Federal Court of Australia

Clarence City Council v Commonwealth of Australia [2024] FCAFC 8

ORDERS

Appellant | ||

AND: | First Respondent HOBART INTERNATIONAL AIRPORT PTY LTD (ACN 080 919 777) Second Respondent | |

and between | HOBART INTERNATIONAL AIRPORT PTY LTD (ACN 080 919 777) Cross -Appellant | |

AND: | THE COMMONWEALTH OF AUSTRALIA Cross-Respondent | |

order made by: | MARKOVIC, STEWART AND ANDERSON JJ | |

DATE OF ORDER: | 15 February 2024 | |

THE COURT ORDERS THAT:

1. The appeal and cross-appeal are dismissed.

2. The parties file submissions on costs, not exceeding 5 pages, within 14 days, and any submissions in response to those submissions within 7 days thereafter.

3. Subject to further order on the request of any party, the question of costs be dealt with on the papers.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

TAD 4 of 2023 | |

BETWEEN: | NORTHERN MIDLANDS COUNCIL Appellant |

and | THE COMMONWEALTH OF AUSTRALIA First Respondent AUSTRALIA PACIFIC AIRPORTS (LAUNCESTON) PTY LTD (ACN 081 578 903) Second Respondent |

and between | AUSTRALIA PACIFIC AIRPORTS (LAUNCESTON) PTY LTD (ACN 081 578 903) Cross -Appellant |

AND: | THE COMMONWEALTH OF AUSTRALIA Cross-Respondent |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The appeal and cross-appeal are dismissed.

2. The parties file submissions on costs, not exceeding 5 pages, within 14 days, and any submissions in response to those submissions within 7 days thereafter.

3. Subject to further order on the request of any party, the question of costs be dealt with on the papers.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

THE COURT:

Introduction

1 The appellants, the Clarence City Council and the Northern Midlands Council (collectively, the Councils), appeal from the decision of the primary judge in Clarence City Council v Commonwealth [2022] FCA 1492 (Judgment). The appeals are made in two proceedings: TAD 3/2023 (Hobart Proceeding) and TAD 4/2023 (Launceston Proceeding).

2 The territories administered by the Councils include the Hobart International Airport and Launceston Airport (Airports) respectively. The Commonwealth owns the land on which the Airports are situated. The appeals principally concern the proper construction of cl 26.2(a) of the lease agreements for the Airports. One lease was entered into between the first respondent in both proceedings (the Commonwealth) and the second respondent in the Hobart Proceeding, Hobart International Airport Pty Ltd (HIAPL). The other lease was entered into between the Commonwealth and the second respondent in the Launceston Proceeding, being Australia Pacific Airports (Launceston) Pty Ltd (APAL). In this judgment, we refer to HIAPL and APAL collectively as the Lessees. We refer to the leases with HIAPL and APAL collectively as the Leases.

3 By operation of ss 52 and 114 of the Constitution, the Councils do not have power to levy rates or charges in respect of the sites covered by the Airports, because the sites are owned by the Commonwealth. Broadly, cl 26.2(a) of the Leases requires the Lessees to make rates equivalent payments to the Councils. The dispute between the parties principally concerns which parts of the airports are rateable and the nature of any obligation on the Lessees to make rates equivalent payments.

4 Although the Councils are not parties to the Leases, they filed applications for declaratory and consequential relief with respect to the proper construction of cl 26.2(a) of the Leases. The primary judge dismissed these applications. By their Notices of Appeal, the Councils contend that the primary judge erred in doing so. The Lessees contend that the Councils have not established any error and the appeal should be dismissed. The Lessees also seek to uphold the primary judge’s decision on different grounds by way of Notices of Contention.

5 Before the primary judge, the Lessees cross-claimed for declaratory relief against the Commonwealth. Their cross-claims raised questions of accord and satisfaction, and estoppel. The primary judge held that these questions were unnecessary to decide. The primary judge nonetheless made certain findings with respect to the Lessees’ contentions concerning accord and satisfaction. The primary judge’s findings and conclusions with respect to accord and satisfaction, and estoppel, are challenged by the Lessees in their Notices of Cross-Appeal. The cross-appeal is expressly stated to arise only if the appeal succeeds.

6 The Commonwealth contends that neither the Councils nor the Lessees have demonstrated error in the reasons of the primary judge.

7 For the reasons given below, the Councils have not established any appellable error in the Judgment. The Councils’ appeal will be dismissed. The cross-appeal must also then be dismissed.

8 Having dismissed the Councils’ appeal, it is largely unnecessary to determine the matters raised in the Lessees Notices of Contention and their Notices of Cross-Appeal. The one issue that it is necessary to determine concerns an alternative construction of the nature of the obligation created by cl 26.2(a) of the Leases advanced by the Lessees in their Notices of Contention. This contention will also be rejected.

Issues on appeal

9 There are five issues raised by the notices filed by the Councils and Lessees:

(1) First, whether the primary judge erred in concluding that the term “trading or financial operations” in cl 26.2(a) of the Leases did not include certain areas of the airports on which aeronautical services and facilities are provided: Councils’ Notices of Appeal, ground 1 (Issue 1).

(2) Secondly, the nature of the obligation created by cl 26.2(a) of the Leases, which:

(a) the Lessees contend imposes no obligation to pay at all (but to use reasonable endeavours to enter into an agreement to make payments in lieu of rates): Lessees’ Notices of Contention, ground 1;

(b) the Councils contend requires the Lessees to pay a rate calculated by the Councils on the basis of valuations made by the Valuer-General of Tasmania pursuant to the Valuation of Land Act 2001 (Tas) and recorded in the Valuation List and notified to the Lessees by the Councils: Councils’ Notices of Appeal, ground 2;

(c) the Commonwealth contends imposes a substantive obligation on the Lessees to make rates equivalent payments to the Councils (as the primary judge found: Judgment [176]) (Issue 2).

(3) Thirdly, whether the primary judge erred in concluding that any cause of action under cl 26.2(a) of the Leases had not been discharged by an accord and satisfaction between the Commonwealth and each of the Lessees: HIAPL’s Notice of Contention, ground 2(h), APAL’s Notice of Contention (ground 2(h)(ii)-(iii)); HIAPL’s Notice of Cross-Appeal, grounds 1-4, APAL’s Notice of Cross-Appeal, grounds 1-3 (Issue 3).

(4) Fourthly, (in the Launceston Proceeding only) whether the primary judge erred in concluding that the Commonwealth was not precluded by estoppel from seeking to compel APAL to make further payments to the Northern Midlands Council: APAL’s Notice of Contention, ground 2(h)(i)-(ii); APAL’s Notice of Cross-Appeal, grounds 4-5 (Issue 4).

(5) Fifthly, whether relief should have been refused in the exercise of the primary judge’s discretion: Lessees’ Notices of Contention, ground 2 (Issue 5).

Background facts

The Leases

10 In 1998, the Commonwealth entered into the Leases for the Hobart International Airport with HIAPL and the Launceston Airport with APAL respectively. Each of the Leases is for a term of 50 years with a 49-year option to renew. Each of the Leases is in materially similar terms.

11 Clause 3.1(a)(i) of the Leases requires that the Lessees provide for the use of the “Airport Site” as an airport. The “Airport Site” is defined to include the whole of the land that is subject to the Leases (cl 2.1).

12 The critical clauses of the Leases which are the subject of the issues in these appeals provide as follows:

26.1 PAYMENT OF RATES AND LAND TAX AND TAXES

The Lessee must pay, on or before the due date, all Rates, Land Tax and Taxes without contribution from the Lessor.

26.2 EX GRATIA PAYMENT IN LIEU OF RATES AND LAND TAX

(a) Where Rates are not payable under sub clause 26.1 because the Airport Site is owned by the Commonwealth, the Lessee must promptly pay to the relevant Governmental Authority such amount as may be notified to the Lessee by such Governmental Authority as being equivalent to the amount which would be payable for rates as if such rates were leviable or payable in respect of those parts of the Airport Site:

(i) which are sub leased to tenants; or

(ii) on which trading or financial operations are undertaken including but not limited to retail outlets and concessions, car parks and valet car parks, golf courses and turf farms, but excluding runways, taxiways, aprons, roads, vacant land, buffer zones and grass verges, and land identified in the airport Master Plan for these purposes,

unless these areas are occupied by the Commonwealth or an authority constituted under Commonwealth law which is excluded from paying rates by Commonwealth policy or law. The Lessee must use all reasonable endeavours to enter into an agreement with the relevant Governmental Authority, body or person to make such payments.

(b) Where Land Tax is not payable under sub clause 26.1 because the Airport Site is owned by the Commonwealth, payments in lieu of Land Tax must be made by the Lessee in respect of those parts of the Airport Site:

(i) which are sub leased to tenants; or

(ii) on which trading or financial operations are undertaken including, but not limited to, retail outlets and concessions, car parks and valet car parks, golf courses and turf farms, but excluding runways, taxiways, aprons, roads, vacant land, buffer zones and grass verges, and land identified in the airport Master Plan for these purposes,

unless these areas are occupied by the Commonwealth or an authority constituted under Commonwealth law which is excluded from making payments by Commonwealth policy or law. Unless otherwise directed by the Lessor, the Lessee will make payments promptly in lieu of land tax at the relevant State rate to the Commonwealth addressed as provided for in subclause 24.1.

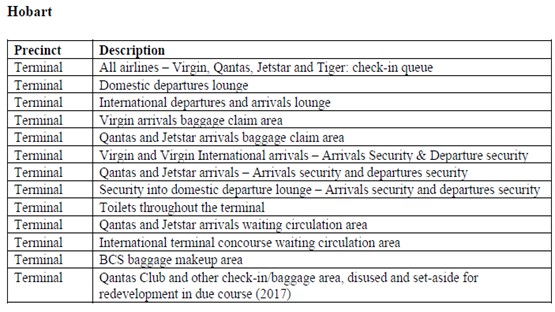

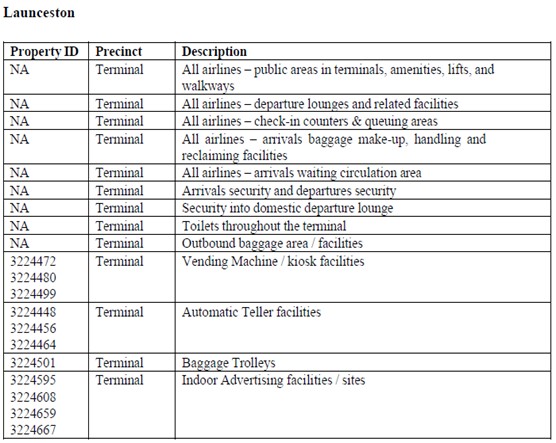

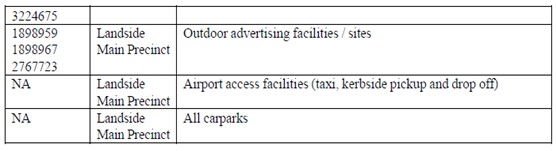

These payments in lieu of Land Tax will be levied on a financial year basis. The Lessee must submit an assessment of the payment in lieu of land tax to the Commonwealth on 31 August of the current financial year with this payment due 30 days later. Land value assessment for the purposes of making payments in lieu of land tax are required at least every three years.

(c) Where Taxes such as stamp duty, payroll tax, financial institutions duty and debits tax imposed by a Governmental Authority are not payable by the Lessee because they are Taxes on transactions, instruments or activities on or related to the Airport Site owned by the Commonwealth, the Lessee must pay to the relevant Governmental Authority such amount as is equivalent to the amount which would be payable for such Taxes if such Taxes were leviable or payable.

13 For the purposes of cll 26.1 and 26.2(a), the word “Rates” is defined to mean “all rates (including water rates and sewerage rates), and levies to defray expenses levied or imposed by a Governmental Authority on land or on owners or occupiers of land in relation to their ownership or occupation of that land”: Judgment [68].

14 The Clarence City Council and the Northern Midlands Council, established under the Local Government Act 1993 (Tas), are respectively the relevant “Governmental Authority” for the Hobart International Airport and the Launceston Airport: Judgment [69].

15 The Leases also contain a term in cl 2.2(g) that “headings in this Lease are for convenience only and are not part of, or to be used in the interpretation or construction of, this Lease”: Judgment [71].

Background to the Leases

16 The effect of cl 26.2(a) of each Lease is to require the Lessees to pay to the Councils a “fictional” or “notional” equivalent to the rates that would have been payable if the leased land was not Commonwealth land. Clause 26.2(a) applies because rates are not payable under cl 26.1. This is because the Commonwealth Parliament has exclusive legislative power, subject to the Constitution, in respect of places acquired by the Commonwealth for public purposes: s 52(i) Constitution. Absent the consent of the Commonwealth Parliament, a State may not tax Commonwealth property: s 114 Constitution. As the Airports are situated on land acquired by the Commonwealth for public purposes, that land is not subject to municipal rates and charges pursuant to the Local Government Act.

17 It is not in dispute that Commonwealth government policy required the Commonwealth to make payments equivalent to rates to local authorities in certain circumstances. The Federal Airports Corporation (FAC), which at the time operated most of the major airports in Australia as “government business enterprises”, agreed to maintain the Commonwealth government’s policy by making payments in lieu of rates for areas of federal airports which were used for commercial activities and for which the FAC received an annual rent: Judgment [14].

18 The primary judge at Judgment [15]-[61] explained in detail the background to the Commonwealth government’s policy concerning the payment of rates equivalent amounts, the privatisation of airports in Australia, the role of the FAC, and the economic regulation of airports in Australia. The parties on appeal took no issue with the primary judge’s summary of these facts and we adopt in these reasons below the primary judge’s summary. The primary judge’s summary is supplemented by reference to documents to which we were taken by the parties in their submissions on the appeal.

Competition Principles Agreement

19 On 11 April 1995, the Commonwealth and the States and Territories entered into the “Competition Principles Agreement” (CPA), which recorded the agreement of the Council of Australian Governments to adopt certain principles of competition policy and to apply competition laws across the public sector: Judgment [15]. It is not in dispute that cl 26.2(a) of the Leases was included conformably with the CPA.

20 One of the overarching purposes of the CPA was to achieve and maintain consistent and complementary competition laws and policies which would apply to all businesses in Australia, regardless of ownership. One of the principles agreed to was the principle of “competitive neutrality”: Judgment [16].

21 Clause 3 of the CPA was headed “Competitive Neutrality Policy and Principles”. It relevantly provided as follows:

(1) The objective of competitive neutrality policy is the elimination of resource allocation distortions arising out of public ownership of entities engaged in significant business activities: Government businesses should not enjoy any net competitive advantage simply as a result of their public sector ownership. These principles only apply to the business activities of publicly owned entities, not to the non-business, non-profit activities of these entities.

…

(4) Subject to subclause (6), for significant Government business enterprises which are classified as “Public Trading Enterprises” and “Public Financial Enterprises” under the Government Financial Statistics Classification:

(a) the Parties will, where appropriate, adopt a corporatisation model for these Government business enterprises … ; and

(b) the Parties will impose on the Government business enterprise:

(i) full Commonwealth, State and Territory taxes or tax equivalent systems;

…

(5) Subject to subclause (6), where an agency (other than an agency covered by subclause (4)) undertakes significant business activities as part of a broader range of functions, the Parties will, in respect of the business activities:

(a) where appropriate, implement the principles outlined in subclause (4);

…

(Judgment [17])

22 Clause 4(3) of the CPA, which was headed “Structural Reform of Public Monopolies”, provided as follows:

Before a Party introduces competition to a market traditionally supplied by a public monopoly, and before a Party privatises a public monopoly, it will undertake a review into:

(a) the appropriate commercial objectives for the public monopoly;

(b) the merits of separating any natural monopoly elements from potentially competitive elements of the public monopoly;

(c) the merits of separating potentially competitive elements of the public monopoly;

…

(Judgment [18])

23 Each of the Airports was, at that time, “a public monopoly” within the meaning of cl 4(3) of the CPA: Judgment [19].

24 The principle of competitive neutrality underlying the CPA was further articulated in the Commonwealth Competitive Neutrality Policy Statement issued in June 1996 (CNPS). It explained that competitive neutrality required that “government business activities should not enjoy net competitive advantages over their private sector competitors simply by virtue of public sector ownership” and “where governments choose to provide services through market based mechanisms that allow actual or potential competition from a private sector provider, that competition should be fair”: Judgment [20]. The CNPS further stated that the implementation of competitive neutrality arrangements was “intended to remove resource allocation distortions arising out of public ownership of significant business activities and to improve competitive processes”.

