FEDERAL COURT OF AUSTRALIA

Commissioner of Taxation v The Trustee for the Michael Hayes Family Trust [2019] FCAFC 226

ORDERS

Appellant | ||

AND: | THE TRUSTEE FOR THE MICHAEL HAYES FAMILY TRUST ABN 91 988 568 719 Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The appeal be dismissed with costs as agreed or assessed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

GRIFFITHS J:

1 I have had the considerable benefit of reading Steward J’s reasons for judgment in draft. I respectfully agree with his Honour’s reasons for dismissing the appeal and with the orders he proposes.

2 There are two additional observations which I wish to make. First, I agree with Steward J that this appeal is fundamentally about mistake and whether or not the mistake can be corrected by principles of construction. This reference to “mistake” is not to be confused with what conventionally is called “the doctrine of mistake”, where remedies lie not in construction but may operate, for example, to render a contract void ab initio or give rise to some other remedy, including a right of rescission. This appeal does not fall to be determined by reference to the conventional doctrine of mistake, but rather by ordinary principles of construction. I respectfully agree with Steward J’s identification and application at [34] to [41] of his Honour’s reasons for judgment of the relevant authorities to the circumstances here.

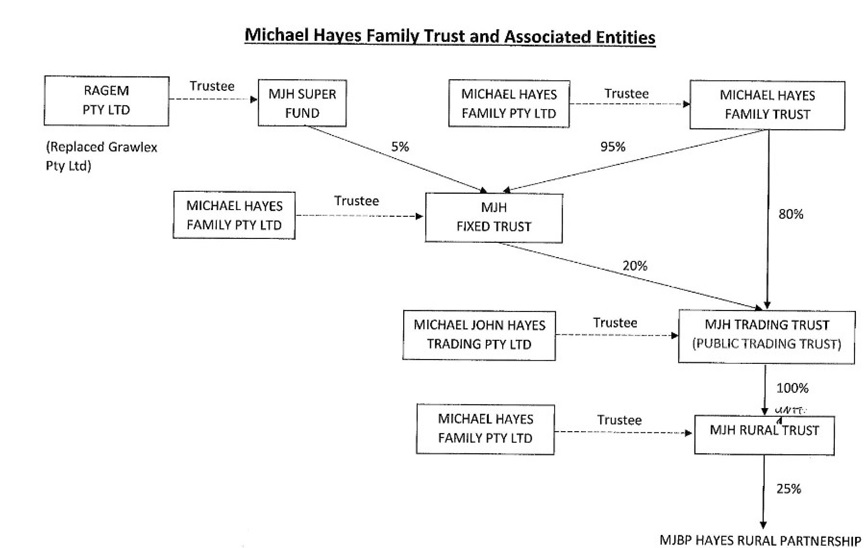

3 Secondly, those authorities all relate to the construction of contracts, but it is notable that the Commissioner’s clearly stated position in the appeal was that “the principles are the same” for the construction of a trust deed. For the purpose of determining this appeal, that position should be acted upon.

I certify that the preceding three (3) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Griffiths. |

Associate:

REASONS FOR JUDGMENT

DERRINGTON J:

4 I agree with the reasons and orders of Steward J.

I certify that the preceding one (1) numbered paragraph is a true copy of the Reasons for Judgment herein of the Honourable Justice Derrington. |

Associate:

Dated: 16 December 2019

REASONS FOR JUDGMENT

STEWARD J:

5 This is an appeal from a judgment of this Court allowing a tax appeal for the years ended 30 June 2010 to 30 June 2014. The appellant (the “Commissioner”) had issued notices of assessment to the trustee of the Michael Hayes Family Trust (the “MHFT”) (the “taxpayer”) on the basis that the trustee was presently entitled, for the purposes of Div 6 of Pt III of the Income Tax Assessment Act 1936 (Cth) (the “1936 Act”) to the income of two other trusts, namely the MJH Trading Trust and the MJH Fixed Trust. The taxpayer was assessed pursuant to s 99A of the 1936 Act. The learned primary judge found that each assessment was excessive because:

(a) the MJH Trading Trust was a “public trading trust” in the applicable years for the purposes of Div 6C of Pt III of the 1936 Act and, as such, was taxable as a company and not as a trust estate in accordance with Div 6 of Pt III of the 1936 Act; alternatively

(b) if the MJH Trading Trust was not subject to Div 6C, but rather Div 6, its trustee had exercised its power to accumulate income in each year, such that neither the MJH Fixed Trust nor the taxpayer was presently entitled to its income.

6 For the reasons which follow I would dismiss the appeal.

Legislation

7 This case concerns Div 6C of the 1936 Act. Generally speaking, a “public trading trust”, as defined, is treated in many respects by the Income Tax Assessment Act 1997 (Cth) (the “1997 Act”) and the 1936 Act as a company. As such, a public trading trust, is not taxed in accordance with the usual provisions dealing with the income of trust estates. The trustee pays income tax like a company and the trust’s distributions are assessed as dividends.

8 The term “public trading trust” is defined by s 102R of the 1936 Act. Amongst other things, the trust must be a “unit trust” which is a “public unit trust”. A “public unit trust” is defined by s 102P of the 1936 Act. It was not in dispute that the MJH Trading Trust was a “unit trust”: cf ElecNet (Aust) Pty Ltd v Federal Commissioner of Taxation (2016) 259 CLR 73. However, the Commissioner did dispute that it was a “public unit trust” as defined.

9 Section 102P relevantly provides:

Public unit trusts

(1) For the purposes of this Division, but subject to the succeeding provisions of this section, a unit trust is a public unit trust in relation to a year of income if, at any time during the year of income:

(a) any of the units in the unit trust were listed for quotation in the official list of a stock exchange in Australia or elsewhere;

(b) any of the units in the unit trust were offered to the public; or

(c) the units in the unit trust were held by not fewer than 50 persons.

(2) For the purposes of this Division, but subject to the succeeding provisions of this section, a unit trust is also a public unit trust in relation to a year of income if:

(a) at any time during the year of income, an exempt entity or exempt entities held, or had the right to acquire or become the holder or holders of, a unit or units in the unit trust that entitled the holder or holders to not less than 20% of:

(i) the beneficial interests in the income of the unit trust; or

(ii) the beneficial interests in the property of the unit trust;

…

…

(4) Subject to subsection (5), a unit trust that, but for this subsection and subsection (7), would be a public unit trust in relation to a year of income by virtue only of subsection (1) shall be deemed not to be a public unit trust in relation to the year of income if, at any time during the year of income, one person or persons not more than 20 in number held, or had the right to acquire or become the holder or holders of, a unit or units in the unit trust that entitled the holder or holders thereof to not less than 75% of:

(a) the beneficial interests in the income of the unit trust; or

(b) the beneficial interests in the property of the unit trust.

…

(7) Subject to subsection (8), a unit trust that, but for this subsection, would be a public unit trust in relation to a year of income by virtue only of subsection (1), shall be deemed not to be a public unit trust in relation to that year of income if:

(a) not less than 75% of the total of money paid or credited by the trustee of the unit trust during the year of income to unitholders as unitholders was paid or credited to one person or persons not more than 20 in number; or

…

…

(10) For the purposes of this section, where any units in a unit trust (except a foreign entity to which subsection 102N(2) applies) are held by the trustee of another trust estate, a person who has a beneficial interest in property of that other trust estate that consists of those units (whether or not that beneficial interest is deemed to be held by virtue of the application of this subsection) shall be deemed to hold those units.

10 For the moment, I note two matters:

(1) first, that a key element of the applicable statutory scheme is that for a unit trust to be also a “public unit trust”, an “exempt entity” must hold not less than 20% of the “beneficial interests” in the income or property of the trust, or, critically for the outcome of this appeal, be entitled to acquire such an interest; and

(2) secondly, that there existed in 2010 a superannuation fund known as the “MJH Superannuation Fund”. It had been established just prior to 2000. It was not disputed that this was an “exempt entity” for the purposes of s 102P because it was a complying superannuation fund.

Facts

11 Save for the issue concerning the accumulation of income, the primary facts found by the learned primary judge were not in dispute.

12 A number of different entities and trusts, established for the benefit of a Mr Hayes and his family, were participants in an arrangement set up in February 2010. The learned primary judge attached to his reasons a diagram showing each applicable entity and trust, and the relationships between each of them. I also attach that diagram as “Annexure A”.

13 On 24 February 2010, two new trusts were created, namely the MJH Fixed Trust and the MJH Trading Trust. At that time, the MJH Superannuation Fund already existed, as did the MHFT (which had been established in 2007).

14 At [61] (reproduced below), the learned primary judge accepted that the commercial purpose and object of the business structure established in 2010 was to ensure that the MJH Trading Trust would be a “public trading trust” for the purposes of Div 6C. In that respect, his Honour found that the events of 24 February 2010 “were not coincidental”. The Commissioner did not suggest otherwise.

15 For the MJH Trading Trust to be a “public trading trust” it had to be a “public unit trust”, as that term is defined by s 102P. Relevantly, this required the presence of an “exempt entity” which held not less than a 20% beneficial interest in the income or property of that trust, or had the right to acquire such an interest. Here, I infer that to secure that outcome, in 2010:

(1) the MJH Trading Trust was established with 20% of the units issued by that trust (20 units) being allocated to the MJH Fixed Trust (the other 80 units were issued to the MHFT);

(2) the MJH Fixed Trust was established with two Absolute Beneficiaries. They were the MJH Superannuation Fund (called the “Second Absolute Beneficiary”), being an “exempt entity”, which held a 5% “Share” in the “Trust Fund” of the MJH Fixed Trust, and the MHFT (called the “First Absolute Beneficiary”) which held a 95% “Share”; and

(3) the MJH Fixed Trust Deed contained a clause purporting to give the Second Absolute Beneficiary an option to acquire any asset forming part of the Trust Fund. Clause 20 was in these relevant terms:

20. ABSOLUTE BENEFICIARY’S OPTION

20.1 Option to Purchase Property The Second Absolute Beneficiary has an option to purchase any asset forming part of the Trust Fund in accordance with this clause 20 (“the Beneficiary’s Option”).

20.2 Exercise of Option The Beneficiary’s Option may be exercised by giving notice in writing identifying the asset in respect of which the Beneficiary’s Option is exercised (“the Asset”) signed by the Absolute Beneficiary or by the Absolute Beneficiary’s solicitors and delivering or posting by prepaid ordinary mail such notice to the Trustee.

The application of this clause was disputed on appeal. On one view, it conferred upon the MJH Superannuation Fund, as an exempt entity, an entitlement to acquire the 20 units held by the MJH Fixed Trust in the MJH Trading Trust. It was not disputed before the primary judge or before this Court (save in one respect which I address below) that those units entitled the trustee of the MJH Fixed Trust to not less than 20% of the beneficial interests in the income or property of the MJH Trading Trust. It was also not disputed that those units were an asset forming part of the Trust Fund of the MJH Fixed Trust.

16 I infer that the foregoing steps were designed to create a structure that complied with the definitional requirements of s 102P of the 1936 Act and thereby to ensure that the MJH Trading Trust would be treated as a “public trading trust”, taxable in accordance with Div 6C of Pt III of the 1936 Act. In my view, the parties intended to achieve that outcome by seeking to confer on the MJH Superannuation Fund, being an exempt entity, the right to acquire units in the MJH Trading Trust that entitled the holder of those units to not less than 20% of the beneficial interests in the income or property of that trust for the purposes of s 102P(2)(a).

17 That inference arises from the structure that was established on 24 February 2010. It emerges from the issue of precisely 20 units to the MJH Fixed Trust by the MJH Trading Trust. It is also discernible from the existence of cl 20 in the MJH Fixed Trust Deed. It further arises from the terms of the deed for the MJH Trading Trust which contains:

(a) a definition of the term “Public Trading Trust” which refers to s 102R of the 1936 Act; and

(b) clause 14.4, which takes precedence over the other provisions of the deed, and which provides for the distribution of net profit “for each year the Trust is a Public Trading Trust”.

18 But there was a problem. The “Second Absolute Beneficiary” for the MJH Fixed Trust was identified in Part 6 of the “Schedule” to the deed for that trust as “GRAWLEX PTY LTD ACN 080 401 092 as trustee of the MJH Superannuation Fund”. A few days before the commencement of the trial, the Commissioner told the taxpayer that Grawlex Pty Ltd (“Grawlex”) had ceased to be the trustee of the MJH Superannuation Fund on 1 July 2007. It had been replaced by an entity called Ragem Pty Ltd (“Ragem”). Thus, at the time of settlement of the MJH Fixed Trust, Ragem and not Grawlex was the trustee of the MJH Superannuation Fund. The Commissioner contended that it followed from this that no “exempt entity” had an entitlement of the kind required by s 102P(2)(a) and that, accordingly, the MJH Trading Trust was not a “public trading trust”.

19 The taxpayer responded by the creation of a “Deed of Rectification” of the MJH Fixed Trust executed by Mr John Ioannou, as settlor, and by the taxpayer, in its capacity as trustee of the MJH Fixed Trust, on the first day of the trial below. It was tendered into evidence. No witness was required by the Commissioner to be cross-examined about this document. It contains the following relevant terms:

Background

A. The Trustee is the trustee of the trust set out in Item 3 of Schedule 1 (“the Trust”) constituted by the deed set out in that Item (“the Deed”).

B. The Settlor is the settlor of the Trust constituted by the Deed.

C. The parties enter into this Deed of Rectification to rectify an error in the details of the “Second Absolute Beneficiary” as described in Item 6 of the Schedule of the Deed.

D. The Settlor and Trustee desire to rectify the Deed.

Operative Part

1. Declaration

1.1 The Settlor confirms and acknowledges that:

1.1.1 the “Second Absolute Beneficiary” as described in Item 6 of the Schedule of the Deed was described incorrectly;

1.1.2 the beneficial interest as to a 5% share of the trust fund (as that term is defined in the Deed) is held by the Trustee of the MJH Superannuation Fund;

1.1.3 the “Second Absolute Beneficiary” should have been, from the date the Trust was established, Ragem Pty Ltd ACN 108 564 914 as trustee for the MJH Superannuation Fund;

1.1.4 he has acted consistently within the terms of the Deed and established the trust fund of the Trust by paying the settlement sum (as that term is defined in the Deed) to the Trustee.

1.2 The parties declare that:

1.2.1 they acknowledged and accepted the terms of the Deed as at the date the Trust was established;

1.2.2 the Trust was duly established;

1.2.3 the “Second Absolute Beneficiary” as described in Item 6 of the Schedule of the Deed was described incorrectly;

1.2.4 the Deed is now rectified pursuant to Clause 2 of this Deed of Rectification;

1.2.5 they have acted consistently with the terms of the Deed;

1.2.6 they continue to acknowledge and confirm the terms of the Deed as rectified by Clause 2.

2. Rectifying Clauses

2.1 As from the date of this Deed of Rectification, the Deed shall be rectified pursuant to Schedule 2 (“the Rectifying Clauses”) and shall take effect from the date of establishment of the Trust.

2.2 The Rectifying Clauses are intended to take precedence over the balance of the Deed and, in the event of conflict between the Rectifying Clauses and the balance of the Deed, the Rectifying Clauses shall prevail.

20 The entry into of this Deed was apparently inspired by the following observation of Hill J. in Davis v Federal Commissioner of Taxation [2000] FCA 44; (2000) 171 ALR 654 at [57]:

As an alternative to an order of rectification the parties could execute a deed rectifying their prior writing. That deed, if truly operating to record that the parties were under a mutual mistake, and also setting out what the parties acknowledge to be the true agreement between them would not, any more than a court order, actually alter the position as between the parties. It would merely record that agreement as it always was. Whether by court order or by deed, rectification requires that there be a mutual mistake, that is to say what is required is that there be a common intention between the parties as to the effect that the instrument they signed would have had which was inconsistent with the effect which the instrument which they executed in fact had: cf Commissioner of Stamp Duties (NSW) v Carlenka Pty Ltd (1995) 95 ATC 4620. Mistake as to the revenue consequences of the agreement would not bring about the same result: Baird v BCE Holdings Pty Ltd (1996) 40 NSWLR 374 at 384.

21 No other evidence was led below concerning the intentions of Mr Ioannou and the trustee of the MJH Fixed Trust in February 2010. In particular, no evidence was led concerning whether the reference to Grawlex was a mistake. It was said by the Commissioner that there might not have been a mistake. Or that the mistake was possibly not the reference to Grawlex but to its identified capacity as trustee of the MJH Superannuation Fund. Given the contents of the Deed of Rectification, which was tendered into evidence, I reject those suggestions. In my view, I can rely upon the uncontradicted evidence contained in the Deed of Rectification, as well as to what I have inferred were the commercial objectives of the parties, to conclude:

(a) that the parties were intending to name as a beneficiary of the MJH Fixed Trust, the actual trustee of the MJH Superannuation Fund, it being the required “exempt entity” for the purposes of s 102P(2)(a) of the 1936 Act; and

(b) that accordingly, in 2010 they had mistakenly believed that Grawlex was that trustee, when, in fact at the time, it was not.

The Primary Judge’s Decision

22 The learned primary judge decided that the assessments issued to the taxpayer were wholly excessive. In a comprehensive judgment, his Honour carefully considered the competing contentions before him and relevantly decided as follows:

(1) First, his Honour rejected the contention that the Second Absolute Beneficiary did not have an exclusive entitlement to acquire the units held by the MJH Fixed Trust in the MJH Trading Trust. The submission put by the Commissioner was that the reference in cl 20.2 in the MJH Fixed Trust Deed to the “Absolute Beneficiary” was to both the First and Second Absolute Beneficiaries because that term is defined in cl 1.1 as meaning “the persons specified as such in Part 6 of the Schedule”. Part 6 of the Schedule lists both beneficiaries. This argument was rejected by the learned primary judge at [48] of the reasons below as follows:

I do not accept this submission. Clause 20.1 confers what it terms the Beneficiary’s Option on the Second Absolute Beneficiary and only on the Second Absolute Beneficiary. Any impact of the definitions clause aside, the natural meaning of the reference in cl 20.2 to “the Absolute Beneficiary” is to the Absolute Beneficiary to whom the Beneficiary’s Option is granted. That is the Second Absolute Beneficiary. It is an odd construction to construe cl 20.2 as requiring that an option granted to but one of the Absolute Beneficiaries to be exercised by a notice signed by each of them. It is also a construction which is at odds with cl 20.3.1, which states:

In the event of the Beneficiary’s Option being exercised, the Trustee shall transfer to the Absolute Beneficiary the Asset in consideration for an amount equal to the market value of the Asset payable to the Trustee.

It is a natural construction of this clause, and one consistent with the like construction of cl 20.2, to construe the reference to the “Absolute Beneficiary” as the person to whom the Beneficiary’s Option is granted, the Second Absolute Beneficiary. Once again, it would be odd to require the trustee to transfer to each of the Absolute Beneficiaries an asset in respect of which an option to purchase had been granted to but one.

(2) Secondly, his Honour construed the reference to “Grawlex Pty Ltd ... as trustee of the MJH Superannuation Fund” as being to the trustee for the time being of that Fund. For that purpose his Honour had regard to the following surrounding circumstances at [59]-[60]:

The relevant circumstances surrounding the execution of the MJH Fixed Trust Deed were events already recited but now desirably collated:

(a) the MJH Fixed Trust Deed was executed on 24 February 2010 between Mr John Ioannou as settlor and [Michael Hayes Family Pty Ltd (“Hayes”) as trustee];

(b) on that same day, 24 February 2010, two further trusts were established:

(i) the MJH Trading Trust, of which MJH Trading Pty Ltd was trustee; and

(ii) the MJH Rural Unit Trust, of which Hayes is trustee.

Also as at 24 February 2010, there was a superannuation fund known as the “MJH Superannuation Fund” constituted, but its trustee, once Grawlex, no longer acted in that capacity, another corporation, Ragem then so acted.

The “surrounding circumstances” were not otherwise identified by the taxpayer in its Appeal Statement. In a case where those circumstances assumed such great importance, that is regrettable. Whilst an Appeal Statement is not a formal pleading, it nonetheless serves the function of identifying the material facts relied upon and should give fair notice of the case that is to be met: Federal Commissioner of Taxation v Resource Capital Fund IV LP (2019) 266 FCR 1 at 29-30 [90]. In this proceeding, that should have included the precise identification of the surrounding circumstances said by the taxpayer to be relevant to the issue of construction. At [61], the primary judge reasoned as follows:

… Hayes submitted that “the commercial purpose and object of the business structure was to ensure that the MJH Trading Trust would be a public trading trust, which required the MJH Superannuation Fund to hold an interest in the MJH Trading Trust through the MJH Fixed Trust”. Better put, in my view, is that the events of 24 February 2010 were not coincidental and the surrounding circumstances mentioned disclose an ambiguity in the MJH Fixed Trust Deed and the existence of a related “constructional choice”. Is it the reference to Grawlex or the capacity as trustee of the Superfund which is to be preferred? For the reason submitted by Hayes, the reference in the MJH Fixed Trust Deed to Grawlex as “Second Absolute Beneficiary” made no sense, unless it did indeed, as at 24 February 2010, act in the capacity as trustee of the Superfund. At the time of execution it was that capacity which was critical. The meaning to give to the nomination in Part 6 of the Schedule to the MJH Fixed Trust Deed as to who is the “Second Absolute Beneficiary” is therefore “the trustee for the time being of the MJH Superannuation Fund”.

(3) Thirdly, the learned primary judge decided that, if necessary, he would have made an order to rectify the reference to Grawlex in the MJH Fixed Trust Deed. His Honour reasoned at [87] as follows:

It being in evidence, I consider that, were rectification sought and necessary, I could and should make like use of the Deed of Rectification in this case. Even though Mr Hayes has not given evidence on this point and Mr Ioannou has given neither oral nor affidavit evidence, each has subscribed to the Deed of Rectification. Considered against the background of the other instruments executed on 24 February 2010 and the original and then identity of the trustee of the Superfund, the statements in the Deed of Rectification as to “error” (background, cl C), “should have been, from the date the Trust was established, [Ragem as trustee for the Superfund]” (cl 1.1.3) and “described incorrectly” (cl 1.2.3) are, applying the requisite standard of proof, consistent only with a conclusion that the reference in the MJH Fixed Trust Deed to Grawlex was the result of a mutual mistake as to the identity of the trustee of the Superfund as at 24 February 2010. I do not accept the Commissioner’s submission to the contrary.

(4) Fourthly, the learned primary judge accepted an alternative submission that the trustee of the MJH Superannuation Fund was deemed, by reason of s 102P(10) of the 1936 Act, to be the owner of the units held by the MJH Fixed Trust in the MJH Trading Trust. The argument put below by the taxpayer was summarised at [95] by his Honour as follows:

Hayes submitted that s 102P(10) applied in this way:

• The relevant unit trust is the MJH Trading Trust.

• The “other trust estate” is the MJH Fixed Trust, the trustee of which holds 20 units in the MJH Trading Trust.

• The “person” who has the beneficial interest in the property of the MJH Fixed Trust is the trustee of the Superfund, which has a beneficial interest in 5% of the property of the MJH Fixed Trust, including its 20 units in the MJH Trading Trust.

• Because the trustee of the Superfund has a 5% interest in each one of the MJH Fixed Trust’s units in the MJH Trading Trust, it is deemed to hold those units.

The learned primary judge accepted this submission. In doing so, his Honour rejected the Commissioner’s contention that s 102P(10) only provided for the tracing of beneficial ownership through multiple trusts to the ultimate beneficiary. Thus, here it was said, the provision only gave the trustee of the MJH Superannuation Fund a 5% interest in the units held by the MJH Fixed Trust in the MJH Trading Trust. It did not permit what was described as an “artificial increase” in that interest. His Honour rejected that argument and said at [98]-[99]:

A difficulty in the Commissioner’s submission, and it appears to me to be a fatal one, flowing from the text of s 102P(10), is that the subsection states, “a beneficial interest in property of that other trust estate that consists of those units” (my emphasis). The subsection uses the indefinite article. Ragem, the trustee of the Superfund has a beneficial interest, namely a beneficial interest in 5% of the property of the MJH Fixed Trust, including its 20 units in the MJH Trading Trust. According to the text of s 102P(10), the specified deeming that follows is comprehensive, not proportionate.

Hayes submitted that, if the Commissioner’s construction were correct it would, “frustrate the apparent purpose of s 102P(10), which is to enable holdings of units by “exempt entities” to be traced through interposed trusts”. As s 102MD of the ITAA 36 stood in the Relevant Years, “exempt entities” included complying superannuation funds. The Superfund was such a fund. Hayes’ further submission was that, “[i]f the tracing did not stop with the complying superannuation fund but continued through the fund to the beneficiaries, it would defeat the purpose of s 102P(10), which was to extend the reach of s 102P(2)”. These submissions, which accord with the text, context and apparent purpose of s 102P(10), should be accepted. The Commissioner made reference to the relevant Explanatory Memorandum in an endeavour to support his construction. That confirms that s 102P was intended to have the character of a tracing provision. It is the text of the legislation, not that of the Explanatory Memorandum which must be construed. Hayes’ construction is not at odds with this. In the present circumstances, application of that construction of s 102P(10) traces the ownership of the MJH Trading Trust through the MJH Fixed Trust, back to the relevant exempt entity, the trustee of the Superfund.

(5) Finally, the learned primary judge agreed with the submission of the taxpayer that, if during the years in dispute the MJH Trading Trust had not been a “public trading trust” subject to Div 6C of Pt III of the 1936 Act, neither the taxpayer (nor the MJH Fixed Trust) was presently entitled to the net income of that trust estate in those years. That is because the trustee had exercised its power in each year to accumulate the income of the trust. At [115], his Honour reasoned as follows:

On the evidence (the financial accounts) and subject to the distribution noted above in respect of the 2011 income year to a non-unitholder, the trustee of the MJH Trading Trust credited its accounting profit to a “Retained Profits Account” rather than distributing it to the unitholders in each year of income. Those accounts are sufficient evidence that the trustee exercised the power in cl 14.7.2: Cajkusic v Commissioner of Taxation [2006] FCAFC 164; (2006) 155 FCR 430, at 436, [20].

23 For these reasons, the learned primary judge allowed the taxpayer’s appeal against the Commissioner’s objection decision.

Amended Notice of Appeal and Amended Notice of Contention

24 The Commissioner’s Amended Notice of Appeal raised the following grounds for consideration:

(a) that the learned primary judge had erred in his construction of the MJH Fixed Trust Deed. In particular, his Honour erred in considering the surrounding circumstances to determine that the definition of the “Second Absolute Beneficiary” was ambiguous;

(b) that the learned primary judge had erred in construing cl 20.2 of the MJH Fixed Trust Deed;

(c) that the learned primary judge had erred in construing s 102P(10) of the 1936 Act; and

(d) that the learned primary judge erred in deciding that the taxpayer had discharged its onus of showing that the power to accumulate income had been exercised by the trustee of the MJH Trading Trust in each year of income in dispute.

25 The taxpayer’s Amended Notice of Contention stated that the decision of the learned primary judge should be affirmed on the following additional grounds:

(a) there was patent as well as latent ambiguity in the definition of the Second Absolute Beneficiary in the MJH Fixed Trust Deed;

(b) it was unnecessary in any event to consider the surrounding circumstances to construe the definition of the Second Absolute Beneficiary in the way the learned primary judge did (that is, to mean “the trustee for the time being of the MJH Superannuation Fund”);

(c) the Deed of Rectification cured, in any event, the mistake of referring to Grawlex without the need for the Court to make orders for rectification;

(d) alternatively, the learned primary judge should have made an order for rectification of the MJH Fixed Trust Deed; and

(e) if Grawlex, and not Ragem, was the true Second Absolute Beneficiary, it held the option to acquire the property of the MJH Fixed Trust, on trust for the MJH Superannuation Fund.

The last contention, the Court was told, had been pressed before the learned primary judge but was not addressed in his Honour’s reasons for judgment, presumably because it was not necessary to do so.

The Construction of the MJH Fixed Trust Deed

26 The Commissioner submitted that the definition of the Second Absolute Beneficiary was not, on its face, ambiguous. Grawlex had been the trustee of the MJH Superannuation Fund, and could assume that capacity in the future. Ambiguity, it was said, only arose because the surrounding circumstances showed that Ragem was in fact the trustee. In the Commissioner’s submission, the learned primary judge erred in considering those circumstances to find latent ambiguity. In Australia, it was submitted, the surrounding circumstances can only be considered if the language used is first found to be ambiguous; in other words, where there is patent ambiguity. The Commissioner relied upon the following well-known passage from Codelfa Construction Pty Ltd v State Rail Authority (NSW) (1982) 149 CLR 337 at 352:

The true rule is that evidence of surrounding circumstances is admissible to assist in the interpretation of the contract if the language is ambiguous or susceptible of more than one meaning. But it is not admissible to contradict the language of the contract when it has a plain meaning. Generally speaking facts existing when the contract was made will not be receivable as part of the surrounding circumstances as an aid to construction, unless they were known to both parties, although, as we have seen, if the facts are notorious knowledge of them will be presumed.

Here, it was submitted that the words used in the definition of the Second Absolute Beneficiary were simply not susceptible of more than one meaning, and were thus not ambiguous.

27 The Commissioner also submitted that, absent patent ambiguity, the only context which could be considered in construing a contract were matters internal to, or identified by, the contract itself. The Commissioner relied upon the decision of French C.J., Nettle and Gordon JJ. in Mount Bruce Mining Pty Ltd v Wright Prospecting Pty Ltd (2015) 256 CLR 104, where at 116 [46] their Honours said:

The rights and liabilities of parties under a provision of a contract are determined objectively, by reference to its text, context (the entire text of the contract as well as any contract, document or statutory provision referred to in the text of the contract) and purpose.

(Footnotes omitted.)

28 The taxpayer did not contend that the interpretative principles concerning the construction of a contract did not also apply to determine the meaning of words used in a trust deed. Rather, it submitted that the better view of those principles is that ambiguity of language is not required to justify a consideration of the surrounding circumstances. It agreed with the learned primary judge (at [58]) that the law is correctly stated by Leeming J.A. in Cherry v Steele-Park (2017) 96 NSWLR 548. In that case, Leeming J.A. (with whom Gleeson J.A. agreed) said at 566 [76]:

There is now a deal of authority for the proposition that whether there is in truth a constructional choice available to a written contract cannot be determined without first at least considering evidence of surrounding circumstances.

29 Leeming J.A. was of the view that the foregoing statement of principle was supported by recent authority of the High Court. His Honour referred to the following passage from the reasons of French C.J., Hayne, Crennan and Kiefel JJ. in Electricity Generation Corporation v Woodside Energy Ltd (2014) 251 CLR 640 at 656-657 [35]:

… The meaning of the terms of a commercial contract is to be determined by what a reasonable businessperson would have understood those terms to mean. That approach is not unfamiliar. As reaffirmed, it will require consideration of the language used by the parties, the surrounding circumstances known to them and the commercial purpose or objects to be secured by the contract. Appreciation of the commercial purpose or objects is facilitated by an understanding “of the genesis of the transaction, the background, the context [and] the market in which the parties are operating”. As Arden LJ observed in Re Golden Key Ltd [2009] EWCA Civ 636 at [28]], unless a contrary intention is indicated, a court is entitled to approach the task of giving a commercial contract a businesslike interpretation on the assumption “that the parties ... intended to produce a commercial result”. A commercial contract is to be construed so as to avoid it “making commercial nonsense or working commercial inconvenience”.

(Footnotes omitted.)

30 At 566-567 [79]-[83], Leeming J.A. observed:

In my view, two more recent decisions of the High Court strengthen the conclusion that “ambiguity” is a conclusion, rather than a precondition to the admissibility of evidence of surrounding circumstances. First, in Victoria v Tatts Group Ltd [(2016) 90 ALJR 392; [2016] HCA 5], the question was the legal meaning of “a new gaming operator’s licence”, noting that the expression “Gaming Operator’s Licence” was defined by reference to a particular licence issued under the Gaming Machine Control Act 1991 (Vic). This is a good example of a recurring phenomenon: any conclusion as to whether the undefined term was ambiguous or instead bore a plain meaning could not be reached without first having regard to the context (notably, new legislation governing the licensing of gambling). A unanimous High Court, without once mentioning any threshold “ambiguity gateway”, allowed the appeal saying at [51] that the construction it favoured was “supported by references to the text, context and purpose”. The High Court then addressed the text (at [52]-[60]) and then the context and purpose (at [61]-[72]) and “other contextual matters” (at [73]-[74]) before concluding (at [75]) that “the text, context and purpose of the 1995 Agreement all support the conclusion” that the term was narrower than had been held by the Victorian Court of Appeal.

Secondly, in [Simic v New South Wales Land and Housing Corporation (2016) 91 ALJR 108; [2016] HCA 47], Gageler, Nettle and Gordon JJ said at [78] that:

“[78] … The proper construction of each Undertaking is to be determined objectively by reference to its text, context and purpose.”

French CJ observed at [18] that construction of a contract:

“[18] … involves determination of the meaning of the words of the contract defined by reference to its text, context and purpose. Resort to extrinsic circumstances and things external to the contract may be necessary to identify its purpose and in determining the proper construction where there is a constructional choice.” (Footnote omitted)

It will be seen that once again no reference was made to any necessity for there to be ambiguity before regard may be had to objective matters external to the contract. Neither judgment in terms stated that recourse could be had to context and purpose without first concluding that the contract was ambiguous. But I do not see why the general statements of principle and their application in Victoria v Tatts Group Ltd and the reiteration of those statements in Simic should not be taken at face value, especially since there is no occasion to overturn any decision of the High Court with precedential force.

For nothing has been said to detract from the continuing authority of the “true rule” formulated by Mason J in Codelfa which was reaffirmed in Mount Bruce Mining Pty Ltd v Wright Prospecting Pty Ltd at [48]. The latter decision otherwise has no bearing on the question, because the High Court expressly observed that whether “events, circumstances and things external to the contract may be resorted to, in order to identify the existence of a constructional choice, does not arise in these appeals”: at [49]. However, Kiefel and Keane JJ observed at [110] that Mason J had not said, in Codelfa, how ambiguity might be identified; his Honour’s reasons instead were directed to how an ambiguity might be resolved.

(Footnotes omitted.)

31 Earlier, in Mainteck Services Pty Ltd v Stein Heurtey SA (2014) 89 NSWLR 633, Leeming J.A. noted that language is “unavoidably contextual”. As a result, recourse to surrounding circumstances will often be vital to determine meaning. Such enquiries are not confined to cases where a pre-existing conclusion has been made that some of the language used in the contract is ambiguous. Thus at 654 [75]-[76], his Honour said:

… Words do not have a “natural” meaning that can be determined in isolation …

What is the legal meaning of a promise to sell “my Dürer drawing”, if the vendor’s wife owns a Dürer drawing which is on display in their home, and the vendor keeps another secretly in his study? What is the meaning of a gift “to my niece Eliza Woodhouse during her life” in a will, if the testator had no such niece, but a grandniece of that name, and another grandniece, who was illegitimate, who lived with him: cf In re Fish; Ingham v Rayner [1894] 2 Ch 83? What is the meaning of cl 7 of the Wild Dog Destruction Regulation 1999 (NSW), which provided “The Wild Dog Destruction Regulation 1994 is repealed”? Contracts, wills and statutes are very different legal texts, to the process of ascertaining whose legal meaning different rules apply, yet all are based on language, and language is unavoidably contextual. If I may repeat what I wrote of the uncertain meaning of the Wild Dog Destruction Regulation in Resolving Conflicts of Laws (2011, Federation Press) at p 13 fn 64, “The meaning of even the seemingly clearest legal text can be unclear; hence the importance of attending to context in the first instance.”

As for ambiguity, Leeming J.A. noted that it is an intrinsically ambiguous term. At 655 [83], his Honour said:

… the approach endorsed in Woodside avoids the difficulty of identifying what is meant by “ambiguity”, itself an ambiguous term, whose perception “differs from one judicial eye to the other”: B & B Constructions (Aust) Pty Ltd v Brian A Cheeseman & Associates Pty Ltd (1994) 35 NSWLR 227 at 234. The various meanings of “ambiguity” in this context are described by M Walton, “Where now ambiguity?” (2011) 35 Australian Bar Review 176 and D Wong and B Michael, “Western Export Services v Jireh International: Ambiguity as the gateway to surrounding circumstances?” (2012) 86 Australian Law Journal 57 at pp 67-69.

32 In Franklins Pty Ltd v Metcash Trading Ltd (2009) 76 NSWLR 603, Allsop P. (as his Honour then was) also rejected the proposition that the existence of ambiguity was required before a Court could legitimately consider the surrounding circumstances of the entry into of a contract. At 616 [14], his Honour said:

The state of the law in this respect is to be ascertained from a number of High Court cases: Maggbury Pty Limited v Hafele Australia Pty Limited (2001) 210 CLR 181 at 188 [11]; Pacific Carriers v BNP Paribas [(2004) 218 CLR 451] (at 461 [22]); Zhu v Treasurer of the State of New South Wales (2004) 218 CLR 530 at 559 [82]; Toll (FGCT) v Alphapharm [(2004) 219 CLR 165] (at 179 [40]) and International Air Transport Association v Ansett Australia Holdings Limited (2008) 234 CLR 151 at 160 [8] and 174 [53]. These cases are clear. The construction and interpretation of written contracts is to be undertaken by an examination of the text of the document in the context of the surrounding circumstances known to the parties, including the purpose and object of the transaction and by assessing how a reasonable person would have understood the language in that context. There is no place in that structure, so expressed, for a requirement to discern textual, or any other, ambiguity in the words of the document before any resort can be made to such evidence of surrounding circumstances.

The Full Court of this Court has agreed with the reasoning in Franklins and in Mainteck and with the proposition that the presence of ambiguity is no precondition to a consideration of surrounding circumstances. Thus in Stratton Finance Pty Ltd v Webb [2014] FCAFC 110; (2014) 314 ALR 166, after considering the application for special leave in Western Export Services Inc v Jireh International Pty Ltd [2011] HCA 45; (2011) 282 ALR 604, Allsop C.J., Siopis and Flick JJ. said at [37] and [40]:

As the reasons in Franklins stated, the conclusion that ambiguity need not be discovered before any resort to legitimate surrounding circumstances in the relevant task was drawn only from existing High Court authority: Maggbury Pty Ltd v Hafele Australia Pty Ltd [2001] HCA 70; 210 CLR 181 at 188 [11]; Pacific Carriers Ltd v BNP Paribas [2004] HCA 35; 218 CLR 451 at 461 [22]; Zhu v Treasurer of the State of New South Wales [2004] HCA 56; 218 CLR 530 at 559 [82]; Toll (FGCT) Pty Ltd v Alphapharm Pty Ltd [2004] HCA 52; 219 CLR 165 at 179 [40] and International Air Transport Association v Ansett Australia Holdings Ltd [2008] HCA 3; 234 CLR 151 at 160 [8] and 174 [53]. The Court’s view was reached in the light of the totality of Sir Anthony Mason’s judgment in Codelfa, and considering the clear words of those later binding High Court authorities.

…

Recently, in Mainteck Services Pty Ltd v Stein Heurtey SA [2014] NSWCA 184, the New South Wales Court of Appeal (Leeming JA, with whom Ward JA and Emmett JA agreed) expressed the view (at [71]) that [35] of Woodside was inconsistent with Jireh. We agree with that conclusion, and with the reasons in elaboration at [72]-[86], and in particular with the comments concerning Codelfa at [78]-[80].

It follows from Cherry, Franklins, Mainteck and Stratton that I do not accept that the learned primary judge erred in considering at [59]-[60] the surrounding circumstances to determine that Grawlex was not the trustee of the MJH Superannuation Fund when the MJH Fixed Trust was settled and that it was mistakenly referred to in the MJH Fixed Trust Deed.

33 The learned primary judge decided at [61] that the reference to Grawlex as the Second Absolute Beneficiary “made no sense”. I also respectfully agree with that observation. However, I think that this case is not really concerned with ambiguity in an instrument (whether patent or latent). In my view, this is a case about mistake. The parties mistakenly referred to Grawlex instead of Ragem. This is a mistake which can be cured by construing the reference to Grawlex to be a reference to the correct trustee of the MJH Superannuation Fund, namely Ragem.

34 The correction of obvious errors by an application of the ordinary principles of construction is well known. As Dixon C.J. and Fullagar J. said in Fitzgerald v Masters (1956) 95 CLR 420 at 426-427:

Words may generally be supplied, omitted or corrected, in an instrument, where it is clearly necessary in order to avoid absurdity or inconsistency.

In that case, the word “inconsistent” was read as meaning “consistent” in a contract for sale.

35 The principle is premised on absurdity and not ambiguity. Indeed, it is applicable even where the language is unambiguous: National Australia Bank Ltd v Clowes [2013] NSWCA 179; (2013) 8 BFRA 600 at [34]-[35] per Leeming J.A., citing Westpac Banking Corporation v Tanzone Pty Ltd [2000] NSWCA 25; (2000) 9 BPR 17,521 at [21] per Priestley, Fitzgerald JJ.A. and Foster A.J.A. and Noon v Bondi Beach Astra Retirement Village Pty Ltd [2010] NSWCA 202; (2010) 15 BPR 28,221 at [46] per Giles J.A. (with whom Macfarlan J.A. agreed).

36 Once again, I turn to Leeming J.A. for the most recent expression of the principle. In Seymour Whyte Constructions Pty Ltd v Ostwald Bros Pty Ltd (In liquidation) [2019] NSWCA 11, his Honour said at [6]-[10]:

Rectification by construction

At common law, if the error is clear, and it is also clear what a reasonable person would have understood the parties to have meant, then the mistake may be corrected as a matter of construction. This is old law. Lord St Leonards said in Wilson v Wilson (1854) 5 HL Cas 40 at 66-67; 10 ER 811 at 822:

“Now it is a great mistake if it is supposed that even a Court of Law cannot correct a mistake, or error, on the face of an instrument: there is no magic in words. If you find a clear mistake, and it admits of no other construction, a Court of Law, as well as a Court of Equity, without impugning any doctrine about correcting those things which can only be shown by parol evidence to be mistakes – without, I say, going into those cases at all, both Courts of Law and of Equity may correct an obvious mistake on the face of an instrument without the slightest difficulty.”

Examples may be found in linguistic errors, such as “inconsistent” being read as “consistent” in Fitzgerald v Masters (1956) 95 CLR 420; [1956] HCA 53, or conceptual errors, such as “lessor” being read as “lessee” in McHugh Holdings Pty Ltd v Newtown Colonial Hotel Pty Ltd (2008) 73 NSWLR 53; [2008] NSWSC 542. The language of a contract is not read like a computer program, such that any slip is fatal.

Two conditions are necessary in order to correct the contractual language in this manner: (a) that the literal meaning of the contractual words is an absurdity and (b) that it is self-evident what the objective intention is to be taken to have been: see Mainteck Services Pty Ltd v Stein Heurtey SA (2014) 89 NSWLR 633; [2014] NSWCA 184 at [117]-[119], approving National Australia Bank Ltd v Clowes [2013] NSWCA 179; 8 BFRA 600, where it was stated at [34]:

“Where both those elements are present ... ordinary processes of contractual construction displace an absurd literal meaning by a meaningful legal meaning.”

Likewise, in the United Kingdom, the court must be satisfied both as to the mistake and the nature of the correction: Pink Floyd Music Ltd v EMI Records Ltd [2010] EWCA Civ 1429; [2011] 1 WLR 770 at [21] (Lord Neuberger); Arnold v Britton [2015] AC 1619; [2015] UKSC 36 at [78] (Lord Hodge).

The court must be satisfied of those matters to a high level of conviction. To use the language of Dixon CJ and Fullagar J in Fitzgerald v Masters at 426-427, it must be “clearly necessary in order to avoid absurdity or inconsistency”. As this Court said in Miwa Pty Ltd v Siantan Properties Pte Ltd [2011] NSWCA 297 at [18], the test of absurdity is not easily satisfied. Any question of absurdity or inconsistency must be identified according to established principles, by reference to the text of the agreement as understood in its factual and legal context: Wyllie v Tarrison Pty Ltd [2007] NSWCA 184 at [46]; Newey v Westpac Banking Corporation [2014] NSWCA 319 at [85]. Courts which are asked to delete, insert or rewrite part of a contract because of what is said to be an obvious error should bear steadily in mind that imperfections and infelicities and ambiguities in contractual language commonly reflect the give and take of negotiations, or the parties’ appreciation that some obscurities are incapable of resolution. As Lord Hoffmann explained, the court does “not readily accept that people have made mistakes in formal documents”: Chartbrook Ltd v Persimmon Homes Ltd [2009] AC 1101; [2009] UKHL 38 at [23].

37 I note the expression of the test as involving two conditions which must be satisfied, namely:

(1) that the literal meaning of the contractual words is an absurdity; and

(2) that it is self-evident what the objective intention is to be taken to have been.

The level of satisfaction about these matters must be “high”.

38 See also Perpetual Limited v Myer Pty Ltd [2019] VSCA 98 at [122]-[127] per Whelan, Niall and Hargrave JJ.A. and Tokio Marine & Nichido Fire Insurance Co Ltd v Hans Bo Kristian Holgersson [2019] WASCA 114 at [77] per Buss P., Beech and Pritchard JJ.A.

39 The foregoing principle of construction has often been used when an instrument mistakenly refers to the wrong party or to a non-existent entity. In In re Fish; Ingham v Rayner [1894] 2 Ch 83 a testator left his residuary estate to his “niece Eliza Waterhouse”. He had no such niece. But his wife did have two grandnieces with that name (one of whom was illegitimate). The English Court of Appeal construed these words as referring to the legitimate grandniece. In F Goldsmith (Sicklesmere) Ltd v Baxter [1969] 3 WLR 522, an agreement for the sale of land referred to a non-existent entity called “Goldsmith Coaches (Sicklesmere) Ltd”. Applying the “known facts”, Stamp J. construed this “beyond peradventure” as “no more nor less an inaccurate description of the plaintiff company, F. Goldsmith (Sicklesmere) Ltd” (at 526). Nittan (UK) Ltd v Solent Steel Fabrication Ltd [1981] 1 Lloyd’s Rep 633 was another case in which a company had been incorrectly identified in an insurance policy. Lord Denning M.R. said:

In this court we are very used to dealing with misnomers. We do not allow people to take advantage of a misnomer when everyone knows what was intended.

In my view, this Court should take the same approach.

40 On the facts and circumstances here, and applying the two-step test articulated by Leeming J.A. in Seymour Whyte, I am amply satisfied:

(a) that applying the literal meaning of the named Second Absolute Beneficiary is an absurdity. It is an absurdity because Grawlex was not, at the time of the settlement of the MJH Fixed Trust, the trustee of the MJH Superannuation Fund and because the parties intended to create a structure whereby an exempt entity, being that Fund, would be a beneficiary of the MJH Fixed Trust; and

(b) that it is self-evident that in those circumstances the objective intention was to refer to the actual trustee, namely Ragem.

41 For these reasons, I would construe the reference to Grawlex to be, as the primary judge held, a reference to the trustee of the MJH Superannuation Fund, which in 2010 (and the income years in dispute) was Ragem.

42 In my view, the decision in Simic v New South Wales Land and Housing Corporation (2016) 260 CLR 85 does not compel a different conclusion. In Simic, a non-existent entity, called the “New South Wales Land & Housing Department trading as Housing NSW ABN 45 754 121 940” was the named beneficiary of a performance bond. The High Court declined to construe that name as a reference to the “NSW Land and Housing Corporation”. I respectfully agree with the learned primary judge (at [64]) that this conclusion was heavily dependent on the principle of “strict compliance” arising from the fact that such securities “create a type of currency” and are treated as being “as good as cash” (at 113 [88] per Gageler, Nettle and Gordon JJ.). As French C.J. said at 92-93 [10]-[11]:

Emmett A-JA was, with respect, correct to hold that the identity of the beneficiary named in the Undertakings was a matter of construction. His Honour was also correct in characterising the strict compliance principle as a matter relating to performance by the issuing institution rather than as a rule of construction. However, the principle is an incident of the purposes of a performance bond, which are inconsistent with an approach to construction that would require the issuing institution to undertake an investigative function where the beneficiary named on the face of the bond is not the same entity as that demanding payment under the bond. In the ordinary case, saving minor slips and misdescriptions, the designation of a person or entity as a beneficiary cannot simply, as a matter of construction, be transmuted into the designation of a different person or entity. Nor can a reference to a non-existent entity be construed as a reference to an existing entity with quite a different name.

The name of the non-existent government department specified in the Undertakings could not be construed by reference to underlying facts, requiring inquiry by the issuing institution, as a reference to the Corporation. Such a loose approach to construction would be inconsistent with the commercial purposes of the Undertakings as performance bonds.

(Footnotes omitted.)

See also 112-115 [83]-[97] per Gageler, Nettle and Gordon JJ.

43 It follows that the trustee of the MJH Superannuation Fund, as the Second Absolute Beneficiary of the MJH Fixed Trust and pursuant to cl 20 of the MJH Fixed Trust Deed (see [54]-[55] below), was the holder of a right to acquire units in the MJH Trading Trust which entitled the holder to not less than 20% of the beneficial interests in the income or property of that Trust. For that reason, the MJH Trading Trust was a “public unit trust” for the purposes of s 102P and, accordingly, a “public trading trust” for Div 6C purposes.

44 I should finally record a wholly new submission made by the Commissioner in his supplementary submissions filed following the hearing of the appeal. It was that the units issued by the MJH Trading Trust did not confer upon their holder any “beneficial interest” in the income or property of the MJH Trading Trust. This was said to follow from cl 3.3 of the deed of trust for the MJH Trading Trust which is in these terms:

For the avoidance of doubt, it is declared that no Unitholder shall have any proprietary, beneficial or other interest in any asset forming part of the Trust Fund.

It was also said to follow from the fact that the MJH Trading Trust had discretionary beneficiaries, from the trustee’s power to redeem units and from its discretion concerning the payment of income, and from a characterisation of the Trading trust as a “discretionary trust”. It was said that the beneficiaries of such a trust have no beneficial interest in the property of the trust.

45 In my view, the Commissioner did not have leave to make this submission. The parties were given leave to filed additional submissions following the hearing of the appeal concerning the construction of deeming provisions in an Act of Parliament, the concept of a “beneficial interest” for the purpose of s 102P(10) and the role of context in construing an instrument. This new submission falls outside of that permission. It also contradicts the very manner in which the Commissioner conducted the case before the learned primary judge and before this Court. The Commissioner accepted for that purpose that the units issued by the MJH Trading Trust were units that satisfied s 102P(2). For these reasons, I will not entertain the new submission.

The Deed of Rectification

46 Something brief should be said about the Deed of Rectification, although like the trial judge, I do not think it was needed here given the conclusion I have reached concerning the proper construction of the MJH Fixed Trust Deed.

47 First, as Gordon J. observed in GE Capital Finance Australasia Pty Ltd v Federal Commissioner of Taxation (2011) 219 FCR 420 at 448 [106], “[r]ectification turns on the subjective intentions of the maker (or makers) of a document: see Carlenka at 331-332; Butlin’s Settlement Trusts at 262; Allnutt v Wilding [2007] EWCA Civ 412 at [11]”. There needs to be “clear and convincing” proof of that intention: see the authorities for this proposition listed at 712 [451] in Franklins. Gordon J. also observed at 450 [117]:

The “usual type” of mistake capable of rectification involves incorrectly recording the intention of the maker of a document. Such a mistake may be rectified by inserting words or deleting words, or substituting different words because the words that are there have the wrong meaning: see Allnutt v Wilding [2007] EWCA Civ 412 at [12]; Butlin’s Settlement Trusts at 260 …

In GE Capital, Gordon J. ordered the rectification of a form (evidencing a choice to join a multiple entry consolidated group for the purposes of Div 719 of the 1997 Act) by the addition of a date which had been mistakenly omitted. Her Honour did so pursuant to relief which had been sought in proceedings issued in reliance upon s 39B of the Judiciary Act 1903 (Cth) (the “Judiciary Act”). I note that the Commissioner had been a party to those proceedings.

48 Secondly, other than the recitals and terms of the Deed of Rectification, no evidence was led from any witness concerning the subjective intention of the settlor of the MJH Fixed Trust. In my view, the remaining evidence, being the Deed of Rectification itself, fell short of being “clear and convincing” proof of that person’s subjective intention. What the Court needed was the testimony of the settlor setting out what had occurred. That such evidence was not adduced is perhaps unsurprising; the issue was only raised by the Commissioner at the very last moment.

49 Thirdly, whilst the Deed of Rectification here may be legally efficacious as between the parties to it, including, perhaps, as between the trustee and the beneficiaries, it cannot bind the Commissioner. The Commissioner can only assess taxpayers by applying the 1936 and 1997 Acts to the “taxable facts” which apply in each year of income, to use the language of Barwick C.J. in Bailey v Federal Commissioner of Taxation (1977) 136 CLR 214. The Deed of Rectification, executed in 2018, in and of itself cannot change or alter those taxable facts.

50 My conclusion is supported by Federal Commissioner of Taxation v Thomas (2018) 264 CLR 382. In that case, the taxpayer obtained from the Supreme Court of Queensland certain “directions” (in the form of declarations) as to the construction of resolutions made by a trustee to distribute net income comprising, amongst other things, certain franking credits. It was contended that these directions bound the Commissioner in his application of Div 207 of Pt 3-6 of the 1997 Act (which contains rules setting out the effect of receiving a franked dividend). That was because, it was said, of the High Court’s decision in Executor Trustee and Agency Co of South Australia Ltd v Deputy Federal Commissioner of Taxes (SA) (1939) 62 CLR 545. That submission was rejected by the High Court. Kiefel C.J., Bell, Keane, Nettle, Gordon and Edelman JJ. said at 407-408 [54]-[55]:

Executor Trustee is authority for the proposition that the general law rights of trustee and beneficiary inter se, to the extent that they are defined by a decision made in duly constituted proceedings, are defined as against the Commissioner unless the decision is set aside. In Executor Trustee, the earlier proceedings had determined rights inter se. There was no question of res judicata or of issue estoppel, and the separate declaration did not generate rights in rem against third parties. And, importantly, the earlier proceedings did not determine the application of the taxation law to those rights.

It follows that Executor Trustee is not authority for the proposition that the Commissioner, or a court under Pt IVC, should determine the application of the taxing acts otherwise than according to law. “When the revenue authorities come to impose a tax in relation to such rights [defined by order of the court], they must ... take them as they in fact actually exist between the parties” (emphasis added). But directions made under the equivalent of s 96 of the Trusts Act do not bind the Commissioner in the application of the taxation laws.

(Emphasis in original and footnotes omitted.)

51 Whilst the Deed of Rectification cannot bind the Commissioner, it was received into evidence, and, in my view, was otherwise able be relied upon by the taxpayer as evidence of the mistake that had been made about the identity of the trustee of the MJH Superannuation Fund.

52 Fourthly, I do not think that the observations of Hill J. in Davis, supra, are necessarily inconsistent with Thomas. The point made by his Honour in that case is that a deed of rectification in relation to an agreement is effective in a tax appeal if all it does is “record that agreement as it always was”. In other words, it will be efficacious if the taxpayer otherwise proves that it confirms a taxable fact which had not been correctly recorded.

53 Finally, I note that the learned primary judge would have made orders rectifying the MJH Fixed Trust Deed pursuant to s 32 of the Federal Court of Australia Act 1976 (Cth) but for his conclusion concerning the construction of that deed. I respectfully agree that this Court probably had jurisdiction to make orders for rectification on the basis of associated jurisdiction. However, it would not, in any event, have been appropriate for this Court to have made orders for rectification in circumstances where such relief had not been formally sought and the facts which might have supported the granting of such relief had never been pleaded. In my view, in a case such as this, a taxpayer seeking orders for rectification should do so by instituting separate proceedings against the Commissioner pursuant to s 39B of the Judiciary Act. It should ordinarily file and serve an originating application setting out the precise form of rectification sought and this should be accompanied by a statement of claim which sets out the material facts in support of rectification, in particular a statement of the subjective intention of the maker or makers of the instrument in question or, in an appropriate case, an affidavit addressing those matters.

Clause 20 of the MJH Fixed Trust Deed

54 The Commissioner had submitted below that the trustee of the MJH Superannuation Fund never held an entitlement to acquire the assets of the MJH Fixed Trust because cl 20.2 in the deed for that trust provided that the option to acquire such assets had to be exercised by the giving of notice by both the First and Second Absolute Beneficiaries. This followed, it was said, from the definition of “Absolute Beneficiary” in the Deed. The point was pressed on appeal.

55 In my view, the learned primary judge correctly rejected this submission. The Commissioner’s construction of cl 20.2 would defeat the very purpose of the conferral by cl 20.1 upon the Second Absolute Beneficiary of “an option to purchase any asset forming part of the Trust Fund”. It would render that option nugatory. For this reason, and for the reasons given by the learned primary judge set out above, the better view is that the reference to the “Absolute Beneficiary” in cl 20.2 of the deed is to the Second Absolute Beneficiary who must sign the notice in writing in order to exercise the option conferred by cl 20.1.

Taxpayer’s Alternative Position

56 The taxpayer submitted that even if the Court were to construe the definition of the Second Absolute Beneficiary in the MJH Fixed Trust Deed as referring to Grawlex simpliciter, it should nonetheless conclude that Grawlex held its beneficial interest in the MJH Fixed Trust on trust for the MJH Superannuation Fund such that s 102P(2) would still apply.

57 The taxpayer’s contention was that because, on this assumption, Grawlex took its beneficial interest in the MJH Fixed Trust as a volunteer, and subject to notice that it was to be held “as trustee of the MJH Superannuation Fund”, equity would have imposed a constructive trust over that interest in favour of that fund. The taxpayer relied upon the decision of the Victorian Supreme Court in Konann Pty Ltd v Commissioner of State Revenue [2015] VSC 23; (2015) 100 ATR 772 (“Konann (VSC)”), upheld by the Victorian Court of Appeal in Commissioner of State Revenue v Konann Pty Ltd [2015] VSCA 278; (2015) 101 ATR 800. The Court was referred to [50]-[51] of the judgment of Croft J. in Konann (VSC) as follows:

A constructive trust is properly described as “a remedial institution which equity imposes regardless of actual or presumed agreement or intention (and subsequently protects) to preclude the retention or assertion of beneficial ownership of property to the extent that such retention or assertion would be contrary to equitable principle”. While it is “remedial” in character, a constructive trust can arise by operation of law from the time at which the relevant circumstances occurred, and its existence does not depend on a prior declaration or order by a court. It follows that “the decree recognises and enforces the trust, but does not create it; the trust arises immediately the circumstances exist in respect of which equity would construe a trust”.

The proper analysis of the circumstances in which a constructive trust may arise in relation to the receipt of trust property raises some debate as to whether a constructive trust arises or whether equity intervenes simply to protect an existing beneficial interest. Thus, in these circumstances, reference has been made to a “borderline” category of constructive trust, in that it is as much a consequence of the continued enforcement of the pre-existing trust against the recipient of the trust property rather, perhaps, than a fresh trust arising. Thus the statement is made in Jacobs’ Law of Trusts:

‘The second borderline category [of constructive trust] concerns third parties who have received trust property in such circumstances that equity will hold them bound by the trust. While the third parties are often called constructive trustees, they are more properly treated as persons against whom the beneficial interest under the primary trust persists because they cannot set up a title as a bona fide purchaser of the legal title without notice. The third party will be subjected to the prior beneficial interest not so much by dint of the imposition of a fresh trust as by the operation against them of the rules as to priority between legal and equitable titles.’

A similar point was made in a previous edition of Lewin on Trusts, describing situations in which the trust estate passes into the hands of a volunteer or a purchaser for value with notice as “cases rather of an existing trust continued and kept on foot than of a new trust created”. In Scott and Ascher on Trusts, the authors state that “[t]he principle that a transferee of trust property who has notice of the trust at the time of transfer takes subject to the trust is so well established that it is unnecessary to cite the numerous cases that so hold”. Similarly, in relation to volunteers or “donees”, the authors state that “it is well-settled law that, when a trustee in breach of trust transfers trust property to one who pays no value, the transferee takes subject to the trust, even if the transferee is without notice of the breach of trust or the existence of the trust”. In any event, whichever perspective is adopted in the analysis, equity will protect the interest of the beneficiary in trust property against the world, rather than against the bona fide purchaser without notice.

(Footnotes omitted.)

58 Counsel for the taxpayer, in my view, properly conceded that the factual substratum of the present case does not sit precisely within the contours of the situations contemplated in Konann (VSC) and the authorities cited therein. He nevertheless invited the Court to find that a trust sprang into existence based on the principles set out above. Given the constructional choice I have adopted with respect to the MJH Fixed Trust Deed, the elasticity of those principles need not be tested on this occasion to determine the appeal. If it matters, and with respect, the taxpayer’s contention under this alternative scenario would probably fail for two reasons:

(1) first, it did not identify any evidence concerning what notice Grawlex had when it was said to have become a beneficiary of the MJH Fixed Trust. In my view, the words in the definition of the Second Absolute Beneficiary which identify the capacity in which Grawlex was to hold its beneficial interest, fall short of demonstrating such notice. Leaving aside what type of notice would be required (cf Farah Constructions Pty Ltd v Say-Dee Pty Ltd (2007) 230 CLR 89), I am also not inclined to infer the existence of notice from the fact that Hayes family members, and in particular Mr Michael Hayes, were directors and shareholders of Grawlex. I do not know enough about Grawlex, and the circumstances in which it was named a beneficiary to make a positive finding about notice, especially given that the trial judge made no finding about that matter; and

(2) secondly, the taxpayer did not really demonstrate or explain that, if Grawlex held its beneficial interest on trust for the MJH Superannuation Fund, it did so on terms that ensured that the trust was a complying superannuation fund for the purposes of s 45 of the Superannuation Industry (Supervision) Act 1993 (Cth). It may be one thing to decide that Grawlex held its interest in the MJH Fixed Trust on trust for the Fund; it is quite another matter to conclude that this trust comprised a complying superannuation fund.

Section 102P(10) of the 1936 Act

59 It will be recalled that the learned primary judge had decided that the trustee of the MJH Superannuation Fund was deemed by reason of s 102P(10) to be the holder of the units held by the MJH Fixed Trust in the MJH Trading Trust. That was because his Honour, for the purpose of applying s 102P(10), was satisfied that:

(a) there were units in a unit trust held by the trustee of another trust. Here those units were the 20 units held by the MJH Fixed Trust in the MJH Trading Trust; and

(b) the trustee of the MJH Superannuation Fund was a person “who has a beneficial interest in property” of the MJH Fixed Trust. As such, in accordance with the language of s 102P(10) it was deemed “to hold those units” – i.e. all of the 20 units.

60 In reaching this conclusion, the learned primary judge was influenced by the use in s 102P(10) of the indefinite article in the identification of the beneficial interest held by the applicable beneficiary: see [98] set out above. This part of the taxpayer’s argument is an alternative to its contentions concerning the operation of cl 20 of the MJH Fixed Trust Deed and the construction of the definition of the Second Absolute Beneficiary. As I have accepted those contentions, it is strictly unnecessary for me to consider the application of s 102P(10). As this matter was, however, fully argued, I shall briefly consider it. For the reasons which follow, I respectfully disagree with the learned primary judge.

61 The Commissioner’s construction of s 102P(10) commenced with an identification of its purpose. He relied upon the Explanatory Memorandum which accompanied the introduction of the Taxation Laws Amendment Bill (No.4) 1985 (Cth). Upon enactment, this Bill introduced Div 6C to the 1936 Act. Relevantly, on page 84, the Explanatory Memorandum states:

Sub-section 102P(10) is designed to allow the beneficial ownership of units in a unit trust to be traced through any interposed trusts to the ultimate beneficiaries.

Being a provision to facilitate the tracing of ultimate beneficial ownership, it made no sense, the Commissioner submitted, to read s 102P(10) in a way which would enlarge effectively the beneficial interest enjoyed by the ultimate beneficiary. Here, he submitted s 102P(10) has the effect of deeming the trustee of the MJH Superannuation Fund to hold 5% of the 20 units held by the MJH Fixed Trust in the MJH Trading Trust, and no more.

62 In contrast, the taxpayer submitted that the conclusion reached by the learned primary judge is entirely consistent with the concept of tracing of ownership interests. Here, it submitted, there has been a tracing to the underlying superannuation fund.

63 I wish to make two observations.

64 First, something should be said about the phrase “beneficial interest in property of that other trust estate” in s 102P(10) as it was raised by the Court, which referred the parties to CPT Custodian Pty Ltd v Commissioner of State Revenue (Vic) (2005) 224 CLR 98 and to Carter Holt Harvey Woodproducts Australia Pty Ltd v Commonwealth [2019] HCA 20; (2019) 93 ALJR 807. In supplementary submissions filed with the Court, the Commissioner submitted as follows:

In this context the term “beneficial interest” in s102P(10) is not used to describe the state of having an ‘interest’ (noting the very wide and general meaning of ‘interest’) at a level of a proprietary right. Although a trustee’s right of indemnity has priority to the beneficiaries’ interest in the property of a trust, this does not affect the existence of the relevant “beneficial interest” that the beneficiaries have in the property of the trust as contemplated by s102P(10). Although as a general principle it might be “impossible to say what [a] trust fund is” until a right of indemnity has been satisfied, that is not relevant to the concept of a “beneficial interest” in the property of the trust for the purposes of this section.

(Footnotes omitted.)

As I understood it, the taxpayer agreed with this construction of s 102P(10). In its supplementary submissions it said:

[The taxpayer] agrees with [the foregoing paragraph] of the [Commissioner’s] Supplementary Submission that although a trustee’s right of indemnity has priority to the beneficiaries’ interest in the trust property, this does not affect the existence of the relevant “beneficial interest” that the beneficiaries have in the trust property for the purposes of s 102P(10). Section 102P(10) does not require that the beneficial interest should be ascertainable, or indefeasible, or that the beneficiary must have a right to demand an immediate transfer of the trust property. It merely requires that the beneficiary has a beneficial interest in the trust property, a requirement that the Absolute Beneficiaries satisfied in this case.

(Footnotes omitted.)

65 The taxpayer also observed that the terms of the MJH Fixed Trust were very different from the terms of the trust considered by the High Court in CPT Custodian Pty Ltd. I agree with that observation. In that respect, cl 2.4 of the MJH Fixed Trust Deed provides:

Notwithstanding any powers conferred upon the Trustee by this Deed or otherwise by law the Trustee shall be taken, at all times, to be holding the Trust Fund as a bare trustee for the Absolute Beneficiaries in proportion to the Share of each Absolute Beneficiary.

The foregoing clause is quite unlike that considered by the High Court in CPT Custodian Pty Ltd. In my opinion, like the deed considered in Charles v Federal Commissioner of Taxation (1954) 90 CLR 598, each of the Absolute Beneficiaries here had the right, perhaps subject to any undischarged right of indemnity held by the trustee, to come together and call for the assets of the MJH Fixed Trust to be transferred to them.

66 In my view, it would not be appropriate for me to consider further how the phrase “beneficial interest in property” is to be construed in light of the subsequent decisions of the High Court in CPT Custodian Pty Ltd and in Carter Holt Harvey Woodproducts Australia Pty. That is because the parties agreed that the trustee of the MJH Superannuation Fund held such an interest in the property of the MJH Fixed Trust.