FEDERAL COURT OF AUSTRALIA

Ultra Tune Australia Pty Ltd v Australian Competition and Consumer Commission [2019] FCAFC 164

ORDERS

ULTRA TUNE AUSTRALIA PTY LTD (ACN 065 214 708) Appellant | ||

AND: | AUSTRALIAN COMPETITION AND CONSUMER COMMISSION Respondent | |

DATE OF ORDER: | 20 September 2019 |

THE COURT ORDERS THAT:

1. The appeal be allowed in part.

2. Order 1 of the orders made on 18 January 2019 be varied by substituting the amount of $2,014,000 for the amount of $2,604,000.

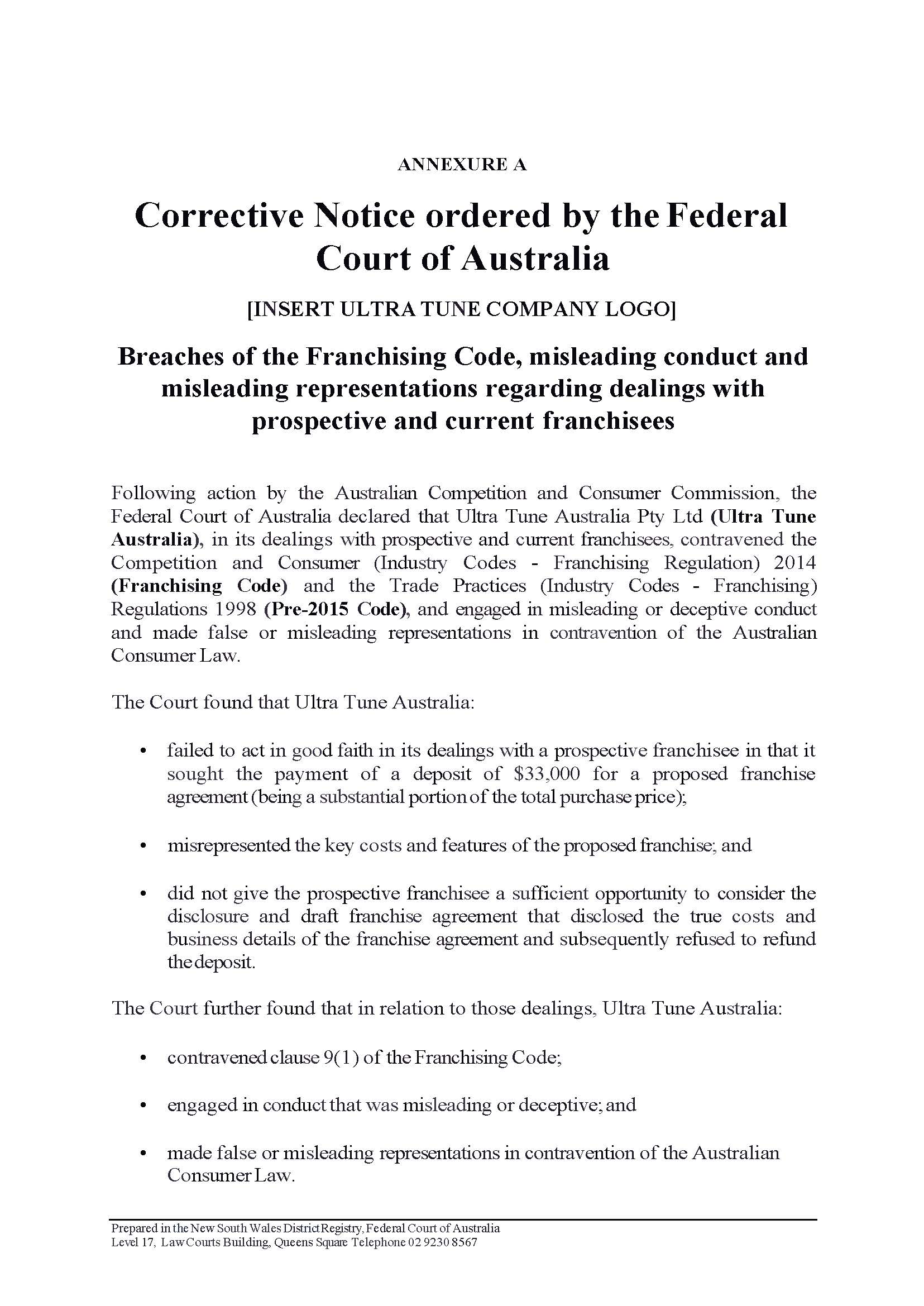

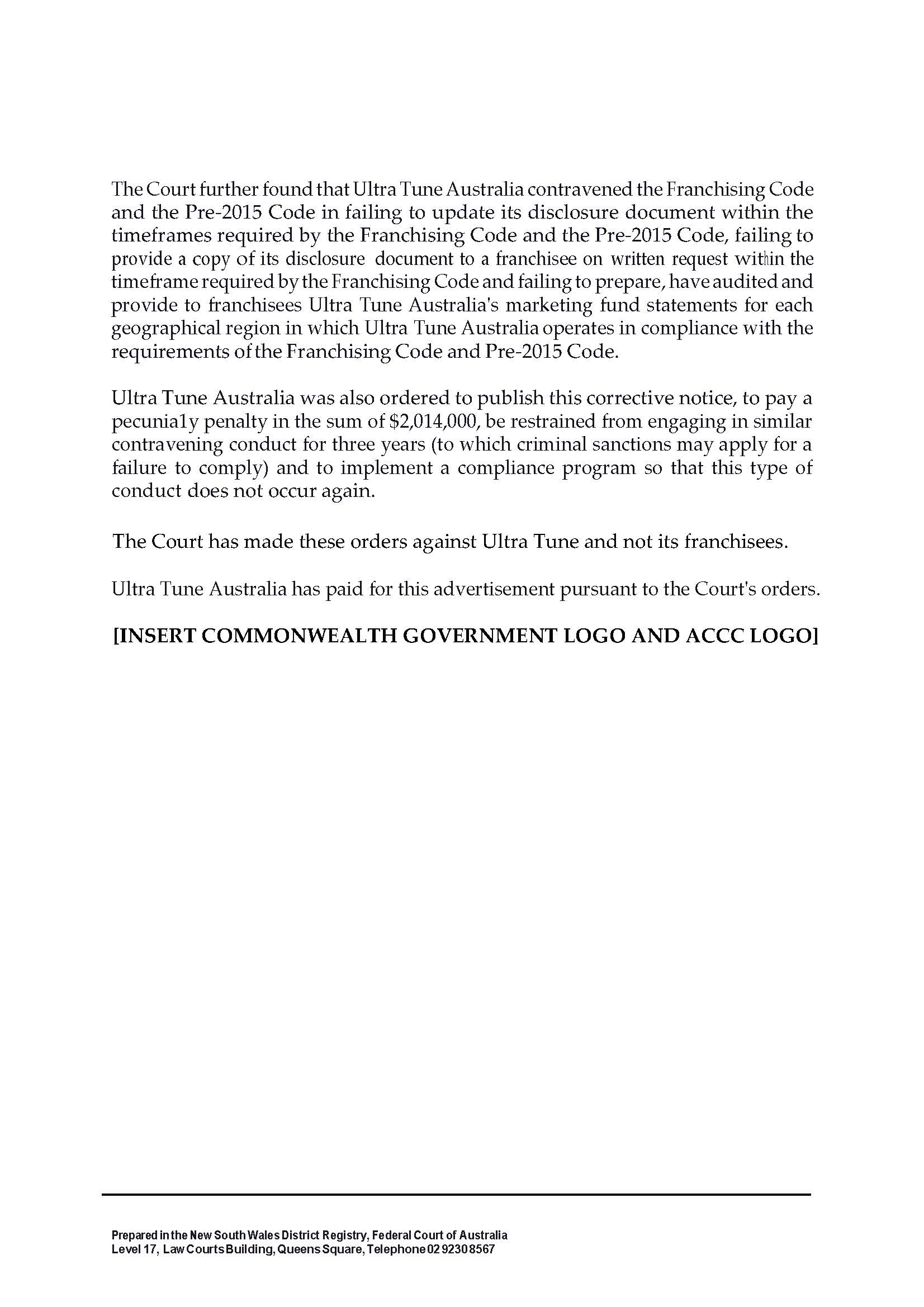

3. Order 4 of the orders made on 4 March 2019 be varied by substituting for Annexure A to those orders, Annexure A to these orders.

4. Subject to order 5 below the respondent pay 60% of the appellant’s costs of the appeal.

5. Either party wishing to be heard on costs may file submissions not exceeding three pages in length identifying the costs order they seek and reasons in support within 7 days of these orders.

