FEDERAL COURT OF AUSTRALIA

Australian Competition and Consumer Commission v Medibank Private Limited [2018] FCAFC 235

ORDERS

AUSTRALIAN COMPETITON AND CONSUMER COMMISSION Appellant | ||

AND: | Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The appeal be dismissed with costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

PERRAM J:

1 The Australian Competition and Consumer Commission appeals from orders made by a judge of this Court dismissing its proceeding after a 12-day trial: Australian Competition and Consumer Commission v Medibank Private Limited [2017] FCA 1006. Its first case at trial was that the Respondent had misrepresented to its customers that they would not be left with any out-of-pocket expenses for pathology or radiology services provided to them whilst admitted as an in-patient in a hospital. It is convenient to refer to pathology and radiology services together as 'diagnostic services'. Its second case was that it had misrepresented to its customers that it would not reduce their benefits under their policies but in fact did so. It had done so, so it was alleged, by terminating agreements it had with various diagnostic service providers which had, until their termination, meant that a number (but not all) of the Respondent's customers who were in-patients in a hospital did not experience an out-of-pocket expense in respect of those providers' services. After that termination, those customers began to experience out-of-pocket expenses. Its third case was that the Respondent had acted unconscionably in the way it had ended those agreements. The trial judge rejected each case and the Appellant now pursues each on appeal.

2 For the reasons which follow I would reject the Appellant's appeal in relation to the two misrepresentation cases. For the reasons given by Beach J, I would reject its appeal in respect of the unconscionability case. The appeal should, therefore, be dismissed with costs.

3 The Respondent conducts its business under two brands: the Medibank Private brand and the ahm brand. The Appellant's cases in relation to the two brands differed although they were closely related. It is convenient to treat its case on the two brands separately.

Medibank Brand: The Diagnostic Cover Representation

4 The case advanced by the Appellant was that the Respondent had misrepresented to its customers that they would not have to bear any out-of-pocket expense in respect of diagnostic services rendered to them as in-patients in a hospital.

5 The Respondent sold private health insurance policies under the brand Medibank Private through three trade channels: in retail stores and kiosks; over the telephone from call-centres operated by a third party referred to as Salmat; and via a webpage it maintains on the World Wide Web. The Appellant contended that the diagnostic services representation had been conveyed through all three channels. It also alleged that it had been conveyed in a variety of documents it posted to customers after they had entered into a policy with the Respondent. As such, the Appellant's case at trial was complex and voluminous. It had to deal with the documents which had been sent and the condition of the website. It also had to try and distil the gist of the actual encounters which took place between its in-store retail staff and consumers and between consumers and the sales representatives working the telephones in Salmat's call centres.

6 Naturally, this was a significant forensic endeavour which makes it no surprise that the trial lasted 12 days. However, despite the sprawling field of combat the Appellant's case had an important central element which was common to almost all of the significant material tendered at trial. It can be found in the post-sale information provided to customers, on its website and in the literature which was provided to both its in-store employees and to the representatives working for Salmat. It took many different forms but from the Appellant's perspective all those varieties of embodiment revealed a similar message.

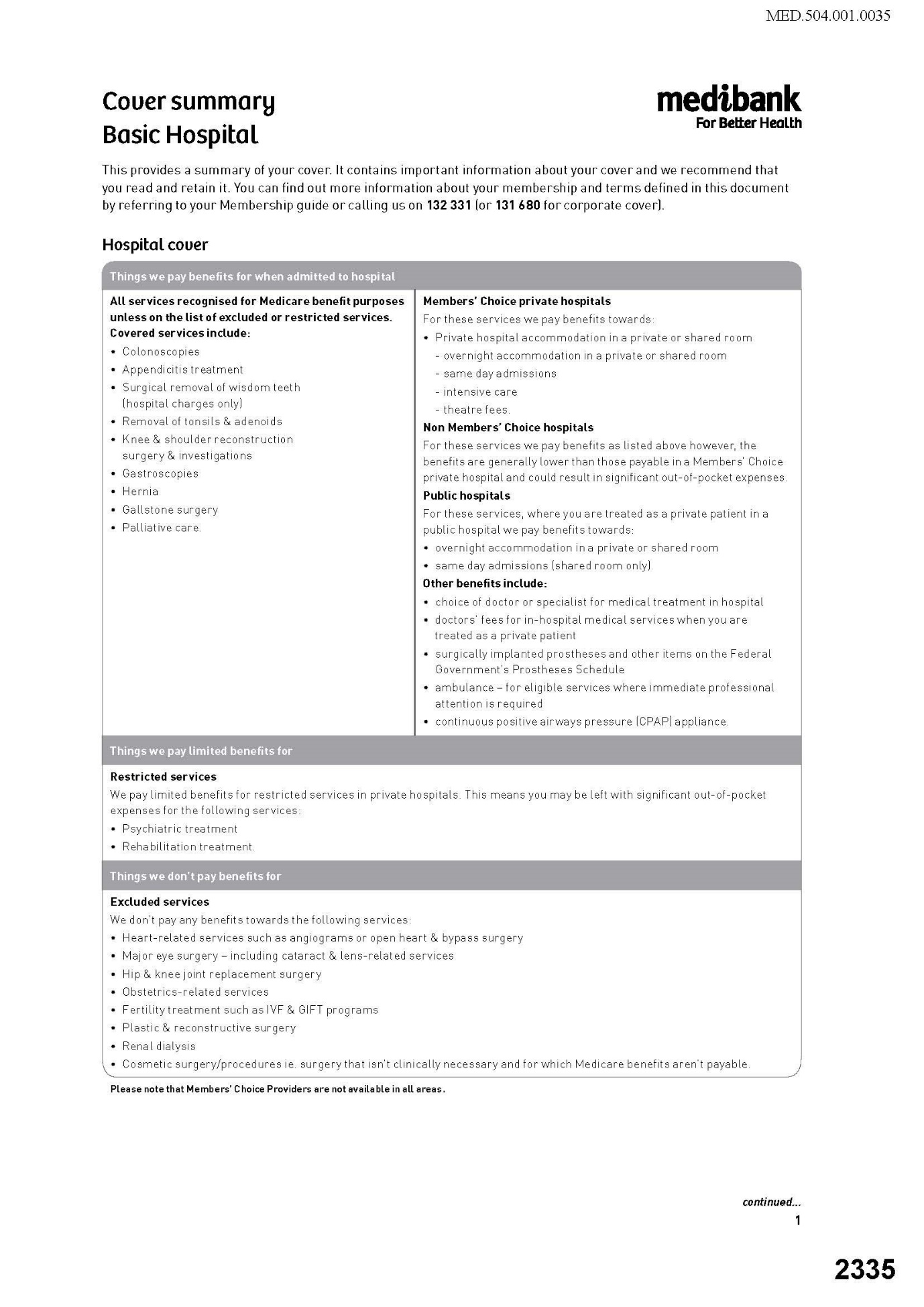

7 In the interests of clarity it is useful to set out one example in full so the point can be understood. The example is a document entitled 'Cover Summary Basic Hospital'. It was two pages in length and was as follows:

8 Before explaining the Appellant's argument it is necessary to provide some matters of context. First, the Respondent issued many different policies with fluctuating cover levels (top cover, basic cover etc.) to different kinds of customers (singles, couples, families). At the trial, it was accepted on all sides that attention could be limited to the 'basic cover' product since it was suitably representative of the issues which arose in relation to all of the Respondent's policies. Secondly, the cover contemplated was of two kinds. One was cover for services recognised by Medicare. The only such services are those provided by medical practitioners. In the case of services provided by a medical practitioner, the Commonwealth pays Medicare benefits in the amount of 75% of what is referred to as the schedule fee for that service. The schedule fee is fixed by the Commonwealth and prescribed in the Medicare Benefits Schedule. Thus the cover described in the first column of the extract above is cover in respect of the cost of medical services in the schedule.

9 Medical practitioners are not bound to charge only the schedule fee and many charge more. Because Medicare pays 75% of the schedule fee in all such cases, the cover mentioned in the first column is cover for the balance of 25% of the schedule fee which the Respondent is required by law to cover. An insurer may provide cover for more than this 25% and thereby reduce, or even eliminate, any 'gap' between the actual cost of the service and the schedule fee. It is, in part, in their coverage of such gaps that the various private health insurers compete with each other.

10 The second type of cover offered under the policy did not relate to services provided by medical practitioners. It related instead to services provided by hospitals such as accommodation, theatre fees, ambulances and so on. These appear in the second column.

11 Returning to the cover summary itself, it was the Appellant's case that the Respondent conveyed the representation that a customer would not be exposed to any out-of-pocket expenses in respect of diagnostic services provided to them as an in-patient in a hospital. One interesting aspect of the argument which may be noted at the outset is that the cover summary does not refer to diagnostic services at all. As will be seen this is not just a curious feature of the Appellant's case but is ultimately closely related to the reason why the diagnostic representation case cannot succeed.

12 The Appellant's theory for why the diagnostic cover representation could be gleaned from a cover summary which does not mention such services (and every equivalent document or material) had three steps:

(a) under the heading 'Hospital Cover' in the first column it was suggested that 'covered services' included all services recognised for Medicare benefits purposes. But this was subject to the proviso that the services be not 'restricted' or 'excluded services';

(b) in the cover summary's treatment of restricted services it was made clear that customers might well be left with substantial out-of-pocket expenses. There were, however, only two such services: psychiatric services and rehabilitation services. It was also clear that no benefits would be paid for 'excluded services' at all. The list for such services was longer but did not include, relevantly, any diagnostic services; and

(c) reading all three sections together the implication was said to be that out-of-pocket expenses would only be incurred for excluded and restricted services. Since diagnostic services were not amongst those kinds of services it followed that no out-of-pocket expense would be payable when a patient received diagnostic services as an in-patient in a hospital.

13 The Appellant buttressed this point with various additional matters of emphasis. For example, stress was placed on the words in the first column 'covered services' which were said to convey, in an insurance context, that the customer would have no exposure to costs.

14 Of course, as a cursory examination of the cover summary quickly reveals, there were matters tending in the opposite direction, too. One of these is the statement in the second column that the Respondent would 'pay benefits towards' private hospital accommodation which might suggest less than full indemnity. On the other hand, the second column is dealing principally with cover for accommodation rather than medical expenses. Also relevant is the balloon on the second page which asks the customer to call before going to hospital to ask about 'any out-of-pocket expenses you might incur'.

15 The trial judge was not persuaded that statements of the kind contained in the cover summary conveyed the diagnostic cover representation. Before explaining his Honour's reasons for those conclusions it should, I think, be acknowledged that at least as a matter of initial impression it is not difficult to understand the Appellant's argument and, indeed, even to see some force in it. What the trial judge's reasons expose, however, is the Achilles' heel of this apparently plausible case. That heel is the fact that the cover summary does not mention diagnostic services. The forensic manoeuvrings by the Appellant to make statements of the kind referred to in the cover summary apply to diagnostic services lays bare critical architectural defects in its case theory. As the trial judge noted at [171] the logic of the Appellant's argument leads to a result which means that there would be no out-of-pocket expenses for any medical services for which benefits were payable (apart from restricted services), not just diagnostic services. There were, in fact, more than 5,000 such procedures.

16 This mattered because there were many statements in the Respondent's written promotional materials which indicated that there could be out-of-pocket expenses in relation to services provided by doctors. One of these included a product sold by the Respondent called 'Gap Cover' which was designed to eliminate or reduce the size of any out-of-pocket expense relating to a doctor's fees (but which could not be purchased in relation to diagnostic services). The trial judge made this point about that material:

'171 If the applicant's contentions were correct, it would follow, as Medibank contended, that on the applicant's view of things, the documents relied upon by the applicant must also convey a representation to the consumer that Medibank indemnifies members for all costs of all included procedures – which number well over 5000 – not just radiology and pathology. And no one could possibly believe or infer that, because, apart from anything else, it flies in the face of repeated warnings about out-of-pocket expenses in the Cover Summaries, the Member Guide and other product documents.'

(emphasis added)

17 No appeal has been brought from the finding in the last sentence. Indeed, as will be seen shortly, it was a finding consistent with the way the Appellant ran its case. So the statements did not give rise to a representation that there would be no out-of-pocket expenses in the case of doctors because there were repeated warnings about out-of-pocket expenses for doctors in the materials.

18 The Appellant's response to this problem was that those warnings did not apply to diagnostic services. Its argument on this topic had matured throughout the course of the litigation. Initially, when the case was opened by senior counsel for the Appellant, the argument was that diagnostic services were not provided by medical practitioners at all. This exchange occurred between the trial judge and senior counsel for the Appellant:

'His Honour: And do you say that these diagnostic services aren't provided by doctors?

Mr Armstrong: No, your Honour. They're provided by diagnostic service providers, pathologists or radiologists. And Medibank itself draws a distinction between doctors and those other medical service providers because – I'm not sure if it's in this version of the member guide, but certainly a later version makes clear that the gap cover program is only available for doctors' charges and it's not available in respect of diagnostic – sorry – pathology and radiology services.

His Honour: I can't even think – do we call radiologist doctors or not in common – I should know something like that, but I ---

Mr Armstrong: I don't know, your Honour. I don't know.

His Honour: Someone will know.

Mr Armstrong: Yes.'

19 This turned out to be wrong. Although patients rarely meet their pathologists or radiologists there is no doubt that these professionals are doctors even if they often work for significant commercial entities. By the time of the appeal this was no longer in contest. The collapse of that front forced the Appellant to retreat to the proposition that even if the providers of diagnostic services were in fact doctors, they would not be perceived as such by consumers. It was necessary for the Appellant to retreat no further, however, and to hold, if it could, this redoubt. Why? If it abandoned altogether the position that diagnostic service providers were to be understood as standing apart from the position of doctors then the logic of its argument would lead unavoidably to the proposition that there would be no out-of-pocket expenses for all medical services. The trial judge recorded the Appellant's submission about this [165] which strongly suggests that at trial the Appellant accepted that consumers would not have thought there would be no out-of-pocket expenses for services provided by doctors:

'165 The applicant submits that "the impression conveyed by Medibank's communications was that diagnostic service providers were a different category of medical service provider relative to other doctors and specialists" and the "implication was that diagnostic charges were in a category of 'MBS treatments' for which members need not be concerned about out-of-pocket expenses notwithstanding that doctors could charge such expenses". Put another way, it was contended that the relevant documents suggested that a distinction was to be drawn, for the purposes of construing Medibank's descriptions of its insurance products in the marketing and product information, between medical practitioners who are doctors and medical practitioners who are pathologists and radiologists.'

(emphasis added)

20 It does not really matter now whether that was the Appellant's case below or not. The trial judge found at [171] that consumers understood that there might be out-of-pocket expenses in the case of services provided by doctors and no appeal has been brought from that conclusion. What that means is that it is critical for the Appellant to establish that the relevant class of consumers (a concept I return to below) would have understood diagnostic service providers not to be doctors to whom could apply the clear statements (accepted by the trial judge) that there could be out-of-pocket expenses. A concerted effort was mounted at trial to do so. The trial judge recorded this attempt and rejected it at [170].

21 So the position on appeal is this:

it is an unchallenged finding of fact that consumers do not distinguish diagnostic service providers from the services of other medical practitioners; and

it is an unchallenged finding of fact that the Respondent's promotional materials did not convey a representation to consumers that they would not be left with an out-of-pocket expense in the case of services provided by medical practitioners.

22 It is then useful to turn to the Appellant's challenge to the interpretation placed by the trial judge on the words 'cover', 'included', 'excluded', 'restricted' and 'towards' in the promotional materials (such as the cover guide). This was ground 2(b)(i) of the notice of appeal and the contention was that his Honour had given these words a meaning that ordinary and reasonable members of the target audience would not have given them. The relevant portion of the reasons are at [168]-[169]:

'168 The simple fact is that diagnostic services are not restricted or excluded procedures, and nothing in the documentary evidence on which the applicant relies suggests otherwise. As Medibank contended, a reasonable consumer would therefore, correctly, understand radiology and pathology services to be included services. The contrary conclusion urged by the applicant relies on the notions that the word "cover", wherever used, must be read to mean "entirely cover" or "indemnify" and that Medibank's documents would lead consumers to believe (contrary to the fact) that diagnostic service providers are a different species of medical practitioner or specialist, which, in turn, would lead the consumer to believe that "diagnostic charges were in a category of MBS treatments for which members need not be concerned about out-of-pocket expenses".

169 The word "cover" cannot be read to mean "entirely cover" or "indemnify". In my view, no reasonable consumer would understand the word "cover", used in the context of statements describing medical procedures to which the policy responds, to mean "indemnify". As Medibank submits, "[a] reasonable consumer would understand the words as they are clearly intended: to identify the types of medical procedures covered by one policy as opposed to another. There is a clear and obvious distinction between the risks covered by insurance and the benefits payable for those risks".'

(emphasis in original)

23 In its written submissions the Appellant developed the point this way:

'[The trial judge] accepted that diagnostic services were presented as "included" in cover, but he focused on the meaning of "cover" and immediately attributed to all consumers an insurance lawyer's awareness of distinctions between "the risks covered by insurance" and "the benefits payable for those risks". He implied an unstated qualification – that "cover" necessarily means partial cover – and rejected out of hand the possibility that one reasonably-open interpretation for an ordinary person might be that a covered or included service was for one for which they were no longer exposed to a risk of out-of-pocket costs. In each respect his Honour erred.'

(emphasis in original)

24 This submission should be rejected for two reasons. First, the meaning his Honour gave to the words was the same meaning that the Appellant accepted at trial they bore in relation to the services of doctors. His Honour did not give them a special or technical meaning; rather, he just refused to give them a different meaning for diagnostic services. A curious feature of the Appellant's argument – surely indicative that something has gone awry – is that it requires one to give the word 'cover' a different meaning in the consumer's mind depending on whether one is talking about doctors (in which case cover means only that benefits are payable which can result in an out-of-pocket expense) or about pathologists and radiologists (in which case it means full indemnity). This is impossible to accept. Secondly, there is in any event no substance to the suggestion that the trial judge substituted an insurance lawyer's views for those of the ordinary reasonable consumers. If anyone was doing that it was the Appellant by suggesting that 'cover' meant full indemnity. Ground 2(b)(i) should be rejected.

25 Next it was submitted (in Grounds 1 and 2(a)) that the trial judge had failed to have regard to the different characteristics of the persons to whom the statements were directed. It does not appear to have been in dispute that the target audience represented a full cross-section of the Australian adult community who had an interest in purchasing policies from the Respondent or renewing policies already held. The Appellant's written submissions contained the following propositions:

'Medibank's communications were directed to members of the public who might be investigating acquiring or changing their private health insurance. That target audience was so large and varied as virtually to constitute the entire Australian adult population. That audience included "the astute and the gullible, the intelligent and not intelligent, the well-educated and the poorly educated".

The learned judge did not address the range of characteristics of that target audience, either in his core reasoning at [161] to [178] or in obiter at [179] to [216]. Then, he did not examine the range of reasonable interpretations that ordinary members of that wide audience might draw from the Medibank marketing and member communications.'

(citations omitted)

26 The question which the trial judge was required to ask himself was what the effect of the conduct was on a reasonable member of the class of consumers involved: Campomar Sociedad Limitada v Nike International Limited [2000] HCA 12; 202 CLR 45 ('Campomar') at 85 [103]. It would certainly be contrary to that approach to ask whether any particular persons within the target audience were misled. However, as I understood the Appellant's submission it was not that the trial judge should have asked himself that prohibited question but rather that, before asking himself whether a reasonable member of the class would have been misled, he should first have acquainted himself with the various sub-classes and their respective characteristics within the target audience. I think there may be some issues of analysis around how the construct of the reasonable consumer is affected by an initial assay of the various factions within the target audience. However, this Court heard no argument on that issue and it would be inappropriate to take that further. It is convenient to assume, therefore, that the trial judge ought to have addressed himself to the range of characteristics of the target audience before asking what the effect of the conduct would have been on the reasonable member of that target audience and that he erred in not doing so.

27 But to make that assumption would only have the consequence of requiring this Court to come to its own view on the same issue. Taking into account the various aspects of the target audience identified in the Appellant's submissions does not cause me to doubt the correctness of the trial judge's conclusions on this issue. This is because it is not in dispute that the Respondent's materials did not convey to consumers that there would be no out-of-pocket expenses in the case of medical services provided by doctors. It is also not in dispute that consumers do not distinguish diagnostic service providers from doctors. Once one has arrived at that position, it is difficult to see how the trial judge could have arrived at any conclusion other than the one at which he did. A consideration of the range of aptitudes of the target audience cannot be material whilst those findings remain unchallenged. Grounds 1 and 2(a) should be rejected.

28 Of course, the Appellant's case was not just based upon the Respondent's written materials. Interactions between the Respondent and its customers involving purely these written materials were limited to those who purchased online and the post-purchase written documents provided to all customers by post after sale.

29 But the Appellant's case also focused on what had been said to the customers who purchased policies as a result of attending one of the Respondent's stores or retail kiosks or, alternatively, as a result of speaking to one of the sales representatives in a Salmat call-centre by means of a telephone. Forensically, this required the Appellant to prove its case in relation to those interactions. What was that case? It was the case set out at ¶¶9-10 of its concise statement:

'9. Medibank markets its Policies to Australian consumers through different channels, including (primarily) via websites, and via sales representatives operating by telephone, in-store or through web-chat using prepared scripts (the Marketing).

10. Since at least early 2012, in the Marketing in respect of each policy, Medibank:

(a) stated that, or to the effect that, the Policy would provide cover for all MBS items, save to the extent that a service was "restricted" or "excluded";

(b) stated that, or to the effect that, where a member received a service that was restricted or excluded, the member might incur an Out-of-pocket Expense; and

(c) did not identify In-hospital Diagnostic Services as restricted or excluded, although other restricted or excluded services were explicitly identified.'

(emboldening in original)

30 This was in fact the same case the Appellant made about the cover summaries which was at paragraph 11:

'11. Further, after selecting and purchasing a policy, members received written summaries of their cover under the policy (Cover Summaries). The Cover Summaries repeated the messages described in paragraph 10.'

(emboldening in original)

31 Mr Brownfield, the Respondent's Divisional General Manager for Customer Channels, gave evidence for the Respondent about the significance of these channels. In the financial year ending 30 June 2012, for example, 47% of the Respondent's customers joined through purchases made through the retail channel and 36% through policies sold via a call-centre (online was 17%). So the retail and call-centre part of the case was a very important aspect of the Appellant's case.

32 The Appellant pursued an orthodox way of proving what had occurred although, as will be seen, it encountered some obstacles in doing so. As a first step, it tendered the written materials which had been provided to the Respondent's retail employees and the sales representatives in the Salmat call-centres. These materials were as follows:

(a) Retail stores and retail kiosks

'Medibank Retail Network – My Best Practice Training Manual' dated 11 June 2013.

A program (or tool) called 'SPOT'. This was an interactive price calculation tool which was used to help retail staff compare the Respondent's products for a customer to identify a suitable cover and to create a personalised quote for the customer. Screenshots from the SPOT tool were put in evidence.

A document entitled 'Tips and Tricks to using SPOT' which described how the SPOT tool might be used.

(b) Salmat call-centre

Salmat staff had access to the SPOT tool.

Salmat itself generated an online based script for its call-centre staff using a system called Mi-Cat. Although these scripts were generated by Salmat it was not suggested that the Respondent was not responsible for their substantive content. Versions of these Mi-Cat documents were in evidence. The Mi-Cat system ceased being used on around 10 July 2013. It is not clear what replaced it.

33 The Appellant's contention in relation to the retail stores was, therefore, that it could be inferred that what appeared in the manual, the SPOT tool and the Tips and Tricks document was likely to have been conveyed to consumers. In the case of the call-centres, the proposition was that it could reasonably be inferred that what was in the Mi-Cat printouts and the SPOT tool was conveyed to consumers.

34 The second step was that these materials contained textual passages that were the same as those appearing in the cover summary (i.e. the reference, inter alia, to out-of-pocket expenses for restricted services). For the same reason that that document conveyed the diagnostic cover representation it could be seen that the same matter must have been represented to customers in-store and via call-centres.

35 It might have been possible to dispose of this argument on the same basis as the cover summary. This would have involved accepting the first step in the Appellant's argument, i.e., that if the representation were made in materials provided to staff and call-centre representatives then it was probably made to the public as well. But the second step would, on this view, be rejected because it would be accepted that customers were aware that there might be out-of-pocket expenses for doctor's fees and that the public would not distinguish doctors from diagnostic service providers.

36 The trial judge did not go down that path because he never got to the second step. This was because the first step was impaired by evidence led by the Respondent. This was the evidence of Mr Brownfield whom I have already mentioned above. He was the person with overall management responsibility for the processes by which new members joined the Respondent and the interactions that customers had with the Respondent during the course of their membership. However, he took up that role only on 17 October 2016. As the Appellant pointed out, that was sometime after 2014 when the events with which this appeal is concerned largely occurred.

37 Mr Brownfield gave evidence about many of the Respondent's promotional materials including evidence about the retail and call-centre channels. He described the current way that retail staff interacted with a customer in-store. He referred to the manual and the SPOT tool to explain what they were. His evidence about how they were used was as follows:

'Medibank does not instruct or require its retail staff to follow a script when speaking with customers. Rather, Medibank trains its retail staff about its insurance policies and makes available to staff various tools and documents to assist staff in dealing with customers. Staff can select from these various resources when speaking with customers and responding to customer queries.'

38 This was evidence about present practices but the case appears to have been approached on the basis that it could be inferred that the practices in 2014 were the same as they were in 2017 when Mr Brownfield gave evidence. The Appellant did not submit that such an inference ought not to be drawn but it did seek to downplay the significance of Mr Brownfield's evidence on the basis that insofar as it related to events in 2014 Mr Brownfield's knowledge was surely derivative since he did not commence in his position until 2016. There are three problems with that submission. First, Mr Brownfield's evidence was about the Respondent's present practices so the premise of the submission is incorrect. A more fruitful argument might have been that it should not be inferred that the practices in place since 2016 were the same as those prior to 2014. Such a contention might have encountered, however, the rhetorical question: why not? The difficulties in answering that question would have been exacerbated by the fact that the Appellant elected not to cross-examine Mr Brownfield. In any event, one need not linger on this issue.

39 Secondly, although the Appellant characterised Mr Brownfield's evidence as hearsay during the course of this appeal, it took no such objection at trial. Its submission is, therefore, an invitation to downplay the weight that is to be given to Mr Brownfield's evidence. This raises essentially an issue about its reliability. To gauge its reliability (on the erroneous hypothesis that it actually was hearsay) it would have been necessary to ascertain from Mr Brownfield the reasons he was willing to act on the correctness of what those who reported to him had informed him about events prior to 2014, i.e., why it was not reliable. That would have required Mr Brownfield to be cross-examined.

40 Thirdly, in that situation the Appellant's argument reduces to the bald proposition that all hearsay which has been admitted should be given little weight simply because it is hearsay. Such a proposition would render the hearsay rule unnecessary – why object to evidence if it can be given no weight? In any event, it is contrary to authority: Federal Commissioner of Taxation v SNF (Australia) Pty Ltd [2011] FCAFC 74; 193 FCR 149 at 158 [25] applying what was said by Evatt J in Walker v Walker [1937] HCA 44; 57 CLR 630 at 638 ('I deny the proposition that, merely because it was "hearsay" and therefore inadmissible, it is necessarily deprived of probative value').

41 Consequently, the Appellant remains saddled, as it was at trial, with Mr Brownfield's uncontested evidence that the manual and the materials provided to retail staff were not used as scripts. The trial judge acted on this evidence to conclude that the first step in the Appellant's argument (the drawing of an inference of likely retail employee behaviour from the contents of the material) should not be taken. This his Honour did at [187]-[188] where he recorded the Respondent's argument about this before himself accepting that argument:

'187 Senior counsel [for the Respondent] also submitted that:

(1) Mr Brownfield "gave unchallenged evidence that Medibank makes available to staff various tools and documents to assist staff in dealing with customers".

(2) To the extent that the applicant contends that those documents were the only documents used by Medibank staff, "there is simply no evidence to support that submission, and it's contrary to the evidence".

(3) The applicant asks the Court to "infer or assume that the only thing that's communicated from a Medibank retail store staff person to the consumer is word-for-word, some words that appear in the training manual …" and that submission is "frankly absurd … because a training manual is a training manual. And one's common experience is you don't walk into a retail store and the retail staff member has a training manual in front of them and is reading from the training manual as they speak to you". He continued: "… They can't go any further than that. Now, it is a simple question of evidence. The evidence they bring to the Court to prove that these representations were made to consumers at the point of sale is simply this training manual". He submitted that what he described as "the high point" of the applicant's case "fails immediately" and that the Court should not be satisfied "that this is what members were told and, with some precision of the sort of words, a representation of this kind was conveyed to members".

188 In my view, for the reasons advanced by Medibank, the Court is unable to conclude on the balance of probabilities that the diagnostic cover representation was at any relevant time made to members, or potential members, of Medibank in a retail store. It is not possible to make such a finding on the speculative basis contended for by the applicant in the absence of any actual evidence about interactions between Medibank staff with its customers in retail stores. Further, it is inherently unlikely that the training materials could ever have been used as a rigid script for such interactions and, indeed, Mr Brownfield swore that they were not. It is also inherently unlikely that the interactions took place without due regard to the brochures and other documents available to consumers at the retail stores. In the event, whether or not it is inherently unlikely, the applicant has failed to discharge its burden of proof in relation to this element of its case.'

42 By Grounds 2(b)(ii) and (iii) the Appellant submitted that the trial judge erred in thinking it relevant that it did not call any member of the target audience and by not accepting the relevance of the Respondent's failure to call any witness as to its training or practices.

43 However, neither of these arguments, even if correct, goes anywhere. Taken at their highest the best that could be said for the Appellant is that the statements appearing in the retail materials were conveyed to the customers in-store. But this is not enough for the Appellant to succeed. Nothing in the retail materials rises any higher than the statements appearing in the documents entitled 'Cover Summary Basic Hospital' set out above at [7]. For the reasons I have already given, it does not convey to the target audience the diagnostic cover representation. For that reason, even assuming the Appellant were right about the use by the retail staff of these materials, the case would still fail. Grounds 2(b)(ii) and (iii) should be rejected with respect to retail channels.

44 It is then necessary to turn to the call-centre evidence.

45 The evidence concerning what occurred in the Salmat call-centres was incomplete. Mr Brownfield explained the existence of Salmat's Mi-Cat materials but not how they were used. He also explained that they ceased being used in July 2013. He did not give evidence in relation to the Mi-Cat materials that they were not used as a script. To look at the Mi-Cat materials is to see immediately why Mr Brownfield gave no such evidence. It is clear that the Mi-Cat materials were a computer generated script designed specifically to guide a call-centre sales representative through a call with a customer and telling them precisely what to say at each juncture of the call.

46 It is difficult to know what to make of Mr Brownfield's evidence that the Mi-Cat system had ceased being used by Salmat in July 2013. It is difficult to imagine, however, that it ceased using instruction sets of that kind (nor does Mr Brownfield suggest that to be so). In this Court neither party made anything about the expiry of the Mi-Cat system. The trial judge, as will be seen, did not regard the matter as material either. In that circumstance, I propose to proceed on the basis that materials like the Mi-Cat materials were in place at the relevant time.

47 The point which the Appellant sought to extract from the Mi-Cat materials was a passage which, in substance, had exactly the same content as the cover summary set out above. It submitted, in relation to that material, that 'there is nothing [in the Mi-Cat material] to suggest that there is a major category of routine services – namely in-hospital diagnostic services – that is likely to be medically necessary, is covered by Medicare, is not identified as a restricted or excluded service, but nevertheless is not subject to the costs-protection that was the reason for the customer seeking [private health] insurance in the first place'.

48 The Respondent's response to this at trial was to submit that the passages relied upon by the Appellant did not constitute the entire universe of information conveyed by the Respondent which, significantly, included the Welcome Packs. It also advanced very similar arguments to those which it had advanced against the cover summary document.

49 The trial judge dealt with this at [195]:

'195 I shall return below to consider in more detail the submissions that arise out of some of the language used in the Salmat documents, including the use of the word "towards", the definition of "Restricted Services", and the information that is provided to new customers in the Welcome Pack. As to the Salmat documents specifically, it is not possible for the Court to draw the inferences sought to be drawn by the applicant with respect to the use of those documents. In particular, the Court cannot be satisfied, on the balance of probabilities, that the documents in evidence constitute the only information with which new customers must necessarily be provided. As to the submission that the Salmat materials constitute the only evidence of the instructions given to call centre operators and that it should be inferred that it "reflects the tone … of the information provided by the operators", I am not satisfied that the evidence allows me to draw that inference. In any event, the Court is unable to conclude, on the balance of probabilities, that the diagnostic cover representation was at any relevant time made to members, or potential members, of Medibank via call centre operators. It is not possible to make such a finding on the speculative basis contended for by the applicant in the absence of any actual evidence about interactions between Medibank staff and customers.'

50 This is largely the same way that his Honour dealt with the retail store material. However, this reasoning appears to overlook the fact that the Salmat materials plainly were scripts (e.g. instructions to the user saying 'MUST READ IN FULL') and that Mr Brownfield's evidence did not suggest otherwise. For that reason, I would accept the Appellant's argument that his Honour erred in dismissing as speculative any attempt to prove the diagnostic representation 'in the absence of any actual evidence about interactions between Medibank staff and customers'. It was not speculative at all. The Mi-Cat materials were plainly scripts; it was an inevitable inference that what was in the scripts was said to consumers. Additional evidence of interactions between staff and consumers was not necessary. If it was to be shown that something other than what was in the Mi-Cat scripts had happened that would be different. For example, if the Respondent wanted to show that the apparent effect of something appearing in the scripts was otherwise than it appeared, then it might want to call some evidence about this. I would therefore uphold ground 2(b)(ii) and (iii) to the extent that they concern his Honour's view that the Mi-Cat materials were not sufficient on their own.

51 However, I do not think this ultimately assist the Appellant. The representation case disclosed by the Mi-Cat material is the same in form as that disclosed in the cover summary document. It therefore has to confront the fact that it does not refer to diagnostic services. This brings it face to face with the trial judge's finding at [171] that consumers understood that there would be out-of-pocket expenses for doctors and his finding at [170] that they did not distinguish diagnostic service providers from doctors.

52 Once one arrives at that point it is impossible to see how anything in the Mi-Cat materials could do better than the cover summary. An ordinary reasonable consumer who spoke with a call-centre representative would have understood that there could be out-of-pocket expenses in the case of the services of doctors and they would not have distinguished diagnostic service providers from doctors. It seems to me therefore that the Appellant's case fails on this point. Grounds 2(b)(ii) and (iii) should be rejected.

53 It is not entirely clear whether the Appellant pursued an argument that the trial judge had erred in fact in concluding that the diagnostic cover representation had not been made although this did appear to be the contention in ground 1. Nevertheless the Appellant's written submissions tended to suggest that the error lay not so much in the finding that the representation had not been made but rather in the legal errors addressed above.

54 On the assumption that such an argument was pursued I would not be disposed to accept it. Such an argument would need to bring itself within the principles in Warren v Coombes [1979] HCA 9; 142 CLR 531. It would need to be demonstrated that the refusal of the trial judge to draw the inference that the diagnostic cover representation had been made had involved error. I do not see how it is possible to arrive at a different conclusion to the one the trial judge arrived at whilst it remains accepted that consumers did not understand from the Respondent's activities that they would not have out-of-pocket expenses for doctor's charges but also did not distinguish the position of doctors from that of diagnostic service providers. To the extent that Ground 1 made this contention it should be rejected.

55 The Appellant's next argument was that the diagnostic cover representation was the dominant message of the Respondent's marketing. If that were correct it followed that it could not necessarily be diluted by subsequent disclaimers. This was ground 2(b)(iv). The Appellant placed particular reliance upon what was said by the High Court in Australian Competition and Consumer Commission v TPG Internet Pty Ltd [2013] HCA 54; 250 CLR 640 ('TPG'). That case reminds one that the misleading nature of a dominant message may not be successfully neutralised by the provision of later accurate information for by then the harm may already have been done in that the customer has been enticed to treat with this merchant rather than some other merchant. On this view of affairs, customers would be enticed to deal with the Respondent because of statements made by in-store staff or call-centre staff along the lines of the cover summary.

56 It is useful to ask, however, what this dominant message could have been at this point in the transaction. It cannot have been the diagnostic cover representation because the marketing materials do not mention diagnostic services at all. It can only have been a representation that there would be no out-of-pocket expenses for all medical services. It is only the later statements in the Welcome Pack that can have left consumers with the impression that there could be out-of-pocket expenses for doctors. But the Appellant does not contend for such a representation.

57 The difficulty for the Appellant is well-illustrated by assuming in its favour that its submission based on TPG is correct. What follows is that the subsequent statements in which it is plainly indicated that there may be out-of-pocket expenses for doctors is insufficient to dispel the dominant message. But what is the dominant message? It is not the diagnostic cover representation. It is instead a representation that there will be no out-of-pocket expenses in the case of any medical service. What follows from an application of TPG to that factual constellation is the conclusion that that representation was made (rather than the diagnostic cover representation). But this is a case which the Appellant has never advanced. Indeed, at trial it accepted that that representation was not conveyed.

58 The difficulty is that the primary judge found the representation never to have been made. TPG is a case concerned with whether a misleading dominant message may be not misleading by later qualification. The question in this case, however, is not about whether the conduct is misleading. It is whether the representation was ever made at all. This suggests that TPG has little to do with a case like this: see especially 654-655 [47]-[49] where the Court explained the different position of consumers in Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd [1982] HCA 44; 149 CLR 191 and TPG.

59 The Appellant's last contention in relation to the diagnostic cover representation was that contained in ground 2(b)(v). To understand this ground one needs to know that the Respondent had a number of customers who at the date of termination of the MPPAs (defined below at [73]-[74]), were, in fact, receiving in-hospital diagnostic services from diagnostic service providers with such MPPAs. Such customers went from the position that they had no out-of-pocket expense in relation to the provision of diagnostic services to a position where, after the termination of the MPPAs, they found themselves having to pay such an expense. These persons have been referred to in the litigation as the recipient members.

60 At trial the Appellant tendered statements of benefits for some of these customers which showed that they had not had an out-of-pocket expense prior to 1 September 2014. The Appellant submitted to the trial judge that the recipient members would have noticed that they handed over their Medibank card to the provider and then paid no out-of-pocket expenses. The trial judge dealt with this submission at [219]:

'219 In my view, there is, with respect, nothing in this submission. First, it is not immediately clear how a member would be able to identify diagnostic services on the face of the statement. Secondly, and in any event, whatever a reasonable ordinary Medibank member would have made of the statements of benefits, nothing in them could be read or construed as relevantly contradicting the information provided to members in the Welcome Pack and other documents, including brochures, and the information available online, about the possibility of incurring out-of-pocket expenses.'

61 On appeal the Appellant contended that the trial judge had failed to address its principal contention, namely, that the Respondent provided a 'no gap' experience to these recipient members. According to the Appellant '[b]y doing so it represented to them that their policies did protect them from out-of-pocket costs for these services'.

62 There are a number of difficulties with this. First, as the Respondent correctly points out, not receiving an out-of-pocket expense in respect of a diagnostic service could be equally caused by either of:

the diagnostic service provider only charging 100% or less of the schedule fee; or

the diagnostic service provider charging more than 100% of the schedule fee and the Respondent doing something to ameliorate the gap.

63 The Appellant's case assumes that a person who received no gap would infer the second rather than the first of these. But no ready explanation is advanced as to why that would be so. Secondly, the statement of benefits identifies the services rendered by their MBS item number. For a consumer to understand what was being said they would either need to know what the MBS item numbers were for diagnostic services or to look them up. Thirdly, it is quite possible that there might be item numbers where there was no out-of-pocket expenses (because the provider only charged the MBS fee) and others for which an out-of-pocket expense was payable. It is very difficult to extract anything clearly from such a document.

64 The trial judge was therefore quite correct to reject the case based on the statement of benefits. Nor, leaving aside the statement of benefits, do I think the fact that the recipient members were spared out-of-pocket expenses for diagnostic services, helps to advance the case on the diagnostic representation case. If an ordinary reasonable consumer did not believe, as a result of the Respondent's promotional activities, that they would not be left with out-of-pocket expenses for doctor's services and that diagnostic service providers were not distinguishable relevantly from doctors, how does it assist to know that the recipient members had out-of-pocket expenses for diagnostic services? It is difficult to see that that fact could have any effect on the other two. Not having to pay an out-of-pocket expense for a diagnostic service could not logically impact on one's views as to whether one would have expenses of that kind in relation to doctors generally; nor is it possible to see why it would have any impact on one's ability to distinguish diagnostic services from those of doctors.

65 I would reject ground 2(b)(v).

Medibank Brand: The Notice Representation

66 The Appellant alleged that the Respondent had also represented to consumers that it would give prior notice to its members of any detrimental change to the level of benefits it would pay under its policies. Such a change had occurred, so the Appellant alleged, but the Respondent had not given notice. Consequently, it had engaged in misleading and deceptive conduct. The Respondent denied that it had made the representation alleged.

67 It is useful to start with the representation itself. The Appellant relied upon the Medibank Member's Guide which was in effect from 16 January 2012. Relevantly, it said this:

'Changes to the terms and conditions of your membership

Please note that all members of Medibank Private are subject to the Fund Rules, which set out the terms and conditions of their cover, as well as the services we pay benefits for. The Fund Rules can be changed from time to time with the approval of the Minister …. If any changes will have detrimental effect on your entitlement to benefits we will provide you with reasonable notice in writing before they are due to come into effect.'

68 This refers to the 'Fund Rules'. The trial judge dealt with these at [77]-[80] in terms which were not suggested to be controversial. The Private Health Insurance Act 2007 (Cth) assumes, but does not appear to require, that a private health fund will have rules. In the Dictionary in Schedule 1 this is said:

'rules, of a private health insurer, means the body of rules established by the insurer that relate to the day-to-day operation of the insurer's *health insurance business and (if any) *health-related business.'

69 Section 93-20(2)(c) relevantly provides:

'93-20 Keeping insured people up to date

…

(2) A private health insurer must ensure that, if a proposed change to the insurer's *rules:

…

(c) is informed about the proposed change a reasonable time before the change takes effect; and

…'

70 A person who acquires a private health insurance policy from Medibank becomes a member of Medibank's Health Benefits Fund. Membership of that fund is governed by the Fund Rules which consist of 'Main Rules' and 'Schedules'. The Main Rules were available in-store and on the Respondent's website. They were also summarised in the Member Guides. The Schedules defined the benefits which were payable in relation to the different products which the Respondent sold. These were not provided to members but were summarised in the Member Guide. The Fund Rules also specified the relevant premiums.

71 The Fund Rules defined the benefits payable to members in respect of hospital treatments, which included benefits for medical procedures, in accordance with the requirements of the Private Health Insurance Act 2007 (Cth). The Fund Rules also defined additional benefits that became payable to a member if Medibank had an arrangement or agreement in place with a private hospital or medical practitioner and the member received hospital treatment from that hospital or practitioner.

72 The implications of that statement are not immediately obvious and require some further explanation. By way of example, the Respondent might have agreed with a particular provider of diagnostic services that the Respondent would pay 10% on top of the schedule fee for its members. The Fund Rules would then provide for that additional 10% to be a benefit. The net effect would not, however, be the receipt of the additional 10% by the member, but rather the amount would pass to the diagnostic service provider.

73 There were three main categories of agreement or arrangement which the Respondent could enter into and which, if in place, provided for additional benefits to be paid to members in that sense. These were Hospital Purchaser Provider Agreements ('HPPAs'), Medical Purchaser Provider Agreements ('MPPA's) and GapCover Arrangements.

74 An HPPA is an agreement between Medibank and a private hospital pursuant to which the hospital accepts payment in satisfaction of amounts that would otherwise be owed by a member to a hospital. An MPPA is an agreement between the Respondent and a medical practitioner pursuant to which the medical practitioner accepts payment by the Respondent in satisfaction of amounts that would otherwise be owed by a member to the medical practitioner.

75 The Respondent had MPPAs with a number of Diagnostic Service Providers. When a medical practitioner had provided an in-hospital diagnostic service to a member, these provided for the Respondent to pay the diagnostic service provider the difference between the relevant schedule fee and the diagnostic service provider's fee. The diagnostic service provider agreed in return not to charge more than a specified fee. MPPAs also commonly provided that either party could terminate the agreement on the giving of 60 days' notice, on most occasions following an initial period of 12 months.

76 On 1 September 2014 the Respondent abolished most of its MPPAs. The effect of this was that in many cases patients who received in-hospital diagnostic services began to receive accounts from the diagnostic service providers. This charge was the difference between the fee charged by the diagnostic service provider and the schedule fee for the service; that is to say, the members became exposed to a gap payment which had previously not been present.

77 At trial, the Appellant submitted that the Member Guide equated the Fund Rules with an entitlement to benefits. Consequently, although couched in language about changes to the Fund Rules, the ordinary reasonable consumer would have understood the statement as being concerned with benefits more generally. Further, the Appellant sought to obtain some benefit from Part E of the Industry Code which, under the heading 'Changes to Hospital Contracting Arrangements', said this:

'We recognise that while not constituting a change to hospital benefits for the purpose of Section 2 above, changes to hospital contracting arrangements between a fund and a hospital can affect a consumer. We understand that requirements for notification of consumers of such changes and transition arrangements are included in the relevant agreements …'

(emphasis added)

78 The trial judge rejected this submission on the basis that the termination of the MPPAs did not effect any change to the Fund Rules. He noted that the benefit payable to a member remained the same both before and after the termination. His Honour illustrated this with an extract from the Fund Rules:

Charge | Benefit |

… | … |

Exceeds the MBS fee and the Professional Attention is provided under a Contract with the Medical Practitioner. | 25% of the MBS fee, plus an amount up to the difference between the MBS fee and the charge, in accordance with the Contract with the Medical Practitioner. |

79 It is true that no change was made to this rule although in each case where an MPPA had been terminated this would appear to mean this rule was no longer relevant since the service would not have been provided under a 'contract with the medical practitioner'. However, neither party made anything of that and it does not appear to have any impact on the logic of his Honour's reasoning.

80 The Appellant also submitted at trial that its case was assisted by notices which the Respondent had sent to its members which notified them of changes to the Fund Rules. These were of two kinds: changes to the amount of the premium and changes to the benefits payable. Here the point was that this reinforced the representation relied upon by the Appellant.

81 The trial judge concluded that there had been no change to the Fund Rules (which was an agreed fact). His Honour therefore concluded that the Respondent had not acted contrary to the assurance in the Member Guide that if there were any changes to the Fund Rules which would have a detrimental effect on a members' entitlement to benefits it would provide them with reasonable notice in writing before the changes were due to come into effect. In relation to the Industry Code his Honour did not think that it helped the Appellant. Indeed, the Industry Code appeared to recognise that changes to the agreement of the kind under discussion were not changes to benefits. His Honour rejected the argument based on the change notices. The fact that change notices had been sent in the circumstances contemplated by the Fund Rules and the Private Health Insurance Act 2007 (Cth) could not assist in making good a case that a notice needed to be sent when neither the Fund Rules nor the Act required it.

82 On appeal the Appellant submitted that the trial judge had applied a lawyer's construction to the words of the Member Guide. The Member Guide did not suggest that there was a distinction between changes to benefits resulting from changes to the Fund Rules 'compared to changes to benefits resulting from other causes'. Further, the trial judge had failed to examine the range of reasonable interpretations that an ordinary member of the target audience might draw. Instead, he had imputed to all consumers an understanding of a highly technical distinction found 'only within the machinery clauses of the Fund Rules'. The Appellant submitted this was contrary to TPG at [53] and Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2014] FCA 634; 317 ALR 73 ('Coles') at 100 [160]. The Appellant also submitted that his Honour had erred in his treatment of the change notices. It was said that the notices did not correct anything in the Member Guide and that if the latter was relevantly misleading then so were the change notices. His Honour had erred in attributing to members a sophisticated understanding of the Member Guide.

83 The Respondent took issue with this submitting that the difficulty for the Appellant was that the terms of representation were clear and that the Member Guide simply did not say what the Appellant sought to extract from it. As to the suggestion that the distinctions drawn by the trial judge were technical, the Respondent denied there was anything technical about them at all. The concept of changes to the Fund Rules was not a technical one. Likewise, his Honour had not failed to take account of the varying aptitudes of the target audience. In relation to the change notices, the trial judge was correct in his conclusion that they did not convey the representation alleged. There was no avoiding the agreed fact that the change notices involved a change to the Fund Rules and hence they could not assist the Appellant's argument.

84 Viewed from a certain perspective there is apparent force in the Appellant's submission. The statement that members would be notified of any changes to Fund Rules which would have a detrimental effect on a member's entitlement to benefits could, in some contexts, be seen as incomplete. It is literally correct but if it formed part of a strategy on the Respondent's part to entice persons into dealing with the Respondent then it would probably be misleading unless qualified. For example, if the statement appeared as the headline component of a marketing campaign like this:

then it would probably have been misleading not to tell potential customers that they would not be notified of the termination of MPPAs which would have the effect of potentially creating a gap payment when there was none before. It would not be to the point, were this a case of headline advertising, that the headline statement was literally correct. Further, that correcting or fuller information is available elsewhere would not dispel the misleading and deceptive nature of the headline advertisement. So in TPG it was misleading to market an ADSL2+ plan at $29.99 per month without also pointing out with at least equal prominence that it had to be bundled with a telephone service costing $30 per month. And in Coles, it was misleading to advertise bread as freshly baked bread which had been par-baked in advance and whose baking was merely completed in store. In that case 'freshly baked' and similar statements were identified as the dominant message.

85 However, the Appellant's case on the notice representation is far from a headline advertising case. To explain why it is necessary to say something of the document containing the alleged representation, the Member Guide. The trial judge dealt with it at [133]-[134]. It was a post-sale document which was sent as part of a Welcome Pack to new members. It was sent by email and within 48 hours of the member signing up. The Member Guide was not the only item in the Welcome Pack. It also contained a cover summary, a brochure entitled 'Quick Tour of Your Cover' and a statutorily required document known as a standard information statement. The Member Guide was also made available on the Respondent's website and at its retail stores.

86 Turning to the Member Guide effective 16 January 2012 itself, the first thing to note is that it is 52 pages long. At page 3 there is a table of contents including an entry for 'Changes to the terms and conditions of your membership' which is said to start at p 9. On the first page the document describes itself this way:

'This guide is a summary of the main Fund Rules and policies of Medibank Private affecting members who are Australian residents.'

87 The passage the Appellant relies on is at the foot of p 9. What is apparent from this is that the Member Guide is not promotional material in the sense that it is not seeking to advertise the Respondent's services. By definition, those who receive the Member Guide have already signed up. This is not to deny its capacity to be misleading per se but only to underscore that it does not involve a headline advertising statement such as those in TPG ('ADSL2+ for $29.99 per month') or Coles ('freshly baked bread'). There is no sense in which the Member Guide can be seen as enticing a consumer into a transaction: see TPG at 654-655 [48].

88 From that flows a second matter. The Member Guide provides information about the Fund Rules in what may fairly be interpreted as an attempt to speak in plain English. As such it is to be seen as an information source. In that context, the statement about changes to the Fund Rules it contains is literally correct. But because it is not part of a stratagem to draw people in the fact that it might be seen as incomplete in itself is of much less moment. This because an analysis of its capacity to mislead needs to be understood in a context which includes the fact that the Member Guide also gave an accurate description of the effect of contractual arrangements with medical practitioners providing in-hospital services (p 24-25). That discussion was not a surreptitious footnote to the section dealing with changes to the Fund Rules. Rather, both were part of a non-marketing document serving as a source of information. In my view, any consumer who decided to embark on a reading of the Member Guide would not be reading it in the fleeting way inherent in the Appellant's submission.

89 In those circumstances, the trial judge was correct to reject this case. I would reject grounds 2(c)(i)-(iv).

The ahm Brand: Diagnostic Cover and Notice Representations

90 As already mentioned, the Respondent offered private health insurance under two brands, the Medibank brand (considered above) and also the ahm brand. The Medibank business was much larger than the ahm business with the latter contributing only 5% of the Respondent's revenues. The principal difference between ahm and Medibank was that ahm was strictly an online business and did not maintain retail stores.

91 The Appellant began its submission by observing that its case in relation to ahm was comparable in volume and complexity to the language used in the case relating to the Medibank brand. Yet despite that the trial judge had despatched its entire case in a single sentence. That is not, however, a correct statement. His Honour dealt with the matter this way:

'221 The diagnostic cover representation is also pleaded in respect of ahm branded products. As outlined earlier, ahm is an online and telephone sales business. Its private health insurance products differ from those branded as Medibank products to some extent, so the relevant documents and the material available on the ahm website differs from the Medibank material.

222 Although the applicant referred to a number of specific ahm documents in an annexure to its written closing submissions, in the end it did not contend that any documents in evidence relating to ahm were relevantly or materially different to the evidence adduced in respect of Medibank or that any different question of construction or principle arises in respect of that evidence for the purposes of the diagnostic cover representation case.

223 Because the diagnostic cover representation case was conducted on that basis, it follows, for the reasons given above in respect of the evidence adduced concerning Medibank branded products, that the applicant has also not established that the diagnostic cover representation was made in respect of the ahm branded products.'

92 That was in relation to the diagnostic services representation. In relation to the notice representation his Honour set out the relevant portion of the ahm Member Guide at [227]-[228]. He then dealt with that at [242]-[243]:

'227 It was not suggested that this version of the Member Guide is not an adequate exemplar. The ahm Member Guide (effective 11 June 2013) is similarly worded:

Fund Rules and policies

When you join ahm Health Insurance, you agree to be bound by our Fund Rules. These are available online at ahm.com.au or you can call us on 134 246 to request a copy. Our Fund Rules, policies and benefits are subject to change from time to time with the agreement of the Minister … If we make changes that affect your cover in a detrimental way we will let you know in writing prior to the change taking place.

228 The reference to "policies and benefits" in the 11 June 2013 ahm Member Guide was deleted from ahm Member Guides on and after April 2014.

…

242 As for the ahm Member Guide effective between June 2013 and April 2014, the applicant says that its case with respect to the notice representation is "particularly strong" because it amounts to a representation that ahm would notify members of any detrimental change to "policies and benefits". I also do not accept that submission. For these purposes, there is no relevant distinction between the expressions "fund rules", "policies" and "benefits" – the benefits payable for each policy are defined by the Fund Rules. As Medibank submitted:

[a]ny changes to benefits payable under a policy must involve a change to the Fund Rules. The Fund Rules prescribe that benefits must only be paid in accordance with the Fund Rules. So too, any change to a "policy" must involve a change to the terms of the schedule to the Fund Rules that define the benefits payable in respect of the policy.

243 Further, the ministerial approval to any relevant change, which is referred to in both the Medibank and ahm Member Guides, is something that is only required for changes to the Fund Rules. The termination of the MPPAs required no such approval.'

93 The Appellant's first submission is that the trial judge failed to give adequate reasons. The Appellant does not cavil, however, with the trial judge's statement at [222] that the Appellant 'did not contend that any document in evidence relating to ahm was relevantly or materially different to the evidence adduced in respect of Medibank'. In that circumstance, it is difficult to see any deficiency in the trial judge's reasons.

94 In fact, the only matter which the Appellant pointed to in its submissions in this Court as to the difference between the ahm materials and the Medibank materials related to the use of words 'partially covered' in the ahm Quick Guide and 'partial cover' on its website. This was, as it happens, also its only substantive ground of appeal relating to the ahm brand.

95 The Quick Guide corresponded to the cover summary used in the Medibank business. Under the heading 'What's partially covered' there was a discussion of restricted services (discussed above). The equivalent statement in the Medibank cover summary was 'Things we pay limited benefits for'. The Appellant submitted that the ahm language was even more reassuring than the Medibank language. Even assuming this difference was pointed out to the trial judge, the point is without merit. The ahm wording is different to the Medibank wording but not in a way which is material.

96 The Appellant also submitted that the Quick Guides were not adequate disclaimers to correct the diagnostic cover representation. But for the same reasons as in the case of the Medibank brand, the diagnostic cover representation was simply not made. The disclaiming effect of the Quick Guides is irrelevant.

97 In relation to the notice representation, the Appellant acknowledged that the trial judge had given some reasons but it submitted that these were inconsistent. The inconsistency arose this way. At [235] and [239] the trial judge had rejected the Appellant's contention in relation to the Medibank brand that the Member guide equated Fund Rules with an entitlement to benefits. The purpose of that argument was to allow the statement in the Member Guide that any changes to the Fund Rules which would have a detrimental effect on the members' entitlement to benefit to serve as a representation about members' benefits. The effect of the submission, if accepted, was that the statement would have required notification of benefit reductions even if they did not result from changes to the Fund Rules (i.e. arising from a termination of an MPPA instead).

98 But, submitted the Appellant, at [242] the trial judge had taken the opposite position:

'242. As for the ahm Member Guide effective between June 2013 and April 2014, the applicant says that its case with respect to the notice representation is "particularly strong" because it amounts to a representation that ahm would notify members of any detrimental change to "policies and benefits". I also do not accept that submission. For these purposes, there is no relevant distinction between the expressions "fund rules", "policies" and "benefits" – the benefits payable for each policy are defined by the Fund Rules. As Medibank submitted:

[a]ny changes to benefits payable under a policy must involve a change to the Fund Rules. The Fund Rules prescribe that benefits must only be paid in accordance with the Fund Rules. So too, any change to a "policy" must involve a change to the terms of the schedule to the Fund Rules that define the benefits payable in respect of the policy.'

99 So the submission is that in dismissing the Appellant's argument at [242] his Honour had done so by equating benefits with the Fund Rules but at [235] and especially [239] he had rejected an argument that the Member Guides equated the two.

100 There is an inconsistency in the trial judge's approach but it does not materially impact the correctness of his Honour's reasoning. At a formal level, it is correct to say, as the trial judge did at [242], that because the benefits are specified in the Fund Rules there is a close relationship between the benefits stated in the Fund Rules and the Fund Rules themselves. I would accept that there is a certain inconsistency with what the trial judge said at [239]:

'239 Further, I reject the submission that the Medibank Member Guide "equates" the Fund Rules with "the entitlement to benefits". It does no such thing.'

101 However, it is clear that the basic point his Honour was making was that the termination of an MPPA does not affect the benefits which are payable under the Fund Rules. Neither the Fund Rules nor the benefits they provide for are altered by the termination of an MPPA. What does happen is that the termination of an MPPA may make a different benefit rule applicable to the member. That, however, does not involve any change in the benefits for which the policy provides and in that regard his Honour's analysis is correct regardless of the suggested inconsistency. The basic problem is that the termination of an MPPA does not effect a change in the Fund Rules or the benefits. I would reject Grounds 3-5 insofar as they apply to ahm.

102 For all those reasons, I would dismiss the appeal insofar as it relates to misrepresentations. For the reasons given by Beach J I would dismiss the unconscionability case. The Appellant must pay the Respondent's costs.

I certify that the preceding one hundred and two (102) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Perram |

Associate:

REASONS FOR JUDGMENT

MURPHY J:

103 I have had the benefit of reading the separate reasons of Perram J and Beach J in draft form. I agree with the orders they propose and generally agree with their reasons.

I certify that the preceding one (1) numbered paragraph is a true copy of the Reasons for Judgment herein of the Honourable Justice Murphy. |

Associate:

Dated: 20 December 2018

REASONS FOR JUDGMENT

BEACH J:

104 I have had the considerable advantage of reading in draft form Perram J's reasons concerning appeal grounds 1 to 5. I agree with those reasons and have nothing to add on those topics. Accordingly, it is only necessary to address appeal grounds 6 and 7 concerning statutory unconscionability.

105 Before addressing these grounds directly it is necessary to deal with some introductory and background matters.

106 The ACCC's case at trial concerning s 21 of the Australian Consumer Law (ACL) relevant to appeal grounds 6 and 7 related to the conduct of Medibank in terminating most of its Medical Purchaser Provider Agreements (MPPAs) with in-hospital pathology and radiology providers concerning pathology and radiology services (diagnostic services) without giving notice of doing so to all of its members.

107 The ACCC's case at trial was that Medibank prior to termination of the MPPAs perceived that if members were told of the change there was a significant risk that they would lapse; the reference to "lapse" refers to members ceasing to insure with Medibank. It was also perceived, so the ACCC said, that publicity about the change would impact Medibank's brand and reputation, and have a negative impact on the lead-up to Medibank's initial public offering.

108 It was said that Medibank knew that consumers including its members:

(a) were unlikely to enquire about and would have difficulty enquiring about the relevant change;

(b) were likely to find out about the change when they were at their most vulnerable;

(c) were likely to be distressed by the change; and

(d) were likely to incur costs for which they did not budget.

109 The ACCC's case at trial was that Medibank's decision not to notify members of the relevant change, or as it described it implementing the non-disclosure strategy, was unconscionable because:

(a) Medibank knowingly exploited what was said to be a lack of understanding by its members of private health insurance (PHI);

(b) Medibank knew that its decision not to notify members would cause them harm; and

(c) not notifying members was unethical because it breached industry norms, which were said to be enshrined in the Private Health Insurance Act 2007 (Cth) (PHIA) and the Private Health Insurance Code of Conduct (Industry Code), to provide consumers with current information about their entitlement to benefits.