FEDERAL COURT OF AUSTRALIA

Ascic v Comcare [2020] FCAFC 105

ORDERS

Appellant | ||

AND: | Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

2. The Appellant is to pay the costs of the Respondent, either as agreed or taxed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

THE COURT:

1 The Appellant in the present proceeding, Mr Marko Ascic, is a former member of the Australian Federal Police. The Respondent to the proceeding is Comcare.

2 Mr Ascic suffered an “injury” in December 1987. He retired in September 1988, being totally incapable of engaging in any work. Initially, compensation payments were made pursuant to the Compensation (Commonwealth Government Employees) Act 1971 (Cth) (the “Compensation Act 1971”). That Act, however, was repealed by the Safety, Rehabilitation and Compensation Act 1988 (Cth) (the “Compensation Act 1988”). The provisions of the Compensation Act 1988 the subject of dispute commenced on 1 December 1988, and that Act establishes Comcare as a body corporate pursuant to s 74.

3 There were necessarily transitional provisions to facilitate the continuation of compensation entitlements upon the repeal of the former Act and the commencement of the latter Act.

4 Mr Ascic has at all material times contended that his compensation payments should have been determined pursuant to s 131(2) of the Compensation Act 1988. He requested Comcare to undertake a review. On 23 December 2015, a Senior Review Officer wrote to Mr Ascic stating (in part) as follows:

I refer to your request for Comcare to conduct an independent review of every determination ever made concerning your entitlement to compensation for incapacity.

I have now completed my reconsideration and, after evaluating the evidence, I have decided that the determinations were correct and I have affirmed them.

The Review Officer concluded that the “total benefits” Mr Ascic was receiving “were less than 95% of [his Normal Weekly Earnings]” and hence that s 131(3) applied and not s 131(2).

5 Mr Ascic sought review of the December 2015 decision by the Administrative Appeals Tribunal. He was unsuccessful, with the Tribunal affirming the decision under review in September 2017: Re Ascic and Comcare [2017] AATA 1436. An appeal from the Tribunal’s decision was dismissed in June 2019: Ascic v Comcare [2019] FCA 819.

6 Mr Ascic now appeals to this Court. He appeared unrepresented. Comcare appeared by Counsel.

7 A Notice of Appeal was first filed in June 2019. Pursuant to leave being granted, an Amended Notice of Appeal was filed in December 2019. The Amended Grounds of Appeal are voluminous, comprising some 23 purported Grounds. What characterises many of these Grounds is the fact that they pay scant regard to the arguments sought to be advanced before the primary Judge and many seek what appear to be a review of the factual merits of the Tribunal decision. Some of the purported Grounds, however, do seek to direct attention to errors said to have been made by the primary Judge. The Amended Notice of Appeal clearly does not conform with r 36.01(2)(c) of the Federal Court Rules 2011 (Cth).

8 At the outset of the hearing of the appeal, Mr Ascic sought to further amend the Amended Notice of Appeal. Leave had previously been refused by a single member of the Court as now constituted at a Case Management Hearing. Mr Ascic was advised that the Court would reconsider the earlier refusal of leave. Even as sought to be amended, the issues Mr Ascic wished to pursue on appeal were not clearly articulated. In such circumstances, the course pursued on appeal has been for the Court itself to review the decision of both the Tribunal and the reasons for decision of the primary Judge. Following the hearing of the appeal, Mr Ascic contacted the Court and indicated that he wished to make further submissions to those he had presented at the hearing. The Court allowed him an opportunity to provide further submissions, and the Respondent a right of reply. The Court has had regard to those additional submissions.

9 The fate of the appeal depends primarily upon the manner in which the Tribunal resolved such facts as were put in issue in the proceeding before it. Those facts were either relevantly agreed or resolved adversely to Mr Ascic by the Tribunal. In particular, an agreed fact was that Mr Ascic’s “Normal Weekly Earnings … was $734.46”.

10 Although Mr Ascic was unrepresented, he was very much alive to the importance of impugning that figure. Even though he may not have formally sought leave to withdraw that concession, either before the Tribunal or the primary Judge, consideration has been given to whether leave should now be granted and whether leave should further be granted to advance a case on appeal which is different to that relied upon before both the Tribunal and the primary Judge.

11 In very summary form, it has been concluded that:

given the agreement as to the normal weekly earnings, the correct or preferable decision was that in fact reached by the Tribunal, namely that Mr Ascic’s claim fell within s 131(3) of the Compensation Act 1988 and not s 131(2);

the Tribunal committed no error in its interpretation or application of ss 123 and 131 of the Compensation Act 1988, nor any error in its interpretation and application of ss 25 and 45 of the Compensation Act 1971; and

the Tribunal did not deny Mr Ascic a reasonable opportunity to present his application for review.

The primary Judge was correct in rejecting similar arguments which were advanced before him. No appellable error is discernible in the reasons of the primary Judge. It has further been separately concluded that:

even if the Tribunal had committed any legal error in the interpretation of the provisions of either the 1971 or 1988 Compensation Act, any error would have been non-prejudicial by reason of the agreement reached as to the normal weekly earnings.

It has also been concluded that:

leave should not be given to Mr Ascic to withdraw his admission as to his normal weekly earnings.

Given these difficulties, the proposed further Amended Notice of Appeal would not have canvassed any different factual or legal issue. Leave to further amend was thus properly refused.

12 The appeal should be dismissed with costs.

SECTION 131 – THE COMPARISON REQUIRED

13 Once the relevant facts have been identified, what may otherwise have presented as a confusing morass of statutory provisions and terminology readily falls into place. But the starting point remains Part X of the Compensation Act 1988 and, in particular, s 131. Part X commenced on 1 December 1988.

14 Part X is titled ‘Transitional Provisions’, and effects the transition from the previous liability to pay compensation pursuant to (relevantly) the Compensation Act 1971, to the liability to pay compensation pursuant to the Compensation Act 1988. Section 128, within Part X, thus provides (in relevant part) as follows:

Liability under previous Acts

Any liability of the Commonwealth, or of a Commonwealth authority, to pay compensation or make any other payment to a person under any provision of the … 1971 Act shall, to the extent that it had not been discharged before the commencing day, be taken to have been incurred by the relevant authority on that day under the corresponding provision of this Act.

Notwithstanding the considerable emphasis placed by Mr Ascic on this provision in his submissions, including the written submissions that were filed after the hearing with leave of the Court, the simple effect of s 128 is that after the commencing date his entitlements were to be payable under the Compensation Act 1988.

15 Within Part X, Div 3 contains what are referred to as “special transitional provisions relating to certain former employees”. Within that Division, s 131 provides for the amount of compensation “former employees” are to receive under the Compensation Act 1988. Section 131 provides (in relevant part) as follows:

Former employees under 65 who are in receipt of superannuation benefits and are unable to engage in any work

(1) This section applies to a former employee who:

(a) on the commencing day, was under 65 and in receipt of a pension under a superannuation scheme; and

(b) is not capable of engaging in any work.

(2) Subject to this Division, if the former employee's total benefit immediately before the commencing day was equal to or more than 95% of his or her normal weekly earnings as at that day, the amount of compensation payable per week to the former employee under this Act is the amount that, when added to the former employee’s superannuation amount, results in a combined benefit equal to 95% of those normal weekly earnings.

(2A) If, as a result of an increase in the amount of a former employee's normal weekly earnings, the amount of combined benefit payable to the former employee under subsection (2) is less than 70% of those increased normal weekly earnings, the amount of compensation must be increased or further increased (as the case may be) until it is equal to 70% of those increased normal weekly earnings.

(3) Subject to this Division, if the former employee's total benefit immediately before the commencing day was equal to or more than 70%, but less than 95%, of his or her normal weekly earnings as at that day, the amount of compensation payable per week to the former employee under this Act is an amount equal to the employee's 1971 amount.

…

16 It was common ground that Mr Ascic satisfied s 131(1) – namely it was common ground that he was a “former employee” who was “on the commencing day” under 65 years of age and a person who was “not capable of engaging in any work”.

17 What was not common ground was whether Mr Ascic fell within s 131(2), as he contended, or s 131(3), as was the contention of Comcare.

18 Both s 131(2) and (3) require a comparison to be made between a former employee’s “total benefit immediately before the commencing day” and the employee’s “normal weekly earnings as at that day…”.

19 As to the former phrase, s 123 provides the following definition:

total benefit, in relation to a former employee, means an amount equal to the sum of:

(a) the amount of compensation payable per week to the former employee under the 1971 Act; and

(b) the employee’s superannuation amount.

It was s 45 of the Compensation Act 1971 which relevantly regulated the compensation payable to employees under that Act. Section 45 provided in part as follows:

(1) Where an injury to an employee results in the employee being totally incapacitated for work, the succeeding provisions of this section have effect.

(2) Subject to this section, compensation is payable to the employee, during the period of the incapacity, of an amount per week equal to -

(a) $90, or such higher amount as is prescribed, plus any amount or amounts required to be added to that amount in accordance with the succeeding provisions of this section; or

(b) the average weekly earnings of the employee before the injury, whichever is the less.

…

(3) If there is a prescribed person who is, or there are prescribed persons who are, wholly or mainly dependent upon the employee, there shall be added to the amount specified in paragraph (a) of sub-section (2) the amount of $23.60 or such higher amount as is prescribed.

(4) If there is a child in relation to whom this Act applies (whether born before, on or after the date of the injury) who is wholly or mainly dependent upon the employee or there are children in relation to whom this Act applies (whether born before, on or after the date of the injury) who are wholly or mainly dependent upon the employee, there shall be added to the amount specified in paragraph (a) of sub-section (2) the amount of $11.25, or such higher amount as is prescribed, for that child or each of those children, but an amount shall not be so added for a child in relation to any time before the date of the birth of that child.

…

(7) If the employee-

(a) is retired from his employment as a result of the incapacity for work; and

(b) as a result of the retirement is in receipt of a pension under a superannuation or provident scheme established or maintained by the Commonwealth or by a prescribed authority of the Commonwealth,

the compensation payable to the employee in respect of each week during the period of the incapacity shall not exceed the amount, if any, by which the average weekly earnings of the employee before the injury exceed-

(c) if a part of the pension is, under the scheme, attributable to contributions for the pension paid by the employee-the part of the pension paid or payable to the employee in respect of that week that is not attributable to those contributions;

(d) if the employee has paid contributions under the scheme, the scheme does not identify a part of the pension as being attributable to those contributions and the Commissioner has determined that if it is reasonable that a part of the pension should be treated as if it were attributable to those contributions – the part of the pension paid or payable to the employee in respect of that week that is determined by the Commissioner to be the part that is to be treated as not attributable to contributions for the pension paid by the employee; or

(e) in any other case-the pension paid or payable to the employee in respect of that week.

Section 45, together with other provisions of the now-repealed Compensation Act 1971, referred to the earnings of an employee. It was s 25 of the Compensation Act 1971 which relevantly regulated the manner in which these earnings were to be calculated. That section provided in part as follows:

…

(2) A reference in the succeeding provisions of this section to earnings of an employee in relation to any employment shall be read as including a reference to any allowance payable to the employee in respect of that employment other than an allowance that is payable in respect of special expenses incurred or likely to be incurred by the employee in respect of that employment.

…

(4) Subject to the succeeding provisions of this section, the average weekly earnings of an employee before the injury shall be calculated in relation to the period immediately preceding the date of the injury in which he was continuously employed by the Commonwealth but any part of that period that was earlier than twelve months before that date shall be disregarded.

…

20 As to the phrase “normal weekly earnings”, it was the Compensation Act 1988 which introduced that notion for the first time. It is “[o]ne of the critical components in the calculation of the compensation payable … to a person incapacitated for work by a compensable injury…”: Comcare v Thompson [2000] FCA 790 at [3], (2000) 100 FCR 375 at 376-377 per Finn J. Section 8 sets forth the manner of calculating such earnings. What the transition from the Compensation Act 1971 to the Compensation Act 1988 required in order for there to be continuity of compensation was, amongst other things, the quantification of an amount so that it could be compared with the newly introduced concept of “normal weekly earnings”. For the purposes of that comparison, ss 25 and 45 of the now-repealed Compensation Act 1971 informed the manner in which (for example) “allowances” and “overtime” were to be included in the quantification of the “earnings of an employee” and the manner in which the “compensation” was to be calculated. Notwithstanding submissions made by Mr Ascic that because the Compensation Act 1971 was repealed it was a “dead act” and has no operation, the relevant provisions of that Act are given operation by s 131(3) of the Compensation Act 1988 and the definition of “total benefit” in s 123.

THE FACTS – NON-PREJUDICIAL ERRORS & NO QUESTIONS OF LAW

21 When seeking Comcare undertake “an independent review of every determination ever made”, the facts then relied upon by Mr Ascic were summarised as follows in the letter from the Senior Review Officer in December 2015:

On 29 September 2015 you wrote an email to Comcare submitting that your compensation for incapacity had been incorrectly calculated because, at the commencement date of the Safety, Rehabilitation and Compensation Act 1988 (‘SRC Act’) you were ‘receiving a superannuation pension of $18,655.73 per annum and Comcare benefits of $14,456.09 per annum’, being a combined total benefit of $33,982 per annum. You also submitted that your normal weekly earnings (‘NWE’) were $33,111.82 at that time and that 95% of your NWE was $32,282.90. You then submitted that your combined benefit was more than 95% of your NWE and that your entitlement to compensation for incapacity should have been calculated, and should still be calculated, under section 131(2) of the SRC Act.

