Federal Court of Australia

AusNet Services Limited v Commissioner of Taxation [2025] FCAFC 21

Appeal from: | AusNet Services Limited v Commissioner of Taxation [2024] FCA 90 |

File number: | VID 206 of 2024 |

Judgment of: | LOGAN, THAWLEY AND KENNETT JJ |

Date of judgment: | 7 March 2025 |

Catchwords: | TAXATION – where appellant was inserted into the ownership structure of three entities which had until then been a stapled group – where transactions occurred on the same day in a predetermined sequence – whether the primary judge erred in concluding that the final transaction was a scheme for reorganising affairs for the purposes of s 615-5(1)(c) of Income Tax Assessment Act 1997 (Cth) (ITAA97) – whether the primary judge erred in concluding that the ratios in 615-20(2) of ITAA97 were equal – whether primary judge erred by departing from facts agreed between the parties |

Legislation: | Acts Interpretation Act 1901 (Cth) s 15AC Corporations Act 2001 (Cth) Evidence Act 1995 (Cth) s 191 Income Tax Assessment Act 1936 (Cth) s 177D, 177F, 260, Pt IVA; former ss 160ZZPA, 160ZZPB, 160ZZPC, 160ZZPD Income Tax Assessment Act 1997 (Cth) ss 1-3, 615-1, 615-5, 615-10, 615-15, 615-20, 615-25, 615-65, 995-1; Subdivs 615-A, 615-B, 615-C, 615-D; Divs 124, 615; Pt 3-90; former ss 124-360, 124-365; former Subdivs 124-G, Subdivs 124-H Tax and Superannuation Laws Amendment (2014 Measures No. 6) Act 2014 (Cth) Tax Law Improvement Act (No 1) 1998 (Cth) Taxation Administration Act 1953 (Cth) s 14ZZO Taxation Laws Amendment Act 1988 (Cth) Taxation Laws Amendment Act 1989 (Cth) New Business Tax System (Capital Gains Tax) Bill 1999 (Cth) New Business Tax System (Consolidation and Other Measures) Bill (No.1) 2002 (Cth) Tax and Superannuation Laws Amendment (2014 Measures No. 6) Bill 2014 (Cth) Tax Law Improvement Bill (No. 2) 1997 (Cth) Acts Interpretation Act 1954 (Qld) s 14C Explanatory Memorandum, Tax and Superannuation Laws Amendment (2014 Measures No. 6) Bill 2014 (Cth) Explanatory Memorandum, Tax Law Improvement Bill (No. 2) 1997 (Cth) Taxation Ruling TR97/18 (17 September 1997) |

Cases cited: | Alcan (NT) Alumina Pty Ltd v Commissioner of Territory Revenue [2009] HCA 41; 239 CLR 27 Baini v The Queen [2012] HCA 59; 246 CLR 469 BBlood Enterprises Pty Ltd v Commissioner of Taxation [2022] FCA 1112; 114 ATR 851 Certain Lloyd's Underwriters v Cross [2012] HCA 56; 248 CLR 378 Cheung v Federal Commissioner of Taxation [2024] FCA 1370 Commissioner for ACT Revenue v Araghi (2013) 7 ACTLR 262 Commissioner of Taxation v Consolidated Media Holdings Ltd [2012] HCA 55; 250 CLR 503 Commissioner of Taxation v Stone [2005] HCA 21; 222 CLR 289 Cooper Brookes (Wollongong) Pty Ltd v Commissioner of Taxation (1981) 147 CLR 297 Damberg v Damberg (2001) 52 NSWLR 492 Europa Oil (NZ) Ltd v Inland Revenue Commissioner (NZ) (No 2) [1976] 1 WLR 464 Federal Commissioner of Taxation v Myer Emporium Ltd (1987) 163 CLR 199 Federal Commissioner of Taxation v Peabody (1994) 181 CLR 359 Federal Commissioner of Taxation v Star City Pty Ltd (2009) 175 FCR 39 Fletcher v Federal Commissioner of Taxation (1988) 19 FCR 442 Furniss v Dawson [1984] 2 WLR 226 Harvey v Minister for Primary Industry and Resources [2024] HCA 1; 98 ALJR 168 Inco Europe Ltd v First Choice Distribution [2000] 1 WLR 586 Inland Revenue Commissioner (NZ) v Europa Oil (NZ) Ltd [1971] AC 760 Isles v Daily Mail Newspaper (1912) 14 CLR 193 Kenny & Good Pty Ltd v MGICA (1992) Ltd [1999] HCA 25; 199 CLR 413 Kingston v Keprose Pty Ltd (1987) 11 NSWLR 404 Melville v Townsville City Council [2003] QCA 456; [2004] 1 Qd R 530 Melway Publishing Pty Ltd v Robert Hicks Pty Ltd [2001] HCA 13; 205 CLR 1 Mornington Inn Pty Ltd v Jordan (2008) 168 FCR 383 Mullens Pty Ltd v Commissioner of Taxation (1976) 135 CLR 290 Northern Territory v Collins [2008] HCA 49; 235 CLR 619 Oakey Abattoir Pty Ltd v Federal Commissioner of Taxation (1984) 55 ALR 291 Peabody v Commissioner of Taxation (1993) 40 FCR 531 PMT Partners Pty Ltd v Australian National Parks & Wildlife Service (1995) 184 CLR 301 Project Blue Sky Inc v Australian Broadcasting Authority [1998] HCA 28; 194 CLR 355 R v A2 [2019] HCA 35; 269 CLR 507 Taylor v Owners – Strata Plan No 11564 [2014] HCA 9; 253 CLR 531 Wentworth Securities Ltd v Jones [1980] AC 74 WorkPac v Rossato (2021) 271 CLR 456 WT Ramsay Ltd v Inland Revenue Commissioners [1982] AC 300 Diplock WJK, "The Courts as Legislators" in Harvey BW (ed), The Lawyer and Justice (Sweet and Maxwell, 1978) 263 Leeming M, Common Law, Equity and Statute (Federation Press, 2023) |

Division: | General Division |

Registry: | Victoria |

National Practice Area: | Taxation |

Number of paragraphs: | 178 |

Date of last submission/s: | 23 August 2024 |

Date of hearing: | 8-9 August 2024 |

Counsel for the Appellant: | Mr J Gleeson SC with Mr A Roe |

Solicitor for the Appellant: | White & Case |

Counsel for the Respondent: | Mr E Wheelahan KC with Mr J Phillips |

Solicitor for the Respondent: | Australian Government Solicitor |

ORDERS

VID 206 of 2024 | ||

| ||

BETWEEN: | AUSNET SERVICES LIMITED Appellant | |

AND: | COMMISSIONER OF TAXATION Respondent | |

order made by: | LOGAN, THAWLEY AND KENNETT JJ |

DATE OF ORDER: | 7 MArch 2025 |

THE COURT ORDERS THAT:

1. The appeal be dismissed with costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

LOGAN J:

1 On 4 June 2015, the Supreme Court of Victoria, acting under the Corporations Act 2001 (Cth) and its inherent jurisdiction, approved three schemes of arrangement in respect of a group of companies then known as AusNet Services. This group consisted of AusNet Services (Transmission) Limited (Transmission), AusNet Services (RE) Ltd as trustee of the AusNet Services Finance Trust (Finance) and AusNet Services (Distribution) Limited (Distribution). Each unit in Finance was linked (or "stapled") to a share in Transmission and a share in Distribution. The effect of this linkage was that, before the implementation of the approved schemes of arrangement, none of the shares or units could be transferred or otherwise dealt with without the others. These stapled securities had been listed on the Australian and Singapore stock exchanges.

2 In accordance with the orders of the Supreme Court of Victoria, these schemes of arrangement were implemented in succession on 18 June 2015. By the end of that day, the appellant, AusNet Services Ltd, hitherto a shelf company, had acquired all the shares in Transmission, all the units in Finance and all the shares in Distribution. The former holders of the stapled securities became shareholders of the appellant. One feature of the implementation of the schemes of arrangement was that Distribution became a subsidiary of the appellant.

3 As Kennett J observes in his judgment, which I have had the privilege of reading in draft, an agreed statement of facts (referred to as the JSAF) was tendered in the original jurisdiction to which was annexed a bundle of documents.

4 Both for the purposes of the trial of the taxation appeal and this appeal, the facts so agreed had all the characteristics for which s 191 of the Evidence Act 1995 (Cth) (Evidence Act) provides. They were not required to be proved by evidence, were not to be disputed and could not be the subject in the proceedings of contradictory evidence. The effect of the section was that it was not open to the Commissioner to advance a factual submission contrary to a fact to which he had agreed: Mornington Inn Pty Ltd v Jordan (2008) 168 FCR 383, at [84], per Stone and Buchanan JJ.

5 Section 191 of the Evidence Act is a "modern extension" of the facility which has long existed for a party to narrow the factual issues in a proceeding by the making of an admission on the pleadings or otherwise formally at trial: Damberg v Damberg (2001) 52 NSWLR 492 (Damberg v Damberg), at 519 per Heydon JA. For reasons which I recently canvassed in Cheung v Federal Commissioner of Taxation [2024] FCA 1370, at [25]-[26], it is desirable in taxation litigation, perhaps even more so than in other civil litigation, to confine issues of fact and law. That in a taxation appeal the onus of proving an assessment to be excessive lies on a taxpayer (s 14ZZO, Taxation Administration Act 1953 (Cth)), does not prevent this. If the parties do so confine the issues, it is important in the administration of justice that the judicial branch decide cases accordingly, save where that might be subversive of such administration and then only after affording the parties an opportunity to be heard.

6 Such subversion might be found in circumstances where an admission made in conformity with s 191 of the Evidence Act is inconsistent with other evidence led at trial. A court might not, subject to observing procedural fairness as to an apprehended inconsistency, act on that agreed fact: Damberg v Damberg, at 522. That is not this case. Instead, given the agreed facts, it was not open to the primary judge to doubt them: Federal Commissioner of Taxation v Star City Pty Ltd (2009) 175 FCR 39, at [95] per Goldberg J (with whose reasons Dowsett and Jessup JJ generally agreed).

7 Further, it seems to me necessarily to follow from the prohibition of contradictory evidence that a trial judge is prohibited by s 191 from drawing inferences contrary to an agreed fact. Yet this is what the primary judge did by failing to act on the values agreed in the JSAF. That could, as the appellants submitted, be characterised as a denial of procedural fairness but I prefer to characterise it, as the appellant also put it, as a violation of s 191 of the Evidence Act.

8 The learned primary judge offered a detailed summary of most but not all of the facts so agreed in her Honour's reasons for judgment (at [9] – [36]). I do not repeat that summary. It does not follow that I accept that all the findings of fact made by her Honour were permissible, in light of the way the case was conducted before her by the parties, especially including the tender of the JSAF. Like Kennett J, I refer to the facts as so summarised and other agreed facts only to the extent necessary to explain my reasons for judgment. I likewise gratefully adopt, without repeating, save for explanatory purposes, the extracts of pertinent statutory provisions and summaries of submissions of the parties and related grounds of appeal, as set out in his Honour's judgment.

9 The primary judge termed the AusNet Services group of companies "the Distribution group" in her reasons for judgment. Her Honour observed (at [79]) of that group that, "As a matter of economic substance, from the time the stapling arrangements were put in place, the business of the Distribution group had been managed and operated as though it were part of a single economic entity that included Transmission and Finance." Her Honour also observed (at [82]) of the sequel to the implementation of the schemes of arrangement that, in relation to Distribution, the effect was "to align its legal structure with its economic structure. Economically it had been operated as though it were part of a wider group involving Transmission and Finance. Post the Distribution scheme, Distribution was legally owned within the same corporate group with a single parent company."

10 It is indisputably correct that, prior to 18 June 2015, in economic substance, there existed a single entity, as described by the primary judge, and that the end result of the implementation of the schemes of arrangement on 18 June 2015 was an economically equivalent, single economic entity, although the legal structure was changed.

11 A perception of Transmission, Finance and Distribution as a single entity is, to an extent, reinforced by Pt 3-90 of the Income Tax Assessment Act 1997 (Cth) (ITAA 1997) pursuant to the provisions of which treated them as a tax consolidated group(s) (TCG) of which Transmission was a head company of one (the Transmission TCG) and Distribution the other (the Distribution TCG). The changes effected by the implementation of the schemes of arrangement still yielded a TCG, albeit one of which thereafter, Distribution became a subsidiary member, with the appellant as the head company.

12 The question in the present appeal is whether, as the primary judge found, Div 615 of the ITAA 1997 applies to the arrangements by which the appellant came to be the holder of the shares in Distribution, with the consequence that it is taken to have made a valid rollover election under that Division and thus is not entitled to an increase in the cost bases of the assets of the former Distribution TCG? As the primary judge correctly observed (at [5]), "An uplift in those cost bases would have the effect of, amongst other things, increasing the capital allowance deductions that could be claimed by the [appellant]".

13 However, with all respect to the learned primary judge, that question is not to be answered by conceptions of economic substance or equivalence but rather by reference to the text of Div 615 in the agreed events which transpired concerning the legal entities affected by the implementation of the schemes of arrangement as approved by the Supreme Court of Victoria. The answer depends on what was done in fact and in law, not economic substance or equivalence: Inland Revenue Commissioner (NZ) v Europa Oil (NZ) Ltd [1971] AC 760 (Europa Oil), at 771 per Lord Wilberforce, Lord Pearson and Sir Frank Kitto; Europa Oil (NZ) Ltd v Inland Revenue Commissioner (NZ) (No 2) [1976] 1 WLR 464 (Europa Oil No 2), at 471-472 per Viscount Dilhorne, Lord Diplock, Lord Edmund-Davies and Sir Garfield Barwick (Europa Oil No 2); Mullens Pty Ltd v Commissioner of Taxation (1976) 135 CLR 290 (Mullens), at 301 per Barwick CJ.

14 More recently, in WorkPac v Rossato (2021) 271 CLR 456, at [62], Kiefel CJ, Keane, Gordon, Edelman, Steward and Gleeson JJ observed:

62 To insist upon binding contractual promises as reliable indicators of the true character of the employment relationship is to recognise that it is the function of the courts to enforce legal obligations, not to act as an industrial arbiter whose function is to synthesise a new concord out of industrial differences. That it is no part of the judicial function to reshape or recast a contractual relationship in order to reflect a quasi-legislative judgment as to the just settlement of an industrial dispute has been emphatically the case in Australia at the federal level since the Boilermakers Case.

[Footnote references omitted]

These observations are by no means confined in their relevance to industrial cases. In the absence of some charter flowing from the text of a taxation statute, it is likewise no part of the judicial function on a taxation appeal (or in assessing the Commissioner's) to reshape or recast a contractual relationship in order to reflect a quasi-legislative judgment as to the just taxation of a particular corporate or natural person or a trust which substitutes what is perceived to be the substance of a transaction over its contractual form.

15 Of course, even in the absence of an anti-avoidance provision, there are taxation cases where, viewed against the context of wider taxable facts, the tax consequence of a contractual transaction may be different from viewing that transaction in isolation. For example, an isolated receipt from a contractual transaction might, when viewed against a wider factual matrix, not aptly be characterised as one on capital account but instead just an incident of the carrying on of a business and income under ordinary concepts: Federal Commissioner of Taxation v Myer Emporium Ltd (1987) 163 CLR 199. But such an outcome in revenue law does not mean that the legal obligations between the parties are recast to be anything other than those created by a governing contract.

16 In dismissing one basis on which the appellant had cast its submission that Div 615 had no application, which concerned an inability, in light of market values agreed between the parties, for the ratio requirements specified in s 615-20 of the ITAA 1997 to be satisfied, given what was entailed in the staggered implementation, over the course of 18 June 2015, of the approved schemes of arrangement, the learned primary judge also observed (at [101]):

Because of the legal interdependence of the schemes, there is an air of unreality to the applicant's submission that immediately prior to the completion of the Distribution scheme, the Transmission and Finance schemes had transferred value to the applicant that was independent of the value of the Distribution. The reality was that all the value accrued to the applicant and in the shares issued by it at the same moment because either all the schemes were completed or none were. There was no moment in time when the applicant could reflect the value of Transmission and Finance and not also reflect the value of its obligation to acquire Distribution in exchange for the issue of shares.

[Emphasis added]

17 However, and once again with all respect, not only is the "reality" upon which her Honour relied to reject this submission at variance with the progressive legal consequences of the staggered, transactional implementation of the approved schemes, and thus also contrary to Europa Oil, Europa Oil No 2 and Mullens, it is also, as will be seen, at variance with facts as to market value agreed between the parties and thus contrary to s 191 of the Evidence Act and the application of s 615-20 of the ITAA 1997 to those facts.

18 There was never any suggestion by the Commissioner in this case that the transactional steps entailed in the implementation of the approved schemes of arrangement were shams.

19 Nor was ever there any suggestion by the Commissioner that the applicability of Div 615 arose because the approved schemes of arrangement fell afoul of Pt IVA of the Income Tax Assessment Act 1936 (Cth) (ITAA 1936). Unlike with s 177D(2)(b) within Part IVA of the ITAA 1936, nothing within Div 615 of the ITAA 1997 conferred upon the primary judge a charter to compare form and substance. Further, unlike its predecessor, s 260 of the ITAA 1936, s 177D of the ITAA 1936 does not operate of its own force. The authority for raising or amending an assessment to cancel a tax benefit in circumstances where it would be concluded that a scheme entered into by taxpayer was entered into for the dominant purpose of obtaining that tax benefit is engaged by the making by the Commissioner of a determination pursuant to s 177F of the ITAA 1936. In this case, there was no such anterior determination by the Commissioner. And as Hill J (Ryan and Cooper JJ agreeing) observed in Peabody v Commissioner of Taxation (1993) 40 FCR 531, at 547, "this Court cannot stand in the shoes of the Commissioner and exercise discretions which the legislature has committed to the Commissioner" (Commissioner's appeal subsequently dismissed by a unanimous High Court (Federal Commissioner of Taxation v Peabody (1994) 181 CLR 359)). That is in marked contrast to the Administrative Review Tribunal (and its predecessor, the Administrative Appeals Tribunal), which does stand in the shoes of the Commissioner when undertaking the jurisdictionally distinct role of reviewing an objection decision and which can itself, subject to observing procedural fairness, make a determination under s 177F of the ITAA 1936: Fletcher v Federal Commissioner of Taxation (1988) 19 FCR 442.

20 Yet further, the very presence in Australian income tax legislation of a general anti-avoidance provision means that a charter for a judicial comparison of form and substance to the end of determining a tax liability by reference to the "economic reality" of events is not to be found in the doctrine of "fiscal nullity" established by the House of Lords in WT Ramsay Ltd v Inland Revenue Commissioners [1982] AC 300 and Furniss v Dawson [1984] 2 WLR 226: Oakey Abattoir Pty Ltd v Federal Commissioner of Taxation (1984) 55 ALR 291, at 297-299.

21 Instead, if one adheres to the text of Div 615 and to s 191 of the Evidence Act in relation to agreed market values and gives effect to those values in light of the legal consequences that progressively occurred on 18 June 2015 as each approved scheme of arrangement was implemented in succession that day, the inevitable result is that s 615-20 of the ITAA 1997 could never be satisfied.

22 On the appeal, the Commissioner embraced the reasoning of the primary judge. For reasons already given, this entails, outside the confines of a contemporary tax avoidance case, endeavouring to resurrect the long-discredited notion of taxation by end result, rather than resolving the controversy by reference to the text of the provisions concerned as applied to the events which in fact and legal character occurred.

23 As it happens, the Commissioner's submissions as to the meaning to afford the text of the provisions of Div 615 entail a departure by him from reasoning which underpinned an early ruling he issued (TR 97/18) on like predecessor rollover provisions, to the exclusion of an adoption of that reasoning by the appellant. Although the Commissioner's position is not without irony, it is axiomatic that the meaning of the text cannot be dictated by a priori assumptions howsoever based, only by the text itself, as read in context and in light of the evident purpose of the provision: Commissioner of Taxation v Consolidated Media Holdings Ltd (2012) 250 CLR 503 (Consolidated Media Holdings).

24 Principled eschewing of a priori assumptions is one thing; an ex post facto consequence of the construction of the text of a statutory provision in accordance with the approach mandated by Consolidated Media Holdings and the authorities discussed therein is quite another. Contrary to a conclusion reached by the primary judge (at 120] and [130]-[135]) and a related submission of the Commissioner, a feature of Div 615 is, as the appellant submitted, that the interposed company must be a shelf company an ex post facto consequence of approaching its construction in this way, not an a priori assumption.

25 Against the background of these general observations and related conclusions, it is now necessary to examine in greater detail the issues raised by the grounds of appeal and, related to that, set out my reasons for these conclusions.

26 A threshold difference between the parties was whether, as the Commissioner contended and the primary judge found, within the composite term "scheme for reorganising its affairs" in s 615-5(1)(c), the word "affairs" carried with it the characteristic that the "affairs" must relate to the "original entity's (be that company or unit trust) ownership structure or whether "affairs" was, as the appellant submitted, not so limited.

27 The Court was pressed in submissions with authorities concerning the meaning of "affairs" in other statutory contexts, some perhaps analogous. But error can lie in analogy in statutory construction. I consider it preferable to approach the meaning of "affairs" just with reference to the meaning of the word as used in the context of Div 615 and having regard to the purpose of that Division.

28 That a difference of views has emerged is not surprising. With all respect to its drafting author, s 615-5(1)(c) employs a confusion of concepts. As a matter of ordinary English, a reference to the "affairs" of a company does not point naturally to its ownership structure or, more perhaps better put, not only to that subject but to everything related to the conduct of the company's existing business or undertaking. Yet immediately after "scheme for reorganising its affairs", s 615-5(1)(c) offers the qualifying description, "the exchanging members dispose of all their shares or units". In my view, when read in context, that qualifying description does indeed narrow the focus of "affairs" in the way the primary judge concluded.

29 Assistance for this conclusion is found in s 615-1. It contains a similar but at least consistent confusion of concepts. Unconstrained by context and as a matter of ordinary English, the "reorganisation" of a "business" might embrace a change in underlying ownership but it might equally, for example, entail a change in managerial arrangements from centralised control to decentralised control without any change at all to the formal ownership structure. Further, as with the "affairs" of a company, a business would not be "reorganised" if that business were substantially altered. Instead, a new set of corporate affairs or a new business would have been created. Once again though, read in context, a focus on a change in ownership of a described type is evident in what is meant in s 615(1) by the "restructuring" of a "business".

30 Regard to purpose also supports the conclusion of the primary judge as to the meaning of "affairs". Division 615 is entitled "Roll overs for business restructures" and is in turn part of Part 3 80, which is entitled "Roll overs applying to assets generally". Division 615 can be seen as having the purpose of offering relief in defined circumstances from the tax consequences which would otherwise follow from the changes in the ownership of assets in circumstances where the formal ownership structure of a business has been changed but, subject to ratios, underlying ownership has not been and the business itself is continued. This purpose is achieved by affording "affairs" the meaning assigned by the primary judge.

31 For all that, s 615-5(1)(c) nonetheless requires that the scheme be one "for" reorganising "its", i.e. a particular company's (or unit trust's) affairs. The preposition "for" introduces the purposive criterion of reorganising. The possessive "its" carries with it a particularly of entity focus. Here, that means there must be a scheme for reorganising [Distribution's] affairs, not those of some other entity or even those of Distribution and some other entity. The ratios for which s 615-20 provides underscore this singularity of entity focus in s 615-5.

32 The conclusion reached concerning the meaning of "affairs" means that the non-reorganisational features of the Distribution scheme to which the appellant pointed are not relevant to the application or otherwise of Div 615.

33 Even accepting, as I do, that "affairs" carries the meaning assigned by the primary judge, there is merit in the appellant's further submission that her Honour's reasoning impermissibly conflates separate businesses and transactional events and, related to that, contravenes in fact finding s 191 of the Evidence Act.

34 By virtue of para 14 of the JSAF, the following were agreed facts:

As at 18 June 2015:

(a) The Transmission tax consolidated group of which Transmission was the head company (Transmission TCG) owned and operated Victoria's primary regulated electricity transmission network (which was privatised in 1997). This network was regulated by the Australian Energy Regulator, and the Transmission TCG's right to provide transmission services throughout Victoria was outlined in its electricity transmission licence. As at 31 March 2014, this network consisted of approximately 6,500 kilometres of transmission lines.

(b) The Distribution tax consolidated group of which Distribution was the head company (Distribution TCG) owned and operated both the electricity distribution network and gas distribution network assets (which were acquired in 2004). The electricity and gas distribution networks were also regulated by the Australian Energy Regulator. As at 31 March 2014, the Distribution TCG distributed electricity to approximately 670,000 customers within its network covering eastern metropolitan Melbourne and eastern Victoria, and distributed gas to approximately 633,000 customers located in its distribution area in central and western Victoria.

(c) Finance operated to provide finance to the Transmission TCG and Distribution TCG, and had loans of approximately $2.8bn in total to the Transmission TCG and Distribution TCG on issue.

35 Further, it was also agreed (JSAF at [15]), and the primary judge recorded (at [29]), that, as at that time, the entities which conducted those separate businesses had separate market values:

(a) Finance's market value was $2.874 billion;

(b) Distribution's market value was $2.025 billion; and

(c) Transmission's market value was $0.525 billion.

36 The agreed facts admitted only of a finding at trial that the Transmission TCG, the Distribution TCG and Finance operated separate (but not unrelated) businesses. Perhaps that is what the primary judge meant at [78] in stating that, before the Distribution scheme "Distribution did not operate a separate stand-alone business". However, her Honour's further statement (at [79]), in the face of expressly acknowledging (at [29]) the agreed fact of separate valuations, that, there is "an air of unreality in positing a moment in time in which Distribution is hypothesised as carrying on a business that had an existence and value independent of Transmission and Finance" is not reconcilable and tells otherwise.

37 The point is that it was agreed that as at the start of 18 June 2015, separate businesses with separate market values existed. Nothing in the Stapling Deed changed this. Nothing in the Implementation Deed in respect of the schemes of arrangement changed this.

38 Further, the very first of the successive steps for which the Implementation Deed provided entailed the "unstapling" of the hitherto stapled entities of Finance, Distribution and Transmission. One might find an "unreality" about this if the Implementation Deed were but a sham. But it bears repeating that there was never any such suggestion. That "unstapling" was a reality in law. At that point, the stapling hitherto provided for by the Stapling Deed dropped away. So even if, contrary to my view, and the agreed facts, that Deed created but one business carried on by the three entities, that was no longer so. Being a reality in law and fact, and in the absence of any statutory warrant, the primary judge was not entitled to look to economic substance to contradict this.

39 Division 615 contains very precise temporal focal points. Section 615-20(2)(b)(ii) requires a determination of market value which is "worked out immediately before the first disposal, redemption or cancellation". Section 615-30(2) requires attention to consolidated group positions "immediately before" and "immediately after" the "completion time".

40 On the agreed facts, and as the appellant correctly submitted, "immediately before the completion of the Distribution scheme, Distribution's attributes were that of a business with an existence and value independent of Transmission and Finance, such that its business affairs could be reorganised independently to those entities".

41 It is necessary to remember that in this case there were three "schemes". The Distribution Scheme was but one of them. It is only that scheme which is aptly described as a "scheme" for the reorganising of Distribution's affairs. Although each scheme was implemented on 18 June 2015, each had different temporal focal points that day entailing different legal relationships. That remained so even though, at the start of that day, there was an expectation of implementation in succession over the course of the day (flowing from cl 5.1(b) of the Implementation Deed, which provides for the schemes to occur sequentially). There is provision in cl 5.1(c) of the Implementation Deed that, if it becomes clear (whether on or before the Implementation Date) that some or all of the steps will not take place, no party is compelled to complete any further steps but that clause does not invalidate a step that has already occurred. Contrary to a finding of the primary judge (at [98]), the three schemes were not the same transaction. The three schemes are most accurately characterised as separate but interdependent. However, the description "interdependent", "is simply shorthand for the combined operation of the various explicit provisions by which the operation of one contract is related to the operation of the other": Commissioner for ACT Revenue v Araghi (2013) 7 ACTLR 262, at [53]. It does not mean there was but one scheme implemented on 18 June 2015.

42 Division 615 required that the position immediately before and immediately after each scheme in question be considered. The statute contained no warrant for conflation of them by reference to a position at the start of 18 June 2015 and the end of that day, looking to economic substance or end result to the exclusion of the positions which sequentially existed in fact and law as each scheme was implemented over the course of that day.

43 Looking to the Distribution scheme and adhering to the required temporal focus in relation to that scheme, it was a factual given that, immediately before that scheme, the appellant was not a shelf company. On the agreed facts, and for reasons detailed below, only if it were a shelf company would the ratio requirements in s 615-20 be satisfied. In that circumstance, and as the appellant correctly submitted, no question of what was termed in the case the "boost" would arise "because there would not be material shares in the appellant already on issue". The "boost" was a shorthand reference to a submission made by the appellant before the primary judge and us that, as a result of the Distribution scheme, the value of the pre-existing shares in the appellant increased. This conclusion entails no a priori assumption as to the meaning of that provision, rather an understanding of the consequence of applying it according to its terms.

44 Before detailing further why the s 615-20 ratio requirements could not be satisfied, it is convenient to resolve a separate statutory controversy as to the meaning and effect of the "and nothing else" qualification, as found, presently materially in s 615-5(1)(c). That specifies as a criterion of application, "under a *scheme for reorganising its affairs, the exchanging members *dispose of all their shares or units in it to a company (the interposed company) in exchange for shares in the interposed company (and nothing else)".

45 On the appellant's case the "boost" was also said to be pertinent because it was "something else" received in the "exchange" referred to in s 615-5(1)(c). Other such "something elses" flowing from the Distribution Scheme were said to be an expectation of increased franked dividends and the benefit of the repayment of outstanding Finance loans without adverse tax consequences. The latter two were, undoubtedly, benefits of the schemes as implemented on 18 June 2015. The appellant submitted that the primary judge erred in not adopting a construction of s 615-5(1)(c) which recognised that more was received for the "exchange" than just shares in the interposed company.

46 Considered as an abstract proposition, divorced from reading the text of s 615-5(1)(c) in context, there is much to recommend the appellant's submission. However, read in context, the focus of this provision is just on the consideration for the exchange. The intention of the parenthetical qualification "and nothing else" is to confine the application of this criterion just to an exchange where shares in the interposed company, as opposed to additional consideration, are received. It does not look to incidental consequences of the "exchange". Adopting that construction is congruent with the notion of the reorganisation, already discussed, for which s 615-5(1)(c) provides and with s 615-1, "in exchange, you become the owner of new shares in another company". It is also congruent with the heading of s 615-5, "Disposing of interests in one entity for shares in a company". I do not therefore accept the construction of s 615-5(1)(c) pressed for the appellant.

47 I return then to the subject of s 615-20 and the ratios for which that section provides. That section requires that the ratios in s 615-20(2)(a) and s 615-20(2)(b) equal one another. It was a feature of the approved schemes of arrangement that, although each was implemented on 18 June 2015, there were different "completion times" that day, flowing from their sequential implementation. The temporal focus in s 615-20 flowing from "completion time" is on the completion time in respect of a specific scheme, materially here the Distribution Scheme. More particularly, for the purposes of s 615-20, the denominator in the ratios referred solely to the shares either issued or disposed of under that scheme.

48 In their submissions at trial, which were repeated before us, the appellants offered this description of the provision in s 615-20 for ratios – "s 615-20 ratios test whether the relative value of shareholdings both before and after the reorganisation, measured as a fraction of the market value of shares issued in exchange under the reorganisation are exactly equal". That description should be accepted as correct. It well conforms with the evident purpose, discussed above, of Div 615. The relief offered is, in effect, where all that has occurred as a result of a given scheme is a reorganisation.

49 Having regard to the agreed market values of Finance, Distribution and Transmission (set out above) the progressive implementation of the approved schemes necessarily carried with it the "boost" alleged by the appellant.

50 Explaining this requires that the events which sequentially occurred on 18 June 2015 now be detailed. It is convenient to do this, as did the appellant in its submissions before the primary judge (on which this account draws) by reference to the steps for which Schedule 1 of the Implementation Deed provided, and then adapting these to the text of s 615-20(2). It bears repeating that it was agreed before the primary judge that those steps took place on 18 June 2015 and in the order for which that deed provided (noting that "NewCo" is the appellant):

Unstapling

"Each of Transmission, Distribution and Trustee [ie, AusNet Services (RE) Ltd as trustee of Finance] Unstaples the Stapled Securities". This step occurred at around 7:42am.

Ineligible Foreign Securityholder transfers

"In accordance with the Transmission Scheme, Transmission, as attorney and agent for each Ineligible Foreign Securityholder, will transfer the Ineligible Transmission Shares held by the Ineligible Foreign Securityholders to the Sale Nominee".

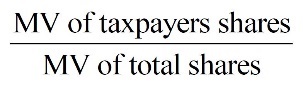

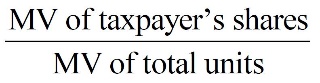

"In accordance with the Trust Constitution Amendments, Trustee, as attorney and agent for each Ineligible Foreign Securityholder, will transfer the Ineligible Units held by the Ineligible Foreign Securityholders to the Sale Nominee".

"In accordance with the Distribution Scheme, Distribution, as attorney and agent for each Ineligible Foreign Securityholder, will transfer the Ineligible Distribution Shares held by the Ineligible Foreign Securityholders to the Sale Nominee".

These steps occurred at around 8:23am.

Transfer of Transmission Shares under Transmission Scheme and cancellation of NewCo Shares

"In accordance with the Transmission Scheme, Transmission, as attorney and-agent for each Eligible Securityholder, transfers all the Transmission Shares to NewCo, in consideration of NewCo issuing one NewCo Share for each Transmission Share, to each Eligible Securityholder".

"At the same time as step (e), NewCo cancels the 2 NewCo Shares held by AusNet Distribution Group under a selective share capital reduction".

These steps occurred at around 9:03am.

Transmission tax consolidated group

"NewCo makes an election [under s 615-30(2) of the Income Tax Assessment Act 1997 (Cth) (1997 Act)] that the Transmission tax consolidated group is to continue in existence at and after Implementation". This step occurred at around 9:30am.

Transfer of Units under Trust Scheme

"In accordance with the Trust Scheme, Trustee, as attorney and agent for each Eligible Securityholder, transfers all the Units to NewCo, in consideration of NewCo issuing the one NewCo Share for each Unit, to each Eligible Securityholder. For the avoidance of doubt, Trustee will not effect this step (h) until after such time on the Implementation Date that NewCo has acquired the Transmission Shares under step (e) and then has elected to continue the Transmission tax consolidated group under step (g)". This step occurred at around 9:56am.

Transfer of Distribution Shares under Distribution Scheme

"In accordance with the Distribution Scheme, Distribution, as attorney and agent for each Eligible Securityholder, transfers all the Distribution Shares to NewCo, in consideration of NewCo issuing one NewCo Share for each Distribution Share, to each Eligible Securityholder. For the avoidance of doubt, Distribution will not effect this step (i) until after such time on the Implementation Date that NewCo has acquired Transmission Shares under step (e), has elected to continue the Transmission tax consolidated group under step (g) and then has acquired the Units under step (h)". This step occurred at around 10:32am.

Consolidation of NewCo Shares

"NewCo converts all the NewCo Shares into that number of NewCo Shares equal to the number of Stapled Securities that had been on issue at the Record Date". This step occurred at around 11:59am

[footnotes references omitted]

51 As can be seen, there was a succession of "completion times" on 18 June 2015. The completion of the several schemes were not simultaneous.

52 Applying the text of s 615-20(2) ratios to the events just described, the sub-paragraph (a) numerator is equal to the market value of all shares in the appellant ("NewCo", the interposed company) owned by each exchanging member. Necessarily, this includes the shares in the appellant issued to each shareholder because of the Distribution scheme and also the shares in the appellant previously issued to each shareholder in respect of the Transmission Scheme and the Finance Trust Scheme. The sub-paragraph (a) denominator is the market value of only those shares issued in exchange for the Distribution shares under the Distribution Scheme.

53 Again applying the text of s 615-20(2) to the events just described, the subparagraph (b) ratio is calculated by reference to a numerator equal to the market value of that exchanging member's shares in Distribution that were disposed of under the scheme; with a denominator being the market value of all the shares in Distribution that were disposed of under the scheme worked out immediately before the first disposal.

54 The construction favoured by the primary judge inserts 18 words into the provision such that it is as if it read, "the *market value of each exchanging member's *shares in the interposed company issued to that member in exchange for that member's shares in the original company under the scheme": (at [117(6)]). It was this construction which was taken up by the Commissioner.

55 There is no warrant for reading any words into the text of s 615-20(2). The cautionary note sounded in PMT Partners Pty Ltd v Australian National Parks & Wildlife Service (1995) 184 CLR 301, at 310, about the reading of limitations and qualifications into the text of statutory definitions is just as important in relation to the text of statutory eligibility criteria. Doing this in this case necessarily changes the integers of, and thus fundamentally alters, the mathematical ratios evident on the face of the text of the provision. The inserted words are, with respect, nothing more than a rationale for a conclusion impermissibly reached by an economic substance driven approach.

56 Within s 615-20(2)(a)(ii), "issued to all the exchanging members" and "completion time" are, as the appellant submitted, directed to "the shareholding consequences of the relevant scheme". They dictate a scheme specific singularity of focus. In contrast, in s 615-20(2)(a)(i), reading "*shares in the interposed company" in context does not dictate that this expression is to be qualified in any way.

57 Having promoted the reading of no less than 18 words into s 615-20(2)(a)(i), the Commissioner submitted that there should be no corresponding qualification of the same expression, "exchanging members", in s 615-25(3)(a). This was an odd submission. If it be right to qualify this expression by the addition of unstated, qualifying words in the one provision, it is no less right in a consistent way to likewise qualify that same expression within Div 615 in the other. On the other hand, just adhering to the text of s 615-25(3)(a) yields a rational meaning well in conformity with the overall purpose of Div 615. As the appellant nicely put it, adhering to the text, "prevents outsiders from owning shares in the interposed company, and avoids entities being able to satisfy the definition of 'exchanging members' by virtue of a pre-existing scheme different to the scheme under consideration". That leaves s 615-25(3)(b) providing for a de minimis exception in circumstances where the "interposed company" has had up to five shareholders that have retained their shareholdings but the market value of their shares is merely trifling.

58 Construing s 615-20 and s 615-25 in this way does not result in a capricious or irrational meaning such that, in accordance with principles of statutory interpretation discussed in Cooper Brookes (Wollongong) Pty Ltd v Federal Commissioner of Taxation (1981) 147 CLR 297, a departure from the literal meaning of the text is warranted. It yields a consistent meaning, revealing that Parliament's intended purpose with Div 615 was to afford rollover relief on a reorganisation in circumstances where the interposed company was of but nominal value. Further and consistently, it discloses it was intended that, if the reorganisation concerned the shareholdings in an entity other than the target entity were also reorganised, Division 615 roll-over would be attracted only where that other entity was of but nominal value.

59 It is possible to discern a like intention in predecessor provisions to Div 615 – s 160ZZPA of the ITAA 1936 and then, s 124-385(3) within Subdivision 124-G. In turn, it is possible to discern in explanatory memoranda touching on such provisions an understanding that the interposed company had to be a shelf company to attract rollover relief to a reorganisation scheme: see in the explanatory memorandum to the New Business Tax System (Capital Gains Tax) Bill 1999 (Cth) which introduced Subdivision 124-M, paras 2.48 and 2.49 and, in paras 2.6, 2.7 and 2.11 of the explanatory memorandum to the New Business Tax System (Consolidation and Other Measures) Bill (No.1) 2002 (Cth), it is made explicit that the consolidation provisions ss 703-65 to 703-80 were being introduced on the basis that the criteria in Subdivision 124-G required a shelf company. A like statement was made by the Minister in the Second Reading Speech concerning that Bill.

60 Ordinarily, the relevance of such secondary materials, which do not relate directly to Div 615, would be moot to say the least. However, with respect to the Tax and Superannuation Laws Amendment (2014 Measures No. 6) Bill 2014 (Cth), which proposed the introduction of Div 615, the related explanatory memorandum stated (para 1.31) that the reason for its introduction of Div 615 was to "consolidate the two separate Subdivisions which provide effectively identical roll-overs for restructures of trusts and companies into a single Division". No intention to change the then prevailing intended reach of the rollover relief is evident from this explanatory memorandum. Even given this linkage with predecessor provisions, perhaps all that can be said of the secondary materials canvassed is that they provide a level of comfort in respect of a meaning evident enough from the text of Div 615, as read in context. In contrast, those same materials serve only to deepen a disquiet about the construction promoted by the Commissioner.

61 It does not follow from accepting the appellant's construction of s 615-20 that it entails acting on an a priori assumption that the interposed company must be a shelf or nominal value company. That is but a consequence of adopting an orthodox approach to statutory construction.

62 Before the primary judge and in submissions before us (as supplemented by a helpful aide-memoire) the appellant illustrated, with reference to the agreed values, the impact of the progressive implementation of the schemes of arrangement if one adopted the construction of s 615-20 promoted by the appellant. For this purpose, the appellant cited an example of the position of a representative security holder holding a 1% interest in each entity. That yielded the following ratios, which I detail by adopting, without further attribution, submissions made to the primary judge by the appellant and repeated before us:

(a) before the Distribution Scheme, there were approx. 6.94b shares issued by the appellant with a market value of $3.4b (a 1% interest being $34m)– with 3.47b issued under the Transmission Scheme and 3.47b issued under the Finance Trust Scheme;

(b) before the Distribution Scheme, all the 3.47b shares in Distribution had a market value of $2.0b (a 1% interest being $20m);

(c) the Distribution Scheme involved an issue of an additional 3.47b shares by the Applicant to all exchanging members (that is, a one-third interest in the Applicant by market value, being one-third of $5.4b - $1.8b); and

(d) following the Distribution Scheme, the combined market value of each of Transmission, Finance and Distribution was $5.4b (a 1% interest being $54m).

82. The resultant ratio, calculated pursuant to s 615-20(2)(a) is:

d) Market value of shares in the Applicant owned by the exchanging member | $54m |

e) Market value of shares in the Applicant issued in exchange for shares in Distribution to all exchanging members (worked out immediately after the completion time) | $1.8b |

f) Ratio | 1:33 1/3 |

83. The resultant ratio, calculated pursuant to s 615-20(2)(b) is:

g) Market value of the exchanging member's shares in Distribution that were disposed of, redeemed or cancelled under the scheme | $20m |

i) Market value of shares in Distribution that were disposed of, redeemed, or cancelled under the scheme | $2b |

k) Ratio | 1:100 |

63 The example given is derived from the agreed facts. Those facts ought, inexorably, to have led to a conclusion that, over the course of 18 June 2015, the "boost" posited by the appellant occurred. It was not possible in the face of s 191 of the Evidence Act, for the primary judge to conclude otherwise.

64 Because the ratios were not equal, it necessarily followed that s 615-20 was not satisfied such that Div 615 was inapplicable.

65 For these reasons, I would allow the appeal, set aside the orders made in the original jurisdiction and, in lieu thereof, order that the appellant's objection be allowed in full with the matter being remitted to the Commissioner for the making administratively of the requisite amended assessments. The Commissioner should pay the appellant's costs of the appeal and in the original jurisdiction.

I certify that the preceding sixty-five (65) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Logan . |

Associate:

Dated: 7 March 2025

REASONS FOR JUDGMENT

THAWLEY J:

66 I agree with the orders proposed by Kennett J and with his Honour's reasons.

67 The preferable construction of s 615-20(2)(a) is that identified by Kennett J at [136]. This construction, which begins and ends with the text of the provision, is consistent with the history of this type of roll-over relief and with all extrinsic material, none of which suggests that a change was intended to be worked as between the ratio previously found in s 160ZZPA(1)(m), later in s 124-365(3) and the present formulation of the ratio in s 615-20(2)(a). This construction works no mischief and meets the statutory objective of providing for the type of roll-over relief concerned. The construction does not involve reading words into the section. If one were to read the provision completely literally, it would produce arbitrary results for no discernible purpose whilst also failing to meet the objective evident in the terms of s 615-20 read in context. A construction that promotes the purpose of a statute is to be preferred over a literal interpretation: R v A2 [2019] HCA 35; 269 CLR 507 at [37].

68 The question whether the primary judge departed from the "Joint Statement of Agreed Facts and Issues" (JSAFI) does not arise for two reasons. First, for the reasons given by Kennett J, the "and nothing else" requirement in s 615-5(1)(c) is directed to the contractual consideration received by a shareholder in exchange for the shares, not an inquiry into whether the exchange resulted in the shareholder receiving a "boost" in value. Secondly, there was no "boost" to the value of the Ausnet shares held by shareholders because, even assuming there was a real market at the relevant point in time, each of the preordained events of 18 June 2015 would have been factored into the value of the shares in Ausnet issued under each of the schemes.

69 In any event, as Kennett J explains, the primary judge did not err in relation to the JSAFI as contended by the appellant. The JSAFI stated that it "set out the facts and issues that one or both of [the parties] considers to be relevant to the resolution" of the proceedings: at [1]. Where a fact was stated, it was often stated by reference to relevant documents in Appendix A to the JSAFI, including in [15] of the JSAFI. The JSAFI stated that both Ausnet and the Commissioner relied on those documents "for their full meaning and effect": at [2]. The JSAFI identified a single issue in a generic way at [26]:

The issue in the proceedings is whether s 615-65 of the 1997 Act applies to the Applicant in respect of its acquisition of the shares in Distribution. The sub-issues are whether the conditions in s 615-5(1) are satisfied such that the Applicant could choose that s 615-65 applies with respect to its acquisition of the shares in Distribution.

70 The documents in Appendix A established, amongst other things, that:

at the start of 18 June 2015, the shares in Transmission and Distribution and the units in Finance were "stapled" to each other and could not be separately traded;

trading in the stapled securities had been halted at the end of 5 June 2015;

nobody could buy or sell any of the stapled securities on 18 June 2015; and

shares in Ausnet had commenced trading on 9 June 2015 but only on a "deferred settlement" basis (on the ASX) or a "when issued" basis (on the SGX), with a settlement date fixed for 24 June 2015.

71 Paragraph 15 of the JSAFI stated:

15. As at the beginning of 18 June 2015:

a) Distribution, Transmission and Finance each had 3,466,913,009 shares or units (as applicable) on issue, with each security holder holding the same percentage shareholding or unitholding (as applicable) in respect of each of Finance, Distribution or Transmission, as set out in Annexure 19;

b) Finance's market value was $2.874 billion;

c) Distribution's market value was $2.025 billion; and

d) Transmission's market value was $0.525 billion.

72 Paragraph 15 reflects an agreement about the respective 'market values' of Transmission, Distribution and Finance (which presumably means the shares in Transmission and Distribution and the units in Finance), on the false assumption that the shares and units in the three entities could be separately traded. In substance, it was a statement about how the agreed total market value of the stapled securities was appropriately allocated as between the three entities within the stapled structure as at the beginning of 18 June 2015.

73 Paragraph 15 cannot sensibly be understood as an agreement that the various shares and units could be separately traded or about what occurred during the course of 18 June 2015. Nor was it an agreement about the 'market value' of the shares in Transmission and Distribution and the units in Finance (or the 'market value' of the net assets those entities) at various times over the course of 18 June 2015.

74 Further, paragraph 15 did not purport to address, and was not an agreement about, the 'market value' of the shares in Ausnet immediately before the Distribution Scheme was implemented.

75 Paragraph 15 was not an agreement reached with respect to, and did not directly engage, the various facts necessary to consider the "boost" argument as raised during the hearing.

76 I agree with Kennett J that the primary judge's approach was not inconsistent with the JSAFI and that there was no breach of procedural fairness.

I certify that the preceding eleven (11) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Thawley. |

Associate:

Dated: 7 March 2025

REASONS FOR JUDGMENT

KENNETT J:

Introduction

77 This appeal concerns one aspect of a series of transactions that took place on 18 June 2015, by which the appellant (Ausnet) was inserted into the ownership structure of three entities—AusNet Services (Transmission) Limited (Transmission), AusNet Services Finance Trust (Finance) and AusNet Services (Distribution) Limited (Distribution)—which had until then been a stapled group. The aspect which is of present concern is the scheme of arrangement by which Ausnet acquired all of the shares in Distribution (the Distribution scheme). This was the last of a pre-ordained sequence of transactions.

78 The issue that divides the parties is whether the rollover provisions in Div 615 of the Income Tax Assessment Act 1997 (Cth) (ITAA97) apply to Ausnet's acquisition of the shares in Distribution. It was the position of both parties that this resolved into two questions, namely:

(a) whether there was a scheme for reorganising the affairs of Distribution for the purposes of s 615-5(1)(c) of ITAA97; and

(b) whether the requirement in s 615-20(2) of ITAA97, that specified ratios concerning the interests of shareholders be equal, was satisfied.

79 Before the primary judge, the matter proceeded on the basis of a comprehensive agreed statement of facts (referred to as the JSAF), to which was annexed a bundle of documents. The facts are summarised in some detail in the reasons of the primary judge at [9] – [36]. They are referred to in these reasons only to the extent necessary to give shape to the questions of law that were argued in the appeal.

The statutory scheme

80 Division 615 provides for what is termed "roll-over relief" in respect of transactions by which the shareholders in a company (or the unit holders in a unit trust) transfer all their shares to a company and become the shareholders in that company. Section 615-1, which is headed "What this Division is about", provides:

You can choose for transactions under a scheme to restructure a company's or unit trust's business to be tax neutral if, under the scheme:

(a) you cease to own shares in the company or units in the trust; and

(b) in exchange, you become the owner of new shares in another company.

81 The consequences of a transaction coming within Division 615 are set out in Subdivs 615-C and 615-D. Relevantly, for the interposed entity, s 615-65(4) provides as follows.

(4) The first element of the *cost base of the interposed company's *shares or units in the original entity that are not taken to have been *acquired before 20 September 1985 is:

(a) the total of the cost bases (as at the completion time) of the original entity's assets that it acquired on or after that day; less

(b) its liabilities (if any) in respect of those assets.

The first element of the *reduced cost base of those shares or units is worked out similarly.

82 The application of s 615-5 depends on a choice being made by a taxpayer (which can be deemed to have been made in some circumstances) concerning a specific kind of transaction, and on that transaction meeting certain requirements. The choice is provided for in Subdiv 615-A. Relevantly, s 615-5 provides:

615-5 Disposing of interests in one entity for shares in a company

(1) You can choose to obtain a roll-over if:

(a) you are a *member of a company or a unit trust (the original entity); and

(b) you and at least one other entity (the exchanging members) own all the *shares or units in it; and

(c) under a *scheme for reorganising its affairs, the exchanging members *dispose of all their shares or units in it to a company (the interposed company) in exchange for shares in the interposed company (and nothing else); and

(d) the requirements in Subdivision 615-B are satisfied.

Note 1: For paragraph (c), see section 124-20 if an exchanging member uses a share sale facility.

Note 2: After the completion of the scheme, later dealings between the interposed company and the original entity may be subject to the rules for consolidated groups (see Part 3-90).

(2) You are taken to have chosen to obtain the roll-over if:

(a) immediately before the completion time (see section 615-15), the original entity is the *head company of a *consolidated group; and

(b) immediately after the completion time, the interposed company is the head company of the group.

Note: The consolidated group continues in existence because of section 703-70.

83 In these reasons I will use the terms original entity, exchanging members and interposed company in the senses established by s 615-5(1)(a), (b) and (c) respectively.

84 Section 615-10 (which is not in play here) makes similar provision in relation to transactions in which the interposed company acquires some of the shares or units in the original entity and the others are redeemed or cancelled.

85 The requirements that apply to the transaction are set out in Subdiv 615-B. One of those requirements is that the interposed company must be the owner of all of the shares in the original entity immediately after all the exchanging members have had their shares or units in that entity disposed of, redeemed or cancelled (defined as the completion time) (s 615-15).

86 The other provisions of Subdiv 615-B that are relevant here are ss 615-20 and 615-25, which provide as follows.

615-20 Requirements relating to your interests in the original entity

(1) Immediately after the completion time, each exchanging member must own:

(a) a whole number of *shares in the interposed company; and

(b) a percentage of the shares in the interposed company that were issued to all the exchanging members that is equal to the percentage of the shares or units in the original entity that were:

(i) owned by the member; and

(ii) disposed of, redeemed or cancelled under the *scheme.

(2) The following ratios must be equal:

(a) the ratio of:

(i) the *market value of each exchanging member's *shares in the interposed company; to

(ii) the market value of the shares in the interposed company issued to all the exchanging members (worked out immediately after the completion time);

(b) the ratio of:

(i) the market value of that member's shares or units in the original entity that were disposed of, redeemed or cancelled under the *scheme; to

(ii) the market value of all the shares or units in the original entity that were disposed of, redeemed or cancelled under the scheme (worked out immediately before the first disposal, redemption or cancellation).

Example 1: There are 100 shares in A Pty Ltd (the original entity), all having the same rights. B Pty Ltd (the interposed company) acquires all the shares in A by issuing each shareholder in A 10 shares in itself for each share they have in A. All shares in B have the same rights. Bill owned 15 shares in A and received 150 shares in B in exchange.

Example 2: There are 1,000 units in the A unit trust (the original entity), all having the same rights. 2 new units in A are issued to B Pty Ltd (the interposed company), and all other units in A are cancelled. Each unitholder in A is issued 10 shares in B for each 100 units they have in A. All shares in B have the same rights. Alison owned 200 units in A and received 20 shares in B in exchange.

(3) Either:

(a) you are an Australian resident at the time your *shares or units in the original entity are disposed of, redeemed or cancelled under the *scheme; or

(b) if you are a foreign resident at that time:

(i) your shares or units in the original entity were *taxable Australian property immediately before that time; and

(ii) your shares in the interposed company are taxable Australian property immediately after the completion time.

615-25 Requirements relating to the interposed company

(1) The *shares issued in the interposed company must not be *redeemable shares.

(2) Each exchanging member who is issued *shares in the interposed company must own the shares from the time they are issued until at least the completion time.

(3) Immediately after the completion time:

(a) the exchanging members must own all the *shares in the interposed company; or

(b) entities other than those members must own no more than 5 shares in the interposed company, and the *market value of those shares expressed as a percentage of the market value of all the shares in the interposed company must be such that it is reasonable to treat the exchanging members as owning all the shares.

The positions of the parties

87 Prior to 18 June 2015 the shares in Transmission, the units in Finance and the shares in Distribution were "stapled" to each other. They could not be traded separately. An arrangement was put to the security holders, and reflected in orders made by the Supreme Court of Victoria, under which the following transactions would occur sequentially on the same day.

(a) The securities were to be unstapled;

(b) the securities held by certain foreign security holders were to be transferred to a nominee (who would, at the end of the process, sell the shares in Ausnet that it came to hold and distribute the proceeds to those foreign security holders);

(c) Ausnet was to acquire all of the shares in Transmission for consideration in the form of shares in Ausnet, and at the same time cancel the two pre-existing shares in Ausnet (which were held by a subsidiary of Distribution);

(d) Ausnet was to make an election that the Transmission tax consolidation group was to continue in existence;

(e) Ausnet was to acquire all of the units in Finance for consideration in the form of shares in Ausnet;

(f) Ausnet was to acquire all of the shares in Distribution for consideration in the form of shares in Ausnet (the Distribution scheme referred to above); and

(g) by resolution of Ausnet's shareholders, all of the shares in Ausnet were to be converted to a number of shares equal to the number of stapled securities previously on issue.

88 The implementation deed, which had been approved by shareholders and was annexed to orders made by the Supreme Court of Victoria, provided for the steps to occur in this sequence and also provided that no party was obliged to perform any step unless the others occurred (or were to occur) on the implementation date. The transactions occurred in accordance with this schedule.

89 As noted earlier, the present case concerns only the Distribution scheme. It was not submitted that Division 615 was to be applied to the whole of what occurred on 18 June 2015 or to any larger subset of those transactions, even though the expression "scheme" (as defined in s 995-1 of ITAA97) could arguably extend to a group of related transactions of this kind.

90 Before the Distribution scheme took effect, Ausnet had 6,933,826,018 shares on issue. The shares in Ausnet that were issued as part of that scheme therefore did not constitute all of the Ausnet shares on issue at the completion time, although it was the case that the only shareholders in Ausnet at that time were former Distribution shareholders. This feature of the scheme led Ausnet to make three broad arguments concerning the application of Division 615.

(a) There was not a "scheme for reorganising [Distribution's] affairs" within the meaning of s 615-5(1)(c) and the primary judge erred in finding that there was (reflected in grounds 1 and 6(a) of the notice of appeal).

(b) The Distribution scheme was not one in which the exchanging shareholders received shares in the interposed company "and nothing else", within the meaning of s 615-5(1)(c), because one effect of the Distribution scheme was to increase the value of the shares in Ausnet that those shareholders held immediately before the scheme came into effect (reflected in grounds 2 and 6(a) of the notice of appeal).

(c) The ratios in s 615-20(2) were not equal, because the individual shareholder's interest at the completion time (s 615-20(2)(a)(i)) included the shares already issued to that shareholder in exchange for their Transmission shares and Finance units (reflected in grounds 3 and 6(b) of the notice of appeal). If this argument is correct, it is also said to provide a further reason why the scheme was more than a "reorganisation" of Distribution's affairs (ground 4 of the notice of appeal).

91 Underlying and informing these arguments is a conception of Division 615 as applying only when the interposed company begins the process as a "shelf company": ie, it has no value before the shares or units in the original entity are transferred to it, and no shares on issue after the reorganisation other than those issued as part of the scheme (apart from up to five shares permitted to be held by other persons under s 615-25(3)(b), which would ordinarily be the shares created upon the registration of the company). The Commissioner contends for a different understanding of the Division. In the Commissioner's thesis, Division 615 governs how the interests in the original entity are rolled over but does not concern itself—other than to the extent seen in ss 615-15 and 615-25(3)—with the nature of the interposed company.

92 It is appropriate to observe at this point that, to the extent that Ausnet's arguments approach the text of Division 615 on the basis that a scheme for reorganising ownership of an entity qualifies for roll-over relief only if the interposed company is a shelf company, they risk falling into the error identified in Certain Lloyd's Underwriters v Cross [2012] HCA 56; 248 CLR 378 at [26] (French CJ and Hayne J) (Cross). The starting point must be the text, rather than any preconceived idea as to what the legislature was aiming at. The limitation for which Ausnet contends must be found in the provisions of Division 615, read in context.

93 Ausnet also raises what is put as a procedural fairness argument (ground 5 of the notice of appeal). The point arises out of the "nothing else" argument which, as put below, relied on distinct market values which Transmission, Finance and Distribution were agreed to have had at the start of 18 June 2015 (JSAF [15]). The primary judge's rejection of this argument is said to have failed to give effect to agreed facts, in circumstances where any perceived deficiencies in those agreed facts were not raised with the parties or allowed to be remedied by valuation evidence. I will address this ground in the context of the "nothing else" argument.

The legislative history

94 In Commissioner of Taxation v Consolidated Media Holdings Ltd [2012] HCA 55; 250 CLR 503 at [39] (Consolidated Media) the High Court (French CJ, Hayne, Crennan, Bell and Gageler JJ) observed:

"This Court has stated on many occasions that the task of statutory construction must begin with a consideration of the [statutory] text". So must the task of statutory construction end. The statutory text must be considered in its context. That context includes legislative history and extrinsic materials. Understanding context has utility if, and in so far as, it assists in fixing the meaning of the statutory text. Legislative history and extrinsic materials cannot displace the meaning of the statutory text. Nor is their examination an end in itself.

(Footnotes omitted.)

95 The first sentence of this extract is a quotation from Alcan (NT) Alumina Pty Ltd v Commissioner of Territory Revenue [2009] HCA 41; 239 CLR 27 at [47] (Hayne, Heydon, Crennan and Kiefel JJ) (Alcan). In the paragraphs following this extract, their Honours canvassed aspects of the legislative history of the provisions there in issue which, as they explained, provided varying degrees of assistance in fixing the meaning of those provisions.

96 As noted earlier, the provisions whose meaning is controversial in the present case are ss 615-5(1)(c) and 615-20(2)(a). Neither is directly the subject of any authority. Because the various submissions concerning their meaning are to some extent intertwined and seek to recruit broader propositions about Division 615, it is useful to set out the key provisions of the successive legislative regimes together. I will return to some aspects of the legislative history in a little more detail in the course of resolving the constructional debates between the parties.

97 The first set of provisions for asset rollovers that needs to be noted is ss 160ZZPA to 160ZZPD of the Income Tax Assessment Act 1936 (Cth) (ITAA36). Section 160ZZPA was enacted as part of the Taxation Laws Amendment Act 1988 (Cth) and erected specific rules for capital gains tax in relation to disposals of units in unit trusts to which it applied. Those disposals were identified by s 160ZZPA(1), which provided as follows.

160ZZPA Exchange of units in a unit trust for shares in a company

(1) This section applies where:

(a) under a scheme that:

(i) is for the reorganisation of the affairs of a unit trust; and

(ii) was entered into, or commenced to be carried out, after 9 December 1987;

2 or more taxpayers (in this section called the 'exchanging taxpayers'), being the holders of all the units (in this section called the 'exchange units') in the unit trust, dispose of all the exchange units to a company (in this section called the 'interposed company'), not being a company in the capacity of a trustee of a trust estate;

(b) the consideration in respect of each of the disposals consists only of non-redeemable shares (in this section called the 'replacement shares') in the interposed company;

(c) the total number of replacement shares is equal to, or is a multiple of, the total number of exchange units;

(d) in the case of each exchanging taxpayer—all of the exchange units held by the taxpayer are disposed of at the same time (in this section called the 'exchanging taxpayer's disposal time');

(e) immediately after the time (in this section called the 'completion time') of the disposals or, if the disposals occurred at different times, the last of the disposals:

(i) the exchanging taxpayers are the owners of all the shares in the interposed company; and

(ii) the interposed company holds all the units in the unit trust;

(f) if the exchanging taxpayer's disposal time in relation to a particular exchanging taxpayer occurred before the completion time—the taxpayer was the owner of the replacement shares concerned at all times during the period commencing immediately after the exchanging taxpayer's disposal time and ending at the completion time;

(g) the unit trust is a resident unit trust in relation to the year of income of the unit trust in which the completion time occurred;

(h) the interposed company is a resident of Australia at the completion time and, if the disposals occurred at different times, at all times during the period commencing at the time of the first of the disposals and ending at the completion time;

(j) in the case of an exchanging taxpayer in the capacity of a trustee of a trust estate—immediately after the exchanging taxpayer's disposal time, the taxpayer holds the replacement shares concerned upon the same trust as the taxpayer held the exchange units that were disposed of to the interposed company;

(k) immediately after the completion time, each exchanging taxpayer owned the replacement shares in the interposed company in the same proportion as the taxpayer held the exchange units in the unit trust that were disposed of to the interposed company;

(m) in the case of each exchanging taxpayer—the ratio calculated in accordance with the formula:

where:

MV of taxpayer's shares is so much of the market value, immediately after the completion time, of the replacement shares owned by the taxpayer immediately after that time as is attributable to the exchange units held by the interposed company; and

MV of total shares is so much of the market value of all the replacement shares, immediately after the completion time, as is attributable to the exchange units held by the interposed company;

is the same as the ratio calculated in accordance with the formula:

where:

MV of taxpayer's units is the market value, immediately before the exchanging taxpayer's disposal time, of the exchange units held by the taxpayer immediately before that time; and

MV of total units is the market value of all the exchange units immediately before the exchanging taxpayer's disposal time;

(n) the interposed company has, by notice in writing given to the Commissioner within 2 months after the completion time, or within such further time as the Commissioner allows, elected that this subsection apply in respect of all the disposals; and

(p) the notice referred to in paragraph (n) is accompanied by a declaration, in a form approved by the Commissioner, with respect to the operation of this section.

98 Section 160ZZPC, which was inserted by the Taxation Laws Amendment Act 1989 (Cth), provided that s 160ZZPA was to apply to a "scheme for the reorganisation of the affairs of a company" in a corresponding way to the way it applied to a unit trust.

99 The rollover provisions were rewritten and moved into ITAA97 by the Tax Law Improvement Act (No 1) 1998 (Cth) (the 1998 Act). The resulting provisions were in Subdiv 124-G (which applied to companies) and Subdiv 124-H (which applied to unit trusts). Relevantly to a case of disposal of shares to a company in exchange for shares in that company, s 124-360 provided as follows.

124-360 Disposal of shares in one company for shares in another one

(1) You can choose to obtain a roll-over if:

(a) you are a *member of a company (the original company); and

(b) you and at least one other entity (the exchanging members) own all the *shares in it; and