FEDERAL COURT OF AUSTRALIA

Bluescope Steel (AIS) Pty Ltd v Australian Workers’ Union [2019] FCAFC 84

ORDERS

First Appellant BLUESCOPE STEEL LIMITED Second Appellant | ||

AND: | Respondent | |

Intervener | ||

ALLSOP cJ, COLLIER AND RANGIAH JJ | |

DATE OF ORDER: | 24 MAY 2019 |

THE COURT ORDERS THAT:

1. The parties have 14 days in which to file and serve submissions as to the form of any orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ALLSOP CJ:

1 This is an appeal by first appellant BlueScope Steel (AIS) Pty Ltd and second appellant BlueScope Steel Limited (together, BlueScope, individually, BlueScope AIS and BlueScope Steel) from the declarations and orders of a judge of this Court delivered on 20 March 2018, giving effect to reasons published on 14 February 2018. In the primary judgment, it was held that the first appellant had contravened item 15 of Schedule 16 of the Fair Work (Transitional Provisions and Consequential Amendments) Act 2009 (Cth) and s 50 of the Fair Work Act 2009 (Cth) by, in broad terms, failing to make appropriate superannuation contributions to its employees.

2 Few facts are contentious. The variety and detail of the industrial awards and agreements applying to BlueScope’s employees and the intricacies of the Commonwealth superannuation framework add some complexity to the matter, but the underlying facts are simple. BlueScope pays some of its employees annualised or aggregate salaries. Employees working under an annualised salary system worked up to 43.5 hours per week (38 hours plus 5.5 “additional hours”) to meet the needs of the business. Further, as well as those engaged under the aggregate salary system, they were rostered to work on public holidays. The employees’ annualised or aggregate salaries included payment for not only the base salary, but also the additional hours and public holidays. The essential difference between the annualised and aggregate salary is that in the former a body of additional hours (5.5 per week) is pre-paid as part of an additional hours component.

3 For the purposes of the proceedings at first instance and on appeal, argument was confined to the employment circumstances of two employees: Mr Storey and Mr Le Clerc. Both were covered by the three relevant industrial instruments: the BlueScope Steel (AIS) Pty Ltd – Port Kembla Works Employees Award 2006 from 2006 to 8 August 2013 (the 2006 Award); the BlueScope Steel Port Kembla Steelworks Agreement 2012 from 9 August 2013 to 24 November 2015; and the BlueScope Steel Port Kembla Steelworks Agreement 2015 from 25 November 2015 to at least the time of the primary proceedings (the 2012 Agreement, the 2015 Agreement, and together, the 2012 and 2015 Agreements). Mr Storey and Mr Le Clerc were covered by different departmental agreements. Mr Storey was covered by the Bulk Operations Enterprise Agreement 2005 from 17 February 2006 to 21 August 2013 and the Bulk Operations Department Agreement 2013 from 21 August 2013 until 16 January 2016. He had an annualised salary until 10 January 2016, after which he had an aggregate salary. Mr Le Clerc always worked for an aggregate salary, pursuant to the Slabmaking – 12 hour Shift Agreement 2004 from April 2004 to 13 January 2013 and the Slab Yard - 12 hour Shift Agreement 2010 from 13 January 2013 to at least the time of the primary proceedings. Relevant provisions in these Awards and Agreements are detailed at [13]-[44] of the primary judgment.

4 In effect, two questions were before the primary judge. First, whether payment for additional hours included in the annualised salary were “ordinary time earnings” for the relevant superannuation legislation. Secondly, whether public holiday payments included in the annualised or aggregate salaries were “ordinary time earnings” for the same legislation.

5 Attention was focused on Mr Storey in relation to the question of whether the “additional hours” and “public holidays” components of the annualised salary fell within ordinary time earnings by reference to his receipt of an annualised salary. In relation to Mr Le Clerc, who was paid an aggregate salary which did not include the “additional hours” element, the question focused solely on the “public holidays” component.

6 Critical to answering these questions is the construction, interpretation and application of the phrase “ordinary time earnings” and “ordinary hours of work” as used in s 6 of the Superannuation Guarantee (Administration) Act 1992 (Cth) ( the SG Administration Act). The application of the phrase involves the correct construction and interpretation of the relevant industrial instruments.

7 For the reasons that follow, subject to giving the parties an opportunity that they sought to be heard on the orders, I would allow the appeal, set aside the orders made by the primary judge, and in lieu thereof dismiss the application.

Threshold questions: Are the instruments relevantly capable of being contravened?

8 The first issue is whether the industrial instruments, insofar as they deal with superannuation contributions, are capable of being contravened. This threshold issue was ground 2 of the Notice of Appeal. The primary judge concluded that the awards (represented by the 2006 Award) were capable of being contravened, and were contravened, for the purposes of Item 15 of Sch 16 to the Fair Work (Transitional Provisions and Consequential Amendments) Act and the enterprise agreements (represented by the 2012 and 2015 Agreements) were capable of being contravened, and were contravened, for the purposes of s 50 of the Fair Work Act.

9 The provisions of the 2006 Award and 2012 and 2015 Agreements, found by the primary judge to have been contravened (cl 7 of the 2006 Award, and cl 7 of the 2012 and 2015 Agreements) are as follows:

7. Superannuation [2006 Award]

7.1 Superannuation Legislation - the Subject of Superannuation is dealt with exhaustively by federal legislation including the Superannuation Guarantee (Administration) Act 1992 (Cth), the Superannuation Industry (Supervision) Act 1993 (Cth), the Superannuation (Resolution of Complaints) Act 1993 (Cth), and section 124 of the Industrial Relations Act 1996. This legislation, as varied from time to time, governs the superannuation rights and obligations of the parties. Subject to this legislation, superannuation is also dealt with by the trust deed and rules of the BlueScope Steel Superannuation Fund and the Superannuation Trust of Australia, and relevant agreements made from time to time between the Company and the unions party to this award, including the BHPSteel - Superannuation Review dated 25 October 1995.

7.2 Salary Sacrifice -

7.2.1 Despite any other provisions of this award, for the purpose of calculating ordinary time earnings, the rate of pay per week prescribed for the purpose of clause 6, Rates of Pay, is reduced by the amount which an employee elects by notice in writing to the Company to sacrifice in order to enable the Company to make a superannuation contribution for the benefit of the employee.

7.2.2 Election Form - For an employee’s election to be valid the employee must complete an election form provided by the Company.

7.2.3 Leave - The reduced rate of pay and the superannuation contributions provided for in this subclause apply for periods of annual leave, long service leave, and other periods of paid leave.

7.2.4 Calculation of other payments - All other award payments, including termination payments, calculated by reference to the employee’s rate of pay will be calculated by reference to the rate of pay per week prescribed for the employee for the purpose of clause 6, Rates of Pay.

7.2.5 Revoking Election - Unless otherwise agreed by the Company, an employee may only revoke or vary his or her election once in each twelve months. Not less than one months’ written notice will be given by an employee of revocation or variation of the employee’s election.

7.2.6 Termination of Scheme - If at any time while an employee’s election is in force, there are changes in taxation or superannuation laws, practice or rulings, that materially alter the benefit to the employee or the cost to the Company of acting in accordance with the election, either the employee or the Company may, upon one months’ notice in writing to the other, terminate the election.

7.2.7 Superannuation Guarantee - The Company will not use any superannuation contribution made in accordance with an employee’s election to meet its minimum employer obligation under the Superannuation Guarantee Administration Act 1992 (Cth) or any legislation which succeeds or replaces it.

…

7. Superannuation [2012 and 2015 Agreements]

7.1 Superannuation arrangements are governed by Federal legislation including the Superannuation Guarantee (Administration) Act 1992 (Cth), the Superannuation Industry (Supervision) Act 1993 (Cth), and the Superannuation (Resolution of Complaints) Act 1993 (Cth).

7.2 The Company will make contributions to an employee’s superannuation account at a minimum in compliance with the Superannuation Guarantee (Administration) Act 1992 (Cth), as varied from time to time. Additionally for permanent employees who are members of the BlueScope Steel Superannuation Fund or Australian Super, subject to these statutory minimum contributions and the Basic Member Contributions an employee makes to their superannuation account, the Company will make contributions into an employee’s superannuation account in accordance with the below scale:

Employee Contribution | Company Contribution |

0 | 9% |

3% | 10% |

4% | 12% |

5% | 14% |

All company contributions are based on an Employee’s Defined Wage, as defined at clause 4 above.

…

7.3.7. Superannuation Guarantee - The Company will not use any superannuation contribution made in accordance with an employee’s election to meet its minimum employer obligation under the Superannuation Guarantee Administration Act 1992 (Cth) or any legislation which succeeds or replaces it.

10 There were two aspects of the primary judge’s approach. First, even if cl 7 of the 2006 Award and cl 7.2 of the 2012 and 2015 Agreements did not contain any binding legal obligation to make superannuation contributions, that did not prevent them being contravened. (His Honour accepted that cl 7 of the 2006 Award was not a binding obligation.) All that was required in this regard was that the provision of the award or enterprise agreement was “a mere acknowledgment of a requirement to make a contribution otherwise imposed by statute and that such a contribution has not been made”: [64] of the primary judge’s reasons. Secondly, the primary judge concluded that cl 7.2 of the 2012 and 2015 Agreements did contain an independent legal obligation to make superannuation contributions.

11 It is necessary to deal with these conclusions at the outset, because if the appellants are correct and neither cl 7 of the 2006 Award nor cl 7.2 of the 2012 and 2015 Agreements contains a legal obligation to make contributions, there can be no relevant contravention.

12 In relation to these threshold questions, my view is that the primary judge was:

(a) correct that cl 7 of the 2006 Award did not contain a legal obligation to make contributions for superannuation;

(b) not correct that cl 7 of the 2006 Award contained an acknowledgment of a requirement to make a contribution;

(c) not correct that to contravene an award or enterprise agreement one needed only to find that there was an acknowledgment of a requirement to make a contribution imposed otherwise and that such had not been made; and

(d) correct that cl 7.2 of the 2012 and 2015 Agreements did contain a legal obligation to make contributions for superannuation.

13 The words of cl 7 of the 2006 Award are entirely free of any text connoting obligation. There is only a recognition that Commonwealth legislation governs the matter of superannuation. Nor does any language acknowledge any requirement to make contributions. The reference to the Commonwealth legislation does not do that. Such lack of acknowledgement of requirement reflects the legislation in which there is no statutory obligation placed on employers to make superannuation contributions on behalf of employees. Rather, the legislation operates as a tax encouraging employers to pay superannuation contributions to avoid a significantly more expensive imposition of a (non-deductible) superannuation guarantee charge, if deductible contributions are not made. In practical parlance it may be said that employers are required to make contributions for superannuation. That is not the legal form or substance. It is unnecessary at this point to explain the precise working of the superannuation legislation.

14 The respondent relied on s 124 of the Industrial Relations Act 1996 (NSW). That section, however, is predicated upon an employer being required by an industrial instrument to pay superannuation contributions to a specified fund. Clause 7 does not require the employer to pay contributions, nor does it require the employer to pay contributions to a particular fund. The provision takes the matter no further.

15 In Parker v Comptroller-General of Customs [2009] HCA 7; 83 ALJR 494 at 501 [29]–[30] French CJ discussed the meaning of the word “contravention”. His Honour first referred to the Oxford English Dictionary meaning as “[t]he action of contravening or going counter to; violation, infringement or transgression”. At [30] French CJ said:

Without essaying an exhaustive definition, the core meaning of “contravention” involves disobedience of a command expressed in a rule of law which may be statutory or non-statutory. It involves doing that which is forbidden by law or failing to do that which is required by law to be done. Mere failure to satisfy a condition necessary for the exercise of a statutory power is not a contravention. Nor would such a failure readily be characterised as “impropriety” although that word does cover a wider range of conduct than the word “contravention”.

16 Whilst the word “contravention” is capable of a wide meaning, in the context of a civil remedy provision which includes the possible imposition of a civil penalty the word includes the notion of violating or infringing a rule or obligation or standard which is required. One would not assume or conclude that Parliament would provide for the imposition of a penalty for doing or not doing something that one was not obliged not to do or not obliged to do. One does not, in my view, contravene a non-obligatory term of an arrangement. Section 51 of the Fair Work Act itself links the imposition of an obligation on a person to a contravention of a term of an enterprise agreement by that person.

17 There can, therefore, be no contravention of cl 7 of the 2006 Award.

18 Clause 7, and in particular cl 7.2 of the 2012 and 2015 Agreements is, however, worded quite differently to cl 7 of the 2006 Award. The clause commences with words which are capable of being understood as words of undertaking and obligation: “The Company will make contributions…” It then proceeds to refer to another additional payment: “Additionally for [certain] employees…the Company will make contributions…” There was little argument but that this was an obligation undertaken. Why would not the similarly worded first sentence also be obligatory?

19 I read cl 7.2 as an undertaking of future conduct by the Company. The difficulty with such cases as Akmeemana v Murray [2009] NSWSC 979; 190 IR 66 and Cook v Chesterton International Pty Ltd [2015] NSWSC 283 is that they proceed on a false assumption. Both Davies J and Young AJA assumed, and expressly stated, that the employer had a duty imposed by law to pay superannuation contributions. That is not so. To the extent that the primary judge appears to have found that it was so, at [61], [64], [71], [73], [90] and [94] of his reasons, I would respectfully disagree. If contributions are not made the employer suffers a tax. This is not an idle distinction, especially in the light of the fact that the superannuation legislation does not confer on an employee any right to require the Commissioner of Taxation to do anything for him or her in respect of superannuation: Kronen v Federal Commissioner of Taxation [2012] FCA 1463; 213 FCR 495 at 505 [50]. There is every reason for those representing employees to include in an enterprise agreement an obligation to pay superannuation at the minimum level that will avoid a charge or tax. That reason is the direct enforceability of the obligation. True it is that if an employer fails to pay the minimum contribution it is then faced with both the imposition of a tax and the possible enforcement of obligations in the enterprise agreement. That problem is easily avoided: comply with the obligations freely entered into in the enterprise agreement. This possible duality of consequences is no reason not to view the enterprise agreement as containing binding obligations which can be enforced on behalf of employees for their protection and proper payment, for instance by seeking relief under civil remedy provisions such as ss 539(2), 540, 545(1), (2)(a) and (b) of the Fair Work Act.

20 It can be accepted that different judges in different factual circumstances when examining contracts of employment and enterprise agreements, including whether or not the former incorporated the latter, have given different weight to factors such as the discernible intention of creation of legal relations, the mere acknowledgement of obligation elsewhere found, the place of aspirational commitment in some industrial instruments, and the like. To the extent that principle from other cases is of assistance in construing cl 7 of the 2012 and 2015 Agreements, I would respectfully adopt what White J said in National Tertiary Education Union v La Trobe University [2015] FCAFC 142; 254 IR 238 at 263–264 [108]:

Although it may be a statement of the obvious, it is appropriate to keep in mind that the document which the Court is asked to construe is an enterprise agreement made pursuant to the regime in Pt 2-4 of the Fair Work Act 2009 (Cth) (the FW Act). It is in the very nature of these agreements that they are intended to establish binding obligations. The manner of making such agreements is subject to detailed prescription and their operation is contingent upon approval by the Fair Work Commission, the obtaining of which is itself a matter of detailed prescription. In my opinion, it is natural to suppose that parties engaging in this detailed process intend that the result should be a binding and enforceable agreement. To my mind, that is an important matter of context when approaching the construction of cl 74.

21 There is nothing aspirational about an employer saying, in language that connotes obligation, that it will make superannuation contributions. Language capable of conveying obligation on the subject of how much employees will receive for their labour is unlikely to be intended as aspirational or non-binding. The superannuation legislation gives no enforceable rights to employees. When they bargain for a form of words that connotes an obligation to pay it at a certain level, I see no reason whatsoever not to accept the words as binding and enforceable.

22 Ground 2 of the Notice of Appeal should allowed as to the 2006 Award and be rejected as to the 2012 and 2015 Agreements.

What were the appellants bound to pay by cl 7.2? Have they contravened the 2012 and 2015 Agreement?

23 The issue then arises as to how one calculates for Messrs Storey and Le Clerc the relevant superannuation contributions. That involves the proper construction of the superannuation legislation and also understanding how the employees were paid. This issue was argued by reference to the structure of the Notice of Appeal. That structure and the approach of the primary judge is better understood if one starts with the central question in the controversy: the proper construction of relevant provisions of the superannuation legislation.

24 Once that task has been essayed, the intricacies of the individual agreements and the arguments on appeal present somewhat less of a challenge.

The proper construction of the superannuation legislation

25 The Superannuation Guarantee Charge Act 1992 (Cth) (the SG Charge Act) and the SG Administration Act are pieces of legislation at the heart of the national economy, of the national arrangements for the financial welfare and financial security of Australian employees and retirees, and Australians generally. As referred to above, an employer in the position of the appellants is under no statutory obligation to make superannuation contributions for the benefit of any employee. The extent to which it does so will affect whether it pays a charge or tax, and if so in what amount. The position was explained by the plurality in Roy Morgan Research Pty Ltd v Commissioner of Taxation [2011] HCA 35; 244 CLR 97 at 101[3]:

Broadly speaking, the effect of the legislation under challenge is that if, as specified in the Administration Act, an employer fails to provide to all employees a prescribed minimum level of superannuation then any shortfall represented by failure to meet that minimum level in full, becomes the Charge. This impost is levied on the employer by the Charge Act. The amount of the Charge is a debt due to the Commonwealth and payable to the respondent, the Commissioner of Taxation: Taxation Administration Act 1953 (Cth), Sch 1, s 255-5. The Charge includes a component for interest and an administration cost. The result is to supply an incentive to employers to make contributions to superannuation for their employees without incurring a liability to the Commissioner for the Charge.

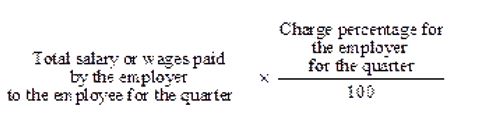

26 Under ss 5 and 6 of the SG Charge Act, a charge is imposed on any superannuation guarantee shortfall of an employer for a quarter (s 5) and the amount of that charge is an amount equal to the amount of the shortfall (s 6). To understand how this works one goes to the SG Administration Act which, by s 3 of the SG Charge Act, is incorporated into, and is to be read as one with, the SG Charge Act.

27 Sections 16 and 17 of the SG Administration Act provide for the charge imposed on the shortfall for the quarter to be payable by the employer and is the total of the individual shortfalls, plus interest, plus an administration component. Section 19 provides for the calculation of an employee’s individual superannuation guarantee shortfall. Relevantly s 19(1) and (2) are in the following terms:

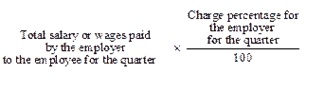

(1) An employer’s individual superannuation guarantee shortfall for an employee for a quarter is the amount worked out using the formula:

where:

charge percentage, for an employer for a quarter, means:

(a) the number specified in subsection (2) for the quarter (unless paragraph (b) applies); or

(b) if the number specified in subsection (2) for the quarter is reduced in respect of the employee by either or both section 22 and 23 – the number as reduced.

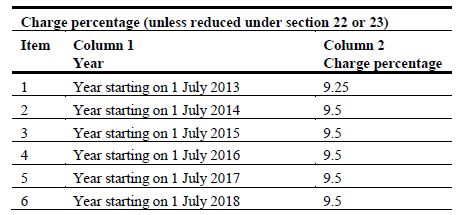

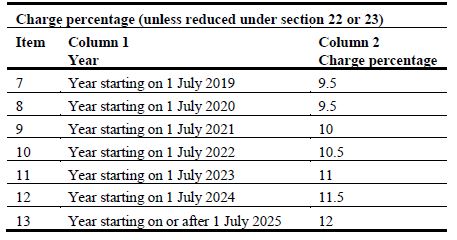

(2) The charge percentage for a quarter in a year described in an item of the table is the number specified in column 2 of the item.

28 It is to be noted that the percentage of the charge is applied to “the total salary or wages paid by the employer to the employee for the quarter”.

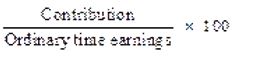

29 The charge percentage can be reduced in respect of the employee by various means, here, relevantly, by s 23. Under s 23, if an employer makes a contribution to a Retirement Savings Account (an RSA) there is a reduction in the charge percentage. Section 23(1) and (2) of the SG Administration Act are in the following terms:

23 Reduction of charge percentage if contribution made to RSA or to fund other than defined benefit superannuation scheme

(1) This section applies only in relation to RSAs and to superannuation funds other than defined benefit superannuation schemes.

Reduction of charge percentage where contributions are made by employer

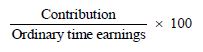

(2) If, in a quarter, an employer contributes for the benefit of an employee to a complying superannuation fund or an RSA, then the charge percentage for the employer (as specified in subsection 19(2)) for the employee for the quarter is reduced by the number worked out using the formula:

where:

contribution is the number of dollars in the amount of the contribution.

ordinary time earnings is the number of dollars in the ordinary time earnings of the employee for the quarter in respect of the employer.

Example: If the contribution is $60 and the ordinary time earnings are $1,000 then the charge percentage is reduced by 6.

30 The phrase “ordinary time earnings” is defined in s 6 of the SG Administration Act, as follows:

6 Interpretation—general

(1) In this Act, unless the contrary intention appears:

ordinary time earnings, in relation to an employee, means:

(a) the total of:

(i) earnings in respect of ordinary hours of work other than earnings consisting of a lump sum payment of any of the following kinds made to the employee on the termination of his or her employment:

(A) a payment in lieu of unused sick leave;

(B) an unused annual leave payment, or unused long service leave payment, within the meaning of the Income Tax Assessment Act 1997; and

(ii) earnings consisting of over-award payments, shift-loading or commission; or

(b) if the total ascertained in accordance with paragraph (a) would be greater than the maximum contribution base for the quarter—the maximum contribution base.

31 Thus, if the contribution divided by “ordinary time earnings” multiplied by 100 is the equivalent of, or more than, the charge percentage in column 2 in s 19(2), the charge percentage for s 19 and ss 16 and 17 will be zero.

32 It is thus critical to understand the meaning of the phrases “ordinary time earnings” and the otherwise undefined phrase “ordinary hours of work” used in the definition of the former phrase.

33 One can begin this enquiry, as the primary judge did at [55]–[58] and [106]–[113], by considering authorities dealing with the phrase “ordinary hours of work” in various contexts. That enquiry may bring one to the conclusion, as it did the primary judge, that there was a choice between a meaning referrable to standard hours to be paid at ordinary rates, and a meaning referrable to the regular, customary, normal or usual hours worked by each individual employee. That was, in significant part, the field of debate on appeal. Whilst those considerations and the cases epitomising them need to be examined, it is best to recall that the task involves a consideration of the text, context, purpose and history of the legislation: Project Blue Sky Inc v Australian Broadcasting Authority [1998] HCA 28; 194 CLR 355 at 381–382 [69]–[71]; and Thiess v Collector of Customs [2014] HCA 12; 250 CLR 664 at 671–672 [22]–[23].

34 First, the text: The definition turns on the expression “earnings in respect of ordinary hours of work”, not merely the word “ordinary” or the phrase “ordinary hours of work”. It is earnings that are the focus (in the phrase being defined: “ordinary time earnings” and in the terms of the definition (“earnings in respect of ordinary hours of work”). The exclusion of the matters in (i)(A) and (B) and the inclusion of the matters in (ii) tend to indicate that “ordinary hours of work” is something referrable to an objective standard, and not an individual factual enquiry about hours ordinarily or usually worked. If “ordinary hours” meant hours customarily or typically worked the matters in (ii) would likely be covered without need for separate mention. Whereas they would not be if the phrase referred to an objective standard that concerned standard hours and ordinary rates of pay.

35 The language of the definition is to be contrasted with the language of ss 11(1)(ba) and 12(3) as to salary and wages. This language is used in s 19 to calculate the shortfall: “Total salary or wages paid by the employer to the employee for the quarter.” Total salary or wages is an all-encompassing expression concerned with hours actually worked that founds the tax – the superannuation guarantee charge, which is intended to be the incentive that encourages the making of contributions. Thus “total salary or wages” can be seen as a likely higher sum than “earnings in respect of ordinary hours of work”.

36 None of the language leads one, necessarily, as a matter of meaning or logic to hours usually or ordinarily worked.

37 Secondly, the context: This is not a provision directed to compensating an individual for the time of his or her labour, or for loss sustained in not being able to work his or her normal hours; rather it is part of a regime implemented by legislation using the taxation power to encourage and facilitate national savings.

38 The context is the payment of salaries and wages in the workplace. In that context, the word “ordinary” and the phrase “ordinary hours” have assumed different meanings depending on context and circumstance. There are circumstances and contexts where the word and phrase can be seen to refer to regular, normal, customary or usual hours; and there are circumstances or contexts where the word and phrase can be seen to refer to the hours of work referred to in applicable industrial instruments as standard hours to be paid at ordinary rates, as opposed to additional hours (even if required, usual, regular, normal or customary) and paid at a special or higher rate. As such, the word and phrase can be seen to reflect the long-recognised distinction between ordinary hours of work and overtime: cf Thompson v Roche Bros Pty Ltd [2004] WASCA 110 at [31].

39 The notion of standard or ordinary working hours has long had a place in the industrial relations landscape of Australia. The standard working week was once 48 hours (Australian Builders’ Labourers’ Federation v Archer (1913) 7 CAR 210); reduced to 44 hours during the 1920s (Amalgamated Engineering Union v J Alderdice & Co Pty Ltd (1927) 24 CAR 755 (the 44 Hour Week Case)); to 40 hours after the War (Standard Hours Inquiry (1947) 59 CAR 581; and to 38 hours in 1983 (National Wage Case (1983) 4 IR 429). The standard of 38 hours was not departed from by the Australian Industrial Relations Commission in 2002 (Re Working Hours Case July 2002 (2002) 114 IR 390. The standard of 38 hours has not been departed from in the award modernisation process. The notion of “ordinary hours of work” remains a working integer of the modern award system: s 147 of the Fair Work Act.

40 By s 62 of the Fair Work Act, 38 hours remains the maximum number of hours that an employer can request or require of a full time employee, unless the “additional hours” are reasonable. Ordinary hours or some means of determining ordinary hours is a necessary part of an award or enterprise agreement for the better off overall test. Section 20 of the Fair Work Act deals with the meaning of “ordinary hours of work” for “award/agreement free employees”:

20 Meaning of ordinary hours of work for award/agreement free employees

Agreed ordinary hours of work

(1) The ordinary hours of work of an award/agreement free employee are the hours agreed by the employee and his or her national system employer as the employee’s ordinary hours of work.

If there is no agreement

(2) If there is no agreement about ordinary hours of work for an award/agreement free employee, the ordinary hours of work of the employee in a week are:

(a) for a full-time employee—38 hours; or

(b) for an employee who is not a full-time employee—the lesser of:

(i) 38 hours; and

(ii) the employee’s usual weekly hours of work.

If the agreed hours are less than usual weekly hours

(3) If, for an award/agreement free employee who is not a full-time employee, there is an agreement under subsection (1) between the employee and his or her national system employer, but the agreed ordinary hours of work are less than the employee’s usual weekly hours of work, the ordinary hours of work of the employee in a week are the lesser of:

(a) 38 hours; and

(b) the employee’s usual weekly hours of work.

41 By [234]–[235] of the Explanatory Memorandum to the Fair Work Bill 2008 the importance of ordinary hours of work to the National Employment Standards was explained:

234 There are a number of concepts that are used regularly in Part 2-2. These are explained below.

235 Various employee entitlements under the NES are based on the employee’s ordinary hours of work.

• The ordinary hours of work for an employee to whom a modern award applies will be the ordinary hours set out in the modern award (all awards are required to provide ordinary hours, or a means of determining ordinary hours) (see clause 147).

• The ordinary hours of work for an employee to whom an enterprise agreement applies will be the hours identified in the enterprise agreement. (An agreement should identify ordinary hours, or a means of determining ordinary hours, in order for the agreement to pass the better off overall test.)

• The ordinary hours of work for an award/agreement free employee (as defined in clause 12) are calculated in the manner set out in clause 20.

42 Whilst not all of the above can be seen as part of the immediate context of the passing of the superannuation legislation, it illuminates the historical and contemporaneous importance of the phrase “ordinary hours of work”. This assists in understanding the use of the phrase in the definition in 1992, in its continuing utilisation in the legislation, and also in the interpretation of the various relevant industrial agreements here.

43 Thirdly, the purpose: The statutory purpose of the superannuation legislation was to secure for workers a minimum level of superannuation by the incentive of the charge, through an efficient mechanism based on self-assessment by employers and administration by employers and the Australian Tax Office. That simplicity and efficiency of administration is threatened if the necessary calculation for each employee, for each quarter is based on an individual factual enquiry and is not calculated by reference to the standard hours at ordinary rates in relevant industrial instruments. Usual or ordinary hours may well vary from employee to employee, and, over time, for the same employee. What is customary or usual would be a factual assessment over the relevant period (each quarter), referable to individuals, and open to factual and individual debate. The statutory purpose of simplicity and efficiency for a minimum level of superannuation would be undermined by the need to find, factually, usual or normal hours for each employee in each quarter; the purpose would, on the other hand, be supported by an interpretation that looked to the relevant industrial instrument for standard hours at ordinary rates of pay. It is, with respect, overly simplistic to say that the legislation was intended to benefit employees therefore should be construed beneficially in their favour: cf Quest Personnel Temping Pty Ltd v Commissioner of Taxation [2002] FCA 85; 116 FCR 338 at 343 [21]. The legislation has a broader social and economic purpose, and whilst for the benefit of Australian employees generally, should be construed with a view to practical efficiency and overall fairness.

44 Fourthly, the enactment history assists in understanding “ordinary time earnings” as earnings referable to standard hours at ordinary rates of pay. It is not just the number of hours, but also their character as paid at an ordinary rate.

45 The enactment history can be seen as part of the context of the legislation in its widest sense: see CIC Insurance Ltd v Bankstown Football Club Ltd [1997] HCA 2; 187 CLR 384 at 408 [88] and Federal Commissioner of Taxation v Jayasinghe [2016] FCAFC 79; 247 FCR 40 at 43 [6]–[7].

46 The regime of the legislation was introduced against the background of industrial awards and was to be integrated into that system. The Information Paper published by the then Treasurer, the Honourable John Kerin (and referred to in the Second Reading Speech), stated at [3.25]:

“The SGLA will operate independently of, but in conjunction with, the award system.”

47 Until changes made to s 23(2), that took effect in July 2008, to which I refer below, the charge percentage was able to be reduced in a number of ways, including through contribution by employers in accordance with industrial awards and set by reference to an employee’s “notional earnings base”. The way the system operated before the amendments made by Act No 82 of 2005 (that took effect in July 2008), was described in the Explanatory Memorandum to the Superannuation Laws Amendment (2004 Measures No. 2) Bill 2004 (the 2004 EM). The desired simplification was described on pp 5–6 of the 2004 EM as follows:

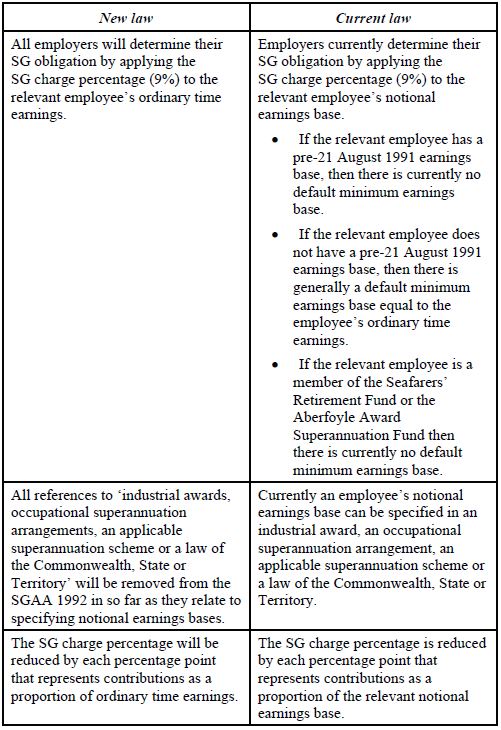

Schedule 1 to this bill will also amend the Superannuation Guarantee (Administration) Act 1992 to simplify the earnings base of an employee for superannuation guarantee (SG) purposes. Specifically, the amendments will:

• remove provisions which currently allow earnings bases that existed prior to 21 August 1991 to be used to calculate an employer’s SG obligation in respect of an employee;

• remove provisions which currently specify an earnings base for employers to calculate their SG obligation in relation to employee members of the Seafarers’ Retirement Fund;

• remove provisions which currently specify an earnings base for employers to calculate their SG obligation in relation to employee members of the Aberfoyle Award Superannuation Fund;

• remove provisions which allow earnings bases specified in industrial awards, superannuation schemes, occupational superannuation arrangements or a law of the Commonwealth, State or Territory to be used for SG purposes; and

• require all employers to calculate their SG liability against an employee’s ordinary time earnings.

48 The context of the amendments was described in the 2004 EM at pp 21–22 as follows:

4.2 The Treasurer announced in Press Release No. 011 of 25 February 2004 changes to provide a more flexible and adaptable retirement income system. The announcement included the Government’s decision to simplify the earnings base provisions of the SGAA 1992 by removing earnings bases that existed before 21 August 1991.

4.3 The SG arrangements currently require employers to provide a prescribed minimum level of superannuation contributions for their eligible employees. The required minimum rate of superannuation contributions is 9% of an employee’s notional earnings base.

4.4 The SGAA 1992 was developed in the context of the occupational superannuation arrangements that existed in the early 1990s. To minimise the impact on business at that time, the SGAA 1992 recognised earnings base provisions that existed prior to 21 August 1991 and allowed these to be used as the basis for determining an employer’s SG obligation.

4.5 Employers who contribute for the benefit of employees without a pre-21 August 1991 earnings base are subject to different rules. Employees without a pre-21 August 1991 earnings base will generally have an minimum earnings base equal to their ordinary time earnings.

4.6 As pre-21 August 1991 earnings bases are generally less than ordinary time earnings, some employers are currently able to pay lower superannuation contributions for their employees than other employers in the same industry.

49 The new law was explained in the 2004 EM at pp 22, 23 and 26 as follows:

4.7 The amendments will remove the current earnings base provisions from the SGAA 1992. The effect of these changes is that the amount against which an employer calculates the contribution necessary to meet their SG obligations in respect of an employee is standardised to ordinary time earnings for all employees. Employers could continue to use notional earnings bases specified in legislation or industrial agreements where these are above an employee’s ordinary time earnings; however, any liability to pay the SG charge would only be assessed against ordinary time earnings.

4.8 Standardising the earnings base used to determine SG obligations to ordinary time earnings extends to the removal of references to industrial agreements, laws of the Commonwealth, State or Territory, an applicable superannuation scheme or retirement savings account from the provisions relating to earnings bases. These instruments currently prescribe notional earnings bases for SG purposes.

…

…

Policy objective

4.21 The policy objective is to remove the complexity and inequity present in the current SG notional earnings base arrangements under the SGAA 1992. The basic principle underpinning this objective is that persons on similar overall levels of remuneration should receive similar levels of compulsory employer superannuation contributions.

Implementation options

Retain the current arrangements

4.22 There would be no change to the existing arrangements. That is, some employers could continue to use pre-21 August 1991 earnings bases in respect of their employees. Under the current provisions of the SGAA 1992, employers could potentially reduce their compulsory superannuation contributions through the use of workplace agreements.

Adopting ordinary time earnings as a standardised earnings base

4.23 Remove all references to industrial awards and statutes from the SGAA 1992 and adopt ordinary time earnings as the standard notional earnings base. This option proposes that the minimum notional earnings base of an employee be their ordinary time earnings.

Adopting salary and wages as a standardised earnings base

4.24 Remove all references to industrial awards and statutes from the SGAA 1992 and adopt salary or wages as the standard notional earnings base. This option proposes that the minimum notional earnings base of an employee be the total of their salary and/or wages.

50 The choice of option 2 was recommended for the following reasons explained in the 2004 EM at p 31:

4.48 The preferred option is option 2, which removes all references to industrial awards and statutes from the SGAA 1992 and adopts ordinary time earnings as the standard notional earnings base.

4.49 This option would remove the complexity and inequity present in the current arrangements without imposing the same level of cost on employers and Government as an earnings base, based on total salary and wages’ would.

51 The notion of “ordinary time earnings” existed from the beginning of the operation of the legislation, but it operated in provisions such as s 14(3) of the original SG Administration Act as a floor of a minimum base. The phrase was originally defined in s 6(1) as follows:

“ordinary time earnings”, in relation to an employee, means:

(a) the total of:

(i) earnings in respect of ordinary hours of work; and

(ii) earnings consisting of over-award payments, shift-loading or commission; or

(b) if the total ascertained in accordance with paragraph (a) would be greater than the maximum contribution base for the contribution period–the maximum contribution base;

52 The phrase “ordinary hours of work” was not expressly linked to industrial awards in 1992. But an understanding of the phrase can be seen in the Explanatory Memorandum to the Taxation Laws Amendment Bill (No 4) 1993 at [13.8]–[13.12] (the Explanatory Memorandum to the Bill for the amendment to the definition of “ordinary time earnings” in s 6(1) that inserted the exclusion in (i) from the words, “other than earnings consisting of” to the end of the paragraph now represented by (i)(B)), in an explanation of the definition of “ordinary time earnings” in s 6(1):

13.8 Under the SGAA an employer's contributions are measured against the employee's notional earnings base. The expression notional earnings base is the earnings of the employee by reference to which the employer's superannuation contribution is calculated. Several earnings bases are available for an employer to use, such as the base set out in the superannuation fund deed, industrial award or an agreement with the employee.

13.9 If there is no acceptable earnings base relevant to a particular employee, then the employee's ordinary time earnings are used. The principal reason for adopting ordinary time earnings as a default base was to achieve consistency with the award superannuation system.

13.10 Subsection 6(1) of the SGAA provides that ordinary time earnings, in relation to an employee, means:

(a) the total of:

• earnings in respect of ordinary hours of work; and

• earnings consisting of over-award payments, shift loading or commission; or

(b) if the total ascertained in accordance with paragraph (a) would be greater than the maximum contribution base for the contribution period - the maximum contribution base. The maximum contribution base, which is increased annually by an indexation factor based on movements in Average Weekly Ordinary Time Earnings, is $20 160 per quarter for the 1993-94 income year.

13.11 Ordinary hours of work, as stated above, may be specified in a statute or under an industrial award. If an employee is not covered by an award but has agreed to work a certain number of hours, those hours are the employee's ordinary hours of work. However, if there is no specific agreement, the ordinary hours of work will be the hours actually worked and any hours of paid leave.

13.12 Lump sum payments on termination of employment in respect of accrued long service leave, accrued sick leave and accrued recreation leave are currently included in the definition of ordinary time earnings.

…

13.13

…

• lump sum payments in lieu of unused sick leave;

• lump sum payments in lieu of unused annual leave, within the meaning of subsection 26AC(l) of the Income Tax Assessment Act 1936 (ITAA); and

lump sum payments in lieu of unused long service leave, within the meaning of subsection 26AD(l) of the ITAA.

53 The above material reveals that the removal of “notional earnings base” leaving “ordinary time earnings” as the single measure was for the purposes of removing complexity and securing consistency.

54 The definition of “ordinary time earnings”, including the expression “earnings in respect of ordinary hours of work” was introduced in 1992, not long after the High Court decision in Catlow v Accident Compensation Commission [1989] HCA 43; 167 CLR 543 in which the majority of the Court considered that the phrase “ordinary time rate of pay” meant “ordinary time rate of pay for the worker’s standard or ordinary hours per week as fixed by award, agreement or contract”: 167 CLR at 561. The construction of those cognate words by the High Court in a cognate industrial field is of some assistance in concluding that the legislature was intending to adopt language with a similar effect: see Ex parte Campbell (1870) LR 5 Ch App 703 at 706:

Where once certain words in an Act of Parliament have received a judicial construction in one of the Superior Courts, and the Legislature has repeated them without any alteration in a subsequent statute, I conceive that the Legislature must be taken to have used them according to the meaning which a Court of competent jurisdiction has given them.

55 See the discussion in the cases referred to in Pearce DC and Geddes RS, Statutory Interpretation in Australia (8th ed, Butterworths, 2014) at [3.44] pp 138–139. See in particular Re Alcan Australia Ltd; Ex parte Federation of Industrial, Manufacturing and Engineering Employees [1994] HCA 34; 181 CLR 96 at 106. The strength of the presumption will depend on the circumstances. Here, it provides some support for a conclusion otherwise reached as to meaning.

56 The text, context, purpose and enactment history do not direct one to a meaning constituted solely by hours (factually) usually worked. They tend to a meaning that provides for an objective standard that aids in simplicity and lack of complexity. The use, from 1992, of the relevant phraseology in a context of industrial awards and instruments; the well-known conception contained within industrial awards and instruments of standards hours at ordinary rates of pay, and of overtime; the need for the phraseology to be practical, general and flexible to pick up all circumstances of employment; and the need for the task set for the employer to administer and the ATO to audit, quarter by quarter, individual by individual, to be as simple or non-complex as possible all direct one to a meaning that reflects those considerations. The meaning that best reflects these considerations and the text, context, purpose and history of the provision is earnings in respects of ordinary or standard hours of work at ordinary rates of pay as provided for in a relevant industrial instrument, or contract of employment, but if such does not exist (and there is no distinction between ordinary or standard hours and other hours by reference to rates of pay) earnings in respect of the hours that the employee has agreed to work or, if different, the hours usually or ordinarily worked.

57 This meaning adopts as central (to the extent that it is present) the distinction long familiar in the industrial and employment context, and widely understood, between earnings for ordinary time and earnings for an additional or greater number of hours beyond ordinary or standard hours. If in a particular context such distinction does not exist in the remuneration for the labour provided, the required comprehensiveness and flexibility of the meaning will fix upon the hours agreed to be worked, or the hours normally worked if different. This is not to give a variable meaning to the expression, it is to recognise that the context and particular circumstances will provide by way of factual application, the answer to the reach of the phrase which has a simple meaning by reference to real life.

58 The cases support this interpretation.

59 Catlow 167 CLR 543 was decided three years before the superannuation regime was introduced. The case concerned the construction of s 95(1) of the Accident Compensation Act 1985 (Vic), which relevantly provided:

In sections 93 and 94, 'the worker's pre-injury average weekly earnings' means –

(a) the average weekly earnings during the 12 months preceding the relevant injury if the worker has been employed by the same employer for that period;

…

calculated at the worker's ordinary time rate of pay for the worker's normal number of hours per week.

60 The question before the Court was framed in the leading judgment of McHugh J at 557:

whether, when a standard number of ordinary working hours has been fixed for a worker's employment, his "normal number of hours per week" for the purposes of the Act are those standard hours or the number of hours he usually worked.

61 The Full Court of the Victorian Supreme Court had overturned the decision of the Accident Compensation Tribunal which had found the phrase “normal number of hours per week” to be the number of hours he usually worked including overtime.

62 McHugh J at 560 made the point (equally relevant to understanding the 1992 superannuation legislation) that terms of employment of most workers are governed by industrial awards or agreement that provide for ordinary time rates of pay for standard hours. His Honour said at 560–561:

Against the industrial background of awards and agreements fixing a number of ordinary hours per week, it seems natural to read the expression "calculated at the worker's ordinary time rate of pay for the worker's normal number of hours per week" as a reference to the ordinary time rate of pay for the worker's standard or ordinary hours per week as fixed by award, agreement or contract. While it is true that on any view the "pre-injury average weekly earnings" calculated under s. 95 is a notional and not an actual figure, it would indeed be surprising if the legislature intended that those earnings are to be calculated by multiplying the ordinary time rate by overtime as well as ordinary hours worked. If "normal number of hours" included overtime hours, some other formula to include the overtime rate would surely have been used.

63 McHugh J then examined three decisions: two of the Industrial Commission of New South Wales, and one of the High Court, heavily relied on by the primary judge and the respondent.

64 The two Industrial Commission cases, John A Gilbert Pty Ltd v Irving [1962] AR 307 and Goodyear Tyre & Rubber Co (Aust) Ltd v Robinson [1961] AR 127 dealt with the phrase “normal weekly number of hours” in the Annual Holidays Act 1944 (NSW) and the Long Service Leave Act 1955 (NSW), respectively. The Commission said in John A Gilbert [1962] AR at 318:

The word 'normal' in its ordinary sense may mean regular or usual, or it may mean conforming to standard. We are of the opinion that, in the definition, a worker's normal weekly number of hours is that number of hours which is fixed by the terms of the worker's employment as the standard of ordinary hours, as distinct from overtime hours, which are to be worked in a week. If 'normal' meant regular or usual, a determination of what was regular or usual would depend on the facts of each case in relation to a period of employment long enough to permit an ascertainment of what was regular or usual, but the language of s. 2(2) suggests that terms of employment may fix in advance the weekly hours which are to be normal.

65 The Commission said in Goodyear [1961] AR at 137–138:

Overtime hours are not hours within a worker's normal weekly number of hours of work; they are hours worked over and above his normal weekly number of hours of work, and a payment which is made for overtime hours cannot, in any sense, be said to be remuneration for one's normal weekly number of hours of work.

66 The previous decision of the High Court in Kezich v Leighton Contractors Pty Ltd [1974] HCA 50; 131 CLR 362 was examined and distinguished by McHugh J. The context was a workers compensation statute. The relevant provision was:

For the purposes of this Act, 'weekly earnings' means the amount of the ordinary wage or salary (including any over award payment) the worker would have received for the ordinary hours he would have worked, if he were not incapacitated for work as a result of the injury.

67 The Court (Gibbs J delivering the leading judgment) held that “the ordinary hours he would have worked” meant the hours which he usually worked. Gibbs J said at 131 CLR at 365:

The word 'ordinary' means 'regular, normal, customary, usual'. A man's 'ordinary hours' of work are the hours during which it is usual for him to work. There is nothing in the expression 'ordinary hours' that connotes payment at any particular rate, and to understand the words as meaning 'hours during which work is done for which overtime is not paid' would be to place upon them a meaning which they simply do not bear. The expression 'the ordinary hours he would have worked' in my opinion means the same as 'the hours he would ordinarily have worked' ...

68 McHugh J recognised the force of this approach (and of the similar approach of Mason J in the same case at 131 CLR at 376) but saw the contexts and provisions as different, saying at 167 CLR at 566:

Indeed, the different context and history of the phrase "normal number of hours per week" in s. 95(1) dictate that it be interpreted as meaning the ordinary or standard number of hours worked and not the usual number of hours worked.

Accordingly, in my opinion, in s. 95 "normal number of hours per week" means the ordinary or standard hours fixed by the terms of the employment. The appellant's "pre-injury average weekly earnings" in this case had to be calculated by determining what were his total weekly earnings calculated by reference to the ordinary time rate of pay for the ordinary hours for the relevant period and then obtaining a weekly average of that sum. As the appellant had more than one ordinary time rate of pay during the twelve months period, his earnings for each of the three periods had to be grossed in accordance with that formula and then averaged over the relevant period.

69 Catlow recognised the two different ways of understanding words such as “usual”, “ordinary” or “normal” in the industrial context. In any particular statute, the terms, context, purpose and enactment history will determine the meaning to be ascribed as that intended by Parliament.

70 In Scott v Sun Alliance Australia Ltd [1993] HCA 46; 178 CLR 1 the High Court was concerned with s 69(1) of the Workers Compensation Act 1988 (Tas) that included the phrase “ordinary time rate of pay”. The Court said the following at 5–6:

The expression "ordinary time rate of pay" is well known in the industrial relations field in Australia and New Zealand. It and similar terms have long been used in legislation (See, e.g., Annual Holidays Act (N.S.W.) 1944, s. 2(1); Workers’ Compensation Act 1956 (N.Z), s. 15(1) (now repealed); Accident Compensation Act 1985 (Vict.), s. 95(1) (now repealed)). Unless the context otherwise requires, "ordinary time rate of pay'' means the rate of pay for the standard or ordinary hours of work in contrast to the overtime or penalty rate of pay for hours of work other than the standard or ordinary hours (Catlow v. Accident Compensation Commission (1989), 167 C.LR. 543, at pp. 555-556, 560). When expressed by reference to a week, it refers to the product of multiplying that hourly rate by the standard thirty-five, thirty-eight or forty hour week, as the case may be, fixed by legislation, industrial award or agreement.

The terms of s. 69(1)(a) indicate that the legislature assumed that there is always an ordinary time rate of pay for the worker for the work on which he or she is engaged. No doubt in most cases this is true because when the 1988 Act was enacted the rates of pay of most workers were covered by industrial awards or agreements.

[Reference was made to the judgment of McHugh J in Catlow]

However, it is not always the case that a worker will have an ordinary time rate of pay. There may be no industrial award or agreement regulating his or her employment, and his or her contract of employment may not distinguish between ordinary and other time rates of pay or may provide for remuneration by a formula which has no temporal element – for example, piece work or commission (See, e.g., Goodyear Tyre & Rubber Co. (Australia) Ltd v. Robinson, [1961] AR (N.S.W.) 127, at p. 137.). If the worker has no "ordinary time rate of pay'', the compensation payable to him or her pursuant to s. 69(1)(a) must be calculated by reference to his or her average weekly earnings.

71 Little assistance is given by Australian Communication Exchange Ltd v Deputy Commissioner of Taxation [2003] HCA 55; 201 ALR 271. The case concerned the operation of s 23 of the SG Administration Act before the amendments removing the concept of “notional earnings base” in 2005. It turned, however, upon the specific wording of an award and the relationship between provisions dealing with full time and casual employees and a somewhat extended definition of “ordinary time earnings” and “ordinary hours of work”.

72 Quest Personnel Temping Pty Ltd v Commissioner of Taxation [2002] FCA 85; 116 FCR 338 was concerned with the meaning of “ordinary hours of work” in ss 6 and 23 of the SG Administration Act. The Court (Gray J) dismissed a challenge to a decision of the Administrative Appeals Tribunal that had agreed with the Commissioner’s assessment of the company’s superannuation guarantee shortfall based on “ordinary hours of work” being the normal, regular, customary or usual hours worked by that employee. That conclusion is not contrary to the meaning which I have posited above. The case concerned data entry operators supplied to the Victorian Police. The standard offer of employment referred to a minimum of five standard shifts each fortnight as notified. The pay for all hours worked was at a standard hourly rate with no loading. Some employees worked more than the minimum. There was a variety of requirements on different employees.

73 Gray J rejected the argument that the minimum hours were the ordinary hours of work and that the additional hours were overtime. That rejection (at 342) was in part based on the lack of any higher rates of pay for additional work. His Honour said at 342–343 [19]–[20]:

19 …The offers of employment specified the minimum hours for which an employee could be called upon to work. The clear import of the word "minimum" was that an employee could be expected to be asked to work more than five standard shifts in a fortnight. An industrial award or agreement usually expresses the maximum hours that an employee may be required to work. It is true that provision is often made for work beyond such standard hours, but it is usual for the award or agreement to provide that such additional work is to attract a higher level of remuneration. This is what marks it out as work performed outside ordinary hours.

20 The phrase "ordinary hours of work" in s 6 of the Act must be construed in the context of the Act and in a way which best promotes the underlying object or purpose of the Act. It is plain from the definition of "ordinary time earnings'' in s 6 that, at least in some cases, ordinary hours of work are to be distinguished from actual hours worked. The Act does not require that the relevant percentage of an employee's total earnings for all hours worked must be paid to a superannuation fund in order to avoid the levy. On the other hand, there will be some cases in which the ordinary hours worked by an employee will be the actual hours worked, because no ground will exist for distinction between the two concepts. An example would be an employee whose terms and conditions of employment are covered by an award and who works the maximum standard hours but no overtime.

(Emphasis added.)

74 I respectfully agree. In Quest, there was no distinction between ordinary hours and ordinary rates of pay and additional hours at a higher rate. All hours were at the same rate. There were minimum hours, but possible or likely additional hours, all to be paid at one rate. In such a case there is no ground to distinguish between different hours, and the only way a notion of “ordinary hours” could be understood was by what usually or ordinarily happened.

75 After referring to Kezich and Catlow, Gray J said at 344 [26]:

The distinction between these two cases appears to rest upon the proposition that the fixing by collective means of standard hours of work, coupled with a provision for remuneration at a higher rate of hours worked beyond those standard hours, will usually lead to the conclusion that the standard hours fixed are to be considered as "normal hours" or, perhaps, "ordinary hours". As I have said, that is not the present case. The offers of employment accepted by the employees in the present case did not purport to fix standard hours, with remuneration at a higher rate for hours in excess of them. They fixed only minimum hours, with hours worked beyond the minimum paid at the same rate as those worked within it.

(Emphasis added.)

76 It can be accepted that if the relevant distinction is not made, in the award or industrial instrument or contract of employment, between, on the one hand, standard or ordinary hours and ordinary rates of pay, and on the other, additional hours at higher rates of pay, then the ordinary hours will be the hours agreed to be worked, or the usual or normal hours worked, if they be different.

Conclusion on the meaning of “ordinary time earnings” and “earnings in respect of ordinary hours of work”

77 In my view the text, context, purpose and enactment history point clearly to the meaning that I set out at [56]–[57] above. The decisions of Catlow, Scott, and Quest support that meaning.

78 It is therefore necessary to turn to the various industrial instruments and agreements here to identify the “ordinary time earnings”.

The Relevant Industrial Agreements

79 The primary judge set out the relevant terms of the Departmental Agreements that affected Mr Storey and Mr Le Clerc (in addition to the 2006 Award and the 2012 and 2015 Agreements):

(a) the Bulk Operations Enterprise Agreement 2005 (Mr Storey) at [13]–[15];

(b) the Bulk Operations Departmental Agreement 2013 (Mr Storey) at [41]–[44];

(c) the Slabmaking – 12 hour Shift Agreement 2004 (Mr Le Clerc) at [16]–[22]; and

(d) the Slab Yard – 12 hour Shift Agreement 2010 (Mr Le Clerc) at [23]–[29].

80 The primary judge also referred to relevant provisions of the 2006 Award (referrable to both Mr Storey and Mr Le Clerc) ([30]–[36]), and of the 2012 Agreement ([37]–[40]).

The Bulk Operations Enterprise Agreement 2005

81 From the provisions of this Agreement the following can be stated in respect of Mr Storey. He was remunerated at an annualised salary. That salary was made up of a “base rate” and “a component which absorbed all additional payments such as penalty rates, allowances, shipping shift premiums, public holiday loadings and payouts and payments for additional hours worked outside the normal rostered hours”: cl 6.1 of the Bulk Operations Enterprise Agreement 2005. The salary was expressly calculated in cl 6.2 as “Base Salary” being “Ordinary Stevedoring Hourly Rate *38 hrs * 52 weeks” and “Overtime” as “5.5 hrs overtime per week x 2.1761 x Ordinary Stevedoring Hourly Rate”. This clearly distinguishes between ordinary hours at an ordinary rate and additional (overtime) hours at a higher rate. Those additional hours were to be required: cl 6.3 of the same agreement, which stated:

Employee’s will be required to work additional hours under the annualised salary system established at clause 6.2. Work undertaken on Additional hours will not be the subject of restrictions. All work required by the company on the Bulk Berth either directly or indirectly as part of operations will be required to be undertaken while on additional work hours.

82 Thus, although the normal or usual hours were almost certain to be greater than 38 hours, the additional hours over 38, which were called “overtime” were paid for in the annualised salary at a higher rather than the 38 hours per week that were paid at an “ordinary” hourly rate. Given the meaning of the phrase “ordinary time earnings” it is therefore wrong to conclude, as the primary judge did, that the earnings in respect of ordinary hours of work is other than the earnings in respect of the 38 hours per week in the calculation of the annualised salary.

The Bulk Operations Departmental Agreement 2013

83 The annualised salary for Mr Storey was stated to be calculated under cl 4 as follows:

Base salary = base stevedoring hourly rate *38 hours * 52 weeks

Overtime rate = 5.5hrs overtime per week * 2.1761 * base stevedoring hourly rate

84 Again the clear distinction is made between ordinary rates of pay for what can be taken to be standard hours (38 per week) and a higher rate for additional hours described as “overtime”.

The Slabmaking – 12 hour Shift Agreement 2004

85 Mr Le Clerc worked under a “12 hour Aggregated Salary System”. The primary judge set out the important provisions of the agreement at [17]–[22] of his reasons. Hours of work were 12 hour seven day continuous shift rosters (cl 5). Ordinary (here used in a sense of normal) hours included weekend shifts (cl 2). Standard hours of work were an average of 38 hours per week over the full cycle of the work roster (cl 5). The aggregated salary was paid in 26 equal fortnightly payments comprising “three components” (cl 10). The three components were a “base salary” addressed at cl 10.1; “additional payments” including public holidays addressed at cl 10.2; and “shift work payment and penalties” addressed at cl 10.3.

86 Clause 10.1 “base salary” was as follows:

10.1. BASE SALARY

Payment for the award wage, over award (bonus) payment, tool allowance for tradespersons and electrical licence payments for electrical tradespersons.

Weekly base salary is calculated by multiplying the employee’s hourly rate (including bonus rate, where applicable) by thirty-eight hours. Base salary for each employee is subsequently calculated by multiplying the weekly base salary by fifty-two weeks.

Calculation is therefore: Base salary = Hourly rate x 38 hours x 52 weeks.

87 The additional payments in cl 10.2 included disability allowances and payments for all public holidays (worked and rostered). The provision for public holidays was somewhat intricate in how it came to additional payment for 146 hours per annum for public holidays:

10.2.1. Public Holidays

Payment is based on the average number of public holiday loading hours for each employee across four crews. With reference to the roster pattern above (Figure 1), each employee will work on average 5.425 of the eleven public holidays per annum and be rostered off on the remaining 5.575 days. Of the 5.425 days worked 4.75 incur public holiday loading while 0.675 days per year receive no loading due to their occurrence on the day of the 1st night shift. Six hours is deducted to avoid double payment of weekend penalties and public holiday loading on Easter Saturday. Public holiday loading is therefore based on an extra twelve hours pay for every public holiday falling on a rostered off shift and an extra eighteen hours for every public holiday worked.

i.e. [(5.575 x 12) + (0.675 x 0) + (4.75 x 18)] – Easter Saturday Deduction | = 152.4 – 6 |

Rounding ….. | = 146 hour per annum |

Calculation is therefore: Public holiday payment = Hourly rate x 146 hours.

88 The allowance made for shift work in cl 10.3:

10.3 SHIFT WORK PAYMENTS AND PENALTIES

Payments for all disabilities and disturbances associated with shift work and the working of regularly rostered shifts on weekends.

10.3.1 Weekend Penalties

With reference to the roster pattern above (Figure 1), employees will work on average four-and-a-half of every ten weekends. Penalties are therefore based on an extra six hours pay on Saturday and an extra twelve hours pay on Sunday.

i.e. [4.514 x 6 (Sat)] + [4.514 x 12 (Sun)] = 81.25 hours per ten weeks.

= 8.125 hours per week.

Calculation is therefore: Weekend payment = Hourly rate x 8.125 hours x 52 weeks.

10.3.2 Shift Allowance

The shift allowance used is that amount paid to an employee on the current 8-hour continuous N/A/D roster system. Currently the rate per hour is $1.6253.

Calculation is therefore: Shift allowance payment = $1.6253 x 38 hours x 52 weeks.

89 Clause 10.4 simply stated the aggregate salary in the three components:

10.4. TOTAL (AGGREGATE SALARY)

The total aggregate salary is the sum of the above three components:

i.e. Aggregate Salary | = Base Salary + Public Holiday Payment + Weekend Payment + Shift Allowance Payment. |

90 Overtime was provided for by cl 11 if on any normal workday an employee worked for more than 12 hours and if a shift or part of a shift was done on a day other than a rostered workday. Clause 11 set out the overtime rates.

91 The proper construction of this agreement leaves no room for doubt that there is a clear distinction in the calculation of remuneration between standard or ordinary hours at ordinary rates of pay (38 hours) and a higher rate of pay for additional hours.

The Slab Yard – 12 hour shift Agreement 2010

92 Relevantly the agreement was in the same terms as the Slabmaking - 12 hour Shift Agreement 2004.

The primary judge’s approach and the grounds of appeal

The primary judge’s approach

93 At [96]–[97] of his reasons the primary judge set out the central questions for decision from the detail of the underlying agreements:

96 It was common ground that BlueScope Steel (AIS) Pty Ltd did not make superannuation contributions to the superannuation account of Mr Storey (or Mr Fernandes) in respect of either:

• the “additional hours component”; or

• the “public holidays component”

of the annualised salary paid to them.

97 In very summary form, the two fundamental questions to be resolved in the present proceeding are:

• whether the “additional hours component” of the annualised salaries were “ordinary time earnings”; and (Storey)

• whether the “public holidays component” paid to the employees as a component of either an annualised salary or an aggregate salary were “ordinary time earnings”. (Le Clerc)

94 The primary judge’s essential conclusions were expressed at [103]–[105] of his reasons:

103 The case for the Respondents centred upon a contention that the phrase “additional hours” as employed in the Bulk Berth Operations Departmental Agreement referred to “overtime hours that have been built into the annualised salary” and that “[p]roperly understood, additional hours are … prepaid overtime hours paid at a penalty premium that the employee may be expected to work”. On the Respondent’s case, the fact that employees work beyond “standard working hours” and the fact that “such hours are mandatory, rather than voluntary, does not affect their characterisation as overtime”. The Respondents further contend that the “case law indicates that overtime does not cease to be characterised as ‘overtime’ and thereby become ordinary time earnings because the overtime is mandatory”.

104 The case for the Applicant was (inter alia) that there was no warrant for the approach of the Respondents in seeking the “dissection of fortnightly payments of annualised salary into various ‘components’” where such an approach was “directly contrary to the face of the agreement that the annualised salary would itself ‘absorb’ (or ‘incorporate’) all additional payments”.

105 It is concluded that:

• there is a clear distinction drawn in the authorities, not surprisingly, between the normal (or ordinary) hours of work and “overtime” (or “additional” hours of work);

and that:

• in many cases the terms of an award or an enterprise agreement will themselves identify the normal (or ordinary) hours of work

but that:

• in the circumstances of the present agreements, the “ordinary hours of work” for the purposes of the Superannuation Guarantee (Administration) Act include the “additional hours” and the “public holidays” for which the agreements make provision in respect to an “annualised salary” – and are so included irrespective of whether an employee actually works “additional hours” or “public holidays”.

It is further concluded that, even if the last conclusion be incorrect, the “ordinary hours of work” includes:

• the “additional hours” in fact worked by an employee.

It necessarily follows that the Respondents erred in not making superannuation contributions in respect to that components, being the “additional hours” component.

95 After those conclusions, the primary judge examined the authorities (Kezich, Quest, Thompson v Roche Bros, Catlow and Scott) and identified from propositions or principles as the background against which to construe the industrial instruments. The primary judge had previously (at [45]–[54]) set out and briefly discussed the relevant provisions of the legislation: the definition of “ordinary time earnings” in s 6(1) and ss 19, 23 and 46 of the SG Administration Act. The primary judge then (at [55]–[58]) examined the meaning of the word “ordinary” in industrial agreements and other statutes, referring to Quest and Australian Communication Exchange 201 ALR 271.

96 Nowhere in the judgment does the primary judge examine the whole definition of “ordinary time earnings” and the crucial phrase “ordinary hours of work” by reference to its text, context, purpose and enactment history from 1992. The primary judge focused in particular on the word ordinary as usual and normal hours. He placed some emphasis at [56]–[57] of the reasons on what Gray J had said in Quest when his Honour had, at 116 FCR 344, referred to Kezich. That use by Gray J of Kezich was, of course, in the context of a contract of employment that made no distinction in rates of pay and had no distinction between ordinary hours and additional hours or overtime.

97 To use Quest as authority for the proposition that in the definition of “ordinary time earnings” in s 6(1) the phrase “ordinary hours of work” simply means the ordinary or usual or normal hours worked (as [57] of the reasons does), is both to misunderstand Quest and to misconstrue the definition.

98 This explains why the primary judge, in his analysis thereafter, both of the authorities (at [106]–[112]) and of the industrial instruments (at [114]–[147]), focused, as relevant determinations, upon the hours provided for in the instruments to be worked and paid for as opposed to the correct enquiry being the hours identified in the industrial instruments to be paid for at ordinary rates.

99 If one first focuses upon the proper construction and interpretation of the definition of ordinary time earnings and gives to that meaning the proper weight to the distinction between standard or ordinary paid hours at ordinary rates and additional hours whether overtime or public holidays at higher rates, the debate about the annualisation and aggregation of salary can be settled tolerably straightforwardly. The employees were being required to work a body of hours that enabled the business to operate efficiently. In that sense, the usual hours that they worked exceeded or in any given period were likely to exceed 38 per week. For the purpose of simplicity and consistency they would be paid for those additional hours and public holidays, even if, as a fact, some were not worked. The salaries, unlike in Quest, were, however, made up or calculated of a base rate and additional components. The base rate was expressed as a standard 38 hours at an ordinary rate. The additional sums were added to the base salary for additional hours at a higher rate.

100 The central consideration for the primary judge for identifying “ordinary hours of work” was the usual or normal demands of how long the employees were usually required to work. This is reflected in the primary judge’s reasons at [117]–[121]: