Investments sent to Mr Wright a letter, later referred to as the Letter of Understanding, “document(ing) the intention of the parties” in relation to the purchase of the properties by the applicant from the Robinsons for $2,193,000 made up as follows:

Broadmoor 1,040,000

Lower Wilmot 753,000

Mannings Jetty Road 400,000

The valuations were said to “reflect the values provided by Mantach Whitmore”. Settlement was to be on terms of 10 per cent deposit and balance on “not less than 30 days or as soon as practicable thereafter”. It was noted that the Robinsons had agreed to purchase the homestead on Broadmoor from the applicant, subject to a subdivision of title. The subdivided area would include the homestead and would be “the minimum amount permitted under planning restrictions”. The price was to be the value placed by the Mantach valuation on the homestead and associated improvements ($118,770) plus for any cleared land “the valuation price of $2500 per hectare”. If cropping land was included in the subdivided property it was to be leased back to the applicant for $1 per year.

124 On 27 February the Pyagra seed arrived in Australia but was detained in quarantine.

125 On 14 March the Commonwealth Bank notified the Robinsons that they were in default, that the Bank was seeking to end the banking relationship and would issue letters of demand shortly. The total amount alleged to be due was approximately $2,335,000. On 17 April the bank appointed Paul John Cook as receiver and manager of Kestrel and related companies.

126 In March Messrs Cottrell and Andriske visited the properties again in the company of the Robinsons and Mr Wright. They discussed issues concerning BRA. The Robinsons had told BRA of the sale and the latter wanted the buyers to take over the existing contracts. Obviously that would not be possible if the buyers were to plant their own pyrethrum, so BRA wanted the crop eradicated, which ultimately occurred. The Cottrell/Andriske legal advice was that contracts of sale could not be signed until BRA confirmed they agreed to their plants being eradicated.

127 On 27 March a Shareholders Agreement was executed. The parties were ABF (the Robinson, Wright and Youl interests), APF Investments (the Cottrell and Andriske interests) and Australian Pyrethrum Farms (the joint venture vehicle). The recitals included statements to the effect that the first stage of the project comprised an initial planting of 500 hectares of pyrethrum in 2001, that the parties intended to expand the project “on a prudent basis” to at least 1000 hectares, and that APF Investments agreed to fund a minimum level of 1000 hectares.

128 On 27 April a meeting of the Board of APF was held at the Youl property at Symmons Plains. Those present included Messrs Cottrell, Macleod, Youl and Wright and Messrs Andriske and Nicolas Robinson as guests. Mr Wright advised that the Pyagra seed release was imminent and that BRA had no capacity to caveat or claim an interest in the Robinson land. On that basis the Board resolved to sign the purchase contracts.

129 Contracts of sale were exchanged on 11 May 2001 with Cottrell and Andriske as purchasers. Subsequently Cottrell and Andriske nominated the applicant as purchaser.

130 The Broadmoor contract contained a term (cl 15.2) for the sale back of the homestead “together with its relevant land and improvements when it is subdivided by the Purchaser and this area including the homestead shall be the minimum amount permitted by the relevant Planning Laws and Regulations”. The vendor undertook to “submit a Subdivision Plan to the Central Coast Council to achieve a separate Certificate of Title to the subdivided property”. The purchase price was to be equal to that stipulated for the homestead and improvements in the Mantach valuation (a total of $118,770) plus cleared land at the “valuation price of $2,500 per hectare”. It was further provided that if “cropping land (was) included in the Subdivided Property, that land must be leased back to the Purchaser for a rental of $1.00 per year”. The clause demonstrates that the parties proceeded on the assumption that all cleared land is not necessarily cropping land.

131 Some problems arose with contamination of a seed bank from Pyagra.

132 Ultimately the contracts were settled on 30 August 2001. In the meantime the Bank of Melbourne (Westpac) had confirmed finance for the purchasers. On 2 July Westpac emailed Mantach stating that it wished to rely on the January 2001 valuations addressed to Boyd Partners “for mortgage purposes relating to proposed Pyrethrum farming”. In a reply of the same date Mantach stated that it had provided valuation reports to Boyds in January 2001 and that the reports “are assigned to Westpac Banking Corporation and may be used and relied on by the bank for mortgage lending purposes”. The valuations were confirmed as still being current. As the reports were being assigned to Westpac “for the same client” no fee would be charged.

