FEDERAL COURT OF AUSTRALIA

Commissioner of Taxation v Pine Creek Goldfields Ltd

[1999] FCA 1267

INCOME TAX – taxpayer engaged in goldmining operations in the Northern Territory – covenant in the mineral lease prevented the taxpayer from mining on, or obstructing, any road on the leased land unless the taxpayer had constructed an alternative road over a route to a standard acceptable to the Minister - taxpayer incurred expenditure on the design, corridor acquisition and construction costs of a diversion of the Stuart Highway which ran adjacent to the open-cut mining pit on the leased land – relocation of the highway enabled the taxpayer to access mineral reserves otherwise inaccessible – whether taxpayer was entitled to deduct the expenditure under s 51(1) of the Income Tax Assessment Act 1936 (Cth) (“the Act”) – whether the expenditure was of a capital nature – whether taxpayer was entitled to deduct the expenditure under Division 10 of Part III of the Act – whether expenditure was “allowable capital expenditure” as defined in s 122A of the Act

Income Tax Assessment Act 1936 (Cth) ss 51(1), 122(1), 122A(1)(a), 122DG

Inland Revenue Commissioners v British Salmson Aero Engines Ltd [1938] 2 KB 482, cited

Hallstroms Pty Ltd v Federal Commissioner of Taxation (1946) 72 CLR 634, cited

GP International Pipecoaters Pty Ltd v Federal Commissioner of Taxation (1990) 170 CLR 124, applied

BP Australia Pty Ltd v Federal Commissioner of Taxation (1965) 112 CLR 386, applied

Sun Newspapers Ltd v Commissioner of Taxation (Cth) (1938) 61 CLR 337, applied

BP Australia Ltd v Commissioner of Taxation (Cth) [1966] AC 224, cited

Alianza Co Ltd v Bell [1906] AC 18, cited

Nizich v Commissioner of Taxation (Cth) (1991) 91 ATC 4,747, cited

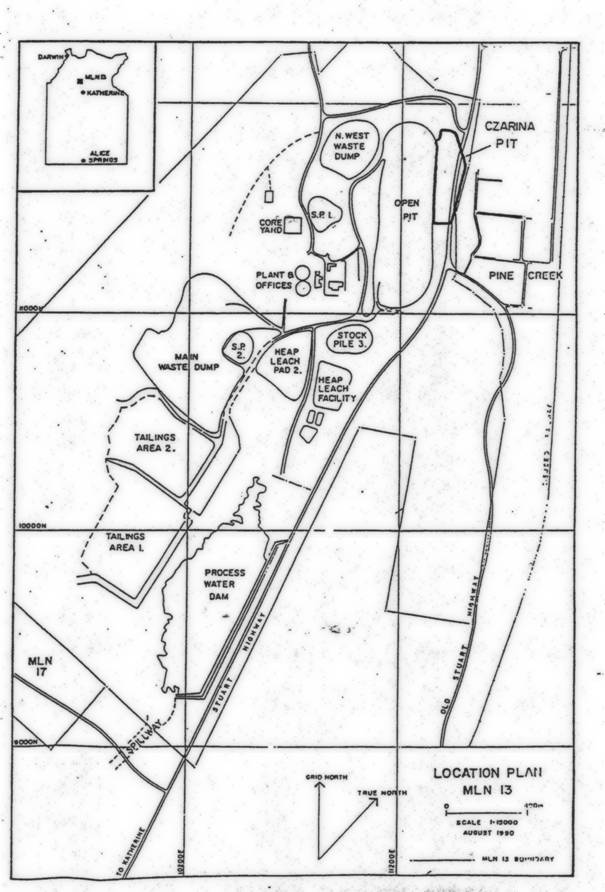

Kauri Timber Co Ltd v Commissioner of Taxes (NZ) [1913] AC 771, cited

Golden Horse Shoe (New) Ltd v Thurgood [1934] 1 KB 548, cited

Knight v Calder Grove Estates (1954) 35 TC 447, cited

Stow Bardolph Gravel Co Ltd v Poole [1954] 3 All ER 637, cited

HJ Rorke Ltd v Inland Revenue Commissioners (1960) 39 TC 194, cited

British Insulated & Helsby Cables Ltd v Atherton [1926] AC 205, referred to

Strick v Regent Oil Co Ltd [1966] AC 295, considered

Cliffs International Inc v Commissioner of Taxation (Cth) (1979) 142 CLR 140, considered

Herring v Commissioner of Taxation (Cth) (1946) 72 CLR 543, considered

Denison Mines Ltd v Minister of National Revenue (1974) 49 DLR (3rd) 450, considered

Commissioner of Taxation v Mount Isa Mines Ltd (1991) 28 FCR 269, discussed

Re Addie & Sons (1875) 2 SC 431, cited

Coltness Iron Co v Black (1881) 6 App Cas 315, cited

Mallett v Staveley Coal & Iron Co Ltd [1928] 2 KB 405, considered

Mount Isa Mines Ltd v Federal Commissioner of Taxation (1992) 176 CLR 141, discussed

Robert Addie & Sons’ Collieries Ltd v Inland Revenue Commissioners [1924] SC 231, considered

United Collieries Ltd v Inland Revenue Commissioners [1930] SC 215, considered

Bean v Doncaster Amalgamated Collieries Ltd (1944) 171 LT 214, considered

Doncaster Amalgamated Collieries Ltd v Bean [1946] 1 All ER 642, cited

Utah Development Co v Commissioner of Taxation (Cth) (1975) 5 ALR 474, considered

Commissioner of Taxation (Cth) v Utah Development Co (1976) 9 ALR 660, referred to

Cyprus Mines Corporation v Commissioner of Taxation (Cth) (1978) 22 ALR 322, considered

Johns-Manville Canada Inc v The Queen (1985) 21 DLR (4th) 210, distinguished

Tucker v Granada Motorway Services Ltd [1979] 1 WLR 683, applied

Robe River Mining Co Pty Ltd v Commissioner of Taxation (Cth) (1989) 21 FCR 1, cited

Commissioner of Taxation (Cth) v Broken Hill Pty Co Ltd (1969) 120 CLR 240, applied

QCT Resources Ltd v Commissioner of Taxation (Cth) (1997) 97 ATC 4,432, cited

COMMISSIONER OF TAXATION v PINE CREEK GOLDFIELDS LIMITED

N 317 OF 1999

LINDGREN, EMMETT and GYLES JJ

SYDNEY

15 SEPTEMBER 1999

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

N 317 OF 1999 |

ON APPEAL FROM A JUDGE OF THE FEDERAL COURT OF AUSTRALIA

|

BETWEEN: |

COMMISSIONER OF TAXATION Appellant

|

|

AND: |

PINE CREEK GOLDFIELDS LIMITED Respondent

|

|

DATE OF ORDER: |

|

|

WHERE MADE: |

THE COURT ORDERS THAT:

1. The appeal be allowed in part.

2. Order 2 made on 29 March 1999 in proceeding NG 1145 of 1997 be varied by adding the words “insofar as it relied on ss 122A(1)(a) and 122DG of the Income Tax Assessment Act 1936 (Cth)”.

3. Otherwise the appeal be dismissed.

4. Each party have leave to apply in relation to the terms of order 2.

Note: Settlement and entry of orders is dealt with in Order 36 of the Federal Court Rules.

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

N 317 OF 1999 |

ON APPEAL FROM A JUDGE OF THE FEDERAL COURT OF AUSTRALIA

|

BETWEEN: |

COMMISSIONER OF TAXATION Appellant

|

|

AND: |

PINE CREEK GOLDFIELDS LIMITED Respondent

|

|

JUDGES: |

LINDGREN, EMMETT and GYLES JJ |

|

DATE: |

15 SEPTEMBER 1999 |

|

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

LINDGREN J:

Introduction

1 I have had the benefit, for which I am thankful, of reading drafts of the Reasons for Judgment of Emmett J and Gyles J. This relieves me of the need to set out the facts and to re-state, by reference to the authorities, the applicable legal principles. There is little, if any, controversy about either.

The issue under s 51

2 I choose, on this occasion, not to add a detailed discussion to the voluminous expositions in the cases of the distinction between capital and income, and between “losses or outgoings of capital, or of a capital … nature” and losses or outgoings on revenue account.

3 In Inland Revenue Commissioners v British Salmson Aero Engines Ltd [1938] 2 KB 482, Lord Greene MR said (at 498):

“[t]here have been many cases which fall on the border-line. Indeed, in many cases it is almost true to say that the spin of a coin would decide the matter almost as satisfactorily as an attempt to find reasons.”

More optimistically, in his much cited judgment in Hallstroms Pty Ltd v Federal Commissioner of Taxation (1946) 72 CLR 634, Dixon J said (at 646):

“For myself, however, I am not prepared to concede that the distinction between an expenditure on account of revenue and an outgoing of a capital nature is so indefinite and uncertain as to remove the matter from the operation of reason and place it exclusively within that of chance, or that the discrimen is so unascertainable that it must be placed in the category of an unformulated question of fact. The truth is that, in excluding as deductions losses and outgoings of capital or of a capital nature, the income tax law took for its purposes a very general conception of accountancy, perhaps of economics, and left the particular application to be worked out, a thing which it thus became the business of the courts of law to do. The courts have proceeded with the task without, it is true, any very conspicuous attempt at analysis, but rather in the traditional way of stating what positive factor or factors in each given case led to a decision assigning the expenditure to capital or to income as the case might be. It is one thing to say that the presence among the circumstances of a case of a particular factor places the case within a specific legal category. It is another thing to infer that the absence of the same factor from some other case necessarily places that case outside the category and gives it an opposite description. But towards that kind of fallacy human reasoning constantly tends, and the decisions upon matters of capital and income contain much reasoning that is quite human.”

4 I regard the present issue as finely balanced, and have found persuasive the reasoning of the learned primary judge as well as that of both of my colleagues. Resisting the temptation to think that “the spin of a coin would decide the matter …. as satisfactorily as an attempt to find reasons”, I agree with the conclusion reached by Gyles J, generally for the reasons stated by His Honour.

5 Particular positive factors that influence me are that the respondent’s expenditure was a once-and-for-all payment for a substantial advantage of an enduring, ongoing or continuing nature, namely, the making of resources, notably the Czarina resource, available for the commencement of exploitation.

The issue under Division 10 of Part III

6 For, substantially, the reasons given by the learned primary judge (his Honour’s judgment is reported at 99 ATC 4382) and by Gyles J (Emmett J did not find it necessary to deal with the present issue) I think that the expenditure in question was an “allowable capital expenditure” within s 122A(1)(a).

Conclusion

7 I agree with the orders proposed by Gyles J for the reasons given by his Honour.

|

I certify that the preceding seven (7) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Lindgren. |

Associate:

Dated: 15 September 1999

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

NEW SOUTH WALES DISTRICT REGISTRY |

N 317 OF 1999 |

ON APPEAL FROM A JUDGE OF THE FEDERAL COURT OF AUSTRALIA

|

BETWEEN: |

COMMISSIONER OF TAXATION Appellant

|

|

AND: |

PINE CREEK GOLDFIELDS LIMITED Respondent

|

|

JUDGES: |

LINDGREN, EMMETT & GYLES JJ |

|

DATE: |

15 SEPTEMBER 1999 |

|

PLACE: |

SYDNEY |

REASONS FOR JUDGMENT

EMMETT J:

8 The respondent, Pine Creek Goldfields Limited (“the Taxpayer”), was, between 1985 and 1993, engaged in goldmining operations at the Pine Creek Goldfield in the Northern Territory. In the years ended 30 June 1991 and 30 June 1992, the Taxpayer incurred expenditure on the design, corridor acquisition and construction costs of a diversion for the Stuart Highway (“the Highway”). The Taxpayer claimed to be entitled to deduct that expenditure from its assessable income for the purposes of the Income Tax Assessment Act 1936 (“the Act”).

9 The appellant, the Commissioner of Taxation (“the Commissioner”), disallowed the claim for a deduction in respect of the expenditure. The Taxpayer objected and the objection was disallowed. The Taxpayer then appealed to the Court from the Commissioner’s objection decision. The appeal was heard by a Judge of the Court who set aside the Commissioner’s objection decision and, in lieu thereof, ordered that the Taxpayer’s objection be allowed. From that decision, the Commissioner has appealed to the Full Court.

FACTUAL BACKGROUND

10 The Taxpayer was established, in February 1985, as the vehicle for a joint venture between Enterprise Gold Mines NL (“Enterprise”) and Renison Goldfields Consolidated Limited (“RGC”). In 1991 the Taxpayer became a wholly owned subsidiary of RGC. The Taxpayer was established to develop and operate a gold mine to the west of the township of Pine Creek. Pine Creek is a small, historic 19th century gold mining town situated on the Highway, 230 km south of Darwin. Gold was first discovered there in the 1870s.

11 On 14 February 1985 a mineral lease, number MLN 13 (“the Lease”), was granted by the Government of the Northern Territory to Enterprise and Circular Quay Holdings Pty Ltd (“the Lessees”). The Lease was transferred to the Taxpayer shortly after it was granted.

12 Under the Lease, the Lessees were granted the following interest:

“A lease of all that piece or parcel of land delineated in red in the plan contained in the first schedule to this lease and all those mines and deposits of gold and other minerals associated or combined therewith… together with the rights, liberties, easements, advantages and appurtenances thereto belonging or appertaining… to hold as tenants in common… for the term of 25 years from the date hereof and subject to the conditions herein and for the purposes of mining thereon for gold and such other materials as are associated or combined in the leased land with the gold ore…”

The Lease also contained the following covenant:

“1. The lessees… covenant with the Territory

………………………………

(d)….to permit the exercise of free ingress, egress and regress at all times….to, from and across the leased land except those areas which….are designated by the lessees as restricted areas…

(g) not to mine on, or obstruct, any road… on the leased land unless the lessees have constructed an alternative road over a route to a standard acceptable to the Minister.”

13 The plan in the schedule to these reasons shows the location of the Highway prior to its diversion. It can be seen that the Highway ran virtually the whole length of the area of the Lease from north to south.

14 There were reserves of gold under and on both sides of the Highway. The Taxpayer commenced to conduct open-cut mining on the land in the Lease in 1985. The open-cut pit, as it had been developed by late 1990, was known as “the Enterprise Pit”. The Enterprise Pit was located to the west of the Highway. The reserves to the east of the Highway were referred to as “the Czarina Resource”. Because of the prohibition contained in covenant 1(g), those reserves were not accessible while the Highway was located where it was.

15 By 1990, the crest of the eastern side of the Enterprise Pit was approximately 35 metres from the Highway. Cracks began to develop between the crest and the Highway. Such cracks can occur over time through the action of weather and local de-stressing. By December 1990, instability of the eastern side of the Enterprise Pit was such that the existing pit design threatened the stability of the Highway. As a result, the Department of Minerals and Energy (“the Department”) ordered that the Taxpayer could not mine to the original design of the Enterprise Pit unless the Highway was relocated.

16 The original design of the Enterprise Pit provided for the angle of the batter on the eastern side of the Enterprise Pit to be 54º. The Department, however, was prepared to grant permission for the Taxpayer to mine to an amended design, involving a substantial shallowing of the angle of the eastern side batter to 35º. That would have had the consequence of substantially reducing the mineable reserves within the Enterprise Pit and would have reduced the life of the mine by one year. The Department refused to allow any steeper slope because of a perceived threat to the security of the Highway.

17 On 17 December 1990, Mr C.F.D. Pease, the general manager of the mine, prepared a report entitled “Enterprise Pit Design and Stuart Highway Relocation Option”. Mr Pease expressed the view, based on the analysis contained in the report, that the Taxpayer’s best option was to relocate the Highway to the east of Pine Creek township. The other options examined by him were to:

· mine the Enterprise Pit, with a 35º slope on the eastern side, in accordance with the amended design permitted by the Department, without any relocation of the Highway;

· mine the Enterprise Pit, with a 40º or a 47º slope on the eastern side, following minor relocation of the Highway, slightly to the east of the then current alignment.

The report indicated that, apart from allowing exploitation of the Czarina Resource, the relocation of the Highway to the east of Pine Creek township would also facilitate exploitation of ore resources “in the southern mining lease”. That appears to have been a reference to the southern end of the Enterprise Pit.

18 The report expressed the opinion that the net present value of the Taxpayer’s operations would be severely restricted if the Highway was not relocated. The report estimated that gold production recovered from a pit with a 47º batter, following minor relocation of the Highway, would be some 3.6 tonnes more than from a pit with a 35º batter and no such relocation. The estimated net present value on the basis of the modification to a 35º batter was $29.775 million. However, the net present value with a 40º batter and minor relocation was estimated at $39.329 million, and with a 47º batter and minor relocation was estimated at $41.148 million.

19 The Czarina Resource was described in the report as being “sterilised” by the Highway. Addition of the ability to mine the Czarina Resource increased gold production by a further 1.842 tonnes. That resulted in an increase in the estimated net present value to $43.305 million. Thus, there would be a significant increase in the net present value as a consequence of either of the relocations proposed. However, the additional increase from the relocation east of Pine Creek, rather than the minor relocation, was relatively small when compared with the increase from a 35º batter to a 40º batter.

20 The report concluded that, on the basis of the study contained in it, the optimum solution to the problem then being encountered was for the Highway to be relocated to the east of the town of Pine Creek during the 1991 dry season. Estimates suggested that minor relocation would cost between $1.2 m and $1.5 m and the relocation to the east of the township would cost between $3.0 m and $3.6 m. There were other variations which are not presently relevant. The Board authorised expenditure of an initial $70,000 to undertake detailed planning work on relocation of the Highway.

21 There were two advantages for the Taxpayer flowing from the relocation of the Highway to the east of Pine Creek township. The first was that the “sterilization” of some of the reserves in the Enterprise Pit, brought about by the remedial action required by the Department, would be reversed and those reserves would once more become available to be mined. This advantage would seem to have been present whether the shorter or longer relocation was to take place. The second was that the Czarina Resource, which could not be mined because it was either under the Highway or on the opposite side of it to the Enterprise Pit, could be mined in the future.

22 On 17 April 1991, the Board of the Taxpayer decided upon the alternative of the relocation of the Highway. In due course it committed the Taxpayer to expenditure of $3.4 million for the design, corridor acquisition and construction of the proposed diversion. Construction of the diversion of the Highway commenced in July 1991 and was completed in December 1991. Mining operations in the Enterprise Pit continued without interruption during that project. In the result, the Highway was relocated to the east of the Pine Creek township. During the years of income ended 30 June 1991 and 30 June 1992, respectively, the Taxpayer incurred expenditure of $105,316 and $3,463,353 on design, corridor acquisition and construction costs in relocating the Highway.

23 There is no dispute as to why the expenditure was incurred. First, the diversion overcame the problem of instability in the Enterprise Pit wall adjacent to the Highway which otherwise would have resulted in the closure of that pit within twelve months. Secondly, and related to the first reason, the relocation prevented the sterilisation of reserves that would not have been able to be mined from the Enterprise Pit as a result of the adoption of the 35º slope. Thirdly, the expenditure enabled the Taxpayer to mine the Czarina Resource.

24 The open-cut mine that was in fact developed to exploit the Czarina Resource was known as the “Czarina Pit”. Development of the Czarina Pit commenced after the relocation of the Highway was completed. It was situated some 20 metres from the outside wall of the Enterprise Pit, on an area of land over which the Highway had earlier run. Authority to commence work on the Carina Pit was received in July 1992.

25 The Enterprise Pit operation ceased in January 1993. In September 1993 mining operations on the Lease ceased following the depletion of the reserves at the Czarina Pit. Gold mining operations ceased in the Pine Creek area in November 1994. There were apparently other mining leases operated by the Taxpayer in the Pine Creek area besides the two pits with which the present case is concerned. However, there was no evidence of the details of such leases.

THE ISSUES

26 The Taxpayer claims to be entitled to deduct the expenditure in question under section 51(1) of the Act. Section 51(1) relevantly provides as follows:

“All losses and outgoings to the extent to which they are incurred in gaining or producing the assessable income, or are necessarily incurred in carrying on a business for the purpose of gaining or producing such income, shall be allowable deductions except to the extent to which they are losses or outgoings… of a capital…nature…”

It was common ground that the expenditure in question was incurred by the Taxpayer in gaining or producing assessable income, or was necessarily incurred in carrying on a business for the purpose of gaining or producing such income. The question that arises under section 51(1) is whether the expenditure was “of a capital nature”.

27 Alternatively, the Taxpayer claimed to be entitled to a deduction under Division 10 of Part III of the Act. Under section 122DG(2), where, in a year of income, a taxpayer incurs allowable capital expenditure, an amount ascertained in accordance with section 122DG is an allowable deduction in respect of that expenditure. “Allowable capital expenditure” is defined in section 122A as being expenditure of a capital nature incurred by a taxpayer, being, relevantly, “expenditure in carrying on prescribed mining operations”. The expression “prescribed mining operations” is defined in section 122(1) as meaning:

“mining operations on a mining property for the extraction of minerals….from their natural site, being operations carried on for the purpose of gaining or producing assessable income”.

28 Thus, losses or outgoings are excluded from the operation of section 51(1) to the extent that they are losses or outgoings of a capital nature. If the expenditure is allowable as a deduction under section 51(1), by definition, it would not be allowable as a deduction under section 122DG. On the other hand, it is possible that expenditure of a capital nature might not satisfy the requirements of section 122DG, such that a taxpayer would be denied any deduction at all in respect of the expenditure. Further, if a taxpayer is entitled to a deduction under section 122DG, the taxpayer is entitled only to a deduction in respect of a proportion of the total amount of the expenditure incurred in the relevant year.

29 The trial judge concluded that the expenditure in question was not of a capital nature and was deductible under section 51(1) of the Act in the year in which it was incurred. Against the possibility that he was wrong in that conclusion, his Honour went on to consider deductibility under Division 10 and concluded that the expenditure would have been deductible under that Division if it were of a capital nature.

REASONING

30 The expenditure in question was incurred in constructing an alternative road, as contemplated by clause 1(g) of the Lease, in order to avoid the prohibition that was otherwise imposed by the operation of that provision. By satisfying the prerequisite of clause 1(g), the Taxpayer was able to proceed with mining in the Enterprise Pit, notwithstanding the proximity of the land on which the Highway was then constructed. The Taxpayer was also able to mine on that part of the Highway that traversed the site of the Czarina Pit.

31 The chief, if not the critical, factor in determining the character of expenditure as being of a capital or revenue nature is the character of the advantage sought by the outgoing – G.P. International Pipecoaters Pty Ltd v FCT (1990) 170 CLR 124 at 137. The issue is that of identifying the relevant advantage. Thus, it is necessary to determine the advantage sought by the Taxpayer in incurring the expenditure. That will depend on what the expenditure is calculated to effect, from a practical and business point of view, rather than upon the juristic classification of the legal rights, if any, secured, employed or exhausted in the process – BP Australia Pty Ltd v FCT (1965) 112 CLR 386 at 397.

32 Expenditure is to be considered of a revenue nature if its purpose brings it within the very wide class of things that, in the aggregate, form the constant demand that must be answered out of the returns of a trade or its circulating capital. Actual recurrence of a specific thing need not take place or be expected as likely – Sun Newspapers Ltd v Commissioner of Taxation (1938) 61 CLR 337 at 362.

33 In this context, a distinction must be drawn between the business entity, structure or organisation set up or established for the earning of profit and the process by which such an organisation operates to obtain regular returns by means of regular outlay, the difference between the outlay and returns representing profit or loss - Sun Newspapers Ltd v Commissioner of Taxation (1938) 61 CLR 337 at 359. Thus, expenditure in the improvement of an asset of a taxpayer will be of a capital nature while expenditure in the working of an asset will be of a revenue nature. The Commissioner would characterise the expenditure of the Taxpayer in question as being expenditure in the improvement of the Taxpayer’s asset, consisting of the Lease. If that is the correct characterisation, the expenditure was of a capital nature.

34 The Commissioner relied on the fact that the Taxpayer had been established “to operate and develop the mine” and the fact that the only business in which the Taxpayer engaged was that of exploiting the gold reserves in the area of the Lease. The Taxpayer had no significant activity other than the development and excavation of the pits contained within the area of the Lease.

35 Relocation of the Highway, so the Commissioner contended, was a once-only cost and gave rise to an advantage for the Taxpayer that, in the Commissioner’s contention, was permanent. Relocation gave a lasting benefit, in the sense that it endured for as long as the Taxpayer’s goldmining business would endure. Without the expenditure, the mining operations of the Taxpayer within that area would have come to an end earlier than would be the case following relocation. The expenditure permitted the mining operations to continue beyond the time when they would otherwise have come to an end.

36 However, the expenditure in question was a once-only expense only in the sense that, once the Highway had been relocated to the east of the Pine Creek township, there would be no need to relocate it again. By reason of any realignment or relocation of the Highway, mining operations would be permitted that would otherwise have been prohibited by clause 1(g) of the Lease. Clause 1(g), however, was not directed specifically to the Highway, which is not mentioned as such in the body of the Lease, although it is shown on the plan annexed to the Lease.

37 The business of the Taxpayer was the exploitation of the Lease. The expenditure in question was of a kind that could well be expected in connection with an open-cut mining operation within the area of a mineral lease that is traversed by a public road. On an earlier occasion, the Highway had already been realigned eastwards in order to permit the continuation of mining operations in the Enterprise Pit.

38 The expenditure in question was not incurred in order to obtain any enduring benefit but was a necessary incident of the operation of an open-cut mine. The expenditure in question removed an obstacle to the continued mining within the Enterprise Pit and to opening up the Czarina Pit. It was an incident of exploiting the Lease to incur the expense of relocating any roadway that interfered with mining operations. Just as removal of part of the overburden covering the ore body, to gain access to that ore body, is an incident of the mining operations, so is the removal of a roadway above the ore body.

39 In the context of the present case, the advantage sought by the Taxpayer was the removal of the restriction of mining on and adjacent to the then site of the Highway. The advantage sought and obtained was consumed by the operation of the business. The advantage did not go to the continued existence or to the extension of the business, but to its day to day operation. It was not an extension of the capital structure or asset, but the ordinary working of an asset comprising a mineral lease. The advantage of gaining access to reserves that would otherwise have been inaccessible was an advantage consumed in the business operation itself. The expenditure was not incurred in setting up or establishing an entity structure or organisation. The expenditure was simply an additional cost of operating the business.

CONCLUSION

40 Once it is accepted that the expenditure was incurred in the continued operation of the Taxpayer’s business, it follows that it should not be characterised as being of a capital nature. Accordingly, it is not excluded from the operation of section 51(1) of the Act. In those circumstances, the Taxpayer was entitled to a deduction for the amount of the expenditure in the year in which it was incurred. It also follows that section 122DG has no application, since a precondition of the application of that provision is that the expenditure be of a capital nature.

41 As I have indicated above, the trial judge ordered that the Taxpayer’s objection be allowed. The objection is based on two alternative, and mutually exclusive, grounds. The consequences are different depending upon whether the objection is allowed on the basis of section 51 or Division 10. His Honour’s order did not draw that distinction.

42 I would substitute for Order 2 made by the trial judge the following order:

“2. The respondent’s objection decision in relation to the applicant’s claim to be entitled to a deduction under section 51(1) be set aside and in lieu thereof the applicant’s objection to disallowance of that claim be allowed.”

43 I would also order the Commissioner to pay the Taxpayer’s costs of the appeal.

|

I certify that the preceding thirty-six (36) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Emmett. |

Associate:

Dated: 15 September 1999

SCHEDULE

|

IN THE FEDERAL COURT OF AUSTRALIA |

|

|

N 317 OF 1999 |

ON APPEAL FROM A JUDGE OF THE FEDERAL COURT OF AUSTRALIA

|

BETWEEN: |

Appellant

|

|

AND: |

Respondent

|

|

JUDGES: |

|

|

DATE: |

|

|

PLACE: |

REASONS FOR JUDGMENT

GYLES J:

44 The clear analysis of the facts and issues by Emmett J relieves me of the necessity to do the same. Indeed, there is little in dispute between the parties as to the relevant facts and issues, although they sharply divide upon the result. I shall mention some additional aspects of the facts in the course of my reasons.

45 The issues presented by this case are complicated by reason of the fact that gold mining, as with other forms of mining, quarrying and some types of forestry, consumes or exhausts the asset of the miner. At the end of the process, the mine is exhausted and no asset of value (at least in the mining sense) remains. This leads to the argument that it is unfair to treat amounts which are represented at the end by no asset as capital. As the trial judge noted in paragraphs 1 and 2 of his reasons, this has led to the mining industry being regarded as something of a special case by Division 10 of Part III of the Income Tax Assessment Act 1936 (Cth) (“the Act”), which authorises deductions for various kinds of capital expenditure incurred in the mining industry.

Section 51

46 This circumstance also leads to special difficulties in dealing with claims for revenue deductions pursuant to s 51 of the Act. Hence, the differences in judicial opinion in this case. The authorities, in my opinion, do not authorise any change in the principles which determine s 51 deductions for expenditure by mining companies, nor any special leniency in applying those principles to particular expenditure. On the other hand, it is not possible to apply uncritically to mining expenditure the tests laid down in judgments such that of Dixon J in Sun Newspapers Ltd v Commissioner of Taxation (Cth) (1938) 61 CLR 337 and of the Privy Council in BP Australia Ltd v Commissioner of Taxation (Cth) [1966] AC 224, dealing with different, and more conventional, situations where it is easier to distinguish the business structure from the process by which it operates.

47 The gravamen of the decision of the trial judge on this point is expressed succinctly in paragraphs 25, 26, 29 and 30 which are as follows:

“25 In the present case the expenditure was not outlaid to bring into existence an “asset or an advantage for the enduring benefit of a trade” to use the language of Viscount Cave British Insulated & Helsby Cables Ltd v Atherton [1926] AC 205 at 213. It is true that the diversion allowed access to reserves not before available, being the Czarina Resource. It is also true that in the result the life of the mining operations was extended for some months. These factors lean to some degree towards the conclusion that the expenditure was capital. But the question of characterising involves balancing often competing considerations.

26 It must be borne in mind that “enduring” does not in this context mean permanent in the sense of perpetual: Commissioner of Taxes v Nchanga Consolidated Copper Mines Ltd [1964] AC 948 at 960. The advantage gained by Pine Creek Goldfield here was in the circumstances hardly enduring in whatever sense that word is used. The expenditure permitted the mining operation to continue, when otherwise it would have come to an end within a short time. The expenditure removed an obstacle to the continued mining at the Enterprise Pit, as well as opening up the Czarina Resource. It restored the taxpayer’s ability to mine gold and the reserves it could mine which had been available to it, but which the crack and subsequent action of the Department of Minerals had denied to it. In my view it should be characterised not as the acquisition of fresh reserves but as part of the business operations of mining which Pine Creek Goldfields carried on, as part of the costs of the trading operations.

27 …

28 …

29 Recurrence is not of itself a test. It is no more than a consideration to be taken into account. So too, recurrence does not mean annually or periodically recurring. Some expenditure such as rent and interest is, in the ordinary sense, recurrent and generally on revenue account: Steele v Commissioner of Taxation [1999] HCA 7 (4 March 1999) (unreported). But deductibility is not limited to such periodic outlays. The present is a case of an outlay of a kind which could be expected to be required from time to time of an open cut miner where the mine is adjacent to a highway. So seen it can be characterised as an ordinary outlay of the business of an open cut miner, expenditure which led to the continuation of the business for the purposes of earning assessable income and produced advantages of a revenue, rather than of a capital nature.

30 The second matter raised by the Sun Newspaper tests is the manner in which the advantage sought is to be used, relied upon or enjoyed. This second matter is obviously closely tied to the first. The advantages sought of continuation of the business and access to reserves previously inaccessible are advantages consumed in the business operations. They have no permanence. The payment is no more than an additional cost of the business.”

48 His Honour is undoubtedly correct in saying that the transaction was not the acquisition of fresh reserves in the technical or legal sense, but from a practical and business point of view it seems to me that this is, in substance, what happened. The expenditure incurred in relocating the highway was the price paid for legal and practical access to mining for the mineral. If, rather than do what was done, the taxpayer had negotiated an amount to be paid to the Minister to obtain a waiver of Clause 1(g) of the mineral lease, I should have thought that it would be clear that such a payment would be on capital and not revenue account. I cannot see any difference in characterisation between the two situations.

49 The fact that the result had no permanence or endurance, in the sense that it was to be anticipated that the mineral, access to which was so procured, would be fairly soon mined, is not to the point. The same could be said of the acquisition of mineral reserves of the same size adjoining an exhausted pit. In that case, as his Honour recognises in paragraph 24, the purchase price would undoubtedly be on capital account. I fail to see any distinction from a practical and business point of view. As I am differing from a trial judge with much experience in this area, I will expand upon my reasoning to a greater extent than I might otherwise have done.

50 In considering the “endurance” point, it needs to be borne in mind that the expenditure in question permitted access to an extra revenue of nearly $14 million (on a net present value basis) and a significant extension of the life of the mine. The evidence is not precise as to the period of extension, but it was at least one year in relation to the Enterprise Pit and the mining of the Czarina Pit was estimated to take 17 months. As mining only commenced in 1985, and ended on this particular mineral lease in 1993, on any view the extension was significant in terms of both time and money. It was certainly not de minimis or ephemeral.

51 As I have said, his Honour noted that expenditure to acquire rights to mine minerals is on capital account, notwithstanding the fact that those minerals will be consumed in the business operations and have no permanence. This would certainly apply to acquiring the right to mine minerals of the volume involved in this case. This has been clear since at least the decision of the House of Lords in Alianza Co Ltd v Bell [1906] AC 18 and has been applied in a series of cases in this, and related, fields ever since – a recent example being the decision of French J in Nizich v Commissioner of Taxation (Cth) (1991) 91 ATC 4,747. (See also Kauri Timber Co Ltd v Commissioner of Taxes (NZ) [1913] AC 771; Golden Horse Shoe (New) Ltd v Thurgood [1934] 1 KB 548; Knight v Calder Grove Estates (1954) 35 TC 447; Stow Bardolph Gravel Co Ltd v Poole [1954] 3 All ER 637; HJ Rorke Ltd v Inland Revenue Commissioners (1960) 39 TC 194). This line of authority cannot be distinguished by saying that it deals, by and large, with acquiring land with minerals or other things in or on it. Minerals in situ are the very stuff of mining. The land is not bought as land, but rather as that which contains the minerals. The business of mining is to get the mineral out of the land.

52 The respondent does not adequately explain why expenditure on the acquisition of the right to mine by acquiring title to minerals differs, from a practical and business point of view, from the expenditure of money to acquire the legal and practical ability to mine minerals within a mining permit which are otherwise unable to be mined.

53 It is not irrelevant that the approval for the expenditure in question was made pursuant to what was called a capital expenditure requisition, was included in the minutes of the meeting of directors of the parent company under the heading “Capital Expenditure: Pine Creek – Stuart Highway Diversion” and was included in the operating and financial reports to the board from time to time in the capital expenditure report. The label which a taxpayer attributes to expenditure in its own records is not decisive for income tax purposes, but, in circumstances such as the present, is a relevant consideration. In the present circumstances this description by the taxpayer and its parent seem to me to accord with commercial reality from a practical and business point of view.

54 It may be helpful to consider later analysis of Viscount Cave LC’s use of the word “enduring” in British Insulated & Helsby Cables Ltd v Atherton [1926] AC 205 at 213, which is referred to in paragraph 25 of the judgment below. In Strick v Regent Oil Co Ltd [1966] AC 295, Lord Wilberforce considered a number of cases, including Knight v Calder Grove Estates (supra), Stow Bardolph Gravel Co Ltd v Poole (supra) and HJ Rorke Ltd v Inland Revenue Commissioners (supra) and said, at 353:

“… In two of them the question of transience was raised and in each it was decided that once the conclusion was reached, on other considerations (the validity of which need not be here considered) the asset acquired was fixed and not circulating capital, the fact that the asset was of a transient character is irrelevant. These authorities do little more than provide illustrations of the character of various types of assets in various trades. The principle seems to emerge that if, on a consideration of the nature of the asset in the context of the trade in question, it is seen to be appropriate to classify it as fixed rather than as circulating capital, the brevity of its life is an irrelevant circumstance. But it would still be correct, in my opinion, where the nature of the asset, taken together with other relevant factors, leaves the matter in doubt, to have regard, amongst other things, to its transient character. No rule can be laid down as to a minimum period of endurance for a capital asset or a maximum permissible period for an item of stock or circulating capital, though obviously the more closely the period of endurance is related to an accounting period the easier it is to argue for a revenue character, but no doubt there is a penumbra the width of which may vary according to the nature of the trade.”

55 In Cliffs International Inc v Commissioner of Taxation (Cth) (1979) 142 CLR 140, each of Gibbs J and Stephen J considered the question of permanent or enduring character because of the way in which they approached the matter. Although each was in dissent as to result, that does not affect the value of what they had to say on this point. At 152-3, Gibbs J said:

“The advantage sought by the payments was of a capital nature. That is so, whether one looks at the “true legal character” of the expenditure or at what it was “calculated to effect from a practical and business point of view”. The sources of those phrases are the authorities cited in Federal Commissioner of Taxation v South Australian Battery Makers Pty Ltd [(1978) 140 CLR, at pp 658-659], where the familiar distinction between expenditure of a capital nature and expenditure of a revenue nature was recently discussed. The true legal character of the expenditure was that of the purchase price of the shares in Basic, as Franki J held in the Federal Court. From a business and practical point of view the appellant sought to acquire Basic’s rights in relation to the temporary reserves – the actual right to occupy and use them for a short period, and the contingent right to obtain, or the possibility of obtaining, mineral leases of the land in the reserves. In the Federal Court Bowen CJ held that the payments were made for the acquisition of the shares and the rights to which they gave access, and Brennan J held that the payments were incurred with a view to obtaining the net assets of Basic. However the matter is stated, what was purchased – whether it was the shares, or the rights and the possibilities inherent in them, or all of these – was an asset or advantage of an enduring, although not perpetual, kind, an asset or advantage that was to form part of the organization set up by the appellant for the earning of profit. The deferred payments were made to acquire this asset or advantage – there was nothing else that Howmet and Mt. Enid had to give for which they could have been paid. In other words, the deferred payments should properly be regarded as expenditure necessary for the acquisition of property or of rights of a permanent character, the possession of which was a condition of carrying on the business of mining at all, within the test stated in Robert Addie & Sons’ Collieries Ltd v Commissioners of Inland Revenue [(1924) SC 231, at p 235], in the passage cited in Colonial Mutual Life Assurance Society Ltd v Federal Commissioner of Taxation [(1953) 89 CLR 428, at p 448]. The rights acquired were of a permanent character within this test, notwithstanding that a mineral lease is a wasting asset, for “When the words `permanent’ or `enduring’ are used in this connection it is not meant that the advantage which will be obtained will last forever.” (Sun Newspapers Ltd and Associated Newspapers Ltd v Federal Commissioner of Taxation [(1938) 61 CLR 337, at p 355] per Latham CJ; see also per Dixon J [(1938) 61 CLR, at pp 362-363]; and Ralli Estates Ltd v Commissioner of Income Tax [(1961) 1 WLR 329, at p 335])”

In the course of an illuminating judgment on this issue, Stephen J at 164-165 said:

“It is true that, if one looks at the substance and not merely at the form of the advantage which the taxpayer acquired, thus looking beyond the formal acquisition of shares, it was not, of course, perpetual in character; but neither was it by any means evanescent. It was of such a substantial duration as suitably to match the needs of the occasion. The activities of any extractive industry are necessarily of a wasting character and, as extractive industry goes, the advantage acquired gave promise, if all went well, as it in fact has done, of substantial duration. In light of what was said by Dixon J in the Sun Newspapers Case [(1938) 61 CLR, at pp 362-363] upon this question of the lasting character of an advantage, it is clear that the present case sufficiently satisfies that criterion. In Strick v Regent Oil Co Ltd [[1966] AC 295] Lord Wilberforce considered at length this criterion of lasting quality. His Lordship considered [[1966] AC, at p 353] a number of cases, including mining cases, in which advantages of relatively short duration had nevertheless been treated as capital assets, payment for them being, accordingly, outgoings of capital. He concluded that “the principle seems to emerge that if, on a consideration of the nature of the asset in the context of the trade in question, it is seen to be appropriate to classify it as fixed rather than as circulating capital, the brevity of its life is an irrelevant circumstance”.”

56 In Herring v Commissioner of Taxation (Cth) (1946) 72 CLR 543, Rich J considered a claim for a deduction for the cost of constructing a road between a public road and the boundaries of a forestry area to which the taxpayer had access by an agreement which contained an obligation upon the taxpayer to construct the road. At 547 his Honour said:

“… I accept the position that the road was constructed in pursuance of the agreement and because it was necessary for the purpose of removing the timber. But even so it amounted, as I think, to an outlay of a capital nature. It is not to the point that the outlay was made in connection with the creation of an asset of which the value for the purpose of profitably working the timber or obtaining royalties therefrom would progressively diminish. That happens when capital is spent in acquiring patents, mining leases or concessions limited in point of time. Income tax law may not always be just in the provisions it makes for writing off against assessable income the cost of such wasting or terminating assets. But that does not make their acquisition or creation any the less an affair of capital. The expenditure on the road formed a necessary outlay to obtain the “enduring benefit” of the expected royalties. Lord Cave LC, in using the phrase “enduring benefit” in British Insulated and Helsby Cables Ltd v Atherton [(1926) AC 205, at p 213], was not thinking of advantages that are permanent. There is a difference between the lasting and the everlasting. The time over which the thing “endures” is a matter of degree and one element only to be considered. Horses in the old days and motor trucks in these are plant and their acquisition for the purpose of transport in business usually involves a capital expenditure. But the horses were not immortal any more than the trucks have proved to be. …”

57 Apart from the value of what Rich J said in relation to the issue of enduring benefit, the decision itself is of importance. The road made accessible timber for the purposes of logging which was otherwise inaccessible. The payment was made pursuant to an agreement, and the road was constructed off the actual timber tenement. The manner in which his Honour continued after the passage which I have set out bears repetition:

“… Another test is that of Lord Dunedin, when Lord President, a test almost as frequently employed as Lord Cave’s was, expenditure made “once and for all” (Vallambrosa Rubber Co Ltd v Farmer [(1910) 5 Tax Cas 529, at p 536]). That test I think can give only one answer if applied to the case of the road. To deepen a shaft in a mine so that in the future the mine may be further worked involves an expenditure of a capital nature (Bonner v Basset Mines Ltd [(1912) 108 LT 764; 6 Tax Cas 146]). So is a lump sum payment by a colliery towards drainage works to allow a coal seam to be worked (Bean v Doncaster Amalgamated Collieries Ltd [(1944) 171 LT 214]). Further examples are to be seen in United Collieries Ltd v Inland Revenue Commissioners [(1929) 12 Tax Cas 1248]; Boyce v Whitwick Colliery Co Ltd [(1934) 18 Tax Cas 655; 151 LT 464]; Taupo Totara Timber Co Ltd v Commissioner of Taxes [(1912) 31 NZLR 617; (1913) AC 771, at p 777]; and Minister of National Revenue v Kellogg Co of Canada Ltd [(1943) SCR (Can) 58, at p 60].

These are but illustrations but they support my conclusion that the cost of the road is altogether an affair of capital.”

It will be seen that the authorities to which his Honour refers are nearly all cases involving mining.

58 Something more should be said about the issue of shafts in a mine, as the trial judge referred to two cases involving the issue – Denison Mines Ltd v Minister of National Revenue (1974) 49 DLR (3rd) 450 and Commissioner of Taxation v Mount Isa Mines Ltd (1991) 28 FCR 269. That the construction and deepening of shafts in a mine is capital expenditure has been clear since no later than Re Addie & Sons (1875) 2 SC 431 and the decision of the House of Lords in Coltness Iron Co v Black (1881) 6 App Cas 315. Denison Mines Ltd (supra) was a very special case. It did not involve a mine shaft, but rather underground passages which were created by actual ore extraction. The critical part of the trial judge’s finding ([1971] CTC 640 at 653-654) was as follows:

“… The activity was in fact current ore extraction to meet the appellant’s immediate need to produce ore. What the appellant did was to extract ore and that was anticipated by the appellant as the direct and immediate result of its expenditures even though the ultimate result of that activity was an asset that endured to the benefit of the appellant’s business. In my opinion the expenditures here in question are current operating expenses laid out as an integral part of the profit-making activity of the company. They were costs incidental to the production and sale of the output of the mine and as such are operating costs. …

The only justification for doing so [treating the expenditure as capital] would be that as a result of the extraction of ore from the passage-ways an asset of enduring benefit to the appellant’s trade resulted. But I have said above, the fact that a capital asset, in the sense of an enduring benefit resulting, does not necessarily make the expenditures expended therefor capital expenditures rather than revenue expenditures.”

59 Earlier, the trial judge, after referring to Viscount Cave LC’s enduring benefit concept, concluded, at 651:

“… these passage-ways have the quality of permanence to render them an enduring benefit within the meaning of the authorities. “Enduring” is a relative term and does not mean “everlasting”. The passage-ways will endure throughout the lifetime of the mine.”

In my view, this authority, if anything, assists the appellant’s arguments rather than the respondent’s arguments.

60 In Commissioner of Taxation v Mount Isa Mines Ltd (1991) 28 FCR 269, Pincus and Ryan JJ examined the established authorities in relation to mining shafts, and distinguished the digging of the decline from the shaft in the following way, at 287-288:

“… First, the decline was dug, not all at once, but in a series of relatively small excavations. Secondly, the decline was not dug as an asset to be used in the mine as a whole, but was made in the process of getting access to the particular part of the ore to be mined “in the near future”, to adapt an expression used by the taxpayer’s counsel. The construction of the decline was a continuing excavation, following the ore body down, dug as close as practicable to the ore body. The Agnew shaft was dug vertically, and was in places a very long way from the ore body.”

Their Honours then concluded:

“… The point is no doubt finely balanced, but the better view appears, with respect, to be that the annual expenditure in extending the decline in each year, substantially for the purpose of immediately mining the ore in the vicinity of the extension, should be deductible under s 51(1). …”

In what was, as their Honours acknowledged, a finely balanced decision, it seems to me that the critical points which tipped the scales were the recurrent nature of the expenditure and the continuous close physical connection with the actual recovery of ore. This provides no analogy to the present circumstances.

61 Another issue in that case is much closer to the present. The taxpayer sought deduction of the cost of construction of an earth and rock retaining wall which performed the function of a tailings dam. The nature of the issue, and the way in which the Court dealt with it, sufficiently appears from the following, at 282:

“… The retaining wall originally built proved unsatisfactory, since there was substantial seepage through it. Another problem which required to be considered was that the time was approaching at which the retained material would reach the top of the wall.

After consideration of other proposals, the taxpayer decided to build a new and substantially higher retaining wall, being that now in question, downstream from the original wall and that was done. At one end, it impinged upon the original wall. As the level of retained material rose over the years, it submerged the original wall.

The submission that the cost of construction of the dam was an outgoing giving rise to a deduction under s 51(1), although not strongly pressed, needs some analysis. The Commissioner contended, of course, that ordinarily a dam wall is excluded from the provisions of s 51(1) by the exception it contains of outgoings “of a capital … nature”. The argument for the taxpayer was principally that the construction of the dam was not a solution to the problem of tailings once and for all, but that on the evidence it appeared that it was necessary to build a new dam from time to time. Reference was made to evidence that “the management of tailings dams is a regular and ongoing matter but it has peaks of activity as, for instance, where one tailings dam reaches capacity or when groynes require construction”. It happens in many businesses, particularly large ones, that the making of capital expenditure of one sort or another is almost continual. As counsel for the taxpayer was inclined to concede, this massive, expensive and permanent structure would seem at first sight to be a matter of capital. It is true that eventually the area contained by the dam wall is filled up and it is necessary to build another one. But that is not sufficient to convert the cost of building of the dam wall into a non-capital outgoing. The judge’s conclusion that s 51 of the Act has no application to the tailings dam must be upheld.”

62 In Mallett v Staveley Coal & Iron Co Ltd [1928] 2 KB 405 a colliery company made payments to its lessor in consideration of his accepting the surrender of one mining lease and of a part of the area demised by another mining lease and releasing the company from its obligations under the first lease and its obligations in respect of the area surrendered under the second lease. The question was whether the payments were capital or income for income tax purposes. At first instance Rowlatt J dealt with the matter succinctly as follows at 409-10:

“It is abundantly clear that when a colliery company acquires a lease the expense of so acquiring it is the expense of acquiring a capital asset and is a capital expenditure, and it has been frequently remarked that it is very hard that there is no provision in the Act for allowing the company to establish a sinking fund or something of that kind to enable them to replace that capital expenditure. But there it is; it is a capital expenditure. If the company sell the lease that they have or part of it at an advantage, I cannot but think that what they receive would be a receipt on account of capital. Here what they have done is to get rid of a part of the area which they thought would be unremunerative, and they thought it well to pay for so doing. In my judgment, all receipts and payments in connection with acquiring and disposing of leases of minerals to be worked by collieries in this way are capital transactions for this purpose. I cannot see any other way of looking at it. The company have got nothing, says Mr Latter, for this expenditure. Perhaps that may be so, but they have got this: they have got a field of minerals which has the advantage of being no longer encumbered with an undesirable part. It seems to me that the whole transaction on the clearest possible principles is a capital transaction.”

That decision was upheld in the Court of Appeal ([1928] 2 KB 405) and was referred to, with apparent approval, by the High Court in Mount Isa Mines Ltd v Commissioner of Taxation (1992) 176 CLR 141 at 150. This is but one illustration of the fact that there need be no acquisition of something which may be termed an asset in balance sheet terms for expenditure to be on capital account.

63 In Robert Addie & Sons’ Collieries Ltd v Inland Revenue Commissioners [1924] SC 231 the Court of Session held that money paid by a mining company at the end of the lease to the lessor pursuant to the terms of the lease in order to restore and compensate for damage done to the surface by mining operations was capital rather than income. In my view, expenditure to satisfy a condition in the lease which has the effect of giving the right to mine in the instant case is a good deal further removed from the notion of revenue than is the restoration and compensation for damage done by mining operations.

64 Two of the cases referred to by Rich J in Herring (supra) are of assistance in resolving this matter. In United Collieries Ltd v Inland Revenue Commissioners [1930] SC 215 the taxpayer carried on the business of colliery and mine owner. Under certain agreements, it was bound to deepen either of two pits, worked by it under a lease, to reach certain lower seams, and to work such seams; the lessor being bound either to bear half of the expense of the opening up of these seams or (as he in fact elected) to accept reduced royalties. The sinking operations were completed in 1914, dewatering had taken place and a small quantity of coal was taken. After a few months, however, it was decided that it was inadvisable then to continue work on these lower seams and water in the pit was allowed to rise again to the upper seams. In 1923 the lower seams were again freed from water. The company claimed a deduction for the costs of this dewatering, contending that if they had kept the shaft free of water from 1914 until 1923 those expenses would have been on revenue account. The Lord President said, at 219-220:

“… Can the cost of this second dewatering – unlike the cost of the first – be said to be part of the ordinary expenditure laid out year by year in order to make profits year by year? Or is it – like the cost of the first dewatering – capital expenditure laid out for the purpose of making a permanent development of the works in which, as and when so developed, a profit-earning business is subsequently to be carried on? When the question is put in that form, it seems to me to be impossible to answer it except in one way. The second dewatering was no part of the ordinary working expenses of the colliery any more than the first. It was a piece of capital expenditure necessary to make, or to complete, part of the permanent works, the completion of which was a condition precedent to setting at work the process of earning profit by mining the lower seams. The distinction between a proper revenue charge and a proper capital charge has in recent years been one of the most frequently recurring problems before the Court in connexion with such undertakings as that of the appellants. I venture to refer to what I said at the beginning of my opinion in the case of Robert Addie & Sons’ Collieries [1924 S.C. 231].

It was not disputed that the expenditure incurred in dewatering the lower seams for a second time would have been a proper capital charge, if it had been the result of natural causes, such as an inrush of water from neighbouring mineral seams. But it was strongly argued that we ought to treat this duplicated expenditure as a revenue cost because of the close relation which exists between the process of keeping a pit (once dewatered) free of water, and the process of dewatering a pit either for the first time or for a second time, if for any reason the water has been allowed to accumulate in it. No doubt the two processes are closely connected, and the question might possibly be one of circumstances and of degree; but they are not in substance more closely connected than is the process of keeping in repair a haulage road in a pit with the process of constructing that haulage road. They both consist in the removal from the strata of whatever is necessary to open – or to keep open – a permanent access to the minerals which are to be worked; but they are entirely different things when considered from the point of view of the person who wants to make money by working the coal as and when made accessible. The dewatering is something he must do as a condition precedent to the working of the minerals to a profit.”

65 That decision was cited with approval by Scott LJ in Bean v Doncaster Amalgamated Collieries Ltd (1944) 171 LT 214 at 216. That case has similarities with the present case. By statute, any colliery company working in the area of the taxpayer’s mine was placed under an onerous duty to construct and maintain such works as might be necessary to remedy any loss of efficiency to the surface drainage due to subsidence from the working of the mines. By 1937 the taxpayer’s workings had approached close to an important watercourse. Some five million tons of coal lay under and beyond this watercourse, but before it could be worked very extensive drainage works would have been necessary in order to comply with the statutory requirements. The company’s preliminary estimate of the cost of those works was £68,000. The drainage board operating under the statute offered to relieve the company of their liability under the statute if they paid £39,000. The company accepted this offer, which made immediately accessible the 5 million tons of coal. The taxpayer claimed to deduct that sum in calculating income for assessment. Scott LJ, at 216, said:

“… The agreement with its 39,000l. expenditure thus procured for the respondents two “enduring advantages”. The first was, in effect, a large new acquisition of workable coal – for the company’s proprietary rights had no commercial reality, unless the surface drainage was maintained in accordance with the Acts. The second was permanent immunity from all the continuing expenditure entailed by the obligations of those Acts. Each of those two considerations is, in my opinion, sufficient by itself to constitute the expenditure in question a capital and not a revenue item in the respondents’ accounts; and it is on that accountancy test that the solution of the problem must nearly always depend.”

du Parcq LJ said, at 218:

“… It appears to me that the company has acquired by this expenditure an advantage for the enduring benefit of its trade, since thereby it has been enabled to work about 5,000,000 tons of coal over a period of six or seven years.”

Uthwatt J said, at 218:

“… the result of the transaction clearly was that the value of the particular coal measures – a capital asset remaining unchanged in character – was increased both for use and exchange. There was, therefore, as the result of the transaction brought into existence, not indeed an asset, but “an advantage for the enduring advantage of the trade of the company”.”

66 When the matter went to the House of Lords (sub. nom. Doncaster Amalgamated Collieries Ltd v Bean [1946] 1 All ER 642), Lord Simon, in a speech with which the other members of the house agreed, expressly approved that statement by Uthwatt J as one ground of decision. In my view, this reasoning is a powerful pointer to the conclusion that the expenditure here in question was capital rather than revenue.

67 I should mention two cases which deal with payments made to acquit obligations in mining agreements.

68 The first is the decision of Newton J in Utah Development Co v Commissioner of Taxation (Cth) (1975) 5 ALR 474. In that case, the taxpayer held an authority to prospect for coal over land in Queensland. It had been issued pursuant to an agreement between the State of Queensland, the taxpayer and another company. It provided that the taxpayer and the third party (“the joint venturers”) were entitled, on request, to be granted a special coal mining lease over any of the lands subject to the authority to prospect. A condition of the grant of such lease was that the joint venturers were liable to pay compensation to lessees of Crown land for damage to the land surface and improvements thereon caused by mining.

69 Special mining leases were applied for in respect of leasehold properties held by two other parties. The joint venturers agreed with one of these parties to pay a sum as compensation for disturbance of the surface area of part of the land, and as consideration for the surrender of her leasehold interest in another part to the Crown which would, in turn, lease it back to the joint venturers. This was to be used for services ancillary to the mining operation. In the case of the other lessee, it was agreed that an amount would be paid to it to surrender its interest to the Crown, which would then grant a special lease to the joint venturers. A portion of that land was included in the special mining lease, the remainder being used for ancillary services and for exchange with other Crown leaseholders whose properties were also included in the special mining lease.

70 The relevant part of the judgment concerned Division 10 of Part III of the Act. It is significant that it does not appear to have even been argued that the amounts paid, or any part of them, were deductible pursuant to s 51. In each case, the payments (inter alia) satisfied, in advance, the condition relating to compensation. The point, for present purposes, is that his Honour categorised the payments as being spent for the purpose of acquiring a mining property or for the purpose of acquiring the right to use a property as mining property (at 490). This must be regarded as a capital outgoing. This aspect of the decision was not affected by the appeal to the High Court (Commissioner of Taxation (Cth) v Utah Development Co (1976) 9 ALR 660).

