FEDERAL COURT OF AUSTRALIA

Arms v WSA Online Limited (ACN 081 121 495) FCA [2005] 943

SIMON ARMS v WSA ONLINE LIMITED (ACN 081 121 495) (Subject to a Deed of Company Arrangement), JAMES HOUGHTON and JAMES STUDENT

VID 228 of 2001

RYAN J

8 JULY 2005

MELBOURNE

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

VICTORIA DISTRICT REGISTRY |

VID 228 of 2001 |

|

BETWEEN: |

SIMON ARMS Applicant

|

|

AND: |

WSA ONLINE LIMITED (ACN 081 121 495) (Subject to a Deed of Company Arrangement) First Respondent

JAMES HOUGHTON Second Respondent

JAMES STUDENT Third Respondent

|

|

RYAN J |

|

|

DATE OF ORDER: |

8 JULY 2005 |

|

WHERE MADE: |

MELBOURNE |

THE COURT ORDERS THAT:

1. There be judgment for the applicant against the first respondent in the sum of $58,331.00.

2. The application as against the second and third respondents be dismissed.

3. The application stand over to a date to be fixed for receiving submissions on the questions of interest and costs.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

VICTORIA DISTRICT REGISTRY |

VID 228 of 2001 |

|

BETWEEN: |

SIMON ARMS Applicant

|

|

AND: |

WSA ONLINE LIMITED (ACN 081 121 495) (Subject to a Deed of Company Arrangement) First Respondent

JAMES HOUGHTON Second Respondent

JAMES STUDENT Third Respondent

|

|

JUDGE: |

RYAN J |

|

DATE: |

8 JULY 2005 |

|

PLACE: |

MELBOURNE |

REASONS FOR JUDGMENT

The background facts

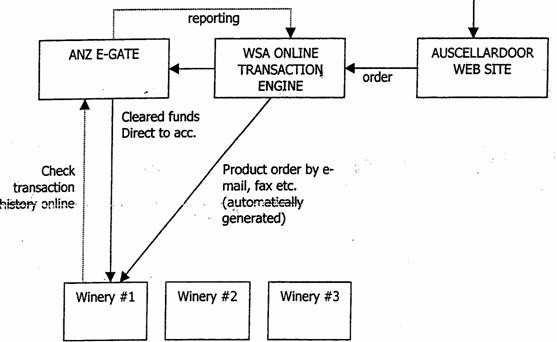

1 The applicant, Arms (“Arms”) had been engaged as Sales and Marketing Manager of Eyton Winery at Coldstream in Victoria until March 1999. Before his resignation from Eyton Winery, after discussion with other people in the wine industry, Arms conceived, the idea of providing a market service for small to medium independent wineries by means of the Internet. He envisaged that a website would be established under the name “auscellardoor” to which retail purchasers would have access to identify wines available from participating wineries and, if so minded, to make purchases of wines which they had selected. It was contemplated that payments would be made by credit card processed through an “e-Gate” facility to be provided by the ANZ Bank. Once the transfer of funds from the purchaser had been cleared, they would be credited, after deduction of a small transaction charge, directly to the account of the vendor winery which was to have its own “merchant agreement” with ANZ e-Gate. Income was to be generated for auscellardoor by charging a commission of 5% on each sale effected through the Internet.

2 The attraction of the concept for participating wineries was that they would pay, on sales effected through the Internet, tax at the rate applicable to “cellar door” sales and would avoid the need to pay a margin, usually of the order of 30%, to agents or distributors who arranged the sale of the wineries products to retail outlets.

3 As he refined the concept, Arms proposed to become an “online wine facilitator” of sales of wine from small to medium wineries directly to the public by means of a website which Arms, through auscellardoor, would own and operate. To that end, he conceived a “business plan”.

‘An opportunity exists to market cellar door business through the Internet, using one site to facilitate the “cellar doors” of a group of wineries.

However to market individual (small) wineries on the Internet is costly, and Internet browsers are looking for sites that accomplish many needs. Individual wineries may be hard to find and limited in the market they cater for. They are unlikely to generate “hits” from clients who are unfamiliar with them.

auscellardoor can accomplish both with a catchy and marketable name and list many small to medium wineries for both sales and information.

The marketing of this business will be in two areas. The marketing to the wineries and then the marketing to the potential customers wishing to buy and/or visit the web site, either to make a purchase or for winery/wine information.

The marketing to the wineries will begin with a launch that stretches 6 months in each wine region in Australia. Each targeted winery will receive a presentation kit, contract and follow up call and visit from myself. In addition, advertising will be aimed specifically at the wineries and operators through Grapegrower and Winemaker and at Wine Australiawhich takes place in November 2000 in Melbourne.’

5 These projections were made of the income stream and capital requirements of auscellardoor in its establishment phase and the early months of its operation:

‘As consumers visit our web site, orders will be then made through auscellardoor and will be forwarded to the relevant winery. A 5% commission will be incurred on all sales and wineries will be invoiced quarterly along with the monthly subscription.

The aim of this business is to offer an alternative selling/marketing opportunity to small-medium sized wineries through what will be a recognised web site address. The launch phase of the business relies on a 20% success rate (170 wineries) in acceptance of the wineries, with a 12 month commitment growing to 26% (250 wineries) by June 2001 and 42% (400 wineries) by December 2002. Sales targets are based on cases per winery over the forecast. I have made assumptions further into the document which I consider to be ultra conservative.

The funding required will be primarily for start up costs which include computers, web page design and set up, software and advertising. Revenue does not begin until May 2000 when advertising begins. My projected costs are in detail further in this document but I anticipate $30,000 is required for commencement. This figure is based upon starting requirements until June 2000 when the first revenue, in the form of subscription payments, will be due.’

|

PROFIT RETURN TO WINERIES |

|

|

RETAIL |

AUSCELLARDOOR |

|

Model 1 |

|

|

$ 90.00 wholesale |

$ 90.00 wholesale |

|

$ 63.00 Agent/Distributor margin 30% |

|

|

|

|

|

$ 90.00 retailer purchase price |

|

|

$126.90 41 % sales tax |

$ 22.23 tax at 26% |

|

$ 10.57 LUC |

|

|

$ 13.75 selling price (30% margin) |

$ 13.00 selling price |

|

|

$ 1.30 auscellardoor (5%) |

|

Return to Winery |

Return to Winery |

|

$ 5.25 per bottle or $ 63.00 per case |

$ 9.45 per bottle or $113.50 per case |

|

Model 2 |

|

|

$150.00 wholesale |

$150.00 wholesale |

|

$105.00 Agent/Distributor margin 30% |

|

|

|

|

|

$150.00 retailer purchase price |

|

|

$211.50 41 % sales tax |

$ 39.00 tax at 26% |

|

$ 17.62 landed unit cost |

$ 22.00 selling price |

|

$ 22.91 selling price (30% margin) |

$ 1.10 auscellardoor (5%) |

|

Return to Winery |

Return to Winery |

|

$ 8.75 per bottle or |

$ 17.65 per bottle or |

|

$105.00 per case |

$211.80 per case |

7 The first column indicates the expected return to the winery on a sale to a retail outlet effected through an agent or distributor and the second column indicates the expected return to a winery if the same wine were sold through auscellardoor’s website.

8 The business plan expressly contemplated that auscellardoor would use the services of the first respondent, WSA Online Limited (“WSA”). In mid-December 1999 Arms met with Julie McDowell and the third respondent, James Student (“Student”), who were representatives of WSA. He outlined to them his proposal for online wine sales and gave them a “draft outline” of a business plan. He emphasised the need for secure processing of electronic payments for purchases made through the website which would not be handled by the business which, it was proposed, would derive income from a commission charged to participating wineries.

9 According to Arms, Ms McDowell and Student told him that his business model was the perfect way to set up an Internet business and that they had extensive experience in designing websites like that which he proposed.

