FEDERAL COURT OF AUSTRALIA

Brasington v Overton Investments Pty Ltd [2002] FCA 1495

RITA BRASINGTON v OVERTON INVESTMENTS PTY LTD & ANOR

N 878 OF 1999

EMMETT J

28 NOVEMBER 2002

SYDNEY

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

N878 OF 1999 |

|

BETWEEN: |

APPLICANT

|

|

AND: |

OVERTON INVESTMENTS PTY LIMITED FIRST RESPONDENT

SECOND RESPONDENT

|

|

JUDGE: |

|

|

DATE: |

|

|

PLACE: |

SYDNEY |

REASONS FOR RULING AND FINDINGS

1 In 1994 the first respondent, Overton Investments Pty Limited (“Overton”), was the owner and manager of the Heritage Retirement Village located at 33 Bernard Road, Padstow Heights (“the Heritage Village”). At that time, the second respondent, John Edward James (“Mr James”), was the managing director of Overton.

2 By lease dated 6 June 1994 (“the Lease”), Overton granted to the applicant, Rita May Brasington (“Mrs Brasington”) and her husband, Sydney James Phillip Brasington (“Mr Brasington”), a term of 99 years in respect of Unit 65 in the Heritage Village (“Unit 65”).

3 Mrs Brasington commenced this proceeding on 30 August 1999. In the proceeding, Mrs Brasington complains about the circumstances in which she and Mr Brasington entered into the Lease. All of her complaints arise out of alleged failure on the part of Overton to make full disclosure concerning the extent of the liability of Mr and Mrs Brasington under the Lease to contribute to the expenses of operating the Heritage Village. Mr Brasington died on 29 April 1995 and the proceeding has been conducted on the basis that Mrs Brasington has succeeded to any rights that may have been vested in Mr Brasington in relation to the subject matter of the proceeding.

4 Prior to the commencement of the proceeding, there had been a history of litigation between Overton and the persons who are lessees of units in the Heritage Village (“Lessees”). The history of the litigation is summarised in my reasons in Murphy v Overton Investments Pty Limited [2000] FCA 801 and [2001] FCA 1725.

the present stage of the proceeding

5 The trial of the proceeding was fixed to begin on 21 October 2002. Mrs Brasington intended to call her daughter, Mrs Beryl Rita Burton (“Mrs Burton”), to give evidence at the trial. Because Mrs Burton was unavailable to give evidence during the period fixed for the trial, Mrs Brasington gave most of her evidence-in-chief, and the evidence of Mrs Burton was given in full, on 10 October 2002. Apart from documentary evidence, Mrs Brasington’s case consists of the evidence of herself and Mrs Burton, together with expert evidence relating to the value of Unit 65 at various times.

6 The valuation evidence is relevant to the question of the relief to which Mrs Brasington would be entitled if she succeeds, including the quantification of any loss or damage that might be an essential element of certain of the causes of action relied on by her. I have rejected valuation evidence in the form in which it was propounded on behalf of Mrs Brasington. However, I indicated to the parties that I would be disposed to give Mrs Brasington a further opportunity of adducing valuation evidence in an admissible form.

7 After Mrs Brasington’s case reached the stage where all evidence intended to be relied upon, other than the valuation evidence, had been adduced, counsel for Overton asked the Court to rule that, on the basis of the evidence at that stage, there should be judgment for Overton. The Court was asked to do so on the basis that, if the Court declined to direct judgment for Overton, Overton would still be entitled to adduce evidence in the proceeding.

8 While all claims for relief are based on the same factual circumstances, Overton accepts that, for its application to succeed, it will be necessary to demonstrate that there is no case to answer in respect of any of the causes of action relied upon. Notwithstanding that, because of the outstanding valuation evidence, Mrs Brasington’s case is not yet finally closed, the parties accepted that it would be convenient for the Court to entertain Overton’s application at this stage. Mrs Brasington, however, does not concede that the proceeding is an appropriate one for the making of such a ruling in circumstances where Overton’s right to adduce evidence would be preserved.

9 The general rule of practice, of course, is that, where an applicant closes its case and the respondent wishes to submit that there is no case to answer and that there should then and there be judgment for the respondent, the respondent effectively elects to call no evidence – see Compaq Computer Australia Pty Ltd v Merry & Ors (1998) 157 ALR 1 at 6-7 and Rasomen Pty Ltd v Shell Company of Australia Ltd (1997) 75 FCR 216 at 233. However, departure from that general rule may be justified where fraud is alleged against the respondent.

10 In a fraud case, a party should not necessarily submit itself to cross-examination before it is seen that there is really some evidence against that party – The Union Bank of Australia Limited v Puddy [1949] VLR 242 at 246. Even in a case where fraud has not been alleged, but the case is analogous to one of fraud, by reason of the seriousness of the allegations that are made, the general rule of practice may also be departed from – ACCC v Amcorp Printing Papers Groups Ltd (2000) 169 ALR 344 and 358.

11 Mrs Brasington claims the following relief:

· orders under s 87 of the Trade Practices Act 1974 (Cth) (“the Act”):

· damages or compensation under s 82 of the Act for contravention of Part V of the Act;

· damages or compensation for giving negligent advice to Mrs Brasington;

· damages for fraudulent misrepresentation;

· damages or compensation resulting from departure by Overton from assumptions made by Overton and Mrs Brasington in entering into the Lease;

· damages or compensation resulting from unconscientious use by Overton of a superior position or bargaining power to the detriment of Mrs Brasington;

· orders under the Contracts Review Act 1980 (NSW) (“the Contracts Review Act”).

12 I propose to make findings on a number of matters about which submissions have been made. The findings will be provisional in the sense that, if I were to refuse Overton’s application for the entry of judgment, but still permit Overton to adduce evidence, and Overton subsequently adduced evidence, different findings might be made in relation to certain of the matters upon which I now make findings.

13 As I have said, Mrs Brasington opposes Overton’s application for the Court to make a ruling. The basis for her opposition is that Overton’s application had the potential to extend the proceeding and to require duplication of submissions. In the events that have occurred, that does not appear to be a concern. Indeed, Mrs Brasington accepts that it would be convenient for me to make findings on matters in respect of which the evidence is complete, since that may facilitate the finalisation of valuation evidence.

THE LEGAL FRAMEWORK RELATING TO UNIT 65

14 The Lease incorporates by reference, as do leases granted to other Lessees, memorandum Y452314 (“the Lease Memorandum”), which had been filed in the office of the Registrar General on 27 July 1989. In addition to the terms of the Lease, the arrangements between Overton on the one hand and Lessees on the other, were regulated by the terms of a deed of trust dated 31 December 1985 (“the Trust Deed”) between Perpetual Trustee Company Limited (“Perpetual”) and Overton.

15 The Lease Memorandum and the Trust Deed contain provisions dealing with the Lease Price, Rent, Lease Deposits, surrender of leases and contribution to outgoings and expenses. The effect of the arrangements that were entered into between Overton and Mr and Mrs Brasington in relation to Unit 65 may be summarised as follows:

· Upon the grant of the Lease, Mr and Mrs Brasington were to pay the sum of $175,000 by way of Lease Price.

· 25 per cent of the Lease Price, being the sum of $43,750.00, represented Total Rent for the first five years of the Term granted by the Lease. The Total Rent was to accrue to Overton and be appropriated monthly. The appropriated Total Rent was to be retained by Overton. If the Lease terminated before the expiration of the first five years, the unappropriated Total Rent was to be refunded to Mr and Mrs Brasington.

· No Rent, as such, was payable in respect of the balance of the Term after the expiration of the first 5 years.

· Upon termination of the Lease, the Lease Deposit, being 75 per cent of the Lease Price, namely $131,250, adjusted by reference to the Lease Deposit payable by any incoming Lessee, was to be refunded to Mr and Mrs Brasington. If the Lease Deposit payable by the incoming Lessee were less than the sum of $131,250, the amount to be refunded would be reduced by the amount of the shortfall. On the other hand, if the Lease Deposit paid by the incoming Lessee exceeded the sum of $131,250, one-half of the excess was to be paid to Mr and Mrs Brasington. The other half was to be retained by Overton.

· In addition to paying the Lease Price, Mr and Mrs Brasington were required, until such time as the Lease is terminated or surrendered, to contribute to outgoings and expenses levied by Overton in accordance with the Lease Memorandum.

16 Under Clause 5(a) of the Lease Memorandum, Mr and Mrs Brasington were required, until such time as the Lease is terminated or surrendered, to contribute to outgoings and expenses levied by Overton in accordance with Clause 5. Under Clause 5(b) Overton is entitled from time to time to notify Mr and Mrs Brasington of Overton’s current estimate of their contribution to the outgoings in respect of Unit 65 and the Heritage Village and facilities thereof in relation to any particular period. Mr and Mrs Brasington are thereupon required to make payment of the amount of such estimated contribution. As soon as practicable after the end of each period in respect of which contribution has been levied, an adjustment is to be made by the payment of any deficiency in the amount of such contributions actually paid or the crediting of any excess against any future such contributions.

17 Clause 5(c) of the Lease Memorandum provides that “the Outgoings” in respect of which Overton may levy contributions include provision for 21 specified expenses, including the following:

· rates and charges payable to any relevant body or authority in respect of the Heritage Village;

· insurance premiums;

· expenditure for maintenance generally of the Heritage Village;

· expenditure incurred in carrying on the operations of the Heritage Village;

· provision for future repairs and other contingencies;

· expenditure incurred in providing meals, domestic and other services, including health services;

· gardening and landscaping expenses;

· salaries and wages of staff of the Heritage Village relating directly to the running of the Heritage Village;

· such other reasonable and proper expenses and outgoings as Overton may from time to time decide.

18 Clause 5(f) provides for the determination of the contribution of each of the Lessees to the total of Outgoings. The determination is based on floor area of the units of the Heritage Village. No question arises in the proceeding concerning the calculation of the appropriate proportion attributable to Unit 65.

19 Clause 5(g) provides that, in addition to the Outgoings, Overton may require Mrs Brasington to pay and to discharge, and to keep Overton indemnified against, all other outgoings, charges and liabilities for which Overton determines Mrs Brasington should be separately liable in respect of Unit 65. That provision includes, but is not limited to, any liability arising from any requirement of any competent authority, where the requirement applies to or in respect of Unit 65.

20 Clause 5(h) provides that any contribution in respect of Outgoings levied by Overton under Clause 5 is to become due and payable within seven days of receipt of notice of the levy. Interest is to be paid on any overdue sum not paid on or before the day appointed for payment. Clause 5(i) provides that, except in the case of manifest error, the determination of Overton as to the amounts payable under Clause 5 is to be binding.

21 The Lease contains a reference schedule (“the Reference Schedule”) setting out nine items to which reference is made in general terms in the Lease Memorandum. The scheme of the documents is that the variable provisions applicable to each Lessee were to be inserted in the Reference Schedule in the lease to that Lessee. The Reference Schedule contains the following items:

Item 1 - Premises

Item 2 - Commencement Date

Item 3 - Termination Date

Item 4 - Total Rent

Item 5 - Lease Deposit

Item 6 - Estimated Initial Outgoings

Item 7 - Guarantor

Item 8 - Fixtures, Fittings and Furnishings

Item 9 - Service and Facilities.

22 The entry under each of those items is intelligible only by reference to the detailed provision of the Lease Memorandum referring to that item. Thus, for example, the term “Premises” is defined in the Lease Memorandum in the following terms:

“Premises means the premises described in Item 1 of the Reference Schedule extending to and including the inner surface of walls, windows and external doors, the upper surface of floors and the under surface of ceilings.”

23 The commencement date in the Lease is 6 June 1994 and the termination date is 5 June 2093. The amount of Total Rent and the amount of Lease Deposit in the Lease are the amounts set out above.

MRS BRASINGTON’S CLAIMS

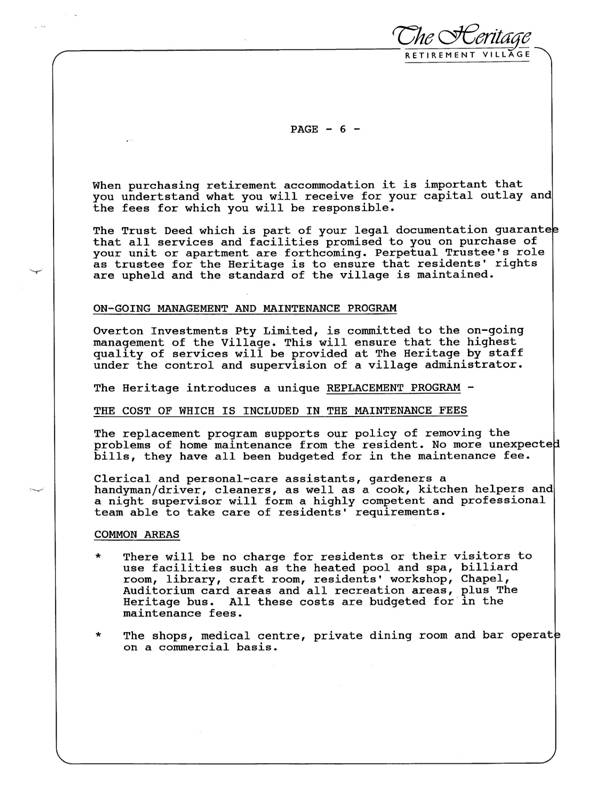

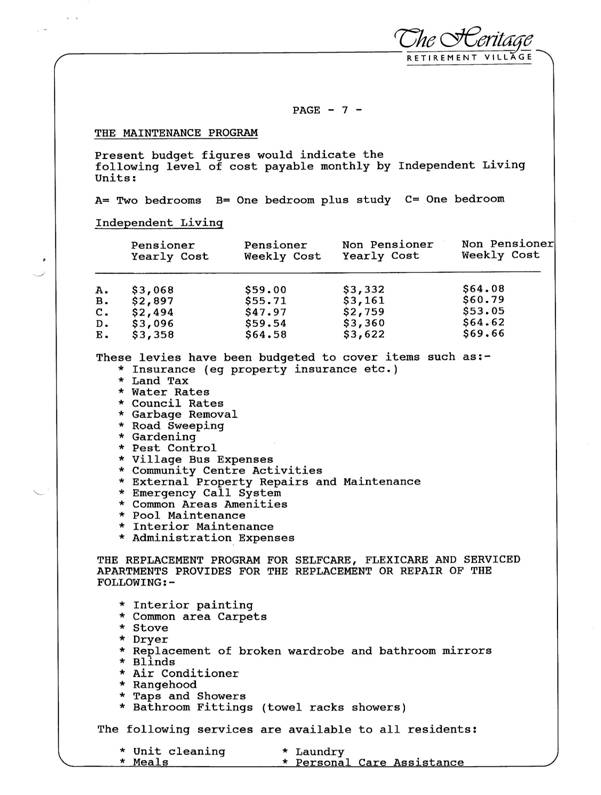

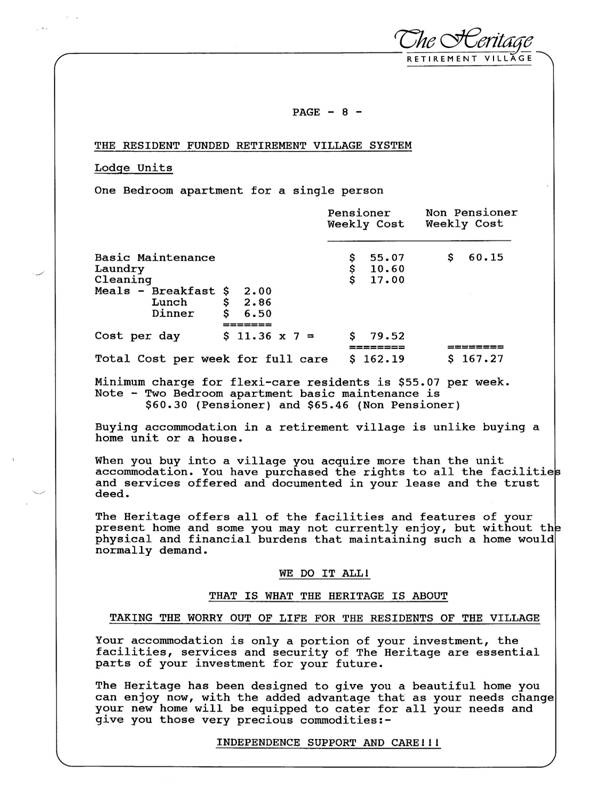

24 In March 1994, printed material describing the Heritage Village (“the Booklet”) was provided to Mr and Mrs Brasington. The Booklet comprises a folder in which 15 separate sheets, which are stapled together, were loosely inserted. The Booklet begins by providing information concerning Overton and the development of the Heritage Village. It describes the accommodation that was to be available in the Heritage Village and the services and facilities available for Lessees. The Booklet then sets out information concerning the maintenance fees for which a Lessee would be responsible. Specifically, pages 6, 7 and 8 of the Booklet are as set out in the Appendix to these Reasons. In April 1994, the form of the proposed Lease, including the Lease Memorandum, was furnished to Mr and Mrs Brasington’s solicitors.

25 Mrs Brasington says that, in reliance upon representations allegedly made by or on behalf of Overton, and by reason of the failure of Overton to advise her and Mr Brasington of certain matters, she and Mr Brasington entered into the Lease. Mrs Brasington also alleges that, throughout the period from 6 June 1994 to 27 November 1996, Overton continued to make the representations and continued to fail to disclose any of those matters. She says that, by reason of the continuing of the representations and the failure to advise of the matters, she paid the amounts levied by Overton pursuant to Clause 5 of the Lease from 1 July 1994 to 28 February 1997 and took no steps to surrender the Lease at a time when the value of the leasehold interest granted by the Lease was not less than the amount that had been paid for its grant.

26 Mrs Brasington’s complaints against Overton arise principally out of Item 6 of the Reference Schedule, which is explained by Clause 5(l) of the Lease Memorandum. Clause 5(l) is in the following terms:

“[Overton] estimates that the initial contribution which [Mrs Brasington] will be called upon to pay will be the amount shown in Item 6 of the Reference Schedule. Such amount constitutes an estimate only and is subject to determination and variation from time to time in accordance with this clause.”

Item 6 of the Reference Schedule was completed as follows:

“$59 per week – pensioner

$64.08 per week – non pensioner.”

27 The critical statement in the Booklet concerns the information furnished as to the maintenance fees payable in respect of units in the Heritage Village. Unit 65 is an “H” Type Unit. The Booklet does not refer to “H” Type Units. However, the proceeding has been conducted on the basis that “H” Type Units are equivalent to “A” Type Units. Thus, in the extract from the Booklet set out in the Appendix, the relevant cost for Unit 65 is that shown opposite “A” Type Units. That is to say, the Booklet states that, for a pensioner, the weekly cost will be $59 and, for a non-pensioner, the weekly cost will be $64.08. They are the figures inserted in Item 6 of the Reference Schedule of the Lease.

Alleged Representations

28 First, Mrs Brasington contends that the following representations were made by Overton:

“(a) The Estimated Initial Outgoings in Schedule 6 of the Lease was an accurate estimate by Overton, of the total outgoings for which the Applicant was liable under the Lease at the time the unexecuted Lease was provided by Overton to the Applicant.

(b) The estimate set out in the information booklet was an accurate estimate by Overton, of the total outgoings for which the Applicant was liable under the Lease at the time the information booklet was provided by Overton to the Applicant.

(c) Substantially all outgoings incurred by Overton in the operation of the Heritage Retirement Village for which the applicant was liable under the Lease, at the time the unexecuted Lease was provided by Overton to the Applicant, had been incorporated into the Estimated Initial Outgoings in Schedule 6 of the Lease.

(d) Substantially all outgoings incurred by Overton in the operation of the Heritage Retirement Village for which the applicant was liable under the Lease, at the time the information booklet was provided by Overton to the Applicant, had been incorporated into the estimate in the information booklet.”

29 Mrs Brasington alleges that each of those representations is implied from the fact that Overton alone knew the precise level of expenditure involved in operating the Heritage Village that was recoverable under the Lease and from the fact that, if the figures in Item 6 and in the Booklet were accurate, then substantially all outgoings incurred by Overton in the operation of the Heritage Village must have been taken into account. The implication is said to arise by reason of material contained both in the Booklet and in the proposed form of Lease. It follows, of course, that the representations could not have been made until April 1994, when the form of the Lease was provided to Mr and Mrs Brasington’s solicitors.

30 Mrs Brasington also contends that Overton made the following further representations:

“(e) The quantum of future total outgoings would be limited to the Estimated Initial Outgoings in Schedule 6 of the Lease plus such increases in costs which were fairly and/or reasonably based on the outgoings comprised in the said Estimated Initial Outgoings.

(f) The quantum of future total outgoings would be limited to the estimate set out in the said information booklet plus such increases in costs which were fairly and/or reasonably based on the outgoings.

(g) Future increases in outgoings would be limited to ensure that if either the Applicant or her husband passed away, the survivor on a single full age pension would always throughout the term of the lease be able to afford to pay all outgoings for which the survivor was liable without recourse to depleting the assets of the survivor.”

31 Those representations are alleged to be implied from the following matters:

“12.11Overton alone knew the precise level of expenditure involved in operating the Heritage Village, which was recoverable under the Lease.

12.16 Overton welcomed as residents, persons in receipt of full pensions, and where Overton was aware that such persons’ income was fixed and would not be able to finance contributions that increased over and above that sum which a resident on a full age pension would be able to afford to pay, without recourse to other income.”

The paragraph numbers are taken from the current form of the Statement of Claim.

32 Mrs Brasington contends that the following representation is also to be implied from matters 12.11 and 12.16 above:

“(k) Overton had not withheld from the Applicant any significant amount of expenditure incurred by Overton and contingently recoverable under the Lease when making ‘the estimates’.”

33 Next, Mrs Brasington contends that, when she visited the Heritage Village in March 1994, the following representation was made on behalf of Overton by Veronica Conroy (to whom I shall refer below):

“(h) the only expenditure incurred by Overton for which [Mrs Brasington] was liable under the Lease at the time of execution of the Lease was the amount of the weekly maintenance/service fee levied at the time of the Lease namely $60.00 per week.”

34 Mrs Brasington also contends that the following express representation was made on behalf of Overton by Veronica Conroy when she visited Mrs Brasington’s home in March 1994:

“(i) future increases in outgoings would be limited to CPI increases.”

35 In addition, Mrs Brasington alleges that the following representation is made expressly in the Booklet:

“(j) if [Mrs Brasington] entered into the Lease they [sic] would have no financial worries for the duration of the Lease arising out of her Lease obligations.”

36 Finally, Mrs Brasington alleges that the following representations were made by Overton:

“(l) the level of outgoings levied by Overton from individual residents under their respective Leases including [Mrs Brasington]would never increase so substantially that the value of the leasehold interest being acquired by [Mrs Brasington]under the Lease would be significantly diminished.

(m) [Mrs Brasington] would never lose the ability to readily procure a replacement Lessee and to surrender the Lease, without sustaining a substantial loss on the Lease deposit if Overton saw fit to recover all outgoings that it was entitled to levy under the lease.”

37 Those representations are said to be implied from the following matters:

“12.11Overton alone knew the precise level of expenditure involved in operating the Heritage, which was recoverable under the Lease.

12.12 [Mrs Brasington] was never able, throughout the term of the Lease, to afford to pay the outgoings contingently liable under Clause 5 of the Lease if, Overton at any time throughout the term of the Lease determined to levy [Mrs Brasington] and her husband for all outgoings recoverable by Overton under Clause 5 of the Lease.

………………………

12.15 Insofar as the level of outgoings levied by Overton under the Lease increased substantially, the value of the leasehold interest of [Mrs Brasington] and her husband would be significantly diminished without sustaining a substantial loss on the Lease Deposit.

12.16 Overton welcomed as residents, persons in receipt of full pensions, and where Overton was aware that such persons’ income was fixed and would not be able to finance contributions that increased over and above that sum which a resident on a full age pension would be able to afford to pay, without recourse to other income.

………………………

12.19 During the period March to June 1994, [Mrs Brasington] informed Overton through its agent, Veronica Conroy, that:-

· [Mrs Brasington] was retired;

· [Mrs Brasington’s] husband was in poor health;

· their income was fixed (being the amount from time to time of the full age pension paid by the Commonwealth of Australia) and would remain fixed for the duration of the Lease;

· future increases in the level of outgoings significantly in excess of “the estimates” would make it extremely difficult for [Mrs Brasington] and her husband to afford to meet their obligations under the Lease; and

· she was concerned about whether they, as pensioners, could afford to live at the Heritage Retirement Village.

12.20 During the course of these inquiries, [Mrs Brasington] specifically inquired of the Agent of Overton, Veronica Conroy, as to:-

· the potential for future increases in outgoings recoverable under the lease; and

· the affordability of the Lease if [Mrs Brasington] was only in receipt of a single full age pension. ”

FALSITY OF ALLEGED REPRESENTATIONS

38 Mrs Brasington alleges that, by reason of the following matters, each of the representations referred to above was false:

“12.1 From 1 July 1992 to 30 June 1993 the level of outgoings for which the Lessees of the Heritage Retirement Village was contingently liable under Clause 5 of their Leases was $1,018,548.

………………………

12.4 Because the level of outgoings for which the lessees of units at the Heritage Retirement Village were contingently liable under Clause 5 of the Lease to Overton under the Lease throughout the 1992-93 financial year was $1,018,548, future increases in outgoings recoverable by Overton under the Lease would greatly exceed the amount of $59.00 per week if Overton at any time in the future determined to recover from [Mrs Brasington] all outgoings recoverable under the lease.

12.5 From the establishment of Heritage Retirement Village in late 1986 to 27 November 1996, Overton:

· did not pass on to Lessees a substantial level of outgoings for which the Lessees were liable under their respective leases; and

· excluded a substantial level of outgoings recoverable under the Lease from its estimate.

12.6 By reason of the matters set out in paragraphs 12.1, 12.4 and 12.5 above:

· the Estimated Initial Outgoings in Schedule 6 of the Lease;

· the estimate of the weekly maintenance/service fee set out in the information booklet; and

· the “level of cost payable based on the present budget figures’ referred to in the information booklet (‘the estimates’);

were not accurate estimates by Overton at the time, of the total outgoings for which residents at the Village were contingently liable under their Leases.

12.7 At all times it was open to Overton to substantially increase the level of outgoings under the Lease without regard to the basis upon which any of ‘the estimates’ had been calculated.

12.8 Further, at all times it was open to Overton to so increase future outgoings recoverable under the Lease that lessees on a single full age pension would not be able to afford to pay all outgoings for which they were liable without recourse to depleting her assets.

12.9 Further, at all times it was open to Overton under the Lease to recover all outgoings incurred for such levels of expenditure as Overton in its sole discretion saw fit to incur:

· even though this involved significant increases in staffing levels, catering expenses and expenses relating to residents’ functions and entertainment; and/or

· even though such levels of expenditure resulted in substantial shortfalls in the Maintenance Fund.

12.10 [Mrs Brasington] was liable under the lease for all losses sustained by Overton in the provision of the services of unit cleaning, laundry, meals and personal care assistance (the user pays services).

12.11 Overton alone knew the precise level of expenditure involved in operating the Heritage, which was recoverable under the Lease.”

Alleged non disclosure

39 Mrs Brasington also alleges that Overton failed to advise her of a number of matters (“the Undisclosed Matters”) as follows:

· the matters referred to as 12.1, 12.4, 12.5, 12.6 12.7, 12.8 and 12.9 in the previous paragraph;

· the falsity of the representations referred to above as (c), (d), (e) and (m);

· Overton had been notified by its accountants that the level of outgoings recoverable from the Lessees for the period to 30 June 1993 had been $1,018,548, as distinct from $453,131, which was the sum recovered from the Lessees.

continuing representations

40 The continued making of all of the representations referred to above is alleged to be implied from the fact that, having been made prior to 6 June 1994, the representations were at no time subsequently corrected by Overton prior to 27 November 1996. On that day, Overton stated unequivocally to the then Lessees, including Mrs Brasington, that it proposed to levy contributions for all expenditure incurred by it in operating the Heritage Village.

loss and damage

41 Mrs Brasington claims, on several alternative bases, that she suffered loss and damage. She asserts that no loss or damage was suffered by her until 27 November 1996 when Overton made the assertion of its entitlement to levy contributions for all expenditure incurred by it in operating the Heritage Village. Alternatively, she says that she suffered loss and damage when she and Mr Brasington entered into the Lease.

42 The primary basis is that cost and damage is to be calculated by subtracting:

· the value of Unit 65 as at the date of judgment plus any liability for outgoings not yet paid as at the date of judgment,

from

· the sum of $175,000 plus interest thereon under s 51A of the Federal Court of Australia Act 1976 (Cth)up to the date of judgment together with any liability for abnormal legal and accounting costs that Mrs Brasington owes to Overton under the Lease.

43 Alternatively, Mrs Brasington contends that the loss and damage suffered is to be calculated by subtracting:

· the consideration that would have been paid for the leasehold interest acquired under the Lease on 6 June 1994:

- by a knowledgeable and prudent Lessee who knew the true level of outgoings recoverable by Overton under the Lease at that time;

or, alternatively,

- on the assumption that Overton had asserted the entitlement to recover all outgoings incurred by it in the operation of the Village that it asserted on 27 November 1996,

from

· the sum of $175,000 plus any liability for abnormal legal and accounting costs.

findings of fact

44 I propose to set out the findings that I would make on the evidence as it stands at present and indicate certain factual conclusions that, in the light of those findings, I would reach in relation to the several causes of action pleaded by Mrs Brasington.

the level of outgoings as at march 1994

45 On 1 June 1992, the Lessees were furnished with a forecast operating budget for the period ended 30 June 1993 (“the 1993 Budget”). The 1993 Budget showed total outgoings for the Heritage Village of $452,000. It provided for income by way of maintenance fees in the sum of $345,900. Fees were shown of five types of unit. The fees shown for “A” Type Units was $64.08 per week for non-pensioners and $59.00 per week for pensioners. No fees were shown for “H” Type Units. The rates calculated for each unit type produced a total of $345,919.45. That figure was rounded down to $345,900 in the budget itself.

46 Pannell Kerr Forster (“PKF”), chartered accountants, were the auditors of Overton. In that capacity, as required by Part 5 of Schedule 1 to the the Retirement Village Industry Code of Practice Regulation 1989 (NSW) (“the Code of Practice”), they reported to the Lessees, in respect of each annual period ended 30 June, on the Maintenance Fund for the operation of the Heritage Village. PKF’s report to the Lessees for the year 1992-93 ended 30 June 1993, dated 17 December 1993, showed total expenses for the period of $490,108. Income was shown as $496,183, giving rise to an operating profit of $6,075.

47 On 10 March 1994, PKF wrote to Mr James in relation to accounting for the Maintenance Fund of the Heritage Village. The letter recorded that PKF had been asked to comment “on the items that, in the first instance may be included in the expenditure of the [Maintenance Fund], and secondly those items which reasonably should be met by [the Maintenance Fund]”. The letter observed that the terms of the Lease Memorandum seemed “to make recoverable from the Lessees any cash flows which may be incurred in association with [Heritage] Village activities”.

48 The letter then went on to observe that the activities of Overton in relation to the Heritage Village could be divided into three categories as follows:

· building and construction;

· holding of investment property for rent;

· management of the ongoing operation of the Heritage Village to a level of enjoyment of the residents of a first class facility.

49 The letter also referred to a fourth activity, “Amberleigh”, which the letter described as a separate development from the Heritage Village. The letter observed that expenditure incurred under the third category set out above would “be the main category for contributions to outgoings, with some transgression into” the first and second categories set out above. The letter then referred to the results for the year ended 30 June 1993, saying that, after a “prior period adjustment” of $43,052, the surplus of $6,075 for the year ended 30 June 1993 was converted to a deficit in the sum of $36,977.

50 Attached to the letter was a spreadsheet described as a “model”, showing that the total expenses of Overton for the year ended 30 June 1993 amounted to $4,232,791. Those expenses covered all of the activities referred to above. The model reallocated the total expenses to the following activities:

Building: $2,177,136

Letting: $745,296

Amberleigh: $291,812

Operating: $1,018,548

Total: $4,232,791

51 The letter went on to say as follows:

“Adopting the attitude of reasonability and eliminating building and letting activities and Amberleigh we suggest $1,018,548 could have been subject to contributions by residents providing all expenditure was necessary and reasonable and as a consequence of operating a first class village. This is exclusive of any sinking fund allocations or provision for replacements under Clause [5(c)(vii) of the Lease Memorandum].

We do note however, that in respect of 1993 year [Overton] adopted a far more moderate approach in levying residents’ contributions. This was probably due to the continuation of policies adopted by a previous management.

Commercially speaking, to continue with this approach would be undesirable to the financial position of [Overton]. Attention to the establishment of a formula for regular increases in contributions on the basis of comprehensive forward projections for the Fund should therefore be a matter of priority, and we understand that this is currently being reviewed.”

52 There is no reason to doubt the accuracy of the figures included in the model attached to PKF’s letter. PKF’s letter was adopted by Overton when it sent a copy of it to the Lessees under cover of notice of meeting on 30 March 1994.

53 A forecast operating budget for the Heritage Village for the period ending 30 June 1994 (“the 1994 Budget”) was prepared during March 1994. It showed total Outgoings of $567,080, with a deficit of $88,080 after allowing for budgeted income. There was no change from the 1993 Budget in the weekly fees calculated as contributions to Outgoings.

54 On 29 March 1994, PKF wrote again to Mr James referring to:

· PKF’s letter of 10 March 1994;

· a letter from Gadens Ridgeway of 24 March 1994;

· the 1994 Budget.

55 The letter of 29 March 1994 referred to “an inventory of the outgoings listed in our model of 10 March 1994”. It appears that the relevant paragraphs of clause 5 of the Lease Memorandum were added to the outgoings shown in the model.

56 PKF’s letter of 29 March 1994 went on to say:

“On the basis of the accounting system which is now being put into place it will require a conscious allocation by [Overton], at the time of incurrence of any expenditure, to identify items to be met through the Maintenance Fund. The outgoings will then be subject to audit review at year-end, giving a considerable degree of assurance that only expenditure that is reasonable and proper will be included on behalf of the Maintenance Fund.

In order to make more specific allocations in relation to the 1993 year, a partial audit of the full company records would be required, due to the lack of formality in the previous accounting system.

However, the maintenance audit work that was performed did go as far as ascertaining that all amounts included in the Maintenance Fund for 1993 were reasonable and proper, even though we will not require to comment on the full extent of expenses that could have been met if [Overton] had not chosen to outlay some amounts from the general account.

Not until performing the exercise of 10 March 1994 were we able to show that in the past such items as salaries and grocery purchases have arbitrarily been apportioned between the Maintenance and General account, regardless of the fact they were all incurred in operating the [Heritage Village] and could reasonably and properly have been included in [Heritage Village] outgoings. We did this by disregarding provisional apportionments and making allocations only where outgoings could reasonably have been incurred across all three activities of building, letting and operating the [Heritage Village].

………………………

We would conclude then that in the absence of manifest error, our allocations of outgoings are sound and consistent with the terms of the lease both from a legal and accounting point of view. The recovery of contributions to outgoings from residents in 1993 could therefore have been $1,018,548. We reiterate that [Overton] in fact adopted a more moderate recovery of $453,131 plus a prior year adjustment of $43,052… .

The purpose of this advice, therefore, is to demonstrate that whatever the amount of the contributions sought by [Overton] over the years, the only basis on which contributions can be levied is set out in the [Lease Memorandum] and the amount recovered must fall within these limits.

We have certified that all of the outgoings put through the Maintenance Fund over the years have satisfied the terms of the Lease. That is now evidence is that [Overton] chose not to recover some outgoings regardless of the fact they could properly and reasonably have been recovered through contributions to outgoings. The 1993 model merely illustrates the extent of this discretion.”

57 After referring to the 1994 budget, PKF’s letter of 29 March 1994 then said:

“On the basis of the above, total budgets and expenditure of $567,080 does not seem unreasonable. Indeed, if total operating expenditure can be anticipated to be in the vicinity of the $1 million demonstrated by the 1993 PKF model, [Overton] is again adopting a more moderate view of recovery under the lease than is actually available to it.”

58 On 28 April 1994, a meeting of the Advisory Committee of the Heritage Village took place at the Heritage Village. Those present included Mr James and Ms Julie Hough of PKF, the author of PKF’s letters of 10 and 29 March 1994. Also present were representatives of the Lessees including Messrs Stewart, Fusedale and Murphy and Mr and Mrs Burnham. In the course of the meeting a number of exchanges took place between Ms Hough and Mr James on the one hand and Lessees on the other.

59 Towards the beginning of the meeting, Ms Hough said:

“The total amount of expenditure incurred in maintaining this Village during the 1993 year exceeded $1 million. The manager sought to recover approximately half of that. In the 1994 year the expenditure incurred in running the Village is probably going to be something in the vicinity of $1 million also. The manager is seeking to recover the figure stated in this budget (referring to the 1994 budget).”

60 Subsequently, Mr Fusedale said:

“May I ask a question please? You made a statement a while ago that there are outgoings in excess of $1 million. That means that all these figures here are understated. Is that right?

61 Ms Hough responded:

“The total expenditure incurred in maintaining the Village for the 1993 year was in excess of $1 million. The process by which that has been ascertained is to take the accounts of Overton Investments Pty Limited and to prepare a statement of a source and application of funds and divide it into the main activities of the Company – they are building, letting activities, running and management of the Village and there is a fourth thing which has no bearing… In allocation of expenditure the gross expenditure of across the board activities… came up to in excess of $1 million. In other words, out of the total expenditure for the Village for the year, in terms of the contract, up to $1 million could have been recovered individually.”

62 There was a further exchange concerning the items from which the excess over the budget would have been derived. Reference was made to wages as being a significant item of expenditure that had not been passed on to the Lessees in full.

63 Subsequently, Ms Hough said:

“In respect of the 1994 financial year, the Company will be continuing to fund, and to an extent subsidising, but its not seeking to recover the full amount of what will be expended in running the Village, and it never has.”

64 Mrs Burnham said “Are we to expect then that $1 million deficiency is at some future date going to be recovered?”. Mr James said “We reserve our rights on that”. Mrs Burnham then said “We better start looking for alternate accommodation”. It may have some significance that Mr and Mrs Burnham did in fact dispose of their leasehold interest in the Heritage Village before the end of 1996.

65 On 4 October 1994, PKF reported to the Lessees on the Maintenance Fund of the Heritage Village for the year ended 30 June 1994. Their report disclosed an operating loss of $128,601, as compared with the 1994 Budget loss of only $88,080. The report contained the following note:

“The operating loss of $128,601 largely represents the expenses incurred through the maintenance fund which were not adequately covered by maintenance levies. During the year management made a conscious decision that the maintenance fund should more realistically reflect the cost of operating the Village. This has resulted in substantial increases in salaries and bus expenses when compared to the 1993 year.

In accordance with… the Trust Deed, the manager is entitled to recoup part, or all of the loss, from the residents.

It is noted that maintenance levies were increased from 1 July 1994 and will now be reviewed on a quarterly basis and adjusted for movements in the consumer price index.”

The report demonstrates that actual expenses for the period were $623,717 as against the figure of $567,080 in the 1994 Budget.

66 The calculations made for 1993 Budget resulted in weekly contributions of $59.00 (for pensioners) or $64.08 (for non-pensioners) in respect of “H” Type Units. Those figures were arrived at on the basis of outgoings of $452,000 for the year ended 30 June 1993. Despite the fact that the 1994 Budget showed total outgoings of $567,080 for the year ended 30 June 1994, no change was made to the level of weekly contributions for the various types of unit and, during the period ended 30 June 1994, Overton made levies at the same rates of $59.00 or $64.08 for “H” Type Units.

67 PKF’s audit report to lessees for the year ended 30 June 1995 showed expenses of $626,173 for the operation of the Heritage Village in that period. Overton subsequently obtained from PKF a supplementary audit report for the year ended 30 June 1995, which showed additional costs of operation of $207,962 for that year. The supplementary report also showed additional items of expense of $35,000 for bus driver and $62,911 for costs of goods sold. On that basis, the total Outgoings for the year ended 30 June 1995 amounted to $927,046, being the sum of the following amounts:

· $626,173

· $207,962

· $62,911

· $30,000.

68 The figure of $927,046 can be contrasted with the budgeted outgoings for the year ended 30 June 1995 of $548,624 and for the year ended 30 June 1994 of $567,080. The budget for the year ended 30 June 1995 did not include user-pay expenses. Apart from any adjustment for that matter, however, the budget for the year ended 30 June 1995 appears to have been prepared on the same basis as the 1994 Budget. Accordingly, it is possible to extrapolate backwards from the figure of $927,046 to conclude that it is more likely than not that, notwithstanding that the 1994 Budget showed expenses of $567,080, the total Outgoings, within the meaning of Clause 5 of the Lease Memorandum, for the year ended 30 June 1994, were in excess of $900,000.

69 That conclusion is corroborated by PKF’s letter of 10 March 1994 and the comments made by Mr James, and by Ms Hough in the presence of Mr James, at the meeting of 28 April 1994. That evidence indicates that the total Outgoings (within the meaning of Clause 5 of the Lease Memorandum) for the year ended 30 June 1994 amounted to $1,018,548.

70 Thus, on the balance of probabilities, total Outgoings, within the meaning of Clause 5 of the Lease Memorandum, for the year ended 30 June 1994, were in the vicinity of $1 million. However, the weekly contribution in respect of “H” Type Units for the year ended 30 June 1994 was calculated by reference to outgoings of $452,000. It follows that the figures of $59.00 (for pensioners) and $64.08 (for non-pensioners) represent a substantial under recovery of the amount for which Overton was required to make levies pursuant to Clause 5(b) of the Lease Memorandum. Had all expenses been brought to account in the Maintenance Fund, the weekly maintenance fees for an “H” type unit, after appropriate adjustment, for the year ended 30 June 1994, would have been in the vicinity of $120.00.

Mr Brasington’s deteriorating health

71 As at March 1994, Mr and Mrs Brasington had lived at 20 Sunny Crescent, Punchbowl (“the Punchbowl House”) for many years. However, by March 1994 Mr Brasington had begun to suffer blackouts, which were becoming more serious and more frequent. . They had been worsening over the previous six months. He was suffering the onset of dementia and had very high blood pressure, which was erratic and hard to control. His condition had been deteriorating such that, in March 1994, he spent about two weeks in Lidcombe Hospital, in relation to his dementia and his deteriorating condition.

72 After Mr Brasington came out of hospital in March 1994, it was difficult for Mrs Brasington to go out and leave him alone. A next-door neighbour would keep an eye on him. Mr Brasington was having difficulty in doing things around the home and Mrs Brasington was concerned about his condition. It became hard to do shopping, or gardening, because of the risk that he would black out. Mr Brasington’s son began coming to mow the lawns and give his parents some assistance.

73 By March 1994, Mr Brasington’s condition had been on Mrs Brasington’s mind for some time and, partly by reason of it, Mrs Brasington had been considering alternative accommodation to the Punchbowl House for some time. She had already booked at another retirement village, waiting for a vacancy to come up .

introduction to the heritage village

74 During March 1994, Mrs Brasington’s grandson, Peter Conroy, the son of her daughter, Patricia Conroy (“Patricia”), telephoned her and told her that there was a unit vacant at the Heritage Village and that it was for sale at around $175,000. Peter Conroy’s wife, Veronica Conroy, is the daughter of Mr John A. Merton (“Mr Merton”), who was a real estate agent with Sanders Hurstville Real Estate Pty Ltd (“Sanders”), which carries on the business of a real estate agent under the name “Sanders Commercial First National”. Sanders acted in some capacity as a real estate agent in connection with the Heritage Village and Veronica Conroy worked with Sanders in some capacity.

75 Mrs Burton was in Queensland from 17 March 1994 to 24 March 1994. While Mrs Burton was in Queensland at that time, Mrs Brasington spoke to her by telephone and told her that there was a unit available at the Heritage Village for $175,000. Mrs Brasington told her that it was going to cost $60 a week that she would have to sell her house to cover the cost of the unit and “that $60 a week was going to cover all the costs, the costs that she wouldn’t have at Punchbowl any more like maintaining the property”.. She said that “the only bills that she would be up for would be electricity, phone and contents insurance” and that She said that “even electricity and contents insurance would be a lower rate at the Heritage [Village] because it was a small place to look after”.

76 Mrs Burton words to the effect that “It sounds alright” and that the price sounded reasonable. She advised Mrs Brasington to speak to Patricia about it. Mrs Burton said that she would do a summing up of what it was costing Mrs Brasington to remain in the Punchbowl House and would compare that cost with what it would cost Mrs Brasington to move to the Heritage Village. Mrs Burton said “I’ll do my sums on it to see if you can afford the $60 a week on the pension”.

77 Mrs Burton said that, while she was in Queensland, she had a second conversation with her mother. She told her that if she could get enough money for the Punchbowl House to cover the cost of a unit in the Heritage Village she could afford the $60 a week on the pension. She said that she asked her Mother whether she was going ahead with it and that her Mother responded “Yes, I want to go ahead with it”. Mrs Burton said “Yes well, its affordable for you”. Mrs Brasington then said that she would put a “holding deposit on”.

78 Mrs Brasington said that, after her conversation with Mrs Burton, she visited the Heritage Village where she met with Veronica Conroy. On that occasion, Veronica Conroy gave Mrs Brasington the Booklet. Mrs Conroy told Mrs Brasington that the price for the proposed unit was $175,000 and that the maintenance would be $60 a week. Mrs Conroy told Mrs Brasington that “everything would be covered by the maintenance except three things, which was the electricity, the phone and the contents insurance”. Mrs Conroy said that everything would be there that Mrs Brasington needed including “the Vitalcall, the swimming pool, the dining room” if she needed it. Mrs Brasington said to Veronica Conroy “it sounds as though I could probably afford it on my pension and possibly could sell my house to pay for the unit without dipping into any other money”. Mrs Brasington told Mrs Conroy that she would sell the Punchbowl House and that she thought she would be able to get enough to buy into the Heritage Village.

79 Mrs Brasington said that she took the Booklet home and “read it and read it”. She said that the things that she recalls that she read were the statements on pages 6 and 7, the precise terms of which are set out in the Appendix to these Reasons. She says that she particularly recalled having read the reference to $59 and all the things that that covered “except the three things that I have already said”.

80 Mrs Brasington visited the Heritage Village again with Mrs Burton after Mrs Burton returned from Queensland. They looked over the Heritage Village, including the dining room and the swimming pool. They then went back to Mrs Brasington’s house at Punchbowl. Mrs Brasington gave Mrs Burton the Booklet. Mrs Burton sat down and read the Booklet in the lounge room and then they talked about it. Mrs Burton said “It sounds good” and Mrs Brasington said that she thought that it was “alright”.

81 Ms Burton recalls that the Booklet contained the information set out below:

· services and facilities, including transport, shopping, recreation, the village bus;

· the pensioner rate of $60 per week mentioned on page 7;

· the ongoing management and maintenance program mentioned at page 6;

· the replacement program at page 6;

· the maintenance fee of $60 per week mentioned on page 7, which covered insurance, land tax, water rates, everything within the weekly maintenance;

· the replacement program covered the interior painting and common carpets, and “all the rest”.

82 Mrs Burton told Mrs Brasington that she had done the sums on what it was going to cost Mrs Brasington to remain in the Punchbowl House compared with what it was going to cost her at the Heritage Village and that “it was very good, really”. Mrs Burton told her mother that the Heritage Village was much better than “staying at Punchbowl”. Mrs Burton told Mrs Brasington that if she stayed at the Punchbowl House she would have to bear the cost of the upkeep of painting the house inside and out, the repairs of a house that was over fifty years old and a garage that was deteriorating badly. She also said that the lawns would have to be mown and referred to the fact that Mr Brasington was too sick to do that and that Mrs Brasington was unable to do it because it was “a very big block of land”. Mrs Burton told her mother that she could afford the unit in the Heritage Village provided she could sell the Punchbowl House for a price that would cover the cost of the unit. She said that, at $60 a week, it was affordable for her.

83 On 19 March 1994, Mr and Mrs Brasington signed an exclusive agency agreement in favour of Sanders, granting exclusive selling rights in respect of the Punchbowl House for the period from 19 March 1994 to 17 July 1994. On 22 March 1994, Mr and Mrs Brasington signed a form of application for lease (“the Application”).

84 The Application was addressed to Overton and was in the form specified in the First Schedule to the Trust Deed. By the Application, Mr and Mrs Brasington applied for a lease, as defined in the Trust Deed, for “Self Contained Unit No. 65 (Stage 4A)”. The Application specified a Lease Price of $175,000. The Application also provided as follows:

“We agree to be bound by the provisions of the Trust Deed and the Lease…and to tender a cheque for the Application Monies payable to the Trustee”.

85 In the space in the Application for “Application Monies Payable” the sum of $1,000 was inserted. On the following day, Overton issued a receipt to Mr and Mrs Brasington for the sum of $1,000, which was expressed to be for “Holding Deposit for Unit 65, the Heritage Retirement Village”.

86 At the foot of the Application the following note appears:

“NOTE: The Applicant(s) has fourteen (14) days from the date of lodgement of this application within which to advise the Manager in writing that he no longer wishes to lease the Unit. In such an event Application Monies received by the Manager or Trustee will be refunded.”

87 Thus, on its face the Application constitutes a binding agreement for the grant and acceptance of a lease, subject to the right of Mr and Mrs Brasington to withdraw within fourteen days.

88 Shortly after Mrs Burton had read through the Booklet with her mother, at a time when her mother still had time to “back out” of the acquisition of Unit 65 if she wanted to, Patricia spoke to Mrs Burton about a possible increase in outgoings at the Heritage Village. Patricia said to Mrs Burton words to the effect “I’m a bit concerned, I’ve just heard there’s going to be a $5 increase in the maintenance, what do you think I should do?”. Mrs Burton said to Patricia “well you’re going to have to mention it to Mum to see how she feels about it”.

89 Several days after paying the sum of $1,000 to Overton, Mrs Brasington had a conversation with Patricia, who said that the outgoings at the Heritage Village “possibly would go up about $5”. She asked her mother whether she thought she would be able to afford that. Mrs Brasington replied: “Well I think so, seeing as I’ve gone this far. I don’t think that will change anything”.

90 At about the same time, Mrs Brasington had a further conversation with Veronica Conroy, who told her that the maintenance was going to go up, “probably about $5 or $6 which was about the CPI”. Veronica Conroy asked whether that was going to make any difference to Mrs Brasington, who replied that she thought that would “be alright…I’ve gone this far. I might as well go on with it”. Veronica Conroy also said that the maintenance “probably would go up that amount from time to time”.

the grant of the lease

91 Mrs Brasington retained Mr Hume of Gould Shaw & Hume, Solicitors, to act in connection with the sale of the Punchbowl House, and in respect of the acquisition of a leasehold of Unit 65.

92 Under cover of letter dated 25 March 1994, signed by Veronica Conroy, Sanders sent to Messrs Gould, Shaw & Hume, the solicitors for Mr and Mrs Brasington, a copy of the Lease “so you may familiarise yourself with it”, as the letter said. On 29 March 1994, Veronica Conroy sent to Mr and Mrs Brasington a copy of a location floor plan, which showed significant dimensions of Unit 65, together with material entitled “Information regarding Heritage Retirement Village required to be given under Retirement Village Code of Practice” (“the Code of Practice Disclosure”).

93 The Code of Practice Disclosure contained information under the following headings:

(a) List of all Costs Payable by the Prospective Resident to enter the Village;

(b) List of all Periodical Charges or Fees Payable by Resident and method of determining any variation;

(c) A List Of Services provided for those Fees;

(d) A List of Any Additional or Optional Services and their Cost;

(e) Costs Associated with Moving From Self Care Units to Apartment Units;

(f) Detailed Budget;

(g) Schedule A to the Retirement Villages Code;

(h) Check List Under Schedule B to the Retirement Villages Code;

(i) Village Rules;

(j) Refund Entitlement;

(k) Requirements in Development Consent to Provide Services.

94 Under heading (b), the weekly cost in relation to “H” Type Units was shown as $59.00 (pensioner) and $64.08 (non-pensioner). Under that heading the following also appeared:

“It should be noted that these amounts are estimates only of the actual liability of the residents and an adjustment may be made at the end of each financial year if the contributions are found to be excessive or deficient.

These fees may be varied, in accordance with clause 5(b) of the Lease, by the management if the Management should arrive at a different estimate of the resident’s liability in respect of any particular period.”

95 Under heading (f), reference was made to “a detailed current budget for the Heritage Retirement Village” annexed as Schedule D. Schedule D is entitled “Heritage Retirement Village Forecast Operating Budget 12 Months 1/7/93 – 30/6/94”. Curiously, the figures in Schedule D are identical to those contained in the 1993 Budget, notwithstanding the terms of the 1994 Budget, which had been circulated to Lessees during March 1994.

96 On 5 April 1994, Mr Merton wrote to Mrs M. Sams, who was then the Lessee of Unit 65, saying:

“I confirm the sale of your unit at the Heritage Retirement Village, subject to the sale of Mr and Mrs Brasington’s house.

To arrange for the surrender of the Lease from Overton Investments Pty Ltd to you it is necessary for you to complete a surrender of Lease form. (copy enclosed herewith)

Please note that this request for Surrender does not become effective until such times as the Brasington’s [sic] execute a lease to Overton Investments Pty Ltd for your unit.”

97 On 20 April 1994 Gadens wrote to Gould Shaw & Hume enclosing a number of documents including:

· bound volume containing the floor plan and the Code of Practice Disclosure that had been sent to Mr and Mrs Brasington by Veronica Conroy under cover of the letter of 29 March 1994;

· the Lease in triplicate;

· copy of the Lease Memorandum.

98 Gadens Ridgeway requested Gould Shaw & Hume to have Mr and Mrs Brasington sign every page of the bound volume “as evidence that your client has received the information required to be disclosed under the Code of Practice”.

99 On 28 April 1994, Veronica Conroy wrote to Mr James saying that Mr and Mrs Brasington had “exchanged on their property” on 20 April 1994.

100 Mrs Brasington acknowledges that before 29 April 1994, she had received a copy of the Lease and had read all of clause 5 of the Lease Memorandum with particular care. She had spent some time reviewing the Lease before she saw Mr Hume because she knew it was important for her to understand the Lease, as it set out her legal rights and obligations upon entering the Heritage Village, and because it was important for her to understand the Lease in order to benefit from the conference with Mr Hume.

101 Before 29 April 1994, Mrs Brasington knew that her liability to contribute to outgoings in the Heritage Village was set out in the Lease Memorandum, and that the Lease Memorandum would define her legal rights and obligations upon entering the Heritage Village. She regarded it as important to obtain a legal instrument, such as the Lease Memorandum and the Trust Deed, which clearly spelt out her legal rights and obligations.

102 On 29 April 1994, Mrs Brasington saw her Mr Hume and conferred with him, for an hour and a quarter in respect to the Lease, the Lease Memorandum and the Trust Deed. Mr Hume explained a number of matters to Mrs Brasington about each of those instruments including, in particular in relation to the Lease Memorandum, clause 3 – “Term”, clause 4 – “Rent”, and clause 5 – “Contributions to Outgoings”. Mr Hume took Mrs Brasington through each of the sub-paragraphs, under the heading Contributions to Outgoings, of the Lease Memorandum. Mr Hume also signed a solicitor’s certificate that indicated that he had explained the contents and the effect of the Lease to Mr and Mrs Brasington and that, in his opinion, they appeared to be aware and appeared to understand their obligations under it

103 In particular, Mr Hume read clause 5(l) of the Lease Memorandum to Mrs Brasington. Mrs Brasington understood after her conference with Mr Hume that the amounts of $59 per week for a pensioner and $64.08 per week for a non-pensioner referred to in Item 6 of the Reference Schedule of the Lease constituted an estimate only, and were subject to determination and variation from time to time, in accordance with sub-clause 5(l) of the Lease Memorandum.

104 Mr Hume drew Mrs Brasington’s attention to the risks of having a bad manager at the Heritage Village, in the context of discussion about what a manager could recover from a resident. Following that discussion, Mrs Brasington knew that expenditure that was incurred in the operation of the Heritage Village and that had not been budgeted for could be recovered from the Lessees, including Mr and Mrs Brasington.

105 By the end of the conference with Mr Hume on 29 April 1994, Mrs Brasington had the clear belief that the provisions set out in clause 5 of the Lease Memorandum would govern what money she and Mr Brasington would have to pay by way of any contribution to outgoings as the term of the Lease went on and that the Lease Memorandum would govern her obligations in relation to outgoings for many years to come. It was Mrs Brasington’s actual belief that the entitlement she and Mr Brasington would enjoy and the obligations that she and Mr Brasington would have would be those entitlements and obligations set out in the Lease Memorandum and the Trust Deed.

106 After her conference with Mr Hume, Mrs Brasington knew that there was no limit on the amount of any variation that might be imposed pursuant to clause 5 of the Lease. She did not think for one minute that the figures in Item 6 of the reference Schedule would never be changed or that the weekly maintenance fee at the Heritage Village would be capped in any way. ^^

107 Mrs Brasington had a precise understanding that the maintenance fees might be varied by Overton provided Overton varied it them in accordance with clause 5 and nothing else. Mrs Brasington regarded it as important that Overton’s power to vary the maintenance fee would be the subject to the clearest possible legal restraints, which were set out in clause 5 that Overton would not have “open slather” to put in whatever it liked as a charge against herself and Mr Brasington for contributions to outgoings, that Overton was constrained by the provisions of the Lease Memorandum and the Trust Deed, and that they had obtained the protection provided by the Lease Memorandum and the Trust Deed, before she proceeded with the Lease.

Mrs Brasington said that she read the Lease before she and Mr Brasington signed it in Mr Hume’s office. She said that she recalled seeing the reference to $59 per week in item 6 of the Reference Schedule. She said that Mr Hume asked her whether she had “read this booklet” and she said that she had “read it and read it”. She said “I don’t know whether I fully understand it, but I have read it through several times”. Mrs Brasington said that the only problem that Mr Hume thought she could have was “If I got a bad manager in”. She responded “We think we've got a good manager, as far as we know”. She and Mr Brasington then signed the Lease.

108 On 3 May 1994, Gould Shaw & Hume wrote to Gadens Ridgeway returning one copy of the bound volume duly executed and the Lease in triplicate duly executed and requesting confirmation that all of Gadens Ridgeway’s requirements had been satisfied subject to payment of the Lease Price of $175,000.

109 Mr and Mrs Brasington moved into Unit 65 on 4 June 1994 and settlement of the grant of the Lease took place on 6 June 1994. On about 9 March, 1995 Mr Brasington moved into a nursing home at Berala and he died on 29 April 1995.

RELIANCE and inducement

110 There will be a question as to the extent, if any, to which Mr and Mrs Brasington placed reliance, in entering into the Lease, on the figures in the Booklet and in the unexecuted Lease. That question will be resolved by reference to the evidence given by Mrs Brasington as to her state of mind and by Mrs Burton as to her own state of mind, to the extent that Mrs Burton participated in the decision-making process on behalf of Mr and Mrs Brasington. It is also relevant to take account of the conduct of Mr and Mrs Brasington and Mrs Burton in relation to the documents and the process of considering and deciding to enter into the Lease.

111 Mr Brasington’s condition was an important matter, if not the primary matter, that Mrs Brasington took into account in making the decision to move to the Heritage Village. Another matter that Mrs Brasington took into account, in making a decision whether or not to sign the Lease, was that it would cost $60 per week, which she could manage out of her pension and which would cover everything in the Heritage Village other than electricity, telephone and contents insurance. A further matter that Mrs Brasington took into account was that the Lease would cost $175,000 and that, when she sold the Punchbowl House, she would have enough to cover the payment of that sum.

112 Mrs Brasington claimed in her evidence in chief that if, before she signed the Lease, she had been informed that there was going to be an eighteen per cent increase in the maintenance fees from 1 July 1994, she would never have signed the Lease. Mrs Burton also said that if she had been aware that there would be an eighteen per cent increase from 1 July 1994, that would have made a difference to the views that she expressed to her mother. She said that her mother would not have been able to afford her unit in the Heritage Village and that she “wouldn’t have let her go into it”. She said that “it was affordable on the pension but the pension doesn’t go up at that rate”.

113 I accept that, before she paid the holding deposit on 23 March 1994, Mrs Brasington had read all of the Booklet and understood that the Heritage Village was a resident funded retirement village. She was aware, from her reading of the Booklet, that the figures contained in it were current only to 9 June 1993, were to be taken as a guide only and were subject to change without notice. She had read and understood the statement in the Booklet that the information in the Booklet did not constitute any representation by Overton or by the agents and that if a reader had any further questions not covered in the notes the reader should contact Overton.

114 Mrs Brasington understood that the information in the Booklet had been out of date for some time and that it was necessary to obtain further information with respect to the current details. Having understood that to be the position, she took no steps to contact Overton directly to obtain any further information before paying the holding deposit.

115 It was perfectly plain to Mrs Brasington that Overton would vary the weekly maintenance fee from time to time from the figure mentioned in the Booklet. She did not believe that the only outgoings she would ever have to pay would be limited to the figure mentioned in the Booklet or that the outgoings would be limited to a particular dollar amount. It was her clearest understanding that her liability to contribute to outgoings would increase upon entering the Heritage Village.

116 After Patricia advised her about a possible increase in the weekly maintenance fee, Mrs Brasington knew that there was an increase proposed over and above the figures mentioned in the Booklet and that she would be liable for the increase. However, she took no steps to contact Overton about the increase. She made no inquiry as to the breakdown of the increase nor what the increase included. Further, Mrs Brasington understood that the reason for the increase over and above the figure of $59 mentioned in the Booklet was that additional expenditure had been incurred by the Heritage Village. She knew that there had been unexpected bills that had not been budgeted for in determining the figure of $59 and that there may be increases in the contribution to outgoings, which had not been budgeted for in the figures mentioned in the Booklet. Knowing that there had been expenses incurred by the Heritage Village that had not been budgeted within the figure contained in the Booklet, Mrs Brasington decided to proceed with the acquisition of Unit 65 in any event.

117 Mrs Burton said that there were a few matters that she relied upon in expressing the view to Mrs Brasington that the unit in the Heritage Village was “affordable”. She said that the matters included the affordability and the worrying concern for elderly people of the maintenance on the Punchbowl House, which was getting near 50 years old. She said that “the lifestyle at the Heritage was a real plus” and that “they could afford it if they could sell Punchbowl at a price that would cover the Unit, which they did”. She said that $60 in maintenance fees was affordable on the pension as they had fewer bills at the Heritage Village and the Punchbowl House was coming up to want its gardens and lawns done as Mr Brasington’s health was deteriorating. She said that she relied on the fact that at the Heritage Village “had the Vitalcall and the care nurse available”. She also referred to the fact that there was a pool and spa and that the maintenance covered all “their repairs and maintenance and the only bills they had to worry about was the phone and the electricity and the contents insurance”. She said that “they looked like being set there for life when they’d made this move”.

118 I accept that the level of weekly maintenance fees was a factor that Mr and Mrs Brasington took into account in their decision to sign the Lease. Mrs Brasington, in effect, made the decision for both of them and the state of her mind and that of her daughter, Mrs Burton, are the relevant states of mind. However, whether maintenance fees in the vicinity of $120 per week would have caused Mrs Brasington to decline to execute the Lease is by no means clear.

119 Mr and Mrs Brasington were entitled to receive the age pension as at March 1994. As from 20 March 1994, as a married couple, Mr and Mrs Brasington were entitled to receive a maximum pension totalling $265.30 per week, depending upon whether they had other income or assets. At that time, the single pension entitlement was $159.00 per week. However there was no evidence before me of the financial position of Mr and Mrs Brasington at that time.

120 Whether the weekly pension for a single pensioner was such that Mrs Brasington could have met the weekly maintenance fees, together with the costs of electricity, telephone and contents insurance from the single age pension is, on the present state of the evidence, a matter for speculation. Despite the evidence of Mrs Burton, that she made calculations on behalf of Mrs Brasington to determine whether or not she could afford the weekly maintenance fees, no evidence was adduced as to the quantum of the likely expenses. In circumstances where Mrs Brasington gave evidence, as did her daughter, Mrs Burton, I do not consider that it is appropriate to draw inferences in Mrs Brasington’s favour as to matters that were within their direct knowledge but about which they gave no evidence.

121 I do not propose to make a final ruling on whether, and, if so, the extent to which, Mr and Mrs Brasington were induced to enter into the Lease by reason of the figures contained in the Booklet and the unexecuted Lease. I consider that is best left until all the evidence is complete.

EVENTS FOLLOWING GRANT OF THE LEASE

122 On 1 July 1994, Overton wrote to Mr and Mrs Brasington (and to all other Lessees) referring to a meeting of the Lessees’ Advisory Committee held on 28 April 1994 and saying:

“whilst not agreeing to the budget for the period commencing July 1st, 1993 and ending June 30th, 1994, [the Advisory Committee] resolved to accept the following actions by [Overton] in relation to the levying of contributions to outgoings, also referred to by some as maintenance fees, for the [Heritage Village]”.

123 The action set out in the letter of 1 July 1994 included the following:

· Effective 1 July 1994 the levy of contributions to outgoings will be increased by approximately 18.37 per cent.

· Effective 1 July 1994 the contribution rate previously known as a “pensioner rate” will be discontinued.

· Commencing from 1 July 1994 the contribution rate will be standardised and the same contribution rate will be invoiced to Lessees occupying the same unit type.

· Effective 1 July 1994 all expenses and revenues associated with the provision of user-pays and flexi-care services will be withdrawn from the administration of the outgoings contribution account. As at this date these expenses and revenues will be integrated into the operation of the Manager.

· Effective 18 July 1994 rates for user-pays and flexi-care services will increase.

· Effective 1 July 1994 and until further notice, whilst the Manager will provide a detailed budget for each financial year, the Manager hereby notifies the Lessees that the rates for contributions to outgoings and the provision of user-pays, flexi-care services will be reviewed and adjusted, as necessary, on a quarterly basis.

124 After receipt from Overton of the letter of 1 July 1994, Mrs Brasington understood that rates of contributions to outgoings would be examined from that time and adjusted upward or downward as would be required by the actual expenditure incurred, that that would occur every three months instead of annually, that any shortfalls or excesses in contributions would be identified and adjusted every three months instead of annually and that if there were large adjustments to be made then Overton would recover those adjustments from the Lessees.

125 Following receipt of that letter, Mrs Brasington knew that, subject to the Lease Memorandum and the Trust Deed, Overton would seek to recover from the Lessees whatever expenditure was incurred in relation to the Heritage Village, that the expenditure would continue to increase in accordance with whatever expenditure was incurred and that, other than what was set out in the Lease and the Trust Deed, there was no limit or cap on the expenditure that Overton could seek to recover from the Lessees. She understood that such expenditure was not limited by CPI or anything else.

126 Mrs Brasington says that, she took no steps to surrender the Lease following receipt of that letter because “I couldn’t afford to”. She says that she “had nowhere else to go. My house, my place, was sold and I had a very sick husband and I wanted to get into this unit as quickly as I could”. She said that, following the increase with effect from 1 July 1994, it was her belief that any further increases “would be CPI, round about the same amount”. She said that she believed that because of what Veronica Conroy had said to her. Mrs Brasington says that the sum of $75.85, that she was required to pay each week from 1 July 1994, covered everything but the three things that she had mentioned “the light, the phone and the contents insurance”.

127 Mrs Brasington decided to act on the advice of The Accommodation Rights Service (“TARS”) with respect to the dispute with Overton that emerged after the letter of 1 July 1994. In conjunction with the other Lessees, she decided that she would take action against Overton in relation to the Code of Practice.

128 Following her attendance at a meeting of Lessees on 13 September 1994, Mrs Brasington had the clearest understanding that Overton would seek to recover from Lessees whatever expenditure was incurred on the operation of the Village, that she would be called upon to meet increases in weekly maintenance fees and, subject to the Lease Memorandum and the Trust Deed, that there was no limit or cap on the expenditure that could be recovered from the Lessees.

129 Following receipt of a letter from TARS dated 21 October 1994, Mrs Brasington knew that Overton had put forward a proposal for a substantial fee increase for the year ending 30 June 1995. At that time, she had no doubt in her mind that Overton was intending to recover the operating loss for the year ended 30 June 1994, and any deficit for the year ended 30 June 1995, if the recommended increase in maintenance fees was not agreed to by the Lessees. She knew that Overton would seek to recover from the Lessees any expenditure incurred in respect to the Heritage Village, regardless of whether that expenditure had been included in a budget.