The Senior Review Officer then went on to state as follows the finding he had made for Mr Ascic’s “normal weekly earnings” and his reasons for his decision as follows:

I agree that your combined superannuation and compensation benefit at the commencement date of the SRC Act was $33,111.82, but I do not agree that your NWE at that time was only $33,982.

Our electronic records of your NWE figures commence from November 1990, and at that time your NWE were $838.96 per week, which is a yearly figure of $43,625.92. It is important to note that the NWE figure is calculated taking into account the earnings of the time of your injury and increasing in line with award increases and also takes into account allowances and overtime.

I have used the November 1990 NWE figure as a starting point. Your figure of $33,982 from November 1988 would need to have increased by approximately 24% in two years to reach the November 1990 figure. I find this extremely unlikely.

I am satisfied that your NWE was significantly higher than $33,982 at the commencement of the SRC Act, such that the combined benefit you were receiving at the time is very unlikely to have been more than 95% of the NWE.

In other words, at the commencement date of the SRC Act, I am satisfied that you were receiving total benefits that were less than 95% of your NWE. The applicable subsection of the SRC Act for the calculation of incapacity at the commencement of the SRC Act was subsection 131(3), being the section relevant to those employees who were receiving between 70% and 95% of their NWE on the commencement date.

Section 131(5) is also relevant. It has the effect of gradually reducing compensation for incapacity until the combined benefit equals 70% of NWE. From reviewing your file, it appears that your compensation for incapacity was reduced in line with that section until 28 June 1991. As at that date, your combined benefit equalled 70% of your NWE.

This was the decision and the reasons for decision which were reviewed by the Tribunal.

22 For the purposes of determining the “correct or preferable” decision, the Tribunal proceeded to accept the facts which had by that stage been agreed between the parties and proceeded to make a series of other findings of fact which were put in issue. Two of the “agreed facts” recorded in a Statement of Agreed Facts and Issues filed with the Tribunal were expressed as follows:

3.5 The Applicant’s superannuation amount “immediately before the commencing day” was $358.76.

3.6 The Applicant’s Normal Weekly Earnings (NWE) “as at that day” was $734.46.

(footnotes omitted).

In addition to these “agreed facts”, the Tribunal also made the following findings of fact, namely:

the weekly amount of compensation payable per week to Mr Ascic from July to December 1988 was $267.30 ([2017] AATA 1436 at [54(a)]);

Mr Ascic’s total benefit as defined in s 123 of the Compensation Act 1988 was $626.06 ([2017] AATA 1436 at [56]); and

as at 1 December 1988 Mr Ascic’s “normal weekly earnings” were $777.59 ([2017] AATA 1436 at [59]).

23 The purpose of now identifying these findings of fact at the outset is to clearly delineate those matters which could be reviewed by the primary Judge and those matters which were left entrusted to the Tribunal alone. The “appeal” before the primary Judge, as repeatedly stressed by the primary Judge, was an “appeal” confined to a “question of law”: Administrative Appeals Tribunal Act 1975 (Cth) (“Administrative Appeals Tribunal Act”). Section 44(1) of that Act provides as follows:

A party to a proceeding before the Tribunal may appeal to the Federal Court of Australia, on a question of law, from any decision of the Tribunal in that proceeding.

…

Although characterised as an “appeal”, the proceeding is an application to this Court exercising its original jurisdiction: Drake v Minister for Immigration and Ethnic Affairs (1979) 46 FLR 409 at 410 per Bowen CJ and Deane J, at 422 per Smithers J. See also: Minister for Immigration and Ethnic Affairs v Gungor (1982) 42 ALR 209 at 219-220 per Sheppard J, at 211-212 per Fox J and Clements v Independent Indigenous Advisory Committee [2003] FCAFC 143 at [11]–[12], (2003) 131 FCR 28 at 33 per Gray ACJ and North J. And, importantly for present purposes, the subject matter and scope of the proceeding is limited to the question of law and does not extend to a re-hearing of the whole matter: cf. Brown v Repatriation Commission (1985) 7 FCR 302 at 304. Bowen CJ, Fisher and Lockhart JJ there observed:

The existence of a question of law is not merely a qualifying condition to ground an appeal from a decision of the Tribunal; rather, it and it alone is the subject matter of the appeal, and the ambit of the appeal is confined to it…

See also: Kowalski v Military Rehabilitation and Compensation Commission [2010] FCAFC 10 at [38] to [39], (2010) 114 ALD 8 at 19 per Marshall, Tracey and Foster JJ.

24 Many of the arguments sought to be canvassed before the primary Judge, and again on appeal to this Court, impermissibly sought to challenge the findings of fact made by the Tribunal and sought, in effect, that this Court should undertake a “re-hearing” and itself make findings of fact – indeed findings of fact contrary to those found by the Tribunal.

25 But, if any argument as to whether the issues sought to be raised before the primary Judge and this Court on appeal constituted a “question of law” is presently left to one side – and if attention be confined to the facts – it emerged that any disagreement as to the facts ultimately had little legal consequence.

26 By reference to Mr Ascic’s submissions to the Senior Review Officer, and as set forth by the Tribunal, on his case the total benefits he was receiving as at the commencement of the Compensation Act 1988 were to be calculated as follows by reference to a total annual income of $33,111.82:

Tribunal Reasons para reference | annual | weekly | |

A superannuation pension payment | 7(a) | $18,655.73 | $358.76 |

Comcare payments | 7(a) | $14,456.09 | $278.00 |

Total | $33,111.82 | $636.76 |

And on his case, his “normal weekly earnings” he was then receiving were to be calculated by reference to the total amount of monies received annually, being a salary component and a component representing penalties and overtime. The total of these two components annually was the sum of $33,982.00 as summarised in the December 2015 letter, namely:

Tribunal Reasons para reference | annual | weekly | |

Salary | 7(b) | $26,375.00 | $507.21 |

Penalties & overtime | 7(b) | $7,607.00 | $146.29 |

Total | $33,982.00 | $653.50 |

The quantification of the salary as being $26,375 corresponds to (inter alia) the amount disclosed in a document titled “Details of salary, wages, etc. for AWE purposes” dated 25 August 1988.