71 The second is Cyprus Mines Corporation v Commissioner of Taxation (Cth) (1978) 22 ALR 322. In that case, an amount was paid to the Library Board of Western Australia under the description of a “royalty” as part of a complex arrangement involving the taxpayer, which conducted a mining operation, another party which had certain rights in relation to an adjoining area, and the State of Western Australia. Smith J said, at 341-342:

“… Although in cl 33(5)(a) of the supplemental agreement the payment is said to be a “royalty”, the payment was not in any sense an outlay made to secure the use and benefit of an asset for a royalty period, nor was the payment geared to the production of ore or quantified by reference to ore mined. It was a payment to be made once and for all by the joint venturers and to be made whether or not any ore was mined. Upon making the payment the joint venturers became entitled to apply for rights of occupancy pursuant to the Mining Act of mining areas, formerly the subject of the Sentinel 1967 agreement and other Crown Land, the subject of a ministerial reserve under the Mining Act for the purpose of prospecting thereon. The occupancy rights to be granted to the joint venturers pursuant to the supplemental agreement did not carry with them the right to mine. Under the agreement that right was to arise only when the joint venturers had demonstrated the feasibility of carrying out a mining operation on the areas of which they had occupation, in which event, subject to compliance by them with other obligations, the joint venturers were to be granted a mineral lease or leases under the Mining Act. Nevertheless, the occupancy rights for which the supplemental agreement makes provision, were valuable rights which the courts will protect (see Delhi International Oil Corporation v Olive [1973] WAR 52). They were rights which, as Mr Kober said, gave the joint venturers access to known iron ore deposits, which deposits if developed in conjunction with other deposits in mining area “B” of which the joint venturers already had occupancy rights under the 1964 agreement, would result in the joint venturers effecting a considerable saving of capital outlay. In these circumstances, notwithstanding the description given to the payment in the supplemental agreement, it seems to me that the real purpose of the payment was to acquire rights to mineral deposits with a view to bringing into existence an asset for the long term benefit of the venture in which the joint venturers were engaged. The outcome of that conclusion is that the expenditure is to be treated, for the purposes of the Act, as being attributable not to revenue but to capital and therefore is not deductible pursuant to s 51(1) of the Act.”

72 The respondent relies upon the decision of the Canadian Supreme Court in Johns-Manville Canada Inc v The Queen (1985) 21 DLR (4th) 210, a decision referred to by the trial judge. In that case, the taxpayer operated an open-pit mine. The facts are adequately summarised in the following passage from the leading judgment, at 212:

“… The law of gravity being what it is, the hole dug in the ground in order to remove the ore must be conically shaped and must expand outwards but on the same slope as the hole is deepened by the removal of ore. Hence the required enlargement of the diameter of the hole at the top of the mining pit necessitates the purchase of land at the periphery of the pit and the removal therefrom of the soil and rock to a substantial depth. The evidence was that for almost 40 years mining operations have required a progressive acquisition of land so as to maintain the walls of the conically-shaped mining pit at a safe angle. As the pit deepens in the course of mine operations its mouth at the surface must widen in order to maintain a safe angle of slope. Consequently, additional land was regularly acquired and any buildings thereon were removed. The soil was then stripped away so that the wall of the pit was pushed back or outwards from its prior location. In the conventional sense of “land”, all that remains of the acquired area is a part of a sloped wall, well below the original surface, between the top of the mine and the exposed ore body at the bottom of the pit. As additional land was acquired, the sloping wall was pushed further outward and consequently the actual location of the surface of each acquisition moves down the wall although the sloped angle of its surface remains generally constant. Any roadways located on the “steps” cut into the face of the wall likewise disappear on each enlargement of the pit and are re-established on the new sloping wall after the surface of the additional lands has been stripped off. All these changes proceed as the removal of the ore body progresses.”

73 As the trial judge noted, there was a 10-point analysis of the facts which led to the Court’s conclusion. His Honour set out two of them. The remainder are as follows:

“1. …

2. These expenditures were incurred year in and year out as an integral part of the day-to-day operations of the undertaking of the taxpayer;

3. These expenditures form an easily discernible, more or less constant, element and part of the daily and annual cost of production;

4. These lands were not acquired for any intrinsic value but merely by reason of location, and after the mining operation for the year in question had been completed, the land had acquired no intrinsic value, and indeed, as was found below, was “consumed” in the mining process;

5. …

6. The lands acquired in any given year do not produce a permanent wall or perimeter to the mining operation but are simply a transitional location of the wall representing the cone surrounding the mining undertaking; and to the extent that the wall of the cone is used for haulage of materials from the bottom of the pit on temporary roads, there may be some transitional asset created, but this asset disappears as the wall of the cone recedes in ensuing taxation years;

7. The nature of these expenditures is made clear when it is appreciated that they have been incurred annually for almost 40 years and there is no evidence whatever to indicate that mining operations can continue in the future without this annual expenditure;

8. The capitalisation of these expenditures will not produce for the mining operator an asset which may be made subject to either capital cost or depletion allowances, the former because no asset recognized in the Income Tax Act is produced, and the latter because these lands contain no minerals which are being removed by the mining operations of the taxpayer;

9. These expenditures did not add to the ore body, nor did they increase the productive capacity of the mine, nor do they bear any relation to any asset engaged in the mining operation, but are simply expenditures for the removal of overburden which, if not removed, would bring the mining operation to a halt;

10. The expenditures relative to the cost of operating the mine are small and are directly related to the cost of operation averaging over a long period about 3% per annum.”

74 Given those findings of fact, the conclusion that the outlay was deductible can be accommodated within established principles, and has very little relevance to the issue now to be determined. I note that the result was referred to by the High Court in Mount Isa Mines (supra) at 150 with no disapproval, although it is recognised as being an unusual case involving, as it did, the acquisition of land. However, I would find it hard to accept everything that was said in the principal judgment in that case, which was plainly heavily influenced by the Court’s view that any factual ambiguity should be resolved in favour of the taxpayer, particularly where the taxpayer did not qualify for the Canadian equivalent of deductions under Division 10. In particular, what is said about dewatering (at 227-8) is inconsistent with the decision of the Court of Session in United Collieries Ltd v Inland Revenue Commissioners (supra) and would be difficult to uphold in light of the principles enunciated in the cases to which I have referred, particularly the decision of the House of Lords in Bean (supra).

75 In Mount Isa Mines the High Court referred to the danger of applying the simple “purpose of the expenditure” test, noting that it too readily invited the answer that the purpose was to increase trading profits, referring to a passage from the speech of Lord Edmund-Davies in Tucker v Granada Motorway Services Ltd [1979] 1 WLR 683 at 693, where he said:

“… To apply that as the sole or principal test is unsatisfactory, for, as the respondents have rightly submitted, the purpose of any payment will generally be to improve a company’s trading profits, even if the purchase is of an obvious capital asset. This could lead to the conclusion (contrary to many long-standing decisions in the field) that the purchase of any asset must be regarded as involving revenue expenditure if it be made in order to reduce recurrent expenditure charged against profits.”

or, as in the present case, to increase profits by mining that which was made available to mine by the expenditure. In my opinion, to categorise the expenditure here as revenue rather than capital is to fall into the same error.

76 All of the expenditure relates to the relocation and reconstruction of the highway off-site. The issue in this case does not involve a claim for deduction of the expenditure of physically removing the road, either in one operation or progressively as mining takes place, nor does it involve the question as to whether, and in what circumstances, the removal of overburden is revenue rather than capital. A discussion of that issue would not, in my opinion, illuminate the present problem. Relocation of the highway (and, for that matter, any other road which might have been caught by the relevant clause of the lease) is the key which unlocks the ability to mine, and buying that key, or having it cut, is capital not income.

77 I am fortified by the terms of s 122A of the Act. If the argument for the respondent, which was accepted below, were correct, then it would follow, in my opinion, that many of the items which are identified as being of a capital nature by that section would be of a revenue nature.

78 Before departing from this aspect of the case, I should briefly refer to two further aspects of the judgment below. The first is the manner in which the trial judge dealt with what he called the “third matter”, namely, the third matter identified by Dixon J, as his Honour then was, in Sun Newspapers (supra) at 363: