FEDERAL COURT OF AUSTRALIA

Marleef Pty Ltd v Metcash Trading Ltd [2001] FCA 1316

TRADE PRACTICES – misleading or deceptive conduct – use of similar marks – whether respondents used name or mark of “Chef’s Pantry” on food products in a way which would make them distinguishable to customers – sufficiency of evidence to establish distinctiveness and reputation with class of members of public – whether a misrepresentation – whether conduct misled or likely to mislead public - whether confusion or uncertainty - whether representation that goods associated with applicant - scope of injunctive relief

TORT – passing off – elements of cause of action – whether reputation established – whether a misrepresentation – scope of injunctive relief

Trade Practices Act 1974 (Cth) ss 52, 53(c) and 80

Federal Court Rules O 38, r 1

Jones v Dunkel (1959) 101 CLR 298 applied

Marks v GIO Australia Holdings Ltd (1998) 196 CLR 494 referred to

Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd (1982) 149 CLR 191 at 197 and 205 referred to

Red Bull Australia Pty Ltd v Sydneywide Distributors Pty Ltd [2001] FCA 1228 at [73] referred to

Taco Co of Australia Inc v Taco Bell Pty Ltd (1982) 42 ALR 177 applied

Equity Access Pty Ltd v Westpac Banking Corporation (1990) ATPR 40-994 at 50, 950 referred to

George Weston Foods Ltd v Goodman Fielder Ltd [2000] FCA 1632 referred to

Crago v Multiquip Pty Ltd (1998) ATPR 41-620 referred to

ACI Australia Ltd v Glamour Glaze Pty Ltd (1988) 11 IPR 269 referred to

Mark Foy’s Pty Ltd v TVSN (Pacific) Ltd (2000) 104 FCR 61 referred to

Campomar Sociedad, Limitada v Nike International Ltd (2000) 169 ALR 677 at 707 applied

Fletcher Challenge Ltd v Fletcher Challenge Pty Ltd [1981] 1 NSWLR 196 referred to

Conagra Inc v McCain Foods (Aust) Pty Ltd (1992) 33 FCR 302 referred to

Betta Foods Australia Pty Ltd v Betta Fruit Bars Pty Ltd (1998) ATPR 41-624 at 40, 839 referred to

Office Cleaning Services Ltd v Westminster Office Cleaning Association [1944] 2 All ER 269 referred to

AG Spalding & Bros v AW Gamage Ltd (1915) 32 RPC 273 referred to

Vieright Pty Ltd v Myer Stores Limited (1995) ATPR 41-405 at 40, 493 referred to

Gordon M Jenkins v Coleman (1989) 23 FCR 38 referred to

MARLEEF PTY LTD (ACN 081 561 435) v METCASH TRADING LIMITED (ACN 000 031 569, METCASH HOLDINGS PTY LTD (formerly known as JOHN LEWIS FOODSERVICE PTY LTD) (ACN 004 380 152) and CAMPBELLS CASH & CARRY PTY LTD (ACN 000 226 399)

V599 of 2001

MARLEEF PTY LTD (ACN 081 561 435) v BIDVEST AUSTRALIA PTY LTD (ACN 000 228 231 and BIDVEST (VICTORIA) PTY LTD (ACN 053 695 855)

V679 of 2001

WEINBERG J

14 SEPTEMBER 2001

MELBOURNE

GENERAL DISTRIBUTION

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

VICTORIA DISTRICT REGISTRY |

V599 of 2001 |

|

BETWEEN: |

MARLEEF PTY LTD (ACN 081 561 435) APPLICANT

|

|

AND: |

METCASH TRADING LIMITED (ACN 000 031 569) FIRST RESPONDENT

|

|

|

METCASH HOLDINGS PTY LTD (formerly known as JOHN LEWIS FOODSERVICE PTY LTD) (ACN 004 380 152) SECOND RESPONDENT

|

|

|

CAMPBELLS CASH & CARRY PTY LTD (ACN 000 226 399) THIRD RESPONDENT

|

|

JUDGE: |

WEINBERG J |

|

DATE OF ORDER: |

14 SEPTEMBER 2001 |

|

WHERE MADE: |

MELBOURNE |

IN PROCEEDING V599 of 2001, THE COURT ORDERS THAT:

1. On and from 17 September 2001, the respondents be restrained, whether by themselves or their officers, servants or agents or howsoever otherwise, from selling, supplying or offering for sale or supply or advertising or promoting for sale or supply, in Victoria, to members of the food service industry or the food processing or manufacturing industry, any food products under or by reference to the mark “Chefs Pantry”.

2. In accordance with O 38, r 1 of the Federal Court Rules the amount which the respondents should be ordered to pay to the applicant be ascertained by the District Registrar, or a Deputy District Registrar, of the Victorian Registry of the Court.

3. The issue of costs be reserved to be determined on a date to be fixed.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

|

IN THE FEDERAL COURT OF AUSTRALIA |

GENERAL DISTRIBUTION |

|

V679 of 2001 |

|

BETWEEN: |

CAMPBELLS CASH & CARRY PTY LTD (ACN 000 226 399) APPLICANT

|

|

AND: |

BIDVEST AUSTRALIA PTY LTD (ACN 000 228 231) FIRST RESPONDENT

|

|

|

BIDVEST (VICTORIA) PTY LTD (ACN 053 695 855) SECOND RESPONDENT

|

|

JUDGE: |

WEINBERG J |

|

DATE OF ORDER: |

14 SEPTEMBER 2001

|

|

WHERE MADE: |

MELBOURNE |

IN PROCEEDING V679 of 2001, THE COURT ORDERS THAT:

1. On and from 17 September 2001, the respondents be restrained, whether by themselves or their officers, servants or agents or howsoever otherwise, from selling, supplying or offering for sale or supply or advertising or promoting for sale or supply, in Victoria, to members of the food service industry or the food processing or manufacturing industry, any food products under or by reference to the mark “Chefs Pantry”.

2. In accordance with O 38, r 1 of the Federal Court Rules the amount which the respondents should be ordered to pay to the applicant be ascertained by the District Registrar, or a Deputy District Registrar, of the Victorian Registry of the Court.

3. The issue of costs be reserved to be determined on a date to be fixed.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

V599 of 2001 |

|

BETWEEN: |

MARLEEF PTY LTD (ACN 081 561 435) APPLICANT

|

|

AND: |

METCASH TRADING LIMITED (ACN 000 031 569) FIRST RESPONDENT

|

|

|

METCASH HOLDINGS PTY LTD (formerly known as JOHN LEWIS FOODSERVICE PTY LTD) (ACN 004 380 152) SECOND RESPONDENT

|

|

|

CAMPBELLS CASH & CARRY PTY LTD (ACN 000 226 399) THIRD RESPONDENT

|

|

|

|

|

|

V679 of 2001 |

|

AND BETWEEN: |

MARLEEF PTY LTD (ACN 081 561 435) APPLICANT

|

|

AND: |

BIDVEST AUSTRALIA PTY LTD (ACN 000 228 231) FIRST RESPONDENT

|

|

|

BIDVEST (VICTORIA) PTY LTD (ACN 053 695 855) SECOND RESPONDENT

|

|

JUDGE: |

|

|

DATE: |

|

|

PLACE: |

REASONS FOR JUDGMENT

background

1 These are two applications brought by Marleef Pty Ltd (“Marleef”) against a number of respondents. The two proceedings raise three causes of action against each of the respondents:

· breach of s 52 of the Trade Practices Act 1974 (Cth);

· breach of s 53(c) of the Trade Practices Act; and

· the common law tort of passing-off.

2 All of the parties are involved, at a non-retail level, in the food service industry as either manufacturers, wholesalers or wholesale distributors of food products. The purchasers and prospective purchasers of the products are members of the food manufacturing and food processing industry including caterers, hoteliers, canteen operators, restaurateurs, retirement home operators, bakers, and sandwich and pie makers.

The Applicant

3 Marleef was incorporated in 1998. It is a food manufacturer and wholesaler, trading under the business name “Chef’s Pantry”. The business name was registered in 1988 and was transferred to the applicant in 1989, and Marleef has been involved in selling fresh cut and processed food products since that time. Every product sold by Marleef bears the distinctive mark shown below:

That is the only mark which Marleef applies to the goods which it sells. The mark is not registered as a trade mark under the Trade Marks Act 1995 (Cth).

4 The fresh food products sold include, for example, sliced tomatoes, sliced asparagus spears, fresh carrots, diced beetroot, tuna salads and fresh vegetable mixes. Marleef also sells, under its “Chef’s Pantry” mark, chargrilled capsicum and other vegetables for antipasto, “vegieburgers” and “value added products” such as lasagne, ravioli, and cannelloni, and . shelf-stable soups, frozen soups and sauces. It has recently begun to sell frozen liquid soup stocks. However, these are not sold under the “Chef’s Pantry” mark.

5 Marleef’s products are generally supplied in blue polythene bags bearing the “Chef’s Pantry” mark in stylised form in black printing. Its salad range is sold in clear vacuum packaged plastic bags with printed adhesive labels while its fresh and frozen soups are sold in four litre clear plastic bags with white printed adhesive labels. Some new lines are sold in white PVC buckets with a black and white label on the lid.

6 Marleef’s “Chef’s Pantry” mark appears on adhesive labels, wrapping, packaging, bags, cartons, signs, stationery, product lists and in its advertising and promotional material. It also displays the mark on its business cards and on its “Chef’s Pantry” website. It promotes the mark by direct mail, and by inclusion within shopping guides, directories and catalogues.

7 It is significant to note that Marleef does not package its products in tins. Nor does it utilise packaging which contains combinations of colours such as red, white and blue. It does not sell any of a range of products, including ice-cream, coconut cream, margarine, cotton seed or vegetable oil, pink or red salmon, tuna in brine, or any non-edible products such as bleach or laundry products.

The Respondents

8 The respondents fall into two groups. The first group consists of the respondents in proceeding V599 of 2001. The first respondent in that proceeding is Metcash Trading Ltd (“Metcash”). The second respondent, Metcash Holdings Pty Ltd (formerly known as John Lewis Foodservice Pty Ltd) (“John Lewis”) is a wholly owned subsidiary of Metcash, as is the third respondent, Campbells Cash & Carry Pty Ltd (“Campbells”).

9 Metcash is a listed public company. It was restructured in 2000, and until June of this year it operated four distinct food and beverage supply or distribution/retail operations in Australia:

· John Lewis Foodservice Pty Ltd;

· Campbell’s Cash & Carry Pty Ltd;

· IGA Retail Distribution (“IGA”); and

· Australian Liquor Marketers (“ALM”).

10 The second group consists of the respondents in proceeding V679 of 2001. The first respondent in that proceeding, Bidvest Australia Ltd, is the parent company of the second respondent, Bidvest (Victoria) Pty Ltd (“Bidvest”).

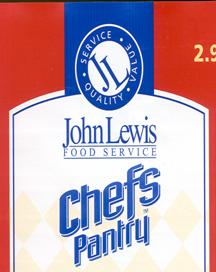

11 On 4 June 2001, Bidvest purchased the business name, goodwill, stock in trade and other assets of the business carried on in Victoria by John Lewis, including the “John Lewis” brand name. That brand name is signified by a logo consisting of a blue circular mark containing the letters “JL” (“the “JL” logo”). In about January 2001, Metcash began using a “Chefs Pantry” mark (with a chef’s hat).

12 It used that mark together with the “JL” logo on a range of food products. Bidvest’s purchase included a quantity of stock bearing that logo, in conjunction with that mark.

13 It should be noted that the sale by Metcash to Bidvest of the John Lewis business excluded any right or title to, or interest in, the John Lewis “Chefs Pantry” mark. It also excluded any right or title to, or interest in, the Australian trade mark application for that mark which had been lodged by Metcash.

14 It was accepted by Marleef that the “Chefs Pantry” name and logo adopted by Metcash was independently conceived by its internal advertising department in conjunction with external consultants. It was no part of Marleef’s case that Metcash had copied or been influenced by the applicant’s “Chef’s Pantry” mark in arriving at its own “JL” logo “Chefs Pantry” mark.

15 When Metcash sold the John Lewis business to Bidvest it retained John Lewis Food Service Pty Ltd. On 26 June 2001, Metcash renamed that company Metcash Holdings Pty Ltd. The John Lewis business acquired by Bidvest comprises a national operation of twelve branches. It supplies food products to the food service industry, e.g. hotels, restaurants, hospitals, airlines, fast food outlets, bakeries, sporting venues, schools, universities and major corporate caterers. It does not supply products to food manufacturers or food processors.

16 John Lewis’ “Chefs Pantry” range of products include:

· tinned asparagus spears 425 grams;

· tinned coconut cream 400 ml;

· tinned whole peeled tomatoes;

· tinned beetroot;

· tinned crushed chunky tomatoes;

· tinned pink salmon 415 grams;

· tinned red salmon 415 grams;

· tinned tuna in brine 425 grams;

· vanilla ice cream 11 litres;

· blended vegetable oil 20 litres;

· blended cotton seed oil 20 litres;

· margarine 1 kilogram; and

· margarine 10 kilogram.

17 These products are sold in small quantities suitable for use in the food service industry and not in bulk volumes suitable for food manufacturers or processors. The products are all packaged in tins, except for margarine and ice cream which are packaged in white plastic containers. They are sold in predominantly red packaging with the John Lewis logo in blue and white.

18 The total sales revenue for John Lewis for the financial years ending April 1999 and April 2000 exceeded $305 million. Its entire range of products also includes dry goods, paper products, dairy goods, confectionary, frozen and shelf foods, cleaning supplies and beverages.

19 Campbell’s is a distributor and wholesaler (via its warehouses) of a range of goods to Australian businesses. These goods include groceries, liquor products, confectionary, stationery, dairy/frozen goods, cigarettes, tobacco, soft drink and general merchandise. Its product range includes approximately 12,000 individual lines. These products are available to businesses and approved trade customers. It does not carry fresh processed vegetables. Nor, in general, does it stock fresh produce. Its target customers are members of the food service industry and small business. Campbells commenced stocking the “JL” logo “Chefs Pantry” products in March 2001.

20 In about April 2001 John Lewis released two catalogues, “Easter 2001” and “April 2001”. Each of these catalogues displayed a range of goods prominently marked “Chefs Pantry”. These included tins of tomatoes and tins of asparagus spears. Campbell’s has also promoted and sold “JL” logo “Chefs Pantry” products.

21 After Bidvest acquired the John Lewis business on 4 June 2001, it continued for a short time to sell “JL” logo “Chefs Pantry” products. In mid-June, it issued a directive to all branches to cease selling products so marked.

22 On 4 July 2001, Bidvest gave an undertaking to the Court that it would not (until the final hearing and determination of these proceedings) sell or otherwise dispose of any stock branded with the “Chefs Pantry” name other than to return that stock to Metcash. By mid-July 2001 all “JL” logo “Chefs Pantry” stock had been returned, and Bidvest had stopped supplying it. Bidvest maintained that it had never been its intention to continue to sell the “Chefs Pantry” stock. It had acquired the “JL” logo, but had never acquired the “Chefs Pantry” mark. The John Lewis stock which had come to it as part of the purchase of the business had included a small quantity of “JL” logo “Chefs Pantry” stock, and Bidvest had never proposed to do any more than off-load that stock.

23 Bidvest knew that Metcash retained a quantity of “JL” logo stock in its Campbell’s warehouses. That “JL” logo stock included some items which were also branded with the “Chefs Pantry” mark. Bidvest was content for Metcash to sell the “JL” logo stock during a transitional period. According to Bidvest’s Managing Director, that transitional period might have extended for anything up to six months.

24 Bidvest was aware when it acquired the John Lewis business that Metcash had prepared a July 2001 catalogue for that business. That catalogue included a wide range of products including some “JL” logo “Chefs Pantry” products. After Bidvest gave its undertaking to the Court, it “quarantined” those “Chefs Pantry” products by directing that none were to be sold.

relief sought by the applicant

25 The applicant seeks, inter alia, the following relief from this Court:

· an injunction restraining each of the respondents from selling, supplying or advertising or promoting for sale or supply, in Australia, to members of the food service industry or the food processing and manufacturing industry, any food products under or by reference to the name “Chefs Pantry” (with or without a hat device);

· delivery up of all products and promotional material bearing that mark;

· a mandatory injunction requiring the respondents to cause to be published a notice correcting the effect of any misleading or deceptive conduct on their part;

· damages or alternatively an account of profits;

· interest; and

· costs.

the issue to be determined

26 On 4 July 2001, I made orders confining the trial of each proceeding to “liability” only. I also ordered that both proceedings be heard together, and that the evidence in each proceeding stand as evidence in the other.

27 Although a substantial body of evidence was led during the course of the trial, it was apparent from the outset that there was really only one issue to be resolved.

28 Mr Caine, who appeared for the respondents in both proceedings, made an open offer on the first day of the trial, to consent to an injunction in the following terms:

“On and from 17 September 2001, the First, Second and Third Respondents in Proceeding No. V599 of 2001 and the Respondents in Proceeding V679 of 2001 (together “the Respondents”) be restrained, whether by themselves or their officers, servants or agents or howsoever otherwise, from selling, supplying, offering for sale or supply, or advertising or promoting for sale or supply, in Victoria, to members of the food services industry or the food processing and manufacturing industry, any food products under or by reference to the mark “Chefs Pantry”. (emphasis added)

29 Mr Caine conceded that there was an arguable case that the respondents, by their use of the “Chefs Pantry” mark, had contravened ss 52 and 53(c) of the Trade Practices Act, and had also committed the tort of passing-off. That concession was qualified, however, and was specifically limited to the respondents’ use of the mark in Victoria. Mr Caine denied that the respondents, by their use of the mark outside Victoria, had contravened those provisions of the Trade Practices Act, or that they had committed the tort of passing-off in any other part of Australia. He submitted that Marleef was not entitled to any relief arising out of the respondents’ conduct going beyond what the respondents were prepared to offer.

30 It follows that the only issue to be resolved in these proceedings is the width of any injunction to be granted to Marleef restraining the respondents from using the “Chefs Pantry” mark, and ultimately the quantum of any damages to which Marleef may be entitled.

The Applicant’s case

31 Ms Tate, who appeared on behalf of Marleef, relied upon a body of evidence in support of her contention that the applicant had a presence outside Victoria or, as she described it, an “Australia wide reputation”, which warranted an injunction restraining the respondents from supplying, in Australia, to members of the food service industry or the food processing and manufacturing industry, any food products under or by reference to the mark “Chefs Pantry”. That evidence included:

· sales by Marleef to interstate customers;

· the supply of goods to interstate entities and national chains;

· enquiries made of Marleef by interstate entities;

· the supply of goods by interstate entities to Marleef;

· negotiations entered into by Marleef with interstate entities and national chains;

· hits upon Marleef’s website;

· general customer and contact lists revealing interstate and international customers;

· facsimiles transmitted to interstate entities; and

· e-mail transmissions sent to interstate entities.

32 The principal witness in support of Marleef’s case was Mr Andrew Grunfeld, the applicant’s Managing Director. He affirmed a number of affidavits. In the first of these, he asserted that Marleef “regularly” sold food products not only in Victoria but also in New South Wales, South Australia, Western Australia and Tasmania. He included a list of Marleef’s “regular” customers. That list contained, however, only four interstate entities, two in New South Wales, one in South Australia and one in Western Australia. He also listed interstate customers and enquiries from 1999 to 2001.

33 Mr Grunfeld’s evidence concerning the interstate activities of Marleef may be broadly summarised as follows:

· In 1999 a business plan was prepared by Mr Grunfeld’s son, Mr Daniel Grunfeld. He is the applicant’s Sales and Marketing Manager. The business plan is a confidential exhibit in this proceeding, and I will not refer to it in any detail. It can be said, however, that it described the main area of supply for Marleef as being within 90 kilometres of the Victorian central business district. It also referred to some of the larger companies supplied by “Chef’s Pantry” being based in Victorian country towns. It noted that “Chef’s Pantry” had focused upon the local market, i.e. the State of Victoria. It identified two other States as potential areas for expansion, and observed that some products were already being distributed in those States. It is significant that there was no mention in the plan of any potential sales by Marleef in any other State.

· “Chef’s Pantry” products had been supplied to customers in New South Wales, South Australia, Western Australia and Tasmania. These products included vegetable burgers, block frozen asparagus, potatoes and potato skins, garlic, onions and ginger.

· Marleef had sold products to national and international companies including a number known to have distribution outlets in other States.

· Marleef had engaged in negotiations with a national supermarket chain and national food suppliers.

· Organisations based interstate had made enquiries of Marleef with a view to purchasing food products.

· A number of interstate companies involved in the food service industry had supplied raw materials to Marleef.

· The “Chef’s Pantry” website received some 200 hits a week, including 50-75 from within Australia.

· Marleef’s customer and contact lists included a number of interstate and international organisations.

34 Ms Tate submitted that the applicant and the respondents were competitors in the supply of food products to the food service industry and the food manufacturing and processing industry. She relied upon the evidence of four witnesses, each of whom had worked in the food service industry for many years and who had dealt with the applicant’s “Chef’s Pantry” business during that time. Those witnesses all said that when they saw the respondents’ “JL” logo “Chefs Pantry” mark, they initially believed that there was a link between the product bearing that mark, and the applicant’s product. She invited me to conclude that although these four witnesses resided in Victoria, and had dealt with the applicant for many years, their evidence applied with equal force to persons in those industries outside Victoria. The fact that they may not have had any dealings with the applicant because of its limited activities outside this State was said to be merely a matter of weight.

The Respondents’ case

35 Mr Caine submitted that although a number of documents suggested that Marleef may have carried out a few sales outside Victoria, there was no evidence, apart from that of Mr Andrew Grunfeld, that Marleef, using the name “Chef’s Pantry”, had any significant presence in any other State. Marleef had called no witnesses from outside Victoria to give evidence of having been aware of its business, or even of having heard of “Chef’s Pantry”. The respondents, on the other hand, had called a number of witnesses involved in the food service industry from outside Victoria, who were unaware of Marleef, and who knew nothing of “Chef’s Pantry”.

36 Mr Caine submitted that Mr Grunfeld’s evidence fell far short of establishing that the “Chef’s Pantry” mark and business were known by any relevant persons outside Victoria. He referred separately to the position in each State.

Queensland

· No sales by Marleef to the food manufacturing or food service industry.

· No evidence that Marleef’s suppliers (such as they were) had any more than a bare knowledge of the “Chef’s Pantry” business.

· No evidence that those suppliers would be likely to be confused about the origin of the “JL” logo “Chefs Pantry” products.

· No evidence that any enquiries had resulted in the supply of product by Marleef.

Tasmania

· Several sales by Marleef to a customer in the food manufacturing industry amounting to no more than a “few hundred dollars”, two or three times a year.

· That customer used Marleef’s product as an ingredient and did not on-sell it under the name “Chef’s Pantry”.

· No sales to the food service industry.

· One company supplied vegetables to Marleef on three occasions in 2000.

· No evidence of any enquiries.

Western Australia

· One sale by Marleef to a customer in the food manufacturing industry in 1999, one sale in 2000, and none in 2001.

· No evidence that the final product was on-sold under the name “Chef’s Pantry”.

· No sales to the food service industry.

· No supplies to Marleef.

· One enquiry.

South Australia

· Several sales of bulk quantities of crushed garlic by Marleef to a customer in the food manufacturing industry in 2000.

· No evidence that the final product was on-sold under the name “Chef’s Pantry”.

· No sales to the food service industry.

· Three companies supplied product to Marleef.

· Two enquiries, one of which resulted in the above sales.

New South Wales

· A customer in the food manufacturing industry purchased a quantity of asparagus in either 1998 or 1999. That product was on-sold, under the name “Chef’s Pantry”, to another entity. That entity used the asparagus as an ingredient, and did not on-sell it under that name.

· A second customer in the food manufacturing industry purchased a quantity of diced onions and crushed ginger in 2000 and possibly some additional product in 2001.

· No sales to the food service industry.

· There were sales, commencing in mid-2001, to a food processor which supplies supermarket chains in New South Wales.

· In previous years Marleef sold “vegieburgers” to a distributor for on-sale to supermarkets in New South Wales and the Australian Capital Territory. Those sales ceased in 1999.

· “Vegieburgers” do not form any part of the “JL” logo “Chefs Pantry” range.

· One company supplied product to Marleef.

· Eleven entities have made enquiries of Marleef with a view to purchasing its product.

· No evidence of any sales having resulted from these enquiries, other than sales in Victoria.

37 Mr Caine then made a more general point concerning the correspondence tendered on behalf of Marleef which demonstrated it had been in negotiations with various entities. He noted that in all but two instances the negotiations were with Victorian companies. Negotiations with a Brisbane based company had been conducted through that company’s office at Knoxfield in Victoria. Negotiations with a New South Wales based company had not resulted in any sales.

38 Mr Caine also made submissions concerning Marleef’s dealings with some twenty entities which trade outside Victoria. He pointed out that the dealings in each case were with a Melbourne or Victorian based contact. Fifteen of the twenty entities were food manufacturers, and only three were in the food service industry. No evidence had been led, on behalf of Marleef, from any representative of the twenty entities.

39 Mr Caine then made submissions concerning Marleef’s correspondence with “other national suppliers” in the food service industry. Beyond establishing that those entities had been in contact with Marleef, he submitted that the correspondence did not assist the applicant’s case. All but two of these entities were from Victoria, and in relation to the two which were not, the correspondence was of no probative value. No evidence had been led, on behalf of Marleef, from any representative of these two entities.

40 Mr Caine submitted that the evidence of the four witnesses who said that they had been misled by the respondents’ use of the “Chefs Pantry” mark was of no assistance to the applicant in seeking to demonstrate that prospective customers outside Victoria would be similarly misled. He noted that the four witnesses had had extensive dealings with the applicant’s mark over many years, and their position did not equate with any person outside this State unfamiliar with that mark.

41 The last matter addressed by Mr Caine was the tender of a “Chef’s Pantry” database print-out intended to show that there had been extensive facsimile and e-mail contact with interstate entities. He submitted that the evidence concerning the facsimile transmissions did not establish that they had been made in the form in which the sample facsimile tendered appeared. The evidence concerning the e-mail contact was of little probative value because of its uninformative nature.

Submissions regarding Mr Grunfeld’s credibility

42 Mr Caine submitted that Mr Grunfeld was a witness who had significantly exaggerated the extent to which Marleef had established an interstate presence or reputation.

43 The attack upon Mr Grunfeld’s credibility was based upon evidence which he gave regarding the use by an employee at Campbell’s of the name “Chefs Pantry” and also upon evidence which he gave concerning the use of the Metcash Consumer Support Centre hotline.

44 Mr Grunfeld said that when visiting Campbell’s Cash & Carry store at Clayton “on or about” 5 May 2001:

“… a telephone rang and a lady answered it saying words to the effect Chefs Pantry, can I help you?”

45 There was evidence on behalf of the respondents from Mr Joseph Lepuschan, the Store Manager, that soon after receiving a Head Office memorandum concerning telephone policy, on 5 December 2000, he circulated that memorandum to all staff members with a direction that they should answer the telephone “Campbell’s Clayton” or “Campbell’s”. Mr Lepuschan said that to the best of his knowledge all staff members at the store followed that direction. He was not required for cross-examination on his affidavit.

46 Ms Jenny McQueen, a casual employee who had worked at the store on 5 May 2001 said that she had never answered the telephone with the words “Chefs Pantry”. She too was not required for cross-examination.

47 Mr Caine submitted that Mr Grunfeld’s evidence regarding this matter defied credulity. It was astonishing that Mr Grunfeld had not made a contemporaneous note of what he claimed was said. His son, Mr Daniel Grunfeld, had accompanied him to the store and may have been in a position to overhear what was said. However, his son had made no diary entry concerning this event, and was not called to corroborate his father’s account.

48 The second matter relied upon by Mr Caine in his attack upon Mr Andrew Grunfeld’s credibility was the evidence which he gave concerning a telephone call that he made to the “Chef’s Pantry/Essential Customer Support Centre” on 1300 135 690. He said that his call was answered by a female operator saying “Chefs Pantry”. Mr Grunfeld referred to that number as being one which appeared on page 3 of the April 2001 catalogue.

49 It was suggested to Mr Grunfeld in cross-examination that he had referred to the number in that way rather than to the number which appeared on page one of the catalogue to deflect attention from the fact that the same telephone number appeared prominently on the front page of the catalogue and was the number for the Consumer Support Centre hotline for all business units of Metcash.

50 The respondents relied upon the evidence of Mr Steven Newton, the National Technical Services Manager for Metcash responsible for coordinating the Metcash Consumer Support Centre hotline. Mr Newton said that the hotline operated 24 hours a day, 7 days a week. Ms Emma Pimm normally manned the support line, but when she was unavailable it would divert to Mr Newton’s office number or to his mobile telephone. Mr Newton pointed out that the Consumer Support Centre hotline was a support line for all business units of Metcash. It was not a hotline dedicated to “JL” logo “Chefs Pantry” products. The hotline serviced not only John Lewis but also Campbell’s, IGA, and ALM. Those business units sold many thousands of different product lines under different names. Mr Newton said that he had never answered the support line with the greeting “Chefs Pantry”. He was not challenged regarding that evidence. Ms Pimm said that she had never answered an enquiry on the support line by saying “Chefs Pantry”. Her evidence too was not challenged.

51 Ms Tate did not make any submissions regarding Mr Grunfeld’s credibility. That was not altogether surprising. Mr Caine’s cross-examination was extremely effective and, in my view, demonstrated that Mr Grunfeld cannot be regarded as a reliable witness. The evidence which he gave concerning the two telephone conversations was inherently implausible, and his refusal to acknowledge the difficulties associated with the account which he gave did him little credit. The applicant’s case regarding its “Australia wide” reputation depends, in part, upon my accepting Mr Grunfeld’s testimony. I regret that I cannot accept that testimony save where it is uncontentious, or is independently supported by documentary evidence.

The applicant’s failure to call Mr Daniel Grunfeld

52 I also regard the failure to call Mr Daniel Grunfeld to give evidence as being of particular significance in this case. It is clear that he was the person primarily responsible for the development within Marleef of the business plan, and that he played an important role in establishing interstate contacts.

53 The evidence was that Mr Daniel Grunfeld was in Melbourne during the trial. Clearly, he could have been called to corroborate at least some aspects of Mr Andrew Grunfeld’s testimony. In accordance with the rule in Jones v Dunkel (1959) 101 CLR 298, the unexplained failure by Marleef to call him may lead to an inference that his evidence would not have assisted Marleef’s case. It should be noted that Mr Daniel Grunfeld affirmed an affidavit earlier in these proceedings. He is plainly in the camp of the applicant, and clearly has significant knowledge of matters of critical importance to these proceedings. In these circumstances, I infer that his evidence would not have assisted Marleef’s case.

the relevant legal principles

The Trade Practices claims

54 Section 52(1) of the Trade Practices Act provides:

“A corporation shall not, in trade or commerce, engage in conduct that is misleading or deceptive or is likely to mislead or deceive.”

55 Section 53(c) provides:

“A corporation shall not, in trade or commerce, in connexion with the supply or possible supply of goods or services or in connexion with the promotion by any means of the supply or use of goods or services:

…

(c) represent that goods or services have sponsorship, approval, performance characteristics, accessories, uses or benefits they do not have…”

56 An action brought pursuant to these provisions has many similarities to an action for passing-off. The elements of these causes of action are not, however, identical and the principles which govern the construction of these sections depend upon the language of the statute rather then common law analogues: Marks v GIO Australia Holdings Ltd (1998) 196 CLR 494. It has been said that s 52 provides “wider protection” than does the tort of passing off: Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd (1982) 149 CLR 191 at 205 per Mason J. See Red Bull Australia Pty Ltd v Sydneywide Distributors Pty Ltd [2001] FCA 1228 at [73] per Conti J. While that may be so, a particular case may give rise to liability under both the Trade Practices Act and the common law tort.

57 As a general rule, for conduct to be misleading or deceptive, the conduct must convey a misrepresentation: Taco Co of Australia Inc v Taco Bell Pty Ltd (1982) 42 ALR 177. Section 52 is not confined to conduct which is intended to mislead or deceive: Equity Access Pty Ltd v Westpac Banking Corporation (1990) ATPR 40-994 at 50, 950. A corporation which acts honestly and reasonably may nonetheless contravene the section: Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd (supra) at 197. Whether particular conduct is misleading or deceptive is a question of fact to be determined in the context of the evidence as to the alleged conduct and the relevant surrounding facts and circumstances.

58 It has been said that the words “likely to mislead or deceive” add little to the section. At most, they make it clear that it is unnecessary to prove that the conduct in question actually deceived or misled anyone. Conduct is likely to mislead or deceive if that is a real or not remote chance or possibility, regardless of whether it is more or less than fifty percent.

59 Section 52 is contained in Pt V which is entitled “Consumer Protection”. The section is intended to protect members of the public in their capacity as consumers of goods and services. It does not expressly state what persons or class of persons should be considered as the possible victims for the purpose of deciding whether the conduct is misleading or deceptive. It is clear, however, that consideration must be given to the class of consumers likely to be affected by the conduct. The matter must be considered by reference to all people who come within the relevant section of the public including the astute and the gullible, the intelligent and the not so intelligent, the well educated and the poorly educated: Taco Co of Australia Inc (supra). The section must be regarded as contemplating the effect of the conduct complained of on reasonable members of the class to which it is directed.

60 In George Weston Foods Ltd v Goodman Fielder Ltd [2000] FCA 1632, a case involving comparative advertising of bread, the relevant class was described as “consumers of bread” who have some interest in the fibre content of bread. See also Crago v Multiquip Pty Ltd (1998) ATPR 41-620.

61 In the present case, the relevant class may be described as members of the food manufacturing and food processing industry and members of the food service industry. It is important to note that these are not customers at the retail level.

62 Although it is not necessary to call evidence that such persons were in fact misled for the purpose of establishing objectively that the conduct was misleading, nevertheless such evidence is admissible to determine why persons were misled and to enable the court to determine how its discretion should be exercised in relation to granting injunctive relief. However, the court must make an objective assessment of whether the conduct contravened the section.

63 In relation to s 53(c), there are many examples of cases where corporations have been found to have falsely represented that their goods were associated with the goods of another. See generally ACI Australia Ltd v Glamour Glaze Pty Ltd (1988) 11 IPR 269 and Mark Foy’s Pty Ltd v TVSN (Pacific) Ltd (2000) 104 FCR 61.

64 It was agreed between the parties that the s 52 and 53(c) claims in the present case would be resolved in the same manner given that, for present purposes, there were no differences of any consequence between the sections.

65 Section 80 of the Trade Practices Act allows the court to grant injunctive relief if satisfied that a person has engaged, or is proposing to engage, in conduct that constitutes or would constitute a contravention of a provision in Pt V. It is clear that injunctive relief granted to restrain a contravention of ss 52 or 53(c) should be “limited to what is necessary in the circumstances of the particular case”: Taco Co of Australia Inc (supra) per Deane and Fitzgerald JJ at 207; Campomar Sociedad, Limitada v Nike International Ltd (2000) 169 ALR 677 at 707. Any injunction should be tailored to meet the case proven and to indicate clearly the conduct which is enjoined.

The Passing-Off claims

66 The tort of passing-off exists to prevent financial loss arising from the defendant’s representation that his goods or services are those of the plaintiff. The action seeks to protect the goodwill associated with the plaintiff’s business: Fletcher Challenge Ltd v Fletcher Challenge Pty Ltd [1981] 1 NSWLR 196. Although it has been said that the precise definition of the tort of passing-off is elusive, the authorities show that there is a need to establish reputation, misrepresentation and the likelihood of damage: Conagra Inc v McCain Foods (Aust) Pty Ltd (1992) 33 FCR 302 and Betta Foods Australia Pty Ltd v Betta Fruit Bars Pty Ltd (1998) ATPR 41-624 at 40, 839 per Goldberg J. There is no requirement of an intent to deceive and no need to prove fraud: Office Cleaning Services Ltd v Westminster Office Cleaning Association [1944] 2 All ER 269. It is sufficient that the defendant’s conduct is calculated or likely, rather than intended, to deceive. The test for determining that question is the likely impression on the casual and unwary customer, and it is no answer that an observant person making a careful examination would not have been misled. The appropriate standard is that of the typical customer for the goods in question.

67 The action protects the goodwill or reputation of the business of the first trader rather than the name, mark or get-up improperly used by the second trader: AG Spalding & Bros v AW Gamage Ltd (1915) 32 RPC 273.

68 It follows that the applicant must prove that the “get-up” under which its products have been sold has become associated in the minds of substantial numbers of the purchasing public, specifically and exclusively, with the applicant’s food products. If the answer to that question is in the affirmative, the applicant must demonstrate that the “get-up” under which the respondents market their food products amounts to a representation by the respondents that the products which they sell are the applicant’s products. If the answer to that question is in the affirmative, the applicant must demonstrate that it is likely that if the respondent is not restrained, a substantial number of members of the public will be misled into purchasing the respondents’ products in the belief that they are the applicant’s products: Vieright Pty Ltd v Myer Stores Limited (1995) ATPR 41-405 at 40, 493.

conclusions

69 These proceedings involve no complex questions of fact or law. The only issue raised for consideration was whether the conduct of the respondents contravened ss 52 and 53(c) of the Trade Practices Act by representing in States other than Victoria, that products sold under the “JL” logo “Chefs Pantry” mark were produced by, or emanated from, Marleef.

70 On the evidence before me, the applicant has failed to demonstrate that the “Chef’s Pantry” line of products which it sells is known, to any significant degree, outside Victoria by persons or entities involved in the food manufacturing and food processing industry, or in the food service industry. The applicant has also failed to demonstrate that it has acquired any significant goodwill outside Victoria, or that it has a reputation outside this State which it is entitled to protect through the tort of passing-off.

71 It was common ground between the parties that Marleef is entitled to injunctive relief, and possibly damages as well, to vindicate its rights arising out of the contraventions by the respondents of ss 52 and 53(c) of the Trade Practices Act. It was also accepted on behalf of the respondents that the tort of passing-off warranted injunctive relief, and possibly damages, in relation to the damage which may have been done to the applicant’s goodwill and reputation in Victoria.

72 As indicated earlier, it is plain that any injunction which is granted should be no wider than that which is warranted in the circumstances. In my view, the applicant is not entitled to the Australia wide injunction which it seeks. Marleef’s business has, for many years, focused upon Melbourne and regional Victoria. While it may have the hope or expectation that its business will, at some future stage, expand into other States, the evidence before me does not demonstrate that it has already done so. To the extent that Marleef is succeeding in making inroads into States other than Victoria, those inroads have to date been insubstantial. Marleef is not sufficiently well known outside Victoria to make it likely that the class of person to whom it wishes to sell its products will be misled or deceived by the use presently made, or potentially likely to be made, by the respondents of the “JL” logo “Chefs Pantry” mark.

73 It follows that although the respondents have contravened ss 52 and 53(c) of the Trade Practices Act by engaging in misleading or deceptive conduct and, in particular, by falsely representing in Victoria that the products sold by John Lewis were produced by, or emanated from the applicant, no such misrepresentation has occurred outside this State. The same is true of the applicant’s claim for passing-off.

74 The applicant’s claim for the wider injunctive relief which it seeks restraining the conduct complained of outside Victoria is refused.

75 I should add that after each side had closed its case in these proceedings, Ms Tate sought leave to amend the statement of claim in the proceeding against Bidvest in order to enable Marleef to rely upon s 75B of the Trade Practices Act. She acknowledged that if I found that the applicant did not have a sufficient presence in States other than Victoria to warrant the grant of an Australia wide injunction in the primary proceeding against Metcash, there would be no basis upon which Bidvest could be derivatively liable, under s 75B, for any contraventions of the Act in those other States. I have found against the applicant in that regard. Accordingly, it is unnecessary to deal with the application for leave to amend.

76 The respondents have consented to the grant of injunctive relief limited to restraining them from contravening the Trade Practices Act and committing the tort of passing-off by supplying their product under the “Chefs Pantry” mark in Victoria. Bivest has made it clear that it has no present or future interest in that mark. In these circumstances, I consider it appropriate to grant the limited form of injunctive relief agreed to by the respondents.

77 Having found that the respondents are liable to pay damages, O 38 of the Federal Court Rules provides that if I consider that the amount of damages to be recovered is substantially a matter of calculation, I may direct that the amount which they shall be ordered to pay be ascertained by the Registrar. This power cannot be exercised where the calculation requires the Registrar to determine facts and exercise judgment: Gordon M Jenkins v Coleman (1989) 23 FCR 38. I have found that the respondents are liable to pay damages to the applicant arising out of their use, in Victoria, since about January of this year, of the mark “Chefs Pantry” on various of their food products. I consider that the Registrar is in a position, based on that finding, to calculate the amount of damages which should be awarded, in accordance with the principles which govern the award of damages in cases of this type. The calculation is likely to involve a number of contentious matters, but that alone is not a reason why that task cannot be delegated to a Registrar.

78 Each side has had a measure of success in these proceedings. The quantum of damages to be awarded to the applicant has yet to be determined. In these circumstances, my preliminary view is that the issue of costs should be reserved to be determined on a date to be fixed.

|

I certify that the preceding seventy-eight (78) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Weinberg. |

Associate:

Dated: 14 September 2001

|

In Proceeding No V599 of 2001: |

|

|

Counsel for the Applicant: |

Ms P. Tate |

|

|

|

|

Solicitor for the Applicant: |

Phillips Ormonde & Fitzpatrick Lawyers |

|

|

|

|

Counsel for the Respondents: |

Mr B.N. Caine |

|

|

|

|

Solicitor for the Respondents: |

Griffith Hack Lawyers |

|

In Proceeding No V679 of 2001: |

|

|

Counsel for the Applicant: |

Ms P. Tate |

|

|

|

|

Solicitor for the Applicant: |

Phillips Ormonde & Fitzpatrick Lawyers |

|

|

|

|

Counsel for the Respondents: |

Mr B.N. Caine |

|

|

|

|

Solicitor for the Respondents: |

Griffith Hack Lawyers |

|

|

|

|

Dates of Hearing: |

3, 4, 5, 6 and 7 September 2001 |

|

|

|

|

Date of Judgment: |

14 September 2001 |