FEDERAL COURT OF AUSTRALIA

Smith v State Bank of NSW Limited [2001] FCA 946

TRADE PRACTICES – misleading and deceptive conduct – bank issued certificate of accreditation to accountant – certificate represented accountant had been assessed by bank for competency and was competent to provide professional advice – accountant an undischarged bankrupt with convictions for fraud – whether representation misleading or deceptive – applicants invested funds in company controlled by accountant – investment a sham – whether representation caused loss – whether a substantial consideration or real inducement

NEGLIGENCE – negligent misstatement – economic loss – bank issued certificate representing that accountant had been assessed for competency and was competent to provide professional advice – accountant an undischarged bankrupt with convictions for fraud – applicants relied on representation in certificate – invested funds in company controlled by accountant – investment a sham – whether bank owed applicants a duty of care – bank realised customers of accountant would act in reliance on representation in connection with matter of business or serious consequence – whether reliance reasonable – whether breach of duty – whether bank took reasonable steps to ensure representations in certificate were accurate

Trade Practices Act 1974 (Cth) ss 52, 53, 82

Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd (1982) 149 CLR 191, applied

Ricochet Pty Ltd v Equity Trustees Executors and Agency Company Ltd (1993) 41 FCR 229, applied

Como Investments Pty Ltd (In liquidation) v Yenald Nominees Pty Ltd (1997) 19 ATPR 41-550, applied

Neilsen v Hempston Holdings Pty Ltd (1986) 65 ALR 302, cited

Sutton v A J Thompson Pty Ltd (in liq) (1987) 73 ALR 233, cited

Henjo Investments Pty Ltd v Collins Marrickville Pty Ltd (No 1) (1988) 39 FCR 546, cited

Tepko Pty Ltd v Water Board [2001] HCA 19; (2000) 75 ALJR 775, applied

TERENCE SPENCER SMITH AND SUSAN JOAN SMITH v STATE BANK OF NSW LIMITED

V 473 of 2000

GRAY J

20 JULY 2001

MELBOURNE

|

IN THE FEDERAL COURT OF AUSTRALIA |

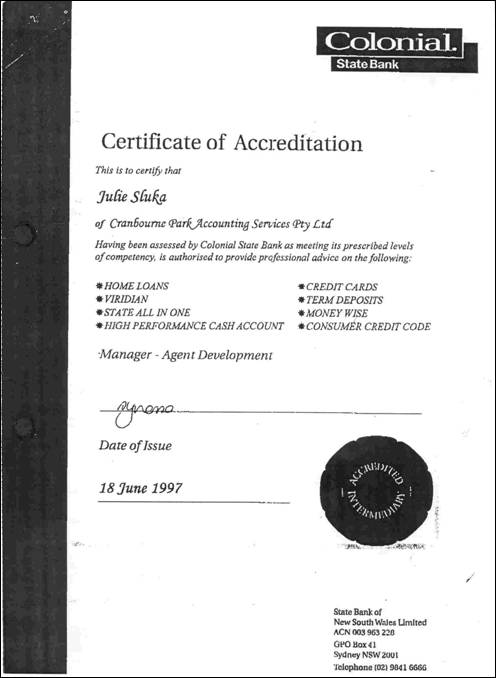

|

|

VICTORIA DISTRICT REGISTRY |

V 473 of 2000 |

|

BETWEEN: |

TERENCE SPENCER SMITH FIRST APPLICANT

SUSAN JOAN SMITH SECOND APPLICANT

|

|

AND: |

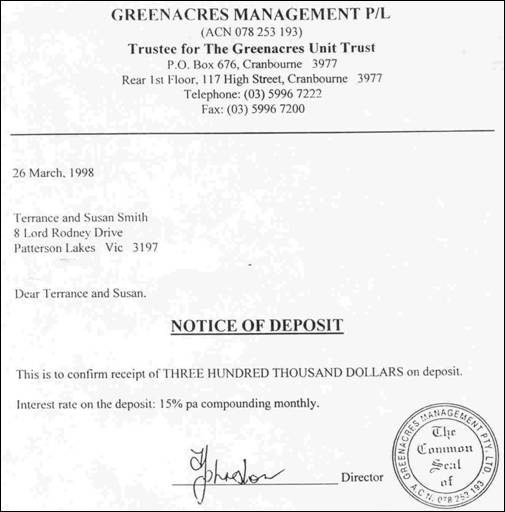

STATE BANK OF NSW LIMITED (ACN 003 963 328) RESPONDENT

|

|

JUDGE: |

GRAY J |

|

DATE OF ORDER: |

20 JULY 2001 |

|

WHERE MADE: |

MELBOURNE |

THE COURT ORDERS THAT:

1. Judgment be entered for the applicants against the respondent in the sum of $380,186.30, including the sum of $80,186.30 by way of interest.

2. The respondent pay the applicants’ costs of the proceeding.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

V 473 of 2000 |

|

BETWEEN: |

FIRST APPLICANT

SUSAN JOAN SMITH SECOND APPLICANT

|

|

AND: |

STATE BANK OF NSW LTD (ACN 003 963 328) RESPONDENT

|

|

JUDGE: |

|

|

DATE: |

|

|

PLACE: |

REASONS FOR JUDGMENT

1 The applicants are a couple who emigrated from England. They arrived in Australia on 11 March 1998. A little over a fortnight later, on 27 March, they placed $300,000 in the hands of a dishonest taxation and business consultant for investment. They have been unable to recover that sum, either from the dishonest consultant or from the company in which the funds were to be invested. They now seek to recover that amount from the respondent bank. They rely on allegations of misleading and deceptive conduct in contravention of s 52 of the Trade Practices Act 1974 (Cth) (“the Trade Practices Act”), contraventions of s 53(c) and (d) of the Trade Practices Act and common law negligent misstatement.

2 In 1997, Douglas Gordon Johnston was an undischarged bankrupt. His period of bankruptcy commenced on 24 August 1994 and he was discharged from bankruptcy by operation of law on 17 February 1998. Mr Johnston had previously been adjudicated bankrupt for a period commencing on 11 December 1984. He also had a criminal record, which included conviction in 1989 on nine counts of acting as an unregistered tax agent and conviction in 1990 on four counts of obtaining property by deception and two counts of managing a corporation whilst insolvent. In respect of the offences of obtaining property by deception, he was sentenced to three months’ imprisonment on each count, the sentences to run concurrently. He was also sentenced to perform 300 hours of unpaid community work.

3 By 1996, Mr Johnston was operating a business as a taxation and business consultant, and an accountancy practice, in conjunction with his then de facto wife, under the name Hrusa Park Accounting Services Pty Ltd. The practice was conducted from premises at the rear of 117 High Street, Cranbourne. As a result of a breakdown in the relationship between Mr Johnston and his de facto wife, another company was formed to conduct the practice. This company was called Cranbourne Park Accounting Services Pty Ltd (“CPAS”). It was incorporated on 12 November 1996. Its sole director and secretary was Ross Zagari. Mr Zagari was a registered tax agent, who conducted an accounting and taxation consultancy business in Essendon.

4 Mr Johnston was the manager of the practice conducted by CPAS. Julie Sluka (formerly Julie Finck) was employed as a receptionist and bookkeeper. She was paid at a casual rate, but her attendance at the office was generally in excess of normal full-time working hours. She seems to have been responsible for the administration of the office. Also associated with the business was Phillip Viney (now known as Phillip Rowse). He had put to Mr Johnston a business proposition that he (Mr Viney) would canvass small businesses to become clients of CPAS on the basis that their books would be kept by CPAS for a fee. Mr Viney persisted in this endeavour until July or August 1997, when he became concerned that CPAS was not attending promptly to the work required for the clients he had brought into the office. He then left.

5 As well as Mr Johnston, Ms Sluka and Mr Viney, CPAS employed several other persons who worked in an open plan office. Although he was a director, and the only registered tax agent associated with CPAS, Mr Zagari rarely attended the office. Throughout Ms Sluka’s employment, she never saw him in the office and she was made aware that he had visited only on two or three occasions while she was out of the office. All tax returns prepared in the office were sent by courier to Mr Zagari’s office in Essendon so that he could sign them as a registered tax agent before they could be lodged.

6 Mr Johnston also had associations with a number of other companies. These associations were not formal, probably because of his status as an undischarged bankrupt. In the case of some companies, members of Mr Johnston’s family were directors. C & D Furniture Makers Pty Ltd and The Complete Furniture Specialists Pty Ltd were engaged in manufacturing and selling furniture respectively. Kazakhstan International Pty Ltd was apparently formed to take advantage of cheap labour opportunities in Kazakhstan by importing furniture made there. Kebab Central Pty Ltd apparently sold prepared food. Tolmie Views Pty Ltd was a company through which Mr Johnston proposed to establish a winery in rural Victoria.

7 From the point of view of this proceeding, the most significant of the other companies with which Mr Johnston was associated was Greenacres Management Pty Ltd (“Greenacres Management”). His daughter Fiona Johnston was a director of this company from 18 April 1997, when it was incorporated and began to trade as an investment fund. Its liquidator has since described the nature of its investment activity as investing in real estate and loans advanced to individual and corporate borrowers. Funds were sourced from individual and superannuation investors, many of whom were clients of CPAS. Greenacres Management acted as trustee for three separate trust funds, known as The Greenacres Unit Trust, The Cranbourne Park Universal Superannuation Fund and The Dreams Come True Trust.

8 In truth, Greenacres Management was a means by which Mr Johnston channelled funds from clients of CPAS who could be persuaded to invest in it to the other business ventures with which he was concerned. Mr Johnston had what was described as a “prospectus”, which he gave or showed to people to persuade them to invest money in Greenacres Management. The document consisted of a letter on the letterhead of CPAS, with attached documents. It was put together by Ms Sluka in the office of CPAS. The attachments included a profit and loss statement for The Greenacres Unit Trust, indicating that it had suffered a net loss of $3,976 in the period to 30 June 1997, and a balance sheet showing net assets as at 31 December 1997 of $424,149, consisting of freehold land subject to a mortgage and secured and unsecured loans. There were projections of anticipated yields and cash flows. A substantial number of documents in the “prospectus” related to some land near Bright in rural Victoria and to a proposal to subdivide that land and sell separate allotments from it. The other real estate was a home unit in Narre Warren, described as “a rental investment”. It was in fact Mr Johnston’s home, which he rented from Greenacres Management.

9 Ms Sluka gave evidence at the trial. She impressed me as a conscientious and loyal worker with considerable ability, who recounted the facts as she recalled them without embellishment. She was ready to acknowledge gaps in her account where she was unable to remember things, rather than to attempt to reconstruct them on the spot. I accept her evidence, particularly as to the manner in which Mr Johnston conducted CPAS and Greenacres Management. Mr Johnston transferred money from one company to another. If he knew that a payment was coming out of one account, he would put money from another account into the first one to cover the payment. If a cheque was about to bounce, he would put funds into the bank account to cover it. He would go to considerable lengths to persuade people to invest money, particularly if one of the companies with which he was associated had an immediate need for funds. In particular, he would offer very attractive rates of return even for quite short periods. Money from one investor would be used to discharge liabilities for interest to other investors and other debts of the various companies. In this way, the funds were diminished, particularly when, as time went by, it became impossible to persuade more people to invest. Around the middle of 1998, Greenacres Management began to default in interest payments to investors. Once Greenacres Management began to default, clients began making angry and abusive contacts with Ms Sluka and other staff in the CPAS office, by attendance in person or by telephone. Ms Sluka was aware of Mr Johnston’s activities. Her awareness created tension between her sense of loyalty to Mr Johnston and her awareness that clients of CPAS, with many of whom she had personal dealings, were being defrauded. By November 1998, Ms Sluka’s health was affected by stress and she went on sick leave. She returned in February 1999, only to resign immediately.

10 On 30 April 1999 a receiver and manager was appointed over the whole of the property of Greenacres Management by order of this Court. On 11 June 1999, the Supreme

Court of Victoria ordered that Greenacres Management be wound up, on an application filed by the Australian Securities and Investments Commission.

11 The respondent is a corporation. During the period when the events the subject of this proceeding took place, it carried on business as a bank. In 1997 and 1998, it was carrying on business under the title “Colonial State Bank”, with a distinctive logo. The logo featured the word “Colonial.” on a red rectangle. The red rectangle overlay a green rectangle, on which were the words “State Bank”.

12 From 1995, the respondent was seeking to develop its business, particularly in relation to housing loans, in Victoria. It was canvassing professional people, including accountants, solicitors and real estate agents to have them act as its agents for various kinds of financial services the respondent offered to the public. There were two kinds of agency arrangement. One involved the agent simply referring clients to the respondent, which would then ensure that one of its employees made contact with each client to advise the client and process any transaction. For this, the agent received a fixed fee for each client. The other kind of agent was known as an “accredited agent”. An accredited agent would deal with the client, gather all the information required by the respondent, and submit the application to the respondent for approval. An accredited agent was entitled to commission.

13 Colin Kinna had a career in banking from 1961 until he was made redundant in 1994. He returned to work with the respondent in 1995 as a business development manager. It was his duty to locate and make contact with professional people who were likely to be willing to act as agents for the respondent. In 1997, he was based at Frankston. A chance meeting in Cranbourne with Mr Viney resulted in an introduction to Mr Johnston. As a result of discussions between Mr Johnston and Mr Kinna, Mr Kinna gave Mr Johnston an application form for CPAS to become an accredited agent of the respondent.

14 The form was headed “Third Party Accreditation”. Ms Sluka filled in the details in the form. It was dated 15 April 1997. The application was made in the name of CPAS, the nature of whose business was described as “public accountants and business advisors”. Mr Zagari’s name and address were included as the sole director. The core products of CPAS were described as “business and taxation accounting services”. Part of the form required details of “Staff Profile”. The information was given that CPAS had four full-time and two part-time staff. The staff to be accredited were designated as Mr Zagari, who was described as “director”, Mr Johnston, who was described as “manager”, and Mr Viney, who was described as “sales manager”. Attached to the form was a sheet headed “Approval Process”. This sheet contained provision for information and comments from various officers of the respondent, including the “Relationship Manager”, the “Area Manager” and the “Regional/National Sales Manager”.

15 Also attached to the application form was a page headed “Information Notes”. Within that page, under the heading “Third Party Principles”, appeared the following text:

“All third Parties are to be treated as if they were all Linked Credit Providers. The Bank may be liable to the consumer for any representation, warranty or statement made by the supplier or its agent and for damages for misrepresentation, breach of sales contract or failure of consideration.

The Bank therefore must take a strict approach in deciding who is a ‘third party’. The Bank must ensure that all third parties are of good reputation, integrity and standing, both from a financial and a conduct point of view”.

16 Mr Kinna was the relationship manager for CPAS. He was responsible for forwarding the application of CPAS to become an accredited agent and for supplying some information about CPAS to the respondent. The processing of the application was managed by Sonia Grosso, who was employed as an “agent representative” in the agent development section of the respondent, based in Sydney. As part of the process, Ms Grosso was required to complete a “compliance check list”. This required her to send the application and associated information to various departments of the respondent. These included “Risk Management” and “Security & Investigations”. Approval on behalf of Risk Management was given by Ted Medcalf, Head of Credit Policy, Risk Management Group, on 18 June

1997. Ms Grosso’s evidence was that the practice was to do the risk management assessment within a day or a relatively short period of time. She said:

“It was to do them as quick as possible. It depended on the circumstance. If it went to Ted Medcalf early in the morning it could have been out that afternoon.

…

[T]he only time it would be a long process was if he wasn’t in the office for a day or two. That’s the only time it would be delayed. It was generally the same day.”

17 One of the items on Ms Grosso’s client’s check list was “Codes Awareness/Product Training”. She attended to this herself, visiting the office of CPAS in May 1997. Mr Zagari was not present. Mr Johnston and Mr Viney were. On the spur of the moment, a decision was made that Ms Sluka should also be trained. The training was conducted in a casual setting, with the participants seated on couches in the reception area of the office. It took somewhere between one and two hours. In her evidence, Ms Grosso described it as follows:

“It was an open forum, we would sit down and go through the manual, go through specific areas that we were required to talk about, including the consumer credit code, the code of banking practice and then general knowledge on our bank’s products. Introducers were all required to do a consumer credit code test, banking code of practice and then a competency on the product suite.”

18 The written test was a “multiple-choice” test, requiring the selection of the correct answer to each question from among several choices. The trainees did not do the tests individually, but as a group. Most of the answers were, in the words of Ms Grosso, “fairly obvious”. Ms Sluka described the process as follows:

“You didn’t need probably half a brain to fill it out but you had brochures to look through before you actually got to sit and tick your answers or circle your answers. Yes, it was very easy.”

19 There were two results from this process. The first was that those who had undergone the training received certificates of accreditation from the respondent. Ms Sluka’s certificate is in evidence. It was in the same form as those given to Mr Johnston and Mr Viney. The certificate is in the following form:

20 The evidence did not make it certain what was the colour of the seal bearing the words “ACCREDITED INTERMEDIARY”. Ms Grosso was not sure, because some of the respondent’s certificates bore gold or green seals, but the applicants and Ms Sluka said that the seal on the particular certificate was red. It is probable that red was the colour. In any event, Ms Grosso conceded in cross-examination that the certificates given to Mr Johnston, Ms Sluka and Mr Viney were designed to resemble certificates of the kind that might be awarded by a TAFE College, following the completion of a course. Ms Sluka framed the certificates and hung them on the office wall, along with the framed certificate of incorporation of CPAS. It is not clear whether Mr Viney’s certificate was ever hung on the wall; he may have left before the certificates were displayed. If his certificate was there, when he ceased to work for CPAS, it was removed from the wall.

21 The second event that followed the process of accreditation was that CPAS and the respondent entered into a written agreement called an “Accredited Agent Agreement”. This agreement contained terms and conditions upon which CPAS was to act as agent for the respondent. In substance, the agency was limited to the soliciting and referral to the respondent of applications for the provision of various financial services offered by the respondent.

22 The accredited agent agreement bears the common seal of CPAS, with the signature of Mr Zagari. Mr Johnston signed it as a witness to Mr Zagari’s signature. Mr Zagari also signed two of the schedules to the agreement. Schedule E is in the form of a statutory declaration as to various matters. The statutory declaration also bears the signature of someone before whom it was apparently sworn. Among the matters to which Mr Zagari swore was the following:

“I am not bankrupt nor are there any proceedings pending against me under any of the laws relating to bankruptcy. The Agent (if a company) is not in liquidation or administration nor liable to be wound up nor is there any action pending against the Agent for its liquidation or administration or any meeting called in regard thereto. No Nominee of the Agent is bankrupt nor are there any proceedings pending against the Agent or any Nominee under any of the laws relating to bankruptcy.”

23 For the meaning of the reference to a Nominee, it is necessary to go to cl 9.1 of the agreement, which is in the following terms:

“9.1 If the Agent is a company or if the Agent is a natural person who

wishes to perform the Services through an employee or a sub-agent it

agrees that:-

9.1.1. it will only perform the Services through a Nominee or

Nominees approved by the Bank in writing and who has or

have agreed in writing to be bound by the terms of this

Agreement;

9.1.2. it will not permit any Nominee to perform the Services until

the Bank notifies the Agent that any training of the Nominee

has been completed to the Bank’s satisfaction;

9.1.3. it is solely responsible for ensuring that each Nominee

complies with all the duties and obligations of the Agent under

this Agreement and for the actions taken and advice given by

the Nominee;

9.1.4. it will indemnify the Bank against any claim, action, damage,

loss, liability, cost expense or payment which the Bank pays,

suffers, incurs or is liable for by reason of any negligent or

reckless action or advice of any Nominee; and

9.1.5. it will be responsible for the remuneration of each Nominee.”

The word “Nominee” is defined in cl 1.1 of the Agreement in the following terms:

“means a nominee named in Schedule A and any other natural person nominated by the Agent as a nominee, employee or sub-agent of the Agent, approved in writing by the Bank and who has agreed in writing to be bound by the terms of this Agreement.”

24 Nobody is named in Schedule A as a nominee. Nobody was approved in writing by the respondent to be a nominee of CPAS. Nobody agreed in writing to be bound by the terms of the Accredited Agent Agreement. I asked Ms Grosso about this in the course of her evidence. She said that this was a normal situation. She said:

“I don’t think I ever saw anyone nominated on that section. My understanding of that, it was generally for - if they were going to nominate another party to be receiving commissions and to be in that sort of capacity, not so much as to be writing business on behalf of Cranbourne Park or whichever introducer it might have been.

…

I think that section actually says, ‘Parties and addresses for service of notices,’ so I didn’t understand that they needed to be noted there if they were to write loans on behalf of the company.”

25 Mr Johnston was therefore never called upon to accept personally the terms of the agreement or to declare that he was not bankrupt. Mr Zagari’s declaration was true if Mr Johnston was not to be regarded as a nominee of CPAS for the purposes of the Accredited Agent Agreement.

26 Either during the accreditation process, or soon after its completion, Ms Sluka submitted proposed designs for business cards to the respondent for approval. Once approval was given and the accreditation process was complete, these business cards were printed. One relating to Mr Johnston is in evidence. It bears the name of CPAS and its registered number, the words “TAXATION AND BUSINESS CONSULTANTS”, the address, the respondent’s logo, the words “Authorised Agent”, the name “Doug Johnston” and the telephone and fax numbers. Cards of this kind were made available to clients of CPAS by, among other means, being displayed on the counter in the reception area of the office in a plastic rack.

27 Once CPAS had become an accredited agent of the respondent, a sign was installed above the doorway to the building in which the CPAS office was situated. The sign bore the name of CPAS, with the words “ACCOUNTING SERVICES”. It also bore the words “TAXATION & BUSINESS CONSULTANTS”, the respondent’s logo, the words “Authorised Agent” and the telephone number. Clients of CPAS who passed through the doorway under this sign were required to climb a flight of stairs to the office of CPAS and to pass through a glass door to enter that office. On the glass door was further advertising

material, indicating that CPAS was an authorised agent of the respondent and displaying the respondent’s logo.

28 The applicants first entered the premises of CPAS within a few days of their arrival in Australia. They were staying with the second applicant’s brother. After they had overcome the effects of their air travel, they began to consider finding employment and a home of their own. In discussions with the second applicant’s brother, they ascertained that they needed to obtain tax file numbers, in order to engage in paid work. The brother had made use of the services of CPAS. He suggested that the applicants should use CPAS to assist them in obtaining tax file numbers. As a result, the applicants attended at the premises of CPAS and met Mr Johnston. He took the necessary steps to enable them to apply for tax file numbers.

29 Within the next couple of weeks, the applicants, or at least the first applicant, had two or three more meetings with Mr Johnston. Before leaving England, they had sold a house. Of the proceeds, a sum in excess of $300,000 had been transferred to the Commonwealth Bank of Australia in Melbourne so as to be available for collection. The first applicant discussed with Mr Johnston the possible investment of $300,000. He indicated that the applicants proposed to buy a house and to invest some of the money in a way that would give them a return, to assist them in paying a home loan. Mr Johnston advised the first applicant to invest the entire sum of $300,000 in Greenacres Management. The first applicant asked whether it would not be better to apply half of this sum towards the purchase of a house and to invest the other $150,000. Mr Johnston persuaded him, and through him the second applicant, that it would be better to invest the whole of the available money in Greenacres Management. He advised that he would assist the applicants to apply for a home loan from the respondent. He said that the fact that they would have a substantial asset by way of an investment in Greenacres Management would assist them to obtain a home loan from the respondent.

30 The applicants agreed to invest $300,000 in Greenacres Management. Mr Johnston gave the first applicant a document in the following form:

31 Although this document is dated 26 March 1998, the money was not paid over until 27 March. On that day, Mr Johnston went with the first applicant to the central business district of Melbourne to visit the Commonwealth Bank. On the way, the first applicant again asked whether it would be better to invest only $150,000 in Greenacres Management and to put the balance towards the purchase of a house. Mr Johnston insisted that the better course was to invest the whole of the $300,000 in Greenacres Management. Accordingly, the bank transferred $300,000 into an old passbook account that the first applicant had opened while in Australia some years earlier. From that account, $300,000 was withdrawn at the same time in the form of a bank cheque payable to “Greenacres Unit Trust”.

32 Mr Johnston also set up a family trust, called the TS Smith Family Trust, for the applicants. The applicants opened a bank account with the respondent in the name of this trust. For a time, the first applicant did some paid work for one of the companies associated with Mr Johnston. Initially, amounts in respect of interest on the deposit with Greenacres Management were paid. The sum of $3,698.70 was deposited in the TS Smith Family Trust bank account on 1 May 1998. The sum of $3,821.99 was deposited on 2 June. The applicants received a cheque from Greenacres Management for $3,821.99, which they deposited in the account on 2 July 1998. The cheque was dishonoured. On 10 August 1998, a further sum of $3,698.70 was deposited. That was the last payment of interest received.

33 During the week following the dishonour of the cheque for interest, the applicants received advice that their application to the respondent for a home loan had been rejected. After speaking with Mr Johnston about this, the applicants sought the advice of a solicitor. They were advised to deal directly with Mr Johnston to see if they could obtain some better security for their investment with Greenacres Management or, as the first applicant put it in his evidence, “something in writing” from Mr Johnston. As a consequence, Mr Johnston executed a document in the following form:

“GUARANTEE

I Douglas Gordon Johnston

of Rear 1st Floor, 117 High Street Cranbourne Vic 3977

do hereby personally Guarantee

1. That the monies, details set forth below, invested in Greenacres

Management Pty Ltd as trustee for the Greenacres Unit Trust; and

2. That the sum of $150,000 will be repaid within 60 days from the date

of this Guarantee.

Name of Unit Investor: Terrance & Susan Smith

Amount: $300,000.00

Date deposited: 27th March 1998

Interest Rate: 15% pa paid into Colonial State Bank

Account Number 235-102983-00”

AS WITNESS our hands and seals the 19th day of August, 1998.”

The balance of the document showed that it was intended to take effect as a deed. The signature clause bore the words “SIGNED SEALED AND DELIVERED”, although no seal appears to have been affixed.

34 When the repayment of the promised sum of $150,000 did not occur within sixty days from the date of the document, the applicants sued both Greenacres Management and Mr Johnston in the Supreme Court of Victoria. They obtained interlocutory judgment for damages to be assessed and costs on 16 December 1998. On 21 December 1998, they obtained leave to amend the statement of claim by deleting their claims for damages and amended the judgment so that it became a judgment for the sum of $303,750.

35 The judgment remains unsatisfied. Mr Johnston is again bankrupt. A sequestration order was made against his estate on 26 October 1999. As I have said, on 30 April 1999 a receiver and manager was appointed over the whole of the assets of Greenacres Management, which was ordered to be wound up on 11 June 1999. The reports of the liquidator to creditors are in evidence. Oral evidence confirming them was given by an employee of the firm of which the liquidator is a member, an employee who has carried out the bulk of the investigatory work of the liquidator. The liquidator does not expect to receive any money from Mr Johnston, because the official trustee has advised that there is unlikely to be a dividend to Mr Johnston’s creditors. By letter dated 7 May 2001, the liquidator indicated to the first applicant:

“I confirm that due to the substantial deficiency in the assets of the Greenacres Unit Trust existing at the date of my appointment, there will not be any return to creditors of [Greenacres Management].”