(v) Forestry leases

133 In December 2002 the applicant granted leases over portions of Broadmoor and Lower Wilmot to FEA for forestry purposes. The areas leased were approximately 25.5 ha (Broadmoor) and 38 ha (Lower Wilmot) and the rentals were $175 per hectare per annum (Broadmoor ) and $150 per hectare per annum (Lower Wilmot). Both leases were to commence on 31 December 2002 and terminate on 31 December 2022.

(vi) Lease of the Broadmoor homestead block

134 On 28 November 2001, pursuant to the Letter of Understanding and the contract of sale, the Robinsons submitted a proposal to the Central Coast Council for the subdivision of the homestead block. On 20 February 2002 the Council rejected the application on the grounds that it was contrary to the applicable Planning Scheme and the State Policy on the Protection of Agricultural Land.

135 On 28 March 2003 Nicolas Robinson forwarded a proposal to Australian Pyrethrum Farms for a 99 year lease of the homestead block on payment of $123,700 ($118,770 for improvements and $5000 for five acres of land).

136 The Cottrell and Andriske interests sought legal advice on the proposal. They were concerned as to the loss of functionality in that no accommodation would be available for a farm manager, and that there would be a loss of value if and when APF Investments chose to sell Broadmoor.

137 Mr Noel Ware of Ware & Partners in a letter of 10 April advised that

…there is no way this condition [in the Letter of Understanding] can be read to include a 99 year lease between the parties if the Robinsons application to subdivide the homestead lot was refused, which it was.

Consequently I believe APF [Properties] has no legal obligation to enter into any form of lease 99 years or otherwise with the Robinsons for the homestead block.

If circumstances have changed since the Letter of Understanding and Contract were entered into between the parties then in our opinion APF [Properties] can either refuse to contemplate leasing the property to him or lease it to him on such terms as can be agreed.

138 There was in evidence a letter dated 9 July 2003 from APF Investments to Westpac signed by Mr Cottrell which refers to extreme disappointment “due to misrepresentation of vendors and negligence of valuers”. Mr Cottrell’s evidence was that the letter was sent over a year later, in August 2004, and the date was mistakenly recorded. In any event, after some further correspondence between the Robinsons and Mr Cottrell concerning the precise area of the homestead block, a lease between the applicant and Robinson Investment Capital was executed on 29 August 2003. The area of the homestead and curtilage was approximately 1.67 hectares. The term, including options, was 99 years. The rental was $122,945 payable within three months and thereafter one dollar per annum. The lease was registered at the Lands Titles Office.

(vii) Sale of Robinson properties

139 By the end of 2003 the project was in trouble. A major factor was the collapse of the market for pyrethrum. The top American insecticide manufacturer switched to a synthetic source. Kenya, the world’s leading producer, had a bumper harvest after many lean years. Management disputes also arose. In early June 2004 it was resolved to put the three properties on the market.

140 Mr Robert Medwin, then with Roberts Real Estate Agency in Ulverstone, was retained as agent for the sale. Mr Medwin has worked in real estate on the North West Coast for over 40 years. He would sell about 60 rural or rural residential properties in a year. He said in evidence, and I accept, that over the years he has accumulated very specific knowledge about the North West Coast of Tasmania including but not limited to the topography, land areas, soil type, climate, land use and compatibility for varied farming purposes.

141 Mr Medwin was familiar with the three Robinson properties and had been so for about 40 years. He could remember “off the top of [his] head” three preceding owners of the properties before they came into the hands of the Robinsons. In early July 2004 he met with, amongst others, Mr Bill MacDonald the CEO of APF, Mr Youl and Christopher Robinson for the purpose of inspecting the three properties.

142 They commenced with an inspection of Broadmoor. Christopher Robinson told Mr Medwin that it was a 300 acre property and that 160 acres was presently planted to crops. Mr Medwin said that he could not see that there were 160 acres (64.7 hectares) being cropped. He asked Mr Robinson for a copy of the paddock plan and crop rotation details. Mr Medwin observed that Broadmoor had steep contours and a large area of the land was bush and planted with forest.

143 A week or two after that meeting Mr Medwin obtained copies of the paddock plan and crop rotation plans together with aerial maps of the property held by FEA. He looked at the Tasmap 1: 25,000 map and formed the view there was “no way” that 64.7 hectares of the property was cropped or capable of being cropped. Some of the land also appeared to be of poor quality soil and would not be worth clearing. He obtained a copy of the water licence. As a rule of thumb one hectare of cropping land will require a licence for 1 ML (1 million litres) of water. The water licence for Broadmoor was 43 ML. He reached the conclusion that 40 hectares of land was capable of being used for cropping purposes.

144 On the same day in early July 2004 Mr Medwin inspected Lower Wilmot. He asked Mr Robinson for the same details as he had for Broadmoor and one or two weeks later was given a copy of the paddock plan and crop rotation details. The paddock plan showed 54 hectares of cropping land. The total water allocation was 63.5 ML. Mr Medwin estimated the total area being 52 hectares. The eight paddocks shown on the paddock plan had an individual size of 54 hectares.

145 In June 2004 Mr Medwin submitted a marketing proposal to Mr MacDonald. It stated that Broadmoor had “40 hectares of pine [sic] cropping land in a sort [sic] after area” and that at Lower Wilmot “52 hectares is prime cropping land”. The proposal gave estimated prices of $600,000 to $650,000 for Broadmoor and $420,000 to $460,000 for Lower Wilmot.

146 The proposal recommended sale by auction with advertising over a five week period in specified Tasmanian newspapers and internet display. In his evidence Mr Medwin defended the length of the advertising campaign, saying

the longer you give purchasers, the more likely they are to procrastinate. Intensive and short advertising campaigns are more likely to attract the market.

147 On 19 June 2004 Mr Medwin received an email from Mr Youl in which Mr Youl calculated the “total cropping area” for Broadmoor as approximately 40 hectares plus probably 5 to 7 hectares taken up with the dam gully, existing dam chemical storage area sheds and access roads, the balance of the 122.43 hectares being existing forest and a small mix of potential cropping land now planted with trees by FEA with the remaining steeper land not suitable for cropping now also planted out with trees. Mr Youl calculated the total cropping area for Lower Wilmot as approximately 60 hectares with the balance of 147.05 hectares taken up with existing forest and non-cropping ground now committed to trees planted by FEA, existing dam areas, ground storage areas, chemical wash down area with evaporation pit, overhead tank and access roads.

148 Some time in July/August, and after he submitted his figures to Mr MacDonald, Mr Medwin received a copy of the Mantach 2001 valuations. They gave him great concern. He disagreed with them in terms of the land area available for cropping and the price.

149 There was a lot of interest in Broadmoor after it was advertised. Mr Medwin took about fifteen couples over the property. Lower Wilmot did not attract the same amount of interest. Mr Medwin considered it not to be in a prime cropping area. It was further inland and relatively isolated.

150 The auctions of all three properties were conducted by Michael Warren, the Manager of Roberts, at the Ulverstone Civic Centre on 10 August 2004. There were approximately 40 persons in attendance. The reserve prices supplied by Mr MacDonald the previous day were Broadmoor $1,000,000; Lower Wilmot $450,000 and Mannings Jetty Road $400,000. Mannings Jetty Road sold at auction at or about the reserve price. Lower Wilmot was passed in and sold shortly after the auction for $450,000. The sale was negotiated with the only bidder. There was no bidding for Broadmoor.

151 I now turn to the factual and legal issues as defined by counsel.

10. DID THE ROBINSONS ADVISE MANTACH OF THE CROPPING AREAS FOR BROADMOOR AND LOWER WILMOT? IF YES, DID NICOLAS ROBINSON HAVE A REASONABLE BASIS TO SO ADVISE?