25 The CNPS noted that competitive neutrality arrangements would apply to “significant government business activities” but not to “non-profit, non-business activities.” The CNPS referred to the fact that government agencies were involved in both business activities and other non-business activities and stated that, in these circumstances, competitive neutrality would be applied to those activities which met the “business criteria”. The business criteria were set out as follows:

For the purposes of competitive neutrality in the Commonwealth sector, to be considered a “business activity” the following criteria must be met:

• there must be user-charging for goods or services (the user may be in the private sector or public sector);

• there must be an actual or potential competitor (either in the private or public sector) ie users are not restricted by law or policy from choosing alternative sources of supply; and

• managers of the activity have a degree of independence in relation to the production or supply of the good or service and the price at which it is provided.

26 An appendix to the CNPS identified Commonwealth organisations “conducting significant business activities”. The FAC was identified as one such organisation. The FAC was categorised as a “Government business enterprise”. That term was said to refer to entities that had “a principal function of selling goods and services in the market for the purpose of earning a commercial return”.

27 The CNPS went on to state that organisations engaging in significant business activities would have the principal elements of competitive neutrality applied to them. The competitive neutrality arrangements that would apply to such businesses included taxation neutrality, to be achieved by removing exemptions or establishing taxation equivalent regimes.

The Role of the FAC

28 As a Commonwealth organisation identified as conducting “significant business activities”, the FAC was required to make ex gratia payments in lieu of rates in the interests of competitive neutrality: Judgment [21]. The FAC Policy Manual dated 10 November 1995 explained:

… in a letter addressed to the [FAC] in 1987, the then Minister for Transport and Communications indicated that it was a long standing Government policy that the Commonwealth make payments equivalent to rates to local authorities in certain circumstances. The Minister went on to say that it had always been the Government’s intention that this policy would continue to apply in relation to Federal Airports, and sought assurance that the [FAC] would continue to make such payments.

The [FAC] subsequently agreed to the continuation of making payments in lieu of rates for areas on airport which were used for commercial activities and for which the [FAC] received an annual rent: Judgment [21].

29 The FAC was established by the Federal Airports Corporation Act 1986 (Cth). Section 6 of that Act provided that the FAC’s functions included:

(a) to operate Federal airports, and participate in the operation of jointly used areas, in Australia;

(aa) to establish airports at Federal airport development sites;

(b) to provide the Commonwealth, governments, local government bodies, and other persons, who operate, or propose to operate, airports or facilities relating to airports (including airports and facilities outside Australia) with consultancy and management services relating to the development and operation of those airports or facilities;

(ba) to assist the Commonwealth and other persons in connection with any or all of the following:

(i) the implementation of the Airports (Transitional) Act 1996;

(ii) preparatory work associated with the implementation of the Airports Act 1996;

(iii) matters relating to the leasing, or proposed leasing, of an airport (within the meaning of the Airports (Transitional) Act 1996) that was or is a Federal airport or a Federal airport development site, including matters relating to the transfer, or proposed transfer, of responsibility for such an airport to an airport-lessee company (within the meaning of the Airports (Transitional) Act 1996);

(c) other functions that:

(i) relate to airports or Federal airport development sites;

…

(Judgment [22])

30 Section 7(2)(a) of the FAC Act provided that the FAC “shall endeavour to perform its functions in a manner that … is in accordance with the policies of the Commonwealth Government”: Judgment [23].

31 Section 8 was entitled “Extent of functions of Corporation” and provided that the functions of the FAC, among other things, extended to “carrying on commercial activities at, or in relation to, Federal airports (including carrying on such activities in co-operation, or as joint ventures, with other persons)”: Judgment [24].

The privatisation of Australian airports

32 During the late 1990s and early 2000s, the Commonwealth entered into a number of long-term leases with airport operators as part of a project to privatise Australia’s federal airports: Judgment [28].

33 Legislation to facilitate the privatisation project was enacted: Judgment [29].

34 The Airports Act 1996 (Cth) established the regulatory arrangements to apply to the airports then owned and operated on behalf of the Commonwealth by the FAC following the leasing of those airports. Certain provisions of the Airports Act applied to “core regulated airports”, which was defined in s 7 to include, among others, the Airports: Judgment [30].

35 Section 3 of the Airports Act recorded the objects of the Act. Amongst other things, that section described the objects of the Act as “to ensure diversity of ownership and control of certain major airports”: s 3(g).

36 Section 31 of the Airports Act imposed a statutory obligation to use each Airport Site as an airport. Section 32(1) of the Airports Act provided that an airport-operator company for an airport must not “carry on substantial trading or financial activities” other than, amongst other things, “activities relating to the operation and/or development of the airport” or “activities incidental to the operation and/or development of the airport”.

37 The Airports (Transitional) Act 1996 (Cth) established a framework to give effect to the Government’s decision to lease all the federal airports effectively as ongoing businesses with staff and management in place: Judgment [31].

38 The simplified outline set out in s 3 of the Transitional Act provided:

• This Act provides for the leasing of certain airports.

• Airport land and other airport assets will be transferred from the [FAC] to the Commonwealth.

• The Commonwealth will grant an airport lease to a company. The company is called an airport-lessee company.

• Immediately after the grant of the airport lease, the Commonwealth may transfer or lease certain assets to the airport-lessee company.

• Certain employees, assets, contracts and liabilities of the FAC will be transferred to the airport-lessee company: Judgment [32].

39 The grant of the Leases was a step in the privatisation project, which involved two “phases”. The second phase occurred in 1998: Judgment [32].

40 In November 1997, as part of the privatisation project, the Commonwealth published an information memorandum in relation to each of the Airports, entitled “Hobart Airport: Phase 2 Federal Airports” and “Launceston Airport: Phase 2 Federal Airports” (IMs). Both IMs were made available to potential bidders: Judgment [34].

41 The IMs were in materially similar terms: Judgment [35].

42 The primary judge at Judgment [36]-[42] referred to the following parts of the IMs, by reference to the IM issued for the Launceston Airport.

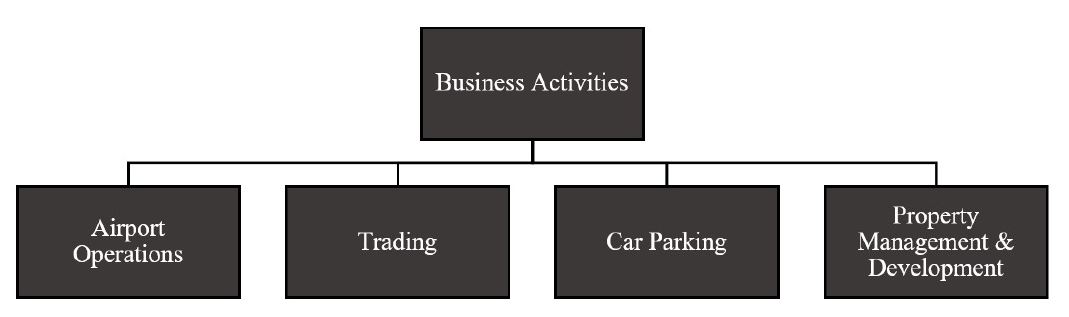

(1) The IMs provided, among many other things, that the “principal businesses” of the Launceston Airport were “airport operations”, “trading”, “car parking”, and “property management and development”. The IMs also described the “commercial potential” of the latter three items.

(2) Section 2.4 was headed “Core Business Activities”, and provided relevantly as follows:

Many of the facilities and businesses located at Launceston airport are operated by third parties such as airlines, government agencies and airport tenants. The principal business activities that are undertaken by Launceston airport are summarised in Figure 2.3.

Figure 2.3: Business Activities

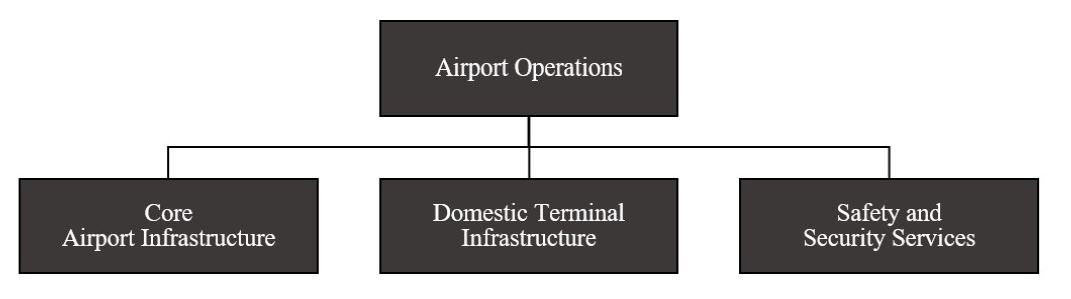

(3) Section 4 was headed “Airport Operations”, and provided relevantly as follows:

4.1 Introduction

LA provides and maintains some core airport, utility and ground access infrastructure at Launceston airport, and arranges various safety and security services at the airport. Operational activities undertaken by LA can be summarised under three broad headings, as illustrated in Figure 4.1.

Figure 4.1: Airport Operations

(4) Section 4.4 was headed “Airport Charges”, and set out, among other things, the “aeronautical charges applying at LA”.

(5) Section 5 was headed “Trading” and said that a “range of trading activities are undertaken at Launceston airport”, including retail in the domestic terminal leased by Qantas and Ansett, car rental, ground transportation, and other miscellaneous trading activities.

(6) Section 6 was headed “Car Parking” and described the car park facilities at Launceston Airport as “Domestic Terminal Public Car Park” and “Other Parking”.

(7) Section 7 was headed “Property Management and Development” and said that the “properties from which LA currently receives revenue fall broadly into three categories” of domestic terminal leases, aviation leases and licences, and non-aviation leases and licences.

43 At the same time, the Commonwealth also issued a document entitled “Phase 2 Federal Airports – General Information Memorandum” (GIM). That document explained that the “Phase 2 airports sale” comprised “the sale of 10 Regular Public Transport airports”, including the Airports. The memorandum explained to potential bidders that each of those airports was a “core regulated airport” which meant that they were governed by the provisions of the Airports Act, which established a regulatory framework for the major federal airports: Judgment [43].

44 The primary judge at Judgment [44]-[48] referred to the following parts of the GIM.

(1) Section 1.3.4 of the GIM was headed “Comprehensive Regulatory Framework for Core Regulated Airports” and relevantly provided as follows:

The non-economic regulatory framework for core regulated airports is designed to protect the public interest without detracting from the commercial attractiveness of the businesses to be sold. In particular:

• the Airports Act reflects extensive consultation with airport users, investors and other stakeholders;

• the establishment of a modern and comprehensive legal framework reduces uncertainty over the obligations placed on the operators of core regulated airports; and

• the airports legislation is designed to substantially reduce Government involvement in airport administration and to encourage airport operators to adopt an approach towards the Commonwealth and the general public that is informative, transparent and interactive.

In relation to the economic regulation of the airports, the stated Government policy is:

• to step back from setting prices and provide a framework in which, over time, airport operators and their customers resolve pricing issues contractually, rather than seek to involve the Government of the day;

• to encourage commercially driven decisions on maintaining existing airport infrastructure and on undertaking new infrastructure developments; and

• to promote the operation of the airports in as efficient and commercial a manner as possible.

The Government has established a framework for economic regulation to apply to core regulated airports. It is overseen by the Australian Competition and Consumer Commission (ACCC).

Key features of the framework are:

• an initial 5 year period during which aeronautical charges (based on the current definition in the FAC Act) will be subject to a CPI-X price cap;

• flexibility for increases in aeronautical charges to accommodate necessary new investment in the provision of aeronautical services, subject to support from principal users and the ACCC;

• a review during the fifth year which will lead to a Government decision on the future approach to economic regulation. Subject to adherence to the price caps in the first five years, the presumption is that the price caps will not continue;

• monitoring quality of service against performance indicators, although service standards will not be mandated; and

• an emphasis on transparency whereby the Airports Act imposes various reporting and accounting requirements on the airport lessee company (and any airport management company) in order to keep track of trends in airport performance.

(2) Section 9 of the GIM was headed “Economic Regulation”. Section 9.1 was headed “FAC Charging Structure” and provided:

Since commencing operations in 1988, and in line with Government policy, the FAC has applied a network approach to aeronautical charges. Consequently, the same aeronautical charges have applied to each of the FAC’s major international gateway airports (except for Sydney airport, which also imposes “peak and shoulder” period charges). In June 1996, the FAC began a process of industry consultation with a view to moving to a system of location and service specific aeronautical charging at the Federal airports and a new aeronautical charging structure came into effect on January 1997.

(3) Section 9.2 was headed “New Pricing Arrangements for Core Regulated Airports” and provided:

The Government intends applying the same pricing policy to Phase 2 core regulated airports as it did to Phase 1 airports. The principal Government objectives for the proposed pricing arrangements at the core regulated airports are to:

• achieve an appropriate balance between public interest and private commercial objectives;

• promote the operation of the airports in as efficient and commercial a manner as possible;

• encourage commercially driven decisions in relation to maintaining existing, and building new, airport infrastructure; and

• protect airport users from abuse of market power by airport operators.

These policy objectives will be met using the same approach to prices oversight of Consumer Price Index CPI-X caps, with different values of X for the different airports and administration of the price cap by the ACCC.

(4) Section 9.3 was headed “Role of the ACCC” and provided:

The need to provide some protection to users is reflected in current arrangements where aeronautical charges levied by the FAC are subject to price surveillance by the ACCC. The ACCC will continue to have an active role in preventing abuse of market power. The Government proposes that the ACCC will have various roles in pricing oversight for core regulated airports. These include:

• administering a price cap for aeronautical charges (including the assessment of any airport operator proposals for aeronautical charging increases outside the price cap);

• monitoring and evaluating quality of service against performance indicators;

• collecting and publishing information on airports, as a further measure to assist public scrutiny and the comparison of airport performance; and

• undertaking a review of pricing oversight arrangements as a basis for recommending to the Government the arrangements to operate after the first five years of the price cap.

45 Another document that was available to any bidder as part of the data room documents was entitled “A revised history of aeronautical charges”. It explained that before the creation of the FAC in 1986, airports, along with air navigation services, were operated by the Commonwealth Department of Transport, and that since 1961, the Commonwealth had “had a formal policy of recovering the costs of providing aviation infrastructure and services from the aviation industry”. That policy was apparently unsuccessful, because between 1961 and the creation of the FAC, the Commonwealth had provided a total subsidy to the aviation industry for the supply of airport, airway and associated services in excess of $2 billion. The document went on to explain:

In October 1983 the Government commissioned an independent inquiry into aviation cost recovery, under the chairmanship of Mr Henry Bosch. The Bosch Report was released in November 1984. In the overview to this report the Inquiry Committee commented “the Committee has concluded that there is virtually no possibility of achieving 100% cost recovery under the present arrangements. If these arrangements are allowed to continue the heavy burdens on the general taxpayer will not be eased.”

As a result of this inquiry the Commonwealth Government transferred the ownership of the major city international airports, their supporting general aviation airports, the major joint civil/defence airports of Darwin, Townsville and Canberra and several other major regional airports such as Launceston and Coolangatta to the FAC from 1 January 1988, with some of the smaller airports transferring on 1 April 1989: Judgment [49].

46 The document also recorded that the FAC had established a schedule of services and facilities for which aeronautical charges could be levied under s 56 of the FAC Act. Those services and facilities were defined in “Attachment C” to the document under two Headings, “Aircraft Movement Areas” and “Passenger Processing Areas”, as follows:

Aircraft Movement Areas

• grounds, runways;

• taxiways, aprons;

• airside safety;

• airfield lighting;

• airside roads/lighting;

• aircraft parking areas;

• nose-in guidance; and

• visual navigation aids.

Passenger Processing Areas

• forward airline support service areas;

• aerobridges;

• buses - airside;

• departure lounges;

• holdings lounges;

• immigration service areas;

• customs service areas;

• public address systems;

• closed circuit surveillance systems;

• lifts/escalators/moving walkways;

• public amenities;

• baggage makeup/handling/reclaim;

• public areas in terminals;

• landside road and lighting;

• security systems;

• covered walkways; and

• flight information display systems.

(Judgment [50])

Economic regulation of the Airports

47 The Commonwealth has at all material times since at least 1998 continued to regulate the price and quality of services and facilities for which aeronautical charges could be levied in the following main ways: Judgment [52].

48 A price cap applied to all charges for aeronautical services as defined by s 56 of the FAC Act, including passenger processing areas, such as departure lounges, baggage handling areas and public areas in terminals. The price cap was administered by the ACCC under the Prices Surveillance Act 1983 (Cth): Judgment [53].

49 On 22 May 1998, shortly prior to the date of the Leases, the Treasurer made Declaration 84 and Directions 13 and 14 respectively under ss 21, 20, and 27A of the Prices Surveillance Act: Judgment [54].

50 Direction 14 directed the ACCC to undertake formal monitoring of “aeronautical related services” at the Airports pursuant to s 27A of the Prices Surveillance Act. That required the ACCC to monitor prices, costs and profits relating to the supply of such services and to report to the Treasurer. The definition of “aeronautical related services” was:

[T]he provision, by an airport operator company, of any of the following

(a) aircraft refueling;

(b) aircraft maintenance sites and buildings;

(c) freight equipment storage sites;

(d) freight facility sites and buildings;

(e) ground support equipment sites;

(f) check-in counters and related facilities; or

(g) car parks (including public and staff parking but not valet parking).

(Judgment [55])

51 Declaration 84 declared as “notified services” the provision of aeronautical services at the Airports, limited to “aircraft movement facilities and activities” and “passenger processing facilities and activities” (as defined in the Declaration), but not including specified services (which corresponded to those defined in Direction 14 as aeronautical related services). This had the effect that such services could not generally be supplied above certain prices: Judgment [56].

52 Direction 13 directed the ACCC, in exercising its powers in relation to the pricing of aeronautical services at the Airports, to give special consideration to specified matters, including the implementation of pricing oversight and the imposition of a price cap on all charges for the declared aeronautical services: Judgment [57].

53 The GIM outlined the operation of the price cap. It stated that it was anticipated that “these arrangements should provide a sustained period of aeronautical price stability for the aviation industry in the transition to the new airport operating environment”. The GIM further stated:

The first five years of the scheme (from the commencement of the airport lease) are viewed as a period of transition to allow stakeholders to adjust to the new operating environment for airports. Towards the end of the first five years, a review by the ACCC is planned in relation to the pricing oversight arrangements for core regulated airports.

It is intended that the review will be based on the premise that the price cap applied to aeronautical charges during the first five years will no longer operate. The review will aim to develop arrangements targeted at those charges where the airport operator has most potential to abuse market power. The existing set of aeronautical charges will be examined, on an airport by airport basis, with the review assessing whether services should be added or removed from surveillance.

A key objective of the review will be to ensure the aviation industry retains appropriate protections. The guidelines also make it clear the ACCC can recommend stronger forms of pricing oversight if operators have a consistent track record of abusing their market power.

54 Section 141 of the Airports Act also required an airport-operator company to prepare certain accounts and statements, which were required to be provided to the ACCC under s 143. Immediately prior to the date of the Leases, reg 7.03(1)(b) of the Airports Regulations 1997 (Cth), which commenced on 12 February 1997, provided, for the purposes of s 141(2) of the Airports Act, that an airport-lessee company (which fell within the definition of airport-operator company under s 5) for a core regulated airport had to prepare:

[C]onsolidated financial statements for the operations, in relation to the airport, of itself and all airport-management companies at the airport, showing financial details in relation to the provision of aeronautical services and non-aeronautical services separately: Judgment [58].

55 Regulation 7.03(4) defined “aeronautical services” as follows:

“aeronautical services” means services and facilities in relation to:

(a) aircraft landings, take-offs and parking, including the provision of:

(i) runways, taxiways, parking aprons and associated lighting; and

(ii) airside roads and grounds, and associated lighting; and

(iii) maintenance and repair services in relation to runways, taxiways, and parking aprons; and

(iv) rescue, fire-fighting and safety services; and

(v) environmental-hazard-control services; and

(vi) services and facilities to ensure compliance with environmental laws; and

(vii) airfield navigation services, including nose-in guidance and visual navigation aids; and

(b) the embarkation or disembarkation and temporary accommodation of passengers, including the provision to passengers of:

(i) toilets, seating, thoroughfares, transfer systems and aerobridges; and

(ii) departure lounges and holding lounges; and

(iii) flight-information and public-address systems; and

(iv) facilities to permit the operation of terminal security services; and

(c) the administrative processing of passengers, including the provision to passengers of:

(i) facilities to enable the operation of customs, immigration and quarantine services; and

(ii) passenger check-in facilities; and

(iii) landside terminal access roads, lighting and covered walkways; and

(iv) baggage handling services; and

(v) facilities to enable the operation of baggage security services.

(Judgment [59])

56 The Airports Act also provided for an access regime. Section 192 (now repealed) required the Minister under the Act to make a determination in respect of each core regulated airport as soon as practicable after the 12-month anniversary of its privatisation. If such a determination was in force, each “airport service” in relation to the airport would be a “declared service” for the purposes of Part IIIA of the Trade Practices Act 1974 (Cth), now the Competition and Consumer Act 2010 (Cth). Part IIIA is headed “Access to Services”. As the Australian Competition Tribunal explained in Re Australian Union of Students (1997) 147 ALR 458 at 462, Part IIIA is “designed to establish a regime to facilitate third party access to services of certain essential facilities of national significance”, and:

Part IIIA is based on the notion that competition, efficiency and public interest are increased by overriding the exclusive rights of the owners of “monopoly” facilities to determine the terms and conditions on which they will supply their services. In Pt IIIA the focus is upon facilities of national significance that it would be uneconomic to duplicate or replicate and that supply a service, access to which would promote competition in another market: Judgment [60].

57 Section 155(1) of the Airports Act also provided that “the ACCC has the function of monitoring and evaluating the quality of airport services and facilities against” (a) performance indicators prescribed under s 153, and (b) such other criteria as the ACCC determined in writing. Examples of performance indicators were given in s 154 and included “indicators relating to the standard of runways, taxiways and apron facilities”: Judgment [61].

Genesis of dispute

58 At the date of entry into the Leases in 1998, the terminals at the Airports were the subject of Domestic Terminal Leases (DTLs). The DTLs leased parts of the terminal to the tenants and conferred on them rights to use terminal infrastructure and common areas, services and facilities. In addition to rent, those tenants were required to pay rates equivalent amounts to the Councils. The terminal precinct at Hobart International Airport has operated as a common-user facility since 2011. The Launceston Airport terminal has operated common-user facilities since 2001. The common user areas of the terminals are no longer the subject of DTLs.

59 After the date of entry into the Leases, the Councils would, from time to time, notify the Lessees of rates equivalent amounts based on valuations conducted by the Valuer-General, and the Lessees would pay those amounts to the Councils. The common user areas of the terminals were included in those valuations and used as a basis for the rates equivalent amounts notified to and paid by the Lessees.

60 Following valuations performed by the Valuer-General in 2013, a dispute arose as to the rates equivalent amounts notified to the Lessees by the Councils for the financial year 2013/14. Those valuations resulted in an increase in the valuations used as the basis for the calculation of rates equivalent amounts by the Councils. Following the Councils’ notification of the rates equivalent amounts for the financial year 2013/14, the Lessees and the Commonwealth took issue with two aspects of the valuation and notification process. First, the Lessees and the Commonwealth disputed the imposition of rates equivalent amounts in respect of each of the areas of the Airport Sites that were not subleased, principally, the terminal precincts, from which the Lessees provided common user facilities and services for a fee. Secondly, the Lessees and the Commonwealth contested the process by which rates equivalent amounts were calculated – that is, based on valuations performed by the Valuer-General pursuant to a statutory regime.

61 The dispute between the Lessees and the Commonwealth on the one hand, and the Councils on the other, in relation to those areas of the terminal precinct that are “rateable” and the process by which rates equivalent amounts are calculated, gives rise to the five issues raised in these appeals which are set out at [9] above.

Issue 1 - The meaning of “trading or financial operations”

Dispute before the primary judge

62 Before the primary judge, the Councils contended that the areas of the Airport Sites specified in Attachment A to the Councils’ amended statements of claim in each proceeding were areas which were required to be, but were not, included in the calculation of the ex gratia rates equivalent payments, because they comprised parts of the “Airport Site” at each of the Airports “on which trading or financial operations are undertaken”: cl 26.2(a)(ii). Those areas were set out by the primary judge at Judgment [163] as follows:

63 We will refer to the areas identified in the tables above as the Disputed Areas.

64 Before the primary judge, the dispute focused on whether “trading … operations” within the meaning of cl 26.2(a)(ii) were undertaken at the Airport Sites: Judgment [214]. The Councils contended before the primary judge that each of the Disputed Areas were areas on which “trading … operations” were undertaken within the meaning of cl 26.2(a)(ii) of the Leases. The Lessees and the Commonwealth contended that the phrase “trading … operations” in cl 26.2(a)(ii) did not capture those areas of the Airports on which aeronautical services and facilities were provided and, consequently, the Disputed Areas did not fall within the scope of cl 26.2(a)(ii).

65 The primary judge agreed with the Lessees and the Commonwealth’s submissions, concluding that the text, purpose and context of cl 26 made it clear that “trading … operations” were objectively intended to refer to “trading operations which do not involve the provision of aeronautical services and facilities”. The primary judge held that the phrase “trading … operations” in cl 26.2(a)(ii) referred to those which were “contestable”: Judgment [223]. Four aspects of the primary judge’s reasons are relevant on the appeal.

66 First, the primary judge held that the word “trading” in cl 26.2(a)(ii) should be limited to matters ejusdem generis to the examples of “trading or financial operations” specifically enumerated in cl 26.2(a)(ii). The primary judge held that the examples of retail outlets and concessions, car parks and valet car parks, golf courses and turf farms related to activities that were “contestable” in the relevant market and that the term “trading” should be limited accordingly. The primary judge also held that the term “trading” should be construed in light of the exclusions to the phrase “trading or financial operations” in cl 26.2(a)(ii). The primary judge referred to a selection of those exclusions, being runways, taxiways and aprons. His Honour observed that each of these exclusions referred to areas used for, or to facilitate, the provision of relevant aeronautical services and facilities for regular passenger transport, and the provision of such services and facilities were “non-contestable”: Judgment [220].

67 Secondly, the primary judge drew on the principles of competitive neutrality to support the conclusion that the phrase “trading … operations” did not include the provision of aeronautical services. Before the primary judge, the parties agreed that the purpose of cl 26.2 was to achieve competitive neutrality. The primary judge accepted that for competitive neutrality to apply, there must be an off-airport competitor for the services supplied on the Airport Sites. The primary judge reasoned that the Lessees could not enjoy any competitive advantage in respect of the provision of relevant aeronautical services and facilities at the Airports, because those services and facilities were not relevantly provided elsewhere. The primary judge therefore concluded that there was no relevant market or competitor for the aeronautical services and facilities provided at the Airport Sites and, in turn, concluded that these services and facilities were not “contestable”. In these circumstances, the primary judge accepted that competitive neutrality had no relevance or application to the provision of aeronautical services at the Airport Sites: Judgment [222]-[224].

68 Thirdly, the primary judge referred to the existence of a separate regulatory regime in respect of aeronautical services and held that this regime meant that the rationale of competitive neutrality had no bearing on or relevance to such services: Judgment [225]-[228].

69 Fourthly, citing as an example the IMs summarised at [42] above, the primary judge held that the documents provided to bidders before the Leases were entered into drew a clear distinction between trading activities and aeronautical operations: Judgment [229].

The Councils’ submissions

70 The Councils submit that the phrase “trading … operations” is not ambiguous. They contend that it is well-established that the terms “trade” and “trading” are not limited to the buying and selling of goods or services but encompasses other activities of a commercial or income-producing nature: Ku Ring Gai Co Operative Building Society (No 12) Ltd (1979) 22 ALR 621 at 624-5 (Bowen CJ), 641-2 (Deane J); Hughes v Western Australian Cricket Association Inc (1986) 19 FCR 10 at 20 (Toohey J); Bank of New South Wales v Commonwealth [1948] HCA 7; 76 CLR 1 at 381 (Dixon J); R v Judges of the Federal Court of Australia; Ex-parte Western Australian National Football League Inc [1979] HCA 6; 143 CLR 190 at 209, 210-11 (Barwick CJ), 281 (Stephen J), 325 (Mason J); Concrete Constructions (NSW) Pty Ltd v Nelson [1990] HCA 17; 169 CLR 594 at 603 (Mason CJ, Deane, Dawson and Gaudron JJ); R v Trade Practices Tribunal; ex parte St George County Council [1974] HCA 7; 130 CLR 533 at 569 (Stephen J).

71 The Councils submit that trading or financial operations are undertaken on the common user areas of the terminal precincts in the Disputed Areas at the Airports. On the Councils’ submissions, the transport of passengers and freight for reward by airlines is a well-recognised trading activity, and the common user areas support the commercial operation of the Airports. The Councils further note that the Leases impose fees and charges for the common user facilities and services, and the generation of revenue flowing to the Lessees for provision of the common user facilities and services is a component of their commercial business operations.

72 The Councils submit that the primary judge erred in construing the expression “trading … operations” in cl 26.2(a) more narrowly, so as to exclude aeronautical services and facilities of the kind provided as part of the common user services and facilities. The Councils submit that the primary judge erred in three respects.

73 First, the Councils submit that the primary judge erred in the misapplication of the ejusdem generis maxim. The Councils submit that the primary judge’s approach conflicts with authorities describing the application of the principle to general expressions following particular or specific words, and its limited application to circumstances where the general words precede the list of examples. In the latter case, the Councils submit that the particular words may only be considered examples of the former: Ambatielos v Anton Jurgens Margarine Works [1922] 2 KB 185 at 194 (Lord Sterndale MR); Ambatielos v Anton Jurgens Margarine Works [1923] AC 175 at 182-3 (Viscount Cave LC); Cody v JH Nelson Pty Ltd [1947] HCA 17; 74 CLR 629 at 639 (Starke J), 647 (Dixon J).

74 The Councils emphasise that cl 26.2(a)(ii) expressly states that the list of examples of activities constituting “trading or financial operations” are not exhaustive. The Councils submit that the primary judge’s construction has the effect of making the enumerated examples limiting rather than explanatory words in circumstances where the examples are expressed not to have that effect. By contrast, the Councils submit that the express exclusions to “trading or financial operations” in cl 26.2(a)(ii) were given a more expansive operation in the absence of textual support for that approach.

75 As noted at [65] above, the primary judge identified the genus of the examples of the activities constituting “trading or financial operations” as being activities that are “contestable” in the relevant market. The Councils submit this places a strained gloss on the ordinary meaning of the examples. In the Councils’ submission, it is not clear why the genus could not be described as, for example, activities from which revenue is derived or which support the generation of revenue. Approached in that way, the Councils submit that the common user facilities and services would comfortably fit within the genus.

76 Secondly, the Councils submit the primary judge erred in using the principle of “competitive neutrality” in a manner that distorted the proper construction of cl 26.2. The Councils submit that the primary judge’s application of the principle of “competitive neutrality” was not supported by the principles expressed in the Competition Principles Agreement (CPA) and the Commonwealth Competitive Neutrality Policy Statement (CNPS). The Councils rely on the following aspects of those documents:

(1) Neither of those documents expressly describes how the principles are to be applied in the context of the privatisation and cessation of public sector ownership of significant government businesses. The Councils submit that their relevance to the proper construction of cl 26.2(a) is therefore to be doubted.

(2) The FAC, which was a government business enterprise, was specifically identified in the CNPS as engaging in significant business activities for which competitive neutrality arrangements were explicitly required, recognising their “principal function of selling goods and services in the market for the purpose of earning a commercial return”.

(3) The competitive neutrality arrangements that applied to government business enterprises included taxation neutrality, to be achieved by removing exemptions or establishing taxation equivalent regimes (TER). Such arrangements were identified in the implementation strategy to apply to the FAC.

77 Further, the Councils submit that the existence of a regulatory regime, particularly one that does not fix prices and provides a degree of independence to the Lessees in relation to the supply of services and the price at which they are provided, is not inconsistent with the application of competitive neutrality principles. The Councils emphasise that any pricing oversight was only ever intended to be short-term and to operate as a “voluntary restraint”.

78 The Councils accept that cl 26.2(a) was included conformably with the CPA. However, the Councils submit that the purpose and the implementation of competitive neutrality align with their construction. In the Councils’ submission, the Airports are in the business of, inter alia, the provision of aeronautical services, which are revenue generating and profit-making activities. Consistently with the principle of competitive neutrality as articulated in cl 3(1) of the CPA (extracted at [21] above), the Councils submit that the Lessees should not enjoy an advantage, flowing from the status of the land on which the Airports are situated, which has the effect of distorting the prices charged for the supply of such services. That is the extent to which, the Councils submit, the commercial purpose of the transaction, its aim or object may be taken into account.

79 The Councils submit the extrinsic material relied upon by the primary judge and the parties to the Leases may not be used to demonstrate that cl 26.2(a) in each of the Leases is ambiguous. The Councils submit that the primary judge was wrong to seize on the so-called distinction between trading activities and aeronautical operations in the information memoranda (provided to the Lessees) as justifying a conclusion that the latter are not trading operations. The Councils submit that this approach by the primary judge ignores the language of s 32 of the Airports Act and strains the ordinary meaning of the words in s 32 that airport-operators must not carry on substantial trading or financial activities other than activities relating to the operation and/or development of the airport.

80 The Councils submit that the construction advanced by the parties to the Leases gives rise to numerous difficulties in the context of the common-user facilities in the terminal precincts of the Airports, such as, for example, difficulties in drawing the boundary between a retail outlet or café and the common user areas.

81 The Councils submit that the third error made by the primary judge was to find that the Disputed Areas of the Airports applied to aeronautical services and facilities which do not have an off-airport competitor. The Councils submit that the Disputed Areas of the Airports are “contestable”. The Councils contend that an object of the privatisation of the Airports was to introduce diversity of ownership and control, to free up the aviation market and create a more efficient and commercial business environment. The Councils submit that the Lessees are in competition with other airports to attract airlines and passengers. The Councils refer to the aeronautical service agreements between the Lessees and the airlines which include incentive schemes to encourage the development of new routes utilising the Airport Sites. The Councils submit that other modes of transport, such as the Bass Strait Ferry also provide competition. For these reasons, the Lessees are, in the Councils’ submission, in competition with each other within the Tasmanian market.

Consideration

82 The Councils accept that the Leases presuppose that the use of the entirety of the “Airport Site” at each of the Airports – that is, all of the land the subject of the Leases – would not amount to a “trading or financial operation”. It follows that the relevant inquiry concerns the identification of those parts of the Airport Site on which “trading or financial operations” (as that expression is used in cl 26.2(a)(ii) of the Leases) are undertaken. More specifically, the question is whether “trading or financial operations” are undertaken on the Disputed Areas, which include, by way of example, the departure lounges, baggage claim areas, toilets throughout the terminal, waiting areas and security areas of the respective airports.

Ambiguity of “trading or financial operations”

83 The proper approach to the construction of commercial contracts, including with respect to the use of extrinsic materials in construing contracts, was set out at some length by French CJ, Nettle and Goron JJ in Mount Bruce Mining Pty Ltd v Wright Prospecting Pty Ltd [2015] HCA 37; 256 CLR 104 at [46]-[49] (French CJ, Nettle and Gordon JJ). In that case, their Honours stated:

The rights and liabilities of parties under a provision of a contract are determined objectively, by reference to its text, context (the entire text of the contract as well as any contract, document or statutory provision referred to in the text of the contract) and purpose.

In determining the meaning of the terms of a commercial contract, it is necessary to ask what a reasonable businessperson would have understood those terms to mean. That inquiry will require consideration of the language used by the parties in the contract, the circumstances addressed by the contract and the commercial purpose or objects to be secured by the contract.

Ordinarily, this process of construction is possible by reference to the contract alone. Indeed, if an expression in a contract is unambiguous or susceptible of only one meaning, evidence of surrounding circumstances (events, circumstances and things external to the contract) cannot be adduced to contradict its plain meaning.

However, sometimes, recourse to events, circumstances and things external to the contract is necessary. It may be necessary in identifying the commercial purpose or objects of the contract where that task is facilitated by an understanding “of the genesis of the transaction, the background, the context [and] the market in which the parties are operating”. It may be necessary in determining the proper construction where there is a constructional choice. (citations omitted)

84 We reject the Councils’ contention that cl 26.2(a) is not ambiguous and that recourse may not be had to evidence of surrounding circumstances when construing that provision for the following reasons.

85 First, the authorities considering the meaning of the operation of “trade” or “trading” support the view that the meaning of that term will vary depending on context. Thus, in Ku Ring Gai at 624-5, a case on which the Councils rely, Bowen CJ quoted Lord Reid in in Ransom v Higgs (1974) 1 WLR 1594 at 1600 in support of the proposition that “[a]s an ordinary word in the English language ‘trade’ has or has had a variety of meanings or shades of meaning”. Lord Reid went on to state that the term “is sometimes used to denote any mercantile operation but is commonly used to denote operations of a commercial character by which the trader provides to customers for reward some kind of goods or services” (emphasis added). In Bank of New South Wales at 381, another case on which the Councils rely, Dixon J acknowledged that the “specialized meaning” of “trade” was the “selling of goods”, but the present primary meaning was wider and that its history emphasised “use, regularity and course of conduct”. These authorities are not consistent with the Councils’ contention that the term “trade” or “trading” necessarily encompasses “activities of a commercial or income-producing nature”.

86 Secondly, in any case, it is not the term “trading” that falls for construction under cl 26.2(a)(ii) of the Leases. The expression used in cl 26.2(a)(ii) is the composite phrase “trading … operations”. The Macquarie Dictionary (online) defines “operations” in various ways, including as “a course of productive or industrial activity”. Taken together, the expression “trading … operations” therefore is directed to portions of the Airports that are actively used for trading. On the Councils’ construction of cl 26.2(a)(ii), the expression “trading … operations” would encompass facilities such as toilets and waiting areas located throughout the terminals of the Airports, on the premise that those facilities are used to enhance or support trading operations or are necessary to make them efficacious. Even on that submission, however, it is apparent that those facilities do not squarely fall within the meaning of “trading … operations”. Instead, for those facilities to fall within the meaning of cl 26.2(a)(ii), the Court would need to adopt a wider construction of “trading … operations” that encompasses the use of facilities in the Airports that support “trading or financial operations”.

87 Thirdly, the language surrounding the expression “trading or financial operations” in cl 26.2(a)(ii) creates ambiguity as to the meaning of that expression. Each of the Councils, the Lessees and the Commonwealth agree that the meaning of that expression extends beyond the examples enumerated in cl 26.2(a)(ii) of “trading or financial operations” (namely, retail outlets and concessions, car parks and valet car parks, golf courses and turf farms). Equally, the parties agree that the meaning of “trading or financial operations” does not encompass the entirety of the Airport Sites other than those parts expressly excluded in cl 26.2(a) (namely, areas occupied by the Commonwealth or a Commonwealth authority, runways, taxiways, aprons, roads, vacant land, buffer zones and grass verges, and land identified in the airport Master Plan for these purposes). It follows that the matter in issue between the parties is the extent to which the concept of “trading or financial operations” extends beyond the examples enumerated in cl 26.2(a)(ii) and, in particular, whether that concept embraces or excludes aeronautical services and facilities. This dispute necessarily raises a constructional choice which requires consideration of the commercial purpose or objects of cl 26.2(a)(ii) as revealed by events, circumstances and things external to the Leases: Mount Bruce at [49].

88 For the above reasons, we agree with the primary judge’s conclusion at Judgment [210] that cl 26.2 involves a “constructional choice”. We also agree with his Honour’s conclusion at Judgment [230] that this is a “paradigm case in which evidence of context and surrounding circumstances may and should be used to resolve the ambiguity or constructional choice”. It follows that we reject the Councils’ submission that the primary judge deployed surrounding circumstances to contradict or displace the plain meaning of the words used in cl 26.2(a)(ii). The approach of the primary judge was to first consider whether the construction of cl 26.2 gave rise to a “constructional choice”. Only after being satisfied of this did his Honour turn to consider the surrounding circumstances to determine the meaning and ambit of the concept of “trading or financial operations” and whether that concept embraces or excludes aeronautical services and facilities. In that regard, the primary judge adopted an orthodox approach to the principles of construction.

89 It follows that, in our opinion, it was permissible for the primary judge to have regard to surrounding circumstances in construing cl 26.2(a).

Text of cl 26.2(a)

90 The primary judge noted that the “starting point” of any construction of cl 26.2(a) is the text of that clause: Judgment [203]. The substance of the Councils’ challenge to the primary judge’s analysis of the text of cl 26.2(a) is his Honour’s application of the ejusdem generis maxim to limit the word “trading” in cl 26.2(a) to the examples specifically enumerated, namely retail outlets and concessions, car parks and valet car parks, golf courses and turf farms. The primary judge stated that each of these examples is “contestable in the relevant market”: Judgment [220]. The Councils’ contention is that the genus of the examples is, in fact, “activities from which revenue is derived or which support the generation of revenue”.

91 We do not consider that the primary judge’s application of the ejusdem generis maxim was in error for the following reasons.

92 It is first necessary to observe three features of cl 26.2(a) of the Leases.

93 First, the express terms of the Leases make it plain that the concept of areas on which “trading or financial operations” are undertaken connotes something less than the Airport Sites in their entirety. Clause 3.1(a)(i) of the Leases provides that the Lessees must provide for the use of the Airport Site as an airport, with the “Airport Site” defined to include the whole of the land that is subject to the Leases (cl 2.1). In turn, the chapeau in cl 26.2(a) provides that rates are leviable “in respect of those parts of the Airport Site” (emphasis added) falling within the categories in cl 26.2(a)(i) and (ii). The introductory phrase in the chapeau has no work to do if the words “trading or financial operations” are understood to encompass the use of the whole of the Airport Site as an airport.

94 Secondly, cl 26.2(a) prescribes, by sub-cll (i) and (ii), two “parts” of the Airport Site which are rateable: areas sub-leased by the Lessees to tenants, and areas on which “trading or financial operations are undertaken”.

95 Thirdly, the parties to the Leases expressly agreed in cl 26.2(a)(ii) that retail outlets and concessions, car parks and valet car parks, golf courses and turf farms each comprise parts of the Airport Site on which “trading or financial operations” are undertaken. The parties to the Leases also expressly agreed that runways, taxiways, aprons, roads, vacant land, buffer zones and grass verges, and the land identified in the airport Master Plan for these purposes do not constitute parts of the Airport Site on which “trading or financial operations” are relevantly undertaken. The text of cl 26.2(a) – that is, both its explicit inclusions and exclusions – thus informs the content of “trading or financial operations” for the purposes of cl 26.2(a)(ii). More specifically, the respective lists of inclusions and exclusions provide textual indicia of the types of activities that would constitute “trading or financial operations” and those that would not.

96 The above matters render untenable the Councils’ proposed construction of the expression “trading or financial operations” in cl 26.2(a)(ii) – that is, that that expression be construed, ejusdem generis by reference to the list of inclusions in cl 26.2(a)(ii), as referring to any “activities from which revenue is derived or which support the generation of revenue”. This is for two reasons.

97 First, whenever the Lessees enter into a sub-lease with tenants within the meaning of cl 26.2(a)(i), they are engaged in an activity from which they derive revenue. A construction of “trading or financial operations” in cl 26.2(a)(ii) as encompassing any activity from which revenue is derived would therefore render cl 26.2(a)(i) otiose.

98 Secondly, a construction of “trading or financial operations” in cl 26.2(a)(ii) as encompassing any activity from which revenue is derived would render almost the entirety of the Airport Sites rateable. The only parts of the Airport Sites identified by the Councils as not rateable on their construction, which would not otherwise fall within the express exclusions in cl 26.2(a)(ii), were vacant buildings that are not sub-let. On the hearing of the appeal, Senior Counsel for the Councils explained that such sites: “don’t constitute vacant land [which is expressly excluded under cl 26.2(a)(ii)] because there are improvements on the land at that particular location, but also, they are not being utilised for trading operations at that particular time”: Ms Cuthbertson SC, Appeal Transcript 12.39-41. However, on this construction, the ordinary infrastructure of the Airports, if in use, would constitute a part of the Airports on which “trading or financial operations” were undertaken. It is difficult to reconcile such an expansive construction of the range of activities falling within “trading or financial operations” with the express exclusions in cl 26.2(a)(ii), which include components of airport infrastructure which plainly are in use, such as runways, taxiways and aprons.

99 We consider that the primary judge was correct to conclude that the list of inclusions and exclusions in cl 26.2(a)(ii) supports the view that the expression “trading or financial operations” captures a more limited range of activities and does not capture parts of the Airport Site that are devoted to aeronautical operations. That is so because, as identified by the primary judge at Judgment [221], the areas that are expressly included within the scope of the clause are of a kind that are not unique to airports, namely retail outlets, car parks and golf courses, and turf farms. Equally, all of the areas that are specifically excluded are areas that are necessary for, or otherwise support, the unique operations and activities of an airport such as runways and taxiways, aprons and buffer zones.

100 The Councils’ challenge to the primary judge’s application of the ejusdem generis maxim goes nowhere. The ejusdem generis maxim is a sub-principle of the noscitur a sociis maxim, which refers to the general principle of construction that the meaning of a word can be gathered from its associated words: Lend Lease Real Estate Investments Ltd v GPT RE Ltd [2006] NSWCA 207 at [30]. This parent principle “is not some exceptional or strained principle of construction; it is an obviously sensible principle to be applied in understanding the meaning of words in their context”: Australian Aviation Underwriting Pty Ltd v Henry (1988) 12 NSWLR 121 at 126 (Hope JA, Priestley JA agreeing). As noted by Dixon J in Cody at 649, it is wrong to use the ejusdem generis maxim “as a piece of abstract or mechanical reasoning”. It instead must be “used as a guide in a process of interpretation which takes into account the whole instrument and the subject matter”. The primary judge’s considered approach gave meaningful content to the expression “trading or financial operations” by reference to the shared characteristics of the matters included and excluded from the meaning of that expression in cl 26.2(a)(ii). There was no error in this approach. For the primary judge to have done otherwise would have been to construe the expression “trading or financial operations” without regard to its immediate context – namely, the list of inclusions or exclusions which immediately followed it.

Purpose of cl 26.2(a)

101 The primary judge’s construction of cl 26.2(a) was supported by an analysis of the surrounding circumstances of the Leases, which were relevant to identifying the commercial purpose of that clause: Judgment [222]-[229]. For the reasons stated at [83]-[89] above, we consider that it was appropriate for the judge to have regard to surrounding circumstances in construing cl 26.2(a). It was common ground before the primary judge that cl 26.2(a) was included in the Leases pursuant to the principles of competitive neutrality. We agree with the primary judge’s conclusion that, at the time the Leases were entered into, competitive neutrality had no relevance or application to the provision of aeronautical services and facilities at the Airport Sites. This is because there was no relevant market or competitor for those services: Judgment [222] and [224].

102 We reject the Councils’ submission that the CPA and CNPS do not support the primary judge’s construction of cl 26.2(a).

103 At the time that the Leases were entered into, cl 3(1) of the CPA stated that the objective of competitive neutrality was to eliminate resource allocation distortions arising out of the public ownership of entities engaged in significant business activities, and to ensure that “[g]overnment businesses do not enjoy any net competitive advantage simply as a result of their public sector ownership”. Clause 4(3) dealt with structural reform of public monopolies. As noted at [23] above, at the time, the Airports were public monopolies. Clause 4(3)(b) provided that, before introducing competition into a market traditionally supplied by a public monopoly, the parties to the CPA would undertake a review into “the merits of separating potentially competitive elements of the public monopoly”. Clause 4(3)(b) thus expressly referred to a separation of contestable and non-contestable elements of a public monopoly, such as the Airports.

104 The CNPS, which was also issued prior to the parties’ entry into the Leases, also emphasised the importance of fair competition specifically where governments provide services “through market based mechanisms that allow actual or potential competition from a private sector provider” (emphasis added). It is true, as the Councils submit, that, in the CNPS, the FAC was categorised as a “Government business enterprise,” and consequently the FAC was characterised as having the “principal function of selling goods and services in the market for the purpose of earning a commercial return”. However, critically, the CNPS acknowledged that government agencies were involved in both business activities and non-business activities. It made clear that competitive neutrality principles would be applied only to those parts of government business activities which “meet the business criteria” (that is, it would not be applied to the non-business activities of government agencies). The business criteria included that “there must be an actual or potential competitor (either in the private or public sector)”.

105 It is thus clear from a review of the CPA and the CNPS that, at the relevant time, the concept of competitive neutrality was intended to apply to “contestable” activities. In the case of the Airports, which were public monopolies, this required inter alia that there be an “off-airport site” competitor for the services supplied on the Airport Sites.