FEDERAL COURT OF AUSTRALIA

Australia China Business Bureau Pty Ltd v MCP Australia Pty Ltd

[2003] FCA 934

CONTRACT – whether a contract is established by a course of dealing between the parties – whether a breach of contract has been established – whether there is a relevant estoppel – unconscionable conduct – no question of principle

Sale of Goods Act 1923 (NSW) s 12(2), 13, 13(2)

Sale of Goods Act 1893 (UK) s 8

Trade Practices Act 1974 (Cth) s 51AA, 51AA(1), 51AB, 51AC, 51AC(10)

Allstate Life Insurance Company v Australia & New Zealand Banking Group Ltd (1995) 58 FCR 26 referred to

Austotel Pty Ltd v Franklins Self-Serve Pty Ltd (1989) 16 NSWLR 582 referred to

Australia & New Zealand Banking Group Ltd v Frost Holdings Pty Ltd [1989] VR 695 cited

Australian Broadcasting Corporation v XIVTH Commonwealth Games Ltd (1988) 18 NSWLR 540 applied

Australian Competition & Consumer Commission v CG Berbatis Holdings Pty Ltd (2003) 197 ALR 153 referred to

Australian Development Corp Pty Ltd v White Constructions Ltd (2001) 189 ALR 266 referred to

Australis Media Holdings Pty Ltd v Telstra Corporation Ltd (1998) 43 NSWLR 104 cited

Barrier Wharfs Ltd v W Scott Fell & Co Ltd (1908) 5 CLR 647 referred to

Booker Industries Pty Ltd v Wilson Parking (Qld) Pty Ltd (1982) 149 CLR 600 referred to

Brambles Holdings Ltd v Bathurst City Council (2001) 53 NSWLR 153 referred to

Branir Pty Ltd v Owston Nominees (No. 2) Pty Ltd (2001) 117 FCR 424 referred to

Brown v Gould [1972] 1 Ch 53 referred to

Burger King Corporation v Hungry Jack’s Pty Ltd [2001] NSWCA 187 referred to

Coal Cliff Collieries Pty Ltd v Sijehama Pty Ltd (1991) 24 NSWLR 1 distinguished

Commonwealth v Verwayen (1990) 170 CLR 394 cited

Fletcher Challenge Energy Ltd v Electricity Corporation of New Zealand Ltd [2002] 2 NZLR 433 considered

Giumelli v Giumelli (1999) 196 CLR 101 cited

Hall v Busst (1960) 104 CLR 206 cited

Kuwait Asia Bank EC v National Mutual Life Nominees Ltd [1991] 1 AC 187 referred to

LMI Australasia Pty Ltd v Baulderstone Hornibrook Pty Ltd [2001] NSWSC 886 applied

May & Butcher Ltd v The King [1934] 2 KB 17 referred to

Media Holdings Pty Ltd v Telstra Corporation Ltd (1998) 43 NSWLR 104 cited

O’Brien v Dawson (1942) 66 CLR 18 referred to

Overlook v Foxtel [2002] NSWSC 17 cited

Peters (WA) Ltd v Petersville Ltd (2001) 205 CLR 126 referred to

Said v Butt [1920] 3 KB 497 cited

Stocks & Holdings (Constructors) Pty Ltd v Arrowsmith (1964) 112 CLR 646 referred to

Telstra Corporation Ltd v Optus Network Pty Ltd (2000) 193 ALR 353 cited

Vroon BV v Foster’s Brewing Group Ltd [1994] 2 VR 32 cited

Waltons Stores (Interstate) Ltd v Maher (1988) 164 CLR 387 cited

Wenning v Robinson (1964) SR (NSW) 157 referred to

Cheshire & Fifoot’s Law of Contract (8th Australian Edition) [5.19]

The Laws of Australia (Law Book Company) Vol 8 [18]

Benjamin’s Sale of Goods (6th ed) 2-046

Sutton Sales and Consumer Law (4th ed) [6.4]

Carter & Harland Contract Law in Australia (4th ed) [2318]

AUSTRALIA CHINA BUSINESS BUREAU PTY LTD v MCP AUSTRALIA PTY LTD & ORS

N 1228 OF 2001

HELY J

5 SEPTEMBER 2003

SYDNEY

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| NEW SOUTH WALES DISTRICT REGISTRY | N 1228 OF 2001 |

| BETWEEN: | AUSTRALIA CHINA BUSINESS BUREAU FIRST APPLICANT

McKECHNIE INVESTMENTS SECOND APPLICANT

McKECHNIE PLC THIRD APPLICANT

|

| AND: | MCP AUSTRALIA PTY LTD FIRST RESPONDENT

WINDOWARE AUSTRALIA PTY LTD THIRD RESPONDENT

SULLIVANS INTERNATIONAL PTY LTD FOURTH RESPONDENT

M T SULLIVAN & CO PTY LTD SIXTH RESPONDENT

MICHAEL SULLIVAN SEVENTH RESPONDENT

|

| BETWEEN: | SULLIVANS INTERNATIONAL PTY LIMITED CROSS CLAIMANT

|

| AND: | McKECHNIE INVESTMENTS BV FIRST CROSS RESPONDENT

McKECHNIE PLC SECOND CROSS RESPONDENT |

| HELY J | |

| DATE OF ORDER: | 5 SEPTEMBER 2003 |

| WHERE MADE: | SYDNEY |

THE COURT ORDERS THAT:

1. The application is dismissed.

2. The cross claim is dismissed.

3. The matter be relisted for agreement or argument on the question of costs.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| NEW SOUTH WALES DISTRICT REGISTRY | N 1228 OF 2001 |

| BETWEEN: | AUSTRALIA CHINA BUSINESS BUREAU FIRST APPLICANT

McKECHNIE INVESTMENTS SECOND APPLICANT

McKECHNIE PLC THIRD APPLICANT

|

| AND: | MCP AUSTRALIA PTY LTD FIRST RESPONDENT

WINDOWARE AUSTRALIA PTY LTD THIRD RESPONDENT

SULLIVANS INTERNATIONAL PTY LTD FOURTH RESPONDENT

M T SULLIVAN & CO PTY LTD SIXTH RESPONDENT

MICHAEL SULLIVAN SEVENTH RESPONDENT

|

| BETWEEN: | SULLIVANS INTERNATIONAL PTY LIMITED CROSS CLAIMANT |

| AND: | McKECHNIE INVESTMENTS BV FIRST CROSS RESPONDENT

McKECHNIE PLC SECOND CROSS RESPONDENT

|

| JUDGE: | |

| DATE: | 5 SEPTEMBER 2003 |

| PLACE: | SYDNEY |

REASONS FOR JUDGMENT

1 The principal issue in this case is whether as a result of conversations, conduct and documents in the period between about 22 July 1998 and 20 May 1999 a valid and binding agreement came into existence between Australia China Business Bureau Pty Ltd, (‘ACBB’) and the first respondent (‘MCP’), under which MCP would procure from ACBB exclusively its requirements in Australia and New Zealand for products falling within nine product categories for a term of five years with an option for a further five years. Alternatively, ACBB asserts that MCP is estopped from denying the existence of that agreement. In the further alternative, ACBB asserts that various of the respondents have engaged in unconscionable conduct in equity, or in breach of s 51AB and 51AC of the Trade Practices Act 1974 (Cth) (‘the Act’).

2 ACBB’s business at the relevant times was described in evidence as the provision of unique customised solutions to clients that need to outsource the design, manufacture and/or packaging of specialised products in order to be competitive in the Australian and Pacific markets. ACBB specialised in ‘off-shore’ manufacturing, with its core focus on the People’s Republic of China.

3 MCP was the largest supplier of window treatments and curtain hardware products in Australia. It was a wholly owned subsidiary of McKechnie Investments BV. McKechnie PLC was the ultimate holding company of MCP. It is not necessary for the purpose of resolving the issues in this case to distinguish between these two companies, and each is referred to hereafter as ‘McKechnie’. On 30 June 2000 McKechnie sold its share in MCP to Sullivans International Pty Ltd, the fourth respondent, a company controlled by Mr Michael Sullivan, the seventh respondent.

4 ACBB asserts that in July 2000 Mr Sullivan instructed MCP to look for alternative suppliers for products and on or about 15 August 2000 MCP purported to repudiate the contract. From about July 2000 until ACBB terminated the contract on 15 March 2001 MCP wrongly refused to procure from ACBB exclusively the products the subject of the alleged agreement.

5 ACBB sues Mr Sullivan, Sullivans International Pty Ltd and the sixth respondent, M T Sullivan & Co Pty Ltd for damages for inducing MCP to breach its contract with ACBB. Except where it is necessary to distinguish between these entities, all are referred to hereafter as ‘Sullivans’.

The people involved

6 The directors of ACBB at the relevant time were Mr Peter Epov and Mr Chuan-Qiang Dong. Mr Epov was also a shareholder in ACBB and the person principally involved in the negotiation of the alleged agreement on behalf of ACBB. Mr Epov was a witness in the proceedings.

7 At the relevant time, Mr Kevan Adair was the Chief Executive Officer of MCP, and the person principally involved on behalf of MCP in the negotiations with Mr Epov. Mr Adair resigned from MCP on 1 September 2000. Mr Tas Sinadinos was the general manager of operations and logistics at MCP until he left MCP in about March 1999. Mr Garry Chenery was the former development manager for logistics at MCP until he took over from Mr Sinadinos as general manager of operations and logistics in about March 1999. He resigned from MCP in about August 2000. Mr Leigh Barker was the former general manager of finance and administration at MCP until he left MCP in or about February 1999. Mr Leigh Roden was the former materials manager for MCP. The evidence does not disclose when he left MCP but he is currently an independent consultant. All of these former officers of MCP gave evidence on behalf of ACBB.

8 Mr Jeffrey McEwen was the general manager, marketing of MCP until 30 November 2000, and since 1 December 2000 has been the general manager of MCP. Mr Nigel Burson is the general manager of MCP New Zealand Ltd which, since 30 June 2000, has been controlled by the fourth respondent. Mr McEwen and Mr Burson gave evidence on behalf of MCP. So too did Mr Michael Sullivan and Mr Gregory Wanchap, a partner of the firm Hall Chadwick, Chartered Accountants and Business Advisers, which was engaged by M T Sullivan & Co Pty Ltd, the sixth respondent, to undertake a due diligence on the proposed purchase of the share in MCP.

Background

9 As the contract is said to have resulted from conversations, conduct and documents over a period of some ten months, a detailed consideration of the factual matrix is required. I have marked with an asterisk (*) in the following paragraphs of these reasons the conversations and documents relied upon in the particulars to [16] of the Further Amended Statement of Claim (‘FASC’) as evidencing the contract.

10 Prior to its dealings with ACBB, MCP purchased products from more than thirty suppliers and in addition to this, employed its own manufacturing processes. After purchase, the products were then packaged into an existing style of packaging in Australia which, in the view of Mr Adair, was inefficient, costly and lacked any coherent quality control or quality assurance management. Mr Adair was appointed Chief Executive Officer of MCP on 26 February 1998.

11 It was Mr Adair’s view that MCP’s procurement strategy needed to be significantly modified in the following major areas:

(a) reduce the then existing suppliers to MCP from thirty to four or five major strategic supply partners, with proven areas of expertise;

(b) enter into strategic alliances with the reduced suppliers which would offer joint benefits from economies of scale and enable a drastic restructure of the Australian operation;

(c) base the strategic alliances on quality control, long term exclusivity between suppliers and MCP and volume related price breaks which would result in a reduced product cost base, reduced fixed costs environment and a more coherent procurement strategy.

12 In March/April 1998 Mr Adair was informed of discussions which had been taking place with Mr Epov since April 1997 about a proposal which, if it came to fruition, would see most of MCP’s products manufactured in China and supplied to MCP by ACBB.

13 In April 1997 Mr Epov had been approached by MCP’s consultant, Gerry Nelson, to see whether ACBB could assist MCP to rationalise its business by having ACBB manufacture and import a significant proportion of their products directly from China. Between April 1997 and July 1998 Mr Epov had a number of meetings with Mr Nelson and later with Mr Sinadinos and Mr Roden to discuss the possible sourcing from China of MCP’s product requirements. Matters which were discussed included the following:

- ACBB would need to better target prices which MCP would provide to it if ACBB was to secure MCP’s business;

- significant costs could be incurred by ACBB in connection with the set up, tooling and material purchasing which would need to be fully covered; and

- ACBB would need a minimum of three years exclusive supply to cover its set up costs and to make the project a worthwhile one.

14 On 22 July 1998 a meeting took place between Mr Epov, Mr Dong, Mr Adair, Mr Sinadinos and Mr Roden. At this meeting Mr Epov was introduced, for the first time, to Mr Adair. ACBB presented its proposal to MCP which involved the following main points:

- ACBB was willing and able to provide significant reductions in pricing available for MCP in respect of nominated products by ACBB directly identifying and dealing with product manufacturers in China;

- to make savings on the prices to be charged to MCP, there needed to be available manufacturing efficiencies with substantial bulk forward orders placed, as distinct from monthly orders in lesser quantities;

- it would be necessary for ACBB to pay up front deposits to the various Chinese factories of not less than 25 per cent of the value of its order, together with guarantees to the supplier for timely payment;

- ACBB would be required to have made an investment in the preparation of industrial design drawings, samples, and in tooling to be provided to the factories in the order of $US500,000;

- ACBB would establish its own exclusive supply system specifically for MCP so that MCP’s competitors could not obtain the same benefits as would accrue to MCP under the terms of the proposal. ACBB would not purchase product from any of MCP’s current product suppliers. It would be a totally ‘green field’ operation. ACBB would establish its own exclusive supply agreements with companies which currently do not manufacture or supply any of the products in the MCP range for either the Australian or New Zealand markets; and

- ACBB and MCP would have a long term supply contract in place and a guarantee from MCP of volume.

15 The matter was left on the basis that the parties would work together to develop an exclusive long term supply agreement. It is clear that the parties had in mind from the outset that ACBB would supply MCP with the nominated products to the exclusion of MCP’s competitors. For example, the minutes of this meeting [PE 16] contain the following:

‘KA – questioned if ACBB is supplying any competitors in Australia or New Zealand or if any of the factories are supplying Australia/New Zealand.

PE – no, on both accounts.

KA – asked that this remain the case.

PE – no problem as long as there was significant and ongoing volume for Australia and New Zealand.’

It is less clear whether the parties also had in mind at this stage of their discussions whether MCP would be obliged to source all or some part of its product requirements exclusively from ACBB, or whether there would be a commitment on the part of MCP to purchase minimum annual quantities from ACBB or, perhaps, some other arrangement.

16 After this meeting, Mr Adair appointed a project management team to evaluate the ACBB proposal. Between 22 July 1998 and 31 August 1998 regular weekly meetings were held between MCP and ACBB personnel to ensure that the project of transferring procurement to ACBB was given top priority. The minutes of a weekly communications meeting dated 10 August 1998 [KA 3] record that Mr Adair was responsible for drafting the ‘exclusivity deal’ with ACBB.

17 In August 1998, at one of the weekly meetings, Mr Sinadinos provided Mr Epov with a schedule of products which MCP wanted to source from China [PE 17]. The schedule was divided into three groups. MCP asked ACBB to cost each individual item in the document within each project, and to give MCP a price that either matched or bettered the target price which MCP would include on a project spreadsheet that MCP would provide to ACBB progressively over the next couple of months. Exhibit PE 18 is an example of such a spreadsheet. Mr Sinadinos told Mr Epov that as ACBB matched or bettered the target price of any project, MCP would transfer to ACBB the business of supplying that product to MCP.

The Heads of Agreement

18 A meeting was scheduled to be held on 20 August 1998 between representatives of ACBB and MCP. The agenda for that meeting shows as the first item of business ‘Exclusivity Deal’. A handwritten annotation was made by Mr Epov on his copy of that agenda [PE 19] as follows:

‘MCP wants exclusive supply deal – must be for us to make this investment.’

19 It is unclear whether the meeting scheduled to be held on 20 August 1998 was in fact held, or if it was held, what happened. A meeting was, however, held on 31 August 1998* between Messrs Epov, Dong, Adair, Sinadinos and Roden at which Mr Adair handed to Mr Epov a copy of a draft of the heads of agreement. That draft is Exhibit PE 20. It is headed ‘Confidentiality/Exclusivity’. Clause (ii) provides as follows:

‘(ii) ACBB agrees to operate exclusively for MCP(A) and MCP(NZ), in the procurement of products in the window treatment area, and will not procure products or services to manufacturers, distributors or retailers of window treatment products in the territories of Australia and New Zealand.’

The draft does not include any other provision in relation to exclusivity.

20 At this meeting it is common ground between Mr Epov and Mr Adair that Mr Adair told Mr Epov that he had discussed ACBB with Mr Hanratty, the Executive Director of McKechnie, who had instructed Mr Adair to sign ACBB up to a long term exclusive supply agreement. It is also common ground that Mr Epov said words to the following effect:

‘ACBB also want a long term exclusive supply agreement otherwise it is not worth pursuing this business with MCP. Exclusivity is the only way we can recoup our investment in this project.’

21 Both Mr Epov and Mr Adair agree that during this meeting there was a consensus that what was in contemplation was mutual exclusivity. Mr Sinadinos’ evidence is to the like effect. So too is the evidence of Mr Roden. In his affidavit, Mr Adair expressed it this way:

‘You will exclusively supply MCP in our markets and in return MCP will exclusively buy from ACBB all the products that we are jointly satisfied that ACBB can handle. There will be mutual exclusivity.’

Although not all the witnesses described mutual exclusivity in terms of ‘all the products that we are jointly satisfied that ACBB can handle’, it seems to me that Mr Adair’s version accords with the probabilities, particularly having regard to subsequent developments. Mr Adair confirmed in cross-examination that the quoted reference was to the process that later became embodied in the process flow chart, which is referred to hereunder.

22 The minutes of the meeting of 31 August 1998 [PE 20A] record the following:

‘Heads of Agreement

KA outlined exclusivity agreement (Heads of Agreement) briefly, stressing the need for a long term strategic alliance. He stressed the need for mutual exclusivity. PE agreed in principle to the agreement and said he would need a couple of days to look through the agreement before signing.’

The minutes also note that Mr Adair was keen to get the Heads of Agreement signed, and then would make prices and quantities readily available to ACBB.

23 On 15 September 1998 [R 1/465] Mr Adair forwarded to Mr Hanratty the draft of the Heads of Agreement which was presented at the meeting held on 31 August 1998. He indicated that the meeting was to be held on the following day to finalise the agreement, and to make any amendments to the agreement.

24 On 16 September 1998 Mr Epov provided Mr Adair with his written comments on the draft of the Heads of Agreement which had been presented to him on 31 August 1998. ACBB’s lawyer had some input into the suggestions which were made. The redrafted Heads of Agreement incorporating the suggested amendments was enclosed with that letter. As with the earlier draft, par (i) provided that ACBB and MCP agreed to work towards a supply agreement to cover the territories of Australia and New Zealand. Clause (ii) provided as follows:

‘ACBB will agrees in that supply agreement to operate exclusively for MCP(A) and MCP (NZ), in the procurement of products in the window treatments area, and will not procure products or services for manufacturers, distributors or retailers of window treatment products in the territories of Australia and New Zealand for a period of five years.’

Other alterations were suggested to the initial draft, including a new provision that the supply agreement which was to be negotiated, would expire five years from its date of commencement, and would be able to be terminated earlier by ACBB or MCP giving 30 days written notice.

25 The document styled Heads of Agreement* was signed by Mr Adair and Mr Epov on 16 September 1998. The agreement as signed differed in some respects from the form submitted under cover of the letter of 16 September 1998. Clause (ii) of the Heads of Agreement, as executed, provided as follows:

‘(ii) ACBB will agrees in that supply agreement to operate exclusively for MCP(A) and MCP(NZ), in the procurement of products in the window treatments area, and will not procure products or services for manufacturers, distributors or retailers of window treatment products in the territories of Australia and New Zealand for a period of 5 years + option for further renewal of 5 years.’

Clause (viii) provided that the supply agreement will expire five years from the date of commencement and will be able to be terminated earlier by ACBB or MCP giving six months written notice. The only provision in the Heads of Agreement which related to exclusivity of supply was cl (ii) quoted above.

26 Only Mr Sinadinos deposes to a conversation between Mr Epov and Mr Adair on the occasion of the signing of the Heads of Agreement. In [25] of his affidavit of 20 December 2002, Mr Sinadinos said:

‘25. At this meeting I recall a conversation which included words to the following effect:

Peter Epov: ACBB needs long term commitment and exclusivity in order to make this deal worthwhile.

Kevan Adair: We are after the same things. Derry Hanratty wants me to quickly sign up ACBB to a long term exclusive supply agreement. The deal is sound it will benefit both MCP and ACBB, we want mutual exclusivity and we also want a long term commitment. We understand that ACBB requires a long term commitment because of the high upfront investment that you will incur. The Heads of Agreement allow the process to start. Later we will enter into a legally binding Trading Agreement.’

This conversation is not included in the conversations particularised in [16] of the FASC as being one of the contractual conversations.

27 ACBB relies on the conversations which occurred at the meeting of 31 August 1998 and on the Heads of Agreement executed on 16 September 1998 as one of the sources of the pleaded contract. However, it is common ground between Mr Epov and Mr Adair that at the meeting of 31 August, Mr Adair said, and Mr Epov accepted, that the Heads of Agreement was intended as an interim document aimed at covering confidentiality and exclusivity until the Trading Agreement was signed. Both parties envisaged that the Trading Agreement, when settled, would replace the Heads of Agreement, which would not have any continuing application after that time.

28 Mr Epov agreed in cross-examination that there is no term in the Heads of Agreement providing that MCP will acquire exclusively from ACBB. In his understanding the effect of clause (ii) was that ACBB promised to act exclusively for MCP in the territory in the area of ‘Windoware’ products. Notwithstanding that evidence, counsel for ACBB, Mr Garnsey QC, submitted that the first two lines of clause (ii) should be construed as meaning that ACBB was to be the sole supplier for MCP(A) and MCP(NZ), otherwise the rest of the clause is redundant and unnecessary. I do not agree with this submission. The first two lines impose an obligation on ACBB rather than upon MCP, and the balance of the clause expands upon the content of that obligation. In my view, Mr Epov was correct in his understanding of clause (ii). He was also correct in his understanding that the Heads of Agreement did not contain any provision to the effect that MCP would acquire products exclusively from ACBB.

29 On 21 September 1998 Mr Adair provided a copy of the Heads of Agreement as executed to Mr Hanratty at McKechnie. He described the agreement as covering ‘tenure’, presumably as reference to the five year term of the agreement.

The project timetable

30 In October 1998 Mr Roden prepared, on the instructions of Mr Sinadinos, a document styled ‘MCP /ACBB Project Timetable’ [PE 22]*. The timetable was handed by Mr Adair to Mr Epov on about 13 October 1998*, and was described by Mr Adair as a timetable for handing over of products to ACBB.

31 The project timetable refers to three groups of projects, described as groups 1, 2 and 3, and in the case of group 1, to projects within that group. The document describes the process expected to be followed leading up to the placement of an order by MCP for the supply of goods. The first step in the process (‘P’) is the preparation by MCP for quotation. That step had apparently been completed by MCP for the projects within group 1 at the time of the preparation of this document, although not in relation to group 2 or group 3. The second step is quotation (‘Q’) by ACBB. That step involved ACBB quoting the price at which it would supply particular goods, and was scheduled to occur in relation to projects within group 1 between 6 November 1998 and 27 November 1998. The third step is described as sample (‘S’) indicating that ACBB was to provide a sample of the particular products to MCP for its consideration. A sample was to be provided in relation to some only of the projects included in group 1, and the expected date for provision of the sample in relation to those projects was indicated on the document. The fourth step in the process is review (‘R’) indicating that the sample would be reviewed either by MCP or MCP in conjunction with ACBB. The final step in the process is described as to discuss/decision (‘D’), referring to the expected date on which MCP would decide whether or not to order the goods on ACBB’s quotation. Mr Sinadinos accepted in evidence that MCP’s decision whether to order based on the quotation given or the sample supplied might be ‘yes’ or ‘no’. The last of the decisions to be made in relation to the projects falling within group 1 was scheduled to occur in the week ending 22 January 1999.

32 The significance of this document is that it describes a process of negotiation expected to result in a decision being made by MCP whether or not to place orders for particular types of goods falling within the groups described as group 1, group 2 and group 3.

A visit to China

33 On 19 October 1998* Messrs Dong, Epov, Adair and Roden visited China to inspect a number of factories which ACBB had selected to manufacture products intended to be supplied to MCP by ACBB. One of the major manufacturers/suppliers selected by ACBB in China was Jing Tai. It is common ground between Mr Epov and Mr Adair that on this visit Mr Adair suggested that ACBB should establish a centralised packing centre in Shanghai which ACBB would control. Mr Epov said that this would involve a significant additional expense but he would investigate the possibility. Mr Adair said that if ACBB agreed to centralise the packaging and quality control, he would facilitate the transfer of as much of MCP’s packaged product to ACBB as is feasible and MCP would give ACBB all of its obsolete packaging for rework. Again, there is a slight difference between Mr Epov’s account of this aspect of the conversation and Mr Adair’s. No one submitted that the difference was material. The version which I have recounted is that of Mr Adair as it is more in accordance with the probabilities.

34 On Mr Epov’s return to Sydney he authorised the establishment of a centralised packing centre in Shanghai and informed Mr Adair of the decision which had been taken. During the course of that conversation reference was made to the additional costs involved in connection with the establishment of the centralised packaging centre in Shanghai, and it is common ground between Mr Epov and Mr Adair that Mr Adair proffered an assurance that MCP would guarantee the volumes of purchases shown on the pricing schedules. Mr Epov told Mr Adair that ACBB expected MCP to adhere strictly to the minimum annual volumes for at least five years. All of ACBB’s costings would be structured around a long term supply agreement with minimum annual volumes.

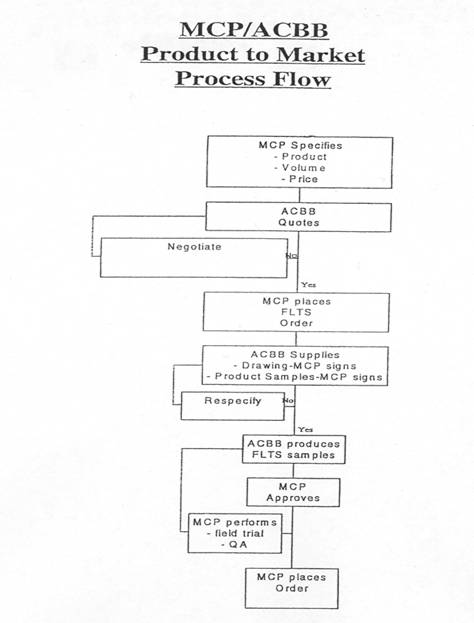

The process flow chart

35 In about November 1998 Mr Sinadinos provided Mr Epov with a document styled ‘MCP/ACBB Product to Market Process Flow’ [PE 22A]*. That document is reproduced hereunder:

36 Mr Sinadinos recalls that when the flow chart was provided to Mr Epov in about November 1998, a conversation* occurred to the following effect:

‘I said: “This is the MCP flow to market, it is mandatory for ACBB to follow and comply with the process. This means that we will get all of our products exclusively from you provided that you follow this process. However, if you stuff up you will have to compensate us for any loss that we suffer.”

Peter Epov: “We are happy with this process.”’

Mr Sinadinos accepted that the reference to ‘stuff up’ was a reference to any failure on the part of ACBB downstream of the placement of an order. Mr Adair’s evidence was that the process flow chart continued to be a central part of the relationship between ACBB and MCP up to, including, and past the time when the trading agreement was signed.

37 If the process shown on the flow chart is followed, it will not necessarily result in MCP placing an order. There are points in the process flow at which decisions are required to be made by MCP. That is obvious on the face of the flow chart, and was confirmed by the evidence of Mr Sinadinos and Mr Roden. MCP might not accept ACBB’s quote and the negotiation for which the process flow chart provides might be unsuccessful. MCP might not approve samples which ACBB produces. The point which the witnesses made was that agreement was always able to be reached in relation to these matters with respect to the products which were exposed to the process flow chart. Thus, for example, Mr Epov’s evidence in cross-examination at T p 82 was as follows:

‘… but was it your real understanding of the arrangement between the parties that MCP under the arrangements then applying would be obliged to purchase from ACBB no matter what the price was, no matter what the state of the sample was? --- No. Well, the commercial logic would dictate if a price is too high, they would not have bought from us or if the sample was not satisfactory, we would have modified the sample, retooled it and brought it back. In reality all of our prices were well below what they have – they originally targeted or what they wanted. The samples were in reality better than anything they ever had and, you know, we produce the best product on the market.

Assuming all that to be so, you acknowledge do you though that one of the possible outcomes of the process would be that MCP would decide not to buy from you? --- Yes, it’s possible that they may have made a decision not to buy from us but it didn’t happen that way.’

38 Neither the flow chart, nor any similar document was used by MCP in relation to its dealings with other suppliers.

39 A management meeting of MCP was held on 11 November 1998. At this meeting it was resolved that Mr Adair and Mr Sinadinos were to report to McKechnie by the end of the month on the evaluation of ACBB’s supply capabilities, expectations and objectives [KA 6].

The initial bulk order

40 On or about 13 November 1998 agreement was reached between ACBB and MCP to proceed with the following product groups in [PE 17]:

(a) hooks and rings (pre-packs only), being certain products falling within ‘project 1’;

(b) stayed and unstayed brackets, being certain products falling within ‘project 6’;

(c) PC rod plastic components, being certain products falling within ‘project 6’;

(d) gold rod, being certain products falling within ‘project 7’; and

(e) PC rod plastic components (gold), being certain products falling within ‘project 7’.

(McEwen [32])

41 On or about 18 November 1998 MCP placed its initial bulk purchase order* with ACBB [PE 27]. The order related to the products referred to above plus Door Stops being ‘project 26’. Apparently quotes had been received from ACBB for some only of the products the subject of the order as at least one page of the attachments to the order contains a notation that only two of the items had been quoted, and quotes for all other items are required. The order itself provides:

‘This order is for the manufacturing of appropriate tooling and dyes to produce in bulk only, the products outlined. Note that the MCP/ACBB product to market process flow chart and initial supply and delivery agreement must be followed at all times.’

42 A document styled ‘ACBB/Windoware initial supply and delivery agreement’ had been sent to ACBB but the letter enclosing the initial bulk order advised that it was not necessary for that agreement to be signed that day. In fact, it was signed by Mr Epov on behalf of ACBB on 18 November 1998. It was not signed by Mr Adair. Subsequently, Mr Epov was advised by MCP that the document was no longer relevant. The front page of that agreement provided as follows:

‘This agreement details the following subjects and assigns responsibility between MCP and ACBB to enable the framework for new supply lines to be established ex ROC. This agreement is part of the trading terms and conditions for supply.

Initial purchase order – first lot to stock (FLTS)

Manufacturing start-up

Packaging start-up

Packaging and labelling specification

Product storage and delivery

Product traceability

QA/QC issues

Planning and inventory management’

There is nothing in this document in relation to minimum volumes or exclusivity of supply.

43 Mr Epov found that the initial bulk order represented less than 30 per cent of the MCP annual volume for that product as projected by MCP during the period July to October 1998.

44 On 20 November 1998 Mr Epov, Mr Sinadinos, Mr Roden and Mr Haines met. At that meeting Mr Sinadinos said that the initial bulk order is far too small and uneconomical to run. To achieve the savings quoted, ACBB must have a minimum 50 per cent to 60 per cent of the annual volume. Mr Sinadinos said that the order was not representative of future orders. MCP will review the bulk order and increase it. At that meeting Mr Sinadinos also tabled a document styled ‘MCP/ACBB Trading Agreement’, and draft key elements were discussed. The document took the form of an index to Part A (Terms and Conditions) and Part B (Operational Requirements) of the proposed agreement.

45 On 26 November 1998 MCP placed a revised bulk order* with ACBB. The revised order included orders for increased quantities of the products the subject of the original order and included an order for hooks and rings (metal components) ‘project 1’ [PE 29]. The purchase order states that the ‘MCP/ACBB Product to Market Process Flow Chart … must be followed at all times’.

46 On 30 November 1998 MCP submitted an initial PC rod order being some products within group 1 ‘project 6’. This purchase order also included the statement in relation to the Flow Chart quoted above.

47 Initially orders were placed by MCP for 54 different products which in turn were to be packaged by reference to three or four different brands. This meant that there were about 198 different packaged items the subject of the initial order.

48 Although ACBB continued to provide quotes on other products, MCP did not place orders with ACBB for any products other than those products falling within the range of the initial orders placed on 18, 26 and 30 November 1998. Once orders were placed with ACBB by MCP with regard to any product category as a result of the flow chart procedure, MCP did not order that same product category from any other supplier. MCP continued to reorder those product categories from ACBB.

The presentation

49 As a result of the resolution passed at a management committee meeting on 11 November 1998 Mr Sinadinos prepared a report styled ‘ACBB Project’ [KA 7]* which was presented to Mr Hanratty and other MCP personnel on 9 December 1998. Among those present at the presentation were Mr Adair, Mr Barker, Mr McEwen, Mr Sinadinos and Mr Chenery. No one from ACBB was present on this occasion.

50 The introduction to the presentation records that ACBB was introduced to MCP in late 1997 as a potential future supply partner. The introduction also records that MCP seeks to develop a partnership with ACBB as a means to eliminating the multitude of middle-men currently standing in the traditional overseas supplier base. MCP will work with ACBB on a long term partnership arrangement as a vehicle to achieve its strategic purchasing goals. The first of the project goals was as follows:

‘Establish an exclusive and confidential supplier partnership with ACBB.’

51 Section 1 of the presentation includes the following:

‘The plan is to specify 14.6M (67% of total FY99 COGS) business for ACBB to quote for supply ex PRC. Based on the FY99 budget the financial analysis shows the ACBB contribution to MCP to be in the order of 3.1M p.a. (assuming all this business goes to ACBB).’

In other parts of the presentation it is assumed that 14.6M business would be transferred to ACBB. Other benefits include the potential to take out 100 ex suppliers as well as ‘exclusivity/confidentiality – competitive edge’.

52 Section 2 of the presentation deals with procedures. It is as follows:

‘To manage the task of specifying > 2500 (SKU’s) products for quotation and resourcing, all targeted products are categorised into groups 1, 2, 3. Product and packaging specifications are being laid down for each product. An agreed procedure with ACBB is documented for bringing products to market.’

The categorisation into groups is a reference to [PE 17]. The documented procedure for bringing products to market is a reference to [PE 22A].

53 Section 5 of the presentation is headed ‘Exclusivity and Trading Agreement’. Under that heading the following appears:

‘A five year exclusivity and confidentiality heads of agreement has been signed between MCP and ACBB. A detailed trading agreement incorporating terms and conditions and operational requirements is currently being finalised with ACBB.’

A copy of the Heads of Agreement was attached to this section of the presentation as was a draft form of the Trading Agreement.

54 Mr Sinadinos recalls that when he presented the slide dealing with section 5 he said:

‘This agreement means that we would not use anyone else for the products supplied by ACBB and in return ACBB will not supply these products to anyone else.’

By ‘this agreement’ he was apparently referring to the Heads of Agreement although, as earlier indicated, there is no express term in that document which would oblige MCP not ‘to use anyone else’ for the products supplied by ACBB.

55 The form of Trading Agreement attached to this section of the presentation was drafted by Mr Sinadinos. It was divided into Part A (Terms and Conditions) and Part B (Operational Requirements) and its subject matter appears at least to some extent to follow the index presented at the meeting on 20 November 1998. The minutes of that meeting [PE 28] include as Item 14 the following:

‘Draft Trading Agreement Key Elements presented by TS for discussion – to be expanded and further presented (refer attached).’

The ‘attached’ is the document which I have described as an index. The Draft Trading Agreement attached to this section of the presentation appears to be the expansion contemplated by Item 14.

56 The Draft Trading Agreement contains provision for the attachment of an Appendix 1 described as ‘ACBB/MCP (Windoware) Exclusivity Agreement’ and for the attachment of an Appendix 2 ‘ACBB/MCP (Windoware) Agreed Procedure for the processing first lot to stock (FLTS) orders’. Appendix 2 appears to be a reference to the flow chart [PE 22A].

57 On 9 December 1998 a MCP management meeting was held at which various MCP executives were present. At this meeting Mr Hanratty said words to the following effect:

‘We are committed now to getting all of these products from ACBB so we don’t want to be stranded. So make sure you get ACBB to sign a trading agreement as soon as you can. I want to lock them in so that we are protected.’

December 1998 China visit

58 On 13 December 1998 Mr Epov met with Mr Roden in Shanghai. During the course of that week they carried out a great deal of work covering production and the refinement of packaging of supply to MCP. The work included inspection of tooling at various factories, product samples, clam shell packaging and selection of printers for labels.

A Draft Trading Agreement

59 On 7 January 1999 MCP submitted a draft of the proposed Windoware/ACBB Trading Agreement to Mr Epov for review and comment. This was the first draft of this document which had been provided to Mr Epov. It appears to be substantially the same as the form of Trading Agreement which was attached to the 9 December 1998 presentation. Many of the provisions in the draft appear to have been objected to by Mr Epov as the word ‘no’ appears in his handwriting next to many of the provisions in the draft [PE 34]. The draft contains no provision as to the duration of the agreement, and apart from the reference to Appendix 1 contains no provision about exclusivity either way. Mr Epov assumed that a copy of the Heads of Agreement was to be attached to the Trading Agreement as Appendix 1.

60 On or about 17 February 1999 a second draft of the Trading Agreement was prepared and submitted to Mr Epov. The second version is near to, but not the same as, the final agreement which was later signed on 20 May 1999. Mr Adair approved both the initial version and the revised version of the Trading Agreement. Again, there is nothing in this draft of the Trading Agreement about exclusivity one way or the other.

61 The matter of the finalisation of a detailed trading agreement with ACBB was raised at MCP management meetings on 21 January 1999 [R1/459] and 10 February 1999 [R1/242].

January 1999 China visit

62 During the period 11 to 16 January 1999 Mr Epov, Mr Dong and Mr Roden met with most of ACBB’s Chinese manufacturers in Shanghai where they reviewed product, tooling and printing. A report of that visit became [PE 35]. During the course of that visit Mr Roden prepared [PE 37] which is a schedule for the placement of continuing future bulk orders. During the course of this visit Mr Roden also gave approval for production of products the subject of the November 1998 bulk orders [PE 36]. This approval is for the production of previous orders and not a new order.

Proposed purchase of the PC Rod Machine

63 In early February 1999 Mr Adair asked Mr Epov whether he would be interested in purchasing a powder coat rod machine from MCP. As ACBB was supplying MCP with PC rods, the piece of equipment was obsolete. On 2 March 1999 Mr Adair offered the PC rod machine to ACBB for $350,000 [PE 38]. By letter dated 15 March 1999 [PE 38] ACBB put to MCP its formal proposal for the purchase of the PC rod machine. That proposal was preceded by an introduction in which ACBB made certain complaints about matters which had caused ACBB to examine its future position with MCP, as its commitment to the Windoware project thus far had been very expensive. Concern was expressed that there were several project groups which ACBB had worked on which had been scrapped at the last minute just before an order was to have been placed with ACBB. Therefore when ACBB looks at the acquisition of the assets in the package ACBB needs to view the matter ‘in the context of our overall relationship’. ACBB needs ‘certain assurances’ from MCP before ACBB can make any further investment into the project.

64 The letter then proposed an acquisition package under which ACBB would purchase from MCP for the sum of $350,000:

(a) the PC rod machine;

(b) the valance rod machine;

(c) the bracket machine; and

(d) three year’s supply of powder coating material.

65 ‘As part of this arrangement’ ACBB proposed that MCP should purchase from ACBB for a minimum period of five years:

(a) all of its PC rod requirements;

(b) all of its aluminium extrusion requirements;

(c) all of its Metal Brackets and components currently supplied by CH Trading – Korea; and

(d) all of its Valance Rod requirements.

(emphasis added)

66 The letter also proposed that Mr Roden should be employed by ACBB to liaise between MCP, ACBB and ACBB’s connections in China.

67 PC rod products fell within ‘project 6’ of group 1, valance rod products fell within ‘project 8’ of group 2. An initial order for PC rod products had been lodged on 30 November 1998.

68 On 18 March 1999 Mr Roden sent a memorandum of Mr Adair [PE 42] on the subject of supplier analysis (post rationalisation)*. A copy of this document was provided by Mr Adair to Mr Epov on 30 March 1999. The document contains a list of all of MCP’s suppliers, the product groups, the annual sales revenues, the new suppliers and a time frame for the transfer of business to the new suppliers. On the face of the document, ACBB is not nominated as the exclusive supplier for many of the product ranges. In some cases ACBB is shown as new supplier #1, in other cases some other body is shown as new supplier #1. In the case of some product ranges ACBB is shown as new supplier #2. For example, in relation to the product range styled ‘Extrusions’ McMetals is shown as new supplier #1 and ACBB is shown as new supplier #2. The analysis shows ACBB as the largest of the eight ongoing suppliers with sales revenue of about $19.963M over a projected twelve month period.

69 Taken at face value, there is a tension between this document and Mr Epov’s understanding of the arrangement that ACBB was to be the exclusive supplier to MCP in the areas where ACBB did supply to MCP. Mr Epov said that in his understanding new supplier #2 was a back-up supplier, and certain of the product ranges listed on this document were not the subject of any exclusivity arrangement between MCP and ACBB. In the case of extrusions, whilst ACBB was the back-up supplier there was a specific arrangement with Mr Adair that the extrusions business would be transferred to ACBB from 1 March 2000. Mr Epov professed an inability to explain much about this document as it was devised by MCP.

70 According to Mr Adair when he handed this document to Mr Epov on 30 March 1999* he said:

‘This document is part of our continuing exclusive arrangement between MCP and ACBB. It lists all of our current suppliers and products and a timetable to transfer, in line with the final supply agreement, products to ACBB for procurement. Some of the products you are already supplying.’

71 On 19 March 1999 there was a meeting between Mr Epov and Mr Adair to discuss Mr Epov’s letter of 15 March 1999*. It is common ground between Mr Epov and Mr Adair that during the course of the meeting Mr Adair said that MCP wants an exclusive agreement with ACBB and that is why MCP and ACBB had been working together towards finalising a supply agreement. In line with the terms of that supply agreement, MCP will purchase all of the products currently supplied by ACBB for the term of the supply agreement. MCP will also purchase, in line with the terms of the supply agreement, all PC rods, CH Trading products, valance rod and aluminium extrusions for the term of the supply agreement.

72 On 22 March 1999 [PE 39]* Mr Adair authorised Mr Roden to send to Mr Epov a list of products that were then being purchased by MCP from ACBB with the purchase prices current at the time. The products listed were mainly pre-pack products falling within group 1 in [PE 17], although some other products, for example, gold rod, were also included. The letter stated that MCP would like to incorporate the price list into the current ‘contract’, Terms and Trading Agreement, as an appendix. This was never done. There were some increases in the prices of some of the products on the list due to increased manufacturing costs and increases in the cost of materials occurring after the date of its preparation. These increases were negotiated with MCP.

73 On 29 March 1999 [PE 40]* Mr Adair wrote to Mr Epov in response to the letter of 15 March 1999 and by way of confirmation of the main points of the meeting of 19 March 1999. The letter confirmed that the machines are to be purchased for a total sum of $350,000. The machines are to be relocated in China. It is anticipated that an agreement referred to as the supply agreement, but which later became known as the Trading Agreement, would be resolved at the meeting scheduled to be held on 29 March 1999. MCP will confirm its commitment to purchase the following ranges of product, in line with the terms and conditions of the supply agreement:

(i) all PC rod for the tenure of the agreement;

(ii) all components currently sourced from CH Trading for the tenure of the agreement;

(iii) valance rod as per the specification of the assets for the tenure of the agreement; and

(iv) MCP will utilise ACBB packing centre in Shanghai for all of its packing and repacking of all packaged goods items for the tenure of the agreement.

McKechnie Metals was the sole supplier of aluminium extrusion to MCP under an agreement which expired in March 2000 [Exhibit C]. The letter recorded that the supply line of the aluminium extrusion range of product would revert to ACBB on 1 March 2000.

74 On 8 April 1999 a meeting took place attended by Mr Adair, Mr Epov, Mr Dong, Mr Hanratty and Mr Burson. Mr Epov’s notes of that meeting are [KAR 35]. The notes include the following:

· ‘Hanratty understood that MCP had intended to transfer a substantial amount of their procurement to ACBB and wanted to know whether we had the capacity to accommodate the various ranges?

· Hanratty was very happy with our efforts to date on the clamshell packaging.

…

· PE emphasised that ACBB only made the serious investment to the MCP project on the basis that there was a commitment from MCP through KRA that there would be an exclusive long term strategic alliance in place between the two parties resulting in the transfer of significant business to ACBB. Tenure and volume were the two keys for the success of this opportunity for both sides.

· Hanratty was suitably impressed. He didn’t see any reason why a progressive transfer of business could not take place with ACBB.

· He liked the concept of long term strategic alliances and talked about the UK experiences and raised the possibility of a 10 year contract between ACBB and MCP with a 10 year option.

· He was satisfied that ACBB could do the work and looked forward to hearing more about the unfolding relationship.’

75 On 16 April 1999 Mr Adair wrote to Mr Epov confirming the result of their recent meeting [PE 41]*. The consideration for the purchase of the three machines was reduced to $225,000. With regard to the purchasing commitments:

‘MCP will confirm its commitment to purchase the following ranges of product, in line with the terms and conditions of the supply agreement:

(i) all PC rod for the tenure of the agreement;

(ii) all components currently sourced from CH Trading for the tenure of the agreement;

(iii) MCP will utilise ACBB packing centre in Shanghai for all of its packing and repacking of all packaged goods items for the tenure of the agreement.

With regards to aluminium extrusions, the supply line of this range of product will revert from its existing supplier McKechnie Metals New Zealand on 1st March 2000 …’

76 On 22 April 1999 [PE 45] Mr Epov wrote a long letter to Mr Adair in response to his letter of 16 April 1999. The purpose of the letter was to advise Mr Adair that ACBB was unable to proceed with the acquisition of the surplus assets as outlined in the letter of 16 April 1999. The letter proceeded to explain why ACBB came to that decision. Initially ACBB was advised that should its pricing be satisfactory then it would secure around $A9M of annual business. Based on this volume of business and on ACBB’s confidence that it could provide favourable pricing, ACBB then made a strategic decision and invested significant resources to secure this $A9M of annual business. ACBB was also advised that the quotation process would be rolled out progressively and that ACBB would be given target pricing and all relevant information by the end of October for all of the product groups upon which ACBB would be required to quote. The date was later extended to the end of November. ‘This still has not been finalised’. ACBB was also advised that as it quoted a product group and its pricing was favourable, then orders would be placed progressively. This did not occur. In 1998 when ACBB quoted MCP on the supply of PC rod out of China, ACBB was told that if it reached a certain price then ACBB would take over the PC rod business. ACBB provided a favourable price and MCP placed a six month bulk order for over 900,000 metres. At that time, there were no preconditions relating to the acquisition of the PC rod machine. Later in February 1999 ACBB were advised (after it had invested in the production of PC rod in China) that whoever acquires the PC rod machine would then inherit the PC rod business. The letter then complains of a failure to place the aluminium extrusion business, the springs business and the valance rod business with ACBB notwithstanding the provision by ACBB of favourable pricing in relation to those products. ACBB then found itself in February 1999 in a situation where in order to secure the PC rod business, it had to acquire an old PC rod machine. In order to help MCP, with whom ACBB had made a strategic alliance, and ‘to finally secure the business’ ACBB verbally agreed on a deal with MCP to acquire certain assets. Part of this deal was that ACBB would be given the extrusion business, yet later ACBB discovers that the extrusion business is not available until the year 2000. Various other complaints are made including that MCP has withdrawn the valance rod machine from the deal even though the valance rod machine and the valance business had been previously confirmed as part of the arrangements on at least five separate occasions. The letter concluded:

‘As I have previously intimated to you, during the past three months Mr Dong and I have been examining our future position with Windoware as well as our commitment to the Windoware project. We are now seriously concerned with the ongoing viability of this business. In view of these circumstances we find that we are unable to proceed with the acquisition of the PC rod machine.’

The Letters of Intent

77 It is common ground between Mr Epov and Mr Adair that at a meeting held on 3 May 1999* Mr Adair gave to Mr Epov a letter dated 3 May 1999 annexing a Letter of Intent [PE 46]*. It is also common ground between Mr Epov and Mr Adair that on that occasion Mr Adair said words to the effect that the Letter of Intent sets out the products that MCP will purchase exclusively from ACBB in line with the terms of the Trading Agreement expected to be finalised shortly.

78 The letter of 3 May 1999 [PE 46]* was written in response to the letter of 22 April 1999, referred to above. The letter referred to teething problems that would need to be sorted out and to the fact that whilst MCP was committing the vast majority of its purchasing to ACBB, this process needs to be carried out with the minimum destruction to MCP’s business. Mr Adair said that as he saw it there are two key issues:

(i) supply commitments from Windoware; and

(ii) PC rod acquisition.

Mr Adair said in the course of his evidence that he did not regard these two issues as being interdependent.

79 To resolve these two issues Mr Adair proposed the following:

‘(1) Windoware will supply (see attached) Letter of Intent, with timings of all of the products we, at this period of time, believe ACBB can procure for Windoware (this could be drafted into a legal document); and

(2) I would propose that we conclude the PC rod acquisition at $A200,000 …’

80 The Letter of Intent attached to the letter of 3 May was signed by Mr Adair. It is convenient to set it out in full:

‘Letter of Intent

Windoware will commit to the following procurement from ACBB, see detailed below, based on the set criteria of volume, price quality and service, as per the terms of the supply agreement, the value of these projections can go up or down and they are our best forecast, based on information to date.

Product Category Timing (order placing) Value

Pre Packs Existing A$1.8 million

CH Trading Oct 1999 A$1.2 million

Extrusions Nov 1999 A$2.0 million

PC Rod Existing A$1.3 million

Others Oct 1999 A$0.5 million

NZ requirement general Oct 1999 A$0.5 million

NZ Extrusions Nov 1999 A$1.5 million

Valance Rod Jun 1999 A$0.4 million

Fly Frame May 1999 A$0.2 million

To enable this schedule of procurement to eventuate on time, I would feel it is essential that Leigh Roden coordinate the entire project as previously discussed.

Kevan Adair’

81 The product categories shown in the Letter of Intent accord with the product categories referred to in par [17] of FASC (to be referred to later in these reasons) except that ‘others’ in the Letter of Intent becomes SE Asian (others) in par [17]. There are nine product categories, one of which is PC rod. Note that pre-packs and PC rod are shown as being the subject of existing orders. The column ‘Value’ records the expected value of projected annual volumes and totals at $A9.4M. The Letter of Intent is not expressed to apply for any particular period. Nor does the Letter of Intent refer in terms to exclusivity. However, it is implicit in the letter that MCP’s requirements for the products in the nine categories specified will be purchased exclusively from ACBB, as the letter expresses an intention to commit to the procurement from ACBB of MCP’s anticipated annual requirements of products falling within the nine product categories described. That expression of intention is not absolute and unconditional; it is based on a belief that ACBB can procure those products for MCP, but that depends upon whether the products meet MCP’s criteria of ‘volume, price, quality and service’.

82 On 4 May 1999 Mr Adair sent a letter to Mr Epov attaching a further Letter of Intent [PE 46]*. The letter was sent following a meeting between Mr Dong, Mr Epov and Mr Adair on 3 May 1999, but no details as to what happened at that meeting emerge from the evidence. Nonetheless, the letter confirmed the main points of that meeting namely:

(i) the attached Letter of Intent covers the volumes of products which will be the subject of orders to be prepared and delivered by MCP to ACBB;

(ii) the assets to be acquired pursuant to the asset disposal are the PC rod assets, the PVC rod assets and the valance rod assets for a total consideration of $A200,000;

(iii) as Mr Roden intends to leave MCP and not to join ACBB, MCP would like to know what ACBB’s proposals are to ensure a smooth transition of business from MCP’s existing supply base to ACBB.

83 Again, it is convenient to set out the Letter of Intent in full. It was signed by both Mr Adair and Mr Epov. It is as follows:

‘Letter of Intent

This letter of intent is between McKechnie Consumer Products trading as Windoware, and ACBB.

It covers the procurement of the products detailed below.

McKechnie Consumer Products, trading as Windoware, will prepare and deliver orders for ACBB for the appendix attached of the products.

McKechnie Consumer Products trading as Windoware, reserves the right to execute these orders based on the existing trading criteria that is set out in the terms and conditions of the supply agreement, between the parties which covers specification, quality, service and pricing.

If the above criteria as mutually determined by the parties is acceptable, McKechnie Consumer Products, trading as Windoware will conclude the procurement of the attached product categories to ACBB.

For: McKechnie Consumer Products

T/a Windoware

Kevan Adair

Chief Executive Officer

For: ACBB

Peter Epov

Chairman and Chief Executive Officer’

84 The ‘Appendix attached’ was Appendix 1 which provided as follows:

‘Appendix 1

Product Category Value

CH product range A$1.2 million

Aluminium Extrusions A$2.0 million

SE Asian (others) A$0.5 million

NZ general requirements A$0.5 million

NZ Extrusions A$2.0 million

Valance Rod A$0.4 million

Fly Frame A$0.2 million’

85 The appendix only contains seven product categories. The two product categories which were described as being the subject of existing orders in the Letter of Intent of 3 May 1999 have dropped out. The ‘value’ of NZ Extrusions has changed from $1.5 million to $2.0 million. The column dealing with the timing of orders has been omitted. Again, there is no reference in the Letter of Intent to exclusivity, but, again, it is necessarily implicit in the letter that MCP will not purchase products within the product categories described from third parties because it intends to obtain its anticipated annual requirements of those products from ACBB. This letter makes it slightly clearer that the intended commitment is subject to the products meeting MCP’s criteria in terms of ‘specification, quality, service and pricing’. These products have yet to pass through the process flow chart [PE 22A].

86 ACBB’s letter of 17 May 1999 [PE 47]* was in response to the Letters of Intent. In that letter, Mr Epov records that over the past eight months ACBB has been working very closely with MCP/Windoware to transfer the procurement of a number of MCP’s product groups to ACBB. The letter continues:

‘The practice has been that as MCP/Windoware identify a product, ACBB then develops design drawings for that product. Once confirmed by MCP/Windoware then ACBB produces samples, tooling and dyes as well as “off tool” samples for MCP/Windoware to confirm before orders are placed with ACBB by MCP/Windoware for the production of those products. Once the products are manufactured ACBB then packs these products complete with labels, bar codes, price tags etc in blister packaging and ships the product to MCP/Windoware in Sydney.’

87 In that letter, ACBB welcomed the confirmation of MCP’s commitment to the procurement from ACBB of an annual purchase of $A9.4M of product (as listed in the attachment to the letter of 4 May 1999) for the next five years. ‘In return for this commitment’ ACBB agreed to purchase the assets identified in the letter of 4 May 1999 on the terms therein specified (emphasis added).

88 Mr Epov’s evidence was that ‘in a sense’ a commitment to purchase product from ACBB was related to the proposed asset purchase, whereas Mr Adair saw the two things as being separate.

Trading Agreement

89 ACBB forwarded its ‘final draft’ of the Trading Agreement to MCP under cover of a fax dated 19 May 1999 (sic) [PE 48]. By a fax transmission on 20 May 1999 [R 1/389] Mr Adair told Mr Epov that he was getting somewhat frustrated at the length of time it is taking to get the Trading Agreement and the Letter of Intent over to MCP. He said that he had until midday on 20 May 1999 to finalise the asset issue at Epping and if the two documents failed to arrive he will have to make alternative arrangements. This was a veiled threat to procure MCP’s products from persons other than ACBB, but according to Mr Adair, as a practical matter he was too far committed to go anywhere else. A meeting was suggested to attempt a resolution of problems referred to in the letter or to negotiate a mutually acceptable exit from the arrangement.

90 The Trading Agreement* was executed under the common seals of both companies, and it is common ground that this execution occurred after the MCP fax of 20 May 1999 [R 1/389], and probably on 20 May 1999.

91 The Trading Agreement is expressed to operate for a period of five years, with the option of further renewal of five years: cl 1(a). There is no indication in the agreement as to which party has the option of renewal or how the option may be exercised.

92 It is agreed that the Trading Agreement covers the territories of Australia and New Zealand ‘between the entities ACBB and Windoware Australia and Windoware NZ’: cl 3(a). Clause 4 is headed ‘Product Specification’ and provides as follows:

‘(a) Windoware shall provide approved product, packaging and carton specifications. ACBB shall manufacture and pack products as specified by Windoware. Any changes to specification must be in writing.’

Clause 5 deals with delivery. The dates of delivery are to be specified in the Purchase Order. Clause 6 deals with payment terms.

93 Clause 7 deals with costs. Clauses 7(a), (b) and (c) are as follows:

‘(a) the price of the goods shall be in accordance with the quotations agreed by Windoware prior to the commencement of supply of the Goods pursuant to any Windoware Memorandum of Purchase Commitment or purchase order;

(b) ACBB shall not alter, vary or amend any price of the goods without:

(i) twelve (12) weeks prior written notice to Windoware;

(ii) the consent of Windoware in writing;

(c) Windoware and ACBB agree that the price of the goods shall be reviewed each year. The first review to be conducted between November 1 and November 15 1999.’

Both Mr Adair and Mr Epov agree that the expression ‘Windoware Memorandum of Purchase Commitment’ is devoid of any content. It is a term which was used in the first draft of the Trading Agreement but which did not survive. Although the letter of 22 March 1999 [PE 39] expressed a wish to incorporate the then current price list into the Trading Agreement as an appendix, this did not occur.

94 In oral evidence Mr Chenery expressed the view that a price review referred to in cl 7(c) could result in an increase or a decrease in price, whereas Mr Epov expressed the view that absent agreement, the review could only result in an increase in price. If there was a failure to agree upon a new price as a result of the review, then the existing price continued to apply, although Mr Epov did not point to any specific conversation with Mr Adair or other MCP executives where an agreement was reached to that effect. Mr Adair’s evidence was that it was within his contemplation that ACBB’s material costs might either increase or decrease over the period of the Trading Agreement. So too would the costs of manufactured goods and transportation of goods. The price review clause was a control mechanism which enabled Mr Adair to be satisfied that he was being supplied with competitive product at competitive prices.

95 One of the product categories referred to in the Letter of Intent (and in the letter of 22 April 1999 [PE 45]) was ‘aluminium extrusions’. The transfer of the aluminium extrusion business to ACBB was the subject of negotiation in April 1999. Prior to the Trading Agreement both Mr Epov and Mr Adair knew that the pricing for extrusions was variable according to movements on the London Metal Exchange.

96 At the time of signing the Trading Agreement both parties knew that the prices for product intended to be the subject of the Trading Agreement might need to vary over its term according to a range of variables including foreign exchange fluctuations [T 362], changes in the costs of materials and costs of manufacture to ACBB, and changes in MCP’s retail market affecting the volumes it would require from ACBB. Reference should be made to [Exhibit M1] by way of example. By facsimile dated 7 May 1999 ACBB (Epov) informed MCP (Roden) of some new pricing for gathering hooks. Mr Epov asked if MCP wished to proceed with the current orders at the new price or wished to cancel those orders. The need for change had occurred because of a change of supplier to ACBB who had committed to an automated process to ensure consistency of supply and product delivery.

97 Clause 8 of the Trading Agreement is a protocol for costs review due to foreign exchange rate fluctuations. Clause 9 provides for the title to the goods to pass to MCP on delivery. Clause 10 provides that the agreement is personal to ACBB and to MCP and neither party is entitled to assign the agreement to a third party. Clause 11 deals with planning and purchase forecasting. Clause 11(b) provides for bulk orders to be raised by MCP twice a year for the manufacture of bulk product. The lead time for bulk orders will be six months ahead of the packing schedule. Clause 11(c) provides that purchase orders will be raised by Windoware every three months for packing products. The lead time for pack orders will be eight weeks ahead of the delivery schedule. Clause 11(d) provides for MCP to issue a delivery schedule to ACBB every month.

98 The Trading Agreement does not contain any exclusivity term of the type pleaded, nor does it contain any provision prohibiting ACBB from supplying products to third parties as well as to MCP. Nor does the Trading Agreement contain any provision obliging MCP to purchase any particular products in any particular quantities from ACBB, apart from the stipulation that bulk orders are to be raised by MCP twice a year.

The second bulk order

99 On 31 May 1999 MCP placed its second bulk order with ACBB [PER 1]. The products ordered in the second bulk order were products of the same groups as the initial bulk orders (including PC rod). Unlike the initial bulk orders this was an order for the actual production of the products ordered. The order did not contain the endorsement which was included on the initial bulk orders that the MCP/ACBB product to market process flow chart must be followed. The second round of orders was delayed from an intended second round expected to be placed in April 1999 [PE 43].

Purchase of PC rod machine

100 At a meeting held between Mr Epov, Mr Adair and others on 7 June 1999 Mr Adair announced that MCP did not wish to proceed with the sale of the PC rod machine at this time. The machine is to be stored and a decision will be made at a later date [PE 49]. Mr Epov raised no objection. Mr Adair was under pressure from Mr Hanratty to sell the PC rod machine. Mr Adair notified Mr Epov that he had an interested purchaser for the machine, but only on condition that MCP purchase the PC rod from the purchaser exclusively. Mr Epov agreed to release MCP from its obligation to purchase PC rod from ACBB. On 25 June 1999 MCP entered into a letter of intent with Rollcraft Victoria [KAR 1] and thereafter a mutual exclusivity arrangement [KAR 2] in relation to PC rod.

101 Paragraph [18] of FASC pleads an agreement between the parties reached in about July 1999 to exclude the product category ‘PC Rod’ from the product categories which MCP would procure from ACBB exclusively.

The dealings with ABC

102 On 15 June 1999 a management meeting of MCP was held. The agreed action included the following:

‘38 No new product briefs to ACBB until first projects are up and running. Contingency plan to cover ACBB products to be prepared, preference to overseas.’

103 At the time of the Trading Agreement ABC was an existing supplier of products to MCP. It was located in Indonesia. Between July 1999 and November 1999 approaches were made to ABC to quote on the full range of products supplied by ACBB to MCP. MCP submits that the dealings between MCP and ABC are inconsistent with the exclusivity provisions for which ACBB now contends. There are two answers to this submission. First, if there was some dispute between Mr Adair and Mr Epov as to the communications between them, Mr Adair’s dealings with ABC may have been relevant to the resolution of that dispute. However, there is no dispute as to those communications, and whatever dealings MCP had with ABC cannot impact upon the legal relationship between ACBB and MCP, if only because ACBB was not privy to those dealings. Second, a consideration of the contemporaneous documents makes it reasonably plain that MCP sought quotations from ABC for both contingency reasons and as cost comparisons: see, eg, [R1/480]. The marketing report for November 1999 of MCP records as follows: [R 1/510]

‘ABC – the ABC contingency offers for ACBB supply has been put on hold. ABC have confirmed that there would be a six month lead time for them to gear up to supply all of the ACBB products.’

104 Accordingly, I reject MCP’s submission that its dealings with ABC are inconsistent with the existence of the contractual provisions for which ACBB contends. Those dealings have no bearing on that question.

The proposed sale of MCP

105 In about October 1999 Mr Hanratty contacted Mr Adair and informed him that a decision had been taken that MCP was to be sold. Mr Hanratty requested Mr Adair to prepare an information memorandum for submission to prospective purchasers. Mr Adair produced two versions of that document. Exhibit [KA 9] is an information memorandum prepared specifically for an institutional investor who had expressed an interest in the purchase of MCP. Exhibit [KA 10] is an alternative version of the information memorandum which was drafted to keep confidentiality to a maximum. In this version, suppliers were referred to by code. Section 2.4 of [KA 10] dealt with major suppliers. It provides as follows:

‘2.4. Major Suppliers

Details of Windoware’s major suppliers are set out below:

Supplier Products Annual

Purchases

A$’000

Supplier A Packaged Blinds 5,522

Wooden Curtain Poles

Supplier B Drapery Hardware 2,389

(Packaged Goods)

Supplier C Drapery Hardware 1,608

(Components)

Supplier D Extrusions/Fly Frame 1,390

Supplier E Valance Rods/Extendables 514

Supplier F Drapery Hardware 399

Supplier G Packaged DIY Awnings 336

Supplier H Steel Coil 300

Supplier I Wooden Poles 290

Supplier J Curtain Tape 171

Supplier K Drapery Hardware 94

Supplier L Curtain Tape 34

Supplier M Plastic Components 180

Supplier N Curtain Rod 390

Supply agreements are in place with suppliers A, B, D and N. These offer protection on tenure and exclusivity …’ (emphasis added).

106 Supplier A is ABC, supplier B is ACBB, supplier C is CH Trading, supplier D is MCK Metals Pacific and supplier N is Taiwan Titan.

107 The Information Memorandum contained a disclaimer to the effect that it does not purport to be accurate and complete or all inclusive or to contain all information that a prospective purchaser may require. It urged recipients to make their own enquiries, and not rely on statements made in the information memorandum.

108 On 13 December 1999 MCP placed its third forward order with ACBB covering pre-packs and gold rods for the months of April to July 2000. MCP was unable to provide an order for August and September at that stage because the forecast for those months was being modified.

109 On 13 January 2000 there was a meeting between Mr Epov, Mr Adair and Mr Chenery in which Mr Epov was informed of McKechnie’s decision to sell the MCP operations in Australia and New Zealand. It is common ground between Mr Epov and Mr Adair that there was discussion about the agreement between ACBB and MCP in which Mr Epov was assured that the agreement would be honoured by the purchaser.

Some executives of MCP are unaware of mutual exclusivity

110 Neither Mr McEwen nor Mr Burson was aware prior to the takeover of MCP by Sullivans that ACBB asserted that MCP had agreed to purchase products exclusively from ACBB. Mr Burson says, in particular, that had he been aware of an exclusivity arrangement he would have ensured that this fact was disclosed in the information memorandum and to prospective purchasers of MCP in response to their enquiries. He was not aware of any purchaser raising the issue of mutual exclusivity during the due diligence process to be referred to hereafter.

111 In assessing Mr Burson’s evidence in this respect, it must be recalled that Mr Sinadinos, who I accept as an honest and reliable witness, says that he explained the mutual exclusivity relationship at the 9 December 1998 presentation at which Mr Burson was present. Mr Burson accepted that he was present on that occasion, but had no recollection of what had occurred.

112 Neither Mr McEwen nor Mr Burson was present at any of the meetings between Mr Epov and Mr Adair referred to above when mutual exclusivity was discussed.

PAO – ACBB exclusivity

113 PAO (Thailand) Co Ltd (‘PAO’) was a manufacturer of products located in Thailand. On 14 December 1999 Mr Adair forwarded a memorandum to Mr Chenery [R 1/511] suggesting that information should be provided to PAO highlighting potential products which PAO could manufacture and quote on. The letter included:

‘We can then go and probably finalise a deal, if we are comfortable whilst we are there.’

114 Mr Adair’s report for December 1999 [R 3/1111] referred to PAO as a potential new supplier who had been set some aggressive target prices which could result in reductions of 20-25 per cent on MCP’s existing cost base with the likes of ACBB and CH Trading.

115 A report from Mr Burson of 28 February 2000 [R 2/739] recorded that he saw PAO as being able to replace both ACBB and CH Trading.

116 On 24 February 2000, Mr Burson, Mr Adair, Mr Chenery and others attended a meeting with representatives of PAO at which Mr Burson obtained pricing information for many of the items which MCP and MCP(NZ) were then purchasing from ACBB.

117 Mr Burson’s monthly report for January 2000 [R 2/731] recorded that he was looking forward to visiting PAO in Thailand in late February to evaluate them as a potential supplier to replace ACBB and CH Trading. A memorandum from Mr Burson of 28 February 2000 [R2/739] indicates that he saw PAO as being able to replace both ACBB and CH Trading.