This view was confirmed by the employee who gave evidence. CPAS was also wound up by order of the Supreme Court of Victoria on 3 March 2000.

36 There can be no doubt that, unless they are able to recover from the respondent, the applicants have lost all of the $300,000 that they invested.

37 By letter dated 24 July 1998, the respondent gave fourteen days notice to CPAS of the termination of the Accredited Agent Agreement. In accordance with the terms of the agreement, consequent upon this notice, the agreement was terminated on 7 August 1998.

38 The case put on behalf of the applicants pursuant to the Trade Practices Act was that, by permitting the display of the signs I have described, and the certificates of accreditation, the respondent represented that:

(a) Mr Johnston had been assessed by the respondent for competency and was competent

to provide professional advice on financial matters;

(b) CPAS and Mr Johnston were suitable persons with whom to invest money;

(c) The services of CPAS and Mr Johnston had the sponsorship or approval of the

respondent; and

(d) CPAS had the sponsorship or approval of or was affiliated with the respondent.

Each of these representations is alleged to have been untrue.

39 Section 52(1) of the Trade Practices Act provides:

“A corporation shall not, in trade or commerce, engage in conduct that is misleading or deceptive or is likely to mislead or deceive.”

40 Section 53 of the Trade Practices Act relevantly provides:

“A corporation shall not, in trade or commerce, in connexion with the supply or possible supply of goods or services or in connexion with the promotion by any means of the supply or use of goods or services:

…

(c) represent that goods or services have sponsorship, approval, performance characteristics, accessories, uses or benefits they do not have;

(d) represent that the corporation has a sponsorship, approval or affiliation it does not have.”

41 As I have said, it is common ground that the respondent is a corporation for the purposes of the Trade Practices Act. In entering into the Accredited Agency Agreement with CPAS, in granting the certificates of accreditation, and in approving the use of the respondent’s logo on CPAS’s signs, the respondent was undoubtedly acting in trade or commerce. Its object was to sell its services, which it regards as “products”, to members of the public and to use CPAS as a means of attracting customers to itself. In addition, the respondent was acting in connection with the supply or possible supply of services and in connection with the promotion of the supply of services, for the purposes of s 53.

42 There can be no doubt that, by means of the certificate of accreditation issued to Mr Johnston, the respondent represented that he had been assessed by it for competency and was competent to provide professional advice on the subjects listed in the certificate. Counsel for the respondent attempted to argue that any such representation was limited to the provision of professional advice as to the “products” of the respondent. It is true that some of the eight subjects listed in the certificate are described in terms that would suggest that they are particular types of services offered by the respondent. In this category can be placed “Viridian” (apparently a kind of mortgage loan that permits the borrower to draw down further funds against his or her equity in the mortgaged property), “State all in one”, “Money wise”, and perhaps “High performance cash account”. In relation to these subjects, the distinctive names indicate that the advice to be given is likely to be limited to a particular product offered by the respondent, even if other banks might offer similar services under other names.

43 No such conclusion could be drawn from the descriptions of the other subjects. Home loans, credit cards and term deposits are services usually offered by banks. No attempt was made by the respondent to use in the certificates of accreditation terms that suggested that the person certified as authorised to provide professional advice was so authorised only in respect of home loans, credit cards and term deposits offered by the respondent. Further, “Consumer Credit Code” is not a description that could relate to any “product” offered by the respondent. The Consumer Credit Code is a legislative instrument, adopted throughout Australia on a substantially uniform basis, to regulate the activities of the providers of credit. The purpose of attempting to ensure that those who worked for the respondent’s authorised agents were assessed as competent in relation to the Consumer Credit Code was that those persons should avoid transgressing the code in their dealings with customers or potential customers. The aim was to ensure that the respondent would not fall foul of the code. In view of the diversity of the eight subjects listed, and the terminology used to describe them, it is not possible to say that a reasonable reader would assume that the holder of a certificate of accreditation had been assessed for competency, and authorised to give professional advice, only with respect to services offered by the respondent.

44 It is plain that the certificate issued by the respondent to Mr Johnston, and displayed in the office of CPAS, contained a representation that Mr Johnston had been assessed by the respondent as meeting its prescribed levels of competency and was authorised to provide professional advice on the eight subjects. The applicants have succeeded in establishing that the respondent made the first representation alleged.

45 I am not able to find that the respondent made the second representation alleged. Nothing in the certificate of accreditation, the signage at the office of CPAS or the business card with the respondent’s logo makes any express statement about the suitability of CPAS or Johnston as persons with whom to invest money. Nor would a reasonable person be likely to construe from the information provided by the certificate, the signage and the card a statement to that effect. There is nothing to indicate any view about the suitability of CPAS or Mr Johnston to receive investment funds.

46 The third representation was made. In the sign and on the business card, information was given that CPAS was the authorised agent of the respondent. In the business card, it is stated that Mr Johnston was a representative of CPAS. Mr Johnston’s certificate of accreditation conveys that he had the approval of the respondent to provide professional advice on the subjects concerned. The representation with respect to CPAS being the authorised agent of the respondent, and the representation that Mr Johnston was a representative of CPAS, were true. CPAS was a party to the Accredited Agent Agreement. Mr Johnston was the manager of CPAS. No reasonable person would construe these statements as meaning more than they said. They did not amount to representations that the services of CPAS and Mr Johnston had a sponsorship or approval that they did not have. The making of these representations could not, therefore, be a contravention of s 53(c) of the Trade Practices Act. The representation by means of the certificate of accreditation that Mr Johnston had the sponsorship or approval of the respondent adds nothing to the first representation and can therefore be disregarded for present purposes.

47 The fourth representation appears to have been pleaded on the basis of a misunderstanding of the effect of s 53(d) of the Trade Practices Act. That provision prohibits a corporation from representing that it has a sponsorship, approval or affiliation it does not have. The representation pleaded is that CPAS had the sponsorship of, approval of or an affiliation with the respondent. It is unnecessary to make any finding as to whether such a representation was made.

48 It is therefore necessary to determine whether the representation that Mr Johnston had been assessed by the respondent as meeting its prescribed levels of competency and was authorised to provide professional advice on the eight subjects named in the certificate of accreditation was misleading or deceptive. The first step is to determine the class of persons likely to be affected by the representation. As Gibbs CJ said in Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd (1982) 149 CLR 191 at 199:

“Section 52 does not expressly state what persons or class of persons should be considered as the possible victims for the purpose of deciding whether conduct is misleading or deceptive or likely to mislead or deceive. It seems clear enough that consideration must be given to the class of consumers likely to be affected by the conduct. Although it is true, as has often been said, that ordinarily a class of consumers may include the inexperienced as well as the experienced, and the gullible as well as the astute, the section must in my opinion by (sic) regarded as contemplating the effect of the conduct on reasonable members of the class. The heavy burdens which the section creates cannot have been intended to be imposed for the benefit of persons who fail to take reasonable care of their own interests. What is reasonable will or (sic) course depend on all the circumstances.”

49 The respondent made the representation in a certificate granted to a person described as the manager of CPAS, which company it authorised to be its agent in Cranbourne. Cranbourne is on the extreme outskirts of the metropolitan area of Melbourne, to the south-east. It is an area of rapid growth, likely to be inhabited by people in a wide variety of occupations, many of whom will be relatively young and therefore will lack experience in matters of business. Inevitably, they will include people like the applicants who have recently emigrated from other countries and lack experience of the way in which business is conducted in Australia. Because CPAS, to the respondent’s knowledge, held itself out as being in the business of taxation and business consultants, many of the people who came to its premises would be those who required help in dealing with the taxation regime or in matters of business. They would be people who were seeking advice as to the conduct of their affairs, because they were ignorant or uncertain as to how to go about conducting those affairs.

50 To such persons, the statements in the respondent’s certificate of accreditation could be expected to give assurance. Plainly, this was the intent of the certificate. The respondent wished that those who read it should rely on it to accept that the person named in it had the characteristics described in it. The first characteristic was that the person concerned had been assessed by the respondent as meeting its prescribed levels of competency. The second was that the person was authorised to provide professional advice on the eight subjects listed in the certificate. The use of the word “professional” is significant. In this context, the word is not used to connote that the advice would be given in return for payment. Rather, it was used to connote that the advice would be given with the requisite expertise and with a measure of integrity. It would be expected that a person giving professional advice would give it in an objective and disinterested fashion. The advice would be expected to be that which was best for the recipient, not that which was in the interests of the adviser.

51 Viewed in this light, the representation was plainly false. The statement that the holder of the certificate had been assessed by the respondent as meeting its prescribed levels of competency, coupled with the appearance of the certificate, conveyed the impression that some serious testing of the competency of the holder had been undertaken. This was certainly not the case. The process through which Ms Grosso put Mr Johnston, Ms Sluka and Mr Viney was far from rigorous. It was wholly inadequate to determine that they were competent to do anything of significance.

52 More importantly, the statement that the holder of the certificate was authorised to provide professional advice about the eight subjects conveyed the impression that the person would do so. So far as Mr Johnston was concerned, there was every indication that he would not. He was a person with a criminal record of offences involving dishonesty. He was an undischarged bankrupt at the time when the certificate was given. As I have found on the basis of Ms Sluka’s evidence, he was determined and ruthless in persuading his clients to pay over their moneys to him so that he could use those moneys for his own purposes in relation to the various business interests that he had.

53 It might be that an astute and prudent person would say that the reference to prescribed levels of competency is meaningless without some indication as to what those levels were. It might be that a literalist would point out that a statement that a person was authorised to give professional advice actually said nothing as to the expertise or integrity of the person. By allowing CPAS to display the certificates of accreditation, however, the respondent was not necessarily communicating with the astute or the knowledgeable, or with literalists. It was communicating with a range of people in whose minds it intended to create a positive impression about those accredited. It can hardly complain if it be found to have succeeded in this ambition. In my view, by allowing CPAS to display the certificate relating to Mr Johnston, the respondent engaged in conduct that was likely to mislead or deceive clients of CPAS as to the quality of advice that they would receive from Mr Johnston about the subjects listed in the certificate.

54 It is then necessary to determine whether the loss of the sum of $300,000 suffered by the applicants was caused by the respondent’s conduct in making the representation. The test for causation in a claim for loss and damage resulting from a contravention of s 52 of the Trade Practices Act has been expressed authoritatively in broad terms. In Ricochet Pty Ltd v Equity Trustees Executors and Agency Company Ltd (1993) 41 FCR 229 at 233 - 235, the Full Court accepted the proposition that liability under s 82 of the Trade Practices Act for a contravention of s 52 can be established where a misrepresentation was but one of a number of factors which induced a loss-making decision. The Court rejected the proposition that it was sufficient to establish liability that the misrepresentation might have induced the decision. At 235, the Court said:

“A finding that a misrepresentation might have induced a decision will not of itself establish as a matter of probability that it did. Consistently with that finding, it may be that, on the balance of probabilities, a party was induced to make a decision by a combination of factors including the misrepresentation. Assuming a non-trivial contribution to the causative process by the misrepresentation, then it may be actionable.

Ultimately, the ‘causative threshold’ beyond which liability attaches to a misrepresentation which is one of a number of factors inducing a decision that produces loss, will be a question of judgment.”

55 Similarly, in Como Investments Pty Ltd (In liquidation) v Yenald Nominees Pty Ltd (1997) 19 ATPR 41-550, at 43,619, a Full Court said:

“The law does not consider cause and effect in mathematical or in philosophical terms. The law looks at what influences the actions of the parties. Acknowledging that people are often swayed by several considerations, influencing them to varying extents, the law attributes causality to a single one of those considerations, provided it had some substantial rather than negligible effect. As Brennan J. said in San Sebastian Proprietary Limited v Minister administering the Environmental Planning and Assessment Act 1979 (1986) 162 CLR 340 at 366:

‘The representation must be a real inducement or one of the real

inducements to engage in the conduct which occasions the loss’.”

56 It is therefore necessary to consider whether the representation of the respondent as to Mr Johnston was a substantial consideration, or a real inducement, influencing the applicants to pay over the money to Mr Johnston.

57 The first question is whether the applicants relied on the representation. On their first visit to the office of CPAS, they saw the sign above the doorway to the premises, and the sign on the door at the top of the stairs. While waiting in the reception area of the office, they both saw and read the certificates hanging on the wall. These included the certificate of accreditation of Mr Johnston. According to the first applicant, his reaction was to think “yeah, this is pretty good, you know, he seems okay.” He said that, in reaching the decision to invest the money with Mr Johnston, his main reason was that he had full trust in Mr Johnston. What caused the first applicant to regard him as trustworthy was that he was an agent for the respondent and that he was accredited to give professional advice. In cross-examination the first applicant said that he noticed all of the subjects on which Mr Johnston was authorised to give professional advice. The second applicant said:

“We were impressed anyway by the signs outside sort of drawing him and the Colonial together but when we actually saw the certificate we were more interested.

Interested in what?---Well, the fact that he [Mr Johnston] wasa Colonialagent, he’d been accredited, he was tested for competency. He was a professional and the Colonial had sort of - they were advertising him probably, I would say.”

The second applicant in cross-examination said that she noticed the subjects on which Mr Johnston was authorised to give professional advice.

58 Undoubtedly, there were other factors influencing the applicants to decide to invest their money with Greenacres Management. A major one was the return they were being offered of interest at the rate of 15 per cent compounding (interestingly, the notion that interest was to compound is at odds with the proposition that it was to be paid on a monthly basis). Fifteen per cent was a high rate of interest at the time. Undoubtedly, the applicants were impressed by the terms of the “prospectus” and by the persuasiveness of Mr Johnston. They were driven by their own dream of investing in real estate. The first applicant gave evidence that he was reassured by the fact that the applicants were paying the money to a corporate entity. He said that they would not have paid it to Mr Johnston personally.

59 To say that all of these were factors in the decision of the applicants is not to deny that the respondent’s representation was also a factor. It may be that the certificate of accreditation of Mr Johnston now has greater weight attached to it in the minds of the applicants than it did at the time when they made the decision. This would not be surprising, given that evidence of this kind is invariably the product of reconstruction. The process of reconstruction would usually result in an honest belief that the facts were such as to cast the best possible light on the claim now being made. Nevertheless, it is probable that the representation by means of the certificate of accreditation did have significant weight in the minds of the applicants. It is not surprising that people who are told by an institution such as the respondent that it certifies as to a person’s competence and authorises that person to give professional advice on specified subjects should believe what they are told. This is the very intention behind the giving of the certificate. Nor is it surprising that belief in such a statement should be given weight by the person to whom it is made when that person makes decisions about related matters. Again, that is the intention of the giver of the certificate. The respondent desired that people should be persuaded by the certificate to part with their money in return for the services offered by the respondent. It is to be expected that people reading the certificate would take it at face value and act on it.

60 It must also be remembered that the advice Mr Johnston gave to the applicants was within the ambit of the subjects on which he was authorised by the respondent to give professional advice. The applicants sought advice about a housing loan. Mr Johnston gave them advice as prospective applicants to the respondent for such a loan. As I have said, his advice was to invest the whole sum of $300,000 with Greenacres Management and to rely on that investment as an asset to assist in obtaining approval for a housing loan from the respondent. The applicants took this course. They accepted the advice relying, in part, on the terms of the certificate, which gave them to understand that Mr Johnston would give them advice that was both competent and professional.

61 In the circumstances, it is not possible to reject altogether the applicants’ assertions that the terms of the certificate weighed in their decision to invest $300,000 with Greenacres Management. That is the very thing likely to have occurred. Counsel for the respondent suggested that the applicants had failed to take reasonable care of their own interests. He relied on the proposition enunciated by Gibbs CJ in Parkdale at 199, to the effect that the burdens created by s 52 of the Trade Practices Act cannot have been intended to be imposed for the benefit of persons who failed to take reasonable care of their own interests. It is by no means clear that the failure of the person seeking relief under s 52 to take reasonable care of his or her own interests is a specific defence. Certainly, it has been established by subsequent authority that there is no obligation on a person to whom misleading and deceptive statements are made to check the accuracy of those statements. See Neilsen v Hempston Holdings Pty Ltd (1986) 65 ALR 302 at 308 - 310, Sutton v A J Thompson Pty Ltd (in liq) (1987) 73 ALR 233 at 239 - 241 and Henjo Investments Pty Ltd v Collins Marrickville Pty Ltd (No 1) (1988) 39 FCR 546 at 558 – 559 per Lockhart J, with whom the other two members of the Full Court agreed on this point. The position seems to be that the question is one of reliance, in the context of the inquiry into the chain of causation.

62 In the present case, it might be said that the applicants did not do what a prudent investor might have done. They paid over a large sum of money to a corporation that had no substance. They did not seek or obtain any security for their investment. They were not professional investors, however. They are to be viewed as people seeking advice as to what to do with the proceeds of the sale of their house in England. To expect of them a standard of care that would apply to a professional investor would be wrong. What was reasonable for them included acceptance of the advice that they were given, in the context of the representation of the respondent that Mr Johnston was competent and authorised to give professional advice in relation to, among other things, home loans.

63 For these reasons, I find that the applicants relied on the statement made by the respondent in Mr Johnston’s certificate of accreditation to the effect that he had been assessed by the respondent as meeting its prescribed levels of competency and was authorised to provide professional advice on the subjects listed in the certificate. That representation was a substantial factor in the decision of the applicants to accept the advice of Mr Johnston and invest $300,000 in Greenacres Management. As I have said, the representation was false. It did actually mislead and deceive the applicants. In this way, it was a cause of the loss they suffered when their investment in Greenacres Management became irrecoverable.

64 The applicants also sued for negligent misstatement. Because of the conclusion I have reached in relation to the claim for misleading and deceptive conduct, it is strictly unnecessary for me to deal with this cause of action. Because it was argued, and in case it should turn out on appeal that I have reached the wrong conclusion on misleading and deceptive conduct, I state my findings and conclusions on this cause of action as well.

65 The first question is whether the applicants fell within the class of persons to whom the respondent owed a duty of care. Because their claim is in respect of “pure” economic loss (ie economic loss not consequent upon damage to any person or property), the class of persons to whom a duty of care is owed is narrower than is ordinarily the case for the common law tort of negligence. With respect to the circumstances in which a duty of care will arise in the making of a statement, Gleeson CJ, Gummow and Hayne JJ said in Tepko Pty Ltd v Water Board [2001] HCA 19l (2000); 75 ALJR 775 at [47] - [48]:

“The statement of principle by Barwick CJ in Mutual Life & Citizens’ Assurance Co Ltd v Evatt regained vitality after the consideration in Shaddock of the reasoning of the majority in the Privy Council in the Evatt litigation. In his judgment, Barwick CJ referred to various features of the special relationship in which the law will import a duty of care in utterance by way of information or advice. They were restated by Brennan J in San Sebastian Pty Ltd v The Minister. Two of the points made by Barwick CJ are of immediate significance for this appeal. The first is the statement that:

‘the speaker must realise or the circumstances be such that he ought to

have realised that the recipient intends to act upon the information or

advice in respect of his property or of himself in connection with some matter of business or serious consequence’.

The second is that:

‘the circumstances must be such that it is reasonable in all the

circumstances for the recipient to seek, or to accept, and to rely upon the utterance of the speaker. The nature of the subject matter, the occasion of the interchange, and the identity and relative position of the parties as regards knowledge actual or potential and relevant capacity to form or exercise judgment will all be included in the factors which will determine the reasonableness of the acceptance of, and of the reliance by the recipient upon, the words of the speaker.’

The first statement emphasises the need for caution lest a duty of care be imposed upon a party who has no appreciation of, and could not be expected to appreciate, the implications of making an error.”

At [75], Gaudron J quoted the first of these passages from Barwick CJ’s judgment in Mutual Life & Citizens’ Assurance Co Ltd v Evatt and said:

“That approach, which was accepted as correct by Mason J in Shaddock & Associates Pty Ltd v Parramatta City Council [No 1], should, in my view, now be accepted as the test to be applied with respect to the knowledge of a person making a statement which is said to constitute a negligent misstatement.”

Her Honour went on at [76] to quote the second of the passages from the judgment of Barwick CJ in Evatt. It appears, therefore, that what Barwick CJ said is now recognised to be the correct formulation of the circumstances in which a duty of care will arise in the making of a statement.

66 In the present case, the respondent was aware that it might be liable to a consumer for any representation, warranty or statement made by someone it appointed as its agent. It said so in its own information notes relating to “Third Party Principles”, attached to the application for third party accreditation. Those principles emphasised the need for taking a strict approach in deciding who was to be placed in that position, by way of ensuring that such persons were of good reputation, integrity and standing, both from a financial and a conduct point of view. It is plain from these expressions of caution that the respondent knew that people would rely on what was said by those it accredited or authorised to represent it and that it would therefore need to choose them carefully. It is clear, then, that the respondent realised, or ought to have realised, that if it made statements about the persons it accredited, the recipients of those statements – potential customers of the respondent introduced by its agents – would act on those statements in connection with matters of business or serious consequence. The very point of accrediting persons was to persuade potential customers that they should rely upon the advice of those accredited, because the respondent had accredited them. Further, it was reasonable in all the circumstances for those with whom the respondent’s agents or accredited persons came in contact, with a view to persuading them to be customers of the respondent, to accept and to rely upon the statements made in an accreditation certificate. Again, this was the intention. The respondent was anxious to expand the numbers of its customers. It took it upon itself to make positive statements about the competence and the authority of those it accredited. It was in a position to test the competence and professionalism of such persons. It desired to present them in the best light it could. In all of these circumstances, the respondent owed to those who read its certificates a duty to take reasonable care to ensure that statements made in those certificates were accurate.

67 In the present case, the respondent did not discharge its duty of care properly. It did not take reasonable steps to ensure that Mr Johnston was someone not only competent but likely to act professionally in giving advice about the subjects to which the certificate related. The testing procedures through which Mr Johnston went were minimal. They did not touch issues of expertise or objectivity. Still less did they deal with issues of honesty. So far as the evidence goes, no inquiries were made to test whether Mr Johnston was a suitable person to be advanced by the respondent as someone authorised to give professional advice. Mr Medcalf was not called to give evidence as to what took place during the brief time that an application for third party accreditation was under his charge in the credit policy risk management group.

68 The respondent knew that Mr Johnston was in effective control of the operations of CPAS. Mr Johnston was the person with whom Mr Kinna dealt. The application for third party accreditation disclosed that Mr Johnston was the manager of CPAS. Ms Grosso’s training session was conducted without Mr Zagari, who was the director, but on the basis that Mr Johnston was the senior person who was to be accredited in respect of CPAS. Accepting that Mr Johnston was not to be regarded as a “Nominee” for the purposes of the Accredited Agent Agreement, no information was sought in relation to him. It was not that Mr Johnston slipped through a net, it was that the respondent had no net which was apt to catch someone like him.

69 There is no doubt that the respondent could have taken reasonable steps to make inquiries about Mr Johnston. If it had sought from him some declaration as to his status, it might have contended that it could rely on information given in such statement, even if it turned out that the information was false. It is clear from Mr Kinna’s evidence that, had the respondent known that Mr Johnston was an undischarged bankrupt, he would not have been given a certificate of accreditation and CPAS would not have become an accredited agent of the respondent. Mr Kinna said that he would have had nothing further to do with Mr Johnston if he had known of Mr Johnston’s bankruptcy. It is easy to accept the evidence of Mr Kinna, an experienced banker, in this respect. Mr Kinna mentioned the possibility of credit checks, while saying that it was not his role to conduct such checks. If the relatively simple step of seeking a credit check with respect to Mr Johnston had been undertaken, it is probable that the fact of his bankrupt status would have been uncovered and the respondent would have had nothing further to do with him. Such a check might well have disclosed Mr Johnston’s criminal record. If it had known of that record, the respondent would have had nothing further to do with Mr Johnston.

70 In its information notes with respect to “Third Party Principles”, the respondent set itself a high standard. It took the view that it “must take a strict approach in deciding who is a ‘third party’”, and that it “must ensure that all third parties are of good reputation, integrity and standing, both from a financial and a conduct point of view”. This is a higher standard than the standard of reasonable care imposed by the law. In fact, the respondent came up to neither standard. It did not take reasonable care to ensure that the statements it made in the certificate of accreditation of Mr Johnston were accurate.

71 It was reasonably foreseeable to someone in the respondent’s position that a misstatement of the kind made in the certificate of accreditation of Mr Johnston would be relied on by people in the position of the applicants. Again, the point must be emphasised that the respondent intended that people should rely on the certificate. It intended that they should be induced by the representation to accept the “professional advice” of the accredited person. Such reliance and inducement were well within the contemplation of the respondent. In the present case, they occurred. As I have found, the applicants relied on the representation in the certificate with respect to Mr Johnston in making their decision to invest money with Greenacres Management. The loss and damage they suffered by so doing was reasonably foreseeable by the respondent.

72 The elements of the cause of action for negligent misstatement are therefore established by the applicants.

73 Judgment should therefore be entered for the applicant in the sum of $300,000. The applicants also claimed interest. Section 51A of the Federal Court of Australia Act 1976 (Cth) provides for inclusion in the sum for which judgment is given of interest at such rate as the Court thinks fit on the whole or any part of the money for the whole or any part of the period between the date when the cause of action arose and the date as of which judgment is entered. It appeared to me that it was not appropriate to allow interest at the rate of 15 per cent compounding, the rate promised on behalf of Greenacres Management. I therefore invited counsel for both parties to see if they could agree on an appropriate rate of interest. They agreed on a rate of 9 per cent per annum, not compounding. This rate appears to provide reasonable compensation to the applicants for being deprived of the use of their money.

74 As I have found, the applicants received payments of interest from Greenacres Management in the early months. The last such payment was made in August 1998. The payment in respect of July 1998 had been dishonoured, however. If the payment received in August is treated as having been made in respect of July, it is appropriate to award interest to the applicants from 1 August 1998 until the date of judgment. I calculate that interest in the sum of $80,160.30.

75 There will therefore be judgment for the applicants in the sum of $380.160.30, including $80,160.30 interest. The respondent must be ordered to pay the applicants’ costs of the proceeding.

|

I certify that the preceding seventy-five (75) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gray. |

Associate:

Dated: 20 July 2001

|

Counsel for the Applicant: |

Mr M Clarke |

|

Solicitor for the Applicant: |

Slater & Gordon |

|

Counsel for the Respondent: |

Mr J Tsalanidis |

|

Solicitor for the Respondent: |

G S Ray |

|

Date of Hearing: |

8 May 2001 – 11 May 2001 |

|

Date of Judgment: |

20 July 2001 |