27 Contrary to this approach, the Tribunal proceeded (relevantly) from the “agreed fact” that Mr Ascic’s normal weekly earnings were $734.46: [2017] AATA 1436 at [27]. Notwithstanding “agreement” as to this amount, Comcare sought to “revise” the figure to $769.13: [2017] AATA 1436 at [28]. The Tribunal made a finding of fact ([2017] AATA 1436 at [59]) that Mr Ascic’s normal weekly earnings was $777.59. The divergence in calculations depended upon what (if any) “allowances” were to be included in the calculation. These various calculations are exposed by the following table:

Agreed normal weekly earnings | $734.46 |

Exam allowance | $21.65 |

Investigator’s allowance | $9.82 |

Spending allowance | $11.66 |

Total | $777.59 |

Higher duties allowance | $2.23 |

Total | $779.82 |

Comcare’s calculation of $769.13 was not fully explained – but that assumes no present relevance. The Tribunal concluded that Mr Ascic was not entitled to the “higher duties allowance”: [2017] AATA 1436 at [59].

28 On Mr Ascic’s case, for the purposes of s 131 he maintained before the Tribunal (albeit by reference to an annual sum) that:

95% of the weekly amount he received calculated by reference to his salary and penalties and overtime was $620.82 ($32,282 annually);

and that this amount was less than:

the total of the benefit he was receiving by way of superannuation and Comcare payments, being $636.76 ($33,111.82 annually).

On Comcare’s case and on the findings of fact as made by the Tribunal, for the purposes of s 131, Mr Ascic was in receipt of:

a “total benefit” of $626.06;

and that sum was:

80.52% of his normal weekly earnings of $777.59:

![]()

The difference between Mr Ascic’s calculation of $636.76 and the Tribunal’s finding as to the “total benefit” is explained by the Tribunal’s finding that the amount of compensation being paid weekly was $267.30, rather than Mr Ascic’s figure of $278.00 (i.e., $358.76 + $267.30 = $626.06).

29 There is little difference in the two calculations representing the “total benefit” Mr Ascic was receiving. On Mr Ascic’s calculation the sum is $636.76; on the Tribunal’s finding the sum is $626.06. That difference assumes no present relevance.

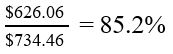

30 What dooms Mr Ascic’s case is the agreed fact that the normal weekly earnings were $734.46 and not his calculation founded upon total monies received annually being $33,111.82 or $636.76 weekly. If this sum of $734.46 stands, then any calculation using either of the proposed amounts for “total benefit” always leads to a percentage of less than 95%. And it matters not whether any or all of the “allowances” are included or excluded – again, the percentage always remains less than 95%. Thus, for example, on the calculation most favourable to Mr Ascic, namely a total benefit of $626.06 and normal weekly earnings of $734.46, and excluding the payment of any “allowances” the percentage is 85.2 %, namely:

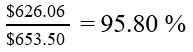

It is only if the denominator ($734.46) is reduced to the sum relied upon by Mr Ascic (i.e., $653.50) that the percentage increases as follows:

31 Without cavilling with the agreed fact as to normal weekly earnings being $734.46, it may be noted that this amount:

equates to an annual salary of about $38,192; and

elsewhere in the Tribunal’s reasons ([2017] AATA 1436 at [46]), there is reference to a “base salary” of $25,048.

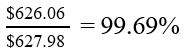

Neither of these figures, obviously enough, is the same as the salary of $26,375 referred elsewhere in the Tribunal’s reasons and (in particular) in the summary of Mr Ascic’s submissions: [2017] AATA 1436 at [7(b)]. If the “base salary” be relied upon, and not either the figure relied upon by Mr Ascic in his submissions nor the agreed figure of $734.46, the percentage calculation obviously enough becomes much more favourable to supporting Mr Ascic’s case. The combined salary and penalties and overtime figure is thus $627.98:

Relevantly, the s 131 calculation then becomes:

Subject to any application to withdraw the admission, why Mr Ascic and Comcare agreed that the normal weekly earnings “as at that day” were $734.46, and the manner in which that sum was calculated, were matters neither inquired into by the Tribunal, nor matters that should have been pursued by the primary Judge. The figure of $734.46 was “agreed”.

32 Before this Court, Mr Ascic advanced a series of further calculations challenging both the quantum of his salary and his total benefit. The starting point for his calculations in this Court was an assertion that he had previously relied upon information provided to him from the Australian Federal Police – but this information, he submitted, was incorrect. In his written Outline of Submissions, Mr Ascic maintained that the “only genuine salary printout [that he] was able to source [was] that of [his] sister; who was promoted to the rank of Senior Constable in 1988 on a salary of $29,708.00”. Proceeding from this starting point, Mr Ascic thereafter advanced a different calculation as to both his normal weekly earnings and total benefit. These submissions concluded (without alteration):

The difference between my and my sister’s salary is now $2,234.94 and this confirms the recent information that was provided to me. (31,942.94 – 29,708 == 2,234.94) and that my total benefit was at 95% instead of 100% of my average weekly earnings.

…

In summary; on the commencing day my salary was $31,942.94, my AWE $44,218.61 and my total benefit was $42,007.68, and these values are in agreement with the parameters that are recorded on the document; unlike any values that have been provided by AFP.

The Tribunal was well aware of the challenge made by Mr Ascic to the calculations that had been undertaken by Comcare, and the challenges he made to the factual accuracy and completeness of the information being provided. Those challenges were also summarised by Mr Ascic in the section of his Submissions to the primary Judge headed “Background to this process”: [2019] FCA 819 at [50].

33 Confronted with this morass of factual information, the Tribunal made its findings of fact.

34 All that these various permutations that have been set forth expose, however, is the danger involved in a Court entertaining an appeal on a “question of law” under s 44 of the Administrative Appeals Tribunal Act and even attempting to go behind the factual calculation undertaken by the Tribunal, namely the final arbiter on questions of fact. The most recent calculation advanced by Mr Ascic founded upon his sister’s salary only emphasises the imperative of this Court leaving the task of making findings of fact to the Tribunal alone. It was the task of the Tribunal alone to unravel the competing calculations being urged upon it, that Tribunal, of course, also having before it the factual basis upon which Mr Ascic had initially sought the independent review of all previous determinations as to the quantum of his compensation.

35 To make a finding of fact or even question Mr Ascic’s normal weekly earnings being $734.46 would involve this Court:

departing from an agreement on the part of Mr Ascic that that was in fact the quantum of his normal weekly earnings;

departing from a finding of fact relied upon by the Tribunal when undertaking its review as to what was the “correct or preferable decision”; and

departing from a finding of fact not only supported by the agreement between the parties, but a finding of fact consistent with at least some of the evidence or other materials available to the Tribunal.

Such a course is not only not available to this Court given the constraints imposed by s 44 of the Administrative Appeals Tribunal Act; but it is a course which would be most imprudent in the present case, given the legislative mandate given to the Tribunal for it to normally be the final arbiter on questions of fact, and where the findings of fact to be made on the available evidence and other materials was hotly contested at the hearing.

36 Other than as providing a “sounding board” against which propositions of law may possibly be tested, all that these various calculations expose is the prudence in both the primary Judge – and this Court on appeal – confining its focus on questions of law and, in particular, the manner in which the relevant statutory provisions have been construed and applied. To go beyond that – and to attempt to venture into the factual merits – would be both beyond the function of this Court and a course fraught with danger.

QUESTIONS OF STATUTORY CONSTRUCTION v QUESTIONS OF FACT

37 If attention be shifted from a review of the factual merits of the present proceeding, and if attention be confined (as it should be) to the identification of “questions of law”, it was possible to distil from Mr Ascic’s Amended Notice of Appeal a number of potential questions of law. The identification of these “questions” could also largely be informed by reference to the “key issues” identified by the Tribunal in undertaking its review: [2017] AATA 1436 at [20].

38 Given the fact that Mr Ascic was unrepresented, considerable latitude was extended to him in the manner in which these questions could potentially be expressed.

39 These “questions of law” principally focussed upon the correct interpretation of two phrases appearing in s 131(2) and (3) of the Compensation Act 1988, namely the phrases:

“total benefit immediately before the commencing day”; and

his “normal weekly earnings as at that day”.

Further “questions of law” could also potentially emerge from the imperative imposed by s 123 of the Compensation Act 1988 to calculate “the amount of compensation payable per week … under the 1971 Act” and, in particular:

whether reliance was properly placed by the Tribunal upon s 45(2) of the Compensation Act 1971 rather than s 45(7);

and, to a lesser extent:

whether the term “payable” in s 25(2) of the Compensation Act 1971 required actual payment to the employee or an entitlement to payment.

40 A further “question of law” potentially arose in respect to:

interpreting the term “payable” in the definition of “total benefit” in s 123 of the Compensation Act 1988, that provision requiring the Tribunal to calculate “the amount of compensation payable per week … under the 1971 Act…”, as to whether the relevant provision of the Compensation Act 1971 was s 45.

41 More open to argument was whether a “question of law” could be discerned in the making by the Tribunal of its findings of fact, being its findings of fact that:

$267.30 was Mr Ascic’s “total benefit” calculated pursuant to s 123 of the Compensation Act 1988.

42 In respect to these issues it has been concluded, in summary form, that no error is discernible in the manner in which either the Tribunal or (more importantly) the primary Judge resolved such questions of law as could be identified, and that any such questions as arose in respect to the Tribunal’s factual findings either gave rise to no question of law, or no question of law which was prejudicial to the Tribunal’s ultimate conclusion.

Immediately before & as at that date

43 Common to both s 131(2) and (3) of the Compensation Act 1988 are phrases requiring the calculation of Mr Ascic’s:

“total benefit immediately before the commencing day”; and

his “normal weekly earnings as at that day”.

44 As to the former phrase, the Tribunal concluded as follows:

[54] As to the amount of compensation payable per week to Mr Ascic under the 1971 Act (and as defined, immediately before the commencing day), the Tribunal finds as follows:

…

(b) The phrase ‘immediately before the commencing day’ for the purpose of Part X of the 1988 Act may (but may not necessarily always) refer to the date of 30 November 1988. As a matter of practicality, the Tribunal considers it reasonable to interpret the words ‘immediately before’ as meaning ‘during the applicable determination period that immediately preceded 1 December 1988.’ Depending upon when that determination period commenced, ‘immediately before’ may refer to, for example, a period of several days or several weeks.

It was in this context that the Tribunal went on to find:

(c) Given that Mr Ascic’s weekly amount of compensation payable remained the same throughout the points in time prior to and after the commencement of the 1988 Act (as confirmed by R2, Annexure C, refer to paragraph 32 above), the Tribunal considers that it can reasonably be inferred that ‘immediately before the commencing day,’ as interpreted at subparagraph 54(b) above, the amount of compensation payable to Mr Ascic at the relevant time under the 1971 Act (i.e. Mr Ascic’s AWE prior to the injury) was $267.30. …

The Tribunal thereafter went on to accept the Comcare submission that the phrase “as at that day” was a reference to 1 December 1988: [2017] AATA 1436 at [57] to [59].

45 The primary Judge referred to these findings and concluded as follows that the Tribunal had committed no error:

[68] The Tribunal then proceeded to calculate what Mr Ascic’s ‘normal weekly earnings as at that day’ (as distinct from ‘total benefit immediately before the commencing day’) …

…

[80] … The Tribunal was correct to conclude that ‘normal weekly earnings’ was an expression introduced to the Commonwealth workers’ compensation scheme by the 1988 Act on 1 December 1988. The concept of NWE did not apply to any period prior to 1 December 1988 as it was not a phrase used in any of the legislation that preceded the 1988 Act. Therefore the phrase, ‘as at that day’, can only refer to the commencement date. This is precisely how it reads. I accept the Comcare submissions (as did the Tribunal), that if the reference was intended to be to a date prior to the commencement day, the phrase ‘normal weekly earnings’ would not have been used because it is a concept foreign to the 1971 Act. The phrase ‘immediately before the commencing day’ does not refer to a fixed date. If the legislature intended to refer to a fixed date, it could easily have done so.

46 It is respectfully concluded that the Tribunal committed no error and that the primary Judge was correct in rejecting Mr Ascic’s arguments. The phrase “immediately before the commencing day” refers to a period prior to the commencing day of the Compensation Act 1988. And the phrase “as at that day” refers “to the commencement date”.

The compensation payable per week & $267.30

47 For the purposes of determining the “total benefit” payable to Mr Ascic, s 123 of the Compensation Act 1988 required the Tribunal to calculate “the amount of compensation payable per week … under the 1971 Act…”. The relevant provision of the Compensation Act 1971 was s 45.

48 Section 45(2) provided that “compensation is payable” by reference to either “$90, or such higher amount as is prescribed” (s 45(2)(a)) or “the average weekly earnings” (s 45(2)(b)), “whichever is the less”. If s 45(2)(a) be applied, the figure was $267.30; if s 45(2)(b) be applied the figure was considerably higher.

49 In finding that the “total benefit” payable to Mr Ascic was $626.06, the Tribunal:

relied upon evidence (inter alia) as to the quantum of those benefits during the period from July to December 1988 ([2017] AATA 1436 at [54]) – that being a period “immediately before” and there being no error of law in so concluding; and

found that “the amount of compensation payable per week … under the 1971 Act…” was $267.30 ([2017] AATA 1436 at [54(c)] and [56]) – that finding potentially involving a question of law as to the phrase “compensation payable”.

50 At least three things may be noted about the finding as to the compensation being $267.30.

51 First, and as noted by the primary Judge, the sum of $267.30 was calculated (in part) by reference to the “prescribed amount” ($192.80); an amount pursuant to s 45(3) in respect to his wife ($50.50) and an additional amount pursuant to s 45(4) in respect to his child ($24.00). The total of these three amounts was $267.30. The figure of $267.30 was also supported by (inter alia) two determinations in June 1988 and another determination in July 1988. That last determination assumed some significance in Mr Ascic’s argument in this Court.

52 Second, any calculation of the amount of “compensation payable per week” was a factual calculation based upon not only the sum of the amounts “prescribed” but also upon such evidence and other materials as were before the Tribunal. Although Mr Ascic, before the primary Judge, apparently argued that the Tribunal should only have had regard to the period between 1 September 1988 and 30 November 1988, the Tribunal had to proceed upon the evidence and material as were before it. And there was no direct evidence of the amount actually paid to Mr Ascic during that period. In such circumstances, no error is exposed by the Tribunal proceeding upon the evidence and other material which was available and, in any event, any error would have been an error of fact giving rise to no “question of law”.

53 In making findings of fact, the Tribunal is not bound by the rules of evidence (Administrative Appeals Tribunal Act, s 33(1)(c)) and there was substantial material upon which such findings as were made could be justified. Such evidence and other materials as were before the Tribunal and that were in fact relied upon were “rationally probative” and not merely “a matter of suspicion or speculation”: cf. Minister for Immigration and Ethnic Affairs v Pochi (1980) 44 FLR 41 at 62 per Deane J. Each of the relevant findings made by the Tribunal, it is respectfully concluded, were well-founded. And, in any event, a wrong finding of fact does not necessarily give rise to a question of law for the purposes of s 44 of that Act: cf. Drenth v Comcare [2012] FCAFC 86 at [26], (2012) 128 ALD 1 at 7 per Rares, McKerracher and Murphy JJ. A tribunal “does not commit an error of law merely because it finds facts wrongly or upon a doubtful basis…”: Minister for Immigration and Multicultural Affairs v Rajalingam (1999) 93 FCR 220 at 257 per Kenny J. There is, it has long been recognised, “no error of law simply in making a wrong finding of fact”: Waterford v The Commonwealth (1987) 163 CLR 54 at 77 per Brennan J. See also: Price Street Professional Centre Pty Ltd v Commissioner of Taxation [2007] FCAFC 154 at [24], (2007) 243 ALR 728 at 735 per Kenny J.

54 Third, the argument seems to assume little relevance. Upon the basis of the submission made by Mr Ascic to the Tribunal, Mr Ascic was contending that “at the commencement date of the 1988 Act, he was receiving … Comcare benefits of $14,456.09 per annum” ([2017] AATA 1436 at [7(a)]) or (expressed differently) $278 per week. That figure was also the one relied upon by Mr Ascic when e-mailing Comcare: [2019] FCA 819 at [56]. Whether the quantum of compensation payable under the Compensation Act 1971 be the sum calculated by the Tribunal ($267.30) or that being relied upon by Mr Ascic ($278.00), the percentage calculation for the purposes of s 131 remains much the same.

55 Any error in respect to the finding that the amount of compensation payable was $267.30 thus involved no error of law or – even if an error could be discerned – was not an error prejudicial to the ultimate conclusion reached by the Tribunal as to Mr Ascic falling within s 131(3) and not s 131(2). A decision of the Tribunal may not be set aside if an error (even an error of law) is non-prejudicial (Walterscheid Australia Pty Ltd v Collector of Customs (1988) 7 AAR 555 at 566 per Davies J) or if the same decision would be reached if the matter were remitted to it for reconsideration: Hill v Repatriation Commission [2005] FCAFC 23 at [83], (2005) 218 ALR 251 at 267. Wilcox, French and Weinberg JJ there observed that it is “well established that, in the context of appeals from the AAT, the court may decline to set aside a decision even where an error of law has been demonstrated provided that it considers that the AAT arrived at a decision that was clearly correct on the material before it”.

56 No appellable error is thus discernible in the reasons of the primary Judge in similarly so concluding: [2019] FCA 819 at [66] to [75].

Compensation – s 45(2) v s 45(7)

57 A question also arose both before the Tribunal and on “appeal” to the primary Judge as to the role s 45(7) of the Compensation Act 1971 played in the calculation of “compensation” for the purposes of s 123 of the Compensation Act 1988.

58 The same question was again sought to be pursued on appeal.

59 Section 45(2) provided that “compensation is payable” by reference to either “$90, or such higher amount as is prescribed” (s 45(2)(a)) or “the average weekly earnings” (s 45(2)(b)). Section 45(7)(d) provided, broadly speaking, that where an employee had paid contributions under a superannuation scheme, the “compensation payable” was not to exceed the amount by which the employee's average weekly earnings before the injury exceeded that part of the pension not attributable to those employee contributions, as determined by the Commissioner for Employees' Compensation. Mr Ascic’s argument was that the quantum of compensation was to be determined pursuant to s 45(7) and not s 45(2).

60 It was perhaps in recognition of the difficulty to be confronted if he were to be held to his agreement as to the normal weekly earnings being $734.46 that Mr Ascic recognised the necessity to increase the quantum of his “total benefit” as calculated pursuant to s 123 of the Compensation Act 1988, that section in turn referring to s 45 of the Compensation Act 1971.

61 If the Tribunal be correct, the quantum of compensation which formed part of the total benefit was $267.30 – namely the amount determined pursuant to s 45(2) of the Compensation Act 1971. Mr Ascic sought to invoke s 45(7)(d) in order to arrive at a quantum of $449.08 for that amount. He submitted that s 45(7) applied to a different class of persons to s 45(2). That was because s 45(2) referred to “employees” and s 45(7) referred to employees that have retired. Since the latter are former employees, s 45(2) can only be applicable to present employees. So, the argument went, s 45(7) applied to Mr Ascic as a retired former employee and s 45(2) did not apply to him. According to Mr Ascic, the making of a determination by the Commissioner under s 45(7) explained why his total benefit immediately before commencement of the Compensation Act 1988 was $449.08 per week, not the prescribed sum of $267.30.

62 Mr Ascic appears to have arrived at the higher figure on the basis of the incapacity benefit determination of July 1988. That determination was for a sum of $5,838.04 and was expressed to be attributable to the period 1 July 1988 to 30 November 1988. But, before the primary Judge Mr Ascic argued that it should only have been attributed to the shorter period from his retirement on 1 September 1988 to 30 November 1988, approximately 13 weeks. Calculated over 13 weeks the weekly benefit would have been $449.08. If this be correct, Mr Ascic’s total benefit would be $807.84 (i.e., $449.08 + $358.76) which would exceed the agreed normal weekly earnings of $734.46. Even accepting the agreement as to the normal weekly earnings, the argument was that if the compensation payable was $449.08, it would be s 131(2) of the Compensation Act 1988 which would apply.

63 There are several difficulties with this argument.

64 First, as can be seen from the summary calculations previously set forth, these figures are quite different to the figures that were put to the Tribunal, although Mr Ascic sought to justify that by saying that he had earlier been proceeding on the basis of incorrect information.

65 Second, it is in any event an argument about a finding of fact, not a question of law, and so it is an argument that neither the primary Judge could have entertained nor an argument that can be entertained on appeal. In his additional submissions filed after the hearing in this Court, Mr Ascic submitted that at [41] of the primary Judge’s reasons, his Honour accepted that Mr Ascic had received the sum of $5,838.04 over the shorter period of 13 weeks. In that paragraph, however, his Honour was simply setting out the grounds of appeal before him, and did not indicate any acceptance of Mr Ascic’s calculations.

66 Third, it overlooks that s 5(7) of the Compensation Act 1971 provided:

A reference to an employee in a provision of this Act that is applicable to an employee at a time after the Commonwealth has incurred a liability in relation to the employee under this Act shall, unless the contrary intention appears, be read as including a reference to a person who has ceased to be an employee.

Hence where s 45(2) refers to an “employee” it encompasses a retired former employee such as Mr Ascic.

67 Fourth, the primary Judge summarised the argument and his reasons for rejecting it as follows:

[76] As to the s 45(7) argument, Mr Ascic contends, by ground 3 and ground 6, that the Tribunal erred by ‘failing to determine the compensation amounts applicable pursuant to s 45(7)’ of the 1971 Act and by finding that the phrase ‘compensation payable’ in s 45(7) refers back to the phrase ‘compensation payable’ used in s 45(2).

…

[78] Mr Ascic seeks to rely on s 45(7)(d) of the 1971 Act which gives Commissioner a discretion in those limited circumstances. No such discretionary determination was in evidence. Nor has it been factually identified at any time. There is no foundation for any argument based on such a determination. The argument that s 45(7) means s 45(2)(a) does not apply to his circumstances cannot be accepted. I accept Comcare’s contention that s 45(7) simply operates to ensure that if either ss 45(7)(c)-45(7)(e) apply, an employee in receipt of a superannuation pension does not receive more by way of compensation for incapacity than a person who is not in receipt of a superannuation pension. I cannot identify error in the Tribunal’s reasoning with respect to the application of s 45(7).

Concurrence is expressed with those reasons. No error is exposed in either the findings of the Tribunal or the reasons of the primary Judge.

Normal weekly earnings & allowances – s 25(2)

68 A factual issue also arose before the Tribunal as to the weekly earnings of Mr Ascic immediately before the commencement of the Compensation Act 1988.

69 The Compensation Act 1971 did not employ the language of “normal weekly earnings…”. The phrase employed by that Act was “average weekly earnings”. Some calculation was thus required to enable a comparison to be made with the phrase first employed in the Compensation Act 1988, namely “normal weekly earnings…”.

70 It was an agreed fact that Mr Ascic’s “Normal Weekly Earnings … “as at that day” was $734.46”.

71 To this figure Comcare wanted to add additional allowances. Presumably it did so in reliance upon s 25(2) of the Compensation Act 1971 and the directive in that subsection to include “any allowance payable to the employee in respect of that employment…”.

72 There was disagreement between Mr Ascic at the hearing before the Tribunal and before the primary Judge as to:

whether any or all of these “allowances” should be included by reason of the fact that Mr Ascic maintained that he never in fact received payment of any of these amounts; and

whether all of the potential allowances should be included or whether the “higher duties allowance” should be excluded.

Again, a question of law could potentially have arisen in respect to the phrase “any allowance payable”. But, at least two points should be made about these issues.

73 First, it may be queried whether any contention developed beyond potentially an erroneous finding of fact being made by the Tribunal and became a question of law for the purposes of s 44(1) of the Administrative Appeals Tribunal Act. But a “question of law” could, it must be accepted, be distilled from an issue as to whether the term “payable” meant actually paid or rather an entitlement to payment, even if the payment had not be received by an employee.

74 Second, even if a “question of law” could be identified, any error was non-prejudicial. What primarily affected the percentage calculation for the purposes of s 131 was not whether any or all of the allowances were to be included, but rather the agreed fact as to the normal weekly earnings being $734.46.

A lack of impartiality on the part of the Tribunal?

75 An oral submission repeatedly made by Mr Ascic during the course of the hearing before this Court was a submission that he had been “overborne” during the course of the Tribunal hearing. Indeed, Mr Ascic maintained on more than one occasion he had been “shouted down” by the Tribunal when he attempted to speak.

76 No affidavit was filed by Mr Ascic in support of any such submission. The transcript of the proceeding before the Tribunal was, however, available. A review of that transcript exposes no support for any allegation or submission that the Tribunal was doing anything other than providing Mr Ascic a “reasonable opportunity” to present his case (Administrative Appeals Tribunal Act, s 39), and pursuing with him questions directed to the submissions he was making and the facts he sought to rely upon.

77 What is self-evident from the transcript is the same questioning throughout the Tribunal hearing as to the amount of the payments to be “fed into” the s 131 calculation. At all times it would appear that clarification of those individual payments was pursued by the Tribunal with Counsel for Comcare and thereafter clarification sought from Mr Ascic. Although there was initial uncertainty as to the factual basis from which the Tribunal was being invited to proceed, that which is apparent from the transcript is a process of seeking the input from both Comcare and Mr Ascic as to what those individual payments in fact were. The exchanges between the Tribunal and Mr Ascic also acknowledge the submissions then being made as to the inadequacy in the records being relied upon by Comcare, and submissions that records had been “fabricated”.

78 The transcript also records the Tribunal hearing commencing at about 10.00am on 28 June 2017 and a short break being taken at 11.55am. That short break was taken so that, according to the Tribunal member, “we would have all had a chance to consider if there’s any final comments that we wish to make…”. Short submissions were thereafter made by both Counsel for Comcare and Mr Ascic, but primarily by Mr Ascic. Nothing in those resumed submissions forms any basis for a finding that Mr Ascic was being denied a full and proper opportunity to make submissions before a Tribunal open to a fair and impartial evaluation of all that it was being told.

79 The submission that the Tribunal denied him procedural fairness is rejected.

The withdrawal of an admission

80 Although no formal application was made by Mr Ascic to withdraw his admission as to his normal weekly earnings being $734.46, consideration has nevertheless been given to whether even at this stage he should be bound by the admission first made in April 2017. Any ability to withdraw from the prior agreement, obviously enough, assumed central importance – and determinative importance – to both the case before the Tribunal and this Court.

81 Counsel for the Respondent opposed the granting of leave. In doing so, she referred in particular to the following observations of Kiefel J (as her Honour then was) in Repatriation Commission v Warren [2007] FCA 866, (2007) 95 ALD 606 at 616:

[34] As a general rule it is only in the clearest case, and for the most cogent of reasons, that a party who has conceded a matter is able to make the validity of what was conceded the basis for overturning a decision: … If there was some error on the part of the tribunal in acting upon the concession, or something approaching injustice to the applicant in holding it to the concession, the court might exercise its discretion to permit it to argue to the contrary of it and require a fresh hearing upon the matter: … The concession on the part of the applicant’s legal representative was perfectly clear. …

(citations omitted).

In that case the concession had been made by Counsel.

82 Even if the admission could be withdrawn, an additional obstacle to be confronted by Mr Ascic would be the obtaining of the leave of this Court on appeal to now place reliance upon an argument not previously advanced before the Tribunal or the primary Judge. Leave to do so can, of course, be granted.

83 Leave, it has been recognised, may more readily be granted where the new argument is “a pure question of law”: Repatriation Commission v Warren [2008] FCAFC 64 at [78], (2008) 167 FCR 511 at 529 per Lindgren and Bennett JJ. Leave has thus been refused where the new argument is not so confined: Ward v Commissioner of Taxation [2016] FCAFC 132 at [31], (2016) 247 FCR 372 at 382 per Robertson, Davies and Wigney JJ. In Princi v Federal Commissioner of Taxation [2008] FCA 441, (2008) 47 AAR 435 at 438, McKerracher J refused to permit an amendment to grounds of appeal, where the basis of the amendment was inconsistent with an agreement reached between the parties as to the basis upon which the matter proceeded before the Tribunal. In so concluding his Honour said:

[9] … This conclusion that the proposed amendment would conflict with the agreed basis of proceeding in the tribunal is not simply a technical point. If it were more form than substance, allowing the amendment might be the better course. However it is entirely conceivable as a matter of substance, that other evidence and arguments would have been relied upon in the tribunal by the Commissioner had the proposed argument been advanced. Indeed the very argument in support of the proposed amendment implicitly accepts that this would be so. The fulcrum of the argument is that the Tribunal failed to identify the scheme. To identify the scheme would have been a process which requires evaluation of the totality of the evidence and arguments at the hearing including the calling of a deal more evidence than the tribunal heard. In the absence of the agreement there may be force in the argument but the whole purpose of the agreement was presumably to narrow the issues to avoid the cost involved in such a process.

In the context of the present proceeding, any application for leave to withdraw the admission would of necessity be an application to change the factual basis upon which much – if not all – of the case before the Tribunal proceeding.

84 In seeking to depart from the agreed $734.46 figure, Mr Ascic placed very much at the forefront of his oral submissions the proposition that he had been overborne or “pressured” by officers of the Respondent to agree to the quantum of normal weekly earnings. And such correlation as there was as between such records as were in fact available and the agreement was explicable, on his case, on the basis that there had been produced to him records which had been “fabricated”. His agreement to the $734.46 figure was thus the product of his being “overborne” to reach an agreement upon the basis of incorrect information.

85 But there was no evidence that that was in fact the case; there was no evidence that Mr Ascic had been “overborne”, nor that the information as was made available to him and the Tribunal was relevantly factually incorrect. Although consideration should be given to the plight of an unrepresented litigant, especially a litigant who had suffered an injury of the kind suffered by Mr Ascic, it is respectfully concluded that leave should not now be given because:

no submission was made to the Tribunal that any pressure or improper influence had been exerted upon Mr Ascic in order to secure his agreement; and

no application had been made to the primary Judge seeking to withdraw the admission, nor was any submission advanced to the primary Judge contending that improper influence had been brought to bear in securing the agreement.

There is, moreover:

nothing in the transcript of the proceeding before the Tribunal to indicate that any impediment was placed in the path of Mr Ascic withdrawing his admission, indeed the transcript only records Mr Ascic having every opportunity to advance such submissions as he saw fit.

And, to the extent that it may now assume importance:

in presenting his oral submissions to this Court on appeal, Mr Ascic did not exhibit any symptom of being “overborne” by those opposing his claims, those persons at least including the same Counsel as appeared for Comcare in the Tribunal proceeding.

It is also not without relevance to note that Mr Ascic had filed in the proceeding before the primary Judge an affidavit going to (inter alia) “threats, intimidation and poor treatment” by the Australian Federal Police: [2019] FCA 819 at [42]. The primary Judge concluded that he would not receive “the affidavit into evidence”. Of present relevance is the fact that Mr Ascic has been given an opportunity both before the Tribunal and the primary Judge to make such challenges to the evidence as he saw fit. It is simply now too late for him to seek to depart from a principal fact upon which the case has to-date proceeded.

86 Although there were other figures as to the “base salary” or annual income of Mr Ascic which did not sit comfortably with the agreed weekly sum of $734.46 ([2017] AATA 1436 at [46]), there was no reason why the Tribunal could not proceed to act upon the agreement reached.

87 Leave to withdraw the admission as to the normal weekly earnings would have been refused, even if sought. The time has well and truly come for Mr Ascic to be held to the facts which he agreed to before the Tribunal.

CONCLUSIONS

88 The appeal should be dismissed.

89 There is no appellable error.

90 Contrary to Mr Ascic’s written Outline of Submissions, the “whole of this Judicial Process” has not been “determined on the basis of unsupported inferences and incorrect interpretations” – the case has been founded largely upon an admission made by him for the purposes of the Tribunal hearing that his normal weekly earnings were $734.46. There is no reason why he should not be held to that admission, no application for leave to withdraw the admission being made to either the Tribunal or the primary Judge.

91 There is no reason why the normal rule should not prevail as to costs following the event. The Appellant should thus pay the costs of the Respondent.

THE COURT ORDERS THAT:

1. The appeal is dismissed.

2. The Appellant is to pay the costs of the Respondent, either as agreed or taxed.

I certify that the preceding ninety-one (91) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justices Flick, Banks-Smith and Jackson. |

Associate: