FEDERAL COURT OF AUSTRALIA

Harts Australia Limited v Commissioner, Australian Federal Police

[2002] FCA 245

ADMINISTRATIVE LAW – search warrants – judicial review of seizure decisions made in execution of search warrants – scope of power to seize under s 3F(1)(c) Crimes Act 1914 (Cth) – challenge to validity of seizure in its entirety on grounds of systematic failure by executing officers to determine whether seized items fell within the terms/conditions of the particular warrant – warrants issued pursuant to an investigation into suspected tax frauds – seizure of paper and electronic documents – return of all material seized sought

ADMINISTRATIVE LAW – search warrants – warrant in connection with complex criminal investigation – public interest considerations – whether search and seizure was conducted reasonably within the bounds of the warrant – whether executing officers had reasonable grounds for suspecting that the document seized would afford evidence as to the commission of one or more of the offences listed in the warrant – relevance of size of proportion of material seized that is outside the warrant – sufficiency of information given to executing officers in relation to warrant conditions

ADMINISTRATIVE LAW – search warrants – seizure of electronic material – scope of power under s 3L(2)(a) Crimes Act 1914 (Cth) to seize equipment that contains “evidential material” together with a mass of non-evidential material – scope of power under s 3L(2)(c)(i) to copy material stored electronically on equipment which comprises in part of “evidential material” and remove that electronic copy from warrant premises – whether it was not practicable to examine or process electronic information stored at the warrant premises pursuant to s 3K(2) – the time allowed to the seizing party to examine and process information in electronic form removed from the warrant premises – whether judicial review should be refused on discretionary grounds if removal of material satisfies the conditions under s 3K but seizure under s 3F is not justified

WORDS AND PHRASES - “suspicion”, “evidential material”, “things”, “process”, “examine”

Administrative Decisions (Judicial Review) Act 1977 (Cth) s 5

Crimes Act 1914 (Cth) ss 3F(1)(c), 3L(1), 3L(2), 3L(3), 3K(1), 3K(2), 3K(3), 3N(1)(a)

Harts Australia Ltd v Commissioner, Australian Federal Police [2001] FCA 175 referred to

Friends of Hinchinbrook Society Inc v Minister for Environment (No 2) (1996) 69 FCR 28 at 77 followed

George v Rockett (1990) 170 CLR 104 considered

Parker v Churchill (1985) 9 FCR 316 cited

Crowley v Murphy (1981) 52 FLR 123 discussed

Dunesky v Commonwealth of Australia (1996) 89 A Crim R 372 discussed

Baker v Campbell (1983) 153 CLR 52 at 83 discussed

Bartlett v Weir (1994) 72 A Crim R 511 at 520 considered

Arno v Forsyth (1986) 65 ALR 125 at 139 considered

Inland Revenue Commissioners v Rossminster Ltd [1980] AC 952 considered

Propend Finance Pty Ltd v Commissioner of Australian Federal Police (1995) 58 FCR 224 considered

Coghill v McDermott [1983] VR751 distinguished

Tran Nominees Pty Ltd v Scheffler (1986) 20 A Crim R 287 at 294 followed

BTR Plc v Westinghouse Brake & Signal Co (Australia) Ltd (1992) 106 ALR 35 considered

Lockwood v The Commonwealth (1954) 90 CLR 177 at 184 cited

Mercantile Mutual Life Insurance Co v Australian Securities Commission (1993) 40 FCR 409 at 412 discussed

Review Committee (Chair: Sir Harry Gibbs) Review of Commonwealth Criminal Law Fourth Interim Report, AGPS, Canberra, 1990 at 303-6 considered

HARTS AUSTRALIA LIMITED (ACN 010 765 394), HARTS PTY LIMITED (ACN 010 093 663) AND STEVEN IRVINE HART, ROBERT THOMAS ADCOCK AND ASTION PTY LIMITED v THE COMMISSIONER, AUSTRALIAN FEDERAL POLICE, MICHAEL JOHN MORRIS, WILLIAM JOSEPH McKAY AND HENRY ALBIEZ, I. BARTLEY, DENICE BIRD, JOHN BROWN, MICHAEL BUTCHER, IVOR CHALMERS, RON C. CRAMP, PAUL DELANY, GEOFF P. EYLES, ARTHUR FADDEN, ALAN FARNELL, ANTHONY FITZSIMON, ROBERT G. GLOVER, JOHN HOPKINS, IAN HOUGHTON, MARK JAGER, STEVEN JAY, CAMERON JEFFS, GEOFF JENSEN, MARIE McCARTHY, MALCOLM McKAY, JOE MANRICKS, METCALFE, ROBERT PENNICOTT, ALLAN PERRY, CRAIG PHILP, PETER ROBERTS, PAUL SHANLEY, G. SWANSON, ALEX TEA, NEIL THOMPSON, WILLIAM VICKERS, G. WALSH, TREVOR WENZEL, BETH WILLIAMS AND IAIN YOUNG

QG 162 OF 1996

DRUMMOND J

13 MARCH 2002

BRISBANE

| IN THE FEDERAL COURT OF AUSTRALIA |

|

| QG 162 OF 1996 |

| JUDGE: | |

| DATE: | |

| PLACE: |

REASONS FOR JUDGMENT

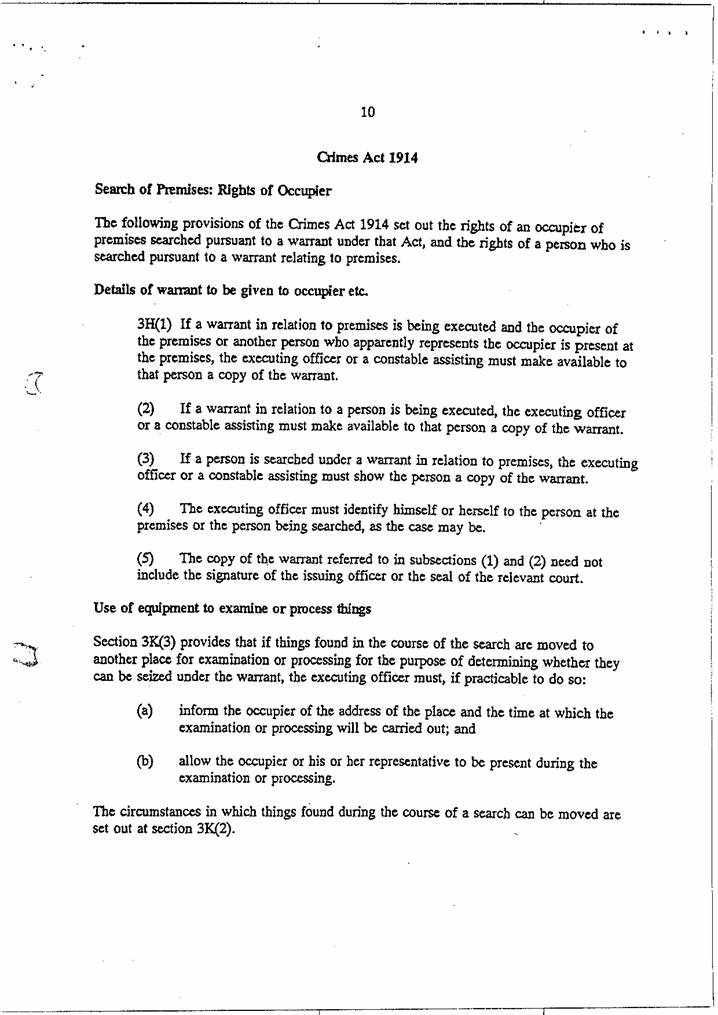

1 In this action, the applicants contend that a very large volume of documents in hard copy and electronic form taken by officers of the Australian Federal Police (“the AFP”) and the Australian Taxation Office (“the ATO”) in reliance on a number of search warrants, were unlawfully seized. By their amended application, the applicants seek review under the Administrative Decisions (Judicial Review) Act 1977 (Cth) (“the ADJR Act”) of “the decisions and/or conduct of the fourth respondents in the course of executing the warrant issued by the third respondent, whereby the fourth respondents [ie, all of the executing officers able to be served] made decisions to, and seized, things whose seizure was unauthorised by the terms of the said Warrant”. Return of all the material taken is sought.

2 Though the amended application, in terms, challenges both decisions to seize and conduct constituted by the seizure of material, review is, I think, available only under s 5 of the ADJR Act. Section 6 permits review of conduct, but only if it is conduct anterior to the making of a reviewable decision. The concept of “a decision” within s 5, however, embraces both the mental process involved in determining to take action and the manifestation of that mental process by the taking of the action in all the activities now challenged. See Salerno v National Crime Authority (1997) 144 ALR 709 at 713 - 714.

3 One of the first applicants, Harts Australia Limited, is the holding company of the companies which comprise the “Harts group”. The other first applicant, Harts Pty Limited, carried on an accounting practice at 240 Margaret Street, Brisbane and at other places in Queensland. The second applicants, Mr Steven Hart and Mr Robert Adcock, are directors of Harts Australia Limited and of Astion Pty Limited (“Astion”), the other second applicant. The applicants’ business included the provision of accounting and tax advisory services. I was told by senior counsel for the applicants at the commencement of the hearing that, after initiation of the proceedings, Mr Adcock became bankrupt and that the proceedings, in so far as they were instituted by him, “are taken to be stayed in the circumstances by s 60 of the Bankruptcy Act”. Whether or not s 60 so operates, I am not asked to make any orders in favour of him in these proceedings now.

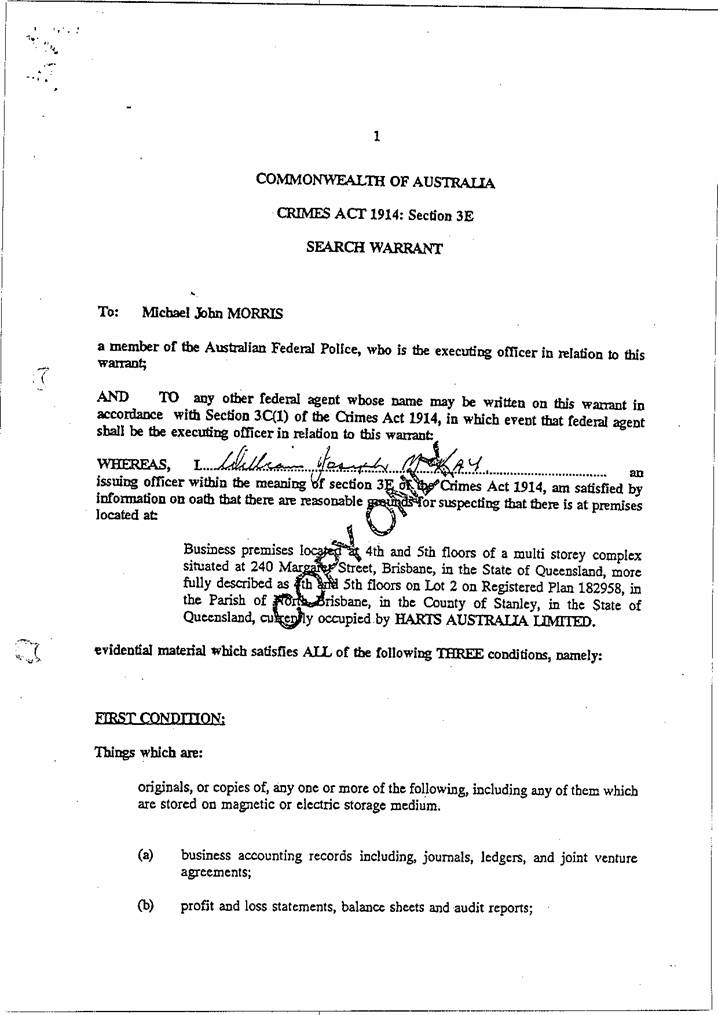

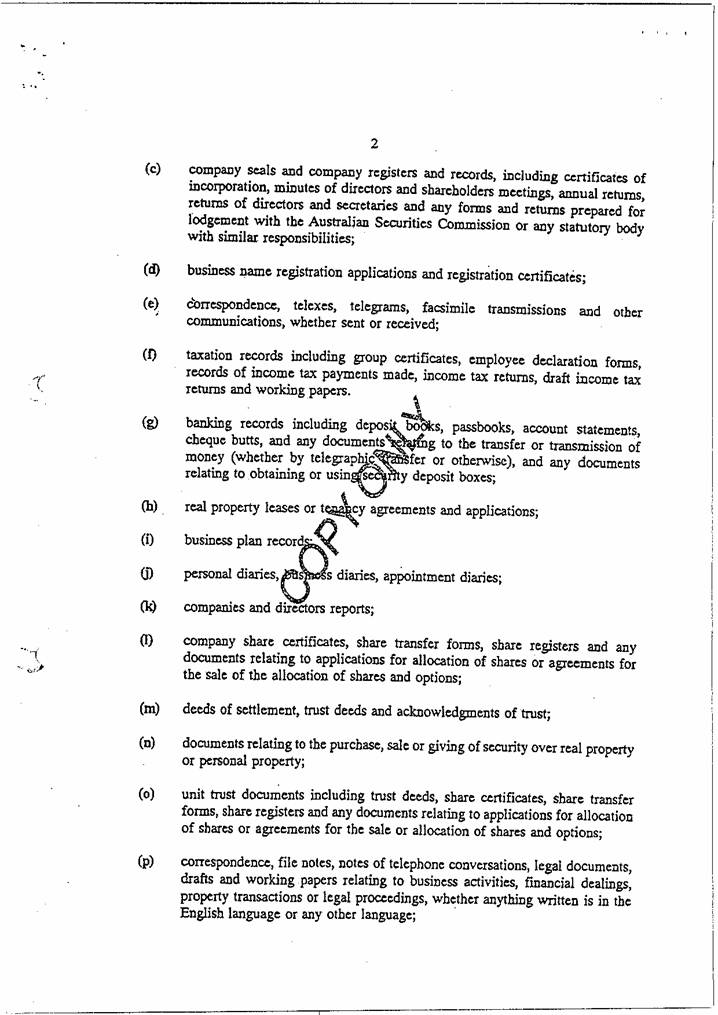

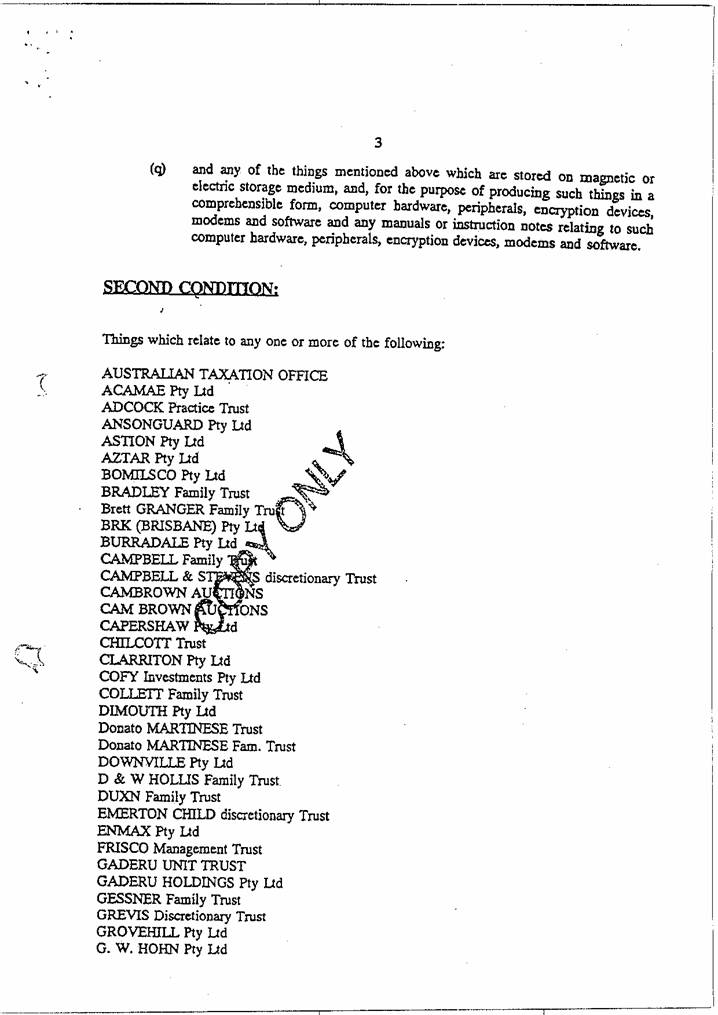

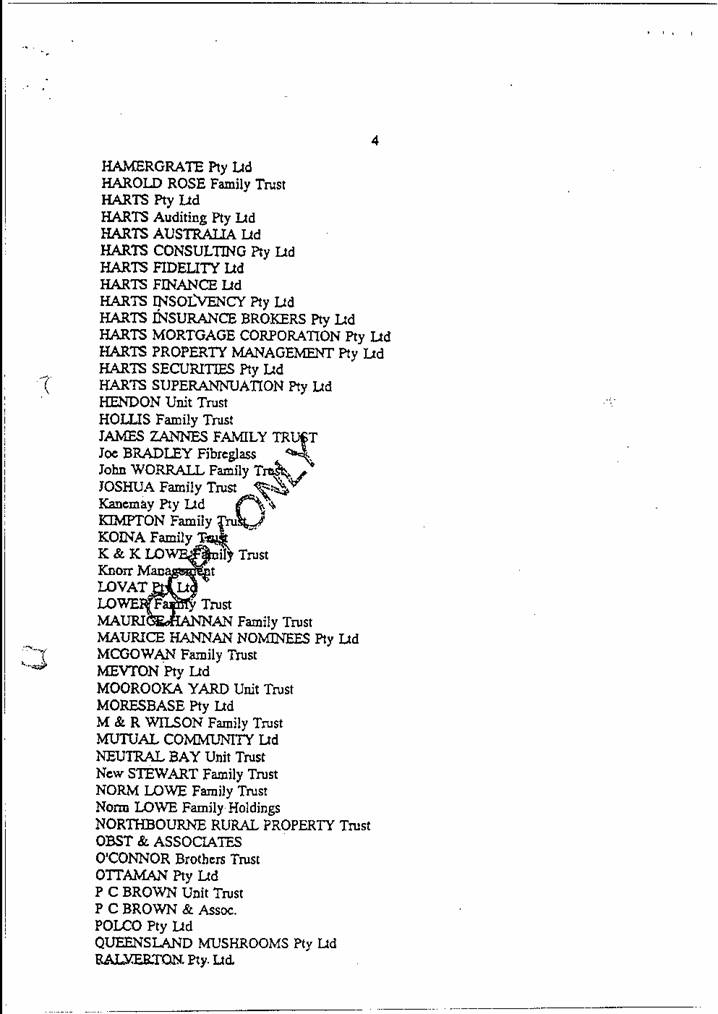

4 A number of warrants in similar form were issued on or about 6 September 1996, authorising the search for documents at a number of premises in south east Queensland. A typical warrant is annexed to these reasons. The warrants were issued in aid of an investigation by the AFP at the behest of the ATO into a range of suspected offences under the Crimes Act 1914 (Cth) (“the Crimes Act”) involving tax avoidance engaged in by the applicants with certain of their clients. They were executed on 9 and 10 September 1996. The major site targeted was the head office of the applicants at 240 Margaret Street. A large number of the documents were taken from there and from the other office premises of the first applicants at Sunnybank and Toowoomba. A smaller, though still large overall, volume of documents were seized at the residences of Messrs Hart and Adcock, from the home of Mr Stevens, Company Secretary of Harts Australia Limited, and from the offices and residences of certain clients of the first applicants. In addition, a very large amount of material in electronic form was taken from some of these premises, either by copying it to AFP tapes or by removing tapes and disks found at the premises; three personal computers were also removed, all of the information stored in them was copied at the AFP’s office and the computers were then returned to their owners.

5 One thousand, one hundred and sixty-seven (1,167) “items” separately recorded in the AFP seizure records were taken. In the cataloguing exercise later referred to, the hard copy component of these 1,167 “items” were broken down into 9,156 “documents”. In all, 97,116 separate pages of material in hard copy form were seized. An AFP officer, Federal Agent Negus, estimated that the electronic material is equivalent to about 260,000 A4 size pages.

6 The applicants’ challenge to the formal validity of the warrants, dealt with as a separate question, failed: see Harts Australia Ltd v Commissioner, Australian Federal Police (1996) 141 ALR 493 (“Harts v AFP (1996)”), on appeal, (1997) 75 FCR 145. The subsequent history of the litigation is set out in Harts Australia Ltd v Commissioner, Australian Federal Police [2001] FCA 175 (“Harts v AFP (2001)”).

7 In terms, the amended application seeks judicial review of each of the many decisions to seize documents. For long, the applicants intended to challenge by this means the lawfulness of the taking of every one of the many thousands of documents by examining the conduct of the officer in question when he or she decided to take each document. The ADJR Act permits such a challenge: see Harts v AFP (2001) at pars [20] to [27]; Williams v Keelty [2001] FCA 1301 at par [41] and Cabal v Attorney-General of the Commonwealth [2001] FCA 583 at pars [79] and [80] and cf Parker v Churchill (1986) 65 ALR 107 at 109 - 110 and 122 - 123. In March 2001, I recorded (in Harts v AFP (2001) at par [10]) the different approach the applicants then decided to adopt to make out their challenge to the taking of the entirety of the documents seized, saying:

“In the course of further argument, applicants’ counsel said that the applicants wanted to show that each of the assisting constables made their seizure decisions with respect to each document he or she seized without knowing whether the particular document came within the warrant, ie, without having held at the time of seizure the requisite belief. But, in explaining how the applicants intended to make out this case, counsel also said in effect that it would be unnecessary for the Court to examine every one of the many documents seized, because it was the applicants’ intention to demonstrate the correctness of its contentions by reference to some only of the documents taken as evidencing the way each of the sixty-six assisting officers went about making the decisions to seize and as showing in an over-arching way that they were all involved in an indiscriminate or “negative search” process in determining what documents to seize when they purported to assist in executing the warrant. Senior counsel acknowledged this as a late change in direction, though one “for the better” in that it involved a departure from investigating the lawfulness of the seizure of each document on a document by document basis. Counsel also agreed that, by his submissions, the applicants had articulated for the first time a basis for challenging the execution of the warrant which may be sustainable and which does not involve the Court having to make a document by document evaluation.”

8 When the applicants here contended that execution of the various warrants involved an indiscriminate or negative search, I understand them to mean that no genuine attempt was made by the executing officers to determine whether the things seized fell within the terms of the relevant warrant and, in particular, within condition 3.

9 The applicants now seek to show that the whole operation involving the execution of all the warrants is fundamentally flawed because the executing officers and the AFP and ATO officers assisting them can be seen to have had no regard to condition 3 of each of the warrants in determining to seize the many items taken. Such a failure, if established, will constitute reviewable error within s 5(1)(e) the ADJR Act by reason of s 5(2)(b). In their amended application, the applicants set up a number of other bases for alleging that all the warrant execution decisions involved improper exercises, within s 5(1)(e) the ADJR Act, of the power conferred by s 3F(1)(c) the Crimes Act on the executing officers. But the only factual basis relied on was the systemic failure already referred to.

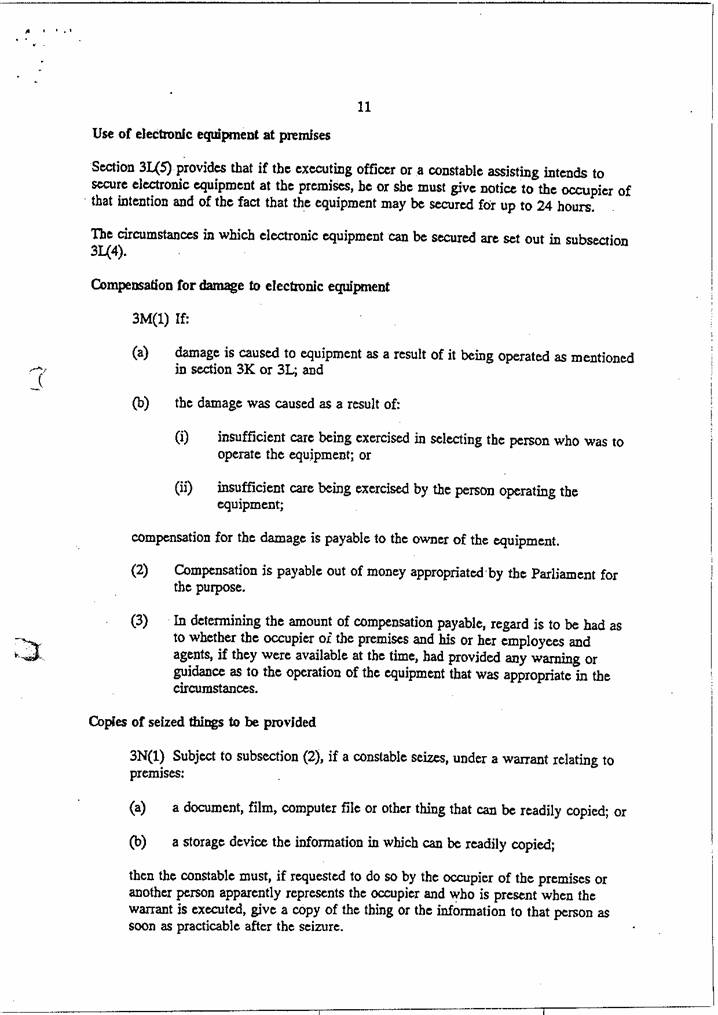

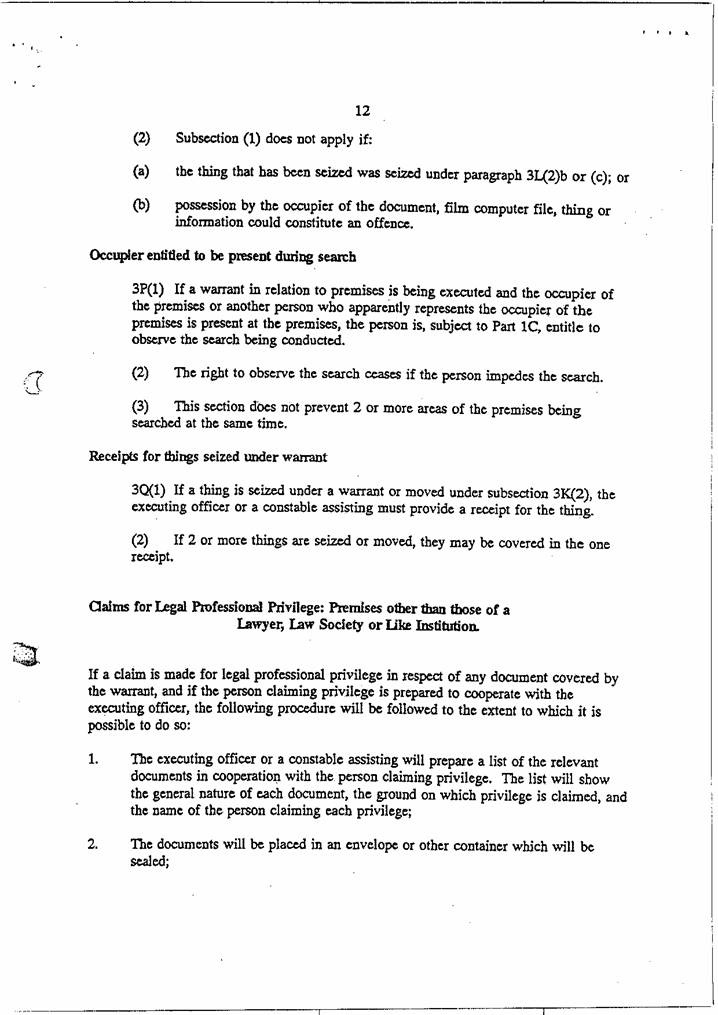

10 It was submitted that this failure, said to invalidate seizure of the whole of the material taken, resulted from a combination of the wide terms of the warrants, the poor briefings given to those involved in their execution and the vagueness of the information available to those responsible for procuring and executing the warrants about the offences listed in condition 3 of each. These matters are said to have left those involved in the execution of the warrants in the position of not being able to know what kind of events or transactions referred to in the documents held at the various premises were likely to be relevant to proof of the commission of those offences. This systemic failure is also said to be strongly evidenced by the wide range of materials seized and by the large volume of material taken in an impossibly short period of time, if considered judgments as to whether documents were within the relevant warrant were to be made. The applicants also rely on the result of the cataloguing exercise conducted in compliance with directions given by the Court (described at pars 146 to 152): a large number of documents were returned by the AFP to the applicants as admittedly not within the warrants, while the applicants have been prepared to concede that only a small number of documents were within the warrants. It is further said, with reference to the material taken in electronic form, that those involved in the execution of the warrants lacked an understanding of the authority conferred on them by ss 3L and 3K the Crimes Act, with the result that the very large volume of electronically stored information was also wrongly taken.

11 In the course of dealing with the new provisions of the Crimes Act governing search warrants in the initial episode of this litigation, I said (in Harts v AFP (1996) at 504) that it is not the warrant which authorises the executing officer to seize material, but rather s 3F(1)(c) the Crimes Act, a statutory authority that is triggered by the issue of the warrant. Once a valid warrant issues, this provision empowers the executing officer to search for and seize “the kinds of evidential material” specified in the warrant. What constitutes “evidential material” is defined in s 3C(1), read with the definition of “thing relevant to an indictable offence” in s 3. The magistrate who issued each of the warrants here in question defined this material by reference to the three conditions set out in each of the warrants: it had to answer the first condition by being information in the form of one or other of the categories of material in paragraphs (a) to (q) of that condition; it had to answer the second condition by being information relating to any one or more of the many persons or organisations listed therein; finally, it had to answer the third condition by being material “as to which there are reasonable grounds for suspecting that they will afford evidence as to the commission of” one or other of the four broadly worded offences listed in the third condition. This last condition thus confines each warrant to “evidential material” as defined in the Crimes Act.

12 All parties acknowledged that each of the warrants justified seizure only if the executing officer formed for himself or herself, in relation to each document taken, the opinion that there were reasonable grounds for the executing officer to suspect that the document would afford evidence as to the commission of one or more of the offences listed in the third condition of the warrant. That required the officer to have an actual suspicion as to each document seized that it was within the warrant and for there to be reasonable grounds for that state of mind.

13 Even if a court, in proceedings limited to judicial review of seizure decisions made under s 3F(1)(c) in reliance on a search warrant, could be required to do so, it is not for this Court to make findings, in relation to each of the very many documents seized by the fourth respondents, on the two issues as to the actual existence of the suspicion and as to it being, in truth, reasonably grounded. In view of the way the applicants have decided to fight the case, the question for determination is whether the matters of evidence referred to above upon which the applicants rely are sufficient to show that, despite what each officer who was asked said about taking into account the third condition of the warrant, none could, in truth, have done that when deciding to seize the material each took.

14 The documents were taken by teams consisting of AFP and ATO officers. The ATO officers who participated in the execution of the warrants stated, whenever asked, that their role was limited to locating possibly relevant documents which they took to the designated AFP officers who made the decision whether they should be seized. AFP Officers Roberts and Cramp said they made decisions to seize documents located by others and presented to them for evaluation. But, apart from that, the evidence suggests that no AFP officer, presented with a document by an ATO officer, turned his or her mind to whether the document should be seized. Instead, it appears that each AFP officer in that situation simply accepted the document presented to him by the ATO officer, generally already enveloped and labelled by the latter, as one within the relevant warrant and accordingly logged it as such in the AFP seizure record.

15 Little turns on a precise identification of the role performed by each ATO officer. The applicants did not seek to obtain any support for their challenge to the execution of the warrants from whether ATO officers formally seized documents or only located them for others to seize. All were expressly made “constables assisting” within s 3F by the relevant warrant holders for the purpose of the warrant exercise. Each was as much entitled as designated AFP warrant holders, by force of s 3F(1)(c), to seize material. The evidence of the ATO officers who were questioned about the matter was generally to the effect that they only took documents to the AFP officers which they thought were within the relevant warrant. Whether or not any ATO officer formally seized material, the question of present importance is whether, in taking material or in selecting material for the AFP to consider, the ATO officers can all be seen to have failed to consider condition 3 of the relevant warrant.

16 Each of the AFP and ATO officers involved in the execution of the warrants who was asked about the matter said they did have regard to condition 3 of the relevant warrant in determining whether to take each of the documents they seized. But, in determining whether such a decision is flawed with reviewable error because the decision-maker failed to take into account a relevant consideration, such as a condition of the warrant, “the reasons given by the decision-maker are not necessarily conclusive of all the factors taken into account in making a decision”: see Friends of Hinchinbrook Society Inc v Minister for Environment (No 2) (1996) 69 FCR 28 at 77 per Sackville J. His Honour cited for this proposition the dictum of Toohey J in Turner v Minister for Immigration and Ethnic Affairs (1981) 55 FLR 180 at 184:

“In many cases it will be clear whether or not the decision maker has taken a relevant consideration into account. That is not to say that the mere assertion by the decision-maker that he has done so will conclude the matter. It may be possible to demonstrate from a consideration of all the reasons leading to the decision, or indeed from the decision itself, that a consideration has not been taken into account in any real sense.”

17 I have set out above the matters relied on by the applicants to make good their contention that, despite what the AFP and ATO officers said, condition 3 of the warrants was universally ignored.

18 Though the Court is not concerned to determine whether any particular seizure was, in fact, justified by the warrant, it is necessary, in order to deal with this contention, to identify what is necessary to show a reasonably grounded suspicion in the present context. Guidance on what needs to be proved to establish such suspicion and reasonable grounds for it is provided by the High Court’s comments in George v Rockett (1990) 170 CLR 104 at 115 - 116, even though the court was there dealing with a statutory provision that differed materially in some respects from the relevant provisions of Pt 1AA the Crimes Act. A suspicion is a different state of mind from a belief. But a suspicion that something exists is more than “a mere idle wondering whether it exists or not”: it is a state of conjecture or surmise that the thing may exist, though proof of the existence of that thing is lacking. For a suspicion to be reasonably grounded, some factual basis for the suspicion must be shown. A reason to suspect that something or some state of affairs exists is more than a reason to consider or look into the possibility of its existence. But the facts which can reasonably ground a suspicion may be quite insufficient reasonably to ground a belief. Circumstances sufficient to show a reason to believe something need to point more clearly to the existence of the subject matter of the belief than circumstances which will be sufficient to show a reason to suspect something. As the High Court pointed out in George v Rockett (ibid) at 119 - 120, the power to issue a search warrant can be invoked in aid of an investigation into whether an offence has in fact been committed (ie, when the investigation may have only limited information suggesting that an offence may have been committed), as well as in aid of proof at the trial, if someone is ultimately charged in respect of the offence. But where a warrant is issued in aid of an investigation, before a reasonably grounded suspicion can arise in relation to a document, the investigation must have reached the stage where reasonable grounds for the statutory suspicion can be shown: George v Rockett (ibid).

19 The suspicion, reasonably grounded, upon which the lawfulness of a seizure under each warrant depends is a suspicion that the document “will afford evidence as to the commission of” one or other of the offences referred to in the third condition of each warrant. This does not require a suspicion that the document will be sufficient to achieve a conviction or that it will be able to be made admissible in evidence at a trial. It is enough to justify seizure if the executing officer suspects, on reasonable grounds, that the document will have relevance to or a probative connection with an issue arising upon an allegation of the offence in question or that the document will in some way implicate the persons named in the warrant in the commission of that offence. See Parker v Churchill (1985) 9 FCR 316 at 326 and George v Rockett (1990) 170 CLR 104 at 119 - 120.

20 The respondents submitted, in answer to the applicants’ reliance on the fact that they have conceded in the cataloguing process that a large number of documents were outside the warrants, that the test for whether the execution of the warrants was excessive was the reasonableness of the conduct of those involved in their execution. They cited no authority for this proposition in their closing submissions, but in their opening contentions they relied on the Full Court decision in Crowley v Murphy (1981) 52 FLR 123 as authority for a similar submission.

21 The court in Crowley v Murphy (ibid) was concerned only with the extent of the search which the warrant holder was permitted to conduct at the office of a solicitor, not himself implicated in the relevant offence, under the warrant. It was not concerned with the validity of decisions to seize particular documents: none had, in fact, been seized because initiation of the litigation had stopped any search being conducted. The Full Court ruled that the scope of the search which a warrant holder was permitted to conduct under the warrant, not being defined in the relevant legislation, had to be governed by what was reasonable in all the circumstances of the particular case. The court did not purport to rule that the authority conferred by the warrant to seize only the documents defined in the warrant was qualified in the sense that the warrant holder could say he acted lawfully in taking documents not within the warrant provided he acted reasonably in all the circumstances of the case in taking those documents.

22 A number of the decisions on warrants are discussed in Dunesky v Commonwealth of Australia (1996) 89 A Crim R 372 (“Dunesky”). There, Lockhart J was concerned with various challenges to the mode of execution of a search warrant issued in aid of a criminal investigation into suspected revenue fraud. One ground of attack was that none of the seizures were justified because no genuine attempt was made by the officers named in the warrant to determine whether the things which were seized fell within the terms of the warrant. Lockhart J, in stating the principles to be applied, said, at 382 - 383:

“A search warrant is a severe intrusion into a person’s privacy, home or place of business. The law takes care to ensure that the powers of police officers entrusted with the task of executing a search warrant are not exceeded; but at the same time it must be borne in mind that execution of a search warrant is a practical exercise carried out by police officers who, though trained in their task of law enforcement, are generally not qualified lawyers. Just as a person’s privacy must be respected so much the investigation of criminal offences not be unreasonably impeded.

To adopt the language of Mason J in Baker v Campbell (at 83):

‘In approaching the scope of the authority given by the warrant we must keep practical considerations steadily in mind. It is simply impossible for a police officer executing a warrant to make an instant judgment on the admissibility, probative value or privileged status of the documents which he may encounter in his search. Generally speaking, it is in the course of the subsequent investigation following seizure of the documents that informed consideration can be given to the documents and an assessment made of their worth or significance in the respects already mentioned. These considerations suggest that para (b) and the concluding words of the section [s 10], in so far as they relate back to para (b), are looking to documents as to which there are reasonable grounds for believing that they will in some way implicate the persons named in the warrant, or, if no person is named, someone in the commission of the offence. …”

23 Lockhart J concluded:

“The obligation of police officers executing warrants is to act reasonably in all the circumstances of the case (Crowley v Murphy at 152-155; Bartlett v Weir at 518). The warrant must be executed according to its terms and in accordance with the requirements of s 10: Dunesky v Elder at 556; 560-561.”

24 The two sentences comprising this last dictum appear to conflict. As is apparent from the entirety of the comments by Mason J in Baker v Campbell (1983) 153 CLR 52 at 83, of which an extract is set out in the judgment in Dunesky, Mason J was not suggesting that a warrant holder could take anything he chose in purported reliance on the warrant and leave it till later on, in the course of a subsequent examination, to determine whether any of the material taken came within the warrant. His Honour was concerned to explain why the executing officer need only have a qualified opinion as to the probative effect of any document seized: the officer did not need, in order to lawfully seize a document, to first form the opinion that it would be admissible, in the strict sense of that term, as evidence at a subsequent trial. Provided the executing officer acts within the warrant, there is no necessary inconsistency between seizing documents in circumstances where the executing officer has an actual belief that there are reasonable grounds for suspecting that they will afford evidence of the commission of an offence the subject of the warrant and that same officer later coming to the conclusion on more detailed consideration of the document that it does not, in truth, have that effect. See also Bartlett v Weir (1994) 72 A Crim R 511 at 520 where Beazley J said, “The lawfulness of the conduct of the police must be judged at the time, and not by what happens afterwards”. This consideration is important in evaluating the significance to the applicants’ challenge to execution of the warrant of the decisions made by the respondents in the cataloguing process.

25 But the decisions all emphasise that warrant holders can only lawfully take documents described in the warrant. However, they recognise that this particular consideration is but one aspect of the task for a court that has to deal with a challenge to the execution of a search warrant in connection with a complex criminal investigation. In those cases, the Court cannot confine itself to the question whether statutory requirements for the execution of a warrant have been strictly complied with. Rather, the task for the Court is one of balancing that consideration with broader public interest considerations. The point is made in Arno v Forsyth (1986) 65 ALR 125, where Lockhart J said, in a case in which a warrant issued in aid of an investigation into a complex tax fraud, at 139:

“It is necessary to reconcile the two competing public interests that offences involving tax frauds should be detected and punished on the one hand and the right of the individual to protection of the law from unjustified interference with his privacy and property on the other. It is in the public interest that those who commit offences involving fraud in relation to tax should be brought to justice. It is at least equally in the public interest that individual liberty should be protected by the courts whose function it is to protect individuals from abuse of power by the Executive arm of government. The balancing of the claims of the due administration of justice and those of the citizen whose rights must be jealously protected is not determined in a sterile vacuum but with due regard to the legislation involved and criminal activity suspected. The complexity of taxation frauds which often involve numerous persons and entities, and the concomitant difficulties associated with the gathering of documentary evidence to support the laying of charges highlights the dangers of too readily striking down warrants on the ground of generality in cases of this kind.”

26 The same point was made in Inland Revenue Commissioners v Rossminster Ltd [1980] AC 952 (“Rossminster”), a case involving a challenge to the execution of warrants issued in aid of an investigation into suspected complex tax frauds. See, eg, p 1,007, per Lord Diplock. The cases, including Baker v Campbell (1983) 153 CLR 52, also recognise the practical difficulties that warrant holders face in complex investigations in having to determine, in the often short period of time while they are at the warrant premises, whether particular documents do come within the warrant description.

27 It is all these considerations that I think have led judges in some cases to say, as was said in Dunesky and Coghill v McDermott [1983] VR 751 at 758, that the test for whether a search and seizure were carried out in excess of the power created by the warrant is one of reasonableness, ie, whether the search and seizure were conducted reasonably within the bounds of the warrant.

28 I do not think there is any room for expanding the authority given by the Parliament by s 3F(1)(c) the Crimes Act to the holder of a valid warrant to seize “evidential material specified in the warrant” to include the seizure of other material, so long as the extended seizure satisfies a vague criterion of being reasonable in all the circumstances of the case. But, in complex investigations that are now common, the seizure of individual documents is often not attacked: rather, the entirety of the warrant execution exercise is challenged as excessive and the Court is asked to declare that the seizure of the entirety of the material taken is not lawfully authorised. In these cases, the Court can properly have regard to whether the conduct of the executing officers was, in a broad sense, reasonable, in evaluating the significance to such a challenge based on matters including the number of documents taken, the period in which they were taken and the number of documents later conceded as having been mistakenly seized. Where such a challenge is made in a complex investigation to the execution of a warrant, it is, I think, a legitimate exercise for the Court in dealing with that challenge to form a view, for example, on whether the proportion of material taken that can be proved to be outside the warrant is unreasonably large, having regard to the width of the search authorised, the stage of the investigation reached and the complexity of the conduct suspected of involving criminal conduct.

29 It is just such an approach the applicants have taken in seeking to show that all of the many decisions to seize documentary material were flawed.

30 The applicants are faced with a difficult task in seeking to attack the execution of the warrants in relation to the documentary material that was seized under the various warrants. (Whether the decisions to remove the material in electronic form that was also taken from a number of the premises were also flawed requires separate consideration.)

31 The validity of the warrants has been upheld. In terms, they authorise a wide-ranging search and the seizure of a wide range of material. The warrants were issued in aid of a broad investigation by the AFP, at the instigation of the ATO, into a range of tax avoidance activities in which the applicants and a large number of their clients were thought to have engaged.

32 As I have said, all AFP and ATO officers who were asked about the matter said they did have regard to the third condition of the warrant when they determined to seize the material each took. In cross-examination, the respondents’ witnesses were pressed to explain why, when they seized or (in the case of the ATO officers) when they located particular documents, they then considered them to be within the three conditions of the relevant warrant. Many of the witnesses candidly admitted that they could not now recall what their thought processes were at the time. That is understandable. Nevertheless, some were prepared, when pressed, to try to explain why they had considered back in September 1996 that a particular document was within the relevant warrant. Much of this evidence is, I think, speculation engaged in in an attempt to offer a reason now why the document might, in fact, be within the warrant. I place little weight on much of this cross-examination.

33 I accept that discrimination was exercised by the searching officers in that at none of the premises was the entirety of the documentation located there seized: a selection was made. The seizure records themselves also contain numerous examples of material located at the premises and then recorded in those records but in respect of which a decision was subsequently made, before the executing officers left the premises in question, that the particular material was not to be seized. All this is suggestive of the formation of a judgment that the material taken was within the warrant.

34 Many of the executing officers were cross-examined. Each was, however, questioned about only a small number of documents each seized. These documents were invariably ones that the AFP has conceded in the cataloguing exercise were wrongly seized. The applicants explained their approach here as designed to show that, because the particular item was so obviously irrelevant, so far as condition 3 of the relevant warrant was concerned, that it was fair to submit that the officer, in seizing every one of the documents he or she took, did that without giving any consideration at all to condition 3.

35 The respondents submit that, while more than 9,000 documents, in total, (many consisting of multiple pages) were identified in the cataloguing process the executing officers were cross-examined about fewer than ninety of these documents all told, ie, fewer than 1 percent (and then, in many cases, only on part of each of these ninety documents). That submission seems to reflect accurately enough the approach the applicants took in this respect. I do not find much assistance in this cross-examination in determining whether the entire execution exercise at all premises was fundamentally flawed, as the applicants submit. To focus as the applicants did on a very small number of documents, which, if considered in isolation from the context in which they were found, appear to be the subject of a blatantly unjustifiable seizure, establishes little.

36 In the course of evidence, I commented on this aspect of the way the applicants were running their case. By way of example, the seizure of the $20 bank note and the veterinarian’s invoice at Mr Adcock’s home, both in item D5 in the seizure record, if looked at in isolation appear to be blatantly unjustified. But, when it emerges that these documents were interleaved in a cheque book and that cheque book was but one of many bound volumes or folders that were taken, the evidentiary significance for the applicants’ case attaching to the seizure of the bank note and the invoice is very much diminished. The respondents were entitled to say that the focus should rather have been on whether the folder or bound volume in which those documents were interleaved was, itself, properly taken. This is especially so when it is recognised that the executing officers who took the bank note and the invoice did so in the course of seizing many documents at the particular premises in the quite short period of time permitted by the warrant. It was not suggested that complaint was made at the time of the seizure of these two items (though the evidence is that complaints were sometimes made about the appropriateness of particular seizures and that sometimes, but not always, documents the subject of such complaints were ultimately not taken). Nor was it submitted that it was unreasonable for the book of cheque-butts to be taken with the bank note and the veterinary invoice left in situ. Their location in the cheque-butts may, for all that emerged at the hearing, have had some significance to the person who placed them in the cheque book, a significance that may have been destroyed or diminished if the seizing officer had abstracted the bank note and the veterinary receipt from the cheque book and left them in the office from which the cheque book was taken. It cannot, therefore, be said that the fact that a bank note and a veterinary receipt were seized is evidencing that the officers involved were acting, in taking the material they did, without regard to the conditions of the relevant warrant. Cf Parker v Churchill (1986) 65 ALR 107 at 123.

37 It would have been of more value as an aid to assessing the nature of the actual search implemented at the various premises if the applicants had cross-examined the various executing officers on a less selective and more random sample of documents each took. Further, there is an air of unreality in cross-examining executing officers about a few of a large number of documents seized by the person nearly six years ago as to the thought processes they went through at the time in determining to seize the particular document.

38 The applicants also sought to find support for their case of an impermissibly wide general search by analysing each document in every folder or book taken and finding support in the fact that, even where a particular folder or book contained one or more documents or entries either admittedly or arguably within the particular warrant, many of the documents in the folder or entries in the book could be said to be manifestly outside the relevant warrant.

39 However, it appears that the AFP had a practice, when officers were executing search warrants, of seizing the entirety of a folder or book in which a document or entry considered to be within the particular warrant was contained. The reasonableness of this practice was not the subject of specific attack by the applicants. There may well be justification for an executing officer to take the entirety of a folder or a book in which he or she locates an individual document or entry itself within the warrant because the context in which the document or entry is found may itself be of assistance in evaluating the true evidentiary significance of that document or entry. Cf George v Rockett (1990) 170 CLR 104 at 120. When an extensive search is being conducted under a warrant in aid of a complex investigation and many documents are taken, further justification for the practice may be found in practical considerations such as difficulties in recording the exact location of the particular document in the folder if it alone were to be taken and whether any complaint is made about seizure of the entire folder. Questions of the reasonableness of the executing officer’s conduct may also arise if an officer were to pull apart a bound volume in order to take only the page considered to be within the warrant or if the officer were to abstract from a folder one or more documents in circumstances in which the owner might be in difficulty in reconstituting the folder in proper order when the documents taken were ultimately returned. Practical issues are also raised where, as happened with some frequency, apparently responsible persons at premises at which warrants were executed, after having the warrants read over to them, identified entire folders of material as those in which the executing officers might be interested, and which the officers then took without further examination.

40 I am not prepared to accept that such an analysis of the material seized advances the applicants’ case, given the absence of any exploration at the trial of the question whether the AFP practice relied on in this case is not supportable. I am not prepared to hold that the AFP practice is unreasonable and leads to the unlawful seizure of material when an entire folder or book is taken in circumstances where there is only one or a few pages or entries identified by the executing officer as coming within the warrant, given that these issues were not explored at the trial.

41 I do not accept that the applicants’ contention based on the cataloguing work done, by and under the supervision of Mr Stevens that only a minuscule number of the documents seized are within the warrant provides any reliable indication that the number of documents seized in respect of which there are reasonable grounds for suspecting that they may afford evidence of the commission of the relevant offences is so limited.

42 Mr Stevens has summarised the applicants’ position as having accepted that only 6 percent of 9,156 hard copy “documents” the subject of the cataloguing exercise were within the warrant. The applicants’ detailed contentions, together with the respondents’ contentions, are contained in Mr Stevens’ exhibit, IRS-5A. Mr Stevens made his judgments by reference to whether documents taken related to Hendon or Northbourne: he did not attempt to assess whether any of the documents taken could be said to relate to any of the other five lines of inquiry because he only learned of their existence late in the piece when he saw the Australian Government Solicitor’s letter of 30 July 1998. But, even allowing for this, it appears that in arriving at this minuscule figure, Mr Stevens adopted an unjustifiably narrow approach to accepting whether a particular document was within the warrant. His approach appears to have been only to concede that a document was within the warrant if it specifically mentioned either Hendon or Northbourne and then only if it could be seen to bear a date within one or other of the financial years mentioned in the statement of the offences in the warrants, ie, the financial years 1991 - 1995.

43 As Lockhart J said in Dunesky at 384:

“It is to be remembered in this case, where the classes of documents which may be seized pursuant to the terms of the warrant are wide indeed, that documents will not fail to satisfy the three conditions contained in the warrant merely because (a) they bear dates outside the period of the commission of the alleged offences specified in the warrant; or (b) they relate also to persons other than persons revealed by the warrant as being suspected of committing the offences; or (c) they relate to some subject distinct from the matter under investigation. Documents may meet all three conditions notwithstanding those matters.”

44 Mr Stevens’ unjustifiably narrow approach can be demonstrated by some examples. In the section of his exhibit, IRS-5A, dealing with documents seized by Federal Agent Delaney at premises J, Cam Brown Auctions’ premises at Eagle Farm, he places documents J10/1 and J13/1 in the disputed category because, though on their face clearly relevant to showing dealings between Harts’ client Brown and the Hendon Unit Trust, they are each dated after the end of the 1995 financial year. In the section dealing with documents seized by ATO Officer Young at 240 Margaret Street, there are a number of groups of pages contained in document A2134 which Mr Stevens has conceded as being within the warrant. They are the forty-five pages making up documents A2134/10, /06, /08, /03, /13 and /12. They comprise financial statements in respect of the McGowan Family Trust for various periods within the 1994 and 1995 financial years, which contain specific reference to Hendon. However, in the same file (A2134), documents /05, /14 and /16, comprising 155 pages in all, are disputed by Mr Stevens, though they consist of financial statements and income tax returns for the same trust in respect of the same two financial years. Apparently Mr Stevens has disputed them because they do not mention Hendon by name. Yet they would appear to cover activities of the McGowan Family Trust in respect of which the other documents provide ground for thinking that they may relate to the financial activities of the McGowan Family Trust, which include activities involving Hendon. Document A2124/1, of thirty-six, pages is disputed: it consists of working papers for the 1995 tax return for the McGowan Family Trust without apparently specifically mentioning Hendon. Document A2132/1 of forty pages described as “[p]roposal for the sale of the business Beaurepaires Tyre Centre at Goondiwindi, presently owned by…The McGowan Family Trust” is conceded as within the warrant, apparently because it includes financial statements for the same financial year for that Trust in which there is specific reference to Hendon. In the same couple of pages, document A2127/1, of six pages is disputed, though it is described as the 1995 tax return for the McGowan Family Trust and specifically mentions Northbourne: the reason for the dispute appears to be that the return is “signed and dated 11/12/95”, ie, after the last of the financial years mentioned in the statement of the offences.

45 It is difficult to accept that there is any reason, on the face of the description of the documents, which could justify Mr Stevens disputing that other documents are within the warrant. For example, in the section dealing with ATO Officer Young’s seizures at 240 Margaret Street, document A10/10, of 184 pages, is disputed though it is described as “1 lever arch folder containing individual property details of investment details re Hendon Unit Trust containing 184 pages relates to Hendon Unit Trust and all contributors and levels of contributions as well as representative from Harts who spoke to client. Mentions years 93, 94 and 95.”

46 In the section of IRS-5A dealing with documents seized by Federal Agent Jay at 240 Margaret Street, copy income tax returns for the 1993, 1994 and 1995 years for the Bradley Family Trust, are conceded by Mr Stevens as being within the warrant, each mentioning either the Hendon or the Northbourne Trust. They are documents A1077/11, /07 and /05. On the same page, document A1017/2, consisting of 271 pages, is disputed, though it includes the financial statements for the Bradley Family Trust for the 1993, 1994 and 1995 years on the basis of which it can be inferred the income tax returns were prepared. Document A1073/038 of ten pages on the same page is disputed, though it includes eight pages of draft financial statements for the Bradley Family Trust for the 1994 financial year and specifically mentions Hendon: there is no apparent reason why this document should be disputed.

47 Material broken down into ninety-four documents for the purpose of cataloguing, consisting of a total of 322 pages, was seized at Mr Wagner’s premises at Kingston. Though they involve dealings between the Wagner Trust and Northbourne Trust and show Mr Hart’s involvement, a number are disputed apparently because they are dated after the end of the 1995 financial year. They are R10/02 (fourteen pages), R12/01 (six pages) and R14/05, /06 and /15 (three pages).

48 On the face of Mr Stevens’ exercise, as recorded in his exhibit IRS-5A, there is sufficient ground in the way he has dealt with seized documents in the cataloguing process of which the above are but a few examples to doubt the reliability of his ultimate contention that only a tiny number of documents are within the warrant.

49 Mr Stevens’ time analysis is also questionable as a basis for inferring an undiscriminating search and seizure.

50 The circumstances in which these warrants were executed neither gave nor required the executing officer much time to ponder long over documents. Quick decisions, as a general rule, necessarily had to be made. That does not necessarily mean the requisite state of mind could not have been formed. Nor does it mean that, on more mature consideration such as that which occurred during the cataloguing process, a different view could have been formed about particular documents without in any way casting doubt on the propriety of the seizure of the documents. As Viscount Dilhorne said in Rossminster at 1,006:

“A great many documents were seized and removed. Many officers were employed in the operation. Lists were made up of what was seized and the time of seizure recorded. A short interval of time between two entries on a list would be a strong indication that there could not have been a proper examination, if one officer dealt with the documents referred to in those two entries, but with a number of officers searching and examining documents, the times of seizure do not in my opinion provide the slightest indication of whether or not before seizure there was examination. The time necessary to form a view whether a file or a document might be required as evidence would vary. If the fraud suspected involved inter-company transactions between a large number of companies, it would not take up much time to decide that a file relating to one of the companies might reasonably be believed as likely to contain material which might be required as evidence; and such a conclusion might properly be reached without looking at every document in the file.”

51 There are numerous reasons why Mr Stevens’ time analysis is flawed. Mr Stevens assumed that each page in each document needed to be perused before a proper decision to seize could be taken. But many company registers and trust deeds were taken: once an executing officer identified such a document from a perusal of only the first page, he might well be justified in seizing the whole. I have already referred to the AFP practice of seizing an entire file where it contained a document identified as within the relevant warrant. Mr Stevens also based his analysis on the assumption that each executing officer perused a document ultimately taken only in the period between when that document was logged in the seizure record in the “time located” column and when the immediately preceding document taken by that officer was similarly logged. As might be expected, the notation in the “time located” column for a document records the time when many executing officers, after having completed their perusal of the relevant document, had determined that it should be seized. The respondents, in their submissions, point to numerous other reasons for rejecting Mr Stevens’ time analysis as of any value as evidencing an undiscriminating search and seizure.

52 But notwithstanding all this, I think the applicants’ attack on the execution of the warrants succeeds in part. Save only for documents that could be thought to be related in some way to the Hendon and Northbourne Trusts (and the RD Moore Family Trust), the AFP and ATO officers brought in to execute the warrants had, I think, little option but to conduct a negative search, ie, to take anything that they thought might turn out at some future stage to be of some relevance to proof of the offences referred to in very general terms in the warrants.

53 A small team under Federal Agent Perry had the carriage of the investigation within the AFP from November 1995, when the ATO called in the AFP, at least until a decision to issue the warrants in question was taken. The main focus of the investigation was on the suspected use by the applicants of a trust, the Hendon Unit Trust, as a vehicle for generating substantial fee income for the applicants by enabling a number of their clients to avoid tax in the financial years 1991 to 1995. In setting out details of the scheme involving the Hendon Unit Trust, it should be recorded that no facts have yet been found as to whether the applicants or any of their clients at whose premises the warrants were executed have been involved in any unlawful tax avoidance scheme or other unlawful activity. Details of the scheme and other activities are taken from allegations made by the respondents in the material filed in the present proceedings which are concerned solely with whether seizure of the documents was lawfully authorised by the warrants.

54 According to Federal Agent Leary, prior to executing the search warrants, the AFP had detailed information that pointed to the Hendon Unit Trust being the centre of an unlawful tax avoidance exercise orchestrated by the applicants. According to this information, the applicants arranged for each client involved to make distributions from the client’s own discretionary trust to the Hendon Trust, purportedly by way of investment in the business activities of that Trust. The client would make a commitment on or prior to 30 June to invest a certain sum in the particular financial year in the Hendon Trust. Twelve percent of this investment would be paid in cash, with 10 percent going to Astion, one of the second applicants and a company controlled by Messrs Hart and Adcock, and the other 2 percent going to Tinkadale Pty Ltd (“Tinkadale”), a company controlled by Mr and Mrs Adcock and Mr Stevens. These sums were retained by Astion and Tinkadale for their own benefit as what were described as management fees. They comprised the benefit to the applicants from the scheme. The balance of 88percent of each client’s investment was, so it was believed by the ATO and the AFP, never paid to Hendon but instead was evidenced only by a journal entry in the books of the client’s discretionary trust for the relevant year as a distribution by that trust to Hendon in the form of a loan to that Trust payable at call. Though Hendon brought to account in its tax returns income amounts equal to 88 percent of each client’s purported investment, the Hendon Trust did not have to pay any tax in any of the years of income because that Trust had large losses accumulated from previous years’ trading against which it was able to write off that income. Each client’s trust claimed in its relevant tax return to have distributed income in an amount equalling 100 percent of the payments made in the particular financial year to Astion, Tinkadale and Hendon. If this investment had not been made into the Hendon Unit Trust by the client trust in the particular financial year, then the client trust would have had to pay tax on undistributed income or the beneficiaries would have had to pay tax on any distributions of income.

55 What made the arrangement attractive to clients, according to the information obtained by the ATO and the AFP, was that the clients were told that the applicants, as controllers of the Hendon Trust, would never demand payment of the 88 percent of the investment purportedly made by each client trust in Hendon: these moneys were instead retained by those controlling each client trust for their own purposes.

56 In interviews conducted by AFP and ATO officers in January 1996, an unidentified client of Harts stated that the Hendon Unit Trust was set up as a means of reducing that particular client’s tax. This client said he was informed by Mr Hart that, apart from the 12 percent cash payment, “they would not have to pay the balance of their investment [in the Hendon Trust] as it would never be called up”. In February 1996, ATO officers obtained information from two unidentified ex-employees of Harts to the effect that each had received a memo from Mr Stevens inquiring whether the employee had any clients interested in putting money into a trust with tax advantages and that, in this context, each ex-employee sighted various documents concerning the Hendon Unit Trust. Each told the ATO officers that Mr Stevens, in response to their query, said the balance of loans or contributions shown in the books of clients who participated in these arrangements as owing to the Hendon Unit Trust would never be called up.

57 In February 1996, ATO officers also interviewed Mr James Zannes and Mr Theodore Tzannes, principals of a car dealership. They told the ATO officers that Mr Hart introduced an investment scheme involving the Hendon Unit Trust to them when he visited them at Moree prior to the end of the 1993 financial year. The 1993 financial year return for the Zannes Brothers Unit Trust showed a net profit of $232,223, of which $200,000 was invested in the Hendon Unit Trust. The Zannes told the ATO officers that, apart from $20,000 paid to Astion and $4,000 to Tinkadale, they did not, on the basis of what they were told by Mr Hart, expect to have to pay anything more of the $200,000 written up as an investment in the Hendon Unit Trust. Mr Theodore Tzannes also said they did not appreciate that “the Hendon Unit Trust was involved in the scheme, or that their trust was actually making a distribution to it” until they applied for a loan from their bank in the first half of 1994. The bank had then obtained the 1993 financial statements for the Zannes Brothers Unit Trust prepared by Harts and queried them about the $200,000 liability to the Hendon Unit Trust recorded in these statements. The Zannes called on Mr Hart to answer this query, which he did by a letter of 21 June 1994, in which he stated “Please be advised that there are no monies owing to the Hendon Unit Trust by the Zannes Brothers Unit Trust.”.

58 The same unidentified client already mentioned also gave information to the effect that documents amending clients’ trust deeds were sent to clients for signing approximately eighteen months after the journal entry distributions to the Hendon Unit Trust were created. This was done, so it was suspected by the AFP, to ensure that the trustees of the client trusts could show that they were authorised to invest in the Hendon Trust in financial years long past. In March 1996, ATO officers obtained information from another ex-employee of Harts to the effect that, though Messrs Adcock and Hart each signed statutory declarations in connection with the tax affairs of the relevant clients to the effect that documentation relating to clients’ trust distributions to the Hendon Unit Trust had been signed prior to 30 June 1993, much of that documentation was, in fact, only executed after the end of that financial year. If true, apart from other possible criminal activities, the applicants also engaged in falsifying documents upon which the tax liabilities of the clients in question depended.

59 Prior to executing the search warrants, the AFP investigation thus had what, on its face, was cogent information that the Hendon Unit Trust was employed by the applicants as a vehicle for unlawful tax avoidance by their clients to the mutual benefit of the clients and the applicants. They also had cogent evidence to suggest that the applicants were involved in backdating or altering financial records and documents in connection with their use of the Hendon Unit Trust for this purpose. Information available to the ATO and AFP from taxation records of fifty-seven trusts that contributed to the Hendon Unit Trust indicated that “at least $13 million of otherwise taxable income has been distributed by way of journalised loans to the Hendon Unit Trust in the 1992/93, 1993/94 and 1994/95 financial years”.

60 The information available to the AFP concerning the Northbourne Holdings Unit Trust suggested that the applicants used this Trust as a tax avoidance vehicle for clients in the same way as they used the Hendon Unit Trust (though the contributions made by journal entry by various of the Harts’ client trusts apparently intended to go to the Northbourne Holdings Unit Trust were written up in the client taxation returns prepared by Harts as having been made to the “Northbourne Rural Property Trust”). Examination of client taxation records by the ATO suggested that approximately $2,700,000 of taxable income was distributed by client trusts to the Northbourne Trust.

61 The investigation, however, was into a range of activities by the applicants, those associated with them and various clients, that extended beyond the schemes said to be centred on the Hendon and “other similar trusts”. It is apparent from Federal Agent Leary’s evidence that, prior to executing the warrants, the AFP also had a range of information, some of it suggesting that various persons in the Harts organisation engaged at Mr Hart’s instigation in the practice of falsifying clients’ financial records on the basis of which tax returns were prepared to reduce the clients’ tax liability. The AFP had information suggesting that balance day adjustment “journal entries” were made within the Harts organisation, quite separately from what was done in respect of clients involved with the Hendon and Northbourne Trusts: this had the effect of reducing clients’ taxable income by overstating the business creditors of clients, by journalising under-valuations of stock on hand or not bringing all stock on hand to account at the end of the financial year. Two persons, an employee and an ex-employee of Harts, provided information to this effect to the ATO in November 1995 and March 1996. This is what was called the third of the seven lines of inquiry in aid of which the police obtained the warrants. The Hendon and Northbourne matters were the first two lines of inquiry.

62 The AFP also had information that Mr Hart, on occasion, received payment from clients for accounting services provided in the form of goods and services. The value of such goods and services was not declared by Mr Hart or his company as income, while charges to the clients which were raised in Harts’ books for the accounting services were then written off as bad debts. Specific reference was made to plumbing and electrical services said to be provided to Mr Hart personally. But the AFP’s information was that there were many instances in which this kind of arrangement was put in place between Mr Hart and personal clients. This was the fourth line of inquiry.

63 AFP information also suggested that a number of entities associated with the applicants had avoided tax by simply not lodging returns. Tinkadale, as trustee for the New Stewart Family Trust, had not lodged tax returns, though, for the 1992 financial year, it had receive a distribution of nearly $70,000 from the Adcock Practice Trust. The Adcock Practice Trust received over $450,000 from Astion and Tinkadale for the financial years 1993 - 1995 inclusive. Advice by Harts to the ATO in respect of Astion and Tinkadale was to the effect that all outgoings from both companies were payments made by them by way of consultant or management fees and were thus taxable in the hands of the recipient. Yet the Adcock Practice Trust had not lodged a tax return for any of the 1993 - 1995 financial years. This was the fifth line of inquiry.

64 Federal Agent Leary also deposes to suspecting a failure by entities to bring to account all income derived during a particular financial year and to overstate deductions. He refers to distributions from various family trusts associated with Mr Hart brought to account in the tax returns for the relevant year by those trusts, but not included in the income of the various recipients. This was the sixth line of inquiry.

65 Finally, the ATO received information in April 1996 to the effect that Harts Consulting Pty Ltd, a company controlled by the applicants, was involved in a scheme with forty-two clients, each of whom agreed to pay a fee of $40,000 to Harts Consulting for a business management report. Only $16,250 of this fee was in fact paid by each client. The client was to claim the full $40,000 as a deduction in the relevant year. Harts Consulting undertook not to call up the balance of the fees and declared as income only the $16,250 cash actually received. This was the seventh line of inquiry.

66 These matters, commencing with the Hendon matter, are identified as the seven lines of AFP inquiry referred to in the letter from the AGS to the applicants’ solicitors of 30 July 1998. This letter was written in connection with the cataloguing exercise. The applicants say it was the first indication to them that the scope of the AFP/ATO investigation in aid of which the warrants were issued in fact extended beyond activities involving the Hendon and Northbourne Trusts.

67 The evidence before me establishes that the many AFP and ATO officers brought in to assist the small number of AFP and ATO officers already involved in the investigation to execute the warrants were briefed, not only about the suspected involvement of the applicants and various of their clients in criminal offences in connection with the Hendon and Northbourne schemes, but also about the range of other suspected offences referred to above.

68 Federal Agent Morris’ briefing notes (exhibit H3) were displayed as part of his PowerPoint presentation at the briefings held on 5, 8 and 9 September 1996. It is apparent from these notes that the AFP and ATO officers there present were given a detailed description of how the Hendon Unit Trust was believed to have been used by the applicants in carrying on tax-related criminal activity. The attention of all those officers was expressly drawn to the belief of the AFP and ATO investigators that the applicants were “defrauding the Commonwealth of Taxation revenue by way of a unit trust called the HENDON Unit Trust as well as a number of other similar trusts of which the structure is set up solely for the purposes of avoiding tax”. That statement is contained in p 2 of the PowerPoint presentation, which I accept was displayed at the briefings. The client table, which Federal Agent Morris displayed at his briefings, shows that those officers were also given quite detailed information about the family and business trusts of twelve of the applicants’ clients who were believed to have avoided tax on very large sums purportedly invested in the Hendon and Northbourne Trusts, particularly in the financial years 1993 to 1995.

69 The Willemse Family Trust was the thirteenth client trust investor included in the table in Federal Agent Morris’ PowerPoint document. Unlike the others, Federal Agent Morris’ table does not show the Willemse Family Trust as having made any payments to either Hendon or Northbourne. Instead, it shows payments by the Willemse Trust to entities described as “RD Moore Family Trust”, “Neutral” and “Sunpro”. The RD Moore Family Trust would, in this context, very likely be understood by those briefed as another “similar trust” to Hendon. The respondents also had information suggesting that the Willemse Family Trust was connected with the Hendon Trust. Federal Agent Leary sets that out in some detail. The Hendon Unit Trust was established in March 1988, with a company called The Westside Commerce Centre Pty Ltd as trustee. Prior to its acquisition by the applicants, that company had acquired, as such trustee, a commercial property in Adelaide called “Hendon Common”, with funding largely obtained from an external financier. In late 1990, this financier entered into possession of the property as mortgagee, the debt owing to it in April 1996 being $19,250,000. By this time, all units in the Hendon Trust were held by another company, RD Moore Pty Ltd, as trustee for the RD Moore Family Trust. A Mr Robert Moore was director and principal shareholder in RD Moore Pty Ltd and the owner with another of the shares in The Westside Commerce Centre Pty Ltd.

70 On 30 June 1993, Mr Moore caused RD Moore Pty Ltd as trustee of the RD Moore Family Trust to grant an option to the applicant, Astion, to buy the units in the Hendon Unit Trust, all of which it owned. Federal Agent Leary says that the AFP had information that though it was Astion which held the call option over the shares in RD Moore Pty Ltd, in August or September 1993, Mr Moore transferred the shares in RD Moore Pty Ltd and thus ownership of the units in the Hendon Trust to Queensland Mushrooms Pty Ltd (“Queensland Mushrooms”), a client of Harts. The directors and shareholders of Queensland Mushrooms, Ms Clark and Messrs J Willemse and P Willemse, are recorded in Australian Securities Commission records as directors of RD Moore Pty Ltd in the period 30 June 1993 to 7 July 1995, when RD Moore Pty Ltd was struck off the register. The respondents thus had information that, for some years from August or September 1993, the Hendon Trust, which was central to one of the tax avoidance schemes that they believed the applicants were engaged in, was owned and controlled by the same people who were the directors of Queensland Mushrooms, who were also associated with the Willemse Family Trust.

71 One of these, Ms Clark, said it was Mr Hart who suggested that the Willemses should buy RD Moore Pty Ltd. She also said, however, she was not aware that RD Moore Pty Ltd, of which she and her two brothers, Messr P and J Willemse, were directors, had any connection with the Hendon Unit Trust, though it seems that the company owned all the units in Hendon: she said she knew nothing about it. Mr P Willemse said the same. Some of Queensland Mushrooms’ financial and other records that were seized contain references to both the Hendon Unit Trust and the Willemse Family Trust. But it does not matter what the true position was among the Willemses and Ms Clark. Even if it is the case that they knew nothing about the connection between their company, RD Moore Pty Ltd, and the Hendon Unit Trust, that is not relevant to the question of the lawfulness of the execution of the warrants at the premises of Queensland Mushrooms.

72 In my opinion, the information that the AFP and ATO officers who were conducting the investigation had suggesting a connection between Ms Clark and Messrs P and J Willemse, the Willemse Family Trust, Queensland Mushrooms and the Hendon Unit Trust through RD Moore Pty Ltd, was sufficient to entitle those officers to form a reasonably grounded suspicion that documents relevant to showing that connection as well as documents at the premises of Queensland Mushrooms that mentioned or related to the Hendon Unit Trust all satisfied condition 3 of the relevant warrants.

73 That these officers held such a suspicion in relation to Queensland Mushrooms and those who controlled it was, I think, conveyed to the mass of AFP and ATO officers involved in the execution of the warrants at one or other of the various briefings by the display of Federal Agent Morris’ PowerPoint document. As I have pointed out, this document expressly drew the attention of those at the briefings to the belief that the applicants were using the Hendon Unit Trust, as well as a number of other similar trusts, solely for the purpose of the unlawful avoidance of tax and the client table in this document is likely to have indicated to those who viewed it that the “RD Moore Family Trust”, to whom the table shows the Willemse Family Trust as having made payments in the 1993 to 1995 period, was one of those “similar trusts”.

74 The document CAJ-1, “Documents Behind the Scheme”, was prepared by Mr McKay of the ATO, who also participated in the execution of the warrants. There are understandable differences in the recollections of various of the officers, some no longer with either the AFP or the ATO, about the range of information they gathered at the briefings. But I accept that CAJ-1 was widely distributed at one of the briefings, probably the one attended by the ATO Officer Jeffs with other ATO and AFP officers in early September. It depicts, though not as in much detail as Federal Agent Morris’ PowerPoint presentation notes, the activities involving the Hendon and Northbourne Unit Trusts. It provides those to whom it was given fairly detailed information about the involvement of Harts’ client trusts in the Hendon scheme and lists seven particular categories of document to be “looked for” as documents associated with the Hendon scheme and therefore to be seized under the warrants.

75 Given the information available to the ATO and the AFP, including that to the effect that Hendon and Northbourne had large accumulated losses and would receive nothing at all from the purported investments in them by the applicants’ clients, it can be inferred that the AFP and ATO officers running the investigation into the applicants’ activities associated with Hendon and Northbourne were of the view that neither entity was engaged in any lawful activity, but had been used by the applicants and their clients entirely as vehicles for unlawful tax avoidance. As I have said, just that view of Hendon “as well as a number of other similar trusts”, including Northbourne, was expressed by Federal Agent Morris at the briefings he gave to AFP and ATO officers involved in executing the warrants.

76 Once it is concluded that the ATO and the AFP investigators had reason to view both Hendon and Northbourne as vehicles employed by the applicants and their clients solely for unlawful tax avoidance and that the officers involved in the execution of the warrants were informed at the briefings they were given of that, I think it follows that any document discovered by any of the executing officers at any of the premises of the applicants or their clients which could be seen to relate in any way to activities involving the Hendon or Northbourne Trusts could be said to be within the relevant warrant. Once the conclusion is reached that all the ATO and AFP officers involved in execution of the warrants had grounds for thinking that both the Hendon and Northbourne Trusts (and the RD Moore Family Trust) were employed by the applicants solely as vehicles for unlawful tax avoidance, it follows, in my opinion, that, for all practical purposes, an officer who considered that a document that answered the first two conditions of the relevant warrant also mentioned or in some other way related to the activities of Hendon or Northbourne (or the RD Moore Family Trust) was entitled without further consideration to seize the document: such a document would necessarily satisfy the third condition of the relevant warrant.

77 The applicants’ challenge to the seizure of any hard copy document that in any way relates to any of these three trusts must therefore fail. The systemic failure to have regard to condition 3 of each warrant now at the centre of the applicants’ case, even if established, cannot invalidate the seizure of any of those documents.

78 The information available to the AFP and ATO officers running the investigation and conveyed to the executing officers at the various briefings in relation to the five lines of inquiry additional to the Hendon and Northbourne lines was, in significant respects, more general than that conveyed to the executing officers in relation to the Hendon and Northbourne lines of inquiry. In relation to these other five lines of inquiry, the executing officers were (with two qualifications) given only the broadest information as to the kind of activities that it was suspected the applicants and various clients had engaged in which might involve the commission of one or other of the offences listed in the warrants.

79 Despite its title, “Documents Behind the Scheme”, CAJ-1 draws the attention of those to whom it was given to a number of areas of activity in which it was thought the applicants and others may have been involved in criminal activity additional to activities concerning the Hendon Trust. It contains more detailed information than that in Federal Agent Morris’ PowerPoint notes about the third line of inquiry, under the heading “False Journal Entries” in Section 2. The briefing document, CAJ-1, thus gave a little more precise guidance to executing officers as to some of the kinds of documents they should look for in relation to this line of inquiry and it appears from Federal Agent Morris’ PowerPoint presentation that those attending his briefings may also have been given some specific, but limited, information of examples of conduct engaged in by Mr Hart in relation to the fourth line of inquiry.