FEDERAL COURT OF AUSTRALIA

The Owners - Units Plan No. 3115 v The Trustees of the Master Builders Fidelity Fund Scheme [2019] FCAFC 227

ORDERS

THE OWNERS - UNITS PLAN NO. 3115 Appellant | ||

AND: | THE TRUSTEES OF THE MASTER BUILDERS FIDELITY FUND SCHEME Respondent | |

DATE OF ORDER: | 13 December 2019 |

THE COURT ORDERS THAT:

2. The appellant pay the respondent’s costs of the appeal.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

THE COURT:

Introduction

1 This appeal concerns a dispute between the owners corporation for a building known as the Elara Apartments (the appellant) and the trustees of a fidelity fund scheme for the Australian Capital Territory (ACT) which is established under a trust deed titled Master Builders Fidelity Fund Trust Deed (the respondent). The Elara Apartments are located at 10 Thynne Street, Bruce, ACT and comprise 120 residential units and four commercial units. As owners corporation for the Elara Apartments, the appellant holds a leasehold estate in the common property of the building pursuant to s 33(3) of the Unit Titles Act 2001 (ACT).

2 The developer of the Elara Apartments was B & T Developments (ACT) Pty Ltd (the developer) and the builder was B & T Constructions (ACT) Pty Ltd (the builder). Construction of the apartments began in June 2005 and was completed in mid 2007. In May 2005, prior to the commencement of construction, the builder applied to the respondent for the Elara Apartments to be covered under the Master Builders Fidelity Fund Scheme (Fidelity Fund Scheme). The builder paid the respondent the required premium of $105,315 and the respondent issued 120 “fidelity certificates” in respect of each of the residential units to be constructed as part of the Elara Apartments.

3 In 2013, the appellant began proceedings in the ACT Supreme Court against the builder seeking compensation for breach of statutory warranties under the Building Act 2004 (ACT) (2004 Act) in respect of alleged defects in the construction of the Elara Apartments. In July 2017, liquidators were appointed to the builder and the ACT Supreme Court proceedings were stayed.

4 On 18 August 2017, the appellant lodged a claim (the first claim) with the respondent seeking payment from the Fidelity Fund in respect of losses arising from the alleged defects in the construction of the Elara Apartments. The respondent rejected the first claim on 23 November 2017 on the grounds that the claim was not submitted, and the basis of the claim did not arise, within the time period stipulated for claims to be made under the Fidelity Fund Scheme.

5 Shortly thereafter, on 18 December 2017, the appellant commenced the present proceeding by originating application and statement of claim. The appellant sought declaratory relief to the effect that the respondent was not entitled to reject the first claim on the grounds stated and was required to consider and assess the claim.

6 Between May and June 2018, 66 unit owners purported to assign to the appellant their rights under the fidelity certificates relating to their respective units in the Elara Apartments. On 5 July 2018, the appellant lodged a further claim (the second claim) with the respondent as assignee of the rights of the 66 unit owners. The respondent rejected the second claim on 3 August 2018 on a number of grounds, but a central ground remained that the claim was made out of time. On 3 August 2018, the appellant sent a further claim form to the respondent in respect of the second claim, purporting to make the claim under all 120 fidelity certificates for the Elara Apartments.

7 On 29 August 2018, the appellant amended its originating application and statement of claim so as to seek declaratory relief in respect of the second claim.

8 On 13 February 2019, the primary judge dismissed the appellant’s application for relief, finding that the respondent was entitled to reject both the first and second claims made by the appellant. The primary judge made the following findings:

(a) First, the fidelity certificates issued pursuant to the Fidelity Fund do not provide an independent and standalone source of legal rights. The relevant legal rights and obligations are primarily to be found in the 2004 Act and related legislative instruments, as well as the Trust Deed (at [97]).

(b) Second, the respondent was entitled to reject the first claim on the grounds that:

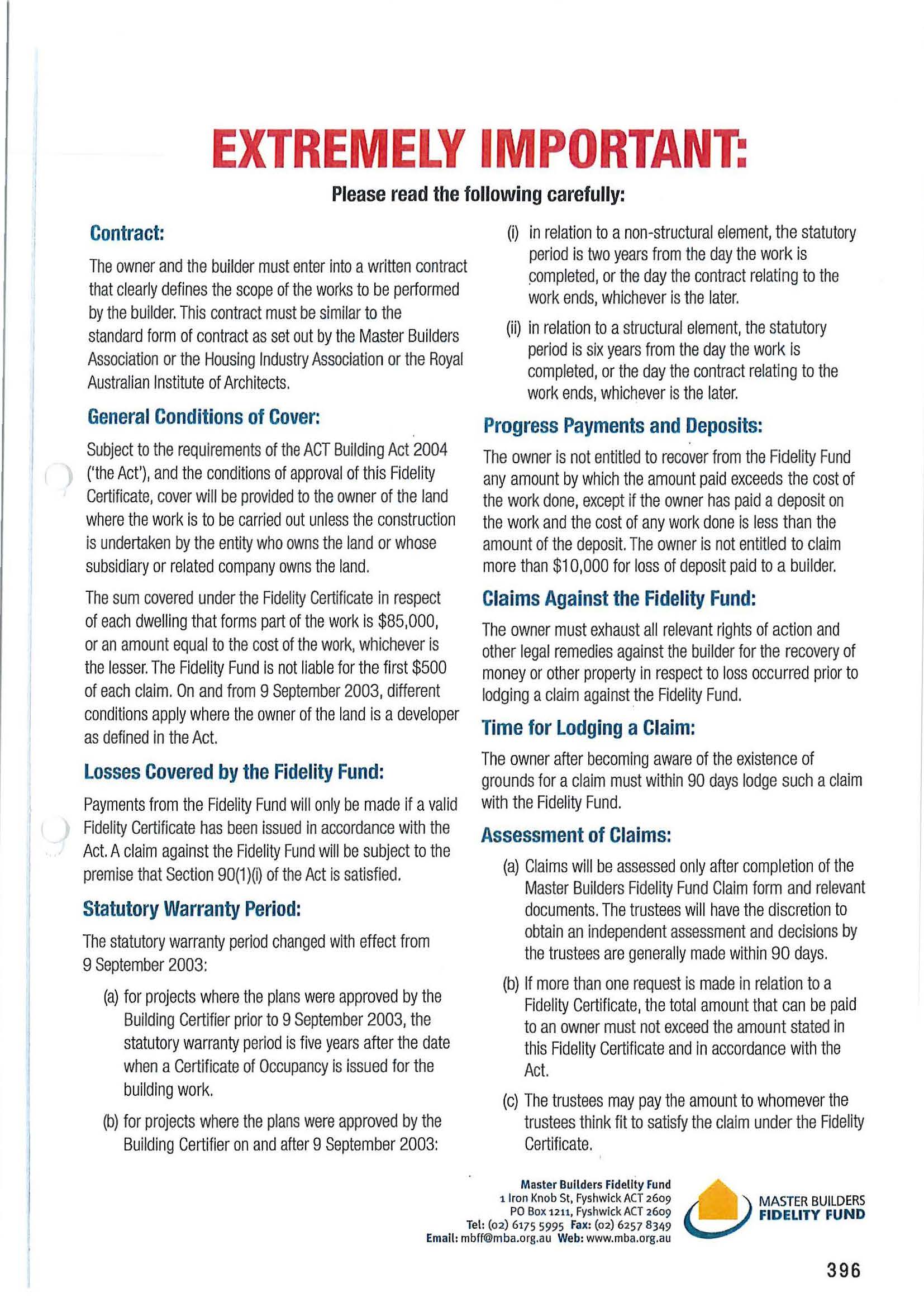

(i) the basis for the claim did not arise within the time period set out in the relevant legislation (at [106]) or within the currency of any of the fidelity certificates for the Elara Apartments (at [111]); and

(ii) the claims were not submitted within the time period set out in the relevant legislation (at [115]) or within the currency of any of the fidelity certificates for the Elara Apartments (at [118]).

(c) Third, in circumstances where the second claim was made even later than the first claim, it necessarily followed that the respondent was entitled to reject the second claim on the same bases upon which the first claim was rejected (at [120]).

(d) Fourth, neither the fidelity certificates, nor the rights arising under the Fidelity Fund, constituted a contract of insurance and, as a consequence, s 54(1) of the Insurance Contracts Act 1984 (Cth) had no application to the applicable terms (at [121]).

9 In reaching the second finding, the primary judge construed the applicable terms of the Fidelity Fund as having the effect that a claim cannot be made against the Fund unless the claimant is unable to recover from the builder under the residential building contract, including in respect of a breach of statutory warranty, because the builder has become insolvent, has disappeared or has died. Further, as the period of cover or benefits afforded under the Fidelity Fund continues until the date that is 5 years from the issue of a certificate of occupancy, the event which causes the inability to recover from the builder, namely the insolvency, death or disappearance of the builder, must itself occur within the five year period of cover (at [108]).

10 Having made the above findings, the primary judge concluded that it was unnecessary to consider two other grounds advanced by the respondent as bases for rejecting the claims lodged by the appellant (at [119]). The second of those grounds was the subject of written and oral argument on the appeal. The respondent did not file a notice of contention to rely on the ground in this appeal. It explained that it did not do so because the appellant had raised the ground in its notice of appeal. Although the issue should have been raised by way of notice of contention, the argument proceeded as if a notice of contention had been filed. By that second ground, the respondent contended that the appellant did not and does not have a right to claim under any of the 120 fidelity certificates issued in respect of the Elara Apartments because the rights attaching to a fidelity certificate accrue to the owner, from time to time, of the property identified on the front of the certificate and, in this case, that was the owner of each unit at the relevant time. The appellant was the legal owner of the common property only and had no capacity to exercise rights which accrued to unit owners.

11 By its notice of appeal filed on 5 March 2019, the appellant contends that the primary judge erred in finding that the respondent was entitled to reject the first and second claims. The appellant principally challenges the second and third of the findings of the primary judge set out above. It does not directly challenge the first and fourth of the findings, although its arguments on the appeal make reference to, respectively, the text of the fidelity certificates and the operation of s 54(1) of the Insurance Contracts Act. The appellant contends that the primary judge should have held that, on the proper construction of the relevant terms and conditions of the Trust Deed, the relevant provisions of Part 6 of the 2004 Act and the terms and conditions of the fidelity certificates:

(a) the fidelity certificates provided cover to the developer’s successors in title in respect of the dwelling to which each fidelity certificate applied against the risk of loss resulting from any of the circumstances described in s 90(1)(f), (g) or (h) of the 2004 Act;

(b) the developer’s successors in title in respect of each dwelling were, respectively:

(i) the owner of the unit and any unit subsidiary shown on the registered units plan as being part of the dwelling; and

(ii) the appellant, as the owner of the common property shown on the registered units plan as being part of the dwelling;

(c) the owner was required to lodge a claim on the Fidelity Fund within 90 days after becoming aware of the existence of grounds for a claim; and

(d) the respondent had a discretion to refuse to consider and assess a claim lodged outside the 90 day period but was not required to do so by the terms of the Trust Deed.

12 The issues raised before the primary judge and on this appeal concern the identification of the terms governing the Fidelity Fund Scheme and the proper construction of those terms. As observed by the primary judge (at [6]), the identification and construction of those terms involves some complexity. Ultimately, we agree with the primary judge that the first and second claims were lodged by the appellant out of time and, as a consequence, the respondent was legally entitled to reject those claims. However, our reasons for reaching that conclusion differ to some extent from those of the primary judge.

13 In explaining our reasons, it is necessary to refer in some detail to the provisions of the Trust Deed governing the Fidelity Fund Scheme, the legislative provisions under which the Fidelity Fund Scheme was established and the legislative history of those provisions and related provisions. In our view, legal rights to payments from the Fidelity Fund are governed by the provisions of the Trust Deed. However, the Trust Deed incorporates by reference certain provisions of the Building Act 1972 (ACT) (1972 Act) (the predecessor to the 2004 Act) and also stipulates that certain matters will be set out in fidelity certificates issued pursuant to the Trust Deed. The broader legislative history and context is relevant in determining the meaning of the provisions of the Trust Deed that are central to this appeal.

14 Given our conclusion that the first and second claims were lodged out of time, it is not necessary to decide the further contention advanced by the respondent that the appellant did not and does not have a right to claim under any of the 120 fidelity certificates issued in respect of the Elara Apartments. In circumstances where that issue was not determined by the primary judge, and its resolution would involve questions of fact as well as law, it is not appropriate that the Court determines the issue on this appeal.

15 It follows that the appeal should be dismissed with costs.

The factual background

16 For the most part, the relevant facts are not in dispute and many were the subject of admissions in the pleadings.

17 The appellant is the owners corporation for Units Plan No. 3115. It was established pursuant to s 38 of the Unit Titles Act 2001 (as in force at the time) upon registration of Units Plan No. 3115 on 7 July 2007, following the completion of the development of the Elara Apartments. The registration of that plan effected the subdivision of the land on which the Elara Apartments were constructed. As the owners corporation for the Elara Apartments, the appellant has the following rights and obligations.

(a) First, upon its establishment, the appellant became the holder of an estate in leasehold of the common property of the apartments pursuant to s 33(3) of the Unit Titles Act 2001 and is the successor in title to the developer in relation to the common property.

(b) Second, pursuant to s 47(1) of the Unit Titles Act 2001 (now replaced by s 19 of the Unit Titles (Management) Act 2011), the appellant holds the common property as agent for the unit owners as tenants in common in shares proportional to their unit entitlement.

(c) Third, pursuant to s 51(3) of the Unit Titles Act 2001 (now replaced by s 24 of the Unit Titles (Management) Act 2011), the appellant is liable to maintain the following areas of the apartments:

(i) the common property;

(ii) load bearing walls, columns, footings, slabs and beams, whether or not they are part of the common property;

(iii) balconies; and

(iv) utility services and utility conduits including structures for the collection, passage and drainage of rainwater, mechanical ventilation, electrical and fire services.

(d) Fourth, pursuant to s 88(3) of the 2004 Act, the appellant succeeded to the rights of the developer in relation to the statutory warranties of the builder.

18 The respondents are the trustees of a trust titled “The Master Builders Fidelity Fund” which was established by trust deed dated 10 September 2002. (In these reasons, we will refer to the group of trustees using the singular “respondent” rather than the plural “respondents”, consistently with the approach adopted by the primary judge and by the appellant in the notice of appeal.) The Fidelity Fund was established following amendments made to the 1972 Act by the Building Amendment Act 2002 (ACT). The amendments (which became Division 6.4 of the 2004 Act) provided for the approval of a building industry fidelity fund scheme governed by a trust deed. The purpose of the scheme was to provide consumers with a similar level of protection as builders warranty insurance. It will be necessary to refer to the terms of the Trust Deed and the enabling legislation in some detail.

19 On or about 15 June 2005, the developer of the Elara Apartments, B & T Developments (ACT) Pty Ltd, entered into a contract with the builder, B & T Constructions (ACT) Pty Ltd, to construct the complex. Pursuant to s 88(1) of the 2004 Act, the contract was taken to include the statutory warranties set out in that section. Construction began in June 2005 and a certificate of occupancy was issued on 25 May 2007.

20 Under s 37(3) of the 2004 Act, before commencing the building work the builder was required to obtain a residential building insurance policy for the work, a certificate issued by an approved insurer stating that the insurer has insured the work under a residential building insurance policy or a fidelity certificate for the work issued by the trustees of a scheme approved under Division 6.4 of the 2004 Act. On 18 May 2005, the builder applied to the Fidelity Fund for fidelity fund coverage of the Elara Apartments. On the same day, the Fidelity Fund issued an invoice in the amount of $105,315, which was subsequently paid by the builder on 16 September 2005, and issued 120 fidelity certificates (numbered sequentially from 44220 to 44339) to the developer in respect of each of the residential units to be constructed for the Elara Apartments.

21 A copy of one of the fidelity certificates was in evidence. The front page of the certificate included the following statements and information:

(a) The certificate was numbered 44339.

(b) The date of issue was 18 May 2005.

(c) The certificate stated that it applied to “one dwelling only” and identified that dwelling as “Block: 4 Section: 34 Unit: 120”.

(d) The certificate stated that it was “issued subject to the requirements of the ACT Building Act 2004 and section 64, and in accordance with the terms and conditions set out in the Master Builders Fidelity Fund Trust Deed”.

(e) The certificate identified the builder as B & T Constructions (ACT) Pty Ltd.

(f) The certificate identified the “Owners/Beneficiaries” as “B & T Developments”.

(g) The certificate was signed on behalf of the Fidelity Fund.

22 At the time the certificate was issued, the construction of the apartments had not commenced and the land on which the construction was to occur was owned by the developer. Thus, the certificates were issued in respect of units that were to be constructed. There was no certificate issued in respect of the common property that would also be constructed as part of the development.

23 At the bottom of the front page of each certificate, the following statement appeared: “Please read the important information overleaf regarding this Certificate”. The appellant relies on the information set out on that page and it is therefore necessary to reproduce it in full:

24 As can be seen, under the heading “General Conditions of Cover”, the certificate stated:

Subject to the requirements of the ACT Building Act 2004 ('the Act'), and the conditions of approval of this Fidelity Certificate, cover will be provided to the owner of the land where the work is to be carried out unless the construction is undertaken by the entity who owns the land or whose subsidiary or related company owns the land.

The sum covered under the Fidelity Certificate in respect of each dwelling that forms part of the work is $85,000, or an amount equal to the cost of the work, whichever is the lesser. The Fidelity Fund is not liable for the first $500 of each claim.

25 Under the heading “Losses Covered by the Fidelity Fund”, the following statement appears:

A claim against the Fidelity Fund will be subject to the premise that Section 90(1)(i) of the Act is satisfied.

26 The appellant places particular reliance on the following statements:

(a) under the heading “Claims Against the Fidelity Fund” (grammatical error in the original):

The owner must exhaust all relevant rights of action and other legal remedies against the builder for the recovery of money or other property in respect to loss occurred prior to lodging a claim against the Fidelity Fund.

(b) and under the heading “Time for Lodging a Claim”:

The owner after becoming aware of the existence of grounds for a claim must within 90 days lodge such a claim with the Fidelity Fund.

27 The appellant says that the effect of those statements is that the beneficiary of the certificate is not entitled to claim against the Fidelity Fund until the beneficiary has exhausted its remedies against the builder and, once those remedies are exhausted, the beneficiary has 90 days in which to submit a claim against the Fidelity Fund. The appellant further contends that the respondent is bound to act in accordance with the statements concerning exhaustion of rights, even though it now accepts that that statement is not a term of the Trust Deed governing the Fidelity Fund Scheme.

28 As noted above, on 25 May 2007 a certificate of occupancy for the Elara Apartments was issued and on 7 July 2007, Units Plan No. 3115 for the Elara Apartments was registered. This resulted in the cancellation of the previous Crown lease for the relevant land and the grant of 125 new Crown leases, comprising 120 Crown leases for the residential units, 4 Crown leases for the commercial units and 1 Crown lease to the appellant for the common property.

29 It is common ground that the period of cover for the fidelity certificates issued in respect of the Elara Apartments ended on the date that is 5 years from the date on which the certificate of occupancy was issued, being 26 May 2012.

30 In this proceeding, the appellant alleges that the residential building work that the builder carried out on the Elara Apartments breached certain of the statutory warranties provided by s 88(2) of the 2004 Act. It alleges that, as a result of those breaches, defects exist in areas of the apartments that the appellant is liable to maintain, being: the common property; load bearing walls, columns, footings, slabs and beams; balconies; and utility services and conduits. It further alleges that, during the period of cover ending on 26 May 2012:

(a) the appellant became liable to repair the defects pursuant to its statutory obligations under s 51(3) of the Unit Titles Act 2001 and, accordingly, suffered a loss resulting from a breach of a statutory warranty within the meaning of s 90(1)(g) of the 2004 Act; and

(b) each unit owner became liable to contribute their proportional share of the cost of repairs through the sinking fund established by the appellant pursuant to s 61 of the Unit Titles Act 2001 and, accordingly, suffered a loss resulting from a breach of a statutory warranty within the meaning of s 90(1)(g) of the 2004 Act.

31 The respondent in its defence does not admit those allegations and says that, even if those liabilities arose, they were not a relevant loss for the purposes of s 90(1)(g) of the 2004 Act.

32 As stated above, the appellant’s application for declaratory relief was dismissed by the primary judge on the basis that the appellant’s claim for payment from the Fidelity Fund was made out of time. Having reached that conclusion, the primary judge did not make any findings in relation to the nature of any losses that had been incurred by the appellant (if any), the time at which any such losses had been incurred and the appellant’s rights to receive payment from the Fidelity Fund in respect of any such losses.

33 On or about 20 May 2013, the appellant began proceedings in the ACT Supreme Court against the builder for breach of statutory warranties.

34 Some four months later, on 19 September 2013, the solicitors for the appellant sent a letter to the Fidelity Fund notifying the Fund of a “possible event that might give rise to a payment from the Fund”. The letter was as follows:

We act for the Owners - Units Plan no. 3115 (the Owners) in relation to this notification of the Master Builders Fidelity Fund (the Fund).

We enclose with this letter:

1. Master Builders Fidelity Fund Scheme Claim Document - your staff were unable to provide us with a copy of the claim form today and so the questions on the claim form have been answered in this document; and

2. a lever arch folder of documents in support.

While we understand the builder, B & T Constructions (ACT) Ply Ltd (the Builder), is not currently dead, disappeared or insolvent, this letter and the enclosed documents are intended to notify the Fund of a possible event that might give rise to a payment from the Fund.

Please note that ACT Supreme Court proceedings were commenced against the Builder by the Owners on 20 May 2013 seeking loss and damage arising from breaches of statutory warranties (under section 88 of the Building Act) by the Builder (Court Proceedings No 185 of 2013).

In the event a settlement agreement is not entered into by the Owners and the Builder, these court proceedings will be pursued to hearing at the end of which it is expected a large judgment will be awarded to the Owners. In the event that the Builder is not be (sic) able to satisfy this judgment, it is expected that the Builder will be wound up and the Owners will seek payment of any outstanding judgment monies from the Fund.

35 It is apparent that, at that time, the appellant believed that it was not entitled to make a claim against the Fidelity Fund until the builder had died, had disappeared or was insolvent, but that the appellant could make a claim once that occurred. As explained below, the appellant was mistaken in both respects.

36 On 25 September 2013, the respondent replied to the appellant’s solicitor, acknowledging receipt of the letter and accompanying documents and stating:

We thank you for the information contained in the folder and the notification of a possible claim against these Fidelity Fund policies. We agree with your statement that a valid claim may not be made on the Fidelity Fund policies referred to as the nominated builder is not deceased, insolvent or has disappeared.

37 It is also apparent that, at that time, the respondent held the same mistaken view as the appellant that no claim could be made against the Fidelity Fund until the builder had died, had disappeared or was insolvent and communicated that view to the appellant. The respondent did not expressly endorse the appellant’s implicit view that a claim could be made in the future once the builder had died, had disappeared or had become insolvent, but nor did it contradict it. No claims were made by the appellant in the proceeding on the basis of the respondent’s communication.

38 On 20 July 2017, liquidators were appointed to the builder, after which the ACT Supreme Court proceeding was stayed.

39 On 18 August 2017, the appellant lodged a formal claim with the respondent (referred to earlier as the first claim). In a covering letter to the claim form, the solicitors for the appellant stated that the appellant had incurred losses by reason of the builder’s breach of statutory warranties because of the appellant’s liability to maintain the common property, and that the losses had occurred during the period of cover for the fidelity certificates. The letter also referred to the statements appearing on the back page of the fidelity certificates (extracted above) and stated:

The point in time at which the Owners Corporation must be taken to have exhausted all relevant rights of action for recovery of money from the Builder to pay for the cost of rectifying the common property is 20 July 2017, being the date on which the Builder went into liquidation. That point marks the date when the Owners Corporation became aware of the existence of grounds for a claim against the Fidelity Fund and the commencement of the 90 day period to lodge the claim with the Fidelity Fund.

40 In a claim form attached to the letter, the appellant circled “yes” opposite the question whether the claim was under the statutory warranty, and circled “insolvency” and “defective construction work” in response to a request to circle the most appropriate circumstance and reason for the claim.

41 On 23 November 2017, the respondent’s solicitor wrote to the appellant’s solicitor rejecting the first claim. The letter stated:

A preliminary investigation of the claim and supporting documentation indicates that it was not submitted, nor did the basis of the claim arise, within the time periods set out within the relevant legislation, or during the currency of any of the Fidelity Certificates issued for these units.

42 On 18 December 2017, the appellant commenced this proceeding.

43 As we have said, between May and June 2018, owners of 66 units at the Elara Apartments purported to assign to the appellant their rights under the fidelity certificates relating to their respective units.

44 On 5 July 2018, the appellant, through its solicitor, lodged a second claim with the respondent as assignee of the rights under the fidelity certificates held by the 66 unit owners (referred to earlier as the second claim).

45 On 3 August 2018, the respondent’s solicitor wrote to the appellant’s solicitor rejecting the second claim. The letter stated a number of procedural and substantive reasons for rejecting the claim. Relevantly for present purposes, the reasons included that:

(a) the claim was made out of time because the fidelity certificates held by the unit owners had expired several years before any claimable event had occurred; and

(b) the claim was made more than 90 days after the event which purportedly gave rise to it, namely the liquidation of the builder on 20 July 2017, contrary to the requirement in s 90(1)(i) of the 2004 Act.

46 On 3 August 2018, the appellant’s solicitor emailed to the respondent’s solicitor a claim form executed by the appellant. The executed claim form was said to be made under all 120 fidelity certificates for the Elara Apartments and not just the certificates in respect of the 66 units whose owners had purported to assign rights to the appellant. In a similar manner to the first claim form, the appellant circled “yes” opposite the question whether the claim was under the statutory warranty, and circled “insolvency” and “defective construction work” in response to a request to circle the most appropriate circumstance and reason for the claim.

Legislative framework under which the Fidelity Fund was established

47 As noted earlier, the legislative framework under which the Fidelity Fund was established was enacted by the Building Amendment Act 2002, which amended the 1972 Act by introducing a new Division 5A into Part 5A of that Act.

Before the 2002 amendments

48 Prior to the 2002 amendments, Part 5A of the 1972 Act contained provisions dealing with statutory warranties (s 58C) and residential building work insurance (s 58E).

49 Section 58C(1) implied certain warranties from the builder into every contract for the sale of a residential building and every contract to carry out residential building work (being a contract to which the builder is a party). Section 58C(2) stipulated that each of the owner’s successors in title succeeds to the rights of the owner in respect of the statutory warranties. In s 58C(4), the term “owner” was defined as, in the case of a contract of sale, the person to whom title in the land on which the building was built is transferred under the contract and, in the case of a building contract, the owner of the land on which the building work is to be carried out. Section 58C(3) stipulated that the statutory warranties expired at the end of the prescribed period after the date on which a certificate of occupancy is issued for the building (which, under reg 19 of the Building Regulations 1972 (ACT), was five years).

50 Under s 34(1) of the 1972 Act, a builder was required to take out insurance in respect of residential building work. Section 58E regulated the content of such insurance policies. Section 58E(1) provided:

An insurance policy issued in respect of residential building work complies with this section if-

(a) it is issued by an authorised insurer; and

(b) it provides for a total amount of insurance cover of at least the prescribed amount, or an amount equal to the cost of the work, whichever is less, in respect of each dwelling that forms part of the work; and

(c) if the builder is not the owner of the land where the work is to be carried out - it insures the owner and the owner's successors in title for the period beginning on the date on which the certifier in relation to the work receives a notification under s 37A(l) or (2) in relation to the builder and ending the prescribed period after the date on which a certificate of occupancy is issued for the work; and

(d) if the builder is the owner of the land where the work is to be carried out - insures the builder’s successors in title for the period beginning on the date on which the title in the land is transferred to another person and ending the prescribed period after the date on which a certificate of occupancy is issued for the work; and

(e) the whole of the premium payable in relation to the respective period has been paid; and

(f) it insures the owner (if the builder is not the owner) and the owner’s successors in title against the risk of being unable to enforce or recover under the contract pursuant to which the work has been, is being or is to be carried out because of the insolvency, disappearance or death of the builder; and

(g) it insures the owner (if the builder is not the owner) and the owner's successors in title against the risk of loss resulting from a breach of a statutory warranty; and

(h) it insures the owner (if the owner is not the builder) and the owner's successors in title against the risk of loss resulting, by virtue of the builder's negligence, from subsidence of the land; and

(j) it provides that a claim under it may only be made within the prescribed period (or some specified longer period) after the claimant becomes aware of the existence of grounds for the claim; and

(k) the form of the policy has been approved in writing by the building controller.

(There was no paragraph (i) in the section.)

51 The prescribed period referred to in s 58E(1)(c) and (d) was five years (reg 20 of the Building Regulations 1972). The prescribed period referred to in s 58E(1)(j) was 90 days.

52 It is also relevant to note the terms of s 58E(7) which provided as follows:

(7) Where–

(a) a builder is not the owner of the land on which the builder is carrying out residential building work; and

(b) as a result of becoming insolvent, the builder fails to complete the work; and

(c) the owner has paid the builder part or all of the cost of the work; and

(d) the work is insured under a residential building insurance policy;

the owner is not entitled to recover from the insurer any amount by which the amount paid exceeds the cost of the work done except, where the owner has paid a deposit on the work and the cost of any work done is less than the amount of the deposit, the owner may recover from the insurer–

(e) an amount equal to the amount of the deposit less the cost of any work done; or

(f) the prescribed amount less the cost of any work done;

whichever is less.

53 It may be seen that s 58E(7) contemplated that an owner may seek to recover from an insurer under a residential building insurance policy losses resulting from the builder failing to complete the work because of insolvency, and placed conditions on the amount that could be claimed. The subsection presupposes that a claim might be made against an insurer by reason of the insolvency of the builder, regardless of whether there was a breach of statutory warranty or negligence on the part of the builder.

The Building Amendment Act 2002

54 The background to the 2002 amendments was explained in the Explanatory Memorandum to the Building Amendment Bill 2002 as follows:

The Building Amendment Bill 2002 (the Bill) amends the Building Act 1972 ("the Act").

Part 5A of the Act (Residential building - statutory warranties and insurance) sets out a system of consumer protection for the owners of new homes and significant changes to homes. It requires builders of new homes or significant additions to existing homes to take out residential building work insurance against which owners can claim if the building work is not completed or there are defects in the work. The insurance protects the owner during construction and for a period of five years from completion. Part 3 of the Act (Building work) includes provisions designed to ensure that the insurance is taken out before work begins.

It has recently become difficult for builders to obtain this insurance. The brokers for one of the two approved insurance schemes were unable to find enough reinsurance to satisfy their insurance company. On 10 April 2002 they announced that they were no longer able to provide residential building work insurance. This has affected more than half of the ACT's house builders and their customers. Further insurance may become available on a commercial basis but the market for insurance is currently volatile. The Bill therefore amends the Act by inserting new provisions in Part 5A that allow the approval, as an alternative to insurance, of a fidelity fund scheme that will provide similar consumer protection.

55 In the Presentation Speech to the 2002 amendments, the then Minister for Planning explained that the amendments were in response to what he described as “a potential crisis in the ACT building industry caused by the withdrawal of [an] insurance broker… from the market for residential building work insurance”. The Minister noted that the 1972 Act required builders to have insurance before they could begin work and that this “insurance protected consumers if the builder goes bankrupt, dies, or for some other reason fails to complete construction and cannot be found” and that “[o]nce construction is complete, homebuyers receive a further five year warranty against construction faults”. The Minister explained that the ACT Government’s objective was to provide choices in the marketplace by establishing a fidelity fund scheme. The Minister stated that the Government was not underwriting the scheme. He further explained that the amendments introduced a new approach to building warranty, and because “it is not an insurance scheme”, a range of safeguards had to be put in place because safeguards under an insurance-based scheme, including the protection provided by the Commonwealth Insurance Act 1973, would not apply.

56 Relevantly, with effect on 17 May 2002, the Building Amendment Act 2002 amended s 34 of the 1972 Act to permit a builder to obtain, in respect of a residential building project, fidelity certificates under an approved fidelity fund scheme instead of insurance. Substantive amendments were made to Part 5A of the 1972 Act to insert additional definitions and divisions as follows:

(a) Division 5A.1 – General – which contained the revised definitional sections;

(b) Division 5A.2 – Statutory warranties – which contained the pre-existing s 58C;

(c) Division 5A.3 – Residential building insurance – which contained the pre-existing ss 58D to 58G;

(d) Division 5A.4 – Approved fidelity fund schemes – which contained provisions empowering the Minister to approve a fidelity fund scheme, to determine the approval criteria for such schemes, to determine prudential standards that must be complied with by an approved scheme, to require the trustees of an approved scheme to comply with the applicable prudential standards and related Ministerial powers;

(e) Division 5A.5 – Auditors and actuaries of approved schemes – which provided for the appointment of an auditor and actuary for an approved fidelity fund scheme; and

(f) Division 5A.6 – Transitional provisions – which enabled regulations to be made addressing transitional matters.

57 Within Division 5A.4, s 58H empowered the Minister to approve a fidelity fund scheme provided the scheme complied with the approval criteria. By s 58K, the Minister was also empowered to determine the approval criteria. Section 58K also stipulated that the approval criteria must, amongst other things, include requirements in relation to the building work for which a fidelity certificate may be issued under a fidelity scheme and the people who can make claims under a fidelity certificate.

58 On 23 May 2002, the Minister signed a determination setting out the approval criteria for a fidelity fund scheme titled Building (Approval criteria) Determination 2002 (being disallowable instrument DI 2002-49) (Approval Criteria), which remains current. Clause 4 set out matters which must be included in a trust deed in order for it to be approved. Relevantly, clause 4 provided:

Fidelity fund trust deed

4. The trust deed must:

(a) require the trustees to assess each application for a fidelity certificate;

(b) allow the trustees to require that, in certain circumstances, a contribution be made to the fidelity fund scheme including for the issue of fidelity certificate;

(c) set out the terms and form of the fidelity certificate to be issued by the trustees;

(d) provide for the issue of a fidelity certificate by the trustees, including a requirement that each fidelity certificate that the trustees issue:

(1) is only issued for residential building work in the ACT that is undertaken by a licensee or a holder of an owner-builder's licence;

(2) is only issued after the full contribution that the trustees require to be paid to the fidelity fund scheme for the issue of the fidelity certificate has been paid;

(3) must state the amount that the owner can request from the trustees under clause 4(f), being at least the amount that is the minimum amount of insurance cover that is required to provided by an insurance policy under section 58E(l)(b) of the Act; and

(4) must state that each of the following matters is at the discretion of the trustees when a request is made by an owner:

(i) whether any payment is to be paid to the owner from the assets of the fidelity fund scheme;

(ii) the amount of any such payment to be paid to the owner; and

(iii) the terms and conditions on which any payment to the owner is to be paid by the trustees from the assets of the fidelity fund scheme;

…

(f) only allow the person (owner) described in column 2 of the table set out below to make a request (request):

(1) in the circumstances set out in column 1 of the table set out below; and

(2) for the period set out in column 3 of the table set out below,

that the trustees pay to the owner an amount, up to the amount stated on the owner's fidelity certificate, out of the assets of the fidelity fund scheme for a part or the whole of any loss stated in clause 4(i) that the owner has incurred:

Column 1 Circumstance | Column 2 Person covered by the fidelity certificate | Column 3 Period for which the owner is covered |

The owner* is not the builder | The owner* and the owner’s* successors in title of the land on which the residential building work is to be, is being or has been carried out | The period that: • begins on the date on which the certifier in relation to the residential building work receives a notification under section 37A(1) or (2) of the Act in relation to the builder who will carry out the residential building work on the land; and • ends at the expiration of the specified period |

The owner* is the builder | The owner’s* successors in title of the land on which the residential building work is to be, is being or has been carried out | The period that: • begins on the date on which the residential building work is to be, is being or has been carried out is transferred to another person; and • ends at the expiration of the specified period. |

*Note: the word "owner" where used in this table has the same meaning as in the Act.

(g) require that only the amount stated on a fidelity certificate under clause 4(d)(3) can be requested by the owner;

(h) require that, if more than one request is made in relation to a fidelity certificate, the total amount that can be paid to an owner must not exceed the amount that is stated on the fidelity certificate;

(i) state that the types of losses in relation to which a request may be made are only those losses which would be recoverable under an insurance policy under sections 58E(l)(f), (g) and (h) of the Act;

(j) require that a request be made within the period that is the prescribed period for the purpose of section 58E(l)(j) of the Act after the owner becomes aware of the existence of the grounds for making the request;

(k) state how an owner can make a request under a fidelity certificate;

(l) subject to clause 4(m), state how a request will be handled by the trustees;

(m) subject to clause 4(t), require the trustees to consider a request from an owner and determine, in their discretion:

(1) whether the trustees will make a payment from the assets of the fidelity fund scheme in respect of the request;

(2) the amount of any such payment; and

(3) the terms and conditions on which the trustees will make the payment, such terms and conditions to include a right for the trustees to take whatever action they consider appropriate in the name of the owner against the builder to recover from the builder any amount paid by the trustees to the owner;

…

(t) prohibit the trustees from refusing to pay an owner under the fidelity certificate on the grounds that the fidelity certificate was obtained by misrepresentation or non-disclosure by the builder;

…

59 The “specified period” referred to in the table at clause 4(f) is defined in clause 1 of the Approval Criteria as, in relation to residential building work, the period prescribed for the purposes of ss 58E(1)(c) and (d) of 1972 Act commencing on the date on which a certificate of occupancy is issued for the building work. As noted above, that prescribed period was 5 years.

60 While the primary purpose of the Approval Criteria was to state the criteria to be applied by the Minister in making a determination whether to approve a fidelity fund, various clauses of the Approval Criteria are expressed as having operative effect. For example, clauses 9 to 11 regulate the persons who may be appointed as trustees of a fidelity fund, and clause 14 imposes prudential obligations on the trustees. As seen below, those operative clauses have been incorporated by reference into the Trust Deed for the Fidelity Fund.

61 Under s 58O of the 1972 Act, the Minister was empowered to determine prudential standards that must be complied with by an approved scheme. Under s 58P, it was an offence for the trustees to fail to ensure that a scheme complied with the prudential standards.

62 On 23 May 2002, the Minister signed a determination setting out the prudential standards applying to an approved fidelity fund scheme titled Building (Prudential Standards) Determination 2002 – Disallowable Instrument DI 2002-48 (2002 Prudential Standards). The 2002 Determination was revoked and replaced in 2005 by the Building (Prudential Standards) Determination 2005 – Disallowable Instrument DI 2005-250 (2005 Prudential Standards). The 2005 Prudential Standards were made by the Minister under s 103 of the 2004 Act.

The 2002 Renumbering

63 With effect from 29 May 2002, the provisions of the 1972 Act were re-numbered and republished as Republication No 7. Part 5A became Part 6, with consequential renumbering of the Divisions within the Part. Other relevant changes were:

(a) s 58C (statutory warranties) became s 62;

(b) s 58E (residential building work insurance) became s 64;

(c) s 58H (approval of fidelity fund schemes) became s 67; and

(d) s 58K (approval criteria for fidelity fund schemes) became s 70.

64 Two minor changes were made to the language of s 64(1) from the previous s 58E(1) which is reproduced above: the phrase “the date on which” became “the date when” and the omission of paragraph (i) was reversed. As discussed below, s 64 is incorporated by reference into the Trust Deed for the Master Builders Fidelity Fund. It is therefore helpful to reproduce s 64(1) in full:

An insurance policy issued in relation to residential building work complies with this section if-

(a) it is issued by an authorised insurer; and

(b) it provides for a total amount of insurance cover of at least the prescribed amount, or an amount equal to the cost of the work, whichever is less, in respect of each dwelling that forms part of the work; and

(c) if the builder is not the owner of the land where the work is to be carried out - it insures the owner and the owner’s successors in title for the period beginning on the date when the certifier in relation to the work receives a notification under s 37A(l) or (2) in relation to the builder and ending the prescribed period after the date when a certificate of occupancy is issued for the work; and

(d) if the builder is the owner of the land where the work is to be carried out – it insures the builder’s successors in title for the period beginning on the date when the title in the land is transferred to another person and ending the prescribed period after the date when a certificate of occupancy is issued for the work; and

(e) the whole of the premium payable in relation to the respective period has been paid; and

(f) it insures the owner (if the builder is not the owner) and the owner’s successors in title against the risk of being unable to enforce or recover under the contract under which the work has been, is being or is to be carried out because of the insolvency, disappearance or death of the builder; and

(g) it insures the owner (if the builder is not the owner) and the owner’s successors in title against the risk of loss resulting from a breach of a statutory warranty; and

(h) it insures the owner (if the owner is not the builder) and the owner’s successors in title against the risk of loss resulting, by virtue of the builder’s negligence from the subsidence of the land; and

(i) it provides that a claim under it may only be made within the prescribed period (or some specified longer period) after the claimant becomes aware of the existence of grounds for the claim; and

(j) the form of the policy has been approved in writing by the building controller.

Approval of the Master Builders Fidelity Fund Scheme

65 The Master Builders Fidelity Fund Scheme was approved by the Minister on 21 June 2002 under what by then had become Part 6 of the 1972 Act. It commenced to operate immediately under the provisions of an unexecuted draft trust deed, which was eventually executed on 10 September 2002. The relevant terms of the Trust Deed are set out below. The terms refer to, and incorporate by reference, provisions within Part 6 of the 1972 Act.

The Building (Residential Building Warranty) Amendment Act 2003

66 Relevantly, two amendments were made to the 1972 Act by the Building (Residential Building Warranty) Amendment Act 2003 with effect from 9 September 2003.

67 First, an amendment was made to the prescribed period for calculating the length of the statutory warranties (in s 62(3)) and for calculating the required period of insurance cover for residential building insurance (in s 64(1)(c)). Those periods were changed such that the end date was calculated by reference to the ‘completion day’ rather than the date the certificate of occupancy was issued. The completion day was defined to be the day the work is completed, or the day the contract for the work ends, whichever is later (save that the work is taken to be completed no later than the day a certificate of occupancy is issued). The Building Regulations 1972 were also amended so that the prescribed period in reg 19 (relating to the statutory warranties) was 6 years after the ‘completion day’ in relation to structural elements, and 2 years after the ‘completion day’ in relation to non-structural elements, instead of 5 years as was the case previously. As a consequence, after the 2003 amendments, the period within which the statutory warranties operated, and the required period of cover under residential building insurance and the fidelity fund, were no longer in alignment.

68 Second, a new subsection (1B) was added to s 64 as follows:

To remove any doubt, an insurance policy issued in relation to residential building work may exclude claims other than those in circumstances in which the builder is insolvent, dead or has disappeared.

69 Thus, residential building insurance policies could be issued on terms that excluded claims except where the builder was insolvent or had died or had disappeared.

The Building Act 2004

70 On 1 September 2004, the 1972 Act was repealed and replaced by the 2004 Act.

71 Relevantly, ss 62 and 64 of the 1972 Act, which dealt respectively with statutory warranties and residential building work insurance, were replaced by ss 88 and 90 of the 2004 Act. The new provisions were in materially the same form as the original provisions, save that (relevantly) s 64(1B) (reproduced above) became s 90(3) and s 64(7) became s 93. However, there was one material change to s 90 other than renumbering the provisions, which reversed the 2003 amendment to the date for calculating the end of the prescribed period of residential building insurance cover. That date returned to the date the certificate of occupancy was issued, rather than the ‘completion day’.

72 The provisions relating to the approval of fidelity fund schemes were replaced by ss 96 to 110 within Division 6.4 without any material change to their terms. Section 166 of the 2004 Act provided that an approved scheme under the 1972 Act was taken to be an approved scheme for the 2004 Act. Because of the operation of ss 82 and 88 of the Legislation Act 2001 (ACT), s 166 continued to operate even though it no longer appeared in republications of the 2004 Act.

The Trust Deed for the Fidelity Fund

73 As noted above, the Master Builders Fidelity Fund Scheme commenced immediately after its approval by the Minister on 21 June 2002. The Fidelity Fund is a trust constituted by a Trust Deed which was executed on 10 September 2002. The Approval Criteria require that the trustees of a fidelity fund must be natural persons and that there must be a minimum of 5 trustees. At the time of its creation, the trustees of the Fidelity Fund were the 5 individuals who signed the Trust Deed. The evidence did not identify the current trustees. In various places, the Trust Deed refers to the “trustees”, the “board of trustees” or simply the “board”. These expressions appear to be synonymous and to be references to the trustees acting collectively.

74 The Fidelity Fund was approved by the Minister exercising powers under the 1972 Act and the Trust Deed refers to that Act. While the 1972 Act was subsequently replaced by the 2004 Act, with consequential renumbering of relevant provisions, no amendments were made to the Trust Deed to bring it up to date with the amended law. A question arises whether references in the Trust Deed to provisions of the 1972 Act are, expressly or by implication, intended to have an ambulatory operation such that they are to be construed as referring to such provisions as amended or replaced from time to time, specifically as re-enacted (and re-numbered) in the 2004 Act.

75 In the appeal, the appellant adopted the approach of giving the relevant clauses of the Trust Deed an ambulatory operation, construing references to the provisions of the 1972 Act as references to the equivalent provisions in the 2004 Act. The respondent adopted the contrary approach. However, on the issues to be determined in this appeal, nothing appears to turn on this question because the relevant provisions of the 1972 Act which have been repealed were re-enacted in materially the same form in the 2004 Act. Therefore, the Trust Deed will have the same effect whether it is taken to incorporate the former or the latter provisions.

76 Without needing to decide the question, we favour the view that the various references in the Trust Deed to the 1972 Act and instruments created pursuant to that Act should be construed, by implication, as references to that Act and instruments as amended or replaced from time to time. Such an implication gives efficacy to the Trust Deed in circumstances where the Fidelity Fund was created to give effect to a statutory purpose and where the terms of the Trust Deed require adherence to legislative and regulatory requirements created for that statutory purpose. The statutory purpose could be impeded or frustrated if the Trust Deed were not construed so as to require adherence to the applicable legislative and regulatory requirements as amended from time to time. An analogy can also be drawn with the modern approach to the construction of a company’s constitution which recognises that constitutions “are instruments of company governance intended to endure and to be capable of operating with flexibility in changing circumstances”: Re GIGA Investments Pty Ltd (in admin) (1995) 17 ACSR 472 at 476 per Branson J, (also reported as Re Ferguson (1995) 58 FCR 106 at 111), referred to with approval in Lion Nathan Australia Pty Ltd v Coopers Brewery Ltd at first instance [2005] FCA 1812; 223 ALR 560 at [77] per Finn J and on appeal [2006] FCAFC 144; 156 FCR 1 at [111] per Kenny J and [244] per Lander J.

77 Nevertheless, it would seem desirable, having regard to the statutory purpose served by the Fidelity Fund, for the trustees to keep abreast of amendments to the legislative framework governing the Fidelity Fund and make amendments to the Trust Deed as required from time to time. Such amendments are contemplated by s 101 of the 2004 Act and clause 68 of the Trust Deed. The latter permits the trustees, with the written consent of the Minister, to vary the provisions of the deed (unless the Minister has specified an amendment that does not require Ministerial approval).

78 Turning to the provisions of the Trust Deed, it is unfortunate that the Deed is riddled with spelling and grammatical errors. In the main, the errors do not obscure the meaning of the clauses. However, as discussed below, there are some aspects of the clauses that are not entirely clear. Further, and as foreshadowed above, the dispute between the parties appears to have arisen, at least in part, by reason of an erroneous statement in the fidelity certificates issued by the respondent pursuant to the Trust Deed to the effect that the beneficiary of the certificate is not entitled to claim against the Fidelity Fund until the beneficiary has exhausted its remedies against the builder.

79 In the preamble to the Trust Deed, clause D states that “This Deed is made with the intent that the benefits and obligations thereof shall ensure (sic) to those builders and members of the public who fall subject to the terms of the trust”.

80 The objects of the Fidelity Fund are set out in clause 2 as follows:

OBJECTS

2. The trustees of the approved scheme must ensure that the approved scheme is maintained solely for the following purposes:

(a) the provision of a fidelity certificate to an owner in accordance with the Act and the trust deed;

(b) the making of a discretionary payment of an amount to an owner pursuant to a fidelity certificate in accordance with the Act and the trust deed;

(c) any other purpose that the Minister may in writing determine from time to time.

81 The reference to the making of “discretionary payments” should be noted. As is reinforced in various parts of the Trust Deed, the decision to make payments to an owner holding a fidelity certificate lies at the discretion of the trustees. That is the key difference between the cover or benefits afforded by the issue of a fidelity certificate and cover afforded by a residential building insurance policy. It is also the reason that the primary judge concluded that the cover or benefits afforded by the issue of a fidelity certificate is not insurance (at [121]).

82 Clause 4 deals with the establishment of the Fidelity Fund. It provides that “The Fidelity Fund scheme is established pursuant to the Building Act 1972 (ACT) and shall be administered pursuant to the disallowable instruments under Pt 6 of the Act”. As observed by the primary judge, the reference to “disallowable instruments” includes relevant parts of the Approval Criteria and the 2005 Prudential Standards.

83 Clause 8 deals with the administration of the Fidelity Fund. It provides that “The trustees of the fund shall at all times administer the fund in accordance with the disallowable instruments created pursuant to Pt 6 of the Act”. Again, as observed by the primary judge, this includes relevant parts of the Approval Criteria and the 2005 Prudential Standards.

84 Clause 9 deals with payments out of the Fidelity Fund. It prescribes the categories of payments that may be made from the Fidelity Fund, which includes “the amount of all claims, including costs, allowed by the board or established against the Fidelity Fund”.

85 Clauses 11, 12 and 13 appear under the heading “Legal Claims Against the Fund”. They provide as follows:

LEGAL CLAIMS AGAINST THE FUND

11. A person may not commence proceedings under this deed against the fund without leave of the board unless:

(a) the board has disallowed that person’s claim; and

(b) the certificate holder has exhausted all relevant rights of action and other legal remedies for the recovery of money or other property in respect of which a pecuniary loss has occurred, being rights and remedies that are available against the builder in relation to whom the claim arose and all other persons who are liable in respect of the loss suffered by the certificate holder, other than any rights or remedies that the claimant may have under other sections of this deed.

12. A person who have (sic) been refused leave by the trustees of the fund under the above sub-section may apply to the Court for leave to commence proceedings against the fund and the Court may make such orders in the matter as they (sic) see fit.

13 The trustees of the fund, after disallowing (either wholly or partly) a claim for compensation from the Fidelity Fund must serve notice and reasons thereof for the disallowance in the prescribed form to the certificate holder.

86 Clause 58 deals with the terms and form of fidelity certificates. The expression “Fidelity certificate” is defined in the Trust Deed to mean “a certificate issued for the building work by the trustees of the Fidelity Fund”. Clause 58 provides as follows (the numerous grammatical errors are in the original):

TERMS AND FORM OF FIDELITY CERTIFICATES

58 (a) The issue of a fidelity certificate by the trustees may be issued on the condition that each fidelity certificate:

(1) is only issued for residential work in the ACT that is undertaken by a Fidelity Fund approved licensed builder;

(2) is only issued after the full contribution that the trustees required to be paid to the Fidelity Fund scheme for the issue of the fidelity certificate;

(3) must state the amount that the owner can request from the trustees, being at least the amount that is the minimum amount of cover that is required to be provided by an insurance policy under the Act; and

(4) must state that each of the following matters is at the discretion of the trustees when a request is made by an owner:

(i) whether any payment is to be paid to the owner from the assets of the Fidelity Fund scheme;

(ii) the amount of any such payment to be paid to the owner; and

(iii) the terms and conditions on which any payment to the owner is to be paid by the trustees from the assets of the Fidelity Fund;

(iv) a claim properly submitted in accordance with Clause 64 may be subject to an assessment by a properly qualified expert appointed by the trustees,

(v) the excess payable by the owner before any payment is made from the assets of the Fidelity Fund.

(b) require the trustees to determine the amount of a contribution to be paid to the Fidelity Fund scheme for the issue of a fidelity certificate including a requirement that the trustees consider the prudential standards and the advice of the actuary for the Fidelity Fund scheme before they determine the amount of the contribution.

87 Again, the discretionary nature of the payments that may be made pursuant to a fidelity certificate is emphasised in clause 58(a)(4).

88 Clauses 60 to 64 stipulate the conditions on which claims may be made against the Fidelity Fund and payments may be made from the Fidelity Fund in satisfaction of claims and the types of losses in respect of which payments may be made. Those clauses are as follows (again, the numerous spelling and grammatical errors are in the original):

WARRANTEE AND LOSSES COVERED BY THE FIDELITY FUND

60. (a) Payments out of the Fidelity Fund will only be made pursuant to a validly issued fidelity certificate and in accordance with sections 62 and 64 of the Act:

(b) For the purposes of assessment of a claim made under a validly issued fidelity certificate, a claim made pursuant to 62 of the Act will be made subject to the premise that section 64(1)(i) of the Act is satisfied.

61. The trustees may pay to the owner an amount, up to the maximum amount stated on the owner's fidelity certificate, out of the assets of the Fidelity Fund scheme for a part or the whole or any loss that the owner has incurred and;

(a) requires that only the amount stated on the fidelity certificate can be requested by the owner;

(b) requires that, if more than one request is made in relation to a fidelity certificate, the total amount that can be paid to an owner must not exceed the amount that is stated on the fidelity certificate;

(c) state that the types of losses in relation to which a request may be made are only those losses which would be recoverable under an insurance policy under sections 64(1)(f), (g) and (h) of the Act;

(d) require that a request be made within the period that is the prescribed period for the purpose of section 64(1)(j) of the Act after the owner becomes aware of the existence of the grounds for making the request.

62. The trustees may pay the amount to whomever the trustees think fit to satisfy the claim under this fidelity certificate.

63. The trustees are prohibited from refusing to pay an owner under the fidelity certificate on the grounds that the fidelity certificate was obtained by a misrepresentation or non disclosure by the builder.

CLAIMS

64 A claim by a Fidelity Certificate Holder must be;

(a) made in writing within 90 days of becoming aware of a possible event that may cause a payment from the Fidelity Fund.

(b) in accordance with a Fidelity Fund claim form.

89 The grammar of clause 61 is particularly problematic. At first glance, it might be thought that the subject of the verbs in paragraphs (a) to (d) of clause 61 is intended to be the trustees. If that were the correct construction, the clause would permit or authorise the trustees to limit payments in accordance with the conditions set out in paragraphs (a) to (d) (the introductory words to the clause are “the trustees may”), but the clause would not mandate those limitations. However, having regard to the relevant contextual material that explains the genesis of the Trust Deed (as per Codelfa Construction Pty Ltd v State Rail Authority of NSW (1982) 149 CLR 337 at 352 per Mason J), it is apparent that clause 61 was inserted in the Trust Deed in order to comply with the requirements of paragraphs (g) to (j) of clause 4 of the Approval Criteria. Clause 4 stipulates mandatory provisions of the Trust Deed. Understood in that context, in our view the intended meaning of paragraphs (a) to (d) of clause 61 is that they are mandatory conditions of the cover or benefits afforded by the Fidelity Fund.

90 It was common ground before the primary judge that the reference in clause 61(d) to s 64(1)(j) of the Act is an error and that the correct reference is to s 64(1)(i) of the Act. As noted earlier, s 58K(1) of the 1972 Act omitted paragraph (i), but that omission was reversed when the 1972 Act was re-numbered in May 2002.

91 The effect of clauses 61 and 62 of the Trust Deed is to incorporate by reference into the Trust Deed the terms of s 62 (which governs statutory warranties) and s 64 (which governs residential building insurance) of the 1972 Act, and which have since been replaced (in materially the same form) by ss 88 and 90 of the 2004 Act.

92 Significantly, the limitation on residential building insurance in s 64(1)(i) of the 1972 Act (now s 90(1)(i) of the 2004 Act) is incorporated three times into the Trust Deed. As noted earlier, s 64(1)(i) stipulated that a complying residential building insurance policy must contain a provision to the effect that a claim under it may only be made within the prescribed period after the claimant becomes aware of the existence of grounds for the claim. The prescribed period is and was at all relevant times 90 days. That condition is incorporated by clauses 60(b), 61(d) and 64 of the Trust Deed.

Issues arising on the appeal

93 The issues that arise on the appeal can be reduced to the following questions:

(a) First, in respect of what events does the Fidelity Fund Scheme provide (discretionary) cover or benefits and, specifically, did such events arise in respect of the Elara Apartments during the period of cover afforded by the fidelity certificates issued in respect of the Elara Apartments?

(b) Second, is there a time period within which the holder of a fidelity certificate must make a claim against the Fidelity Fund and, if so, did the appellant make a claim within time? A related question is whether the trustees have the discretion to waive any applicable time period.

(c) Third, did the appellant have the right to make a claim against the Fidelity Fund in circumstances where fidelity certificates were ostensibly issued in respect of the 120 units at the Elara Apartments but not in respect of the common property?

94 Our short answers to those questions are as follows:

(a) The Fidelity Fund Scheme provides (discretionary) cover or benefits in respect of the occurrence of each of the events referred to in paragraphs (f), (g) and (h) of s 64(1) of the 1972 Act, now found in s 90(1) of the 2004 Act, which occur within the period of cover afforded by the Scheme, being a period ending on the date 5 years after the issue of a certificate of occupancy for the building concerned. In the present case, the period of cover for the Elara Apartments ended on 26 May 2012. The appellant alleges that, during that period of cover, losses were incurred by reason of a breach of statutory warranty by the builder. If the allegation were correct, that is an event in respect of which the Fidelity Fund Scheme provides cover or benefits. However, that allegation has not been admitted by the respondent and no factual finding has been made in relation to the allegation. Accordingly, we are unable to determine on this appeal whether an event, to which the Fidelity Fund responds, occurred during the period of cover for the Elara Apartments. If the appeal were upheld, that is a question that would have needed to be remitted to the primary judge. As we have determined that the appeal should be dismissed, such a remittal is unnecessary.

(b) The holder of a fidelity certificate must make a claim against the Fidelity Fund within the period of 90 days of becoming aware of the existence of grounds for the claim. The evidence does not reveal when the appellant became aware of the losses incurred by reason of a breach of statutory warranty by the builder. However, the appellant must have been aware of the losses, or grounds for making a claim in respect of the losses, at least by the time it commenced proceedings in the ACT Supreme Court against the builder on 17 May 2013. The appellant did not make the first claim against the Fidelity Fund until 18 August 2017, which was well outside the required period for making a claim. Even if the appellant’s letter of advice to the Fidelity Fund on 19 September 2013 could be regarded as making a claim, it was also outside time. The same answer applies to the second claim. We do not consider that the trustees have a discretion to waive compliance with the applicable time period.

(c) As the trustees were entitled to reject the appellant’s claim against the Fidelity Fund because it was made outside the applicable time period, it is not necessary to determine whether the appellant had the right to make a claim against the Fidelity Fund. The resolution of that issue would involve complex questions of fact and law. As this issue was not the subject of factual findings or consideration by the primary judge, it is not appropriate to seek to determine the issue on this appeal.

95 Our reasons for those answers follow.

A preliminary issue: identifying the source of legal rights and obligations

96 Before turning to the issues that arise on the appeal, it is necessary to identify the source or sources of the legal rights and obligations of a person holding a fidelity certificate issued under the Fidelity Fund Scheme. A number of potential sources have been identified by the parties in argument before the primary judge and on this appeal. In particular, before the primary judge, the appellant advanced an argument that the fidelity certificates themselves provided an independent and standalone source of legal rights. That argument was rejected by the primary judge and the appellant did not maintain the argument on the appeal. While the respondent primarily looked to the Trust Deed as the source of legal rights and obligations, it sought to incorporate, as an operative provision of the Trust Deed, clause 4 of the Approval Criteria as a relevant source of legal rights.

97 In our view, the source of legal rights and obligations arising in respect of the Fidelity Fund Scheme is the Trust Deed, and not the statutory provisions under which the Fidelity Fund Scheme has been established. The provisions of Division 6.4 of the 1972 and 2004 Acts are facultative in nature. Those provisions empower the Minister to approve a fidelity fund scheme, including by determining the criteria by which to approve such a scheme. But neither those statutory provisions, nor the instruments made under those provisions, provide a source of rights or obligations to persons who hold a fidelity certificate under such a scheme. Rather, those provisions contemplate the scheme being established through an approved trust deed.

98 The Trust Deed for the Fidelity Fund Scheme incorporates by reference various provisions of the 1972 Act and statutory instruments made under that Act. However, those provisions only have operative force in respect of a person holding a fidelity certificate issued under the Fidelity Fund Scheme in so far as they are incorporated as terms of the Trust Deed. While the primary judge stated that the relevant legal rights and obligations “are primarily to be found in the 2004 Act and related legislative instruments, as well as the Deed” (at [97]), we do not understand his Honour’s reasons to be based on a different understanding of the source of the relevant legal rights and obligations. His Honour’s reasons properly proceeded from an examination of the terms of the Trust Deed, including the statutory provisions that are incorporated by reference.

99 We agree with the primary judge that the fidelity certificates issued pursuant to the Trust Deed are not an independent source of legal rights and obligations of the person holding the certificate. Nevertheless, the fidelity certificate is an important instrument. The provisions of Division 6.4 of the 1972 and 2004 Acts, the Approval Criteria and the Trust Deed all contemplate that a person’s rights under the Fidelity Fund Scheme in respect of a particular residential building project will arise upon the issue of a fidelity certificate. The content of the fidelity certificate is governed by clause 58 of the Trust Deed. Significantly, clause 58(a)(3) stipulates that the certificate must state the amount that an owner can request from the Fidelity Fund (which must be at least the amount that is the minimum amount of cover that is required to be provided by an insurance policy under the Act). Thus, in respect of a particular residential building project, the certificate defines, for the purposes of the Trust Deed, the amount that can be requested by the holder of the certificate from the Fidelity Fund.

100 We also agree with the primary judge that clauses 4 and 8 of the Trust Deed incorporate by reference relevant provisions of the Approval Criteria and the 2005 Prudential Standards. However, not every clause of those instruments is incorporated as an operative provision of the Trust Deed. In particular, the respondent’s reliance on clause 4 of the Approval Criteria goes too far. As set out above, clause 4 of the Trust Deed states that the Fidelity Fund Scheme is to be administered pursuant to the disallowable instruments under Part 6 of the Act and clause 8 states that the trustees must administer the Fidelity Fund in accordance with the disallowable instruments created pursuant to Part 6 of the Act. The disallowable instruments undoubtedly include the Approval Criteria and the 2005 Prudential Standards. However, not every provision of those instruments is relevant to the administration of the Fidelity Fund or the Scheme more broadly. For example, clause 2 of the Approval Criteria stipulates the procedural requirements for making an application to the Minister for approval of the scheme. Clauses 3 to 8 are to similar effect, requiring an executed copy of the trust deed accompanying the scheme to be lodged and specifying mandatory terms in the trust deed. None of those provisions relate to the administration of the Fidelity Fund or the Scheme. They specify requirements that must be complied with in order for the scheme, including the underpinning trust deed, to be approved. In contrast, and again by way of example, clause 4 and 8 of the Trust deed may well be regarded as incorporating by reference, as operative terms of the Trust Deed, the provisions of clauses 12 and 14 of the Approval Criteria which are expressed as obligations imposed on the trustees.

First issue: in respect of what events does the Master Builders Fidelity Fund Scheme provide cover or benefits?

The primary judge’s conclusions

101 As noted earlier, the primary judge concluded that a claim cannot be made against the Fidelity Fund unless the claimant is unable to recover from the builder under the residential building contract, including in respect of a breach of statutory warranty, because the builder has become insolvent, disappeared or died. His Honour’s conclusion was based on the construction of s 90(1)(f) of the 2004 Act (which replaced s 64(1) of the 1972 Act, being the provision that was incorporated into the Trust Deed by clauses 60 and 61, reproduced above). It will be recalled that s 90(1)(f), (g) and (h) stipulated the risks that must be covered by residential building insurance (and which, by incorporation, also stipulate the risks covered by the Fidelity Fund). His Honour reached the following conclusions about the effect of those terms:

[107] …I consider that, properly construed, the risks which are covered under the Fidelity Fund Scheme are the same as those which are covered under a residential building work insurance policy as provided for in s 90 of the 2004 Act. Those risks are:

(a) the risk (which, in the case of the Fidelity Fund Scheme, is perhaps more accurately described as a condition to the trustees making a payment from the Fidelity Fund) of the owner or the owner’s successor in title being unable to enforce or recover under the relevant residential building contract against the builder because of the insolvency, disappearance or death of the builder (i.e. s 90(1)(f)); and

(b) the risk of loss resulting from a breach of statutory warranty (i.e. s 90(1)(g)); and/or

(c) the risk of loss resulting, because of the builder’s negligence, from subsidence of the land whether the residential building work was carried out (i.e. s 90(1)(h)).