FEDERAL COURT OF AUSTRALIA

Australian Competition & Consumer Commission v Oceana Commercial Pty Ltd [2003] FCA 1516

SUMMARY

1. In accordance with the practice of the Federal Court in some cases of public interest, the following summary has been prepared to accompany the reasons for judgment delivered today. The summary is intended to assist understanding of the decision of the Court. It is not a complete statement of the conclusions reached by the Court or the reasons for those conclusions. The only authoritative statement of the Court’s reasons is that contained in the published reasons for judgment. The published reasons for judgment and this summary will be available on the Internet at www.fedcourt.gov.au.

2. These proceedings concern the sale of residential units at the Gold Coast in 1997 and 1998. The principal respondents involved in the marketing in question are Oceana Commercial Pty Ltd and Markfair Pty Ltd, which were then respectively called Coral Reef and Investlend. Coral Reef engaged a company called NAPC to market the properties and Investlend was used to provide financial advice to prospective purchasers. Mr Bilborough, the fifth respondent was associated with both companies and Mr Quinlivan, the sixth respondent, with Investlend. It has been found that these companies through Mr Bilborough and Mr Quinlivan acted in concert to carry out what has been called the ‘NAPC Scheme’. The steps the Commission alleged were involved in it appear at[17]of the reasons for judgment and the Court’s further comments on it and at [167]. The part the other respondents, apart from the bank, played in it is explained at [6].

3. The ACCC alleged that the conduct of the scheme as a whole was misleading and deceptive conduct within the meaning of s 52 of the Trade Practices Act 1974 (Cth). That aspect of the case has not been established as a matter of law (see [168] to [179]).

4. It has been established that it was possible that purchasers may have been misled about two matters by the representatives of NAPC and Investlend. They were told that the purchase price was the unit’s market value and they were told that the unit would increase in value at the rate of 8 per cent per annum over the following ten years.

5. To establish that the representation about market value was misleading or deceptive it was necessary for the ACCC to prove that the units were sold at a price substantially greater than their true value. The ACCC’s evidence did not establish that fact (see at [223] to [238]).

6. The representation about the rate of capital growth which was made by the Investlend representative in the process of undertaking what was called a ‘property investment analysis’ for purchasers was found to be misleading. (See at [239] to [248]). That was because it was not shown that the companies in question and Mr Bilborough and Mr Quinlivan had any reasonable basis for a belief that the rates were a reliable guide to value.

7. Another aspect of the case involves particular purchasers, Mr and Mrs Gleeson. In connexion with them it has been found that the companies misled them as to the rate of capital growth they could expect and also as to the true role of the Investlend advisor. They were told that that person was a ‘qualified financial advisor’, implying that they were quasi-professional people who were giving advice to the Gleesons which would be in their interests. The impression conveyed was that they were separate from the marketer NAPC. In fact they were engaged in the process of selling properties with NAPC. There is no suggestion that the advisors were qualified. They were simply trained to present their ‘analysis’ and apply pressure.

8. Coral Reef and Investlend have been found liable for breach of s 52. Some but not all of the other respondents have been found liable as accessories to the contravention of s 52. They are the fifth and sixth respondents and the seventh and eighth respondents. There are separate findings made with respect to each of the respondents. The developer and the directors, the third, eleventh and twelfth respondents have not been found liable.

9. The two solicitors (the tenth and thirteenth respondents) were joined to the proceedings because they were on a ‘panel’ of solicitors to whom Investlend referred prospective purchasers at a point when the contract was to be signed. It was alleged that they were guilty of misleading conduct because they did not alert their clients to a number of matters, including the relationship between NAPC and Investlend. It was also alleged that they knew most of the details of the NAPC scheme. This has not been established. With respect to Mr Pointon it was found however that he knew sufficient to have required him to make disclosures to his clients. No orders could however be made because the ACCC is not able to seek orders against him under the Fair Trading Act 1989 (Qld) as it sought to do. It was not shown that he was an accessory to the company’s conduct as alleged by the Commission (see [286] to [304]). The case against Mr Johanson was not established.

10. It was not alleged that the bank knew of or participated in the scheme of marketing. Mr and Mrs Gleeson sought a loan from it to enable them to conclude the purchase. The bank’s valuer had advised the bank that they may have paid too much for the property and that they may not have understood local market conditions. The ACCC alleged, on various bases, that the bank was obliged to provide them with the content of the valuation or alert them in some way so that they might seek their own advice. To succeed the ACCC needed to establish that the Gleesons were in a position such that their ability to make a judgment as to their best interests was seriously affected, or that the bank behaved unconscionably. This requires a consideration of all the circumstances pertaining to the Gleesons and the bank. They did not establish either proposition (see at [322] to [341]).

11. It is necessary to add that in the publicity attending the proceedings reference was made to ‘two tier marketing’. It was said that this involved the sale of units at one price to people who were familiar with the Gold Coast property market and at a much higher figure to people drawn from places distant. There was no evidence tendered at the hearing of such a market (see at [235]).

AUSTRALIAN COMPETITION AND CONSUMER COMMISSION v OCEANA COMMERCIAL PTY LTD, MARKFAIR PTY LTD, ADVANCED COMMERCIAL DEVELOPMENTS PTY LTD, COMMONWEALTH BANK OF AUSTRALIA, CHRISTOPHER RUSSELL BILBOROUGH, DUDLEY JAMES QUINLIVAN, SHANE ANDREWS, MICHAEL BYROM, PETER EGGENHUIZEN, GREGORY POINTON, DEAN CORNISH, JOHN GROUNDS, RODNEY JOHANSON

Q232 of 2001

KIEFEL J

BRISBANE

18 DECEMBER 2003

FEDERAL COURT OF AUSTRALIA

Australian Competition & Consumer Commission v Oceana Commercial Pty Ltd [2003] FCA 1516

TRADE PRACTICES – misleading and deceptive conduct – whether whole course of conduct constitutes misleading and deceptive conduct – scope of s 52 – whether specific representations by companies and their employees constitutes misleading and deceptive conduct – whether solicitors engaged in misleading and deceptive conduct by failing to disclose information to their clients – non-disclosure – silence – whether a reasonable expectation of disclosure – effect of exclusion clauses – accessorial liability – whether knowingly concerned

TRADE PRACTICES – Unconscionable conduct – whether the purchasers were at a special disadvantage – whether the bank acted unconscionably

REMEDIES – injunctions – declarations – scope of relief

Statutes

Australian Securities and Investments Commission Act 2001 (Cth)ss 12CA, 12CB, 12CC, 12DA, 12DG

Trade Practices Act 1974 (Cth) ss 52, 51A, 51AA, 51AC, 80, 75B, 51AAB

Fair Trading Act 1989 (Qld) ss 38, 98

Property Agents and Motor Dealers Act 2000 (Qld) ss 364, 366

Cases

Ahern v The Queen (1988) 165 CLR 87 (Applied)

Australian Broadcasting Corporation v Lenah Game Meats Pty Ltd (2001) 208 CLR 199 (Discussed)

Australian Competition & Consumer Commission v CG Berbatis Holdings Pty Ltd (2003) 197 ALR 153 (Discussed)

Australian Competition & Consumer Commission v Berbatis Holdings Pty Ltd (2000) 169 ALR 324 (Discussed)

Australian Competition & Consumer Commission v Commonwealth Bank of Australia [2003] FCA 1397 (Discussed)

Australian Competition & Consumer Commission v Danoz Direct Pty Ltd [2003] FCA 881 (Discussed)

Australian Competition & Consumer Commission v Universal Sports Challenge Ltd [2002] FCA 1276 (Discussed)

Australian Competition & Consumer Commission v Simply No-Knead (Franchising) Pty Ltd [2000] FCA 1365 (Discussed)

Blomley v Ryan (1956) 99 CLR 362 (Referred to)

Bridgewater v Leahy (1998) 194 CLR 457 (Approved)

Burg Design Pty Limited v Wolki (1999) 162 ALR 639 (Approved)

Campomar Sociedad, Limitada v Nike International Limited (2000) 202 CLR 45 (Discussed)

Commercial Bank of Australia Limited v Amadio (1983) 151 CLR 447 (Approved)

Commonwealth Bank of Australia v Finding (2001) 1 Qd R 168 (Approved)

Commonwealth Bank of Australia v Smith (1991) 102 ALR 453 (Distinguished)

Demagogue Pty Ltd v Ramensky (1992) 39 FCR 31 (Approved)

Fraser v NRMA Holdings Ltd (1995) 55 FCR 452 (Discussed)

Golby v Commonwealth Bank of Australia (1996) 72 FCR 134 (Approved)

Henjo Investments Pty Limited v Collins Marrickville Pty Limited (1988) 39 FCR 546 (Approved)

Hornsby Building Information Centre Pty Ltd v Sydney Building Information Centre Ltd (1978) 140 CLR 216 (Discussed)

Hurley v McDonald’s Australia Ltd (2000) ATPR 41-741 (Discussed)

ICI Australia Operations Pty Limited v Trade Practices Commission (1992) 38 FCR 248 (Approved)

Kimberley NZI Finance Ltd v Torero Pty Ltd (1989) ATPR (Digest) 53,193 (Approved)

Lam v Ausintel Investments Australia Pty Ltd (1989) 97 FLR 458 (Discussed)

Lezam Pty Ltd v Seabridge Australia Pty Ltd (1992) 35 FCR 535 ((Approved)

Melway Publishing Pty Limited v Robert Hicks Pty Limited (2001) 205 CLR 1 (Approved)

Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd (1982) 149 CLR 191 (Approved)

Poseidon Ltd v Adelaide Petroleum NL Ltd (1992) 105 ALR 25 (Approved)

Rhone-Poulenc Agrochemie SA v UIM Chemical Services Pty Ltd (1986) 12 FCR 477 (Discussed)

Spencer v The Commonwealth (1907) 5 CLR 418 (Discussed)

State Government Insurance Corporation v Government Insurance Office of New South Wales (1991) 28 FCR 511 (Approved)

Taco Company of Australia Inc v Taco Bell Pty Ltd (1982) 42 ALR 177 (Approved)

Ting v Blanche (1983) 118 ALR 543 (Discussed)

Yorke v Lucas (1984) 158 CLR 661 (Approved)

Other Authorities

Miller’s Annotated Trade Practices Act 1974 (24th ed)

AUSTRALIAN COMPETITION AND CONSUMER COMMISSION v OCEANA COMMERCIAL PTY LTD, MARKFAIR PTY LTD, ADVANCED COMMERCIAL DEVELOPMENTS PTY LTD, COMMONWEALTH BANK OF AUSTRALIA, CHRISTOPHER RUSSELL BILBOROUGH, DUDLEY JAMES QUINLIVAN, SHANE ANDREWS, MICHAEL BYROM, PETER EGGENHUIZEN, GREGORY POINTON, DEAN CORNISH, JOHN GROUNDS, RODNEY JOHANSON

Q232 of 2001

KIEFEL J

BRISBANE

18 DECEMBER 2003

FEDERAL COURT OF AUSTRALIA

Australian Competition & Consumer Commission v Oceana Commercial Pty Ltd [2003] FCA 1516

Index

BACKGROUND

THE STATUTORY PROVISIONS

THE ALLEGATIONS

against Coral Reef, Napc and Investlend

The NAPC Scheme Generally

The NAPC Scheme and the Gleesons. 14

Against Mr Bilborough

Against Mr Quinlivan

Against the NAPC and Investlend Representatives

Against Redwind and its Directors

Against Mr Pointon

Against Mr Johanson

Against The Bank

the evidence

the marketing and sale of units by napc & Investlend

Redwind’s agreement with napc

the marketing and sale of unit 29 to the Gleesons

the solicitors

the period to settlement - the bank

WHETHER CONTRAVENTIONS

The napc scheme and seciton 52 trade practices act 1974 (Cth)

particular representaitons in the course of the napc scheme

Non-disclosures and the scheme

non-disclosures and the Gleesons

Representations made to the Gleesons

whether market value representation misleading

whether representation of average annual capital growth rate misleading

the liability of coral reef and investlend

the LIABILITY OF Mr Bilborough

the liability of Mr Quinlivan

the liability of Mr Eggenhuizen

the liability of Mr byrom

the liability of Mr Andrews

THE KNOWLEDGE AND COMPLICITY OF Redwind AND ITS DIRECTORS

THE LIABILITY OF Mr Pointon

THE LIABILITY OF Mr Johanson

THE CASE AGAINST THE BANK

ORDERS

AUSTRALIAN COMPETITION AND CONSUMER COMMISSION v OCEANA COMMERCIAL PTY LTD, MARKFAIR PTY LTD, ADVANCED COMMERCIAL DEVELOPMENTS PTY LTD, COMMONWEALTH BANK OF AUSTRALIA, CHRISTOPHER RUSSELL BILBOROUGH, DUDLEY JAMES QUINLIVAN, SHANE ANDREWS, MICHAEL BYROM, PETER EGGENHUIZEN, GREGORY POINTON, DEAN CORNISH, JOHN GROUNDS, RODNEY JOHANSON

Q232 of 2001

KIEFEL J

BRISBANE

18 DECEMBER 2003

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

|

QUEENSLAND DISTRICT REGISTRY |

Q 232 OF 2001 |

|

|

BETWEEN: |

AUSTRALIAN COMPETITION AND CONSUMER COMMISSION APPLICANT

|

|

|

AND: |

OCEANA COMMERCIAL PTY LTD (ACN 070 287 991) FIRST RESPONDENT

MARKFAIR PTY LTD (ACN 065 542 761) SECOND RESPONDENT

ADVANCED COMMERCIAL DEVELOPMENTS PTY LTD (ACN 076 810 672) THIRD RESPONDENT

COMMONWEALTH BANK OF AUSTRALIA (ACN 123 123 124) FOURTH RESPONDENT

CHRISTOPHER RUSSELL BILBOROUGH FIFTH RESPONDENT

DUDLEY JAMES QUINLIVAN SIXTH RESPONDENT

SHANE ANDREWS SEVENTH RESPONDENT

MICHAEL BYROM EIGHTH RESPONDENT

PETER EGGENHUIZEN NINTH RESPONDENT

GREGORY POINTON TENTH RESPONDENT

DEAN CORNISH ELEVENTH RESPONDENT

JOHN GROUNDS TWELFTH RESPONDENT

RODNEY JOHANSON THIRTEENTH RESPONDENT

|

|

|

DATE OF ORDER: |

||

|

WHERE MADE: |

BRISBANE |

|

THE COURT DECLARES THAT:

1. That the first and second respondents, Oceana Commercial Pty Ltd, formerly known as Coral Reef Group Pty Limited, and Markfair Pty Ltd, formerly known as Investlend Pty Ltd, did between November 1997 and November 1998 contravene s 52 of the Trade Practices Act 1974 (Cth) by misleading purchasers as to the rate by which residential units at the Gold Coast would increase in value over the following ten years by applying a rate of annual growth of 8 per cent when they had no reasonable basis for so representing.

2. That each of the fifth, seventh and eighth respondents were knowingly concerned in such contraventions and that the fifth respondent conspired with the first, second and sixth respondents and National Asset Planning Corporation Pty Ltd to effect the contraventions.

3. That the sixth respondent was knowingly concerned in such contraventions and conspired with the first, second and fifth respondents and National Asset Planning Corporation Pty Ltd to effect the contraventions in the period from November 1997 to 9 September 1998.

4. That in or about September 1998 the first and second respondents contravened s 52 of the Trade Practices Act 1974 (Cth) by misleading purchasers namely Mr and Mrs Gleeson about the rate by which the unit they were to purchase would increase over the following years by applying an annual rate of 8 per cent per annum, when they had no reasonable basis for so representing and by representing Investlend Pty Ltd as a qualified financial advisor who would act in their interests.

5. That each of the fifth, seventh and eighth respondents were knowingly concerned in those contraventions and in the case of the fifth respondent, conspired with the first and second respondents and National Asset Planning Corporation Pty Ltd, to effect those contraventions.

6. Adjourn for further hearing the question of costs.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

QUEENSLAND DISTRICT REGISTRY |

Q 232 of 2001 |

|

BETWEEN: |

AUSTRALIAN COMPETITION AND CONSUMER COMMISSION APPLICANT

|

|

AND: |

OCEANA COMMERCIAL PTY LTD (ACN 070 287 991) FIRST RESPONDENT

MARKFAIR PTY LTD (ACN 065 542 761) SECOND RESPONDENT

ADVANCED COMMERCIAL DEVELOPMENTS PTY LTD (ACN 076 810 672) THIRD RESPONDENT

COMMONWEALTH BANK OF AUSTRALIA (ACN 123 123 124) FOURTH RESPONDENT

CHRISTOPHER RUSSELL BILBOROUGH FIFTH RESPONDENT

DUDLEY JAMES QUINLIVAN SIXTH RESPONDENT

SHANE ANDREWS SEVENTH RESPONDENT

MICHAEL BYROM EIGHTH RESPONDENT

PETER EGGENHUIZEN NINTH RESPONDENT

GREGORY POINTON TENTH RESPONDENT

DEAN CORNISH ELEVENTH RESPONDENT

JOHN GROUNDS TWELFTH RESPONDENT

THIRTEENTH RESPONDENT

|

|

JUDGE: |

|

|

DATE: |

|

|

PLACE: |

BRISBANE |

REASONS FOR JUDGMENT

BACKGROUND

1 These proceedings involve the marketing and sale of residential units at the Gold Coast in the years 1997 and 1998. At issue is the means by which they were sold. The Australian Competition & Consumer Commission (‘the Commission’) alleges that sales were effected using a system of marketing which contravened the Trade Practices Act 1974 (Cth) (‘the Act’). The fifth and sixth respondents, Mr Bilborough and Mr Quinlivan, and companies with which they were associated, Coral Reef Group Pty Limited (‘Coral Reef’), National Asset Planning Corporation Pty Ltd (‘NAPC’) and Investlend Pty Ltd (‘Investlend’), are alleged to have implemented a system of marketing referred to in the amended statement of claim as the ‘NAPC Scheme’. An allegation that they were responsible for having devised the scheme was not pursued.

2 The NAPC scheme involved a number of steps commencing with telemarketing. This was followed by a seminar at which the benefits of investing in property at the Gold Coast using negative gearing principles and, for those who qualified, an in-home ‘consultation’. At this point prospective purchasers were encouraged to attend at the Gold Coast. Those who accepted were allocated a ‘runner’ whose task was to show them selected properties and introduce them to the ‘financial advisor’. The properties were chosen from a number where Coral Reef had an agreement for marketing. Up to this point the steps were undertaken by representatives of NAPC. The financial advisor was a representative of Investlend. The financial advice consisted primarily of a computer analysis which provided them with projections of income and of the value of the unit at certain points in the future amongst other things. A purchaser was then taken to a solicitor to whom NAPC and Investlend usually referred purchasers.

3 The Commission seeks declarations or injunctions, but not pecuniary penalties, based upon the knowledge or participation of the respondents in the NAPC scheme as a whole. The Commission accepts that not all of the steps in the scheme would constitute a contravention of s 52 of the Act. It nevertheless contends that the conduct of the scheme can be characterised as conduct that is misleading and deceptive or conduct which is likely to mislead or deceive.

4 The Commission’s case also relies upon the use of specific misrepresentations in the carrying out of the scheme in the relevant period. Principal amongst them are statements as to the present and future values of the units being sold, the latter involving the rate at which the unit was said to increase in value. Non-disclosures of aspects of the scheme, such as the existence of a marketing arrangement and a substantial fee to be paid by a developer pursuant to it, are also relied upon.

5 The NAPC scheme is alleged to have been applied to particular purchasers, Mr and Mrs Gleeson. No relief is sought on their behalf. They were purchasers of a unit in a development called the Chevron Palms Units at Chevron Island, Surfers Paradise, in September 1998. Specific misrepresentations are alleged to have been made to them. The Commission also relies upon non-disclosures as misleading and deceptive conduct.

6 In addition to the respondents referred to above, a number of others are said to have been involved in the NAPC scheme. Redwind Pty Ltd, as the third respondent was then named, was a developer who entered into an agreement with Coral Reef for the marketing of its Chevron Palm units. It is also sought to make liable its directors, Mr Cornish and Mr Grounds (the eleventh and twelfth respondents). The eighth and ninth respondents, Messrs Byrom and Eggenhuizen, were NAPC representatives and, respectively, a runner and an in-home consultant. Mr Andrews, the seventh respondent, acted for Investlend as an advisor. Each of them dealt with Mr and Mrs Gleeson. The tenth and thirteenth respondents, Messrs Pointon and Johanson, are solicitors whose firms were on a ‘panel’ maintained by NAPC and Investlend. They dealt with purchasers of marketed properties. Mr Pointon acted for Mr and Mrs Gleeson in the purchase of their unit and Mr Johanson acted for Redwind in the same conveyance.

7 The fourth respondent (‘the bank’) stands in a somewhat different position from the other respondents. A reference to ‘the respondents’ in these reasons does not include a reference to the bank. It was the Gleesons’ bank with respect to the purchase of the unit and held a valuation of the property. It is not alleged that it took part in, or knew of, the NAPC Scheme. It is alleged that, by reason of a valuation it had obtained, it knew of the use of such a marketing scheme in the sale to the Gleesons and that the purchase price was well above the unit’s market value. Its liability is said to depend upon its failure to alert the Gleesons to these matters.

THE STATUTORY PROVISIONS

8 Section 52(1) in Part V of the Act provides that:

‘A corporation shall not, in trade or commerce, engage in conduct that is misleading or deceptive or is likely to mislead or deceive’.

Conduct within the meaning of s 52 includes refusing to do an act: s 4(2).

9 Section 51A is relied upon by the Commission in connexion with representations alleged to have been made as to the future value of properties sold. It provides:

‘Interpretation

(1) For the purposes of this Division, where a corporation makes a representation with respect to any future matter (including the doing of, or the refusing to do, any act) and the corporation does not have reasonable grounds for making the representation, the representation shall be taken to be misleading.

(2) For the purposes of the application of subsection (1) in relation to a proceeding concerning a representation made by a corporation with respect to any future matter, the corporation shall, unless it adduces evidence to the contrary, be deemed not to have had reasonable grounds for making the representation.

(3) Subsection (1) shall be deemed not to limit by implication the meaning of a reference in this Division to a misleading representation, a representation that is misleading in a material particular or conduct that is misleading or is likely or liable to mislead.’

10 Section 75B(1) (‘accessorial liability’) relevantly provides that a reference in this Part to a person involved in a contravention of a provision of Part V shall be read as a reference to a person who:

‘(c) has been in any way directly or indirectly, knowingly concerned in, or party to, the contravention; or

(d) has conspired with others to effect the contravention’.

Allegations of a conspiracy are now restricted to the first and second respondents and the fifth and sixth respondents.

11 Section 80(1) of the Act relevantly provides that the Court may grant injunctions, on the application of the Commission, in such terms as are deemed appropriate where it is satisfied that a person has engaged in conduct that contravenes Part IVA or Part V or where they have been knowingly concerned in the contravention.

12 Sections 51AA(1) and s 51AC, in Part IVA of the Act, are relevant to the case brought against the bank:

‘51AAUnconscionable conduct within the meaning of the unwritten law of the States and Territories

(1) A corporation must not, in trade or commerce, engage in conduct that is unconscionable within the meaning of the unwritten law, from time to time, of the States and Territories.’

‘51AC Unconscionable conduct in business transactions

(1) A corporation must not, in trade or commerce, in connection with:

(a) the supply or possible supply of goods or services to a person (other than a listed public company); or

(b) the acquisition or possible acquisition of goods or services from a person (other than a listed public company);

engage in conduct that is, in all the circumstances, unconscionable.

(2) A person must not, in trade or commerce, in connection with:

(a) the supply or possible supply of goods or services to a corporation (other than a listed public company); or

(b) the acquisition or possible acquisition of goods or services from a corporation (other than a listed public company);

engage in conduct that is, in all the circumstances, unconscionable.

(3) Without in any way limiting the matters to which the Court may have regard for the purpose of determining whether a corporation or a person (the supplier) has contravened subsection (1) or (2) in connection with the supply or possible supply of goods or services to a person or a corporation (the business consumer), the Court may have regard to:

(a) the relative strengths of the bargaining positions of the supplier and the business consumer; and

(b) whether, as a result of conduct engaged in by the supplier, the business consumer was required to comply with conditions that were not reasonably necessary for the protection of the legitimate interests of the supplier; and

(c) whether the business consumer was able to understand any documents relating to the supply or possible supply of the goods or services; and

(d) whether any undue influence or pressure was exerted on, or any unfair tactics were used against, the business consumer or a person acting on behalf of the business consumer by the supplier or a person acting on behalf of the supplier in relation to the supply or possible supply of the goods or services; and

(e) the amount for which, and the circumstances under which, the business consumer could have acquired identical or equivalent goods or services from a person other than the supplier; and

(f) the extent to which the supplier's conduct towards the business consumer was consistent with the supplier's conduct in similar transactions between the supplier and other like business consumers; and

(g) the requirements of any applicable industry code; and

(h) the requirements of any other industry code, if the business consumer acted on the reasonable belief that the supplier would comply with that code; and

(i) the extent to which the supplier unreasonably failed to disclose to the business consumer:

(i) any intended conduct of the supplier that might affect the interests of the business consumer; and

(ii) any risks to the business consumer arising from the supplier's intended conduct (being risks that the supplier should have foreseen would not be apparent to the business consumer); and

(j) the extent to which the supplier was willing to negotiate the terms and conditions of any contract for supply of the goods or services with the business consumer; and

(k) the extent to which the supplier and the business consumer acted in good faith.’

13 Section 51AA(2) provides that s 51AA does not apply to conduct that is prohibited by s 51AC.

14 There have been changes effected with respect to conduct in connexion with ‘financial services’. Section 51AAB(1) of the Trade Practices Act provides that s 51AA does not apply to conduct engaged in relation to financial services. Section 51AF(2) likewise provides that s 52 does not apply to such services. By s 4 of the Act ‘financial services’ has the same meaning as in Division 2 of Part 2 of the Australian Securities and Investments Commission Act 2001 (Cth). It is there defined in such a way as would include the provision of a loan facility. From 11 March 2002 that Act dealt with unconscionable conduct in relation to the provision of financial services (ss 12CA - 12CC) of Division 2 and with misleading and deceptive conduct in connexion with those services (s 12DA). The latter is in the same terms as s 52 of the Trade Practices Act. Section 12CA mirrors s 51AA of the Trade Practices Act and s 12CB contains similar proscriptions to s 51ACbut the list of matters which the Court may have regard to are fewer than in s 51AC(3). Section 12GD provides the Court with power to grant injunctions ‘on the application of the Minister, the Commission or any other person’ where conduct is engaged in which constitutes a contravention of Division 2. The ‘Commission’ is the Australian Securities and Investments Commission.

15 Section 38(1) of the Fair Trading Act 1989 (Qld) is in the same terms as s 52 of the Trade Practices Act 1974 (Cth) save that the prohibition extends to the conduct of a natural person. Section 98(1) and (2) of that Act provides that an injunction may be granted against a person if they have engaged in such conduct. Section 98(3) however provides that the power of the Court to grant an injunction restraining a person from engaging in such conduct:

‘(b) does not include the power to grant an injunction restraining a person from engaging in conduct that constitutes or would constitute a contravention solely of section 38 … unless -

(i) the application is made by the Minister or the commissioner on the grounds that a consumer is, or consumers generally are or would be, adversely affected by the conduct; or

(ii) the application is made by a person who is, or would be, adversely affected by the conduct as a consumer’.

The ‘commissioner’ is the Commissioner for Fair Trading. A question may arise as to the Commission’s reliance upon the Fair Trading Act provisions.

THE ALLEGATIONS

against coral reef, NAPC and Investlend

The NAPC Scheme Generally

16 The first respondent, Oceana Commercial Pty Ltd was, until 22 December 1999, Coral Reef Group Pty Limited and I shall refer to it as ‘Coral Reef’ in these reasons. Mr Bilborough was its sole director and shareholder. Coral Reef obtained units from developers on the Gold Coast for the purpose of their marketing and sale. It was the signatory to an agreement with Redwind for the marketing of what are described in the pleadings as the Chevron Units. They have, however, been called the ‘Chevron Palm Units’ elsewhere and by the witnesses in the proceedings and I will also refer to them by that description. NAPC was previously called Coastal Reef Pty Ltd. I shall continue to refer to it as NAPC. It was in voluntary liquidation at the commencement of the action and is not a party to it. Mr Bilborough was its sole director and shareholder. It was involved in marketing the properties and obtaining potential purchasers.

17 The second respondent traded as ‘Investlend (Australia)’. Up until 9 September 1998 its shares were held equally as between Mr Quinlivan’s wife and Mr Bilborough. Mr Quinlivan managed it. Its function was to provide financial advice to prospective purchasers brought to it by the NAPC representatives and to obtain finance for the purchase. After 9 September 1998 Mr Bilborough alone is alleged to have owned and controlled it. It is not suggested that Mr Quinlivan had a role in Investlend after this time. The NAPC scheme is alleged to have been utilised by Coral Reef, NAPC and Investlend to effect sales of some 900 to 1000 properties in the period in question. Many of the steps involved in the scheme are not in dispute. It is however necessary to set out the whole of the allegation concerning its operation.

‘17. The NAPC Scheme operated in the following manner:

(a) Coral Reef would enter into a marketing arrangement with a developer for a particular development of residential units in the City of the Gold Coast;

(b) pursuant to the marketing arrangement, Coral Reef would be paid a marketing fee per unit for negotiating the sale of units in the development at the marketed price;

(c) the marketing fee:

(i) was substantially in excess of the maximum commission payable to a licensed real estate agent regulated under the Auctioneers and Agents Act 1971 (Qld) who negotiated a sale for the same purchase price as the marketed price;

(ii) was, on average, approximately $30,000 per unit, and on occasions as high as $35,000 per unit;

(d) Coral Reef and the developer would agree the marketed price at which the residential units were to be sold;

(e) the marketed price of each unit was substantially in excess of:

(i) the price at which a developer could reasonably expect to sell the unit without engaging a marketer;

(ii) the fair market value of that unit;

(f) Coral Reef would in turn engage NAPC to undertake the marketing;

(g) NAPC would compile and maintain a stock-list of residential units available for sale from each developer at their respective marketed prices;

(h) NAPC would engage telemarketers to canvass members of the public at a location removed from the City of the Gold Coast (“the targeted location”) in order to:

(i) produce a sufficient group of persons to attend an investment seminar conducted by NAPC at the targeted location;

(ii) determine whether such persons were qualified to participate in the investment seminar, and to purchase a unit in a residential development marketed by Coral Reef and NAPC;

PARTICULARS

Pursuant to the NAPC Scheme members of the public were qualified by earning a minimum income of $30,000 to $40,000 per annum and having a minimum equity in a residential property (usually the family home) of at least $60,000.

(i) if a member of the public was qualified to attend the investment seminar and expressed interest in doing so NAPC would send them a written invitation;

(j) NAPC arranged to conduct an investment seminar at a venue at the targeted location;

(k) at the investment seminar NAPC represented to the members of the public who attended (the “prospects”) that:

(i) NAPC, the presenter, and the other in-house consultants were paid for or sponsored by a group of Gold Coast developers wishing to promote the Gold Coast;

(ii) if they bought an investment property and paid it off, they would have a valuable asset and rental income to support them in their retirement;

(iii) they could negatively gear their purchase against their present income and rental received from the investment and that investment properties on the Gold Coast accordingly cost relatively little to buy and were affordable even by people with modest means;

(iv) rich people exploit the same means to get wealthy, and reduce their income tax at the same time, and that the process was perfectly legal;

(v) investment opportunities on the Gold Coast offered unique benefits in terms of capital growth;

(vi) The Gold Coast averaged capital growth on property values in excess of 10% per annum;

(vii) they could arrange an in-home consultation where an in-home consultant would attend at their home to explain more fully property investment on the Gold Coast and negative gearing with regard to their particular circumstances;

(viii) if they were suitable persons to purchase an investment property on the Gold Coast, they would be offered free or subsidised travel to, and accommodation on, the Gold Coast to inspect investment properties;

(l) the investment seminar was conducted according to a script, a copy of which is available for inspection during business hours at the office of the applicant’s solicitors;

(m) NAPC engaged consultants to attend upon those prospects who requested an in-home consultation;

(n) at the in-home consultation, the consultant made representations to the prospects:

(i) in the terms pleaded in subparagraphs (k)(ii) to (vi) hereof;

(ii) that they were his or her clients and that NAPC and its staff acted in their interests;

(o) further, at the in-home consultation, the consultant engaged by NAPC:

(i) assessed and made a note of the personality type of the prospects, which was recorded on a proforma document to be sent to NAPC and Investlend, as pleaded in subparagraph (p) hereof, without the prospects’ knowledge;

(ii) made a list of the features of the investment proposal that most appealed to the prospects which was recorded on a proforma document to be sent to NAPC and Investlend, as pleaded in subparagraph (p) hereof, without the prospects’ knowledge;

(iii) obtained details of the financial position of the prospects which was also recorded on the proforma document to be sent to NAPC and Investlend, as pleaded in subparagraph (p) hereof;

(iv) determined whether the prospects met the minimum financial criteria, referred to in subparagraph (h)(ii) hereof;

(v) attempted to convince prospects who did meet the requisite criteria to travel to the Gold Coast to get free advice from a financial consultant and to inspect some properties they may care to purchase;

(vi) offered prospects free or subsidised travel to, and accommodation on, the Gold Coast to inspect prospective investment properties;

(p) in the case of each prospect who agreed to travel to the Gold Coast, the in-home consultant:

(i) completed a pro forma document devised by NAPC which recorded personal details of the prospect, together with the information pleaded in subparagraphs (o)(i), (ii) and (iii) hereof;

(ii) forwarded a copy of such document to NAPC and Investlend;

(q) upon such document and information being received:

(i) NAPC assigned a “runner” to the prospect to show the prospect investment properties when they travelled to the Gold Coast;

(ii) Investlend assigned a “financial adviser” to the prospect;

(r) each of the runner and the financial adviser were given a copy of the document referred to in subparagraph (p) hereof;

(s) upon arrival at the Gold Coast, prospects would be met by their assigned runner who would:

(i) introduce them to their assigned financial adviser at Investlend;

(ii) show them residential units only from the stocklists maintained by NAPC;

(iii) reiterate the benefits described in subparagraphs (k)(iii), (v) and (vi) of investing in residential units on the Gold Coast;

(iv) if prospects agreed to purchase a residential unit, introduce or take them to a solicitor, who would act for them on the conveyance of the unit;

(t) upon being introduced to the prospects by their assigned runner, the financial adviser at Investlend would:

(i) explain negative gearing and show prospects an analysis of properties they could consider purchasing;

(ii) review the prospects’ financial position to determine the amount which they would be able to borrow;

(iii) by computer assisted financial analysis, represent what were purported to be the financial benefits of the proposed investments;

(iv) use in such demonstration:

(A) the marketed price as the fair market value of the residential unit;

(B) a capital growth rate of 7% or 8%;

(v) represent that capital growth rates on the Gold Coast exceeded 10% per annum, and that it was accordingly reasonable and conservative to use a capital growth rate of 7% or 8% to assess the investment;

(u) if prospects agreed to purchase a residential unit, the financial adviser at Investlend would:

(i) prepare a finance application, to be submitted to a lender to enable the purchase to proceed, for which Investlend charged the prospects a fee;

(ii) prepare documentation necessary to arrange insurance for the residential unit;

(v) after the finance documentation was completed either the financial adviser or the runner would organise a solicitor to act for the prospects in the purchase of the residential unit, with such solicitor chosen from a panel of firms.

(w) Johanson and Pointon, and their respective firms Short Punch and Greatorix and Perrin Pointon, were on the said panel of firms.’

18 In relation to the NAPC scheme, it is alleged that each of Coral Reef, NAPC and Investlend ‘engaged in a course of conduct, namely the operation of the NAPC Scheme, including the operation of the scheme in its application to the Gleesons, that contravened s 52 of the Act …’.

19 In par 22(a) to (f) and (g) it is alleged that some elements of the scheme were or were likely to mislead or deceive. I have highlighted in par 17 set out above those statements which are dealt with in par 22 as contravening conduct. Paragraph 22 is in these terms:

‘22. The representations made to prospects as part of the NAPC Scheme were misleading or deceptive, or likely to mislead or deceive in that:

(a) NAPC, the seminar presenter and the in-house consultants were not paid for or sponsored by a group of Gold Coast developers wishing to promote the Gold Coast, but in fact were paid from marketing fees derived from the sale of marketed properties;

(b) NAPC and its representatives did not act in the interests of the prospects, but in fact acted in their own interest to derive a marketing fee which was not disclosed to the prospects;

(c) investment opportunities on the Gold Coast did not offer the prospects unique benefits in terms of capital growth;

(d) residential units on the Gold Coast did not enjoy capital growth in excess of 10% per annum;

(e) there was no reasonable likelihood that the marketed properties would return capital growth in the order of 7% or 8% per annum. Insofar as such a representation was as to a future matter, none of the participants in the NAPC Scheme had reasonable grounds for making the representation and the applicant relies on section 51A of the Act;

(f) the marketed price was not the fair market value of the marketed property;

(g) it was not reasonable and conservative to use the marketed price as the value of the residential unit to assess the benefits of the investment;

(h) it was not reasonable and conservative to use 7% or 8% per annum growth rates to assess the benefits of the investment.’

20 It is also alleged that, in order to induce the belief that NAPC and Investlend were separate businesses, they maintained separate offices.

21 Those representations pleaded in parts of par 17, and dealt with in par 22, are later alleged to amount to individual contraventions on the part of NAPC or Investlend. Whilst some respondents contended that the Commission’s case, in connexion with the NAPC scheme, was limited to its operation as a whole, these allegations are clearly alternative. Other respondents are said to be liable as accessories under s 75B(1). I shall deal with them separately in these reasons.

22 The third aspect of the Commission’s case, concerning the application of the scheme generally, is based upon non-disclosures to purchasers. At par 20 it is alleged:

‘20. Each of Coral Reef, NAPC, Investlend, Bilborough, Quinlivan, Andrews, Byrom, Eggenhuizen, Pointon and Johanson:

(a) knew of the NAPC Scheme, the part other respondents played in it, and agreed to participate in it;

(b) knew that the purpose of the NAPC Scheme was to identify prospects and induce them to purchase marketed properties at the marketed prices in the belief that those prices were fair market value;

(c) believed, and acted on the belief, that prospects would be unlikely to purchase marketed properties if they knew of:

(i) the existence of the marketing arrangement;

(ii) the nature, existence or magnitude of the marketing fee;

(iii) the fair market value of the marketed properties;

(iv) the fact that the marketer was not acting in their interests;

(v) the relationship between NAPC, Investlend, Coral Reef and the developer;

(vi) the fact that the income or remuneration of NAPC, Investlend, the telemarketers, the in-home consultants, the runners and the financial advisers depended on persuading prospects to buy marketed properties; and

(d) at no time disclosed any of the matters pleaded in subparagraph (c) hereof to prospects or purchasers of marketed properties;

(e) believed, and acted upon the belief that no other marketing participant would disclose any of the matters pleaded in subparagraph (c) hereof to prospects or purchasers.’

It is later alleged, in par 64, that the non-disclosures of the matters referred to in par 20(c) amount to a contravention of s 52 by Coral Reef, NAPC and Investlend, although there is some doubt as to whether these claims are pursued, as I later observe.

23 I will not set out each of the allegations of conspiracies affecting the first and second respondents. In summary, where it involves conduct of the other or of NAPC they are said to have been knowingly concerned in that conduct or to have conspired with the other parties to act unlawfully. These allegations extend to the operation of the NAPC scheme generally, its application to the Gleesons, and representations and non-disclosures in the course of it to purchasers generally.

The NAPC Scheme and the Gleesons

24 The pleading then turns to the sale, through the use of the NAPC Scheme, of Unit 29 in the Chevron Palms development to Mr and Mrs Gleeson on 24 September 1998, with the first contact occurring on 27 August 1998. It is alleged that the application of the scheme to the Gleesons involved conduct contravening s 52, principally because of misrepresentations. Not all respondents are said to be liable for each misrepresentation. Liability is also said to arise by reason of non-disclosures to the Gleesons.

25 It is alleged that on or about 31 January 1997 Coral Reef entered into a marketing agreement ‘the Chevron Marketing Agreement’ with Redwind. The eleventh and twelfth respondents, Messrs Cornish and Grounds, were directors of Redwind. Mr Johanson, the thirteenth respondent, was a member of the firm of solicitors, Short Punch & Greatorix, and acted for Redwind. It is alleged that the agreement was made pursuant to, and utilising, the NAPC Scheme and provided for a marketing fee in an amount by which the purchase price for each unit sold exceeded $130,000. It is alleged that Redwind agreed with Coral Reef that the units be sold at prices of between $159,900 and $164,900. Coral Reef is then said to have engaged NAPC to market the Chevron Units ‘using the NAPC scheme, at prices between $159,900 and $164,900’ and that these prices were substantially in excess of the fair market value of the units.

26 Mr and Mrs Gleeson resided in Cairns in northern Queensland. They were invited by a telemarketer to attend an investment seminar on 8 September 1998 and did so. At that seminar representatives of NAPC were alleged to have said to them (par 33(d)):

‘…

(i) that NAPC was sponsored by a group of developers to promote the Gold Coast;

(ii) that there were negative gearing benefits of purchasing investment properties on the Gold Coast;

(iii) that the capital growth stemmed from infrastructure spending in the region, that the infrastructure spending was continuing and that the rate of capital growth would continue;

(iv) that no other region of Australia offered a comparable growth rate to the Gold Coast;

(v) that no other form of investment yielded the same level and certainty of return as property investing on the Gold Coast;

(vi) by providing documents including newspaper clippings promoting Gold Coast investment, that there were sustained high property growth rates on the Gold Coast;

(vii) that investment in residential property on the Gold Coast would provide a secure and high rate of capital growth;’

27 The seminar was followed up with a personal consultation at the office of Mr Gleeson on 15 September 1998. Mr Eggenhuizen was NAPC’s representative on this occasion. He is alleged to have made representations to them (par 33 (f)):

‘(f) …

(i) that the Gleesons were his clients and clients of NAPC and that he and NAPC acted in the interests of its clients;

(ii) that by use of negative gearing principles known to him and NAPC, an investment property could be purchased for $165,000 and would have a net cost to the Gleesons of about $27 a week;