10 Arms also said that he was told that WSA could design a website which could securely process electronic payments between wineries and purchasers, manage “business to consumer” transactions and process orders from customers to participating wineries. As well, according to Arms, Ms McDowell and Student represented that WSA had the expertise to design and construct a website for the business and had recently designed or developed websites for Transurban and the ANZ Bank.

‘Phase 1

Initial scope of Ozcellardoor.com.au

- strategic recommendations

- logistics of web site

- Site map

- media and loyalty initiatives

- project timings

- cost estimate of subsequent phases

4,000

Creation of presentation kit

- Overview of concept for presentation to cellars

- Ozcellardoor.com.au web site graphics

- Cellar page

- Limited interactive presentation tool

8,500 – 12,500

Phase 2

Web site and administration function production

- Completion of web site

- Completion of administration function

- Administration user tuition

- ISP account creation and web site registration

8,000 – 15,000

Ongoing costs

- ISP monthly account charge 100 - 200

- Support as required from WSA Online 1,000 – 1,500

Phase 3

Media initiatives

- To be discussed’

12 At the same time, Arms gave Student a revised version of his business plan which included passages from which extracts have been reproduced at [4] to [6] above.

‘Phase 1

Initial scope of auscellardoor.com.au and creation of presentation kit

- Outline of strategy promotional and market model $1600

- Website look and feel and mock-ups $6200

- PowerPoint or other interactive presentation $2480

- Brochure/promotional material

- Design $2480

- Film & print 1000 $2100

Total $14860

Phase 2

Strategy

Complete detailed marketing strategy and program $3600

Web site and administration function production

Completion of web site

Completion of administration function

Administration user tuition

ISP account creation and web site registration

$8,000 - $15,000’

14 Later, on about 10 January 2000, Arms signed a quotation bearing that date which was in substantially the same terms as the quotation described at [13] above. Thereafter, Arms had several meetings with Student in the course of one of which Student furnished him with a document dated 23 January 2000 which essentially embodied a marketing strategy for targeting the two groups of customers whom auscellardoor needed to enlist, being the subscribing wineries and the purchasers of wine online to whom the product of the wineries would be sold.

15 On 31 January 2000, WSA rendered an invoice to Arms for $7,340 for work described as “Initial Development of Strategy and presentation kit.” Payment was made on that invoice on or about its date.

16 At one of their meetings in late January 2000, Student introduced Arms to the second respondent, James Houghton (“Houghton”) whom, according to Arms, Student described as the “guru of interactive website design and development.” At that meeting or shortly afterwards, Houghton told Arms that he was aware of a financial transactions product called “ANZ e-Gate” which would be “perfect” for Arms’ business and would enable payments to be made by visitors to the website by means of all major credit cards in return for which each winery would pay a transaction fee of between 2% and 2.5%.

‘ANZ has a new product called e-gate, which is a transaction clearing facility in the same vein as Surelink, but with a number of advantages.

The initial discussion was relating to Auscellardoor - looking at a way to have a single e-commerce structure and engine that would allow e-commerce purchases to be cleared directly into the bank account of the relevant winery.

ANZ are happy to set up a system where WSA is the prime e-gate client, with each of the member wineries (or any other WSA clients) as individual merchants:

This means that while the wineries have their own merchant agreement with ANZ e-gate, and they can go online to review their transactions at any time, all transaction reports will flow via WSA.

Once WSA has set up an e-gate interface and account, additional wineries (or any other businesses) can be added to the system by simply filling in a form and paying a small set up fee (costs are coming soon).

This effectively gives WSA an EPOS cleared e-commerce engine where all transactions are cleared direct into the third party business' bank account without the set up costs associated with setting up single clients through surelink or the like, and an integrated reporting and stats function across all accounts.’

‘Key benefits:

▪ Auscellardoor will market your products to the world.

▪ Auscellardoor will return you around twice as much as traditional distributors.

▪ Auscellardoor gets you online with minimum fuss - you get your own web site, where your customers can purchase online. You can even register your own Internet domain name.

▪ Auscellardoor gives personal visitors to your cellar door an easy way to order in the future without visiting/phoning/faxing - through your own web site.

▪ Every existing customer you move online (rather than sell by phone or mail order) will save you time and administration costs.

▪ Auscellardoor gives small wineries a level playing field online.

▪ Auscellardoor promotes winery tourism and visits.

Why is auscellardoor different?

▪ Nobody else offers you your own web site, e-commerce facilities plus central marketing.

▪ Auscellardoor does not require you to process credit card transactions - it's all orders are already cleared.

▪ Auscellardoor clears each transaction direct into your bank account through ANZ. And you can check your transaction history online 24 hours a day.

▪ Auscellardoor is independent and passionate about the wine industry.

▪ Auscellardoor is professionally developed using the marketing, design and technical expertise of the B&T Interactive Agency of the year, WSA Online.’

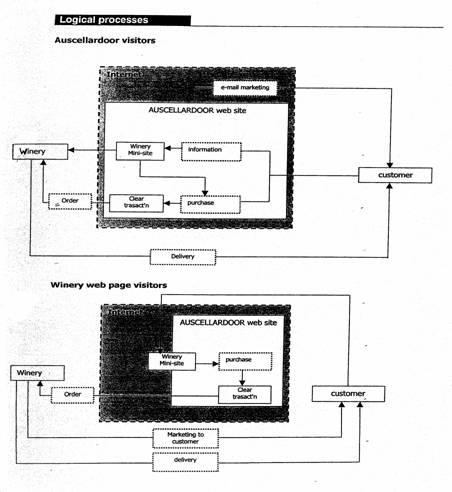

19 In about mid-March 2000, at another meeting, Student and Houghton gave Arms a further document descriptive of the business of auscellardoor which contained these passages:

‘Auscellardoor will be positioned as a directory of small and medium, sized wineries. Each winery will have its own page (or mini-site as required) giving general information about the winery, with a facility to order wines 'direct from the cellar door'.

Users will also be able to search for wines by variety, style and region across all wineries. This lends the site a versatility that other wine sites do not offer, being useable as:

· A directory of wineries.

· Home pages for individual wineries.

· An online wine retailer.

Wineries will be charged a basic subscription to the service ($100 per month), which will include a basic home page and the e-commerce transaction facilities. Auscellardoor will levy a 5% commission on sales for handling the transaction. It is anticipated that wineries will be able to purchase more sophisticated 'mini-sites' at additional cost.

Deliveries will be organised directly by the wineries.’

‘Multi-purpose site for users

The Auscellardoor site can fulfil a number of functions for users:

· A wine industry information resource.

· A wine tourism planning resource.

· An e-commerce retailer.

The use of appropriate editorial could be used to emphasise some or all of these aspects.’

‘Objectives of phase 1 marketing

Establish Auscellardoor as an innovative, unique and exciting online venture.

Establish Auscellardoor membership as a win-win proposition for wineries that delivers:

· A low-cost e-commerce web presence.

· An easy method for existing customers to make repeat purchases.

· Easier administration of sales through electronic transactions (when compared with mail-order or telephone transactions).

· A better margin than retail on sales.

· New business through Auscellardoor promotion of the site.

Establish the Auscellardoor organisation and venture as honest, substantial, likely to succeed, and having the best interests of the Wineries at heart.

Create an easy path to signing-up with Auscellardoor.’

20 In relation to those flow diagrams, Houghton explained that a visitor to the website would make a purchase, the transaction would be cleared and the order placed with the winery which would deliver direct to the customer.

21 After his successive meetings, principally with Houghton and Student, Arms decided to retain WSA to design and construct the auscellardoor website and to use the ANZ e-Gate facility. During February and March, Arms began approaching wineries with a view to their participating in the website. To that end, WSA produced a “trade presentation kit” which included a form on which each winery was to provide bank details to enable moneys to be deposited in its account, a brochure and a mock-up of the website contained on a compact disc. The brochure extolled the benefits of auscellardoor for the wineries but did not descend to particulars of the mechanism for effecting credit card payments. It did note, under the heading “The benefits to you”:

‘Currently, a $100 sale to the distributor will gross the winery approximately $6 per bottle. An equivalent sale from the cellar door will earn close to $14 per bottle. On the same $100 sale, taking into consideration all setup and transaction costs, aus cellardoor will return approximately $12 per bottle.’

