FEDERAL COURT OF AUSTRALIA

PKT Technologies Pty Ltd (formerly known as Fairlight.Au Pty Ltd) v Peter Vogel Instruments Pty Ltd [2019] FCAFC 216

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Order 1 made by the primary judge on 23 October 2018 be set aside and in lieu thereof there be an order as follows:

1. There be judgment for the first respondent/cross-claimant against the applicant/first cross-respondent in the amount of $366,158.50 (exclusive of interest).

2. The appeal by PKT Technologies Pty Ltd (formerly known as Fairlight.au Pty Ltd) (Fairlight) be otherwise dismissed.

3. The cross appeal by Peter Vogel Instruments Pty Ltd (PVI) be dismissed.

4. Fairlight file and serve on or before 10 December 2019 written submissions limited to three pages as to the order(s) which should be made as to costs and the reasons therefor.

5. PVI file and serve on or before 16 December 2019 written submissions limited to three pages in response to Fairlight’s submissions.

6. Fairlight, if so advised, file and serve on or before 19 December 2019 written submissions limited to two pages in response to PVI’s submissions.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

BESANKO AND BANKS-SMITH JJ:

1 We have had the advantage of reading the reasons for judgment of Stewart J. Subject to one matter, we agree with his Honour’s reasons. The matter upon which we disagree with Stewart J relates to the appeal by PKT Technologies Pty Ltd (formerly known as Fairlight.Au Pty Ltd) (Fairlight) against the primary judge’s award of profits for the infringement of the registered trade mark (see PKT Technologies Pty Ltd (formerly known as Fairlight.Au Pty Ltd) v Peter Vogel Instruments Pty Ltd [2018] FCA 1587; 135 IPR 463). Unlike Stewart J, we would dismiss the challenge by Fairlight to the primary judge’s award.

2 In our opinion, the primary judge dealt with the arguments presented to him and those arguments were the arguments repeated on the appeal to this Court. His Honour has not been shown to have erred in his treatment of those arguments. Section 228 of the Trade Marks Act 1995 (Cth) was not relied on before the primary judge. It was referred to in passing when it was said that the principle upon which Fairlight relied i.e., the statement in Davison M J and Horak I, Shanahan’s Australian Law of Trade Marks and Passing Off (6th ed, Thomson Reuters, 2016) (Shanahan’s) (set out below at [13]) was consistent with s 228. The arguments of Fairlight were advanced by reference to that statement. Furthermore, to the extent that it might be said that s 228 has been alluded to in the submissions made on the appeal, it is to be noted that, in any event, this Court has not had the benefit of fully developed submissions on the scope and operation of s 228. A matter not clearly argued below and not the subject of developed submissions in this Court should not, in our respectful view, be entertained. Experience shows that what might appear clear without the benefit of full submissions and the citation of relevant authorities may well, at the least, be much less so after that is done.

3 The starting point is the evidence and submissions put to the primary judge. Fairlight tendered expert evidence from Ms Elizabeth Jean Smith to the effect that the proceeds of sales of the Fairlight CMI App for the period from March 2011 to 30 June 2012 to customers in Australia and in overseas countries totalled $137,485.30. At the conclusion of the hearing before the primary judge, both parties relied on more than one set of written submissions. It seems that in the first half of May 2017, Peter Vogel Instruments Pty Ltd (PVI) made a short submission to the effect that with respect to the infringement of trade mark, there was no evidence of sales in Australia. Fairlight made written submissions to the primary judge in the second half of May 2017 which contained a reference in a footnote to written submissions made at the original trial nearly two-and-a-half years earlier. Those earlier written submissions made reference to s 228, but even in those submissions, the emphasis was on sales, offers for sale, or marketing or promotion in Australia. In any event, when the issue of extraterritoriality specifically arose in late May/early June 2017, Fairlight filed its submissions dated 6 June 2017. The primary judge was entitled to proceed on the basis that those submissions were Fairlight’s submissions on the topic. The contents of those submissions relevant to the present point were as follows.

4 Fairlight filed short submissions on 6 June 2017. The submissions contained the following:

6. Consistent with section 228(1) of the Act, as noted in Shanahan’s:

It would appear there can be use in Australia for the purposes of the Act when a sale or offer for sale occurs in Australia but the goods are located, or the services will be provided, abroad.

7. PVI asserts, by reference to data maintained by Apple, that sales of the Fairlight App occurred overseas. This says nothing about the location of the infringing use. It also says nothing about the location of where the transaction took place or the mechanism as to how it occurred. PVI, who seeks to pare back the account by reference to allegedly overseas sales, bears the onus of establishing these matters. It has failed to do so. Submissions are not evidence and merely because a sale occurs to someone in the USA or elsewhere does not establish that the offer for those goods (and/or the sale) has not taken place in Australia.

(Emphasis added.)

5 The submissions then go on to assert that it is sufficient if the act of marketing or the act of offering for sale took place in Australia, even if the actual contract of sale took place overseas. That position certainly, insofar as it refers to offers for sale, is consistent with the statement in Shanahan’s. Fairlight then made these submissions:

11. PVI is an Australian company, which conducted its business in Australia and received income in Australian dollars into a bank account in Australia from its misuse of the Fairlight trade mark. PVI applied the trademark to the Apps, and used the trade mark, in the course of its business, by uploading the Apps in Australia. Any sales by Apple were on the instruction, or at the direction, of PVI in the course of its business in Australia and, after the App was uploaded, PVI caused Apple to continue selling the Apps.

12. In conducting its business in Australia, and consistent with PVI having told the AAT that it sold the Apps, PVI allowed an intermediary to sell the App on its behalf and remit the revenue (after a deduction made by Apple) to PVI. Indeed, there has been a declaration that PVI’s infringement involved it using the trade mark in the course of trade and it marketing and selling Apps, and a finding that it infringed by using the trade mark in Apps. Consequently, PVI must account for all profits made from sales of the Apps. As noted by Windeyer J in Coldbeam the infringer must “give up his ill-gotten gains to the party whose rights he has infringed”.

(Footnotes omitted.)

6 In our opinion, it is clear from these submissions that there was no direct reliance on s 228 at all. Fairlight was, in fact, basing its argument on the statement in Shanahan’s.

7 The reasoning of the primary judge on this issue was as follows.

8 The primary judge noted that Fairlight contended that the total sales of the Fairlight App made by PVI during the relevant period was $137,485 (at [131]). PVI contended that of the total sales made, only $9,357 worth related to sales made to Australian consumers (at [132]). The primary judge found that $9,808 worth of sales related to sales made to Australian consumers and that the balance related to sales made to customers in other countries (at [133]). The first question before the primary judge was whether the starting point for calculating the profits for which PVI was liable to account was the total sales of ($137,485) or merely Australian sales ($9,808). The primary judge referred to ss 20, 120(1) and 126(1) of the Trade Marks Act.

9 The primary judge referred to the presumption that general words used in a statute are interpreted to apply within territorial limits (at [137]). His Honour saw nothing in the Act which might lead to the conclusion that that presumption had been rebutted.

10 The primary judge said that it was well-established that a person may infringe a registered mark by using it in relation to goods that he or she exports for sale abroad (at [138]). The primary judge said that similarly, a person outside Australia may also infringe a registered mark by taking orders from Australian customers for goods that he or she proposes to export to Australia. That was because in each case there would have been a use by that person of the registered trade mark within Australia. The primary judge considered that the present case was “rather different” (at [138]).

11 The primary judge said that in this case, Fairlight sought to recover profits made from sales made by PVI in other countries in which there could never have been any infringing use of the registered trade mark (at [139]). His Honour said that selling goods, or offering them for sale, in a foreign country under or by reference to a particular trade mark, did not constitute an infringing use of the trade mark registered under the provisions of the Trade Marks Act.

12 Fairlight submitted that the declaration made by the Full Court in Peter Vogel Instruments Pty Ltd v Fairlight.Au Pty Ltd [2016] FCAFC 172; 343 ALR 387 was not limited to the use of the registered trade mark within Australia. The primary judge rejected that submission for the reason he gave (at [140]) and there is no challenge to that particular conclusion.

13 The primary judge then noted (at [141]) that Fairlight relied on the following statement in Shanahan’s at p 53:

It would appear there can be use in Australia for the purposes of the Act when a sale or offer for sale occurs in Australia but the goods are located, or the services will be provided, abroad.

(Footnote omitted.)

14 It may be noted at this point that this quotation is taken from the reasons for judgment of Williams J in Re the Registered Trade Mark “Yanx”; Ex parte Amalgamated Tobacco Corporation Ltd [1951] HCA 28; 82 CLR 199 at 204–205. It appears in the section in Shanahan’s under the heading “Export”. Section 228(1) of the Trade Marks Act is referred to in this section.

15 The primary judge said that he respectfully agreed with the statement in Shanahan’s, but it was concerned with the question of trade mark use and nothing more (at [142]). The primary judge noted that there was no issue in this case that there was a use of the Fairlight mark in Australia. His Honour referred to the decision of Merkel J in Ward Group Pty Ltd v Brodie & Stone Plc [2005] FCA 471; 143 FCR 479 at [36]–[43]. His Honour said there was no doubt that PVI authorised the use of the Fairlight mark in Australia on the Apple iTunes website which was directed to (inter alios) consumers in Australia. He said that despite the fact that there was no issue that there was use of the Fairlight mark in Australia, it did not follow that Fairlight could recover from PVI the profits from sales the latter made in other countries unless it is shown that they arose out of offers to sell that were made in Australia.

16 The primary judge went on to address a submission by Fairlight that the profits obtained by PVI from the sales of the Fairlight Apps to consumers in Australia and other countries overseas were profits attributable to the infringing use. His Honour said that, as he understood the submission, an inference should be drawn that the sales made to customers in other countries were the result of infringing use “(presumably in advertising and promotions)” that occurred in Australia. The primary judge said that while he did not think it was open to serious dispute that sales made to Australian consumers were the result of infringing use, “the evidence does not permit such a conclusion to be drawn in respect of sales to customers in other countries” (at [143]).

17 The primary judge concluded that he was satisfied that the profits which Fairlight were entitled to recover were confined to those made by it from sales to Australian consumers (at [144]).

18 Ground 5 of Fairlight’s Notice of Appeal is in the following terms:

5. The trial judge erred in awarding the Appellant $9,808 (exclusive of interest) by reason of the Respondent having infringed its trademark by unlawful sales of Apps, rather than the amount of $137,485, by:

(a) failing to address, or address adequately, the relevant evidence; and

(b) failing to give adequate or proper reasons.

19 Its written outline of submissions with respect to this topic were very brief. They were as follows:

Ground 5: award of $9,808 for infringement of Fairlight.au’s trademark

38. In awarding Fairlight.au $9,808, rather than $137,485, for PVI’s infringement of its trademark, the Remittal Judge failed to address the submissions advanced by Fairlight.au that PVI conducted its business in Australia, received taxable income in Australia, and was paid in Australian dollars into a bank account in Australia.

39. The Remittal Judge, with respect, failed to address, adequately or at all, the relevant evidence, and also erred by failing to give adequate or proper reasons.

(Footnote omitted.)

20 The written outline of submissions contains a reference by way of a footnote to submissions lodged by PVI, not Fairlight, pursuant to leave granted on 23 May 2017. We think this is an error and the reference is intended to be to Fairlight’s submissions dated 6 June 2017 pursuant to the leave granted by the primary judge on 23 May 2017.

21 The thrust of Fairlight’s oral submissions on the appeal is contained in the following passage:

Now, we say that – we say that as a matter of substance rather than form the fact that the app was developed here, it was placed on a computer here, that the company was here, that it was selling them from here, that it was receiving the income here, was banking into account [sic], the fact that it puts it on a server that may distribute it in a world-wide fashion, it is a – we say, with respect to his Honour’s observation, it is entirely artificial to say in those circumstances, if I am in my living room in the – or I’m in my office in the CBD and I breach someone’s trademark by doing all those things and reaping the rewards here, that I’m not making an offer to sell in Australia, albeit the fact that someone in Iceland, for example, may be downloading it on their computer screen there. We’re either right or wrong about that. That’s our submission.

(Emphasis added.)

22 The passage which we have emphasised is significant because it shows that, consistent with its submissions to the primary judge, Fairlight’s submissions proceed, and have proceeded, on the basis that, absent proof of a sale in Australia, it must show that it was making an offer to sell in Australia in relation to customers who download their App in countries other than Australia. The primary judge rejected that argument because, as his Honour put it, the evidence did not permit such a conclusion in respect of sales to customers in other countries which we take to mean a conclusion that such sales arose out of offers to sell that were made in Australia or advertising and promotions that occurred in Australia. That factual conclusion about sales, offers for sale and marketing or promotions in Australia has not been shown to be wrong.

23 Fairlight’s challenge to the primary judge’s award for trade mark infringement must be dismissed.

24 In our opinion, the orders which should be made are as follows:

(1) Order 1 made by the primary judge on 23 October 2018 be set aside and in lieu thereof there be an order as follows:

1. There be judgment for the first respondent/cross-claimant against the applicant/first cross-respondent in the amount of $366,158.50 (exclusive of interest).

(2) The appeal by PKT Technologies Pty Ltd (formerly known as Fairlight.au Pty Ltd) (Fairlight) be otherwise dismissed.

(3) The cross appeal by Peter Vogel Instruments Pty Ltd (PVI) be dismissed.

(4) Fairlight file on or before 10 December 2019 written submissions limited to three pages as to the order(s) which should be made as to costs and the reasons therefor.

(5) PVI file on or before 16 December 2019 written submissions limited to three pages in response to Fairlight’s submissions.

(6) Fairlight, if so advised, file on or before 19 December 2019 written submissions limited to two pages in response to PVI’s submissions.

I certify that the preceding twenty-four (24) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justices Besanko and Banks-Smith. |

Associate:

Dated: 5 December 2019

REASONS FOR JUDGMENT

STEWART J:

INTRODUCTION

25 This appeal and cross-appeal concern questions of quantification of contractual damages, damages and liability for copyright infringement, and damages for trade mark infringement.

26 This is the second time this dispute has come to the Full Court. Relevantly, its history includes a trial before Edmonds J (the trial judge) whose judgment is reported as Fairlight.AU Pty Ltd v Peter Vogel Instruments Pty Ltd (No 3) [2015] FCA 1422; 116 IPR 118, an appeal to the Full Court constituted by Besanko, Edelman and Burley JJ whose judgment is reported as Peter Vogel Instruments Pty Ltd v Fairlight.Au Pty Ltd [2016] FCAFC 172; 343 ALR 387, and a remittal hearing on limited issues relating to the quantification of damages before Nicholas J (the remittal judge) whose judgment is reported as PKT Technologies Pty Ltd (formerly known as Fairlight.Au Pty Ltd) v Peter Vogel Instruments Pty Ltd [2018] FCA 1587; 135 IPR 463. This is an appeal and cross-appeal from the judgment on remittal.

Factual Background

27 The relevant factual findings, which were not disturbed in the first appeal, are set out in the judgment of the trial judge at [1]-[30]. They are further summarised in the judgment of the Full Court at [1]-[19]. No purpose is served in repeating them at any length. For present purposes, the following summary will suffice.

28 In 1975, Peter Vogel, an electronics engineer, co-founded a company called Fairlight Instruments Pty Ltd with which he remained associated for approximately 14 years. In 1979, Fairlight Instruments developed the world’s first digital music synthesiser capable of sampling natural or instrumental sounds. It was known as the Fairlight Computer Musical Instrument, or the Fairlight CMI. Mr Vogel enjoys a reputation as a co-founder of Fairlight Instruments and as the designer of the Fairlight CMI.

29 PKT Technologies Pty Ltd (formerly known as Fairlight.Au Pty Ltd and which is referred to as Fairlight hereafter) was incorporated in 2003. Fairlight is the owner of the Fairlight trade mark in Australia. From August 2010 onwards Fairlight was controlled by KFT Investments Pty Ltd.

30 In 2009, Mr Vogel decided to build a 30th anniversary commemorative version of the Fairlight CMI. He entered into negotiations with Fairlight aimed at facilitating the production of the commemorative version which he called the Fairlight CMI-30A. A new company, Fairlight Instruments Pty Ltd, was established by Mr Vogel in October 2009. The name of this company was subsequently changed to Peter Vogel Instruments Pty Ltd (PVI). As a result of these negotiations, PVI and Fairlight entered into a written agreement titled “Development and Licensing Agreement” dated 15 August 2010.

31 The Agreement contemplated PVI producing the CMI-30A and a personal computer compatible version thereof known as the Series IV or CMI-IV, which were collectively referred to as the “CMI Products”. For that purpose Fairlight would provide to PVI customised software developed for the CMI Products and a licence for the use of the Fairlight mark for the CMI Products, and it would supply core components for those products.

32 PVI agreed to pay Fairlight $200,000 plus GST by way of four equal instalments. Fairlight agreed to produce the core components and the necessary software for PVI and to transfer the software and its source components to PVI.

33 Between February 2011 and April 2012, PVI made payments totalling $200,000 plus GST to Fairlight in satisfaction of its payment obligations under the Agreement.

34 From August 2010 to May 2012, PVI promoted the CMI-30A, including at the National Association of Music Merchants annual music trade shows in Los Angeles.

35 During this period, development of the software by Fairlight to be used in the CMI-30A progressed. PVI was unhappy with the progress of the CMI-30A software development and made this known to Fairlight on multiple occasions.

36 In March 2011, PVI issued an information memorandum in which it sought to raise $500,000 through a share placement. PVI required this capital to develop the CMI Products and other products including applications (Apps) for both iPhone and iPad which were promoted and sold on the Apple iTunes store under the Fairlight trade mark. The Apps could be purchased and downloaded by customers in many countries including Australia. As will be seen, the financial projections in the information memorandum are at the heart of PVI’s claim for damages.

37 In May 2012, PVI received a letter from Fairlight purporting to terminate the Agreement and withdraw the trade mark licence.

38 Before the purported termination of the Agreement by Fairlight, PVI had sold a total of 14 CMI-30As to customers with the majority (10) ordered in or around March 2011.

39 By July 2012, when PVI ceased using Fairlight’s trade mark to sell Apps, it had received $137,485 in its Australian bank account from sales of the Apps.

40 From 2007, Fairlight sold software known as ‘Dream II’ as part of the ‘Crystal Core’ CC-1 card. Customers who purchased a CC-1 card had the capability to further upgrade to Version 3.2 of the ‘Dream II’ software. Included in this version of Dream II was software which was called ‘Sound Design Sampler’ (SDS). Fairlight later admitted in its defence to the cross-claim that the SDS software included source code which was written for PVI for the CMI-30A. The SDS software was provided by Fairlight to two third parties after April 2012, i.e. after the final payment by PVI under the Agreement.

Procedural History

The trial judgment

41 The trial judge found that by the terms of the Agreement, PVI was granted a licence to use the Fairlight trade mark worldwide, but only in relation to two products being the CMI-30A and the Series IV. From this finding it was clear that PVI had breached the terms of the trade mark licence by developing the Apps and marketing them under the Fairlight name. The trial judge rejected the proposition from PVI that the Apps were solely for the purpose of marketing the CMI-30A and Series IV, or that Fairlight had entered into a binding oral agreement with PVI which allowed it to use the trade mark for the Apps. It was found that the Agreement had been validly terminated by Fairlight on 30 May 2012 as a result of the trade mark breach by PVI.

42 PVI also made cross-allegations in the primary proceeding that Fairlight had by its purported letter of termination invalidly repudiated the contract and defaulted on various requirements of the contract including by delay and deficiency in the development and provision of the software. The trial judge rejected the claim of deficiency as being without substance because the words of the Agreement contained no obligations or implied terms to provide software of the claimed types or functions. The delay claim was also rejected, as was the repudiation claim.

43 The trial judge also rejected PVI’s claim that it was entitled to damages for infringement of its copyright over the software developed by Fairlight for the purposes of the Agreement but used by Fairlight for its own purposes.

The first appeal

44 The Full Court rejected PVI’s appeal against the primary judge’s finding that the development and sale of the Apps had infringed the trade mark licence conferred by the Agreement.

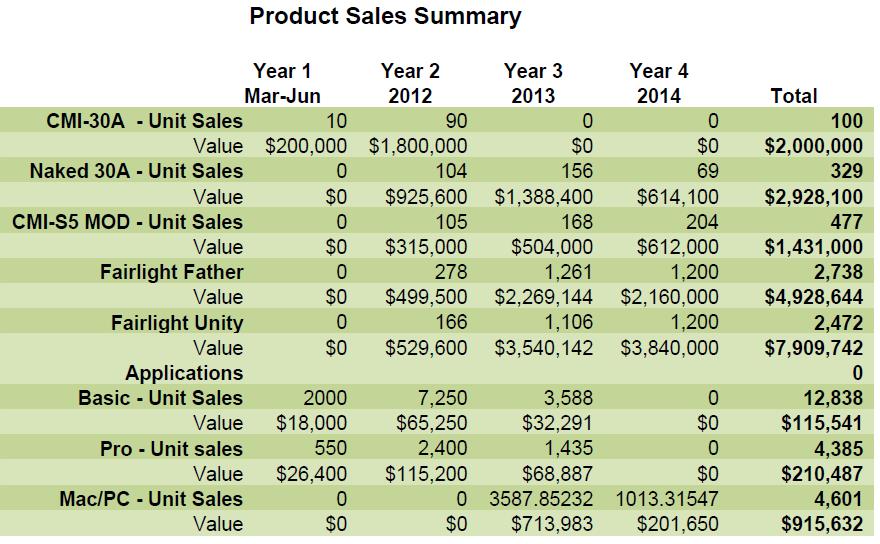

45 The Full Court upheld PVI’s appeal on the question of copyright, finding that the primary judge erred in finding that PVI was not entitled to damages for infringement of copyright. It went on, however, to find that the copyright infringement was only established over two products containing infringing SDS software licences sold after the date on which the copyright assignment took effect.

46 The final distilled issue upon which PVI appealed from the judgment of the trial judge was that the purported termination of the Agreement on 30 May 2012 was not valid. The Full Court in allowing the appeal on this ground found that the withdrawal of the trade mark licence by Fairlight was not the end of the Agreement between the parties. On this basis the Full Court found that Fairlight had repudiated the Agreement by not performing after its withdrawal of the trade mark licence. PVI had accepted that repudiation and was entitled to damages.

47 The Full Court made declarations in substitution of the orders of the trial judge to the following effect:

(1) Fairlight had validly withdrawn the right for PVI to use the Fairlight name and brand by letter dated 30 May 2012;

(2) Thereafter PVI did not have any right, licence or authority to use the Fairlight name and brand with respect to the CMI Products;

(3) PVI contravened s 120 of the Trade Marks Act 1995 (Cth) by using the Fairlight trade mark from about March 2011 with respect to the Apps and in marketing and selling the Apps;

(4) PVI is the owner of the copyright in the software developed by Fairlight pursuant to the agreement; and

(5) Fairlight had, by the sale of two copies of the Dream II program to third parties after April 2012, infringed PVI’s copyright.

48 The Full Court remitted the matter to the primary judge for the purpose of determining:

(a) on the evidence adduced at the trial held in December 2014, and subject only to any order of the primary judge allowing further evidence to be adduced, any damages to which the cross-claimant is entitled for repudiation of the Agreement by the cross-respondent and infringement of copyright;

(b) taking an account of profits to which the applicant may be entitled for infringement of the FAIRLIGHT trade mark;

(c) the entitlement of the parties to costs on the claim and cross-claim; and

(d) the disposition of the proceedings.

The remittal proceeding

49 As Edmonds J had in the meantime retired from the Court, Nicholas J heard the remittal proceeding. No further evidence was adduced in the remittal proceeding. It was based on the evidence that had been adduced before the trial judge.

Damages for repudiation

50 PVI advanced its claim for damages for repudiation on the basis that PVI lost the chance to profit from further performance of the Agreement in the amount of $9.5 million. This was referred to as its expectation damages. In the alternative, if the Court could not be satisfied that the Agreement would have proven profitable, then PVI claimed reliance damages and mitigation losses in the amount of $1.28 million.

51 The remittal judge found (at [33]) that it was “extremely unlikely that PVI would have ever made a profit from the Agreement”, citing the issue that products outlined in the information memorandum on which the projected revenues were dependent were not subject to the licencing agreement – once the licensing agreement was validly terminated loss of revenue from those products could not be ascribed to repudiation of the Agreement (at [48]). His Honour went on to discount the amounts set out in the information memorandum on the basis that the reliability of the numbers was diminished by the poor actual sales of the CMI-30A and Series IV and the sales numbers also included products not within the scope of the trade mark licence. These findings led the remittal judge to reject PVI’s claim for expectation damages. His Honour then stated (at [54]):

But it does not follow that PVI is not entitled to recover any damages in respect of Fairlight’s repudiation of the agreement. As I will explain, this is a case in which I am satisfied that PVI was likely to have recouped some additional portion of the expenditure incurred by it in the course of its performance of the agreement had the agreement not been repudiated by Fairlight.

Reliance damages

52 Following this paragraph the remittal judge went on to assess what he called the “reliance damages”. His Honour first rejected (at [55]-[57]) the overarching submission by Fairlight that because PVI had sought “to prove and recover expectation or loss of profit damages” it was “precluded from making any claim for reliance damages”.

His Honour then assessed the reliance damages claim which was put forward by PVI with reference to the figures provided in a report of Fairlight’s expert before the trial judge, Mr Hood. The remittal judgment (at [59]) records PVI’s “reliance damages” to have been claimed as follows (with the last two columns of the table inserted by me to record the conclusions of the remittal judge in respect of each component, subject to a “lost opportunity” reduction dealt with further below, and the paragraphs of the judgment from which the conclusions appear):

Description of Amounts | Claimed | Allowed | Remittal judgment | |

(a) | Mr Hood’s reliance damages | $508,724 | *$508,724 | [60]-[61], [84] |

(b) | Mr Hood’s mitigation costs | $209,860 | nil | [79]-[80] |

(c) | Additional mitigation costs | $66,484 | $36,566 | [83] |

(d) | R&D costs | $472,575 | *$472,575 | [61-63], [71]-[72], [84] |

Total damages | $1,257,643 | $330,956 |

* ultimately allowed as to 30%, remittal judgment [92].

53 In fact, only items (a) and (d) were treated by the remittal judge as reliance damages, with (b) and (c) being treated as PVI’s claims for the expenses incurred by it in trying to mitigate the losses that it would otherwise have suffered as a consequence of the repudiation. It is apparent from the fact that the judgment (at [84]) arrived at a figure of $981,299 for “wasted expenditure”, that items (a) and (d) in the amounts reflected in the table were allowed and added together to arrive at that sum although, as will be seen, the reasoning of the remittal judge does not quite support these figures in full.

54 With respect to item (a), the remittal judge reasoned (at [60]) that Mr Hood had calculated PVI’s reliance damages at $508,724, although he had subsequently revised this figure to $504,635 which he proposed to accept. However, when the sum for this item was later added to the sum for item (d) the higher amount was used apparently in error, although Fairlight made no issue of this error of $4,089 against it, accepting that it was de minimis.

55 With respect to item (d), the remittal judge recorded (at [62]) that Mr Hood had calculated the research and development (R&D) expenditure as $472,575, although it was said (at [70]-[71]) that Mr Vogel’s unchallenged affidavit evidence was that the figure was $478,053. His Honour nevertheless apparently used the figure of $472,575 in his final calculations, which represents an error of $5,478 in Fairlight’s favour.

56 The remittal judge characterised (at [66]) the principal issue in relation to the R&D expenses as being one of causation, i.e. were those expenses reasonably incurred by PVI for the purpose of performing the agreement. The judge inferred (at [67]) that PVI would not have incurred those expenses had it not entered into the agreement with Fairlight. His Honour then accepted (at [68]) that R&D expenditure that related solely to the products the subject of the Agreement would be recoverable under either the first or the second limb of the rule in Hadley v Baxendale (1854) 9 Exch 341.

57 It was held (at [72]) that expenditure of $478,053 on R&D expenditure was not unreasonable for products that were forecast to generate sales revenue of $2 million over a 15 month period. Fairlight’s submission that the R&D expenditure may have produced something of value which should have been brought into account in determining whether the expenditure was wholly or partly wasted was rejected (at [73]-[74]).

58 As explained, by adding the figures in (a) and (d) in the table, the remittal judge (at [84]) arrived at a figure of $981,299 which he found had been expended on performing the Agreement (i.e. in reliance on it being performed by Fairlight) and which “might qualify for recovery of wasted expenditure”. However, his Honour found (at [84]) that it would be unjust to award the whole $981,299 because it is highly unlikely that all of that expenditure would have been recouped from performance of the Agreement had Fairlight not repudiated it. That approach was consistent with the earlier finding that PVI would not have made a profit on the Agreement which is why no loss of profits could be awarded (as explained at [51] above). Doing the best he could, with “a degree of guesswork and speculation”, in what he described as a “loss of opportunity analysis” the remittal judge (at [92]-[93]) allowed 30% of this figure, concluding that the reliance damages that were claimable were $294,390. The lost opportunity referred to was PVI’s lost opportunity to recoup at least some of its expenditure.

Mitigation costs

59 Item (b) in the table, being “Mr Hood’s mitigation costs”, was rejected (at [79]) on the basis that they were unsubstantiated. That was in particular because they were ultimately calculated on the basis of a mitigation strategy that would involve refunding customers on the 14 sales of the CMI-30As that had been sold, but there was no evidence that any refunds had actually been paid or that there was any liability to do so (at [77]-[79]).

Additional mitigation costs

60 Item (c) in the table, being “additional mitigation costs”, was explained (at [81]) as costs expended in a failed attempt to modify the software for the CMI-30A to work without the components Fairlight refused to supply. These costs were found to be $66,484 from which had to be deducted an amount of $29,918 that had been received for R&D tax incentives during the relevant year. The resultant figure that was allowed is $36,566. See the remittal judgment at [81]-[83].

Conclusion on damages for repudiation

61 The figure of $36,566 for additional mitigation costs was added (at [93]) to the reliance damages of $294,390, referred to above at [59], to arrive at a total figure of $330,956 as PVI’s damages for Fairlight’s repudiation of the Agreement.

Damages for copyright infringement

62 On the question of damages for copyright infringement, the remittal judge found (at [108]) that the compensatory damages available to PVI were limited to $3,000 on the basis of only two sales of the software at $1,500 each. However, his Honour went on to also award damages under s 115(4) of the Copyright Act 1968 (Cth) which allows the Court to make an award of additional damages if it is satisfied that it is proper to do so having regard to the particular matters referred to in the section and any other relevant matters. The remittal judge ordered that Fairlight pay $50,000, “a significant award of additional damages”, for what his Honour considered to be “a quite flagrant infringement of PVI’s copyright in the CMI-30A software”.

Damages for trade mark infringement

63 The remittal judge went on to determine the amount which should be awarded to Fairlight against PVI by way of account of profits for infringement of Fairlight’s registered trade mark. This account of profits resulted from the use by PVI of the Fairlight name in the sale of the Apps from March 2011 onwards. The remittal judge held (at [132]) that in relation to the total sales made of $137,485 which Fairlight sought an account of, only $9,808 worth related to sales made to Australian consumers. His Honour found that the relevant sections of the Trade Marks Act operate within territorial limits and that there is no requirement with reference to the purposes or policy of the Trade Marks Act to extend this territoriality. Because of this, it could not be said that there was an infringing use of the registered mark in this case because the selling and offering for sale of the goods was through the Apple iTunes website and therefore occurred in a foreign country. His Honour also rejected the proposition that the overseas sales were a result of the infringing use in Australia.

64 PVI had argued in the remittal hearing that any profits made by PVI from sales of the Fairlight Apps were not shown to be profits made as a result of selling the Fairlight Apps under the Fairlight name. After citing the reasons of Windeyer J in Colbeam Palmer Ltd v Stock Affiliates Pty Ltd [1968] HCA 50; 122 CLR 25 at 37-38, the remittal judge rejected the relevance of this contention (at [146]) stating:

I am satisfied that the Fairlight mark was used by PVI in relation to the Fairlight Apps for the purpose of conveying a false representation to potential purchasers that there was a connection between the Fairlight Apps and the owner of the Fairlight brand. At the very least this use was likely to indicate to potential purchasers that the Fairlight App was sold with the permission of the owner of the Fairlight brand.

65 Finally, his Honour went on (at [147]) to reject any claim by PVI for deduction from the account of profits for general business overheads stating that PVI had failed to “show (bearing in mind it has the onus) how and in what proportions various categories of its business overheads were attributable to the obtaining of the relevant profit”.

Conclusions on damages

66 The remittal judge disposed of the claims and cross claims at [148]-[149] stating:

148 It follows that there should be a judgment in favour of PVI against Fairlight for $383,956 (exclusive of interest) comprising:

(a) damages for wrongful repudiation in the amount of $330,956; and

(b) damages for copyright infringement in the amount of $53,000.

149 There will also be orders that:

(a) PVI pay to Fairlight the amount of $9,808 (exclusive of interest) being the profits attributable to PVI’s infringement of the registered trade mark;

(b) permit Fairlight to set-off that amount (and any interest thereon) against the judgment entered in favour of PVI.

67 Orders were made to the above effect.

THE PRESENT APPEAL AND CROSS-APPEAL

A preliminary issue

68 PVI was represented at the remittal hearing by Mr Vogel (as director of PVI) with the leave of the remittal judge (at [4]). PVI’s written submissions in the appeal and the cross-appeal bear Mr Vogel’s name as “Solicitor for the Respondent/Cross-Appellant”. When asked about this at the commencement of the hearing Mr Vogel explained that he had recently been admitted as a solicitor and holds a qualified practising certificate and he accordingly appeared for PVI as solicitor instructed by his supervising solicitor Mr Goldie. Mr Goldie sat at the bar table with Mr Vogel.

69 Because Mr Vogel has an obvious personal interest in the appeal through his interest in PVI he was asked by the Court whether he was aware of his duties and obligations under the solicitors’ rules. He answered affirmatively and assured the Court that he was well aware that he is an officer of the Court and that his first responsibility is to the Court.

70 In those circumstances, and mindful also of the cost and inconvenience to the parties and the Court of not proceeding with the hearing on the allocated date, the Court allowed Mr Vogel to appear on behalf of PVI.

Fairlight’s notice of appeal

71 Having abandoned a challenge to the remittal judge’s finding on “flagrant” copyright infringement, Fairlight advanced the following grounds of appeal:

(1) The judge should not have awarded PVI reliance loss damages because there was no evidence to establish that it had suffered such losses, and it failed to establish why it could seek reliance damages rather than the usual measure of expectation damages for repudiatory termination.

(2) The judge should not have awarded additional mitigation costs to PVI and should not have calculated mitigation damages by including amounts that concerned PVI’s costs of developing the Apps that it used unlawfully by infringing Fairlight’s trade mark.

(3) The judge should not have awarded $294,390 for loss of opportunity to PVI. It was contrary to the evidence that PVI had incurred further expenditure of $981,299 which might qualify for recovery as wasted expenditure. It was further wrong to reduce that amount by 30% in circumstances where there was no evidentiary basis for doing so. The judge also failed to give adequate or proper reasons in this respect.

(4) The judge should not have awarded Fairlight only $9,808 for PVI’s infringement of the trade mark by unlawful sales of the Apps and should rather have awarded the amount of $137,485.

PVI’s notice of cross-appeal

72 PVI’s notice of cross-appeal advanced the following grounds:

(1) The judge erred in finding that it was highly unlikely that PVI would ever have made a profit from the agreement had Fairlight not repudiated it, and accordingly erred by rejecting PVI’s claim for expectation damages.

(2) The judge erred by awarding only 30% of the wasted reliance damages of $981,299.

(3) The judge erred in ordering that PVI pay Fairlight $9,808 on account of profits for the infringement of Fairlight’s trade mark.

(4) The judge erred by failing to make KFT jointly liable for the damages for copyright infringement.

The issues for consideration

73 It is convenient to arrange the issues raised by the notice of appeal and cross-appeal in the following way and consider them in that order:

(1) First, PVI’s claim for expectation damages, which the judge rejected and which is the subject of PVI’s cross-appeal.

(2) Second, PVI’s claim for reliance damages, which the judge allowed in part and which is the subject of appeal and cross-appeal.

(3) Third, PVI’s claim for additional mitigation damages, which the judge allowed and Fairlight appeals from.

(4) Fourth, Fairlight’s claim for an account of profits for infringement of its trade mark, which the judge allowed in part and which both Fairlight and PVI appeal from.

(5) Fifth, whether KFT should have been jointly liable with Fairlight for breaching PVI’s copyright which is the subject of PVI’s cross-appeal.

PVI’s Claim for Expectation Damages

A preliminary issue: the claim was previously abandoned

74 Fairlight opposed PVI’s expectation loss claim in this Court on the basis that that claim had been expressly abandoned in the first appeal and that PVI should not have been allowed to revive it before the remittal judge. Fairlight referred to paragraph [32] of the remittal judgment where it is said that “a real question arises as to whether PVI should now be permitted to maintain a claim for expectation loss given its submissions to the Full Court” because “the appeal was conducted on the basis that PVI did not make any claim for expectation damages”.

75 The issue arose in the following way.

76 In its written submissions in the first appeal Fairlight submitted that PVI’s claim for reliance damages could not be sustained because it had sought expectation damages on the basis that it was possible to predict what position PVI would have been in had the contract been performed. It was submitted that in those circumstances PVI had no basis to also claim reliance damages, and Commonwealth of Australia v Amann Aviation Pty Ltd [1991] HCA 54; 174 CLR 64 at 86 was referred to.

77 PVI’s submissions in response, specifically in answer to that submission, were that “PVI no longer pursues any claim for expectation damages” and that “accordingly there is nothing to preclude it from seeking reliance damages”. Those submissions were signed by senior and junior counsel and represent a forensic choice made by PVI in order to avoid what it perceived as the consequence of a submission put by Fairlight succeeding.

78 Fairlight’s written submissions in the remittal hearing stated that “in its submissions to the Full Court, PVI … abandoned any claim for expectation losses and only sought reliance losses”. Orally, Fairlight submitted to the remittal judge that because of that abandonment PVI should not be allowed to seek expectation losses in the remittal hearing.

79 In general a party is bound by its forensic elections and how it conducts its case, including by counsel who exercise a wide discretion: Metwally v University of Wollongong [1985] HCA 28; 60 ALR 68 per Gibbs CJ, Mason, Wilson, Brennan, Deane and Dawson JJ at 71 lns 35-45; Nudd v R [2006] HCA 9; 225 ALR 161 at [9] per Gleeson CJ; Ship Hako Endeavour v Programmed Total Marine Services Pty Ltd [2013] FCAFC 21; 211 FCR 369 per Rares J at [46]-[47].

80 PVI submitted before us that it should be allowed to go back on its election because the outcome of the first appeal was not predicated on whether expectation damages were sought and the remittal for the determination of damages was “at large” and did not exclude expectation damages.

81 In my view that is not reason enough to allow PVI to change course in the remittal hearing. It solemnly abandoned expectation losses in the appeal to avoid an argument that was put against it. No explanation was advanced to justify this change in course and it is difficult to know just what influence that had in the appeal and then in the remittal hearing. PVI’s claim for expectation damages should have been dismissed on the basis that it had been abandoned.

82 For completeness, I will nonetheless go on to consider PVI’s appeal against the remittal judge’s dismissal of the expectation damages claim on the merits.

PVI’s submissions

83 PVI’s submissions in the cross-appeal criticised the remittal judge’s rejection of its claim for loss of profits, or expectation damages, on two grounds.

84 First, PVI submitted that the remittal judge erred in concluding that the reliability of the projections contained in the information memorandum was greatly diminished by the actual sales achieved compared to what was projected. The error was said to lie in the remittal judge’s reliance on the trial judge’s finding that the evidence did not establish that Fairlight was in breach of the agreement due to any delays that occurred in the delivery of computer software to PVI and thus that it was not shown that the poor actual sales compared to the projections was caused by any breach by Fairlight.

85 Secondly, PVI submitted that the remittal judge erred in excluding from projected profits products not covered by the licence to use the Fairlight trade mark. It was submitted that this was an error because the Full Court had found that the Agreement was not confined to the Fairlight branded products and that products that were not the subject of the licence referred to in the Agreement were contemplated by both parties.

Consideration

86 It is uncontroversial that the general rule is “that where a party sustains a loss by reason of a breach of contract, he is, so far as money can do it, to be placed in the same situation, with respect to damages, as if the contract had been performed”: per Parke B in Robinson v Harman (1848) 1 Exch 850 at 855; 154 ER 363 at 365 quoted by Mason CJ and Dawson J in Amann Aviation at 80.

87 The award of damages for breach of contract protects a plaintiff’s expectation of receiving the defendant’s performance. Contractual damages are therefore sometimes referred to as “expectation damages”, although they are equally well described as loss of profits. In either event, it is the net benefit or revenue from the contract which is the proper measure, and not the gross benefit or revenue; by that distinction I mean that the cost of the plaintiff’s own performance in order to earn the performance of the defendant that is expected as a consequence of the contract must be taken into account.

88 A plaintiff must prove, on a balance of probabilities, that their expectation of a particular outcome, as a result of performance of the contract, had a likelihood of attainment rather than being a mere expectation: Amann Aviation per Mason CJ and Dawson J at 80.

89 Where it is not possible for a plaintiff to demonstrate whether or to what extent the performance of a contract would have resulted in a profit for the plaintiff, it will be open to the plaintiff to seek to recoup expenses incurred, damages in such a case being described as reliance damages or damages for wasted expenditure: Amann Aviation per Mason CJ and Dawson J at 81.

90 In order to make good PVI’s two grounds of criticism of the remittal judgment in its rejection of PVI’s expectation damages claim, Mr Vogel took the Court through a bundle of “key documents” extracted from the appeal books. He submitted that those documents constitute evidence sufficient to justify the projections in the information memorandum as being good and realistic. On this point, as identified, PVI had to show, on a balance of probabilities, that its projected profit under the contract had a likelihood of attainment rather than being a mere expectation.

91 For the most part, the documents in question are no more than self-serving statements in advance of the key events recording PVI’s expectations, or stated expectations, at that time. This is reflected in, for example, the information memorandum which records that it contains “forward-looking projections which may not be achieved and prospective investors should rely on their own assessment rather than these figures in making their investment decision” and that “other figures and projections presented herein should not be relied on as the Directors make no guarantees as to actual future results”.

92 Fairlight’s forensic accounting witness, Mr Hood, who had considerable experience and expertise in, amongst other things, business plan preparation, business advice and feasibility analysis, drew attention to the fact that PVI’s information memorandum which contained its forecasts was not supported by an independent accountant’s report or an independent expert’s report. He expressed the opinion that in respect of a start-up business which is actively seeking capital, prospective financial information must be viewed with a level of professional scepticism. He said that in the absence of it having been reviewed and verified by a qualified accountant or other appropriate specialist, it cannot reasonably be relied on. These points were well made, and were not challenged in cross-examination.

93 The information memorandum sets out the following table of projected revenue and expenditure:

• A second round of capital is now being raised to fund production and continue product development. The current business plan suggest the following financials are achievable:

Part Year 1 March-June | Year 2 | Year 3 | Year 4 | |

Revenue (est) | $247,400 | $4,290,150 | $8,566,846 | $7,477,750 |

EBITDA* | -$507,412 | $367,036 | $2,310,355 | $2,748,427 |

Investment | 500,000 |

*Earnings before interest, tax, depreciation and amortization

94 It also sets out a product sales summary as follows:

95 The memorandum also sets out a statement of projected cashflows, from which the revenue and EBIDTA figures appearing in the table reproduced at [94] above are drawn.

96 PVI’s loss of profits claim depends substantially on these forecasts. From the product sales summary it can be seen that it was forecast that 100 CMI-30A instruments would be sold in 2011 and 2012. Analysis of the forecasts shows that the overall profit of the venture depended on the sale of products other than the CMI Products (reflected in the table as CMI-30A and Naked 30A, and not including the CMI-S5 MOD which is a different product). This is because forecast revenue in the first two years was less than expenditure, and thereafter (when the venture moved into a profit position) no further sales of the CMI-30A were forecast and revenue from the Naked 30A was projected to be modest.

97 The principal difficulty for PVI is that it sold 12 of the CMI-30A instruments in around March 2011, no more in the balance of 2011 and then only two in 2012. PVI thus fell a long way short of its forecast set out in the information memorandum for those two years.

98 Mr Vogel had taken orders for the CMI-30As from March 2011 and he accepted that there was no impediment on anyone placing an order from that time. The trial judge found (at [115]) that the software for the instruments was good enough to sell them to third parties, and that there was no evidence of any complaint by a customer of PVI after having purchased an instrument. Mr Vogel’s evidence that he had sold the 14 CMI-30As to customers believing they were deficient was rejected by the trial judge (at [115]) on the basis that Mr Vogel would not have shipped deficient product and that he shipped the instruments because he considered they were of sufficient quality to comply with PVI’s contractual obligations to its customers and that he had not had a single complaint from the company’s customers.

99 Those findings were not overturned in the first appeal. There was therefore no basis to contend that the poor sales were as a consequence of the delays and other deficiencies in performance by Fairlight that PVI repeatedly complained of. Those deficiencies and delays as contractual breaches had in any event been rejected by the trial judge which rejection had been upheld in the first appeal.

100 In the circumstances, the projections on which PVI based its expectation damages were clearly and dramatically undermined by actual performance in the period prior to the repudiation. The forecasts were accordingly rightly rejected as being reliable indicators of actual performance. There was no error in the findings and reasoning of the remittal judge in this respect.

101 With regard to the second criticism, PVI could only claim losses suffered by it as a consequence of loss of sales on non-CMI Products if it could show that such losses satisfy the test for causation, i.e. that they “may fairly and reasonably be considered either [as] arising naturally, that is, according to the usual course of things, from such breach of contract itself or … may reasonably be supposed to have been in the contemplation of both parties, at the time they made the contract, as the probable result of the breach of it”: Hadley v Baxendale at 151 (emphasis added).

102 With regard to the first limb of that test, it was found in the first appeal that PVI had the rights to sell only the CMI Products under the Fairlight trade mark and not the other downstream products, whereas PVI’s profit projections depended on the sale of the downstream products as well. The sale by PVI of the non-CMI Products is the basis for Fairlight’s successful trade mark infringement claim, so it cannot be that PVI’s failure to sell as many of those products as it had projected that it would could “according to the usual course of things” give rise to a claim in damages.

103 There is nothing in this case to suggest that the second of the limbs in Hadley v Baxendale was satisfied with regard to loss of sales of non-CMI Products. It was not established that Fairlight knew that PVI contemplated such sales and that they depended on successful performance of the Agreement. It is also the case that to the extent that the sale of the Apps depended on the success of the CMI Products, the projections in respect of the sale of the Apps must also fail on the poor sales of the CMI Products.

104 In the circumstances, PVI’s cross-appeal with regard to its expectation damages must fail.

PVI’s Claim for Reliance Damages

105 Fairlight criticises the remittal judge’s finding that PVI was entitled to reliance loss damages for Fairlight’s repudiation on two broad grounds. I will consider each in turn.

Reliance losses as an alternative to expectation losses

106 Fairlight submitted that the remittal judge was in error in allowing PVI to advance a claim for reliance loss in the alternative to a claim for expectation loss. Fairlight submitted that in order for a plaintiff to claim reliance damages it must be unable to establish its expectation losses because of the conduct of the defendant.

107 Fairlight relied on, in particular, the following statement by Brennan J in Amann Aviation at 106-107:

A plaintiff’s inability to quantify his lost benefits is no justification by itself for casting on the defendant an onus to prove that the plaintiff would not have recouped reliance damages had the contract been performed. What justifies the reversal of the onus is the defendant’s repudiation or breach which denies, prevents or precludes the existence of circumstances which would have determined the value of the plaintiff’s contractual benefits.

108 Fairlight submitted that although that statement deals with the question of onus, its effect is that what is required to claim reliance losses is that the plaintiff must come to court, as it did in Amann Aviation, and say that because of the promisor’s conduct, it has been denied or prevented or precluded from establishing its expectation losses, and that because of that it ought to be entitled to claim reliance losses. Fairlight rather pointed to evidence provided by Mr Hood which it stated showed that expectation losses could have been calculated but were not because of the actions of PVI alone.

109 Fairlight submitted that the remittal judge’s reasoning (at [90]) that to require proof on the balance of probabilities of what further sales of CMI Products would have been made by PVI were it not for Fairlight’s repudiation of the Agreement “would be impractical and unjust”, applied the wrong test.

110 I do not see that Fairlight’s submission is supported by authority or justifiable in principle. With regard to authority, TC Industrial Plant Pty Ltd v Robert’s Queensland Pty Ltd [1963] HCA 57; 180 CLR 130 held that the buyer was not bound to elect between claiming for expenditure uselessly incurred as a result of the seller’s breach and claiming loss of the profits it would have earned had the goods been fit for purpose, but could recover both. Gaudron J in Amann Aviation (at 155), with reference to TC Industrial, held that it may be expected that a claim for wasted expenditure will ordinarily be framed as an independent claim or in the alternative to a claim for damages for loss of profits. Her Honour made it clear that any loss which would have been involved in performing the contract must be brought to account. Those statements count against the proposition that there is any bar or precondition to claiming reliance losses as an alternative to expectation losses.

111 If a plaintiff is unable to prove losses, either because it cannot calculate those because of the defendant’s conduct such as, for example, repudiating the contract, or because the contract would have produced a loss for the plaintiff, any losses that it would have suffered as a result of performance of the contract must be brought into account thereby reducing its reliance losses. In both scenarios, losses are calculated on the basis that the contract was concluded, not that it was not concluded.

112 If the losses are readily calculable, they are easily brought into account. If they are not readily calculable, whether or not that is specifically as a consequence of the conduct of the defendant, they must still be brought into account. The manner in which that is done, and the degree of certainty required, is addressed below in relation to Fairlight’s challenge to the remittal judge’s reduction of PVI’s reliance damages based on an assessment of the extent to which they might have been recouped had the Agreement been performed.

Admissibility of PVI’s evidence on reliance losses

113 Fairlight submitted that the amount of overall reliance expenses, before discount, which the remittal judge concluded had been incurred, namely $981,299, was not a reliable figure and was not based on the evidence. In particular, Fairlight submitted that to the extent that that figure relied on Mr Vogel’s affidavit evidence, it should not have been relied on because the relevant evidence was inadmissible.

114 Before the trial judge, Fairlight submitted long schedules of objections to PVI’s evidence. The schedules were preceded by an introduction which included the following:

An option for dealing with evidential objections

Peter Vogel’s evidence is almost entirely inadmissible. … The affidavits are a combination of submissions, opinion, statements about subjective state of mind, hearsay and a range of irrelevant material about contractual intention, pre-contractual discussions, emotional responses (e.g. frustration) and other matters. The affidavits are argumentative in many parts. The applicant submits that one approach the Court may wish to take is that recently adopted by McDougall J in Kids for Life v Chamberlain Group [2014] NSWSC 1561 (7 November 2014) where His Honour said the following:…

115 Paragraphs [7]-[12] of that judgment of McDougall J were then set out, including the reference to the statement by Gibbs J in Hughes v National Trustees, Executors and Agency Company of Australasia Ltd [1979] HCA 2; 143 CLR 134 at 153 that:

in general, it is the duty of a judge to reach his [sic] decision on evidence that is legally admissible, and to put evidence only to those uses which the law allows.

116 Fairlight then concluded its introduction to its objections to evidence as follows:

The applicant appreciates that the respondent’s affidavits were not prepared with legal assistance; this does not excuse the wholesale inadmissibility of them. The applicant does not wish to expend large amounts of time dealing with each of the following objections if the Court wishes to adopt another course such as the one I have raised above.

117 At the trial, senior counsel for Fairlight accepted the trial judge’s stated approach to the objections which was that where objection is taken to evidence on grounds of relevance he would allow it in subject to relevance, where there is opinion evidence he would treat it solely as submission, and where evidence is clearly hearsay he would confine that evidence to proving that the communication occurred rather than the truth of the content of the communication.

118 In the event, no specific rulings were made by the trial judge on the objections that had been taken to PVI’s evidence.

119 In written submissions to the remittal judge, Fairlight took the position that “PVI’s evidence is almost wholly inadmissible opinion and speculative” and “it is indeterminable whether PVI’s claimed research and development (R&D) costs were thrown away, had created an asset or were available to PVI for future leverage”. As with the trial judge, the remittal judge did not make any specific rulings on the objections that were taken by Fairlight.

120 Mr Vogel’s evidence relevant to his reliance losses and R&D expenses was initially set out in his affidavit of 5 September 2013. He stated in paragraph [31], to which no objection was taken, that R&D expenditure for 2010-2011 was $589,088 and for 2011-2012 it was $345,511, except for about $30,000 which was for developing the CMI-30A. At paragraph [241] he said that PVI’s tax return shows R&D expenditure for 2010-2011 of $604,662. The annexed tax return records an aggregate R&D amount of $604,882. It also records an R&D tax offset of $649,346 and calculates an allowable R&D tax offset of $194,803.80.

121 Mr Hood then dealt with reliance losses and R&D expenses in his report of 27 June 2014 which was annexed to his affidavit of 26 September 2014. He prefaced all of what he said as follows:

5.6.1 The inconsistencies between the amounts claimed in PVI’s Amended Fast Track Cross-Claim and Peter Vogel’s affidavit of 5th September 2013, and the inconsistencies within Peter Vogel’s affidavit of 5th September 2013, raise serious questions about the accuracy of the amounts being claimed by PVI.

5.6.2 It is also important to note that none of the information provided to me has been independently audited. All of the information provided has been prepared by or on behalf of PVI and Peter Vogel. The lack of an independent audit also raises questions about the veracity of the information on which PVI’s claims are based.

122 Mr Hood also clarified in Appendix 6 to his report, being a letter dated 26 June 2014, that the qualification set out in paragraph 5.6 with respect to the accuracy of the information provided to him applies to the whole of his report. He said that the financial information provided to him was unaudited and has several discrepancies. He then said that “for practicality’s sake, notwithstanding the qualification set out in paragraph 5.6, I have to rely on the financial information that has been provided to me in arriving at my expert opinion on the quantification of damages”.

123 With regard to R&D expenditure, Mr Hood set out what Mr Vogel had said in his affidavit and what appeared in the annexed documents referred to above, and pointed out the inconsistencies in the figures. He concluded as follows:

5.3.7 Notwithstanding that there does not appear to be any strong supporting documentation for the 2011-12 and 2012-13 years, the amount of expenditure relating to the development of the CMI-30A referred to in paragraphs 241, 242 and 243 of Peter Vogel’s affidavit of 5 September 2013 only totals $751,292.

124 With regard to reliance damages, Mr Hood stated as follows:

6.2.2 Based on the assumption that PVI’s 2011 and 2012 unaudited profit and loss statements … are correct, and that the variances of the figures … are immaterial (and ignoring the R&D inconsistencies detailed above), then:

• The total expenses shown in those years, including expenses declared as costs of goods sold, total $1,299,016.

• Gross research and development expenditure was $718,292 ($604,662 and $111,630), inclusive of app development costs of $31,088. FY13 R&D expenditure of $63,000 (as per Peter Vogel’s affidavit) was excluded from my calculation as this amount was not able to be substantiated by supporting evidence, and furthermore these amounts were allegedly incurred after the business disruption event occurred.

• This leaves residual non-R&D related costs of $580,724. There was no substantiation of the $120,000 marketing expenditure in Peter Vogel’s affidavit, however any marketing expenditure for FY11 and FY12 years will implicitly be included in this amount.

• Net research and development costs would be reduced by the grants received, and costs related to the app development, leaving $325,869 ($718,292 less $31,088 less grants received $361,335).

6.2.3 …

6.2.4 The “Reliance Damages” calculated (assuming the full accuracy of the financial information provided) would therefore be $580,724. It is indeterminable whether the research and development costs were thrown-away, had created an asset, or are available to Peter Vogel or PVI for future leverage.

(Further detail on these calculations can be found at Appendix 3)

125 Mr Hood concluded as follows:

7.1 It is indeterminable whether the research and development costs incurred by PVI were thrown-away, had created an asset, or are available to Peter Vogel PVI for future leverage. It is therefore my opinion that these costs should not be included in PVI’s claim for damages.

7.2 I have quantified that damages in relation to PVI’s claim include residual non-R&D related costs of $580,724. This constitutes PVI’s total expenses for FY2011 and FY2012 of $1,299,016, less all research and development costs of $718,292.

7.3 …

7.4 It is also my opinion that there is no quantifiable loss of profits in relation to PVI’s claim.

7.5 I have determined that sales of the CMI-30A would have to materially exceed 100 units to result in a profitable outcome in the 18 month period in question (business disruption period).

126 Mr Hood furnished a further report dated 19 September 2014. In it he stated that he had reviewed the financial statements and tax returns of PVI for the 2011 and 2012 financial years that had been provided to him on 5 September 2014. He stated that the purpose of his report was to analyse the new information provided and to comment on whether it impacts on his opinions stated in his report of 27 June 2014.

127 Ultimately, Mr Hood arrived at an amended calculation of reliance damages excluding R&D amounting to $524,359.

128 Mr Vogel’s affidavit of 17 November 2014 sought to reply to Mr Hood’s reports. In paragraphs [4]-[16], Mr Vogel set out an explanation with regard to R&D expenditure in 2011, 2012 and 2013, including with reference to documentary support. In Fairlight’s schedule of objections, objection was taken to some of these paragraphs (the whole or parts of paragraphs [8]-[15]) on the basis that they were hearsay, opinion, submission or conclusion, but for the most part they are explanatory of how Mr Vogel calculated the losses and they are otherwise underpinned by documents which are business records. To the extent that the remittal judge relied on anything in these paragraphs, I do not see that as having been in error.

129 Mr Vogel then concluded as follows on R&D expenditure:

17. In summary, R&D expenditure relating solely to the CMI-30A was:

2011: $604,882 – minus $31,088 relating to app development

2012: $113,630

2013: $66,484

Total: $753,908

18. R&D tax incentive rebates were:

2011: $194,804

2012: $51,133

2013: $29,918

Total: $275,855

19. Nett R&D expenditure relating to the CMI-30A was therefore $478,053.

130 Although Fairlight objected to those paragraphs, they merely summarise what had been said before and are unobjectionable.

131 In relation to reliance damages separate from R&D costs, Mr Vogel stated as follows:

29. I generally agree with Mr Hood’s methodology and finding in relation to reliance damages of $580,724 above and beyond R&D costs.

132 That paragraph was not objected to by Fairlight.

133 Mr Vogel also set out in some detail (in paragraphs [30]-[44]) why the R&D expenditure had no residual value. All but two of those paragraphs (being [31] and [33]) were objected to. Much of what Mr Vogel says in the relevant paragraphs is factual on what can be expected to be within his own knowledge and experience. There are some statements that are clearly opinions, such as that the project failed because of poor management by Fairlight ([38]), but these are not material to the ultimate finding that the R&D expenditure produced no value to PVI because it did not get the software that it had bargained for.

134 During the oral evidence of Mr Hood two schedules that had been prepared by him were tendered. They became Exhibit 16 and Exhibit 17. The first reflected what was referred to as scenario 1. Mr Hood explained that in his earlier calculations he had not taken into account any income earned from the sale of the CMI-30As. Scenario 1 now took this into account. The second document reflected what was referred to as scenario 2. He explained that this was “as per” the other scenario but, as I understand his evidence, assumes that the net R&D expended relates solely to the intellectual property related to the CMI Products and that that expenditure was successful, and is thus correctly “expensed”. It arrives at a figure of $504,635 for reliance losses excluding R&D expenses. This is apparently the figure referred to by the remittal judge at paragraph [60] of the remittal judgment.

135 Although now put as a matter of admissibility, Fairlight’s real complaint about the remittal judge’s reliance on the evidence of Mr Vogel, and in particular on the documentary evidence that underpins it such as unaudited management accounts, tax returns and financial statements, is one of weight – Fairlight submitted to the trial judge and the remittal judge that the information is unverified and unreliable.

136 It is also not without significance that Fairlight elected not to challenge Mr Vogel on the evidence it objects to. That was a forensic election that it made – in respect of which I refer to the principle and cases cited in paragraph [80] above. If that evidence was admissible, then it is unchallenged and can be accepted.

137 There is nothing relied on by the remittal judge in his calculation of reliance losses that I consider should have been ruled as inadmissible by him. The figures ultimately used by Mr Vogel and Mr Hood were drawn from management accounts, profit and loss statements and tax returns of PVI. Although those documents were not audited, and it was submitted that what they reflect may be wrong and is unsupported by primary documentation, the accuracy or reliability of what they reflect was not challenged. The remittal judge made no error in relying on those figures.

138 This ground of appeal must accordingly fail.

Recoupment of reliance expenses if the Agreement had been performed, and costs of performance

Fairlight’s submissions

139 Fairlight submitted that PVI had failed to prove that it would have recovered its expenditure were it not for the repudiation of the Agreement. It submitted that there was no evidence to support a finding that PVI would have recovered that expenditure. Fairlight pointed to various references in Amann Aviation to the effect that, in assessing reliance loss, any loss which would have been involved in performing the contract must be taken into account so as to avoid the plaintiff being placed in a better position than if the contract had been performed: Mason CJ and Dawson J at 82, 84 and 86, Brennan J at 99, and Gaudron J at 155. It was submitted that the error was that the remittal judge did not bring into account the loss that would otherwise still have been suffered by PVI, regardless of the repudiation.

140 Fairlight submitted that the remittal judge was in error by reducing actual operating expenses by projected gross revenue from sales (referred to by the remittal judge as a lost opportunity of recoupment) without taking into account further operating expenses that would have been required after the repudiation in order to achieve those sales. Fairlight cited this statement by Brennan J in Amann Aviation 99-100:

The situation of a plaintiff “if the contract had been performed” is, of course, a hypothetical situation with which the plaintiff’s actual situation is compared. When a contract is rescinded for breach by a defendant, the hypothesis postulates that the contract is still on foot. On that hypothesis, the benefits to which the plaintiff would have been entitled had the contract been performed (let the benefits have a value of $B) can be apportioned among three components: the amount expended by the plaintiff in performing or preparing to perform the contract prior to rescission ($x); the further amount which the plaintiff would have had to expend to perform the contract ($y); and the amount of profit or loss that would have eventuated had the contract been performed ($z).

141 Fairlight submitted that the remittal judge failed to take into account the $y component, i.e. operating costs after the repudiation on the hypothesis that the Agreement had continued. This submission overlooks that the referenced portion of Brennan J’s judgment deals with expectation losses. His Honour went on to deal with reliance losses starting at 104, and at 105 stated that when a contract is rescinded for breach and that breach, by preventing the performance of the contract, has made it impossible for the plaintiff to prove that the net value of his contractual benefits ($B - $y) exceeds the wasted expenditure incurred in reliance on the defendant’s promise prior to rescission ($x), it is just to shift to the defendant the ultimate onus of proving that, had the contract been performed, the net value of the plaintiff’s benefits would not have covered the expenditure he had incurred before rescission. On that reasoning, the onus lay on Fairlight to prove the $y amount, which it failed to do. In any event, as I will show, in my view the remittal judge adequately took into account the costs of performing the Agreement had it, hypothetically, been performed.

142 Still in relation to the first point, Fairlight submitted that the remittal judge erred in discounting the reliance losses by 70% (or, putting it conversely, allowing reliance losses to the extent of 30% – as explained at paragraph [59] above) because that figure is not explained or justified. It was submitted that it appears to, or could, relate to an example given by the remittal judge in paragraph [89], although that is not clear. It was submitted that the figure of 30% was extravagant and should not have been used, and that there was a failure to explain the underlying rationale.

PVI’s submissions

143 Cross-appeal ground 2(d) says that the remittal judge erred by awarding only 30% of the wasted $981,299 as damages. PVI made only very limited submissions, not directed specifically to this issue, affirming ground 2(d). It also made submissions in support of the remittal judge’s conclusions in answer to Fairlight’s submissions in the appeal. I incorporate those in my consideration of Fairlight’s submissions below.

Consideration

144 It is correct that the remittal judge did not expressly take into account the operating costs that would have been required to recoup the expenditure. However, the approach adopted by the remittal judge was at a higher level of generality. It was put like this:

[92] I will allow a percentage of the wasted expenditure claimed (excluding mitigation costs) which reflects my assessment of the value of the lost opportunity. In my view an appropriate percentage figure is 30% which yields a figure of $294,390 (i.e. 30% of $981,299). This figure reflects my view that, while the prospects of PVI recovering all of its expenditure were extremely low, the opportunity to recover at least some of that expenditure that was lost was not insignificant and of considerable value to PVI given Mr Vogel’s reputation, and the time, effort and money that had been already spent on research and development for the CMI Products as of May 2012.