(iii) that capital growth rates on the Gold Coast were in the order of 11% per annum so that a $165,000 property could be conservatively expected to increase on average by 8% per annum, making it worth $390,000 in 10 years time;

(iv) that the Gleesons would need to buy several such properties over time to reach the $1 million in 17 years time that would be required for their retirement;

(v) that other forms of investment offered either insufficient returns or were too speculative to compare with the benefits of negative gearing of investment in Gold Coast real estate;

(vi) that a line of credit was the best way to finance the transaction;’

28 It is also alleged that he advised them about negative gearing and purchasing investment property on the Gold Coast and to have provided a booklet and newsletter published by NAPC:

‘(g) …

(i) advised the Gleesons about options for negative gearing and purchasing an investment property on the Gold Coast;

(ii) provided documents to the Gleesons about the benefits of negative gearing;

(iii) provided a newsletter from NAPC which included representations that:

(A) NAPC provided “a comprehensive service to [its] clients which extends from obtaining an investment property to its specific finance and insurance requirements, rental and maintenance, through a group of professional proactive companies affiliated with [NAPC]”;

(B) “Through our knowledge and research at NAPC and Investlend, we try and analyse what will be the best area and price range for our clients”;

(C) “Our aim is to reach out to the Australian community, and encourage individuals to seek and obtain a secure financial future that will allow them to enjoy a better quality of life”;’

…

(iv) provided an NAPC booklet which contained representations including:

(A) NAPC “is a group of entities who operate primarily as property marketers, offering a complete service to investors in residential and commercial real estate. This service includes assessing the requirements of individual investors, identifying the most appropriate properties for their specific negative gearing qualities and providing sound financial analysis to enable potential clients to make informed decisions”;

(B) “Investors are also protected by the use of independent solicitors, registered to operate in the state in which the asset is acquired. Solicitors are compelled to act in the best interest of their clients and face onerous consequences should they not adhere to the stringent requirements of their professional body”;

(C) NAPC “recommends the use of accredited Investment Financial Advisors who in turn arrange finance for the client’s investment only through major Banks and Financial Institutions which are backed by the Reserve Bank of Australia or Government regulated authorities”;

(D) NAPC “prides itself on doing the research for the client”;

(E) “Client’s protection and satisfaction is our objective”;’

29 He encouraged them to visit the Gold Coast and view properties and to that end offered them discounted airfares and accommodation. He subsequently provided details concerning the Gleesons to NAPC and Investlend on 16 September 1998.

30 On 24 September 1998 the Gleesons were shown Unit 29 in the Chevron Palms development by Mr Byrom who is alleged to have represented (par 33(o)):

‘(o) …

(i) the purchase price of $164,900 was fair market value for Unit 29;

(ii) units at the Chevron Units were rented out at $90-$100 per night;

(iii) there was no “low season” for holiday rentals on the Gold Coast, only “peak time” and “mid season”;

(iv) Unit 29 would be a profitable investment for them to purchase;

(v) NAPC was providing independent advice to the Gleesons and was acting in their interests;

(vi) Investlend was providing independent advice to the Gleesons and was acting in their interests;

(vii) Pointon would act as an independent legal adviser for the Gleesons in relation to their purchase of Unit 29;’

31 Mr Byrom then took the Gleesons to the offices of Investlend and introduced them to Mr Andrews. As Investlend’s representative he is said to have represented to them that (par 33(q)):

‘(q) …

(i) the purchase price of $164,900 was fair market value for Unit 29;

(ii) the purchase price of $164,900 was the appropriate price to use to analyse the benefits of buying Unit 29 as an investment;

(iii) Unit 29 would be a profitable investment for them to purchase;

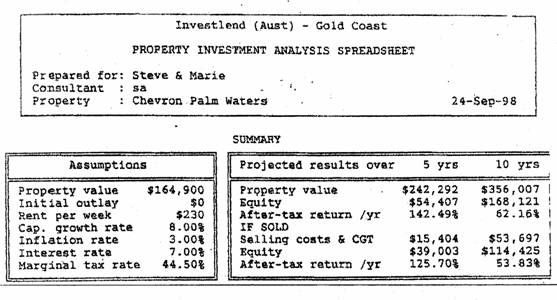

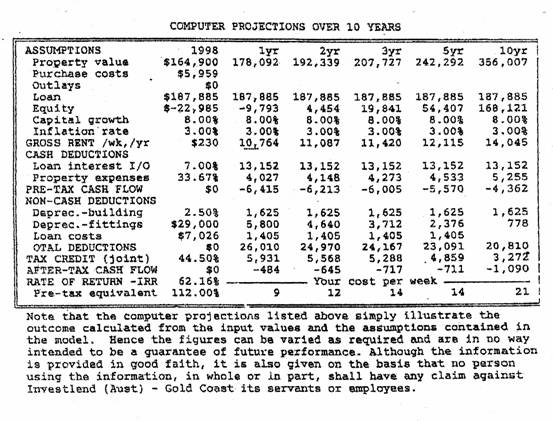

(iv) it was reasonable to apply a capital growth rate of 8% per annum to the purchase price for Unit 29 in analysing the benefit of purchasing it as an investment;

(v) they would be able to sell Unit 29 for $242,292 after 5 years, with selling costs and capital gains tax of $15,404;

(vi) they would be able to sell Unit 29 for $356,007 after 10 years, with selling costs and capital gains tax of $53,697;

(vii) there would be no net outgoing to them in buying Unit 29, after negative gearing, even if rent and occupancy figures were less than those represented by Byrom;

(viii) Investlend was providing independent advice to them and was acting in their interests;’

32 I have highlighted those particulars which are relied upon by the Commission as founding the contravening conduct. Although no relief is sought on their behalf, it is alleged that Mr and Mrs Gleeson decided to purchase the unit ‘in reliance on the representations made to them by NAPC, Investlend, Eggenhuizen, Byrom and Andrews’.

33 The representations are alleged to have been misleading or deceptive, or likely to mislead or deceive, in that:

‘41 …

(a) NAPC, the seminar presenter and Eggenhuizen were not paid for or sponsored by a group of Gold Coast developers wishing to promote the Gold Coast, but in fact were paid from marketing fees derived from the sale of marketed property;

(b) NAPC and its representatives did not act in the interests of the Gleesons, but in fact acted in their own interest to derive a marketing fee which was not disclosed to the Gleesons;

(c) Investlend and its staff did not act in the interests of the Gleesons, but in fact acted in their own interest and in the interest of the other marketing participants;

(d) investment opportunities in marketed property on the Gold Coast did not offer the Gleesons unique benefits in terms of capital growth;

(e) residential units on the Gold Coast did not enjoy capital growth in excess of 10% or 11% per annum;

(f) there was no reasonable likelihood that the marketed properties would return capital growth in the order of 7% or 8% per annum. Insofar as such a representation was as to a future matter, none of the participants in the NAPC Scheme had reasonable grounds for making the representation and the applicant relies on section 51A of the Act;

(g) the marketed price of Unit 29 was not the fair market value of that property;

(h) it was not reasonable and conservative to use the marketed price of Unit 29 as the value of the unit to assess the benefits of the investment;

(i) it was not reasonable and conservative to use 7% or 8% per annum capital growth rates to assess the benefits of investing in Unit 29;

(j) there was no reasonable likelihood that the Gleesons will be able to sell Unit 29 for $242,292 in December, 2003. Insofar as such a representation was as to a future matter, none of the participants in the NAPC Scheme had reasonable grounds for making the representation and the applicant relies on section 51A of the Act;

(k) there was no reasonable likelihood that the Gleesons will be able to sell Unit 29 for $356,007 in December, 2008. Insofar as such a representation was as to a future matter, none of the participants in the NAPC Scheme had reasonable grounds for making the representation and the applicant relies on section 51A of the Act;

(l) Investlend was not an independent financial adviser to the Gleesons, but rather was a marketing participant;

(m) Unit 29 was not a profitable investment for the Gleesons to purchase;

(n) the rentals and occupancy rates advised were not achievable by Unit 29;

(o) Pointon did not provide independent legal advice to the Gleesons, but was a marketing participant.’

34 There are also allegations of non-disclosures to the Gleesons with respect to the matters referred to in par 20(c):

‘76. Each of Coral Reef, NAPC and Investlend, by failing to disclose to the Gleesons any of the matters pleaded in paragraphs 20(c)(i) - (iv), by reason of the matters pleaded in paragraphs 16 to 20 and 34 to 36 has contravened section 52 of the Act and section 38 of the Qld Act.’

35 The same observations made earlier concerning the conspiracy allegations and accessorial liability of Coral Reef and Investlend for the conduct of the other and for NAPC’s conduct apply here.

Against Mr Bilborough

36 Mr Bilborough is alleged to have been knowingly concerned in or a party to the operation of the NAPC scheme, its application to the Gleesons and in the making of each of the representations made in the course of the scheme. He is also alleged to have been knowingly concerned in or a party to the contraventions of s 52 of the Act constituted by the non-disclosures of Coral Reef, NAPC and Investlend (par 65). He is also alleged to have conspired ‘with others’, in the carrying out of the scheme, to contravene s 52. So far as concerns the non-disclosures and misrepresentations alleged to have been made in the course of the scheme generally, he is alleged to have conspired with either or all of Coral Reef, NAPC and Investlend.

37 The only allegation involving s 38 of the Queensland Act now relied upon by the Commission is contained in par 65. It involves a number of the personal respondents:

‘65. Each of Bilborough, Quinlivan, Andrews, Byrom, Eggenhuizen, Pointon and Johanson, by failing to disclose any of the matters pleaded in paragraph 20(c), by reason of the matters pleaded in paragraphs 16 to 20:

(a) has contravened section 38 of the Qld Act;

(b) was knowingly concerned in or party to the contravention by Coral Reef, NAPC and Investlend of the provisions alleged in the preceding paragraph; and

(c) further or alternatively conspired with Coral Reef, NAPC and/or Investlend to contravene those provisions.’

38 So far as concerns the case involving conduct in the nature of representations to the Gleesons, Mr Bilborough is said to be liable as an accessory for each of them, on the basis that he was knowingly concerned in them as contraventions. Allegations of conspiracy are also made in this context, and in par 77, which relates to the non-disclosures of the matters listed in par 20(c)(i)-(vi) to the Gleesons:

‘77. Each of Bilborough, Andrews, Eggenhuizen and Byrom, by failing to disclose to the Gleesons any of the matters pleaded in paragraph 20(c)(i)-(vi), by reason of the matters pleaded in paragraphs 16 to 20 and 34 to 36:

(a) has contravened section 38 of the Qld Act;

(b) was knowingly concerned or party to in the contravention by Coral Reef, NAPC and Investlend of the provisions alleged in the preceding paragraph; and

(c) further or alternatively conspired with Coral Reef, NAPC and/or Investlend to contravene those provisions’.

39 For the reasons earlier mentioned reliance is no longer placed upon s 38 of the Queensland Act here and the allegations of conspiracy would be limited to Mr Bilborough.

Against Mr Quinlivan

40 It is likewise sought to make Mr Quinlivan liable for the operation of the NAPC scheme generally, its application to the Gleesons, the making of representations in it and the non-disclosures to purchasers. With respect to each of these contraventions of s 52 he is alleged to be liable as an accessory, as being both knowingly concerned in the contravention or having conspired with others in it. It is also sought to make him liable under s 38 of the Queensland Act (par 65).

41 The case concerning the Gleesons brought against him is more limited, by reason of his non-involvement after 9 September 1998. It is sought only to make him liable as an accessory to the representation, made at the seminar, that NAPC was sponsored by a group of Gold Coast developers. It is not sought to make him liable for non-disclosures to Mr and Mrs Gleeson.

Against the NAPC and Investlend Representatives

42 It is sought to make each of Mr Eggenhuizen, Mr Byrom and Mr Andrewsliable as accessories to the contravention of s 52 constituted by the conduct of the scheme as a whole, including its application to the Gleesons.

43 In relation to the specific representations within the scheme, Mr Eggenhuizen is said to have been knowingly concerned in those made at the seminar concerning sponsorship by the developers; that investment opportunities offered unique benefits in terms of capital growth; that the Gold Coast averaged capital growth in property values in excess of 10 per cent per annum; and for both the representation made at the seminar and in the in-home consultation that prospective purchasers were clients. He is not said to have been knowingly concerned in what was thereafter represented in the in-home consultation and following. In particular he is not alleged to be involved in the later representation about the use of 8 per cent per annum to assess capital growth, although it is alleged in par 20 that he knew of the scheme as a whole.

44 Mr Andrews is alleged to have been knowingly concerned in the representations that the sale price was a property’s market value and as to the reliability of capital growth rates at 7, 8 and 10 per cent. Liability on the part of Mr Byrom is not alleged to arise from his participation in any specific representations made in the course of the scheme.

45 Each of the three representatives are alleged to have contravened s 38 by the non-disclosure to purchasers of the matters listed in par 20(c) and to have been knowingly concerned in Coral Reef, NAPC or Investlend’s contravention constituted by similar non-disclosures.

46 So far as concerns the Gleesons Mr Eggenhuizen is sought to be made liable as an accessory for the representation at the seminar concerning sponsorship by developers; and for his statement that the Gleesons were his clients; for those contained in the NAPC newsletter and booklet concerning NAPC’s role and that NAPC and Investlend were providing independent advice; and for his statements about capital growth rates. He is also said to be accessorily liable for Mr Andrews’ statements to that effect but not the representation as to price and market value. It is sought to render him liable as an accessory to the s 52 contravention constituted by the companies’ non-disclosures and for his failure to disclose the matters referred to in par 20(c) to the Gleesons.

47 The case against Mr Andrews, as an accessory, concerning the representations to the Gleesons rests upon statements in NAPC’s material provided to them; upon his statements that NAPC and Investlend were providing independent advice and acting in their interests; and upon the statements as to market value and as to the application of capital growth rates.

48 So far as concerns Mr Byrom, and the case concerning the Gleesons, it is also sought to make him liable as an accessory to the statements made by Mr Eggenhuizen about their being clients of NAPC, for the statements about NAPC in the newsletter and booklet and for his and Mr Andrews’ statements about NAPC and Investlend providing independent advice. He is also said to have participated in the representation as to market value. Liability based upon the non-disclosures to the Gleesons of the matters in par 20(c) is alleged against him in the same terms as against Mr Eggenhuizen and Mr Andrews.

Against Redwind and its Directors

49 It is alleged that on 31 January 1997 Coral Reef entered into a marketing agreement with Redwind with respect to the Chevron Palm development. Redwind, through Mr Cornish and Mr Grounds, is alleged to have known that Coral Reef, through NAPC, would market the units using the NAPC scheme; of the extent of the marketing fee; that the marketed price of the units in the development was in excess of their fair market value; that Redwind itself would receive an amount for the units which was substantially in excess of their market value; and that prospective purchasers would not be informed of these matters (par 24). In view of its valuation evidence I do not understand the Commission to press the allegation concerning the amount Redwind received. Paragraph 25 alleges that the marketing agreement:

‘(a) was made pursuant to and utilising the NAPC scheme;

(b) provided for a marketing fee in the amount that the purchase price for each unit sold exceeded $130,000’.

50 It is then alleged, in par 26, that Redwind agreed with Coral Reef that the Chevron Palm Units would be sold at prices between $159,900 and $164,900 each. It is sought to make each of Redwind and Mr Grounds and Mr Cornish liable as having been knowingly concerned in the application of the scheme generally to the Gleesons. It is also sought to make them liable as accessories for the representation as to the price for the unit being its market value. Liability on their part is not however based upon the non-disclosures to the Gleesons.

Against Mr Pointon

51 It is not in issue that Mr Pointon, a member of the firm of Perrin Pointon, acted for Mr and Mrs Gleeson in connexion with their contract to purchase the unit and the settlement of it. He and his firm are also alleged to have been on the panel utilised by NAPC and Investlend. It is alleged that he knew of the NAPC scheme and the part others played in it and he is alleged to have been knowingly concerned in the contravention of s 52 constituted by the operation of the whole scheme and in the application of the whole scheme to the Gleesons.

52 An alternative basis for liability is alleged to arise from Mr Pointon’s non-disclosures. In relation to disclosures to purchasers generally, liability is founded upon the matters referred to in par 20(c). He is alleged to have contravened s 38 of the Queensland Act thereby and to have been knowingly concerned in NAPC and Investlend’s contraventions.

53 In relation to Mr and Mrs Gleeson it is alleged that:

‘37. Between 24 September 1998 and 21 December 1998 Pointon:

(a) owed a duty to act with reasonable care, skill and diligence as the solicitor for the Gleesons and to inform them of all matters known to him that were relevant to them purchasing Unit 29;

(b) knew how the NAPC Scheme worked;

(c) knew that the purchase price for Unit 29 paid by the Gleesons included a marketing fee of $34,900;

(d) knew that Unit 29 was being marketed to the Gleesons pursuant to the NAPC Scheme;

(e) knew that commissions were paid to marketing participants in the NAPC Scheme, and that marketing fees were paid to Coral Reef and NAPC;

(f) knew that the purchase price being paid by the Gleesons was not the fair market value of Unit 29;

(g) knew that the Gleesons had not been informed by any other marketing participant of the commissions and marketing fees to be paid to Coral Reef, NAPC or the other marketing participants;

(h) knew that the Gleesons had not been informed by any other marketing participant that the purchase price was not the fair market value for Unit 29;

(i) knew that an earlier client of his had signed a contract to purchase Unit 29, but was released from the contract and had the deposit of $1,000 refunded upon claiming that NAPC had colluded with Investlend in relation to the purchase;

(j) did not advise the Gleesons of any of the matters within his knowledge set out in subparagraphs (b) to (i) hereof;

(k) knew that if he informed the Gleesons of the nature or extent of the marketing fee for Unit 29 he would no longer get referrals from NAPC or Investlend;

(l) was a marketing participant’.

In par 78 the following contravention is pleaded:

‘78. Pointon, by failing to disclose to the Gleesons any of the matters pleaded in paragraphs 37(b)-(i), by reason of the matters pleaded in paragraphs 16 to 20 and 37:

…

(b) was knowingly concerned in or party to the contravention by Coral Reef, NAPC and Investlend of the provisions alleged in paragraph 76;…’

(Paragraph 76 refers back to par (20(c)).

54 Allegations that he also contravened s 38 of the Queensland Act by reason of non-disclosures to the Gleesons and that he was a conspirator are not pursued. In relation to the specific misrepresentations alleged to have been made to the Gleesons he is sought to be made liable as an accessory for that relating to the purchase price being the market value of the unit.

Against Mr Johanson

55 It is not controversial that Mr Johanson acted as Redwind’s solicitor both in relation to the marketing agreement with Coral Reef, and associated agreements, and with respect to the conveyance to the Gleesons. He and his firm are also alleged to have been on the panel. Mr Johanson is alleged to have known of the scheme and the part played by the other respondents in it.

56 It is sought to make him liable as an accessory to the conduct of the scheme and the consequential breach of s 52, for its application to the Gleesons and the non-disclosures to purchasers generally of the matters in par 20(c). It is sought to hold him liable personally for the non-disclosures to purchasers generally under s 38 of the Queensland Act. So far as concerns the misrepresentations alleged to have been made to the Gleesons, he is alleged to have been an accessory to that concerning the unit being sold at market value.

57 Additionally it is alleged against him that:

‘38. Between about 24 September 1998 and 21 December 1998 Johanson:

(a) acted as attorney and assolicitor for Redwind in relation to its sale of Unit 29 to the Gleesons;

(b) knew how the NAPC Scheme worked:

(c) knew that the purchase price for Unit 29 paid by the Gleesons included a marketing fee of $34,900;

(d) knew that Unit 29 was being marketed to the Gleesons pursuant to the NAPC Scheme;

(e) knew that commissions were paid to marketing participants in the NAPC Scheme, and that marketing fees were paid to Coral Reef and NAPC;

(f) knew that the purchase price being paid by the Gleesons was not the fair market value of Unit 29;

(g) knew that the Gleesons had not been informed by any other marketing participant of the commissions and marketing fees to be paid to Coral Reef, NAPC or the other marketing participants;

(h) knew that the Gleesons had not been informed by any other marketing participant that the purchase price was not the fair market value for Unit 29;

(i) knew that NAPC and Coral Reef were marketers;

(j) knew of the terms of the contract between Redwind and Coral Reef to market the Chevron Units;

(k) knew that a fee of $34,900 was paid to Coral Reef from the sale proceeds of Unit 29;

(l) knew that he and his firm had previously acted for purchasers of property marketed pursuant to the NAPC Scheme, which they knew to be marketed property and had failed to disclose that fact, or the nature or the extent of the marketing fees involved, to their clients;

(m) knew that a previous purchaser of Unit 29 had claimed that Redwind had colluded with NAPC and Investlend in relation to the purchase of Unit 29 and that Redwind had subsequently agreed to release that purchaser from its contract and had repaid the deposit;

(n) was a marketing participant;

(o) did not disclose the nature, existence or extent of the marketing fee to the Gleesons’.

58 The contravention constituted by this knowledge and the failure to disclose the marketing fee is not pleaded. The Commission disavowed reliance upon s 38, in par 77 (referred to at [37] above) which related to some disclosures to the Gleesons and in any event that plea did not ever refer to Mr Johanson. I therefore take it to be part of the narrative relevant to the non-disclosures to purchasers generally.

Against The Bank

59 Paragraph 46 of the amended statement of claim is in these terms:

‘46. The CBA:

(a) knew that the purchase price of Unit 29 was $164,900;

(b) knew that the fair market value of Unit 29 was approximately $100,000;

(c) knew that the purchase price of Unit 29:

(i) was substantially in excess of its fair market value;

(ii) included selling costs that were well in excess of standard Real Estate Institute of Queensland rates; and

(iii) was an inflated purchase price that could not be recouped upon further resale;

(d) knew that the Gleesons resided and carried on business in Cairns;

(e) knew that the fair market value of Unit 29 was not sufficient of itself to support a loan in the amount applied for by the Gleesons;

(f) knew that, if the Gleesons proceeded to make the proposed loan agreements, the benefits to the CBA included:

(i) receipt of loan fees;

(ii) receipt of interest on the sum borrowed over the term of the loan; and

(iii) the opportunity to sell additional services and products, such as insurances, to the Gleesons over the term of the loan;

(g) knew that, notwithstanding that the Gleesons had sought loans very substantially in excess of the fair market value of Unit 29, the total value of the security offered by the Gleesons was ample for the loans sought and that the benefit to the CBA would be greater if the loans sought were provided than if only loans sufficient to purchase Unit 29 at its fair market value were provided;

(h) knew, or had reason to believe, that the Gleesons believed the fair market value of Unit 29 to be approximately $164,900;

(i) knew that the Gleesons were unaware that the fair market value of Unit 29 was approximately $100,000;

(j) knew or had reason to believe that the Gleesons were unaware that the purchase price of Unit 29:

(i) was substantially in excess of its fair market value;

(ii) included selling costs that were well in excess of standard Real Estate Institute of Queensland rate; and

(iii) was an inflated purchase price that could not be recouped upon further resale;

(k) knew or had reason to believe that the Gleesons had been misled, by persons using investment seminar marketing techniques, as to the fair market value of Unit 29;

(l) knew, or had reason to believe, that the Gleesons, as its customers, would rely on the CBA to tell them if it knew of allegations or evidence of any misleading conduct by third parties in relation to their purchase of Unit 29;

(m) knew that, if the Gleesons had been aware of any of the matters pleaded in subparagraphs (b), (c) or (k) they would not have:

(i) proceeded with the purchase of Unit 29; or

(ii) proceeded with their finance application or entered into the loan agreements;

(n) did not disclose the contents of the valuation to the Gleesons;

(o) did not advise the Gleesons of the substance of the matters referred to in paragraph 45 hereof;

(p) did not take any step to alert the Gleesons to the facts set out in subparagraphs (b), (c) or (k)’.

It is then alleged that that conduct, in the context of the Gleesons’ application for finance, amounts to a contravention of s 52. Alternatively, it is alleged that the bank has engaged in conduct which is unconscionable, contrary to s 51AC(1)(a) or alternatively s 51AA.

the evidence

THE MARKETING AND SALE OF UNITS BY NAPC & Investlend

60 The use of a system of marketing involving many of the steps pleaded by the Commission as the NAPC scheme was admitted by Mr Bilborough, although he referred to it as ‘the Coral Reef system’. It is also clear from the evidence of the Gleesons, and from the evidence of other purchasers of NAPC-marketed properties called by the Commission, that the steps were generally those outlined by the Commission. I did not understand the respondents to dispute this. Transcripts of the evidence given by Mr Bilborough, Mr Quinlivan and Mr Pointon pursuant to under s 155 of the Act, particularly that relating to Mr Bilborough, also confirm aspects of the scheme. The Commission’s evidence includes records of some sixty meetings between 4 July 1996 and 1 December 1998 at which one or both of Mr Bilborough and Mr Quinlivan were usually present. They extend to some hundreds of pages. There are some references amongst them which are relevant to confirm the operation of the scheme and how it was managed by NAPC and Investlend and which provide some detail of aspects of it which assume some importance in these proceedings. The scripts used by NAPC representatives for the seminar and the in-home consultation fall into the latter category.

61 Neither Mr Bilborough nor Mr Quinlivan gave evidence at the trial. In his s 155 examination Mr Bilborough explained that the system of marketing commenced in about 1994 or 1995 and that about 1,000 properties were sold by NAPC in its best year. It was a large operation with about 300 people engaged in it at its height.