22 In the course of his approaches to various wineries, Arms represented that, for each purchase made from the website, the winery would receive a payment from the customer’s credit card after transaction fees had been deducted, that credit card transaction fees were between 2% and 2.5% and a commission of 5% would be payable to auscellardoor after the sale had been processed. It was further stated that the winery would receive at least 92.5% of the retail sale price and have to pay a monthly subscription of $100 to auscellardoor.

‘I agree to participate on the auscellardoor.com.au internet site. / agree to pay $100 per month subscription and a 5% commission on sales for purchases made via auscellerdoor.com.au web site. I understand that this commitment is for a minimum of 12 months.

I am aware that / must inform auscellardoor.com.au of any relevant information such as price changes, new releases, vintage changes, forthcoming events or any information that will assist the sales and marketing of my winery.

I authorise auscellardoor to use the information provided by me in the use of marketing and advertising of the auscellardoor website.

I also understand and accept auscellardoor to be my exclusive internet portal with the exclusion of your own internet site.

|

Payment to be made |

Annually |

||

|

|

Biannually |

||

|

|

Quarterly

|

||

|

Payment can be made in the following ways: |

|

||

|

|

Cash Cheque Visa |

||

|

|

Diners B/card A/mex’ |

||

24 In parallel with its discussions with Arms, WSA was obtaining information from the ANZ Bank about the use, as an Internet trading engine, of ANZ e-Gate which the Bank was then promoting. The first meeting between WSA and the ANZ Bank occurred on 7 February 200 when Houghton had an introductory discussion with Laird who was then the ANZ Sales Manager for ANZ e-Gate.

26 Houghton had another meeting with Laird on 24 February 2000 which was also attended by Doug Fitcher, a credit card merchant sales representative for the ANZ Bank. According to Laird, it was agreed at that meeting that the ANZ e-Gate licence would belong to WSA and “the credit card merchant facilities would belong to the individual wineries who would subsequently come along and sign up to the auscellardoor website.”

‘ANZ eGateTM - Shaping the Future for Payments

What is ANZ eGate?

Whether you are selling on the web, through a mail order service or accepting payments through an IVR system or Call Centre, ANZ eGate provides a simple and secure payment service. Your Customers will be able to purchase from you or make payments to you 24 hours a day, 7 days a week.

Payments may be accepted from MasterCard, Visa, Bankcard, American Express or Diners Club cards. In addition to quick and efficient credit card payments, you can also take advantage of the store credit feature. Store Credit allows you to pre-approve your customers for purchases, up to a limit that you specify for each customer. Additional payment methods to support B2B trading are being considered.

ANZ eGate is supported by convenient reporting, enabling Merchants to improve their Customer management capabilities.

ANZ eGate is the first of a family of services that is being developed to support ANZ business customers in. exploiting the web.

Benefits of Becoming an ANZ eGateTM Merchant

ANZ eGateTM provides the following benefits:

· Customer confidence in using a secure bank branded payment system;

· Decreased payment risk - verification and authorisation of transactions by ANZ;

· Instant Payment approval;

· Simple order and transaction confirmation services for ease of reconciliation;

· Store credit capability;

· Customer relationship management through standard reporting facilities;

· Automation of entire sales and payment process;

· Lower processing costs;

· Comprehensive support.

Who should use it?

ANZ eGate can be used by merchants of any size. Generally we would prefer customers that would process more than 600 payments per annum. It becomes more cost effective for larger merchants.

In addition to purchasing ANZ eGate, you will need to qualify and be approved for your chosen payment methods. In most cases this means that you will need to be approved as a Credit Card merchant.

How do I connect to ANZ eGate?

There are two different ways to connect to eGate,

The Interactive interface is very easy to implement for small, simple web based merchant applications - typically less than 10 products for sale. This method takes the Buyer through an interactive process to capture payment and delivery information and provide a receipt. You are automatically advised of payments captured in this way.

Most merchants will use the Application Programming Interface (API) to directly integrate their application with ANZ eGate. This provides maximum flexibility and power. The development required on the interface is generally very small. Your application delivers the payment details to the eGate interface and eGate processes the payment and advises the result to your application.

Your application does not need to be Internet based, or to operate over Internet. However, direct Internet access is required for communication between ANZ eGate and your application.

How to Become an ANZ eGateTM Merchant

The ANZeGate information web site http://xxxx.yyy.zzz has more details about ANZ eGate and application forms.

The developer toolkit and assistance is also available from http://xxxx.yyy.zzz.

Or phone the ANZ eGate help desk on 1800 xxx xxx.’

28 At a further meeting early in May 2000, Student told Arms that the website would not be operational by 15 May 2000 but would be fully operational by 1 July of that year. However, on 23 June 2000, Student told Arms that Houghton had made a mistake in describing how the ANZ e-Gate facility would operate and that Arms would have to arrange for each participating winery to become a “merchant” accredited by each of the ANZ Bank, Diners Club and American Express. Student further said that, to achieve that accreditation, each winery would have to provide to each of the ANZ Bank, Diners Club and American Express acceptable profit and loss statements for the last two years and a business plan. Because he had already enrolled about 30 wineries and the website was to be launched within five days, Arms regarded it as impossible to require wineries to comply with the conditions necessary to become individual merchants.

29 As a result of the information conveyed to him by Student, Arms, on 23 June 2000, telephoned Laird and expressed concern about the time being taken to get the e-Gate facility up and running. He conveyed to Laird that he had been led to believe that “if WSA buys the e-Gate licence, the credit card merchant facilities are automatically given through to the wineries.” Laird arranged to meet Arms over the ensuing weekend of 24-25 June and explained that the ANZ e-Gate facility required an application form from each participating winery which had to be accompanied by two years’ financial statements and had to be sent to a dedicated person within the ANZ Bank for assessment. Although his preference was for each winery to become an approved merchant, Laird indicated that the problem could be overcome by auscellardoor becoming the accredited merchant. He had no knowledge of other arrangements whereby multiple ANZ approved merchants sold through a single website although he recalled one attempt where some 80 application forms had been sent to proposed individual merchants but only 10 or 15 had been returned. In his evidence, Laird denied ever having told a representative of WSA that wineries proposing to sell through auscellardoor would not be required to process credit card transactions or that all orders would be already cleared.

30 Immediately after his meeting with Laird, Arms, on 26 June 2000, wrote to Student the following letter setting out his perception of the difficulties inherent in his becoming a merchant in relation to the ANZ Bank, Diners Club and American Express:

‘A quick note to put you in the picture of where we are up to with banking and the affects these changes make. I will give you an example based on a $200 sale.

Customer -> $200.00 -> Auscellardoor paid by Amex.

Amex takes 3.8% = $192.40.

ANZ e-gate takes 1.75% = 188.90. – This is what is deposited into A.C.D account

I need to transfer $195.00 into the wineries account as per our negotiations of approx 2.5%.

I then invoice them for 5% commission Three months later which equates to $10.00. My profit is $3.90 (1.95%). This is not taking into consideration for FID TAXES and how much extra work is involved in manually transferring funds.

I will also stress that I now believe that A.C.D is in breach of the Liquor Licensing regulations which prevent a business or person accepting money for wine without a Licence.

I realize that you don’t have an answer on the spot but we need a solution.

Maybe Jim can help with the answer. I will be in touch.’

31 After being advised by Student on 29 June that the website was fully operational with the ANZ e-Gate facility, Arms engaged in an advertising and promotional campaign in connection with which he incurred expenses of $16,215.40 including $13,171.40 payable to WSA Media Buying, a firm associated with WSA.

|

‘Known costs at this stage are as follows (subject to negotiation): |

||||

|

Establishment and licence fee (to WSA once-off) |

$1500 |

|||

|

Set up for each merchant |

$95 |

|||

|

Monthly access fee (for each member account) |

$5 |

|||

|

Transaction fee per transaction |

$0.90 (up to 500 pm) |

|||

|

|

$0.70 (501 - 1,000) |

|||

|

|

$0.55 (1,001 - 5,000) |

|||

|

|

$0.40 (5,001 - 10,000)

|

|||

|

Merchant fee |

(TBA - around 2%) |

|||

|

|

|

@ 1,001-5,000 trans. |

||

|

Approximate cost per sale (@ $10) |

$0.75 |

|||

|

(excluding WSA margins) (@ $100) |

$2.55 |

|||

|

|

(@ $500) |

$10.55 (3.1%)

|

||

WSA could charge by monthly service fee, per transaction as a flat fee, and/or take a percentage of revenue.

Summary of opportunity

This seems like an excellent opportunity to build a fully 'shrink-wrapped' transactional solution as part of any e-commerce development. This could form part of the hosting package, or be used with clients that host elsewhere.

· Few, if any of WSA's direct competitors are currently offering a cooked up package like this.

· Enable WSA to provide simple and cost-effective e-commerce solutions for all but the largest clients (who will generally want to integrate directly with their existing merchant and financial arrangements).

· Provide WSA with ongoing transactional revenue.

· Assist in locking clients into an ongoing relationship with WSA.

· Potential to automatically analyse server logs and transactional information and cross-relate data (across a single client or multiple clients).

Suggest following steps:

1. Ensure technical viability.

2. Establish the likely demand amongst present and potential clients (via BMs and PMs).

3. Negotiate initial deal with ANZ.

4. Trial with Auscellardoor (or other upcoming project).’

33 On or about 8 July 2000, Arms executed a form of agreement between himself and WSA which identified Student as the “WSA Online Project Manager.” The body of the document was in these terms:

|

‘Costings |

||||||||

|

|

|

|

||||||

|

Phase 1 |

|

|

||||||

|

|

||||||||

|

Initial development of auscellardoor.com.au concept and creation of trade presentation kit: |

||||||||

|

|

|

|

||||||

|

|

- Outline of strategy promotional and marketing model |

$ 1600 |

||||||

|

|

- Web site look and feel and mock-ups |

$ 6200 |

||||||

|

|

- Web site look and feel and mock-ups - Model 2 |

$ 3200 |

||||||

|

|

- 3 x Model 2 sites |

$ 3000 |

||||||

|

|

- PowerPoint or other interactive presentation |

$ 2480 |

||||||

|

|

|

|

||||||

|

|

Total |

$16,480 |

||||||

|

Phase 2 |

|

|

||||||

|

|

|

|

||||||

|

Strategy |

|

|

||||||

|

|

Complete detailed marketing strategy and program |

$ 3600 |

||||||

|

Development |

|

|

||||||

|

|

Web site and administration function production (approximate pricing subject to development of full specification). |

|

||||||

|

|

|

|

||||||

|

|

Completion of web site |

|

||||||

|

|

Completion of administration function |

|

||||||

|

|

Administration user tuition |

|

||||||

|

|

ISP account creation and web site registration |

|

||||||

|

|

|

$15000 |

||||||

|

|

|

|

||||||

|

|

Additional web site functionality: |

|

||||||

|

|

|

|

||||||

|

|

Integration with ANZ e-Gateway* |

|

||||||

|

|

Integration with secure transaction environment (Verisign)* |

|

||||||

|

|

Membership module* |

|

||||||

|

|

|

- database capture |

|

|||||

|

|

|

- modification of database via interface |

|

|||||

|

|

|

- Password nomination |

|

|||||

|

|

|

- Forgotten password function |

|

|||||

|

|

Shopping cart function* |

|

||||||

|

|

Regional Maps within Australia |

|

||||||

|

|

Integration with unique models via single interface |

|

||||||

|

|

|

|

|

|||||

|

|

(see also, site map for explicit detail) |

|

||||||

|

|

|

$ 23,130 |

||||||

|

|

ANZ e-Gateway |

$ 1,500 |

||||||

|

Credits |

|

|

|

|||||

|

|

Credit of development time - offset e-Gateway |

$ 1,000 CR |

||||||

|

|

|

|

||||||

|

|

Total |

$42,230 |

||||||

|

|

|

|

||||||

|

|

Final Total - WSA Online |

@155/hr |

$58,710 |

|||||

|

|

Final Total - WSA Online |

@200/hr |

$75,755 |

|||||

|

|

|

|

||||||

|

|

Sweat for equity contract 50% |

$37,878 |

||||||

|

|

|

|

||||||

|

External cost elements required (all external elements are to be paid directly by auscellardoor): |

||||||||

|

|

|

|

||||||

|

|

Verisign 128-bit encryption certificate |

$1747.25 |

||||||

|

|

Additional design of logo and site |

$2000 |

||||||

|

|

Brochure/promotional material |

$2910 |

||||||

34 As a result of what he had learned from Laird, Arms decided that auscellardoor should become a merchant for the purpose of the ANZ e-Gate facility and, to that end, he completed, on 25 June 2000, a standard form “ANZ e-Gate Merchant Application.” That form required an applicant to indicate whether the services required included “Visa”, “Mastercard”, “Bankcard”, “Diners Club and American Express.” In the event of either of the latter two services being required, the applicant had to supply either or both a “Diners Club Merchant Number” or an “American Express Merchant Number.” An applicant was also required to indicate the expected number of ANZ e-Gate transactions per month, the expected monthly value of ANZ e-Gate sales and the expected average transaction size for ANZ e-Gate sales. The standard form also indicated that any business applying for an ANZ e-Gate merchant facility was required to provide the following financial information:

* ‘Financials including profit and loss report and balance sheet for the business, a business plan and projected cashflows

* Company constitution and certificate of incorporation and board resolution (if business is incorporated)

* Partnership Deed (if business is a partnership)

* Trust Deed and a statutory declaration stating that the trust deed is complete and correct (if business is a trust)

* Business Name Registration or Australian company Number Certificate’

35 The standard form also noted that the information was required “even if a customer has an existing Merchant facility for other ANZ products.” The auscellardoor application was accepted by the ANZ Bank on 29 June 2000.

37 In late October at a further meeting with Hooke and Brad Allen, the Managing Director of WSA, Arms said that he had had enough, the situation was completely untenable, the ANZ e-Gate facility and the website were still not operating properly and he, Arms, was going to see his lawyers. On 28 October 2000 Arms wrote this letter to Brad Allen of WSA:

‘I would like to document to you the situation concerning the ANZ E-gate facility and the position I know find myself in as a result. As discussed with you I will be seeking compensation for the E-Gate in Four areas, Firstly, paying for a system that clearly does not work and has not worked. Secondly for the loss of revenue on sales and Thirdly the I will seek the money I have spent on Advertising, this has been wasted due to only 1 order been generated independently of myself since the launch of Auscellardoor. Lastly and most importantly Auscellardoor has not grown and developed due to the lack of orders, which is vital for the participating Wineries to remain with Auscellardoor.

Brad, I have sought out preliminary advice, which advises me that I will need to pursue WSAonline for compensation as the contract to supply ANZ E-gate is with ANZ and WSA. I don't want to go down that avenue but I would prefer to pursue ANZ with WSAonline. I have detailed the following as the reasons for my pursuit of compensation.

Breakdown of Orders.

Test orders 67

Orders generated from Simon Arms-17

Failed Orders - 6

Orders –1

The only order that has been generated independently and due to the advertising and with the ANZ E-gate system working was on the 20th of September for Mrs. Robbi Ellis.

There has been 6 failed orders which have been Mastercard transactions where the Declined E-mail comes back to the customer, this occurs with every Mastercard and all have been cards which have been valid. I have manually facilitated 4 of these transactions myself with 1 customer not willing to replace the order and 1, which received the order without ever paying for the stock. No customer has reordered after the ordeal nor do I imagine have recommended Auscellardoor as a result of this embarrassment.

There is a further 17 orders which have either been for myself or close friends which I have put the order through for. The orders that I have placed are to create the impression to the participating wineries that we are receiving orders.

As Auscellardoor only accepts Visa and the almost out of use Bankcard I believe many potential customers have ordered wine only to delete the order at the last step due to our ordering restrictions. I have received 9 phone calls and 3 E-mails to this affect with countless others not bothering to contact me.

ANZ E-gate was first introduced to me In March this year by Jim Houghton; it was sold to me on the basis that it would facilitate transactions with all credit cards and clear funds directly to a Wineries bank account. On the 26th of May (1 week prior to launch of Auscellardoor) I was informed by James Student that I will need to see all wineries and have them fill out Credit applications for the E-gate which would require a full Two years of Financial records and in addition I will need them to fill out Diners Club and American Express applications also. A lack of communication from ANZ to Jim Houghton and to James Student was the reason for the mess. I met with David Laird from ANZ on the Saturday the 27th of May and the solution which was to be short term was for myself to be the merchant for all the Wineries and transfer all funds following a transaction. On the Monday I met with Diners Club and organized a merchant facility with them at a cost of 3.75% per transaction and forwarded the number to James and David. David assured me that the system would be in place prior to going live and he would do everything in his power to achieve this. I would also like to point out that David and James were aware that I was now running an illegal business due to the liquor licencing regulations which prevent me from accepting money for alcohol. A situation which still occurs.

I have now endured many broken promises and endless frustrations and demanded a meeting with David Laird, which Cameron Hook coordinated. On the 27th of September myself, David Laird, Cameron Hook and James Student met at WSAonlines office and agreed that the situation could go on for no longer. David Laird agreed to assist in the merchant facility requirements for participating wineries and to have a E-gate specialist come into WSA and fit a new version of E-gate which would facilitate all credit cards. I received the merchant requirements more than two weeks later via Cameron and as at the 26th of October no-one had contacted myself or WSA to fit a new version of the E-gate. As of late Friday a E-gate expert will come to WSA on Wednesday to fit version 2, I spoke with both David Laird on Friday the 26th and apologized many times and agreed with me that this has been a disgrace and I should pursue compensation.

I also spoke to Wayne Fox from ANZ and with absolutely no urgency said that this is a minor problem and it is probably a coding error which could have been fixed previously. This comment came after I said that E-gate accepts Visa and Bankcard, he could not understand this and that was his response.

Brad, I am not overstating the fact that Auscellardoor is in serious trouble which is due to the inability of the ANZ E-gate system not functioning. In addition there has been no effort or urgency from ANZ to get it fixed or right, considering the ANZ E-gate has been discussed since March they have had more than 7 months to have the system working. In addition ANZ are aware that Auscellardoor is an illegal business due to their lack of assistance and communication and lastly a commitment to a business that relys on their system and professionalism.

Brad, I would like to discuss with you at your earliest convenience the way to move forward and to seek compensation. My aim is to resolve this in conjunction with yourself and quickly as this business needs it.’

38 Those complaints elicited this reply by letter from Allen on 30 October 2000:

‘Thankyou for your letter and corresponding documentation re: the ongoing ANZ - e-gate nightmare. I have passed the information onto David Laird and requested immediate response. As you know WSA Online has been diligently working through the issues trying to drive ANZ to make good their promise.

Re: your intention to proceed with litigation - I completely agree - however to litigate against WSA Online I feel is unwarranted. I hope to meet with you at your earliest convenience to discuss the situation further; however in the mean time I will pass on your letter to our representatives and receive a formal opinion.’

39 Despite the difficulties and complaints recounted at [36]-[38] above, Arms and the Chief Financial Officer of WSA, had, on 25 July 2000, signed a “sweat for equity” agreement under which WSA was to take an equity of 10% of the business of auscellardoor in return for remitting $50,000 of the first $100,000 to be charged for services to be provided by WSA. On 11 October 2000, WSA issued a press release announcing that the auscellardoor website “goes live today and can be found at www.auscellardoor.com.au.” That press release included this testimonial by Arms:

‘Simon Arms, CEO of auscellardoor, came to WSA Online with the concept of a 'purchase direct' winery site in late 1999. WSA worked with Simon to develop the business strategy and the marketing model before designing and building the site, the back-end database and content management system.

According to Arms; "When I first spoke to WSA, auscellardoor was an idea. My background's in the wine industry so I felt very confident that auscellardoor would appeal to the smaller upmarket wineries that have great problems getting cost effective distribution and shelf space through mainstream channels.

"WSA brought the online expertise to the party: They helped build a strong business case for the site and added significant value to the concept through their understanding of e-commerce business and marketing issues, and their ability to directly apply this knowledge to the design of the website. Each activity and objective of the site was considered in advance and the site and the marketing activities that go around it were designed with usability and business outcomes in mind."’

40 On 31 October 2000, the present solicitors for Arms wrote this letter to WSA:

‘I advise that we act on behalf of Simon Arms. Our client conducts a business selling wine via the internet.

I am instructed that our client entered into a contract with WSA Online Ltd (“WSA”) on 10 January 2000. Pursuant to that contract, WSA was required to develop the website at www.auscellardoor.com.au, including the installation of fully functional e-commerce facilities at the site.

The site was launched on 1 July 2000. At no time during the operation of the site have the e-commerce facilities been fully functional. The e-commerce facilities have repeatedly rejected valid cards and have failed to process purchase orders.

As a result of WSA’s failure to comply with its contractual obligations, our client has incurred expenses in attempting to rectify the problem and has suffered damage to his business as a result of having been unable to process numerous transactions.

Please provide the following within 48 hours:

1. a timetable for finalisation/rectification of the electronic commerce facility at the site; and

2. a commitment to negotiate in good faith in relation to compensating our client for the damage suffered by his business.

If we do not receive this timetable and your commitment to negotiate within the next 48 hours, we will seek our client's instructions in relation to enforcement of his legal rights in this matter.’

‘Following our conversation an Wednesday the 8M of November and also with David Lard from the ANZ Bank on the same day I have outlined my claim for compensation for the E-gate system not working as agreed.

Firstly, the issues as they stand.

1. Jim Houghton and James Student sold the ANZ E-gate facility to me from WSAonline. Jim Hougton’s information came directly from the ANZ Bank. The E-gate system was to facilitate all credit cards on the Auscellardoor Website and clear funds within a 24 hour basis

2. David Laird on Saturday the 24th of June 2000 met with me to assist in the launching of ANZ E-gate with the Auscellardoor Website for the 1st of July 2000. As per my notes David confirmed to me the ANZ E-gate would facilitate all credit cards within 24 hours and would be ready for the 1st of July 2000.

3. The site has been tested for ANZ E-gate over 60 times in the initial launch, the system was never passed as workable but promised from WSAonline and ANZ that it work.

4. On the 15th of September 2000 Peter Vucic who is an ANZ E-gate employee again tested the site and again discovered the E-gate not to be functioning. This test was not requested by me and no action was taken by Peter following his test to either contact me to assist or rectify the problem.

5. On the 27th of September a “Crisis” meeting was held with myself David Laird, Cameron Hook and James Student to rectify the E-gate issue. Despite this meeting and further assurances the system still does not work.

6. In early October a decision was made by Ryf Quaill and myself to halt any further advertising as I was receiving adverse feedback from the ANZ E-gate facility. In addition the MasterCard facility was also taken away from the options.

7. I have documented cases of customers phoning and E-mailing me with concerns over no full credit card facility, Credit Card bounces due to the ANZ E-gate and customers have actually ordered and then signed off due to the problems.

8. I have been in contact to Wayne Fox to ANZ to tell me that it is a simple coding problem and could have been fixed strait away, with no urgency. I have never heaved from him again. Our conversation took place in late October.

I would therefore like to claim the following;

Advertising Expenditure $20,000- as all advertising was booked with the assurance from ANZ that the system would work. The Website has attracted a steady and constant amount of users.

Cost of ANZ E-gate to Auscellardoor. $500.

Loss of Business $20,000 - Due to poor or no sales to the Wineries I am not able to pursue money owed from existing Wineries nor am I able to pursue further Wineries.

Loss of Customers $10,000 - As a result of customers not coming back or purchasing from Auscellardoor I am claiming this amount.’

42 Early in 2001, Arms consulted Stephen Foxworthy and Andrew Davidson, who had previously been involved as consultants to WSA in the development of the auscellardoor website and were then working with a business called “Rare Media”. Rare Media was engaged to cure remaining problems with the auscellardoor website and add extra functional features including a newsletter facility. That work was completed, according to Arms, within three or four months. However, the retainer of Rare Media did not come to an end until April or May 2004.

Resolution of the issues raised by the pleadings

43 The causes of action pleaded against WSA are for breach of contract and contraventions of the Trade Practices Act 1974 (Cth) (“the TPA”). Arms also seeks to make Student and Houghton personally liable on the basis of contraventions, by the same representations as are alleged against WSA, of ss 4 and 9 of the Fair Trading Act 1999 (Vic) (“the Fair Trading Act”).

(i) The claim for breach of contract

44 In par 6 of his second amended statement of claim Arms has alleged that, before entering into an agreement in writing with WSA dated 10 January 2000, he:-

‘ … informed the Respondent that the Applicant required the services for the purposes of producing a website which would allow the Applicant to operate the Business as follows:

(a) the Applicant would act as a facilitator of sales made by wineries to customers;

(b) payments for sales would be made by the customers directly to the wineries electronically through the website; and

(c) the Applicant would receive a commission of 5% of all sales transacted through the website

(the Purposes).’ (original emphasis)

“The services” had earlier been defined in par 5 of the statement of claim as “strategic business advice, design, technical development, marketing and costing services”.

‘(a) the services will be rendered with due care and skill, and

(b) the services supplied under the Agreement would be reasonably fit for the Purposes and would-,be of such a nature and quality that they might reasonably be expected to achieve the Purposes.’

‘(a) it was not viable for each of the wineriesto be the merchants for the sales made through the Website; and the only viable option was for the Applicant to be the merchant. The Applicant refers to parts (e) & (f) of paragraphs 13 & 15;

(b) transaction fees associated with each purchase would be 1.75% to the ANZ Bank plus, with respect to American Express, 3.8% and with respect to Diners Club, 3.75%;

(c) the Website was difficult to use and customer orders frequently failed;

(d) the payment procedure was not secure because, until December 2000, the Applicant received in his email in-box, the customer name and credit card details when a customer transacted a purchase via the Website;

(e) until December 2000 purchases could not be processed by Diners Club, American Express or Mastercard credit cards;

(f) the Applicant was unable to use the Website to design websites for the wineries because of the above defects in the Website;

(g) the Website contained spelling mistakes and parts of the Website did not operate as they should;

(h) an error occurred on the Website with respect to Shottesbrooke Winery which included the text “there is no reason to visit this winery, there are no features and nothing worth seeing”; and

(i) the Website could only list the first10 wines of a range of any winery.’

‘(1) In every contract for the supply by a corporation in the course of a business of services to a consumer there is an implied warranty that the services will be rendered with due care and skill and that any materials supplied in connexion with those services will be reasonably fit for the purpose for which they are supplied.

(2) Where a corporation supplies services (other than services of a professional nature provided by a qualified architect or engineer) to a consumer in the course of a business and the consumer, expressly or by implication, makes known to the corporation any particular purpose for which the services are required or the result that he or she desires the services to achieve, there is an implied warranty that the services supplied under the contract for the supply of the services and any materials supplied in connexion with those services will be reasonably fit for that purpose or are of such a nature and quality that they might reasonably be expected to achieve that result, except where the circumstances show that the consumer does not rely, or that it is unreasonable for him or her to rely, on the corporation's skill or judgment.’

48 The concept of “consumer” for the purpose of, amongst other provisions of the TPA, s 74, is explained by s 4B, which, so far as is relevant, provides:

‘(1) For the purposes of this Act, unless the contrary intention appears:

… … …

(b) a person shall be taken to have acquired particular services as a consumer if, and only if:

(i) the price of the services did not exceed the prescribed amount; or

(ii) where that price exceeded the prescribed amount - the services were of a kind ordinarily acquired for personal, domestic or household use or consumption.

(2) For the purposes of subsection (1):

(a) the prescribed amount is $40,000 or, if a greater amount is prescribed for the purposes of this paragraph, that greater amount;

(b) subject to paragraph (c), the price of goods or services purchased by a person shall be taken to have been the amount paid or payable by the person for the goods or services;

… … …

(3) Where it is alleged in any proceeding under this Act or in any other proceeding in respect of a matter arising under this Act that a person was a consumer in relation to particular goods or services, it shall be presumed, unless the contrary is established, that the person was a consumer in relation to those goods or services.’

49 It was submitted by Mr Cawthorn for WSA that the evidence amply demonstrated that the amounts actually paid by Arms for the services provided by WSA exceeded $40,000 and were as high a $53,007.50 for “initial development of strategy”.

50 It was responded for Arms that he was to be presumed to have been a “consumer” of the services provided by WSA because WSA had not discharged the onus imposed by s 4B of the TPA of establishing that the price of the services exceeded the prescribed amount of $40,000. The quotation signed on 10 January 2000 stipulated a price of $14,860 for Phase 1, a price of $3,600 to complete a detailed marketing strategy and program under Phase 2 and a price range of $8,000-$15,000 for the completion of the website and the other services to be provided under Phase 2. Not even an indicative price was stipulated for the “media initiatives” under Phase 3 which were “to be discussed”. In the result, it was contended, the maximum price which could be imputed as payable for WSA’s services under the contract was $33,460.

51 In the same context, Counsel for Arms submitted that what is to be taken to be the price of services as contemplated by s 4B(2)(b) of the TPA is the price stipulated in the contract pursuant to which the services are provided which, in this case, was concluded on 10 January 2000. However, it is to be remembered that s 4B(2)(b) stipulates that the price of “services purchased by a person shall be taken to have been the amount paid or payable by the person” for the services (emphasis added). That formulation, I consider, permits regard to be had to the total amount paid and payable for the services acquired by the presumptive consumer. It is not predicated solely on the price “to be paid” under a particular contract for the supply of goods but directs attention also to the services “purchased” in the past tense. That suggests to my mind that, where the supply of services has been completed, it is open to the supplier to discharge the onus under s 4B(3) by showing that the total price paid and payable for the services so supplied exceeded $40,000, irrespective of whether the supply was referable to one or more contracts. In this case it is not disputed that the total price paid by WSA for services rendered exceeded $40,000.

52 Counsel for Arms submitted that, in any event, it was an implied term of the contract between him and WSA that WSA would exercise reasonable care and skill in providing the services contracted for; see e.g. Costa Vraca Pty Ltd v Berrigan Weed and Pest Control Pty Ltd (1998) 155 ALR 714 where Finkelstein J observed, at 720:

‘Whether there was one contract or a number of them it is clear that there is to be implied in that contract or those contracts a term that Berrigan would carry out its services with the reasonable care and skill to be expected from a person providing the services that Berrigan provided: Bolam v Friern Hospital Management Committee [1957] 1 WLR 582 at 586; Chin Keow v Government of Malaysia [1967] 1 WLR 813. Such an obligation would require Berrigan to take reasonable precautions to ensure that its spraying rig was not contaminated with any chemical that might damage or destroy Costa Vraca’s tomato crop.’

See also Astley v Austrust Ltd (1999) 197 CLR 1 at 22.

53 In the light of those authorities, and in case I be wrong about the correct interpretation of s 4B of the TPA, I have proceeded on the assumption that it was an implied term of the contract between WSA and Arms that WSA’s services would be rendered with due care and skill and would be reasonably fit for the purpose for which they were supplied.

54 It was contended on behalf of Arms that the breaches which had occurred of the implied terms of the contract were constituted by the same conduct as was involved in making the ANZ Requirements Representation, the Production Representation and the Best Method Representation which are discussed below. Those breaches were said in Counsel’s written submissions to be:

‘a. The misrepresentations about the requirements of the ANZ Bank; and

b. The failure to provide the website as promised.

Further, the failure of the site to operate for the four months from July to November 2000 constitute a breach of the statutory implied term. The evidence of the failure of the website to be fit for the purpose during this period is clear, uncontradicted and uncontested:

a. Between July and the end of October only 1 transaction was completed through the website from an independent consumer.

b. The site was tested by WSA over 60 times without success and there were numerous failed attempted purchases.’

55 Breaches of the implied terms of due care and skill and fitness for purpose were said to be demonstrated by the fact that the auscellardoor website did not operate effectively for four months from July to November 2000. There were numerous minor defects like the spelling mistakes and the insulting reference to Shottesbrooke Winery which were the subject of complaints summarised at [36] to [38] above. However, whatever view be taken of those “glitches”, the fact remained that only one independent consumer had successfully prosecuted a transaction by means of the website in the period between July and October 2000. It was said on behalf of Arms that it was immaterial that most, if not all, of the failures and defects during this period were attributable to shortcomings in the design or installation of the ANZ e-Gate system. WSA had introduced and recommended ANZ e-Gate to Arms and was responsible as head contractor for any lack of care and skill exhibited by the ANZ Bank as a sub-contractor to WSA.

57 It was urged on behalf of WSA that there was no evidence that an exercise of due care and skill would have averted any of the detrimental features of the auscellardoor website identified in the particulars to par 19 reproduced at [46] above. Secondly, it was said, Arms had accepted that many of the defects there listed had been cured in the course of WSA’s retainer. They were said to be matters inevitably encountered in the development of a website which are overcome by adjustments in the nature of “tweaking” the system.

58 In the same context it was said that Arms had failed to prove that it was not viable for each of the participating wineries to be a merchant for sales made through the auscellardoor website. All that had been shown was that he, Arms, considered the ANZ Bank’s requirements for the provision of two years’ financial statements and the like to be so onerous as to inhibit him from requesting the wineries to comply with them.

59 It was next submitted for WSA that, even if a term that it would exercise due care and skill in performing the agreement might be implied to give business efficacy to the agreement, there was no admissible evidence to demonstrate what was the appropriate standard of care and skill for a website designer in the circumstances of the present case; see Provincial Insurance Pty Ltd v Consolidated Wood Industries Pty Ltd (1991) 25 NSWLR 541 at 556. Nor was there any complementary expert evidence to the effect that WSA’s performance of the agreement had fallen short of the appropriate degree of care and skill.

60 In view of the concession noted at [56] above and the fact that I am not satisfied on the evidence that there was a breach of any term of the contract other than that constituted by the falsity of the ANZ Requirements Representation discussed below, it is unnecessary to express a concluded view on other aspects of Arms’ claim against WSA for breach of contract.

(ii) The representations

61 The case sought to be made by Arms based on a contravention of s 51A of the TPA depended on two sets of representations, the first of which was pleaded as follows in par 7 of the second amended statement of claim:

‘7. Prior to entering into the Agreement, the First Respondent and the Third Respondent represented that:

(a) the First Respondent would provide services to the Applicant which would be fit for the Purposes; and

(b) operating in accordance with the Purposes was the best way to operate the Business

(the First Representations).’

‘13. In February and March 2000 the Respondents represented that:

(a) the first Respondent would provide services to the Applicant which would be fit for the Purposes;

(b) operating in accordance with the Purposes was the best way to operate the Business;

(c) the maximum transaction fee payable by the wineries would be 2.5% per purchase;

(d) the Website would be operational by 1 July 2000;

(e) the wineries would not be required to process credit card transactions; and

(f) in order to effectively run the Business and operate the Website, the Applicant was not required to obtain any documentation from the wineries other than a form, with provision for banking details, included in the Trade Presentation Pact and a standard form ‘agreement’ document.

(the Second Representations).’

63 In his final submissions, Mr Riordan SC, who appeared with Mr M E King of Counsel for Arms, collapsed the First Representations and the Second Representations into three alleged representations, the substance of which was said to be:

a. In order to effectively run the business and operate the website, the applicant was not required to obtain any documentation from the wineries other than a form, with provision for banking details. (“the ANZ’s Requirements Representation”)

b. The respondents would produce a website which would allow the applicant to make sales of wine on behalf of wineries through the internet, with payment being effected electronically to the winery. (“the Production Representation”)

c. Operating in accordance with the proposed method was the best way to operate the applicant’s business. (“the Best Method Representation”)

I have adopted the same analysis in examining the representations allegedly made in contravention of the TPA. I have assumed that any representation not comprehended as part of one or other of the ANZ’s Requirements Representation, the Production Representation and the Best Method Representation was no longer pressed as affording a basis for any of the relief which Arms has claimed.

(a) The ANZ Requirements Representation

‘Australia and New Zealand Banking Group Limited

ACN 005 357 522

Information Paper

ANZ eGate – Application Process

To facilitate a direct transfer of funds from Auscellardoor to your account please provide the following details”

|

Winery Name: |

|

|

Banking Details |

|

|

Bank Name and Address |

|

|

Account Name |

|

|

BSB |

|

|

Account Number |

|

|

Any enquiries or assistance required, please contact: |

|

Simon Arms 9417 347 288’ |

65 WSA contended that it was at all relevant times made clear to Arms that, if individual wineries were to become “merchants” for the purposes of having their wine purchased by customers using credit cards processed through ANZ e-Gate, they would have to complete applications to the ANZ Bank, Diners Club and American Express respectively. It was said to be notorious that merchants, not customers, pay the fees or charges, expressed as a percentage of the value of each transaction, to the company whose credit card is used by a particular customer. Arms should therefore have known that each winery, as a prospective merchant, would have to demonstrate its creditworthiness to the respective credit card providers.

66 In any event, Mr Cawthorn argued, there was no evidence that any representation was made either orally or in writing to the effect alleged in par (f) reproduced at [62] above. Rather, the applicant’s case seemed to be that Houghton had information from Laird about the need for wineries to supply two years’ financial statements and the like which he failed to disclose to Arms. The Court was invited to prefer the evidence of Houghton on that point to that of Laird.

‘That does not, however, mean that a corporation which purports to do no more than pass on information supplied by another must nevertheless be engaging in misleading or deceptive conduct if the information turns out to be false. If the circumstances are such as to make it apparent that the corporation is not the source of the information and that it expressly or impliedly disclaims any belief in its truth or falsity, merely passing it on for what it is worth, we very much doubt that the corporation can properly be said to be itself engaging in conduct that is misleading or deceptive.’

68 Arms’ understanding was said to coincide with WSA’s perception of itself as a mere conduit of information from the ANZ Bank because he wrote, in point 1 of the letter of 8 November 2000 quoted at [41] above that “Jim Houghton’s information came directly from the ANZ Bank.”

69 It was next submitted that for Arms to establish a misrepresentation or misleading or deceptive conduct as to the “two years’ financial statements” he had to show that to have been an “unusual and unexpected circumstance” attracting the application of the principle discussed by a Full Court of this Court in Demagogue Pty Ltd v Ramensky (1992) 39 FCR 31 where Black CJ said, at 32:

‘Silence is to be assessed as a circumstance like any other. To say this is certainly not to impose any general duty of disclosure; the question is simply whether, having regard to all the relevant circumstances, there has been conduct that is misleading or deceptive or that is likely to mislead or deceive. To speak of "mere silence" or of a duty of disclosure can divert attention from that primary question. Although "mere silence" is a convenient way of describing some fact situations, there is in truth no such thing as "mere silence" because the significance of silence always falls to be considered in the context in which it occurs. That context may or may not include facts giving rise to a reasonable expectation, in the circumstances of the case, that if particular matters exist they will be disclosed.’

See also per Gummow J at 40 where his Honour observed:

‘"Conduct" within the meaning of s 52 includes refusing to do an act and refusal to do an act includes a reference to "refraining (otherwise than inadvertently) from doing that act": s 4(2). But in any case where a failure to speak is relied upon the question must be whether in the particular circumstances the silence constitutes or is part of misleading or deceptive conduct. The expanded meaning given by s 4(2) to "conduct" should not distract attention from the fundamental issue in the case at hand.

Spender J indicated in the passage I have set out earlier in these reasons, that the present case concerns both a positive misrepresentation, as to the provision of vehicular access, and misleading conduct from the failure to say anything about the Road Licence, with the whole of the circumstances creating in the respondents the clear but erroneous impression that there was nothing unusual concerning access to the site.’

70 In these circumstances, it was suggested, Arms could have avoided any misapprehension by himself approaching Laird or some other officer of the ANZ Bank concerned with the administration and development of ANZ e-Gate.

71 Further, in relation to the requirement to supply two years’ financial statements, it was contended on behalf of WSA that Houghton was entitled to assume that wineries to be enlisted by Arms would either already be accredited as merchants by the credit card providers or would have no difficulty in satisfying the requirements for obtaining such accreditation. Arms’ former employer, Eyton Winery, had apparently been accredited to make sales to credit card holders.

72 The evidence revealed that the “paperwork” for ANZ e-Gate was not available on 7 April 2000 because it was still being settled by the ANZ Bank’s legal officers or advisers. Moreover, Houghton attested to a belief that the subscribing wineries, as established businesses, should have no difficulty in becoming “ANZ merchants” and that Arms probably would not want to do business with those which could not. Houghton, it was said, had no motive for deliberately refraining from disclosing to Arms whatever information he had about the ANZ Requirements.

73 It was next said on behalf of WSA that Arms always knew that subscribing wineries would have to obtain separate accreditation as Diners Club and American Express “merchants” because his system was designed to take all major credit cards.

75 I am satisfied that Arms was told at the meeting on 7 February 2000 by one or other of Student or Houghton that wineries could be added to the website “by simply filling in a form” or “by filling in a simple form” and paying a small set-up fee. The difference between the two formulations of the representation is, I consider, immaterial, because the form of application to become an ANZ e-Gate merchant, as ultimately developed by some time in June 2000, was far from “simple” and required more of an applicant by way of provision of financial statements and projections and company or partnership details than “simply filling in” the form. However, I incline, on balance, to a finding that WSA told Arms that additional wineries could be added by “simply filling in a form” because that was the expression used by Houghton in his note, reproduced at [17] above, of his discussion with Laird.

‘Merchants

To become a Merchant your customer needs to complete a Merchant Application form located on the ANZ Website at www.anz.comunder ‘What’s New at ANZ’. Form needs to be mailed to:

Ø ANZ eGate Help Desk

5th Floor Podian Level 530 Collins Street

Melbourne Victoria 3000

Applications are processed within 10 days, unless your customer is applying for a new Merchant facility, in which case it would take longer.

Once the application is approved your customer will be contactedby ANZ who will advise that accreditation should be undertaken and that ANZ eGate software can be installed. A fee schedule will also be provided at this stage. Accreditation is conducted by a third party approved by ANZ.

Merchants will need to use the ANZ eGateMerchant Test System before processing any payments, to ensure that ANZ eGate software has been integrated correctly.

After successful testing, Merchants will be formally accredited and issued with an ANZ eGate Merchant Identifier.

Technical support is available on the ANZ eGate Website or alternatively ANZ has a Solution Provider Program through which various companies offer the skills to integrate ANZ eGate into the systems environments of your customers.’

77 The document in which that recital appeared was exhibited to an affidavit by Houghton and, I infer, came to his notice in or shortly after December 1999. There is no evidence as to when the Merchant Application form referred to in the passage just quoted was first available on the ANZ website www.anz.com. Nor does the evidence disclose the terms in which the application form was then expressed.

78 However, Houghton has deposed that, shortly after a meeting in early February 2000, he e-mailed Arms the website address for ANZ e-Gate. The evidence does not disclose that Arms ever availed himself of the facility to visit that website.

79 In my view, by approving the presentation kit which was to be used by Arms in approaching wineries to become participants in the auscellardoor website, WSA impliedly represented that an applicant winery would not be required to do more to become an ANZ e-Gate merchant than complete the relevant documents in the kit, being those reproduced at [23] and [64] above. This was not a case of “mere silence” in the sense explained by the Full Court in Demagogue Pty Ltd v Ramensky (supra). In relation to the application form required by ANZ e-Gate before a winery could become a merchant, WSA had made itself responsible for compiling, or at least approving, the contents of the presentation kit, knowing that it was to be used by Arms in seeking to persuade wineries to become subscribers to the auscellardoor website. After WSA told Arms that wineries could be added to the system by simply filling in a form and allowed the presentation kit to go to wineries without the inclusion of an ANZ approved form, Arms was entitled to assume that completion of the forms in the kit would suffice as an application by a winery to become an ANZ e-Gate merchant.

80 It was not reasonable in the circumstances as they existed between February and June 2000 to expect Arms himself to approach Laird or somebody else within the ANZ Bank to find out what were the contents of the application form which it required to be completed by prospective e-Gate merchants. There is much force in the submission advanced by Mr Riordan that WSA was concerned to maintain itself as an intermediary between Arms or auscellardoor and ANZ e-Gate. WSA was itself to hold the ANZ e-Gate licence and saw in that arrangement an opportunity to add customers other than auscellardoor to the facility. WSA saw in the arrangement an opportunity to derive for itself “ongoing transactional revenue” and regarded auscellardoor as a suitable vehicle for a trial of that arrangement; see the internal WSA memorandum reproduced at [32] above. Moreover, WSA took no steps before 23 June 2000 to introduce Arms to Laird or any other representative of the ANZ Bank involved in the administration of ANZ e-Gate. The meetings on 7 February, 24 February, 9 March, 7 April and 23 June 2000, which are recounted at [25]-[27] of these reasons, all occurred in the absence of Arms between representatives of WSA on the one hand and Laird and other representatives of the ANZ Bank on the other. Even as late as 20 June 2000 Student sent, to an assistant to Laird at the ANZ Bank, an email which contained these passages:

‘I will be the point of contact from here on in for WSA Online in relation to ANZ eGate.

… …

I would like to explain the structure of how we will be using ANZ eGate:

Auscellardoor is a new web site to be launched on the 30th of this month. They are selling wines on behalf of 25 different wineries around australia. The Auscellardoor web site is ecom enabled, and after receiving an order from the end customer, will capture their credit card details and clear the transaction via ANZ eGate. The merchants (in this structure) are the wineries, not auscellardoor. Therefore, there will be 25 separate merchants. But the point of contact for all the participating wineries is:

Simon Arms

Auscellardoor

03 9696 9673

So, all correspondence – where applicable – to the wineries, should be directed to him. Also, the applications will be coming to you via fax, so could you please send me your fax number.

2.

In relation to the merchant accounts, I would have thought a merchants bank account would need to be nominated, or are you setting one up? … …’

The last two passages suggest that Student was unaware, or had forgotten, what was required to complete an application to become an ANZ e-Gate merchant and whether the application form provided for the nomination of the merchant’s bank account.

81 It is no answer to Arms’ complaint under this head to say that Houghton was entitled to assume that the wineries would already be accredited as merchants with Visa, American Express, Diners Club and the other credit cards contemplated as usable on the auscellardoor website. It was made clear in the extract from the “Produce & Services Pack” reproduced at [76] above that the requirement to complete and mail an ANZ e-Gate Merchant Application form applied even to those customers who had an “old” merchant facility. When Arms completed his Merchant Application on 25 June 2000, he was able to include American Express and Diners Club among the services available to him as an e-Gate merchant by supplying his respective existing merchant numbers for those credit card providers but was not exempted from providing to the ANZ Bank the rest of the considerable volume of information required by the standard form ANZ e-Gate Merchant Application.