152 The evidence of Mr Mantach was that for the purposes of the 1997 valuations he inspected the Robinson properties on 14 March 1997. He went first to Broadmoor where Nicolas and Christopher Robinson were living in the homestead. He drove around Broadmoor in the company of Nicolas Robinson. He made a file note which is headed by the words “P992 and 993”. Underneath there is a plus and minus sign and the figures and words “200 ac cleared”. The numbers P 992 and 993 refer to the two titles which made up Broadmoor. Two hundred acres referred to a statement that Nicolas Robinson made to him that 200 acres of the property had been cleared. Two hundred acres is roughly 81 hectares. Mr Robinson told him that all the cleared land was used for cropping purposes.

153 At the time of his inspection Mr Mantach had with him a 1:25,000 Tasmap of the area. The map was produced in 1992 from aerial photography carried out in 1988. The Tasmap 1:25,000 maps are published by the Tasmanian Department of Environment and Planning. They are produced from aerial photographs taken at irregular intervals. They show title boundaries (although stated to be not authoritative) and topographic detail including roads and watercourses. Forested areas are coloured green. Contour intervals are 10 metres with 50 metre index contours.

154 After the inspection of Broadmoor, which took about an hour, Nicolas Robinson and Mr Mantach drove to Mannings Jetty Road and then to Lower Wilmot which is about 16 kms south of Broadmoor. Nicolas Robinson told him that there was 70 hectares of cropping land at Lower Wilmot. Mr Mantach also had with him the Tasmap for this area.

155 After the inspection Mr Mantach returned to his office in Launceston. On 21 March Nicolas Robinson faxed him some information. Mr Mantach said in his evidence that he has since learned that this material was extracted from a valuation report produced by Mr Brian Chandler dated 24 August 1992 (see [87] above). He never received the full version of the Chandler Report until he was given it by his solicitors in April 2007. As already noted, the Chandler Report gave an area for Broadmoor of approximately 52 hectares of cropping land and approximately 30 hectares of grazing slopes and flats. However, what was said to be the extracts from the Chandler Report faxed to Mr Mantach in March 1997 obviously come from a different document than the Chandler Report which was in evidence. They are in a different font. In the 1997 document there is the following passage:

2.7 Areas Cleared

The following land types exist on the property;

· [X] hectares chocolate loams, varying from level to sloping ground.

· [X] hectares non arable grazing land

· [X] hectares, watercourse and 3 dams.

Where the X appears a figure has been obliterated. Opposite the first dot point appears the handwritten figure 40. Opposite the other two dot points there is a bracket and the handwritten figure 6. The significance of this document and the differences between it and the Chandler Report were not explored in evidence. In any event, Mr Mantach had not requested the information faxed to him. He assumed it was taken from some other report and he already had the material in it so he did not pay much attention to it.

156 In preparing his 1997 valuation report Mr Mantach used a scale rule to calculate the amount of cleared land shown on the Tasmaps for Broadmoor and Lower Wilmot. This exercise involved marking regular geometric shapes on the cleared (non-forested) area shown in the map, calculating the area of those shapes from the scale and then estimating the area of such irregular shapes as remained. This process produced in the case of Lower Wilmot an area of 70 hectares, which was consistent with the figure Nicolas Robinson had given him. However in the case of Broadmoor the scaling indicated a cleared area of 68 ha. In his witness statement Mr Mantach said:

I telephoned Nicolas Robinson to discuss the discrepancy. I specifically recall him telling me that the Robinsons had done some clearing at the edge of the bush since the time the map had been created in 1992, and that accounted for the difference. He had previously told me that all the cleared land was used for cropping purposes.

157 It will be recalled in his 1997 valuation (see [88] above) Mr Mantach stated that

[b]y scaling off a map and by discussions with the owners there is [sic] approximately 82 ha of gently undulating banks and slopes that have been cleared and are used for cropping purposes.