6. Any party which is served with a submission under order 5 may file and serve a submission in reply not exceeding three pages in length identifying the costs order they seek and reasons in support within a further 7 days thereafter.

7. Costs will be determined on the papers if necessary.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

THE COURT:

1 Ultra Tune Australia Pty Ltd has appealed against the primary judge’s determination that it contravened a disclosure obligation owed to franchisees in cl 15(1) of the Franchising Code (Schedule 1 to the Competition and Consumer (Industry Codes – Franchising) Regulation 2014 (Cth)) and the imposition of penalties in respect of that and other admitted contraventions of the disclosure obligations in the Franchising Code.

2 We have decided that the appeal against the primary judge’s conclusion that Ultra Tune contravened cl 15(1) of the Franchising Code should be dismissed but the appeal against penalty should be allowed.

The Franchising Code

3 The primary judge defined the contraventions to which the appeal is confined as the first category of alleged contravention. As explained by the primary judge in his reasons for judgment (Australian Competition and Consumer Commission v Ultra Tune Australia Pty Ltd [2019] FCA 12):

12 The first category of contravention concerns alleged failures by Ultra Tune to comply with various types of disclosure obligations under the codes. The alleged contraventions to which civil penalty consequences attach under the Franchising Code were:

(1) a failure to maintain disclosure documents in relation to Ultra Tune’s four State-based regions, summarised in the table at [15] below (there being a single combined disclosure statement for metropolitan and regional NSW), by failure to update them within four months after the end of the 2015-16 financial year (that is, by 31 October 2015): cl 8(6) of the Franchising Code;

(2) a failure to prepare financial statements for the marketing funds for the five Ultra Tune marketing regions (there being separate funds for metropolitan and regional NSW) within four months of the end of the 2014-15 financial year (that is, by 31 October 2015): cl 15(1)(a) of the Franchising Code;

(3) a failure to ensure that financial statements for the marketing funds for the five Ultra Tune marketing regions included “sufficient detail” for the 2014-15 and 2015-16 financial years: cl 15(1)(b) of the Franchising Code;

(4) a failure to provide to franchisees the financial statements for marketing funds and an auditor’s report for the five Ultra Tune marketing regions relating to the 2014-15 financial year within 30 days of them being prepared: cl 15(1)(d) of the Franchising Code; and

(5) a failure to provide a disclosure statement when requested by a franchisee on 16 December 2015: cl 16(1) of the Franchising Code.

13 With one exception, Ultra Tune admits to the above contraventions. The exception is that Ultra Tune denies the allegation referred to at [12(3)] above that it failed to disclose “sufficient detail” in statements prepared for its marketing funds, contrary to cl 15(1)(b) of the Franchising Code, asserting that the obligation was met. That issue aside, the main areas of controversy between the parties in relation to the alleged disclosure contraventions is to the quantum of the penalties to be imposed, largely based on how many contraventions took place as a matter of statutory construction.

4 The primary judge also explained the statutory provisions and the relevant requirements of the Franchising Code.

5 Accordingly, the primary judge’s reasons record that:

26 Part IVB of the CCA [Competition and Consumer Act 2010 (Cth)] provides for the creation and enforcement of “industry codes”. The purpose of an industry code is to regulate the conduct of participants in an industry toward other participants or consumers in the industry. “Franchising” is included as an industry for the purposes of Part IVB: s 51ACA(3). An applicable industry code may be a voluntary industry code: s 51ACA(1)(b)). It may also be a mandatory industry code, which must be declared to be mandatory by regulation: ss 51ACA(1), 51AE. Both the Pre-2015 Code and the Franchising Code are examples of mandatory industry codes. By reason of what is now s 51ACB (and was formerly s 51AD), a corporation must not, in trade or commerce, contravene an applicable industry code.

27 Under Part IVB of the CCA, the ACCC [Australian Competition and Consumer Commission] has been entrusted with various regulatory powers in relation to applicable industry codes. These include the power to issue a public warning notice (s 51ADA), certain investigative powers (Division 5), and the ability to seek orders for redress of a contravention (s 51ADB). From 1 January 2015, the ACCC has also had the power to issue an infringement notice (Division 2A), and the ability to seek the imposition of civil penalties for breach of a civil penalty provision of an applicable industry code (s 76(1)).

6 His Honour also noted at [32] that the provisions of the Franchising Code refer to a civil penalty of 300 penalty units and that, at the relevant time in 2015, a penalty unit was prescribed to be $180 under s 4AA of the Crimes Act 1914 (Cth). Thus the maximum penalty for any contravention of the Franchising Code was $54,000 in 2015.

7 The relevant provisions of the Franchising Code with which this appeal is concerned are cl 8 and cl 15. By cl 8(1) a franchisor must create a document (a disclosure document) relating to a franchise that complies with subcll (3), (4) and (5). By cl 8(2) the purpose of a disclosure document is to give prospective or renewing franchisees information from the franchisor to help the franchisee to make a reasonably informed decision about the franchise and current information from the franchisor that is material to the running of the franchised business. By cl 8(3) the information in a disclosure document must be in the form and order of Annexure 1 to the Franchising Code. In Annexure 1, para 15.1 provides that for marketing or other cooperative fund, controlled or administered by or for the franchisor, to which the franchisee may be required to contribute, certain details must be contained in the disclosure document including, relevantly:

(f) the kinds of expense for which the fund may be used;

(g) the fund’s expenses for the last financial year, including the percentage spent on production, advertising, administration and other stated expenses;

8 Clause 8(6) of the Franchising Code states:

After entering into a franchise agreement, the franchisor must update the disclosure document within 4 months after the end of each financial year.

Civil penalty: 300 penalty units.

9 Clause 15(1) is as follows:

(1) If a franchise agreement provides that a franchisee must pay money to a marketing or other cooperative fund, the franchisor must:

(a) within 4 months after the end of the last financial year, prepare an annual financial statement detailing all of the fund’s receipts and expenses for the last financial year; and

(b) ensure that the statement includes sufficient detail of the fund’s receipts and expenses so as to give meaningful information about:

(i) sources of income; and

(ii) items of expenditure, particularly with respect to advertising and marketing expenditure; and

(c) have the statement audited by a registered company auditor within 4 months after the end of the financial year to which it relates; and

(d) give to the franchisee:

(i) a copy of the statement, within 30 days of preparing the statement; and

(ii) a copy of the auditor’s report, if such a report is required, within 30 days of preparing the report.

Civil penalty: 300 penalty units.

The primary judge’s reasons

10 The primary judge recorded that Ultra Tune is a franchisor for motor vehicle engine repair and maintenance services provided by a national network of approximately 200 franchises operating in New South Wales (divided into metropolitan and country), Queensland, Victoria and Western Australia: [1].

11 In the 2014 - 2015 financial year, Ultra Tune had 185 franchisees. In 2015-2016 it had 200 franchisees: [15].

12 Although no penalty could be imposed for contraventions of the Franchising Code before 1 January 2015 (referred to as the Pre-2015 Code) the primary judge said at [68] that these contraventions were relevant because they meant that the later contraventions could not be said to be out of character. In the primary judge’s words at [68]:

These earlier contraventions therefore additionally operate as a prism through which to view the later contraventions. However, care must be taken to ensure that the penalty is proportionate to the instant contravention and that no element of the pecuniary penalty imposed for later contraventions is reflective of any sanction for these earlier contraventions: see Construction, Forestry, Maritime, Mining and Energy Union v Australian Building and Construction Commissioner (The Non-Indemnification Personal Payment Case) [2018] FCAFC 97 at [22].

13 The primary judge noted at [69] that Ultra Tune admitted that contrary to cl 17(1)(a) of the Pre-2015 Code, it failed to prepare annual financial statements within four months of the end of the 2011-12 and 2012-13 financial years as required. For the 2011-12 financial year, the statement was completed on 30 November 2012, instead of by 31 October 2012. For the 2012-13 financial year the statement was completed on 28 November 2013, instead of by 31 October 2013: [69]. Ultra Tune also admitted that contrary to cl 17(1)(c) of the Pre-2015 Code, it did not provide annual financial statements and auditor’s reports to any franchisee as required to be done within 30 days of preparation, no such statements having been provided for the 2011-12 financial year, the 2012-13 financial year or the 2013-14 financial year: [70]. Ultra Tune admitted that, contrary to cl 6(1) of the Pre-2015 Code, it failed to create a disclosure document within four months after the end of the 2014-15 financial year, that document having been completed on 5 December 2014 instead of by 31 October 2014: [71].

14 For conduct after 1 January 2015 (which enabled the imposition of civil penalties) the primary judge recorded that:

(1) Ultra Tune admitted that, contrary to cl 15(1)(a) of the Franchising Code, it failed to prepare marketing fund statements within four months after the end of the last financial year for the 2014-15 financial year (that document having been completed on 24 December 2015 instead of by 31 October 2015): [74].

(2) Ultra Tune admitted that, contrary to cl 15(1)(d) of the Franchising Code, it did not provide to franchisees the annual financial reports and auditor’s reports for the marketing funds for the 2014-15 financial year within 30 days of their preparation. Those reports had been completed on 24 December 2015, so were required to be provided to each franchisee who was required to contribute to the marketing funds (which was all franchisees) by 24 January 2016. In fact, however, as the primary judge said at [75]:

1. “the annual financial statement and auditor’s report for the Queensland region was provided to two Queensland franchisees on 28 January 2016;”

2. “the annual financial statement and auditor’s report were provided to a single NSW franchisee on 29 January 2016, following a specific request by that franchisee; and”

3. “the annual financial statement and auditor’s report for each region was provided to the other 182 franchisees for the 2014-15 financial year on 11 August 2016, over seven months after they were created rather than within the necessary 30 days, and therefore over six months late.”

(3) Ultra Tune admitted that, contrary to cl 8(6) of the Franchising Code, it did not update its disclosure documents for the 2015-16 financial year within four months after the end of the 2014-15 financial year, being 31 October 2015. Those documents were not completed until 26 February 2016, so were almost four months late, taking almost twice as long as required: [76].

(4) Ultra Tune admitted that, contrary to cl 16(1)(b), it did not provide a disclosure document to a franchisee in Morayfield within 14 days of a request made on 16 December 2015, that document having not been provided until 23 March 2016, over three months after the request was made.

15 The appeal against penalty relates to the contraventions in (1) to (3) above, there being no appeal against penalty in respect of the contravention in (4).

16 The primary judge said this at [73] by way of general observation about the admitted contraventions:

On any view, the admitted disclosure contraventions of the Franchising Code described below were substantial, and in the case of the more lengthy delays described were of a relatively high level of objective seriousness when due regard is had to the reason why these requirements exist in the first place and the extent of the non-compliance. The later the provision of such information, the less use it is and the closer it comes to not providing it at all. Such requirements are now able to be deterred by the sanction of substantial pecuniary penalties, taking into account the number of franchisees affected in relation to information that was not provided to them as required.

17 The primary judge then dealt with the disputed disclosure contraventions. His Honour recorded at [78] that:

In accordance with cl 15(1) of the Franchising Code, the statements for the 2014-15 and 2015-16 financial years were required to detail all of the relevant marketing fund’s receipts and expenses for the previous financial year. Given that Ultra Tune maintained a separate marketing fund for each of the five Ultra Tune regions listed in the table at [15] above, it was required to prepare annual statements for each of those funds. It is not in dispute that for both financial years:

(1) Ultra Tune did so in the form of a profit and loss statement for each region’s fund;

(2) had the statements audited; and

(3) provided the statements and auditor’s reports to the franchisees.

18 As his Honour put it at [79]:

What is controversial, however, is the adequacy of those statements in terms of meeting the standard required by the Franchising Code. In respect of both financial years, the ACCC alleges that the financial statements that were prepared by Ultra Tune did not have “sufficient detail” as specifically required by cl 15(1)(b) of the Franchising Code. Ultra Tune disputes this.

19 At [81] his Honour identified that the question of construction that arises is as to the proper meaning of the expression “sufficient detail” in cl 15(1)(b). This issue, his Honour said, had not been the subject of any previous authority (and no such authority has been identified in this appeal): [81]

20 In construing the obligation the primary judge correctly identified at [82] it is:

…important to also note that cl 15(1) is evidently related to cl 31, which imposes direct requirements on how marketing fees are to be used. This provides an important contextual basis for understanding a key practical use of the information that is required to be disclosed, informing what information needs to be included to be useful and to achieve the regulatory purpose. Of particular relevance is cl 31(3), which provides:

Despite any terms of a franchise agreement, marketing fees or advertising fees may only be used to:

(a) meet expenses that:

(i) have been disclosed to franchisees under paragraph 15.1(f) of the disclosure document; or

(ii) are legitimate marketing or advertising expenses; or

(iii) have been agreed to by a majority of franchisees; or

(b) pay the reasonable costs of administering and auditing a marketing fund.

21 The primary judge continued noting that:

83 Ultra Tune prepared its financial statements for both the 2014-15 and 2015-16 financial years for the purposes of cl 15(1) in the form of profit and loss statements for each Ultra Tune region. Those statements were uniform in structure. Each took the form of an ordinary balance sheet, with a limited number of line items listed as either “income” or “expenses” together with dollar figures and percentages reflecting each item’s proportion of the overall expenditure. For the most part, the total income of each fund for the 2014-15 financial year was in the order of $6.7 million, with a similar expenditure. The 2015-16 financial year also had similar levels of income and expenditure.

84 Included as expenses in the financial statements were a large number of minor items that generally did not account for more than 20% of the total expenditure of the funds in question. These included items described as “Gift Vouchers”, “Printing & Stationary” (sic), “Seminars and Meetings”, “Administration Fees”, “Fleet Administration” and “Customer Support”. In the case of each financial statement, the majority of the relevant fund’s expenditure was constituted by a single item, which was described simply as “Promotion & Advertising – Television”. For example, in the case of the NSW Metro marketing fund for the financial year 2014-15, this item comprises 76.65% of the total expenditure of the fund.

22 The primary judge concluded that Ultra Tune’s financial statements did not satisfy the requirement of cl 15(1)(b) of the Franchising Code. The primary judge said:

85 Ultra Tune defends the adequacy of its financial statements, which it says are sufficiently detailed for the purposes of cl 15(1)(b). It says that the reference to “meaningful information” in cl 15(1)(b) does no more than emphasise that what is required is an accounting, not a bookkeeping, exercise. It is said to be sufficient that the figures in each financial statement are classified and recorded such that a franchisee can see what the major sources of income and expenses were. According to Ultra Tune, that is exactly what its statements do. I do not accept these submissions.

86 It may be seen from its terms, and its relationship with cl 31(3), that cl 15(1) seeks to promote transparency and accountability in the way that marketing fees are used by a franchisor. It does so by requiring a franchisor to disclose “sufficient detail” of a fund’s receipts and expenses so as to give “meaningful information” to the franchisees about sources of income and items of expenditure, particularly with respect to advertising and marketing expenditure. The ACCC submits that the notion of “meaningful information” conveys at a textual level that the financial statement must have some explanatory force and permit meaningful insights to be gained by the franchisee. I agree.

87 The minimal requirement that Ultra Tune submits is enough would have the effect of denying any real, practical content to the express requirement to give “sufficient detail of the fund’s receipts and expenses so as to give meaningful information” about “sources of income” and “items of expenditure, particularly with respect to advertising and marketing expenditure”. What is required to be provided is sufficiently detailed meaningful information, which is necessarily information that is useful and practical, not merely minimal accounting information.

88 That said, it should be acknowledged that cl 15(1)(b) is not particularly clear or prescriptive as to what is required to give “meaningful information” about a marketing fund’s income and expenditure. However, the general intention of the provision is plain enough, namely that the franchisee should be in a position to know what the income and expenses of the fund are for the purpose of making some meaningful assessment of whether that use is appropriate. The references to “sufficient detail” and “meaningful information” must be understood with that purpose in mind.

89 To be more prescriptive might have reduced the capacity for franchisors to tailor the information provided to a wide range of different circumstances, given the diverse range of economic activities in which franchise arrangements exist. To accommodate those different circumstances, cl 15(1)(b) has a protean quality. What is sufficient detail to give “meaningful information” on a fund’s income and expenditure will vary from case to case. Similarly, what may be a sufficient level of detail for certain items or categories of expenditure may be insufficient for others, bearing in mind also that cl 15(1)(b)(ii) necessarily requires a focus “particularly with respect to advertising and marketing expenditure”. As a general proposition, the more significant an expense is, the more important it will be to a franchisee, and therefore the greater the level of detail that will be required to facilitate an informed assessment by the franchisees concerned. There may be cases in which more detail is needed for a lesser expenditure in order to understand why it is appropriate. In each case, however, the adequacy of the statement must be considered and assessed as a whole.

90 The parties made reference to extrinsic material that was said to aid in construction of cl 15(1)(b). Such material, however, must also be approached with caution to the extent that Parliament may have made “aspirational” statements of its intentions that are not reflected in the terms of the Franchising Code. As emphasised by Spigelmann CJ in R v JS [2007] NSWCCA 272; 230 FLR 276 at [142], the task of the courts is to determine what Parliament meant by the words it used; it is not to determine what Parliament intended to say.

91 Here, the extrinsic materials do not go further than confirming that the purpose of the provision is to provide accountability and transparency in the use – and potential misuse, or even inappropriate or ineffectual use – of marketing funds…

…

93 Ultra Tune notes in written submissions that the term “annual financial statement” at cl 15(1)(a) is not defined in the Franchising Code or the CCA, but is well known to accountants, auditors and businesses generally, comprising a profit and loss statement and balance sheet. Ultra Tune further submits that if additional information was required as contended by the ACCC, no profit and loss statement or balance sheet would comply with the requirement, and it would “turn into something that no longer was an annual financial statement as … understood by accountants, auditors and businesses.” This argument cannot be accepted, as it places undue emphasis on the form of what the statement would take, according to what is submitted to be an industry-accepted standard, above the express substantive requirements of cl 15(1)(b) as to what is required by way of sufficiency of detail.

…

97 The substantial deficiency of Ultra Tune’s marketing fund statements lies in how the preponderance of the funds’ expenditure has been itemised. As described above, the most significant expense is identified simply as “Promotion & Advertising – Television”. Ultra Tune submitted that the line item descriptions made it plain that the “vast bulk of the money spent … was on television advertising”. The problem with describing that expense in such bare and general terms is that, notwithstanding that there might be some granularity in the description of a large number of minor expenses, the statements provide no meaningful information about how most of the fund has in fact been used. It certainly does not provide sufficient detail so as to give meaningful information about advertising and marketing expenditure as expressly required by cl 15(1)(b)(ii).

98 Put another way, where it is indicated that approximately 80% of a fund has been applied to something as non-specific as “Promotion & Advertising – Television”, the statement does little more than suggest, in a circular fashion, that Ultra Tune spent the majority of the marketing fund on marketing. This is plainly inadequate for the purposes of cl 15(1)(b)(ii), and certainly would not assist in ascertaining whether the money was expended on “legitimate marketing or advertising expenses”. In these circumstances, a franchisee would have very limited information to inform its understanding of the item. To whom have the fees been paid? What services were obtained, and when? Almost any other questions cannot even be posed, let alone answered, yet it is plain enough that the intent of cl 15(1)(b) is that franchisees be placed in a position whereby they can assess and question how the money they, along with all other contributing franchisees, have provided, has been spent. The information provided is not just lacking the quality of providing “meaningful information”; it has the active quality of providing largely meaningless information except as to raw quantum, begging the question as to what the money was spent on, and how and when. None of the franchisees could have made any useful assessment as to the appropriateness of this item of expenditure based on the financial statement provided by Ultra Tune.

23 The primary judge rejected Ultra Tune’s submission that a newsletter containing more information about expenditure was relevant, saying at [99]:

Although the terms “sufficient detail” and “meaningful information” are subjective, and franchisees may otherwise be aware of specific advertising campaigns, it is clear from the text of cl 15(1)(b) that sufficient detail must be included in the financial statement itself, without recourse being had to other materials, perhaps aided by what might appear in an auditor’s report.

24 His Honour also rejected Ultra Tune’s submission that any adverse finding had to meet the civil standard of proof dictated by the reasoning of Dixon J in Briginshaw v Briginshaw (1938) 60 CLR 336 at 360-2, now reflected in s 140(2) of the Evidence Act 1995 (Cth). His Honour said that Ultra Tune had not identified any evidentiary shortcoming: [100].

25 The primary judge said this at [101]:

I reject Ultra Tune’s submissions referred to above, and more generally. They simply do not grapple with the requirement imposed by cl 15(1)(b) when read with cl 31(3). It follows that I do not accept that Ultra Tune’s financial statements for the 2014-15 and 2015-16 financial years came even close to meeting the requirements of cl 15(1)(b). I therefore find that those contraventions have been easily established.

26 The primary judge rejected Ultra Tune’s submission that it was relevant that this was the first case about the provision and its position was reasonably open to it. In the primary judge’s words at [102]:

First and foremost, I do not accept that Ultra Tune’s approach was reasonably open to it. Further, Ultra Tune failed to change its practices and approach with the introduction of the Franchising Code on 1 January 2015, despite being a large national company with a large scale franchise business. Sophisticated legal advice was not required to understand that its stance was untenable.

27 According to the primary judge at [103]:

In all the circumstances, this was a serious shortcoming and, especially for a large franchisor spending such a large sum of money in a marketing fund, a serious contravention. It was a deficiency for which Ultra Tune provided no real explanation beyond a denial of the manifest inadequacy of what was provided. That stubborn approach calls for a significant deterrent penalty, to encourage future and ongoing compliance by Ultra Tune, as well as franchisors more generally who might otherwise be tempted to skimp on the information provided to their franchisees. To do otherwise would be to countenance ignoring the clear policy objectives of the Franchising Code by making this a hollow requirement, able to be treated in as cavalier a way as Ultra Tune has done.

28 At [104] his Honour said:

A franchisor may be well advised to err on the side of candour, rather than secrecy, or take the risk of expensive adverse consequences and significant reputational harm. Candour is wise in any event, because it inevitably helps to build trust with franchisees, which in turn is likely to facilitate advancing their mutual interests. The use to which a marketing fund is put can and should easily be the subject of meaningful disclosure to franchisees so that they can properly assess how the money they have been required to contribute has been spent.

29 In considering the overall issue of penalties for the disclosure contraventions the primary judge noted that under s 76(1) of the Competition and Consumer Act 2010 (Cth) (the CCA) the Court is to have regard to all relevant matters including:

(1) the nature and extent of the act or omission and of any loss or damage suffered as a result of the act or omission;

(2) the circumstances in which the act or omission took place; and

(3) whether the person has previously been found by the Court in proceedings under Pt VI or Pt XIB of the CCA, to have engaged in any similar conduct.

30 The primary judge also noted the various factors which have been said to be relevant including, for example, in Competition and Consumer Commission v Singtel Optus Pty Ltd (No 4) [2011] FCA 761; 282 ALR 246 at [11]: [303]. He referred also to the purpose of a civil penalty as protective of the public interest in promoting compliance, Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union [2017] FCAFC 113; 254 FCR 68 at [98]: [304].

31 The primary judge identified as a key issue in dispute whether each act or omission by Ultra Tune in relation to its disclosure obligations “should be characterised as being a contravention in relation to each franchisee to which the obligation in some way related, or whether some form of aggregation is required, either as a matter of law, or as a matter of approach having regard to practicality or fairness”: [306]. He correctly observed at [307] that:

The number of contraventions and the maximum penalty for each is important because it sets the overall maximum penalty that is applicable. The Court is required to form a view as to how serious each contravention is, how serious the overall effect of all the contraventions is, and what the individual and overall penalty should be, including by way of adjustment so that the aggregate sanction is proportionate to the conduct. This ensures that the overall penalty imposed is just, as a matter of what is known in the criminal law as “totality”. It should not be a crude mathematical exercise, but necessarily there is a mathematical relationship between these related components.

32 His Honour concluded at [312] that there is a single obligation, capable of constituting only a single contravention for a given financial year:

(1) of maintaining each disclosure document for each of Ultra Tune’s four State-based regions, and thus up to four such contraventions;

(2) of preparing the single marketing fund statement for each of the marketing funds for the five Ultra Tune marketing regions, and thus up to five such contraventions; and

(3) of ensuring that the single marketing fund statement for each of the marketing funds for the five Ultra Tune marketing regions contains “sufficient detail”, and thus up to five such contraventions.

33 His Honour considered that a “failure to prepare a document, to maintain a document, or to have enough detail in a document does not amount to a greater number of contraventions merely because it is required subsequently to be given to, say, 100 franchisees rather than 10 franchisees”: [313]. However, the number of franchisees, he considered, would be relevant to penalty. In contrast, the obligation in cl 15(1)(d) to give the franchisee the statement involves a separate contravention for each franchisee: [316].

34 His Honour’s approach resulted in the following at [318]:

Number and type of disclosure obligation contraventions | Maximum penalty | Competing positions | |

4 | Failure to maintain each of the four separate disclosure documents by updating each within four months of the end of the 2014-15 financial year: cl 8(6) | $216,000 | Ultra Tune admitted the conduct, but disputed the number of contraventions. The ACCC seeks a penalty of $200,000 (four contraventions x $50,000) |

5 | Failure to prepare each of the five financial statements for the five separate marketing funds within four months of the end of the 2014-15 financial year: cl 15(1)(a) | $270,000 | Ultra Tune admitted the conduct, but disputed the number of contraventions. The ACCC seeks a penalty of $250,000 (five contraventions x $50,000) |

10 | Failure to ensure that each of the five financial statements for the five separate marketing funds included “sufficient detail” for each of two financial years, 2014-15 and 2015-16: cl 15(1)(b) | $540,000 | Ultra Tune denied that the conduct had taken place and in any event disputed the number of alleged contraventions. The ACCC seeks a penalty of $350,000 (ten contraventions x $35,000) |

185 (financial statement) 185 (auditor’s report) | Failure to provide to franchisees one of the five different marketing fund financial statements that related to their region within 30 days after each having been prepared for the 2014-15 financial year, to be grouped with the simultaneous and parallel alleged contravention of the failure to provide to franchisees an auditor’s report for each of those marketing fund statements: cl 15(1)(d). | $9.99 million (financial statement) $9.99 million (auditor’s report) (maximum arrived at by multiplying the number of contraventions (185) by the maximum per contravention ($54,000) | Ultra Tune admitted the conduct, but disputed the number of contraventions. The ACCC seeks a penalty of $62,500 (185 contraventions treated as five courses of conduct x $12,500) – an average of just over $337 per contravention, although that sum will be less for regions with a larger number of franchisees and more for regions with a smaller number of franchisees |

1 | Failure to provide a disclosure statement when requested by a franchisee on 16 December 2015 (and required to be provided within 14 days of the request):cl 16(1) | $54,000 | Ultra Tune admitted this contravention. The ACCC seeks a penalty of $30,000. |

Total sought by ACCC: | $892,500 | ||

35 In respect of matters otherwise relevant to penalty, the primary judge said:

(1) “I consider that Ultra Tune’s conduct in this case, including the downplaying of the significance of even admitted contraventions, indicates that Ultra Tune has predominantly manifested the wrong kind of sorry – that is, sorry that it has been caught – rather than sorry that it engaged in the conduct, both admitted and denied, in the first place”: [321].

(2) “Specific deterrence looms large, as does general deterrence lest any other franchisor be tempted to conduct a franchise business in a like manner. Such conduct, by both Ultra Tune, and by others contemplating the same or similar behaviour, will only be likely to be deterred if the penalties imposed are large enough to ensure that this cannot be seen as a mere cost of doing business, or a chance worth taking, because of the greater returns to be made from franchisees, and prospective franchisees, who are not appropriately armed with the information they need to make sound business decisions, in entering into, and continuing franchise arrangements and in spending substantial sums of otherwise unchecked money on marketing funds. Importantly, there was no evidence to indicate that the contravening conduct was aberrant or out of character for Ultra Tune, as opposed to the robust and headstrong way it chose to do business”: [322].

(3) “Ultra Tune…is a substantial national company, now with at least 200 franchisees. It ought to be among the most professional of franchisors, yet plainly it is far from that and appears to have little or no aspiration to be of that calibre.” [323].

(4) “The conduct in relation to the disclosure contraventions was deliberate in the sense that the failure to comply was a consequence of deliberate actions or omissions, rather than inadvertence. Those contraventions took place over a substantial period of time. They involved conduct on the part of the most senior levels of management, including Mr Chong who was company secretary and in-house counsel. There was no suggestion of responsibility on the part of lower level staff, but rather that priority was evidently not given at the highest levels in the company to even informing itself as to what was required to comply with its obligations, let alone to ensuring compliance took place. The evidence was limited as to corporate culture, but it was not established, as a matter of mitigation, that Ultra Tune has a corporate culture conducive to compliance with the Franchising Code or the ACL. There was passing reference to compliance training, but limited evidence as to content, delivery, or response to this case. The corrective response, to the extent it was shown at all, was, at best, leisurely. There was no evidence of active obstruction in relation to the non-disclosure contraventions, but little to suggest an active approach to remedying the defects as a matter of urgency or priority”: [324].

(5) “Ultra Tune is a major franchisor, operating in four States. It has been in this business for many years. Despite that, the evidence reveals that it has failed to take its franchisor obligations seriously. For that reason, each of the disclosure obligation contraventions can be viewed, in that context, and not in some kind of splendid isolation, as being in, or towards, the worst category”: [330].

36 The primary judge at [328] said that he was required:

…to consider each penalty to be imposed for each contravention, or course of conduct involving multiple contraventions, and then to effectively step back, consider the total amounts involved, and make any necessary adjustments to ensure that the overall penalty is just and appropriate as a matter of totality. Many of the penalties that the ACCC seeks are harsh and often reflect a very high proportion of the maximum penalty, which is, at least in the criminal law, to be reserved for the worst category of offending. I consider that this principle applies with equal force and effect to civil penalties, because, as with gaol terms for criminal offences, the maximum pecuniary penalty reflects the legislature’s view as to what the worst category of contravention should attract by way of penalty.

37 Having regard to these matters, the primary judge imposed penalties as follows:

Number and type of disclosure obligation contraventions | Maximum penalty | Individual contravention penalty assessment | |

4 | Failure to maintain each of the four separate disclosure documents by updating each within four months of the end of the 2014-15 financial year: Franchising Code, cl 8(6). | $216,000 | The overall penalty that the ACCC seeks of $200,000 is severe, but reasonable when due regard is had to the 185 franchisees at that time. The maintenance of disclosure documents is essential to the proper functioning of the Franchising Code. In all the circumstances, there is no need for totality adjustment. |

5 | Failure to prepare each of the five financial statements for the five separate marketing funds within four months of the end of the 2014-15 financial year: Franchising Code, cl 15(1)(a). | $270,000 | Again, as a starting point, the overall penalty that the ACCC seeks of $250,000 is condign but reasonable. However, that starting point is in need of totality adjustment, in part due to the interplay with the remaining disclosure obligation contraventions. Having regard to the following contraventions, a final penalty of $150,000 for these five contraventions is appropriate. |

10 | Failure to ensure that each of the five financial statements for the five separate marketing funds included “sufficient detail” for each of two financial years, 2014-15 and 2015-16: Franchising Code, cl 15(1)(b). | $540,000 | The overall penalty that the ACCC seeks of $350,000 is entirely reasonable, especially as Ultra Tune stubbornly adhered to its position that no more information was required. It does not require totality adjustment. |

185 (auditor’s report) | Failure to provide to franchisees one of the five different marketing fund financial statements that related to their region within 30 days after each having been prepared for the 2014-15 financial year, to be grouped with the simultaneous and parallel alleged contravention of the failure to provide to franchisees an auditor’s report for each of those marketing fund statements: Franchising Code, cl 15(1)(d). | $9.99 million (financial statement) $9.99 million (auditor’s report) (maximum arrived at by multiplying the number of contraventions (185) by the maximum per contravention ($54,000) | The overall penalty that the ACCC seeks of $62,500 is inadequate. It fails to reflect the seriousness of the conduct. The course of conduct approach also fails to have regard to the impact on the 185 individual franchisees who did not receive the information that they were entitled to, when it remained of most use to them. As a starting point, each dual contravention of not providing the financial statement and not providing the auditor’s report when required warrants a serious starting point sanction of $10,000. However, when that is multiplied by 185 contraventions, the overall penalty is excessive and disproportionate as it totals $1,850,000. Adjusted for totality, a penalty of $2,000 per dual contravention produces an overall penalty of $370,000. |

1 | Failure to provide a disclosure statement when requested by a franchisee on 16 December 2015 (and required to be provided within 14 days of the request): Franchising Code, cl 16(1). | $54,000 | The penalty that the ACCC seeks of $30,000 is appropriate in all the circumstances. The obligation to provide a disclosure statement promptly when requested requires support by such a sanction so as to forcefully encourage compliance by Ultra Tune and by other franchisees. |

Total: | $1,100,000 | ||

The disputed contravention

38 Four grounds of appeal, grounds 1, 2, 3 and 5, relate to Ultra Tune’s contention that the primary judge erred in finding that it had contravened cl 15(1)(b) of the Franchising Code.

39 In respect of ground 1, Ultra Tune referred to the principle that in the context of a penal statute if the language of the statute remains ambiguous or doubtful after the application of anodyne construction principles then the ambiguity or doubt may be resolved in favour of the subject by refusing to extend the category of the criminal offence: Beckwith v The Queen (1976) 135 CLR 569 at 576 and 585.

40 Ultra Tune noted that in Deming No 456 Pty Ltd v Brisbane Unit Development Corporation Pty Ltd (1983) 155 CLR 129 at 145 the plurality said:

…the prima facie construction of those parts of the section which impose obligations is that any real ambiguity persisting after the application of the ordinary rules of construction is to be resolved in favour of the most lenient construction.

41 Ultra Tune submitted that the primary judge’s reasons do not expose consideration of this principle, which is an aspect of the rule of law, despite the primary judge having expressed the view that the provision was not particularly clear and was subjective: [88] and [99]. On this basis cl 15(1)(b), by reason of its ambiguity, engaged the principle of lenity which ought to lead to the conclusion that Ultra Tune had not contravened the provision.

42 In respect of ground 2, Ultra Tune referred to the inconsistency of in terrorem penalties and the rule of law. At the centre of this ground are the primary judge’s observations that by its “stubborn approach” of putting arguable contentions about cl 15(1)(b), a significant deterrent penalty was required to be imposed to ensure compliance by Ultra Tune and other franchisors “who might otherwise be tempted to skimp on information”: [103]. Ultra Tune characterised [104] of the primary judge’s reasons as a threat that franchisors should err on the side of candour, or risk expensive adverse consequences. Ultra Tune said that the message is that if there was doubt as to the content of an obligation, a franchisor better not exercise its constitutional right to have the matter determined by the Court. Such an approach, said Ultra Tune, is contrary to the rule of law. Central to the rule of law is the need for coherence, clarity, and reasonable certainty and that liability not be the product of discretion, choice, sentiment, or intuition. Much less, said Ultra Tune, should liability be found in the face of uncertainty expressly on the ground that it will serve as a warning to others. The primary judge’s reasoning, it was submitted, exposes this error of principle. If the requirements of the rule of law had been applied, no contravention of the uncertain obligation imposed by cl 15(1)(b) would be found.

43 In respect of ground 3, Ultra Tune said that the primary judge, having correctly identified the relevance of cl 31 and the antecedent disclosure documents, did not then reason by comparing what had prospectively been disclosed as authorised categories of expenditure with the actual expenditure in the cl 15(1) financial statement. In Ultra Tune’s words, if looking at those two documents a reader could discern that money had been spent as disclosed and in what proportions between the disclosed classes, then the contextually relevant cl 31 would have strongly favoured a finding of sufficiency. The disclosure documents identified permitted categories of expenditure including for Broadcasting (e.g. Television, Radio). Viewed against this disclosure the cl 15(1) statements were very precise as the reader could discern that the expenditure had been for the permitted purpose of “Promotion & Advertising – Television”. This, said Ultra Tune, meant that the statutory purpose had been satisfied. The reader could tell that the expenditure fell within the disclosed permitted class of expenditure.

44 Further, it was within common human experience to understand precisely what was meant by promotion and advertising on television. The description accurately and sufficiently conveyed what this part of the fund was spent on. It could not be said that this descriptor was not useful and practical. The primary judge’s focus on the percentage of the fund spent on television advertising was misplaced. The information did not become less informative because it comprised the major item of expenditure. While “sufficient” involves an evaluative determination, the primary judge put a substantial gloss on the provision in discerning that generally the greater the expenditure the greater the level of detail required. Contrary to the primary judge’s conclusions, financial statements do not reveal the when, how and why of expenditure. Nothing in the provision discloses any purpose of disclosure of the when, how and why of the expenditure. The principal purpose is that the franchisee can ascertain if the expenditure is one of the items disclosed as a permissible kind of expenditure in the disclosure document. Further, said Ultra Tune, the primary judge described the provision as being both subjective in [99] and as containing “objective requirements” in [100]. Either way, the uncertainty lay in the statutory obligation and not the quality of the evidence.

45 In respect of ground 5, and in the face of the primary judge’s finding that the statutory obligation was not particularly clear or prescriptive, it must also have been relevant to both the existence of the contravention and the penalty to be imposed if a contravention had been proved that cl 15(1) requires the statement to be independently audited by a registered auditor. It must have also been relevant in this case that the auditor had issued unqualified audit statements to the effect that the statements were in accordance with cl 15(1) of the Franchising Code. The primary judge did not take these facts into account as relevant to the existence of the contravention and, if the contravention was proved, penalty.

46 We are not persuaded by Ultra Tune’s submissions that the primary judge erred in finding that it had contravened cl 15(1) by not ensuring that the statements included sufficient detail of the fund’s receipts and expenses so as to give meaningful information about, relevantly, items of expenditure, particularly with respect to advertising and marketing expenditure. The construction proposed by the ACCC and accepted by the primary judge at [86] that the text of cl 15(1)(b) requires the financial statement to have “some explanatory force and permit meaningful insights to be gained by the franchisee” is to be preferred. Ultra Tune did not propose any alternative construction. The inescapable fact is that cl 15(1) is not concerned with a mere financial statement. The words “sufficient detail…so as to give meaningful information about…items of expenditure” must be given work to do. While the work those words do involves an evaluative exercise calling for the making of a judgement, the obligation is not ambiguous or uncertain in any manner that would require the class of contraventions to be confined by the principle of lenity. The application of the principle in Beckwith does not arise. The primary judge did not err by not applying that principle.

47 The problem with Ultra Tune’s approach is that it would give the key words describing what more than a mere financial statement is required no work to do. On Ultra Tune’s approach it would be sufficient if the item itself and the proportion of expenditure spent on the item appeared in the financial statements. Under the provision, however, there must be information “about” the item. In the present case, there is no information about the item when it is readily apparent that meaningful information could have been provided. For example, it is obvious that such information could have included a breakdown of expenditure by reference to pay TV or free to air, or the channels on which the television advertising had appeared. The facts of the particular case will determine the issue of sufficiency which lends support to the primary judge’s observation at [104], that a franchisor would be well advised to err on the side of candour. As it is, the financial statements contain only the item itself and no information about the item.

48 It may be accepted that one important purpose of the statutory regime arises from the relationship between cl 31 and cl 15. Clause 31 provides that the marketing or advertising fees may only be used to meet expenses that have been disclosed to franchisees under para 15.1(f) of the disclosure document. That paragraph provides for the disclosure document to identify the kinds of expenses for which the fund may be used. In this context, it is a clear purpose of the provisions that franchisees be able to tell if the actual expenditure for the year has been for the kinds of expenses prospectively identified in the disclosure document. But this is not the only purpose of cl 15(1). That provision also has the purpose of ensuring franchisees are given sufficient details so as to constitute meaningful information about the items of expenditure. It makes sense that while prospective kinds of expenditure may only be able to be dealt with at a relatively high level of generality, actual expenditure is capable of being disclosed in greater detail. In the present case, as we have said, the greater detail which could have been provided and would have been meaningful to the franchisees is obvious. It is the channels on which the advertising appeared and the percentage of the expenditure on a per channel basis.

49 By only disclosing the item on which there had been expenditure in the form of “Promotion & Advertising – Television” Ultra Tune did not provide sufficient detail so as to give meaningful information about the item as required by cl 15(1)(b)(ii) of the Franchising Code. The contraventions for each of the financial years 2014-2015 and 2015-2016, accordingly, were established and the primary judge did not err in so concluding.

Clause 15(1) – the number of contraventions

50 Ultra Tune submitted that cl 15(1) creates a single obligation to prepare, have audited, and give to franchisees a statement complying with the various requirements of cl 15(1). Ultra Tune noted that each obligation is sequentially conjoined by the word “and” so that as a matter of textual analysis there is a single obligation to do all of the things in the sub-paragraphs. Further, the words “Civil Penalty: 300 penalty units” appear once only at the foot of cl 15(1). Section 76(1) of the CCA empowers the Court to impose one pecuniary penalty in respect of each act or omission to which the section applies. The section applies only because Ultra Tune contravened a civil penalty provision in an industry code. The relevant civil penalty provision is cl 15(1) as a whole. Ultra Tune contended that there was a single contravention in respect to each of the marketing funds (subject to the application of grouping principles). The primary judge’s contrary approach, which involves breaking down cl 15(1) into its component parts, does not reflect the text of the provision.

51 The respondent, the ACCC, supported the primary judge’s approach but contended that if Ultra Tune’s approach were correct, then a contravention would exist for each franchisee, that is, 185 in total in the 2014-2015 financial year and 200 in total in the 2015-2016 financial year.

52 We are persuaded that cl 15(1) creates a single contravention. The text of cl 15(1) reflects that its purpose is directed to the provision of information to franchisees. Clause 15(1) involves a cascading series of obligations for the preparation, auditing, and giving to the franchisee a statement which satisfies the requirements of the provision. The clause can be contravened in a multiplicity of ways, the culmination of which is to give to the franchisee (which must mean each franchisee) the required statement. How many of the series of obligations are breached is relevant to the objective seriousness of the contravention. We accept the construction contended for in the ACCC’s notice of contention.

53 That cl 15 is a single contravention is borne out by the practical application of the clause. For example, if a franchisor does not prepare the required statement, it will be in breach of cl 15(1)(a) and liable to a penalty of 300 units. That franchisor is only in breach of that one obligation, the others, which are premised on the existence of the statement, can have no application. That is to be contrasted with the situation where a franchisor does prepare a statement, albeit late and lacking sufficient detail to comply with the obligations in cl 15(1)(a) and (b). On the primary judge’s analysis, that franchisor would be liable for two contraventions and accordingly exposed to a penalty greater than 300 units. The clause ought not to be construed such that a franchisor who attempts to comply with it is in a worse position than a franchisor who does not.

54 It follows that we do not agree with the primary judge’s analysis of the number of contraventions of cl 15(1) as summarised in the tables at [318] and [331]. On our approach, the table would be as follows:

Number and type of disclosure obligation contraventions | Maximum penalty | |

4 | Failure to maintain each of the four separate disclosure documents by updating each within four months of the end of the 2014-15 financial year: cl 8(6) | $216,000 |

185 | Failure to prepare an annual financial statement as required by cl 15(1)(a) and (b) and to have that statement audited as required by cl 15(1)(c) and to give that statement and any auditor’s report to each franchisee as required by cl 15(1)(d) for the 2014-2015 year. | $9.99 million |

200 | Failure to prepare an annual financial statement as required by cl 15(1)(b) and to give that statement and any auditor’s report to each franchisee as required by cl 15(1)(d) for the 2015-2016 year. | $10.8 million |

1 | Failure to provide a disclosure statement when requested by a franchisee on 16 December 2015 (and required to be provided within 14 days of the request):cl 16(1) | $54,000 |

Imposition of penalties

55 While we agree with much of what the primary judge said about the imposition of penalties, the fact that we take a different view about the number of contraventions necessitates appellate review of the penalties imposed.

56 Before returning to the imposition of penalties, it is necessary to record the other instances where our conclusions differ from those reached by the primary judge.

57 First, we consider that Ultra Tune’s approach to the obligation imposed by cl 15(1)(b) was reasonably arguable. While we agree with the primary judge that Ultra Tune did not provide sufficient detail so as to provide meaningful information about the item of expenditure “Promotion & Advertising – Television”, Ultra Tune’s argument had a rational foundation in the statutory scheme. It is part of the purpose of cl 15(1)(b) to enable franchisees to ascertain if actual expenditure matches the kind of expenditure prospectively disclosed in the disclosure document. Given this, Ultra Tune’s position in respect of this aspect of the litigation was not based merely on the “manifest inadequacy” of what it had provided. It was based on an arguable proposition that its disclosure fulfilled the statutory purpose. This is in the context where this is the first consideration of cl 15(1). Accordingly, in respect of this aspect of the litigation, at least Ultra Tune’s conduct cannot be characterised as a “stubborn approach” which, of itself, called for a “significant deterrent penalty”.

58 This said, there is force in the primary judge’s description of Ultra Tune having acted in a “cavalier” way with regard to its obligations under the Franchising Code. The evidence is clear that the person within Ultra Tune responsible for compliance with the disclosure obligations did not know about the new requirements in cl 15(1)(b) and did not get around to dealing with the obligations under the provision because priority had been given to some litigation instead.

59 Second, the fact that the relevant person did not know about the obligation in cl 15(1)(b) also establishes that while Ultra Tune’s contraventions of that provision may have been egregious, they were nevertheless inadvertent. The primary judge, however, characterised all of Ultra Tune’s disclosure contraventions as deliberate in the sense of being the consequence of deliberate acts or omissions. This is true in respect of the defaults in respect of the time requirements, but not in respect of the content of the financial statements where a fairer description would be contraventions resulting from egregious inadvertence.

60 Third, given these considerations we are unable to agree with the primary judge that the disclosure contraventions are in or towards the worst category of case. The contraventions are objectively serious for all of the other reasons the primary judge gave (summarised above and with which we agree), but its conduct did not involve a wilful failure on Ultra Tune’s part to do what was required of it. Ultra Tune did what it believed was required, albeit belatedly in 2014-2015. As a result, it cannot be said that the contraventions are in or towards the worst category of case.

61 It necessarily follows from these conclusions that we agree with Ultra Tune that the basis upon which the primary judge imposed penalties involved error. Accordingly, the task of imposing penalties must be performed by this Court. As a result, Ultra Tune’s other appeal grounds (excluding ground 15 relating to the corrective notice) are otiose. For the sake of completeness, however, we should record our view that we do not agree that the primary judge failed to apply the principle of totality. The primary judge correctly identified the principle at [328] and in the table at [331], which expressly stated that the starting point for the imposition of a penalty for contraventions of cl 15(1)(a) was in need of a totality adjustment “in part due to the interplay with the remaining disclosure obligation contraventions”.

62 The balance of Ultra Tune’s submissions about penalty focused on what it referred to as the single course of conduct or one transaction or grouping principle. Most recently, in Australian Building and Construction Commissioner v Construction, Forestry, Maritime, Mining and Energy Union (The Nine Brisbane Sites Appeal) [2019] FCAFC 59 the Full Court found that the trial judge had erred in concluding that only one maximum penalty was available where there were multiple contraventions that constituted a single course of conduct. This was identified as the same error as occurred in Australian Competition and Consumer Commission v Yazaki Corporation [2018] FCAFC 73; 357 ALR 55 at [241]. Allsop CJ at [11] and [12] in The Nine Brisbane Sites Appeal said:

11 …that error, in my view, had its genesis in the task that the primary judge set herself immediately antecedently. Her Honour asked whether there was a single course of conduct as if (in the absence of the relevant operation of a provision such as s 557 of the Act) there were a single thing or conception of “a course of conduct”. As the Full Court said in Transport Workers’ Union of Australia v Registered Organisations Commissioner [No 2] [2018] FCAFC 203; 363 ALR 464 (TWU v ROC) at [91]:

… Absent the relevant application of a provision such as s 557(1) of the Fair Work Act, the task is to evaluate the considerations informing the contraventions (factual and legal) in order to impose appropriate penal relief that does not punish twice for the same conduct. To use a phrase such as “a course of conduct” may imply that there is such an abstracted concept to be found, and once found it implies a single contravention or a single maximum penalty. That is the danger of the phrase. Rather, it is necessary (in the absence of a statutory enquiry such as in s 557(1)) to examine all the conduct and enquire how its course and its explanation factually and legally informs the imposition of penal orders, in particular to avoid double punishment. We see nothing in Williams or The Agreed Penalties Case that was intended to displace the need to consider the statute in question and to recognise that the object of the course of conduct principle is to avoid double punishment.

12 The danger in the use of the phrase identified by the Full Court in TWU v ROC occurred here: in finding a single course of conduct, the primary judge confined the penal response to one determined by reference to one maximum penalty. The preferable enquiry, conformable with the purpose of the principle and with what was said in TWU v ROC is “to examine all the conduct and enquire how its course and its explanation factually and legally informs the imposition of penal orders, in particular to avoid double punishment.” This enquiry may involve the finding of factual and legal overlap and interrelationship among the contraventions. A conclusion that there is such an interrelationship or overlap, and so, to use the expression, a course of conduct, does not mark the end of the enquiry, but the beginning of one: How, given the nature of the interrelationship or overlap, should that affect the proper fixing of penalties for the found contraventions so as to avoid multiple punishment for the same offending?

63 In the present case, Ultra Tune argued that the contraventions of both cl 8(6) and cl 15(1) of the Franchising Code in the 2014-2015 financial year were interrelated. Clause 8(6) required the disclosure document to be updated within four months after the end of each financial year. Clause 15(1)(a) required the preparation and auditing of the annual financial statement within the same four month period for the purpose of giving that document to the franchisees. The obligations under cl 8(6) could not be performed until the auditors had performed their obligations under cl 15(1)(a) of the Franchising Code and Item 21.4 of Annexure 1 thereto (the requirement for a statement about the franchisor’s solvency). As Ultra Tune put it, for the 2014-2015 financial year:

All contraventions stemmed from the financial statements and auditor’s reports (ie the two separate auditor reports, the first being required under cl 15(1)(c) and the second being required under cl 21.4 of Annexure 1 to the Code) being given late to the Appellant by the third providers…

64 Ultra Tune said that the following evidence explained the delay in the 2014-2015 marketing fund financial statements and audit reports:

(1) Up to financial year 2014, the registered company auditor who had audited the marketing fund financial statements was Mr Neil Turner.

(2) On 16 September 2015 Ultra Tune’s accountants sent an email to Mr Turner asking him to audit the annual financial statements for 2014-2015. Mr Turner replied that he had resigned as a registered company auditor.

(3) On 22 September 2015 Ultra Tune approached another firm to act as auditors. However, to expedite the audit in early December 2015 Ultra Tune approached Mr Griffiths to undertake the audit and provide signed audit reports which was done on 24 December 2015.

65 Ultra Tune also said that the earlier delays in its compliance with the requirements of cl 8(6) and cl 15(1) of the Franchising Code (not amenable to a civil penalty), on analysis, were also caused by delays by the former external accountants and auditors. Further, that it was relevant to penalty that two separate registered auditors had signed off on financial statements relevantly in the same terms as the financial statements the primary judge had found to be manifestly inadequate. Ultra Tune said that while it might have been open to the primary judge to give this latter fact limited weight, it was not open to his Honour to remain silent about either that fact or the circumstances in which the earlier financial statements and audit reports had been delayed which showed delay by the external service providers to Ultra Tune.

66 The ACCC said that the delays in compliance by Ultra Tune with its obligations were significant. The disclosure document and annual financial statement for the 2014-2015 year were meant to be completed by 31 October 2015 and the annual financial statement was then required to be given to franchisees within 30 days thereafter. Two franchisees in Queensland received the annual financial statement and auditor’s report for Queensland on 28 January 2016. One franchisee in NSW received the annual financial statement and auditor’s report for NSW on 29 January 2016. The other 182 franchisees did not receive the annual financial statement and auditor’s report until 11 August 2016 (over eight months after the due date) and, when it was received, it did not comply with the requirements of cl 15(1)(b). Ultra Tune’s reference to delay by external service providers does not provide an adequate explanation for these delays. In any event, it is Ultra Tune’s obligation as franchisor to ensure that it complies with the requirements. As a major franchisor operating in four states, Ultra Tune should have taken its obligations more seriously. The ACCC said further that the contraventions of cl 8(6) affected 185 franchisees and the penalty the primary judge imposed of $200,000 can be apportioned to $1,081 per franchisee. The contraventions of cl 15(1) affected 185 franchisees in 2014-2015 and 200 franchisees in 2015-2016 and the total penalties imposed of $870,000 can be apportioned to $3,756 per franchisee for 2014-2015 and $875 for 2015-2016. The ACCC said these are modest sums in the context of the sums paid to Ultra Tune by its franchisees and the importance of the information being provided to franchisees in a timely manner to assist them in their ongoing decision-making.

67 We otherwise agree with the primary judge that the contraventions were objectively serious by reason of the length of the delay in the ultimate provision of the required documents to franchisees the effect of which was largely to undermine the statutory purposes of transparency and accountability of Ultra Tune’s expenditure, the fact that the overall delay in 2014-2015 is not explained by the conduct of the external service providers, Ultra Tune’s history of non-compliance with the applicable provisions in circumstances where it is ultimately Ultra Tune’s responsibility alone to ensure compliance, and the large number of franchisees adversely affected by Ultra Tune’s contraventions.

68 We agree with the primary judge that the circumstances with respect to cl 8(6) should be treated as four contraventions given that Ultra Tune arranged its business so as to provide four separate disclosure documents for individual regions. We consider the penalty of $200,000 imposed by the primary judge reflects his view that the contraventions were in or towards the worst category of case, a characterisation which we do not accept in all of the circumstances. We consider that a penalty of $130,000 or about 60% of the maximum penalty reflects the objective seriousness of these contraventions. We do not consider that this amount needs to be reduced by reason of the principle of totality but accept Ultra Tune’s submissions that given the connection between the cl 8(6) and cl 15(1) contraventions further consideration should be given to that principle by reference to all penalties imposed.

69 The cl 15(1) contraventions should be considered separately for the 2014-2015 and 2015-2016 financial years. Ultra Tune’s obligations in each year were to prepare and give to each franchisee complying documents within the time periods prescribed. The fact that the maximum penalty increases per franchisee, in our view, correctly reflects the fact that the greater the number of franchisees affected, the more objectively serious the contraventions. For each year, however, there is an obvious element of double punishment which is apparent. The documents required to be prepared and provided are the same for each franchisee in each of Ultra Tune’s five marketing regions. If none of the documents are prepared and provided as required, then a franchisor will necessarily commit a contravention for each franchisee in each region. The contraventions will result from the same facts of non-preparation relating to each of the five marketing regions.

70 In this case, in 2014-2015 there was the failure to comply with the time and content requirements in cl 15(1) and in 2015-2016 the failure to comply with the content requirements of that clause. It is apparent from this analysis that the contraventions for 2014-2015 are objectively more serious than those for 2015-2016. The latter contraventions related only to the contents of the document. The failure to provide the required content (in both years) flowed from an egregious inadvertence as to the content of the obligations upon the company. The auditors had given unqualified opinions that the financial statements complied with the requirements of cl 15 (also in both years). It follows that any penalty for the 2015-2016 financial year should be materially less than the penalty for the 2014-2015 financial year, even taking into account the increased number of franchisees in the 2015-2016 financial year. We also do not consider that any penalty for the 2015-2016 financial year should reflect the characterisation that Ultra Tune “stubbornly adhered to its position that no more information was required” given that Ultra Tune’s position was reasonably arguable having regard to the terms of the statutory scheme and the unqualified auditor’s reports.

71 In all of the circumstances, and having regard to the fact that the contraventions for the 2015-2016 financial year arose out of a single act with respect to the preparation of the five annual financial statements (one for each marketing region), it is apparent that a penalty on a per franchisee basis would involve a substantial element of double punishment. It is also impossible and to a degree artificial to seek to eliminate such double punishment by ascribing individual amounts to each contravention for each franchisee. It is more appropriate to identify an overall total recognising that it is the proper sum for all the contraventions per franchisee avoiding double punishment. Having regard to all the circumstances, including the continuing inadvertence of the senior management of the company as to the proper content of the financial statement (what we have earlier called “egregious inadvertence”) the contraventions in 2015-2016 should attract penalties totalling $150,000. This can be seen as $750 per franchisee. This, we consider, reflects the relevant degree of seriousness of all the circumstances, and proper and appropriate attention to specific and general deterrence.

72 As to the 2014-2015 financial year, these contraventions were more serious as involving both time and content. Having regard to all the circumstances, including the egregious inadvertence of management as to their responsibilities as to content and the serious delay involved, the contraventions should attract penalties totalling $200,000. This can be seen as a little under $1,100 per franchisee.

73 We emphasise that in respect of neither 2014-2015 nor 2015-2016 have we calculated the total penalties mechanically by reference to numbers of franchisees. Rather, we use these calculations to aid in an assessment of the appropriate overall response to the necessary deterrence, specific and general, flowing from all the circumstances and the objective seriousness of the conduct.

74 The total penalties, accordingly, may be represented as follows:

Number and type of disclosure obligation contraventions | Maximum penalty | Imposed penalty | |

4 | Failure to maintain each of the four separate disclosure documents by updating each within four months of the end of the 2014-15 financial year: cl 8(6) | $216,000 | $130,000 |

185 | Failure to prepare an annual financial statement as required by cl 15(1)(a) and (b) and to have that statement audited as required by cl 15(1)(c) and to give that statement and any auditor’s report to each franchisee as required by cl 15(1)(d) for the 2014-2015 year. | $9.99 million | $200,000 |

200 | Failure to prepare an annual financial statement as required by cl 15(1)(b) and to give that statement and any auditor’s report to each franchisee as required by cl 15(1)(d) for the 2015-2016 year. | $10.8 million | $150,000 |

1 | Failure to provide a disclosure statement when requested by a franchisee on 16 December 2015 (and required to be provided within 14 days of the request):cl 16(1) | $54,000 | $30,000 |

75 We do not consider that the overall total of these penalties requires any further adjustment by reference to the totality principle. The total amount of $510,000, in our view, fairly and justly reflects the objective seriousness of the contraventions and fulfils the need for specific and general deterrence. The penalties are not so low as to be capable of being seen as an acceptable cost of doing business yet are not so high as to suggest a level of objective seriousness which we do not consider is warranted on the facts.

The corrective notice

76 Ultra Tune made it clear that if it succeeded on this ground alone it would not seeks costs of the appeal. On that basis the parties should have been capable of agreeing the amendment to the notice as sought by Ultra Tune, the sole purpose of which was to make it clear that the franchisees were in no way responsible for the contraventions. Ultra Tune provided an amended notice which has been referred to in the orders.

The orders

77 Those orders reflect the fact that part of the civil penalties which the primary judge imposed were not subject to any challenge in this appeal (that is, the sum of $1,504,000). For the penalties subject to challenge the difference between the penalties imposed by the primary judge and on appeal results in a total penalty of $2,014,000 (rather than $2,604,000). We have also reached a preliminary view that based on their respective levels of success in the appeal, the ACCC should pay 60% of Ultra Tune’s costs of the appeal, but the parties have been given a further opportunity to address the issue of costs in writing.

I certify that the preceding seventy-seven (77) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Chief Justice Allsop, and Justices Jagot and Abraham. |

Associate:

Dated: 20 September 2019